Abstract

Theories of ‘growth models’ explain capitalist diversity by reference to shifting drivers of aggregate demand in different national economies. This article expands the growth models framework beyond its conventional focus on debt-driven and export-driven demand, through an ideational analysis of Thatcher’s vision of a property-owning democracy, and Blair’s knowledge-driven growth agenda. Drawing on policymakers’ statements, it shows how these hypothetical growth models differed from the debt-driven growth model that ultimately prevailed. Using data on the distribution of wealth and wages, it highlights how both approaches failed to generate sustainable demand; in Thatcher’s case, because of an insufficiently broad distribution of capital ownership, in Blair’s case, because of an insufficiently broad distribution of lucrative knowledge work. This indicates that explanations of dysfunctional growth models need to consider not just the split of national income between labour and capital, but also the distribution of both labour income and capital income between households.

Keywords

Introduction

Theories of ‘growth models’, as with many analyses in the field of political economy, focus upon the social, institutional, political and economic structures that underpin developments in politics and the economy. In contrast to theories of capitalist diversity that highlight supply-side differences in the institutional configuration of production – the relationships (or lack thereof) between government, organised labour, the educational system and private firms (e.g. Hall and Soskice, 2001) – the growth models approach emphasises the significance of demand, drawing attention to the different ways in which developed democracies have sought to substitute for broad-based wage-led increases in aggregate demand since the crisis of Fordism in the 1970s. 1 The extent to which post-Fordist demand is driven by business investment, government spending, exports and/or private consumption (which itself might reflect either or both of wage growth and expanding household debt) has implications for the political and economic configuration of countries. It influences the composition of their economies (their relative reliance upon finance, manufacturing, in-person services and so forth, both for productivity growth and for employment), as well as their policy options (Baccaro and Pontusson, 2016). Growth models also have implications for the relationship between countries: with countries that relied on credit-fuelled household consumption to drive demand often acting as export markets for countries that maintain demand by running a persistent current-account surplus (Johnston and Regan, 2018).

Interestingly, these analyses suggest that many of these post-Fordist growth models are (more or less) dysfunctional – that is to say, incapable of producing stable growth over the longer term. In place of rising demand predicated upon broad-based wage growth, countries such as the United Kingdom and the United States have instead depended on debt-fuelled household consumption as a source of demand, a form of ‘privatised Keynesianism’ reliant upon the ongoing availability of cheap credit, often secured against booming house prices (Crouch, 2009; Hay, 2013; Jessop, 2015). But countries that rely upon export-led growth (such as Germany) might find themselves in a similarly unsustainable position, if demand in the markets that they are exporting to is also reliant upon debt-fuelled household consumption.

This raises an important question: how do countries come to adopt dysfunctional growth models? The goal of this article is to show the centrality of ideas to this process. Building on Lavoie and Stockhammer’s (2013) insightful typology of growth models, it argues that studying the way in which growth models were explained and justified by key political actors provides insight into how popular support for dysfunctional growth models has been mobilised and sustained. Moreover, to the extent that we can interpret these ‘hypothetical growth models’ not just as propaganda or ‘statecraft’, but as a reflection of the cognitive beliefs of policy elites, these ideas (and their shortcomings) may have played a causal role in the (unwitting) adoption of dysfunctional growth models.

Specifically, this article reconstructs the growth models implicit in the property-owning democracy discourse of the Thatcher era, and the knowledge-driven growth discourse championed by Tony Blair. It shows how these hypothetical growth models differed, not just from the dysfunctional debt-driven reality of the British growth model, but also from the hypothetical growth model that Lavoie and Stockhammer describe as ‘neoliberalism in theory’. This analysis helps to explain both the appeal and the limitations of these growth models, and how they related to the realities of UK economic policymaking in recent decades.

Clearly, analyses of the economic policies and ideologies of Thatcher and Blair are legion; any article-length treatment of this subject can only present a highly reductionist account of the pluralism of British political debate and policymaking under the two longest-serving Prime Ministers of modern times. Moreover, neither Thatcherism nor Blairism was particularly concerned about the demand-side of the economy. In keeping with the dominant economic orthodoxies of their times, their respective agendas focused on supply-side reforms to increase productive capacity, assuming that demand would follow. Nevertheless, by focusing on the demand implications of these economic policy programmes, we gain valuable insight into the evolution of the UK growth model in particular, and the origins of dysfunctional growth models more broadly.

To this end, the article begins by outlining Lavoie and Stockhammer’s (2013) classification of countries depending on their comparative reliance upon profit-led or wage-led demand, and whether their distributional policies favour capital or labour. Only where demand and distribution are aligned would we expect to see a stable growth process. The following section explores how Thatcher’s imagined ideal of a ‘property-owning democracy’ satisfied this criterion, implying a profit-led demand model under pro-capital distributional conditions. However, it also highlights how this model required capital to be widely distributed within society. While the fire-sale of state assets gestured in this direction, Thatcher ultimately presided over a concentration of productive capital in the hands of a wealthy few. The penultimate section examines how the concept of knowledge-driven growth, championed by Blair, implied a shift in bargaining power from capital to labour, and thus a stable wage-led growth process – despite only minor changes in economic policy direction. Interestingly, the New Labour government did coincide with a shift in the distribution of national output in favour of wage earners. However, the fact that this shift also coincided with increased income inequality meant that the proceeds of growth once more accrued to individuals with a lower marginal propensity to consume, undermining wage-led growth. Both cases highlight the importance not just of the distribution of national income between capital and labour, but also the distribution of national income within capital and labour shares (Behringer and van Treeck, 2019; Clift and McDaniel, 2021). The article concludes by highlighting some of the broader implications of this analysis, both for academic political economy, and for the practice of economic policy in developed democracies today.

