Abstract

Cost stickiness, which is also termed cost asymmetry, describes the asymmetric relationship between revenue and cost. In this study, we examine whether high-speed railway (HSR) connection affects the cost stickiness of tourism firms. Employing a sample of 324 Chinese tourism firms from 2003 to 2018 and applying a difference-in-difference (DID) method, we find that the cost stickiness of tourism firms increases after HSR connection. Our results also reveal that the relationship between HSR connection and cost stickiness is more pronounced in firms with higher free cash flow (FCF), higher labor costs, and in state-owned enterprises (SOEs). Our research advances an in-depth understanding of the cost behavior in tourism firms and sheds light on the policy effect of HSR connection.

Introduction

High-speed railway (HSR) has been developing rapidly in China. By February 2020, China has 35,388 km HSR in operation, which accounts for about two-thirds of high-speed track worldwide. It has been evidenced that HSR introduction has a significant impact on tourism development (Albalate et al., 2017; Chen and Haynes, 2012; Gao et al., 2019). Existing literature finds that the opening of HSR provides a positive shock to tourism firm value because of the enhanced tourist mobility (Zhang et al., 2020a), and firms from communication-intensive and travel-dependent industries benefit more in terms of productivity, profitability, and growth through the reduction of communication costs after HSR connection (Kuang et al., 2021). Evidently, firm value and firm profitability are fundamentally determined by revenue and cost, so focusing only on tourism firm revenue fails to explain where the change in profitability derives from. Although the effects of HSR connection on tourism firm value, firm revenue, and firm profitability have been examined in existing studies (Albalate et al., 2017; Gao et al., 2019; Kuang et al., 2021; Zhang et al., 2020a), limited research has focused on the cost and cost behavior of tourism firms. According to cost management literature, cost stickiness, which is also termed cost asymmetry, plays an important role in earnings prediction and earnings quality of firms (Banker et al., 2013; Banker and Byzalov, 2014). In this context, we explore the association between HSR connection and cost stickiness to open the black box of tourism firms’ cost management activities.

Cost stickiness describes the asymmetric relationship between revenue and cost, and arises when the amount of increased costs with increased sales is higher than that of decreased costs with declined sales changing in the same proportion (Anderson et al., 2003). Prior literature revealed that as managers believe that sales decrease is only temporary, they are reluctant to trim redundant resources when faced with sales reduction (Anderson et al., 2003; Chen et al., 2019). Consequently, costs would not change in the same proportion as when sales increase, thus forming cost stickiness (Anderson et al., 2003). Cost stickiness has significant implications. Previous literature indicated that efficient cost management contributes to more accurate earnings prediction (Banker and Chen, 2006; Weiss, 2010) and higher future earnings of firm (Anderson et al., 2007), whereas deficiencies in resources adjustment decisions may induce high operating risks (Holzhacker et al., 2015) and ultimately damage firm value (Baños-Caballero et al., 2014; Dhole et al., 2019).

Existing literature shows that the selling, general, and administrative (SG&A) cost ratio (calculated as the ratio of SG&A costs to total assets) reflects the operating efficiency of firms and the capacity to control costs of managers (Anderson et al., 2007; Chen et al., 2012). In our sample, the SG&A cost ratio of tourism firms is 19.3%, which is much higher than that in other industries (Table 1 in the Appendix). Considering the high proportion of the SG&A cost ratio and the materiality level of SG&A costs in the tourism industry, it is vital for both researchers and practitioners to understand how managers in tourism firms make deliberate decisions to adjust resources and control the SG&A spending. However, literature on cost behavior in the tourism industry is limited. Our research fills this gap and provides important empirical evidence on how tourism firms make cost adjustment decisions.

Generally, cost adjustment decisions are made by the top management team (TMT), so managers are crucial in the process of cost adjustments (Anderson et al., 2003; Banker et al., 2013). Previous literature has documented that managers are mostly empire builders who increase the firm size in excess of the optimal size to satisfy their own ambitions (Hope and Thomas, 2008; Jensen, 1986), and those managers with empire building incentives would retain additional resources when sales decrease (Chen et al., 2012). However, research focusing on managerial empire building in the tourism industry is limited. Given the dramatic impact of managerial empire building behavior on corporate governance efficiency, our study explores managerial behavior in the tourism industry by examining the heterogeneous effect of HSR connection on cost stickiness under different levels of empire building incentives.

In addition to managerial empire building incentives, cost structure also has a significant influence on cost adjustment decisions (Anderson et al., 2003; Balakrishnan and Gruca, 2008). Tourism is a labor-intensive industry, and labor costs constitute a significant proportion of the total costs. Therefore, the complexity levels of cost adjustments in the tourism industry could be distinctive. In existing tourism literature, it remains unexplored how tourism managers adjust costs under different complexity levels of resource adjustments after HSR connection. We use the unit labor cost as the complexity level of cost adjustments to analyze the heterogeneous effect of HSR connection on cost stickiness. Addressing this issue can advance the understanding of how tourism managers allocate resources in different complexity levels of cost adjustment decisions.

Exploiting the difference-in-difference (DID) method, we find that the cost stickiness of Chinese listed tourism firms increases after HSR connection. Moreover, the association between HSR connection and cost stickiness is more pronounced in firms with higher levels of free cash flow (FCF) and higher unit labor costs, which provides important evidence of the heterogeneous effects of empire building incentives and unit labor costs. Our additional analysis also indicates that such an impact is more significant in state-owned enterprises (SOEs).

Our study has theoretical and practical implications to understand the tourism industry and tourism firms’ cost behavior. Firstly, to the best of our knowledge, it is the first study to investigate how HSR connection affects the asymmetric cost behavior of tourism firms. Prior literature mostly investigated the impact of HSR connection on firm value and firm profitability in the tourism industry (Kuang et al., 2021; Zhang et al., 2020a), but little attention has been paid to the link between HSR connection and corporate cost behavior. Our study bridges tourism literature with cost management literature, which advances the understanding of tourism firms’ cost behavior with the influence of HSR.

Secondly, different from previous tourism literature that examined agency problems by investigating the role of ownership structure (Al-Najjar, 2015; Yeh, 2019), board characteristics (Al-Najjar, 2014), and managerial compensation structure (Kim and Gu, 2005), our study analyzes the managerial empire building incentives from the perspective of cost behavior, which complements the tourism literature and widens the angle of studies on the agency problems of tourism firms. We find that the opening of HSR triggers managerial empire building incentives, which also has practical implications for shareholders to take proactive actions to prohibit managers from conducting opportunistic activities before the efficiency of the business falls.

Thirdly, our study extends tourism literature by investigating the labor cost stickiness of tourism firms. Previous literature employed listed firms from different industries as their sample to study labor cost stickiness (Gu et al., 2020; Prabowo et al., 2018), however, the extent of labor cost stickiness varies with industries. Our study focuses on the tourism industry in which labor costs account for a significant proportion of the total costs. We find that tourism firms are more likely to retain human resources when sales shrink after HSR introduction, which sheds light on the employment and macroeconomy in the cities with and without HSR connection.

The rest of the paper is organized as follows. The Literature review and hypotheses development section reviews extant literature and develops hypotheses regarding the influence of HSR connection on corporate cost stickiness; the Methodology section presents the research methodology; the Results section provides the research findings; the final section concludes with results discussions, research implications, limitations and prospects.

Literature review and hypotheses development

HSR connection and the development of tourism industry

Literature on the consequences of HSR connection falls at two levels: the regional level (Chen and Haynes, 2012; Gao et al., 2019; Masson and Petiot, 2009) and the firm level (Kuang et al., 2021; Zhang et al., 2020a, 2020b).

At the regional level, vast literature explores the influence of HSR connection on the regional tourism economy, but the conclusions are inclusive. For example, Chen and Haynes (2012) find that HSR boosts foreign arrivals and overseas tourism revenues in China using the provincial-level data from 1999 to 2010. Masson and Petiot (2009) conclude that tourism activities are reinforced after HSR connection owing to the main impact of agglomeration. However, the negative relationship between HSR connection and tourism growth is also found in previous literature (Albalate and Fageda, 2016; Albalate et al., 2017). The studies attributed the negative impact of HSR connection on the tourism development to the substitution impact of peripheral hospitality (Gao et al., 2019) and airline service reduction (Dobruszkes and Mondou, 2013).

HSR connection also affects firm behavior profoundly. Prior literature showed that HSR connection promotes tourism firm value through the enhanced tourist mobility (Zhang et al., 2020a). Kuang et al. (2021) find that firms from communication-intensive and travel-dependent industries obtain increased profitability and growth after HSR connection. Zhang et al. (2020b) argue that HSR connection accelerates the flow of innovation factors among different regions and induces the spillover effect of technology innovation, thus promoting firm innovation. Moreover, analysts’ earnings forecasts are more accurate after HSR connection through their increased visits to firms (Kong et al., 2020).

Although previous literature examined the impact of HSR connection on the regional development in the tourism industry and firms’ behavior, the reason for the mixed effect of HSR connection remains a myth. Firms’ cost behavior is an important determinant factor of corporate profitability, so the association between HSR connection and cost behavior of tourism firms would provide great significance for an in-depth understanding of HSR effects.

The determinants of cost stickiness

According to Anderson et al. (2003), costs are sticky when they respond to business activity augments more than to contemporaneous activity reductions. The level of cost stickiness is determined by three factors: managerial empire building incentives, adjustment costs, and managerial expectations (Anderson et al., 2003; Banker et al., 2020; Chen et al., 2012).

Managerial empire building incentives point to managers intentionally expanding firm size beyond the optimal level to maximize their personal interests. Managers with empire building incentives are more likely to increase excessive resources when activities rise and are less likely to cut unused resources when activities decline. Prior literature used FCF to measure the magnitude of managers’ overspending and found that empire building incentives positively affect cost stickiness (Chen et al., 2012). Cannon et al. (2020) document that the level of cost stickiness is lower after the enforcement of international mergers and acquisitions laws, which means that good corporate governance reduces the level of cost stickiness through curbing opportunistic managerial behavior.

