Abstract

This study investigates how the fee-oriented business model in the hospitality industry is associated with corporate tax avoidance. Using a sample of international hospitality firms, the results from OLS and entropy balancing estimations indicate that greater reliance on fees is associated with lower tax avoidance, reflected in higher effective tax rates. We attribute this higher tax burden to lower incentives of fee-oriented businesses to engage in tax avoidance to preserve their reputation—a strategic asset. This study provides insights into a societal benefit of the widespread adoption of the fee-oriented business model in the hospitality industry, namely increased corporate tax contributions.

Introduction

Most hospitality firms now favor fee-oriented 1 business models over riskier capital investments (Brookes and Roper, 2012; Poretti and Heo, 2022; Roper, 2017; Sohn et al., 2013; Woo et al., 2023), which makes it the ‘new norm’ (Blal and Bianchi, 2019). This rapid and wide-scale development brings research on its implications in a number of hospitality-related domains (Ji et al., 2024). Among others, most recent archival research focuses on firms’ performance (e.g., Ji et al., 2024; Seo et al., 2021) and corporate financial reporting (e.g., Poretti et al., 2023a; Poretti et al., 2024; Weisskopf, 2024). While fee-oriented strategies redefine the value creation process, taxation, which is one of its central elements, remains a significant yet underexplored gap in the existing literature. In this context, this study investigates the association between the extent of fee reliance and tax avoidance in the global hospitality industry.

Tax matters represent a long-standing area of interest in the hospitality and tourism industry (Spengler and Uysal, 1989), for several reasons. First, “there is evidence that tourism is relatively heavily taxed” (Forsyth and Wyer, 2002: 377) and taxation levels are sometimes even considered as ‘unfair’ (Ihalanayake and Divisekera, 2006). Second, the competitiveness of the hospitality sector is affected by taxation through both prices customers must pay and costs borne by firms (European Commission, 2017). In this respect, Altin et al. (2020) show that tax policy is one of the institutional factors affecting corporate birth and death rates in the hospitality sector—unlike other business sectors. This feature is confirmed by the Organization for Economic Co-operation and Development (OECD) mentioning a “disproportional impact of taxes on tourism enterprises” (OECD, 2014: 75).

Taxation issues have also become a major global concern prompting increased regulation, which the Country-by-Country Reporting exemplifies. An action of the OECD, this reporting obligation requires the standardized disclosure of aggregate data on the global allocation of economic activity, income, profit, and taxes paid among tax jurisdictions in which the largest multinational companies do business. Its intent is to provide more data so as to curb tax avoidance more effectively, something that is not clear from early empirical evidence carried out in this area (e.g., Joshi, 2020; Overesch and Wolff, 2021).

Tax avoidance is defined in broad terms as the reduction in the firm’s taxes relative to its pretax accounting income (Dyreng et al., 2010; Huseynov and Klamm, 2012), which captures the overall corporate aim to reduce the firm’s explicit tax burden (Schwab et al., 2022). In the study, we measure tax avoidance with the effective tax rate 2 (ETR) conventionally used in tax research (e.g., Dyreng et al., 2010; Huseynov and Klamm, 2012). In other terms, we do not consider specific tax-related behaviors such as tax sheltering (Dyreng et al., 2010).

Given cross-firm variations in tax avoidance (e.g., Chen et al., 2021; Gallemore et al., 2014), empirical research has explored (hindering and fostering) determinants associated with it. However, to the best of our knowledge, studies on the existence and direction of the association between the use of specific business models 3 —such as those based on fees—and tax avoidance have not been carried out, although there are arguments supporting a negative relationship. In this study, we explain why fee-oriented firms may be less likely to engage in tax avoidance activities under a cost-benefit analysis of the corporate tax strategy (Gallemore et al., 2014; Wilde and Wilson, 2018).

Along the resource-based view, the reputation of fee-based hospitality firms is an essential strategic intangible asset (Li and Singal, 2019). 4 Past empirical research shows companies fear incurring reputational costs upon disclosure of tax avoidance activities (Graham et al., 2014; Wilde and Wilson, 2018). Tax-related reputational harm may consequently lead to an ex ante monitoring effect by stakeholders, resulting in a higher corporate tax burden (Graham et al., 2014; Krieg and Li, 2021). Within this framework, Austin and Wilson (2017) show that firms with valuable consumer brands adjust to the downside their tax avoidance activities to mitigate potential reputational costs. Building on this perspective, we posit that hospitality companies following a fee-oriented strategy highly rely on their reputation, making them particularly sensitive to reputational risks associated with the detection of tax avoidance. Thus, we expect a negative association between the extent of the fee-oriented business model and tax avoidance.

We test this hypothesis on a sample of 611 firm-year observations from publicly listed hotel and restaurant companies from 2004 to 2018. We estimate regressions with OLS and entropy balancing. The latter allows to account for the fact that adopting a fee-based strategy is an intentional (and not random) decision. The findings show a significant and negative relationship between the extent of the fee-orientation and tax avoidance. Put differently, in terms of tax rate, we find that a higher degree of reliance on fees (measured with the fee-income ratio) is associated with a higher ETR. Additional regressions further indicate that this effect is more pronounced as fee-orientation rises.

