Abstract

Major multi-territory streaming services such as Netflix, Prime Video, and Disney+ dominate this new sector of video distribution, but the economic features of internet-distributed video enable a diverse sector. This article examines 16 non-US-based multi-territory services and 10 national/regional markets to investigate the other types of transnational streaming businesses emerging. The analysis assesses the ownership of the 16 services, as all but one emerge from existing corporations with activities in the audiovisual or distribution sector, to identify the implications of different ownership priorities. It then pairs the ownership analysis with data on the size and country of origin of the services’ content libraries. The findings identify subcategories of multi-territory streamers and, by considering an array of national markets, reveal the counter-strategies available to non-US-based services.

The capacity to develop businesses based on distributing on-demand video to audiences across national borders is an unprecedented and fascinating aspect of streaming video – especially by those based on subscriber funding. The affordance of transnational distribution has reignited the imagined globalism that was the zeitgeist of the turn of the century, although lessons learned about transnational capitalism since have appropriately tempered the heady speculation common at that time.

The business opportunity of streaming has extraordinary implications for culture and brings exponential adjustment to processes of late 20th-century business internationalization and mass audience splintering (Lotz, 2022). Audiovisual industries steadily shifted from domestic roots to a decidedly transnational business over the late 20th century (Steemers, 2004). At the same time, distribution technologies such as cable and satellite expanded choice and fragmented audiences, which rescoped businesses based on providing video and the range of video storytelling that could be commercially viable. The direct-to-consumer business of multi-territory streamers significantly compounded those disruptions through their ability to meaningfully embrace consumers without the persistent nation-based structures of business models that prioritize building national audiences for advertisers. Although a transnational technology such as satellite allowed similar reach, the core business remained mired in national organization because of advertisers’ purchase of nationally delimited audiences (Chalaby, 2008).

Paradoxically, nation remains salient, even crucial, to understanding the implications of streaming in culture despite technological and business affordances that allow exceptional transnationality. ‘Streaming’ does not arrive uniformly or with consistent effect in countries around the globe. Rather, how it is experienced and adopted are strongly shaped by pre-existing national conditions. A national lens remains critical because streaming does not erase underlying conditions and histories, or factors such as population scale and wealth. Instead, streaming intervenes in established national sectors with incumbent technological, economic, and regulatory dynamics that structure the array of services – streaming and otherwise – available to a user. Streaming exists alongside established audiovisual sectors that are nationally specific and shape how viewers perceive the need and value of these services, rather than there being some common global appetite for their offerings. National conditions specify a broader audiovisual context of competing and complementary services and supply the basis of pre-existing cultural norms and expectations.

In addition to variation in national conditions, neither all streamers, nor even all ‘global streamers’ operate with the same business model or corporate strategy. For instance, our analysis of Netflix libraries revealed the libraries of this ‘US streamer’ to feature more titles produced outside the US, while studio-based services such as Disney+ and Paramount+ overwhelmingly offer US-produced titles (Lotz et al., 2022). In grappling with Straubhaar's (1991, 2007) crucial work on the value of ‘proximity’ in the pre-streaming, pre-fragmentation era, we argue that stronger theory building will emerge from seeking patterns among carefully contextualized examinations of streaming in specific national markets than from approaching streaming by assuming a global frame. We argue for the need to begin by building contextually grounded cases and then deriving more general knowledge through assessing patterns that emerge, rather than attempting top-down theory building that assumes transnational commonality.

Multi-territory streaming services originating from US-based corporations have dominated the study and discussion of streaming. This is unsurprising given the hegemonic status of US audiovisual industries in exporting productions and in the early multi-territory efforts of these services, despite the first on-demand and streaming services developing elsewhere. The major players in the US-based sector can be divided among pure-play, streaming endemic services (Netflix); studio-based services that offer libraries dominated by movies and series produced over decades (owned-IP) that extend existing audiovisual businesses into streaming (Disney+, Paramount+, HBO Max); and services that complement companies’ primary businesses by offering video (Prime Video, AppleTV+) (Lotz, 2022).

Much less is widely known about non-US-based services, many of which also offer multi-territory service. The streaming ecosystem in most countries blends a variety of multi-territory and domestic services, as well as ad-supported video services, some of which operate similarly to subscriber-funded streamers, while others operate more in accord with the logics of ephemeral video (Lotz, 2021b) and social media (YouTube; Instagram; Facebook). 1 Such services are often strongly complementary in their content offering, although competitive to the extent that viewer time is limited, or there is competition for a finite pool of advertiser funds. Despite the appearance of commonality that offering video provides, the underlying business models, strategies, and priorities of the services can vary significantly, especially as related to content costs and the scale needed to be profitable (although few are profitable at this point).

The frame of ‘streaming wars’ has dominated much of the press and Wall Street conceptualizations of the US market, and this frame is often erroneously projected onto the broader transnational scene, despite the peculiarity of US conditions. The dynamics of the US market have disproportionately guided investor and expert thinking, which has limited the conceptual imagination of these services as businesses and as cultural entities. Of course, the assertion of a US lens on multifaceted global communities is nothing new or distinctive for the audiovisual sector. However, the US is home to very particular audiovisual industrial dynamics and context, specifically (1) its history of extraordinary levels of multichannel adoption (‘pay-TV’) that operated with different economic norms from many markets and (2) the non-competitive market conditions that allowed very high fees to be charged across a sizeable population. Those fees buoyed Hollywood content creators through the early 21st century, and those content creators now face a far more competitive sector in which producers outside the US have paths to audiences that Hollywood cannot control. Nor can Hollywood continue to outspend others based on revenue from an uncommonly large and wealthy domestic audience to maintain historic levels of dominance.

A key affordance of streaming services is their efficiency in reaching viewers across national borders to create audience scale for titles that would be too niche, a strategy that contrasts with seeking multinational scale by federating at the national level (e.g. a Disney channel on every national cable/satellite system) (Lotz, 2021a, 2022). The affordance of transnational audience aggregation has the potential to diminish the structures that have ordered the global audiovisual competitive field to date, although of course capitalism and basic economic principles remain in place. Revenue source is a key variable differentiating streaming video services and remains a significant area of experimentation. Our focus tends toward subscriber-funded services (SVOD – subscription video on demand); however, major established services have recently integrated ad-funded tiers, and there has been a greater variety of funding models and tiers among services based outside the US, necessitating that we make revenue model less central in this analysis. Nonetheless, we remain focused on services designed to distribute professionally produced, scripted content.

The other articles in this special issue provide context-based analysis of a handful of nations. They track different stories of how streaming has adjusted national ecosystems in subtle and not so subtle ways that have led to different implications of streaming. Patterns certainly appear across the cases, but the divergences are particularly noteworthy for adding sophistication to our understandings. The divergences reveal the often taken-for-granted features that significantly structure industrial practice in assumptions of common ‘global’ operation. This article deviates from the others in its method and approach but not its goal. It analyses macro-level data of streaming libraries and the ownership of non-US-based streaming services to investigate some of those patterns and to expand our previous work beyond Netflix.

It remains difficult to access a range of data about streaming services. Meaningful data about consumption – except in rare and most-viewed cases – continues to be elusive and poorly contextualized. Even simple data such as subscriber reach is not reported consistently, nor do services reliably offer information about their ever-evolving libraries of titles. The sector has grown mature enough that third-party services have emerged that offer data of seeming reliability from which we can begin to devise more systematic insight. 2

This analysis examines patterns in ownership and library composition features of 16 non-US-based services to develop a fuller picture of the services that have emerged in the last decade. Our approach to selecting these titles prevents us from claiming our findings as generalizable; rather, we aim to model an approach to investigating video streaming that surfaces the variability among services, their strategies, and their owners. We compare the composition of the country of origin of titles in their libraries and assess patterns relative to ownership of the service and the extent of multi-territory scale. We do not claim this group as the ‘largest’, ‘most important’, or representative services but rather indicative of a complex and diverse market, and thus useful for broadening the pervasive US- and Western Europe-centric lens. Their selection derives from our expert assessment of them as relatively established services – amidst a still-emergent sector – that appear committed to being video service providers rather than casual value addition, as well as their inclusion among services for which Ampere Analysis, a data and analytics firm specializing in the SVOD sector, collected exhaustive library data that enables a combination of structural and content analysis. This collection of services also usefully spans both an array of national and multi-territory markets in different regions, and is numerous enough to reveal patterns about the sector distinct from those evident in the otherwise common emphasis on US-based services.

