Abstract

Industrial policy rarely features in analysis of post-crisis economic policy change in Britain, despite manufacturing featuring centrally in the ‘rebalancing’ narrative espoused by elites since 2008. The article seeks to interrogate the character of recent governments’ approaches to industrial policy and manufacturing industries. It does so through the prism of Peter Hall’s ‘three orders of policy change’ framework, with particular reference to its application to macroprudential regulation by Andrew Baker. The article argues that the framework must be furnished with additional variables, namely, the type of institutional arrangements related to the policy area, and the status of the associated economic activities within the wider growth model, in order to better understand how ideas, institutions and interests interact in processes of policy change. The article finds little evidence of a ‘paradigm shift’ and suggests that innovations in industrial policy have served to reinforce the foundational assumptions of the British growth model.

Keywords

Introduction

The nature and extent of economic policy change since the financial crisis have been an important concern within British political science in recent years, with analyses often framed by longstanding debates within political economy in particular over the causal role that crises play in the transformation (or otherwise) of policy regimes and their ideological framing (Baker, 2015; Bell and Hindmoor, 2015; Blyth, 2013a; Engelen et al., 2011; Gamble, 2014; Hay, 2013; Hay and Smith, 2013). Industrial policy rarely features in such analysis where the British case is the main or exclusive focus (although see Berry (2015) and Craig (2015) for partial exceptions). Yet industrial policy change has been a recurring feature of political discourse in Britain since 2008, as demonstrated principally by the ‘rebalancing’ narrative espoused largely by Conservative politicians and particularly by then Chancellor of the Exchequer George Osborne’s now infamous rhetoric on ‘the march of the makers’. In general, this discourse extols the importance of rebuilding Britain’s manufacturing sector, therefore suggesting the need for a stronger focus by government on supporting manufacturing industries through industrial policy (Berry and Hay, 2016; Froud et al., 2011). The discourse appears to have been matched by a plethora of policy initiatives emanating principally from the Department for Business, Innovation and Skills (BIS) (led under the 2010–2015 coalition government by the Liberal Democrat cabinet minister Vince Cable) which suggest new directions in British industrial policy in favour of a stronger role for government in relation to the market, and the value of a sectoral as well as horizontal approach to industrial policy. Although the Conservative Party’s interest in industrial policy arguably waned after the 2015 election, if not before, Theresa May appeared to make industrial policy one of her key priorities in her first speech after replacing David Cameron as Prime Minister following the European Union (EU) referendum.

As such, we are confronted with a case whereby British policy-makers are claiming that industrial policy is changing or will change in response to economic crisis, yet scholarly interest in this possibility has been muted. This article is an attempt to fill this lacuna. Industrial policy is often defined with reference to the distinction between ‘horizontal’ approaches (improving the general business environment across the whole economy) and ‘vertical’ approaches (supporting a single set of industries). The distinction has in fact been a significant feature of policy-making discourse in Britain, especially recently, but it should be pointed out that this article assumes the latter is more appropriate in terms of defining industrial policy. Industrial policy essentially involves deliberately favouring particular industries over others, irrespective of market signals. This will involve favouring and indeed empowering some private economic actors over others, but also represents a means by which the behaviour of these actors is kept in check, as they are incentivised to pursue public goods. The public good at the heart of industrial policy is essentially productivity. It is for this reason that supporting manufacturing industries is at the core of most meaningful industrial policy definitions because, irrespective of how well this is captured by statistical typologies, as the term theoretically encompasses all instances of technology being applied to natural resources, the sector is the progenitor of productivity growth within capitalist systems (Chang, 2014: 256–267). Of course, other forms of state regulation may resemble industrial policy in some ways (especially, as explored below, in relation to shaping market forces), but generally speaking, it is the long-term and risky nature of the investment required to upgrade manufacturing processes that generates the ‘market failure’ which industrial policy seeks to remedy.

The article surveys post-crisis industrial policy in Britain through the prism of Peter Hall’s (1993) institutionalist ‘three orders of policy change’ framework—used to explicate the shift from Keynesianism to monetarism in British macroeconomic policy in the late 1970s and early 1980s—but particularly as applied by Andrew Baker (2015) to post-crisis change within financial regulation in Britain. First-order change refers to the revision of numerical or quantitative terms associated with existing policy instruments, and second-order change denotes the replacement of these instruments with alternative policy levers. Third-order change is largely synonymous with a Kuhnian ‘paradigm shift’ and relates both to the ideas and assumptions that underpin key policy priorities and the ordering of priorities within economic statecraft. The three orders of change may occur concurrently rather than consecutively; Hall’s argument is that processes of first- and second-order change, involving policy learning and entrepreneurship, are necessary before third-order change can be complete. Baker, however, introduces a new variable into the framework, based on the notion that there are ‘varieties of economic crisis’. Simply, while Hall documented policy change during and after the ‘slow burn’ crisis of Keynesianism, involving sluggish growth and obstinate inflation, in the 1970s, Baker is documenting policy change following the ‘explosive’ financial crisis of 2008. As such, he sought to demonstrate that the third-order paradigm shift in financial regulation occurred relatively quickly after the crisis, as elites appeared to agree on the need for macroprudential regulation, but that the first- and second-order implementation of the related policy instruments has been much more difficult due to contestation by key stakeholders.

The focus here on industrial policy allows further reflection upon the difference that the density and status of the institutional arrangements make to the character of policy change and how it is discussed publicly by elites. It is certainly the case that elites have pronounced significant industrial policy change in the post-crisis period—yet the practical significance of the new programmes actually implemented is less clear. The article’s objective is to understand what industrial policy change tells us about post-crisis economic statecraft in Britain and what we can learn from this case about the process of post-crisis economic policy change in general. It is recognised, however, that unlike macroeconomic policy and financial regulation, the institutional framework within Britain around industrial policy cannot be taken for granted. The analysis here is essentially developed through an institutionalist lens since policy is ultimately a function of institutions but recognises both variations in institutional forms and the political-economic contexts within which policy-making institutions operate. One of the key, specific concerns here is the role of a particular set of policy-making and delivery bodies within a wider institutional framework of economic statecraft. This necessitates a focus on both the material context which shape hierarchies among institutions and the ideational meanings replete in seemingly technocratic inter-institutional dialogue.

