Abstract

How do elections affect the government’s attempt to raise taxes? Previous studies have focused on the effect of elections on the timing of tax increases, arguing that the government is less likely to decide to raise taxes as the election approaches. However, they lack the micro-foundations to explain how elections discourage the government from implementing tax increases. To address this shortcoming, the current study focuses on individual ruling party politicians and shows that the competitiveness of elections in their districts gives them an incentive to oppose the government’s attempt to raise taxes, using data derived from the House of Representatives elections in Japan. This implies that the electoral prospects of individual ruling party politicians are behind the government’s decision to delay the tax increase.

Introduction

The stagnation of economic growth in many advanced countries and the expansion of financial globalization have made it increasingly difficult for governments to rely on traditional sources of welfare spending, such as income and corporate taxes. As a result, consumption taxes have become an important means of financing welfare spending since the 1970s (Aaron, 1981; James, 2015; Kato, 2003; OECD, 2001; OECD, 2014; Timmons, 2010). However, tax increases, including consumption taxes, are generally considered unpopular with voters (Park et al., 2017). Nevertheless, there are times when ruling parties have to implement tax increases even under such circumstances (Elmelund-Præstekær and Emmenegger, 2013).

In this situation, how do elections affect governments’ attempts to raise taxes? A substantial body of literature has primarily focused on the impact of election timing on government decision-making, arguing that governments tend to schedule a tax increase after elections (e.g., Berry and Berry, 1994; Chang et al., 2021; Foremny and Riedel, 2014; Persson and Tabellini, 2003; Rogoff and Sibert, 1988; Tillman and Park, 2009).

However, these studies lack the micro-foundations to explain how elections discourage the government from implementing tax increases in the sense that they treat the government as a coherent single entity with its own preferences and strategies, although in reality, the government consists of individual politicians of the ruling party.

To address this shortcoming, the current study focuses on individual ruling party politicians and examines how the competitiveness of elections in their districts gives them an incentive to oppose the government’s attempt to raise taxes. Faced with an unpopular government proposal to raise taxes, ruling party candidates must balance two conflicting goals: maximizing votes and remaining loyal to the party leadership. Such conflicting goals lead the candidates to adopt policy positions closer to the median voter in order to maximize their votes in competitive elections, while in non-competitive elections, leading them to adopt positions further from the median voter in order to remain loyal to the party leadership. Therefore, we hypothesize that ruling party candidates better represent the median voter in more competitive elections and that such effect of electoral competitiveness is more pronounced as leading opponents adopt positions closer to the median voter.

We test these hypotheses by analyzing panel data of the Liberal Democratic Party (LDP) candidates from the three House of Representatives elections in 2012, 2014, and 2017. Japan serves as a best-case study because the government attempted to raise the consumption tax during this period and the LDP is known for its strong party discipline. This study contributes to the literature by suggesting that the electoral prospects of individual ruling party politicians are behind the government’s decision to delay the tax increase.

Research question

This study examines how elections affect governments’ attempts to raise taxes, given that tax increases are generally unpopular with citizens. A substantial body of literature has focused primarily on the impact of the timing of elections on government decision making, arguing that governments tend to plan tax increases after elections. The ruling party that implements a pre-election tax increase tends to lose votes in subsequent elections (Tillman and Park, 2009). Given this pessimistic outlook on the electoral consequences of a tax increase, politicians are most likely to enact tax increases when the next election is far away and the electoral risk associated with implementing tax increases is minimized (Berry and Berry, 1994; Chang et al., 2021). In other words, politicians tend to avoid tax increases, especially close to elections. Indeed, Foremny and Riedel (2014) find that the growth rate of local business tax rates is lower in pre-election and election years. In addition, Persson and Tabellini (2003) suggest that pre-election tax cuts are common in democratic countries, while painful fiscal adjustments are made after elections. Rogoff and Sibert (1988) argue that politicians may cut taxes before elections in order to appear competent to citizens.

Consistent with the implications of previous studies on electoral competition and government decisions on the timing of tax increases, Finnegan (2023) finds that higher levels of electoral competition are associated with government decisions to reduce gas tax rates in twenty high-income democracies between 1988 and 2013.

However, by treating the government as a coherent single entity with its own preferences and strategies, these studies have paid little attention to the micro-foundations of how elections lead the government to refrain from implementing tax increases, while in reality the government is composed of individual politicians from the ruling party who have electoral incentives to influence the government’s decisions. For example, the consumption tax increase in Japan was delayed at the request of the members of the LDP, including 42 lawmakers who gathered in October 2014 to ask Prime Minister Shinzo Abe to delay the consumption tax increase. The Asahi Shimbun, one of Japan’s leading newspapers, documented: 1 “Some of the younger lawmakers, whose electoral base is weak, are aware that they cannot ignore public opinion, which is wary of the tax increase.” In response, Prime Minister Abe announced that he would suspend his plan to raise the consumption tax to 10% for a year and a half.

