Abstract

In response to the labour market effects of the COVID-19 pandemic, the European Union (EU) implemented ‘Temporary Support to mitigate Unemployment Risks in an Emergency’ (SURE). This instrument enables loans to be made under favourable conditions from the EU to affected Member States, covering part of their costs for national short-time work (STW) schemes or similar policies. In essence, STW prevents unemployment by helping employers to temporarily reduce the working hours of their personnel, while providing these employees with income support from the state for the hours not worked. During the COVID-19 crisis, non-standard workers in particular experienced job loss or a reduction of working hours, while often having inadequate access to social security. This article assesses the inclusiveness of SURE in terms of providing, via national STW, support to all workers. Firstly, it explores the options provided by the SURE Regulation to finance STW schemes which also cover non-standard workers. Secondly, it gives an EU-wide overview of which schemes and which types of workers have been supported. Thirdly, the paper analyses in detail how three Member States – Belgium, Cyprus and Poland – have used SURE to support non-standard and self-employed workers. The article adds to the currently scarce analyses on how SURE is used by countries with various STW systems. Moreover, it shows whether SURE may fit the growing EU focus on providing access to social security for all types of workers irrespective of their employment relationship, as for instance codified in the EU Pillar of Social Rights.

Introduction

The COVID-19 outbreak has had a severe impact on working hours and earnings across the globe (ILO, 2020). Yet, the pandemic affected Member States and workers unequally, highlighting economic divergences between Member States, differences according to employment status, and inequalities between women and men (Vanhercke et al., 2021: 158). In particular, workers on non-standard contracts (temporary and self-employed workers) have been affected by the labour market shocks, as well as women, foreigners, workers in microenterprises and those who are underpaid and poorly educated (Pouliakas and Branka, 2020: 30). Ideally, workers who have lost their job are covered by income replacement schemes such as unemployment benefits (UB). In the first months of the pandemic, most EU countries used existing social protection schemes and introduced new measures to give additional economic and social support (Ebbinghaus and Lehner, 2022); for instance, they relaxed the eligibility conditions of the social security schemes, or upgraded the benefits (Spasova et al., 2021). Many governments broadened the scope of income replacement through the introduction of ad-hoc liquidity support packages, for example supporting the income of self-employed workers (Schoukens and Weber, 2020: 4). Still, not all types of workers benefit equally from income support. In particular, workers in the most precarious forms of employment face gaps in social protection (Spasova et al., 2021). Also, protective measures offered by short-time work (STW) schemes have not always been accessible to freelancers, self-employed workers, and workers on temporary contracts, exposing them more to the risk of economic shocks (Eurofound, 2020a).

At European level, the European Commission has contributed to mitigating the effects of the pandemic on the labour market, through, among other measures, the temporary instrument SURE, which aims to help protect jobs and workers (European Commission, 2020a). On 2 April 2020, the Commission published SURE, and already in May 2020 the Council adopted the proposal. SURE has provided a total of 98.4 billion EUR, and has given loans to 19 Member States 1 to cover unexpected and severe increases in the actual and planned public expenditure on STW schemes. Such schemes provide subsidies for temporary reductions in the number of working hours in organisations affected by temporary shocks. The rationale is that such schemes give employers who suffer temporary drops in demand or production a means to reduce their employees’ working hours, instead of making them redundant. The workers receive income support to mitigate the financial consequences of the loss of working hours. To finance the loans to Member States, the Commission borrowed on financial markets and then provided credit to Member States on favourable conditions. SURE ran until 31 December 2022. It is seen as significant not only due to its financial support to Member States, but also because of its nature as a supranational instrument (Corti and Crespy, 2020: 2). It could even be a step towards a European unemployment benefit reinsurance scheme, and thus potentially deepen the EU social project (Anderson and Heins, 2021: 23; Andor, 2020; Béland et al., 2021; Corti et al., 2023).

This article aims to assess whether SURE may be seen as an instrument that, via its eligibility criteria as well as through its actual use by Member States, offers support to all types of workers regardless of their employment relationship. Therefore, the article covers workers on an open-ended employment contract, yet also those in non-standard employment, which in this article includes workers who have a temporary job or are self-employed. The article gives a broad overview of the situation in the EU, as well as exploring three countries in depth: Cyprus, Belgium and Poland. This is a diverse case selection, with the purpose of determining how inclusiveness of workers in STW plays out in different domestic settings. Belgium and Poland already had STW schemes before the pandemic: the Belgian scheme was set up before 2008, while Poland developed an STW scheme during the financial crisis (Cahuc, 2019). Cyprus, however, developed its smaller (seasonal workers) STW initiatives into a broader, more encompassing scheme during the pandemic. Furthermore, Belgium and Cyprus received additional financial support after a second request in March 2021, and Cyprus also received a third and a fourth round of financial support in September and December 2022 respectively. Our information on national schemes stems from academic literature, national reports, Commission proposals and Council decisions on granting financial support under SURE, as publicly available on the Commission's website together with SURE legal documents. By examining diverse cases, we see various ways in which Member States have opened up or have continued to open up their STW schemes to a broad range of workers, in a context where additional funding has become available. In our contribution, we discuss how, at a time when additional financial means were provided by SURE, Member States might have been able to continue or even expand their STW schemes, rather than limiting the use of STW. Such use at the national level could be guided, even in a soft way, by the Regulation establishing SURE. The Regulation sets conditions for the receipt of funding which may affect national choices, although these conditionalities are relatively soft and leave ample room for national design and implementation (e.g. Bekker, 2021).

The article starts with a brief description of the literature on EU initiatives to improve the rights of non-standard workers and to provide access to social security for all workers, including debates on establishing an EU-level unemployment insurance. This is followed by a brief outline of SURE, including the conditions that the Member States need to fulfill in order to be eligible to receive support. Subsequently, the article gives an EU-wide overview of the types of workers who have benefitted from SURE. Next, the article outlines national STW schemes in Cyprus, Belgium and Poland. The conclusion considers whether and how, in a context with additional financial means, Member States have been able to continue or even expand their policies to offer temporary income support to a broad range of workers irrespective of their employment relationship.