Growth models

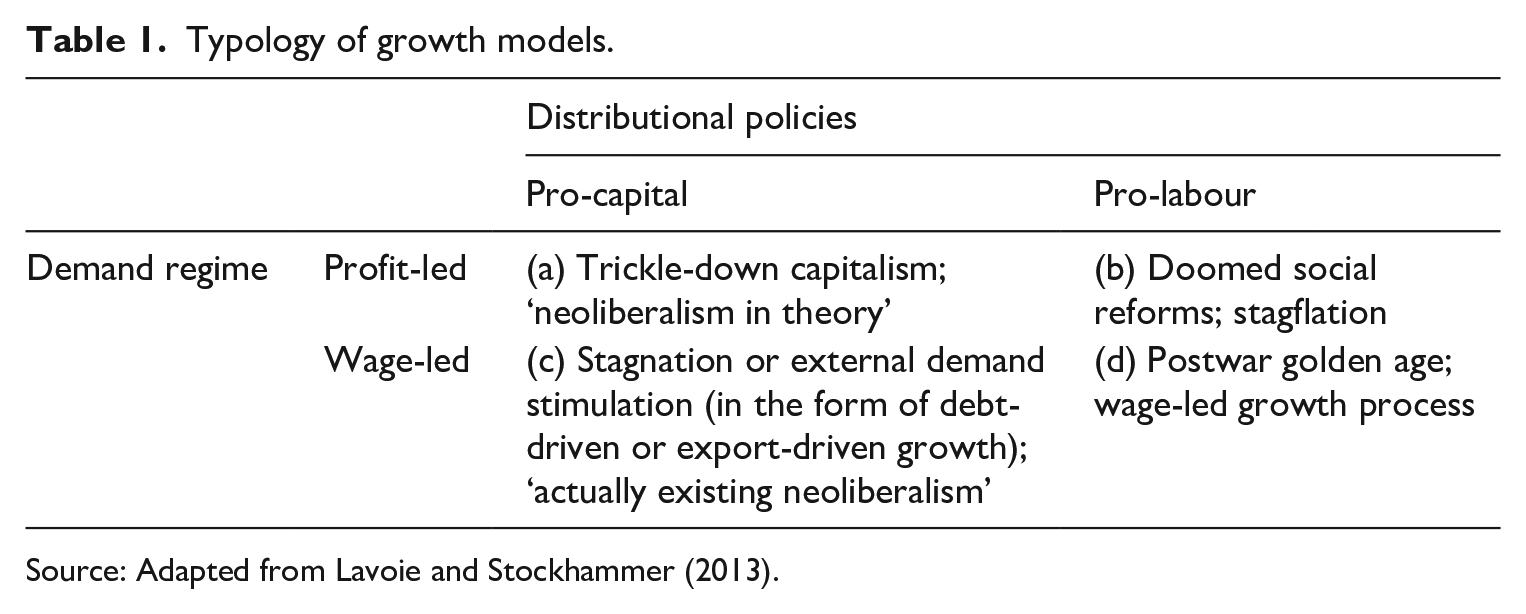

How do countries come to adopt dysfunctional growth models? A schematic answer to this question can be found in one of the key contributions to the growth models literature: Lavoie and Stockhammer’s (2013) account of wage-led growth. The authors identify a typology of growth models, differentiated along two dimensions (see Table 1). On this account, the ‘distributional policies’ of a particular country can be configured so as to distribute overall output (to a greater or lesser degree) towards capital or towards labour. Demand can depend (to a greater or lesser degree) upon the spending of profit-earners, in the form of business investment and/or spending by households that receive income from capital, or the spending of wage earners (a country’s ‘demand regime’).

Typology of growth models.

Source: Adapted from Lavoie and Stockhammer (2013).

Dysfunction arises when growth is wage-led but distributional policies funnel national income towards capital, or when growth is profit-led but distributional policies funnel national income towards labour. In both of these cases, there is insufficient demand to sustain economic growth, leading either to stagnation, or to the adoption of unsustainable substitutes, such as debt-driven consumption, or net exports to economies engaging in debt-driven consumption. This analysis draws heavily on neo-Kaleckian macroeconomics. Kalecki (1944) argued that redistribution of income from rich capitalists to poor labourers offered the best way of generating the aggregate demand necessary to driving full employment (stimulating consumption, thereby stimulating capital investment and thus job creation). More recently, scholars have noted that the demand implications of shifting the distribution of national output from capital to labour in this way are ambiguous: Bhaduri and Marglin (1990) note that increased profits can stimulate higher levels of capital investment and thus employment, consumption and growth. If the former dynamic dominates, growth is ‘wage-led’; if the latter holds true, growth is ‘profit-led’ (see also Baccaro and Pontusson, 2016).

On Lavoie and Stockhammer’s account, dysfunctional growth regimes have arisen from an anti-clockwise journey around Table 1, beginning in the bottom-right quadrant (d), representing the Fordist compromise of the postwar era. This period was characterised by pro-labour distributional policies, such as strong trade unions, comprehensive employment rights and collective wage-bargaining arrangements. When growth is ‘wage-led’, such policies imply a virtuous circle of mass consumption incentivising greater business investment, enhancing productivity to drive up wages and profits alike, ensuring consumption continues to grow.

Arguably, however, this outcome depends upon the managed international capital flows of the Bretton Woods era, and is incompatible with the globalisation of trade and finance. As the postwar economic order unravelled over the course of the 1970s, attempts to skew national income towards labour (or even maintain the existing distribution) did not produce domestic investment but rather import-driven consumption, currency devaluation, inflation and unemployment: the doomed social reforms attempted by the likes of Mitterrand in the early 1980s (Hall, 1986). In an era of globalisation, growth is necessarily profit-led, and pro-labour distributional policies would thus stymie growth, as per cell (b) of Table 1. (The extent to which this diagnosis of globalisation is empirically accurate is of course contestable – for a useful summary of the often-weak evidence, see Hay and Wincott, 2012, especially Chapter 3.)

If this analysis is correct, and growth is profit-led – namely, if higher profitability encourages greater investment, job creation and consumption – then pro-capital distributional policies should drive up growth, as spending by businesses and owners of capital supports aggregate demand. Pro-capital distributional policies include many of the economic reforms familiar from the last 40 years of neoliberal economics: labour market flexibility, reductions in trade union powers, lower minimum wages and decreased welfare spending. Lavoie and Stockhammer identify this growth model with the theory of trickle-down economics commonly associated with neoliberalism, corresponding to cell (a) of Table 1.

There is a paradox here however: why should businesses reinvest their profits, on the trickle-down account? Where is the demand to inspire that business investment coming from? If the distribution of national output is skewed in favour of capital, then one possibility is that this demand will come from recipients of capital income. This form of sustainable capital-led growth assumes either (1) that there are only small differentials between capital and labour income, in terms of their recipients’ propensity to consume (Baccaro and Pontusson, 2016; Lavoie and Stockhammer, 2013) or (2) that capital anticipates demand from future wage earners, who see a substantial productivity-driven expansion in their wages, even after adjusting for an enlarged capital share of national income. If these assumptions do not hold, then demand under pro-capital distributional policies must either fall short (leading to unused capacity and unemployment), or come from an alternative source, such as debt-driven household consumption or net exports.

Debt-driven household consumption cannot be sustained indefinitely; at some point, unavailability of credit will lead to a shortfall in demand, and thus damage growth. Strikingly, Lavoie and Stockhammer argue that the same is generally true for net exports too. This needs further explanation: might export-led growth not be a viable strategy for countries in a neoliberal era, with the wage demands of disciplined labour lowered in order to maintain international competitiveness, and businesses investing in future productive capacity in return (a pattern commonly associated with the coordinated market economies of northern Europe, as per Hall and Soskice, 2001)? Lavoie and Stockhammer point out that such a dynamic can only apply in a limited number of countries at any given time. Because the world as a whole is a closed economy, demand for these exports in the net-importer countries must come from (1) higher debt levels, (2) a higher propensity to consume among recipients of capital income and/or (3) productivity-fuelled wage growth. To the extent that (1) predominates, net exports are as unsustainable a source of demand as debt-driven consumption – leading Lavoie and Stockhammer to characterise both these possibilities as examples of pro-capital distributional policies in the context of a wage-led growth regime, corresponding to cell (c) of Table 1.

