Abstract

Considering the growing significance of CSR in the corporate world, this study critically reflects the extant CSR literature and CSR practices, and proposes a conceptual CSR framework, called Strategic CSR, to highlight the importance of developing and implementing CSR practices that can create and optimize both social and business value. Strategic CSR incorporates four existing concepts and frameworks: creating shared value, enlightened stakeholder theory, resource-based theory, and CSR fit perspective. The essential argument for Strategic CSR is that businesses should develop and implement CSR practices that are directly related to the businesses’ core operations and competencies. This study also discusses several additional important issues to consider in developing and implementing Strategic CSR to enhance the understanding of the framework along with tourism and hospitality industry examples. This study conducted survey of which results generally support the proposed framework. Lastly, the study suggests several research directions for CSR scholars.

Keywords

Introduction

Social responsibility has always been an integral aspect of the business whether it was evident to the public or not. Since the Industrial Revolution, it has become more prominent mainly due to businesses’ growing size and influence (Carroll, 2008). The modern concept of corporate social responsibility (CSR) is generally believed to have originated in the 1950s (Carroll, 1999). Ever since, the concept and practice of CSR have gradually evolved over the following several decades, receiving persistent attention in the academic literature. Especially, in the 2000s, CSR attracted even more significant attention, including the tourism and hospitality literature. While sustainability (i.e., environmental) issues have undeniably fueled public and corporate interest in CSR, a shift towards viewing CSR from a broader perspective has also contributed to this surge. People used to perceive CSR as purely philanthropic with little consideration for its business rationales. For example, Milton Hershey, the founder of The Hershey Company, invested in the local community by providing affordable housing and improved community services for his employees. Furthermore, he founded the Milton Hershey School (formerly known as the Hershey Industrial School) for orphans with most of his wealth.

However, today, an increasing number of business professionals and CSR scholars argue that a firm’s CSR investment should be considered integral to its core business strategies (Lee et al., 2023) because only in that sense, CSR investments will consistently create not only social but also business value, and become sustainable through all economic conditions including recessions. Some refer to this concept as Strategic CSR (e.g., Chandler, 2017; Kuokkanen and Sun, 2020; Kuokkanen and Sun, 2024; Lee, 2022), while others call it Integrated CSR (Wicks et al., 2010). The current study denotes the concept as Strategic CSR, and discusses its application in the tourism and hospitality context. In essence, we propose that Strategic CSR is a CSR strategy that a firm implements as a part of its core business strategies, meaning that it must be directly linked to the firm’s core business competencies and operations. Accordingly, Strategic CSR aims to create social and environmental value as well as business value, similar to a firm’s product and marketing strategies.

To lay out the foundation and propose the concept of Strategic CSR, this study will discuss various issues concerning CSR. First, the study will explore definitions of CSR, noting variations in them. Specifically, we will highlight two distinct types among various definitions of CSR to frame the discussion around the concept of Strategic CSR. Next, the study will introduce the concept of Strategic CSR grounded on the framework of creating shared value (Porter and Kramer, 2011), the enlightened stakeholder theory (Jensen, 2001), the resource-based theory (Barney, 1991), and the CSR fit perspective (Elving, 2013). It will critically assess tourism and hospitality firms’ actual CSR practices through the lens of Strategic CSR. Following this, empirical survey data on consumers’ perceptions of CSR definitions and practices from the Strategic CSR perspective will be presented and discussed. Lastly, the study will provide research implications for future studies from the Strategic CSR perspective.

Definition of CSR

To gain a comprehensive understanding of CSR and Strategic CSR, the definition of CSR should be first discussed. However, our intention is not to exhaustively cover the various types and components of all CSR definitions (such as the work done by Dahlsrud (2008)) but rather to illustrate key distinctions among varying CSR definitions. Through this, we aim to provide readers with a better understanding of how CSR can be viewed from different perspectives. Moreover, another goal is to clarify an issue regarding Strategic CSR; it is not a new concept but has been recognized in a broad sense for some time. Based on our review of the CSR literature, many definitions of CSR encompass a range of components that fall into two general viewpoints: one that excludes anything that aligns with a firm’s interests and the other that proposes shared value between owners and other stakeholders. This section presents and compares two main CSR definitions that illustrate these differing viewpoints.

