Abstract

In the wake of the deepest and longest recession that the United Kingdom has experienced since the 1930s, the consequences of Brexit and now COVID too, this article examines the origins, sustenance and puncturing of the growth dynamic it enjoyed since the early 1990s. It identifies what is termed the ‘Anglo-liberal growth model’ and its social policy corollary, ‘asset-based welfare’, considering the symbiotic yet increasingly tense and dynamic interdependence of the two. It argues that although both are compromised by the compound shocks of the crisis, Brexit and COVID, they have in fact become more not less intertwined and interdependent in these more troubled times. It considers the implications for the long-term sustainability of this fractious coupling and the wider consequences for UK economic performance and social welfare in the years ahead.

Keywords

Introduction

Since around the turn of the century, ‘asset-based welfare’ (ABW) has emerged as a putative public policy solution to the growing problem of Anglo-liberal welfare residualism. It seeks (or sought for as long as it lasted) to take advantage of the benign economic conditions of the ‘great moderation’ (Blanchard and Simon, 2001) – more precisely of ‘non-inflationary continuous expansion’ (NICE) – before the crisis and the distinctive model of growth with which it came to be associated in countries such as the United Kingdom, Ireland, Australia and the United States. It is predicated on the simple idea that if privately acquired assets are likely to grow in value stably and predictably over time, then their acquisition by citizens is a better way to insure themselves against the loss of income of unemployment, ill health and, above all, retirement than publicly funded and collectively provided welfare. Duly incentivised and appropriately supported through public policy, ABW might help to insure citizens collectively against an increasingly uncertain future.

Put in such terms, it is tempting to see ABW as a peculiar, distinct and – in its origins at least – distinctly Anglo-liberal public policy solution to a distinctly Anglo-liberal problem. But such a solution has come to acquire and continues to acquire today a potentially far wider relevance in a context of demographic change and the austerity demanded by the European debt state’s creditors (an idea well-captured in Wolfgang Streeck (2014) description of the ‘consolidation state’). As such, ABW has increasingly come to be seen as offering a solution of a more general kind. In the process, and particularly since the crisis, it has become more widely diffused beyond its Anglo-liberal core (for a wider consideration of its complementarity with other growth models in Europe, see Benoit and Hay, 2023).

For its proponents and supporters, ABW was (and to some extent, still is) seen as a way of compensating citizens-as-workers for a combination of growing public welfare residualism (itself reinforced by austerity), the gradual inter-generational dissolution of the social citizenship contract and for their declining profit share. It represents a passing of the responsibility for such compensation to citizens themselves from the state. It is, in short, an individualisation and a liberalisation of the responsibility for meeting anticipatable welfare needs, requiring citizens to balance prospective public and private income streams and to engage in individuated risk assessment in asset portfolios. Indeed, it is precisely in this respect that it is Anglo-liberal both in its origins and in the disposition it reflects. It constitutes a potentially neat and seemingly attractive solution to the dual problems of retrenchment and population ageing. Or at least it did, before the onset of global financial crisis, Covid and Brexit.

This article seeks to assess the viability of ABW in an era in which the asset-appreciation on which it was first predicated is neither stable nor guaranteed. The argument unfolds in three stages. In the first, I chart the rise of ABW in its European heartland, the United Kingdom, before the crisis – examining, in particular, its typically unacknowledged dependency on what I will term the ‘Anglo-liberal growth model’. In the second, I consider the challenge posed by the crisis, above all to the previously unproblematic interdependence of ABW and Anglo-liberal growth. I see the crisis, reinforced by COVID and Brexit, as driving a wedge between Anglo-liberal growth (reliant as it on private debt-fuelled consumption) on one hand and ABW (reliant on the deferral of consumption inherent in long-term asset-accumulation) on the other. In a shorter final section, I consider the implications of this for the sustainability of ABW in the light of the still ongoing attempts of consecutive UK governments since 2008 to re-prime the asset-price dynamics on it rests.

The specificity of Anglo-liberal ABW

The term ABW, at least as I will use it in what follows, refers to a public policy solution (or, more accurately, a prospective solution) to both a specific and a wider problem. The specific problem is the growing failure of public pensions to provide for (and, in so doing, to meet the expectations of) an ageing population in a context of sustained (and now accelerating) welfare residualism, exacerbated by post-crisis austerity, Brexit and the legacy of the COVID crisis. The more general problem, of which the UK predicament is but an example (albeit of a particularly acute kind), is the wider crisis of affordability of public pension provision in a context of long-term population ageing, increases in life expectancy and a secular decline in birth rates. It is this that has made ABW so attractive to public policy-makers beyond the United Kingdom and the Anglosphere (Benoit & Hay 2023).

Before moving to a more detailed and substantive account of Anglo-liberal ABW policy, it is important to understand both the origins of the term and its use in what follows. The term itself was first used in the UK context by Blair’s New Labour administration in direct reference to the normative political theory of Michael Sherraden (1991; McKernan and Sherraden, 2008). Following Thomas Paine and Antonie-Nicolas Condorcet, Sherraden argued that poverty eradication strategies were better predicated on transfers of assets rather than income since, in contrast to the latter, assets need actively to be tended by their recipients if they were to generate an effective income stream. This activation of the recipient was seen as normatively preferable in Sherraden’s (somewhat paternalistic) moral political economy.

Such a conception clearly appealed to New Labour thinking with its emphasis – as in Giddens’ (2013) ‘third way’ – on the obligations and duties of citizenship as well as with its more practical focus on labour-market activation strategies. But there is a need for caution here. For it would be wrong to imply that Sherraden’s normative justification for ABW ever fully captured New Labour’s rationale for exploring the social policy corollaries of the growth model it has inadvertently served to build. And if the relationship between the originating idea and the practice to which it has given rise was, from the start, somewhat tangential, it has only become more so in the two decades following the first public use of the term.

As this suggests, rather than the expression of a strong normative commitment to assets over income and benefits as a means to deliver welfare, ABW is perhaps better understood as a rather more pragmatic and expedient social policy complement to what I will term the Anglo-liberal growth model.

By this, in turn, I refer to the pervasive model of growth that emerged in the United Kingdom and in a number of other economies in the 1990s and that was largely responsible for the sustained period of growth that these economies enjoyed before the global financial crisis (on the specificities of the Irish case, see Hay et al., 2008; Ó’Riain, 2014; Smith, 2005; and on Australia, see Adkins et al., 2020, 2021, 2023). That model of growth has more typically been referred to as ‘privatised Keynesianism’ (Crouch, 2008, 2009).

Here, as elsewhere (Hay, 2013), I prefer to refer to it as the ‘Anglo-liberal’ growth model. But it is important to be clear about what such a term implies and does not imply. There is plenty of room for ambiguity here and it is important to clear up that ambiguity before we proceed further. In a literature typically dominated by comparative institutionalist perspectives, the term ‘Anglo-liberal’ might be assumed to refer to a variety of capitalism or welfare capitalism (and hence to all liberal or Anglo-liberal market economies). To use the term in this way, in referring to the existence of an Anglo-liberal growth model, would be to imply that all such economies (all similarly configured capitalisms) are likely to share a growth model of a similar or equivalent kind. That is not my claim here. For by Anglo-liberal, in the context of these reflections, I refer to an ideational dispositional and not to an institutional form (whether of capitalism, of the state or of the welfare state). What I am suggesting is that the UK growth model over this period bears the imprint of the bringing to bear of a recognisably Anglo-liberal (as distinct from neoliberal, republican or social democratic) sentiment or disposition to questions of growth (see also Berry, 2021; cf. Macnicol, 2015). While we might expect the prevalence of an Anglo-liberal disposition to co-vary with institutional variables (such as the form of one’s capitalism), I am not claiming that the Anglo-liberal growth model that I identify here (and that others have termed ‘privatised Keynesianism’) is likely to be present in the same way wherever Anglo-liberal institutions or capitalisms are to be found. Anglo-liberalism, as a dispositional, can be applied in rather different ways and is, as such, likely to be both case-specific and to leave rather different traces on the growth models it inspires. 1

Central to the UK Anglo-liberal growth dynamic is the role played by private rather than public debt (typically secured against a rising property market) and the associated release of equity (and, more simply, the sale of assets) that it facilitated in boosting aggregate demand and in fuelling consumption (Crouch, 2008, 2009; Hay, 2013; Watson, 2010).

It was this, I suggest, that made possible ABW. And by that, in turn, I mean the encouragement, incentivisation and direct facilitation through public policy of the accumulation by citizens of appreciating assets to provide for future welfare needs. It implied, as it continues to imply, the deferral of consumption by citizens and it proceeds through an essentially financialised model of saving-as-investment. It, too, is Anglo-liberal (rather than neoliberal) in character in that the private insurance model that it proffers is both understood to deliver a collective or public good and is actively supported by public policy. 2

What is clear is that Anglo-liberal ABW and the Anglo-liberal growth model in this understanding share a common reliance on stable asset-price appreciation and, in turn, easy access to credit and a stable low inflation–low interest rate equilibrium (or ‘non-inflationary continuous expansion’). In what follows I seek to explain how this worked – for as long as it worked – and what has happened since it ceased to be the case.

ABW as a renegotiation of the citizenship contract

Crucial to ABW is the assumption by citizens of an individual (and individuated) responsibility for securing the means for the satisfaction of their prospective welfare needs through the accumulation of assets. No less crucial is the taking of responsibility for any associated deferral of consumption necessary for the accumulation of such assets. The assets they acquire (or more accurately, the anticipated proceeds that come from divesting of them at some point in the future) effectively insure them against the risk that the public benefits to which they are (or will, at the relevant time be) entitled will prove insufficient to cover their welfare needs.

The logic is, then, essentially one of compensation. And the degree of compensation required needs calculating. Implicitly, then, citizens become responsible not just for acting responsibly but working out what that means, by gauging (or projecting) for themselves:

- the extent of their future welfare needs (and their cost);

- the extent of the deficit or shortfall arising from the anticipated failure of extant public pension (and associated) rights to cover such needs (and their cost);

- the extent of the asset-appreciation (and associated deferral of consumption) likely to be necessary to achieve a sufficient accumulation of assets over the required time frame to compensate for such a shortfall; 3 and arguably,

- the extent to which a crash course in actuarial mathematics or, at minimum, financial literacy might be a condition of assessing any or all of the above.

