Abstract

The role of central banks in perpetuating and tackling the economic patterns associated with climate change has increasingly been subject to academic and political attention. The Bank of England is no exception, having received a new mandate to ‘facilitate the transition to net zero’ in March 2021. This follows the Bank’s utilisation of its monetary tools to repeatedly stabilise the economic status quo since 2008, despite its ecological consequences. This article reveals the perceptions within the British state of the new mandate and the forms of institutional change demanded by it, based on a series of elite interviews with Treasury officials and other UK monetary policy experts, as well as a discourse analysis of Bank publications and speeches. We find that Bank actors lobbied for the new mandate to legitimise its development of climate risk assessments and licence internal dialogue on the implications of its monetary policy. But the mandate is perceived to be in immediate conflict with, and subservient to, the Bank’s primary structural objective of maintaining price and financial stability, due to the potentially destabilising effects of private capital realignment during a net zero transition. Institutional change within the Bank is thus limited to extending its pre-existing function of mitigating risks to financial stability rather than facilitating decarbonisation through market-shaping governance of the financial sector.

Keywords

Introduction

Recent years have shown central banks to be simultaneously complicit in supporting and promoting economic patterns of ecological degradation while also being potentially powerful actors capable of accelerating a transition to sustainability through its governance of global finance and monetary policy interventions (D. Bailey, 2020; Dikau et al., 2021; Gabor et al., 2019; Mikheeva and Ryan-Collins, 2022; Robins et al., 2021; Volz, 2017). Our focus in this article concerns the Bank of England (henceforth, ‘the Bank’) which has historically exacerbated the ecological crisis by shoring up the stability of the environmentally unsustainable economic status quo through its asset purchasing programmes, or Quantitative Easing (QE), disproportionately benefitting carbon-intensive industries and its light-touch regulation of the City of London’s globally significant financial sector (D. Bailey, 2023; Dafermos et al., 2020; Gabor et al., 2019; Matikainen et al., 2017; Ryan-Collins, 2019; Volz, 2017). At the same time, the Bank has developed measurements of climate-related financial risks (CRFRs) and fostered international discussions among fellow central banks through the co-founding of the Network for Greening the Financial System (NGFS). The new remit of the Monetary Policy Committee to ‘facilitate the transition to net zero’, bestowed upon it by the Treasury in 2021, may prompt or legitimise a contemplation of the Bank’s institutional practices and the governance of profoundly unsustainable economic activity. This contemplation of institutional practice is highly significant in a Central Bank that oversees the activities of the one of the global economy’s primary financial sectors.

In this article, we offer a timely investigation of the perceptions of the Bank’s new remit within the British state and the extent to which the new mandate is substantially disrupting existing practices and prompting institutional change in the Bank in the context of extraordinary environmental, economic, and political circumstances. For this analysis, we deployed a twofold methodology. First, we conducted seven semi-structured elite interviews online with high-ranking Treasury officials and UK monetary policy experts. Second, we conducted a discourse analysis of the Bank’s climate-related financial disclosure reports and the 17 Bank documents and speeches that included the phrase ‘net zero’ between 2016 and 2022, all of which were sourced from the Bank’s internal publication library. Our methodological approach permitted an examination of the perceptions of the new remit and corresponding institutional evolutions from within the institutions of the British state principally tasked with economic governance.

Our investigation found that the Bank invited the ‘net zero’ mandate from the Treasury to legitimise the Bank’s ongoing introspection on the CRFRs of its monetary operations and its consequences for policy. Equally, Bank officials have also welcomed a significant degree of ‘strategic ambiguity’ of the mandate that allows those actors to interpret the mandate as they deem fit (van’t Klooster, 2022). Interviewees were keen to stress that the mandate has sparked serious dialogue and discrete changes within the Bank – led by an internal ‘Climate Hub’ that is collaborating with the Bank’s various departments – but a transition to Net Zero alignment is seen to be economically destabilising and is thus ultimately in immediate conflict with, as well as subservient to, the Bank’s ingrained and primary objective of maintaining price and financial stability. The Bank’s inscribed structural logic will preclude any transformative governance of the financial sector that facilitates rapid transformation, and instead inculcates only limited, market-friendly, and incrementalistic measures that enable long-term economic shifts. We find that any changes instigated by the mandate will not, therefore, substantially challenge the Bank’s existing modus operandi.

In the following sections, we begin by contextualising the introduction of the new remit to facilitate the transition to net zero before detailing the findings of our empirical investigation into the internal debates concerning the interpretations of the remit and its policy implications as perceived by our interviewees. We then outline the policy implications of the mandate for the Bank as proposed, situating net zero within its hierarchy of objectives of monetary policy. Finally, we analyse the ongoing climate politics of the Bank as it contends with CRFRs for the stability of the UK economy before offering some concluding remarks.

The Bank of England and the transition to net zero

The Bank of England as an institution has been shaped and reshaped over time by a series of political actions and changing interpretations of its role, which have determined its institutional objectives and strategies, empowered its operations, and bestowed upon it a degree of operational independence (BoE, 2018; King, 2012). The Bank’s power and more overtly ‘political’ tendencies of the post-war period were restrained in the ‘stagflation’ crisis to the narrow monetarist focus on ensuring price stability (Bezemer et al., 2018; Ingham, 2004). This narrow focus on inflation was formalised by New Labour after their election win in 1997, when Gordon Brown bestowed ‘independence’ upon the Bank. The Bank of England Act 1998 stated explicitly that the Bank of England’s monetary policy objectives were to ‘(a) to maintain price stability, and (b) subject to that, to support the economic policy of Her Majesty’s Government’ (BoE, 2018). This technocratic approach to economic governance was embraced on Threadneedle Street, where the Bank resides, and became seen as essential to retaining the operational independence and depoliticised status of the Central Bank.