Theory and hypothesis

To address the shortcoming, we focus on individual ruling party politicians and examine how the competitiveness of elections in their districts gives them an incentive to oppose the government’s attempt to raise taxes. More specifically, we argue that the more competitive elections are, the more likely it is that candidates of the ruling party will represent the median voter on the issue of a tax increase by deviating from the party leadership.

Candidates in elections pursue two potentially conflicting goals (Fujimura, 2007): maximizing votes (Mayhew, 1974) and remaining loyal to the party leadership (Fujimura 2009). They must balance these goals when deciding what positions to take on issues. To maximize votes, candidates align their positions with the median voter (Downs, 1957; Mayhew, 1974), but doing so may conflict with the campaign promises of the party leadership, which can lead to penalties such as withdrawal of party endorsement and reduced opportunities for promotion. Thus, candidates’ positions on unpopular issues are a function of the estimated costs and benefits of aligning with the median voter by deviating from the party leadership. Indeed, Kam (2009) suggests that legislators may rebel against the party leadership for reelection in the expectation of a boost in popularity.

Accordingly, we posit that in non-competitive elections, ruling party candidates are more likely to diverge from the median voter by remaining loyal to the party leadership. Conversely, in competitive elections, they are more likely to align with the median voter by deviating from the party leadership. Furthermore, the Downsian model of electoral competition posits that the closer the positions of opposing candidates align with those of the median voter, the more likely it is that ruling party candidates will represent the median voter on the issue of a tax increase, as otherwise, they risk losing.

The theoretical predictions lead to the hypotheses to be tested by exploiting the case of three Japanese lower elections of 2012, 2014, and 2017. Japan provides a unique opportunity to test the hypotheses for three reasons. First, the LDP, which remained in power during this period, is known for its strong party discipline (Umeda, 2019). LDP legislators are known to rarely deviate from the party line when voting in the Diet plenary session, as they are fearful of losing the electoral endorsement of the party leadership (Uchiyama, 2023).

Second, the consumption tax increase was a consistent point of contention in these House of Representatives elections, as Japan experienced two consumption tax increases during this period. The Democratic Party of Japan (DPJ) pledged not to raise the consumption tax during its term in office in its manifesto for the 2009 general election, which it won by a landslide. However, in the wake of the Greek financial crisis, the DPJ government changed its mind and in June 2012 signed an agreement with the former ruling parties, the LDP and the Komei Party (KP), to raise the tax rate from 5 to 10% in two stages.

After defeating the DPJ in a general election in December 2012, Prime Minister Shinzo Abe of the LDP implemented the planned first phase of the tax increase to 8% in April 2014. Although he was supposed to raise the rate to 10% in the second phase scheduled for October 2015, Abe announced in November 2014 that he would delay the increase until April 2017, citing the greater-than-expected negative impact of the first consumption tax increase on the country’s fragile economy.

With the opposition still weak and voters satisfied with the postponement of the tax increase, the LDP won another big victory in the December 2014 general election. Abe was expected to raise the consumption tax as planned in April 2017, but he decided in June 2016 to postpone the tax increase again until October 2019, with the next general election due in the foreseeable future. After securing a majority in the October 2017 election, Abe finally raised the consumption tax rate to 10% in October 2019.

This situation ensures the theoretical assumption that politicians are faced with a difficult decision of how to position themselves on unpopular tax increases in their election campaigns in order to pursue two conflicting goals: maximizing votes and remaining loyal to the party leadership. Kato (1997) highlighted the similar dilemma faced by novice LDP politicians in the 1980s. Drawing on the literature arguing that lawmakers seek not only to ensure their reelection but also to increase their influence in the legislature and within the party (Cain et al., 1987; Fenno 1977), Kato (1997) contrasted young LDP lawmakers who opposed the introduction of consumption tax because of their weak electoral base with veteran LDP lawmakers who supported the introduction of consumption tax to enhance their influence within the party. Such conflicts between novice and veteran LDP politicians with different motivations were severe enough to lead to the split within the LDP in 1993.

Finally, the three Japanese House of Representatives elections in the 2010s provide a unique opportunity to test the hypotheses, as data are available on candidates’ attitudes toward the issue of a consumption tax increase during this period.

The UTokyo-Asahi Survey (UTAS) 2 asked candidates the same questions on the tax increase in all three elections. The response rates are high, with almost all of the ruling party candidates responding. This is because the coverage of the responses on the Asahi Shimbun, one of the most representative national newspapers, incentivizes the candidates to participate in the survey (Takenaka, 2010).

The following are the hypotheses to be tested:

LDP candidates tend to align their positions on the consumption tax issue more closely with the position of the median voter as electoral competitiveness increases.

LDP candidates tend to align their positions on the consumption tax issue more closely with the position of the median voter as the policy positions of the most popular opposition party candidates are closer to the position of the median voter.