Literature review and hypothesis development

Literature review

Prior literature on tax avoidance has been longstanding (Shackelford and Shevlin, 2001). Given the variation observed between companies in the extent of tax avoidance, one stream of literature pertains to the factors that influence involvement in tax avoidance activities. 5 Internal corporate determinants have been the most widely investigated. Studies report associations between firm’s attributes such as multinational activities (e.g., Rego, 2003), consumer-based brand equity (Austin and Wilson, 2017) or asset redeployability (Hasan et al., 2021) and tax avoidance. Ownership structure, through shareholding concentration (Badertscher et al., 2013) and the presence of family firms (Chen et al., 2010) for example, is also associated with the propensity to engage in tax avoidance. Several corporate governance characteristics (Armstrong et al., 2015) as well as personal features (Duan et al., 2018) and compensation packages of executives (e.g., Gaertner, 2014) are reported to influence tax-avoidance choices. Finally, antecedents from the company’s environment (institutional factors, external market, external governance, and social networks) also impact the level of tax avoidance (Wang et al., 2020).

Within this stream of literature, researchers have developed the idea of an ‘under-sheltering puzzle’ (e.g., Desai and Dharmapala, 2006; Weisbach, 2002). According to Gallemore et al. (2014: 1103), the under-sheltering puzzle refers to the “question of why so many firms do not avail themselves of tax avoidance opportunities”. In other terms, research on the factors that explain why some companies have higher ETRs than others is still warranted.

Hypothesis development

As a whole, the tax avoidance literature examines many determinants but ignores the fee-oriented business model while we argue it is worth examining. To justify the existence and direction of a relationship between reliance on fees and tax avoidance, we combine two rationales.

First, along the resource-based view, resources are defined as “the tangible and intangible assets a firm uses to choose and implement its strategies” (Barney, 2001: 54). The attributes (value, rareness, imperfect imitability, and degree of substitutability) of a company’s resources form the basis for sustained competitive advantage (Barney, 1991). This theoretical orientation is one of the perspectives adopted to explain the success and development of fee-orientation arrangements (Mariz-Pérez and García-Álvarez, 2009), franchises and management contracts being both based on the ownership of intangible assets (Sohn et al., 2013). Among others, Barney (1991) names positive corporate reputation as a potential source of sustained competitive advantage.

Brand name and its accompanying reputation is at the heart of the franchising package (Barthélemy, 2008; Wu, 2015). This is a strategic asset franchisors have long been using to improve firm performance (Wu, 2015). Peterson and Dant (1990) identify a recognized trade name as an antecedent of the franchise option choice. A highly-reputed image thus has the potential to influence the franchisee’s decision to buy-in to a franchisor brand, especially in the hospitality industry (Yeung et al., 2016). Indeed, Combs and Ketchen (1999: 869) contend that “brand name reputation […] may be more valuable in experiential service industries than in industries where quality can be determined prior to purchase.” Roh and Yoon (2009) analyze ice cream franchising operations and find that consumer brand recognition represents the main driver to opt for franchising. In a related vein, Xiao et al. (2008) report that “hotel chains that have strong brand awareness […] are most attractive to potential Chinese franchisees” in a study of 182 Chinese hotels. Companies using a fee-oriented business therefore have an incentive to significantly invest (and subsequently maintain) in their reputation because they derive associated fee-based revenues from it. Seo et al. (2021) have recently pushed the reasoning further by mobilizing the dynamic capabilities view (Teece et al., 1997), which places emphasis on the processes that deploy resources. A dynamic view should also be taken of the company’s reputation and image, since reputation evolves as a result of factors both internal and external to the company. Among the factors likely to affect image is the public uncovering of inappropriate corporate tax behavior.

Second, significant reputational consequences may be incurred when avoidance conduct comes to light. Hanlon and Slemrod (2009) show a significant stock price decline associated with public revelation of tax shelter behavior. Graham et al.’s survey (2011) reports that roughly 70% of corporate tax executives respondents agree that potential harm to their firm’s reputation is an important factor in deciding not to implement a tax planning strategy. Dhaliwal et al. (2022) find that a higher level of tax avoidance is positively associated with negative media sentiment during heightened period of scrutiny, which they attribute to firms bearing tax-related reputational costs. As an example, Jang et al. (2022) note that the reputation of Starbucks has been downgraded due to corporate social irresponsibility acts including tax avoidance.