Yet the Global Financial Crash of 2008 prompted significant changes to the objectives and practices of the Bank, which included the broadened focus on the stability of the financial system, in addition to its role of ensuring price stability, and the innovation of QE. These new responsibilities were enshrined in the Banking Act 2009 and the Financial Services Act 2012, leading to the conduct of ‘macroprudential policy’ by the Bank’s Financial Policy Committee (FPC), which entailed assessing and monitoring systemic financial risks and ensuring the resilience of major commercial banks in the face of systemically destabilising volatility (Baker, 2018). It is within these myriads of opaque and evolving legislative frameworks that the Bank’s agency to act on environmental questions can be situated.

Debates on the Bank’s agency to act on climate change certainly precede the new remit. Some have argued that the macroprudential remit combined with the increasingly evident risks to financial stability pertaining to climate change could plausibly have seen environmental considerations become ingrained in the Bank’s governance (Baker, 2018). Former Governor Mark Carney expressed fears that an unchanged monetary policy would incur a ‘climate-driven Minsky moment’ (Carney, 2017) – a sudden collapse in asset prices that ripples throughout the financial system and global economy – a future also projected by a range of macroeconomic modelling exercises (Batten et al., 2016; Dafermos et al., 2018; Dietz et al., 2016). Meanwhile, the Bank of England under the leadership of Carney became one of the founding members of the NGFS (NGFS, 2018), a network of Central Bank and financial regulators that aimed to ‘integrate the monitoring of climate-related financial risks into day-to-day supervisory work, financial stability monitoring and board risk management’, as well as ‘integrate sustainability into their own portfolio management’ (BoE, 2022b). The Bank has been an important mainstay in the NGFS, which now has 114 members.

The Bank has made great strides in the development of CRFR measurements. CRFRs are themselves typically categorised in terms of physical and transition risks. Physical risks relate to, for example, extreme weather events (e.g. droughts, floods, and storms), as well as longer-term gradual changes in the climate (e.g. sea-level increase, changes in rainfall), all of which will have a considerable impact on economic and financial instability. Transition risks meanwhile refer to the risk arising from technological innovations, changing consumer preferences, or political action that may be equally destabilising (Bolton et al., 2020; BoE, 2019b, 2022b; Svartzman et al., 2021). Precise calculations of risk are beset by contestation over variables such as technological and market-based innovations and fiscal policy trends, as well as the ‘radical uncertainty’ of ecological tipping points and chain reactions that can swiftly dispel linear trends; but the FPC within the Bank is keen to address what they see as the insufficient information available to financial institutions so that risk can be ‘priced in’, and new financial trajectories forged, by undertaking the Bank’s first future climate scenario projections in their 2021 Climate Biennial Exploratory Scenario (CBES) (Bolton et al., 2020; Chenet et al., 2021; BoE, 2022c). The lack of data on the precise implication of CRFR has incidentally proved problematic for central banks and supervisors to determine the implications for CRFR, as they rely on data from the past to determine the future.

As such, monetary policy could arguably have been ‘greened’ far before 2021, yet the macroprudential remit and CRFRs have had no immediate impacts on the Bank’s operations. This is at least partly due to the risks that ‘green’ monetary policy poses to financial stability due to its adverse impacts on the businesses in the core economy and the possibility of ‘inflating green asset bubbles’ that could later deflate with destabilising consequences (BoE, 2022a). The macroprudential remit represented a potential moment of change, given the systemic risks posed by climate change, but the conservative interpretation adopted by the Bank thus far in light of the risks to financial stability has limited action to the market-friendly approach of petitioning financial institutions to disclose their exposure to CRFR and subjecting them to climate-related ‘stress testing’ (Tooze, 2019). Meanwhile, the Bank’s QE schemes have continued to be shaped by the asset purchases of the capital markets (often referred to as ‘market neutrality’) and have thus mirrored the failure of the capital market to price in CRFR. This is despite the calls by many (including the NGFS, 2018) to exclude assets with significant CRFRs in future QE schemes.

In acknowledgement of the risks to price and financial stability posed by climate change, former Bank governor Mark Carney and other financial supervisors have encouraged financial markets and central banks alike to transition towards more sustainable investments (albeit no consensus has been struck on a taxonomy of financial investments, see Gabor et al., 2009; NGFS, 2021). The United Kingdom’s (UK) model of financialised capitalism contributes to CRFR, with lending to fossil fuel companies by UK commercial banks, particularly Barclays, having increased since the Paris Agreement (Banktrack, 2022), as the City of London is deeply and increasingly imbricated in polluting economic activity across the global economy.

The net zero targets were seen as a potential catalyst for seismic political, economic, and ecological change in the UK (HM Treasury, 2021; Krebel, 2021). Theresa May adopted the target in the aftermath of an Intergovernmental Panel on Climate Change (IPCC) report (2018) and mounting public concern and activism that increasingly focused on government inaction rather than corporations or consumers (Doherty et al., 2018). It was a key feature of the 2019 Conservative Party manifesto, and its significance only grew amid the pandemic and the widespread appetite to ‘build back better’ (YouGov, 2020); a sentiment which was echoed by the current and former Bank Governors (A. Bailey et al., 2020).

