Abstract

This article explores how the relationship between crime and property values is reshaped by the transformation of houses into investible assets. Departing from neoclassical economics of crime, we introduce the notion of “capitalization of crime” to illustrate how crime is utilized to generate forward-looking financial expectations and shape housing markets in gentrifying neighborhoods. The study, based in Haifa, Israel, combines quantitative and qualitative data to demonstrate how investors and renters each play a role in constructing the value of crime by capitalizing crime in opposite directions. First, using a geographic information system to map crime alongside real-estate prices, we show that the effect of crime on property values is offset by prospects of future gentrification, thereby contributing to housing speculation. Second, using digital ethnography, we show how renters use “crime” to dampen investor expectations, reduce rents, and delay their displacement. Thus, our study adds to the established body of critical criminology, which examines the manipulation of crime for economic and political gains. It further contributes to emergent debates in urban criminology by explicating how the financialization of rental housing is remaking urban politics of crime and criminalization.

This article presents insights from an ethnographic study of crime and property values. It demonstrates how crime is used to shape the housing market by differentially positioned social actors. Rather than treating the market as an impartial arbiter among individual preferences, which simply reveals “the cost of crime” (Domínguez and Raphael, 2015), our study shows how crime is strategically and actively capitalized. We argue that under conditions of asset price inflation, which exacerbate inequality and infuse social life with financial norms and rationalities, crime is financialized through the construction of forward-looking expectations of the effects it will have on property values.

Attempts to estimate the impact of crime on property values have become pervasive, as part of the broader neoliberal campaign to make law enforcement amenable to cost–benefit calculations (Anderson, 2021). The idea undergirding this effort is to assert the value of crime reduction in measurable, seemingly objective, and hence uncontestable terms. Yet, despite innumerable improbable presuppositions embedded in microeconomic models, and the use of increasingly advanced statistical methods, the price of crime remains intractable, if not impossible, to measure. This, we argue, is not simply because crime imposes endless intangible costs, which are beyond economic calculation—a proposition most economists will easily accept. Rather, it results from the conflictual and performative nature of valuation through the social process of capitalization.

Technically, capitalization is a conventional mode of pricing assets based on their expected future earnings. Although the principle is probably as old as capitalism itself, the formula of capitalization was significantly formalized and popularized in recent decades—including through the financialization of housing (Aalbers, 2019; Levy, 2017). Today, not only is it used by accountants, financiers, and investors to aggregate, trade, and compare diverse types of assets, but it also informs everyday decisions, as a kind of rule-of-thumb in economic matters. We capitalize every time we try to determine whether to invest in anything now by estimating the value it will have for others later. We capitalize every time we try to decide how to act, based on our ideas and expectations of how the future will or will not be like the past or the present. Capitalization thus involves both speculative and specular dimensions: not only an attempt to anticipate the uncertain, but also to gauge what others anticipate, and how their anticipations will inform their actions (Bichler and Nitzan, 2009; Dupuy, 2014).

Our thesis, indicated in the title “the capitalization of crime”, suggests that in the city of real estate—where houses are popular investible assets— “crime” is harnessed to produce forward-looking expectations that shape property values. Drawing both on the technical meaning of capitalization, as the present value of future income, and on the colloquial sense of capitalizing on something to turn it into one's advantage, we aim to show how “crime” is reshaped by the financialization of housing. Through a grounded case study, we argue that the capitalization of crime happens in two primary ways that are intimately related. On the one hand, with the rise of real-estate as a central site of popularized investment, high levels of crime can persist alongside rising costs of houses, since anticipated neighborhood transformations are figured into current values. On the other hand, and as a result, crime is also used to challenge rent extraction, by serving as an indication of the growing disparity between rising prices and “real” neighborhood value. In the contemporary city, we thus claim, “crime” is used to generate, justify, and criticize the price of housing.

In making this argument, we draw inspiration from critical criminological and sociological investigations that highlighted the use and abuse of “crime” to achieve various economic and political ends—primarily to galvanize broad-based support for neoliberal transformations. Numerous studies have shown how crime is used to facilitate the expansion of political repression against oppositional movements and organized labor (Hall et al., 1975), legitimate administrative undemocratic security measures (Simon, 2009), and expand racist incarceration in an age of declining social welfare (Alexander, 2012; Wacquant, 2009). In the urban context, research has demonstrated how crime is used to justify housing segregation (Atkinson and Millington, 2019), dismantle public housing (Disney et al., 2020), and further gentrification (Golash-Boza and Oh, 2021). In all these cases, “crime” is a pretext for achieving other ends; a discursive construction that both occludes and expresses the fundamentally unequal nature of social relations. We build on this critical tradition to claim that, in the era of house price inflation, rising inequality, and shifting ideologies of valuation, “crime” is used to negotiate real-estate prices through participating in the construction of neighborhood value.

As endless studies have shown, and as most urban residents understand, gentrification involves the displacement of poor, often racialized residents, and their replacement by middle-class newcomers, resulting from and leading to property value appreciations (Freeman, 2016; Stein, 2019). Thus, gentrification is conventionally enacted as part of the future-oriented logic of contemporary urban management, which only invests public funds in creating opportunities for private accumulation (Weber, 2021). This has massive implications not only on patterns of police repression, but also on how and to what ends law enforcement services are distributed to different neighborhoods. In this article, we are primarily concerned with the way in which gentrification is predicated and generated through the strategic use of “crime” to produce narratives and images of neighborhood transformation: not only by urban elites and decision-makers, but also by affected residents. Here, we extend works in cultural criminology, which relate how stories, images, perceptions, and sentiments surrounding crime and unsafety impact and legitimate the distribution of harms across neighborhoods (Peršak and Ronco, 2021; Wacquant et al., 2014) In our case, cultural knowledge of gentrification constructs crime in the forward-looking idiom of capitalization.