EU policies for non-standard workers, STW and SURE

The EU has considered the position of non-standard workers in various directives and policies. In the 1990s it implemented directives on part-time work, fixed-term work and temporary agency work. Although these directives aim at protecting non-standard workers, they have been criticised for not protecting those workers in the most precarious labour market positions (O’Connor, 2013). As of the 2000s, the European Employment Strategy (and later on the European Semester) has addressed the negative consequences of segmented labour markets that create a division between permanently employed and well-protected ‘insiders’, and ‘outsiders’ with fewer rights (O’Connor, 2013). These EU employment policies have been reviewed critically and at times have been found to promote flexibility rather than offering sufficient security to workers (e.g. Burroni and Keune, 2011). In recent years, the need to provide more security to workers has received renewed attention. For instance, the EU Pillar of Social Rights (2017) includes the principle of access to secure and adaptable employment. Some specific initiatives reflecting this principle are the Directive on transparent and predictable working conditions (2019) and the proposed directive on improving working conditions for platform work. Both these initiatives deliberately seek to provide some degree of security to quite vulnerable groups, for instance platform workers, casual workers, domestic workers and workers with short employment relationships.

Apart from better working conditions, the Pillar addresses the right to access social protection regardless of the type and duration of the employment relationship. SURE seems to fit this latter aim as it supports national STW schemes. Moreover, SURE seems to build on longer-running discussions on the development of an EU unemployment (re-)insurance. After the great financial crisis of 2009–2012, the Commission suggested options for establishing automatic fiscal stabilisers, for instance by re-insuring national unemployment benefit schemes in the euro area or by supporting the Member States’ capacity for public investment in case they are hit by a crisis and have to cope with lower revenues and increased spending on unemployment benefits (Dullien, 2013; Kuhn et al., 2020; Vandenbroucke et al., 2020). As yet, no such EU unemployment scheme has been implemented. However, SURE might be seen as a step in the direction of an EU unemployment insurance, albeit a temporary scheme. SURE is a (semi-) automatic stabiliser that acts in the area of employment protection and supports national public spending capacity during external shocks (Fernandes and Vandenbroucke, 2020). It makes it easier for employers to temporarily reduce the working hours of their staff. Reducing working hours is a strong alternative to making workers redundant, and helps to maintain permanent employment levels during economic downturns while maintaining the income of employees (Cahuc, 2019). Moreover, employers may retain their skilled and experienced personnel and prevent future re-hiring costs. STW may encompass a total as well as a partial reduction in the number of hours worked (Eurofound, 2020a). The Commission refers to SURE as the emergency implementation of a European unemployment reinsurance scheme with a particular aim to respond immediately to the pandemic, while underlining that SURE does not preclude the establishment of a permanent unemployment reinsurance scheme (European Commission, 2020b). Thus, future evaluations of the use of SURE may provide further input to the debate on an EU-level unemployment insurance.

There are however quite some differences between SURE and the idea of an EU unemployment (re-) insurance scheme. For instance, SURE is a job insurance scheme that protects jobs rather than an unemployment insurance scheme that gives income support to redundant workers (Andor, 2020; Fernandes and Vandenbroucke, 2020). This difference sparks an interesting question regarding non-standard workers, including the self-employed. Do these groups of workers benefit more from job insurance or from unemployment insurance schemes? Particularly in cases of inadequate access to unemployment benefits, a job insurance scheme might be a better alternative for these groups of workers, if this indeed allowed the prolongation of temporary employment contracts and/or continued assignments for self-employed workers. It could potentially increase the job security of temporary contracts or income security by continued assignments for the self-employed. Currently, the degree to which workers may access STW depends on the Member State. Cahuc (2019) argues that often, STW schemes are more attractive to workers who have an open-ended employment contract than to temporarily employed or self-employed workers. Yet, Mueller and Schulten (2020) state that in the past decade, many EU countries have opened up STW to part-time and fixed-term employees and temporary agency workers.

The positive experiences of Member States with STW schemes has facilitated the implementation of SURE at the EU level (Alcidi and Corti, 2020). However, evaluations of national STW show concerns which might also be relevant to SURE. First, STW may distort the labour market and lead to inefficiency (Cahuc, 2019). For instance, STW may help to retain jobs even if there is no demand for them. This may reduce the reallocation of labour and thus hinder the move towards more productive jobs. Second, STW schemes are not always able to preserve the jobs of non-standard workers. STW often excludes temporary workers, as they do not always qualify for payments (Andor, 2020). Accordingly, temporary workers may be excluded from the labour market, and thus require access to unemployment insurance after all, if they are eligible for it. According to this concern, SURE might not be able to play a positive role in retaining the jobs of non-standard workers. Therefore, from the viewpoint of the non-standard worker, a critical reflection on the need to protect jobs versus workers is welcome. Also from this perspective, the next section first gives a brief description of SURE and its eligibility criteria.

The introduction of the SURE scheme and initial assessments

After a swift adoption, SURE was activated in September 2020. In the same month, 16 Member States were granted financial support through the scheme, and later on the support was expanded to 19 Member States. The legal basis of the SURE instrument is Article 122 TFEU, of which the first part calls for a collective solidarity response between Member States and the second part enables the Union under certain conditions to grant financial assistance to the Member States in cases of exceptional situations beyond their control. Financial support through SURE is provided through loans made on favourable terms, which Member States should use to cover costs of STW or relevant measures with the aim of protecting employment. Every six months, the Commission assesses whether the exceptional circumstances causing the severe economic disturbances in the Member States still exist and reports to the Council. The application process is that a Member State makes a formal request to the Commission, after which the Commission initiates a proposal for a Council decision either to provide or not to provide financial assistance (European Commission, 2020a, 2020b). The amount of 100 billion EUR needed for SURE has been raised through social bonds and is backed up by 25 billion EUR of guarantees paid voluntarily by the Member States. In essence, SURE provides financial assistance to those Member States that cannot protect employment due to a sudden and severe increase in their public expenditure, enabling them therefore to cover the cost of doing so (Article 2 SURE Regulation).