Why, then, do governments adopt (and persist with) dysfunctional growth models? Interestingly, the mismatch Lavoie and Stockhammer posit between ‘neoliberalism in theory’ and ‘neoliberalism in practice’ suggests that ideas may play an important role in explaining growth model dysfunction. One possibility is that political actors may have intended to bring about the stable growth model of ‘neoliberalism in theory’, but due to mistaken beliefs about the prevailing demand regime, instead made decisions that resulted in dysfunctional ‘neoliberalism in practice’. On this account, choice of growth model can be explained (at least in part) by policymakers’ ‘instrumental’, ‘epistemic’, ‘causal’ or ‘cognitive’ beliefs about the economy, neatly described by Vivien Schmidt as ideas about ‘what is, and what to do’ (Schmidt, 2008: 306; see also Béland and Cox, 2010; Campbell, 1998; Hall, 1993). 2 Alternatively (and potentially also additionally), the idea of ‘neoliberalism in theory’ may have helped to secure popular support for ‘neoliberalism in practice’, by promising that pro-capital distributional policies would result in broad-based economic growth (a critique of trickle-down economics as propaganda often levelled by Marxist scholars – see, for example, Harvey, 2005). In this instance, policymakers need not have believed the case for ‘neoliberalism in theory’ for themselves. They might have self-consciously acted in the capitalist interest, promoting pro-capital distributional policies as an end in themselves, as on the Marxist account; or they might have been indifferent as to the outcomes of this economic policy agenda, choosing it primarily for its strategic merits in terms of partisan politics, as scholars of ‘statecraft’ have sought to argue with reference to both Thatcher and Blair (Bulpitt, 1986; Burnham, 2001).

Irrespective of whether ‘neoliberalism in theory’ reflects mistaken cognitive beliefs on the part of policymakers, or a more-or-less disingenuous way of securing popular support, Lavoie and Stockhammer’s account suggests that understanding policy elites’ ideas will help to explain the adoption and persistence of dysfunctional growth models. The remainder of this article will evaluate this ideational explanation of growth model dysfunction by reference to two examples from recent UK political history: Thatcher’s property-owning democracy and Blair’s knowledge-driven growth.

Thatcher and property-owning democracy

That Thatcher saw the British economy as entering an era of profit-led demand was evident from her first speech as Conservative leader:

the way to recovery is through profits, good profits today leading to high investment, leading to well paid jobs, leading to a better standard of living tomorrow. No profits mean no investment and that means a dying industry geared to yesterday’s world, and that means fewer jobs tomorrow. (Thatcher, 1975)

Consistent with this outlook, Thatcher embarked upon a series of supply-side reforms that sought to improve profitability, at the expense of labour’s share of national income. These pro-capital distributional policies included wide-ranging tax cuts for businesses and higher earners; changes to the scope and generosity of the welfare state, reducing support for lower income households; and labour market reforms designed to disempower trade unions and diminish employee rights. To the extent that demand entered into the equation at all, the assumption appears to have been that businesses would invest and recipients of enhanced profits would consume, thereby sustaining demand through a trickle-down effect.

Yet, this interpretation of the Thatcherite growth model omits an important part of her policy agenda, one that was also foreshadowed in her 1975 conference speech. In her opening oration, Thatcher (1975) depicted herself as ‘following in the footsteps . . . of Anthony Eden, who set us the goal of a property-owning democracy – a goal we still pursue today’. Thatcher would return to the idea of property-owning democracy repeatedly throughout her premiership, intertwining it with the theme of popular capitalism:

We Conservatives believe in popular capitalism – believe in a property-owning democracy . . . The great political reform of the last century was to enable more and more people to have a vote. Now the great Tory reform of this century is to enable more and more people to own property. Popular capitalism is nothing less than a crusade to enfranchise the many in the economic life of the nation. (Thatcher, 1986)

The concept of a property-owning democracy had a long history in Conservative Party intellectual circles, as an alternative to socialist nationalisation and state provision (Francis, 2012; Howell, 1984). Under Thatcher, the idea would become closely associated with two initiatives in particular: the sale of publicly owned housing stock, under the auspices of the ‘Right to Buy’ scheme, and the privatisation of state-run enterprises (Béland, 2007; Edwards, 2017).

The ‘Right to Buy’ legislation allowed tenants of state-owned council housing to purchase their homes at heavily discounted prices, transferring a substantial quantity of assets from the public sector to private individuals. As one of the architects of the 1980 Housing Act noted, accurately, ‘no single piece of legislation has enabled the transfer of so much capital wealth from the state to the people’ (Heseltine, 1980). The new law allowed tenants of council housing of at least 3 years’ standing to purchase their homes at a hefty discount (from a 33% reduction on market price up to 50%, for residents with a tenancy of 20 years or longer). Local authorities were obliged to offer mortgages to purchasers (Wilson, 1999).

The Thatcher government’s privatisation plans resulted in a further transfer of wealth from the public sector to the private sector. Notably, privatised industries were not simply auctioned-off to the highest bidder. Employees and members of the general public were generally given the opportunity to purchase shares too, and were often prioritised ahead of larger investors when share offerings proved oversubscribed (Parker, 2009, 2013); Oversubscriptions were themselves hardly surprising given the generous discounts on offer. The privatisations of British Telecom in 1984 and British Gas in 1986 were accompanied by broad-based marketing campaigns, intended to raise public awareness of the sell-offs and encourage average households to invest in equities for the first time. Indeed, the privileging of small investors caused consternation in some Conservative circles, where the trade-off between pursuing a property-owning democracy, generating a fiscal surplus for the Treasury, and pleasing ‘big City investors’ was explicitly acknowledged (Francis, 2012: 293). These tensions highlight how broadening asset ownership did not always sit comfortably alongside more conventional pro-capital distributional policies.

Significantly, ‘property-owning democracy’ appears to offer an alternative to trickle-down economics as a means of resolving the problem of demand under a pro-capital distributional regime – at least, in theory. Recall that the key puzzle of a profit-led demand regime is what incentivises businesses to invest. Trickle-down economics requires consumption demand from capital owners, implying labour and capital have broadly comparable marginal propensities to consume, a conjecture that finds limited empirical support in modern capitalist societies (Stockhammer, 2015). By contrast, property-owning democracy posits a wider distribution of capital, and thus a wider distribution of capital income – aligning the tendency to consume capital income more closely with the average household’s marginal propensity to consume.

Such a growth model would however require a far-reaching redistribution of the total capital stock. The Thatcher government’s redistributive efforts focused only on government-owned assets, and even then only a fraction of these were redistributed to poorer households with a higher marginal propensity to consume. Although between 1979 and 1988, the percentage of the population who owned shares increased almost threefold, this still represented only around one in five people (Marsh, 1991: 474). Between 1979 and 1997, the proceeds of privatisation averaged a mere 0.7% of gross domestic product (GDP) per year (Coutts and Gudgin, 2015: 35): even accounting for the fact that hefty discounts ensured that the value of the capital purchased exceeded the price paid, the volume of productive assets redistributed was clearly modest. Indeed, strictly speaking, only the discounted portion of these assets was redistributed rather than merely exchanged, as these assets were sold at an undervalue rather than given away for free (aside from modest allocations of share capital to existing employees – see Parker, 2009, 2013). And, although there is minimal data available regarding the characteristics of the households that participated in these share sales, it seems probable that the primary beneficiaries were more affluent households with a lower marginal propensity to consume. Certainly, the majority of shares were sold to financial institutions, to the benefit of them and their customers (Parker, 2013: 520–521).