As part of a cost-benefit rationale, the fear to bear tax-related reputational costs can ex ante lead to managerial discipline and lower tax avoidance activities (Krieg and Li, 2021). In our setting, this aspect is reinforced by two elements. First, reputational costs are particularly marked for companies with valuable consumer brands (Austin and Wilson, 2017). These authors contend that “firms with the greatest exposure to reputational damage among consumers […] engage in lower levels of tax avoidance to minimize unwanted scrutiny that could impair the firms’ reputation” (2017: 67). Second, tax behavior is now considered as part of corporate social responsibility―an increasingly important dimension of hospitality firms’ performance (Rhou and Singal, 2020). The society holds an interest in knowing whether companies pay their ‘fair share’ of taxes (Huseynov and Klamm, 2012), which allows stakeholders to exert pressure on companies. This ex ante continued monitoring is alike to constrain tax avoidance (Krieg and Li, 2021).

Combining both rationales, we argue that the strong reliance on reputation of fee-oriented hospitality firms leads them to avoid actions that could result in reputational costs, such as tax avoidance if detected. Consequently, our hypothesis is the following:

There is a negative association between the extent of the fee orientation and tax avoidance.

Methodology

Sample

To build our sample, we first collected all publicly listed hotel and restaurant firms on LSEG Datastream from 2004 to 2018 (887 firm-year observations). 6 We only retained companies for which annual reports are available on their respective corporate websites. Then, management and franchise fees, international presence, corporate governance information, and tax fees expenses were all manually collected in annual reports and proxy statements. All other control variables were retrieved from LSEG Datastream. Firm-year observations without any valid value for our measures were excluded. The final sample comprises 611 firm-year observations for 60 different companies over the 2004-2018 time period. The most represented countries are the United States (U.S.) (57%), the United Kingdom (21.6%), and France (8.7%). 7

Model development

To investigate the association between the adoption of the fee-oriented business model and tax avoidance, we use both OLS and entropy balancing estimations. The rationale for using entropy balancing lies in the fact that the decision to follow a fee-oriented strategy is not random, which might create endogeneity. As a result, entropy balancing allows us to create two groups of firms, the treated one (i.e., firms that have a fee-income ratio greater than 0) and the control one (i.e., firms having a fee-income ratio equal to 0). Weights are assigned to the control group to make both groups’ covariates more comparable, with a focus on the first three moments. Our model reads as follows:

Results

Descriptive statistics

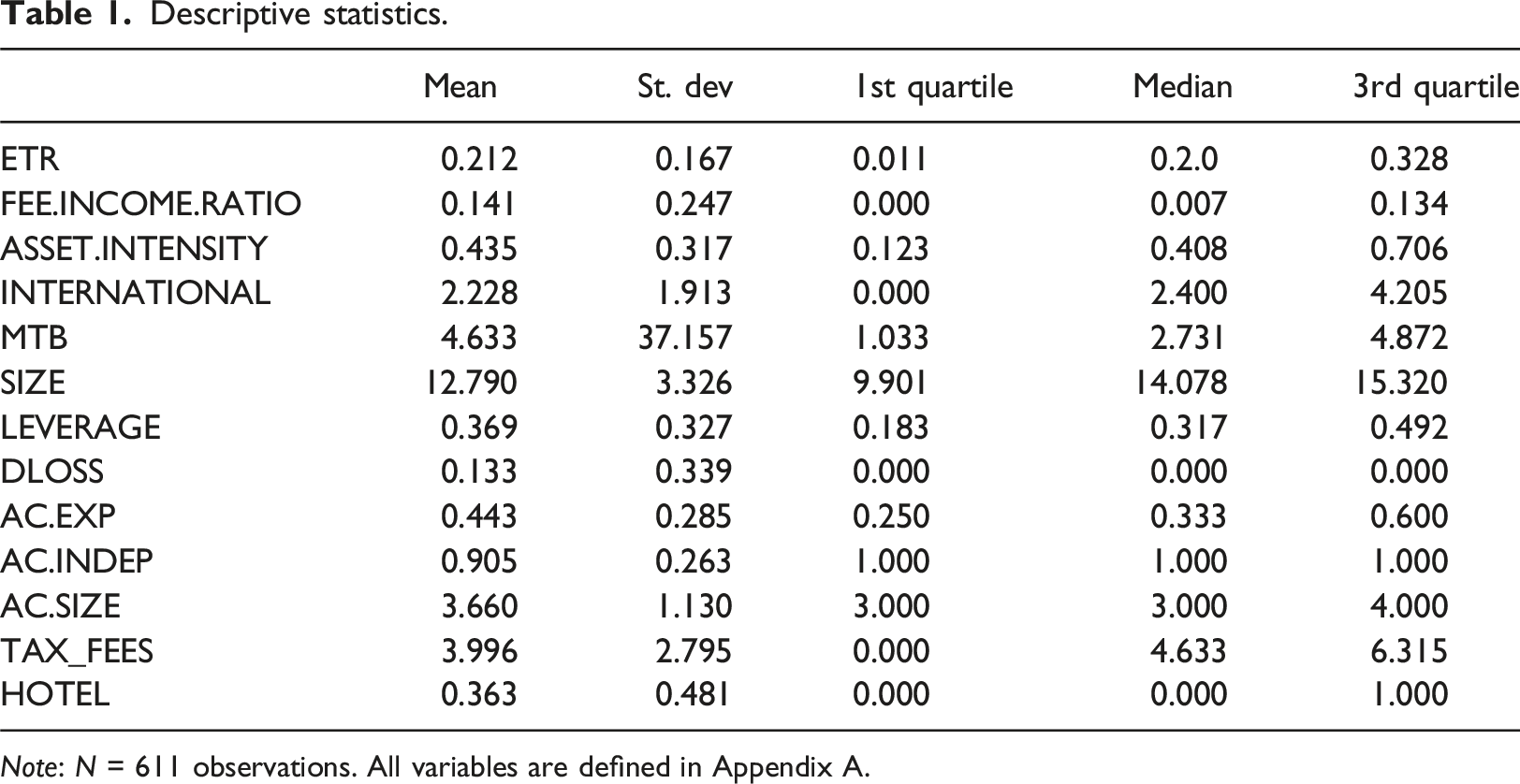

Descriptive statistics.

Note: N = 611 observations. All variables are defined in Appendix A.

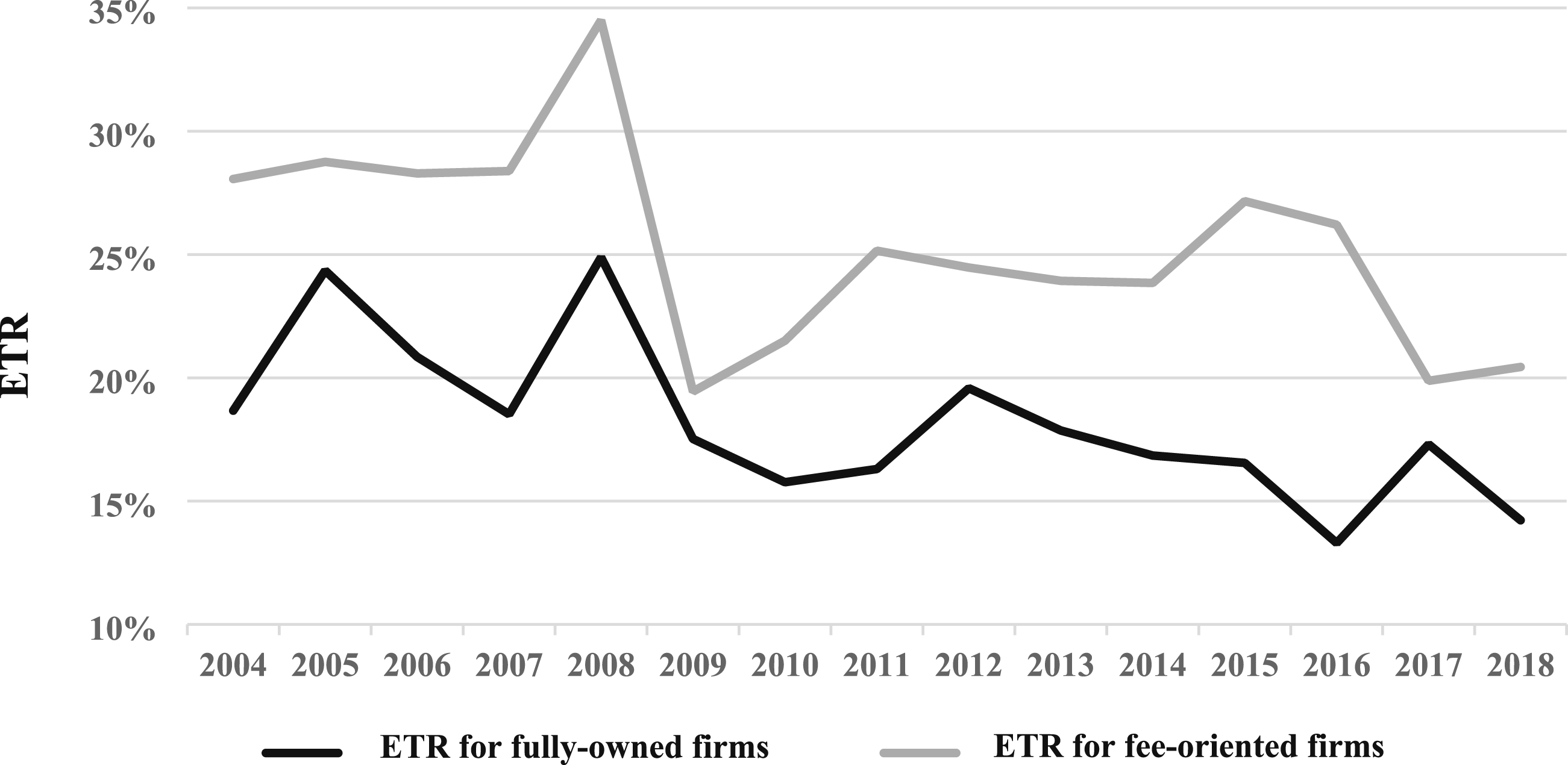

ETR through time. Note: Based on a sample of 611 firm-year observations. Fee-oriented firms have a fee-income ratio greater than 0%.

