Abstract

This study examines the impact of geopolitical risk (GPR) on corporate investments within the Indian hospitality sector. The findings indicate a significant negative relationship between GPR and corporate investment levels. Notably, even financially stable firms cannot completely offset the detrimental effects of GPR. Additionally, investment reductions during periods of heightened GPR are found to be more substantial than the increases observed during periods of reduced GPR. However, the strategic implementation of security measures can substantially mitigate the challenges associated with GPR. These insights offer valuable guidance to regulators and business leaders in emerging markets when making informed investment decisions.

Keywords

Introduction

The uncertainties induced by geopolitical risks (GPR) are often a matter of grave concern to governments, businesses, and individuals to undertake or continue investments (Caldara and Iacoviello, 2022; Wang et al., 2019). An uncertain business condition prompted by GPR may confound managers to form a reasonable view of the future business outlook. For instance, a recent policy report by the Government of India (GoI) expresses severe apprehensions regarding the Russia-Ukraine conflict and its likely impact on the Indian economy. 1 According to the report, the current geopolitical instability predisposes the economy to higher inflation and subdued corporate investments, besides other detrimental implications. The latest financial stability report furnished by the International Monetary Fund (IMF) also highlights the adverse influence of GPR on global growth and investment potential. 2 Given the prominence of GPR in determining corporate investments, a nascent body of literature focuses on this relationship (Balli et al., 2019; Rumokoy et al., 2023; Wang et al., 2019). This article contributes to the ongoing debate by empirically examining the influence of GPR on corporate investments in the Indian hospitality industry and the impact of security force deployment.

Specifically, the primary objective of this paper is to empirically investigate the impact of geopolitical risk (GPR) on corporate investments in the Indian hospitality sector, specifically focusing on the hotel and restaurant industry. The study aims to uncover how GPR influences investment decisions, with a particular emphasis on how these risks constrain capital-intensive initiatives like capacity development and service enhancement. Additionally, the paper explores whether financial flexibility among firms mitigates the adverse effects of GPR while examining the role of security force deployment as a potential buffer against the challenges posed by GPR. By focusing on an emerging market, the study seeks to contribute valuable insights into the unique vulnerabilities of the Indian hospitality sector in the face of geopolitical uncertainties, which have often been underexplored in existing literature.

The focus of our research is timely and relevant on three credible grounds. First, India is a prominent representative of the emerging market universe. It contributes 3.5% to the global nominal Gross Domestic Product (GDP) and is pegged to become one of the world’s top three GDP contributors by 2029. 3 The contributions from the hospitality sector would be critical to India’s growth story. According to KPMG’s estimates, the Indian hospitality sector will likely flourish at a compounded annual growth rate (CAGR) of 16.10%, yielding US$ 342 billion (approx.) by 2022. 4 On the one hand, following domestic economic progress, discretionary public spending on quality hospitality experiences may increase, corresponding to incremental disposable income. 5 On the other hand, a potential source of revenue for the sector will be increased business travel due to new trade opportunities in a growing economy. The Indian business travel market is already worth US$ 35.60 billion in 2022 and is expected to grow to US$ 59.50 billion by 2028. The predicted CAGR of 8.71% during 2023-2028 in the business travel and accommodation segment could transpire as a catalyst for the growth of the Indian hospitality sector. 6

Second, it is well-known that institutional voids expose emerging economies, such as weaker law and order enforcement mechanisms and prompt conflict resolution procedures (Gray, 1997; Khanna and Palepu, 2010). Moreover, higher macroeconomic risk susceptibility of emerging markets than their developed counterparts affects tourist inflows (Tiwari et al., 2019). Thus, the hindrances regulators face in controlling the uncertainty swiftly pose severe concerns to the hospitality sector. Notably, previous studies examining the influential role of uncertainties in shaping corporate decisions in the hospitality sector are mainly confined to developed markets (Akron et al., 2020; Das et al., 2020). Given the criticality of these relationships, unravelling the association between uncertainties and corporate investments in the hospitality sector in an emerging market appears indispensable.

The third reason stems from the fact that while economic and political uncertainties (EPU) affect all sectors somewhat uniformly, the impact of GPR can vary across sectors (Cam, 2008; Kannadhasan and Das, 2020). Thus, a sector or industry-specific focus becomes a pertinent choice to diagnose its vulnerability to GPR (Rumokoy et al., 2023). This study explicitly focuses on the hotel and restaurant industry in the Indian hospitality sector. 7 As the hotel and restaurant industry is capital intensive (Akron et al., 2020), regular investments in capacity development and renovation are unavoidable to enhance the quality of experience for the patrons. The investment hindrances sparked by GPR may constrain strategic expansion or service improvisation goals of firms in the industry (Jallat and Shultz, 2011).

Our study unearths a clear inverse association between GPR and corporate investments within India’s hotel and restaurant industry. This relationship remains consistent across various measurements of both dependent and independent variables. Interestingly, even companies with greater financial flexibility cannot fully offset the detrimental impacts of GPR. Additionally, we observe that firms in this sector reduce investments to a greater extent in response to increases in GPR compared to decreases of an equivalent magnitude. However, we find that strategic deployment of security forces can significantly mitigate the challenges posed by GPR.

Literature and hypothesis development

Caldara and Iacoviello (2022) posit that uncertainties triggered by geopolitical events may constrain firm-level investments, with at least two possible underlying mechanisms explaining this association. First, the ‘real options channel’ proposes that firms may view their investment choices as a series of real options. When the degree of uncertainty is high, the option value of investment delay is also high, given the adjustment costs (Wang et al., 2019). Put differently, unless the firms are certain about the returns from new investments, they may keep the project(s) on hold, thus depressing investments. Several studies have empirically validated this channel (Guiso and Parigi, 1999; Kang et al., 2014; Leahy and Whited, 1995). Second, the ‘cost of external financing channel’ propounds that lending institutions often impose higher risk premiums to compensate for increased default risk under uncertainty (Bernanke, 1983; Gilchrist et al., 2014). The lenders usually feel discouraged from extending funds under uncertainty as a translucent view of the future economic outlook prevents them from ascertaining the proposed project’s future cash flows.

Following this theoretical prediction, Wang et al. (2019) examine the relationship between GPR and corporate investments using a sample of U.S. firms across different industries. After controlling for firm-level characteristics, their results reveal a strong negative association between them. Similar results are recently reported by Rumokoy et al. (2023) using a firm-level sample of the metal and mining industry in Australia. The findings of this study support the real options channel and hence, a negative relationship. In a related context, Kim and Mun (2022) investigate the impact of terrorist attacks on corporate investments using U.S. firm-level data within all industries except the financial and utility industries. More specifically, the tourist inflow is affected because of terrorist incidents (Aloui et al., 2021). Their results suggest that the relationship is primarily negative except for the firms with overconfident Chief Executive Officers (CEOs). While studies are broadly conducted in the context of the developed world, the focus on emerging markets has been limited. Adding to the gravity of the issue is the fact that the hotel and restaurant industry is mainly capital-intensive. Further, it is evident from previous studies that tourist arrivals are vulnerable to a state of uncertainty (Demir and Gözgör, 2018). Consequently, the performance of the firms in the hotel and restaurant industry may suffer in the phases of high uncertainty (Ozdemir et al., 2023). Thus, rising uncertainties and limited tourist arrivals may discourage firms in this industry from undertaking investments (Akron et al., 2020).

