Abstract

This article assesses the usefulness of the growth models perspective for understanding contemporary British capitalism in the context of its ongoing ‘productivity puzzle’ and stagnating economic growth. The analysis of British capitalism supports our argument that growth models perspective analyses currently have limited capacity to understand the developmental trajectory of growth models, the instabilities and dysfunctionalities of these models, and how growth comes to be distributed differently across models. Through analysis of capital investment patterns and labour market characteristics, it reveals the importance of the ‘politics of productivity’, embedded in state institutions, which shapes the nature and distribution of economic growth. The article outlines a new framework for growth models analysis that ‘brings the supply-side back in’ for a more holistic approach to the political economy of capitalist growth (and non-growth). It argues this is critical for understanding patterns of political economic development in the British model of capitalism and beyond.

Keywords

Introduction

The British model of capitalism is an important case within comparative capitalism debates. The Comparative Political Economy (CPE) literature traditionally understands the British model as a ‘liberal’ or ‘market-led’ economy (see Coates, 2000). British Political Economy scholarship, particularly since 2008, fleshed out the British model’s reliance upon financial capitalism to support economic growth. For several decades, increasing private debt, especially consumer credit fed by house price inflation, propped up the faltering model as real wages and living standards stagnated (see Crouch, 2009; Hay, 2009; Watson, 2010). More recently, CPE scholars developed a new ‘growth models perspective’ (GMP) 1 (see Baccaro and Pontusson, 2016), focused on key demand drivers of growth. This important work has shifted focus away from Varieties of Capitalism’s (VoC) firm-focused, supply-side approach (Hall and Soskice, 2001) which dominated earlier comparative capitalism work. GMP draws upon and dovetails with elements of British Political Economy scholarship to produce a coherent image of the British economy’s ‘growth model’. Britain’s ‘consumption-led’ (as opposed to ‘export-led’) model is fuelled by both real wage growth and high household debt (Baccaro and Pontusson, 2016: 176). This article assesses the utility of this GMP framework for understanding British capitalism’s evolution, using this to shed light on wider CPE debates about ‘growth models’ (GMs).

Empirically, British capitalism presents an interesting dilemma for comparative scholarship and GM analysis, given its ongoing so-called ‘productivity puzzle’ (PP). Britain’s acute lack of productivity growth since the early 2000s is not readily explained by any single factor or thesis. The PP is a broader international phenomenon, yet Britain’s productivity shortfall is twice as severe as other G7 economies (Sidhu, 2018). Some estimates suggest that productivity growth is 19.7% below its pre-2008 trend, a slowdown unprecedented in 250 years (Crafts and Mills, 2020). Enduringly, low productivity since the mid-2000s and sluggish growth since 2008, features apparently baked into the British economy, throw up a paradox. Contemporary CPE scholars increasingly focus on, and delineate, ‘models’ of growth within 21st-century advanced capitalisms, yet these political economies are characterised more by instability, crisis and stagnation than by growth. ‘GM’ analysis has flourished just as capitalist growth itself has largely deserted advanced economies. We utilise the British case, and the PP, to explore the implications of this for comparative capitalism debates and GM analysis.

While GMP scholarship has contributed valuably to our understanding, the British case reveals the need for a more holistic approach to the political economy of capitalist growth (and non-growth). Myopically focusing on national models of growth may distract from important uneven distributional characteristics and regional disparities within capitalisms. Furthermore, GMP’s understandable turn away from VoC’s supply-side insights commits the opposite but equally significant fallacy of prioritising demand drivers of growth at the expense of the supply-side. The GMP overlooks ‘the politics of productivity’, that is, the set of contingent rules, norms and ideas bound up within the state that shape supply-side evolutions of the economy, affecting growth trajectories.

We focus on the influential GMP framework as a key intervention in comparative capitalism debates. GMP, we argue, contains key analytical and assumptive weak points that pose problems for understanding capitalism comparatively, in Britain and beyond. These assumptions circumscribe GMP’s ability to understand the developmental trajectory of GMs, the instabilities and dysfunctionalities of these models, and the dynamics of how growth is distributed differently across models. GMP scholarship not only overstates the coherence of GMs, but it also misses the contingency, haphazardness and path dependencies that shape capitalist development. Taking a longer view reveals how GMs are a diachronic phenomenon, and snapshots offer too fleeting a glimpse of political economies. We apply sectoral and geographical analyses to the British case, examining how capital investment and labour market dynamics affect the PP. The GMP struggles to understand the nature and developmental trajectory of the British political economy, crucially misreading labour market outcomes integral to its wage-led growth model conception. These dynamics, and Britain’s wider ‘politics of productivity’, are key to understanding British capitalism, hence the need to bring the supply-side back centre-stage within CPE.

The article begins by exploring CPE’s macro-turn, before analysing the political economy of the British growth model. A third section establishes our threefold critique of GMP’s limitations, while the fourth section utilises the PP to advance an empirical application of our central argument. A final section underlines our findings’ wider importance for comparative capitalisms and outlines a more holistic approach to GM analysis. This considers both demand and supply-sides, and their interaction, to better understand contemporary capitalism in Britain and beyond.

CPE’s macro-turn

International Political Economy has, in recent years, attempted to bring the macro economy back into focus. In a nod to the French regulation school (see Boyer, 2015), Blyth and Matthijs (2017) draw links between shifts in temporally specific global macro regimes, their consequences, such as rising inequality, and contemporary political dilemmas, including austerity in the Eurozone, Trump and Brexit. In tandem, CPE has undergone a significant, collective about-turn. The chief target of this ‘macro-turn’ is VoC (see Hall and Soskice, 2001), long dominant within CPE. Influenced by New Keynesian economics, and centred on ‘comparative institutional advantage’ rather than growth per se, VoC focused on firms and economic actors pursuing comparative advantage through supply-side arrangements (see Baccaro and Pontusson, 2018: 7–12). VoC makes sense of institutional configurations and inter-relationships, shedding light on how markets operate, labour market characteristics, corporate governance dynamics, welfare, education and training regimes, and distributional outcomes. All these are integral to the ‘politics of productivity’ at the heart of our argument. Significantly, VoC does not presume particular growth patterns or drivers within British or other capitalisms.