The range of measures that SURE might support seems quite broad, giving Member States considerable latitude in deciding where to target EU funding (European Court of Auditors, 2022). The primary condition for using the instrument is that a Member State ‘may request Union financial assistance under the instrument where its actual and possibly also planned public expenditure has suddenly and severely increased as of 1 February 2020 due to national measures directly related to STW schemes and similar measures to address the socio-economic effects of the exceptional occurrences caused by the COVID 19 outbreak […] where applicable, in support of relevant health-related measures’ (Article 3 SURE Regulation). Thus, SURE supports not only STW but also similar schemes, which gives Member States freedom to uphold spending in particular schemes that match their labour market needs. Additionally, health-related measures may be supported. Moreover, it is not only existing expenditure which may be supported, but possibly also planned public expenditure, leaving some room for new schemes to emerge at Member State level. Article 1 of the SURE Regulation further broadens the scope by stating that SURE is aimed at protecting employees as well as the self-employed, meaning that it may support schemes that encompass more than just employees in regular employment relationships. Temporary workers are not specifically mentioned by the Regulation and seem to fall within the scope of the term ‘employees’.

There is not much literature assessing SURE; however, some pros and cons are mentioned. These resemble the concerns expressed regarding national STW schemes, described above. Among the positive characteristics are that SURE a priori encompasses both employees and the self-employed, thus including, at first sight, a broad range of different types of workers (Corti and Crespy, 2020). Moreover, loans may be accessible relatively easily, on completion of a simple procedure. Also, SURE has instigated policy innovation via its funding, allowing, for instance, a number of Central and Eastern European Member States to massively scale up their STW schemes (Ebbinghaus and Lehner, 2022). Another possible advantage is the rather low level of conditionality attached to the loans. The only aspects that might indicate conditionality are the counter-cyclical operation and the match with a national STW or similar scheme (Andor, 2020: 139–142).

One possible negative aspect described in the literature is that for some Member States, the SURE funds may be too limited. Moreover, due to its temporary nature, SURE gives short-term relief, yet may be unable to address unemployment in the long term (Corti and Crespy, 2020; Corti et al., 2023). On the one hand, one could argue that the high degree of unconditionality in SURE might mean that its only benefit is providing an interest rate differential which makes it cheaper for some Member States to finance their STW schemes. On the other hand, having access to more affordable loans might mean that Member States opt to uphold existing STW schemes or even to expand these schemes to a wider range of workers in society. Even though this article cannot study causal relationships between SURE and the development of national schemes, it illustrates whether and how SURE has provided a positive context of financial support, which enabled Member States to protect the jobs of diverse groups of workers. Before entering into detailed descriptions of STW in Belgium, Cyprus and Poland, the next section gives an EU-wide overview of how Member States have used SURE, particularly with regard to covering non-standard workers.

Overview of the use of SURE

The support that SURE gives to national STW schemes is based on the positive experiences that many governments have had with STW since 2008, in response to the financial crisis (Andor, 2020; Calmfors and Holmlund, 2011). The examples which inspired the EU to develop SURE emerged from the bottom up. In particular, Austria, Belgium, France, Germany, Italy, Luxembourg and Portugal have had relatively large and well-established STW schemes for a long time (Muller, 2020), as have Bulgaria, Croatia, Slovakia, and Poland. Of these countries, Belgium, Italy, Portugal, Bulgaria, Croatia, Slovakia and Poland applied to SURE. There is some lack of clarity in the literature on which countries did not have (comprehensive) STW schemes in place prior to the pandemic, but references are made to Sweden, the UK and Greece (Cahuc, 2019; Muller, 2020) and also Cyprus, Estonia, Latvia and Slovenia (Muller, 2020). Of these countries, Cyprus, Estonia, Latvia, Greece and Slovenia applied to SURE. The instrument was thus able to reach countries with extensive as well as less extensive experience with STW.