These lead to the article’s most important claims, that is, that in assessing post-crisis economic policy change, we need to assess not only the type of crisis that has seemingly occurred but also the place of the economic activities (and the surrounding policy framework) said to have experienced crisis within the wider model of economic growth. Hall and Baker could take for granted not only that an identifiable institutional framework in the policy area being studied existed but also that the economic activities to which it pertained related to core features of the British economy. The fact that this is not the case in relation to manufacturing and industrial policy not only helps us to understand the nature of the change that has occurred, it may also paradoxically explain why elites were able to adopt such a radical pro-manufacturing discourse in the wake of the 2008 crisis: they were able to speak freely, and perhaps somewhat duplicitously, because the possibility of paradigm change within British industrial policy was so distant, even inconceivable. The discourse on industrial policy may have seemed to invoke radical ideas, but its meaning was ultimately conservative insofar as it upheld and perhaps even reinforced the dominant assumptions of sound economic management more generally. The article first explores the Hall/Baker analytical framework, in the context of other developments in institutionalist scholarship and political economy in general, before examining in depth the development of British industrial policy (and associated discourses) since 2008, with reference to the historical context of manufacturing decline.

Policy change, institutions and growth models

Peter Hall’s 1993 paper ‘Policy paradigms, social learning, and the state’ has proven to be a landmark publication in the development of institutionalist thought. Hall developed the notion that policy-making processes are sites of learning, experimentation and entrepreneurship, and inverted conventional wisdom on how paradigm shifts in post-crisis policy transformation may occur, in that such phenomena are shown to precede paradigmatic change as the perception that a crisis is evident takes root among elites. The emergence of alternative intellectual frameworks in response to perceived crises is of course part of the context within which policy learning, experimentation and entrepreneurship occur, but third-order change is only secure once piecemeal and technocratic reforms gain wider political support, leading to the political elite in general reordering the hierarchy of economic policy goals.

Of course, Hall’s conclusions were based on a single case study, that is, British macroeconomic policy in the late 1970s and early 1980s, as Keynesian instruments were replaced by monetarist instruments. In examining financial regulation following the 2008 crisis, Andrew Baker (2015) introduces a variable not substantively considered by Hall, that is, the variety of crisis to which elites are seeking to respond. The crisis of Keynesianism was ‘very much a slow burning long term economic crisis of stagnation’ typified by a persistent lack of growth and rising inflation (Baker, 2015: 348–349), but the 2008 crisis, especially in relation to the finance sector (hence its normal designation as a financial crisis), was ‘explosive’, ‘dramatic’ and ‘extreme’ and related not to a persistently under-performing economy, but rather an exigent ‘malfunction’ in the financial system (Baker, 2015: 348, 353–354). Falling liquidity and asset prices, and severe credit tightening, created both an empirical demonstration of the falsity of the efficient markets paradigm that had hitherto underpinned financial regulation and an urgent need for an alternative approach to regulation to be enacted.

What quickly emerged was a near-universal endorsement of macroprudential regulation, principally in the form of capital requirements on financial institutions, among economic policy-makers in Britain (and replicated elsewhere). As such, ‘the sequencing at work in the case of the macroprudential ideational shift was exactly the reverse of that evident in the case of the UK macroeconomic policy in the 1970s’ (Baker, 2015: 354–355). However, while third-order change came easily, subsequent first- and second-order change has been slower, with significant debate over the precise details of the new restrictions on financial institutions. As Baker explained in greater depth in an earlier article, the application of new forms of financial regulation has become contested, thereby risking the dilution of the policy content (Baker, 2013; see also Baker and Widmaier, 2014). Yet as Baker’s earlier analysis and direct engagement with Hall demonstrates, while the process of policy change may be explicable due to the variety of crisis, macroprudential regulation is also a very different type of policy change than Hall’s monetarist shift, in terms of both policy form and content. Indeed, macroprudential regulation actually resembles industrial policy as understood here, insofar as it is focused on shaping a particular industry, both empowering the finance sector (by mitigating its volatility) and curbing the excesses, in the name of public good, that a largely market-based structure appears to permit. Ostensibly, macroeconomic policy has no such objectives and focuses rather on the environment within which all industries operate. Although it is clearly not the case that monetarism faced no opposition, this perhaps helps to explain how its implementation faced a less organised (and perhaps less politically astute) form of resistance.

Baker’s engagement with Hall’s approach, two decades on, is clearly cognisant of subsequent developments within institutionalist theory, including within Hall’s own work. The ‘varieties of capitalism’ framework, developed by Hall and David Soskice (2001), have rightly been criticised for appearing to endorse a form of rational choice institutionalism, with different capitalist varieties each producing policies consistent with the form of equilibrium dictated by their institutional configuration (Clift, 2012; Hay, 2005). But it is, at root, an attempt to demonstrate the role of material context in shaping processes of policy learning within institutions and has subsequently been applied as such (see also Streeck, 2011). Mark Blyth (2013b), one of the leading advocates of constructivist or discursive institutionalism, argues that the ‘three orders’ framework hinges around a tension between Hall’s rational choice proclivity and a constructivist account of policy innovation which emphasises the ontological significance of the ideational realm. For Blyth, the aftermath of the 2008 crisis means the constructivist dimension of Hall’s work has been vindicated, precisely because of the absence of paradigmatic change in relation to macroeconomic policy. First- and second-order change in the immediate wake of the crisis did not coalesce with third-order change because the third order, for Blyth, is to some extent autonomous. Ideas gain weight within institutionalised processes, but cannot be reduced to them.

