Abstract

There is a major blindspot regarding our understanding of different structural models of platformization beyond the dominant Anglo-American markets. This article develops a typology of political economic models of platformization by using the case of music platformization. In order to generate such a typology, the article proposes that we start by identifying variables present in any music market around the world. Three different variables are proposed: (1) platform dependence; (2) dominance of ‘global’ platforms; and (3) the degree of platform and recording industry integration. To illustrate how these variables result in structurally distinct models of platformization, the article briefly discusses the cases of South Korea, the Netherlands and Nigeria. In doing so, a framework is provided through which to interpret the experiences and conditions of musicians, and other cultural producers, in diverse platform ecosystems.

Keywords

Introduction

In this short article we draw upon the political economy of communication tradition, which reminds us that if we want to understand the impact of any media technology, we must first situate it within wider economic and political structures (Mosco, 1996). The cultural platforms that are the focus of this special issue enter into pre-existing industries (advertising, television, music, publishing, etc.). We thus argue that – in terms of the influence of platforms on cultural producers – the relationship between platforms and legacy cultural industries is just as important as any of their ‘disruptive’ technological affordances.

Of course, the precise manner in which platforms engage with legacy cultural industries, and the structural organization of this relationship, differs considerably around the world. This is yet another reason why we should not universalize the experiences of cultural producers under Anglo-American platform capitalism (see Steinberg et al., 2024). Comparative case studies that attempt to understand the effects of platforms on cultural producers from a more global perspective are thus essential. But how should case studies be selected? And on what basis?

It may seem reasonable to include cases from distant geographic regions. However, this approach can sometimes reproduce a form of cultural essentialism. Rather than, for example, assuming the shared experience of cultural producers across Asia and juxtaposing them to American cultural producers, we propose a more inductive approach. The first step is to identify political economic variables that affect cultural producers in any cultural industry undergoing platformization. These variables can be generated by asking three very simple questions that apply to any market: (1) How dependent are cultural producers on platforms? (2) Who controls these platforms?, and (3) What is the relationship between these platforms and legacy cultural industries?

A typology of different structural models of cultural platformization can be generated from the answers to these three questions. The experiences of cultural producers within these various models can then be compared and contrasted.

To demonstrate how such a typology can be developed, we will use the case of music streaming platforms (MSPs) and the recorded music industry, or recording industry. While music artists upload content to many different types of platforms simultaneously, we will consider audio-focused music streaming services such as Spotify instead of social media platforms like YouTube or TikTok that distribute a more diverse array of music-related content. This is both due to lack of space and because we want to highlight relations to legacy cultural industries (in this case, the recording industry). MSPs carry a greater proportion of music that has been financed, produced and pre-licensed from traditional record industry firms and producers. Our hope is that this example will prove productive for researchers studying the relationship between platforms and producers in other legacy cultural industries such as film, publishing and journalism.

Based on the three questions posed above, three different variables will be proposed: (1) platform dependence; (2) dominance of ‘global’ platforms; and (3) degree of platform and recording industry integration. To illustrate how these variables result in structurally distinct models of music platformization the article will briefly discuss the cases of South Korea, the Netherlands and Nigeria.