The implicit model of the citizen here is not just the citizen as savvy investor (Finlayson, 2009; Langley, 2020; Watson, 2010), but the citizen as actuarial mathematician. It is perhaps unsurprising in this context that the introduction of Child Trust Funds (a form of ABW targeting the young) was linked directly to classes in financial literacy in schools (enshrined in the National Curriculum) and the rolling out of financial literacy education for adults (with the Citizens’ Advice Bureau’s Financial Skills for Life) and with the newly created Financial Services Authority being given with a mandatory responsibility for financial education from its inception.

But it would be wrong to see ABW as simply the acquisition of new responsibilities by citizens. It is also, crucially, the passing or displacement of responsibility for meeting the future welfare needs of citizens to those very same citizens from the state. It is, in effect, a re-negotiation (or, in the absence of any dialogic process of deliberation involving citizens, the retrospective imposition) of a (revised) citizenship contract. And one which makes citizens responsible, at the individual level, for something – their collective insurance against social risk – for which the state was previously their guarantor.

What arguably made this possible, both economically and politically, was (1) sustained asset-value appreciation; (2) a growing awareness among public-policy makers of such asset-value appreciation; and (3) a confidence on their part that this was likely to be sustained. Had any one of these conditions not been met, it would not have been credible to think that future welfare needs could be secured through such an individuation of responsibility (sustained, encouraged and reinforced, of course, by a variety of direct and indirect public policy interventions and incentives).

And what, in turn, made all of that possible was the Anglo-liberal growth model itself and the ‘great moderation’ (both as an established empirical trend and, just as significantly, as an economic thesis). But what arguably also contributed to the willingness of policy-making elites to buy into such thinking was a combination of additional factors and beliefs. Among these were: (1) demographic change and the sense that ABW might provide a serendipitous solution to it at a time when no other solution was on offer; (2) the recognition that it was already the case, a decade before the credit crunch and the global financial crisis, that welfare residualism was threatening broad swathes of future retirees with prospective precarity in old-age; (3) the pervasiveness of economic liberalism and with it the idea that citizens should be encouraged to take individual responsibility for their welfare wherever possible; and (4) the, at least ostensibly egalitarian, sentiment in New Labour’s thinking that access to the (at the time, high yielding) asset appreciation strategies of the wealthy should be broadened (and that the poor, as it were, should be invited and/or dragged to the asset-appreciation banquet). 4

In short, a variety of ideational, economic, socio-economic and political conditions conspired to make ABW look like a serendipitous, mutually advantageous and even credibly egalitarian complement to the Anglo-liberal growth model – its social policy corollary, in other words. That combination of factors was not set to endure.

Anglo-liberal growth before the crisis

To understand the initial appeal to policy-makers of ABW in its UK ‘home’, we need to understand the evolution of the growth model of the United Kingdom in the period before the crisis. We will come to its current plight in less auspicious conditions presently.

Most commentators now acknowledge that, from some time in the mid-1990s, the United Kingdom came to develop a particular kind of growth dynamic, often now referred to as a model. It has been termed, variously, the ‘new financial growth model’, ‘privatised Keynesianism’ or ‘house-price Keynesianism’. For reasons already set out, I prefer the simplicity of the ‘Anglo-liberal growth model’. While it is certainly credible to trace its origins in the particular ‘variety of (welfare) capitalism’ to which the United Kingdom conventionally belongs (Esping-Andersen, 1990; Hall and Soskice, 2001), its emergence as a growth model might more directly be traced to a series of core market liberal reforms since the 1980s (Hay, 2013). Yet the resulting growth model is best seen as a largely unanticipated and unsought consequence rather than the product of a more conscious strategy – the application of a disposition rather than the unfolding of a plan. This notwithstanding, from around the turn of the century onwards it is not difficult to discern within the UK government, HM Treasury especially, a more conscious and strategic awareness of this as a growth model. What was initially stumbled across serendipitously came to be acknowledged as the basis of growth and, indeed, the premise for a series of other strategies, particularly the concerted move towards ABW.

Establishing the preconditions of Anglo-liberal growth

It is not difficult to discern in the political decisions, which set the context for Anglo-liberal growth (and, indeed, in the dispositions of those making them) a persistent market liberalism. The step-level decrease in interest rates which set the economy on the path to sustained consumer-driven economic growth occurred, of course, in the most unpropitious of circumstances – with the devaluation of sterling arising with its forcible ejection from the Exchange Rate Mechanism in September 1992 (‘Black Wednesday’). Yet, crucially, this was further reinforced by two decisions made by the incoming Labour administration of Tony Blair in 1997. These were the granting of operational independence to the Bank of England and, perhaps more significantly still, the commitment to the stringent spending targets set by the outgoing government of John Major (arguably, at a point when the latter had already discounted the prospect of its own re-election). Although this self-imposed fiscal conservatism was almost certainly the product of perceived electoral expediency (bound up with notions of how best to be seen to be economically competent) rather than with more directly economic judgements, this latter decision led Blair’s administration to run a substantial budget surplus between 1997 and 1999. The resultant rescaling of national debt served to increase the sensitivity of demand in the economy to interest-rate variations and, in the process, helped further to institutionalise a low interest rate–low inflation equilibrium. This was the foundation on which Anglo-liberal growth would rest and, of course, ultimately perish (at least in its initial incarnation).

Yet, as is now increasingly acknowledged, it was not just low interest rates that served to inflate the growth bubble (and the asset-price bubble sustaining it) – certainly in the United Kingdom. Crucial, too, was the liberal and increasingly highly securitised character of the mortgage market (Schwartz, 2009; Schwartz and Seabrooke, 2008; Watson, 2008). For it was this that allowed mortgage debt to be packaged in such a way that the originators of loans bore little or none of the risk associated with the credit they were extending – at least for as long as house prices remained stable or rising. And, while house prices were on an upwards trajectory, the returns to be gained on mortgage-backed securities made them a very high-yielding investment vehicle indeed. Of course, mortgage-backed securitisation was established first in the United States, with Fannae Mae, for instance, buying mortgages and selling them on as securities from as early as 1938 (Thompson, 2009). It would take the liberalisation and deregulation of financial markets in the mid 1980s to bring this to London (Oren and Blyth, 2019). But once this occurred, London and New York effectively engaged in a game of competitive deregulatory arbitrage, establishing in the process the regulatory preconditions for the inflation and bursting of a bubble in mortgage debt. To be clear, policy-makers (on both sides of the Atlantic) did not seek to liberalise financial markets in order to make possible the mortgage-backed securitisation that would serve to channel credit to the housing market, driving up demand and prices. They did so more because their pro-market (‘Anglo-liberal’) disposition inclined them to think this was an inherently good thing to do. But the effect was the same.

As such, a conviction as to the allocative efficiency of lightly regulated markets was a necessary, if not sufficient, condition of Anglo-liberal growth. Thus, it was the passing of the Financial Services and Building Societies Acts of 1986 that paved the way for US investment banks to establish mortgage-lending subsidiaries in London (Langley, 2006). They brought with them the securitisation of mortgage debt, albeit at a level far below that reached in the United States. The practice was rapidly diffused throughout a retail banking sector swollen by the demutualisation of the building societies (Wainwright, 2009). Once again, a liberalising disposition was responsible for establishing a core institutional precondition (here mortgage securitisation) of the emerging Anglo-liberal growth model.

The essence of the Anglo-liberal growth model

It is tempting to see in the growth model, which has characterised the UK economy since the early 1990s rather more conscious strategising than is genuinely warranted. As already suggested, it is simply inaccurate to see policy-makers as animated from the start by a vision of the growth model that they were inadvertently serving to build. The Anglo-liberal growth is best seen to have been stumbled across accidentally (Crouch, 2009; Hay, 2011, 2013).

It was consumer-led and private-debt-financed. Once established, it was undeniably supported by high levels of public expenditure – with the reinvestment of public sector wages in the housing market, for instance, playing a significant role in pushing up prices, thereby facilitating equity release and boosting consumer demand. Yet it was the easy access to credit, much of it secured against a rising property market, which was its most basic precondition. This served to broaden access to – and (for at least a decade) to improve affordability within – the housing market, driving a developing house-price bubble. Once inflated, this was sustained and, increasingly, nurtured, by interest rates that remained historically low throughout the boom – and which, with the benefit of hindsight, had to remain unprecedentedly low for the boom to last (see also Wood and Stockhammer, 2023).

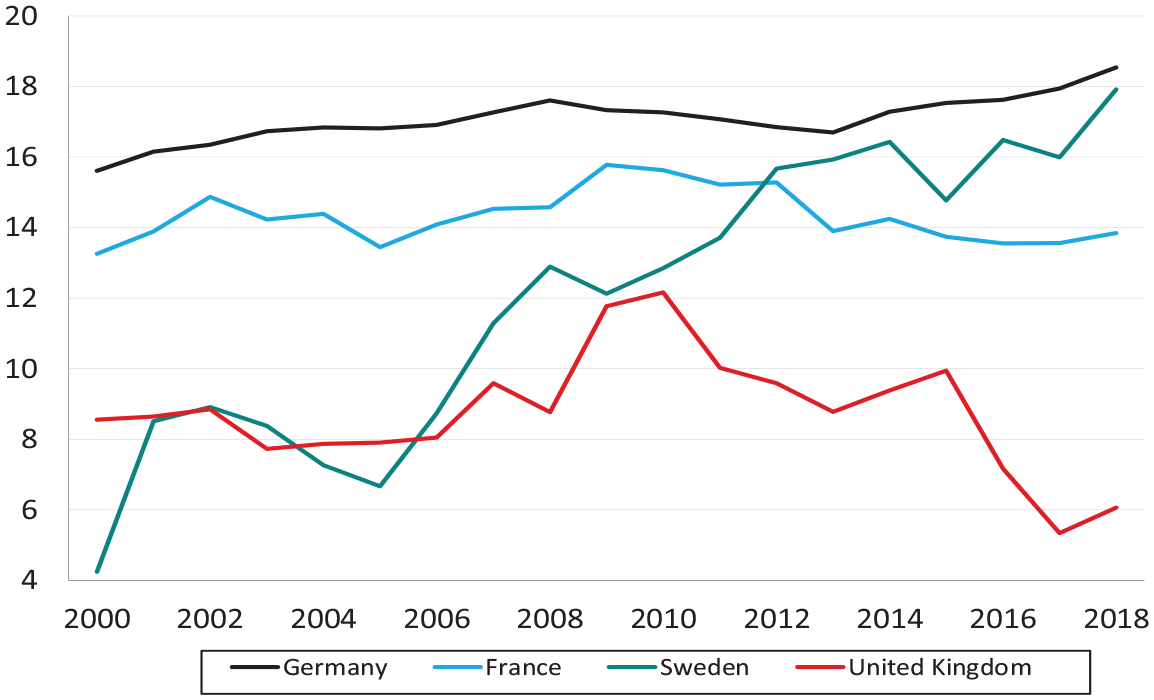

To all intents and purposes it appeared that a virtuous cycle had been established, in which the preconditions of growth were mutually reinforcing. The features of this growth model can be relatively simply described. Sustained low interest rates and a highly competitive market for credit provided both the incentive and the opportunity (certainly in the period before the global financial crisis) for first-time buyers to enter a rising market and for established home-owners to extend themselves financially, by either moving up the housing ladder, or releasing the equity in their property to fuel consumption. There was little incentive to save, as the precipitous decline of the United Kingdom in the savings ratio shows so clearly (see Figure 1).