Critiques of VoC questioned its underlying rationalist assumptions and its ontological prioritisation of the firm (see, for example, Hay, 2005). Dissatisfied with VoC’s firm-level micro-foundations, macro-oriented CPE set out an influential GMP framework, re-conceptualising comparative capitalisms analysis (see Baccaro and Howell, 2017; Baccaro and Pontusson, 2016; Hall, 2018; Johnston and Regan, 2016; Streeck, 2016). GMP analysis provides important fresh avenues for models of capitalism research – shifting away from analysing supply-side production regimes towards studying the economy’s demand-side.

The GMP focuses on a diversity of forms of ‘demand regimes’ in developed economies, each assumed to deliver growth. Drawing on post-Keynesian (specifically neo-Kaleckian) theory (see Bhaduri and Marglin, 1990; Kohler and Stockhammer, 2021; Stockhammer, 2013), this macro-CPE work distinguishes two different models for generating and sustaining demand: consumption-led and export-led growth. Both emerged after the collapse of the post-war Fordist wage-led model, but they have different distributional implications (see Baccaro and Pontusson, 2016). We consider these in relation to the British case in more detail in the next section.

The British model in the political economy literature

In earlier CPE accounts, the British economy has traditionally been characterised as ‘market-oriented’ or a ‘liberal market economy’ (LME), rather than a ‘coordinated market economy’ (CME) such as Germany (Coates, 2000; Hall and Soskice, 2001). The British economy’s LME characteristics include its highly liberalised markets for labour and finance, competitive market dynamics defining inter-firm and state-firm relations, and the importance of ‘shareholder value’ in corporate governance (see Hall and Soskice, 2001: 8–9, 27–30). VoC sees these supply-side characteristics as the institutional foundations of British comparative advantage. Similar interpretations are also found in institutionally attuned British Political Economy accounts of post-war capitalism (see Coates, 2018; English and Kenny, 2000; Gamble, 1981). British allegiance to circulating/financial rather than manufacturing/industrial capital (see Glyn and Sutcliffe, 1972), alongside a lack of private productive investment, has historical roots in British ‘gentlemanly capitalism’ (Cain and Hopkins, 2002). The ‘aristocratically dominated’ financial sector eschewed ‘close, long-term relations with local manufacturing industry’ and instead pursued short-term profit elsewhere (Coates, 2000: 51). The British state’s historical and institutional path dependencies, including a deep-seated antipathy to public intervention and the public realm, frustrated post-war modernisation (see Gamble, 1981; Hutton, 1995; Marquand, 1988), leaving the British economy weakly organised, relying heavily on limited Keynesian demand-management techniques (Shonfield, 1969).

The New Right under Margret Thatcher reorganised the British economy in the 1980s (see Gamble, 1988; Hall, 1993), eroding trade union rights and power, and reducing welfare generosity. Pursuing strict fiscal conservatism and a partial application of monetarist principles (see Clift, 2020), Thatcher orchestrated significant financial market liberalisation, heralding a new, distinct growth dynamic (see Coates, 2018; Crouch, 2009; Gamble, 2012, 2019; Hay, 2013; Lavery, 2019). Amid the decomposition of the post-war international Keynesian order, there was a structural shift from manufacturing to services. New Right restructuring entailed stagnating wages and rising inequality, contributing to demand shortfalls (Lavery, 2019: 21–25). The key characteristic of Britain’s ‘Anglo-liberal growth model’ (Hay, 2013: 25) from the 1980s up to 2008 was ‘easy access to credit, much of it secured against a rising property market’ that drove ‘largely consumer-led and private-debt-financed’ growth (see Watson, 2010). Britain was unusually heavily dependent upon financial services, constituting nearly 10% of economy. The resultant tax receipts were vital for sustaining public finances. Private debt, especially mortgage debt, compensated for declining wage-led demand and government expenditure. Crouch (2009: 390) memorably labelled this regime ‘privatised Keynesianism’.

There has been no detailed GMP examination of the British case, although key contours are sketched out by Baccaro and Pontusson (2016) for the purposes of comparison. The main driver of British economic growth is reportedly household consumption, achieved through real wage growth and significant increases in household debt (Baccaro and Pontusson, 2016: 176). Germany and Britain are seen as ‘mirror images’. Germany created a low-wage labour market in private services to facilitate its export-oriented growth strategy, dampening domestic demand and keeping production costs low. Meanwhile, the British economy generated ‘labor-market conditions favorable to unskilled (service-sector) workers’ (Baccaro and Pontusson, 2016: 177). British exports are a much smaller proportion of the economy and less sensitive to wage levels, concentrated in high-value financial and business services that do not compete on cost (Baccaro and Pontusson, 2016: 191). This Baccaro and Pontusson (2016: 184) see as confirmed by their counter-intuitive finding that ‘the wage share has held up better in the United Kingdom’ compared to countries with ‘more coordinated systems of wage bargaining’ and ‘less dramatic declines of union membership’.

The GMP captures many key attributes of privatised Keynesianism detailed above. However, the GMP lacks an appreciation of the historical and institutional specificities that have shaped British capitalism. Importantly, it does not capture the linkages between the supply and demand sides, and the dysfunctions contained therein. For example, while this model sustained prosperity for a growing middle class in the 1990s and 2000s, it was premised upon a fragile ‘low interest rate–low inflation equilibrium’, designed to nurture the boom (Hay, 2013: 25–26). Buoyant consumption and a growing labour-intensive service sector masked industrial decline and poor human capital development. Low interest rates reinforced historical patterns of weak productive investment (Hay, 2013: 27). Financialisation of the British economy exacerbated pre-existing sectoral and regional imbalances in wealth, investment and economic dynamism (see Berry and Hay, 2016). Following the crash, this fragile financialised model was shored up through extraordinary ‘monetary indiscipline’ (see Green and Lavery, 2018). Reflecting these dysfunctionalities and fragilities, an arresting feature of Britain’s growth model has been its ongoing productivity crisis.