Adjustment costs are defined as the costs incurred when managers increase firm scale or cut down firm resources (Anderson et al., 2003; Banker and Byzalov, 2014). They usually include redundancy pay; recruitment cost during the hiring process; and organization costs (e.g., loss of morale among remaining employees, and the erosion of human capital during termination) (Anderson et al., 2003). When resource adjustments are related to human resources, adjustment costs refer particularly to layoff and recruitment costs (Banker et al., 2013). In general, when the adjustment costs of cutting resources are high, managers tend to remain redundant resources with sales reduction and augment required resources with an increase in sales (Anderson et al., 2003). Therefore, cost stickiness increases with the level of upward adjustment costs.

Managerial expectation is another determinant of cost stickiness. When managers are optimistic about future demands, they are more likely to retain unused resources during sales decrease as they believe that sales reduction is only temporary (Anderson et al., 2003). Accordingly, they will utilize these resources after the demand recovers, which can increase firm’s cost stickiness. On the contrary, pessimistic managers would decrease unused resources (Banker et al., 2020).

Hypotheses development

The impact of HSR connection on cost stickiness can be analyzed from two aspects. Firstly, the opening of HSR affects the level of cost stickiness by triggering managers’ empire building incentives. Specifically, as HSR connection escalates the tourist arrivals and tourism revenues (Albalate and Fageda, 2016; Chen and Haynes, 2012), managers have incentives to expand the business and hire additional employees to accommodate the increasing demands. The process of enlarging firm size provides opportunities for managers to conduct empire building behaviors (Hope and Thomas, 2008; Masulis et al., 2007), such as investing resources more rapidly when sales rise, but retaining slack resources when sales decline. Consequently, the SG&A expenditure would increase with the surge in sales. However, owing to empire building incentives, managers would not cut resources when sales decline, which induces a higher level of cost stickiness.

Secondly, HSR connection influences the cost stickiness of tourism firms by affecting adjustment costs. According to previous studies, HSR connection augments levels of labor costs of firms by improving the regional labor productivity rate (Arbués et al., 2015; Deng, 2013), decreasing the labor supply (Dalenberg and Partridge, 1997; Lin, 2017), and promoting population mobility (Ortega and Verdugo, 2014). As a result, both the recruitment costs and redundant costs of firms would increase. When sales shrink, managers tend to retain unutilized employees rather than dismissing them because layoff costs are high (Anderson et al., 2003). When sales increase, although recruitment costs increase, managers will still revive additional committed resources, such as recruiting more employees, because managers consider that the benefits of adding resources outweigh the adjustment costs incurred by increasing resources after HSR connection (Banker et al., 2013). Consequently, the costs of tourism firms would increase more when the activity rises than they would decrease when activity falls by an equivalent amount, leading to a greater extent of cost asymmetry.

The cost stickiness of the tourism firms would increase after HSR connection.

According to the economic theory of cost behavior, the most crucial conceptual underpinning of cost management research is that costs result from managers’ resource commitment decisions, which are dedicated by various constraints, incentives, and behavioral biases (Banker et al., 2018; Cooper and Kaplan, 1992). Therefore, existing literature integrates the determinants of cost stickiness and boils them down to three aspects: managerial empire building incentives, adjustment costs, and optimistic expectations (Anderson et al., 2003; Banker et al., 2020; Chen et al., 2012). In the first hypothesis, we propose that HSR connection affects cost stickiness through managerial empire building incentives and adjustment costs. To verify the mechanism of such incentives and costs, we explore the moderating impact of empire building incentives and adjustment costs on the relationship between HSR connection and cost stickiness of tourism firms in the next two hypotheses. Firstly, we examine the impact of empire building incentives on the relationship between HSR connection and cost stickiness. FCF, which is defined as net cash flow from operating activities excluding cash outflows supporting regular operations and maintaining capital assets, has been proved as a good proxy for empire building incentives (Chen et al., 2012). Prior literature showed that firms with abnormal levels of FCF are related to more over-investment activities (Jensen, 1986; Richardson, 2006). For instance, when FCF is high, managers are strongly motivated to over-invest in projects with negative net present value (Chen et al., 2012). Specifically, they would choose to add more resources when sales rise and delay cost cutting when sales decline. As a result, the costs of tourism firms are stickier. After HSR connection, managers in firms with high levels of FCF tend to engage in empire building activities aimed at increasing their personal utility and perquisite consumption (Hope and Thomas, 2008; Stulz, 1990). Therefore, the impact of HSR connection on cost stickiness would be amplified in firms with higher levels of FCF.

The relationship between HSR connection and cost stickiness is more pronounced for tourism firms with higher FCF. Secondly, we intend to examine the moderating effect of adjustment costs. Labor costs constitute a large proportion of SG&A costs as tourism is a labor-intensive industry. The unit labor cost reflects the difficulty of adjusting the labor resources of the tourism industry, and a higher unit labor cost represents a higher adjustment cost (Dierynck et al., 2012). Existing literature demonstrates that compared with firms whose unit labor costs are lower, firms with higher unit labor costs pay higher redundancy fees and have higher opportunity costs of recruiting new employees (Anderson et al., 2003). After the opening of HSR, firms are prone to retain employees during the periods of sales declining, with the consideration of high adjustment costs of labor resources. Therefore, we conjecture that tourism firms with higher unit labor costs would have a stronger influence on cost stickiness after HSR connection.

The relationship between HSR connection and cost stickiness is more pronounced for tourism firms with higher unit labor costs.