The key contention of constructivist or discursive institutionalism is that inter-subjective ideas about economic context are as important as (or constitutive of) the materiality of economic life in terms of shaping economic policy (Blyth, 2002; Hay, 2006; Schmidt, 2010). The perspective does not simply rest on the assumption that ‘ideas matter’ within institutionalised environments. The aim is not simply to bring ideas back in, but rather to use ideational analysis to demonstrate the connections between institutional practice (and change) and wider political and economic contexts, insofar as these are reflected in the conduct of situated, reflexive agents (cf. Bell, 2011). (Indeed, constructivist institutionalism is not immune to the charge that it remains wedded to a materialist ontology in explaining how new ideas are ultimately generated (Berry, 2011: 26–31, 43–48).) In this way, the operation of institutions is shaped by their (re)production within a particular socio-economic context and also by the agents of (re)production, who will have (both conflicting and complementary) ideas about this context, and the nature and purpose of the institutions they are situated within.

Clearly, unless institutionalists are able to bring the wider material and ideational environment into analysis of policy-making institutions, they will struggle to account for how new policy ideas are generated. Baker (2015: 354) is able to side-step this problem by focusing on a dense set of institutional practices within which the idea of macroprudential regulation had ‘a prior intellectual presence’ domestically and internationally. This gives Baker licence not to inquire into the genesis of the set of ideas in question and therefore raises doubts about the applicability of his approach to areas of policy where the same conditions might not pertain. The existence (or otherwise) of a prior intellectual presence for a more activist approach to industrial policy is probably inconsequential given the subservience and vulnerability of industrial policy-making bodies within the wider economic policy arena. However, even in the case of macroprudential regulation, it appears that relevant ideational factors are being overlooked, insofar as Baker neatly distinguishes between disruption in the ‘foundational assumptions’ of financial regulation since 2008 and continuity in those pertaining to macroeconomic policy. Yet it is surely the case that the disruptive ideas in the former case remain largely consistent with the ideas that continue to underpin the latter (Geoffrey Underhill (2015: 463–464) makes this point in relation to macroprudential regulation among international institutions). This should not surprise us given that, at the highest elite level, there is a significant overlap across the groups of policy-makers that determine both macroeconomic policy and financial regulation. As explored below, we can say the same about industrial policy, even if the same dynamic produces different results. The institutionalised overlaps between different policy-making institutions must be part of any institutionalist account of policy change.

As such, although this applies to every policy area to some extent, it is clearly the case that, especially in Britain, industrial policy outcomes do not simply consist of the policy choices that industrial policy institutions produce. There are clearly fewer formal institutions dedicated to industrial policy, and those that do exist do not enjoy a commensurate degree of autonomy from more powerful bodies and established practice. The ‘growth model’ analytical framework developed by Colin Hay (2013) with reference primarily to the British case, but with antecedents in the more comparative varieties of capitalism and regime theory literatures, offers a useful device for recognising the interaction between institutions, ideas and economic practice. A growth model is understood here as the coalescence of the main sources of growth within the economy (especially insofar as they are distinguishable from other economies), the orientation of political and economic institutions configured to enable the associated economic activities (and reconfigure these activities when necessary), the ideas about economic life (and how it should be governed) that sustain the established order and the distribution of wealth and power that both results from and helps to reproduce the status quo.

The seemingly limited importance of manufacturing to the British economy compared with similar economies obviously helps to explain the limited attention post-crisis industrial policy has received among political scientists and political economists, yet acknowledging this status is also crucial to understanding how industrial policy has developed in recent years. It was noted earlier that there were ostensible similarities between macroprudential regulation and industrial policy, suggesting that Baker’s work demonstrates that the focus of the latter on one particular sector enabled an organised, yet subtle, form of resistance. Of course, the industries impacted by the two policy areas differ substantially in terms of their centrality to the British economy (or at least its distinguishing features). It is perhaps not the existence of organised resistance to industrial policy change which matters most, but rather the absence of any organised advocacy.

Industrial policy in post-crisis Britain

The implication for the current inquiry is that post-crisis industrial policy change matters, but it should not be approached as equivalent to macroeconomic policy or financial regulatory change. Hall and Baker were able to take for granted that the policy area being studied was of paramount importance to the growth model (in Hall’s case, of any capitalist economy, and in Baker’s case, certainly the British economy) and that there existed a dedicated and relatively dense set of institutions and institutionalised practices to study for signs of transformation. Analytically, manufacturing and industrial policy have a lower status within the British growth model. Whether occurring before, after or alongside third-order change, there is less scope for first- and second-order policy changes within actual policy mechanisms, since the required institutional arrangements are under-developed. After briefly discussing the relevant historical context in terms of manufacturing decline and industrial policy traditions in Britain, this section details policy and discursive changes relating to manufacturing and industrial policy, drawing upon official policy documents, public remarks by policy-makers and, to a lesser extent, material related to the perspectives of non-governmental elite actors.

Historical context

Although ‘declinist’ accounts of British economic history remain controversial, there is little doubt that, defined in conventional terms, the British manufacturing sector has been in decline for a very long period of time, arguably since the late 19th century. Manufacturing output and employment have fallen significantly as a proportion of overall output and employment in the British economy, and British manufacturing has fallen significantly as a proportion of global manufacturing on the same measures. Furthermore, the faster pace of manufacturing decline in the postwar era is not simply a function of the recent and fairly rapid economic development of East Asian countries; Britain has also been losing higher skilled manufacturing jobs to Organisation for Economic Co-operation and Development (OECD) countries in recent decades and has shown few signs of developing high-tech or advanced manufacturing economies on any significant scale (English and Kenny, 2000; House of Commons Library, 2015; Matthews, 2007; Pilat et al., 2006; Williams et al., 1983). Decline has continued since the 2008 crisis. The manufacturing sector suffered disproportionately during the recession; even before the very recent turmoil associated with Brexit, output was more than 6% below its pre-crisis ‘peak’ in 2007, and manufacturing had shrunk in relative terms to comprise an even smaller portion of the British economy. A total of 300,000 manufacturing jobs have been lost over this period—yet this actually represents a slower rate of job losses than has been evident from the 1980s onwards, and particularly the immediate pre-crisis years. 1