British capitalism’s PP

Productivity increases are crucial for economic growth, traditionally determining workers’ living standards, yet Britain is experiencing an enduring, perhaps systemic, productivity downturn. The British economy shifted in the mid-2000s from a 20th-century-long historical trend productivity growth path of circa 2.2% per annum, to a much more meagre 0.3%–1%. While this productivity slowdown is an international phenomenon, comparisons suggest Britain’s problem is particularly acute (Sidhu, 2018). This productivity slump has puzzled economists, with Office for Budget Responsibility (OBR) director Robert Chote noting, ‘nobody knows quite why it is happening’ (Chote, 2016). The OBR and others, tied to standard equilibrium economic assumptions, initially anticipated financial sector recovery and post-crash, ‘catch-up’ growth, restoring Britain’s prior path (OBR, 2017b). Increasingly, however, analysts accepted a ‘new normal’ of lower British potential growth (OBR, 2017a). Collapsing productivity explains weak British growth – 1.1% annually since the 2008 crisis, compared with 3.1% in 1949–1979 and 2.5% in 1980–2008 (Office for National Statistics (ONS), 2021). Numerous economic theories seek to explain this ‘puzzle’ (see Haldane, 2017). Pessoa and van Reenan (2014) contend that low wages and flexible labour markets have led to ‘capital shallowing’ during the downturn as workers replace structures and equipment, explaining the paradox of declining unemployment alongside stagnating British productivity (Pessoa and van Reenan, 2014). Other accounts highlight slowing technological innovation and diffusion, and looser monetary conditions, halting the ‘creative destruction’ of firms (see Coates, 2018: 262; Haldane, 2017: 5–6).

British productivity falling off a cliff highlights a problem with GMP’s focus on demand drivers of assumed growth. In neglecting the supply-side, and overlooking the ‘politics of productivity’, GMP struggles to account for how political economies are often characterised more by instability, crisis and stagnation than by growth. While VoC scholarship contains its own flaws and limitations, its framework permits analysis of labour market characteristics, how markets operate, and distributional and other issues that are missing in GMP’s pre-occupation with the demand drivers of growth. The GMP, in assuming a priori the presence of national economic growth, fails to conceptualise fully the developmental trajectory of GMs, the instabilities and dysfunctionalities of these models, and how growth is distributed differently across models. Exploring the British PP in more detail, as we do below, illustrates these points.

The limits of the GM literature

How does the GMP neglect the development and trajectory of GMs? Per post-Keynesian theory, the GMP literature shifted analytical focus from the supply-side to the demand-side (see Baccaro and Pontusson, 2016; Johnston and Regan, 2018; Stockhammer, 2013). While this has generated many valuable insights, the supply-side is problematically absent from these accounts. Tellingly, Baccaro and Pontusson’s influential 2016 paper makes no mention of productivity – seemingly throwing the productivity baby out with the supply-side bathwater. Singular focus on the demand-side leads to a ‘lampposts and lost keys’ problem. Hope and Soskice (2016: 215–216) note, for instance, how ignoring the supply-side means neglecting German reunification, which significantly reshaped German labour market characteristics. More recent GMP scholarship has begun to address the supply-side, although productivity remains marginal (see Baccaro and Benassi, 2017; Baccaro and Pontusson, 2019).

GMP rightly rejects VoC’s ‘efficiency-theoretical and economistic’ underpinnings (Streeck, 2016: 244; see Baccaro and Pontusson, 2016: 178), yet it makes its own questionable assumptions about stability, efficiency and coherence in GMs and their capacity to deliver growth and productivity gains. The GMP, like VoC before it, largely overlooks the state (for critiques, see Clift, 2012, 2021; Crouch, 2005) and its role in shaping how GMs develop (see Hope and Soskice, 2016). In stripping their framework of supply-side ‘institutional equilibria’, Baccaro and Pontusson (2016: 176) underplay core political economy insights into the social and institutional embeddedness of markets, firms and the economy (see Clift, 2021; Coates, 2005: 13). In each case, path dependency tells us that institutional and policy initiatives aimed at refounding a growth model are overlain on dense webs of interrelated institutions that are fundamental to capitalism’s workings (North, 1990; Pierson, 2004). Snapshots of demand regimes do not capture the supply-side dysfunctionalities of British capitalism and its institutional embedding, including its low-skill, low-wage flexible labour market; a welfare settlement with diminished automatic stabilisers that subsidise low pay; and low levels of productive investment. Put differently, by marginalising the supply-side institutional context, GMP analyses lack sufficient appreciation of the ‘politics of productivity’.

Second, how does the GMP literature overlook the inherent instability and dysfunctionality of GMs? Under-appreciation of the politics of institutional creation and reproduction feeds a somewhat problematic tendency towards functionalism. The real-world evolution of GMs is fortuitous, involving contingency and unintended consequences. They were not planned or pre-ordained. GMP scholars overstate the coherence of GMs and understate this haphazardness. Despite the passing acknowledgement that ‘all growth models are fundamentally precarious’ (Baccaro and Pontusson, 2016: 185), there is insufficient recognition of potential instability and dysfunctionality (e.g. flatlining productivity). Caveats notwithstanding, positing a ‘growth model’ assumes a level of stabilising functional coherence – that is, in delivering economic growth. Institutions and policies are seemingly ‘called forth’ by the GM’s functional requirements, assuming perfect information and foresight, and no impediments to establishing the functionally necessary institutional order. Yet, careful historical analysis indicates that capitalist evolution is not determined by pure economic logics or imperatives of efficiency, but by politics, accident and unintended consequence (Coates, 2000; Jackson, 2001).

The iniquitous pathologies of the British economy since the 1980s have sown the seeds of 21st-century problems (see Coates, 2018; Hay, 2013; Lavery, 2019). Acknowledging this means admitting more instability and potential dysfunctionality into understanding GMs and how they change (see, for example, Baccaro and Howell, 2017; Boyer, 2015; Howell, 2019; Kohler and Stockhammer, 2021). While Baccaro and Pontusson (2016: 196–201) do note that, in particular, credit-financed consumption is unstable, as seen in 2007–2008 (Baccaro and Pontusson, 2016: 185–186), their overriding impression is of Britain’s consumption-led growth facilitating higher real wages as compared to export-led GMs, and that wages have been able to grow in line with rising productivity. Neither of these is a safe assumption.

Finally, how does GMP literature neglect how growth is distributed? Analysing the politics of productivity is vital not just because of its effects on comparative institutional advantage (à la VoC), but because it directly shapes patterns of economic growth and distribution (see Behringer and van Treeck, 2019; Hein et al., 2020; Hope and Soskice, 2016: 218–219). Our analysis highlights how demand- and supply-sides interact, with adverse distributional outcomes associated with Britain’s highly fragmented service-sector labour market, marked by a very large financial sector, resulting from successive governments’ policy decisions.