An example of the first viewpoint can be illustrated by McWilliams and Siegel (2001: 117) who define CSR as “actions that appear to further some social good beyond the interests of the firm and that which is required by law.” As of October 5, 2024, their article has been cited 11,927 times, and we firmly believe, albeit without concrete statistics, that this high citation count is predominantly due to the widespread citation of this definition in numerous CSR studies. This definition explicitly excludes any social or environmental activities by a firm as CSR activities if those activities create value for the firm. For example, consider a case in which a hotel implements an environmental program that requires guests to make a request to clean their room, meaning that when guests do not make the request, their room will not be cleaned. While this initiative is undoubtedly environmentally friendly and enables the hotel to make a positive impact on the environment through reducing resource use, it is also likely to result in cost savings for the hotel. If such savings are perceived as aligning with the firm’s interests, this environmentally friendly program would not be considered a CSR activity based on McWilliams and Siegel’s definition. Furthermore, this definition also excludes any efforts by a firm that create social and environmental value from being classified as CSR activities if the firm undertakes those activities solely to comply with laws and regulations. For example, if a restaurant in a European Union Member State uses non-plastic straws because of the regulation that banned several types of single-use plastic products including single-use plastic straws in 2021, its practice would not be considered a CSR activity based on McWilliams and Siegel’s definition because the restaurant implements the practice to comply with the regulation.

However, when interpreting McWilliams and Siegel’s definition, it is important to exercise caution and consider the firm’s overall intention to engage in CSR activity. We believe they do not mean to exclude any well-intended social and environmental programs from being considered CSR activities simply because those activities happen to generate some business value. For example, we do not expect that it is McWilliams and Siegel’s intention to strictly disqualify a restaurant firm’s donation to local childcare services in poor communities as a CSR activity simply because such donation may create a positive image for the firm, possibly resulting in an increase in revenue which aligns with the firm’s self-interests. We would interpret ‘the interest of the firm’ based on the firm’s overall intention in implementing its CSR activity. For example, if a firm genuinely cares about a hunger issue, and thus implements a donation program to help the cause, then although such an implementation would likely lead to a positive brand image and, consequently, a more significant market share, the firm’s donation program should still be considered a CSR activity even based on McWilliams and Siegel’s definition. However, if the firm’s primary intention is to create business value alongside social value through its engagement in the hunger relief program, it would not be considered a CSR activity according to McWilliams and Siegel’s definition.

An example of the latter viewpoint can be found in the definition of CSR proposed by the European Commission (EC). It is somewhat lengthy, but it is worthwhile discussing the entire definition. EC defined CSR as “the responsibility of enterprises for their impacts on society. Respect for applicable legislation, and for collective agreements between social partners, is a prerequisite for meeting that responsibility. To fully meet their corporate social responsibility, enterprises should have in place a process to integrate social, environmental, ethical, human rights and consumer concerns into their business operations and core strategy in close collaboration with their stakeholders, with the aim of maximising the creation of shared value for their owners/shareholders and for their other stakeholders and society at large, [and] identifying, preventing and mitigating their possible adverse impacts” (The European Union, 2011).

There are clear distinctions between the two CSR definitions. While McWilliams and Siegel’s definition excludes a firm’s activities from being considered CSR activities if they create business value or are undertaken merely to comply with regulations and laws, the EC views a firm’s activities that create business value and are implemented to comply with laws and regulations as CSR activities. Specifically, the EC definition states, “Respect for applicable legislation, and for collective agreements between social partners, is a prerequisite for meeting that responsibility.” Also, their previous version unequivocally states that “following the law” is a part of CSR. This implies that even when a firm implements social and environmental activities that adhere to regulations and laws, such activities are considered CSR activities. Accordingly, based on the EC definition of CSR, the restaurant example presented earlier regarding the use of non-plastic straws due to the EU regulation should be classified as a CSR activity. This definition also aligns well with the Pyramid of CSR model proposed by Carroll (1991) where the legal dimension is part of the four CSR dimensions (i.e., Discretionary, Ethical, Legal, and Economic).

Moreover, we should pay attention to the concept of ‘shared value’ between owners and other stakeholders, mentioned in the EC definition. Porter and Kramer (2011) proposed the concept of ‘Creating Shared Value” (CSV), which promotes activities that simultaneously create social (including environmental) and business values. The EC definition appears to have embraced the same concept, suggesting that a socially responsible firm should create value for various stakeholders (e.g., local communities, consumers, suppliers, etc.) and society at large, as well as for its owners/shareholders. In other words, a socially responsible firm should aim to generate social, environmental, and business values concurrently, where the business value is not an accidental byproduct of its well-intended CSR activities. The EC definition clearly states that the creation of this business value must be maximized along with social and environmental value. In other words, if a firm implements activities that only create social/environmental value, not business value, such activities are not considered CSR activities based on the EC definition. This represents a significant difference between the two types of CSR definitions and directly relates to the concept of Strategic CSR proposed in this study. Accordingly, this study supports and promotes the second viewpoint of CSR proposed by the EC.