By comparison, the Right to Buy scheme involved a greater volume of assets, sold at larger discounts, to a broader cross-section of society. Between 1980 and 1996, local councils, housing associations and new town corporations sold almost 1.8 million dwellings under the scheme, the bulk of them in the period 1981–1990 (Wilson, 1999). The proportion of owner-occupied housing stock increased from 52% in 1971 to 58.6% in 1981 and 68% in 1991 (Backhouse, 2002). However, for owner-occupiers, appreciation in the value of housing stock did not amount to a new income stream that could be used to supplement consumption spending. To realise these gains required either selling the asset (therefore relinquishing future capital appreciation), or else borrowing against it. In theory, it might be argued that such borrowing-for-consumption is not necessarily an example of debt-led demand: net household debt might be stable, if households only borrow against long-run trends in asset appreciation and capital accumulation. Nevertheless, there is a clear affinity between this hypothetical growth model and its debt-driven counterpart, as both presuppose the growth of the financial system and the expansion of consumer credit, leveraging up households such that they become more vulnerable to market shocks; the difference is that the hypothetical growth model also assumes that households and lenders have the foresight to navigate this, smoothing demand across the asset-price cycle.

A further problem with property-owning democracy as a growth model relates to changes in patterns of ownership. Over time, the distribution of capital (and capital income) will be reshaped through the market choices of private actors. The fact that returns on capital are brought within reach of poorer households with a higher marginal propensity to consume means that, over time, their share of wealth will decline relative to that of more affluent households that save and reinvest a higher proportion of those returns. Even in a property-owning democracy, pro-capital distributional policies will lead to a concentration of capital income among those with a lower marginal propensity to consume.

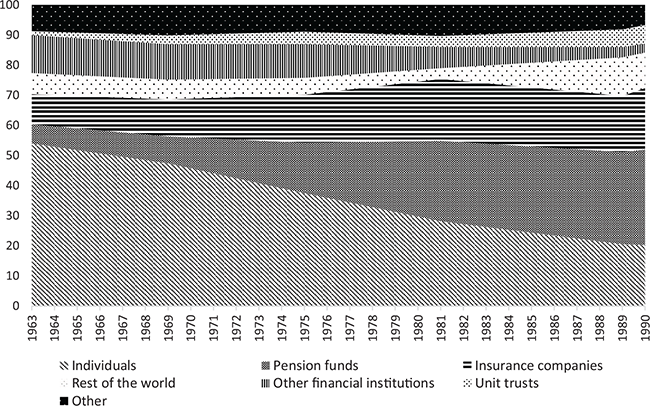

Such dynamics were clearly visible in the UK context. Over and above the modest extent of the initial redistribution of capital that Thatcher’s privatisation agenda achieved, analyses of share ownership patterns suggest that only around 40% of the original purchasers of shares in newly privatised companies still held their stake by the end of the 1980s (Marsh, 1991: 474). Viewed in terms of market capitalisation, the overall trend in share ownership in UK companies over the Thatcher years was away from small retail investors, towards larger institutional investors – in 1975, individuals owned 37.5% of UK quoted shares, but by 1990, they only held 20.3% (Figure 1). 3 It was common to see a rapid decline in shareholdings in newly privatised companies, as small investors cashed-out. The number of shareholders in British Steel fell from 650,553 when privatised in 1988 to 335,224 by March 1991, while the number of shareholders in BAA fell from 2,187,500 in July 1987 to 798,643 in June 1990 (Parker, 2013: 520). The effect of Thatcher’s reforms on home ownership was more durable, reflecting the tendency of people to remain owner-occupiers once they have stepped on to the ‘housing ladder’. Nevertheless, UK home ownership levels peaked in 2003 (Heywood, 2011), and, despite a modest uptick from 2016, they remain markedly lower than their historical high (Pacitti and Tomlinson, 2020). The secular trend towards lower property ownership levels looks set to continue, as younger cohorts increasingly struggle to raise deposits amid wage stagnation and rising property prices (Cribb et al., 2018).

Ownership of UK-listed shares (percentage total market value).

To summarise, then, in theory, the growth model of property-owning democracy offers a solution to the demand deficiencies of trickle-down economics. Broadening capital ownership can bring the marginal propensity to consume capital income into alignment with wage income, rendering stable growth viable under neoliberal distributional policies. In practice, however, this growth regime requires an ambitious initial redistribution of the total capital stock (not just publicly owned assets), and this redistribution must be periodically repeated – putting it in tension with conventional pro-capital distributive policies. Faced with the modest scale of Thatcher’s redistributive achievements, it is reasonable to query whether her government genuinely sought to implement a property-owning democracy and was simply mistaken in its analysis or thwarted in its efforts, or whether her version of property-owning democracy should be considered primarily as a rhetorical gloss applied to a more conventional profit-led growth model, as Marxist scholars or analysts of Conservative ‘statecraft’ might argue.