It is worth mentioning that most of these studies related to the firms in the hospitality industry consider EPU to be a proxy of uncertainty as it affects tourism in various ways (see Ersan et al., 2019; Gong et al., 2024; Khan et al., 2021; Lee and How, 2023; Man Wai Leong et al., 2024; Payne and Apergis, 2022). While we concur that EPU is a good measure of uncertainty, we also argue that the firms in this industry may stand more vulnerable to GPR than EPU. This argument seems logical as EPU mainly consider uncertainties related to economic or political nature where risks of losing lives or a severe physical injury are relatively minuscule. In the case of GPR, the exposure to probable war casualties and adverse economic consequences is relatively extreme. 8 Further, the impacts of GPR in this industry can aggravate in the case of emerging markets with higher institutional voids. Therefore, we examine the effects of GPR on the hotel and restaurant industry firms in an emerging market, that is, India. In light of the above discussion, we form our first hypothesis:

GPR negatively affects the corporate investments of firms in the hotel and restaurant industry. The second channel (i.e., ‘cost of external financing channel’) argues that under conditions of uncertainty, the default risk is high, and so is the risk premium on borrowings by the firm (Pástor and Veronesi, 2013). While it is relatively easy to conceive that a higher cost of credit under uncertainty (Kaviani et al., 2020) would affect corporate investments (Gilchrist et al., 2014), it is interesting to understand how firms with relatively lower financing constraints behave under such conditions. Firms can fund their planned investments from internally generated capital or from raising external financing. Simply put, a firm can be regarded as less constrained if it has sufficient resources to fund its investment plans (Kaplan and Zingales, 1997). In the hospitality industry, customers primarily derive value from the quality of their living and dining experiences (Weiermair and Fuchs, 1999). To augment service quality, these firms must invest recurrently. A discontinuity to upgrade or renovate existing facilities may affect customer satisfaction. Under the state of uncertainty, firms may have limited access to external funding due to higher risk premiums. Thus, it is instinctive that firms with constrained internal capital will refrain from investing. However, questions like how the firms with sufficient internal capital (less constrained) respond in such a situation and whether these firms use internal capital to mitigate the investment cut in response to GPR are worth examining. However, theoretically, as uncertainties amplify, the option value to wait for precise information increases (Dixit et al., 1994). Thus, managers are better off adopting a “wait and watch” approach, especially when these investments are irreversible (Bernanke, 1983). Since the firms in this industry typically invest in irreversible projects (Akron et al., 2020), the managers, even in the lesser constrained firms, may refrain from investing under uncertainties prompted by GPR. Nevertheless, it is also reasonable to argue that the lesser constrained firms may be marginally less impacted (in undertaking new investments) than more constrained firms. This leads to our second hypothesis:

GPR negatively affects the corporate investments of firms in the hotel and restaurant industry; even when they are less constrained, the impact is not completely mitigated.

Data and research design

Sample selection

In this article, we assess the impact of GPR on corporate investments, using a sample of Indian firms in the hotel and restaurant industry spanning the years 2003 to 2020. Our sample period starts in 2003 as the data for one of the critical control variables (Economic Policy Uncertainty (EPU) for India) 9 is available from 2003. The accounting data is extracted from the Centre for Monitoring Indian Economy’s (CMIE) Prowess database. To finalize our sample, we drop firm-year observations with missing values. In addition, the variables are winsorized at 1% and 99% of the distribution to eliminate the influence of outliers. Finally, our sample for analysis is condensed to 3943 firm-year observations for 395 hotel and restaurant industry firms. The key independent variable GPR is represented by the GPR index created by Caldara and Iacoviello (2022). 10

Measurement of variables

Measuring corporate investments

The dependent variable, corporate investment, is defined as the annual capital expenditure scaled by lagged total assets (CAPEX/TA) following the previous literature (Akron et al., 2020; Bates et al., 2009; Gulen and Ion, 2016; Wang et al., 2019). Also, following Akron et al. (2020), an alternative measurement of corporate investment is modelled for testing the robustness of our baseline results. In this case, the annual capital expenditure scaled by lagged total revenues (CAPEX/TR).