While political discourse around manufacturing since 2008 (or more precisely 2010) suggests that policy-makers are responding to an exigent crisis in the sector, it would clearly be inaccurate to describe British manufacturing as having experienced an ‘explosive’ crisis in 2008, despite the impact of the subsequent recession; there was no malfunction, but rather, arguably, an exacerbation of extant trends. Overall, the events of 2008 do not represent a significant moment of upheaval for British manufacturing. Does this mean that manufacturing has experienced a ‘slow burn’ crisis? Perhaps, but the decline of manufacturing has been treated by policy elites not as a problem to be solved, but rather a habitual condition or a fact to be accommodated—or indeed celebrated, insofar as it might be considered the flipside of other, more welcome economic trends. If manufacturing ever was central to the British growth model, it became significantly less so by the late 20th century. This was both demonstrated and reinforced by the failure to firmly establish industrial policy mechanisms in the late 19th and early 20th century as Germany, Japan and the United States ‘caught up’ to the manufacturing capacity developed in Britain following the industrial revolution. This view relies of course upon the definition of industrial policy (and its relationship with manufacturing) advanced in the ‘Introduction’ section. British policy-makers would generally claim that Britain has long upheld a functional industrial policy regime, albeit one that operates ‘horizontally’ to improve the general business environment across the whole economy, rather than ‘vertically’ to support a single set of industries.

As such, direct support for manufacturers has generally taken the form of ‘soft’ interventions such as advice services and the dissemination of best practice and tax allowances for R&D or capital investment (Buigues and Sekkat, 2009). British industrial policy has often essentially taken the form of regional policy—an orientation that intensified in the 1990s and especially after the election of Tony Blair’s Labour government in 1997. However, while through regional policy mechanisms parts of the state appeared to take on a more interventionist pose, this was often limited, again, to defensive moves, in support of regions undergoing hardship associated with deindustrialisation. Interventions have often took the form of offering investment incentives to foreign corporations. Most often, the regional layer simply replicated the horizontal approach of national government, and indeed probably reinforced it, by encouraging all regions to pursue similar economic objectives, often in competition with each other and paradoxically with little sense that strategies were genuinely ‘place-based’ (Bailey et al., 2015; Bailey and Driffield, 2007). It should be noted that in the 1970s, Harold Wilson’s Labour government introduced a more interventionist approach, involving direct subsidies and planning agreements, although the agenda became largely focused on defensive interventions to rescue unproductive firms and industries (Coates, 2015). While short-lived, this episode is interesting for illuminating a point made in the previous section, that is, that policy change in relation to manufacturing may be propelled not simply by a perception of crisis in British manufacturing, but rather difficulties in the economy more generally requiring a renewed focus on the manufacturing sector—yet this may in fact help to explain its ephemerality. In contrast, we can speculate that policy change associated with macroprudential regulation arises from the perception of crisis which pertains to the finance sector alone, rather than the economy more widely. These perceptions may differ precisely because manufacturing and finance occupy different places within the British growth model, but the constraining effect on policy innovation is nevertheless quite similar.

Post-crisis industrial policy and discursive change

Industrial policy became more prominent within British economic policy before the establishment of the coalition government in 2010. Gordon Brown created BIS in 2008, to coincide with the return to front-line politics of Peter Mandelson, as both Business Secretary and First Secretary of State (the de facto Deputy Prime Minister). BIS was of course largely a reinvention of the Department of Trade and Industry (DTI), which Brown had split a year earlier into the Department for Business, Enterprise and Regulatory Reform (BERR) and the Department for Innovation, Universities and Skills (DIUS), although it retained oversight of higher education, which had not been part of DTI. The new department published the flagship statement of Labour’s post-crisis industrial policy—the green paper New Industry, New Jobs—in April 2009 (HM Government, 2009). New Industry, New Jobs explained that the two key flaws of British industry were low R&D spending and a lack of success in translating scientific expertise into commercial products. Many of the policies that the coalition would go on to champion as their own were developed during this period, including greater venture capital investment through the Technology Strategy Board (which was established in 2007), more investment in skills, initiatives to improve access to finance for some small and medium-sized enterprises (SMEs) and efforts to introduce a more strategic approach to government procurement (with, again, a focus on SMEs).

Interestingly, manufacturing featured relatively little in New Industry, New Jobs, although the paper did coincide with the announcement of some new funding for advanced manufacturing research centres. It is also worth noting that BERR and DIUS had in September 2008 jointly announced a new ‘manufacturing strategy’, although the accompanying document focused on celebrating what Labour had already done in government rather than advocating a new approach (BERR and DIUS, 2008). New Industry, New Jobs endorsed a more ‘strategic’ approach for government in supporting the British economy’s ‘competitive strengths’ and indeed alluded to industrial policy’s institutional subservience by explaining that ‘[t]his means making Britain’s economic and industrial strength the remit of not just the Department for Business, but of all Government departments’ (HM Government, 2009: 5; emphasis original). However, the paper also repeatedly stressed that the Brown government rejected a mythical ‘Old Labour’ view of the state, outlining ‘important limits’ to state intervention based on a ‘pragmatic but not dismissive [view] about the way markets work’. ‘The last thing the Government wants to do’, BIS explained, ‘is revive old theories or to invent a new ideology in managing the economy’ (HM Government, 2009: 21, 33–34).

Since 2010, the notion of ‘rebalancing’ has become one of the defining motifs of the coalition and Conservative governments, with an apparent imbalance between manufacturing and the finance sector, one of the core features of the rebalancing narrative. In his 2011 budget speech, then Chancellor of the Exchequer, George Osborne, argued that ‘manufacturing is crucial to the rebalancing of our economy’; the finale of his speech added oratorical flair to this statement and indeed has quickly entered British political folklore: We want the words ‘made in Britain’, ‘created in Britain’, ‘designed in Britain’, ‘invented in Britain’ to drive our nation forward. A Britain carried aloft by the march of the makers. That is how we will create jobs and support families. We have put fuel into the tank of the British economy. And I commend this Budget to the House. (Osborne, 2011)

The budget also marked the publication of the coalition’s ‘plan for growth’. The document’s foreword—co-signed by Osborne and Business Secretary Vince Cable, a Liberal Democrat minister—offers a quite remarkable critique of Britain’s pre-crisis growth model, based as it was on ‘rising levels of debt, over-leveraged banks and an unsustainable property boom’. The foreword also bemoans a severe decline in manufacturing output and employment and points longingly towards the success of Germany in developing a high-tech manufacturing base and maintaining its share of world exports (HM Treasury and BIS, 2011: 3–4). Critical scrutiny of the ideological connotations of the rebalancing concept suggests that it offers a rather conservative narrative of post-crisis economic policy change (Berry and Hay, 2016; Froud et al., 2011), undermining the notion that wholesale change in British economic statecraft is being pursued. But this does not preclude a priori the possibility of meaningful industrial policy change.