Strategic CSR (S-CSR)

Conceptual framework

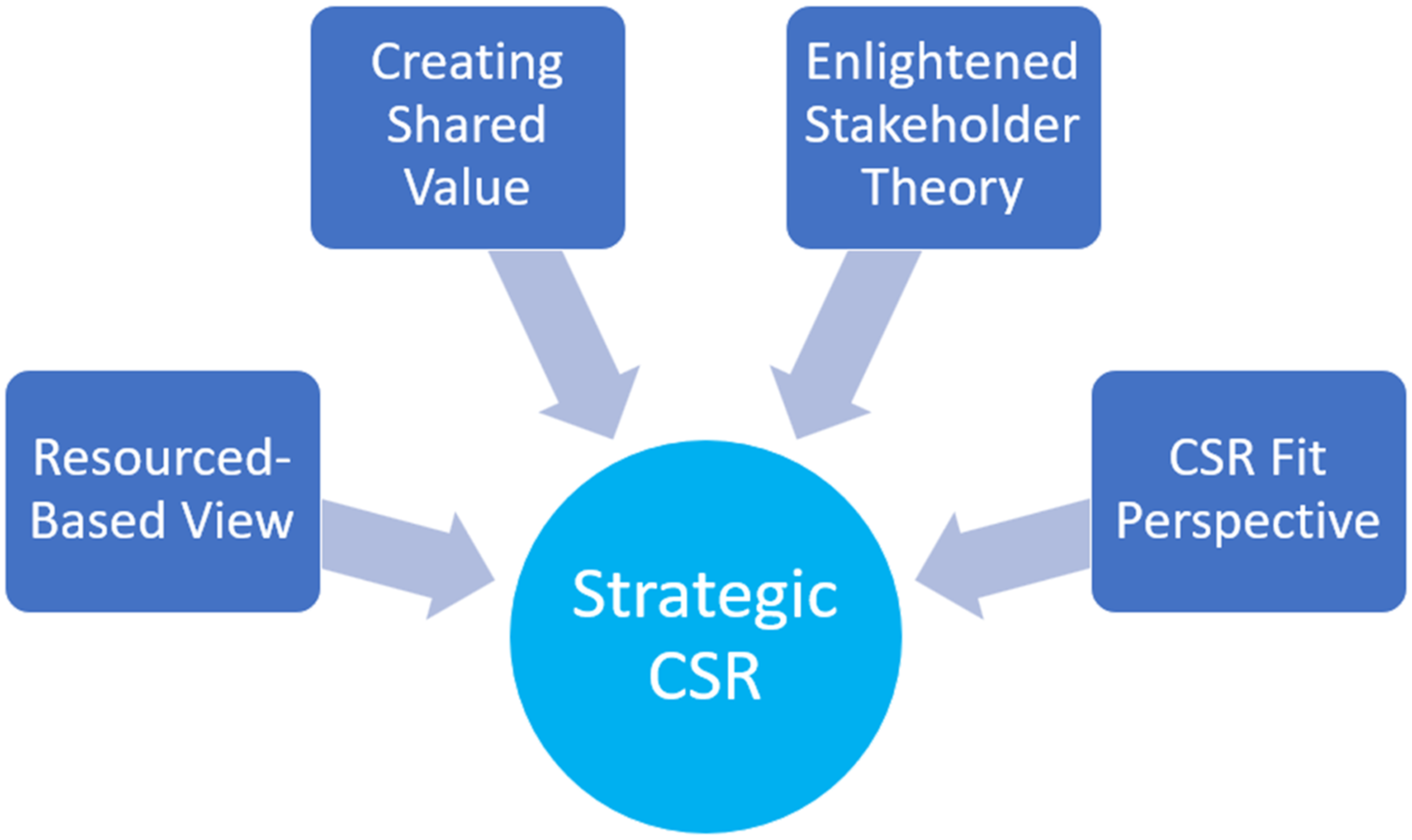

As a central concept of this paper, we propose that businesses adopt their CSR practices closely and directly related to their core business operations and competencies to simultaneously optimize both social and business value in the long term. Conversely, any value (social and/or business) created through non-strategic CSR activities (that are not directly related to the company’s core business operations and competencies) will represent non-optimized value. The concept we are proposing here, Strategic CSR (S-CSR), integrates four main conceptual frameworks from the extant literature: creating shared value, enlightened stakeholder theory, resource-based theory, and CSR fit perspective.