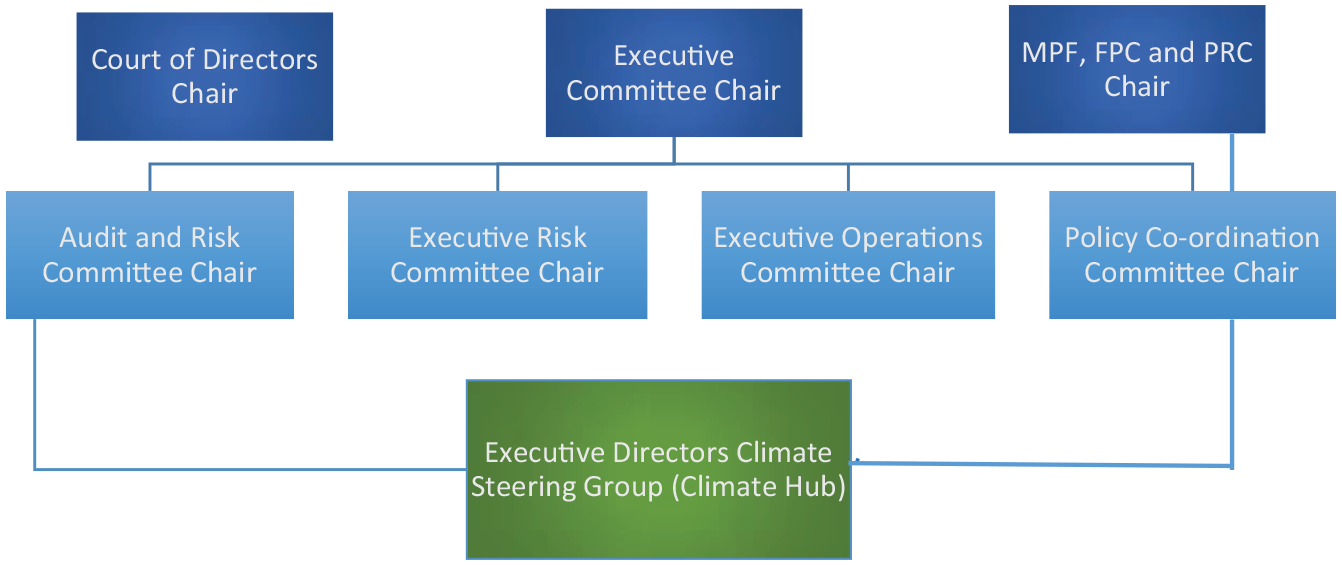

The mandate to ‘facilitate the transition to net zero’ was bestowed upon the Bank’s Monetary Policy Committee (MPC) in March 2021 by then Chancellor Rishi Sunak (BoE, 2021a). After the new objective was announced, the Bank publicly committed to undertake a review of its Corporate Bond Purchase Scheme to ‘account for the climate impact of the issuers of the bonds’ (BoE, 2021b), and later committed to incrementally ‘tilting’ their portfolio away from carbon-intense firms (BoE, 2021c). The new remit had then prima facie prompted a recontemplation of the institutionalised practice at the Bank (Figure 1).

The institutional structure of the Bank.

The Bank’s net zero mandate merely follows the previous, and ultimately less heralded, revision of the FPC remit 1 year prior, in which Sunak authorised the institution to continue assessing CRFRs and to support the UK government’s green finance objective detailed in the Green Finance Strategy (BoE, 2020, 2021d).

It should certainly not be presumed that the new remit to ‘facilitate the transition to net zero’ will perfunctorily trigger changes to the construction of UK monetary policy. As noted by Campiglio et al. (2018), ‘what central banks and financial regulators will do to support a smooth low-carbon transition will depend on what their mandate allows’ but also ‘how this is interpreted and their willingness to act’. The interpretation and implementation of the new remit will be conditioned by its pre-existing structural logics, objectives, policy tools, and resources that the leadership exhibited within the heterogeneity of semi-autonomous departments and committees, and the power relations that shape and circumscribe the interpretations of the Bank’s role (Gabor, 2021). Just as the institutional and policy consequences of the macroprudential remit were subject to interpretation by actors within the Bank, the interpretations of the goal to ‘facilitate the transition to net zero’ will be crucial in determining its impact.

The Bank’s Executive Director, Mark Hauser, was quick to dampen expectations of institutional change commensurate to the scale of the climate crisis. He argued that the transition to net zero must be largely financed by private capital rather than the state – refuting the speculation that monetary policy would be reoriented towards financing a net zero transition – and that the role of the Bank must be limited to modest subsidies of green bonds and only penalise financiers of unsustainable economic activity as a last resort (Hauser, 2021). Hauser’s comments came in the wake of, and potentially in response to, the observation that central banks, such as the European Central Bank (ECB), had provided direct monetary financing of government spending since the Global Financial Crisis in 2008 (van’t Klooster, 2022). Such fiscal–monetary policy integration has led scholars to formulate ways in which this might be directed towards environmental ends, casting a critical light over central banks in turn.