There are elements of both horizontal and sectoral policies in coalition industrial policy. Access to finance has been an important objective, although this agenda has focused horizontally on supporting SMEs, rather than manufacturers in particular. It has included loan guarantees that could amount to around £2 billion, in addition to the Bank of England’s Funding for Lending scheme, although this scheme was initially used predominantly to support mortgage lending. The British Business Bank enabled a more direct form of lending to SMEs, albeit with funds of only around £1.5 billion. Other horizontal measures include additional efforts to focus government procurement on SMEs, some additional funding for apprentices and the creation of enterprise zones offering tax and planning concessions (and superfast broadband) for companies relocating to these areas. It is certainly the case, however, that the coalition government was comfortable in its public discourse with endorsing also a sectoral approach to manufacturing, with the emphasis in its 2012 industrial strategy on 11 key sectors as the focus of government action. Many of the sectors constitute or encompass manufacturing industries or industries which might feed directly into manufacturing (aerospace, automotives, life sciences, nuclear, offshore wind) but also include many less directly relevant to industrial production (agricultural technologies, construction, information economy, international education, oil and gas, professional and business services) (HM Government, 2014). Supporting advanced manufacturing, in general, was singled out in The Plan for Growth as an important industrial policy priority. This is borne out by some of the sectoral strategies, but also in the creation of the Advanced Manufacturing Supply Chain Initiative (at a cost of around £240 million) and, more specifically, catapult centres—most of which have some connection to high-tech manufacturing industries—where firms and universities can collaborate on R&D and access common, publicly funded resources (the centres are expect to attract private funding in the medium-term). The coalition also consistently expanded tax allowances related to capital investment, which primarily benefit manufacturers.

Clearly, however, the notion that there has been a significant shift of resources—or an allocation of new resources—to vertical industrial policy would be an over-statement. Assessing the plan as a whole, it is clear that manufacturing and industrial policy played a relatively restricted role within the coalition’s growth plan. In The Plan for Growth, arguments that might support a more interventionist industrial policy run alongside support for fiscal conservatism, lower taxes and deregulation, and flexible labour markets (albeit with a higher skilled workforce). Increasing investment and exports is stated as one of four main ambitions, yet attracting foreign direct investment (FDI) is listed as the main specific goal in this regard—the prospect of nurturing domestic investment is not explicitly referenced. Crucially, it is not simply the Treasury’s leadership of the growth plan that accounts for the restricted place of vertical industrial policy. In ‘sector analysis’ published by BIS in 2012, the department stressed that ‘[h]orizontal policies, such as setting the legal and regulatory frameworks in which businesses across the economy operate, form the bedrock of industrial strategy’, but added, ‘[w]ithin this framework, it is crucial to take into account sector-specific effects’ (BIS, 2012: 7). The coalition’s rhetorical focus on sectors is justified by officials almost entirely in terms of the government’s support for the overall business environment. They did, however, concede that some sectors have a higher risk of innovation failure than others—therefore circumscribing quite carefully the grounds upon which government may intervene in particular sectors to correct market failures.

There was clearly an appetite, however, among BIS ministers to have gone much further. In a 2011 speech, Vince Cable (2011), while maintaining that ‘picking winners’ is illusory, argued that government has a ‘legitimate and necessary’ role in supporting manufacturing innovation: One of the first decisions I took was to put manufacturing at the centre of our long term economic vision … Manufacturing contributes disproportionately to overall levels of productivity as well as generating half the UK’s exports of goods; and is responsible for much of the business R&D in this country and the innovation which drives growth. So providing the right framework of incentives and support will have a material effect on future rates of growth. (Vince Cable, 2011)

Crucially, he argues that R&D in some high-tech manufacturing industries is not only ‘risky’ (an argument which correlates with the overall coalition position) but also ‘simply too complex or resource-intensive for an individual company to make the necessary investment’. Cable offers therefore a more strident critique of private sector efficiency than most of his coalition partners. In an open letter to David Cameron and Deputy Prime Minister Nick Clegg (Cable’s party leader) in 2012, seemingly an attempt to bypass the Treasury and George Osborne (and perhaps even his own department), he argued that there is still something important missing [in the government’s industrial strategy]—a compelling vision of where country is heading beyond sorting out the fiscal mess; and a clear and confident message about how we will earn our living in the future … Market forces are insufficient for creating the long term industrial capacities we need. (Cable, 2012)

He continued that ‘our actions, frankly, are rather piecemeal’.

He appears to have enjoyed the support of Conservative science minister David Willets, who argued in favour of a sectoral approach to industrial policy in a 2012 speech, surmising that ‘[g]overnments find themselves making decisions about allocation of resources and we should not pretend that we do not. The coalition’s pledges on rebalancing the economy depend on such a view’. The Cable view was also largely endorsed by former Conservative minister Michael Heseltine, whose 2012 review for the coalition government No Stone Unturned review is often credited with propelling the Conservative Party’s newfound interest in devolution (as discussed in the next sub-section). However, Heseltine also advocated emphatically the notion that the state, at both national and local levels, must support strategically important industries, such as those related to advanced manufacturing, and commit substantial resources to this task.