Platform dependence

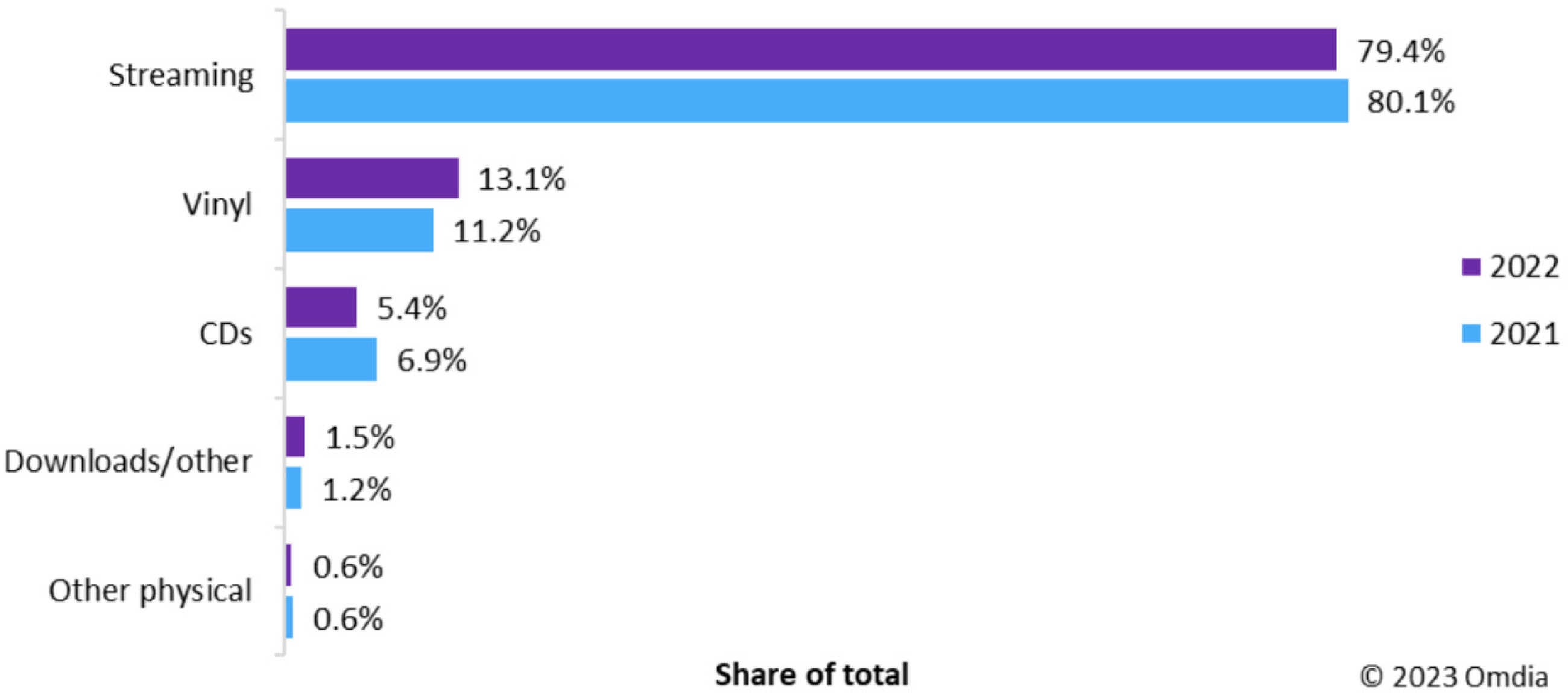

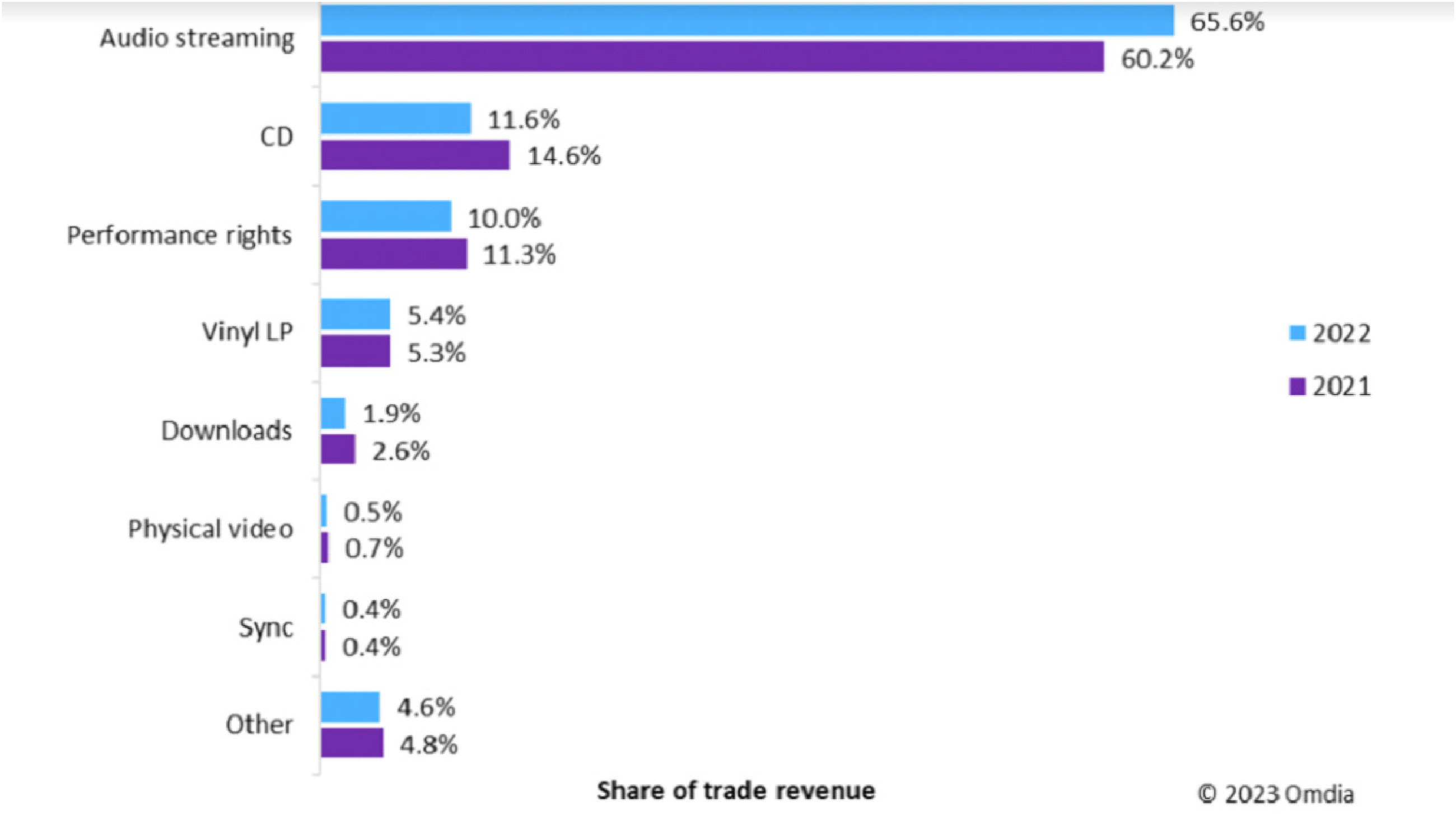

While music streaming has emerged as a mainstream mode of music consumption, there are still considerable differences in uptake around the world. In turn, musicians in different markets are more or less dependent on the income and publicity generated by MSPs. For example, in the Netherlands streaming is easily the biggest revenue source for the Dutch recording industry (see Figure 1). Next door in Germany, however, streaming takes a somewhat more modest share of overall recorded music revenues, due in part to the persistent strength of CDs in the German market (see Figure 2).

