Abstract

Taking the tourism and related industry companies listed in Shanghai and Shenzhen of China from 2006 to 2019 as samples, this paper examines the impact of board interlock on corporate risk-taking and its micro-mechanism. Empirical evidence shows that board interlock can significantly improve corporate risk-taking, but the degree of influence varies from industry to industry. For the external risk sensitivity of industry, in the industry with high external risk sensitivity, the “quantity embedding” of interlocking directors has a stronger promoting effect on enterprise risk-taking. However, in industries with low external risk sensitivity, the “quality embedding” of interlocking directors has a stronger promoting effect on enterprise risk-taking. For the degree of industry competition, the more intense the industry competition, the stronger the role of board interlocks in promoting enterprise risk-taking. Further analysis shows that the intensity of information effect and the intensity of resource effect vary with the degree of information asymmetry and the type of directors.

Introduction

“Creative destruction” is a process of constantly destroying old structures and establishing new ones. This provides sustained impetus to economic growth (Schumpeter, 1950), and brings greater risks. Enterprises are the protagonist of “creative destruction” in social economy. Corporate risk-taking plays an important role in promoting their own value and productivity, as well as the growth of the national economy (Aghion et al., 2013; John et al., 2008; Sanders and Hambrick, 2007; Wahal and McConnell, 2000). From the micro perspective, the higher level of corporate risk-taking usually indicates higher capital expenditure of enterprises (Bargeron et al., 2010). This indicates that enterprises are taking full advantage of investment opportunities. In addition, the higher level of risk-taking can enhance the innovation enthusiasm and long-term competitiveness of enterprises (Cucculelli and Ermini, 2012; Hilary and Hui, 2009; Low, 2009). From the macro perspective, although choosing relatively safe investment opportunities can bring more stable returns, it also keeps the productivity of the whole society at a low level (Acemoglu and Zilibotti, 1997). High-risk projects can bring higher expected returns than low-risk projects. It can accelerate the capital accumulation of the whole society, promote technological progress, improve social productivity, and achieve long-term economic growth (De Long and Summers, 1994; John et al., 2008).

The existing literatures are usually based on the principal-agent framework, and study the way to enhance corporate risk-taking, from the perspectives of management incentives (e.g., Choy et al., 2014; Kim and Lu, 2011), decision-making autonomy (e.g., Pathan, 2009; Sheikh, 2019) and personal characteristics of executives (e.g., Faccio et al., 2016; Li and Tang, 2010). These studies provide extensive evidence that corporate risk-taking is influenced by internal governance mechanisms, but informal institutional factors are not well considered. Chinese society is a typical “guanxi society.” “Guanxi transaction” has a profound cultural foundation, and social network has become one of the important ways for many Chinese enterprises to obtain resources (Wong, 2007). The social networks of enterprises cover many aspects, such as enterprise-enterprise, government-enterprise, and association-enterprise. As a supplement to the formal system, enterprises can seek information and resources needed for risk-taking through various types of social networks (Cohen et al., 2008). Among all social networks of enterprises, interlocking director relationship has a unique position. The board is the core of corporate governance structure, and board interlocks drive the interaction among enterprises through personal interaction, which is likely to be a valuable resource for enterprises (Zheng, 2011). Wind Database statistics showed that as early as the end of 2012, 98.95% of listed companies in China had interlocking directors. This shows that interlocking directors have become a necessary aid to the operation of Chinese enterprises.

Board interlocks are not a new topic in corporate finance. However, existing studies on board interlocks are rarely based on a specific industry. Ooi et al. (2015) pointed out that board capital includes human capital and social capital. The optimal combination of human capital and social capital of the board in the firms should be varied between industries. The human capital of the board may be more important for corporate management decision in some specific industries, such as manufacturing and information technology industries that require specific knowledge and skills. However, the social capital of the board may be more important for management decision in hotels, travel agencies, and other tourism-related service industries. Tourism is a relational phenomenon (Merinero-Rodríguez and Pulido-Fernández, 2016), and the completion of tourism activities requires multi-enterprise cooperation. For example, travel agencies and hotels establish good relationships to ensure that their services are promoted. Hotels near the airport terminal or railway station usually cooperate with taxi companies to pick up and drop off customers. Tourists-oriented retailers cooperate with travel agencies so that tourists can visit their retail exhibition halls. In addition, the supervisory role of the board of directors on strategic planning and implementation is relatively more significant in tourism enterprises. This is due to the reason that the operation of tourism is easily affected by seasonality, inflation, and rapidly changing consumer demand, and tourism companies must frequently adjust their strategies according to the rapidly changing environment (Pechlaner and Sauerwein, 2002).

Although board interlock is common in the travel industry because of its strategic importance, most tourism and hospitality literatures have investigated the board size (e.g., Peng et al., 2021; Yeh, 2018), board structure (e.g., Jarboui et al., 2015; Ooi et al., 2015) and the ownership of directors (e.g., Yeh, 2018, 2021), only a few studies paid attention to board interlock. Keiser (2002) conducts an exploratory analysis of the industry affiliations of board members in the airline, hotel, and restaurant industries. However, this study used only descriptive statistical data (e.g., the number of board members and industry relationships generated by board interlocks), and did not put forward a relationship hypothesis to examine the consequences of board interlocks. Song et al. (2021) focus on board interlock of catering industry, and investigated the influence of board interlocks on financial performance. Ooi et al. (2015) and Yousaf et al. (2021) show the positive correlation between social capital of board and company performance in tourism. Those studies in the tourism industry only focus on the “quantity” embeddedness of interlocking directors and the relationship between interlocking directors and financial performance. They do not pay attention to the “quality” embeddedness of interlocking directors, and do not examine the relationship between interlocking directors and enterprise risk-taking. In addition, the test results that board’s social capital has a positive effect on firm performance in tourism literature are not consistent with the findings of Carpenter and Westphal (2001) taking industrial and service firms as samples. This contradictory phenomenon further indicates that it is necessary to re-test the consequences of interlocking directors based on sub-industries.

This study focuses on tourism and related service industries, and examines the impact of board interlocks on corporate risk-taking. Tourism is not a single, isolated industry, but a collection of businesses of all selling travel-related services, linked by competition and cooperation relationships (Leiper, 2008), or a tourism industry network composed of travel and tourism-related industries (Gee, et al., 1989; Wu and Song, 2011). Referring to Wu and Song (2011) and Liu (2015), this paper argues that modern tourism activities are supported by a series of industries with different degrees of contact with tourism activities, including catering, hotel, tourism, transportation, retail, and real estate industries. Among them, catering, hotel and tourism industries are the tourism core industries that are familiar to the public (Gee, et al., 1989). Transportation, retail and real estate industries are tourism support industries 1 . The main contributions of this paper are as follows. First, the paper provided empirical evidence for the relationship between the board interlock and corporate risk-taking under the background of Chinese listed tourism and related industry firms. To our knowledge, this paper is the first attempt to empirically study the relationship between the board interlock and corporate risk-taking in tourism industry. Second, this paper investigated the relationship between board interlocks and corporate risk-taking under different backgrounds. The results show that the effectiveness of “quantity” embeddedness and “quality” embeddedness of board interlocks change with the degree of industry competition and the external risk sensitivity of industry. We drew more specific research conclusions and provided the theoretical basis of multiple embeddedness. Third, this paper revealed the mechanism of board interlock on corporate risk-taking. We found that board interlocks can exert both “information effect” and “resource effect.” Further, the results of this study will suggest practical guidelines for professionals and stakeholders in the tourism and related industries as to how a firm can compose a board for improving corporate risk-taking.

The structure of this paper is as follows: the second part focuses on the logical relationship between interlocking director network and corporate risk-taking, and puts forward research assumptions; The third part expounds the research design; The fourth part tests the hypothesis and analyzes its robustness; The fifth part further analyzes the mechanism of interlocking directors affecting corporate risk-taking; The sixth part is the research conclusion and management implications.

Literature review and research hypothesis

Board interlock

According to the “embeddedness” theory, the economic behavior of any entrepreneur or enterprise carrying out various activities in its social structure is inevitably embedded in the social network relationship. In this network, they exchange resources and information with other organizations or people, thereby forming “social capital” (Granovetter, 1985). China is in a period of transition economy. Compared with the mature market economy, the fundamental difference lies in the different degree of development of institutional systems. In a mature market economy, the network relationship between enterprises is a supplement to the formal system, while in a transitional economy, the network relationship between enterprises is a substitute for the imperfect formal system (Zhu and Li, 2011). Therefore, board interlocks network, an inter-enterprise network formed by directors serving on the boards of two or more companies (Mizruchi and Stearns, 1988), is particularly important for Chinese listed companies.

In the analyses of the influence of board interlock, it mainly emphasizes its information, resource, and control incomes. These benefits are obtained through relational embeddedness and structural embeddedness (Granovetter, 1973). Relational embeddedness refers to the relationship characteristics between network members, including the trust degree and close relationship degree (Coleman, 1990). Relationships with high interaction frequency, deep affection, and frequent reciprocal exchanges are called strong relationship. Structural embeddedness refers to the location characteristics of members in the network, including density, connectivity, and hierarchical structure (Wasserman and Faust, 1994). In the board interlock network, relational embeddedness is repetitive communication and cooperation between enterprises, which is conducive to strengthening information sharing and resource complementarity among enterprises. In the existing literature, relational embeddedness data is generally from questionnaire (e.g., Ferraris et al., 2018; McEvily and Marcus, 2005). Due to the difficulty in issuing questionnaires, we studied the impact of board interlocks on corporate risk-taking from the perspective of structural embeddedness.

Structural embeddedness focuses on directors’ positions in the network structure (Gulati, 1998), and a high level of structural embeddedness is conducive to promoting information and resources sharing, social monitoring, and reputation effects (Gulati and Gargiulo, 1999; Polidoro et al., 2011). “Quantity” embeddedness and “quality” embeddedness can measure two different dimensions of interlocking directors in the social network. Therefore, this paper analyzed the influence of interlocking directors on enterprise risk-taking from the aspects of “quantity” embeddedness and “quality” embeddedness.

The relationship between board interlocks and corporate risk-taking

The risk-taking behavior of enterprises is a resource-consuming activity (Almeida and Campello, 2007; Fazzari et al., 1988). Without enough support, companies will face resource constraints, resulting in low investment efficiency and even investment failure (Chen et al., 2013). The resource dependence theory and collusion theory are two prominent perspectives in support of obtaining information and resources from board interlocks. Resource dependence theory believes that organizations need to acquire resources from the environment, and no organization is self-sufficient (Pfeffer and Salancik, 2003). The board interlocking, as a link between multiple companies, is a key strategy that can help a company obtain information and resources from other companies. This can reduce environmental uncertainty and improve enterprise competitiveness (Campello et al., 2012). Collusion theory believes that board interlock is an arrangement for reciprocal transactions between affiliated companies. And the enterprise can obtain resources and information (Koenig et al., 1979; Koenig and Gogel, 1981; Mizruchi, 1996). Based on the above analysis, this paper argues that interlocking directors can improve enterprise risk-taking through information effect and resource effect.