Gross household savings ratio (% of disposable income), 2000–2018.

Instead, citizens-as-consumers were increasingly encouraged to think of their asset purchases as investments which they might cash in to fuel their consumer habit – in effect, down-payments on future consumption. Crucially, for as long as inflation remained low, credit remained cheap and assets were appreciating, consumption potential, consumer spending and economic output were almost guaranteed to grew in tandem.

In the academic literature, the story is generally told in terms of the rise (and, for those who get to it, the demise) of ‘privatised’ or ‘house-price Keynesianism’ (Crouch, 2009; Montgomerie, 2023; Watson, 2010). The Keynesian analogy cannot, however, be taken too far, nor should it be taken too literally. But it does usefully serve to highlight the key link in the Anglo-liberal growth model between (private) debt, aggregate demand and consumption. In effect, it strips the growth model to its absolute core.

To understand why Anglo-liberal growth might be considered a form of ‘privatised Keynesianism’, it is first important to remind ourselves of traditional or public Keynesianism. In this conception, public spending – sustained, where necessary, through government debt – is the key to promoting demand within the economy. In other words, when the economy is in recession or, indeed, more simply when consumer spending is falling, it is deemed to be the responsibility of the state to inject demand into the economy through increased expenditure (either by expending some portion of an accumulated fiscal surplus or, where this is not possible, through public borrowing). Putting (public) money in the pockets of (private) citizens, whether through tax reductions or welfare spending, boosts demand and consumption with consequent positive effects on levels of economic activity and output. But this is not the only benefit. For such measures are also likely to prove stabilising of the macro-economy over the business cycle. They are, in other words, counter-cyclical. Demand is injected into the economy in recession and a fiscal surplus can be accumulated to improve the condition of the public finances once the anticipated growth dividend is achieved. This management and amelioration of the business cycles allows Keynesians to believe that governments can reduce ‘peak to trough’ variations in unemployment, economic activity and growth, thereby stabilising the domestic economy.

Privatised Keynesianism works rather differently. It assigns a similar role to that played by public debt in traditional Keynesianism to private debt. In the UK variant, such debt has typically taken the form of credit secured against (rising) property prices. For so long as a low inflation–low interest rate equilibrium persisted, a virtuous and seemingly self-sustained growth dynamic endured. This was, in effect, the engine of the growth model. Consumers, in this benign environment, faced powerful incentives to enter the housing market since credit was both widely available on competitive terms (there was a liquidity glut) and returns to savings were low. The result was growing demand in the property market and house price inflation. In such a context, and buoyed by interest-rate spreads, mortgage lenders actively chased new business. In the process, they increasingly came to extend credit to those who would previously have been denied it (at an often punitive interest-rate premium), and to extend additional credit to those with equity to release.

The incentives thus clearly encouraged expansion in both the demand for and supply of prime and sub-prime lending alike, high loan-to-value ratios and, crucially, equity release designed to fuel consumption. That consumption, in turn, sustained a growing, profitable and highly labour-intensive services sector whose expansion both masked and compensated for the ongoing decline of the manufacturing economy. This was further reinforced by low levels of productive investment as credit flows to business were crowded out by positions taken on high-yielding asset-backed securities or other collateralised debt obligations (Reisenbichler and Wiedemann, 2022).

This, for as long as it lasted, was all well and good – though it did serve to redirect the supply of credit from the productive to the consumer economy. But arguably, it is precisely where the Keynesian analogy breaks down that problems begin. Classical (or public) Keynesianism is predicated on the existence of the business cycle. Its very rationale is to manage aggregate demand within the economy in a counter-cyclical way, thereby limiting peak-to-trough variations in output growth and unemployment.

Yet, privatised Keynesianism could not be more different in its (implicit) assumptions about the business cycle. These are distinctly non-Keynesian. Whether taken in by the convenient political mantra of the ‘end of boom and bust’ or convinced, like Robert Lucas (2003: 1), that the ‘problem of depression prevention has been solved’, privatised Keynesianism simply assumed that there is no business cycle. Consequently, measures which might otherwise be seen as pro-cyclical appeared merely as growth enhancing. The effect was that the implicit paradigm that came to support the growth model neither saw the need for, nor was capable of providing, macroeconomic stabilisation. If, perhaps as a result of an inflationary shock, the low interest rate-low inflation equilibrium were to be disturbed, then mortgage repayments and ultimately mortgage default rates would rise, housing prices would fall, equity would be diminished and, crucially, consumption would fall – as disposable income would be squeezed by the higher cost of servicing outstanding debt and as the prospects for equity release to top up consumption diminished. But it was in fact far worse than that; for there were feedback effects too. Lack of demand translated into unemployment with further adverse consequences for mortgage default rates, house prices and so forth. The virtuous circle rapidly turned vicious. This is precisely what happened in the heartlands of Anglo-liberal growth, the United States in 2006 and the United Kingdom and Ireland in 2007.

ABW and Anglo-liberal growth

But that is to get ahead of ourselves. For ABW, certainly as a public policy stance, was conceived and implemented in the United Kingdom well before there was any inkling that the growth model on which it rested might not prove stable in the medium-to-long term. Indeed, its very credibility depended on what, with the benefit of hindsight, looks more like the ‘post-business cycle delusion’ (and the hubris accompanying it) – the misplaced confidence that the problem of recession-prevention had (in Lucas’ terms) been resolved, and resolved permanently. For it was (presumably) only on the basis of such an understanding that one would be prepared to stake the future welfare of one’s citizens’ on the vagaries of the housing market, the stock market or the performance of a variety of other investment-grade asset classes. 5

But, thus understood, ABW made perfect sense. For if assets were stably to continue to increase in value at rates higher than the growth rate of the economy more generally (as they had been doing for decades), then they were likely to give to citizens a better return on their investment than the equivalent contribution, say, to an inflation- or wage-inflation indexed public pension scheme. Even if one might not go so far (in the first instance, at least) as to replace the latter with the former, there was certainly a credible case for seeing ABW as a means of compensating citizens – above all, in a context of population ageing – for the anticipated shortfall in the capacity of public pensions to replace earnings in retirement.

In short, for ABW to be seen to be an excellent idea, all that was required was a confidence in the sustainability of the existing growth model. Such confidence was not in short supply.

But a misplaced confidence in the sustainability of the growth model was not the only flaw in ABW thinking. For the asset acquisition, it mandates encouraging the accumulation and holding of assets (in the form of a portfolio) over a considerable period of time. And the longer such assets are to be held for, the more macroeconomically consequential that withholding is likely to become. For asset accumulation is both a deferral of consumption and a displacement of more conventional savings strategies. We arrive at a crucial point. For it is here that one starts to identify a first tension with the growth model itself. For, stripped to its core, privatised Keynesianism relies on the release of the equity that accrues as assets appreciate. Such equity release fuels consumption and serves, in effect, as the motor of growth. Yet ABW entails foregoing such equity release (and the additional consumption and associated growth it enables in the short-to-medium term) in the hope that the equity amassed in the long-term is sufficient to source consumption in retirement (or in the event of an unanticipated loss of income – whether through sickness, disability or unemployment). In short, what is rational at the level of the individual turns out to be irrational collectively.

Put differently, the move from an Anglo-liberal growth model unencumbered by ABW to one in which the two are closely coupled is, all things being equal, likely to suppress aggregate growth levels. The ‘privatized Keynesian’ equivalent of Keynes’ ‘multiplier’ has been stripped from the equation. The associated loss in growth potential might well be a price worth paying for a reduction in the anticipated rate of precarity among the elderly, the sick and the unemployed. But the point is that there is a trade-off between short-term and long-term equity release; and the turn to ABW is far from neutral with respect to the management of that trade-off. This is a crucial point with potentially important implications to which we will return presently.

But there is a second tension here too; and, arguably, it is of even greater significance. Put most simply, ABW relies on the growth model delivering steady and stable growth (or, at least, the steady and stable asset appreciation that is the very precondition of such growth); and yet, the need for ABW (the public pension shortfall it is intended to fill) rises in inverse proportion to such growth. The moment growth and asset appreciation founder is precisely the moment it is needed most. That, in a nutshell, is the UK economic predicament today – a question of stick or twist. The legacy of the global financial crisis, the legacy of Brexit (especially the Brexit that Brexit is turning out to be) and, indeed, the Covid crisis all make ABW more not less necessary; but they all make ABW more elusive and more difficult to attain.