Our study also builds and extends urban criminology's concern with housing systems (Atkinson and Millington, 2019) and gentrification, by focusing on the politics of crime that ensue between investors and renters. Criminology has done much to explicate the relationship between revanchist “governing through crime” (Simon 2009) interlaced with the rise of mass homeownership since the mid-20th century. Yet, one important phenomenon of our era is the reversal of this trend and the emergence of new social antagonisms between renters and rentiers (Risager, 2021; SJ Smith et al., 2022). This relationship stands at the heart of our article.

Our ethnographic setting is Hadar HaCarmel (henceforth: Hadar), a neighborhood in Haifa, Israel. Hadar has been primed for gentrification for over two decades, with local policymakers actively seeking to attract private investment and more affluent residents to this disinvested area. Here, as in many other places, gentrification was promoted by inducing the market to capitalize—that is, price in advance—forthcoming transformations. Yet, things did not turn out quite as planned. Instead of attracting homeowners, from 2008, Hadar became a popular site for real-estate investors (Or, 2020). In the context of rising house prices everywhere in Israel, gentrification creates pool of safe renters and continuously creates appreciation potential. However, residents complain that rising property values and rents are “out of touch” with the actual neighborhood situation—pointing to rising levels of crime and unsafety to highlight the difference between high price and low neighborhood value.

The article begins by laying out conceptual signposts that guide our investigation. We then explain our use of mixed methods. Following a short exposition of Hadar, we present our story in two acts. First, we present a series of maps we created using data on reported crime and property values, between 2016 and 2021. According to this data, property values in some parts of Hadar that are undergoing gentrification, rose dramatically despite of persistently high levels of reported offending. Contextualizing this finding, we contend that rising prices capitalize anticipated crime reductions through displacement and gentrification. However, in the next section, we show how the discrepancy between rising prices and growing insecurity—as well as veritable fears of displacement—compel Hadar's millennial renters to “capitalize on crime” to depress the cost of housing. We show how renters use social media to sensationalize crime in the neighborhood, contest the rising cost of housing within ongoing disadvantage, and dampen investors’ projections through collective action. These antagonistic strategies of capitalization demonstrate how the proliferation of financial rationalities creates a new politics of criminalization in a city increasingly dominated by the logic of assets.

Theoretical framework

A growing body of research, conducted by economists and criminologists of neoliberal persuasions, seeks to measure the cost of crime through its impact on property values. Originally derived from Gary Becker's classical “economics of crime” essay (Becker, 1968), the initial purpose was to discover the “implicit cost” of crime to make it amenable for business-like management (Rizzo, 1979; Thaler, 1978). Grounded in neoclassical value theory, which centers utility or “preference”, this science begins from the assumption that property values reflect, among many characteristics and amenities, also a certain “crime premium”, what people are willing to pay for safety. Then, algebraically setting up completely competitive markets, where numerous individuals maximize pleasure, economists use a method called hedonic regression to isolate crime's value as an externality (Ceccato and Wilhelmsson, 2020; Ihlanfeldt and Mayock, 2010; Tita et al., 2006). Anyone familiar with neoclassical economics will not be surprised to learn that the operation is circular (Robinson, 2021): First, housing prices are used to “reveal” crime, then crime is used to explain differences in property values. The ideological uptake is clear, however. To ensure the “efficient allocation” of law enforcement and public services to defend and appreciate property values “maximizes value” for cities and taxpayers (Risager, 2022).

Given the abstract nature of econometric models and the messy nature of the world, it is unsurprising that empirical studies of the crime–property relation point in many different directions. Some indicate crime reduces property values by significant extents, whereas others find no such effect, or identify it only with regards to specific offenses (Kirk and Laub, 2010; MacDonald and Stokes, 2020). Economists provide many possible explanations of such inconsistencies, methodological as well as theoretical. They also caution against exogenous intervening factors and mistaking correlation with causality (Maximino et al., 2014). They maintain, however, that the fear of crime is a (negative) externality that can be accurately measured and priced, and thereby objectively valued.

A highly questionable proposition by itself, the problem of pricing crime is centuated by the fact that houses are assets, namely vehicles of capital accumulation. If the complications of capital theory could be safety ignored by the economists of crime in the 1970s (Hilber, 2017), when the financialization of housing was only in its inception, such an omission can hardly be sustained today, when houses are increasingly conceived as popular vehicles of investment.

Since the global financial crisis in 2008, and then in the wake of the COVID-19 pandemic, central banks throughout the world have declared notoriously low interest rates. Expansionary monetary policies in an environment unhospitable to productive investments and of stagnant wages sent many investors, big and small, to put their money in residential real estate (Ucoglu, 2021). The transformation of homes into investible assets increases the penetration of financial technologies, norms, modes of reasoning and justification into the everyday life of the urban fabric (Aalbers, 2019; Robin, 2022; Rutland, 2010; Wagner, 2021).

Among other things, the rise of household real-estate investment changes how houses are socially valued. As an investible asset, the price of a house does not represent the utility of housing services (even if utility, a metaphysical notion, could be priced in the first place). Rather, it represents the current value of future incomes the property is expected to generate from rents. This idea is encapsulated in the popular formula of capitalization, used to value assets based on their expected pecuniary yields, above the rate of interest, and adjusted for risk and duration. A variety of online experts, investment consultants, and YouTube channels proliferate the basic rules of capitalization to household investors interested in evaluating potential properties based on their projected yields or “cap rates”. Calculating potential future profits is also facilitated by the growing availability of data on real-estate transactions, which helps investors extrapolate into the future based on past trends.

Because houses are a main instrument of saving and accumulation, homebuyers—whatever they personally prefer—are governed by the constant effort to predict price trajectories and anticipate trends in “the market” in general. And, arguably, since everyone is simply making decisions by trying to anticipate what others will demand, patterns of self-organization—like hype or panic—are as prevalent in the housing market as they are in the stock exchange. Thus, what people believe and expect about the future trajectory of a specific neighborhood is sometimes more Important than what is actually the case.