We also predict that as the election becomes more competitive, ruling party candidates will feel more pressure to move toward the median voter if they see their opponents as representing the median voter, because otherwise their opponents will attract more votes that are decisive enough for them to lose the election. Therefore, we hypothesize the interaction effect of electoral competitiveness and rival candidates’ issue positions: 3

The effect of electoral competitiveness is conditioned by the positions of the most popular opposition party candidates; namely, the effect of electoral competitiveness is stronger the closer the policy positions of the most popular opposition party candidates are to the position of the median voter.

Research design

The Japanese Diet has two chambers: the House of Representatives and the House of Councillors. The House of Representatives, which we examine in this study, uses a mixed-member majoritarian electoral system. The electoral system combines two electoral tiers: single-member majoritarian and proportional representation (PR). Under the current House of Representatives electoral system, 289 members are elected from the majoritarian tier with single-member districts (SMDs) and 176 members from the closed-list PR tier with 11 regional districts. An electorate votes for a candidate in SMDs and for a party in PR districts. SMD candidates may also be on a PR list. A candidate with a plurality of the votes wins an SMD seat, but some SMD losers on the PR list may win PR seats, depending on the ratio of their votes to the SMD winners. Under this electoral system, PR votes determine which SMD losers win PR seats, but they have no effect on who is elected from the SMDs. The SMDs had an average of 4.31 candidates in 2012, 3.25 in 2014, and 3.23 in 2017, although not all of them compete substantively.