“Quantity” embeddedness of board interlocks and corporate risk-taking

The high level of “quantity” embeddedness of interlocking directors, the more other enterprises directly related to the company, the wider the channels for enterprises to obtain information and resources, the richer the information and resources that can be collected and exchanged. Then, this forms the company’s scale advantage in information and resource (Granovetter, 1985; Salman and Saives, 2005). Under same conditions, the influences of “quantity” embeddedness of board interlocks on risk-taking are shown in the following three aspects. First, seeking the investment projects and evaluating the investment value can increase the costs of information and transaction to enterprises. And information asymmetry is an important factor for underinvestment and inefficiency investment (Bai et al., 2005; Lin and Li, 2001). Tourism enterprises with high “quantity” embeddedness of board interlocks can more comprehensively and accurately grasp the information such as the supply and demand level of tourism market, industry development trends, customer preferences, financial status of partners, etc. This can help them better understand project risks and uncertainties, reducing investment costs and improving investment efficiency (Bartjargal and Liu, 2004). Second, board interlocks are often well-known social celebrities. This kind of interpersonal network resources and reputation resources can play a guarantee role and help companies reduce financing costs (Hillman and Dalziel, 2003). When profitability is poor, and there is no effective collateral, it is often difficult to obtain debt financing for companies. However, interlocking directors can use their reputation to endorse the borrower and implicitly guarantee of company’s debts. Finally, the resources of a single tourism enterprise are limited. Thus, it is necessary for the tourism firms to constantly communicate and cooperate with others to acquire more resources, such as talents, technology, and capital. Tourism enterprises with a higher level of “quantity embedding” of interlocking directors can obtain more such resources from other companies in the social network (Bagul and Mukherjee, 2018). This can reduce the uncertainty of business environment and transaction costs, and improve the corporate risk-taking (Zhang et al., 2015). For example, if the director of a travel company is also a board member of an investment company, he/she can support the financing of the travel company if it needs additional capital to expand business. Therefore, this study puts forward the following assumption:

“Quality” embeddedness of board interlocks and corporate risk-taking

The high level of “quality” embeddedness indicates that the company’s position in the social network is critical, with access to key information and resources. According to the “structural hole” theory, companies that occupy the “bridge” position in social networks can build a communication platform for companies that have no direct connection. The more structural holes companies occupy, the more heterogeneous information and resources they can obtain (Zona et al., 2018). A tourism company occupies a rich structural hole in the supply network can contact different companies in a wide range and collect valuable heterogeneous information and resources, so as to gain an early insight into the opportunities and risks existing in the network. This can help the company make venture capital decisions (Luo et al., 2016). For example, if a director of a hotel group serves as a director in both a catering company and a real estate development company, the relevant market information and management experience accumulated from participating in the management of real estate companies and catering companies may help the hotel group achieve business diversification and chain operation. In addition, companies with rich structural holes act as “bridges” in the network. They can collect and sort out the flowing information and resources, and decide the flow direction, thereby playing a certain control role in other companies’ resource acquisition and business decisions (Burt, 2000). One of the factors that affect the venture capital activities of tourism enterprises is the uncertainty that enterprises’ inability to control the trading activities (Chen, 2015), while the structural hole in the network increases the control power of the enterprises and reduces the uncertainty. For example, if tourism companies with rich “structural holes” find potential venture capital opportunities, they can use their control advantage to prevent information and resources from transmitting to the third party, thereby reducing potential competitors and the uncertainty of transactions. Based on the above analysis, this paper puts forward the following assumption:

The relationship between board interlocks and corporate risk-taking under different backgrounds

The external risk sensitivity of industry

“Quantity” embeddedness and “quality” embeddedness depict two different structural embedding characteristics. The “quantity” embeddedness is the number of cooperative relationships of enterprises in cooperative network. The larger the quantity, the wider the sources of information and resources of enterprises. The “quality” embeddedness is the key position of enterprise in cooperative network. The higher the quality, the more critical information and resources are available to the enterprise. “Quantity” embeddedness and “quality” embeddedness show the scale advantage and control advantage of enterprises with external information and resources, respectively. A factor that affects the type of advantages required by enterprises is the extent to which their corporate strategies are influenced by external information, technology, and environments (Rowley et al., 2000). Enterprises must spend more on the collection of external information and resources in an unstable environment. However, in a more stable environment, the uncertainty of the future direction is small and the environmental interference is less (Lant et al., 1992), enterprises only need to obtain key information and resources. Tourism is seriously affected by a series of exogenous crises such as natural disasters, wars, terrorism, and disease outbreaks (Lydecker, 1986; Ross, 2005), so board interlocks with rich network connections are more important for it. Tourism enterprises must obtain information and resources as much as possible to track market changes and resist risks, and then find a wider range of alternatives to solve complex problems in unstable environments (Carpenter and Westphal, 2001). As for the industries that are less affected by market fluctuations, board interlocks who occupy the core position are much more important for them. The reason may be that the market environment is not their first consideration. They prefer to seize the core position in the market, that is, occupying the position of “bridge” by mastering key information and resources. Therefore, this paper puts forward the following assumption.

The positive correlation between the “quantity” embeddedness of board interlocks and enterprise risk-taking in industries with high sensitivity to external risks is stronger than that of industries with low sensitivity to external risks. The “quality” embeddedness of board interlocks and enterprise risk-taking in industries with low sensitivity to external risks is stronger than that of industries with high sensitivity to external risks.

The degree of industry competition

The role of the social network can be influenced by the characteristics of the actors (Burt, 1992), and the degree of industry competition of the enterprise is the characteristic factor of the enterprise’s operation and investment efficiency, so the role of the interlocking directors depends on the degree of industry competition. In monopoly industries, enterprises gain a dominant position in financial activities such as operation and investment by the virtue of their monopoly position. Therefore, enterprises rely less on the role of the network formed by the concurrent positions of directors, and rely more on the direct monopoly position to gain negotiating advantage (Park and Luo, 2001). However, in highly competitive industries, enterprises cannot achieve significantly better returns than other enterprises through their own position. To gain more market share and invest in more effective projects, enterprises in competitive industries need to occupy favorable market position and overcome uncertainty through their social networks (Luo, 2003; Park and Luo, 2001). Most industries involved in tourism are traditional labor-intensive industries with low entry thresholds. Some industries are in a state of excessive competition, and the market order is chaotic, resulting in most tourism enterprises operating at low profit or straggling to survival (Yi, 2006). In this management environment that requires keen insight and the ability to process complex information, board interlocks who directly or indirectly participate in the management process of the company can be more capable of reducing uncertainty and establishing core competence (Barroso-Castro et al., 2017; Carter and Lorsch, 2004), thereby resisting business risks. Therefore, this paper hypothesizes that the positive impact of board interlocks on enterprise risk-taking may be amplified with the increase of industry competition.

The degree of industry competition has a positive moderating effect on the relationship between board interlocks and corporate risk-taking.

Research design

Data

This paper takes China’s tourism and related industries as the samples. According to the China Securities Regulatory Commission’s “Guidelines for the Classification of Listed Companies,” the study collected the data of listed companies in the catering, hotel, tourism, real estate, transportation, and retail industries listed on Shanghai and Shenzhen Stock Exchanges from 2006 to 2019. Although some companies belong to the six industries, their actual business is far from the tourism industry. To ensure the rigor of research, this study checked the business scope of each sample company in the basic database one by one, and excluded as follows: companies in the real estate industry only involve auxiliary facilities business (such as construction molds, machinery, and equipment); companies in the transportation industry only involve cargo transportation, loading, and unloading; companies in the retail industry only involve technology development and sales. The paper also excluded following companies, such as ST (Special Treatment), PT (Particular Transfer), and serious data missing. Finally, there were 236 company samples (4 catering companies, 6 hotel companies, 25 tourism companies, 94 real estate companies, 33 transportation companies, and 74 retail companies) with a total of 2159 observations. The data comes from Chinese authoritative database-CSMAR. The index selection mainly includes three aspects: director network, corporate risk-taking, and other company characteristics.

Models and estimation methods

This study constructs model (1) to test H1a and H1b. The model was specified as follows:

To test H2, this paper first identified industries with high external risk sensitivity and industries with low external risk sensitivity according to the test results of model (2). Then, we verified whether there are differences in the effect of board interlocks on enterprise risk-taking based on the estimation results of model (3).

In model (3),

To test H3, this paper added the degree of industry competition and the interaction between industry competition and board interlocks into model (1), and obtained the measurement model (4).

Variables measure

Corporate risk-taking (Risk

i,t

)

Common indicators of corporate risk-taking include the volatility of return on assets (Roa) (e.g., Boubakri et al., 2013; John et al., 2008; Ozdemir et al., 2021), stock return volatility (e.g., Bargeron et al ., 2010; Coles et al., 2006), debt ratio (e.g., Faccio et al., 2011, 2016), and the possibility of firm survival (e.g., Faccio et al., 2016). Due to the special institutional and policy environment in China, the living conditions of listed companies in China can be affected by government policies. Therefore, this paper uses the volatility of return on assets to measure the risk-taking level of Chinese enterprises, the volatility of return on net assets adjusted by industry, and annual average and the volatility of stock returns to measure the risk-taking in the robustness test.

Roa is measured by dividing earnings before interest and taxes by total assets at the end of the year. To reduce the impact of industry and cycle, the paper refers to John et al. (2008) and Yu et al. (2013), subtract the annual industry average from Roa to get Adj_Roa. Then, took every 3 years

2

(t-2 to t year) as an observation period of paper, and calculated the SD and range of Adj_Roa adjusted by the industry according to equations (5) and (6). Based on the processing methods of Faccio et al. (2016) and Song et al. (2017), the paper multiplied the result by 100 to obtain Risk1 and Risk2, which measure the level of corporate risk-taking. The processing can make the results more intuitive, and does not affect its significance.

Board interlocks (Network i,t )

Degree centrality and structural hole are two indicators to measure interlocking directors. Degree centrality mainly describes the extensive degree of connection between individual actors and other actors in the network (Freeman, 1978), and directors in the central position have more network connections in the network. Therefore, the degree centrality can be used to measure “quantity” embeddedness. The higher the degree centrality, the richer the resources and information that interlocking directors can bring. Structural hole mainly depicts the non-redundant connection between two individuals. Individuals occupying the structural hole can form social capital and gain benefits by controlling communication channels between non-redundant contacts (Burt, 1992). Therefore, the structural hole index can be used to measure “quality” embeddedness. The higher the structural hole index, the more heterogeneous resources and information the interlocking directors can obtain. The specific measurement methods of degree centrality and structural holes refer to Freeman (1978) and Burt (1992).

(1) Degree centrality (Degree i )

Degree centrality specifically measures the total number of other individuals directly related to the individual. it is used to measure the direct influence of the individual. The formula is

(2) Structural hole (CI i )

There are four indexes to measure structural holes: effective scale, efficiency, constraint, and grade. The most widely used is the constraint index. The formula is

Corporate network embedded in this paper is based on all board members, including executive directors and non-executive directors, and each director is regarded as an individual. The specific measurement steps are as follows. First, each director member of all companies in each year was identified. The age, gender, education, and work experience of the director were used to distinguish the directors with the same name but different person, and code them separately. Second, this paper established the link between individuals by writing a program to form an overall network, thereby generating a basic file that can be read by Pajek. Finally, the average value of the network embedding index of each director member is used as the enterprises’ embedding index (Li et al., 2017).

The degree of industry competition (Compe i,t )

In the existing literature, the degree of industry competition is measured by the characteristics of industry structure (such as product differentiation, industry concentration, industry average profit rate, number of enterprises in the industry, etc.). Referring to Pan (2005) and Yeh et al. (2012), this paper adopts the popular Herfindahl-Hirschman Index (HHI) to measure the degree of industry competition. The formula is

Control variables

According to prior research, this paper mainly selects the following control variables. Ⅰ. The life of enterprise (Age i,t ) was measured by the number of years from the date of establishment to the statistical year (taking natural logarithm) (Faccio et al., 2016); Ⅱ. The size of enterprise (Size i,t ) is defined as the natural logarithm of the total assets of the company at the end of the year (Bruna et al., 2019); Ⅲ. Actual controller type (Owner i,t ) was set as 1 for state-owned enterprises and 0 for private enterprises (Boubakri et al., 2013); Ⅳ. Revenue growth rate (Growth i,t ) is the year-on-year growth rate of the annual operating income of company. This ratio controls the company’s growth ability (Coles et al., 2006). Ⅴ. Asset-liability ratio (Lev i,t ) is the ratio of total assets to total liabilities (Armstrong and Vashishtha, 2012). Ⅵ. Shareholding concentration (Share i,t ) is measured by HHI of the shareholding ratio of the top five major shareholders (Faccio et al., 2011); Ⅶ. The degree of separation of the two rights (Separation i,t ) is the difference between control right and ownership right (Li et al., 2017); Ⅷ. Board size (Board i,t ) is the total number of company’s directors (Li et al., 2017). Ⅸ. The number of independent directors (Ind_board i,t ) (Li et al., 2017). Ⅹ. The gender of CEO (CEO_fem) was set as 1 for female and 0 for male. Ⅺ. The tenure of CEO (CEO_ten) is the number of years that the CEO has been in the position (Coles et al., 2006), converted from the number of tenure months. XII. CEO equity compensation (CEO_equ) is the ratio of equity and option value to CEO’s total compensation, and the formula refers to Bergstresser and Philippon (2006). In addition, this paper sets industry dummy variables to control the possible impact for the impact of industry environment differences on organizational risk. And the annual dummy variables are controlled for the impact of changes in annual trends on organizational operations and risk-taking.