The average FEE.INCOME.RATIO is 14%. This shows that, in fact, many companies are adopting a ‘plural form’ strategy (Bradach, 1997; Bradach and Eccles, 1989). In this organizational combination, companies own their outlets in parallel to those managed under fee agreements. INTERNATIONAL has a mean of 2.2. The average MTB is 4.6, the average SIZE is 12.79, and the average debt-to-asset ratio (LEVERAGE) is 0.369. Companies report a loss (DLOSS) in 13% of firm-year observations. Audit committees are, on average, composed of 3.66 members (AC.SIZE), generally all independent (AC.INDEP has a mean of 0.905), and include at least one finance or accounting expert (AC.EXP) in 44% of cases. The average value of TAX.FEES is equal to 3.996. Finally, 36% of our sample is composed of hotel firms (HOTEL).

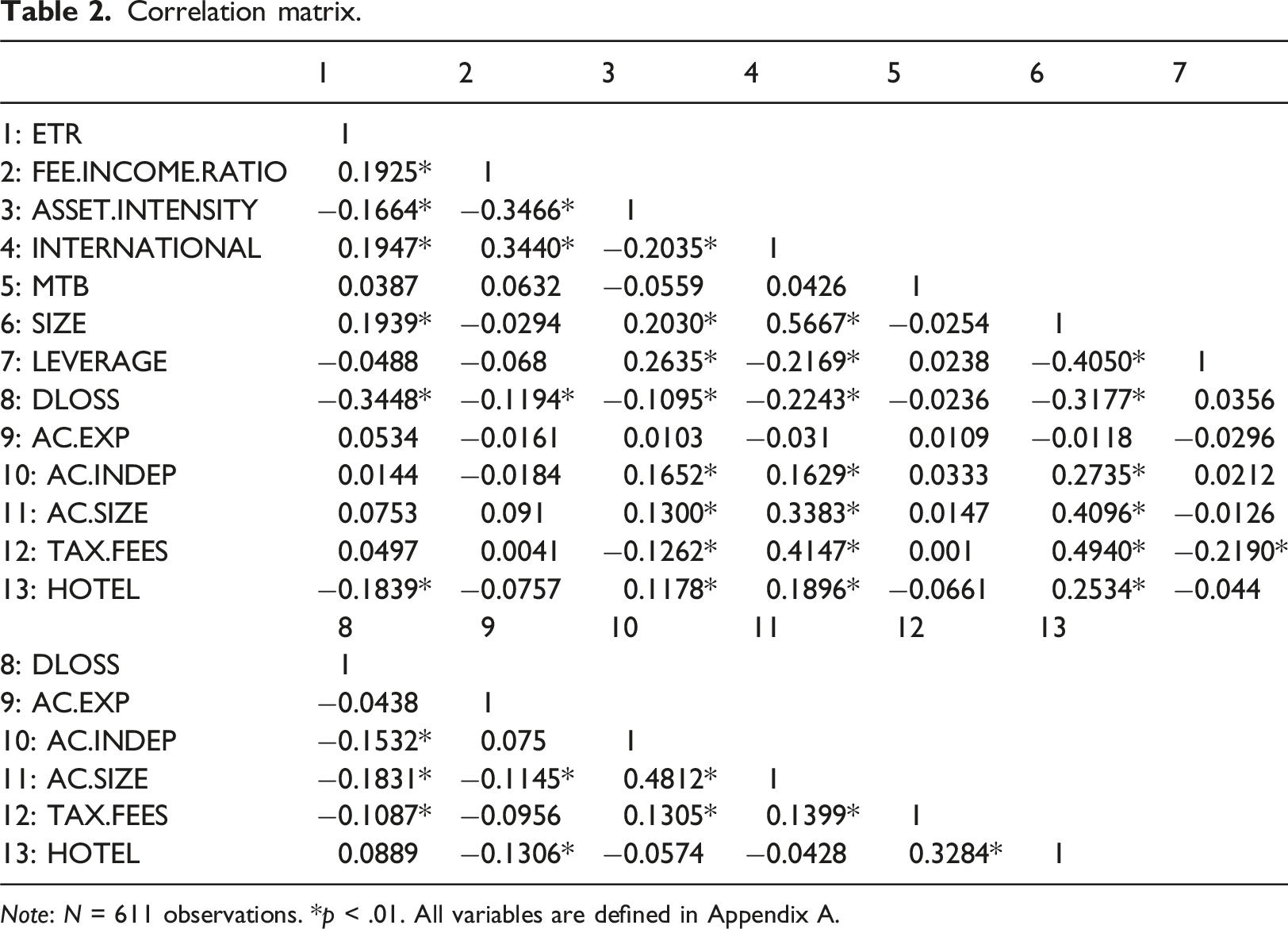

Correlation matrix.

Note: N = 611 observations. *p < .01. All variables are defined in Appendix A.