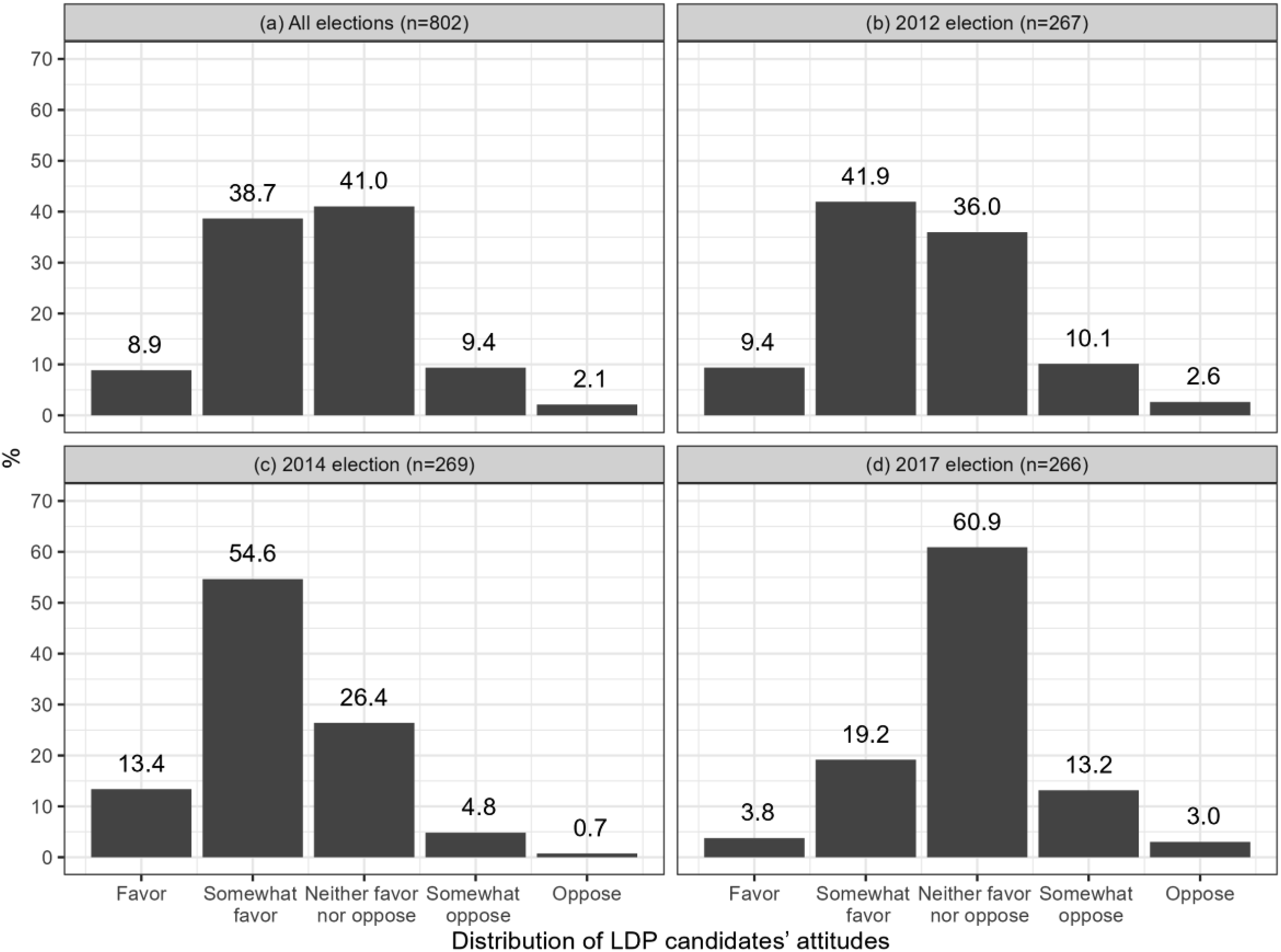

Figure 1 shows the distribution of LDP candidates’ attitudes toward the consumption tax increase in the House of Representatives elections of 2012, 2014, and 2017, using the UTAS data. The questions asked whether the candidates favor or oppose the tax increase to 10% in a long run on a five-point Likert scale.

4

Distribution of LDP candidates’ attitudes toward the consumption tax increase.

Figure 1(a) pooled all LDP candidates who ran in the three elections and shows that their positions on the tax increase are not very coherent, with 47.6% in favor or somewhat in favor, 41.1% neither in favor nor opposed, and 11.4% opposed or somewhat opposed, even though the LDP’s manifesto had consistently advocated raising the consumption tax to 10% in these three elections. 5 This suggests that LDP candidates strategically took positions on the tax increase, weighing the risk of losing the confidence of the party leadership and their electoral competitiveness.

It is also worth noting that there is a significant difference in the distribution of their attitudes across elections. Panels (b), (c), and (d) of Figure 1 show how the LDP candidates who ran in the respective elections expressed their positions on the tax increase, suggesting that in the 2012 and 2014 elections, the LDP candidates’ attitudes are relatively cohesive, centered on the party leadership advocating for the tax increase, while the substantial proportion of candidates moderated their positions toward the opposition side in 2017. Overall, there is ample room to explain the variation in LDP candidates’ attitudes toward tax increases even under strong party discipline.

The dependent variable is the quadratic distance between LDP candidates’ and median voters’ positions on consumption tax increase in the SMDs. Because the UTAS survey data do not include respondents from all SMDs, the median voters’ positions are measured by applying the method proposed by Kim and Fording (1998, 2003) to the Japanese context. 6

Kim and Fording (1998) argue that by assuming a proximity model in spatial voting, in which voters cast ballot for the party with its position closest to their own preferences, election results can be treated as in a poll, i.e., those who vote for a party prefer the party’s position on an ideological spectrum. The ideological positions of the parties are estimated using data from the Comparative Manifesto Project, a series of expert surveys conducted by Laver and Budge (1992), and are aligned accordingly on the right-left (RILE) scale. Since the parties’ vote shares are assumed to represent the percentage of voters whose preferences are closest to the parties’ positions, the median voter position is estimated by calculating the 50 percentiles on the scale.

The methodological challenge is to estimate the median voter position on the tax increase issue, rather than the ideological scale, in each SMD, rather than a country. To address this problem, we use the method developed by Shibutani (2023) that substitutes the Comparative Manifesto Project data by the UTAS candidate survey data. The first step is to calculate the mean of responses of each party’s candidates to the question about their attitude toward raising taxes by 10% on a five-point Likert scale from “Oppose (1)” to “Favor (5)” using UTAS data. The second step is to align the parties according to their means on the tax increase issue scale. Finally, assuming that the parties’ PR vote shares in each SMD represent the percentage of voters whose preferences are closest to the parties’ positions on the tax increase issue, the median voter positions in the SMDs are estimated by calculating the 50 percentiles.

More formally, suppose that the policy positions of N parties are arranged in ascending order as

On the other hand, in the above equation, there may be two policy positions of a political party that satisfy

Under this condition, if

Thus, the quadratic distance between LDP candidates’ and median voters’ positions on consumption tax increase is measured by

The independent variable for Hypothesis 1 is electoral competitiveness, measured by the vote share of LDP candidates (Taniguchi 2020). This absolute measure of the electoral competence of LDP candidates allows us to assess the extent to which the LDP candidate perceived the election as competitive, regardless of the number of opposition candidates. We multiply the relative vote share of LDP candidates by −1 to ensure that a higher value is associated with more competitive elections from the perspective of LDP candidates. 7

A possible problem with this variable is that it is measured retrospectively by election results, i.e., LDP candidates did not know their resulting vote share when they responded to the tax increase question on the UTAS. This may lead to reverse causality in the sense that their position on the tax increase question affects their vote share. However, our measure of electoral competitiveness is still reasonable because of the generally strong association between pre-election media coverage and election outcomes (Lewis-Beck and Stegmaier 2014; Traugott 2014), suggesting that LDP candidates’ perceptions of electoral competitiveness are highly correlated with their vote share. Indeed, there are some notable studies that use the same measure of electoral competitiveness 8 (e.g., Powell 1982).