Empirical analysis

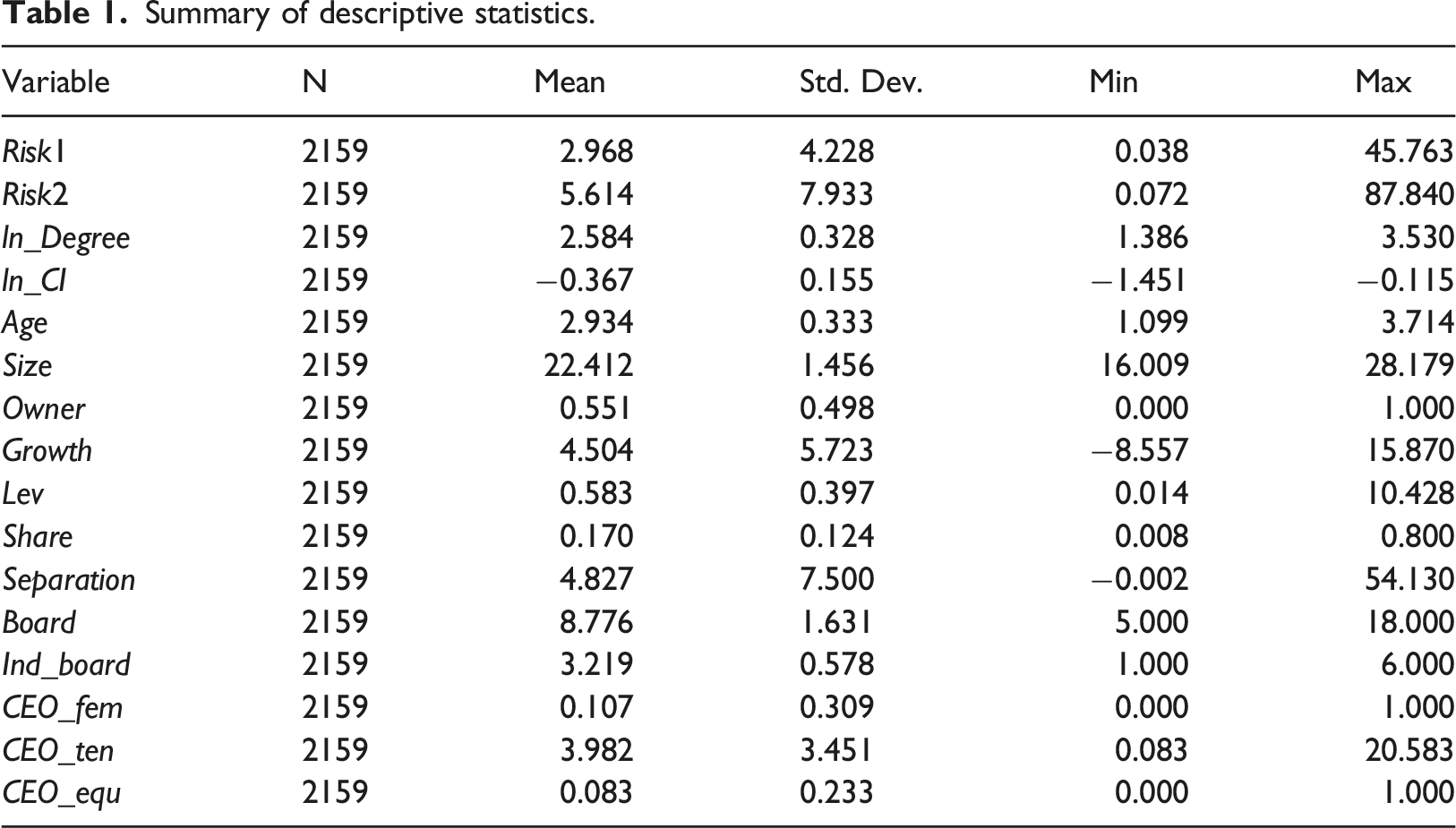

Descriptive statistics

Summary of descriptive statistics.

Multiple regression results

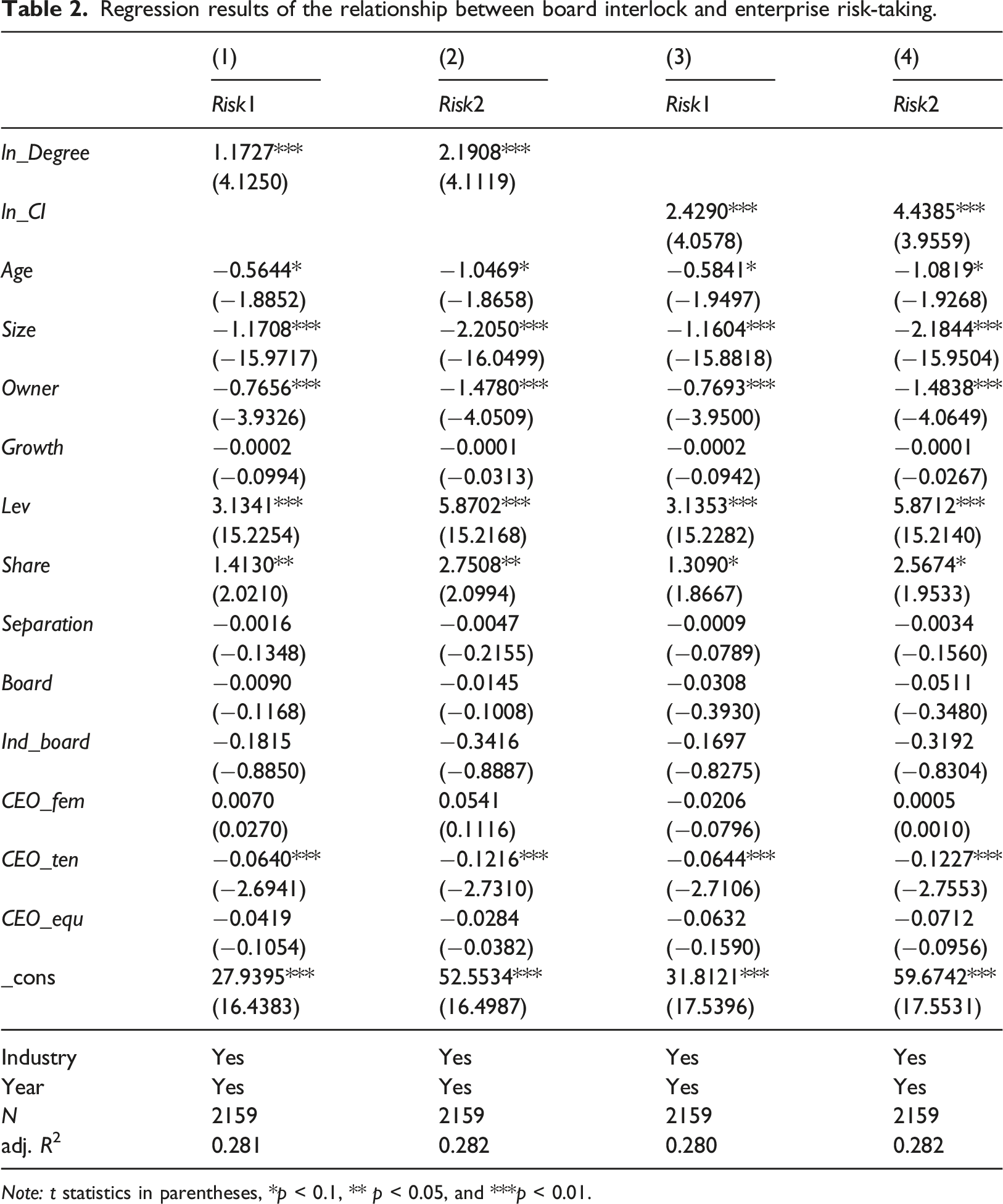

Regression results of the relationship between board interlock and enterprise risk-taking.

Note: t statistics in parentheses, *p < 0.1, ** p < 0.05, and ***p < 0.01.

According to the coefficient estimation results of control variables, start-ups and small enterprises are more likely to invest in risky projects, mature and large enterprises are more inclined to risk aversion projects. Compared with non-state-owned enterprises, state-owned enterprises have a lower-risk appetite, similar to Li and Yu (2012) and Huang et al. (2013). The higher level of corporate debt, the higher level of risk-taking. Company’s equity concentration has a positive relationship with risk-taking. This is consistent with Faccio et al. (2011), Amihud and Lev (1981). Since the sensitivity of the wealth of executives to fluctuations in the value of corporate stocks is a convex function, the relationship between fluctuation of corporate stock value and the value of equity held by senior executives is also convex. This has resulted in company executives becoming more and more willing to take risks when equity concentration increases (Guay, 1999). There is a significant negative correlation between CEO tenure and risk-taking. This indicates that the longer the CEO tenure, the more the companies tend to invest in risk-averse projects. Other control variables did not get the uniformly significant regression coefficients.

Regression results of board interlocks and corporate risk-taking under different backgrounds