Importantly, GMP analyses too often overlook uneven growth distribution. Like VoC before it, the GMP presumes a nationally coherent and homogeneous economy. This assumes a priori a degree of model coherence and stability. Problematically, this perspective irons over institutional particularities and flattens out granular within-nation political economic differentiation. Thus, like VoC (Blyth, 2003; Crouch, 2005; Hay, 2019), GMP analyses superimpose abstract ideal typical models on real existing economies as if they were an account of their actual properties. Consequently, patterns of uneven development are ignored (although see Regan and Brazys, 2020). Below we demonstrate how within-national differentiation shapes the distributional implications of GMs. The next section explores the British PP, looking first at capital investment and then labour market outcomes.

Britain’s PP and GM analysis

Capital investment and growth: Sectoral analysis

The British PP highlights the need to bring the supply-side and the ‘politics of productivity’ back in. In the GMP, growth dynamics are read back from the different components of aggregate demand (Hope and Soskice, 2016: 210). Yet, exploration of public and private investment in Britain, including investment in Research and Development (R&D), shows how the capital investment landscape systematically embeds the British model’s dysfunctionalities. Returning to the pathologies and ethos of the British state, and the consequences of the New Right’s rise (Thain and Wright, 1995: 2–3), academics and officials alike have noted how, following the 1976 International Monetary Fund (IMF) crisis (Ludlam, 1992), British capital spending and public investment nosedived. This resulted from a changed British public expenditure framework, enacting planning and control via cost–benefit analyses that instilled a bias against capital spending (Balls and O’Donnell, 2002; Thain and Wright, 1995: 4–6). It was politically easier to reduce capital investment, even if that damaged British productivity and growth potential. GMP’s relative silence on the state means that it neglects evolutions in British public infrastructure investment and their productivity impacts.

Yet capital investment, both public and private, across the British economy’s different sectors matters for economic dynamism. British economic and political power has long been highly centralised in London. A strongly London-centric development pattern ‘privileges interest-bearing financial capital at the expense of capital in the production of tradeable commodities’ (Ingham, 1984; MacLeod and Jones, 2018: 121; Thompson, 2014: 37–43), a sedimented preference with roots in British Empire (see Coates, 2018: 84, 212; Overbeek, 1990: chs 3 and 4). Under Thatcher, British economic policy became even more sympathetic to international capital’s preferences (Godley, 1988; Lavery, 2019: 698), exacerbating problems for already-struggling British manufacturing (Crafts, 1991; Tomlinson, 1990). British capital is historically short-termist rather than focused on long-term productive investment (see Coates, 2000, 2005; Hutton, 1995; Lavery, 2019: 21; Marquand, 1988), meaning British industry has not benefitted proportionally from the City’s status as Europe’s largest financial centre (Ingham, 1984).