Methodology

Data

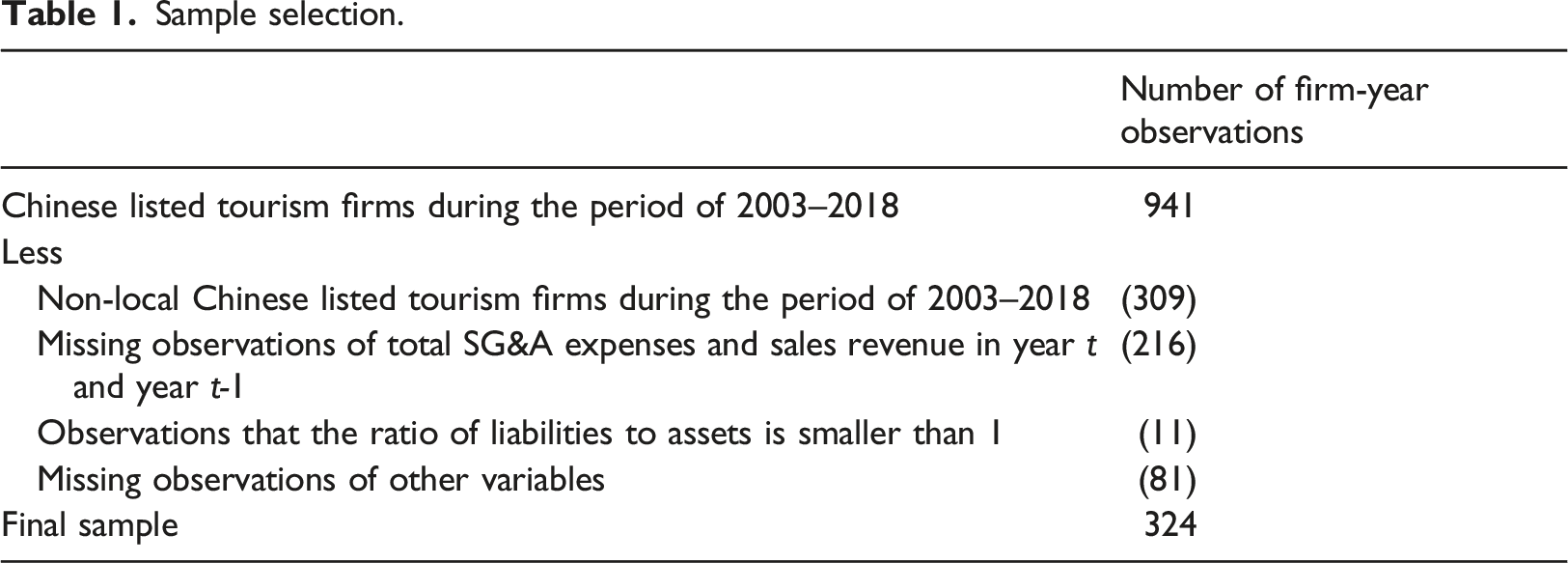

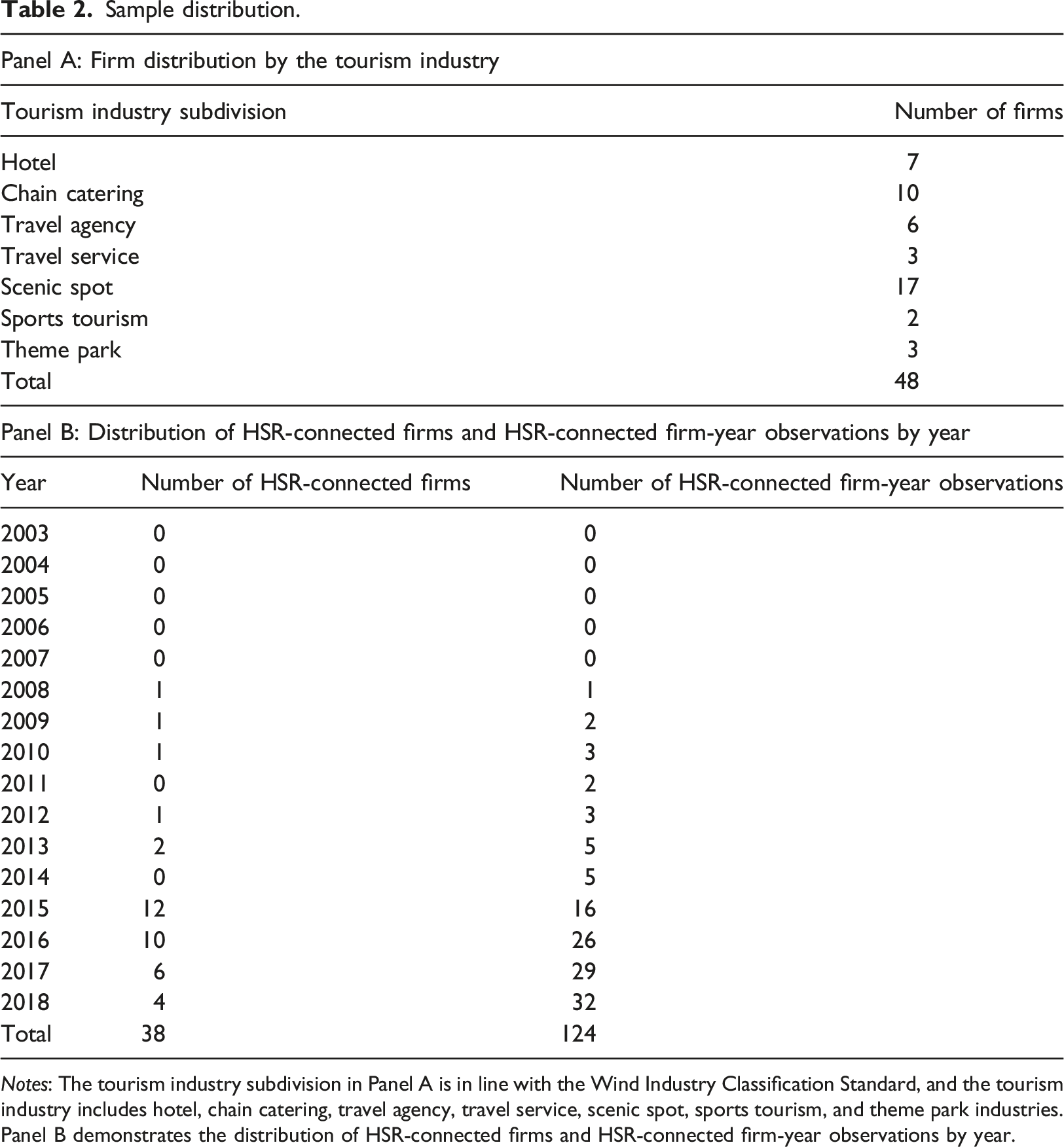

Our sample consists of local listed tourism firms in China from 2003 to 2018. The local listed tourism firms refer to listed tourism firms that operate over 80% of their businesses locally. Tourism firms that have branches all over the country are excluded from our sample. We retain only local firms to precisely capture the net effect of HSR connection on tourism firms. If the whole sample includes non-local firms, the impact of HSR connection on cost stickiness would be calculated repeatedly due to the different locations of non-local samples. We choose tourism firms according to the industrial classification standard used by the Wind database, which includes hotel, chain catering, travel agency, travel service, scenic spot, sports tourism, and theme park industries. Cost management data are collected from the China Stock Market and Accounting Research (CSMAR) database and the Wind database. We collect the HSR data from the Chinese Research Data Services (CNRDS) database and then manually check the data with the National Railway Administration of the People’s Republic of China.

Sample selection.

Sample distribution.

Notes: The tourism industry subdivision in Panel A is in line with the Wind Industry Classification Standard, and the tourism industry includes hotel, chain catering, travel agency, travel service, scenic spot, sports tourism, and theme park industries. Panel B demonstrates the distribution of HSR-connected firms and HSR-connected firm-year observations by year.

Empirical models

We establish the logarithmic model to measure cost stickiness (Anderson et al., 2003; Banker et al., 2013)

We employ equations (2) and (3) to study the influence of HSR connection on cost stickiness (Banker et al., 2013; Gao et al., 2019). Firstly, we include the variables expected to affect how SG&A costs change as sales increase on the right side of the equation, and coefficient β1 on the left side, as in equation (2). Then we introduce equation (3) to capture the determinants that influence changes in SG&A costs when sales decline. These determinants include HSR connection and other control variables that may affect the asymmetric cost behavior of tourism firms

HSR

i,t

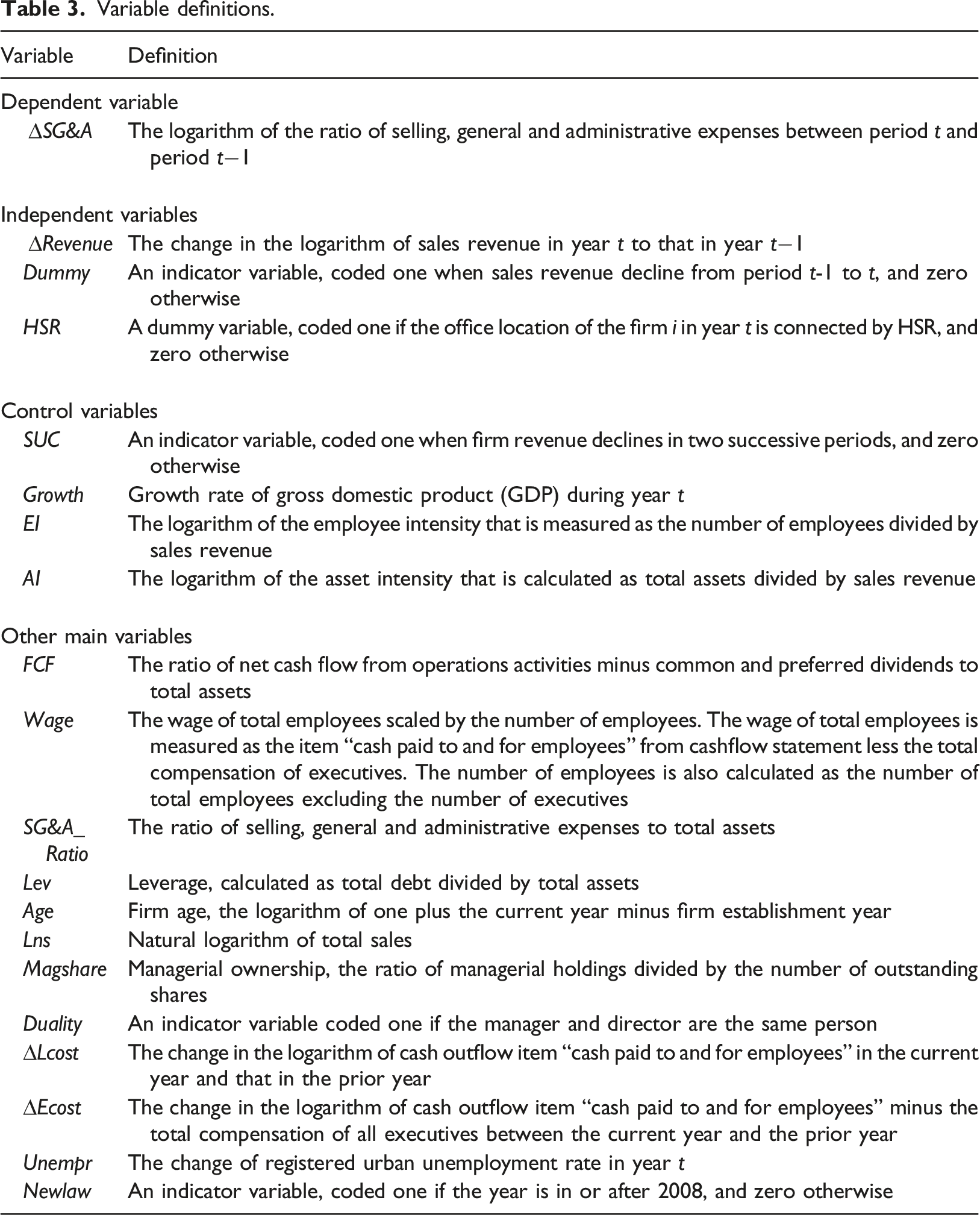

is our key independent variable. It is coded one if the office location of the firm i in year t is connected by HSR, and zero otherwise. Moreover, given that many HSR lines in the sample were opened in December and considering the lagging effect of HSR connection, we lag the HSR variable of these lines by 1 year (Albalate et al., 2017; Gao et al., 2019). The dummy variable SUC equals 1 when the sales revenue of the tourism firms decline in two successive periods, and zero otherwise. Growth represents the growth rate of gross domestic product (GDP) during year t. We also include AI and EI in equations (2) and (3) to control the influence of adjustment costs, respectively. AI is the logarithm of asset intensity (ratio of total assets to sales revenue), and EI is measured as the logarithm of employee intensity (ratio of the number of employees to sales revenue). Substituting equations (2) and (3) into equation (1), we establish our main model as follows

As the opening time of HSR varies across cities, we employ a staggered DID method to discuss the causal effect of HSR connection on cost stickiness of tourism firms in equation (4). The treatment group refers to firms whose cities became connected by HSR between 2003 and 2018, whereas the control group comprises firms that are located in non-HSR-connected cities. v i represents the firm fixed effect, which fully controls the fixed differences between firms in treatment groups and control groups. u t is the year fixed effect, which controls the fixed differences of treatment (control) groups before HSR opening years and after HSR opening years. Coefficient β3 captures the net effect of HSR connection on the cost stickiness of tourism firms, and the standard errors are clustered at the firm level to alleviate the bias caused by the serial correlation (Petersen, 2009).