Academic research on the dominant understandings of the remit within the Bank and its operations remains limited. However, Dafermos et al. (2022) have already cast doubt on the extent to which the Bank’s recently reformed approach to the £20 billion Corporate Bond Purchase Scheme (CBPS) purchased through the Asset Purchase Facility, a potentially important component of ‘greening’ monetary policy insofar as it reduces bond yields and creates more favourable financial conditions for investment for certain sectors and firms, is aligned with a net zero transition (Dafermos et al., 2022). They concluded that the CBPS ‘climate scorecard’ that evaluates the bond issuers’ climate performance and incremental tilting strategy towards stronger climate performers demonstrated limited ambition on the environmental mandate. They argued that the approach insufficiently penalises polluting companies (at least in the first stage) and remains rooted in the principle of market neutrality. Indeed, the tilting strategy may even lead to even higher subsidies for high-carbon activities in their assessment, due to the framework of replicating the sectoral composition of corporate bond purchases in a ‘market neutral’ way, because it requires tilting of CBPS holdings to be conducted within sectors rather than towards more peripheral but sustainable sectors. As such, the Bank’s approach will only reduce the carbon intensity of the CBPS portfolio marginally (approximately 7% according to the authors’ own estimate), which will represent a very weak facilitation of a climate transition (Dafermos et al., 2022).

How, therefore, has the new remit been interpreted within the UK’s Central Bank and the British state more broadly? Can we expect the aforementioned reforms to the CBPS to be the limits of the policy and operational reforms resulting from the new remit? Our research project was designed to investigate the differing perceptions of the new mandate, discern the debates on the policy and operational implications of these interpretations for the Bank’s governance, and understand the political, economic, and ecological conditions in which the mandate would be conducive to more ambitious forms of policy action.

Perceptions of the mandate from within the British state

To provide an empirical account of perceptions within the British state of the Bank’s new mandate, our study combined a series of seven elite interviews with anonymised Bank officials, Treasury officials, and other monetary policy experts. Interviews were coupled with a discourse analysis of the public discourse of senior Bank officials on the topic of the revised remit published by the Bank. It yielded several noteworthy insights into the provenance of the remit, the dominant understanding of its consequences for Bank operations, and the impacts of CRFR on the internal politics of the Bank.

We found, first, that the new mandate was the result of informal lobbying from Bank officials (Interview: Treasury B). Although the mandate was formally bestowed by the Treasury, this followed months of informal discussions between Treasury and Bank actors in which representatives of the latter made a case for a revised remit to give meaning to the FPC’s Climate Financial Risk Forum (CFRF) analytics and the MPC authority to act upon these risk assessments in the construction of policy (Interview: Monetary policy expert A). The new remit does not, therefore, represent ‘metagovernance’ by the Treasury – that is, an attempt to govern the Bank’s operations (Sørensen and Torfing, 2005). But it was instead prompted by senior Bank officials more attuned to climate-related economic issues than Treasury actors (reflected in the size of the team seconded to COP26 from the Bank according to one interviewee) and keen to legitimise the Bank’s prior institutional ‘mission creep’ on climate issues. This mirrored the revisions made to the FPC remit a year prior and enabled greater internal coherence between the FPC and MPC, which had (with far less fanfare) received a revised remit in 2021 of having consideration for the environment.

Contrary to prevailing assumptions that the Bank has been slow to incorporate environmental policy into its decision making, several interviewees asserted that the mandate is being taken seriously in the Bank (ibid). CRFR metrics are seen as being increasingly important in the Bank and the question of how to ‘green’ the operation of the Bank is being discussed in every single unit within the institution. According to one interviewee, the Bank is looking to be ‘preemptively reactive’ in the case of climate change and they are trying to find creative solutions to green monetary policy (interview: Monetary policy expert B, C). The remit could also foreseeably legitimise the monetary financing of a ‘green investment bank’ through bond purchases, according to another interviewee, and indeed this may be where the Bank is best suited to facilitate the transition by creating fiscal space for development banks, such as the new UK Infrastructure Bank, the Department for Energy Security and Net Zero (DESNZ), and other fiscal policy-making institutions.

Equally, however, we found that the Bank would not have welcomed the overbearing imposition of a more specific mandate that threatened their operational independence by demanding unbending and obligatory strategies of governance (Interview: Monetary policy expert B). As such, the flexibility that the new remit’s ambiguity offers the Bank was embraced as much as the remit itself. The mandate does not micromanage or constrain the bank and nor does it disqualify the bank from taking any action it deems appropriate.

The new remit is intentionally opaque in terms of what is being offset (through carbon capture and storage (CCS) or the purchasing of carbon credits from other countries) in the net zero calculations, the goal of merely ‘facilitating’ a transition, and the timescales of this transition. It is thus opaque by design in ways that allow for flexibility regarding meaning and implications. As such, understanding the scale and character of institutional change will strongly depend on the interpretation of the remit by Bank actors on Threadneedle Street. Rather than a fundamental reorientation of the Bank at present, the remit thus typifies a form of ‘strategic ambiguity’, wherein legally and politically empowered technocratic monetary actors can address new political issues without incurring the politicisation of the central bank (van’t Klooster, 2022).

The perception of the mandate and its institutional implications are still subject to internal contemplation, conflict, and contestation, but these perceptions are being actively and strongly shaped by the Bank’s ‘Climate Hub’. Interviewees confirmed that it was established in 2015, shortly after Mark Carney’s Tragedy of the Horizon speech (BoE, 2015). It consists of approximately 12 experts and is currently led by Sarah Breeden, who is seen as passionate about this subject and has recruited a lot of people from her former team in Executive Deposit Takers. The Climate Hub is seen as a ‘one stop shop’ on green monetary policy, but primarily seeks to collaborate with all units of the Bank on integrating climate issues into the respective operations of each team. The Climate Hub is the centrifugal force of the Bank’s ‘hubs and spokes model’ of green institutional change, offering practical advice and instigating conversations on the environmental aspects of all policies and operations (Interview: Treasury A, C). The Hub instigates dialogue with each unit within the Bank on the environmental aspects of policy and operations.