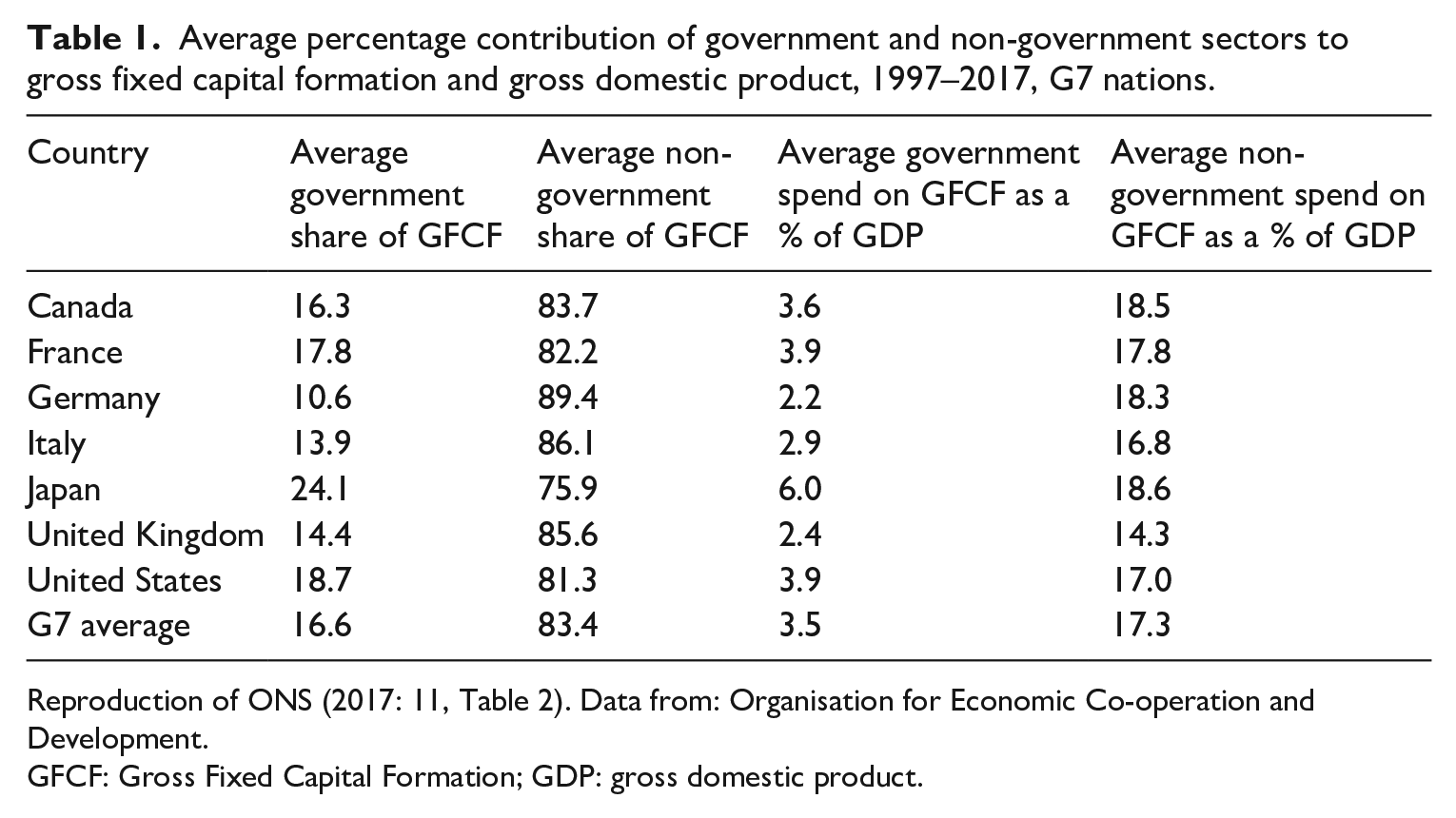

The British state’s built-in antipathy to public investment and lack of strategic support for manufacturing industries were telling then and clearly still shape the investment landscape. Comparative analysis of Gross Fixed Capital Formation (GFCF), which measures expenditure on non-financial assets from both the public and non-government sectors expressed as a percentage of gross domestic product (GDP), reveals this. Over two decades from 1997, British average GFCF levels were the lowest of any Organisation for Economic Co-operation and Development (OECD) nation, with both private and public investment lower than the G7 averages (see ONS, 2017: 2; see Table 1). Similarly, R&D investment in Britain (1.7% of GDP in 2017) – crucial to high-end production – is well below that of Germany (3.0%) and France (2.2%), and lower than EU (2.0%) and OECD (2.4%) averages (Rhodes, 2019: 15). This significant under-investment reflects the historical dynamics outlined above, with clear implications for British jobs, productivity and economic growth.

Average percentage contribution of government and non-government sectors to gross fixed capital formation and gross domestic product, 1997–2017, G7 nations.

Reproduction of ONS (2017: 11, Table 2). Data from: Organisation for Economic Co-operation and Development.

GFCF: Gross Fixed Capital Formation; GDP: gross domestic product.

A lack of industry and manufacturing investment resulted in rapid and sustained de-industrialisation from the 1980s (Gamble, 1990: 204–2011), alongside technological innovation and service-sector expansion especially in finance, banking and producer services. British mines, heavy industry and factories shut due to the deep 1980–1981 recession. Today, production industries including manufacturing comprise just 13% of economic output, compared to nearly 80% for services (Booth, 2021). Financial deregulation in the context of intensifying international competition fuelled this shift (Martin, 1989: 396). Limited state intervention through industrial and regional development policies, however, meant no substantive regeneration in former industrial heartlands. The service industries that emerged to replace some manufacturing failed to develop in hardest-hit de-industrialised regions. Those with low or moderate skills levels had to accept low wages and precarious working conditions (see, for example, Crouch, 2010: 32–33; O’Donovan, 2020: 261).

Repeating historical patterns, government efforts since the 1990s sought to enhance the British workforce’s skills. Under New Labour, higher education was greatly expanded. There was investment in the science base, but the coherence and scale of these efforts remain questionable. Age-old problems of comparatively weak educational outcomes and inadequate vocational and technical skills infrastructures, unearthed during the British decline debates (see English and Kenny, 2000), endured. The British state’s pathologies means its education and training system perennially struggles to equip the workforce with the requisite skills and knowledge (Coates, 2000: 47; Crafts, 1993). Comparatively higher productivity growth in manufacturing than services meant service expansion and manufacturing erosion directly impacted growth (see Haldane, 2017: 10). The British PP is at least partly explained by the economy’s reliance upon low-productivity, low-skilled service-sector employment (Berry, 2014; Berry and Hay, 2016; Lavery, 2019) and government’s unwillingness to pursue more interventionist or directive ‘upskilling’ to assist transition towards high-end exports.

Britain’s laissez-faire approach to industrial restructuring exacerbated the shift towards a largely domestically oriented service-sector economy, resulting in a cavernous gap between a minority of highly productive firms and a majority of productivity ‘laggards’. British exports are mainly high-end financial and business services. By international standards, the British economy has a long, thin upper tail of highly productive ‘frontier’ firms (the 99th percentile of firms) that tend to be export-oriented. These are around a third more productive than domestically oriented firms (Haldane, 2017: 14). New Labour attempted a partial shift from the laissez-faire Thatcherite approach, championing ‘post-neoclassical endogenous growth theory’ as part of its attempt to use public power to forge a ‘knowledge-intensive’ economy (Balls and O’Donnell, 2002; O’Donovan, 2020). However, interventions were more market-conforming than market-shaping, with new public management dictates prevailing within the public sector. The fiscal philosophy of the age meant investment expanded through private finance initiative projects that lacked the developmental state ethos whose absence Marquand (1988) mourned. Despite increased investment in education, ongoing labour market liberalisation designed to facilitate the knowledge economy only exacerbated the divergence between high- and low-productivity firms. Some firms have excelled under increased global competition, deploying better technology and more educated sections of the workforce, but many low-skill, low-pay jobs remain (see O’Donovan, 2020: 261; see also Crouch, 2010; Iversen and Soskice, 2019: 138–142).

Britain’s politics of productivity has resulted not in a homogeneous national growth model, but in uneven, iniquitous development, regional disparities and a disjuncture between the ‘frontier firms’ and productivity laggards (see Berry and Hay, 2016; Haldane, 2017). The sectoral shift towards services (and particularly finance) had clear geographic implications, with severe adverse consequences for Northern England, Scotland and Wales, and a massive concentration of economic prosperity and dynamism in and around London. Investment data reflect this geographical imbalance, with GFCF spend heavily focused on the South. Averaged across 2000–2016, 38% of total investment was allocated to the South of England (London, the SE and SW) alone, while Northern Ireland and Wales received just 3% and 4%, respectively. Moreover, there is a huge regional disparity in R&D funding, with highs of £963 per capita spend in the East of England, £741 in the South East and £629 in London, and lows of £267 and £238 in the North East and Wales, respectively (Rhodes, 2019: 11).

This has significant knock-on productivity effects. London (the most productive region) and the South East of England are the only two regions of the British where productivity is above the British average; productivity in London is 63% higher than in Wales (the least productive region) (ONS, 2018b). The much higher concentration of ‘frontier firms’ in London and the South East undoubtedly contributes to this (Haldane, 2017: 14). Investment patterns reinforce these trends, with Foreign Direct Investment (FDI) biased towards the South East and overall incidence of FDI projects increasing fivefold in Southern England between the mid-1980s and mid-2000s, compared to just 1.4 times in the North (Wren and Jones, 2009: 16, Table 6). This links to geographically disparate attempts to build a knowledge economy, with the geographical distribution of high-skilled knowledge work being ‘extremely uneven’, exacerbating pre-existing patterns of interregional inequality (O’Donovan, 2020: 261). Britain’s economic recovery from the 2008 crisis reflected the consequences of this divergence. By 2016, only in London and the South East had GDP-per-head growth exceeded the pre-crisis peak (Haldane, 2016: 23, Chart 11).