The second part of the article then examines one regional and eight national markets in order to compare the library composition of a range of US- and non-US-based multi-territory and domestic services to investigate the array of complementarity and competition emerging. The selection of these markets enables us to assess dynamics across a few large countries, as the situation for smaller ones will be very different – as was also the case before streaming, and across regions to compare a range of English and non-English-dominant markets, those with a strong history of US imports, and others that have engaged in only limited Western content trade. The case selection is intended to provide indicative rather than generalizable results.

Contrasting non-US-based services

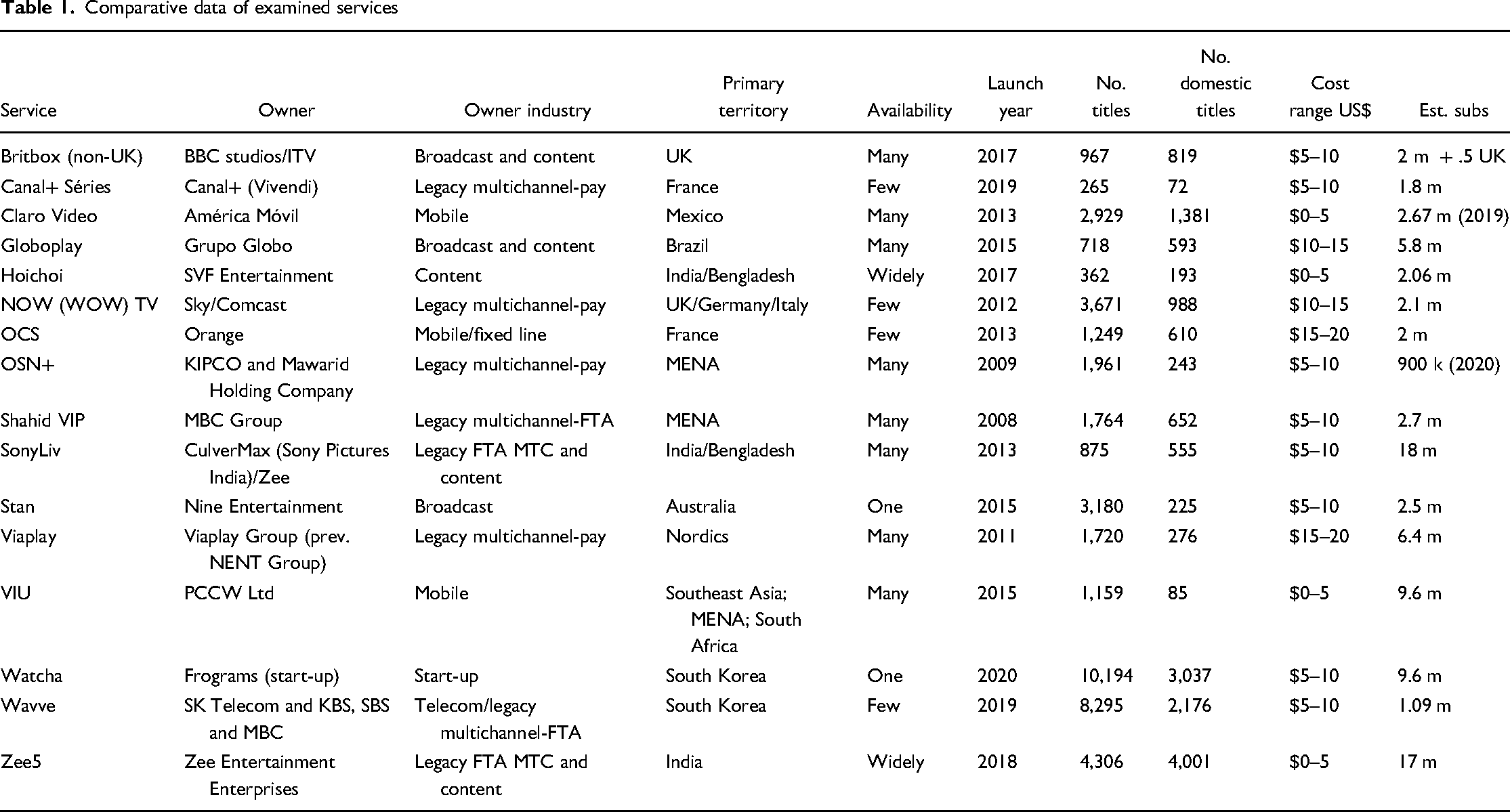

This first section examines 16 non-US-based, mostly 3 multi-territory services: Britbox, Canal+ Séries, Claro Video, Globoplay, Hoichoi, Now TV, OCN, OSN+, ShahidVIP, SonyLIV, Stan, Viaplay, Viu, Watcha, Wavve, and Zee5. 4 Table 1 highlights key features of the services for quick context and comparison. 5 Notably, Chinese services iQIYI, Tencent Video, and Yoku-Tudou are not included here, despite all of them ranking among the estimated seven most-subscribed services worldwide. The reason for this exclusion is multi-fold. Foremost, although each of these services has an SVOD element, a clear stand-alone SVOD market does not exist in China, which makes comparison very difficult. Furthermore, the particular political economy of China makes it unlike any other territory considered and makes assessments true for Chinese streamers difficult to project more broadly while the services originating elsewhere have not been able to operate in much of the Chinese market.