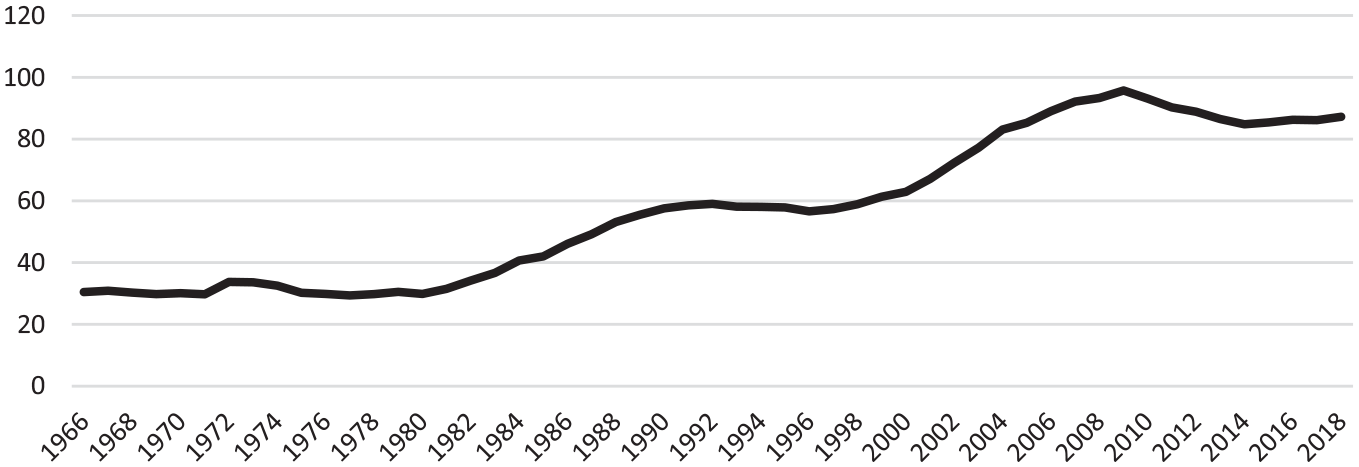

Nevertheless, understanding the hypothetical growth model advanced by the Thatcher government still illuminates the evolution of the United Kingdom’s actual growth model. Most obviously, it highlights another way in which ‘neoliberalism in practice’ might be justified, which may hold more popular appeal than the comparatively austere injunctions of trickle-down economics. In practical terms, too, the policies associated with the creation of a property-owning democracy contributed to the emergence of a debt-driven growth model. The sale of public assets created demand for consumer credit products to help households to purchase and manage these assets (Edwards, 2017). The burgeoning financial services industry facilitated the rapid expansion of household borrowing, from circa 30% of GDP in 1980 to circa 60% of GDP by the early 1990s (Figure 2). That growth unravelled so dramatically following the housing price crash of 1989 indicates the extent to which demand had relied upon debt (often related to short-term trends in asset prices, particularly housing), rather than stable long-run trends in wages coupled with broadly distributed capital income and gains (Backhouse, 2002; Hay, 2013; Wood and Stockhammer, 2020). At the same time, the reliance of demand upon debt should come as little surprise, given the relatively limited degree to which Thatcher’s government actually redistributed capital and capital income.

United Kingdom household debt as a percentage of GDP.

Blair and the knowledge economy

Blair’s government has often been portrayed as continuing the Thatcherite growth model, relying upon rising house prices and increasing household debt as a driver of demand, a growth model that ultimately unravelled with the credit crunch of 2007–2008 (Carstensen and Matthijs, 2018; Hay, 2013; Jessop, 2015). Certainly, Blair left many of the pro-capital distributive policies of the Thatcher era in place, including deregulated labour markets, private sector involvement in the provision of public services, and low taxes on corporations and high-income individuals (Taylor, 2007). Demand in the United Kingdom remained stubbornly dependent upon average households, who typically owned minimal capital other than a share in their own homes – and whose confidence as consumers depended upon rising house prices as collateral.

Yet, these were not the terms in which key architects of New Labour presented and justified their policies; and they may not have been the terms in which they understood these policies either. Senior Labour figures argued that the bargaining power of labour could be strengthened in spite of pro-capital distributional policies, provided government invested adequately in skills and digital infrastructure. Translated into growth models terminology, New Labour was effectively claiming to have devised a new form of wage-led growth.

In order to understand the logic behind this hypothetical growth model, it is necessary to revisit the understanding of the ‘knowledge economy’ that rose to prominence in UK and US policy circles during the 1990s (e.g. Coyle, 1999; Reich, 1991). According to this account, advanced capitalist democracies were undergoing a shift away from economic growth based upon the physical production of physical goods and services, towards economic growth based upon intellectual labour, often culminating in the production of intangible outputs such as new designs, processes and software code. Knowledge-intensive sectors of the economy – such as computer programming, the creative industries, finance or pharmaceuticals – would become increasingly important as providers of jobs and drivers of productivity growth. Knowledge work would play an increasingly prominent role in other sectors, too, as routine functions such as processing sales or providing generic information were automated, liberating human workers to focus on designing and maintaining these systems, or providing bespoke advice tailored to individual customers. The production of ‘knowledge’ depended upon the advanced skills and expertise of knowledge workers, and thus countries that could offer businesses a bountiful supply of highly educated labour would capture the lion’s share of this growth (O’Donovan, 2020).

On this account, the rise of the knowledge economy promised to shift bargaining power away from capital and towards (skilled) labour, due to the declining relevance of traditional capital to the production process, relative to the ideas and expertise of staff. Influential figures within and around New Labour were quick to emphasise this point. As Geoff Mulgan – who would go on to lead the Number 10 Policy Unit under Blair from 2003 to 2004 – claimed in his 1997 book, Connexity:

In the twenty-first-century economy the most valuable things are rarely physical, and it is possible to create wealth almost out of nothing, or rather nothing more than ideas . . . Virtual companies are being established without an office and in some cases without even a staff. Others have no easily definable property. Small software companies regularly emerge as if from nowhere to become corporate titans, just as traders now deal on world markets from remote cottages. (Mulgan, 1997: 214)

If capital is of declining economic importance relative to skilled labour, then it follows that successful businesses need to treat their knowledge workers well in order to reap the benefits of their expertise. As a Department of Trade and Industry white paper put it, ‘modern and successful companies draw their success from the existence and development of partnership at work’ (Department of Trade and Industry, 1998: 3). Charles Leadbeater, a sometime adviser to the 10 Downing Street Policy Unit during the Blair years, made a similar point in his 1999 book, Living on Thin Air:

A traditional company is founded on the assertion of the shareholders’ property rights. A know-how company is founded on an agreement among producers to relinquish their rights to their work and to combine together . . . As economies become more knowledge-intensive, there will be more know-how-based companies, owned through social contracts between knowledge workers rather than by traditional shareholders. (Leadbeater, 1999: 177–178)

Framed in the language of growth models analysis, these commentators were claiming that the rise of the knowledge economy implied a shift in the distribution of national income, away from capital and towards labour. Crucially, this shift did not require a major change from the labour market policies of the neoliberal era (Addison and Siebert, 2002). Rather than empowering workers vis-à-vis capital through a formal change in their employment rights, policymakers instead had to provide workers with education, which would strengthen their bargaining position due to underlying changes in the composition and needs of the economy. As the Department of Social Security insisted in a 1998 green paper, ‘employment security increasingly depends not on attachment to a single employer, but on having skills that will attract a range of employers’ (Department of Social Security, 1998: 43). Blair (2007) himself put the point even more bluntly, declaring in one of his final speeches as Prime Minister that ‘the challenge today is to make the employee powerful, not in conflict with the employer but in terms of their marketability in the modern workforce’. By ensuring individual workers had marketable skills, advanced capitalist economies could enjoy all the efficiency gains of flexible labour markets, while simultaneously strengthening the bargaining power of employees relative to their employers.