First, the concept of creating ‘shared value’ is incorporated into S-CSR. Porter and Kramer (2011) proposed creating shared value as the next step beyond traditional CSR, suggesting that businesses should simultaneously create both business and social value, that is, the value shared between shareholders and other stakeholders. While it is apparent that all CSR practices are intended to create social value, generating business value (or shareholder value) from these CSR practices has not always been readily accepted. Creating business value is a critical and essential component of S-CSR because, without it, businesses will struggle to sustain their CSR initiatives through varying business conditions, especially during recessionary periods. Traditional CSR often focused on philanthropic activities, where creating business value was not a focal point, but rather a secondary goal or not even a goal at all. Hence, this conventional approach to CSR investments has hindered top management teams from developing sustainable CSR strategies as, without business value, CSR investments can be seen merely as cost centers, typically the first to be cut whenever businesses struggle. By adopting S-CSR, CSR investments will create business value as a primary importance along with social value which can encourage top management teams to view CSR strategies as integral to their core business strategies. This shift of thought toward S-CSR can motivate top management teams to embrace the CSR strategy that can not only help their firm survive even the most challenging times but also improve the firm’s opportunity to create a competitive advantage through enhanced business value.

Second, the enlightened stakeholder theory proposed by Jensen (2001) is also embedded in S-CSR. Jensen (2001) expanded on the traditional stakeholder theory by introducing a critical component, maximizing long-term value. He argued that by adopting the stakeholder perspective, businesses should be able to create and maximize long-term business value. Jensen introduced the long-term component because he believed that financial markets might not immediately comprehend the full implications of companies’ CSR investments, leading to inaccurate value estimation of the investments. Therefore, financial markets need to be educated on understanding the full impacts of firms’ CSR investments, and it may take time for them to recognize the true value of the investments. Our S-CSR incorporates this long-term value aspect, aligning with Jensen’s enlightened stakeholder theory that financial markets tend to require time to realize the true value of companies’ CSR investments. Accordingly, we argue that S-CSR will create (and optimize) long-term business value from CSR initiatives.

The last two essential components integrated into S-CSR are the resource-based theory (Barney, 1991) and the CSR fit perspective (Elving, 2013). These two theories support the idea of S-CSR which tends to optimize both social and (long-term) business values. First, in the CSR context, the resource-based theory argues that a company’s CSR investment can improve its relationship with various stakeholders. For instance, CSR engagement can enhance a company’s brand image, thereby improving its relationship with customers. Similarly, it can boost employee morale, job satisfaction, and job commitment, leading to improved relationships with employees. Consequently, the company’s improved relationship with various stakeholders will likely give it a better opportunity to utilize its stakeholders’ resources.

In addition to the resource-based theory argument, the CSR fit perspective (Elving, 2013) supports the idea of how S-CSR tends to optimize both social and (long-term) business value. CSR fit refers to “the observed link between a CSR domain and a company’s products, image, positioning and/or target groups” (Elving, 2013: 281). A CSR fit is considered high or congruent when the company and the CSR appear to serve or share similar values or causes (Gupta and Pirsch, 2006) which aligns well with the argument of S-CSR that a company’s CSR should be closely and directly related to its core business operations and competencies. Various studies provide empirical support for a high CSR fit’s positive effect on CSR outcomes among relevant stakeholders (e.g., Han et al., 2013; Kuo and Rice, 2015; Elkington, 1994). These studies explain the positive effect of CSR fit with the reasoning that high CSR fit is more self-explanatory and raises fewer critical questions about the organization’s intrinsic motives (De Jong and van der Meer, 2017). In other words, a high CSR fit is believed to create a positive effect because it aligns with the public’s expectations about the types of issues the company should address (Elving, 2013). On the other hand, when there is a low CSR fit, cognitive elaboration regarding extrinsic contextual factors (e.g., competitive pressures and financial motivations) in people increases, which in turn, reduces positive reactions to CSR activities (Du et al., 2010). Additionally, De Jong and van der Meer (2017) argue that high CSR fit is judged more positively for the following intrinsic reasons: the CSR activities may be perceived (1) to be more stable and structured, (2) to have a clearer association with the organization as a whole instead of specific individual members within the organization, (3) to be more professional and less amateurish, and (4) to be an indication that social responsibility is an integral part of the organization without extrinsic (self-focused) motives. Figure 1 illustrates the framework of S-CSR with these four components. Strategic CSR framework.