ABW policy

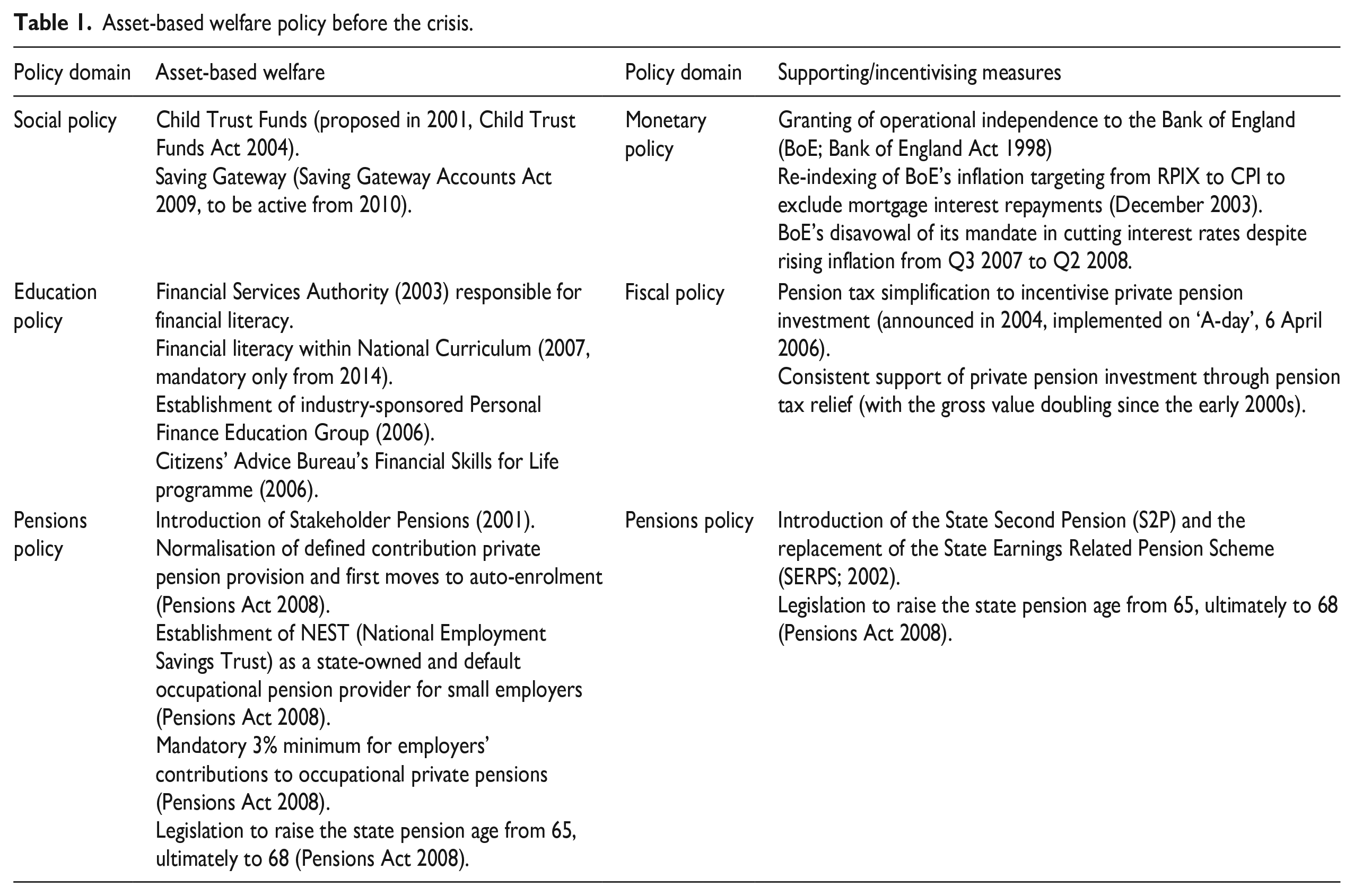

Although the United Kingdom was (and, arguably, remains) very much in the ABW vanguard (to the extent that it has become something of a model to be emulated, Benoit & Hay, 2023), there is a certain irony here. For while the term arguably characterises well – and certainly as well as any other single term – the broad social policy disposition of successive UK administrations since the turn of the century, in the first instance the substantive policy commitment was actually quite light. As Table 1 shows clearly, in the period before the crisis, it was spread quite thinly over a range of policy domains and supported by an array of monetary and fiscal policy commitments.

Asset-based welfare policy before the crisis.

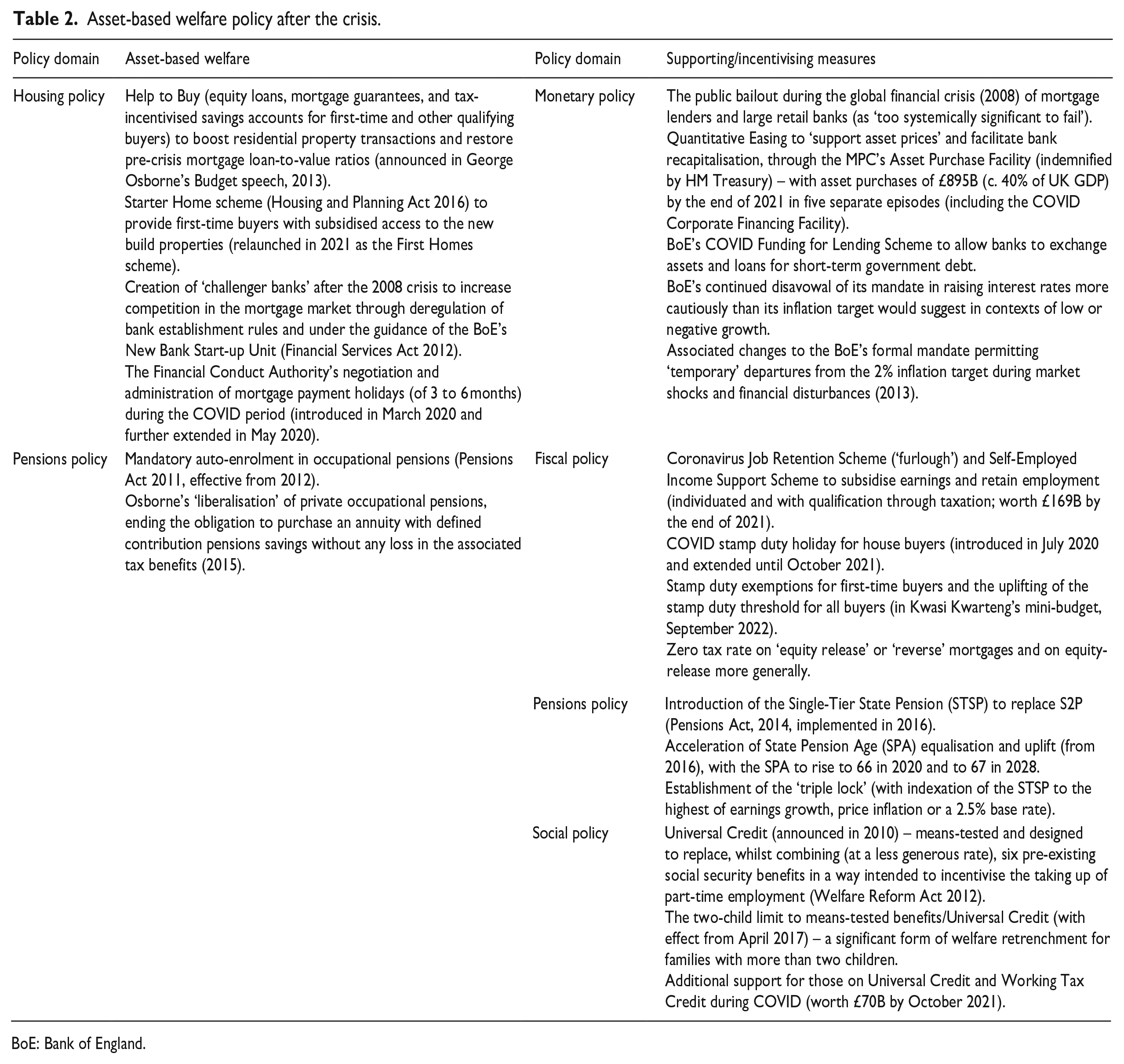

This reflects a combination of factors: first, that this was a disposition rather than a policy stance per se; second, that the policy innovation associated with ABW was typically designed to incentivise rather than to impose participation; third, the ambition was to achieve not a rapid and immediate transformation so much an inter-generational re-socialisation; and, fourth, the initial measures were, simply, quite timid. The broad commitment to ABW has nonetheless proved sticky and, as we shall see presently, even if the core focus of ABW since the crisis (under the Coalition administration of Cameron and subsequent Conservative administrations) has narrowed, the range and diversity of measures supporting ABW in adversity has grown significantly (see Table 2).

Asset-based welfare policy after the crisis.

BoE: Bank of England.

The chronology of all of this is important and there are at least three rather different temporal processes at work here. 6 The first is the simple ‘before’ and ‘after’ of the global financial crisis. The crisis is a game-changer in two respects. First, it compromises significantly the Brown administration’s existing substantive ABW programmes, as we shall see presently, resulting in a scaling back of the scope of ABW (under the incoming Coalition administration) to pensions and housing policy. Second, it simply makes establishing and sustaining the macroeconomic conditions for stable asset-appreciation much more difficult – problems further reinforced by both Brexit and COVID. This changes significantly the form of the public policy interventions supporting ABW.

If this is a dichotomous temporal effect, the other two temporal factors are more cyclical in character – the business cycle and the electoral cycle. But they too are closely tied to the crisis. For the crisis brings a (belated) recognition of the existence of a business cycle which, in the benign conditions of the ‘great moderation’, had been assumed to have been suspended. That recognition comes to have massive implications for the macroeconomics of ABW (as we shall see). And that, in turn, becomes the focus of the Coalition and successive Conservative administrations that pick up the ABW mantle. Their disposition, as we shall again see, is at times rather more neoliberal than Anglo-liberal. But their commitment and their investment in public policy interventions to make ABW work is unwavering.

ABW before the crisis

In the initial phase of its development, before the onset of the crisis, ABW was essentially limited to four policy interventions, only two of which are easily cast as social policy interventions. These were, respectively, the introduction of Child Trust Funds and the Savings Gateway. But arguably rather more significant were the more general and indirect supporting measures introduced at around the same time, namely the promotion of financial literacy in schools as a part of the National Curriculum and the somewhat more amorphous attempt to proselytise the responsible investor citizen as welfare provider (reinforced by the promotion of direct enrolment in private pensions; Finlayson, 2009; Leyshon, 2020; Watson, 2010). Of these measures, it is only the third and fourth that persist. But perhaps most significant of all were the series of macroeconomic and fiscal reforms which led, initially by accident and increasingly by design, to establish and sustain the conditions of Anglo-liberal growth (see Table 1 and for a fuller account Crouch, 2009; Hay, 2013).