The external risk sensitivity of industry

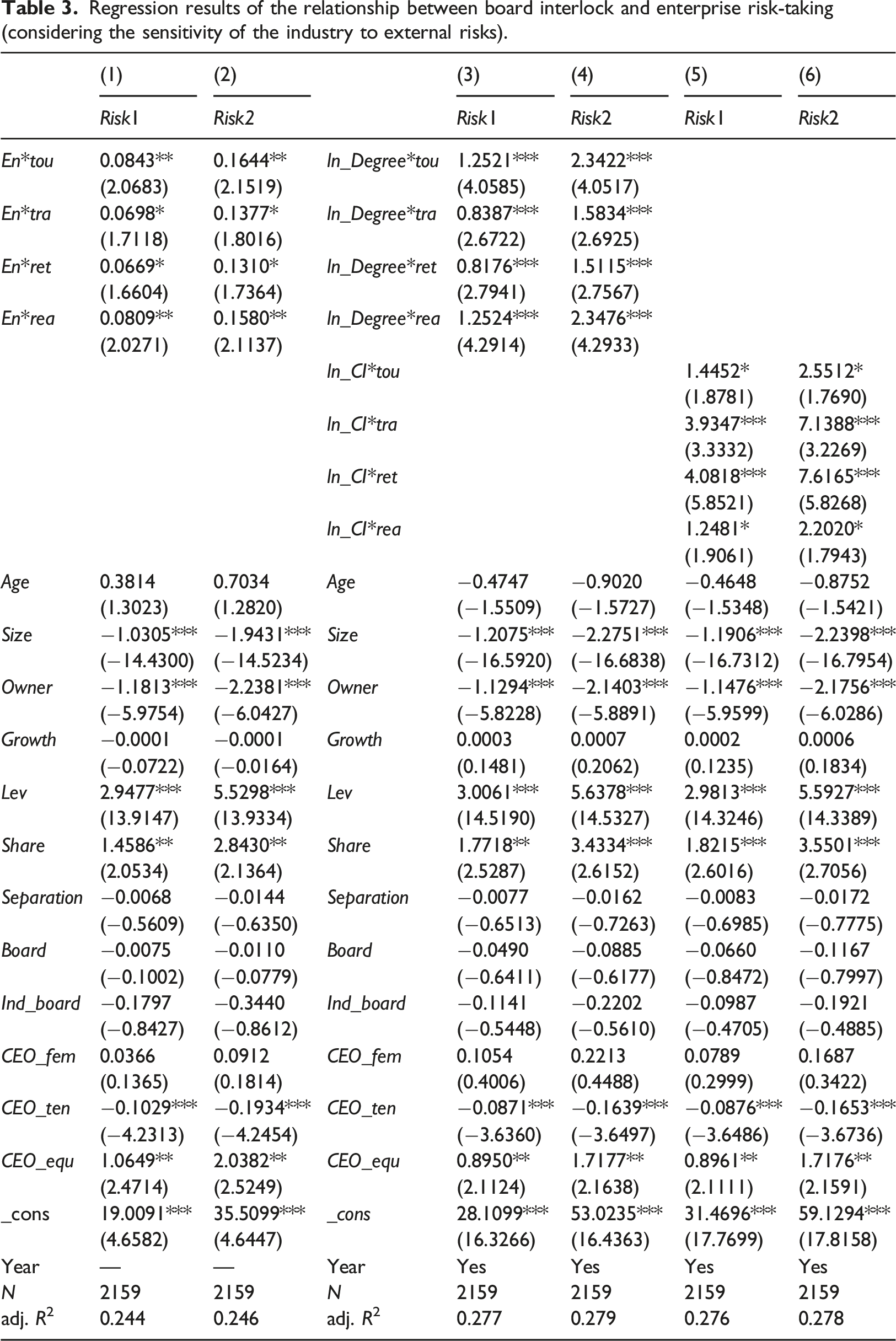

This paper divided the sample enterprises to compare the differences between industries. To avoid too many dummy variables interfering with the estimation results, the sample enterprises are divided into four categories. The first is the tourism core industries(tou), including catering, hotel, and tourism industries; the second is transportation industry(tra); The third is retail industry(ret); the fourth is real estate industry(est).

Regression results of the relationship between board interlock and enterprise risk-taking (considering the sensitivity of the industry to external risks).

The estimation results of columns (3)–(6) in Table 3 show the influence of board interlocks on corporate risk-taking in different industries. The results show that the positive influence of board interlocks on enterprise risk-taking has been supported in different sub-industries, supporting H1a and H1b. Comparing the coefficients of board interlock in different industries, it can be found that when the explanatory variable is degree centrality, the corresponding coefficients of industries with high external risk sensitivity (tourism core industries and real estate industry) are greater than those with low external risk sensitivity (retail industry and transportation industry). When the explanatory variable is structural hole, the corresponding coefficient and significance of industries with low external risk sensitivity are greater than those with high external risk sensitivity. As introduced in the research design, degree centrality and structural hole show two different characteristics of directors’ network. Degree centrality indicates the scale of information and resources acquisition, and structural hole indicates the control of information and resources. The difference in coefficients shows that the “quantity” embeddedness of industries with high external risk sensitivity (tourism core industries and real estate industry) can improve corporate risk-taking more than that of industries with low external risk sensitivity (retail industry and transportation industry). The “quality” embeddedness of industries with low external risk sensitivity can improve corporate risk-taking more than that of industries with high external risk sensitivity, supporting H2.

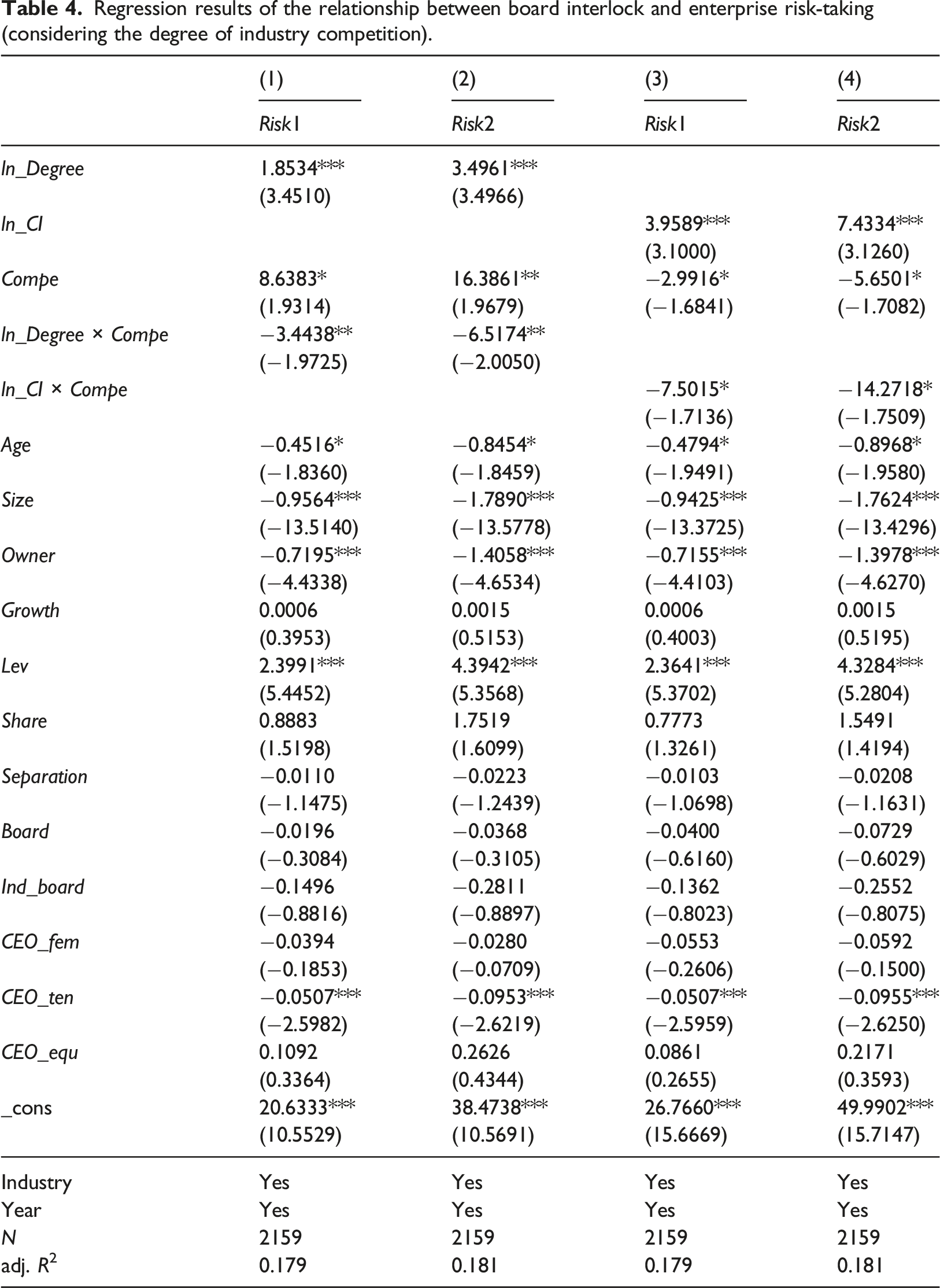

The degree of industry competition

Regression results of the relationship between board interlock and enterprise risk-taking (considering the degree of industry competition).

Robustness test

Endogenous problem

To overcome the possible endogenous problems, such as sample selection bias, mutual causality, and missing variables, this paper adopted the propensity score matching (PSM) method, instrumental variable method, and the fixed effect model to test the robustness of research conclusions.

(1) PSM method

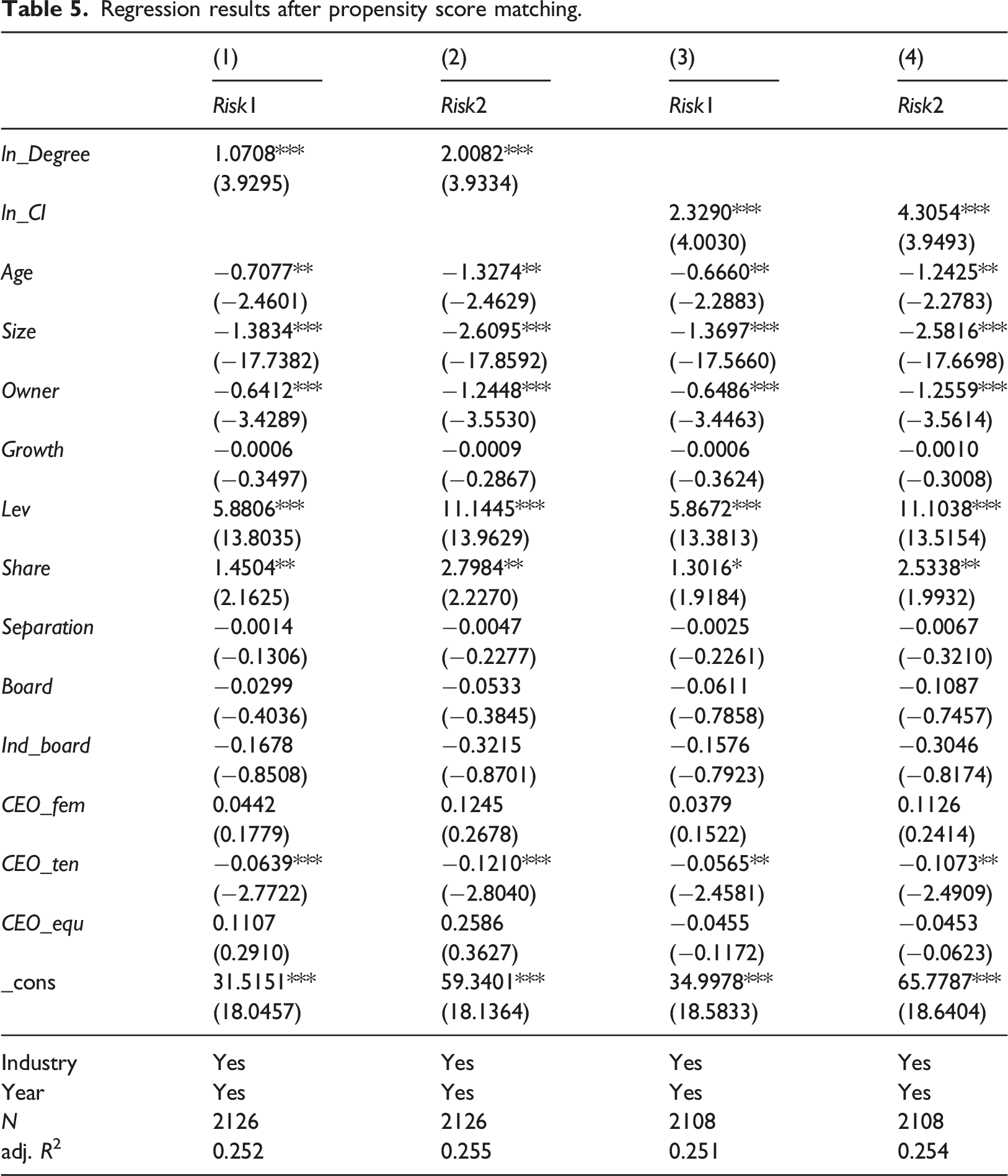

The directors’ networks may be affected by environment and firms’ characteristics. This may result in significant differences between the characteristics of enterprises with the high level of board interlock and those of enterprises with the low level of board interlock. If these characteristics also affect corporate risk-taking, there may be interference factors in the relationship between board interlocks and corporate risk-taking observed by model (1). To solve this problem, the paper used the PSM proposed by Rosenbaum and Rubin (1983) to control and eliminate the sample selectivity error. The steps are as follows. First, the enterprises with high-level interlocking boards are defined as the experimental group, and the enterprises with low-level interlocking boards are defined as the control group