The independent variable for Hypothesis 2 is the quadratic distance between the most popular opposition party candidates’ and median voters’ positions on consumption tax increase in the SMDs. The most popular opposition party candidates are defined as the opposition party candidates with the highest vote share in the respective SMDs. Finally, to test Hypothesis 3, we run a regression with the interaction term between the proximities of LDP candidates and the most popular opposition candidates to the median voter, assuming that the latter moderates the effect of the former.

We use the following variables as controls. A cabinet member dummy 9 is included because the duties of cabinet members may make candidates’ positions more consistent with the party’s manifesto. It is coded 1 if a candidate holds cabinet positions as a minister, vice minister, or parliamentary secretary, and 0 otherwise. Similarly, a party executive dummy is coded 1 if a candidate holds the LDP internal positions, including President, Vice President, Secretary-General, General Affairs Committee Chairman, Policy Research Council Chairman, Election Strategy Committee Chairman, Diet Affairs Committee Chairman, Election Strategy Committee Deputy Chairman, and Special Advisor to the President.

Population density per 1000 and the percentage of workers in the tertiary sector 10 are added as measures of urbanization to partially control for differences across electoral districts, as urban areas may have more competitive elections and more citizens concerned about the consumption tax increase.

A conservative opposition party candidate dummy is coded 1 if the most popular opposition party candidate is from one of the conservative opposition parties, 11 and 0 otherwise. This dummy variable is included because conservative opposition party candidates are more likely to compete with the LDP candidate for similar voter bases and to share policy positions. In addition, previous studies (e.g., Achen, 1978; Fiorina, 1974; Wittman, 1983) have pointed that policy attitudes depend on electoral terms, so we added the number of terms of the LDP candidates and the number of terms of the most popular opposition party candidates to account for the strength of their incumbency advantage. These variables take the form of the natural logarithm of the number of terms plus one, because the marginal effect of the incumbency advantage diminishes as the number of terms increases.

The SMD-only candidate dummy is coded 1 if the LDP candidate ran only from an SMD and 0 if the LDP candidate was also listed on the PR, as Japan’s parallel mixed-member system allows an SMD loser to be elected from the PR if listed. The redistricting dummy 12 is coded 1 if the district boundaries changed from the previous election, and 0 otherwise.

The loser dummy is coded 1 if, in the previous election, the LDP candidate not listed on the PR was defeated in the SMD or the LDP candidate listed on the PR was not elected by either the SMD or the PR, and 0 otherwise. The “zombie” candidate dummy (Pekkanen et al., 2006) is coded 1 if, in the previous election, the LDP candidate listed on the PR lost in the SMD but was elected by the PR, and 0 otherwise. Together, the resulting reference category is the SMD winner. Electoral outcomes in the previous election may influence candidates’ positions in the current election in the sense that previous electoral defeats lead candidates to shift their policy positions in the direction of the median voter in the subsequent election (Fowler 2005), while victories strengthen their own policy ideology, bringing them closer to the preferences of the median voter in competitive races with minimal changes.

The descriptive statistics.