Child Trust Funds featured in Blair’s 2001 Election Manifesto and were his second government’s core ABW programme. The details of the policy were set out in the 2001 Budget, with the Child Trust Funds Act being approved in 2004 and the first vouchers only being issued in January 2005. Their introduction was the only social policy innovation of this period with universal availability (though not universal coverage). The funds were described in the Act itself as ‘long-term private savings accounts for children’ and were to be held in a series of private high-street banks, which had agreed to participate in the programme. Participation was voluntary, with parents choosing on behalf of their children. If they opted into the scheme, the fund was capitalised at birth, held in the name of the child, and set to mature at 18. It was only at this point that the fund-holder (by this stage, young adult) would be granted access to the fund, with no end-use restrictions. At the opening of the account itself the state would contribute an initial tax-free payment of £250 (£500 for children in low-income households), with a further equivalent payment when the child reached the age of 7. The scheme was designed to offer tax-efficient parental contributions of up to £1200 per year and promoted in such terms. Although the accounts themselves were all structured in a very similar manner, a range of rather different types of investment fund were available. These varied in terms of the relative privileging in the investment portfolio that they gave to different asset types (bonds, equities, the housing market and so forth), with parents invited to choose between them on the basis of the trade-off between the risk and the potential return that each offered.

The scheme was introduced with much fanfare and considerable advertising; but uptake by parents on behalf of their children was modest. No less interesting is that the introduction of the scheme was, with absolutely no sense of irony, accompanied by and linked directly to the introduction of a parallel programme of financial literacy education in schools – enshrined in various parts of the National Curriculum. Indeed, this was not just limited to a small section on the calculation of compound interest (to be illustrated with examples drawn from Child Trust Funds) in the Math curriculum. Somewhat ironically, given what was to happen to these schemes during the global financial crisis, it also included an (admittedly basic) introduction to financial risk (such as might have helped their parents choose between a Child Trust Fund privileging investment in the property market over one privileging equities, for instance).

The scheme was advertised (both publicly and by the private banks in which the funds were lodged) as an effective strategy for acquiring (where otherwise it would be impossible to acquire) the capital to fund investment in human capital (higher education fees and maintenance), entry into the housing market (a deposit for a house), business start-ups or to meet the cost of a wedding. These adverts, unsurprisingly, played on the aspirations of citizens in a way not dissimilar to Thatcher’s promotion of the image of a property- and share-owning democracy to council house tenants two decades earlier (see also Wood, 2018). In very similar terms, it connected social mobility (here, inter-generational) 7 to the assumption by an individual of an individuated responsibility for managing financial risk.

A similar conception of the idealised citizen-as-investor is found in New Labour’s other flagship ABW policy, the Saving Gateway. This was a rather ill-feted and modest attempt to encourage and boost the savings of low-income households and those typically denied access to financial services (Rablen, 2010). Introduced in the 2009 Saving Gateway Account Act, the programme was in fact never implemented, falling victim (like the Child Trust Funds) to a combination of the global financial crisis and the incoming Coalition administration led by David Cameron before the legislation that enacted it (which had been passed in 2009) even had time to come into effect. But the policy is interesting, if not for its substantive significance, then certainly for what it demonstrates about Labour’s thinking at the time. For it is the closest that Blair or Brown came to embracing the moral philosophy of ABW espoused by Michael Sherraden (1991; McKernan and Sherraden, 2008) – in which, rather than benefits, the poor would be given assets that they would need to tend and nurture if they were to appreciate sufficiently to meet their welfare needs.

The implications of the first phase of implementation of ABW in the United Kingdom are threefold. First and crucially, New Labour’s millennial commitment to ABW shows, for the first time, a clear awareness within government (and in HM Treasury in particular) of the Anglo-liberal growth model. An understanding of the specific link that had emerged between easy access to credit, private debt, asset acquisition and appreciation, equity release, consumption and growth is clearly revealed as a (at least) background set of assumptions making possible the transition to such a model of ABW (Lowe et al., 2012). Second, each related public policy intervention represents a move towards the privatisation and individuation of responsibility for meeting welfare needs, with the symbolic burden of responsibility increasingly shifting from the state to its citizens. The state’s role is, in the process, recast as a provider of financial literacy and the opportunity (reinforced by both positive and negative incentives) to participate in ABW. Third, this implies a new model of welfare provision – a ‘public-plus’ system – of residual public welfare plus private asset accumulation in which it is envisaged that citizens’ assets will be (and will need to be) traded in to meet future welfare needs for which the state either cannot or will not assume responsibility (access to higher education, residential care, an adequate income in retirement and so forth).

This, in turn, raises an intriguing question. Judging from its content what was the nature of the challenge to which ABW was a response? If ABW was the solution what was the problem? Here, as ever, it is important to differentiate between what politicians tell themselves (in Vivien Schmidt (2008) terms, their ‘coordinative discourse’) and what they choose to declare publicly (their ‘communicative discourse’). The public rationale was clear. ABW was a response to demographic change and the projected incapacity of public pensions (and public welfare more generally) to provide in accordance with citizens’ expectations. The private rationale is, of course, more difficult to discern. But one suspects that it was more about managing welfare retrenchment and recalibrating the expectations of citizens. ABW provided a means to make public welfare retrenchment more tolerable (at least to those willing to take up the opportunity that afforded them). It was also a means to make public welfare retrenchment more manageable politically. For higher the levels of participation achieved, the lower the degree of precarity and poverty anticipated (assuming, of course, that all went well).

What is also interesting here is the implicit tension from the outset between ABW, on one hand, and growth, on the other. For the holding and nurturing of assets it implies entails a deferral of consumption (the suspension of housing equity release, for instance). Yet, as the government knew well, it was precisely the non-deferral of consumption that had become the motor to growth during the great moderation (for a more empirical demonstration of this, see Hay et al., 2006; Hay, 2009). In the context of sustained growth that trade-off was manageable. It was, after all, citizens themselves who were charged with responsibility for striking the balance between immediate and deferred consumption as they took on responsibility for meeting their future welfare needs. But in a context of low or no growth, the situation was likely to prove rather less tenable, since the deferral of consumption required by ABW might credibly start to make the difference between growth or recession. It would not take long for the proposition to be tested.

ABW in adversity

The story of the crisis itself has been told many times before and there is no need to dwell on it in any detail here. But, in essence, from the second quarter of 2006 oil prices, inflation and interest rates rose in parallel – in the United Kingdom, the United States and in the Eurozone. Interest-rate rises in Europe were, in fact, much less pronounced than they were in the United States. Yet, unremarkably, the increases in mortgage repayments to which they gave rise, combined with a reduction in disposable income associated with rising prices, led to a squeeze on consumer demand and an increasingly sharp fall in the number of housing transactions – followed soon thereafter by a no less sharp and accelerating depreciation in house prices.

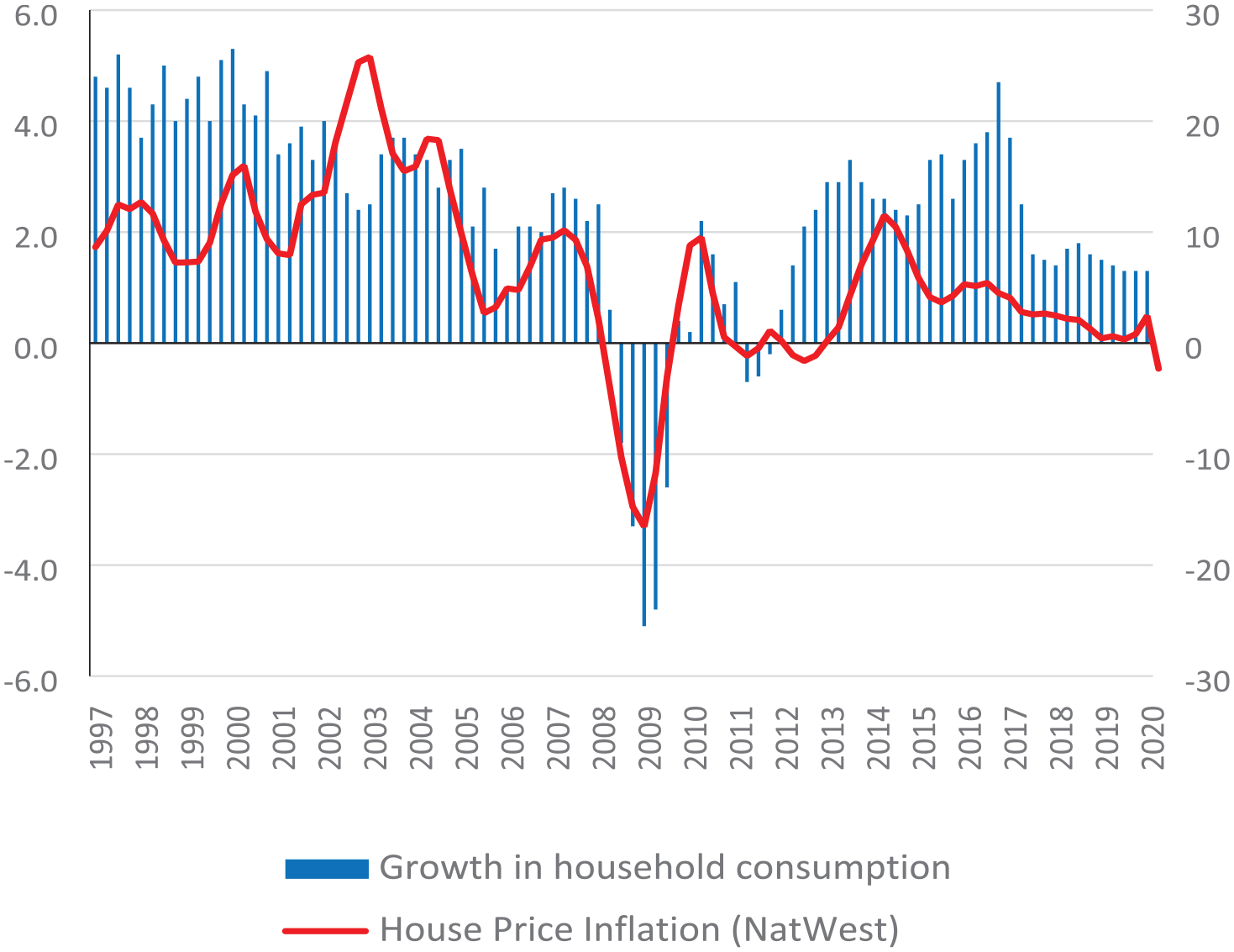

As Figure 2 shows, having grown on average at 12% per annum since the early 1990s, residential property prices in the United Kingdom were, in the final quarter of 2008, falling at close to 20% per annum.