Contrary to the focus placed on the Climate Hub by interviewees, our discourse analysis found that the Hub is scarcely mentioned in the Bank’s documents, warranting a mention in one official publication on prudential regulation (BoE, 2021e). This is not an insignificant institutional development, however, despite its recognition in the Bank’s publication and the lack of immediate policy changes resulting from the Climate Hub’s orchestration of internal discussions around the Bank’s operations. The institutionalisation of the Hub, in combination with the strategic ambiguity of the remit given to the MPC and FPC, provides a great degree of political indeterminacy regarding future monetary policy construction around the net zero transition.

The interpretation of the remit through processes of internal dialogue and collaboration with the Climate Hub shapes the impacts of the strategically ambiguous remit in two interconnected ways. The first is that it produces a variegated institutional change within the Bank. In other words, not every unit in the Bank will equally incorporate climate issues into its operations. Some units have already demonstrated a willingness to go beyond their obligations. For instance, the FPC has embraced climate policy through publishing disclosure reports that advance CRFR analytics and align with Taskforce on Climate-related Financial Disclosures commitments (BoE, 2021c; BoE, 2021e), while other units remain unaffected by the remit (at least in the short term). Interviewees tended to place greater rhetorical emphasis on some elements of bank operations rather than others, with most conceiving it in terms of risk management and thus under the purview of the FPC (Interview: Monetary policy experts: A, B, BoE, 2022b).

The second way that the collaborative approach to discerning the remit shapes the Bank’s evolution is that the new remit is seen in the context of and conditioned by pre-existing structural logic and institutional practices. This has produced conservative re-examinations of existing practice to discern opportunities for modification at the margins, rather than any drastic overhaul of existing institutional practice rooted in a recognition of the financial transition necessary to achieve decarbonisation targets or the precautionary principle (Chenet et al., 2021). This has often simply prompted minor or incremental evolutions of practice aligned with pre-existing trajectories and orthodox economic frameworks rather than path-shaping institutional transformation.

A clear manifestation of this is the continued internal focus on CRFR as the lens through which climate issues are understood rather than projections of a net zero transition, which dovetails with the recent development of the FPC’s analytics. In other words, the Bank continues to view climate change as a multitude of risks posed by climate change to financial stability, rather than the imperative to reorient policies to ensure ecological stability. Climate change has therefore become synonymous with ‘market failures’ and significant financial losses (BoE, 2022b). This focus has been referred to as a ‘prudential’ approach as opposed to a ‘promotional’ approach that seeks to align private finance with a low-carbon transition (Baer et al., 2021). The remit has, according to interviewees, bolstered the capacity of the Bank to manage CRFR through ‘iterative risk management enhancements’, for which ‘Pillar 2 is being used as a template’ (Interview: Monetary policy expert A, BoE, 2022c). Therefore, Bank action on the net zero mandate will not necessarily catalyse a drastic transformation of existing institutional practice. In contrast, existing institutional practice powerfully conditions interpretations of the new remit and, for some in the Bank, the mandate is validatory rather than catalytic.

Perceptions of the policy implications of the mandate: Price stability, net zero, and the Bank’s hierarchy of objectives

Although it can, and indeed has, been easy to overstate the impact of the mandate on the Bank, we found that the pre-existing institutional objectives of ensuring price and financial stability have been crucial in shaping the integration of the remit into the Bank’s various operations. There was a consensus among all interviewees, unsurprisingly, that the mandate is subservient to these pre-existing institutional objectives of the bank, just as in other central banks (Dafermos et al., 2018; van’t Klooster, 2022). It is a much lower priority and, indeed, in the minds of some Bank actors, it is not a ‘real mandate’ but rather an objective for which they must ‘have regard for’ when designing policies to achieve its primary objectives (BoE, 2022a).

This hierarchy of institutional objectives will only be reinforced at times of economic crisis (i.e. at times when the Bank has become a significantly more powerful and interventionist actor in economic governance). In these circumstances, in which path-shaping macroeconomic change becomes possible, the Bank has unequivocally prioritised re-stabilising the financial sector and the economy more broadly, often at the expense of environmental objectives. Indeed, recent crises, from the Financial Crisis to COVID-19, have shown that the Bank views make liquidity available for aviation or automotive companies as a higher-priority objective than environmental considerations (D. Bailey, 2023; Matikainen et al., 2017). According to interviewees, we can expect future crises to still be met by measures which support the firms and industries systemically integral to the prevailing national economy, regardless of the climate risks pertaining to ‘locking in’ the status quo.

The hierarchy of objectives is important to explicate here, not least because of the conflicts that exist between the objective of ensuring financial stability and the goal to facilitate a transition to net zero. The fear of many in the Bank is that a transition to net zero entails destabilising the ecologically intensive sectors of the national economy (including the aviation, automotive, construction, and energy sectors) and simultaneously creating ‘green asset bubbles’ in ways that undermine the Bank’s core objectives. For Bank officials, this results in an unfortunate need to balance the two elements of CRFR – medium-term physical climate risks and short-term climate transition risks. This is not an insuperable dilemma according to some state actors, but does require a governance strategy infused with incrementalism, which neither invokes instability through the immediate fire sale of fossil fuel assets nor the instability wrought by ecological breakdown. Medium-term timescales are central to the Bank’s strategy of managing its new mandate while meeting its pre-existing objectives.