3

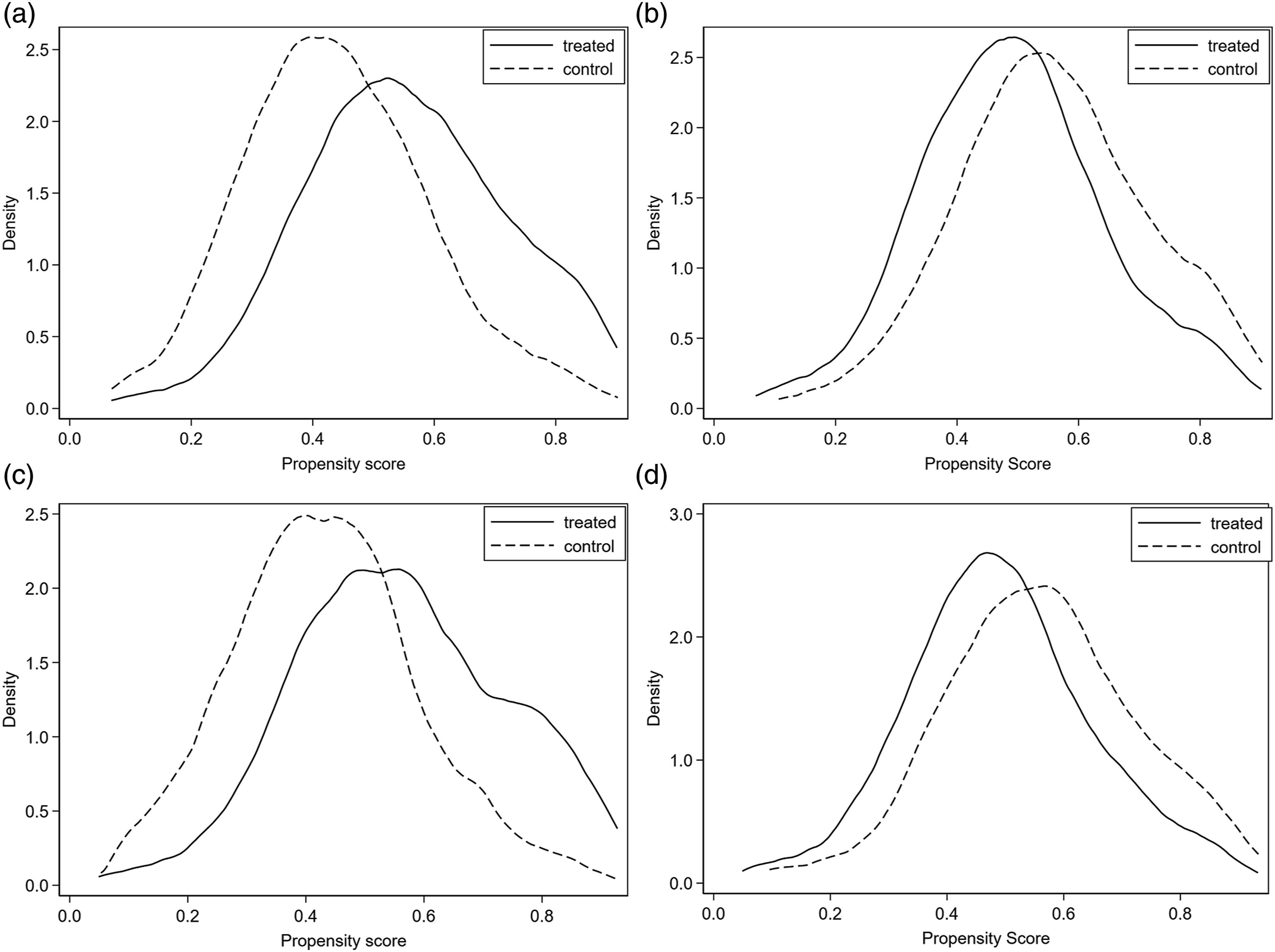

. Second, the tendency score is estimated using Logit model, where the explained variable is whether the enterprise has high-level interlocking directors, and the explanatory variable is enterprise age, enterprise size, type of actual controller, income growth rate, asset-liability ratio, degree of separation of two rights, concentration of equity, number of board of directors, number of independent directors, CEO’s gender, tenure, and equity incentives. Third, this paper uses one-to-one nearest neighbor matching method to match the samples. The advantage of this matching method is that the processing group information can be fully utilized. The kernel density function curves before and after the nearest neighbor tendency score matching between the treatment group and the control group are shown in Figure 1. After the nearest neighbor matching, the probability density distributions of two groups of preserved samples are more similar (Figure 1(b) and (d)). This indicates that the characteristics of the two groups of firms are very close after matching, and the selectivity bias of samples was basically eliminated. Kernel density distribution of the propensity score of treatment group and control group before and after matching. (a) Kernel density of tendency score before matching (Group according to ln_Degree); (b) kernel density of tendency score after matching (Group according to ln_Degree), (c) Kernel density of tendency score before matching (Group according to ln_CI); (d) kernel density of tendency score after matching (Group according to ln_CI).

Regression results after propensity score matching.

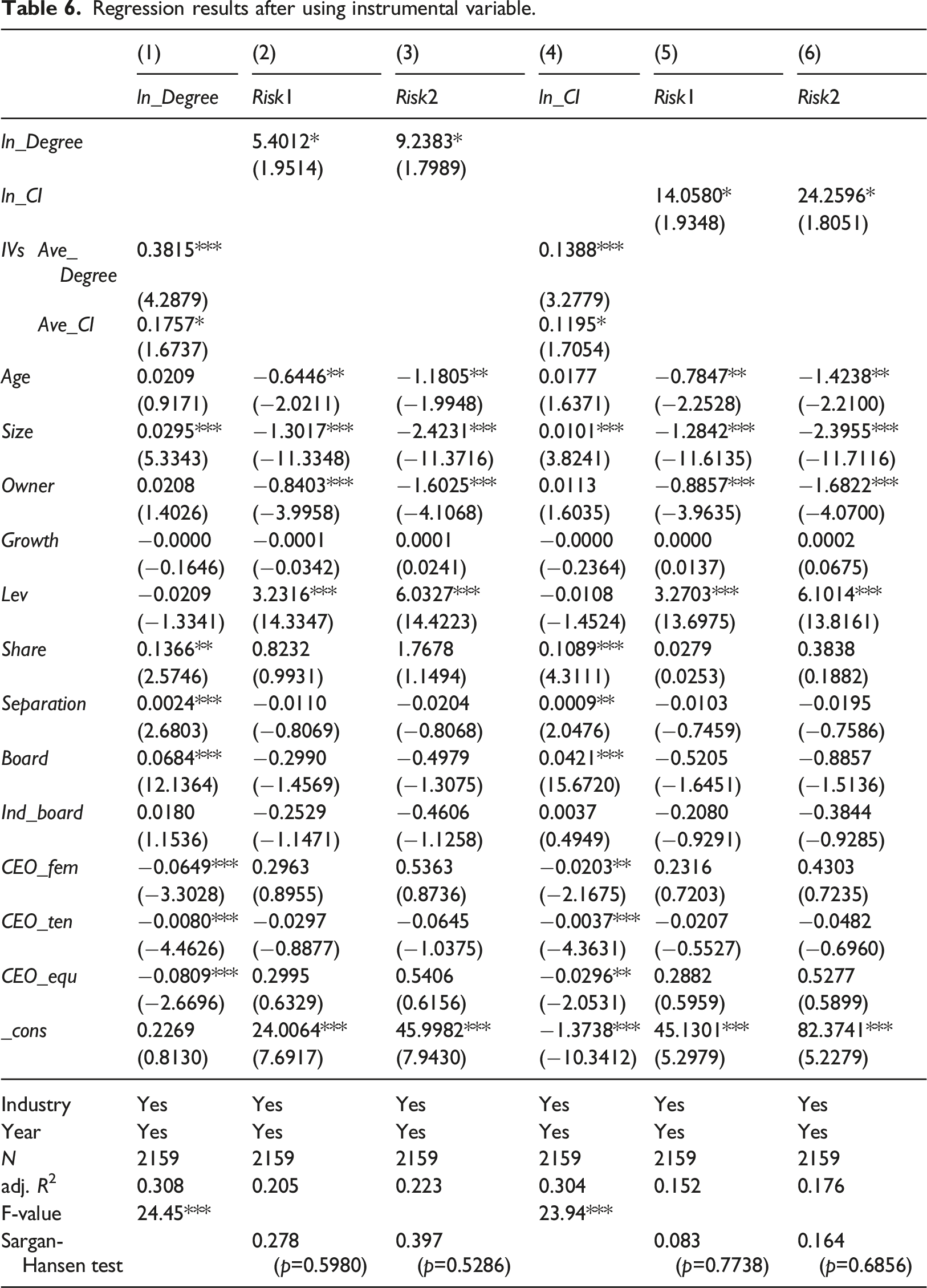

(2) Instrumental variable method

Although this paper tries to control factors that may affect corporate risk-taking, the empirical results may be affected by some unobservable factors. This problem of missing variable will lead to biased estimation coefficients. In addition, a higher level of risk-taking may result in a greater demand for corporate network relationships. To alleviate the endogenous problems caused by missing variables, measurement errors, or reverse causality, this paper further adopted the instrumental variable method for robustness testing. There are two conditions for the selection of instrumental variables. First, it is correlation, that is, instrumental variables need to be related to endogenous variables. Second, it is exogenous, that is, instrumental variables need not to be related to random disturbance terms. Based on the research of Zhang et al. (2016), this paper uses the average annual social network index of the industry as instrumental variables (IVs). The reason is that the annual average of degree centrality and structural hole are determined by the characteristics of board interlocks of each enterprise, and they do not directly affect the venture capital decisions of individual enterprises.

Regression results after using instrumental variable.

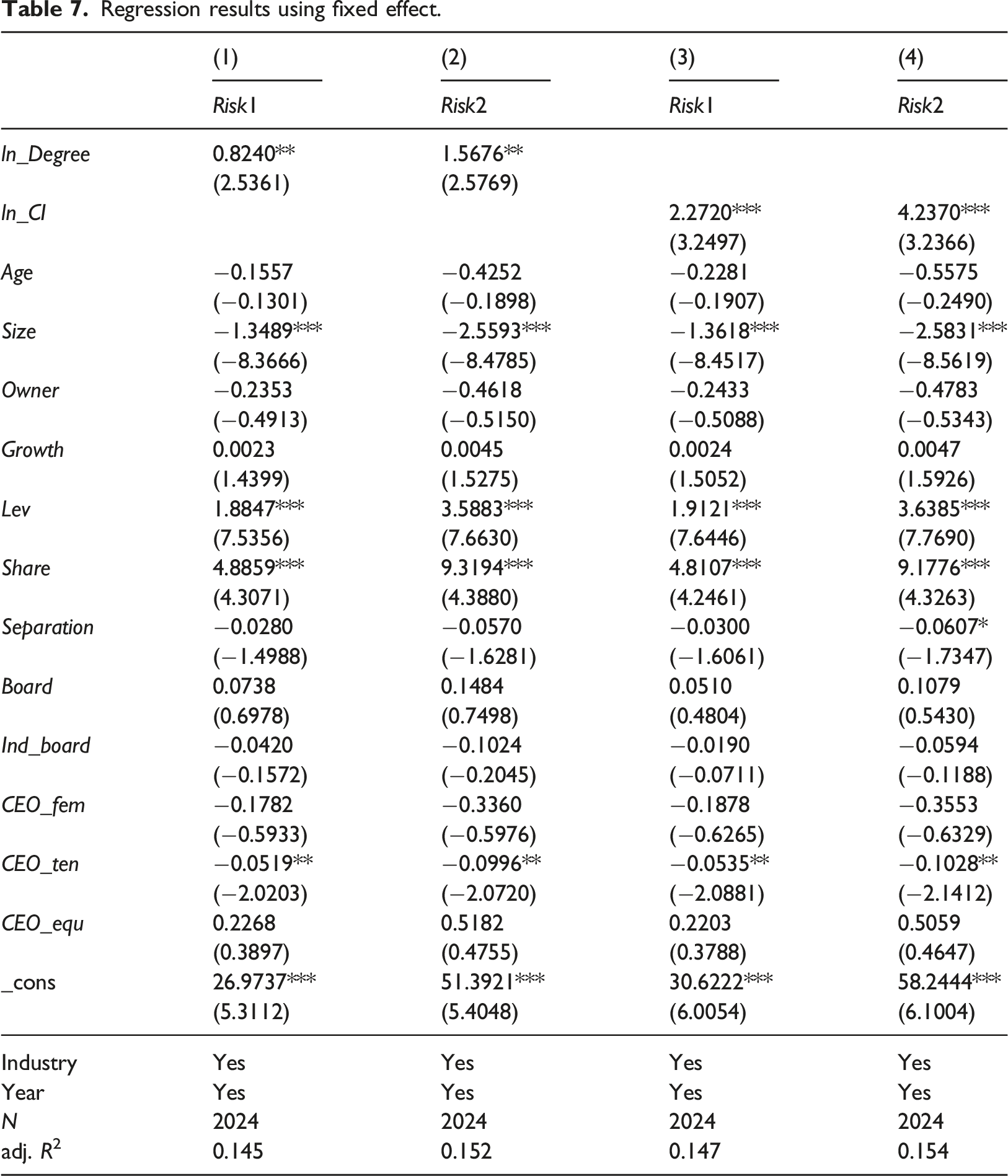

(3) The fixed effect model

Regression results using fixed effect.