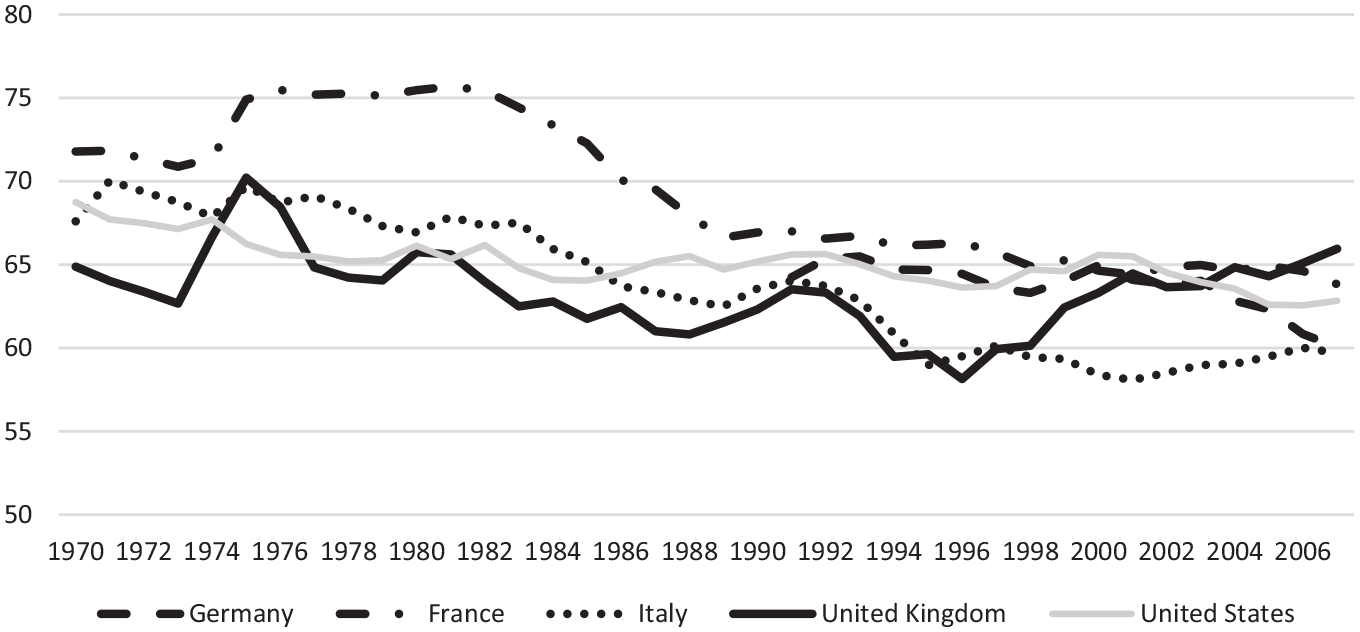

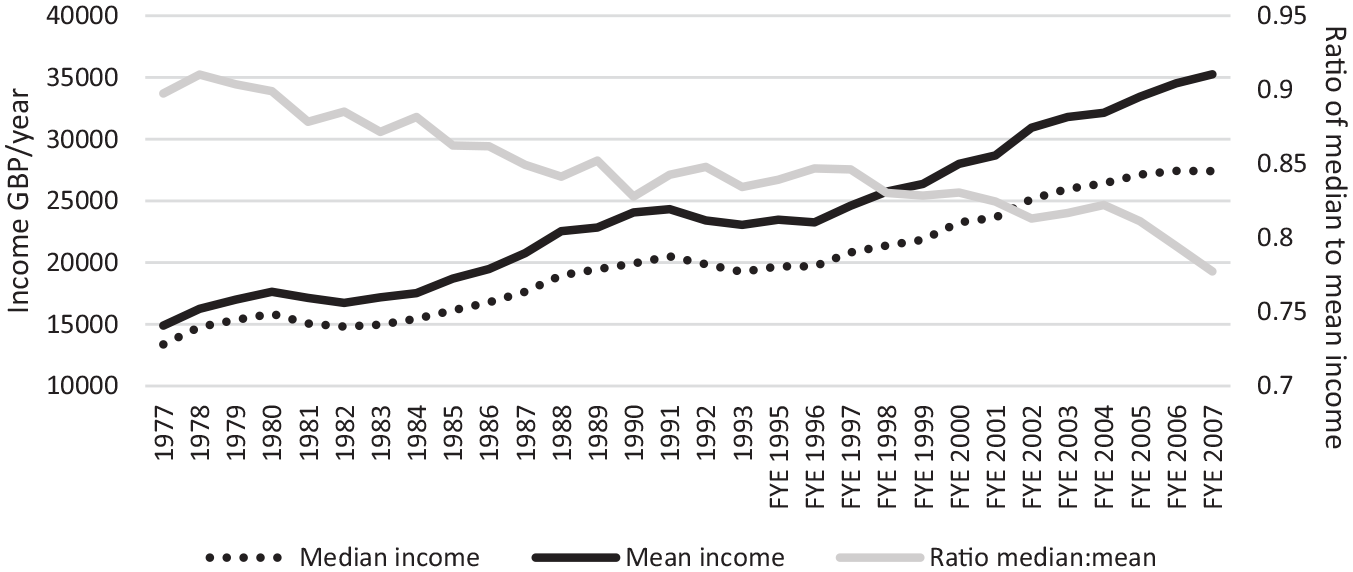

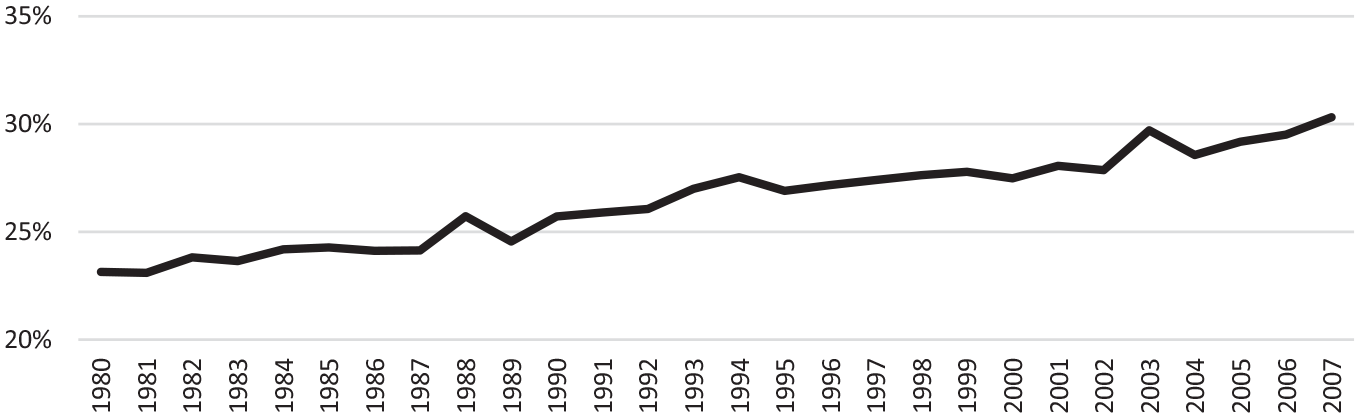

Interestingly, the claim that the rise of the knowledge economy involved a shift in bargaining power from capital to labour is consistent with UK data. As Figure 3 indicates, in the United Kingdom, the wage share of national income increased from the mid 1990s to the early 2000s, leaving it higher by the time Blair stood down than at any point since Thatcher took office. In and of itself, however, this shift was insufficient to change the United Kingdom’s growth model to broad-based wage-led demand, because it also coincided with rises in income inequality. While the decline of median income levels relative to mean income levels that took place over the 1980s halted in the early 1990s, the trend resumed from 1997 onwards (Figure 4), and the share of national income accruing to the top 10% of earners continued to increase over this period, albeit at a slightly slower rate than in the 1980s (Figure 5). In growth models terms, this pattern might be seen as an alternative form of ‘neoliberalism in practice’. Even though the distribution of national income shifts away from capital back towards labour, because the distribution of wage income between households is skewed in favour of the more affluent (who have a lower marginal propensity to consume), the expected demand benefits fail to emerge. This raises an important methodological point: analyses of growth models need to pay greater attention to the distribution of wage increases, rather than assuming that increases in the labour share straightforwardly translate into broad-based wage-led demand (Carvalho and Rezai, 2016).