This is not to suggest that Cable et al. offered a genuinely radical vision for a paradigmatic shift in industrial policy—they broadly advocated a more clinical focus on (advanced) manufacturing and supported higher spending on industrial policy, but stopped short of arguing against other post-crisis economic policy objectives (such as deficit reduction) or questioning the wider institutional framework within which industrial policy mechanisms were situated. Justin Bentham et al. (2013: 2) refer to it as ‘a non-disruptive form of policy innovation’. Nevertheless, even this mild critique appears to have struggled to gain support not only within government but among elites more generally. Senior BBC economics journalist Evan Davis’ (2012: 84) book Made in Britain—published to accompany a documentary series of the same name—argued that manufacturing decline ‘is a sign of success, not failure’. He argued that rebalancing was required following the financial crisis, but only ‘to make some adjustments to our course rather than reverse the direction we have taken’ (Davis, 2012: 7).

Management consultancy McKinsey made similar arguments in an influential 2010 report titled ‘How to compete and grow’. They argue that while governments should adopt economic policies ‘tailored’ to particular sectors, manufacturing cannot be relied upon to deliver the jobs and growth jeopardised by the 2008 crisis (Manyika et al., 2010: 11–12). The authors unhelpfully elide job creation and output growth in this regard; manufacturing may be indispensable to the latter in the long term through productivity improvements, even while contributing disproportionately less to the former. Nevertheless, the report was cited in the BIS (2012: 7) sector analysis, by way of circumscribing the scope of the rebalancing agenda, with the document stating simply that ‘McKinsey have argued that the competitiveness of sectors matters more than the sector mix in producing growth’.

The Cable position did enjoy the support of both the Confederation of British Industry and the Trades Union Congress (TUC) in pursuing the new industrial strategy after 2010 (Bentham et al., 2013)—yet this is most significant insofar as it signifies the absence of a more radical approach to industrial policy among the trade unions. Even manufacturing trade body EEF (2015) has restricted itself to fairly limited or ‘non-disruptive’ proposals for supporting British manufacturing: its 2015 ‘manifesto for manufacturing’ advocated higher investment in skills and infrastructure, as well as lower taxes, but also largely endorsed the government’s record in establishing catapult centres and widening access to finance for SMEs. Hence, in industrial policy debates, we see the inverse of the organised resistance to macroprudential regulation identified by Baker; advocates of industrial policy largely accepted the conservative connotations of the coalition government’s discourse. Even if some groups would like government to be slightly more ambitious or to implement reform more quickly, there are few signs of sustained, widespread pressure for a more genuinely radical agenda, even among manufacturers.

Death and resurrection? 2014 onwards

By 2014, it was clear that George Osborne, as chief economic policy-maker, had shifted decisively away from the idea of an activist industrial policy or at least any position that might constitute a paradigm shift: despite the threadbare evidence, his speeches began to celebrate the coalition’s success in rejuvenating British manufacturing (see Osborne, 2014a, 2015). A speech dedicated to manufacturing in 2014 euphemistically reduced industrial policy to the notion of ‘backing businesses’ as part of the ‘long term economic plan’, alongside deficit reduction, cutting tax, and investing in education Osborne (2014b). The post-election budget in 2015 also marked the publication of the Conservative government’s ‘productivity plan’. The associated document Fixing the Foundations did not contain a single reference to manufacturing. There is a clear lack of strategic thinking evident in Fixing the Foundations; it lists the two drivers of productivity rather vaguely as ‘long term investment’ and ‘a dynamic economy’. Objectives related to ‘long term investment’ include skills, infrastructure, science and innovation, albeit with tax cuts at the top of the agenda, and alongside highly tenuous references to the Osborne agenda around reforming pensions tax relief (which was abandoned in early 2016). A flexible labour market appears to be the main objective of the ‘a dynamic economy’ category (with the inclusion of Osborne’s contentious ‘high pay, low welfare’ rhetoric). This section of the document also prioritises ‘planning freedoms, more houses to buy’ (HM Treasury, 2015: 7).

Revealingly, the final objective listed in this category is ‘Resurgent cities, a rebalanced economy and a thriving Northern Powerhouse’; the productivity plan therefore endorses Conservative plans for devolution to newly formed city-regions (HM Treasury, 2015: 41). In this regard, the coalition and Conservative governments appear to have continued the traditional role of sub-national layers in the delivery of industrial policy—yet their approach encompasses a subtle but important variation on previous practice. The coalition abolished Labour’s regional layer of industrial policy, the Regional Development Agencies (RDAs), as soon as it took office. It replaced them with Local Enterprise Partnerships (LEPs), relatively loose networks of local civic and business leaders, with few resources to invest or powers by which to leverage private investment, broadly organised on a smaller, city-regional basis (although the Regional Growth Fund, which offers seed investments to projects able to attract private investment in areas most affected by public sector cuts, has distributed £2.7 billion since 2010). As the structure of local government is reorganised around mayor-led city-regions with lower revenue grants from central government, we can broadly interpret these changes as a hollowing out of the (fairly limited) regional layer of vertical industrial policy that Blair and Brown had augmented, in favour of a reinforcement of purely horizontal industrial policy mechanisms at the local level.

Yet just as it appeared the true colours of ‘Osbornomics’ were being revealed, 23 June 2016 happened, and in the aftermath of Britain’s decision to leave the EU, Theresa May replaced David Cameron as Prime Minister, and George Osborne was banished to the backbenches. May (2016) made a noteworthy speech during her abbreviated leadership election campaign in which she advocated ‘proper industrial policy’ and criticised Osborne’s record in this regard, implying that more radical ‘economic reform’ was necessary to improve productivity. The speech in fact echoed a speech in 2013 (when May was Home Secretary) in which she advocated ‘a more strategic role for the state in our economy’ (while simultaneously eschewing a so-called ‘beer and sandwiches’ approach to industrial policy and ‘failed seventies-style corporatism’) (May, 2013). The 2016 campaign speech also included a rebuke for Osborne’s approach to regional policy, in calling for ‘a plan to help not one or even two of our great regional cities, but every single one of them’. Yet her speech concentrated on issues around corporate governance rather than industrial policy per se and made only a passing reference to manufacturing when signalling she would have blocked the takeover of leading British-based pharmaceuticals firm AstraZeneca by global giant Pfizer had it proceeded (her words were revealed as rather hollow when she acquiesced in the first week of her premiership to the takeover of Britain’s world-leading microchip producer ARM by the Japanese firm SoftBank). She also neglected to address what impact ‘Brexit’ might have on British manufacturing exports, despite stating categorically in the same speech that ‘Brexit means Brexit’. The speech advocated, at most, a Cable-lite industrial strategy, calling simply for ‘a better research and development policy’ and ‘more Treasury-backed bonds for new infrastructure projects’, in an unwieldy list which also included policy proposals on domestic energy costs and house-building.