Comparative data of examined services

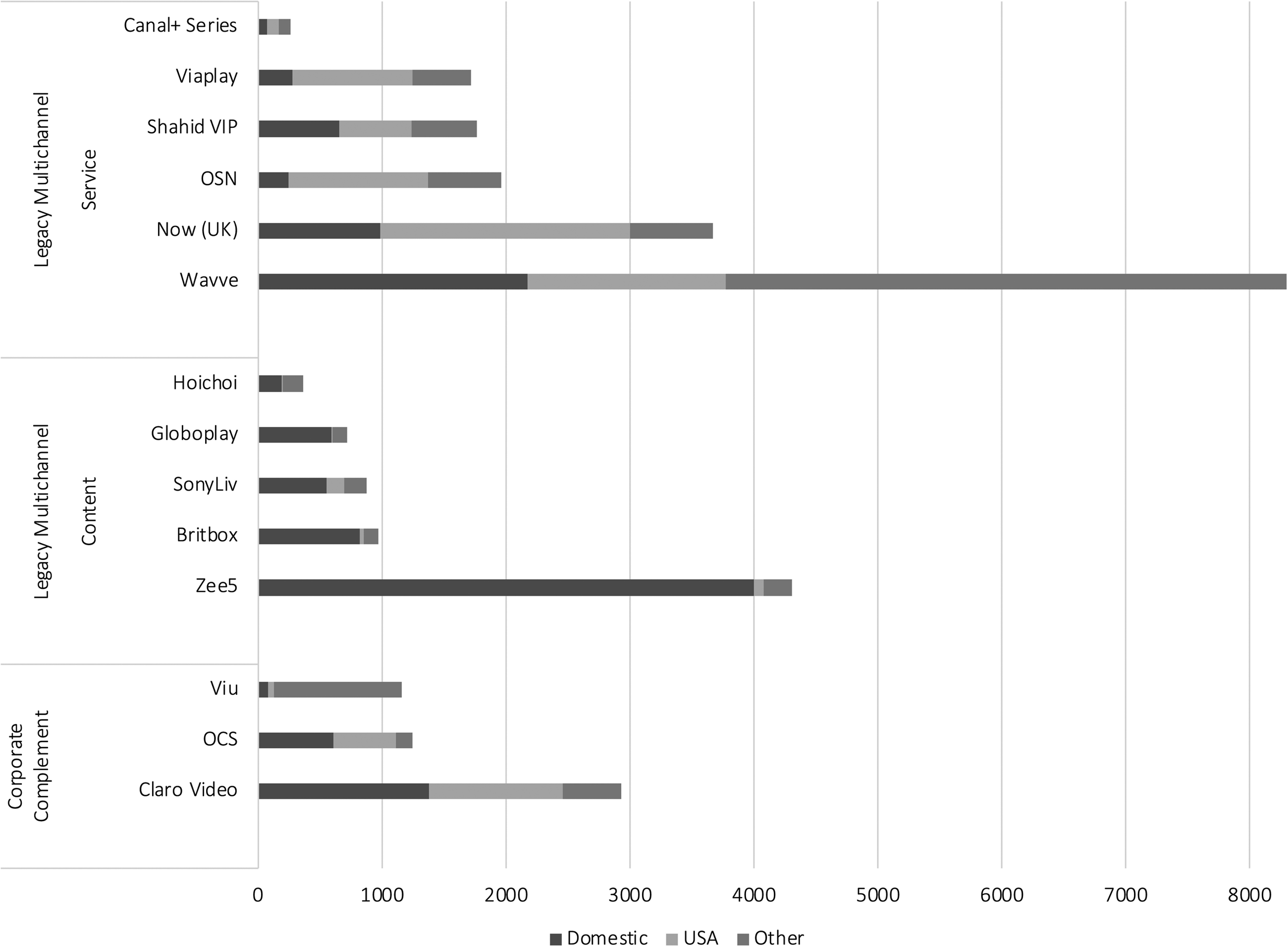

The most notable feature to emerge across this sample of services ties to ownership. Only one of these services, Watcha, can be considered as endemic in the way Netflix, Prime Video, and AppleTV+ have grown video services from no underlying audiovisual or telecommunication enterprise. Nor are any others focused on streaming alone. Just as many of the US-based, multi-territory services have emerged from companies with existing businesses in audiovisual production and distribution, most of the services considered here are owned by companies based in producing or distributing video. Assessing the core of those established businesses is difficult. They all span a continuum from those that are primarily service providers (NowTV; OSN) to those that have been focused on content production (Hoichoi), with several that have supported multichannel service businesses primarily reliant on ads (Zee5) or subscriber fees (Canal+) that are also engaged in varying levels of content production in support of those channels. 6 It is thus difficult to discretely sort the services, but we’ve done so in the following discussion and Figure 1 with an eye to whether the core competency of the company derives from revenue from service provision or production experience/ownership of a recognizable library of titles.

Streaming services most aligned with companies with established multichannel businesses include Canal+ Séries, NowTV, OSN, Shahid, Wavve, and Viaplay, and to a lesser extent Zee5. 7 These services can be considered as ‘corporate extensions’ (Lotz, 2022) and are advantaged by experience and expertise in providing entertainment services, from strong name recognition, and often long relationships with individual consumers. This makes marketing a new service relatively easy for these companies. Establishing streaming services also helps diversify their companies and hedges against shifts in the ecosystem of services and related competitive dynamics. The services have the potential to expand their pre-digital customer base by attracting consumers not already accessing the company's multichannel offering (as many bundles were broader and more expensive than some consumers desired) and to ensure a continued role in the ecosystem in situations in which streaming services are viable replacements for viewers dissatisfied with legacy multichannel service or offerings.

Two subcategories can be identified among the services emerging from companies with established multichannel businesses. One category encompasses those companies that dominated multichannel service using satellite or cable and relied significantly on subscriber fees for revenue (Now TV, OSN, also Binge and Crave discussed later). These legacy subscriber-reliant businesses differ from those that developed in national markets with greater multichannel competition, many of which relied more on advertising revenue and made content production central to their business (Globoplay; Hoichoi; SonyLIV/Zee5). This difference has encouraged different strategies among the services. The legacy subscriber-reliant services tend to be more market specific and have existing relationships with Hollywood studios and exclusive content deals. The legacy advertising-reliant services have extended into multiple territories and tend to have a higher percentage of domestic titles in their libraries.

The predominance of companies with established multichannel businesses is unsurprising, rather more peculiar is the limited extent to which such businesses have emerged in the US. This is an instance where national variability is worth noting in some detail, and shows why it is crucial not to project US dynamics on the global marketplace. The structural operation of multichannel services differs significantly across national markets, and the dynamics most common outside the US are quite different from those of the US that developed from a particular regulatory landscape. Companies such as Viaplay Group and MBC Group (owners of Viaplay and Shahid respectively) have operated in more competitive multichannel environments, with business based more on advertising than the subscriber revenue that drives the US system. This ownership pattern is not evident among the US-based streamers because of the structural separation (excepting Comcast/NBCUniversal/Peacock) of multichannel service providers such as Charter and Cox from channel operators, which are commonly tied to content conglomerates built around content creation such as Disney, Viacom, and Warner Bros./Discovery. The US multichannel providers have evolved into monopoly internet providers rather than developing businesses in the streaming video space, while in many of the countries considered here, the norm in multichannel service has featured a more competitive field of multichannel and internet services/packages. 8

Notably, few of the non-US-based companies that have developed subscriber-funded streaming services have significant businesses in internet provision. This again underscores the very different business foundations and competitive norms in different countries. Instead, for many of the non-US-based streamers emerging from legacy multichannel operators, adding a streaming option enables them to maintain and upsell consumers willing to pay for the enhanced on-demand capabilities offered by streaming. In most cases, these services do not aim for the type of global scale characteristic of the US-based streaming services. Rather, they offer streaming to ensure they are not replaced in their market and have an opportunity to grow their market share by extending into more markets even if only achieving minor market presence. To be clear, this analysis aims to illustrate the diversity among the companies that are developing streaming services and their related market advantages and reasons for their discrepant strategies. The non-systematic selection of services prevents us from making claims about the sector more broadly. Rather, we have found developing reliable cross-nation expertise challenging and hope to offer frames that others might find useful in developing context-based analysis.

The second type of company developing multi-territory streaming services includes those built on developing content, often for co-owned broadcast or ad-supported multichannel services such as Britbox, Globoplay, Hoichoi, SonyLiv, Zee5 and, to a lesser extent, Canal+ Séries. They too can be considered as corporate extensions based on strategies similar to those of US-based services such as Disney+, Paramount+, and Max (formerly HBO Max).

US-produced content has circulated around the globe more extensively than that produced by other countries, but it is important to recognize the structural advantages that have supported this Hollywood hegemony rather than assuming this is the result of some natural preference. Crucially, the affordances of internet-distributed video diminish the structural advantages that have aided Hollywood in international distribution and make global reach more feasible for other national industries. Companies/organizations such as ITV, BBC, Canal+, SVF Entertainment, Grupo Globo, and Zee Entertainment have long histories in highly populous countries. Their brands are well known domestically, and they are identifiable ‘national’ providers based in countries that have developed significant diasporas around the globe. Many of these companies with significant content holdings have experience providing packages of channels to viewers as well.

To be clear, it is unlikely that most countries can develop streaming services with significant multi-territory reach. It is already the case that fewer than a dozen countries have robust enough funding available to national screen industries to produce the scale of scripted content required. It is, however, likely that a category of service will develop that can scale with significant adoption as regional/diasporic providers, or achieve niche adoption across a broader geography; Viaplay and Zee5 arguably illustrate these respective strategies already. These services have a head start in the market, which positions them well to partner with or acquire others with some intellectual property holdings but too few to support a service. An under-exploited aspect of streaming to date is the availability of back catalogue produced outside the United States. Such titles add value to national or regional libraries in the same way as US back catalogue, although the value proposition may be for a narrower range of viewers with affective nostalgia, or for whom domestic content is a particular priority. Often this intellectual property is spread across many smaller producers, which has left it inaccessible because few hold enough titles to support a service, or because pre-digital contractual arrangements with talent prove too cumbersome to navigate.

Mobile service providers such as Mexico's América Móvil (Claro Video), France's Orange Telecom (OCS), and PCCW Limited (a Hong Kong-based ICT that owns Viu) comprise a third business sector that has supported the development of multi-territory streaming services. The value of a streaming service for a company deriving most of its revenue from mobile data provision is likely more that of a corporate complement in contrast to corporate extension. Access to a video service adds value for service subscribers, differentiates the provider in the marketplace, and is an asset in subscriber retention.

Again, pre-existing national ecosystems established in an era of analogue and wire-based video distribution led to different strategic expansions for legacy players in different countries, strategies derived from competitive conditions, technological norms, and regulatory structures. Where many of the established multichannel companies have derived significant historical revenue from advertising, the mobile providers are more attuned to subscriber maintenance priorities, which may lead to different approaches to developing streaming services; it can also lead the companies to have different goals and priorities for streaming services designed to complement, rather than extend the existing corporation. Many mobile providers have partnered with video services in an attempt to add value for subscribers or create a point of market differentiation. We’ve tried to focus on those that appear to be developing legitimate streaming offerings. Indeed, Viu's streaming strategy appears largely unrelated to PCCW's core operation – Viu is mostly available in markets separate from the company's mobile coverage; this may be a case of corporate diversification.