In addition to changing how houses, neighborhoods, and cities are valued, the financialization of housing is reinforcing massive social disparities. For while some households can use their savings or draw on loans to augment their wages with rents or “passive earnings”, others, without access to financial markets or inherited wealth, find it increasingly difficult to enter the housing market altogether. Thus, the transformation of homes into investible assets is reinforcing historical inequalities of wealth among dominant and subaltern sectors—marked by status, ethnicity, and race—and may be creating new social antagonisms between generations: property-owning baby-boomers and property-less millennials (Adkins et al., 2020). Recent empirical studies show that, for the first time since the mid-20th century, homeownership in the West is in decline relative to renting (SJ Smith et al., 2022).

Housing systems and the politics of crime and criminalization are intimately related (Atkinson and Millington, 2019). Over the past several decades, criminologists have done much to explicate the relationship between the rise of mass homeownership—the housing regime designed to substitute for the dismantled welfare state—and the politics of criminalization (Disney et al., 2020; Gregory, 2016). We know that the rise of mass homeownership not only relied on the claim that public housing is criminogenic, but also created the so-called “silent majority” supporting revanchist law-and-order campaigns (Garland, 2002; Simon, 2009; Wacquant, 2008). The rising middle classes, who became property owners through governmental policies of subsidizing credit, could be easily swayed to support “order policing” and displacement to defend and appreciate their property values (Beck, 2020; Beck and Goldstein, 2018). Nowhere is this more evident than in processes of gentrification, where, as endless studies documented, new middle-class residents take an active role in criminalizing and thereby displacing their poor, typically racialized, neighbors (Golash-Boza and Oh, 2021; Kellogg, 2015).

Although the adverse effects of gentrification are well documented, it is conventionally embraced as a blueprint for redevelopment by cities contending with neoliberal austerity (Freeman, 2016; Kallin, 2021; Risager, 2022). The conscious effort to gentrify neighborhoods to “solve,” or rather displace, crime and other social problems to other jurisdictions or marginal neighborhoods has been dubbed “institutional gentrification” (Freeman, 2016). Institutional gentrification thrives on the premise that crime rates and property values are inversely correlated; where crime rises property values drop and vice versa. Although criminologists have long doubted this simplistic premise, describing multiple ways in which crime and property values may be related in different contexts and situations (Kirk and Laub, 2010; MacDonald and Stokes, 2020; Skogan, 1986), the belief remains pervasive and guides urban policy in many locations.

This belief persists arguably because contemporary urban governance is increasingly shaped by financialized logics of futurity to order, govern, and compete over affluent residents and investments. This mode of future-oriented governance depends on conventional narratives that help solicit, shape, and nudge “the market” into action (Weber, 2021). One such narrative is gentrification. Indeed, more than 50 years after being coined by sociologist Ruth Glass, the term “gentrification” has become a household concept (Stein, 2019). The notion, though still debates, broadly represents re-investment in the housing stock, improved local amenities and, crucially, the displacement and replacement of local population. A conventional template for harvesting “rent-gaps” (N Smith, 1979)—which residents, homeowners, planners, and policymakers anticipate—the prospect of gentrification can be used to predict, and profit from, forthcoming urban transformations. It is widely recognized today, including by mainstream economists, that the capitalization of future neighborhood changes begins as soon as plans are “in the money”; that is, on the table (Carrillo and Yezer, 2022; Hilber, 2017).

Methodology

Most studies that investigate the relationship between crime and property values rely solely on quantitative data—police-recorded offenses and real-estate transactions. Researchers often admit the limited and distorted nature of reported crime data, resulting from well-known disparities in reporting patterns, and the proactive “crime-producing” nature of police work (Buil-Gil et al., 2021; Skogan, 1974). Yet, in the absence of alternative measures, such data is nevertheless presented.

Although both crime patterns and real-estate market trends can be shaped by many contextual and institutional factors (e.g., interest rates and inflation, unemployment, demographic trends), most quantitative studies bracket historical, local, and macro-economic processes affecting the studied neighborhoods. Thus, they cannot go beyond hypothesizing, in a completely theoretical manner, why crime and property values do or do not move together, and under what circumstances a correlation could be expected. Qualitative and ethnographic studies of crime and property values fare much better in theorizing the institutional relationship between crime and property values, especially during gentrification. However, because researchers are justifiably reluctant to use biased crime data, most studies omit discussions of data altogether. By this omission, they abandon the task of taking up ideology on its own grounds.

The growing availability of data on real-estate prices and sales—once only available to real-estate brokers and professional investors—is facilitating the rise of ordinary household investors by democratizing valuation. It makes both potential sellers and potential buyers aware of how “the market” values their neighborhood and its future trajectory, whether it is over-hyped or still has appreciation potential. In 2010, Israeli Tax Authority gave online public access to a unified repository of governmental real-estate data. The online database provides information on all transactions by address, a rich source of information for investors, policymakers, the press, commercial lenders, and online brokerage services. Taking this into consideration, in this study, we do not take data at face value, nor do we ignore its social power. Instead, we combine quantitative and qualitative methods to unearth how the relationship between crime and property values is produced, interpreted, negotiated, and challenged.

At the outset of our study, we used the geographic information system (GIS) to map local reported crime patterns and property transactions, to get a sense of how they may or may not be moving in tandem. This was done in two steps:

Conventional “crime mapping.” We used a police open database for 2016−2021, which includes offense subcategories at statistical area (census tract) level. Mapping property transactions and values. Using Tax Authority data on property sales, we examined temporal and spatial trends in real-estate values. This dataset covers the years 1998−2022 and includes specific details about the properties and their full addresses. We focused on the 5-year period corresponding to our crime data and aggregated the sales to the scale of statistical area.

Unlike crime figures, which are notoriously problematic, property values seem to reflect the objective forces of supply and demand and cover all pertinent events (sales). Yet, as we shall see in detail, property values are not simply a measure of a historical state of affairs. Instead, they exert performative power. Because asset prices translate future expectations into current values, they express collective beliefs about the likelihood and the gains to be made from neighborhood redevelopment, and these in turn inform individual choices and behaviors. Actors do not only respond passively to market signals, however. Rather, as we shall see in detail, differentially situated actors seek to shape future prices in their favor. Here the value of “crime” becomes central.