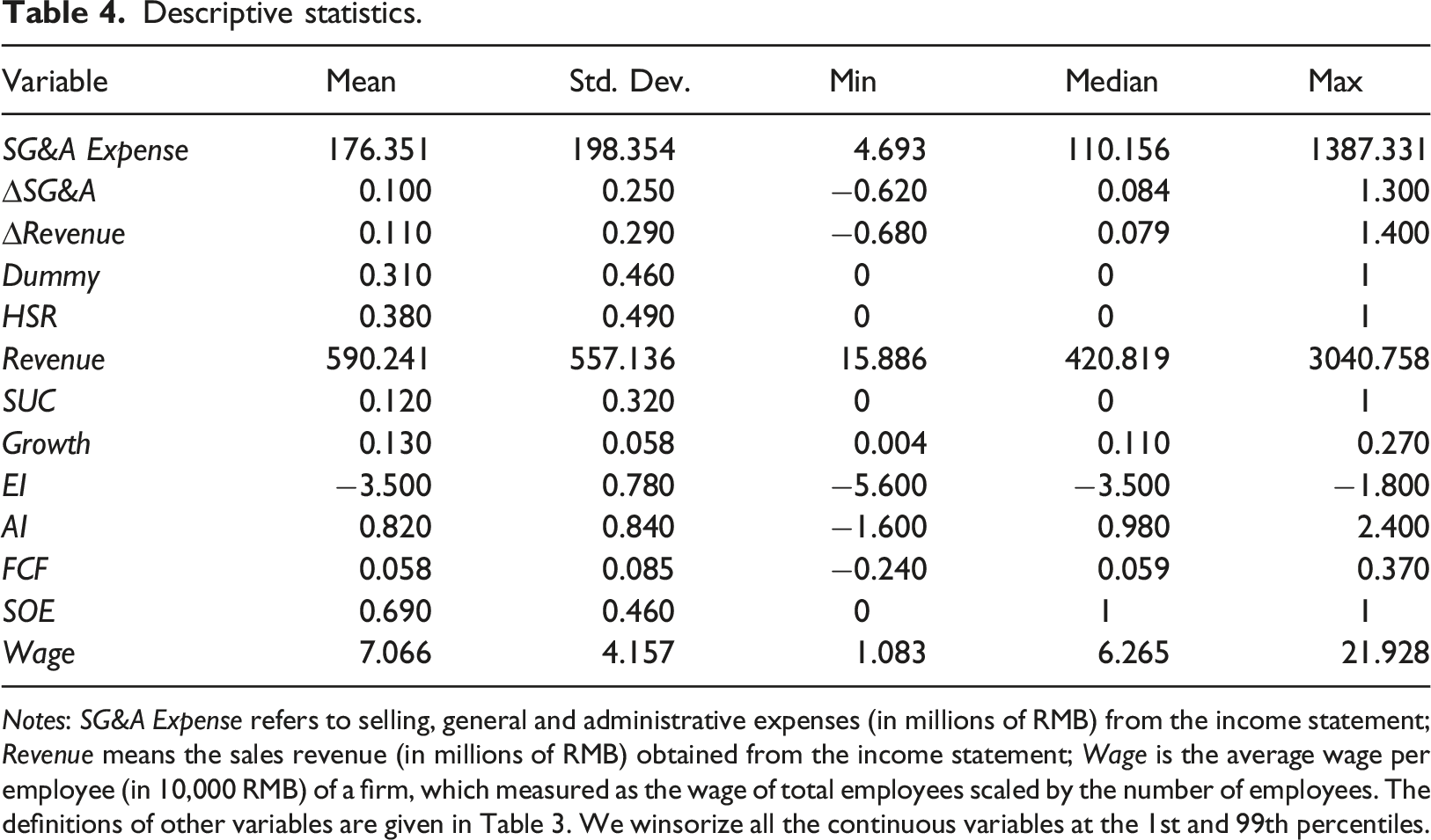

Descriptive statistics

Variable definitions.

Descriptive statistics.

Notes: SG&A Expense refers to selling, general and administrative expenses (in millions of RMB) from the income statement; Revenue means the sales revenue (in millions of RMB) obtained from the income statement; Wage is the average wage per employee (in 10,000 RMB) of a firm, which measured as the wage of total employees scaled by the number of employees. The definitions of other variables are given in Table 3. We winsorize all the continuous variables at the 1st and 99th percentiles.

Results

Hypotheses testing

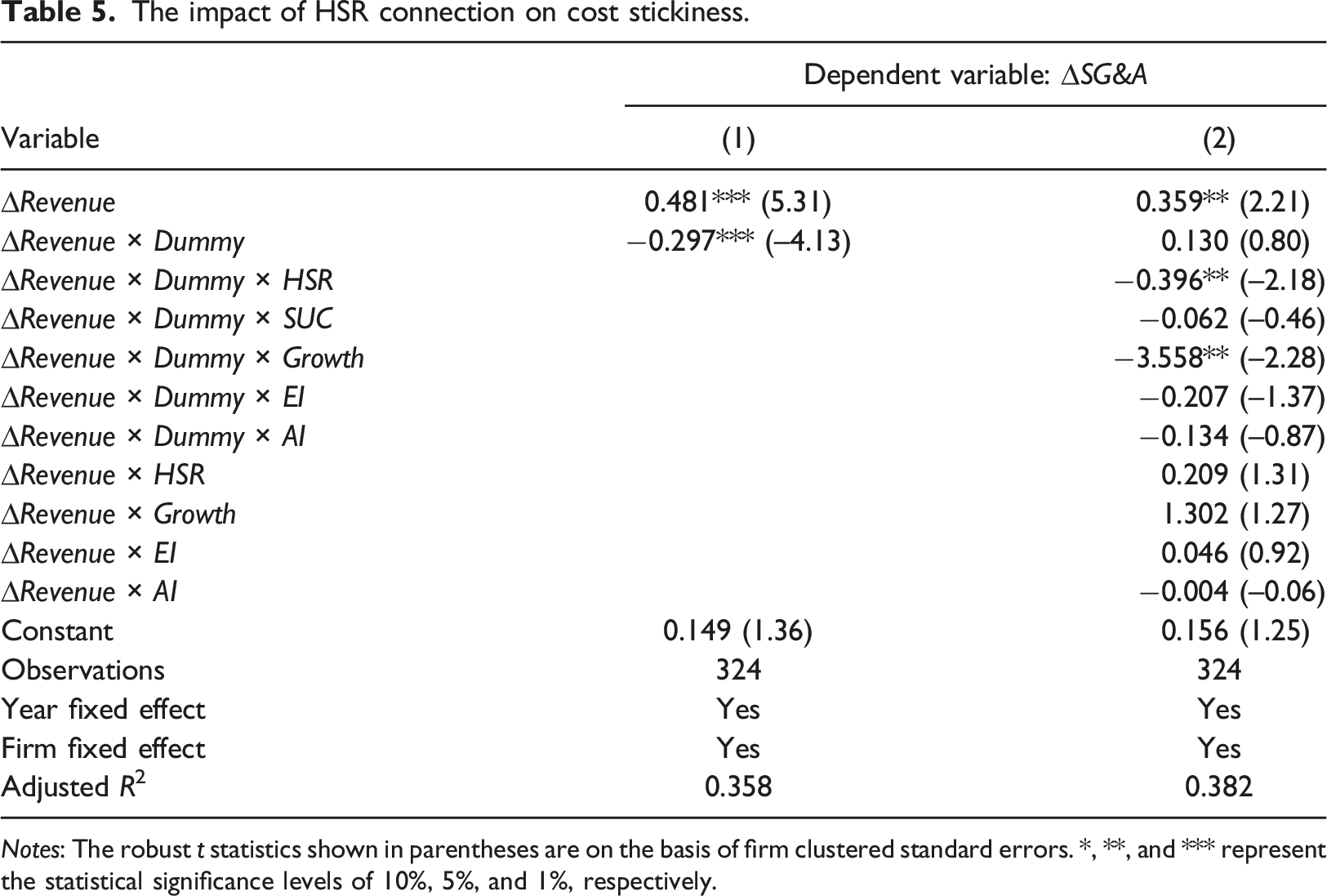

The impact of HSR connection on cost stickiness.

Notes: The robust t statistics shown in parentheses are on the basis of firm clustered standard errors. *, **, and *** represent the statistical significance levels of 10%, 5%, and 1%, respectively.

We do not focus on the interaction term ∆Revenue × Dummy in Column (2) because it could not reflect the original level of cost stickiness in the tourism industry, as shown in equation (2). If we want to calculate the level of cost stickiness, we must consider the joint effect of other control variables.

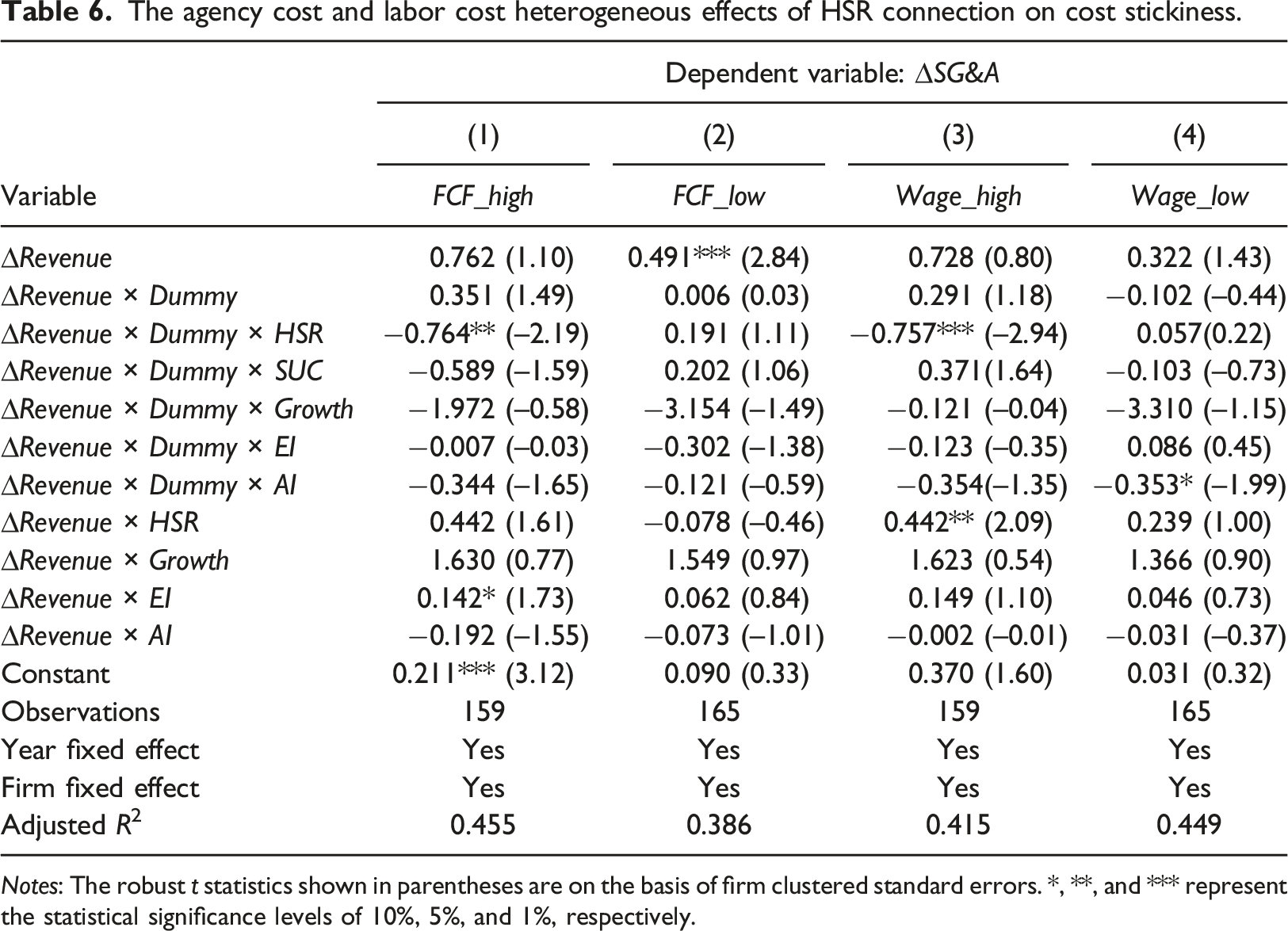

The agency cost and labor cost heterogeneous effects of HSR connection on cost stickiness.