Measuring GPR and other macro uncertainties

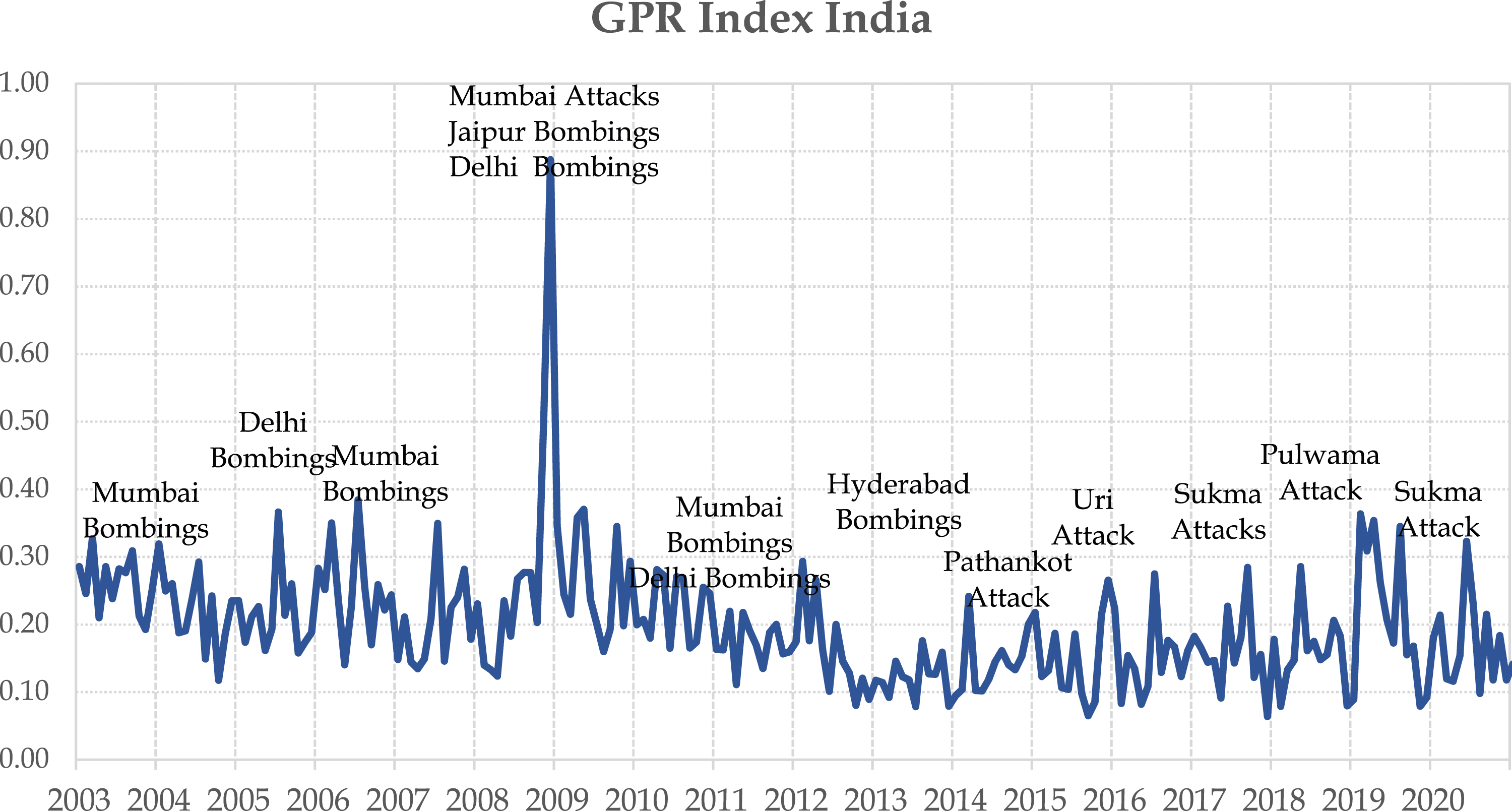

The variable of interest in our study is GPR, which is proxied by the GPR index constructed by Caldara and Iacoviello (2022). Several studies in the recent past have used this index as a measure of geopolitical uncertainty (Das et al., 2019a, 2019b; Demiralay and Kilincarslan, 2019). We use the Indian GPR index, which is constructed based on the count of the number of articles appearing in leading national newspapers discussing the events of geopolitical conflicts. The predefined set of keywords used to construct the index include words such as: ‘war,’ ‘insurrection,’ ‘rebel,’ ‘nuclear missile,’ ‘atomic war,’ ‘bomb,’ ‘hostage,’ ‘terror attacks,’ ‘insurgency’ and many others. The Indian GPR index over the study period is exhibited in Figure 1, which indicates some critical geopolitical events. Geopolitical risk in India. This figure plots the continuous spectrum of geopolitical risks in India for a period spanning from 2003 to 2020. The figure also highlights some of the crucial historical events.

Since the GPR index is available at a monthly frequency, following Akron et al. (2020), we consider the annual average of the monthly natural logarithmic GPR value (GPRL.Avg.) to match the yearly frequency of the firm-level data. This measure is primarily used for our baseline and subsequent regression model estimates. In addition, we will consider two alternative specifications of the GPR index to test the stability of our estimates. The first is the highest value of the monthly natural logarithm of GPR (GPRL.Max.) in a year. Further, the first logged difference in annual GPR data (ΔlnGPR) is the second alternative specification. Lastly, we also include the annual natural logarithmic average of international GPR (GPRL.International) and GPR threat (GPRL.Threat) to perform robustness checks.

Wang et al. (2019) argue that it is critical to distinguish GPR’s impact from other macroeconomic uncertainties. This approach could help control confounding effects. Thus, we control for two crucial sources of uncertainties, the Indian EPU (EPU) and the Financial Stress Index (FSI), in our baseline estimates. The EPU index will control for uncertainties arising from economic and political instabilities, such as expectations related to changes in government, tax regime, monetary policy, and regulations, among others. We use the Indian version of the EPU index provided by Baker et al. (2016). 11 Similarly, to control for stressed financial conditions in the economy, we consider the FSI of India. This is a composite index suggested by Park and Mercado (2014) that captures the stress in four major financial markets: (a) the banking sector, (b) the equity market, (c) the debt market, and (d) the foreign exchange market. 12 Like GPR, we also took an annual natural logarithmic average of EPU. In the case of FSI, we take only the annual average of FSI following previous literature as it encompasses negative values during the phases of low-stress periods (Das et al., 2022a, 2022b).

Measuring other control variables

We control for all firm characteristics that are likely to determine corporate investments. The control variables, such as Growth opportunities, Cash flows, Firm size, Leverage and Profitability, are considered following Gulen and Ion (2016), Wang et al. (2019), and Akron et al. (2020). Further, Non-debt tax shields and Liquidity are controlled in congruence with Keating and Zimmerman (1999). These financial variables indicate different aspects of a firm’s performance, financial health, and potential growth, providing a comprehensive picture of its operational and financial standing for undertaking corporate investments. Investments in hospitality firms greatly rely on growth opportunities as they are motivated to invest in new facilities or renovate existing ones to capture market share and improve customer experiences. Cash flow availability is crucial as it provides internal funding, reduces reliance on external financing, and enables firms to finance capital projects while maintaining liquidity. Additionally, larger firms generally have more resources and access to capital, allowing them to leverage economies of scale and undertake significant investments.

Leverage has a dual impact on investments as high debt levels can restrict investment due to debt obligations, but it can also facilitate investments when borrowing costs are manageable. Profitability enhances investment potential, as profitable firms can reinvest earnings into capital projects without increasing debt. However, low profitability limits investment capabilities, pushing firms to prioritize essential projects. Non-debt tax shields, like depreciation and tax credits, lower the effective tax burden, enabling firms to conserve cash and reinvest in physical assets. Finally, liquidity is essential for ensuring firms meet operational expenses while investing in capital projects. Finally, high liquidity allows firms to make timely investments, whereas low liquidity might constrain investments due to a focus on cash preservation. Together, these factors shape the investment strategies of hospitality firms, which is essential to control. The construction of these variables is elaborated in Appendix A1.

Descriptive statistics

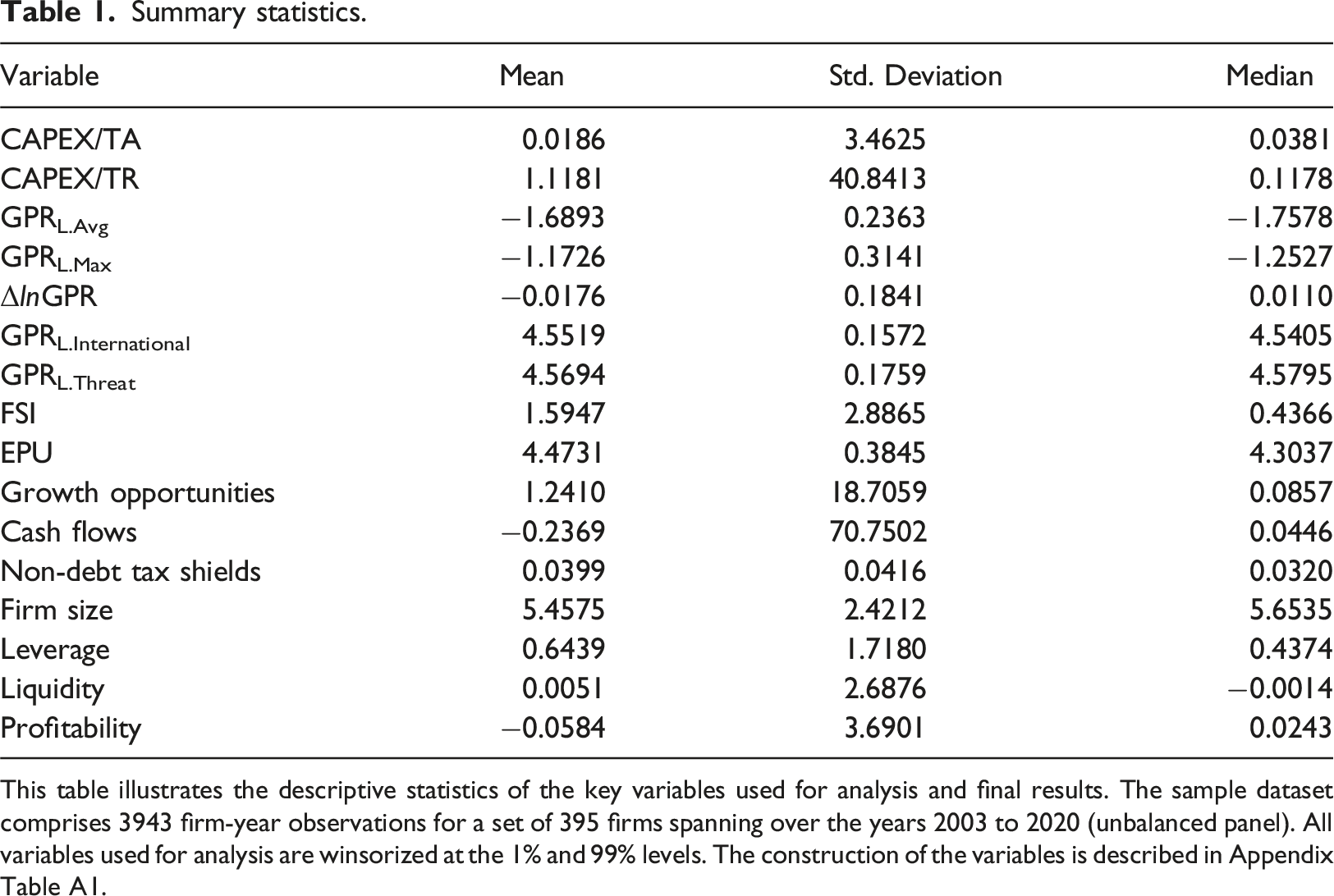

Summary statistics.