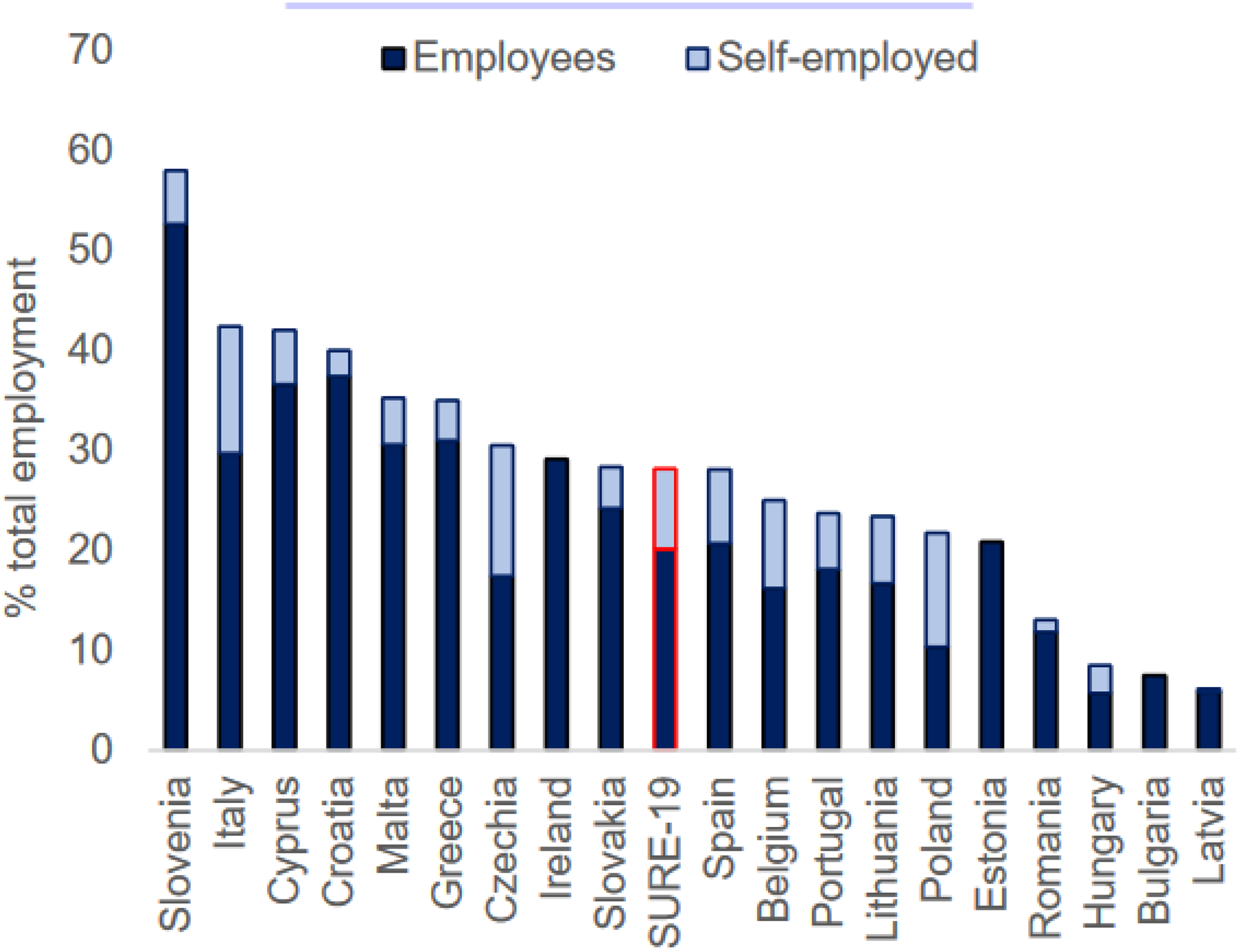

By March 2022, SURE had supported around 34 million people and 2.9 million firms (European Commission, 2022a). This represents almost 30% of total employment and one quarter of firms in the beneficiary Member States. In particular, small firms have benefitted from SURE, as well as firms in the wholesale and retail trade, accommodation and food services and manufacturing. In 2020 and 2021, the workers supported included about 22.25 million employees and 8.75 million self-employed, who were covered by STW schemes and similar measures (see Figure 1). This means that SURE, via the national schemes, was indeed able to support self-employed workers. The figures, however, do not distinguish between regular and temporary employment contracts. In some countries such as Italy, Czechia, Poland and Belgium, self-employed form a relatively large part of the workers supported, whereas in some countries, such as Latvia, Ireland, Bulgaria and Estonia, the self-employed do not seem to be supported via SURE (see Figure 1).

Workers covered by SURE in 2020 (% of total employment). Source: European Commission (2022a).