Results

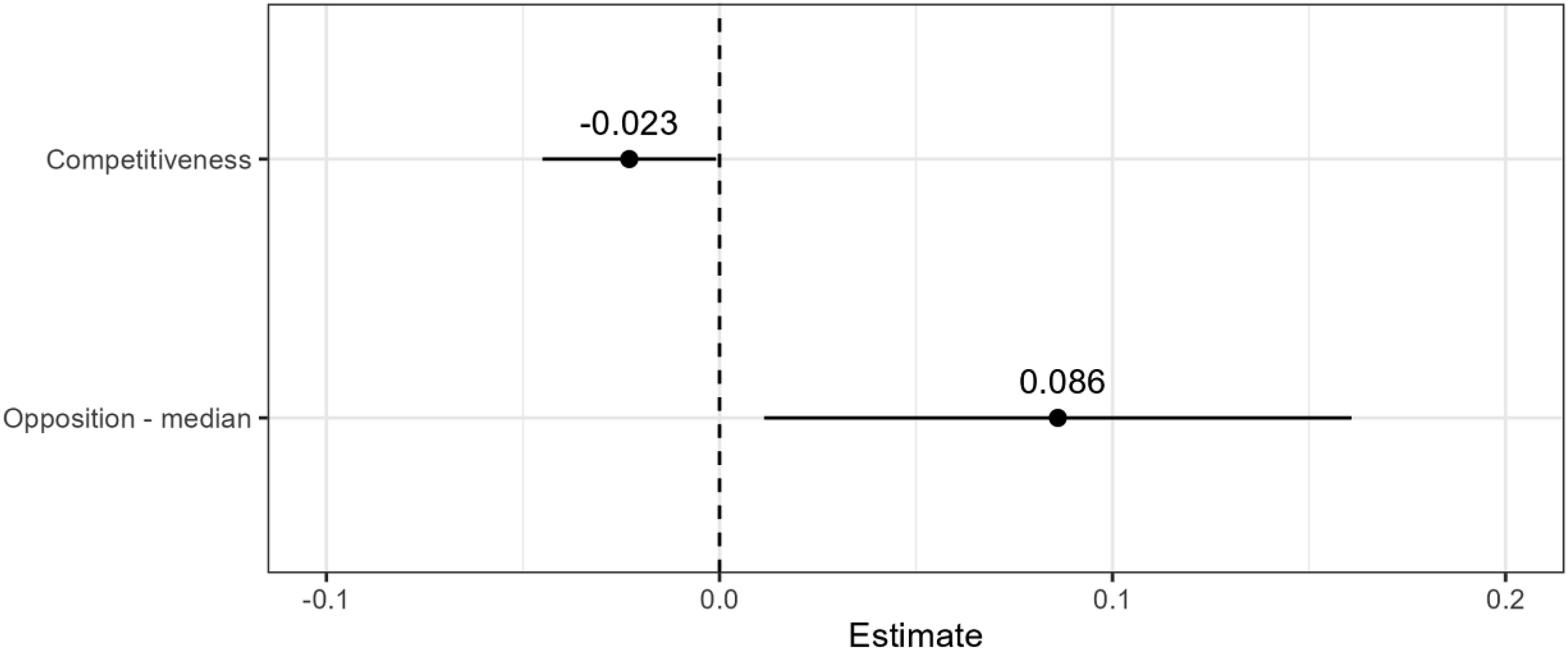

Figure 2 presents the estimated coefficients of each independent variable on [LDP-median] shown as dots, along with the 95% confidence intervals shown as horizontal lines (see Model 1 in Table B1 in Appendix B for the full results). According to this figure, we find supportive evidence for Hypothesis 1 that the estimated effect of the [Competitiveness] on [LDP-median] is - 0.023, which is significantly negative at the 5% level. This implies that [LDP-median] decreases as the election becomes more competitive. To provide a more substantive interpretation, as shown in Table 1, the difference between the minimum and maximum values of [Competitiveness] is 59.939. Thus, due to the variation in electoral competitiveness, the LDP candidate and the median voter are at most 0.023 × 59.939 = 1.379 points close to each other on the issue dimension of raising the consumption tax. The results of ordinary least squares (OLS) regressions.

As for Hypotheses 2, we also find supportive evidence that the estimated effect of the [Opposition - median] on [LDP-median] is +0.086, which is significantly positive at the 5% level. This implies that [LDP-median] decreases as the position of the most popular opposition party candidate becomes closer to the median voter’s position. To provide a more substantive interpretation, as shows in Table 1, the difference between the minimum and maximum values of [Opposition-median] is 6.006. Thus, due to the variation in [Opposition-median], the LDP candidate and the median voter are at most 0.086 × 6.006 = 0.517 points close to each other on the issue dimension of raising the consumption tax.

