Abstract

This study examines the effect of physical climate shocks on firm investment behaviour across 43 emerging economies. Drawing on 8775 firm-year observations from the tourism and hospitality (T&H) sector, we find that firms operating in high climate-risk environments exhibit systematically lower investment efficiency. The results indicate that heightened climate exposure prompts a shift toward conservative financial strategies—namely, reduced capital expenditure, greater earnings retention, and increased reliance on short-term financing. These findings underscore the economic costs of climate volatility at the firm level and highlight a structural trade-off between financial resilience and long-term growth in emerging markets.

Keywords

Introduction

The tourism and hospitality (T&H) sector plays a critical role in driving economic growth and employment, particularly in emerging economies 1 (Chon et al., 2020; Eleftheriou and Sambracos, 2019). At the same time, it remains structurally vulnerable to physical climate shocks, given its exposure to weather-dependent demand, fixed-location infrastructure, and limited risk-transfer mechanisms (Lee et al., 2021; Scott et al., 2019). While transition and liability risks—such as regulatory change and emissions disclosure—have received considerable attention in the literature (Chava, 2014; Michailidou et al., 2016), the effects of physical climate volatility on firm-level behaviour remain underexplored. While recent research by Arian and Naeem (2025) extends this discussion by analyzing how climate risk affects corporate investment efficiency across a broad range of industries in emerging economies, their study adopts a generalized approach without isolating sector-specific dynamics. In contrast, the present study focuses explicitly on the Tourism and Hospitality (T&H) sector—one of the most climate-sensitive industries—thereby addressing a significant gap in the literature. These shocks can damage infrastructure, disrupt operations, and weaken financial performance (Pintassilgo et al., 2016), with consequences that, like the COVID-19 pandemic, often transcend borders. In emerging markets—where adaptive capacity and institutional resilience are limited (Buhr et al., 2018)—understanding firm-level responses becomes especially important. Location plays a central role in shaping climate exposure: firms operating in high-risk regions often anticipate lower returns and respond with financial conservatism (Huang et al., 2018). For T&H firms, such adaptation is complicated by their dependence on fixed, climate-sensitive destinations (Scott et al., 2019).

Using panel data from 675 tourism and hospitality firms across 43 emerging economies (2007–2019), we examine how exposure to physical climate shocks affects firm-level investment efficiency. Climate risk is proxied by the Germanwatch Global Climate Risk Index, capturing both acute and chronic climate events at the national level. We find that firms operating in high-risk environments consistently exhibit lower investment efficiency, reflecting disruptions to operations and financial planning. In response, these firms adopt more conservative financial strategies—retaining earnings, reducing dividends, and favouring short-term debt over long-term commitments. These results point to a trade-off between immediate financial stability and sustained capital investment. Our empirical approach links firm-level financials with cross-country climate risk data, offering new evidence on climate-related behavioural shifts in a sector that is both economically significant and structurally exposed.

Data and empirical strategy

Climate risk and investment efficiency measures

National-level climate risk is proxied using the Global Climate Risk Index (Germanwatch), which combines absolute losses, losses relative to GDP, fatalities, and fatalities per capita (Kreft et al., 2013; Rivera and Wamsler, 2014). Investment efficiency is measured using Biddle et al. (2009), with (−1) absolute residuals from a regression of investment on lagged revenue growth. As a robustness check, we apply McNichols and Stubben (2008), using Tobin’s Q and internal cash flow. Investment is defined as the net change in tangible and intangible assets, scaled by lagged total assets.