Notes: The robust t statistics shown in parentheses are on the basis of firm clustered standard errors. *, **, and *** represent the statistical significance levels of 10%, 5%, and 1%, respectively.

To test H3, our sample is also split into two groups according to the median values of wage per employee in year. Wage_high (Wage_low) is the dummy variable coded one if the wage per employee is above the median values of the sample in that year. Columns (3) and (4) of Table 6 present the results. The significantly negative coefficient of ∆Revenue × Dummy × HSR only exists in the Wage_high group, not in the Wage_low group, indicating that the positive influence of HSR connection on cost stickiness holds in firms with high levels of wage per employee. Thus, H3 is supported.

Additional analysis

Ownership property heterogeneity

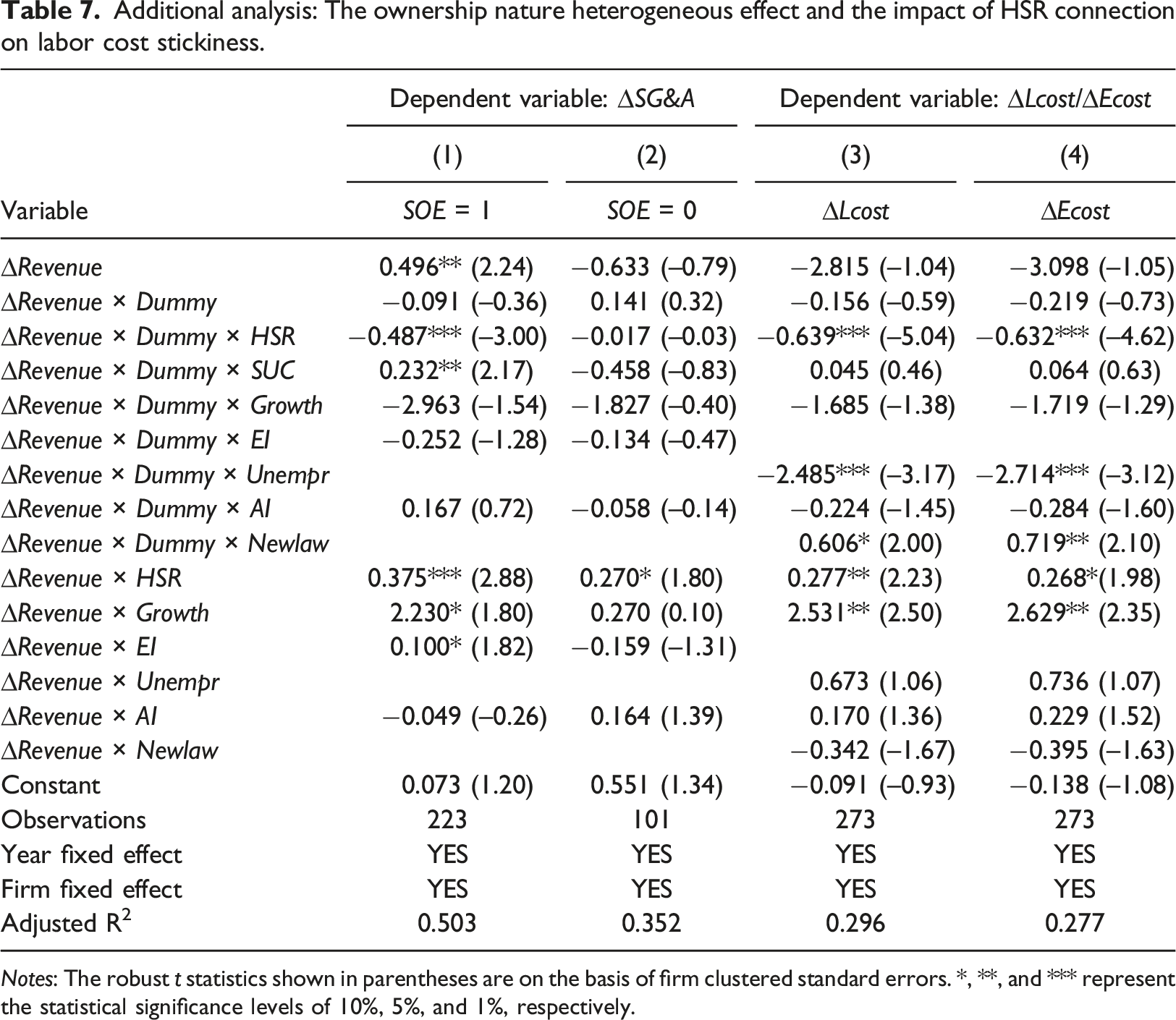

After discussing the heterogeneous effect of HSR connection on tourism firms’ cost stickiness in terms of different levels of FCF and labor costs, we further explore the moderating role of firms’ ownership to understand the causal effect of HSR connection on increased cost stickiness. In China, SOEs need to fulfill some social tasks, such as avoiding layoffs to retain the employment rate and maintain social stability (Gu et al., 2020; Lin et al., 1998). After the opening of HSR, to achieve political promotions and social goals, SOEs are prone to retain redundant resources, such as labor force with sales declining, inducing a higher level of cost stickiness.

Additional analysis: The ownership nature heterogeneous effect and the impact of HSR connection on labor cost stickiness.

Notes: The robust t statistics shown in parentheses are on the basis of firm clustered standard errors. *, **, and *** represent the statistical significance levels of 10%, 5%, and 1%, respectively.

HSR connection and labor cost stickiness

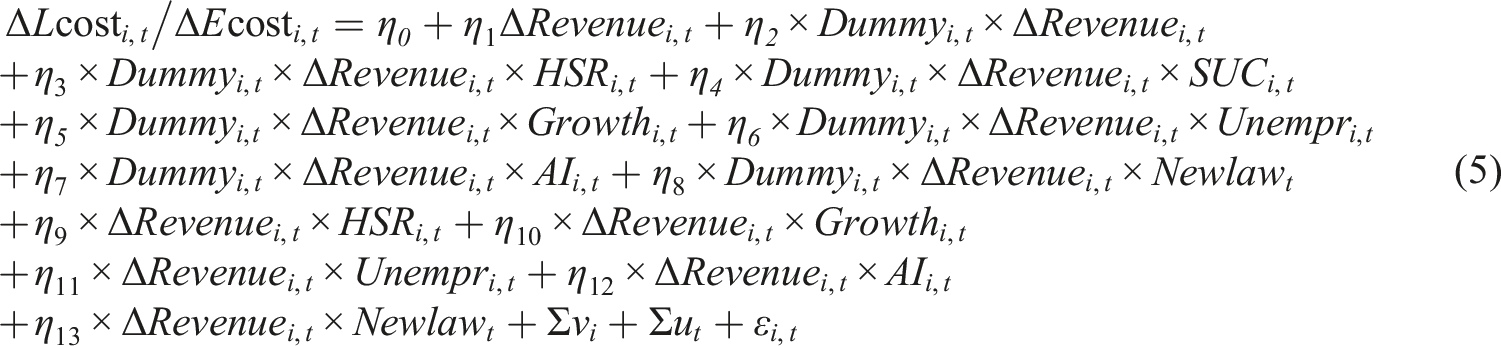

As tourism is an employment-intensive industry, labor costs comprise a significant portion of SG&A costs in tourism firms. If the impact of HSR connection on cost behavior exists, then the adjustment of employees in tourism firms should also be influenced by HSR and labor cost stickiness would change correspondingly. Following Gu et al. (2020), we use equation (5) to verify whether HSR connection has an impact on labor cost stickiness. Equation (5) is quite similar to equation (4), with only slight differences

Two variables (i.e., ∆Lcost and ∆Ecost) are used to measure the dependent variable (i.e., changes in labor costs) to improve the robustness of our results. ∆Lcost is calculated as the logarithmic change of labor costs (cash outflow item “cash paid to and for employees”) in year t to that in year t-1. ∆Ecost is the logarithmic change of employment costs (“cash paid to and for employees” minus the total compensation of all executives) during period t minus the logarithmic change of that during period t-1. Unempr is measured as the change of the registered urban unemployment rate in year t. Newlaw is an indicator variable coded one if the year is in or after 2008, and zero otherwise. We choose 2008 as the cut point because it is the year of implementing employment protection legislation. The coefficient of η3 is our primary focus, which is expected to be negative. Other specifications in equation (5) are the same as in equation (4).

Columns (3) and (4) in Table 7 present the impact of HSR connection on labor cost stickiness. In both columns, the interaction term ∆Revenue × Dummy × HSR is significantly negative at 1% level, verifying that after HSR connection, changes in labor costs are also asymmetrical, and changes in SG&A costs mostly derives from changes in labor costs.