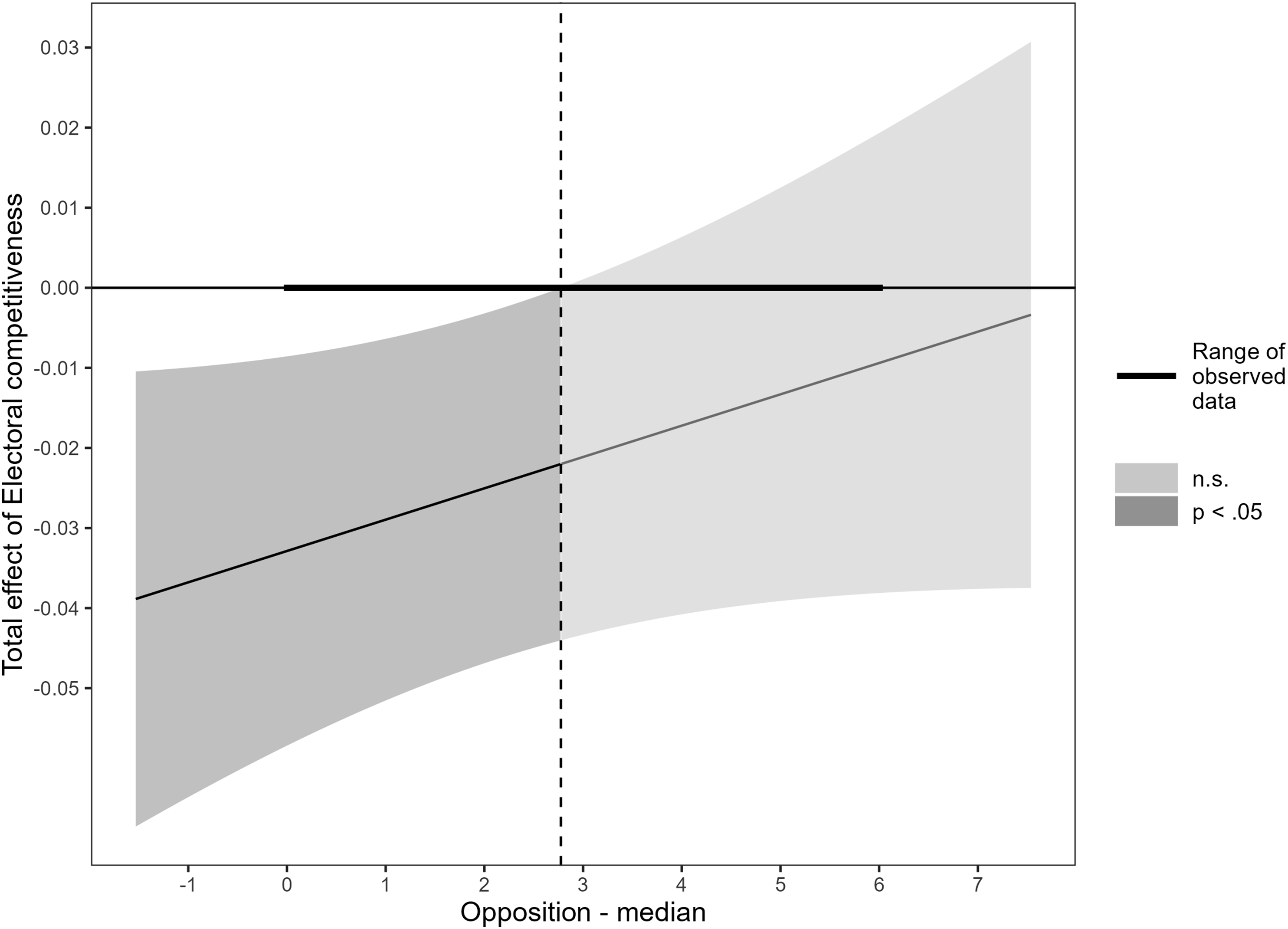

To test Hypothesis 3, we proceed with the multiple regression with the interaction term (see Model 2 in Table B1 in Appendix B for the full results). Figure 3 shows the estimated coefficients of [Competitiveness] as a linear function of [Opposition-median]. According to this figure, the total effect of [Competitiveness] becomes negative as [Opposition-median] decreases and is significantly negative at the 5% level when [Opposition-median] is smaller than 2.77 in the quadratic distance or 1.66 in the Euclidean distance. This suggests that the LDP candidate, even when facing a highly competitive election, do not represent the public on the issue of the consumption tax increase and is loyal to the party leadership when the rival opposition candidate does not represent the public. The total effect of electoral competitiveness by the distance between Opposition-median.

As a robustness check, we estimate the same model using a different measure of median voter positions on tax increases. Although the current measurement has the advantage of providing median voter positions that vary across SMDs, it is problematic in that the dependent variable, calculated using the weighted median based on the PR vote share of political parties, may be artificially correlated with the independent variable, electoral competitiveness measured by the SMD vote shares of LDP candidates, and may also be influenced by citizens’ support for the LDP on issues other than the tax increase.

To address this concern, we use the median voter position on the tax increase in the UTAS voter survey data, which is constant across SMDs, as an alternative measurement of median voter positions (“Robustness check 1”). To justify using the constant median voter positions across SMDs, we conducted an ANOVA to test whether the means of responses to the tax increase question differ significantly across SMDs in which respondents are available in the UTAS voter survey data, and found that for all three elections, there was no statistically significant difference at the 5% level. The full results using this measure of median voter position (Table B2 in Appendix B) are generally consistent with the original findings.

As a further robustness check, we use the multilevel regression and post-stratification (MRP) method, an approach that has been widely used in recent studies to estimate policy positions at the district level (“Robustness check 2”). Hanretty et al. (2018) demonstrate the effectiveness of MRP in estimating voters’ district-level policy positions, and this method has been used, for example, in studies of state-level policy support in the United States (e.g., Lax and Phillips, 2009). However, the use of MRP as a primary analytical method in Japan is problematic due to several data limitations. First, survey responses are not available for all SMDs. Second, SMD-level data on income and employment, which are thought to strongly influence voters' attitudes toward taxes, are not available, while the UTAS does not collect individual-level income data. Third, MRP typically includes urbanization as a district-level demographic variable that is already included in our main model, so including the urbanization variable in MRP may raise methodological concerns. These limitations lead us to avoid using MRP as the primary method for estimating median voter positions in SMDs.