This table illustrates the descriptive statistics of the key variables used for analysis and final results. The sample dataset comprises 3943 firm-year observations for a set of 395 firms spanning over the years 2003 to 2020 (unbalanced panel). All variables used for analysis are winsorized at the 1% and 99% levels. The construction of the variables is described in Appendix Table A1.

Model specifications

We specify a similar baseline model following Wang et al. (2019) to explore the empirical relationship between GPR and corporate investments. The regression specification for testing the first hypothesis is expressed as follows:

We first select a measure of financing constraint to test how heterogeneity affects the relationship between GPR and corporate investments. To that end, following the literature, we consider average net worth to be an indicator of financing constraints (Bose et al., 2021). 14 To devise our empirical strategy, we follow a similar regression framework as Fan et al. (2021). The model expressed in eq. (1) is first re-estimated by way of a sub-sample analysis (stated as eq. (2)). The sub-sampling is done by bifurcating our sample based on the median of average net worth. Firms with an average net worth above the median are classified as ‘lesser constrained’ (sub-eq. (2.i)), ‘constrained’ (sub-eq. (2.ii)) otherwise. 15

Thus, the equation is to be re-estimated as:

In addition, we also use an interaction term between GPR and lesser constraints dummy (LESS) to gauge the moderating effects of financing constraints. The variable of interest in our case is GPR*LESS; it captures the impact of lesser financing constraints on the relationship between GPR and corporate investments. If lesser financing constraints can mitigate the negative impact of GPR on corporate investments, then the coefficient of the interaction term (GPR*LESS) should be positive. Thus, the revised eq. (1) is specified as follows:

Empirical results and discussion

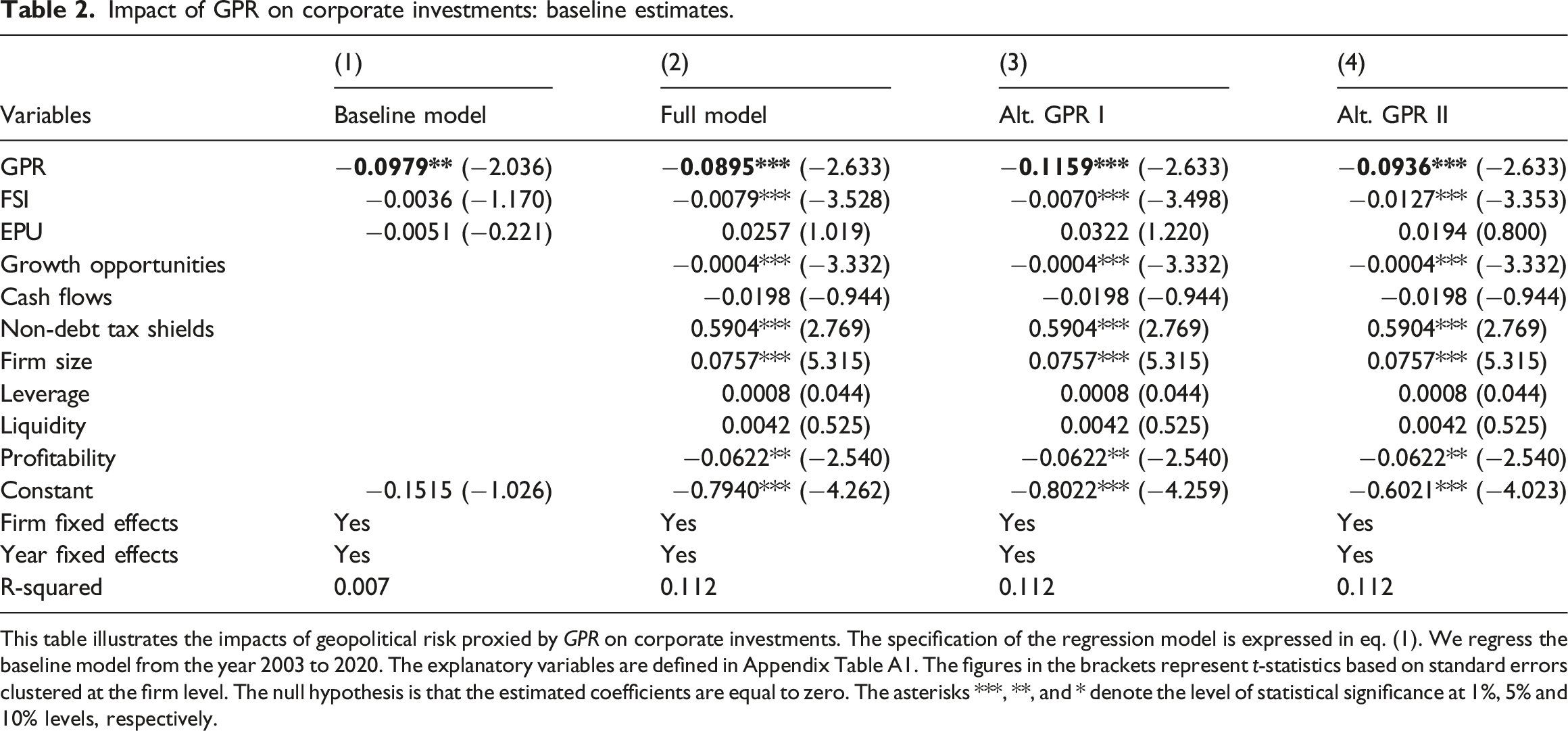

Impact of GPR on corporate investments: baseline estimates.

This table illustrates the impacts of geopolitical risk proxied by GPR on corporate investments. The specification of the regression model is expressed in eq. (1). We regress the baseline model from the year 2003 to 2020. The explanatory variables are defined in Appendix Table A1. The figures in the brackets represent t-statistics based on standard errors clustered at the firm level. The null hypothesis is that the estimated coefficients are equal to zero. The asterisks ***, **, and * denote the level of statistical significance at 1%, 5% and 10% levels, respectively.

In addition, we also test for two alternative measurements of GPR. In the baseline regression, we measure GPR as the annual average of the monthly natural logarithmic GPR value. In the first alternative measurement (Alt. GPR I), we consider GPR as the highest value of the monthly natural logarithm of GPR in a year. The coefficient of GPR again appears significantly negative in Column (3). The second alternative measure of GPR (Alt. GPR II) is constructed as the first logged difference in annual GPR. The result for the regression model with Alt. GPR II is reported in Column (4), which reiterates similar findings. Overall, the significant and negative associations between GPR and corporate investments are robust across the alternative GPR measurement specifications.