To mitigate concerns regarding multicollinearity issues, we analyzed variance inflation factors (VIFs) in our main tests. The results indicate that VIFs (untabulated) are not higher than 2.5 for independent variables, meaning that our tests do not suffer from any multicollinearity.

Main analysis

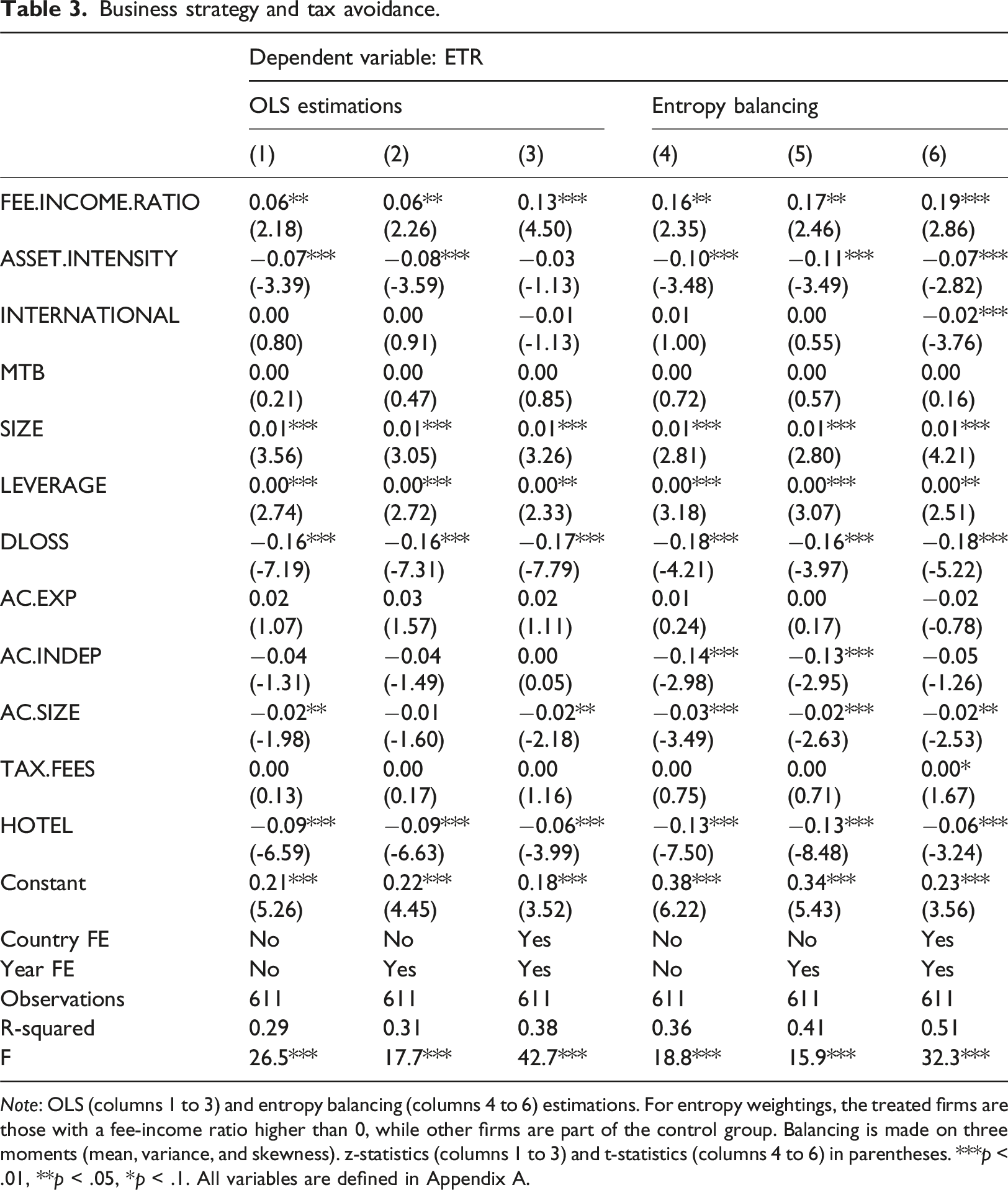

Business strategy and tax avoidance.

Note: OLS (columns 1 to 3) and entropy balancing (columns 4 to 6) estimations. For entropy weightings, the treated firms are those with a fee-income ratio higher than 0, while other firms are part of the control group. Balancing is made on three moments (mean, variance, and skewness). z-statistics (columns 1 to 3) and t-statistics (columns 4 to 6) in parentheses. ***p < .01, **p < .05, *p < .1. All variables are defined in Appendix A.