House price inflation (annual), 1997–2020.

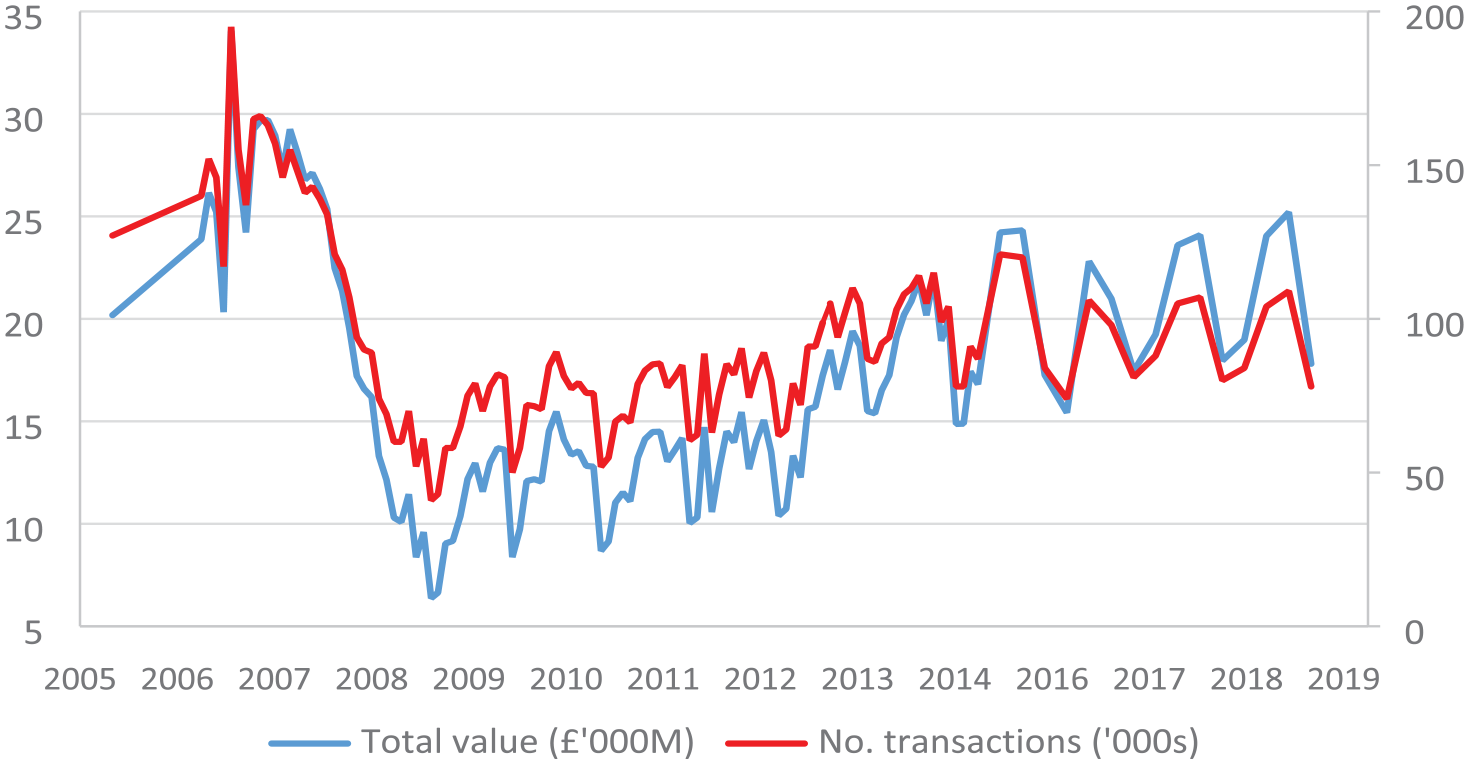

And as Figure 3 shows, housing market transactions were not faring much better.

UK housing transactions (number and value) 2005–2019.

This brought about a quite brutal transformation in personal fortunes. In late 2006, the average UK earner living in the average home was seeing a wealth effect associated with house price inflation equivalent to three-quarters of her pre-tax annual average earnings (Watson, 2010). In other words, were she to have released all the equity in her home, she could effectively have doubled her spending power. Yet, 2 years later, with property prices in free-fall, annual house price deflation in the United Kingdom was equivalent to over 120% of the pre-tax earnings of the average citizen (Hay, 2011: 19). Any residual equity was seeping away at an alarming rate.

The housing market was no longer a source of growth but an impediment to it – because the low inflation–low interest rate equilibrium upon which its rise had depended had been disrupted, reducing demand for property and cutting off at source the equity that had drip-fed consumption for a decade and a half. Crucially, the asset appreciation at the heart of the asset-based welfare strategy had vanished. The result was a highly corrosive combination of falling house prices and equity depreciation which, in combination with high interest rates and high and rising commodity prices, led directly to falling demand and, in due course, to rising unemployment. It has also led to a most dramatic decline in taxation revenues and the most significant deterioration in the condition of the public finances since at least the 1930s. It is to this that we now turn.

After successive bouts of ‘foul-weather Keynesianism’ (Hay, 2011: 23; Montgomerie, 2023) in which, crucially, assets prices were supported through massive volumes of Quantitative Easing (over five phases and amounting to over 40% of GDP), the banks were bailed and public spending largely maintained in the attempt to shore-up growth, the new administration of David Cameron and his Liberal Democratic coalition partners, turned to austerity. 8 Figure 4 shows the governments projections in 2014 for public spending as a share of GDP. Austerity would, of course, prove far more difficult to implement than to commit to. But the policy stance was clear.

Total public spending (actual and projected) in 2014.

None of this was very promising either for the resumption of growth or for ABW. Indeed, just as Gordon Brown’s Labour administration had flirted temporarily with foul-weather Keynesianism, so the Cameron–Clegg coalition turned to a strategy (arguably more rhetorical than substantive) for ‘rebalancing the economy’ (Berry & Hay, 2016). The principal priorities of this were: austerity (the restoration of ‘balance’ to the public account); reducing private debt; increasing private savings; increasing business investment; improving the trade balance; reducing the economy’s dependence on financial service provision (particularly through a re-emphasis upon manufacturing); and boosting regions other than London and the South East (Berry, 2022). Other than the commitment to austerity, none of this was to last for long. And it is not difficult to understand why. For in the absence of both a new growth model and, crucially, the growth such a model might provide, it was difficult to see how these ostensibly laudable commitments were going to be funded or made compatible – one with another or with growth.

By late 2012, then, talk of rebalancing had, to all intents and purposes, been dropped. Austerity certainly remained the government’s primary declared economic imperative. But its attentions now increasingly turned to two additional priorities: (1) the attempt to breathe new life into the Anglo-liberal growth model (from early 2013 onwards) through the targeted injection of demand into the housing market and (2) the incentivisation of the turn to ABW (from October 2012). This change in policy focus is also not very difficult to explain. For such growth as there had been since the crisis was fleeting and modest at best and, especially in a context of public austerity achieved through additional welfare residualisation, the need for a private complement to publicly funded welfare was rising.

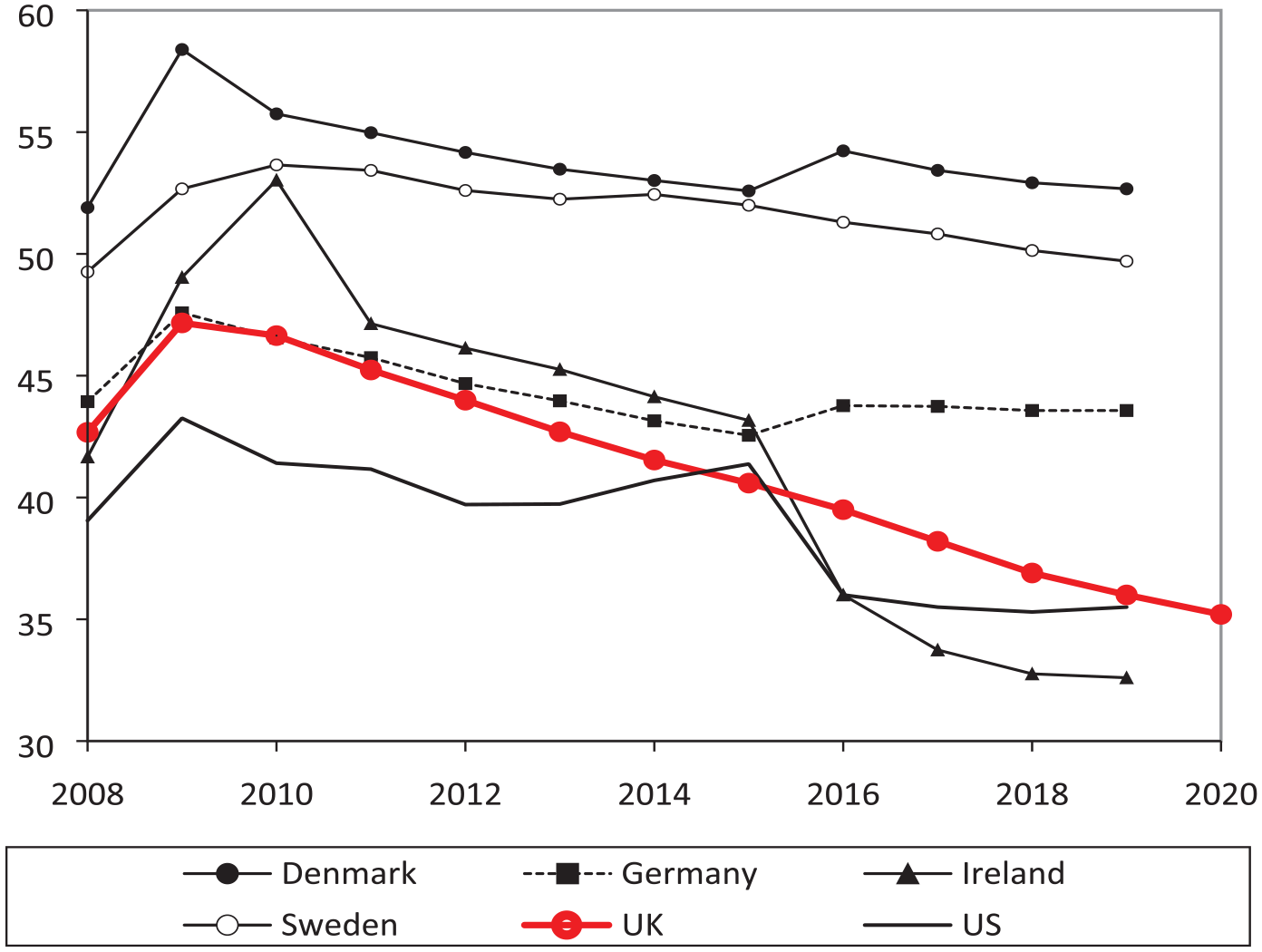

This is perhaps most clearly seen in Figure 5, which shows public pension replacement ratios for 2014 and 2018 for the United Kingdom and a number of OECD comparators. It demonstrates that not only were UK public pensions at the time among the least generous of OECD economies, but they were not in the process of becoming more generous.