The Coalition Government from 2010 vaunted a ‘rebalancing’ of British capitalism to limit its unusually heavy dependence upon financial services. Reinvigoration of the Midlands and the North promised to forge a ‘Northern powerhouse’ through transport and other infrastructure investments redressing regional inequalities, but delivery was meagre. The North East and parts of the Midlands remained profoundly scarred by de-industrialisation. A lack of regeneration investment or public provision meant parts of the British economy never recovered from the 1980–1981 recession. Instead of rebalancing, post-2008 a laissez-faire approach prevailed, which equated to ‘the revival of the financial growth model’ (Gamble, 2012: 72). Financial sector reforms such as Project Merlin ‘were in fact steered away from attempts at reforming the evident failures in British neoliberal model of finance-led capitalism’ (Grimshaw, 2013: 576). Anaemic growth saw politicians push for a quicker fix – pursuing policies more congruent with the economy’s existing crisis-prone institutional path dependencies. The Bank of England and government introduced policies to restart house price appreciation as the economy’s underpinning source of value (Green and Lavery, 2018; Hay, 2013). Failed ‘rebalancing’ leaves British growth and productivity characterised by disjuncture; a rupture between its highly productive, export-oriented financial service and business service firms, clustered in the economically prosperous South, and a lower skilled, domestically oriented, service-sector economy in the rest of Britain that lags behind.

Labour market outcomes and the distribution of growth

Overlooking the politics of productivity means neglecting critical dynamics of how British economic growth is generated, including sectoral and geographical dysfunctionalities and disparities. Britain’s PP highlights further GMP limitations in appreciating how demand is generated and distributed within economies. Baccaro and Pontusson (2016: 184) note counter-intuitively that ‘the wage share has held up better in the United Kingdom’ compared to countries with more coordinated systems of wage bargaining and stronger unions. Alongside growing household debt, GMP identifies this as important for British consumption-led growth. Yet this resilient labour share characterisation is problematic, blind to the institutional specificities of the British labour market. In particular, it under-appreciates the financial sector’s distorting role. Correcting this misrepresentation highlights how the production regime shapes the demand regime.

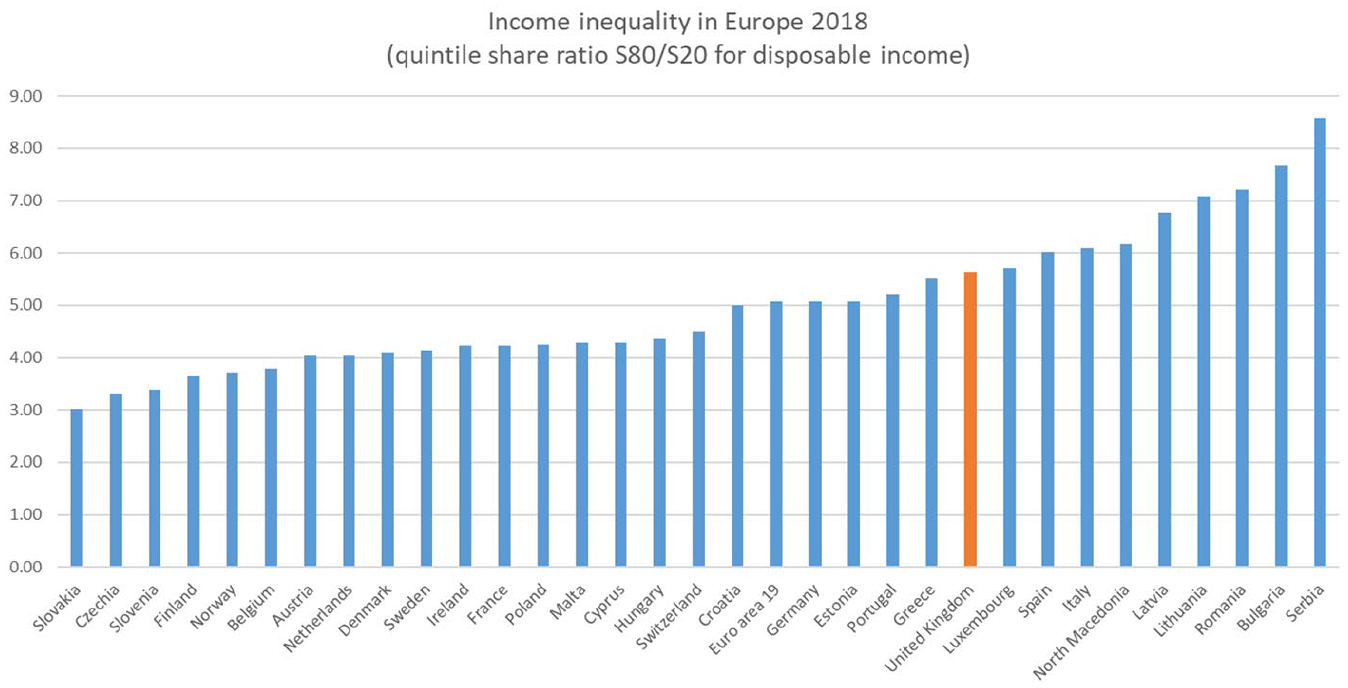

Income inequality data reveal how Britain is more unequal than its major European competitors are. The ratio between disposable income for the top and bottom 20% of earners is higher in Britain (5.63) than in Germany (5.07) or France (4.23) (see Chart 1 below). Measured in terms of the Gini Coefficient, British income inequality stood at a coefficient of 0.351 in 2012, compared to 0.305 in France and 0.289 in Germany, according to OECD data. 2

Income inequality in Europe.