GDP wage share at current factor costs.

Divergence in mean and median income levels.

Post-tax income share of top 10%.

In theory, New Labour’s knowledge-based growth model might have addressed these distributive problems. If increasingly unequal salaries were a consequence of demand for highly skilled workers, then increasing the supply of these workers (through social investment in education) should curb the premium they command. Highly educated young workers were indeed among those enjoying significant wage increases during this period; Walker and Zhu (2008) document an increase in the wage premium enjoyed by the top quartile of young UK graduates between 1994 and 2006 (of 12% for men and 10% for women), despite the expansion in higher education that took place from the late 1980s onward. Blair (2000) seemed to subscribe to this analysis of the origins of wage inequality, arguing that knowledge-driven growth would – without further intervention – ‘be the sole domain of elite knowledge workers’; his social investment agenda was intended to combat these trends and ‘democratise the new economy’.

As with Thatcher’s property-owning democracy, there is a question as to whether New Labour’s actions matched its analysis. True, public spending on education did increase – from 4.1% of GDP in 1997 to 4.9% of GDP in 2007 – helping to achieve improved teacher-to-pupil ratios, and improved student performance in national standardised tests (Smithers, 2007). Whether these efforts were sufficient to shift the United Kingdom’s growth model is another matter. During Blair’s time in office, the gap between mean and median income continued to grow (see Figure 4), suggesting that New Labour’s educational investments did not succeed in reducing wage inequality. Absent broad-based wage-led growth, the conventional account of the Blair years as a period in which demand was fuelled by household borrowing, which ultimately proved unsustainable, is still valid. During this period, borrowing functioned in part as a substitute for rising wages as a source of improved living standards for lower income households, and as a source of demand for the economy as a whole (Bunn and Rostom, 2014; Stockhammer, 2015).

Does this discredit knowledge-driven growth as a growth model? Not necessarily. Arguably, 10 years is too short a time-period over which to assess the adequacy of Labour’s educational investments. Alternatively, perhaps the theory was not at fault, but the implementation: many contemporary critics queried whether the scale of social investment carried out by Blair was sufficient to match his professed ambitions (see, for example, Hutton, 2001). Might New Labour’s intended growth model have been feasible, granted a longer time horizon (and perhaps also a shift in the quantity and quality of educational investment)? Baccaro and Pontusson highlight Sweden as an example of a country that also bucked the downwards trend in the wage share of GDP in the late 1990s, but which displayed a smaller increase in wage inequality than the United Kingdom – arguing that its ‘balanced growth model was made possible by the (growing) importance of knowledge-intensive, high value-added, goods and services in the Swedish export mix’ (Baccaro and Pontusson, 2016: 176–177).

It remains an open question as to whether continued investment over a longer time horizon, or a more ambitious social investment agenda, would have transformed New Labour’s hypothetical growth model from theory into reality. The idea that educational investment will pave the way for broad-based wage-led growth assumes that inequalities in income in the knowledge economy era are primarily attributable to inequalities in education. Although there is an extensive (largely US-focused) literature arguing that technological progress pushes up demand for higher skilled workers, increasing wage inequality (Autor et al., 1998; Goldin and Katz, 2009), this is not the only possible explanation of these income disparities. Wage inequality might also reflect the disempowerment of lower paid workers through de-unionisation (Kristal and Cohen, 2017), the rent-seeking behaviours of the highly paid (Hargreaves, 2018; Piketty et al., 2014) or superstar effects arising from winner-take-most market dynamics (Gabaix et al., 2016). Improving the supply of highly skilled workers does not address these sources of wage inequality.

Even if wage inequality can be traced back to increased demand for highly skilled workers, and even if supply-increasing educational investment were to reduce the wage premium they command, this would not guarantee a shift to broad-based wage-led growth. Such growth requires two elements: not just wage increases broadly distributed among wage earners, but also an increase in the wage share of national income. It is not inconceivable that increasing the supply of skilled labour might weaken the bargaining power of labour relative to capital. The outcome depends upon multiple factors, including how technological change augments and/or substitutes for different skillsets, elasticity of demand for different kinds of labour and the prevalence of rents (European Commission, 2007: 237–272). Figure 3 reminds us that, contrary to the dominant 1990s account of knowledge-driven growth, the rise of the knowledge economy was not accompanied everywhere by increases in the labour share. This should not come as a surprise, given many knowledge-intensive companies derive competitive advantages from capital as opposed to labour, monopolising intangible assets such as intellectual property and user networks, which are not superseded as rapidly as earlier advocates of knowledge-driven growth anticipated. Viewed in comparative context, the recovery of the labour share in the United Kingdom appears anomalous – and, while a more detailed exploration of this divergence lies beyond the scope of this article, the rise of the knowledge economy and a policy agenda predicated upon knowledge-driven growth cannot readily explain this recovery, as these factors were also present in countries that experienced different trends. Despite some excellent recent scholarship on transitions to the knowledge economy (e.g. Durazzi, 2019; Hope and Martelli, 2019), more research is needed into the variables driving such differing results.

In sum, New Labour’s model of knowledge-driven growth remains at the level of hypothesis, not conclusively disproven, but subject (at the very least) to multiple contingencies and caveats. Nevertheless, as with property-owning democracy, this hypothetical growth model had real-world consequences. It served to legitimise the United Kingdom’s actual growth model, justifying the continuation of pro-capital distributive policies by a centre-left government (and quite possibly justifying those policies to that government too). Furthermore, it facilitated the expansion of household debt in more subtle ways. So long as households, banks and government alike were persuaded of the productivity miracle of knowledge-driven growth, expanding household debt could be viewed as relatively unproblematic, secured as it was against the expectation of future wage gains – giving both regulators and lenders a reason to countenance further borrowing.