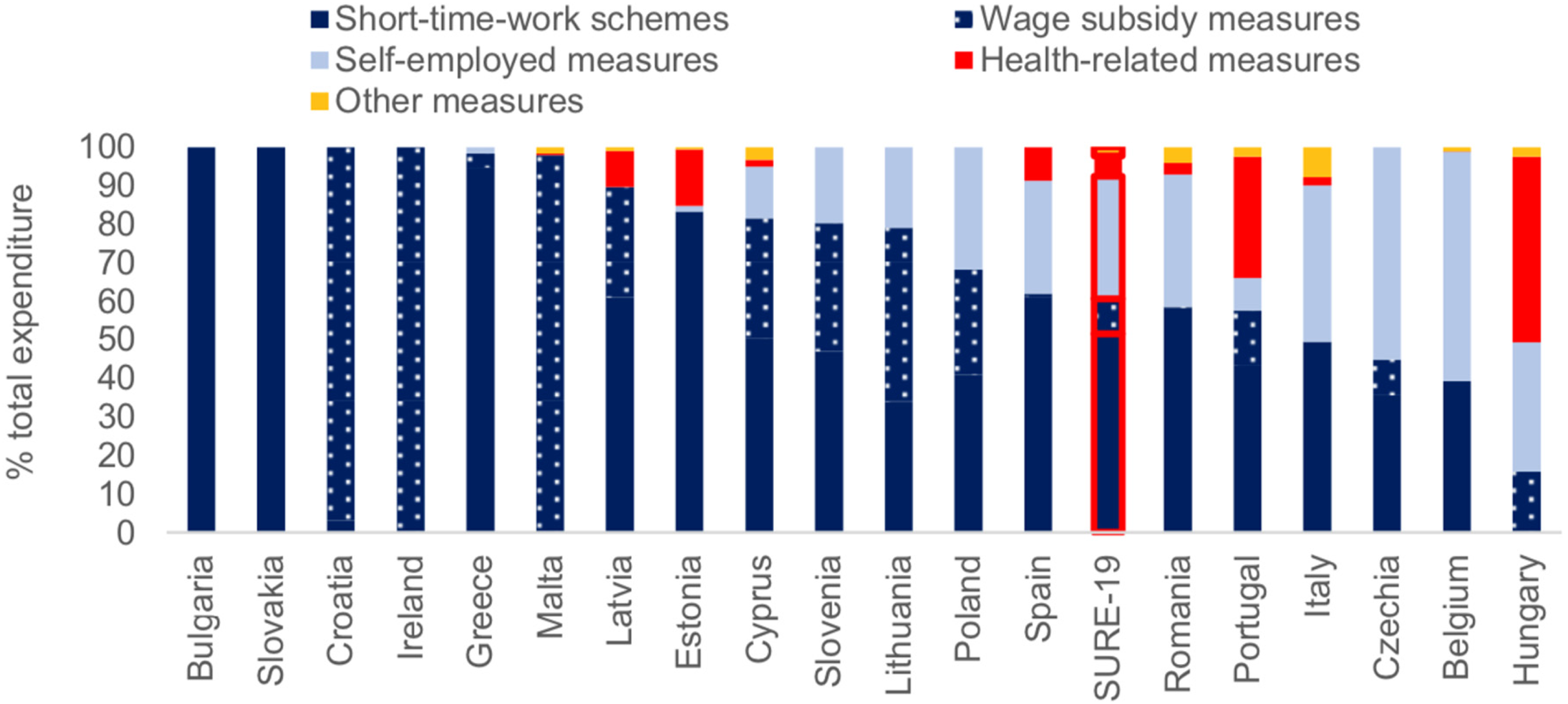

The Commission calculates that SURE contributed to preventing a rise in labour market inequality across Member States, meaning that the evolution of the average unemployment rate between SURE and non-SURE Member States since the COVID-19 pandemic has been relatively similar. This was not the case at the time of the financial crisis (2009–2013), when there was considerable divergence in unemployment rates between core and periphery countries (Andor, 2022). The Commission (2022b) estimates that SURE effectively prevented 1.5 million people becoming unemployed in 2020. These figures should be interpreted with care. The Commission (2021) acknowledges that results are informative; however, it is difficult to design a counterfactual scenario of labour market performance without existence of the SURE scheme. Moreover, the positive outcome may result from a wide range of factors, of which SURE is only one. Based on the self-reporting of Member States, the Commission calculates that 50% of public expenditure on measures that are SURE-eligible is used for STW schemes (European Commission, 2022b). Another 32% is spent on ‘similar measures’ for the self-employed. This appears to be a relatively large part of the funding. It seems that the ‘similar measures’ referred to in the Regulation in practice predominantly refer to measures for the self-employed. Only 9% of SURE expenditure is allocated to wage subsidy schemes, while 5% is spent on health-related measures. About 6% of expenditure has gone to ‘other’ measures that support job retention and workers’ incomes. Wage subsidy schemes may offer a more flexible form of support for firms as these can manage their hours freely without any reporting requirements. Moreover, wage subsidy schemes may incorporate groups of workers with flexible contracts who fall outside the scope of insurance-based short-term employment schemes (Cantillon et al., 2021: 333). However, SURE evaluations do not report in detail on this. Most Member States (16 out of 19) spend at least part of the support from SURE on STW schemes (see Figure 2). From the figure it seems that, regarding the three countries this article explores in detail, Belgium has used SURE-eligible measures to support self-employed workers, as have Poland and Cyprus. Additionally, in Poland and Cyprus considerable public expenditure was devoted to wage subsidy measures. The next section focuses more closely on the measures taken by Cyprus, Poland and Belgium.

Public expenditure on SURE-eligible measures by type of expenditure. Source: European Commission (2022a).

The use of SURE in Cyprus, Belgium and Poland

This section describes the STW schemes in Belgium, Cyprus and Poland, in order to provide more detailed information on the type of workers that benefitted from SURE-supported schemes. For all three countries the application process went swiftly, with a Commission proposal in August 2020 and a positive Council decision in September 2020. The analysis assesses the arrangements of the national STW schemes and whether and how self-employed workers and employees on temporary employment contracts are covered by the schemes.

Short-time work and SURE in Belgium

Via SURE, Belgium became eligible to finance some new as well as existing measures:

The temporary unemployment scheme; The COVID-19 related replacement income for the self-employed: ‘crisis bridging rights’; The COVID-19 parental leave; Various regional and community income schemes, such as a compensation premium for companies for expenditure to support the self-employed and one-person companies; Health-related measures in the German-speaking community.

In March 2021, Belgium made a new request for additional financial assistance from SURE for existing as well as new measures. In April 2021, the Council agreed on additional financial assistance, amounting to more than 8 billion EUR.

The roots of the Belgian STW scheme lie in the law-decree of 28 December 1944 on social security of workers (temporary unemployment), allowing employers to suspend some employees from working, either totally or partially (see also working time flexibility, Labour Act of 29 March 2012). This applies to blue-collar workers, to employees in case of economic hardship, and to those whose employability has been affected due to bad weather conditions or a case of force majeure, upon the condition that all recuperation days have been exhausted and a collective agreement has been concluded (ETUC, 2020). Furthermore, the measures need to be temporary and they must involve a group of workers, for example all workers employed in one sector within a company. Since 2016, the beneficiaries (i.e. the workers) are granted 65% of their wage regardless of their family composition and marital status. In case of a total suspension of working activities, the benefit is granted for four weeks, and at least one working week must then go by before being eligible again for the grant. Moreover, when work is suspended for short periods of time, the employee must work either at least three days per week or at least one week every two weeks. If the suspension is for a longer period, the employee must work less than three days a week or less than one week every two weeks.

In response to COVID-19, Belgium relaxed the requirements for STW between March 2020 and June 2022 (RVE, 2022). A more flexible application of the concept of force majeure applied during this period, meaning that all cases of temporary unemployment due to COVID-19 were considered as cases of force majeure (Hendrickx et al., 2020). Additionally, Belgium increased access and coverage for employees whose work was reduced or suspended due to a reduced workload or the social distancing measures imposed by the government. Measures were opened up further to new types of workers, including white-collar workers, temporary workers, and employees who had been working abroad in an infected region and upon their return were placed in quarantine. Still, Belgium only exceptionally allowed temporary workers to be maintained on the job retention scheme after their contract had expired (Drahokoupil and Müller, 2021), while at times access to other types of social security schemes for the most precarious types of workers remained difficult (Van Lancker, 2021).

The benefit for temporary unemployment of workers is based on the earned wages, averaging 70% of a (capped) gross salary (Hendrickx et al., 2020), with a supplementary ‘corona’ grant of 5.63 EUR per day, making the actual STW allowance higher than the statutory 70% (Mueller and Schulten, 2020). Moreover, employers may pay a supplement on top of the benefit for temporary unemployment (Hendrickx et al., 2020).

Belgium also introduced special parental leave due to COVID-19, which does not affect the right to the regular parental leave, and which is also financially supported by SURE (Van Lancker, 2021). This leave allowed parents to take time off to provide additional care for their children, due to the closure of a nursery or school, or because they were unable to work when a child is in quarantine. The allowance was higher than under regular parental leave. According to the Council decision, this special leave can be considered to be a similar measure to STW schemes, as explained in Regulation (EU) 2020/672, as it grants income support to employees and helps preserve their job by enabling parents to take care of their children. The scheme was open to employees working full time or at least 75%, and also covered fixed-term employees, as long as they had been employed by their employer for at least one month. Temporary agency workers were also eligible, but also had to have been employed for at least one month (Van Lancker, 2021: 14).