To capture the social life of crime and property values, how they become entangled at the neighborhood level, our study observes debates on housing prices and crime taking place on neighborhood social media venues. We monitored three neighborhood Facebook groups, each with a few thousand members, for six consecutive months, between October 2021 and July 2022. We also sampled two neighborhood WhatsApp groups, each including several dozen members. Virtual communities are not a representative sample of the local population. They overrepresent residents comfortable with online conversations in Hebrew, namely, young, Jewish, educated middle-class residents, rather than Arab and Russian speakers, the poor, elders, and migrants. Thus, online groups mostly provide a view into class and generational dynamics among different segments of the urban gentry.

Hadar as an investment destination

Over little more than a decade, real estate emerged as one of the main topics on Israeli public agenda (Ansenberg, 2022). Between 2008 and 2021, property values rose by 125%. As elsewhere, the trend was driven by lower interest rates and few investment alternatives, combined with tight supply of land, demographic pressures, and expectations of further asset price inflation (Ministry of Finance, 2022). The trend is most apparent in Tel Aviv, Israel's commercial and financial center, notable for being “the most expensive city in the world” (The Economist, 2021), but also expands outwards—including to the northern city of Haifa, where housing prices are two to three times lower than the Tel Aviv average.

Hadar, the neighborhood that concerns us here, is Haifa's old city center. The neighborhood was established in the 1920s by Jewish entrepreneurs and agencies in the context of Zionist colonization but lost about half of its population by 1970. In the 1980s, while ultra-orthodox Jews and Palestinian Arabs began moving into the area, Hadar was identified by geographers and planners as one of few neighborhoods in Israel exhibiting incipient signs of gentrification, because some bohemian, white-collar middle-class residents settled there (Amir and Carmon, 1996). Hadar also saw its fair share of housing speculation, most notably during the 1990s mass migration from the former USSR, which occasioned an unprecedented rise in rents and property values (Amir and Carmon, 1996). Today, Hadar is home to over 40,000 residents, many of whom are low-income Jews, Arabs, and migrant workers. It is one of the poorest neighborhoods in Haifa and suffers many typical harms resulting from spatial segregation: urban blight, lack of public services, and prevalent illicit activities and shady establishments, such as gambling, brothels, and “drug stations.”

With its architecturally pleasing housing stock and dense urban pattern, Hadar was primed for gentrification since the early 2000s. The reconstitution of “personal safety” was, and remains, central to this effort. In 2000, the mayor established a special commission, which included policemen and social workers, to devise a plan for renewing the neighborhood. Drawing on theories of social disorganization, the commission recommended strengthening Hadar through community development. In 2005, a survey carried out by the newly established Neighborhood Administration found that personal safety was the number one problem troubling residents and blocking redevelopment. Given budgetary constraints, the municipality adopted two strategies. First, it raised the profile of the neighborhood and improved collective agency by encouraging university students and various Zionist “missions” to settle in the neighborhood (Yebelberg and Komemi, 2016). Second, it sought to direct limited “strategic” public investments to specific areas in the hope of spurring private investment.

The hope of attracting “young families”—the desired gentry—did not make much headway, however, due to a combination of factors: Haifa's weak job market; its association with postindustrial environmental degradation; the neighborhood's steep terrain, limited parking, and high volume of transportation; and the preference of middle-class Israelis for suburban housing, ethno-national and class segregation. Whatever the case, Hadar's fortunes began to change after the financial crisis in 2008, as monetary expansion drove many investors to purchase apartments in the neighborhood. By 2012, the ratio of resident-homeowners to renters in Hadar was 44% to 56%, a dramatic sociological fact, given that some 70% of Israelis live in their own houses (Swirski and Hoffman-Dishon, 2016).

Hadar is attractive to investors because of the high yields it generates and its appreciation potential. Yields or “cap rates” are calculated by dividing the property's expected “cash flow”—anticipated income from rent minus expenses—by the property's total asset value. This means that places where property values are relatively low, compared with the rents they can generate, produce higher returns on investment, especially where appreciation is projected. As suggested by one newspaper highlighting Hadar as an investment destination: “The goal of the investor is to rent out the apartment, get the highest possible return, and after a few years to sell it and enjoy the value appreciation. Thus, two elements are required: low real-estate prices and relatively reasonable rents.” (Or, 2021).

In Hadar, investors can collect “reasonable” rents from a relatively safe pool of new renters, who came to the neighborhood following gentrification efforts over the past two decades. Middle-class renters—students, young professionals, and bohemians, both Jews and Arabs—are attracted to Hadar's urban feel and amenities, such as coffee shops, bookshops, and public transportation. Rent, although gradually inflating, is still relatively low in city-wide and national terms. According to our estimations, rents in Hadar are about three times lower than in Tel |Aviv (2500 NIS for a two-bedroom apartment, compared with 7000 NIS). From the investors’ perspective, this new pool of renters is preferable to low-income residents who live from hand-to-mouth, without credit or even bank accounts. New middle-class renters can be counted on to pay on time, often with guarantees from their parents, thereby reducing the risk of investing in Hadar. Thus, the combination of low property values, resulting from years of urban decay and the typical proliferation of poverty and informality, combined with Hadar's brand of institutional gentrification, made the neighborhood a preferred investment destination.

Capitalizing gentrification

In 2021, Haifa became the second most preferred city for real-estate investment (Ministry of Finance, 2022). Hadar was flagged by the press as “one of the neighborhoods that made most money for investors” (Horesh, 2020, 2021). During the pandemic, spurred on by another wave of financial incentives, a host of small and larger investors bought apartments and buildings in bulk, for rental, “flipping,” or speculative purposes in the neighborhood. Offending and victimization seemed to be on the rise as well. A report published by Haifa's Department of Welfare in December 2020 alerted that, according to surveys conducted by its social workers, there had been a significant decline in residents’ feelings of personal safety. The sentiment appears to be shared by residents across sectors—among men and women, Jews, and Arabs. Residents reported fear of walking alone in the vicinity of their dwelling, as well as in the general area of the neighborhood, due to unseemly encounters with drug addicts, and with persons they recognized as criminal offenders. They also reported a fear of becoming victims of street violence— verbal, physical, sexual, and financial (Municipality of Haifa, 2021).