Net public pension generosity (replacement rates; % of pre-retirement income).

This is the context in which the policy innovation of the Cameron–Clegg coalition should be interpreted. The details of this to ABW and the attempt to re-secure the conditions of asset-appreciation on which it rested are set out in detail in Table 2.

In terms of the housing market, the key measures here were the various Help to Buy schemes and the introduction of what were termed Starter Homes. Help to Buy was targeted at first-time buyers and involved a series of specific measures designed to facilitate access to the housing market for those for whom it would otherwise be impossible. It included equity loans, mortgage guarantees, specific tax-incentivised savings accounts for those intending to use the funds to purchase property and reduced deposits for first-time buyers purchasing a newly built home. The scheme was announced in George Osborne’s 2013 budget, introduced later in the year and further extended a year later and again in 2015 (Ronald et al., 2016).

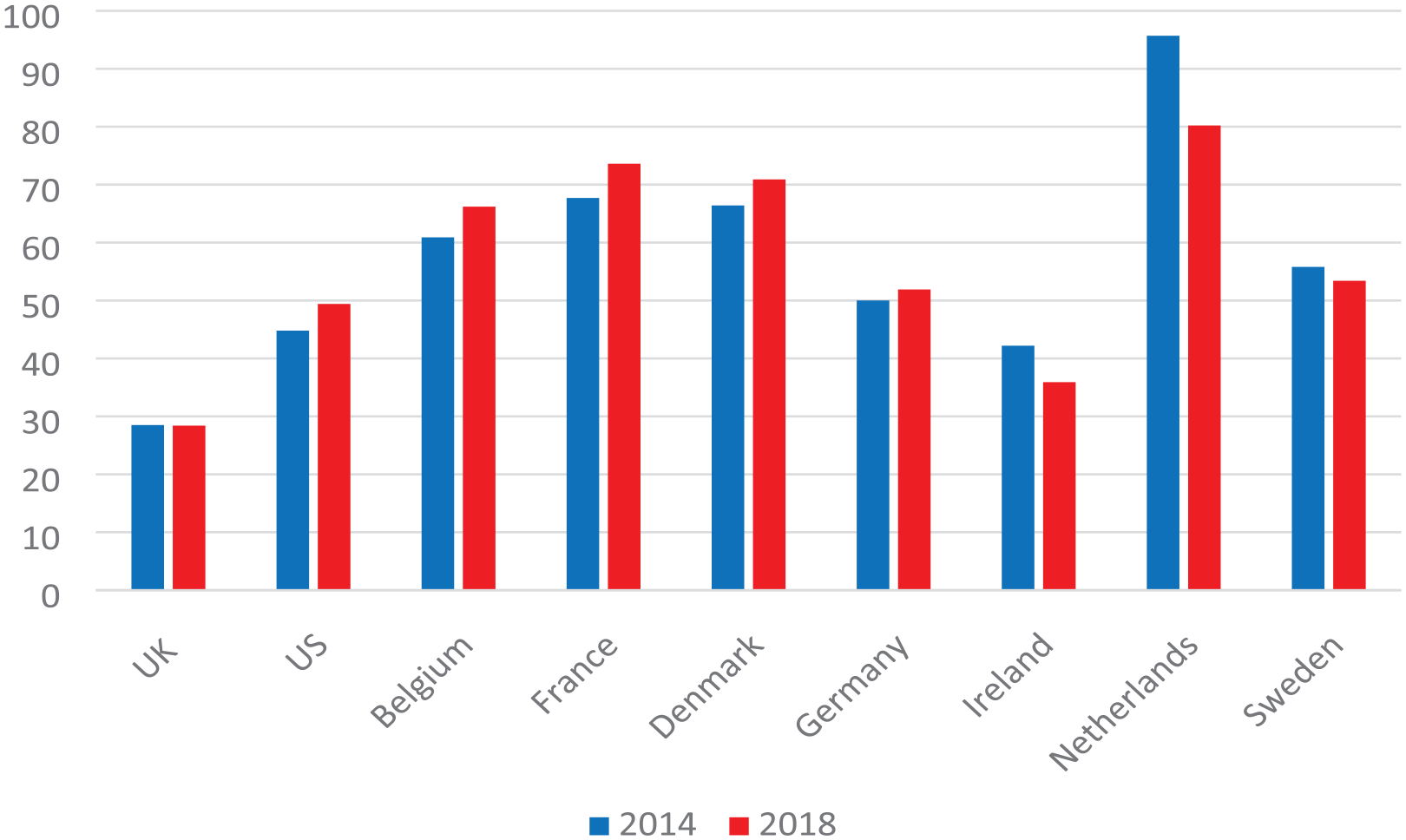

The immediate result was a small boost to the UK housing market (more pronounced in some areas than others) and a broadening of access to the market, above all for first-time buyers. However, it is crucial to note that the effect was marginal. While the rate of homeownership among UK adults aged 18–34 was 57% in 1981 and 55% in 2001, it had fallen to 13% by 2013. By contrast, 78% of those aged over 65 were homeowners in 2013 (up from 49% in 1981). If home-ownership is the key to ABW, then access to it remains highly uneven. Osborne’s Help to Buy schemes did little to alter that, as Figure 6 suggests.

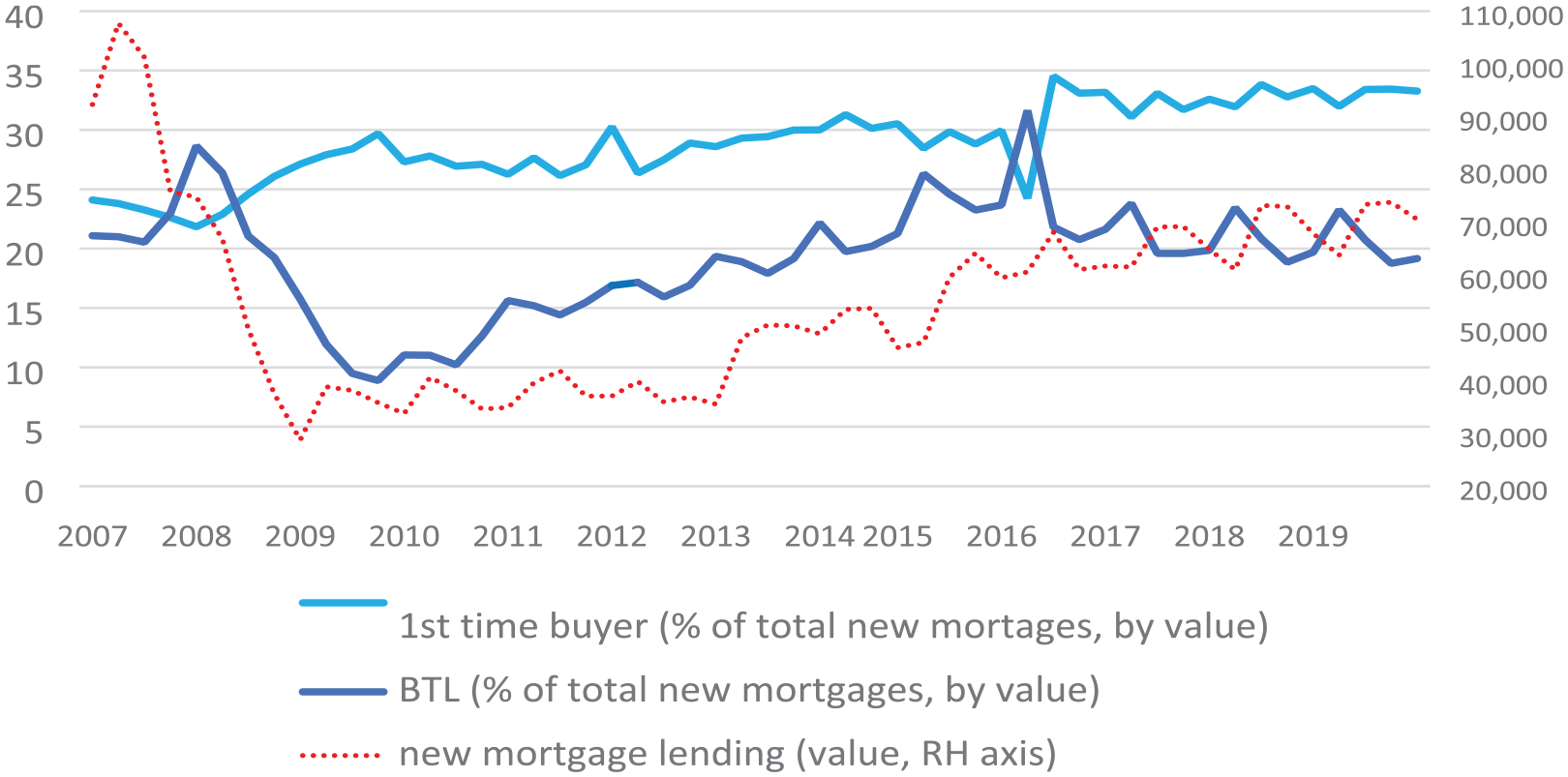

First-time-buyers and Buy-to-let as share of new mortgage lending (% by value).