It is in this context that we can locate the strategies for meeting the new net zero mandate. The CBPS was immediately identified by the Bank as a scheme ripe for reform after the mandate was announced (BoE, 2021b; BoE, 2021c), with numerous interviewees reaffirming that it was seen as ‘the primary monetary pool tool for facilitating net zero’, and the strategy of incrementally ‘tilting’ the portfolio away from unsustainable economic activity was borne of the perceived need to balance the dual sources of potential instability (Interview: Treasury D, monetary policy expert C). This tilting should serve to benefit more sustainable companies over time by reducing the yields on their bonds and creating more favourable conditions for financing green investments, while increasing the costs of borrowing for companies more threatened by CRFR; which has been the impact on eligible companies since the CBPS scheme was launched in 2016 (see Boneva et al., 2018; D’Amico and Kaminska, 2019).

There are internal debates in the Bank over how powerful the CBPS will be in realigning finance, with one interviewee claiming that it is like ‘trying to empty a swimming pool with a mug’ (Interview: Treasury C). The CBPS is a relatively meagre scheme – as we noted above at £20bn in contrast to total Bank holdings of £895bn – and so can be seen as a minimalist and non-disruptive response to the mandate. Albeit some have contended that the Bank’s corporate bond purchases also have significant wider ‘signalling effects’ on the financial markets that should not be downplayed (Dafermos et al., 2022).

The internal belief is that a great deal of energy had been poured into establishing a framework that adequately incorporates CRFR into bond purchases. This, however, has already been questioned by the analysis revealing that CBPS reforms will potentially undermine a realignment of private capital in aid of a sustainability transition through a continued commitment to market neutrality (see Dafermos et al., 2022). Given that the CBPS is the Bank’s flagship policy for facilitating a transition, the meagreness of the scheme and this critique of its reform casts doubt on the Bank’s commitment to incorporating the environmental mandate into its monetary policy operations.

A link can incidentally be drawn between the Bank’s tendency to purchase assets from carbon-intensive industries through its asset purchasing schemes and the United Kingdom’s continued reliance on such fuels. However, the Bank does not consider the macroeconomic shocks to the UK economy as being caused by climate risk. Rather, Governor Andrew Bailey’s (BoE, 2022d) recent assertation that the Bank will tame inflation makes no reference to the fact that the UK economy is exhibiting symptoms of an economy reliant on fossil fuels, nor that a more expedient transition to net zero would be the cure.

Despite the new mandate, therefore, the Bank remains far more comfortable developing CRFR assessments than facilitating a transition through ‘greening’ monetary policy. Numerous interviewees emphasised the role of the FPC in pushing for corporate disclosure of climate risk, the inclusion of CRFR in the Bank’s own analytics, strengthening its prudential regulation, and the provision of stylised future climate scenarios and their consequences for financial stability (of which the CBES is now the key example), which can serve as ‘roadmaps’ for commercial banks, equity firms, and insurance companies. To co-create a sense of direction with private actors, the Bank convenes the CFRF, alongside the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA), as part of its ‘macro financial’ workstream at the NGFS. The forum brings together climate scientists, policymakers, asset managers, and commercial bank representatives to disseminate research on CRFR and deliberate the financial aspects of a transition. These measures suggest that the Bank hopes that filling ‘information gaps’ will lead rational market actors to voluntarily adopt investment strategies that target firms less threatened by CRFR. Such a scenario would save the Bank from taking measures more coercive than the gradual and modest leveraging measures introduced already.

As such, under the new remit, the Bank looks set to continue developing its role in addressing ‘information gaps’ through CRFR assessments (under the stewardship of the FPC) and eschew any significant leadership role in instigating path-shaping economic changes that promote decarbonisation through the MPC (Baer et al., 2021; BoE, 2015; Chenet et al., 2021; Ryan-Collins, 2019). The pervasive belief among interviewees was that the democratically accountable (and more overtly political) fiscal policymakers in government must take responsibility for tackling the big issues of the day, including climate change and the transition to net zero. The Bank’s role, as interviewees perceive it, is to protect and enhance the stability of the UK financial system throughout the transition. As Sarah Breedon put it in a recent speech, ‘the Bank’s role in the transition is to understand how different transition pathways could affect the macroeconomy, the stability of the wider financial system, and the safety and soundness of the firms we regulate’ (Breedon, 2022). The policy implications of the mandate for the MPC, as such, appear to be minor.

The climate politics of the Bank of England

The expansion of the mandate is emblematic of significant institutional evolution within the Bank, even if it is not directly a catalyst for dramatic institutional transformation. The mandate to facilitate the transition to net zero has licenced, legitimised, and promoted the pre-existing analysis of CRFR – which continues to be the lens through which Bank actors understand the issue of climate change and the need for transition (Baer et al., 2021; Chenet et al., 2021) – and the deployment of these measurements in the Bank’s operations. This is key to understanding why Bank officials lobbied the Treasury for an expanded remit.

As we have shown, however, thus far the remit has been interpreted in distinctly conservative terms. The interpretations of the mandate and its implication for Bank operations have been conditioned by the Bank’s pre-existing and higher-priority objectives, its inscribed structural logics, and the epistemological supremacy of neoclassical economics that inculcates dereference to free markets as the optimal allocators of monetary resources and precludes any major subversion of market forces (Dikau and Volz, 2021; Svartzman and Althouse, 2022); conditions which have historically been circumscribed by the structural power of vested interests in the financial sector (Gabor, 2021; Ingham, 1984; Talani, 2011). These institutional characteristics and power dynamics have engendered enduring forms of governance within the Bank historically and have swiftly subsumed ambitions of leadership on mitigating CRFR.