National wire infrastructure also leads to very different national conditions. In some countries mobile data provides the primary or sole internet connection, while others have strong wired infrastructure that has had a competitive advantage for in-home streaming use. The competitive dynamics within countries lacking strong wire infrastructure are likely to change significantly with the expanded rollout of 5G data technology that reduces the advantages fixed-line internet providers have held. Even beyond that, national approaches to regulation and competition have supported different levels of mobile innovation such as standard available speed and cost. 9

Crucially, none of these non-US-based services dominate the markets they reach, underlining how the most useful frame for understanding the sector of video streaming involves not simply looking at who is ‘winning’ in terms of subscribers, but also the market offerings that suggest opportunities of complementarity. The analysis now combines the insight provided by ownership differences among non-US-based streamers with analysis of some basic features of the libraries they offer. We first consider services available in disparate markets for context and then integrate them into specific national markets along other US-based and domestic services to assess differences in strategy and the relative complementarity to direct competition among them.

Correlation between ownership and library

Figure 1 depicts data from Ampere Analysis regarding the size of different service libraries and the country of origin of the titles in the different libraries organized by type of ownership. 10 We acknowledge that country of origin is an imperfect categorization. It fails to capture the significant range in how extensively features of a culture are imprinted on a title's storytelling and it does not account for ‘runaway production’. However, some blunt tools are needed to assess data at scale and country of origin does help distinguish among the libraries in a way that reveals strategic differences. The analysis here sorts titles according to domestic, US, and ‘other’ national origin based on the home country of the service. In our analytic process we composed versions of this sorting that expanded the domestic category to include geo-culturally or linguistically similar countries. Only in the case of the Middle East and Northern Africa (MENA), which we subsequently elected to treat as a region, did this expansion significantly change the balance of library composition. 11 Sevices Stan and Watcha that are only available in a single country are excluded from Figure 1.

Service libraries: size and country of origin

In terms of library scale – the number of titles in a library – we see patterns by ownership category. Services developed by legacy multichannel providers tend to be larger – in the range of 1800 to 2000 titles. This size is comparable to US-based owned-IP services such as Disney+; and roughly half that of Netflix, which offers a library of approximately 5000 titles. The size of library offers an indication of the extent to which a service is designed to complement an array of other video sources or be a comprehensive offering. This comparative look at library size also indicates some services’ blending of characteristics of different ownership types. For instance, Canal+ Séries a legacy multichannel service provider that is also part of a company with content production, but it is an intentionally narrow offering to serve a customer segment unwilling to pay for a larger bundle that includes movies and sports; it is strategically small. In contrast, the scale of Zee5’s library belies how Zee Entertainment has both extensive legacy content and multichannel operations.

The two Korean services, Watcha and Wavve, stand out; their libraries have more than twice the number of titles as others in a country with a comparatively underdeveloped streaming sector. Korea's 2022 premium streaming revenue amounted to only $1.7 billion (according to data from Media Partners Asia) in a country with a population of 52 million people, compared to $2.8 billion in Australia, with half Korea's population. The Korean services rely on a different model for remunerating content licence holders. Rather than licensing all titles offered in a library, for example through a flat payment fee as currently standard in the industry, Korean scholar Suk Kim reports a blending of contract terms. 12 Some combination of revenue share, minimum guarantee, prepayment (an advance), and monetization per view are used (also see examples of Izzy and ChaiFlicks in the Israeli market discussed by Wayne and Sienkiewicz, 2022). These methods enable the sizeable libraries by requiring less spending to have titles available in a library and focusing remuneration on those titles watched, even if many titles go unwatched or rarely viewed.

While the size of libraries tends to reflect strategies consistent with the ownership of companies launching services and the extent to which they are aimed at supporting other businesses – such as adding value to a mobile phone offering – examining the composition of libraries in terms of the country of origin of those titles is more useful for illustrating how services differentiate themselves. Unsurprisingly, the non-US-based companies provide more domestic content to their ‘home’ countries than the US-based services offer in those markets (see Lotz et al., 2022 for a detailed look at Netflix's distinctness from other US-based services in this regard). Among the services considered here, those from companies with long histories in content production offer more domestic titles and very few US titles in comparison with services emerging from companies that are legacy multichannel service providers – although both types of services often focus on offerings from a single market (most do offer multi-territory service, as discussed later). Services from legacy multichannel service companies have larger libraries, though fewer domestic titles relatively and in absolute numbers in several cases. The value proposition of these services ties into that blend: exclusive US content, greater title breadth, though fewer domestic options.

These differences highlight the complementarity of services in the market, and the extent to which they are not easily interchangeable. Notably, consumer desire is mixed: more domestic content may compel some while others prioritize the US titles or broader array. Also, consumers often ‘stack’ these services, or subscribe to more than one, so this variance in value proposition is evaluated relative to other services in the market.

The lack of a clear pattern among the libraries of services developed by mobile-dominant companies underscores the lack of natural advantage that contributes to their content strategy; services from companies that own libraries of titles have prioritized those properties, while the legacy multichannel services have existing relationships with US studios that likewise enable their differentiation through exclusive access. Notably, Claro Video and Viu are endemically multi-territory services, with Claro Video extending into many markets in Latin America, although expanding Claro Video's ‘domestic’ count to include titles from countries geographically, culturally, or linguistically proximate to Mexico only yields a few more titles. 13 Viu reaches very diverse geographic markets in spanning Southeast Asia, MENA, and South Africa, and may be most recognizable for its strong library of Korean dramas. The variability of the libraries from mobile-dominant companies suggests a range of strategies supports these companies’ endeavours in the sector.

Few consumers have access to all or even most of the services being compared here. It is helpful to see the library balance among the complement of 16 services for macro-level comparison, but in considering consumer perspectives, it is more informative to consider library composition among services in a national market. Examining the services available in a sample of markets better reveals how different library strategies support a consistent range of service types in a market.

National market analysis

Another way to appreciate the structural conditions that have allowed a variety of streaming services and strategies to develop is to consider specific national markets. Such analysis enables a perspective that better matches that of the consumer who has little regard for the multi-territory scale of services but is most interested in the array of options specifically available. Although the look at national markets here focuses only on the streaming market, a more rigorous analysis would encompass the linear and AVOD (advertisement-based video on demand) options in the market, and consumers’ relative satisfaction with the value such services offer. The other articles in this special issue illustrate such deeper contextual examination of the broader video culture and the role of regulation, infrastructure, and national economies.

This section examines one regional and eight national markets: Australia; Brazil; Canada; France; Germany; India; MENA; South Korea; and the United Kingdom. These markets are selected to include contexts with developed streaming marketplaces, a variety of geographic regions, and to contrast English and non-English-language-dominant markets. Notably these are exceptional markets: they have the requisite combination of national wealth and population scale that enable a range of services, in particular single-territory services prioritizing the domestic market. It is not likely that they offer a model for other countries. Rather, services that are most likely to achieve sustainable subscriber-funded businesses will emerge from these markets and a few others. The analysis illustrates the challenges facing some services and how the competitive advantages of streaming may differ from those that structured linear distribution and previous trade norms. Detailed briefs about each of the national markets are available at the Global Internet TV Consortium web site and provide descriptive context for those unfamiliar. 14