The results above support our first hypothesis, and the findings are consistent with the past literature and the theoretical prediction of the ‘real options channel’ (Akron et al., 2020; Caldara and Iacoviello, 2022). The GPR coefficients of Alt. GPR I and Alt. GPR II are not only significantly negative but also marginally strong compared to the GPR coefficient in the baseline model. Such a finding re-emphasizes the severity of GPR in terms of business confidence and new investments. Further, another interesting observation is that while the coefficients of GPR are consistently negative across various specifications, the coefficients of EPU remain largely insignificant. This phenomenon is somewhat concomitant with the findings of Tiwari et al. (2019), who argue that in India, the negative impacts of GPR on tourism are direr than those of EPU. Lastly, the coefficients of FSI are mostly negative and significant. This finding is consistent with the theoretical intuition as financial stress will widen the credit market frictions and restrict new investments (Ko, 2022).

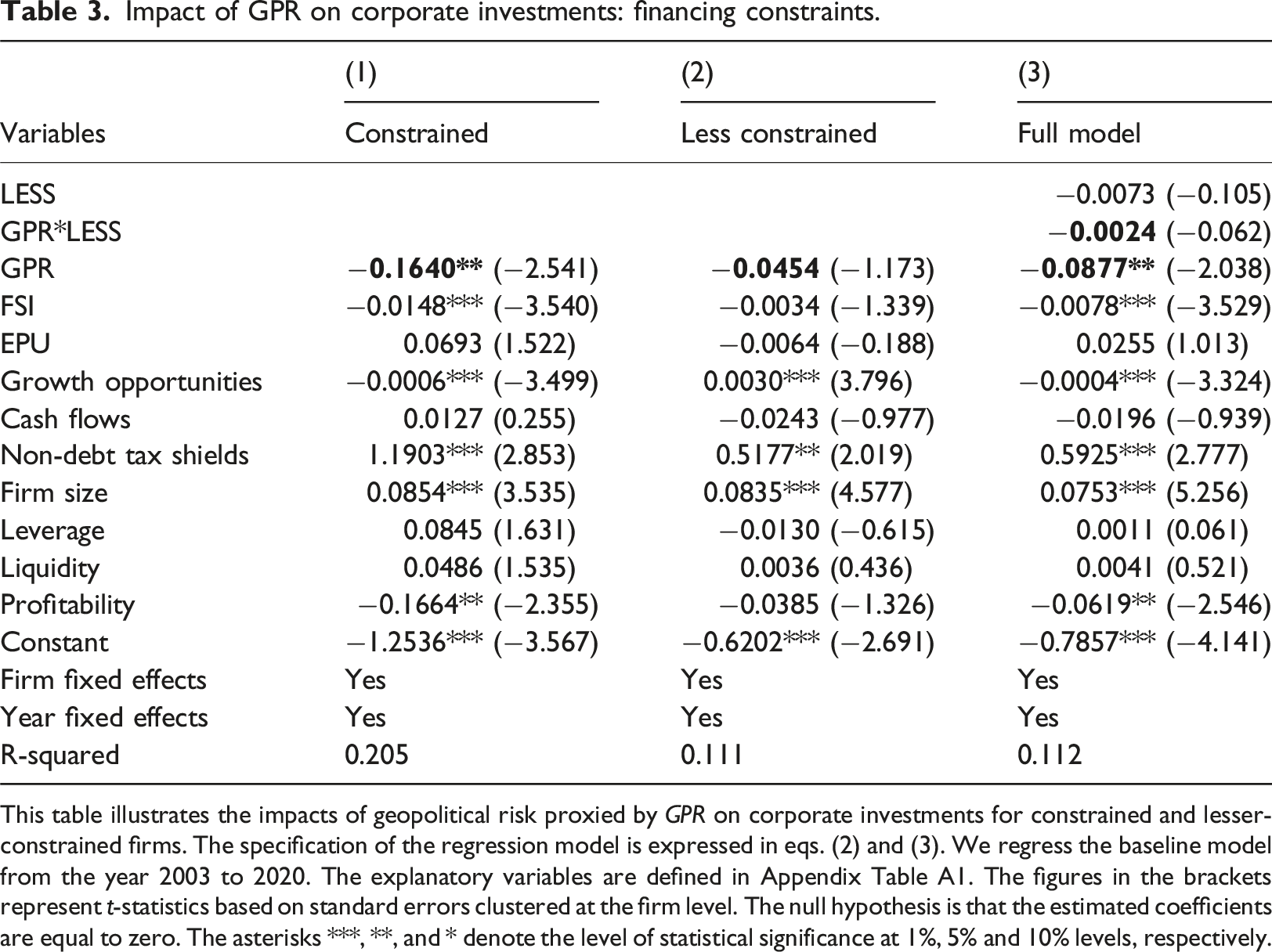

Impact of GPR on corporate investments: financing constraints.

This table illustrates the impacts of geopolitical risk proxied by GPR on corporate investments for constrained and lesser-constrained firms. The specification of the regression model is expressed in eqs. (2) and (3). We regress the baseline model from the year 2003 to 2020. The explanatory variables are defined in Appendix Table A1. The figures in the brackets represent t-statistics based on standard errors clustered at the firm level. The null hypothesis is that the estimated coefficients are equal to zero. The asterisks ***, **, and * denote the level of statistical significance at 1%, 5% and 10% levels, respectively.

This result supports our hypothesis that the severity of GPR may only be reduced for the lesser constrained firms; however, it cannot be eliminated completely. Such a result can also be predicted theoretically using the ‘cost of external financing channel.’ The firms that are more dependent on external financing may have to cut down investment spending more aggressively compared to their peers with fewer constraints. Another interesting observation is that while the coefficient of FSI is significantly negative for constrained firms, as reported in Column (1), it is insignificant for lesser constrained firms in Column (2). The FSI indicates stressed conditions in the debt and banking sector. In a way, it re-emphasizes the higher vulnerability of constrained firms to credit market frictions.

Finally, we consider the full model reported in Column (3). In this result, our coefficient of interest in the interaction term between GPR and lesser constraints dummy (LESS) is used to reaffirm the moderating effects of financing constraints. The interaction term coefficient (GPR*LESS) should be positive if the lesser financing constraints eradicate the adverse influence of GPR. We observe a consistent result as reported in the sub-sample analysis. The interaction term coefficient (GPR*LESS) stands negative, however insignificant. Thus, the results confirm that even firms with relatively lower reliance on external financing may fail to neutralize the severity of GPR upon investments. 16