Industry examples

Examples from the industry may effectively illustrate the concept of S-CSR. Starbucks implements Coffee and Farmer Equity (C.A.F.E.) practices that promote ethical sourcing. By adopting the C.A.F.E. practices, local farmers can grow coffee plants in a more environmentally friendly way while achieving enhanced yield rates and higher-quality coffee beans. As a reward, they receive a premium on coffee bean prices and a longer-term contract that enables them to have a more sustainable and stable livelihood. Quite clearly, this CSR activity is directly related to Starbucks’ core business operations and competencies centered on serving customers quality coffee, thus making the activity likely to qualify as S-CSR. By implementing this CSR initiative, Starbucks can create social value by improving local farmers’ well-being and making farming more environmentally friendly. This social value can be an optimized one because Starbucks could utilize its expertise and rich operational experience in developing the C.A.F.E. practices, with value creation continuing as long as the company’s operations are sustained. At the same time, Starbucks can also create business value by improving the quality of its products and the relationship with its suppliers. In addition, improvement in brand image, customer loyalty, and employee satisfaction (thereby reinforcing their loyalty) can be achieved.

Let’s investigate another industry example, one from Marriott. Marriott partnered with the Government of Amazonas in Brazil to protect and preserve the Amazon rainforest, a specific area called the Juma Sustainable Development Reserve, committing USD 2 million in 2008 (Guadalajara, 2016). In 2016, the State Secretary of Environment for Amazonas awarded Marriott a certificate of carbon emissions reduction for their contribution, the first such certificate ever granted by the state government to a foreign private institution partnered with a non-governmental organization in Brazil. This CSR activity by Marriott certainly improves environmental protection and conservation, thus creating social value. Marriott, however, does not possess any particular expertise in the environmental protection of rainforests. Accordingly, this CSR activity is unrelated to Marriott’s core business operations or competencies, limiting their contribution to financial support alone. Moreover, Marriott employees did not directly participate in this CSR initiative, preventing personal experience and engagement. Their experience regarding this CSR activity was likely, at the most, indirect primarily through internal communication. Hence, even though this initiative could generate a positive image and foster favorable sentiments about the company among customers and employees, such positive outcomes are expected to be limited and certainly not fully optimized. Based on our evaluation, therefore, this CSR activity by Marriott is not considered S-CSR.

However, let us consider another CSR activity by Marriott. Since 2016, Marriott has been providing human trafficking awareness training at both managed and franchised properties, achieving the milestone of training over one million associates in 2022. In recent years, Marriott has further expanded this anti-trafficking program to the entire hotel industry by making it available online. There are countless real cases and testimonies from Marriott employees highlighting their efforts in identifying and reporting on human trafficking incidents. To determine whether this CSR initiative pertains to a strategic one or not, we would again evaluate this CSR activity based on its relevance to Marriott’s core business operations and competencies. For Marriott and its employees, identifying and reporting on human trafficking incidents are integral to their hotel business operations. Moreover, Marriott employees’ close attention to their customers and business ambiance, one of Marriott’s core competencies, is fundamental to the success of this training program. Marriott leverages its expertise to effectively contribute to this program. Due to these characteristics, Marriott should be able to optimize its contributions to this social cause (i.e., optimized social value) by utilizing its resources efficiently. Due to the program, employees who either directly identify/report human trafficking cases or indirectly experience it by observing such cases are very likely to develop great pride in their jobs and organizations. This enhanced attachment to the company can improve employees’ morale and loyalty to the company, consequently reducing their turnover intention (i.e., enhanced business value), a critical issue particularly in the hotel industry. Based on this analysis, Marriott’s human trafficking awareness training is considered S-CSR.

Survey findings

We conducted a survey to understand people’s perceptions of the S-CSR concept. Specifically, we asked two types of questions: one regarding how people perceive the inclusion of economic/business value in the concept of CSR and the other concerning how people perceive CSR activities related to a business’s core operations and competencies. We used a 7-point Likert scale with 1 being strongly disagree, 4 being neither agree nor disagree, and 7 being strongly agree. We collected 310 responses in July 2023, with respondents aged 18–25 (32.6%), 26–40 (33.5%), and 41+ (33.9%). The sample included 153 males, 155 females, and two ‘others’ (no further information was provided for ‘others’).

We asked the following two questions to see how people perceive the inclusion of economic value in the concept of CSR: “Please imagine a company that actively engages in socially responsible and environmentally friendly practices that improve social well-being and environmental conditions. If such actions simultaneously help improve profitability or create economic value for the company, the company is being socially responsible” (mean value of 5.51) and “Please imagine a company that actively engages in socially responsible and environmentally friendly practices that improve social wellbeing and environmental conditions. Even if such actions do not help improve profitability or create economic value for the company, the company is being socially responsible” (mean value of 4.68). The mean value difference between the two questions is statistically significant at the 1% level, demonstrating that people more strongly perceive an activity that enhances social well-being and environmental conditions as well as creates economic value as CSR, supporting our concept of S-CSR.