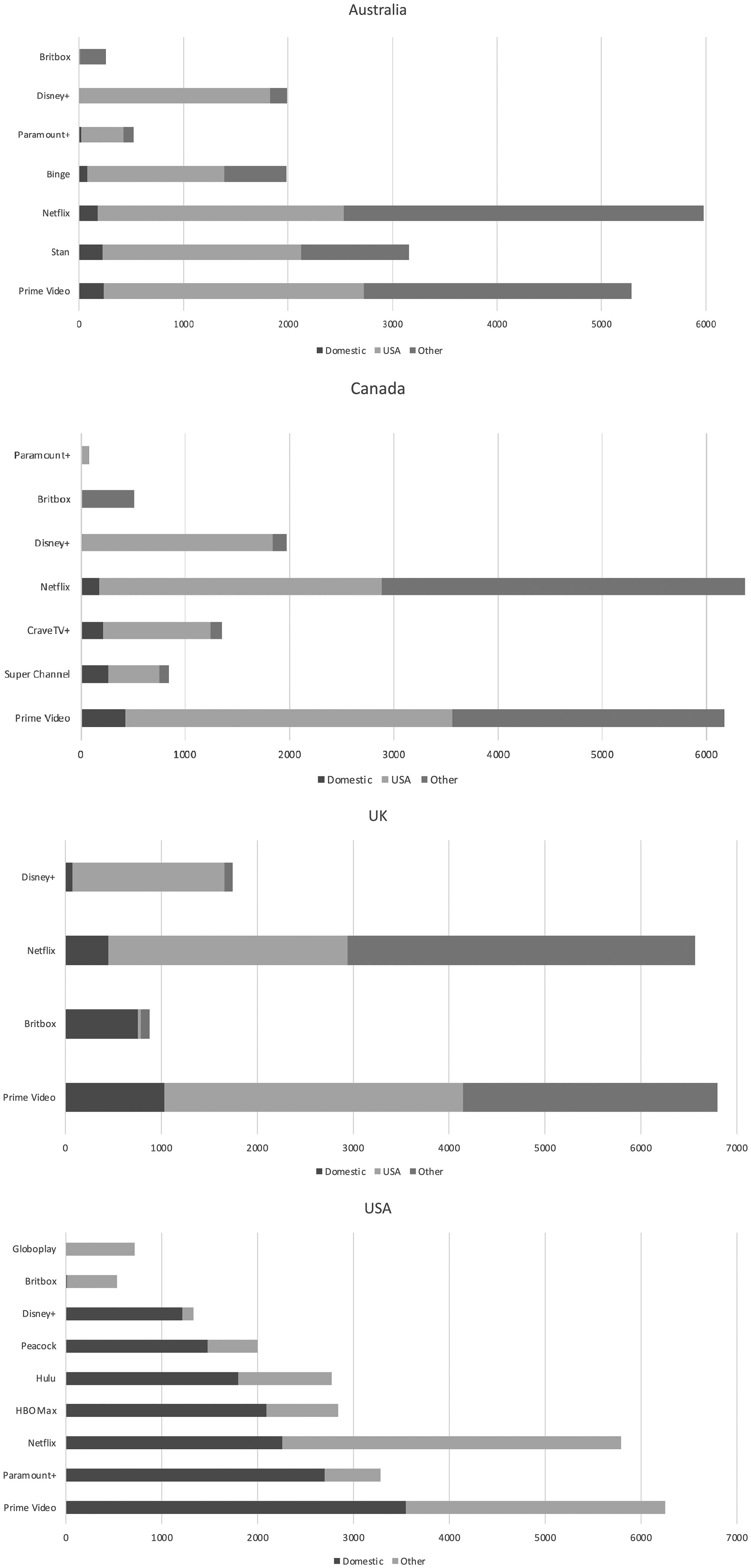

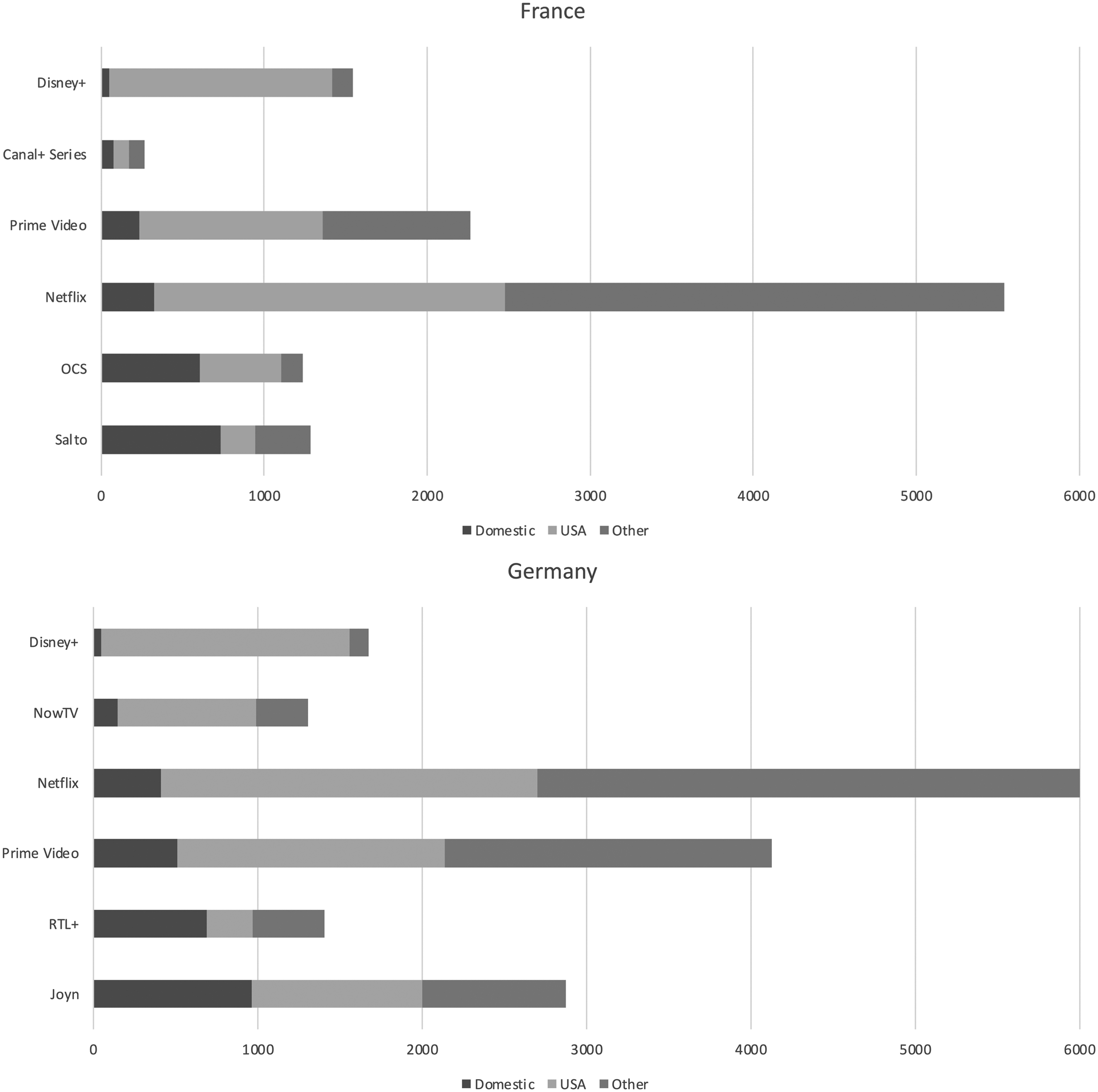

The analysis here focuses on the library composition of the major services in the market, including those from the US. The national market figures (Figures 2–7) offer insight about the nine markets as well regarding the similarities and contrasts among them.