Further analysis

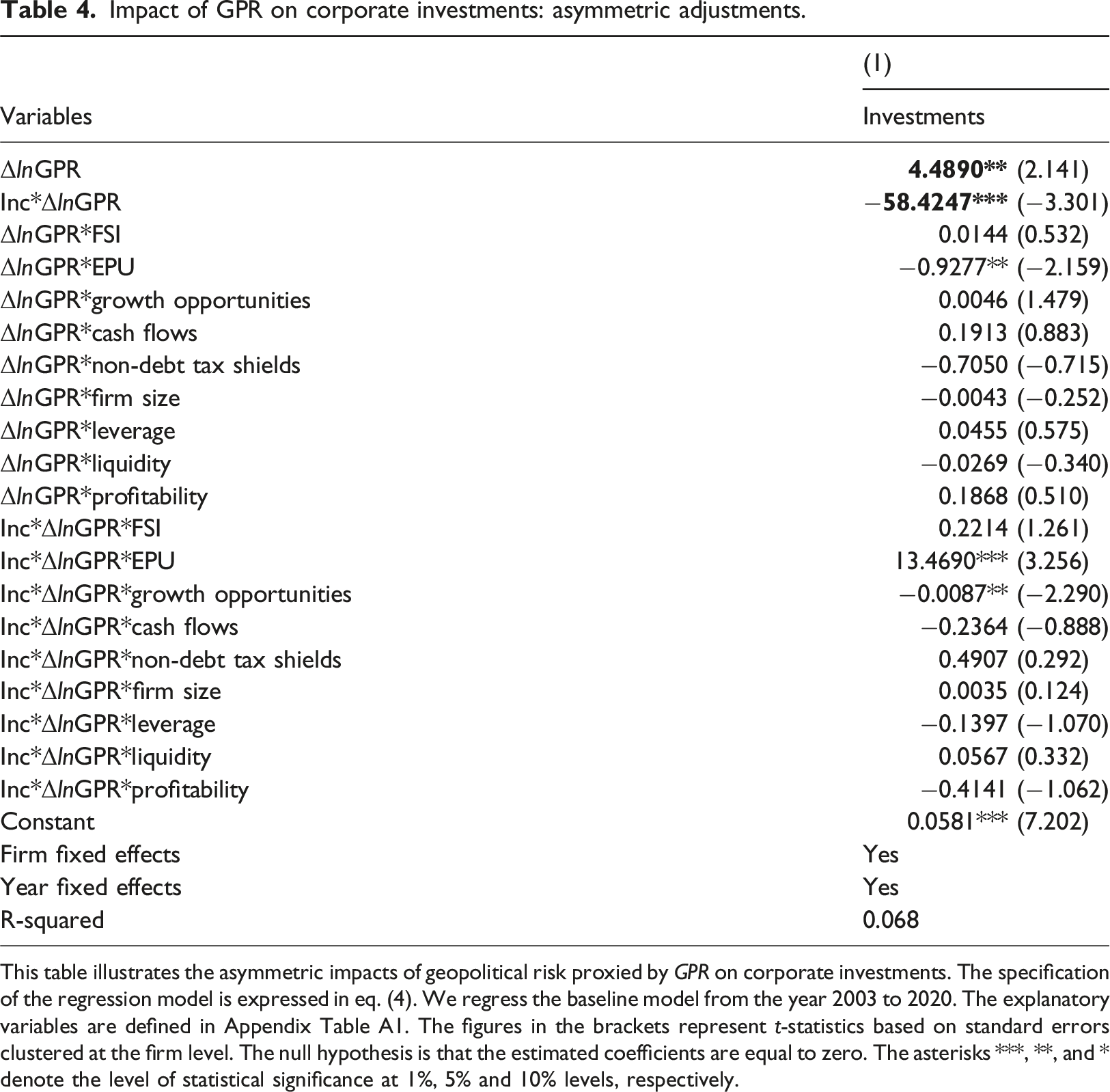

This section furthers our understanding by exploring two additional dimensions of the relationship between GPR and corporate investment. First, we examine whether GPR has an asymmetric impact on corporate investment. Second, we also evaluate whether the deficit in the deployment of security forces can exacerbate the negative impact of GPR caused by perceived weaker enforcement of law and order. In addition to the basic results, these findings can be useful from the perspective of policy formulation in practice. We initially assess the asymmetric corporate investment adjustments by firms. To achieve this objective, we modify the regression model specified in eq. (1) by following the asymmetric adjustment models suggested by Anderson et al. (2003). The revised regression model is specified below:

Impact of GPR on corporate investments: asymmetric adjustments.

This table illustrates the asymmetric impacts of geopolitical risk proxied by GPR on corporate investments. The specification of the regression model is expressed in eq. (4). We regress the baseline model from the year 2003 to 2020. The explanatory variables are defined in Appendix Table A1. The figures in the brackets represent t-statistics based on standard errors clustered at the firm level. The null hypothesis is that the estimated coefficients are equal to zero. The asterisks ***, **, and * denote the level of statistical significance at 1%, 5% and 10% levels, respectively.