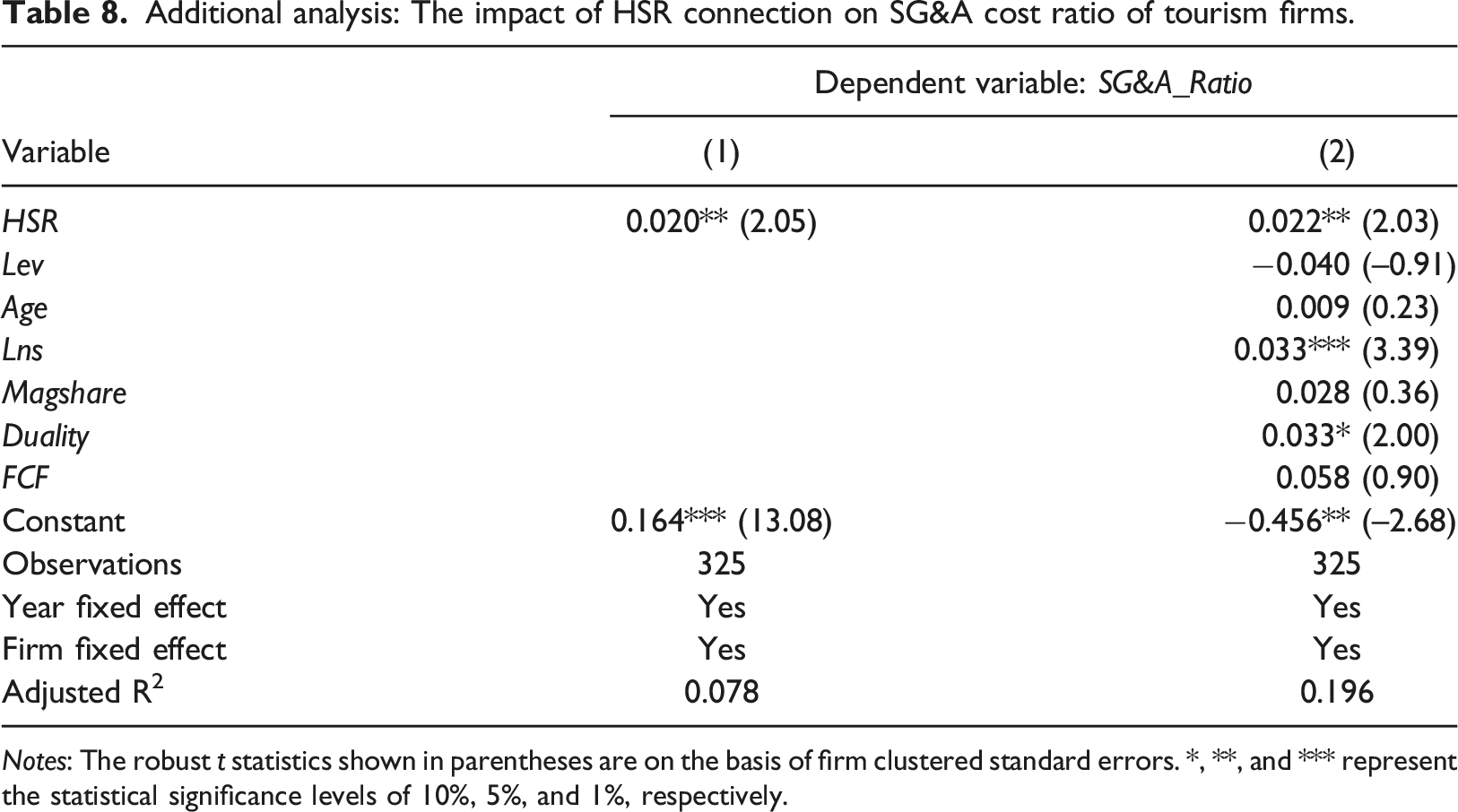

The impact of HSR connection on firm cost

Additional analysis: The impact of HSR connection on SG&A cost ratio of tourism firms.

Notes: The robust t statistics shown in parentheses are on the basis of firm clustered standard errors. *, **, and *** represent the statistical significance levels of 10%, 5%, and 1%, respectively.

Robustness check

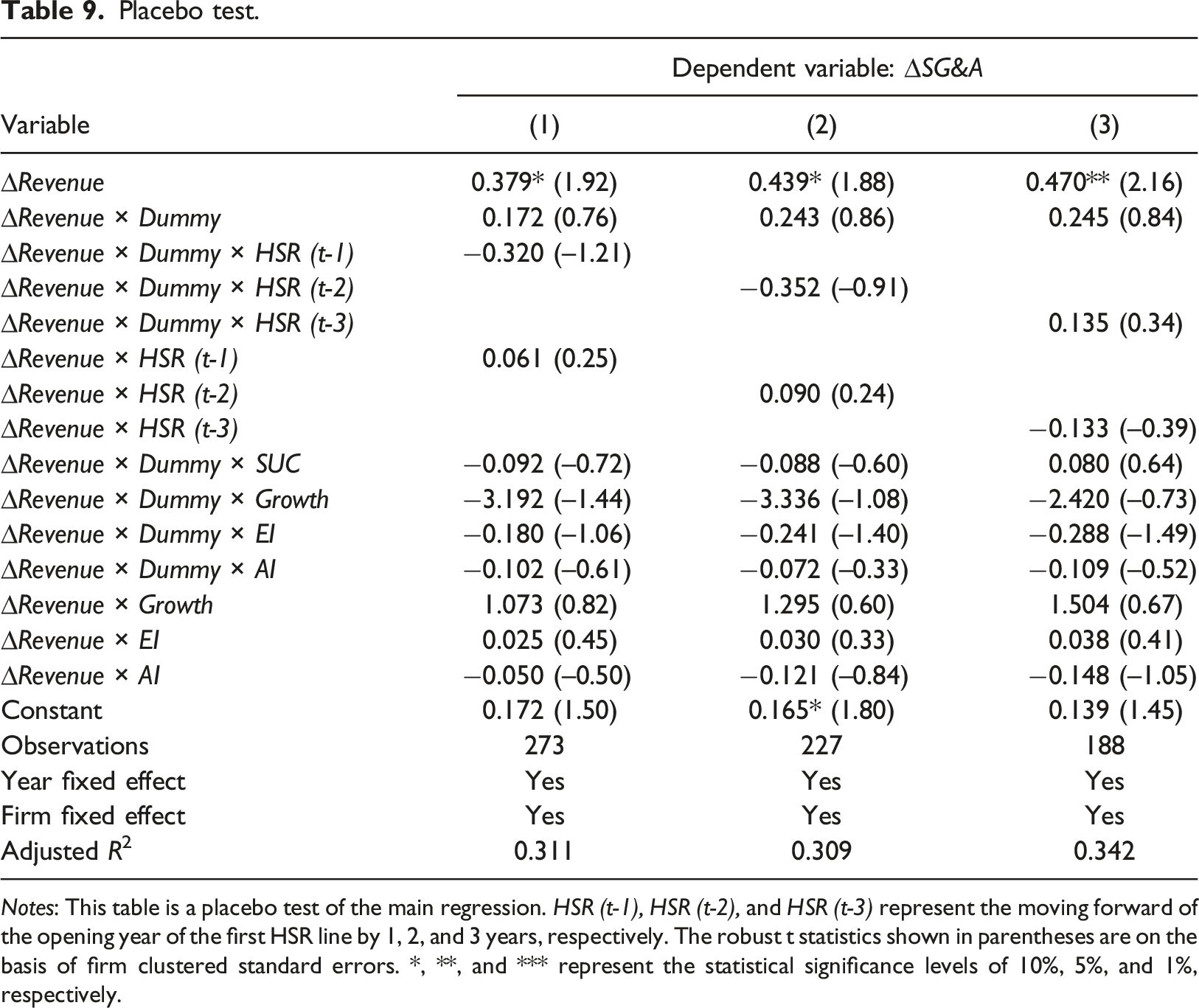

Placebo test

Placebo test.

Notes: This table is a placebo test of the main regression. HSR (t-1), HSR (t-2), and HSR (t-3) represent the moving forward of the opening year of the first HSR line by 1, 2, and 3 years, respectively. The robust t statistics shown in parentheses are on the basis of firm clustered standard errors. *, **, and *** represent the statistical significance levels of 10%, 5%, and 1%, respectively.

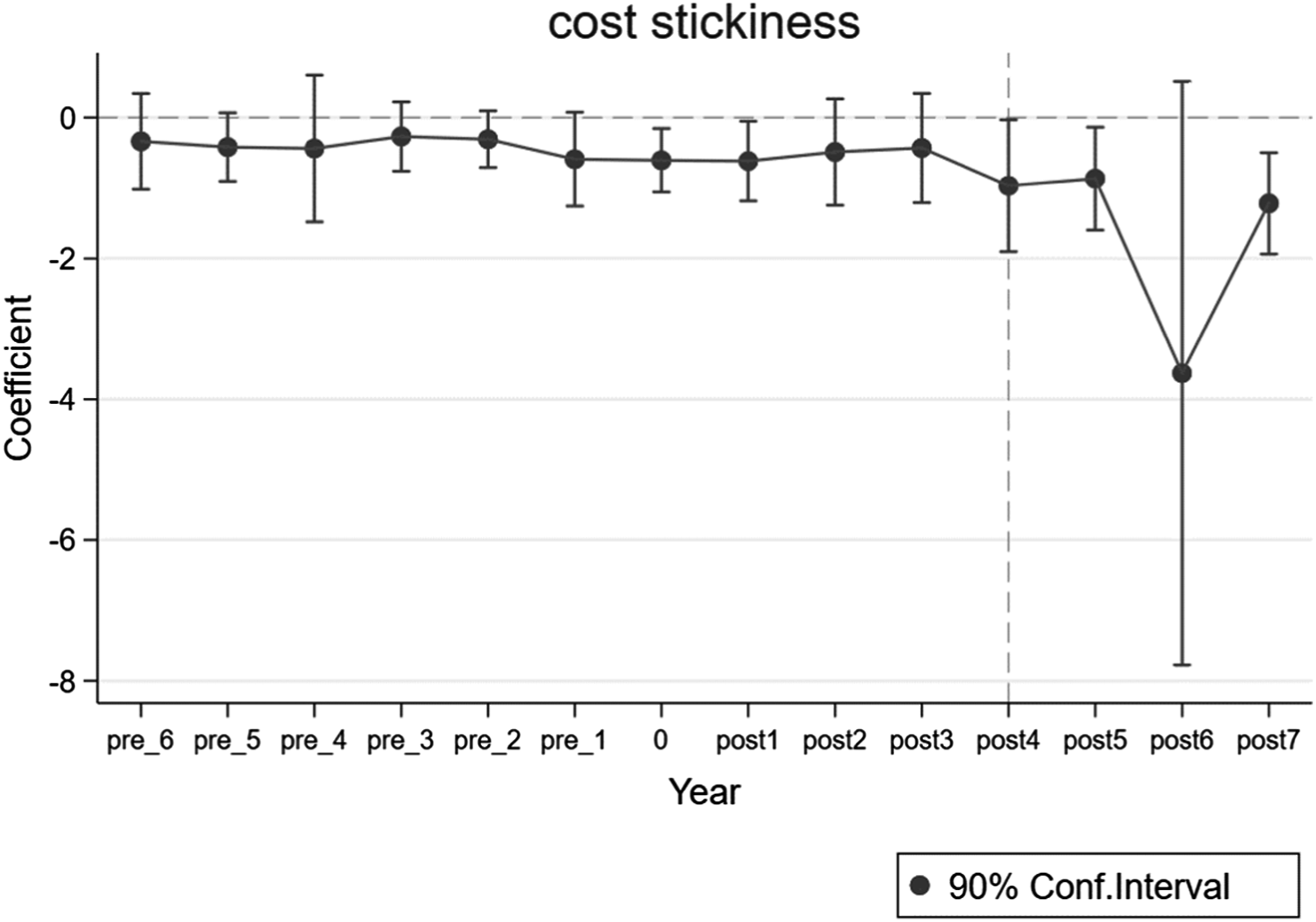

Common trend test

Fulfilling the common trend assumption before using the DID method, which can ensure the causality relationship between HSR connection and cost stickiness, is necessary. Specifically, the common trend assumption requires that treatment and control groups have the same trend before the event occurs. Following prior literature (Beck et al., 2010; Moser and Voena, 2012), we verify the common trend assumption by showing the significance of the coefficients of the HSR dummy variable in Figure 1. As illustrated, the coefficients of the HSR dummy variable on cost stickiness are insignificant for all 6 years before HSR connection at the 10% level, which indicates that no significant difference in the degree of cost stickiness exists between treatment and control groups before HSR connection, satisfying the parallel trend hypothesis. The impact of HSR on cost stickiness is significant in the first, fourth, fifth, and seventh years after HSR connection, which demonstrates the dynamic effect of HSR opening on cost stickiness. Common trend test.