Library composition of major services in English-dominant markets

Library composition of major services in France and Germany

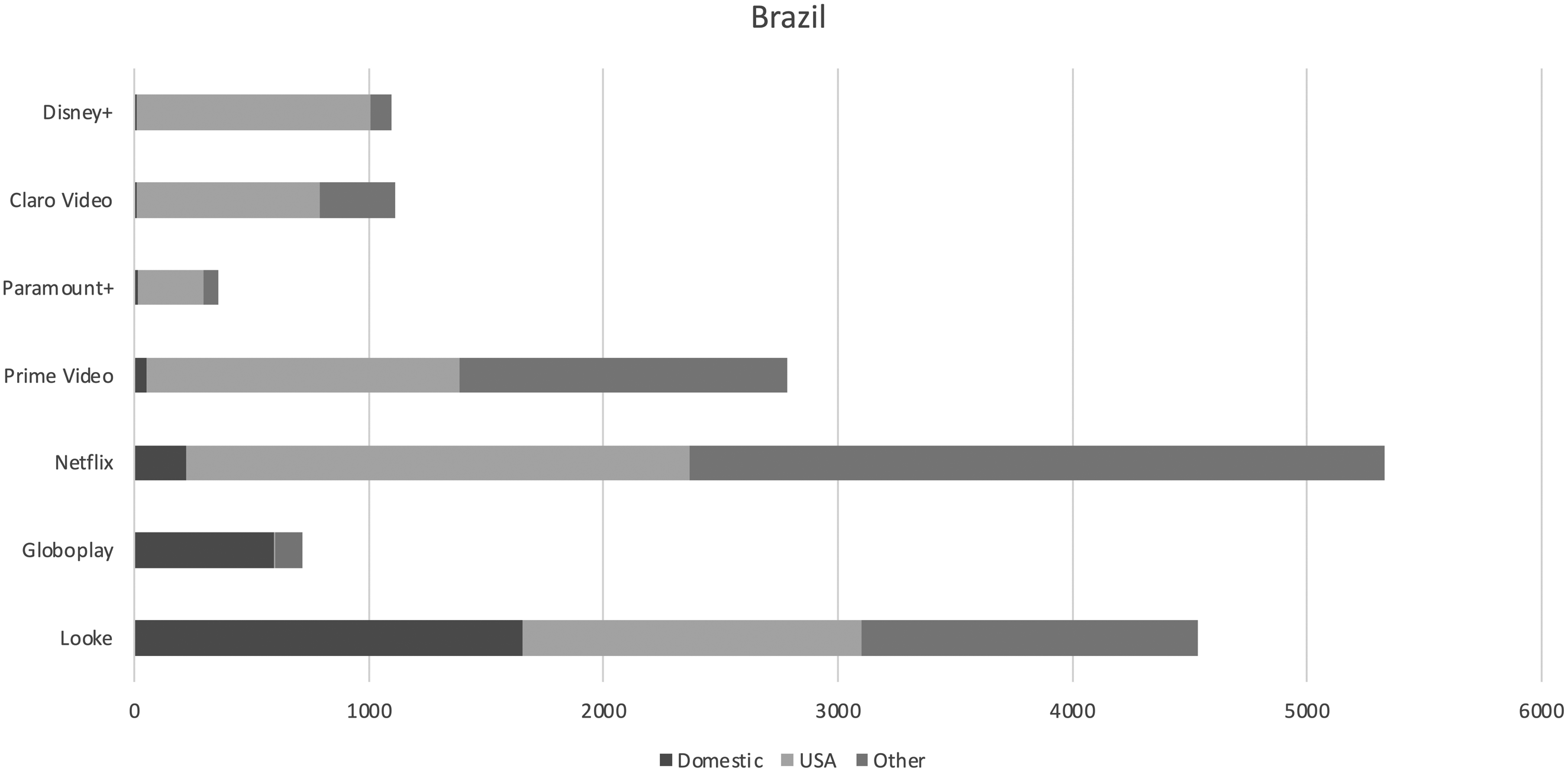

Library composition of major services in Brazil

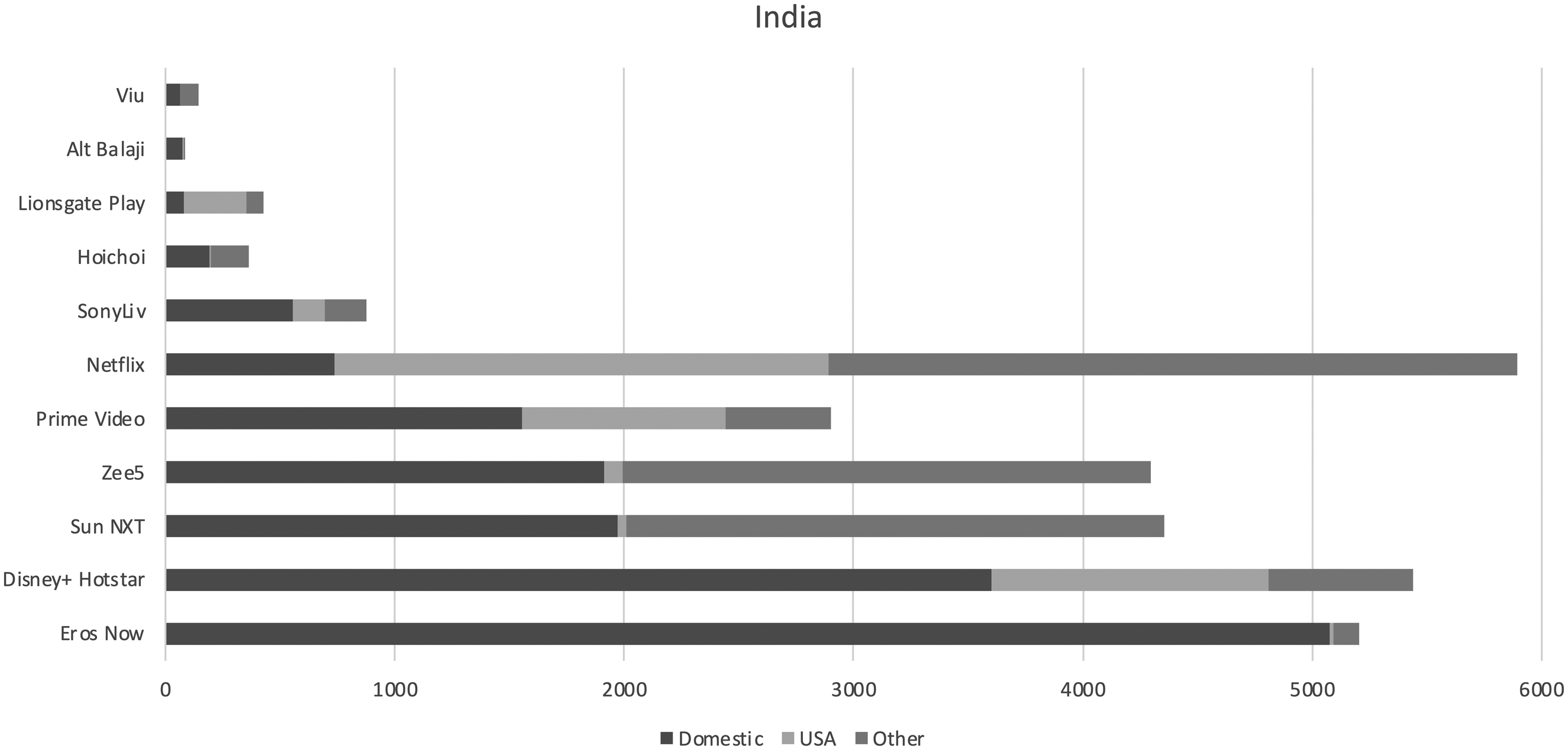

Library composition of major services in India

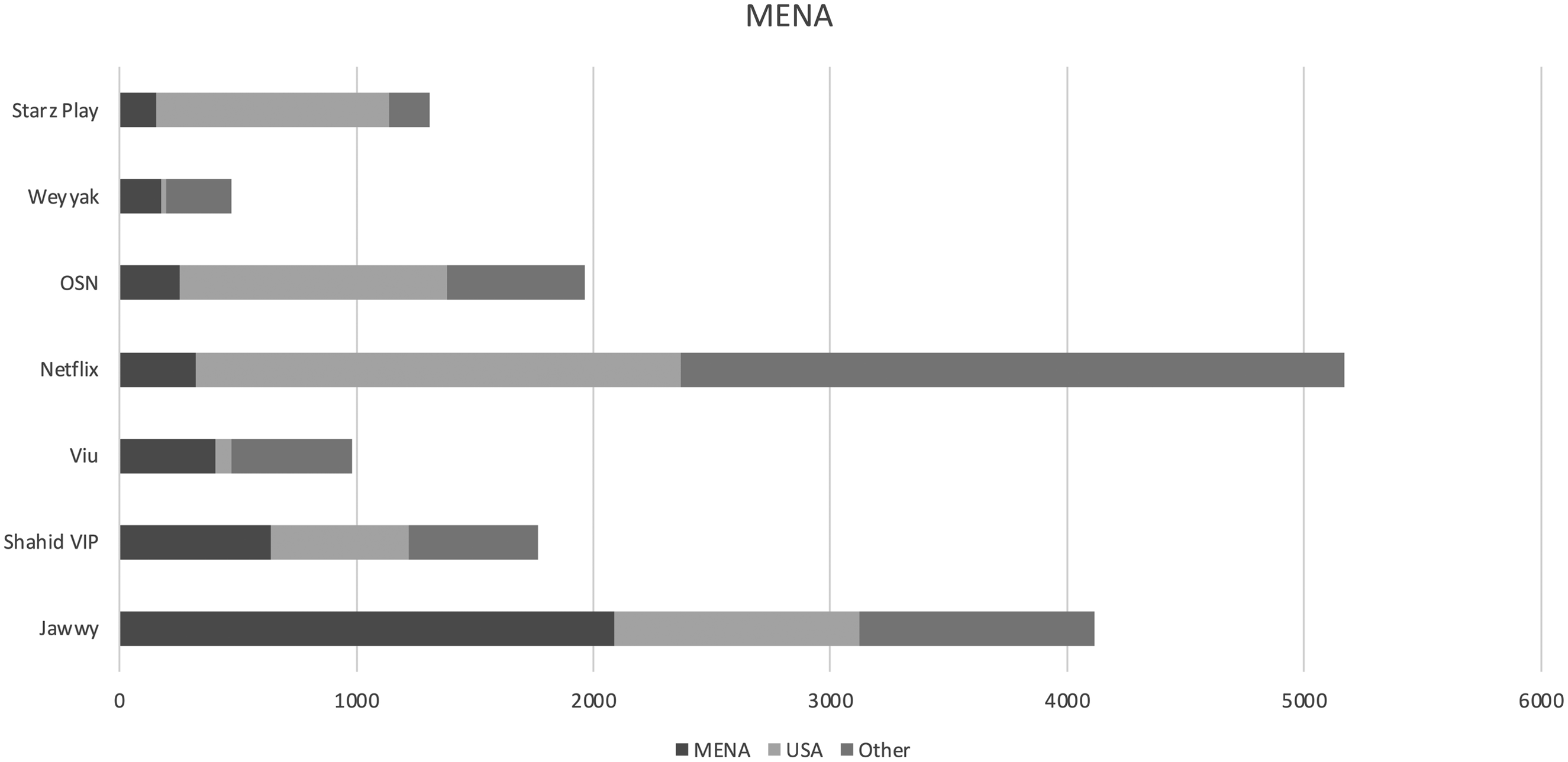

Library composition of major services in MENA

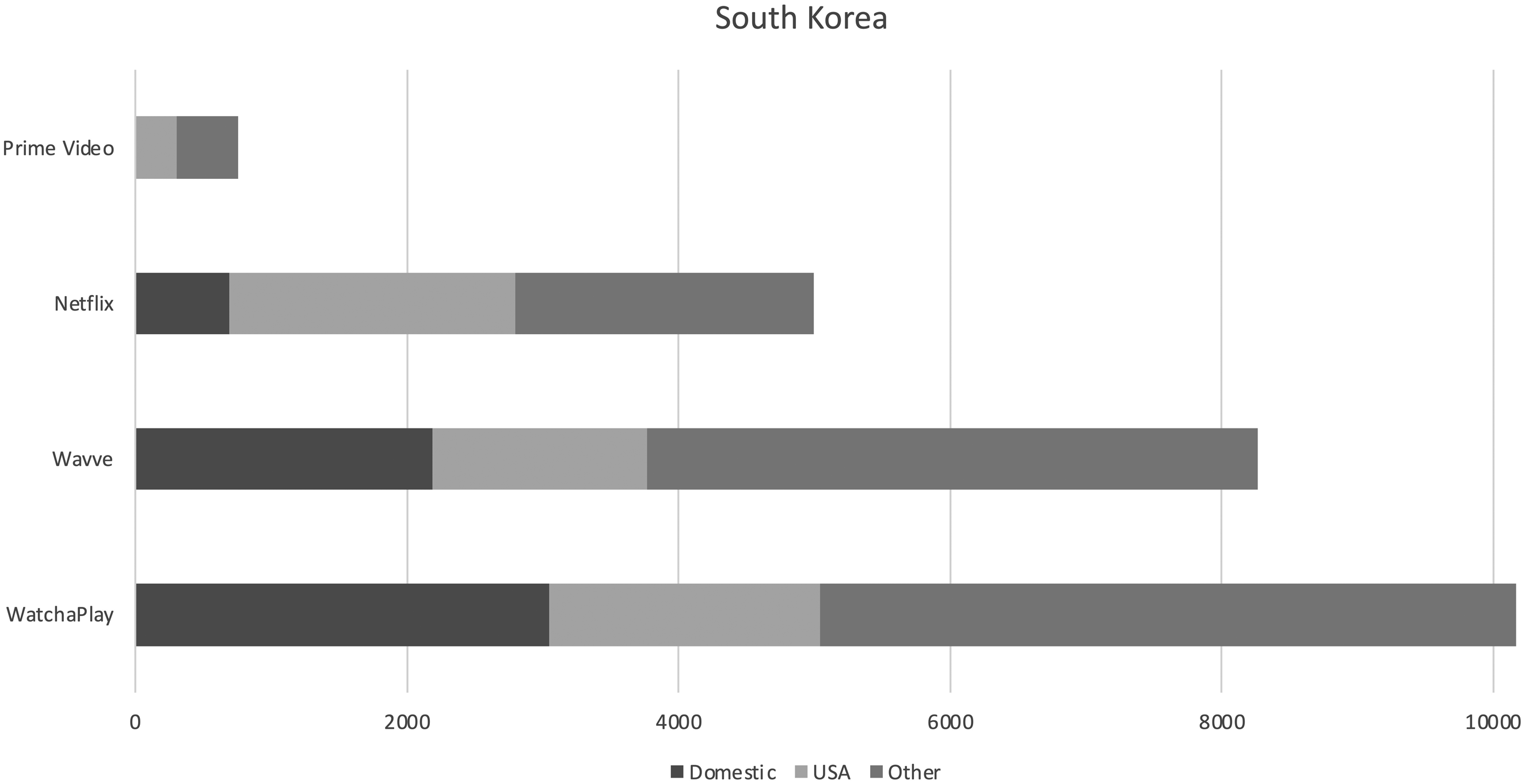

Library composition of major services in South Korea

Notably, neither Australia (population 26 million) nor Canada (38 million) has a service offering significant domestic content. As English-language dominant markets, the dominance of US-produced titles in both markets likely explains the strong adoption of services despite this lack. In contrast, the UK's Britbox service offers nearly all UK-produced titles, and the US-based services offer more titles produced in the UK (population 67 million) than elsewhere (although separate analysis is required to assess the extent to which those titles should be regarded as particularly British). Britbox subscription is quite low, subscribed to in fewer than 6% of UK households according to the 2022 Ofcom Media Nations report. Instead, US-based services dominate adoption and use in these markets. The UK, Australia, and Canada do have AVOD with deeper libraries of domestic titles that might provide a level of domestic service satisfactory in these markets. Of course, the new domestic content on these AVOD services derives from domestic linear channels that increasingly struggle to attract audiences sizeable enough to cover the costs of commissioning drama and comedy – at least in countries with smaller markets (see Potter and Lotz, 2022).

All three English-language dominant markets have a service from a legacy multichannel service provider (Binge, Crave+, and NowTV). The strategy across these services is similar: offer a lower cost version of the existing multichannel service aimed at expanding the reach of the company. In all three markets, these