We used GIS to map data on crime and property values, to try and better understand their interaction. Here is what we found:

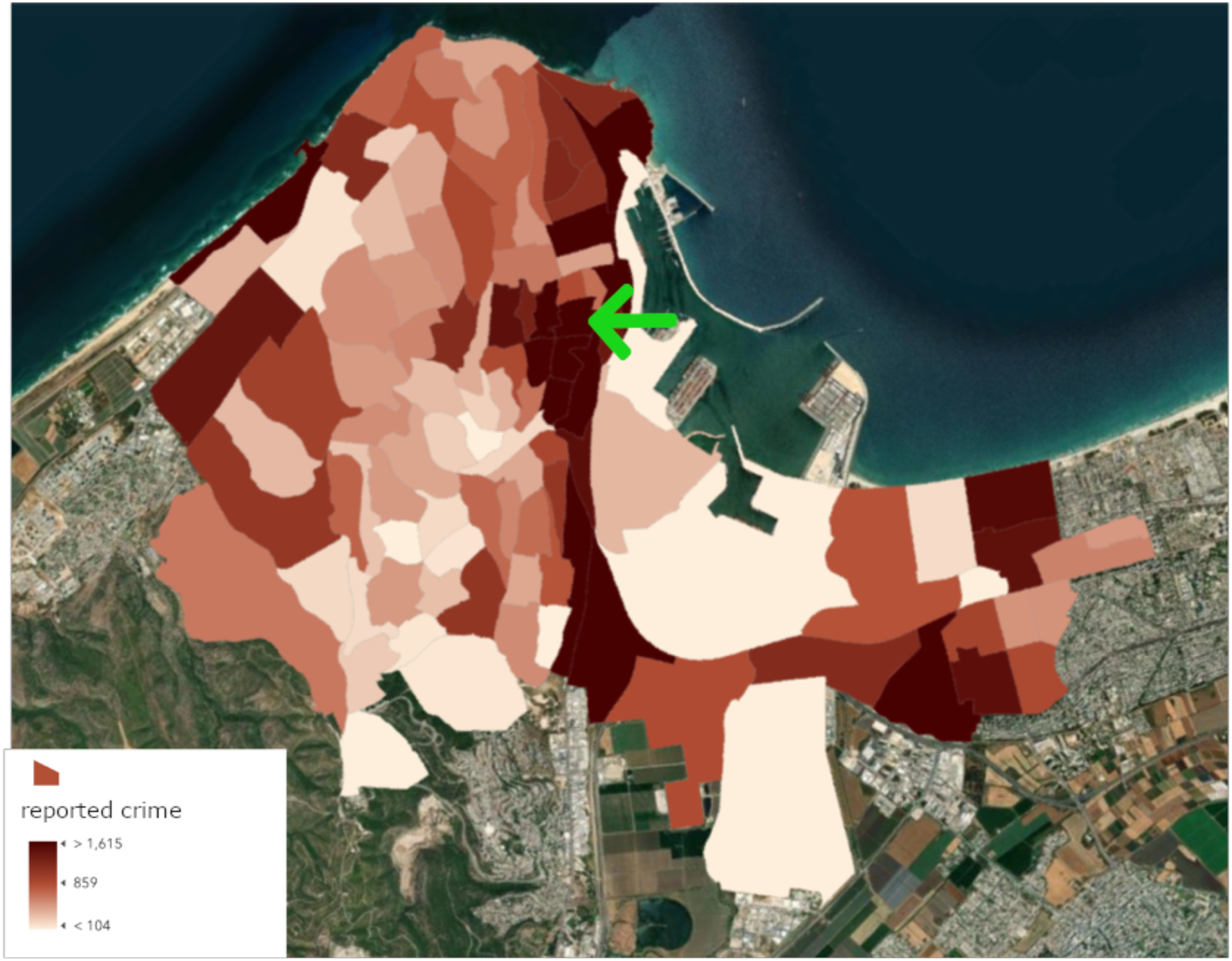

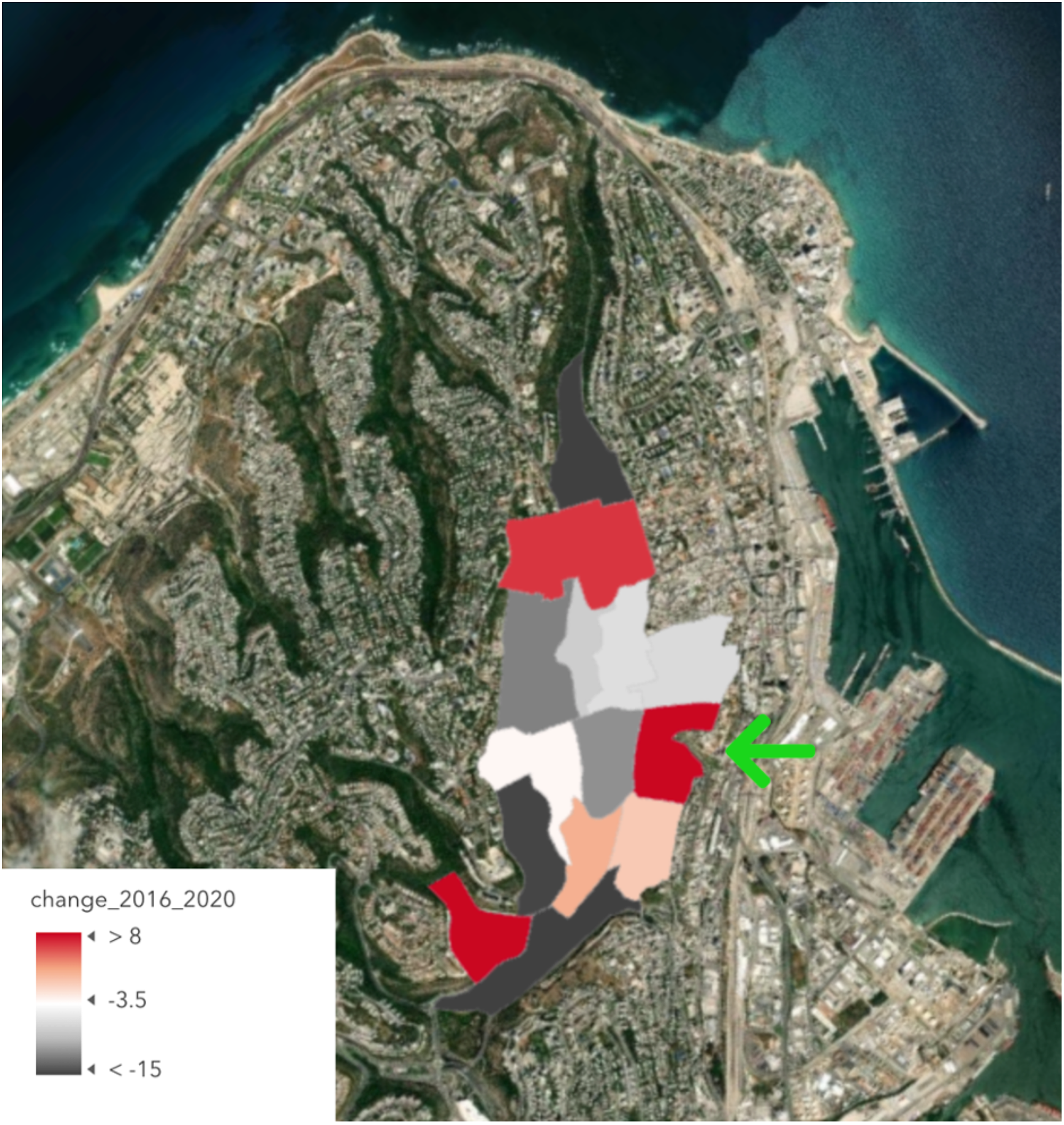

Hadar records one of the highest crime rates in the city of Haifa and is part of a broader “crime corridor” stretching south to north (Figure 1). Within Hadar, the number of recorded crimes is highest in the Talpiot Market area, in aggregate and across all subcategories, and the rate of crime is highest when normalized to population (Figure 2). Three statistical areas in Hadar saw rising property prices between 2016 and 2021: the ultra-orthodox Geula Residence Hassidic enclave, the area surrounding Baha’i Gardens, and the Talpiot Market area. Other areas saw property prices drop or stagnate. Talpiot Market recorded the highest growth in property values, of 17% (Figure 3).

The findings reveal consistently high crime rates in Hadar, relative to more affluent parts of Haifa. Property value appreciations are outstanding in some parts of the neighborhood, including Talpiot Market, which is the current site of municipal investment and hype. The market district, one of Hadar's poorest areas, was “discovered” by Tel Aviv investors circa 2016, and in 2018 was chosen by the newly elected mayor as a flagship renewal project. The plan, approved by the planning committee, involves renovating the old market hall and reviving surrounding streets with local businesses and restaurants to make it a culinary tourism attraction (Horesh, 2020). Thus far, these developments have not occasioned much crime displacement, as the figures above make evident. High levels of reported crime are correlated with rising property values.

Reported crime, city of Haifa 2016–2021. Source: Israel Police.

Reported crime, Hadar HaCarmel, 2016–2021. Source: Israel Police.

Change in property values, 2016–2021. Source: Israel Tax Administration.

Drawing on existing research (Kirk and Laub, 2010; MacDonald and Stokes, 2020), we could explain this counterintuitive, yet unexceptional, correlation of high crime rates and appreciating property values by hypothesizing that the high crime rate is an effect of gentrification. In other words, it results from the arrival of new “targets” to the area, from a higher level of reporting by new residents, and a higher police presence. All these possibilities can be sustained. However, surrounding areas, which are not undergoing gentrification, record similarly high levels of offending. Furthermore, our ethnographic surveys of the neighborhood and conversations with residents corroborate the welfare department's report cited earlier. Young and older residents of virtually all sectors complained about a rising fear of victimization in Hadar during the pandemic and thereafter.