Next, we asked questions on how effective a restaurant company is in implementing 11 different CSR practices. These 11 practices vary in relevance to the restaurant business’s core operations and competencies. We present only the top and bottom three responses here. First, the three CSR practices that participants perceived to be most effective for the restaurant business are: “Engagement in a food donation program for feeding the hungry” (mean value of 5.83), “Engagement in a food waste reduction program” (mean value of 5.81), and “Provision of nutritious food” (mean value of 5.75). On the other hand, the three CSR practices that participants perceived to be least effective are: “Engagement in an education program to teach computer programming to youth” (mean value of 4.86), “Engagement in an endangered species protection program” (mean value of 5.13), and “Engagement in a tree planting program” (mean value of 5.22).

For the hotel business, we asked a similar set of 11 questions (modified specifically for the hotel business). The top three CSR practices are “Provision of shelter for the homeless” (mean value of 5.73), “Engagement in a water waste reduction program” (mean value of 5.68), and “Energy consumption reduction at hotel operations” (mean value of 5.62). The three CSR practices rated least effective for the hotel business are “Engagement in an education program to teach basic automobile mechanic skills to youth” (mean value of 4.67), “Engagement in an endangered species protection program” (mean value of 4.84), and “Engagement in a tree planting program” (mean value of 5.16). These results clearly show that people perceived those CSR activities closely aligned with the business’s core operations and competencies to be more effective, supporting our argument for S-CSR.

Other things to consider in implementing S-CSR

Several issues deserve additional attention when developing and implementing S-CSR. First, the central vision of S-CSR, simultaneously creating social and business value (in the long term), needs to be openly recognized and embraced by organizations. Many businesses may be more familiar with the concept of CSR from a normative perspective, focusing on the ethical obligation to engage in CSR because it is the right thing to do rather than its potential for business value (Donaldson and Preston, 1995). Based on this normative perspective, many may even feel that creating business value from CSR is unethical. This perspective, however, has been a key deterrent for CSR to be widely and consistently practiced because businesses adopting this normative perspective typically engaged in passive CSR practices such as making donations and they stopped or reduced such engagements whenever unfavorable business environments arose. When CSR practices were implemented inconsistently in this manner, their impact on society was marginalized, and CSR was often perceived as a cost center or social tax that did not benefit the business. It is also important to note that this normative viewpoint might be prevalent among other stakeholders, such as consumers, and such a viewpoint must change. Society, including multiple stakeholders, must embrace the idea of creating business value from CSR activities. Accepting this idea will encourage businesses to integrate their CSR strategy into a valuable business strategy. This shift will lead them to invest more resources in developing the right CSR strategy and to carefully monitor, evaluate, and modify it, ensuring greater consistency in its implementation.

Second, although the concept of S-CSR applies to all stakeholders, primary stakeholders must be able to see meaningful value creation for themselves from S-CSR initiatives. Business value creation is an essential outcome of S-CSR. Therefore, attention to this matter in practice is vital for ensuring that what a company is developing and implementing is indeed S-CSR. If primary stakeholders cannot buy into a CSR investment because they have difficulty seeing meaningful business value creation, such activity will be unlikely S-CSR. At the same time, businesses should provide adequate education and information for their stakeholders (mainly primary stakeholders) regarding the potential outcomes of S-CSR activities, especially the long-term impacts, as they may not have enough knowledge to recognize the true value of S-CSR.

Third, while there are numerous relevant environmental and social issues to consider as part of a company’s CSR strategy, we argue that each company must develop its own CSR strategy by focusing on a few essential themes as its flagship CSR programs. In other words, attempting to address every issue should be strongly avoided. Reinforcing the importance of S-CSR, these focused CSR themes or programs should be highly relevant to the company’s core business operations and competencies. It is, in fact, not so difficult to understand the rationale behind this; all businesses have limited resources. In addition, many stakeholders, including primary stakeholders (consumers, employees, and investors), tend to have limited capacity to understand and remember each company’s CSR strategy. Even when evaluating one company at a time, consumers are more likely to remember the company’s CSR themes and programs when the message focuses on one or two major issues or themes (Kramer, 2018). This is particularly important to keep in mind since many businesses, especially large corporations, have a strong tendency to implement or, at least, promote as many CSR initiatives as possible. While it is essential to understand the various needs and expectations of multiple stakeholders, including non-primary ones such as activists and the local community, allocating limited resources to accommodate all those issues will be neither practical nor efficient. Aligned with this argument, the sustainability chief officer of AT&T once said in an interview that it is extremely important to say ‘no’ to many issues in order to focus on what they do best (McReynolds, 2023). Furthermore, we argue that businesses should consider both ‘relevance’ and ‘scale’ together when identifying and evaluating S-CSR practices. Some CSR initiatives can be highly relevant to the business’s core operations and competencies, while their impact scale may be marginal. Ultimately, it is important for businesses to identify those CSR initiatives that are both relevant and significant in scale so that the impact of the S-CSR initiatives can be optimized.