The higher priority objectives include price and financial stability, which sit at the top of the Bank’s hierarchy of objectives and are often in conflict with the notion of a transition. Adopting a more radical approach to facilitating a transition would, certain actors in the Bank believe, threaten short-term financial instability by creating green asset bubbles and exacerbating the financial environment for carbon-intensive firms ‘in transition’, placing unnecessary expectations on some organisations and making others illiquid (BoE, 2022a). Simultaneously, there is an awareness that insufficient movement by financial markets and central banks will escalate medium-term CRFR. This of course takes place in a context of an already inflationary UK economy (due to Brexit, COVID-19 crisis management policies and the Russian invasion of Ukraine). The threat of financial instability, in both the short and medium terms, is seen to be stark. Therefore, while the Bank is conscious not to inflate green asset bubbles, it is also conscious of the bursting of carbon asset bubbles littered throughout the United Kingdom’s pre-existing growth model.

Nonetheless, the Bank, by its own calculations is set to ‘fall off the tightrope’ (BoE, 2022a). Since we undertook our interviews, the Bank has published the results of its CBES pathways, a key measure cited by interviewees, and the results outlined three potential pathways for the Bank (2022c): (1) Early Action (EA) – in which the Bank’s climate policy is ambitious from the outset, requiring an adjustment to the economy which may have an impact on growth in the short term, (2) Late Action (LA) – the implementation of policy is delayed by a decade leading to a more compressed transition resulting in short-term macroeconomic and financial disruption, and (3) No additional Action (NAA) – the absence of any further transition policies incurring a permanent macroeconomic disruption to the UK economy. The Bank asserts that its net zero objectives can be achieved through both the EA and LA scenarios. The CBES projections reveal that the Bank is set to miss the carbon budget and portfolio divestment targets that are aligned to a 1.5°C pathway and are thus in the LA scenario. This dovetails with the analysis of the CBPS by Dafermos et al. (2022). As such, our analysis found that this is less of a ‘balancing act’ than an ‘unbalanced act’. The prioritisation of price and financial stability in the Bank ensures a bias to the status quo (regardless of how slow the pace of transition in the capital markets is) that subjugates the task of managing medium-term CRFR by prompting a transition of financial investments.

This ‘unbalanced act’, reflected in the Bank’s implicit adoption of the LA, will only be exacerbated in any economic crisis. It is in cases of financial and economic volatility in the Bank that not only becomes even more powerful as an actor of economic governance through its various monetary interventions. But in these situations, the imperative of ensuring short-term financial stability will become even more central to the Bank’s market-reinforcing agenda, and as such attention will focus on shoring up the status quo, regardless of its environmental impacts or the implications for CRFR. The precarity of ‘walking the tightrope’ is only made more acute by the fact that the Bank’s attempt to arrest short-term financial instability, in turn, contributes to future crises incurred by extreme ecological conditions; just as, indeed, the COVID-19 pandemic was partly caused by ecological conditions (Carlson et al., 2022; Tooze, 2020).

These conflicting imperatives between managing short financial instability risks and medium-term CRFR are the result of decades of inaction on climate change by political authorities and industries globally. The Bank finds itself embedded in a crisis-ridden political economy and is now attempting to synthesise conflicting imperatives. Moreover, the tensions between financial stability and climate stability will only get worse the longer political action remains incommensurate to the scale of the net zero challenge.

Bank officials are insistent that a transition must be led by government actors through fiscal policy tools (and not unfairly given the government’s greater scope, democratic legitimacy, and policy instruments) (BoE, 2021e, 2022b, 2022c). As noted above, the Bank maintains that its role is limited to ensuring, as much as possible, financial stability throughout what could be a turbulent economic transition to net zero. Within the narrow parameters of its institutional scope, Bank officials affirmed that they were doing all they could to promote a transition. The current UK government, however, has also eschewed leadership on the transition to net zero, with ambitious net zero targets having not been followed by similarly ambitious fiscal action, despite Andrew Bailey’s purported enthusiasm to ‘build back better’ (A. Bailey et al., 2020).

It is in this context that we can locate the bank’s limited strategies for managing CRFR through efforts to improve the quality and transparency of information regarding CRFR and the exposure of different firms. Through developing risk assessment metrics and petitioning financial institutions to disclose their exposure, the expectation is that rectifying ‘information gaps’ will guide investors in new directions (Baer et al., 2021; Carney, 2015; Chenet et al., 2021; Stheeman, 2022). Existing institutional practice and neoclassical economic knowledge here is crucial is mediating the agenda in ways that produce this strategy of encouraging change through information provision and market mechanisms. Yet the Bank remains a site of contestation, and thus many Bank actors are seeking to be proactive in finding creative solutions to the problem within the entanglements of their current responsibilities and numerous Bank publications suggest that the Bank could go further.

There are numerous policy instruments that the Bank could, in principle, justifiably utilise in light of the modified mandate. The Bank’s asset purchases or the Energy Markets Financing Scheme (the successor to the Special Liquidity Scheme introduced following the Financial Crisis) could be directed towards the transition. In addition, the government’s mobilisation of state resources in the COVID-19 pandemic relied on significant covert assistance from the Bank to create greater fiscal space through the asset purchasing facility and the ‘Ways and Means’ facility, which could once again be seen to represent advantageous capacity in facilitating large-scale green public investment programmes (Bailey, 2020). As such, we should be careful not to endow any sense of inevitability on the environmental substance of the Bank’s future policies. The Bank is still in the early stages of measuring CRFR and integrating the implications into its risk management operations. It is plausible that the mutable remit could be reinterpreted in future years as the climate crisis becomes more destabilising and other central banks in the NGFS adopt bolder green measures. Currently, however, dominant interpretations on the ambiguous environmental mandate within the British state have been conservative and there is little indication that it will significantly affect monetary policy or the institutional disavowal of any ‘market-shaping’ role.