Given Hadar's longstanding “potential” and effective neglect, we suggest that property value appreciations are driven more by expectations of gentrification than by actual changes on the ground. This is evident in real-estate adverts, directed primarily to investors, marking Talpiot as “the up and coming” area and listing high “cap rates,” of some 4% to 7%, which local apartments (particularly when “split” into smaller units) are expected to generate. Rising prices indicate that “the market” expects gentrification, meaning that higher rents will induce population displacement and compel the authorities to devote more efforts to “cleaning up the neighborhood.” In other words, both criminalization and displacement, and the inequality of local service distribution based on status and wealth, are capitalized in advance into higher property values. The municipality helps feed the hype by announcing plans for future redevelopment that are immediately capitalized into higher property values. A trend of rising prices draws more investors to the area because they indicate the market “forecasts” future appreciations. Rising prices spell more confidence in the future of the neighborhood, while also helping to bring this future about by enacting it, in value terms, now. Viewed through the lens of capitalization, it is apparent that property values do not reflect real material changes but expectations.

Recent studies on “investification” found that neighborhoods overwhelmed by private investors can produce high earnings despite growing disadvantage (Hulse and Reynolds, 2018). This situation is evident in Hadar, where most investors are private individuals, upper-middle-class households, and pensioners. Because they only own their properties, rather than live in them, they are not typically present in situ to carry out everyday functions, like cleaning and maintenance. Nor are they present to carry out neighborly surveillance, which theories like “broken windows” advocate (Wilson and Kelling, 1982). A few larger investors are active in various municipal forums, but most seem to be simply cruising on property value appreciations brought about by the cheap supply of credit, which accentuate the capitalization effects of municipal planning (Hilber, 2017). Thus, the costs of housing rise in the context of sustained disadvantage and declining sense of personal safety.