Netherlands, recorded music trade revenue by source share, 2021 and 2022

Germany, recorded music trade revenue by source share, 2021 and 2022

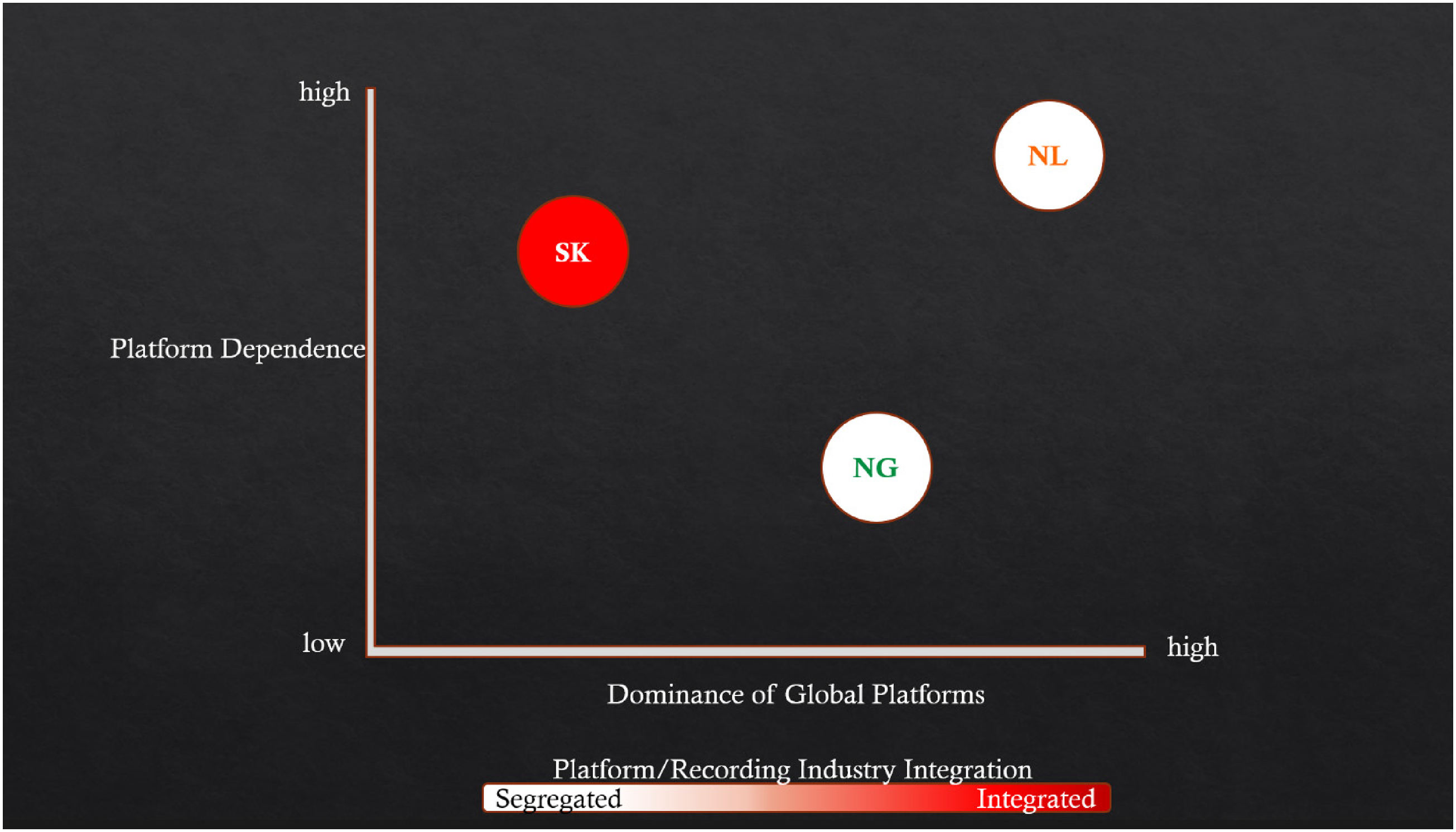

Three models and representative countries.

While these numbers don’t tell the entire story, they provide some insight into the relative dependence of musicians in different markets on streaming platforms for income, visibility, and communication with fans. Platform dependence is thus an important variable to consider when studying the implications of platformization in any one cultural market, or when comparing the experiences of producers across different markets.