In the present moment, the context in which the Bank operates has dramatically changed, with potential consequences for the internal interpretations of the mandate and its scope for facilitation. The Bank has rapidly switched from fighting pandemic-related deflationary pressures to fighting inflationary pressures caused by supply side shocks to the economy, bringing forth new contradictions and tradeoffs between tackling price inflation, ensuring macroeconomic stability, and the governance of CRFRs. The Bank has been accused of exacerbating this change, given that it considered inflation to be a ‘transitory’ phenomenon in the first instance 1 (BoE, 2021f). Some have argued that, given that current inflation levels are linked to fossil fuel energy prices, the case for greener interpretations of the Bank’s existing mandates and strategies have been bolstered to decrease the possibility of similar inflationary shocks taking place in the future. Yet the new circumstances have several potential implications for the Bank’s agency in acting upon the net zero transition. Ultimately, inflationary pressures have likely reasserted the Bank’s primary objective and peripheralised lower priority goals. Meanwhile quantitative tightening, which the Bank began in 2021, temporarily renders discussions of ‘green QE’ moot, albeit the Bank remains poised to recommence bond purchasing at the outset of any crisis, as the events of the 2022 ‘mini-budget’ indicate. Higher interest rates, while worsening financial conditions across the economy, will have more deleterious impacts on smaller enterprises than industry incumbents in ways which will compromise path-shaping economic change (Packoff, 2023).

All the while, total investment in low-carbon sectors must more than double in the next 10 years to align global economy with decarbonisation targets (IEA, 2020). A dramatic and immediate shift in private investment patterns is needed if climate targets are to be met. There are few signs that large financial centres such as the City of London are turning away from industrial activities unaligned with Paris towards low-carbon investments. As Dafermos et al. (2022: 2) point out, the climate emergency cannot be addressed through economic policies that simply tinker around the edges. A sharp reduction in emissions requires bold changes in the design of economic policies and the implementation of unprecedented measures that will transform the structure of our financial systems.

The Bank’s governance continues to be incommensurate with the scale of transformation required to govern such a shift. The Bank’s new mandate has become entangled with pre-existing and conflictual structural logic in ways that make unconducive to the bold changes to monetary policy required to transform the financial sector on the scale and on the timescales necessary to meet decarbonisation targets.

Conclusion

Reorienting finance away from industries associated with ecological degradation is a vital component of a sustainability transition, and the politics of central banks is one of the key sources of political indeterminacy in this transition. The financial power of the City of London renders the UK’s Central Bank a key global actor, which endowed great salience to the expansion of the Bank of England’s remit to ‘facilitate the transition to net zero’ (BoE, 2021a). The interpretation of the new mandate and the consequential institutional change within the Bank is crucial in determining the governance of finance amid the purported transition to net zero.

A series of semi-structured elite interviews combined with a discourse analysis of Bank documentation and speeches, however, revealed that Bank actors lobbied for the new mandate to legitimise ongoing climate risk assessment developments and licence internal dialogue on its policy implications. The ‘strategic ambiguity’ of the mandate has enabled discussions around institutional reform orchestrated by the Climate Hub operating a ‘hubs and spokes’ model, which has resulted in variegated internal change within the Bank strongly conditioned by existing institutional objectives, frameworks, and practices. The FPC has been emboldened to incrementally advance its development of CRFR assessments, but the impacts on the MPC have been far more liminal. The mandate to facilitate a transition is not only seen to be subservient to pre-existing monetary policy objectives but in conflict with them, insofar as the transition entails the political disruption of the financial sector that threatens the core objectives of price and financial stability.

These findings suggest that the new remit is emblematic of long-run developments on CRFR rather than a catalyst for the green transformation of monetary policy. The remit may prompt minor institutional modifications to Bank operations, but it has not shaken the Bank’s pre-existing structural logic or its conviction that its role is to ensure stability while the more overtly political actors in the government lead on the transition. The Bank, therefore, will likely continue to eschew any strong market-shaping forms of governance that promote decarbonisation. Our analysis of the Bank contributes an empirical account of the institutional evolution of one of the key central banks in the global economy in the Anthropocene (Dikau and Volz, 2021; Siderius, 2022; Svartman et al., 2021). It provides an initial, albeit tentative, response to accusations that central banks afford little attention to the social or environmental implications of their monetary operations (van’t Klooster and Fontan, 2020). This examination of the Bank of England instead shows a greater institutional sensitivity to environmental impact, though its actions remain in some way short of the change required to align monetary policy with the UK’s Net Zero objectives. Such an institutional reappraisal speaks not only of the ongoing debates about the technocratic changes brought about by the Financial Crisis (Spielberger, 2022, van’t Klooster, 2022), but also of the broader politicisation of political and economic institutions once considered insulated from environmental politics (Dafermos et al., 2018; Marquardt and Lederer, 2022). What remains uncertain, and undoubtedly the subject of future scholarship, however, is whether the Bank maintains its present ‘market neutral’ position as CRFRs continue to intensify.