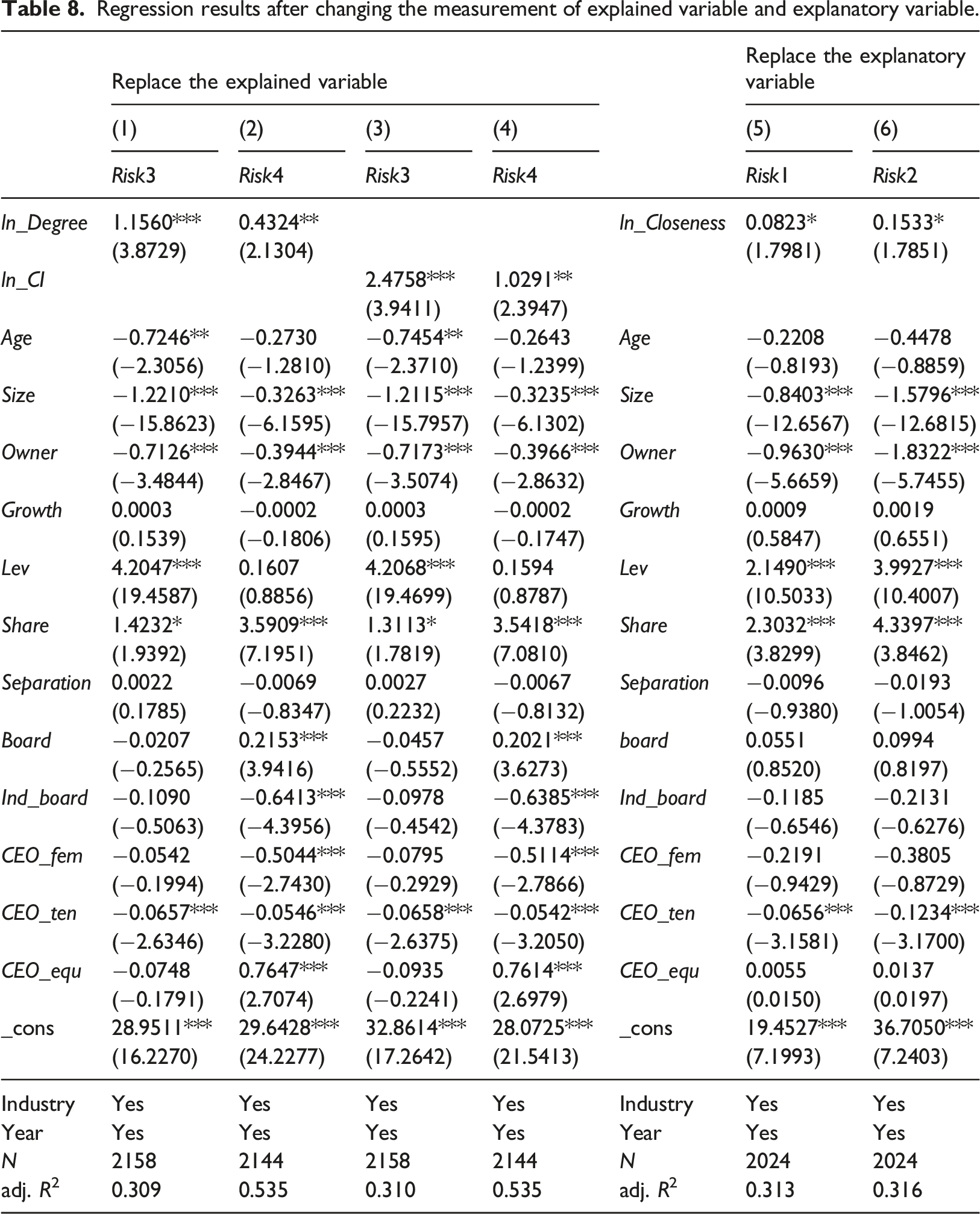

Changing the measurement of explained variable and explanatory variable

Regression results after changing the measurement of explained variable and explanatory variable.

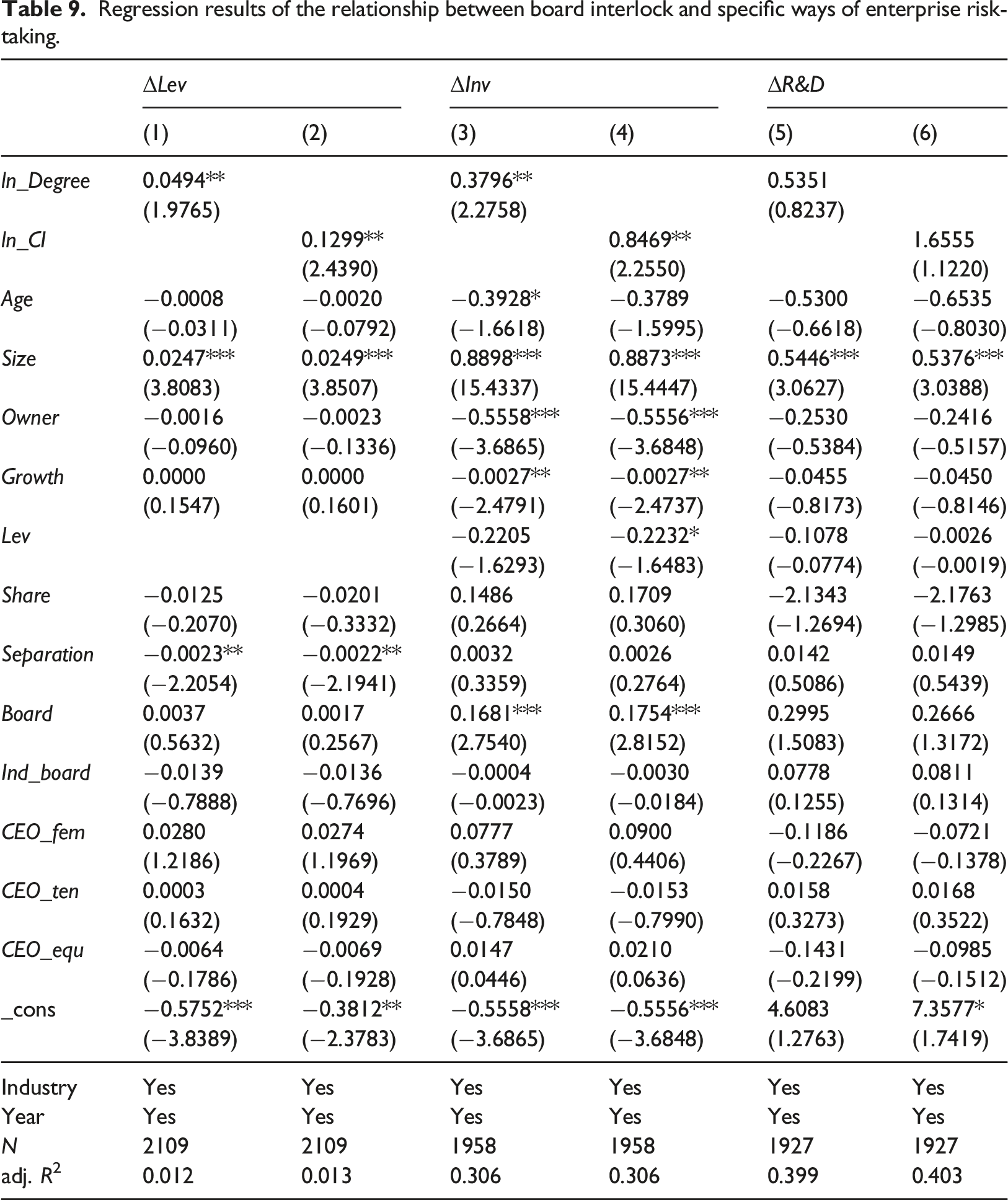

In addition, considering that the volatility of the return on assets and the volatility of stock returns, which measure the risk-taking level of enterprises, are the outcome variables based on performance indicators. This paper further investigated the influence of board interlocks on specific venture capital activities, including debt financing, capital investment and R&D innovation. External financing is risker than internal financing. The lower the debt financing, the more cautious the company is (Hackbarth, 2008). Therefore, high debt indicates that enterprises are more inclined to risk-taking. The capital investment is also a sign of the risk-taking tendency of enterprises. A high level of capital investment indicates that enterprises can carry out a wider range of business activities. In addition, different from the general management activities, enterprise innovation activities have the outstanding characteristics of long cycle, high uncertainty of output, and high adjustment cost (Holmstrom, 1989). Therefore, the higher the investment related to enterprise innovation, the higher the level of enterprise risk-taking. Referring to Hutton et al. (2014) and Zhang et al. (2015), this paper replaced the enterprise risk-taking variables in model (1) with financial leverage (ΔLev), investment level (ΔInv), and R&D intensity (ΔR&D), and examined the influence of interlocking directors on enterprise financing, investment, and innovation, respectively. ΔLev is the change between current asset-liability ratio and previous asset-liability ratio. ΔInv is the change between the current capital expenditure and previous capital expenditure divided by total assets, where the capital expenditure is calculated as all outlays on capital expenditure and acquisitions, less receipts from the sale of property, plant and equipment. ΔR&D is the change between the current R&D expenditure and previous R&D expenditure divided by total assets.

Regression results of the relationship between board interlock and specific ways of enterprise risk-taking.

According to the regression results in Tables 8 and 9, it can be found that whether the risk-taking is measured by outcome variables or by the specific ways, the relevant results all show that interlocking directors can improve the enterprise risk-taking.