Another ‘similar measure’ that has received funding from the SURE scheme is the so-called ‘COVID-19 bridging right’. This measure has extended the existing replacement income for the self-employed. This benefit was paid in cases where the social distancing measures applied by the government caused total or partial interruption of self-employed activities or a voluntary interruption of at least seven consecutive calendar days within a month. Moreover, a number of regional and community schemes provide income support to the self-employed, one-person companies, and other types of employees who are not eligible for other kinds of income support. Overall, Belgium may be seen as having quite a robust STW scheme that protects many workers well (Cantillon et al., 2021). The self-employed were also well covered during the COVID-19 crisis. It seems that particularly the most vulnerable workers whose employment contracts end or who have very short tenures benefit less from STW. The next country to be examined is Cyprus.

Short-time work and SURE in Cyprus

Cyprus is eligible to receive an amount of 632 million EUR under SURE. According to the Council decision, Cyprus is eligible to finance the following measures:

The special leave scheme for parents; The schemes supporting companies implementing a partial and total suspension of operations; The special scheme for the self-employed; The special scheme for hotel units and tourist accommodation; The special scheme to support businesses related to the tourism industry or affected by tourism or associated with businesses that are subject to mandatory total suspension; The special scheme for supporting businesses exercising special predefined activities; The subsidisation scheme for very small and small enterprises and the self-employed; The sickness benefit scheme.

Before the COVID-19 pandemic, Cyprus only had a STW scheme for seasonal workers (Eurofound, 2021). In response to the pandemic, Cyprus designed new measures that eventually became eligible to receive support from SURE.

Cyprus’ existing measure of income support known as ‘suspended employment in the tourism/catering industry’ applies to employees working in the tourism industry (hotels and restaurants) and in activities related to tourism (ETUC, 2020). This measure is based on an agreement between the Ministry of Labour Welfare and Social Insurance, the employer organizations and the trade unions aimed at preserving the employment relationship between employers and employees over the winter months. The measure came into force in the second half of the 1980s and was reformed in 2003 (Eurofound, 2021). It grants partial unemployment benefits to workers whose employment is temporarily suspended fully or partially for reasons of seasonality (from 1 November to 31 March). During the unemployment period, employees are entitled to unemployment benefits paid by the state, reduced by 2.8% of their basic salary which is paid by the employer. A similar measure is in place for restaurants and recreational centres. This measure has been in force since 1992 following a multi-employer collective agreement between the employers’ representative organization and the trade unions (Eurofound, 2021); it is also endorsed by the Ministry of Labour Welfare and Social Insurance. This collective agreement applies only in the regions of Ayia Napa and Protaras, two touristic areas, where most of the enterprises suspend their operations during winter. According to the regional collective agreement, employers continue to pay part of the employees’ salary, amounting to 10% of the basic salary during the suspension period. Employees benefitting from this measure are entitled to unemployment benefit reduced by the amount paid by the employer.

On 27 March 2020, new legislation (Law 27(I)/2020) came into force which gave power to the Minister of Labour Welfare and Social Insurance to implement extraordinary measures in response to the COVID-19 crisis (Cleridou, 2020: 2). On the basis of this law, the national authorities were granted the power to introduce special support schemes for the unemployed in all sectors (not only in the hotel and tourist industries), and subsequently introduced a series of ‘special unemployment benefits’ (Article 7 of Law 27(I)/2020) (for a description of these schemes see below, points 1–3). Ιn the hotel and tourist sectors, the measures expanded the scope of the established measures as well as extending the period of coverage (for a description see below, points 4–5).

Overall, the series of special unemployment benefits that were introduced include (PWC, 2020; Voskeritsian, 2021):

The special scheme for the complete suspension of business activities (Act ΚΔΠ130/2020. This applied to businesses which experienced a reduction of more than 80% in turnover in compliance with the government’s ‘COVID’ measures. The scheme was introduced in March 2020 and its duration was extended every month until the end of January 2021. The special scheme for the partial suspension of business activities (Act ΚΔΠ131/2020). This applied to businesses which experienced at least a 25% decline in turnover in compliance with the government’s ‘COVID’ measures. The scheme was applicable from March till June 2020 and was then replaced by the schemes mentioned below. The measure was reintroduced in January 2021 until October 2021 (at the time of writing). The special scheme for businesses in certain economic sectors. This measure was created for companies that do not operate in the sectors specified in Law 27(I)/2020 and experienced, or foresaw experiencing, a 40% reduction in their total turnover compared with the same period in 2019 (this was changed to 35% in August 2020 and back to 40% from September 2020 onwards). This scheme was introduced in June 2020 and lasted until December 2020. The special scheme for hotels and hospitality (Act KΔΠ393/2020). This scheme offered income compensation to support employees in the hotel industry and other businesses providing tourist accommodation which completely suspended their activities or experienced a decline in turnover of more than 40% compared with the same period in 2019 (this was changed to 35% in August 2020 and changed back to 40% from September 2020). In November 2020 an additional criterion applied: companies that were not operating in November 2019 (and hence had no basis for comparison) could apply to the scheme if their occupancy was lower than 60%. The special scheme for business linked to, or affected by, tourism, or for businesses linked to suspended businesses that were subject to mandatory total suspension or experienced a decline in turnover of more than 55% (Act KΔΠ270/2020). Schemes (4) and (5) were introduced in June 2020 and were in force until October 2021 (at the time of writing). Both schemes applied to everyone whose employment was linked to the tourism or hotel or restaurant sectors. For instance, the schemes opened up the ‘suspended employment in tourism/catering industry’ regime to also include travel agents, airport handlers, shipping company employees, etc. Also, the schemes amended the period of application of the measure, to extend it beyond the ‘winter months’.

A precondition for the employer to receive the grant was that employees should not be dismissed during the period of receipt of the grant (ETUC, 2020). The duration of payment depended upon the period of suspension of the employer's activities due to the pandemic.