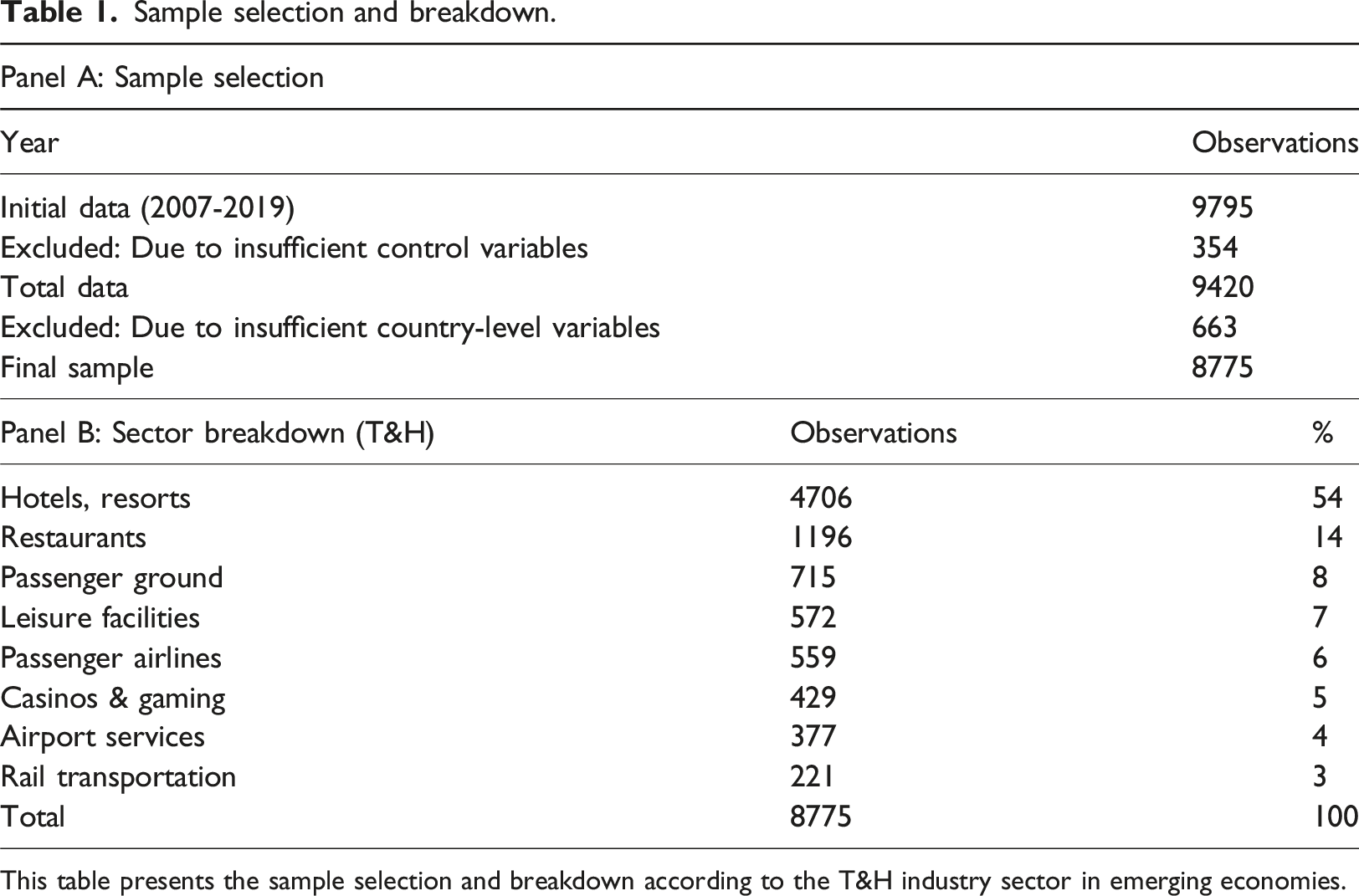

Sample selection and breakdown.

This table presents the sample selection and breakdown according to the T&H industry sector in emerging economies.

To assess the impact of climate risk on investment efficiency, we estimate the following baseline model:

Results and discussion

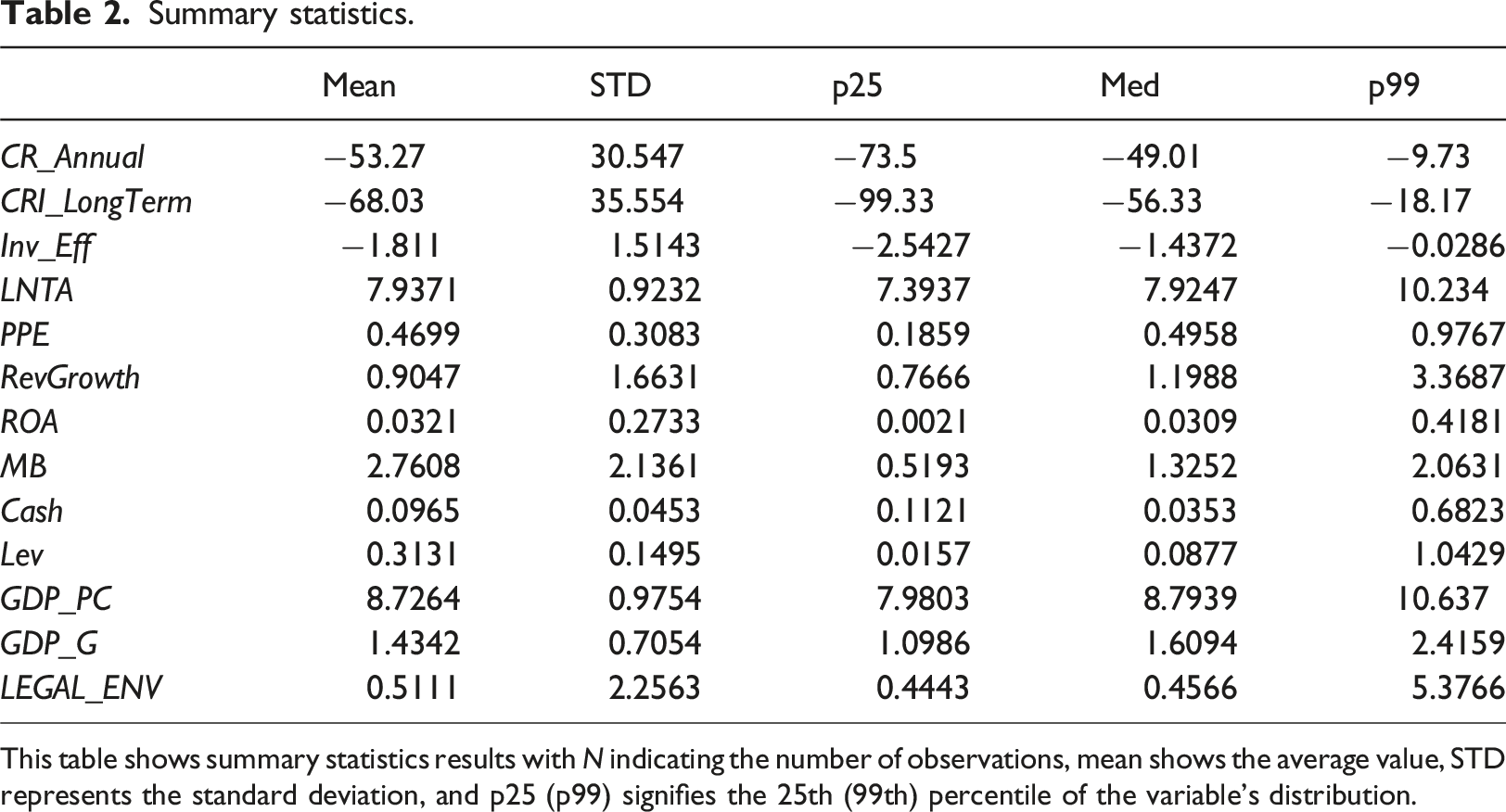

Summary statistics.

This table shows summary statistics results with N indicating the number of observations, mean shows the average value, STD represents the standard deviation, and p25 (p99) signifies the 25th (99th) percentile of the variable’s distribution.