services currently derive significant value as the exclusive access to HBO programming – a distinction questionable in the future as Warner Bros./Discovery expands the international footprint of its Max service. Paradoxically, the loss of exclusive and distinctive US content, if these exclusive HBO deals end, may weaken these services’ capacity to fund and commission domestic content.

The non-English-dominant markets are all a little bit different. Domestic services consistently offer more domestic titles than the domestic services in English-dominant countries that rely heavily on US-produced content instead. Much of the variation among markets such as Brazil, France, Germany, India, MENA, and South Korea is due to the pre-digital norms and the corresponding variation in strategic opportunities they provide.

European markets such as France and Germany have been strong adopters of the US-based services. Both countries have introduced local content expectations on foreign streamers that are among the most stringent in Europe, and the French services feature a considerable percentage of French titles. Generally, the market composition and service balance in the countries is quite similar. Despite having domestic services with higher levels of domestic content, Ampere data suggest the US-based streamers attract more subscribers. Of course, this might be a matter of complementarity, such that linear services (and their on-demand extensions) offer adequate domestic content and the streamers are sought based on the US and foreign content they offer.

Brazil has long been dominated by Globo. It has many hours of content that it can offer without significant cost, and it is strongly domestic and distinctive from the US-based services available in Brazil (see Meimaridis, 2024 in this special issue). This strong domestic base has made it possible for Globoplay to launch in other countries. Though it is unlikely to be more than a niche service outside of Portuguese-speaking markets, it is an expansion with considerable potential.