Dominance of ‘global’ platforms

Alongside the question of how dependent musicians are on platforms, there is a related question: which MSPs are musicians in different countries dependent upon? Not only does the rate of streaming adoption differ considerably, so does the relative dominance of global streaming services in different countries. ‘Global’ here refers to MSPs not tailored to a specific market or region but rather addressed to a ‘universal’ consumer. Spotify, for example, is available in a standardized design in 184 countries and territories around the world (United States Securities and Exchange Commission, 2022: 21). There are, however, many national or regional MSPs that outperform Spotify across Asia, the Middle East and Africa. We can thus distinguish between music markets wherein national or regional MSPs are dominant, and markets that are dominated by the global (mainly Western) MSPs. This variable has significant implications for the ability to regulate platforms: it is easier for any government to raise streaming rates on domestic MSPs than on international companies, for example. We may also posit that a locally based MSP might do more to promote music from that country, but this is of course an empirical question that must be researched.

Degree of platform and recording industry integration

A third important variable that needs to be considered is the structural relationship between MSPs and the recording industry. The degree to which the companies that operate MSPs are integrated into the recording industry varies considerably around the globe. In North America and Europe streaming services are structurally independent of legacy record companies and their still-dominant distribution channels (Arditi, 2020). However, this is certainly not the case everywhere, as we discuss below. This variable is critically important when considering the relative autonomy and agency of music artists and record labels.

Three models

Any music market can be assessed according to these three structural variables: platform dependence can range from ‘low’ to ‘high’; as can the dominance of global platforms and the degree of platform and recording industry integration. Doing so allows us to identify distinct ‘ideal type’ models of music platformization, from which we can then compare the experiences of music artists. 1 Due to space constraints, we will describe the characteristics of only three possible models that emerge from these variables, and briefly discuss a representative country for each (see Figure 3).

Model #1 is characterized by ‘high’ platform dependence; ‘high’ dominance of ‘global’ platforms; and a ‘low’ degree of platform and recording industry integration. While there are many music markets that fit this description, we can take the Netherlands as a specific example. The Netherlands is a global leader in music consumption via streaming and streaming revenue as a proportion of overall recording industry revenues (IFPI, 2021). The streaming landscape is dominated by global MSPs – in particular Spotify. There are no leading Dutch music platforms. The Dutch recording industry operates separately from the platform companies. In markets that fit into this model, online platforms mainly distribute and pay royalties for content produced and owned by record companies and music artists.

Model #2 is characterized by ‘medium’ platform dependence; ‘low’ dominance of global platforms; and a ‘high’ degree of integration between platform companies and the recording industry. South Korea provides us with a clear example of a country that fits into this model. The first music market to introduce the subscription model of music streaming, South Korea has one of the world's highest rates of streaming consumption (IFPI, 2022). However, streaming accounts for a smaller share of overall recorded music revenues than in the Netherlands, as artists – especially Kpop idols – still sell a large (and growing) number of CDs to their fans (Dyson, 2023c). While international services such as Spotify and Apple Music are present in South Korea, their market share is tiny compared to leading Korean platforms, such as Melon. While MSPs in the Netherlands (and other countries that exhibit a low degree of integration) mainly distribute content that is produced by record companies and music artists, the leading streaming services in South Korea are involved not only in distribution but also in the production of content. Vertical integration is exercised by the telecom and social media conglomerates that developed and operate the leading Korean streaming platforms (Lee, 2009). This is accomplished through direct deals, investments, joint ventures and strategic partnerships with music and management companies (Park et al., 2023). While this model would seem to provide tech companies with greater control over the careers of music artists, this is a hypothesis that needs to be researched.