Fourth, organizations should not be afraid of getting criticized for their CSR practices. Recently, ‘greenhushing’ has been discussed extensively in both scholarly and practical outlets. Greenhushing is defined as a case where companies under-promote their CSR activities because they worry about being accused of greenwashing, which occurs when companies over-promote their CSR activities. Due to this concern, many companies avoid actively publicizing their CSR efforts. However, we strongly argue that as long as companies have a genuine and sincere intention to advocate for a thoroughly developed CSR strategy with a long-term plan, they should not be afraid of promoting their CSR actions appropriately (not too little or too much). While criticism is inevitable, we believe that with a strong and sincere commitment, companies should openly share their CSR efforts with their stakeholders and the public and be willing to accept constructive criticism. In responding to the critiques, companies should focus on making consistent improvements to achieve their CSR goals. When companies demonstrate a genuine and long-term commitment, stakeholders and the public will eventually recognize their true intentions regarding their CSR efforts and can even become strong advocates for the company and its CSR initiatives over time.

Nonetheless, there can be CSR cases that businesses may need to consider engaging in even when the CSR cases are not directly related to the business’s core operations or competencies. When such cases justify themselves as urgent social and environmental issues that require urgent attention, businesses may need to tackle the issues despite the lack of direct connection to the businesses’ core business operations or competencies. For example, during the height of the COVID-19 pandemic, the demand for healthcare service workers was enormous and many of them traveled to areas experiencing severe shortages in need of care. Many hotels opened their doors to such healthcare workers who did not have a place to stay, sheltering them clearly as a socially responsible act. In this instance, hotels leveraged their business competency and capacity to help society, thus maximizing social value through their actions. However, if the shortage of accommodations continues despite the support from many hotels, other businesses, including restaurants, might participate in providing necessary assistance even if this particular action is not directly related to their core business operations or competencies. While it might be argued that their actions do not achieve optimized social value, there are larger issues at hand. In such situations, any help may be even perceived as contributing to social value optimization. This discussion is essential because some proponents of S-CSR may strictly argue for the criterion set in this study, the link between the company’s CSR strategy and its core business operations and competencies, without carefully considering unique demands for some particular social and environmental issues.

Lastly, we suggest that businesses should consider the particular difficulty of measuring the impact of their CSR strategy regarding many social issues. This is not to propose that businesses should disregard social issues as part of their CSR strategy. However, when developing their CSR strategy, they must clearly understand the challenge of accurately measuring the impact or value of their investment in social initiatives as it is inherently difficult. Consider the following case; Company A donates a certain amount of money to Oxfam for poverty eradication while Company B donates the same amount of money to the International Alliance of Women to improve gender equality. How can you measure and compare the impact of these two CSR activities? Should we consider these two CSR activities to have the same impact because of the same donation amount? We, however, know that is not an accurate way to measure the true impact or value of such actions. It is difficult in this case because there is no objective way to measure the impact or value. For environmental CSR activities, we often use objective criteria such as greenhouse gas emission reductions to measure the impact or value of the activity, while for social activities, the impact and value are often based on personal judgment. For instance, while Person A may believe gender discrimination is more important than poverty, Person B may argue the opposite. Although we do not have a clear solution for this issue at the moment, it is apparent that companies must find a way to quantify the value and impact of their CSR investment in social issues. Considering the general trend of governments requiring many businesses (e.g., publicly traded corporations) to disclose not only environmental but also social issues, companies should pay more attention to this particular issue when developing their CSR strategy.