Anyone employed by a company was eligible to receive support, including standard and non-standard workers, meaning workers with a temporary work contract, platform workers, temporary agency workers, multiparty employment, etc. (Law 27(I)/2020). Nevertheless, an application could only be submitted if the employee was insured with the Social Insurance Services in January 2020 (Act KΔΠ189/2020). In that case, the benefit covered 60% of the employee's original salary or 60% of the employee's social insurance units earned in the year before, whichever was the greater, calculated according to the Social Insurance Law, and ranging between a maximum of 1214 EUR and a minimum of 360 EUR. If the employee was not entitled to unemployment benefit, i.e. was not registered with the Social Insurance Services, the amount of the benefit was calculated based on 60% of the monthly gross salary paid in January 2020, or if hired after January 2020, on 60% of the monthly gross salary in the month of hiring (Voskeritsian, 2021).

For the unemployment benefit paid under the – already established – STW schemes for seasonal workers (described above in points 4 and 5), a different calculation method applies. More precisely, the amount is calculated in accordance with the established rules, i.e. employees are entitled to unemployment benefits paid by the state, reduced by 2.8% of their basic salary paid by the employer, or if a collective agreement is in place (regions of Ayia Napa and Protaras), employers continue to pay 10% of the employees’ basic salary.

Moreover, Cyprus implemented ‘similar measures’ to the STW scheme with a view to supporting the self-employed. In particular, the so-called ‘Supplementary budget, temporary framework for state aid measures to support the economy in the current COVID-19 crisis’ provided subsidies for very small and small enterprises and the self-employed who employ up to 50 employees (Act ΚΔΠ129/2020). This special scheme also applied to the self-employed who could not exercise any activity or who experienced up to 25% turnover reduction due to the restrictive measures imposed by the government in response to the pandemic. The benefit ranged between a maximum of 900 EUR and a minimum of 300 EUR, as a lump sum grant. Nevertheless, this scheme was not open to certain professions – the list was updated on a monthly basis – based on the effects of COVID-19; also, a self-employed person was not eligible to receive this benefit if they were receiving unemployment benefit or any other benefits from the Social Security Fund (Voskeritsian, 2021).

Cyprus introduced a special leave scheme providing wage compensation to parents employed in the private sector who have children up to the age of 15 or children of any age with disabilities (ETUC, 2020). This was a measure in addition to the normal parental leave. It can be described as a STW measure since it provides income support to employees (standard and non-standard workers as long as they were registered with the Social Insurance Services in January 2020 or had a legal employment contract since day one of employment in the month of hiring) who need to take care of their children due to closure of school or other institutions or due to infection from COVID-19, while preserving their employment. A similar measure introduced a sickness benefit scheme providing wage compensation to private sector employees and to the self-employed. To receive this benefit, an individual must be either classified as a vulnerable individual (according to a list published by the Ministry of Health, e.g. must have a chronic disease), have been placed in quarantine by the authorities or infected by COVID-19. The benefit covers 60% of the employee's original salary or 60% of the employee's social insurance units earned in the previous year.

This section explained that Cyprus did not have any kind of STW scheme in place prior to the pandemic, with the exception of the seasonal worker (sectoral) schemes. To mitigate the impact of the pandemic on employment and finance, Cyprus designed new measures and extended the current sectoral STW schemes that were also eligible to receive support from SURE.

The next section describes the SURE and STW structure in Poland.

Short-time work and SURE in Poland

Poland is eligible to receive an amount of 11.2 billion EUR under SURE. According to the Council decision, Poland may finance the following measures:

A reduction in social security contributions for the share of expenditure related to the support of self-employed persons, all social cooperatives (regardless of the number of employees) and, for companies employing up to 50 people, the share of expenditure in respect of employees who were continuously in employment; A downtime benefit for self-employed persons and those working under civil law contracts; Subsidies towards salaries and social security contributions of companies and other entities that use short-time work or voluntarily reduce working time or when the employees were continuously in employment; Subsidies to self-employed persons without employees;

Loans convertible into subsidies granted to self-employed persons, micro-companies and non-governmental organisations, for the amount actually converted

According to the Commission (2022a), Poland has reported lower total public expenditure on SURE-related measures than the amount granted, as measures changed due to a stronger than expected rebound in the economy. In recent months the Commission has been in consultation with the Polish authorities to discuss next steps, including postponing the disbursement of the remaining funds. In December, Poland received the remaining 1.5 billion EUR.

Like Belgium, Poland already had a STW scheme prior to the COVID-19 pandemic (ETUC, 2020). The government implemented the ‘Act on the alleviation of the impact of the economic crisis on employers’ to provide support for temporary layoffs and STW, whereby employers experiencing temporary financial issues could reduce the working time of employees to a maximum of 50% of their normal working time for a period of up to 6 months (ETUC, 2020). If so, according to the Act, an employer is eligible to apply for temporary state assistance to cover part of the workers’ remuneration. The Act further states that the employee is eligible to receive from the employer at least 50% of his/her current remuneration but not less than the national minimum wage (ETUC, 2020). Employees are also partially reimbursed by the state.

To counteract the economic effects of COVID-19 and in response to the public health crisis, the Polish government introduced a package of three legislative acts (Aidukaite et al., 2021). One of the legislative acts, named the ‘Anti-Crisis Shield’, proposed social policy measures including employment protection and support for businesses’ economic activity (Eurofound, 2020b). For employers to receive employment protection they must have been either forced to stop their activities due to COVID-19 or they were left with no other option but to reduce working time. In case of the former, employers must prove a reduction in turnover and could then receive compensation of all labour costs up to 50% of the minimum wage. Small and medium enterprises could receive support proportional to the degree of loss in turnover, covering up to 90% of all labour-related costs if loss in turnover reached 80% (Aidukaite et al., 2021).

Regarding reductions in working time, the authorities rapidly adjusted the ‘Act on the alleviation of the impact of the economic crisis on employers’ by simplifying access to the scheme for firms (ETUC, 2020). This was done by reducing the thresholds for the economic justifications that a business needs to provide to request STW support. In particular, according to the new rules, a company can claim a subsidy if its revenue has fallen by a minimum of either 15% or 25% (ETUC, 2020). If one of these conditions is fulfilled, the employer can reduce the working time of employees by 20%-50% and receive benefit support up to 50% of the average pay including the social security due for 3 months from the state (Guaranteed Employee Benefits). Moreover, the employer has the option to suspend business activities and receive a benefit support of 50% of the statutory minimum wage (ETUC, 2020). If the employer is receiving state support through the STW scheme, it cannot dismiss employees. Furthermore, the employer is obliged to reach and sign an agreement with trade unions or employee representatives either before or after submitting an application for state aid in order for the application to be valid and complete (ETUC, 2020).