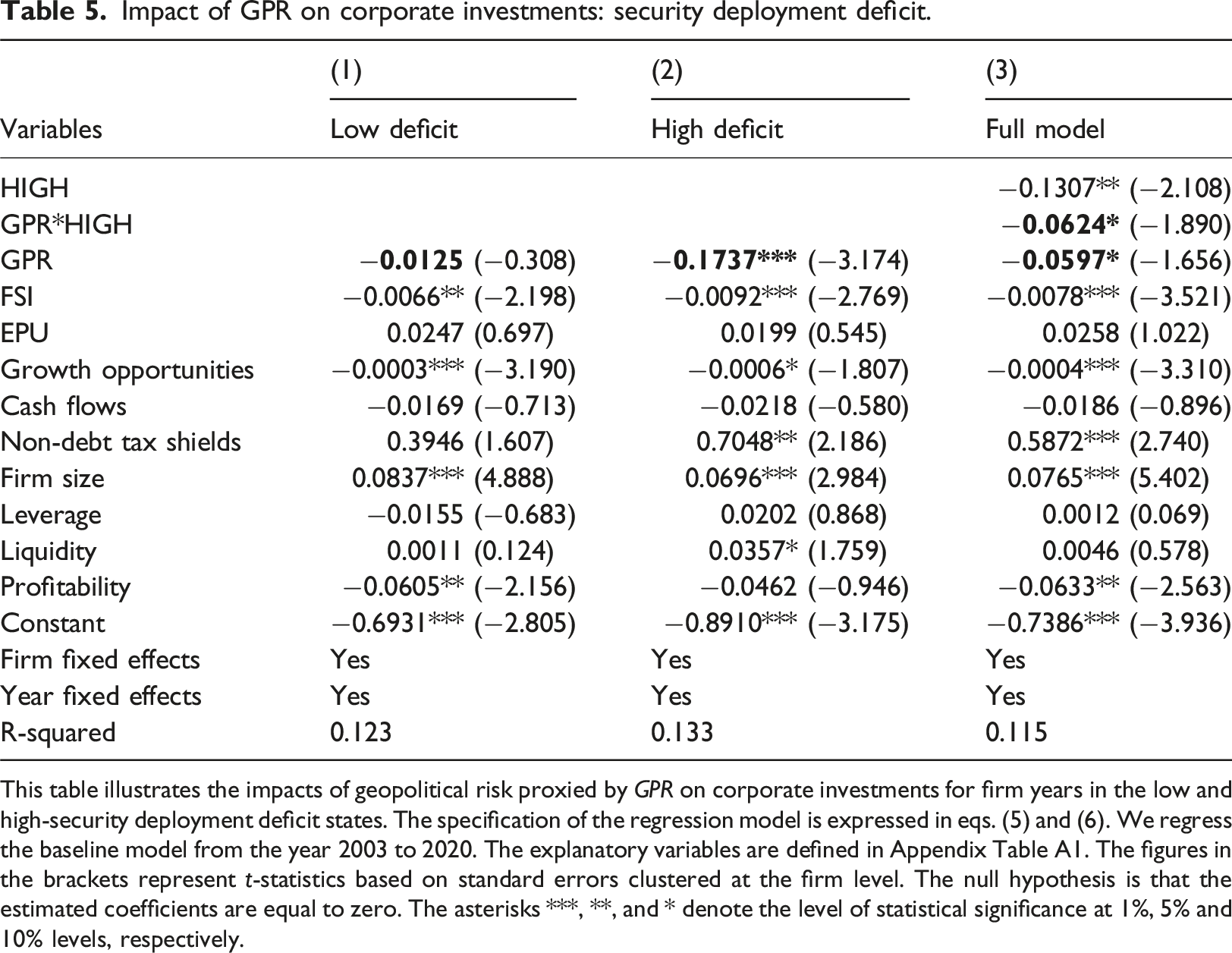

We further explore whether the deficit in the deployment of security forces can accentuate the influence of GPR on corporate investments. In India, police forces are delegated the responsibility of enforcing civil law and order. They are also the most perceptible representative of the government in the hour of crisis. 19 Nevertheless, it is somewhat paradoxical to note that India’s police force is also one of the weakest in the world in terms of the public-to-police ratio. The United Nations (U.N.) has recommended an optimal ratio of 222 police personnel per 1,00,000 population. However, there are only 144 police personnel per 1,00,000 population in India. 20 Consequentially, under-deployment of police personnel leads to a higher workload and poor work-life balance. For instance, a recent survey by the Centre for the Study of Developing Societies (CSDS) reveals that average police personnel work for 14–16 h a day. 21 These factors could be attributed as the antecedents for inefficient police action and security lapses eroding public confidence in them.

Impact of GPR on corporate investments: security deployment deficit.

This table illustrates the impacts of geopolitical risk proxied by GPR on corporate investments for firm years in the low and high-security deployment deficit states. The specification of the regression model is expressed in eqs. (5) and (6). We regress the baseline model from the year 2003 to 2020. The explanatory variables are defined in Appendix Table A1. The figures in the brackets represent t-statistics based on standard errors clustered at the firm level. The null hypothesis is that the estimated coefficients are equal to zero. The asterisks ***, **, and * denote the level of statistical significance at 1%, 5% and 10% levels, respectively.

Next, we also use an interaction term between GPR and high-security deployment deficit dummy (HIGH) to captivate the moderating effects of security deployment. The variable of interest in our case is GPR*HIGH; it describes the impact of a high-security deficit on the relationship between GPR and corporate investments. If a high-security deficit exacerbates the negative impact of GPR on corporate investments, then the coefficient of the interaction term (GPR*HIGH) should be negative and significant. Thus, the revised eq. (1) specification is as follows:

The empirical results derived from eq. (6) are reported in Column (3), Table 5. The results restate our findings of the sub-sample analysis. Our coefficient of interest GPR*HIGH remains negative and statistically significant. Thus, the empirical evidence suggests that the degree of security implementation can mitigate the impediments of GPR on corporate investments.

Robustness test results

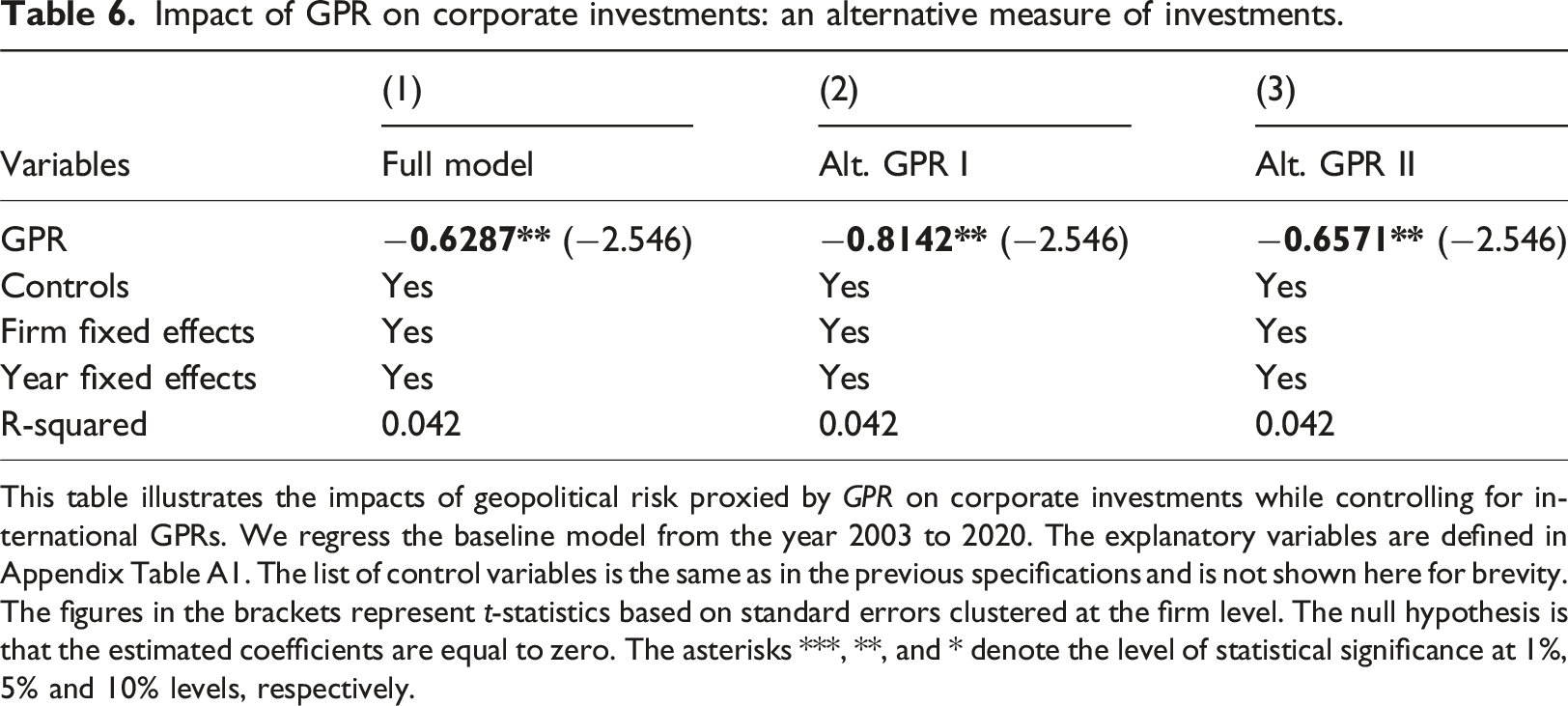

Impact of GPR on corporate investments: an alternative measure of investments.

This table illustrates the impacts of geopolitical risk proxied by GPR on corporate investments while controlling for international GPRs. We regress the baseline model from the year 2003 to 2020. The explanatory variables are defined in Appendix Table A1. The list of control variables is the same as in the previous specifications and is not shown here for brevity. The figures in the brackets represent t-statistics based on standard errors clustered at the firm level. The null hypothesis is that the estimated coefficients are equal to zero. The asterisks ***, **, and * denote the level of statistical significance at 1%, 5% and 10% levels, respectively.