Suggestions for future research

Our arguments for S-CSR still require substantial empirical validation. Therefore, we suggest several directions for future research concerning the concept of S-CSR. Five specific recommendations are listed below. 1. Identifying and evaluating which CSR activities constitute S-CSR would be a crucial question to answer for future CSR scholars. For this task, we argue that industry characteristics and each company’s unique features, such as the nature of its core business and its vision and mission, must be closely considered and examined since such characteristics and features represent the company’s core business operations and competencies. While it can be argued that each industry (e.g., the hotel, the restaurant, the cruise, the airline, etc.) may establish its standardized characteristics as guidance, we firmly believe that each company must identify its own unique attributes to develop the most appropriate S-CSR strategy for itself. For example, companies even within the same industry can have different visions and missions which can significantly influence each company’s S-CSR strategy. This investigation may be conducted from various stakeholders’ perspectives such as consumers, employees, or shareholders since each group may vary in their thoughts and opinions on the company’s core business operations and competencies. These differing viewpoints can influence their perspectives on what should constitute their S-CSR practices. This investigation can also be extended to the comparison between primary versus non-primary stakeholders. Nevertheless, we believe that strong commonalities regarding core business operations and competencies, and overall viewpoints on S-CSR should exist across various stakeholder groups. Certainly, this would remain an empirical question, and examining potential differences across multiple stakeholder groups could add value to our understanding of the S-CSR framework. 2. After identifying and evaluating suitable S-CSR practices, we recommend a thorough investigation of various business outcomes of implementing S-CSR versus non or less S-CSR initiatives. In general, we posit that S-CSR should be able to produce better business outcomes. This can be examined from consumers’ or employees’ perspectives through experimental design or cross-sectional survey studies. Additionally, this can be tested at the company level by analyzing various firm-level business outcomes derived from S-CSR versus non or less S-CSR activities. It should be noted that various firm-level business outcomes may be traditional accounting performance measures like profitability (e.g., return on assets), market-based performance measures (e.g., Tobin’s q or stock returns), or various risk measures (e.g., business risk, systematic risk, etc.). Moreover, we encourage CSR researchers to explore other firm-level business outcomes or behaviors such as borrowing or general financing behaviors, bond ratings, risk-taking behaviors, corporate governance policies, and the tendency to implement certain major strategies like internationalization or franchising. Another crucial issue that needs particular attention in this context is the long-term value creation aspect of S-CSR. CSR scholars should develop improved ways to measure the long-term value of CSR practices. This will enable them to empirically compare the long-term value of S-CSR versus non-S-CSR. The last suggestion in this stream of research is about examining the social impact of CSR practices. Specifically, the social impact generated by S-CSR and non-S-CSR can be compared. The concept of S-CSR argues that the social impact will be optimized through S-CSR, and, thus, be greater than the social impact created by non-S-CSR. 3. As part of the examination of various business outcomes or the impact of S-CSR, future research should incorporate our emphasis on prioritizing a few primary CSR activities (i.e., avoiding trying to do everything), considering both relevance to core business operations and competencies and measuring the ‘scale’ of the impact. For example, comparing and drawing implications from focused S-CSR versus diverse S-CSR (or non-S-CSR), and between large-scale S-CSR versus small-scale S-CSR can be interesting topics for investigation. However, as various stakeholders (e.g., customers, local communities, and shareholders) become more educated about various CSR issues, they may become more knowledgeable and caring for a wider range of CSR topics. Accordingly, it will be interesting to observe how stakeholders perceive a company’s focused versus diverse S-CSR strategies differently and how these different S-CSR strategies will create value over time. 4. The role of cultural influences in the context of S-CSR is another venue for future CSR researchers. Cultural differences across different countries and regions are known to play an important role in shaping companies’ CSR strategy (Song and Kang, 2019) and such influences are expected to extend to the concept of S-CSR. For example, cultures can influence how to identify particular CSR practices as S-CSR more or less, and furthermore, the impact of S-CSR on various corporate outcomes (e.g., accounting performance, market-based performance, various risks, etc.) can vary across countries or regions with different cultural backgrounds. 5. Lastly, although not directly related to the concept of S-CSR, we recognize the increasingly significant role of artificial intelligence (AI) in virtually all business fields today (Dogru et al., 2024). This leads us to believe that AI’s role in identifying, evaluating, developing, implementing, and maintaining S-CSR through utilizing big data and machine learning will be critical in the future. Therefore, we eagerly encourage the exploration of Al’s role in the context of S-CSR.

Conclusion

Considering the growing significance of CSR in the corporate world, this study critically reflects the extant CSR literature and CSR practices, and introduces the conceptual CSR framework, Strategic CSR (S-CSR), illustrated with real industry examples and empirical survey data. S-CSR incorporates the following four concepts: creating shared value, enlightened stakeholder theory, resource-based theory, and CSR fit perspective. The essential argument for S-CSR is that businesses should develop and implement S-CSR practices that are directly related to the businesses’ core operations and competencies. Additionally, this study discusses several additional issues to consider in developing and implementing S-CSR to enhance the understanding of the framework. The results of this study’s survey generally support the S-CSR framework and suggest several research directions for CSR scholars. Consequently, we hope to stir intellectual discussions among CSR scholars with our proposal of S-CSR and make meaningful contributions to the CSR literature and practices as a result.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Correction (January 2025):

In the published version of the article, the references “Kuokkanen, H., & Sun, W. (2020)” and “Kuokkanen, H., & Sun, W. (2024)” were omitted. These reference citations have now been added in the second paragraph on page 2, and the missing reference details have been included in the reference section. The online version of the article has been updated to reflect these changes.