Model #3 is characterized by ‘low’ platform dependence; ‘medium’ dominance of global platforms; and a ‘low’ degree of integration between platform companies and the recording industry. Nigeria is a prime example of a music market that fits the characteristics of this model. Nigerian musicians rely to a large extent on financial support from corporate brand sponsorships (Serres, 2023). However, while streaming consumption (and therefore royalty revenues) in Nigeria remains relatively low, it is projected to grow rapidly (Versus Africa, 2021). Nigerians access music through global platforms, as well as domestic and regional MSPs, such as the Chinese-owned but Nigerian-based ‘Boomplay’ – the largest MSP in Africa. Streaming platforms in Nigeria are owned and operated separately from the Nigerian recording industry. 2 Boomplay is operated locally by Nigerian staff and claims to host ‘the largest catalogue of African music’ (Boomplay, n.d.). Epitomizing China's soft-power-through-hardware approach, Boomplay gained its leading position in Africa by being pre-installed on phones made by Transsion – a Shenzhen-based mobile phone manufacturer that is the leading smartphone seller in Africa (Avle, 2022; see also Tse et al., 2024).

Conclusion

In this short article we have argued that there is a major blind spot regarding our understanding of different types – or structural models – of platformization beyond the dominant Anglo-American markets. While platforms certainly introduce new logics into cultural sectors and new affordances for cultural producers, we need to be careful not to fetishize platforms as a technological form. As with previous media technologies (i.e. the phonograph, terrestrial radio, television, etc.), platforms enter into and mediate pre-existing cultural industries and markets (Hesmondhalgh and Meier, 2018). The structural organization of the resulting industry ecosystem differs around the word, and this is a difference that matters for cultural producers.

This article proposes a conceptual approach for studying and comparing the experiences of cultural producers in diverse platform ecosystems around the world. Through the example of MSPs we have offered a typology of different structural models of cultural platformization. Due to space constraints, we were only able to illustrate three possible models, but there are of course more combinations of variables resulting in different models.

The task for researchers is to try to understand and interpret empirical research into the lives and careers of cultural producers within the context of these different models of platformization. This allows researchers to test how and to what extent structural factors impact the lives and careers of producers. Researchers could use a range of different methodologies – from large-scale surveys that compare income derived from platforms in different countries, to multi-sited ethnographic research examining experiences of creative autonomy under contrasting models. Importantly, the questions that generate the variables that make up each of the models should be seen as research prompts that can be reflexively tested and amended in response to empirical evidence gathered on the ground.

A typology such as the one proposed here facilitates more nuanced statements regarding the effects of platformization. For instance, it has often been claimed that platformization has reduced gatekeepers and ‘furnished the potential for individual producers to be economically emancipated from legacy media companies’ (Poell et al., 2022: 50). However, the intense degree of vertical integration exemplified by South Korea's music industry requires us to qualify this statement. Perhaps the potential for ‘emancipation’ is less likely for musicians in countries that fit into Model #2. Likewise, the extent to which platformization results in cultural producers becoming increasingly ‘platform dependent’ (Nieborg and Poell, 2018) is likely as much a result of the particular industrial ecosystems such platforms are embedded within as it is an outcome of the platforms themselves. Thus, one contribution of the proposed approach is to remind researchers to look beyond the platform in order to understand the implications of ‘platformization’.

As researchers, we need to locate platformization within the broader political economic and sociocultural contexts of cultural production. At the same time, we need to understand particular characteristics of local culture/tech entanglements and resist representing these as mere mutations of a standard Western model (De Beukelaer 2017; Perullo 2011). A typology of platformizations helps us to better understand ‘how platformization takes shape within and through particular contexts’ (Poell et al., 2022: 20), allowing scholars to develop an empirically grounded and truly global understanding of cultural production in an era of online platforms.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Korean Studies Grant 2020: Academy of Korean Studies (grant number AKS-2020-R82).

Notes

Author viographies

Robert Prey is a media scholar who studies the relationship between technology, capitalism and culture. Dr. Prey's ERC funded project ‘PlatforMuse’ focuses on how musicians are adapting to ‘platformization’ in Nigeria, South Korea and the Netherlands.

Seonok Lee is a sociologist with expertise in global labor migration, racial hierarchies, class, and gender. She is currently researching platform workers and the gig economy in the Netherlands and South Korea.