Mechanism analysis: information effect or resource effect

Board interlocks and information asymmetry

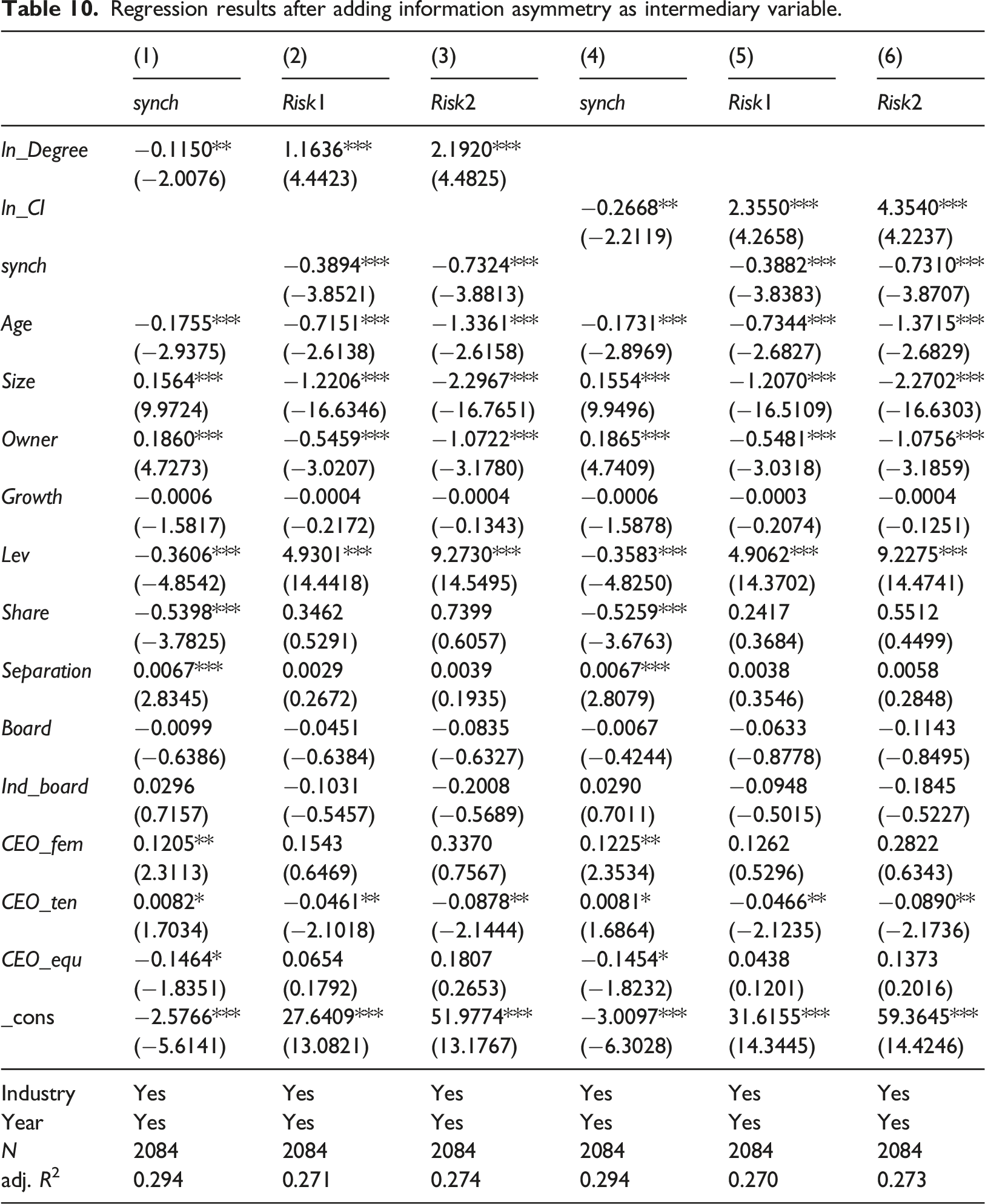

In line with the research of Easley et al. (1996), Morck et al. (2000), and Zhu et al. (2007), this paper adopted the method from the literature of financial market microstructure to capture the degree of information asymmetry about the corporate value in the securities market by using the correlation between changes in corporate stock prices and market average changes (i.e., stock price synchronicity). Theoretically, the basic information of a company affects its stock price, the better the company’s operation, the higher the stock price. However, in the noisy stock market, the opacity of information will lead to the extent that the stock price reflects the information of the company becomes smaller, and the stock price of the company is guided by the market fluctuation. Therefore, stock price synchronization can measure the degree of information integration into stock price of listed companies. The higher the stock price synchronization is, the less the company information is reflected in stock price, and the higher the degree of information asymmetry between the capital supplier and the enterprise. Referring to Jin and Myers (2006), this paper estimated the annual goodness of fit R2 of individual stocks by model (8), and used equation (7) to logarithmic R2, and finally obtains the stock price synchronicity index Synchit.

According to Baron and Kenny (1986), the mediating effect test consists of three steps: I. The explanatory variable significantly affects the explained variable; II. The explanatory variable significantly affects the intermediate variable; III. After controlling the explanatory variable, the intermediate variable significantly affects the explained variable. The step 1 is shown in model (1), the step 2 and step 3 are shown in model (9) and model (10):

Regression results after adding information asymmetry as intermediary variable.

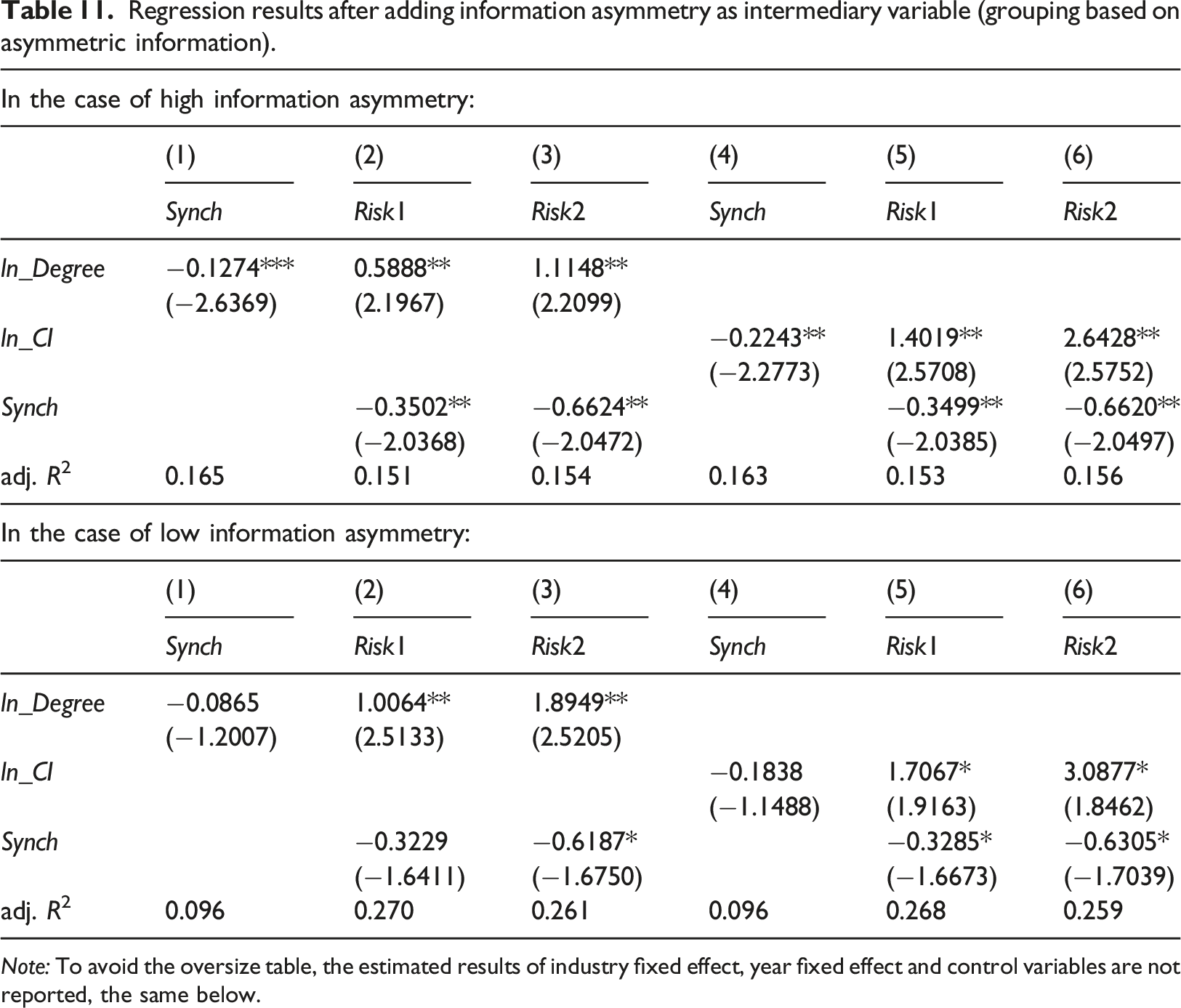

Information effect and resource effect: heterogeneity of information asymmetry

Based on the theoretical analysis, the paper believe that the board interlock will affect corporate risk-taking through information effect and resource effect. And the above empirical results confirm the transmission mechanism of “board interlock–information effect–corporate risk-taking.” Resource effect involves variety resources of enterprise, and it is difficult to measure by indicators or directly tested by intermediary effect. This paper assumes that board interlocks can only influence corporate risk-taking through information effect and resource effect. Therefore, the empirical logic is as follows: if information asymmetry is part of the intermediary of interlocking director to promote enterprise risk-taking, there are resource effect and information effect. If information asymmetry cannot act as an intermediary between the board interlock and corporate risk-taking, only resource effect exists. To explore the existence condition of information effect and resource effect, the paper further divided the degree of information asymmetry into high group and low group by median, and the mediating effect of samples for each group is tested.

Regression results after adding information asymmetry as intermediary variable (grouping based on asymmetric information).

Note: To avoid the oversize table, the estimated results of industry fixed effect, year fixed effect and control variables are not reported, the same below.

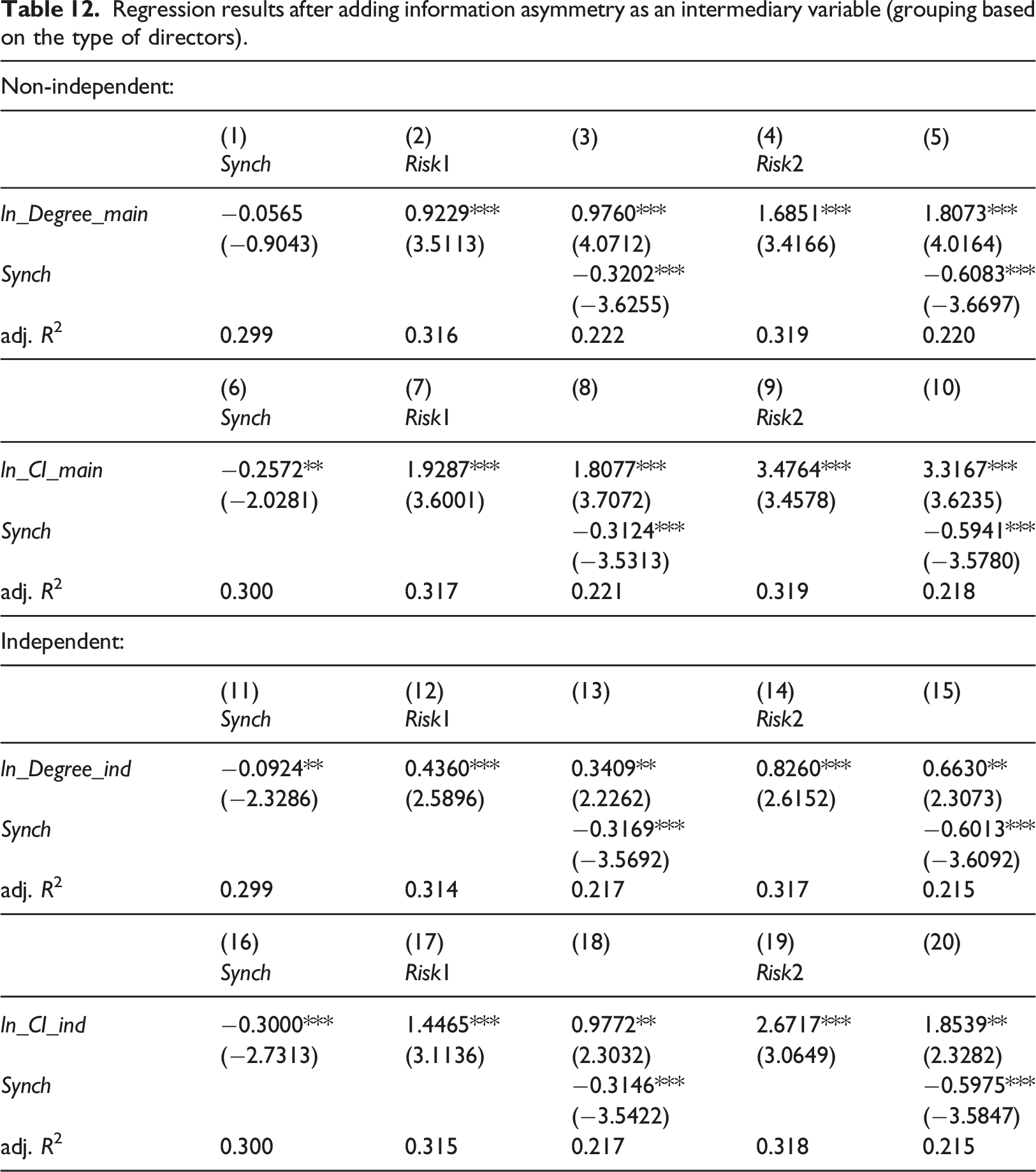

Information effect and resource effect: different types of directors’ interlock 4