The distinct division between a minority of very high-productivity firms and the majority of other firms produces inequities within the labour market (see Coates, 2018: 98; Iversen and Soskice, 2019). The British labour market has enabled a relatively small number of (mostly) university graduates to access well-paid work in high-wage service-sector work (financial and professional services), in firms that are disproportionately clustered in London and South East England (Haldane, 2017: 32, Chart 22A+B). Financial sector wages are high across the continent, but disproportionately so in Britain. Whereas the average European financial sector ‘wage premium’ is 28%, and c. 35% in Germany and c. 22% in France, the British wage premium is over 45% (Denk, 2015: 16–17). OECD research highlights that financial sector employment raises the British Gini coefficient particularly acutely (adding 0.026), compared with France (0.007) and Germany (0.002) (Denk, 2015: 23). Meanwhile, precarity, low skill levels, low-productivity service-sector work and low wages characterise much of the wider British labour market. At 21.3%, Britain has a larger pool of low-wage earners (those earning two-thirds or less of the national median gross hourly wage) than the EU average (17.2%) (Eurostat, 2016). It has the eighth highest concentration of low-wage earners in Europe, just behind Germany (22.5%) and far ahead of France (8.8%) (Eurostat, 2016). There is, moreover, significant geographical inequality within this. Given the sectoral shifts described above, only London, the South East and the East of England are above the British average for gross disposable household income (GDHI) at the regional level 3 (ONS, 2018a: Table 2). GDHI in the North East, Northern Ireland and Wales is less than 60% of the level in London (ONS, 2018a: see Table 2).

Britain’s politics of productivity has produced deeply uneven patterns of sectoral and geographic growth that directly influence labour market outcomes. This is all missing from GMP’s characterisation, however. The British labour market is far from the ‘mirror image’ of Germany’s low-wage model. The GMP’s conception of British demand regime is limited by its failure to fully account for the financial sector’s distorting effects at the heart of British production regime. For instance, calculation of the ‘labour share’ includes bonus payments, which are disproportionately high in Britain because of its oversized financial sector. As Stockhammer (2015: 6) has noted, the inclusion of ‘sharply rising management remuneration’ as part of the labour share in national accounts distorts the picture, suggesting misleadingly that it has not fallen in the Britain and United States as dramatically as in Europe and Japan. In the pre-crisis period, British annual bonuses peaked at 7.1% of total pay in 2008 (ONS, 2016: 4). These bonuses were heavily concentrated in the financial and insurance sectors, and there is significant intra-country variation in this concentration. For example, OECD data show that bonus-related pay makes up around 22.5% of British finance sector remuneration, but less than 5% in the rest of the economy. By contrast, in France and Germany, bonuses are less inequitably distributed; bonuses are less significant in finance (at around 15%–16% of sector pay) and more significant in the wider economy (at around 8%–9% of pay) (see Denk, 2015: Figures 5, 13).

This has a direct effect on the labour share statistic. As Bell and Van Reenan (2010: 3) note, British income inequality has increased significantly, ‘driven by increasingly large bonus payments made to the better off’. Workers in the top decile of earners have benefited, their share of the total wage bill rising by 5.9 percentage points between 1979 and 2008, from 19.8% to 25.7%. Meanwhile, all other workers have lost out, with losses ‘rather evenly spread across the lower nine deciles of the wage distribution’ (Bell and Van Reenan, 2010: 3, 5). Importantly, ‘almost the entire increase in wage inequality over the last decade is a result of increased bonuses going to workers at the top of the wage distribution’ (Bell and Van Reenan, 2010: 10). Thus, the notion of British labour share ‘holding up’, critical for mooted strong wage-led demand regime underpinning the British growth, is erroneous. Extreme income inequalities resulting from British supply-side orientation, especially the predominance of financial capitalism, maintain an artificially high ‘labour income share’ that distorts the image of Britain’s growth model.

Turning from distribution to the productivity implications of British labour market characteristics, the institutional complementarities that comparative capitalisms scholarship identifies explain how flexible labour markets interact with particular education policies and skills regimes. Parts of the matrix of economic institutions within a political economy fit together, and efficiency gains (or losses) accrue from these felicitous (or unfortunate) interconnections and symbiotic, synergistic inter-relationships (see North, 1990; Pierson, 2004). Within ‘stakeholder’ capitalism, commitments to develop and enhance human capital within the firm dovetail with institutions and regulations that place limits on hiring and firing. Stakeholder labour market institutions make ‘poaching’ of skilled workers difficult, incentivising in-firm training and ‘upskilling’ the workforce. Internal corporate governance structures tend to induce loyalty and empower the workers through representation on the board – prioritising ‘voice’ over ‘exit’ (Hirschman, 1970). Enhancing of human capital in this way benefits the firm, the employees, and the economy as a whole. The societal impact is increasing productivity, facilitating moves towards higher value-added commodity production. An education infrastructure that is supportive of industrial requirements and ‘patient capital’ financing relations with regional or local banks that enable firms to prioritise long-term firm strategy are also features of this model (Hutton, 1995).

All of these institutional characteristics contrast with the British labour market’s low-wage, low-skill proclivities. The British economy has long been more driven by a short-termist shareholder value logic, favouring ever-freer capital and labour markets. More restrictions on hiring and firing are anathema to British policy-makers. They are not deemed a price worth paying for increased scope to build skills and enhance human capital. This arguably restricts the path to higher productivity growth. These drivers help explain the British economy’s specialisation in the low value-added service sector at the expense of higher skills and higher value-added production. A lack of training and ‘upskilling’ is a key characteristic of British capitalism, with government ‘active’ labour market policies strongly geared towards making workers available for any (low-quality) job, rather than investing in human capital. Education and training reforms by successive British governments have not materially improved ‘human capital formation’ (Berry, 2014). Compared to the Nordic states, for example, the British invest much less heavily in service provision and in human capital formation, skills, training and education, including higher education and activation policies (Iversen and Stephens, 2008; Stephens, 2010: Tables 35.1, 35.2), explaining superior Nordic economic performance.

These labour market, education and skills infrastructure characteristics are primary institutional and systemic factors underpinning Britain’s PP. Britain’s flexible low-wage labour market led businesses to invest in labour rather than on capital following the GFC. This process of ‘capital shallowing’ adversely affects productivity by both increasing labour hours and reducing the stock of capital (Pessoa and van Reenan, 2014). As Sarah O’Connor (2015) in the Financial Times notes, ‘Whether you choose to call it a “jobs miracle,” a “productivity disaster” or a “cost of living crisis,” you are describing the same phenomenon: very strong employment gains relative to economic output, with the corollary of dreadful productivity and wage growth’. This supply-side dysfunctionality constrains productivity growth and alter the labour market’s distributional dynamics, and yet goes unaccounted for in the GMP framework.