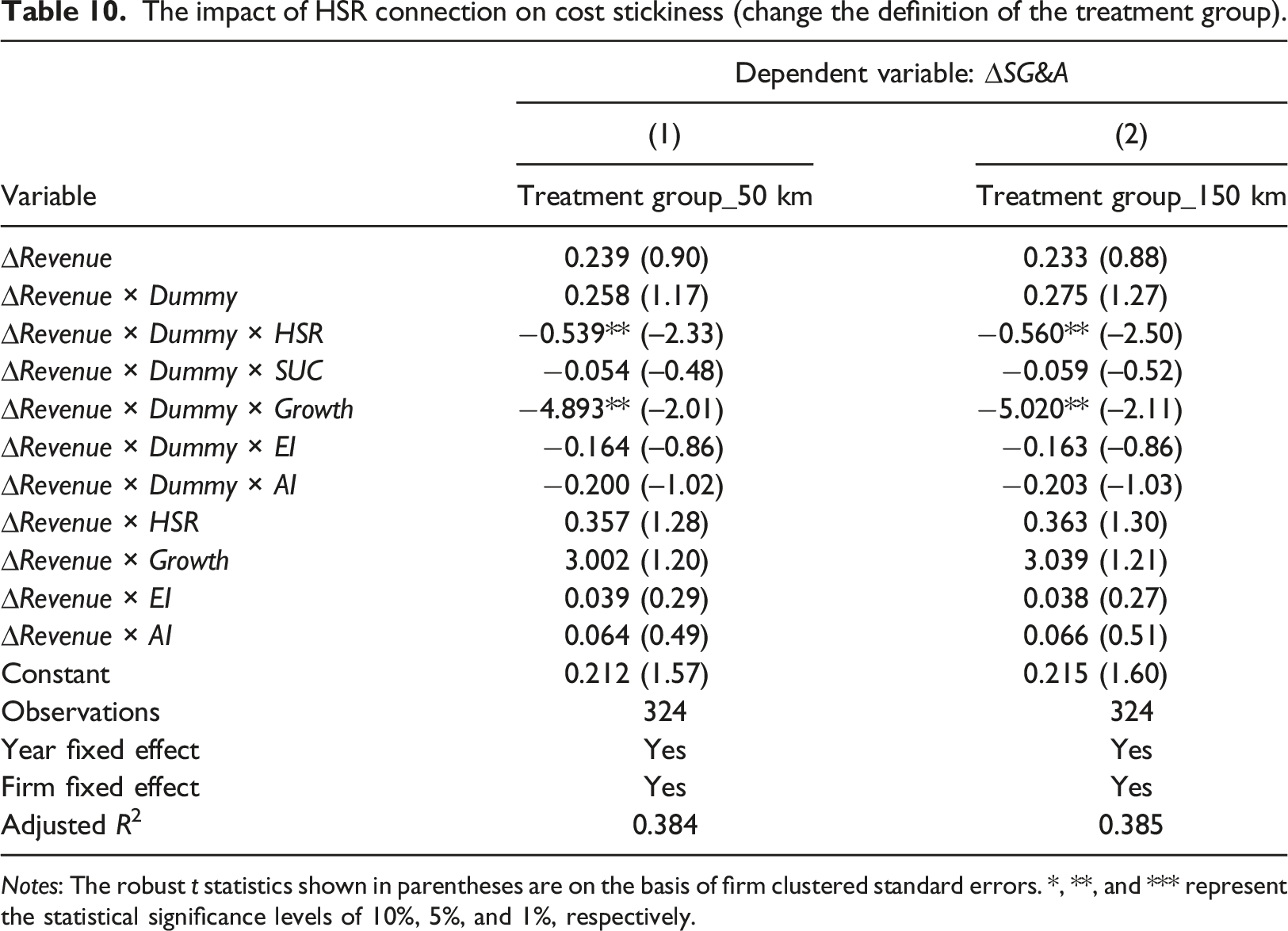

Change the definition of the treatment group

As firms that are not located in HSR-connected cities but adjacent to HSR-connected cities are also affected by the opening of HSR, we conduct the robust test by including firms that are close to the HSR-connected cities as the treatment group. Specifically, if a firm is located in a city that is 50 or 150 km away from the HSR-connected cities, then it is included in the treatment group. Accordingly, variable HSR i,t is coded one if firm i is located in or adjacent to the HSR-connected city in year t, and zero otherwise.

The impact of HSR connection on cost stickiness (change the definition of the treatment group).

Notes: The robust t statistics shown in parentheses are on the basis of firm clustered standard errors. *, **, and *** represent the statistical significance levels of 10%, 5%, and 1%, respectively.

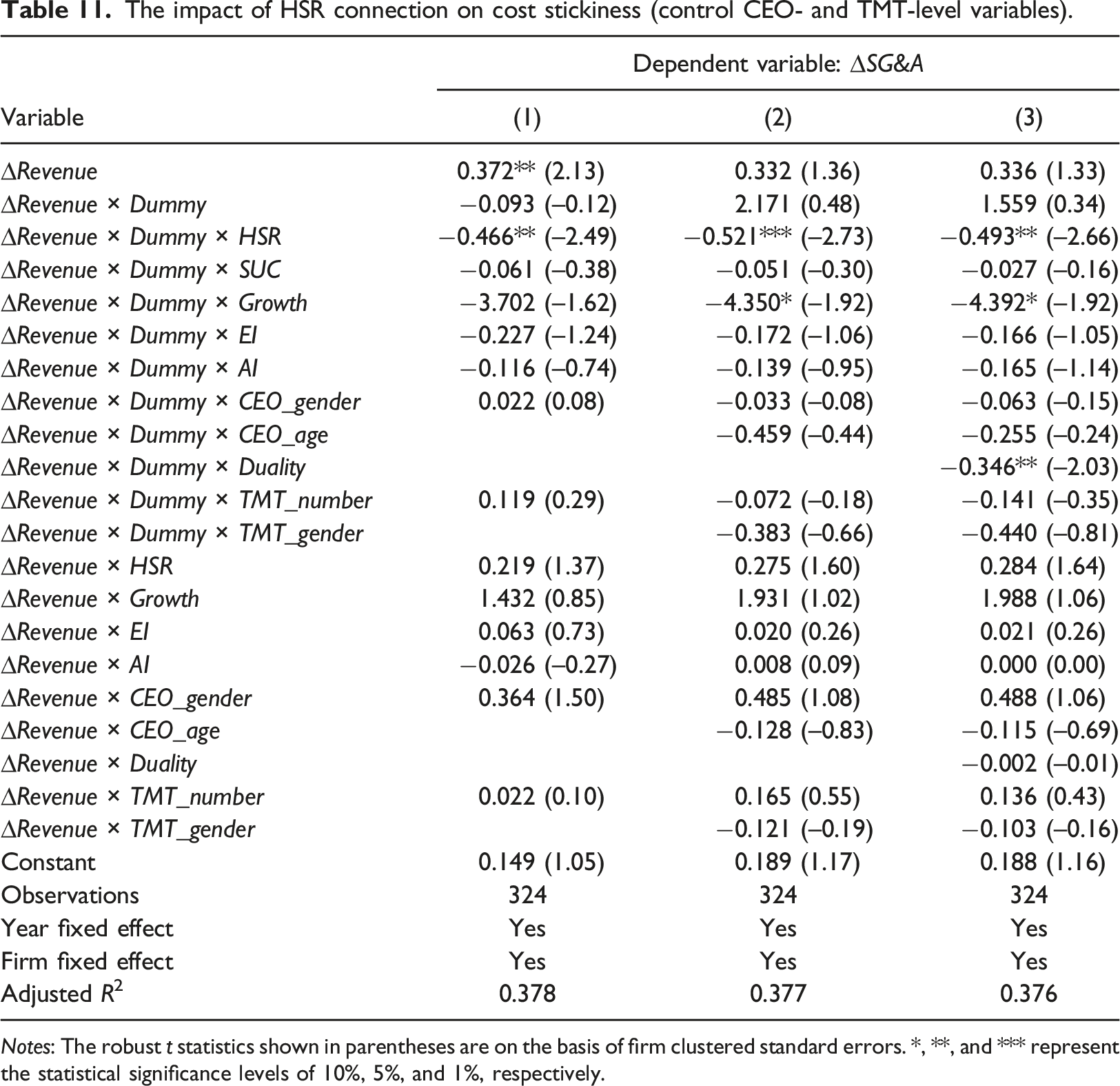

Control the chief executive officer (CEO)-level and TMT-level variables

As the cost management decisions are generally made by TMT, managers play an important role in the process of cost adjustment activities (Anderson et al., 2003; Banker et al., 2013). We control the CEO- and TMT-level characteristics in our model, and re-examine the impact of HSR connection on cost stickiness of tourism firms. Specifically, we control CEO gender, CEO age, and CEO duality as CEO-level variables, and the number of TMT and the ratio of the number of female executives to the number of TMT as TMT-level variables. CEO_gender is a dummy variable coded one when the CEO of the firm in year t is female, and zero otherwise. CEO_age is the age of the CEO, which is calculated as the logarithm of one plus the age of the CEO. Duality is an indicator variable, which is equal to one if the CEO and the board chair is the same person, and zero otherwise. TMT_number refers to the number of TMT in year t, and TMT_gender is the number of female executives divided by the number of TMT.