Hadar has been gentrifying for over three decades. Its “potential,” especially when fueled by municipal plans and strategies, is apparently endless. However, rising property values and rents amid persistent poverty and growing inequality, including between generations, seems to be undermining the social coalition of gentrification. This is evident through the reaction of millennial renters to rising housing costs, to which we now turn.

Capitalizing on crime

Much like municipal policymakers and investors, Hadar's millennial renters anticipate gentrification. This generation came of age after the 2008 financial crisis, which in Israel, like elsewhere, gave rise to “occupy”-style social justice mobilizations (Ansenberg, 2022) that are cognizant of how house market trends are affecting their neighborhood. However, many of them see gentrification as the way of the world, almost a force of nature, which can hardly be stopped by residents. Consider the following comment, left by one renter on a Facebook thread discussing the rising cost of housing: Investors identify potential and do everything in their power to realize it. Realtors have an interest in prices appreciating, because they make larger profits and have more work (early investors sell at a profit to new investors, who have been convinced that the place is “safe.”) So, in general, to keep the prices from rising the place must suck. No security, no sanitation, nothing […] Initiatives to make the area more habitable defeat the purpose.

Hadar renters follow commonsense in relating house prices to the actual situation or “real value” of the neighborhood. However, as prices rise beyond what seems reasonable or fair, renters turn to Facebook to sanction rental ads and challenge landlords directly. In a broadly established but completely informal manner, hundreds of millennial renters “ad-bust” any rental listing that seems overpriced, relative to the quality of the property and the perceived value of neighborhood. Any overpriced rental ad is met with dozens of raging comments and its landlords sometimes become targets of online shaming. In these ad-busting campaigns, crime is highlighted above all else as a measure of the low quality of local services and of the neighborhood's overall value.

For example, a one-bedroom apartment in Talpiot offered for 2500 NIS attracted a slew of ironic comments like “Does the price include easy access to brothels and drug stations?” or “Does the price include a premium for shots fired, rats, decay, and garbage?” as well as more straightforward complains like “The price is outrageous! The whole place is controlled by mafia families and unsafe after dark and even during the day.” One commenter wrote: “sure you want someone to finance your mortgage, but I wouldn’t live in that dingy area if you paid me.” Note how in these comments, crime is ironically treated as an amenity, as if it added some coveted quality to the apartment's value. Renters also allude to the financial notion of premium payments, as if crime was some special service. The final comment asserts renters’ refusal to service investors’ mortgage payments, which amounts to financing their own impending displacement.

In addition to contesting the price of rentals, the comments aim to warn potential investors and renters about customary prices in the area, alerting them what prices might be “out of touch with the neighborhood”. This is especially crucial from the renter's perspective because they fear Tel Aviv price expectations will overwhelm local standards: “Our neighborhood is not a safe place. Any investor posting a two-room apartment for more than 2200 shekels is a crook and his post will be targeted. People here are neither suckers nor spoiled. Hadar is not Tel Aviv.”

This is an example of how the risk of crime (“this neighborhood is unsafe”) turns into reputational risk posed by renters (to investors). It contains an implicit threat to other investors that their real-estate purchases might not yield expected returns or might be riskier than they imagined because people will be unwilling to pay the prices they expect or demand to live in a “bad neighborhood.” Other comments reflexively link price to the temporality of gentrification, saying the investors are running ahead of themselves: “shootings, drug crime and prostitution, and the police aren’t doing their work. Wait at least two years. There's no reason for the rent to go up yet.”

Renters seem to be aware that housing prices in Hadar are driven by general trends amplified by hype and speculation. This is evident in their debates on how to resist rent increases following the pandemic: “Post twice a week about shootings in the area”, one commentator suggested, whereas others posted comic memes depicting “Hadar residents enjoying the popular gameshow, Gunshots or Fireworks.” Both comments express an ironic, though clearheaded view of the role of images and reputation in making neighborhoods trendy or “bad” (Peršak and Ronco, 2021; Wacquant et al., 2014). Whether or not they are personally troubled by crime or unsafety is less important than their understanding of how images of crime and danger affect the price of housing. In this sense, their efforts to “criminalize” the neighborhood, associating it with violence and unsafety, is almost the opposite of what typically happens during gentrification. Usually, criminalization is used to defend and appreciate values, whereas here it is used to keep prices low, by spoiling Hadar's reputational value.

Renters seem to hope that news on Hadar's persistent “crime problem” would send signals to the market about the unpromising progress of gentrification, leading to lower demand for local housing. Where real-estate brokers, investment consultants, and the municipality are all actively promoting the neighborhood as teaming with “potential”, renters attempt to sensationalize crime to create counter-expectations. Furthermore, by engaging in collective action in Facebook's quasi-market space, Hadar renters are intimating their refusal to be “risk-free” or “safe” payers. Presumably, not only the risks posed by crime as such are being counter-capitalized by renters, but also their collective power to impose a conventional price as measure of the neighborhood's “real” value through “the moral authority of the (Facebook) crowd” (cf. Thompson, 1971).

The force of renter's social media activism becomes apparent through the responses it elicits from investors. Take this comment, for example: Determining what prices are “expensive” or “outrageous” without seeing, understanding, or analyzing the real-estate market is ignorant. Everything increases in value. Real-estate investors […] play an integral role in the neighborhood's “facelift” and positive transformation. Commentators [who criticize them] don’t act out of solidarity or public concern but aim to maintain or lower their rents. They don’t seem to understand they are shooting themselves in the leg. Without real-estate entrepreneurs, the area will continue to be neglected, and will remain populated by weak residents who have no influence on law enforcement and other government agencies.