Additional analysis

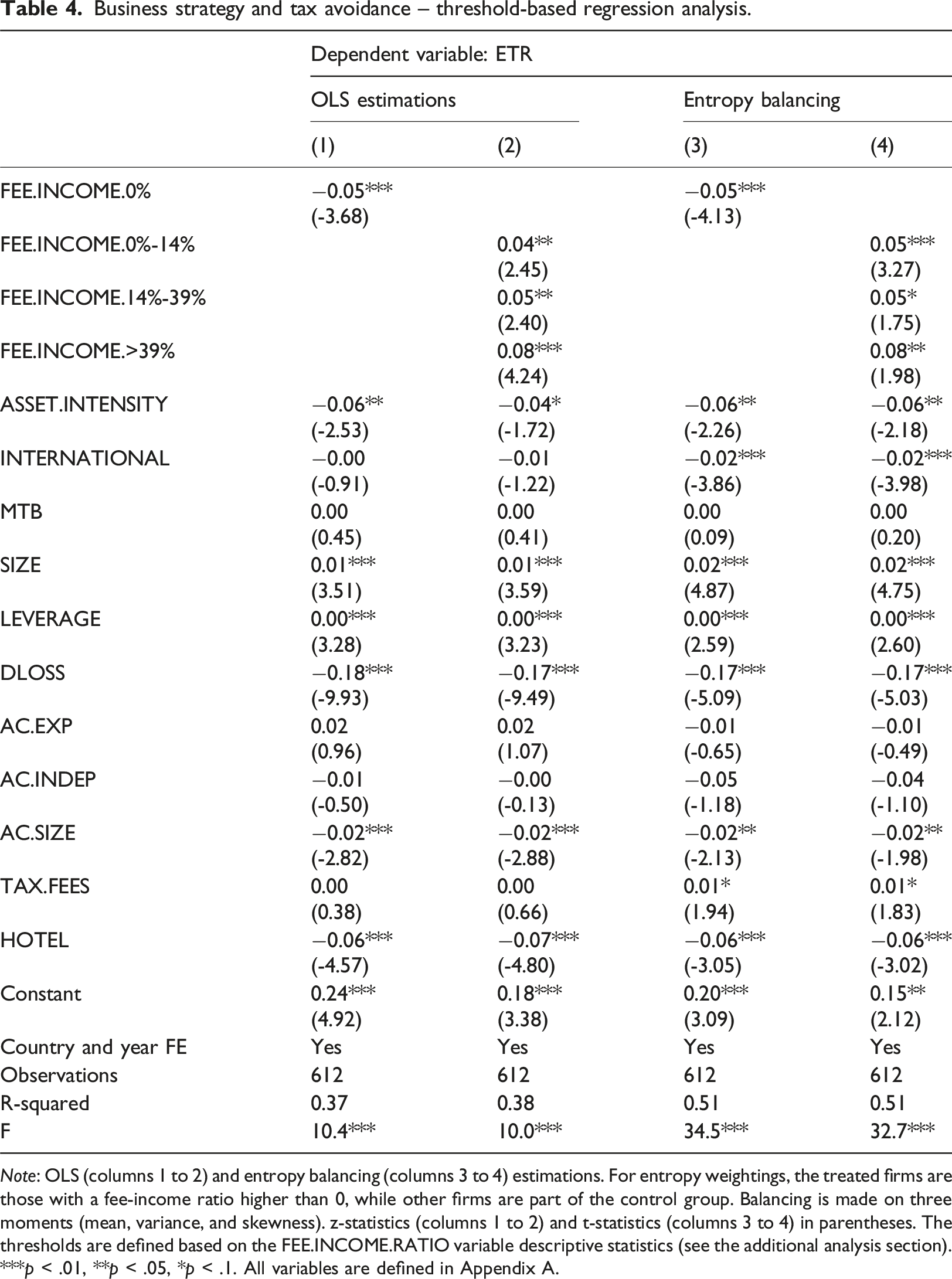

Business strategy and tax avoidance – threshold-based regression analysis.

Note: OLS (columns 1 to 2) and entropy balancing (columns 3 to 4) estimations. For entropy weightings, the treated firms are those with a fee-income ratio higher than 0, while other firms are part of the control group. Balancing is made on three moments (mean, variance, and skewness). z-statistics (columns 1 to 2) and t-statistics (columns 3 to 4) in parentheses. The thresholds are defined based on the FEE.INCOME.RATIO variable descriptive statistics (see the additional analysis section). ***p < .01, **p < .05, *p < .1. All variables are defined in Appendix A.

Next, in column 2, we differentiate fee-oriented companies depending on the level of their fee-income ratio. More precisely, we create three groups of companies: companies with a fee-income ratio above 0% and below or equal to the mean ratio of 14% (FEE.INCOME.0%-14%), companies with a fee-income ratio above the mean and below or equal to the mean plus one standard deviation (14% + 25% = 39%) (FEE.INCOME.14%-39%), and companies with a fee-income ratio above 39% (FEE.INCOME.>39%). The results indicate that the higher the fee-income ratio, the higher the effect on the ETR as the positive and significant coefficients on the three variables evidence. Interestingly, the coefficient on each variable related to the fee-income gradually increases with the level of the fee-income ratio. The results hold with OLS estimations as well as with entropy balancing, which further indicates the robustness of these findings. These results may be paralleled with the fact that “the impact of brand name value on chain performance is likely to be contingent on the proportion of franchised outlets in the chain” (Barthélemy, 2008: 1453). As the degree of reliance on fees of hospitality firms included in our sample increases, so do the stakes involved in preserving reputation and therefore tax reputational costs.