Similarly, many of the Indian services are seeking subscribers abroad. The Indian market is very crowded and low priced, and, though a populous country, the low levels of wire infrastructure make streaming a primarily mobile screen phenomenon – at least until the rollout of 5G. But in addition to its expansive domestic market, India has content libraries that rival Hollywood, and distinctive audiovisual content popular with a broad diaspora and fans globally. The libraries of Indian services are strongly domestic, and although Netflix takes 20% of the revenue from subscriber-funded streaming in the market (due to high price), it does not rank in the five most-viewed services according to Media Partners Asia (2022). The absence of Netflix from top use is a global rarity; instead, domestic services dominate the market (admittedly, now-Disney-owned, Hotstar is challenging to properly categorize but the composition of its library illustrates its difference from the Disney+ service common elsewhere). Many of the India-based services are looking to find a balance of domestic and international subscribers. Of course, India is a single country, but the diversity of languages supports a multifaceted streaming sector specializing in different languages enabling more regional opportunities (Hoichoi's Bengali focus, for example). Tiwary (2024, this volume) also notes how important streaming services have been for diversifying the perception of Indian film from beyond Hindi cinema and Bollywood.

MENA has similar structuring dynamics. 15 Like India, it was a strongly ad-supported sector before streaming, so the challenges of converting consumers to paying for content has limited the market. Also, like India, the MENA market was not historically as strongly saturated with US content. The weaker Western pull has made it a target for non-US, multi-territory services such as Viu, with its substantial Korean drama library, and Indian company Zee has launched a streaming service called Weyyak in the region that offers Indian titles with Arabic dubbing.

MENA-based services OSN and ShahidVIP both offer a mix of US and regional content and are libraries of comparable size, however, their libraries are quite different in composition. OSN has nearly twice the US titles, many of which derive from a greater number of exclusive deals with US studios that have been slow to market their own services in the region. ShahidVIP has Disney titles from 2020 while OSN has Paramount, Warner Media, Sony, Discovery, MGM, and Lionsgate. OSN offers a much larger number of US titles than ShahidVIP, however, OSN has just over a third the number of regional titles that ShahidVIP provides. Shahid's greater quantity of regional titles supports the ability of the service to operate outside the region as a provider of Arabic content in other markets.

South Korea is an entirely different context. It had nearly 100% multichannel penetration of pay-TV services before streaming (cable companies that transitioned to IPTV – internet protocol TV) and has remained at those levels. In much of the world streaming has taken hold because of underlying consumer dissatisfaction with such services, but uptake has been slower in Korea in a way that suggests viewers were satisfied with the considerable choice and value IPTV offered. But the country's competitive dynamics made it difficult to develop different kinds of content beyond the romances known to do well and export strongly (see Kang, 2024 in this issue). The streaming services have helped to expand the storytelling range and illustrate viewer interest in genre dramas (Kang, 2023). Given that the market dynamics are so different, it should be unsurprising that the services are as well. In addition to the noted uncommon size of the Korean streamers’ libraries, much of the content is not exclusive. In comparing the Watcha and Wavve libraries in our data, we found 50% of Wavve titles are available on Watcha and 41% of Watcha is available on Wavve.

Conclusion

Understandings of streaming as a business, and in terms of its cultural implications, have suffered from a tendency by industry, journalists, and scholars to assume that frames used for previous video distribution technologies and businesses can simply be imposed on this sector. This impulse to presume past paradigms of operation are relevant is further exacerbated by a tendency to conflate all streaming services as sharing a common mode of operation when they are significantly differentiated by structuring characteristics related to geographic reach, library specificity, library ownership, and corporate purpose (Lotz, 2022), and of course revenue model and mechanism for paying for content (existing ownership, licensing, revenue share) are also foundational dynamics. Finally, the propensity to project norms of the US marketplace on other countries further impoverishes the ability to look at the complex and varied relationships among services in other contexts. All of these industrial factors intersect with vastly different historical video cultures, especially when moving beyond Western countries. Different national screen storytelling characteristics have prepared viewers to expect and desire content with different features and that perform a variety of socio-cultural functions.

The analysis presented here helps move beyond a US-centric frame to assess how the emergence of streaming offerings from outside the US reveals new perspectives tied to different corporate owners that in turn affect the content strategies of services. The national market analysis also reveals emerging patterns of how markets encompass an array of complementary services rather than indicating that there is a competitive field with great similarity. As the sector matures, common business processes of consolidation are likely. Analysis of how different types of companies might value streamers, and the varied value propositions streamers can offer, helps suggest how this consolidation may take place. Rather than assuming consolidation is an inherently negative development or a threat to a multiplicity of voices, an understanding of competitive dynamics helps to reveal whether having fewer services threatens to result in homogenization of service priorities or strengthens complementarity in a market to make heterogeneity sustainable. The current market conditions remain largely unsustainable and the paths to sustainability have been blocked by misguided thinking tied to business norms of linear video and ad-support. The analysis here exemplifies thinking endemic to the affordances of streaming and dynamics of a pluriform audiovisual ecosystem.

By assessing both the ownership of streaming services across an array of national contexts and the features of the libraries they offer, it is possible to imagine the coming competitive dynamics. Although US-based services are likely key players in that imagined future, there is no reason to expect them to be the sole dominant force, and strategic policy aimed at addressing current and coming competitive conditions, as opposed to those built for past distribution technologies, might better ensure the achievement of cultural policy goals.

Rather than considering all streaming services as competing with all others, we might more productively consider the various paths to sustainability that exist. None of the services considered are likely to break into the tier of major multi-territory services already occupied by Netflix and Disney+. Prime Video also figures here but is complicated by its status as a corporate complement. As major multi-territory services, Netflix and Disney+ have global availability and have been adopted by a majority (more than half) of homes in multiple markets based on widely published estimates. Notably, the two services are strategically different: Disney+ remains invested in its mass-market brand that has long been produced in the US but targeted to the globe. In contrast, Netflix is a much more international service, with only 40% of its libraries’ titles produced in the US (Lotz et al., 2022). The distinction between the services may develop further as they launch tiers relying on advertising as well as subscriber payment. Here too, although they are taking the same action by introducing advertising to pure SVOD businesses, the implications may differ because of their different content strategies.

Many of the services discussed here appear aimed at developing into minor multi-territory services, which we distinguish as those global or nearly global in availability that achieve scale either through adoption by a ‘significant market’ (10–50% of homes) in multiple territories or mass adoption in one major market and niche adoption (<10% of homes) in several others. To a large extent, the ‘competition’ is to become the global Indian, Korean, Middle Eastern, etc. service that achieves dominant share in the home market from which to support a multi-territory niche offering (for example, Globoplay). To that end, the collaboration behind Wavve in the South Korean market is an interesting case. A joint venture of SK Telecom and the country's commercial broadcasters may lead to the success of a multi-territory service specializing in Korean content to an extent impossible without collaboration. Specialty services – those with very specific content such as Mubi and Crunchyroll – might also persist in a variation of this multi-territory aim; they may achieve only niche adoption anywhere but manage sustainability through lower content costs or higher subscriber fees due to the high level of passion that compels their limited subscriber base.

Opportunity for domestic/regional services remains alongside these multi-territory players. Again, the ‘competition’ is more in category and in market – a question of becoming the dominant provider of content otherwise un- or under-available, most often domestic/proximate. Based on current services in several markets, the competition looks to be a contest between the legacy multichannel-owned services and services developing from existing content owners. As Figures 2–7 illustrate, in many cases the legacy multichannel services’ businesses have been based on importing content from the US while services from existing content owners tend to be strongly domestic. Ownership may not predict outcomes; rather, market by market, the question of what consumers prioritize and what other multi-territory services offer may be determinant.

This examination prioritized subscriber-funded services (or those not purely ad-supported) in order to create continuity in terms of the business priorities the services face. It remains unclear how the range of ad-supported options in a market will affect uptake of subscriber-funded services and thus the scale such services can achieve. For example, UK consumers spend considerably on services with quite limited British content and spend little on those primarily featuring British content. This is due to the wide availability of AVOD services from major British channels as well as the substantive free offering of BBC iPlayer. Brits may find adequate domestic offerings from these ad- and publicly funded services. But the extent to which ad-funded services can afford to commission content as revenues from broadcasting diminish, particularly the expense of scripted content, also remains uncertain.

Given the domestic specificity of sport culture in much of the world, the role of sports rights adds another layer to emerging competitive dynamics. Such rights are likely most relevant to domestic/regional services or as a strategy to boost subscription in a particular territory. Much depends on the parochiality of a sport and the multiplicity of sports in the market, of course relative to market size and wealth.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Australian Research Council, (grant number DP190100978).

Notes

Authors' biographies

Amanda D Lotz is a professor and leads the Transforming Media Industries research program in the Digital Media Research Centre at Queensland University of Technology.

Oliver Eklund completed his PhD at the Digital Media Research Centre at Queensland University of Technology.