The impact of HSR connection on cost stickiness (control CEO- and TMT-level variables).

Notes: The robust t statistics shown in parentheses are on the basis of firm clustered standard errors. *, **, and *** represent the statistical significance levels of 10%, 5%, and 1%, respectively.

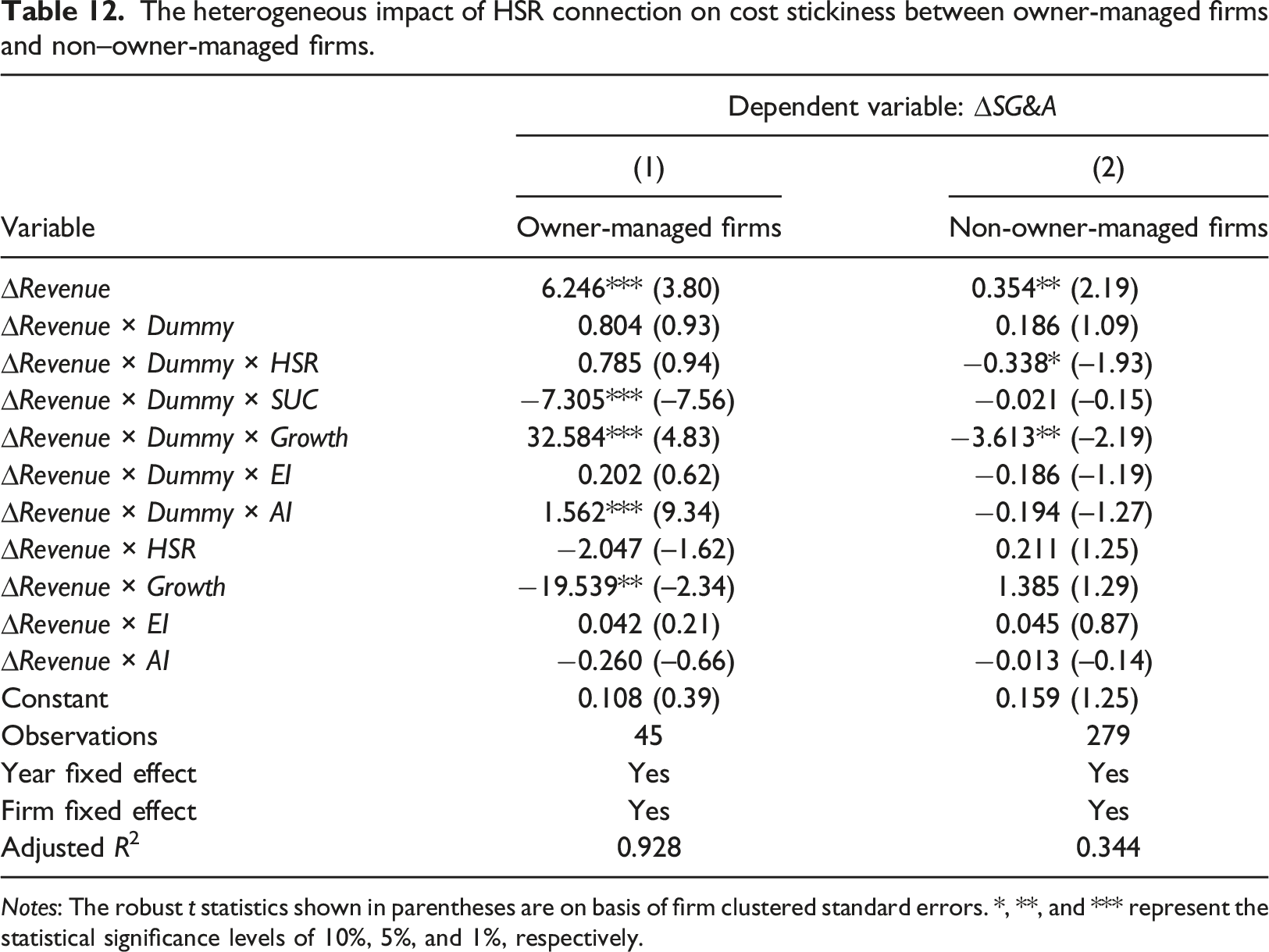

Strengthen the managerial empire building hypothesis

The heterogeneous impact of HSR connection on cost stickiness between owner-managed firms and non–owner-managed firms.

Notes: The robust t statistics shown in parentheses are on basis of firm clustered standard errors. *, **, and *** represent the statistical significance levels of 10%, 5%, and 1%, respectively.

Conclusions and discussions

This study examines the impact of HSR connection on cost behavior of the tourism firms by using the DID method. The whole sample contains Chinese listed firms in the tourism industry from 2003 to 2018. Our results show that cost and cost stickiness of tourism firms increase after HSR introduction, indicating that HSR has a dark side. The relationship between HSR connection and the degree of cost asymmetry of tourism firms is more pronounced in firms whose FCF and unit labor costs are higher. Moreover, we compare the ownership heterogenous effect of HSR connection on cost stickiness, and our results suggest that the influence is more significant in SOEs than that in non-SOEs. We further investigate the relationship between HSR connection and labor cost adjustment decisions, and evidence that the degree of labor cost stickiness in tourism firms is higher after the introduction of HSR. As a robustness check, we confirm the validity of the DID method by conducting a placebo test and a common trend test.

Theoretical implications

Taken together, these results contribute to an in-depth understanding of cost behavior in tourism. Firstly, different from prior literature that mostly explored the relationship between HSR introduction and tourism growth (Albalate and Fageda, 2016; Gao et al., 2019), our study complements the tourism research by examining the impact of HSR connection on cost stickiness of tourism firms, which advances the understanding of corporate cost management and firm operating efficiency in the tourism industry after the opening of HSR, and further reflects managerial resource adjustment decisions based on the future development of tourism firms.

Secondly, our research extends tourism literature by analyzing agency problems of tourism firms from the perspective of cost stickiness. Most of the prior literature analyzed agency problems in the tourism sector by examining the role of ownership structure (Al-Najjar, 2015; Yeh, 2019), board characteristic (Al-Najjar, 2014; Ooi et al., 2015; Song et al., 2021; Yeh, 2018), CEO characteristic (Trinh and Seetaram, 2022), and managerial compensation structure (Kim and Gu, 2005). However, scant tourism literature examines agency problems from the perspective of firms’ cost behavior. Our study explores the moderating impact of managerial empire building incentives on the association between HSR connection and cost stickiness, which widens the angle of studies on the agency problems of tourism firms.

Thirdly, we advance the understanding of labor cost adjustment decisions in tourism firms by studying labor cost stickiness. Prior works demonstrated the existence of labor cost stickiness and their samples are composed of listed firms (Gu et al., 2020; Prabowo et al., 2018), but these studies overlooked industry differences. Our results focus on the tourism industry in which labor costs account for a significant proportion of the total costs. We find that labor cost stickiness of tourism firms increases after HSR connection, indicating that firms are prone to retaining more human resources when sales shrink after HSR connection in the tourism industry.

Practical implications

This study also highlights important practical implications for shareholders, managers and employees of tourism firms, and policy-makers. Firstly, it demonstrates that managers in tourism firms are more likely to exhibit empire building behaviors after HSR connection. That is, managers tend to overinvest and increase firm size, exceeding the optimal level, which would consequently jeopardize firm profitability and shareholder wealth in the long run (Hope and Thomas, 2008). Shareholders could intervene at an earlier stage to prohibit managers from conducting opportunistic activities before the efficiency of business falls. At the same time, shareholders need to evaluate whether the current cost management decisions are rational, and facilitate the implementation of more informed cost adjustment plans. Eventually, this may ensure that tourism firms are exempt from high operating risks and develop healthily.

Secondly, the increased cost stickiness after HSR connection would aggravate the operating risks of tourism firms, which may bring further financial constraints for firms (Baños-Caballero et al., 2014) and lead to the reputation losses of managers (Jian and Lee, 2011). Managers of tourism firms should make informed cost management decisions according to the current economic environment after HSR introduction, and improve firm governance structure such as strengthening the internal control to avoid opportunistic behaviors.

Thirdly, our research shows that labor cost stickiness increases after the opening of HSR, implying that tourism firms are not inclined to lay off employees when sales decrease after HSR connection. The conclusion provides implications for employees choosing where to seek employment in the tourism sector, and cities connected by HSR are excellent options for them.

Fourthly, although previous studies indicated that HSR connection boosts local economic growth (Albalate and Fageda, 2016; Campa et al., 2016), our research reveals that HSR connection has a dark side for tourism firms, manifested in cost stickiness increases after HSR opening. The increased cost stickiness both exacerbates firm operating risks and raises firm labor costs. Consequently, policy interventions aimed at controlling for excessive expansion of tourism firms and providing supporting measures to help companies limit the increase of labor costs are recommended.

Limitations

Our study has some limitations. Firstly, our sample size is limited because we need data of two consecutive years to measure changes in SG&A expenses and sales revenue. Besides, to analyze the net impact of HSR connection on the cost behavior of tourism firms, we exclude non-located firms that have branches all over China. Secondly, managers’ attitude (e.g., optimistic or pessimistic) and estimate towards tourism development could be important factors that influence the resource adjustment decisions of tourism firms. However, appropriate proxies to measure them are limited so far. If reliable measures could be identified, we would have a deepened understanding of the association between HSR connection and tourism.

Supplemental Material

Supplemental Material - Does high-speed railway affect the cost behavior of tourism firms? Evidence from China

Supplemental Material for Does high-speed railway affect the cost behavior of tourism firms? Evidence from China by Fangjun Wang, Lizhu Ma, Baojun Gao and Yang Stephanie Liu in Tourism Economics

Footnotes

Acknowledgements

The authors gratefully acknowledge helpful comments received from workshop participants at 2021 European Accounting Association (EAA) Annual Conference and Xi’an Jiaotong University.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the financial supports from National Natural Science Foundation of China under Grant [71972152, 71771182, 72072143, and 72011540408].

Supplemental Material

Supplemental Material for this article is available online

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.