It is worth noting that, unlike The Plan for Growth in 2011, Fixing the Foundations was published solely by the Treasury (despite its foreword being co-signed by the new Business Secretary, Sajid Javid). Its publication therefore marks symbolically the neutering of BIS (and its ministers) that had begun towards the end of the coalition era. The November 2015 spending review imposed a 20% budget reduction on the department from 2015 to 2020, matching that it had endured 2010–2015. Although the science budget was partially protected, cuts included the abolition of the Manufacturing Advisory Service. After leaving office, Cable promulgated more systematically the notion that the Treasury had undermined his industrial policy ambitions, in a letter co-authored with Labour’s former business spokesperson Chuka Umunna. Cable and Umunna (2015) criticised the Treasury for perennially ‘undermining or abandoning productive, long term government interventions’. Theresa May has actually replaced BIS with the Department for Business, Energy and Industrial Strategy, but her approach to the departmental configurations of industrial policy remains unclear. While the return of a direct reference to industrial policy in the department’s name is noticeable, so too is the fact that the department has lost responsibility for higher education and trade policy (both integral to industrial policy) and effectively been merged with the Department for Energy and Climate Change.

Industrial policy has been an important feature of the early tenure of Jeremy Corbyn, the left-wing member of parliament (MP) selected as leader of the Labour Party after the 2015 election. His ally and shadow chancellor John McDonnell has drawn upon Marianna Mazzucato’s (2013) work on ‘the entrepreneurial state’ to advocate higher levels of public investment in advanced manufacturing R&D, principally through a national investment bank (see Stewart, 2015), although Corbyn (2015) himself has (seemingly inadvertently) criticised the tax allowances offered to many companies to incentivise R&D and capital investment, by denouncing so-called ‘corporate welfare’ (see Farnsworth, 2015). There is little evidence of a coherent Corbyn industrial policy approach, with the incoherence of Corbyn’s position underlined by his own apparent indifference regarding Brexit. In contrast, Corbyn predecessor Ed Miliband had a much clearer approach to industrial policy, albeit not one that differed significantly from that pursued by the coalition. Reviews led by Mike Wright (2014) (Executive Director of Jaguar Land Rover) for the party, and former Labour cabinet minister Andrew Adonis for Labour-friendly think-tank Policy Network (2014), essentially endorsed the direction of policy development proposed by Vince Cable, albeit with higher levels of public investment. Adonis (who later accepted a role within the Conservative government as chair of the National Infrastructure Commission) was slightly more critical of existing practice, in that his review made the case for a stronger BIS department. Nevertheless, even as the Conservative Party moved away from this agenda in 2014 and 2015, Labour did not make industrial policy a feature of its 2015 election campaign.

Conclusion

The period since the 2008 crisis in Britain has seen a plethora of initiatives related to industrial policy, often focused on manufacturing. Policy innovation was propelled, it seems, by a new degree of comfort among policy elites, especially since 2010, towards acknowledging the unbalanced nature of Britain’s pre-crisis economy. The agenda seemed to wane after 2014—indicating perhaps the hollow nature of the ‘paradigm shift’—but the ascendance of Theresa May following the referendum on EU membership perhaps signals the resumption of the coalition government’s earlier agenda. Yet process of policy change has followed neither Hall’s nor Baker’s account of the ‘three order’ of post-crisis policy change in relation to, respectively, macroeconomic policy and macroprudential regulation. Industrial policy innovation is not the product of a ‘slow burn’ crisis in manufacturing that resulted in a policy learning process because manufacturing decline has been at least decades in the making. There is also the fact that apparent innovation was clearly triggered by the crisis of 2008, with little evidence of incremental policy change before this point. But 2008 was above all a financial crisis which did not disproportionately disrupt existing trends within the manufacturing sector. The rebalancing narrative implicated manufacturing but essentially represented the co-option of the motif of manufacturing decline into attempts by elites to manage wider economic problems. Innovation has stalled not because key stakeholders have resisted meaningful reforms at a later stage of implementation, but rather because the relevant policy-making bodies lack the power, resources, expertise and even inclination to push for a more radical industrial policy agenda. Generally speaking, post-crisis industrial policy innovation represents a shift in policy discourse not matched by policy substance. In fact, the radical discourse smuggles some quite conservative meanings into elite framing of manufacturing decline, which have served to constrain innovation ideationally and reinforce rather than address incoherence within industrial policy delivery mechanisms.