Conclusion

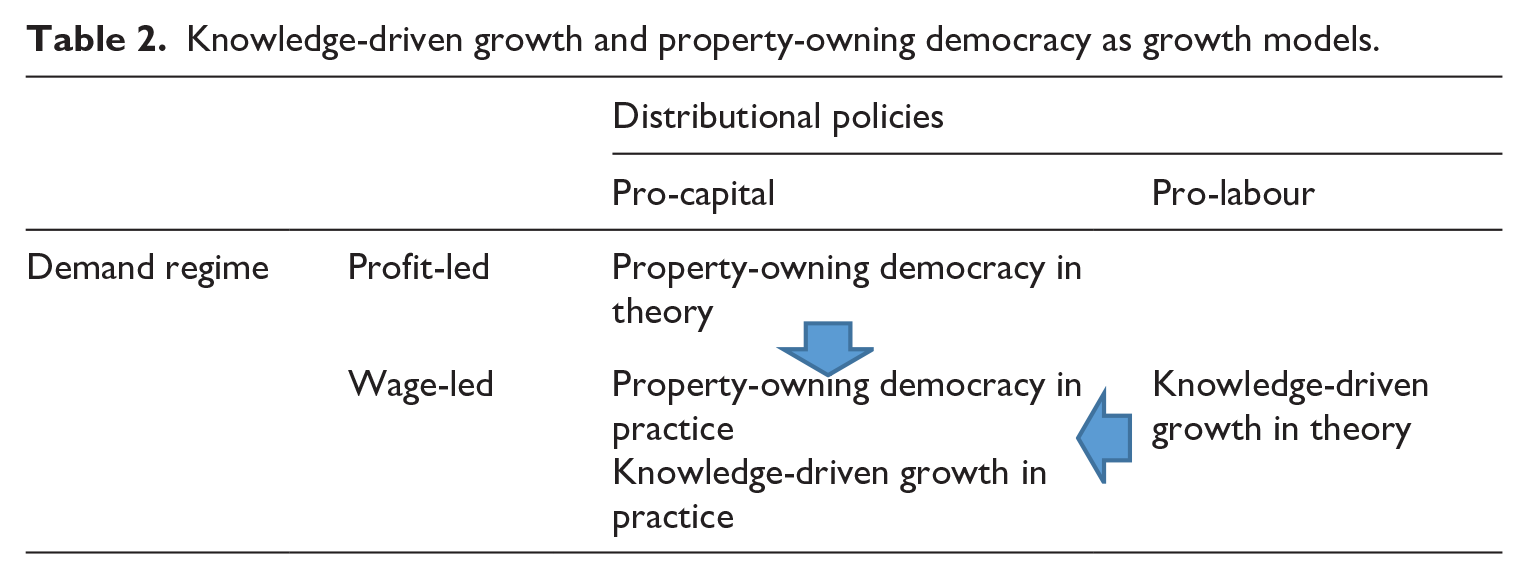

Both Thatcher’s property-owning democracy and Blair’s knowledge economy implied different growth models to the pro-capital distributional policies under wage-led demand conditions that they ultimately produced (see Table 2). These hypothetical growth models posited that the distribution of capital and wage income (respectively) would broaden substantially: had this been achieved, it would have resolved the demand deficiencies associated with ‘neoliberalism in practice’. Thatcher’s property-owning democracy implied that capital income would be widely distributed, placing it at the disposal of households with a higher marginal propensity to consume. Blair’s knowledge economy implied a shift in national income from capital to skilled labour, meaning working households with a higher marginal propensity to consume would receive a larger share of national income, provided the education system endowed them with the skills necessary to seize these opportunities.

Knowledge-driven growth and property-owning democracy as growth models.

In neither case was the hypothesised growth model achieved. Redistribution from the public sector to the private sector under Thatcher broadened the range of households in receipt of capital income (share ownership levels increased from 7% to 20.5% of the adult population between 1979 and 1988), yet this was still far from aligning capital income with wage earners’ marginal propensity to consume. Moreover, when measured by value, individuals’ share in total UK-listed equity declined over the Thatcher years. The emergence of the knowledge economy, at least in its UK form, did coincide with a shift in national income towards labour, but this also coincided with a shift in the distribution of income within labour, towards higher earners with a lower marginal propensity to consume. Educational investment might have mitigated this problem in the long-run, but this was not guaranteed, as Blair’s investment agenda might have proved too modest; skills biased technological change may not have been the root cause of these wage inequalities; and even if it had been, a surfeit of skilled workers might have weakened labour’s bargaining hand vis-à-vis capital. In other words, neither policy agenda produced a shift towards a more stable growth model, whether profit-led (in Thatcher’s case) or wage-led (in Blair’s case), and this dysfunction can be attributed to an insufficiently broad distribution of profits on one hand, and wages on the other hand.

The foregoing analysis has ramifications both for the academic study of growth models, and for the practice of public policy in developed democracies. For scholars of political economy, it highlights how analysing growth models in terms of pro-capital or pro-labour shifts in national income alone can provide a misleading picture. If we fail to recognise the potential for capital to be widely distributed, we fail to appreciate how property-owning democracy might offer a route towards stable broad-based profit-led demand. If we fail to recognise the potential for labour income to be narrowly distributed, we fail to appreciate how wage-led demand might fall short even as the distribution of national income shifts in favour of labour. If we are interested in understanding the patterns and pathologies of aggregate demand, we must consider not just the distribution of national income between labour and capital, but also the distribution of income within labour and capital.

In practical policy terms, these historical episodes point to the possibility of alternatives to the export-led and consumption-led growth models that have dominated recent scholarship (for a complementary critique of this literature, albeit from a different methodological/historical perspective, see Kohler and Stockhammer, 2021). Stable profit-led growth under pro-capital distributive policies is, on Lavoie and Stockhammer’s framework, precluded due to low marginal propensity to consume among wealthier households and/or slow income growth among wage earners, forcing a reliance on either net exports or credit-driven household consumption as a source of demand. Yet, a more egalitarian distribution of wealth, as implied by property-owning democracy, would mean that the returns on capital would be more widely distributed, thereby accruing to households with a higher marginal propensity to consume. Obviously, the fact that these returns are consumed rather than reinvested means that over time, poorer households will see their share of wealth decline relative to wealthier households that save or reinvest those returns. The challenge facing advocates of a property-owning democracy is thus how to create and maintain a democratic distribution of property.

Knowledge-driven growth, too, offers an alternative growth model to the approaches that Lavoie and Stockhammer characterise as ‘actually existing neoliberalism’. In theory at least, the increasing importance of skilled labour to knowledge-intensive production processes could empower skilled workers to negotiate a higher share of the proceeds of growth – even under distributional policies that might conventionally be viewed as pro-capital. In practice, the rise of the knowledge economy has seen the labour share of national income continue to fall in many developed democracies, and many knowledge-intensive business models have proven to be highly capital-intensive. Nevertheless, some varieties of knowledge capitalism may be less capital-intensive than others, or may see increases in capital intensity augment the productivity of (skilled) labour to the overall benefit of the labour share (European Commission, 2007). In the United Kingdom, the labour share did increase in the late 1990s, raising the prospect of broad-based wage-led growth. However, this development also coincided with a rise in wage inequality, skewing the proceeds of growth towards households with a lower marginal propensity to consume. Increasing the supply of suitably-skilled workers might mitigate this wage inequality; but it is also possible that educational expansion may simultaneously weaken the bargaining power of labour vis-à-vis capital, reducing the labour share and undermining prospects for balanced wage-led growth.

While this article has focused on the UK case, these policy lessons are of wider applicability. Over the last 40 years, market-driven and knowledge-driven approaches to growth have dominated the economic policy agenda in diverse developed democracies (Hall, 2015). To the extent that economic policy today remains beholden to some combination of these strategies, actually existing growth models are likely to remain dependent upon credit-fuelled consumption and/or net exports as a substitute for broader-based wage-led demand – unless the distributive issues that give rise to dysfunctional shortfalls in demand are addressed.

Footnotes

Acknowledgements

The author would like to thank Craig Berry and Sean McDaniel, as well as two anonymous reviewers from BJPIR, for invaluable comments and suggestions on earlier iterations of this paper.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.