Other investors are more circumspect about reputational hazards. Admitting some of the renters' complains are justified, primarily because they concern crime and unsafety, one investor implored renters not to go to the media: True, we face issues of drug stations, weapons hidden in yards, shootings, cleanliness, lighting, [security] cameras […] but bringing issues to the media will work against us. There are other ways to apply pressure, media is not necessary, it will boomerang. There are efforts to attract good population […] Negative press will keep positive and good people away.

How should we understand renters’ practice, given our understanding of gentrification and criminalization? Even though they highlight problems of neighborhood safety and appear to have aggressive opinions on crime, they are not revanchist homeowners seeking to defend their property values. On the contrary, their efforts are geared to maintaining the low cost of housing, and if anything, they seem to be criminalizing the investors, whose actions may be legal but are nevertheless treated as morally reprehensible. Some renters understand their action as active resistance to gentrification, and we grant their good intentions. Yet, they might not be fully cognizant of the effects their actions could have on low-income marginalized residents. Renters generally assert the right of all residents, regardless of their economic status, to security and safety. They also tend to demand municipal investment in welfare and education, rather than simply police intervention. Yet, even if this is not what renters intend, clearly, overstating Hadar's “crime problem” could lead to enhanced administrative surveillance and police brutality against poorer residents. This, combined with the rising costs of housing in the neighborhood, spells an uncertain future for the most vulnerable tenants.

Discussion and conclusion

Criminologists have long been skeptical about the idea that crime affects property values in a straightforward and commonsensical way. As Skogan long observed: “Concern about crime does not in itself determine levels of investment, the confidence of residents in the future, or property values […] Where people are optimistic about the bundle as a whole, crime counts for less” and vice versa (Skogan, 1986: 221). Indeed, as we sought to show in detail, it is what people expect and believe about a neighborhood's trajectory and its “potential” that affects the meaning of crime and, consequently, its price or value. This is doubly true when houses are primarily considered as investment assets.

The neoclassical science of crime and property values provides ideological foundations of gentrification by legitimating unequal distribution of law enforcement and other public services to induce property appreciations and legitimating the rising cost of housing based on “consumer preference.” Instead of pursuing a full-fledged theoretical critique of this pervasive ideology in this article, we merely aimed to demonstrate how its underlying premises are unsustainable by showing how crime is being capitalized—in opposite directions—by investors and by renters at the neighborhood level. Our study suggests that the effect of crime on property values has little to do with utility or consumer preference, and everything to do with the power of images and expectations. Furthermore, the effect of crime on property values cannot be scientifically measured because it cannot be distinguished from the social construction of neighborhood “feel,” reputation, and status.

The capitalization of crime, a notion we ethnographically developed in this article, aims to capture how the politics of crime is reshaped by the transformation of houses into investible assets. First, we sought to show how the production of expectations of crime reduction and displacement through conventional patterns of gentrification are capitalized into house prices long before they take place on the ground. Through the series of maps presented, we saw that high levels of crime do not reduce property values. If anything, they only make the area more attractive to investors. This paradoxical situation depends on two primary factors: the cultivation of a safe pool of middle-class renters, and the ongoing production of expectations of future price appreciation in the context of protracted gentrification and ongoing disadvantage. Because everyone knows, or seems to know, what gentrification typically entails, future crime reductions through displacement and gentrification provide a script for house price capitalization.

Second, we sought to demonstrate how the meaning of urban crime is reshaped by the logic of capitalization. In this connection, we focused on how the capitalization of crime into property values is subverted by renters, who use crime and danger to reduce housing prices and delay their impending displacement. Crime is the main idiom used to express the discrepancy between future-oriented prices and perceptible neighborhood value. It is strategically harnessed by Hadar's milletmeal renters to challenge the rising costs of rents, reduce demand, impose rent control, and dampen profit expectations. Aware of the forward-looking nature of financial calculations, Hadar's renters capitalize (on) crime to shape property values to their advantage.

Notwithstanding the specificity of context, and therefore the limited generalizations that could be drawn from the case, Hadar is important for what it can tell us about the shifting politics of crime in financialized rentals. Whereas most studies of gentrification and criminalization focus on the relationship between new homeowners and displaced lower-class residents, our study looked at the protagonists of a new housing regime: investors and “middle-class” renters. Although these two groups are certainly not the only, perhaps not even the most quantitatively significant, segments of the urban population, they mark the consolidation of a new order of stratification, which demands criminologists’ attention. This is true even if booming housing markets begin to plummet in the wake of another global recession, because in the absence of public housing or similar alternatives class polarization is likely to persist and even expand among rentiers and renters. The research we conducted in Hadar may thus be read as a preview of possible future developments in the urban politics of crime and criminalization. Based on the findings presented in this article, we suspect that “crime” will increasingly become a point of contention among unpropertied residents and private landlords who double as brokers of municipal services.

The broader meaning of the capitalization of crime, which demands further research and contemplation, concerns the transformation of the very meaning of crime through the idioms and temporal narratives of financialization. Our study only began drawing connections between urban criminology and the social studies of finance. It leaves us with a troubling sense of how crime is transformed in the present capitalist dispensation. For across and through the diverse strategies of capitalization we met in this article, “crime” was treated as an exchange value, a complete abstraction. Crime, for everyone concerned—policymakers, residents, and investors—is reduced to price, to number, to relative advantage. This is why we refrained from defining crime, giving it any substance, or explicating its cultural signification. In the struggle to profit from crime—whether real or imagined—actual harms, mostly affecting the poorest residents, are completely neglected.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Insurance Institute of Israel

Author biographies

Eilat Maoz is a social anthropologist studying conflict formation and transformation. She conducted this research as a postdoctoral fellow at the Smart Social Strategy Lab at the Technion. Her Recent publications include the book “Living Law: Policing the Occupation” (Hebrew, 2020) and “Black Police Power: The Political Moment of the Jamaica Constabulary.” (2023).

Meirav Aharon Gutman is an urban sociologist at the Faculty of Architecture and Town Planning at the Technion. Her recent publications include “Social Topography: Studying Spatial Inequality Using a 3D Regional Model” (2018) and “Border Disorder: On Urban Boundary Work and Crime in a Divided City.” (2021).