Bringing the supply-side back in: A path to future GM analysis

The GMP has much to commend it for; the framework advanced by Baccaro and Pontusson (2016) has valuably brought demand-side issues back into mainstream CPE debates around models of growth and comparative capitalisms. In doing so, it has advanced our understanding of the forces driving how economies responded to the crisis of wage-led Fordism in the 1970s. It has corrected some of the pitfalls and oversights apparent within the VoC literature by better appreciating the drivers of economic demand, how states help reproduce these patterns of demand and how economies fit into the global economy. Nevertheless, this article has highlighted some problematic theoretical premises of the GMP. Primarily, these result from its oversight of the supply-side of the economy and thus the politics of productivity. The consequence of this, we suggest, is an impaired capacity to understand the developmental trajectory of GMs, the instabilities and dysfunctionalities of these models, and how growth comes to be distributed differently across models.

There have already been steps taken within the GM literature that help to adjust for some of these limitations. The work of Baccaro and Howell (2017) and Howell (2019), for instance, though operating very much within the GMP framework, permits a much greater appreciation of the instability and dysfunctionality of GMs. This includes pointing out how contemporary GMs are unstable in part due to their lack of ‘a well-functioning institutional mechanism ensuring that aggregate demand grows in tandem with aggregate supply’ (Howell, 2019: 464). Outside of the GMP, Hassel and Palier’s (2021) edited collection provides an important holistic framework for analysing GMs. They contend that ‘we need to combine (and not substitute) an understanding of how the supply-side of the economy adjusts to existing and changing institutions with an analysis of how aggregate demand is driving economic growth’ (Hassel and Palier, 2021: 13). The authors propose an ‘augmented synthesis’ of demand-focused and supply-side-focused accounts in order to ‘provide a more detailed and differentiated account of existing regimes’ (Hassel and Palier, 2021: 17) in much the same way we have argued for here. Indeed, this article has demonstrated the importance and relevance of a more holistic approach for understanding the British model of capitalism and its productivity crisis. To recap, three lines of analysis have emerged.

First, exploring Britain’s PP has underscored the necessity of bringing the supply-side back into GM analyses to understand how historical path dependencies and institutionally mediated regulatory reform processes shape patterns of productivity, economic growth and distribution. Extreme income inequalities resulting from the supply-side orientation of British capitalism, especially the predominance of financial capitalism, distort ‘labour income share’ statistics. This conceals the British labour market’s highly iniquitous outcomes – indicating wages do less to fuel high household demand than GMP’s image of Britain’s growth model recognises. Comparative GM analyses thus need to relax assumptions of internal model coherence and appreciate how certain rules, norms and ideas, historically bound up within state institutions, direct supply-side economic policy in particular directions. This will likely increase model complexity, but it avoids neglecting or assuming away all the rich granularity of evolving capitalist institutions that is the empirical lifeblood of CPE analysis.

Second, CPE scholarship should be wary of relying upon economic efficiency and stability assumptions. The GMP literature often assumes that if GMs demonstrate coherence, growth and productivity gains will follow. This reflects a broader penchant within rationalist political economy for stabilising equilibrium assumptions about the ‘normal’ operations of a growth model (for a critique, see Baccaro and Howell, 2017). These can neglect the negative pathologies of instability and fragility to which capitalist GMs are prone (see, for example, Boyer, 2015; Kohler and Stockhammer, 2021). Britain’s PP reflects not temporally specific failings, but structurally embedded dysfunctionalities in Britain’s model of capitalism. We should heed Hay’s (2016: 527) counsel by focusing on ‘the pathological/disequilibrating interaction between capitalist institutional configurations and particular growth strategies’, as well as ‘the institutionalised rationalities in and through which such cumulatively destabilising practices became habitualised’.

Finally, comparative GM analysis must develop a more nuanced conception of ‘national’ GMs. The GMP literature assumes a within-nation ‘convergence’ dynamic whereby the supposedly efficient and coherent logic of British growth model induces the rest of national economy to emulate London. Unsurprisingly, it has failed to do so. Capitalism, after all, is shaped by public policy (e.g. regional (under)investment, skills and education policies) and is embedded in distinct social contexts, sustained by specific institutional infrastructures. The logical corollary of this is not a monoculture, but a variegated picture both between and within nations (Clift and McDaniel, 2021). Tendencies towards instability and dysfunction causing uneven geographic development crucially explain aspects of Britain’s PP, yet are simply not visible in much GMP literature. GMP’s overriding demand-side focus neglects linkages between the supply- and demand-sides, and fails to grasp how the production regime can shape the demand regime.

Our analysis thus complements recent comparative capitalism work by charting a new path for GM analysis, offering a more contingent, open-ended account of capitalist change, with a central focus on the relationship between the supply and demand components of the economy (Hassel and Palier, 2021). This means deconstructing capitalist forms into constituent elements (Crouch, 2005: 440), potentially throwing up fewer generalisable trends and complicating ideal typical categorisations. However, this new holistic strategy is instrumental to effectively analysing patterns of economic development.

This will be essential for understanding and analysing attempts by policy-makers to shape new models of growth over the next decade. In the British case, the Conservative government has promised renewed post-Brexit economic dynamism and pledged to ‘level up’ the economy. However, the ability of initiatives such as ‘freeports’ and a British ‘ARPA’-style blue skies research agency to renew the economy’s productive tissue remains in question, given the historical and institutional legacies documented here, and the dismal record over many decades of previous governments promising to boost Britain’s long-term growth potential. Indeed, while Brexit represents a significant political economic change, without considerable political determination its enactment is liable to entrench British capitalism’s pre-existing dysfunctions and instabilities. Simultaneously, manufacturing and other productive sectors of the British economy have been hit hard by the COVID-19 pandemic, magnifying existing distributional asymmetries. Beyond the British case, the European Union is responding to pandemic-related supply-chain shocks through attempts to strategically reorient its productive sectors, promoting ‘self-sufficiency’ and ‘economic resilience’. Understanding the politics of productivity is thus more important than ever for making sense of the evolution of contemporary British and European capitalisms.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Ben Clift gratefully acknowledges the support of the Leverhulme Trust Major Research Fellowship (MRF-2017-063) which enabled his research on this article to be undertaken.

{kind=link}