Nevertheless, MRP may still be useful for robustness checks. In our MRP model, we include respondents’ gender, age, education, and ideology as individual-level variables. At the SMD level, we include the proportion of the population aged 65 and over, primary industry workers, single households, households with children under 18, 13 and the combined proportional vote share for parties opposing and calling for a delay in tax increases at the time of the election. 14 The results using MRP-estimated median voter positions (Table B3 in Appendix B) are generally consistent with the original results.

Conclusion

This study examined how elections affect the government’s attempt to raise taxes. Regarding the election and implementation of unpopular policies such as tax increases, previous studies have mainly focused on the impact of election timing on the ruling party’s decision to raise taxes. However, these studies have failed to consider the micro-foundations to explain how elections discourage the government from implementing tax increases. To address this shortcoming, the current study focused on individual ruling party politicians and showed that the competitiveness of elections in their districts gave them an incentive to oppose the government’s attempt to raise taxes.

We tested the hypotheses by estimating unbalanced panel data regression models with candidate-year fixed effects using data from three House of Representatives elections of 2012, 2014, and 2017 in Japan. Our results showed that LDP candidates tended to take the position closer to the median voter when facing a competitive election, and this tendency was more pronounced when the leading opposition candidate becomes closer to the median voter’s position.

The results of this study provide important insights that deepen our understanding of the behavior of ruling party politicians, particularly with respect to alignment with the median voter on tax increase policies. First, the electoral prospects of individual ruling party politicians are behind the government’s decision to delay the tax increase. Ruling party politicians facing a competitive election may deviate from the party leadership in order to maximize their own votes, even if it means revolting against the party’s election manifesto. This suggests that ruling party politicians influence the government’s decision to delay the tax increase.

Second, this study contributes to the literature of electoral competitiveness and representation. Some scholars argue that competitive elections lead to a convergence of their policy positions toward the median voter (Ansolabehere et al., 2001), while others hold that competitive elections give candidates incentives to represent special interests and thus candidates move away from the median voter (e.g., Fiorina, 1974; Powell, 1982). The current study provides supportive evidence for the former camp when important issues such as tax increase is at stake. For issues that are important to voters, candidates may change their opinions to get elected. In other words, the more important an issue is to citizens, the more politicians will represent them by bringing their own views closer to the median voter.

Third, previous studies of politicians’ attitudes toward the issue of tax increases have emphasized individual factors such as ideology and educational attainment (Osterloh and Heinemann, 2012; Janeba, 2014; Ashworth and Heyndels, 1997). In contrast, we examined electoral contexts as determinants of politicians’ issue positions, shedding a new light on how electoral competitiveness shapes their strategic positioning. Our study underscored the importance of considering the nuanced strategies that ruling party members employ during elections, particularly with respect to policy positions that may be unpopular but strategically important for electoral success. By examining these dynamics, we contribute to a more comprehensive understanding of legislative behavior and the interplay between electoral incentives and policymaking within political parties. These insights have broader implications for understanding and adapting to the complexities of contemporary political landscapes in Japan and beyond.

Furthermore, this study has complex implications for representative democracy. Even legislators belonging to parties that advocate tax increases are likely to listen to voters when their own re-election is uncertain. At the same time, this behavior not only encourages populist actions by politicians, but also raises the possibility that politicians will pander to voters only during elections and subsequently follow the party’s policy agenda to steadily advance tax increases. The implications drawn from this study require cautious interpretation and further research.

However, there are additional issues that deserve further investigation. First, although we have already addressed these issues, endogeneity remains a persistent challenge. One way to deal with this problem is to employ a two-stage least squares (2SLS) approach by estimating instrumental variables for electoral competitiveness, although the search for reasonable and feasible instrumental variables is generally challenging.

Second, this study used relative vote shares as a measurement of electoral competitiveness, but there is an ongoing debate and no consensus on how to measure electoral competitiveness. One of the remaining challenges for this study is to carefully consider possible measurements that better reflect the reality of electoral competition among candidates.

Fourth, a single-country study has a limitation in terms of its generalizability. One must be cautious in generalizing the results of this study to other countries in the sense that they are the product of Japan-specific factors. Future research should test our hypotheses with other countries and examine the validity of our findings across countries.

Nevertheless, as discussed in Sections 3 and 4, we believe that there is merit in looking at the Japanese case in order to draw some general insights into the government’s decision making on tax increases. Given the strong party discipline in the Diet, the political bargaining between the parties over the timing of the tax increase in the 2010s, and the availability of data on the attitudes of LDP candidates, Japan is the best possible case for examining how the electoral context affects politicians’ individual policy preferences, which ultimately shape the ruling party’s tax policy.

Footnotes

Acknowledgements

I would like to thank Takeshi Iida, Hideo Ishima, Hirofumi Miwa, Tsubasa Nishimura, Masaki Shibutani, and anonymous reviewers for their helpful comments. Any remaining errors are the authors' own responsibility. This work was supported by JST SPRING, Grant Number JPMJSP2129.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by JST SPRING, Grant Number JPMJSP2129.