Directors of listed companies in China are generally divided into two categories: executive directors and non-executive directors. The executive directors are the directors who participate in the operation and management of company. They are responsible for actively fulfilling the decisions of board, and regarded as the representative of company’s managers. Non-executive directors include related non-executive directors and independent non-executive directors (i.e., independent directors). Although the related non-executive directors are not company’s employees, they have a non-independent relationship with the company. For example, they may be major shareholders of the company, representatives of suppliers and distributors, recently retired senior managers, or relatives and close friends of the chairman or general manager. While, independent non-executive directors do not hold other positions in the company other than directors. There is no relationship between them and the major shareholders of listed company that prevents them from making independent and objective judgments. According to the classification of directors, there are significant differences in the connection relationship between different types of directors and companies. Independent directors are weakly connected to the company management, while executive directors and related non-executive directors (collectively referred to as non-independent directors) have strong connection with company management. To explore the different influences of the non-independent board interlock and independent board interlock on corporate risk-taking, this paper calculated the degree centrality and structure hole according to non-independent directors and independent directors, respectively.

Regression results after adding information asymmetry as an intermediary variable (grouping based on the type of directors).

Discussion and conclusion

This paper takes 2006–2019 listed companies in tourism and related industries in Shanghai and Shenzhen as samples to examine the relationship between the board interlock and corporate risk-taking. In addition, this paper further examined the information effect and resource effect. According to the analysis results, the study finds that there is a significant positive relationship between the board interlock and corporate risk-taking. A possible explanation is that, if a director of a hotel firm also takes roles as director in other strategically related firms (hotel supplies suppliers, hotel interior design, online travel agents, etc.), the director can help the hotel firm to establish a stable relationship with its economic related parties (Song et al., 2020). This can reduce the uncertainty of the business environment and transaction costs, and improve the level of corporate risk-taking. The study also finds that the role of board interlocks in promoting risk-taking is influenced by the external risk sensitivity of industry and the degree of industry competition. For the external risk sensitivity of industry, the “quantity embedding” of interlocking directors has a stronger promoting effect on enterprise risk-taking in the industry with high external risk sensitivity (tourism core industries and real estate industry), while the “quality embedding” of interlocking directors has a stronger promoting effect on enterprise risk-taking in industries with low external risk sensitivity (transportation and retail industry). For the degree of industry competition, the fiercer the industry competition is, the stronger the promotion effect of “quantity” embeddedness and “quality” embeddedness of board interlocks on risk-taking.

By examining the mechanism of board interlock on corporate risk-taking, the study finds that board interlock affects corporate risk-taking through information effect and resource effect. Companies that occupy the central position or core position of corporate network are more likely to send positive signals to the outside capital. Therefore, the high level of board interlock can reduce the information asymmetry between the supply and demand sides of capital. In addition, the board interlock can enhance the enterprise’s ability of obtaining resources to improve the corporate risk-taking. Further analysis shows that the intensity of information effect and resource effect changed with the degree of information asymmetry. When there is a high degree of information asymmetry between the enterprise and the external environment, the board interlock can affect corporate risk-taking through information effect and resource effect. However, when the degree of information asymmetry between the enterprise and the external environment is relatively low, the information effect no longer works, and board interlock mainly improves corporate risk-taking through resource effect. One possible explanation is that when the transparency of corporate information is low, external investors need to obtain information about the future performance of the enterprise from the interlocking directors. However, when the transparency of corporate information is high, external investors can easily search for relevant information of the enterprise. The paper also finds that the non-independent board interlocks have a greater role in improving the corporate risk-taking than the independent board interlocks, and it mainly enhances corporate risk-taking through resource linkage. However, the information effect intensity of independent board interlock is higher than that of non-independent board interlock.

Theoretical contribution

First, from a theoretical perspective, this study contributes to the tourism and hospitality literature pertaining to corporate governance by revealing the positive relationship between board interlocks and corporate risk-taking, supporting the proponents of the resource dependence theory and the collusion theory. Although many hotel and tourism literatures have investigated the factors of corporate risk-taking, they mainly focus on the diversification of the board of directors (Lee and Thong, 2022; Ozdemir et al., 2021), CEO characteristics (Lee and Moon, 2016), CEO overconfidence (Seo and Sharma, 2018), and executive compensation incentives (Seo and Sharma, 2013). There are also some studies on chain directors, but these studies mainly examine the impact of board interlocks on the financial performance of tourism enterprises (Ooi et al., 2015; Song et al., 2021; Yousaf et al., 2021). In the tourism industry, this paper shows that the positive impact of board interlocks on corporate risk-taking. This indicates that enterprise social network is of great significance to the development of tourism enterprises. It is helpful to understand the informal institutional factors that influence the risk-taking of tourism enterprises.

Second, the results show that the impact of board interlocks on the risks of tourism companies depends on the degree of industry competition and the industry sensitivity to external environment, contributing to the corporate governance literature. The operation of the business has higher uncertainty with the intensification of industry competition. The results show that interlocking directors are an important factor to reduce this uncertainty. This indicates that making full use of the board interlocks may be the key for tourism firms to gain competitive advantage when they expand business in highly competitive market. In addition, the study classifies the sample enterprises according to the external risk sensitivity of industry, obtained more accurate results, and expanded the theory of structural embedding. In the theory of structural embedding, there are two different views on the significance of network structure to enterprises. Social capital theory (Coleman, 1984) holds that tight network can promote the trust and cooperation among members, thereby facilitating the formation of corporate social capital. However, in structural hole theory (Burt, 1992), loose network embedding is helpful for embedded enterprises to obtain non-redundant information, and enterprises in structural holes can gain competitive advantage. This study indicates that these two views are not contradictory. And different network structures are valuable for specific industries. For example, tourism core industries (tourism, catering, and hotel industries) and real estate industry are easily influenced by external environment, their board interlocks need to play a role of “quantity” embeddedness, establishing a relatively tight network structure, and contacting with as many enterprises as possible to obtain a large amount of information and resources. For industries that are not easily affected by external environmental factors, such as transportation and retail industries, it is necessary for their board interlocks to play a role of “quality” embeddedness, establishing a relatively loose network structure, and occupying the position of structural holes to obtain heterogeneous information and resources. However, no matter what kind of network structure it is. Only if the enterprise is in the dominant position in the network can it guarantee that the enterprise has the ability to resist risks.

Finally, this paper reveals the mechanism of board interlocks on corporate risk-taking. This not only provides empirical evidence for Burt (1992), but also provides theoretical reference for tourism and related enterprises to build director networks. Larcker et al. (2013) describes the role of the board interlock as “information effect” and “resource effect,” while Chuluun et al. (2017) only considers the “information effect” of board interlock. This paper responds to their research by empirical test, and holds that the board interlock can exert both “information effect” and “resource effect.” In addition, this study proves that when the degree of information asymmetry between the enterprise and the external environment is low, the information effect no longer plays a role. This clarified the existence conditions of “information effect” and “resource effect.” Further, this paper divided board interlock network into strong relationship network (non-independent interlock directors) and weak relationship network (independent interlock directors). The results show that strong relationship mainly exerted resource effect, while weak relationship mainly exerted information effect. This is basically consistent with the weak connection advantage theory proposed by Granovetter (1973). Compared with non-independent directors, there is a weak connection between independent directors and the management of the company. This weak connection is more likely to play the role of “information bridge” (Cai et al., 2010). And it is more likely to transfer important information in certain groups to other individuals who do not belong to these groups.

Management implications

First, it is suggested that listed companies in tourism and related industries increase the level of board interlocks. Facing the complicated and changeable business environment, it is very important for enterprise to improve the risk-taking ability, especially with the acceleration of China’s market-oriented process and the enhancement of information and resource mobility. If an enterprise can occupy a central network position or a rich structural hole position, it will undoubtedly obtain information, resources, and control advantages to enhance the corporate risk-taking. However, the test results of the control variable in this paper show that the board size is negatively correlated with corporate risk-taking, just like Song et al. (2021). Therefore, tourism enterprises should increase the level of board interlocks while keeping the board size small, so as to give full play to the function of board interlocks. Second, the effectiveness of interlocking directors varies between different industries. For industries that are vulnerable to external risks such as tourism, hotels, restaurants and real estate, enterprises should improve the level of board interlocks’ “quantity” embeddedness, that is, establishing more contacts with other companies to obtain more information and resources. For the transportation and retail industries, enterprises should increase the level of board interlocks’ “quality” embeddedness, that is, occupying the structural hole position in interlocking directors’ network to obtain heterogeneous information and resources. Third, with the increasing industry competition, tourism companies should improve the level of interlocking directors to gain more information and resources, thereby resisting external risks. For example, when the homogenization is increasing in tourism products and services, tourism companies can hire directors who work in the information technology industry to help them innovate their products and improve their competitive advantages. Finally, enterprises should adjust their strategies according to the degree of information asymmetry. For example, for start-ups, the information transparency is generally lower than that of mature enterprises. Therefore, the company can increase the level of independent board interlock to build information connections with external environment. Enterprises can also adjust board interlocks according to corporate needs. For example, when a travel company needs extensive resource support, it can improve the level of non-independent board interlock. When a travel company needs to communicate information with the external environment, it can increase the level of independent board interlock.

Limitations and future prospects

This paper also has some shortcomings, which need to be considered in future research. First, the research only pays attention to board interlock, ignoring the existence of other types of relationships. The existing management relationship network of company also includes alumni relationship, hometown relationship, club member relationship, and other community member relationships. Future research can consider the impact of different types of relationship network on corporate risk-taking. Second, this study proves that the external risk sensitivity of industry and the degree of industry competition can affect the role of board interlocks in promoting enterprise risk-taking. Other possible adjustment variables should be introduced in future research, such as the degree of marketization, senior executives’ risk preferences, corporate social responsibility, etc. Third, the samples used in this paper are the data from tourism and related industry companies listed on the Shanghai and Shenzhen main board. Therefore, there may be general problems when applying the results to other countries and industry backgrounds. In the future research, it is suggested to add the small and medium-sized board and the new third board listed companies, and to examine the relationship between the board interlock and corporate risk-taking under the background of other countries. This can improve the external effectiveness of this relationship. Fourth, this paper studied linear influence of interlocking directors on enterprise risk-taking. However, the network embedding may have a nonlinear influence on enterprise risk-taking with the increase of interlocking directors’ network density. Future research can investigate the linear and nonlinear relationship between network embedding and enterprise risk-taking.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Social Science of China (No. 19ZD25).

Notes

Author biographies

Chen Hao is a PhD candidate in the School of Business at East China Normal University. Her research interests include corporate growth strategy, tourism economics, service economy, as well as tourism planning and development.

Xuegang Feng (PhD) is a professor at East China Normal University, China. He is the dean of the School of Business and the director of the Center for Tourism Planning and Development at ECNU. His research interests include tourism planning and development, tourism economics, hospitality management, and service management.

Dandan Wu is a PhD candidate in the School of Business at East China Normal University. Her research interests include digital economy and tourism industry development, as well as tourism planning and management.

Xiaodong Guo (PhD) is a professor in the College of Earth and Environmental Sciences at Lanzhou University, China. His research interests include tourism planning and development, tourism economics, and rural tourism.