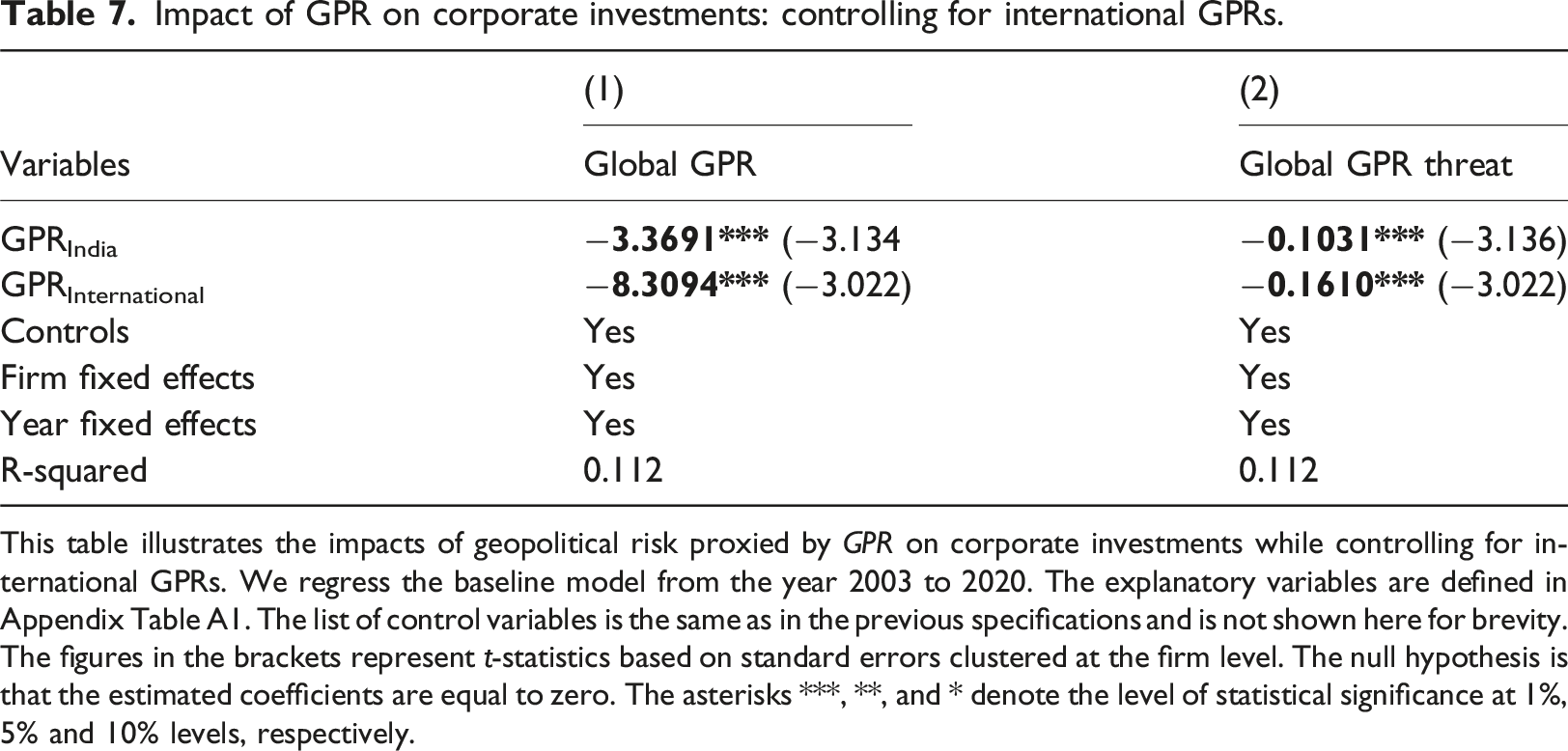

Impact of GPR on corporate investments: controlling for international GPRs.

This table illustrates the impacts of geopolitical risk proxied by GPR on corporate investments while controlling for international GPRs. We regress the baseline model from the year 2003 to 2020. The explanatory variables are defined in Appendix Table A1. The list of control variables is the same as in the previous specifications and is not shown here for brevity. The figures in the brackets represent t-statistics based on standard errors clustered at the firm level. The null hypothesis is that the estimated coefficients are equal to zero. The asterisks ***, **, and * denote the level of statistical significance at 1%, 5% and 10% levels, respectively.

Conclusions and policy implications

In conclusion, our study provides critical insights into the intricate relationship between GPR and corporate investment in India’s hotel and restaurant industry. By investigating the impact of GPR on corporate investments, we extend the existing literature on how firms respond to geopolitical uncertainty, specifically in the context of emerging markets. The findings confirm that GPR has a significant and negative effect on investment levels within the hospitality sector, reinforcing previous research that emphasizes the pervasive influence of geopolitical tensions on corporate decision-making.

A key contribution of this study is the identification of an asymmetry in how firms respond to geopolitical risk. Our research reveals that firms react more sharply to increases in GPR than to its decline. When geopolitical tensions rise, firms exhibit a pronounced reduction in investments, indicating a heightened sensitivity to adverse events and a risk-averse approach during periods of uncertainty. Conversely, when GPR levels decrease, firms are less responsive in resuming or ramping up their investments. This asymmetry underscores the disproportionate impact of geopolitical instability on business strategies and the cautious nature of firms in re-entering investment cycles after periods of elevated risk.

Interestingly, the study finds that internal financing, which is typically considered a buffer against external shocks, does not significantly shield firms from the negative effects of geopolitical risk. This finding challenges the conventional wisdom that internal financial resources can help firms maintain stability during turbulent times. Instead, it highlights the all-encompassing nature of geopolitical uncertainty, which can disrupt even those firms with relatively robust financial health. This insight is particularly relevant for policymakers and business leaders, underscoring the need for broader risk management strategies beyond financial hedging.

A notable finding in our research is the mitigating role of security measures. We find that firms located in better security infrastructure are better able to withstand the negative impacts of GPR. This suggests that perceptions of safety and security play a crucial role in maintaining business continuity in the face of geopolitical threats. By deploying appropriate security measures, firms can reduce the adverse effects of GPR on investment decisions, highlighting the importance of a proactive approach to risk management. In an industry like hospitality, where customer perceptions of safety are paramount, this finding is particularly significant.

Our study also has broader implications for other emerging markets facing similar geopolitical challenges. The insights gained from India’s hospitality sector can be applied to industries in other countries where geopolitical instability is a concern. We advocate for the adoption of comprehensive risk management strategies that include both financial and non-financial measures, such as enhanced security protocols and resilience-building initiatives.

In light of these findings, we suggest that future research should explore the effects of GPR on other aspects of corporate decision-making, particularly revenue expenditures. Understanding how firms adjust their operational spending in response to geopolitical uncertainty could offer valuable insights into their adaptive strategies. Additionally, examining the role of government policies in mitigating the effects of GPR on industries would provide further clarity on how external interventions can support corporate resilience.

Overall, this study enriches the understanding of how GPR affects corporate investments, particularly in emerging markets. It offers actionable recommendations for firms and policymakers to overcome uncertain geopolitical landscapes, emphasizing the importance of proactive risk management and security measures to safeguard investments and ensure long-term growth in the hospitality sector.

Lastly, despite its contributions, this study has certain limitations. First, it focuses exclusively on India’s hotel and restaurant industry, limiting generalizability across other sectors or countries. Future research should explore different industries and regions to better understand the broader effects of GPR. Second, we rely on aggregate GPR indices, which may not fully capture the impact of specific events. Future studies could examine firm-level exposure to explore the granular impacts of GPR on individual companies. Additionally, the role of government policies in mitigating GPR effects warrants further investigation to develop more comprehensive risk management strategies. Nevertheless, these limitations facilitate future research.

Supplemental Material

Supplemental Material - The role of security measures: Addressing geopolitical risk in Indian hospitality investments

Supplemental Material for The role of security measures: Addressing geopolitical risk in Indian hospitality investments by Debojyoti Das, Pranav Dharmani, Anupam Dutta and Sankarshan Basu in Journal of Tourism Economics.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.