What Osborne did manage to achieve, however, with the seemingly active compliance of the at least nominally independent Monetary Committee of the Bank of England, 9 was the return to (initially quite steep) house-price inflation (see Figure 2). Yet, since the vote for Brexit in 2016, even that has proved difficult to sustain.

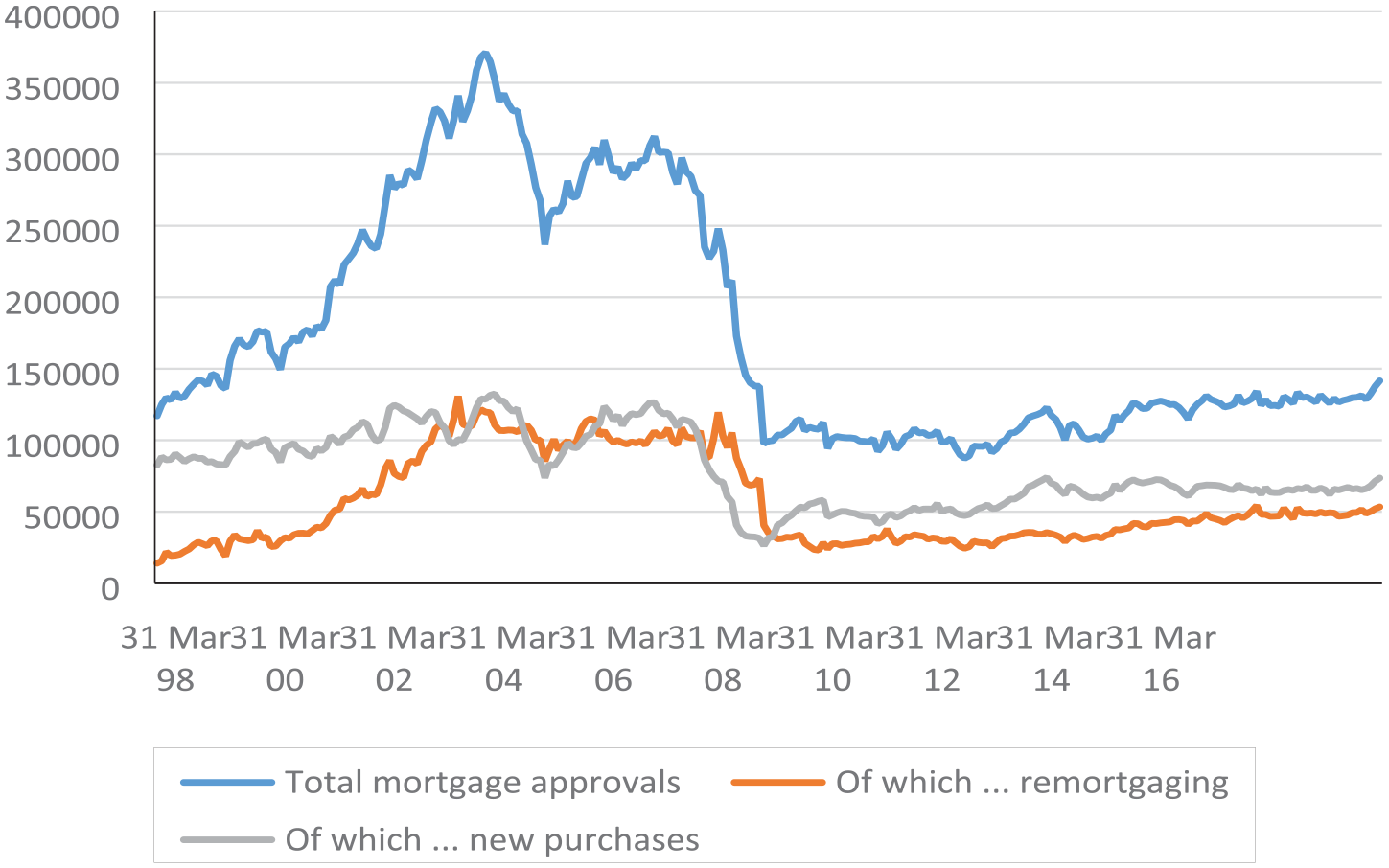

The overall impression is of a housing market far less able reliably to sustain an ABW strategy and to ensure widening access to its potential benefits, as Figure 7 strongly implies.

Monthly mortgage approvals.

Yet, if Anglo-liberal growth and stable asset-appreciation were becoming ever more elusive during this period, this did not prevent the governments of Cameron, May and Johnson ratcheting up the pressure on citizens to take more responsibility for their own welfare futures.

Crucial to this was the policy turn to the mandatory auto-enrolment of all new employees in private pensions from 2012 and the proposals for a new ‘single-tier’ state pension (Berry, 2021). This enshrined for the first time the idea of a ‘public-private mixed pension model’; it was finally implemented in 2016. As Craig Berry (2016: 16–17) put it at the time:

by redefining the purpose of the state pension as enabling private retirement saving by individuals, the reform represents a subtle form of welfare retrenchment through which the state withdraws from any attempt to provide a genuine income-replacement benefit for pensioners, instead offering a framework within which individuals can become self-reliant (see also Berry, 2021).

This has been reinforced, as Declan French et al. (2018: 143) note, by conscious attempts backed by a series of regulatory reforms, to actively encourage if not yet to mandate ‘pensioners to use their housing wealth to help pay for the cost of their social care, to release money to adapt their homes and to support their incomes’ (citing House of Lords Select Committee, 2013). Although uptake is as yet modest, not least because poverty in old age in the United Kingdom is rather more a prospective problem than an immediate one, lifetime and reverse mortgages, home reversion contracts and a variety of other mechanisms of housing equity release in retirement are all on the rise (French et al., 2017; Wood and Stockhammer, 2023). This is the cutting edge of ABW.

A final and no less significant pension reform introduced in 2015 gives citizens with defined-contribution or defined-benefit private pensions enhanced financial flexibility. In the decade prior to their retirement, they are now to be given access to their pension fund and removed of the obligation to purchase an annuity. Instead they will be encouraged and incentivised (through significant taxation benefits) to take the pension (or a portion of it) as a lump sum (to be treated as income, with the first 25% tax free). The rationale is again one of giving citizens the capacity and incentive to take responsibility for the financial risk associated with meeting their future welfare needs (Berry, 2021: 58–59, 192–193, 196–200). The incentives are clearly structured to encourage those aged 55–65 to play ABW in the housing market, boosting house price inflation further in the process.

But there are indirect effects too. With fewer annuities, more of pensioners’ net wealth is likely to be subject to inheritance tax; and since annuity funds are massive investors in the market for corporate bonds market, the net effect is likely further to reduce the supply of credit to business. So much for the rebalancing of the economy, it might well be suggested.

Conclusion

As all of this suggests, even if the Anglo-liberal growth model is not all that it was once cracked up to be, the ABW model to which it gave rise and which is predicated upon it is still very much alive and well – in the minds and dispositions of UK policy-makers.

But ABW after the crisis and above all in the wake of Brexit and the COVID crisis is a somewhat different creature to ABW before the crisis. What started life as a set of social policy initiatives designed to widen access to the proceeds of asset appreciation has become, over time, more narrowly focussed on the needs of citizens to take responsibility from the state for meeting their own future welfare needs. In the process, and above all in a context in which growth and asset-appreciation are no longer guaranteed, the policy focus has changed and broadened. Direct ABW policy today is more modest in its scope and range – and ever more focussed on mandatory enrolment in defined contribution occupational pensions.

But it has acquired (as the comparison between Tables 1 and 2 shows clearly) a far greater range of buttressing measures. These are about restoring the growth on which ABW is predicated in a context in which austerity and hence the need for ABW has grown. In adversity, the public policy commitment to support ABW (through attempts to recreate the macroeconomic conditions of asset-appreciation and the microeconomic incentives for taking responsibility for one’s future welfare) becomes more extensive as the core policy measures are restricted to mandatory defined contribution pensions enrolment.

ABW was always about compensating citizens for the likely and growing incapacity of public welfare to meet future welfare needs. It was also about passing responsibility to them from the state for meeting such needs. Those needs have not gone away. Indeed, they have been exacerbated by the global financial crisis, its immediate legacy, austerity, and by Brexit and Covid too. But in the absence of a steady and stable Anglo-liberal growth model and the kind of steady and stable growth with which it came to be associated in the period before the crisis, the ABW solution to the problem of welfare residualism is illusory. There are two elements to such a conclusion.

First, as I have suggested, ABW entails a deferral of consumption (through the accumulation of assets to meet future welfare needs). This can only have the effect of diminishing and suppressing growth in the short- to medium-term, especially in an economy whose growth has become so dependent on private debt-fuelled consumption. In short, ABW is parasitic upon the very growth that the growth model is there to produce. In the relatively benign context of the ‘great moderation’, that was not much of a problem. But that is not the situation of the UK economy today. What was once benign is no longer.

And, second, ABW is designed to compensate the poor and the prospectively poor. But it is based on asset appreciation strategies which yield returns on – and in proportion to – the value of those assets. Put simply, it rewards disproportionately the asset-rich; and the asset-rich have no need of ABW (they do not need compensation for the low value of their public pension). Asset-based investment strategies are, then, wealth multipliers (see also Adkins et al., 2020, 2021; Montgomerie, 2023; Wood, 2020). This massively limits the extent to which ABW is likely to prove an effective compensation for those who suffer most from growing Anglo-liberal welfare residualism. Thus, even when it works well (in yielding a good and stable return on the assets acquired), it does little or nothing to temper the effects of welfare retrenchment for those previously reliant on public welfare. For it is, and can only ever be, regressively redistributive.

Finally, and most crucially, welfare retrenchment and welfare residualism in the United Kingdom are ongoing and accelerating – and their effects are inter-generational. They were in place even before the crisis, they have been significantly reinforced by austerity and they are set to be reinforced further by both Brexit and the legacy of the COVID pandemic. If the preceding analysis is correct, the consequences of this inter-generational acceleration of inequality for precarity will be very severe indeed. The consequences – social, economic and political – are likely to be profound.

Footnotes

Author’s note

For the purpose of open access, the author has applied a Creative Commons Attribution (CC BY) licence to any Author Accepted Manuscript version arising from this submission.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.