The authorities also introduced a downtime benefit for the self-employed and individuals employed under civil law contracts who have experienced a decrease in income due to the pandemic (Florczak, 2020). Civil law contracts are alternative forms of employment that involve contracts to perform a specified task, order contracts or cooperation with self-employed persons. These contracts do not provide protection defined in labour law provisions, and their application is limited by the law even though they are very common (Chłoń-Domińczak et al., 2021). In 2020, the self-employed could receive a lump sum benefit equal to 80% of the minimum wage (Florczak, 2020). Non-standard workers, such as those employed under civil law contracts, also received a lump sum benefit up to 80% of the minimum wage as compensation for a fall in revenue. Additionally, the authorities have introduced a measure that offers loans convertible into grants to the self-employed, micro companies and non-governmental organizations (Florczak, 2020). The loans can be converted into grants if the recipient continues its activities for three months after the loan is paid. Importantly, for the measure to meet the requirement of being public expenditure (so it can qualify for support under Regulation (EU) 2020/672), only expenditure relating to loans being converted into grants is considered.

Similarly to Belgium and Cyprus, Poland also established a scheme for working parents with children staying at home due to school or day-care closure or infection by COVID-19. This measure applied also to non-standard workers and the self-employed (Chłoń-Domińczak et al., 2021). In particular, if a creche, kids club, kindergarten or school was closed, insured parents with children up to the age of 8, or up to the age of 18 in the case of children with special education needs, were entitled to an additional care benefit during the whole period of closure at 80% of their previous salary (Aidukaite et al., 2021). Moreover, employees or self-employed workers returning from abroad and their household members in quarantine were eligible for a grant of 80% of their gross salaries or average revenue.

Chłoń-Domińczak et al. (2021) discuss the lack of immediate support to people who became unemployed due to the pandemic, as the measures were introduced only in July 2020. Moreover, the support provided to non-standard workers and the self-employed was lower than for standard employees, since ‘the lockdown allowance could be claimed up to five times, while regular workers were covered by both the co-financing of wages and social insurance contributions; they could also claim unemployment benefit’ (Chłoń-Domińczak et al., 2021: 39). Nevertheless, the report acknowledges that the lockdown allowance was a novelty, since prior to the pandemic, workers on civil law contracts did not have access to any social security benefits if they were not registered with the Social Insurance Services.

Main findings and conclusion

This section compares countries and answers the question of whether and how SURE, via the national STW scheme, may benefit non-standard and self-employed workers. The majority of countries that have received financial support via SURE have been able to use this in national STW schemes that are open to workers as well as to the self-employed (see Figure 2). The three detailed case studies show how countries have done this, indicating that the countries have either modified or introduced STW schemes with the aim to provide support to standard employees, non-standard workers, as well as to the self-employed. Additionally, in all three countries schemes have supported working parents whose children could not attend school due to lockdowns or COVID-19 infections. Thus, the pandemic has been a time for experiments on opening up STW schemes to businesses and workers who normally would not be covered. The three countries show how STW schemes have been broadened or opened up by making eligibility requirements more flexible or by lowering applicable thresholds. This seems to be most evident in Belgium, where a very broad definition of force majeure was implemented and the scheme was extended to also cover white-collar workers and non-standard employees. Regarding Poland, clear reference is made to individuals employed under civil law contracts, who form a relatively large group of non-standard workers. Due to the introduction of STW, they too can receive financial support if they experience a reduction in their income. The situation in Cyprus tends to be less clear-cut. Even though STW measures were introduced to support employees, and the established STW schemes for seasonal workers opened up their scope and period of application, still, no clear or specific measures were implemented to support non-standard workers. However, all three countries have some type of STW scheme to support the self-employed. This is quite an innovative way of supporting workers without an employment contract. It is in line with the Pillar of Social Rights, which advocates the access of workers to social security irrespective of their employment relationship and duration. Support via STW might even be crucial for non-standard workers, as they often have less access to unemployment benefits. Thus, in the absence of income protection, giving job protection via STW arrangements might be a key facility for those in a more vulnerable labour market position. Lastly, the three countries have all developed schemes for parents whose children were not able to attend school due to COVID-19. These include (mostly) parents with non-standard jobs, although sometimes only those working in the private sector.

Overall, this article suggests that when receiving EU financial support via SURE, policy innovation occurred at the national level, including the broadening of STW to non-standard workers. This is in line with the broad range of schemes that the Regulation establishing SURE allows, mentioning support to STW and similar schemes, as well as to workers and self-employed; in the three countries it was even extended to parents who had to stay at home due to the closure of schools. However, although SURE stimulated national STW, the inclusiveness and quality of support still depends on national choices and policy design.

Although policy innovations may be seen at the national level, the three countries also show that STW schemes are less able to protect the most vulnerable workers, for instance workers with a short tenure or workers whose temporary contract has been terminated. Also, there are different degrees of support, amount and duration of income replacement. In cases where STW does not suffice, other income support schemes should be in place that mitigate the effects of unemployment. Not only do jobs need to be protected, but workers need protection as well. However, in reality unemployment benefit schemes are not always accessible to the most precarious workers (e.g. Spasova et al., 2021). Whereas SURE provides assistance to national schemes covering workers with different types of employment relations, further steps could be taken to ensure access of workers to adequate income support, irrespective of their employment relationship. Moreover, given the temporary nature of both SURE and of most of the national STW schemes developed during the pandemic, it is time to think about more structural schemes that can mitigate the fall in income of all types of workers, even outside times of crisis. This could be done by developing more inclusive job protection (STW) and/or more inclusive income protection (unemployment benefits).

Footnotes

Acknowledgements

We would like to thank the anonymous reviewers for their constructive and helpful feedback.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.