Conclusion

This article investigates the relationship between the fee-oriented business model, which has grown significantly among hospitality firms, and corporate tax avoidance behavior. Our findings show a significant and negative relationship on an international sample of restaurants and hotels. In other words, the more companies rely on the fee-based model, the greater their tax contribution, indicating a lower level of commitment to tax avoidance activities.

The OECD (2013: 13) observes that “domestic and international rules on the taxation of cross-border profits are now broken and that taxes are only paid by the naive”. So, are fee-oriented hospitality firms naiver than their non-fee counterparts? We contend they are not. Rather, their higher tax payment may be explained by lower incentives arising from reputational concerns―the result of a detailed cost-benefit analysis. This finding contributes to the literature exploring the so-called ‘under-sheltering puzzle’, the question being: “what is holding […] firms back from taking advantage of known tax avoidance opportunities being used by other firms?” (Gallemore et al., 2014: 1106). We are contributing to this line of research by identifying a business model at the root of this phenomenon. Our findings reveal that dependence on a fee-oriented business model represents a context in which tax avoidance is effectively constrained. More precisely, we argue that revelation of tax avoidance activities results in higher reputational costs for fee-oriented firms, whose reputation is a strategic asset, deterring them from lowering their ETR.

The question then arises as to ‘who’ actually bears the tax burden (Dyreng et al., 2020). Indeed, parties bearing the corporate tax incidence are not always clearly identified and are not always the first that come to mind, that is, shareholders. In our setting, shareholders of fee-oriented hospitality firms, although with an higher effective tax rate, might not ultimately bear the corporate tax incidence as the corporate tax burden may fall on stakeholders (employees, consumers, …) (Dyreng et al., 2020).

From an empirical perspective, this study’s findings contribute to the literature on business strategies in the hospitality industry. Various studies highlight the advantages and drawbacks of pursuing an asset-light and/or fee-oriented strategy (Dogru et al., 2020; Li and Singal, 2019; Poretti and Blal, 2020; Poretti et al., 2023b, 2024). By documenting that fee-oriented companies are associated with lower tax avoidance, our study adds an important piece to the puzzle. Our study also broadly contributes to the literature on tax avoidance from the perspective of reputational costs. While Austin and Wilson (2017) highlight an inter-industry dynamic, our research takes a step further by demonstrating that the level of analysis can be narrowed to a single industry. 10 In the case of the hospitality sector, firms facing high ex ante reputational costs also tend to report a higher ETR. Moreover, whereas Austin and Wilson (2017) adopt a customer-centric approach, our analysis takes a more internally focused perspective through the lens of the fee-based strategy adopted.

Our findings have significant practical implications for both hospitality firms and policymakers. Hospitality firms’ top managers and board members should not neglect the tax implications different business strategies have. Firms that heavily rely on fee-based revenues should be aware that their tax contributions are likely to be higher than their asset-heavy counterparts, which may sustain their reputation among stakeholders. Since reputation is a more strategic asset for fee-oriented firms within the hospitality industry, a virtuous circle seems at work. Indeed, fee-orientation leads to higher tax contributions, which may help maintain reputation, thereby fostering customer loyalty and potentially supporting business growth.

For policymakers, the study highlights the importance of understanding that different business models influence differently corporations’ tax-related behaviors. Policymakers might also consider developing targeted tax incentives or support mechanisms that reward transparency and fair tax practices, thereby encouraging firms to act in a fair and sustainable manner.

This study is not without limitations, which provides research avenues. While the sample provides a comprehensive overview of international hotel and restaurant companies, further studies could consider expanding the sample to smaller non-listed companies, although data availability is a common issue with hospitality studies (Li and Singal, 2019). Moreover, investigating firms in other hospitality sub-industries, such as airlines, casinos, and travel agencies, might also be interesting. Additional analyses on specific ETR levels (e.g., Schwab et al., 2022), high levels of fee-derived revenues (Gillis and Combs, 2009; Gillis et al., 2020), and tax materiality (e.g., Lynch et al., 2021) would also allow to provide a more comprehensive and detailed glance at the findings. Finally, further theoretical insight could be gained through interviews with practitioners involved in the oversight of fee-based strategies. Such interviews would help assess whether complementary theoretical lenses, beyond the reputation-based explanation, are relevant to fully capture the dynamics linking business model structure and tax avoidance within the hospitality industry. 11

Supplemental Material

Supplemental Material - Hospitality firms’ FEE orientation and tax avoidance

Supplemental Material for Hospitality firms’ FEE orientation and tax avoidance by Cédric Poretti and Tiphaine Jérôme in Tourism Economics.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

All data generated or analyzed during this study are included in this published article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.