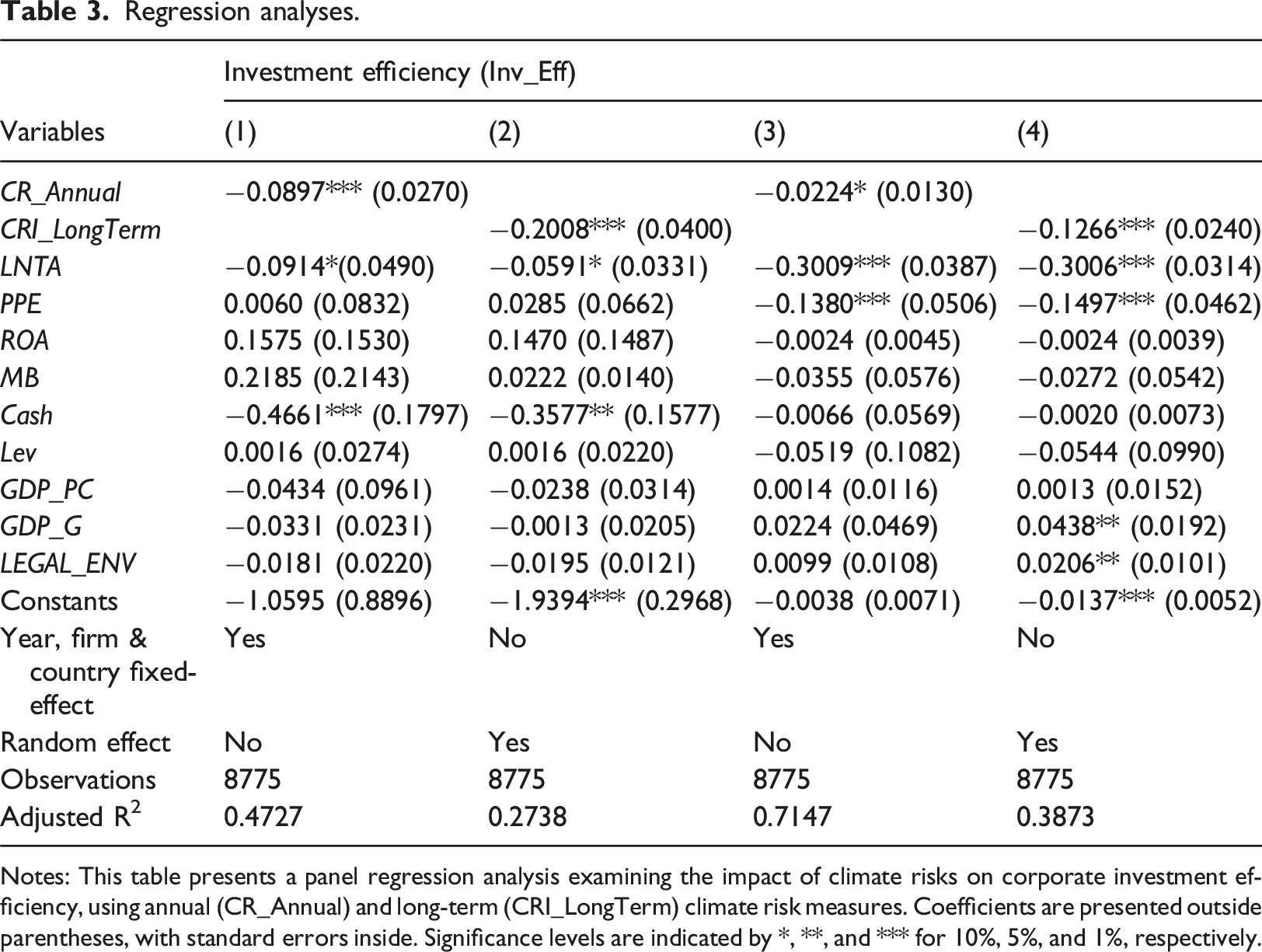

Regression analyses.

Notes: This table presents a panel regression analysis examining the impact of climate risks on corporate investment efficiency, using annual (CR_Annual) and long-term (CRI_LongTerm) climate risk measures. Coefficients are presented outside parentheses, with standard errors inside. Significance levels are indicated by *, **, and *** for 10%, 5%, and 1%, respectively.

To address endogeneity, we instrument CR_Annual with Alt_CR_Annual, following Gholami et al. (2023). 2 The IV results support the main findings and meet standard diagnostics. Robustness checks using the ND-GAI index (Huang et al., 2018), exclusion of outlier countries, weighted least squares, and country fixed effects further validate the results.

This study examines how physical climate risk affects investment efficiency in tourism and hospitality firms across 43 emerging economies. Using 8775 firm-year observations (2007–2019), we find that firms in high-risk environments adopt conservative financial strategies—retaining earnings, reducing dividends, and relying on short-term debt—at the expense of long-term investment efficiency. These robust findings highlight the behavioural costs of climate shocks in structurally exposed sectors. While such conservatism may boost short-term resilience, it can hinder capital formation and competitiveness. Firms must integrate climate risk into financial planning, with policymakers supporting adaptation through sustainable finance and capital access.

Supplemental Material

Supplemental Material - Economic Costs of Climate Shocks for Firms in Emerging Economies

Supplemental Material for Economic Costs of Climate Shocks for Firms in Emerging Economies by Adam Arian, Hassan F. Gholipour, Richard Busulwa, John Sands in Tourism Economics.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.