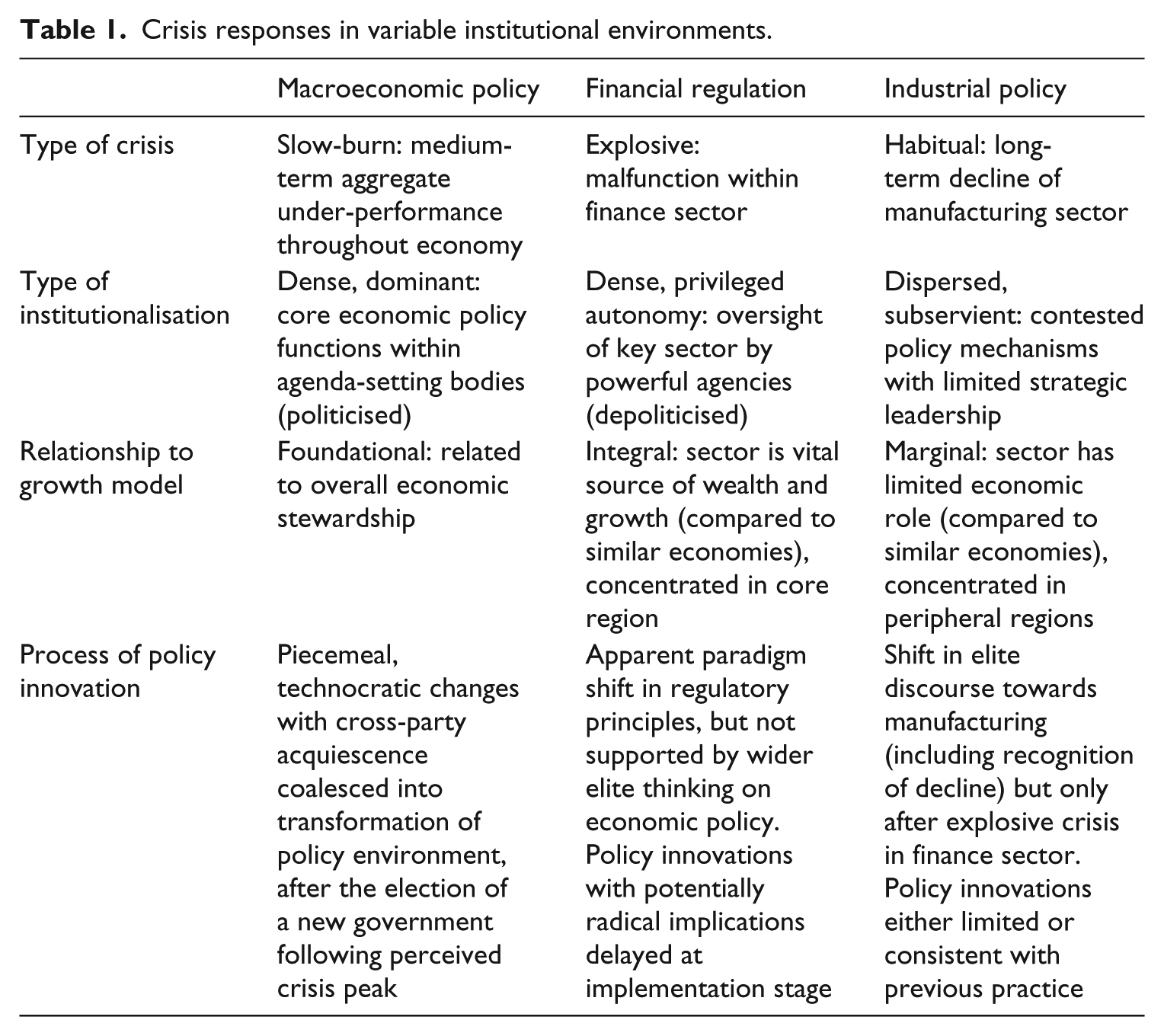

Baker adds a ‘variety of crisis’ variable to the ‘three orders’ framework to account for the process of policy change in relation to macroprudential regulation; this is a highly relevant variable to this study, but Table 1 summarises two further variables required to account for post-crisis industrial policy change in Britain since 2008. First, the differences in the institutional framework in which policy is forged are a decisive factor. Macroeconomic policy and financial regulation both have well-established institutional processes encompassing powerful public bodies—the former houses key economic policy functions discharged by agents with near-peerless authority to set agendas, and the latter comprises largely depoliticised bodies which enjoy a privileged autonomy within government (partly because of the patronage of the former framework), including the de facto ability to reform its own formal structures. Of course, these differences may help to further explain the different processes of policy change identified by Hall and Baker—the depoliticised institutions of financial regulation may have empowered policy insiders to resist change more fiercely, despite evidence of economic malfunction in the finance sector. Yet industrial policy provides an even starker contrast. Industrial policy mechanisms are operated by a relatively junior government department or local authorities. In fact, the shape and powers of both institutional settings are highly dependent on the preferences of agents elsewhere within the institutional framework of Whitehall and are frequently reformed via top-down processes to suit wider political initiatives. It is little surprise that radical policy discourse translates into, at most, moderate reform. The opponents of macroprudential regulation have an arena in which to contest reform, whereas the advocates of industrial policy have far more limited opportunities to promote their agenda.

Crisis responses in variable institutional environments.

We must also consider, second, the status of the associated economic activities in the British growth model. Manufacturing clearly plays a subordinate role in the economy. Even if we were to accept that elite actors sought to substantially boost manufacturing through a more activist industrial policy in the wake of the financial crisis, we can conclude that the paucity of the ideational and institutional resources available to them represented a significant barrier to meaningful change. Clearly, macroeconomic policy and financial regulation do not perform the same function within the growth model: the former plays a foundational role in establishing the parameters within which capitalism operates, whereas the latter performs a function similar to that which might be envisaged for industrial policy, insofar as it seeks to protect a certain set of industries while constraining their ability to threaten the public good. However, while the industries in question for financial regulation are integral to the British growth model, this is not the case for industrial policy and the manufacturing sector. As such, whereas the macroprudential regulation agenda acts in part to contain demands for more radical policy change, in industrial policy, radical policy rhetoric serves to obscure the limited capacity of the British state to deliver policy innovation.

It is clear that an industrial policy paradigm shift has not occurred in Britain (and is not likely to). But the case raises important questions about post-crisis economic policy change in general. While there has been a great deal more noise around industrial policy since 2008, and especially 2010, it seems that this noise paradoxically serves the same purpose as the pre-crisis silence from most parts of the political elite regarding manufacturing and industrial policy. The ongoing attempt by some key actors to proselytise the importance of manufacturing and the need for a new industrial policy approach may actually serve to reinforce its subservience, insofar as the discourse is framed by the conservative rebalancing narrative, therefore circumscribing the limits of policy innovation. Clearly, while the discourse challenges some of the tenets of neoliberal economic statecraft, we can more fully evaluate the significance of this shift by studying its status within a wider institutional and ideational environment. Thus, we can better comprehend how what could be seen as a partial repudiation of neoliberalism can nevertheless serve to reinforce a growth model animated by neoliberalism. This may have important implications for how policy change in the wake of capitalist crises is understood, insofar as ideas, institutions and interests are shown to interact in different ways due to a wide variety of factors.

Footnotes

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.