Abstract

As geopolitical rivalry intensifies, Western states have moved to compete with China’s Belt and Road Initiative (BRI). However, the mobilisation of funds for global infrastructure remains paltry, suggesting that Western states cannot contest Chinese dominance here. Why? Through comparative political economy analysis of China and the United States, we argue that serious competition cannot be willed into being by state managers thinking geostrategically. States’ strengths and weaknesses are rooted in structural political economy dynamics. Where state managers’ plans jibe with, or express, the interests of powerful social forces and the capital and productive forces they command, a powerful impact results. This is true of China, whose BRI is principally a spatio-temporal fix for industrial overcapacity and over-accumulated capital. Conversely, where geopolitical ambitions are divorced from powerful groups’ interests and material realities, results are lacklustre. This applies to the United States, characterised by infrastructural decay, industrial hollowing-out and a dominant financial sector largely disinterested in infrastructure. Although US state managers are turning towards increased state spending on domestic infrastructure, internationally, the West’s continued neoliberal approach still relies on the already-failed approach of mobilising private capital into infrastructure investment.

Introduction

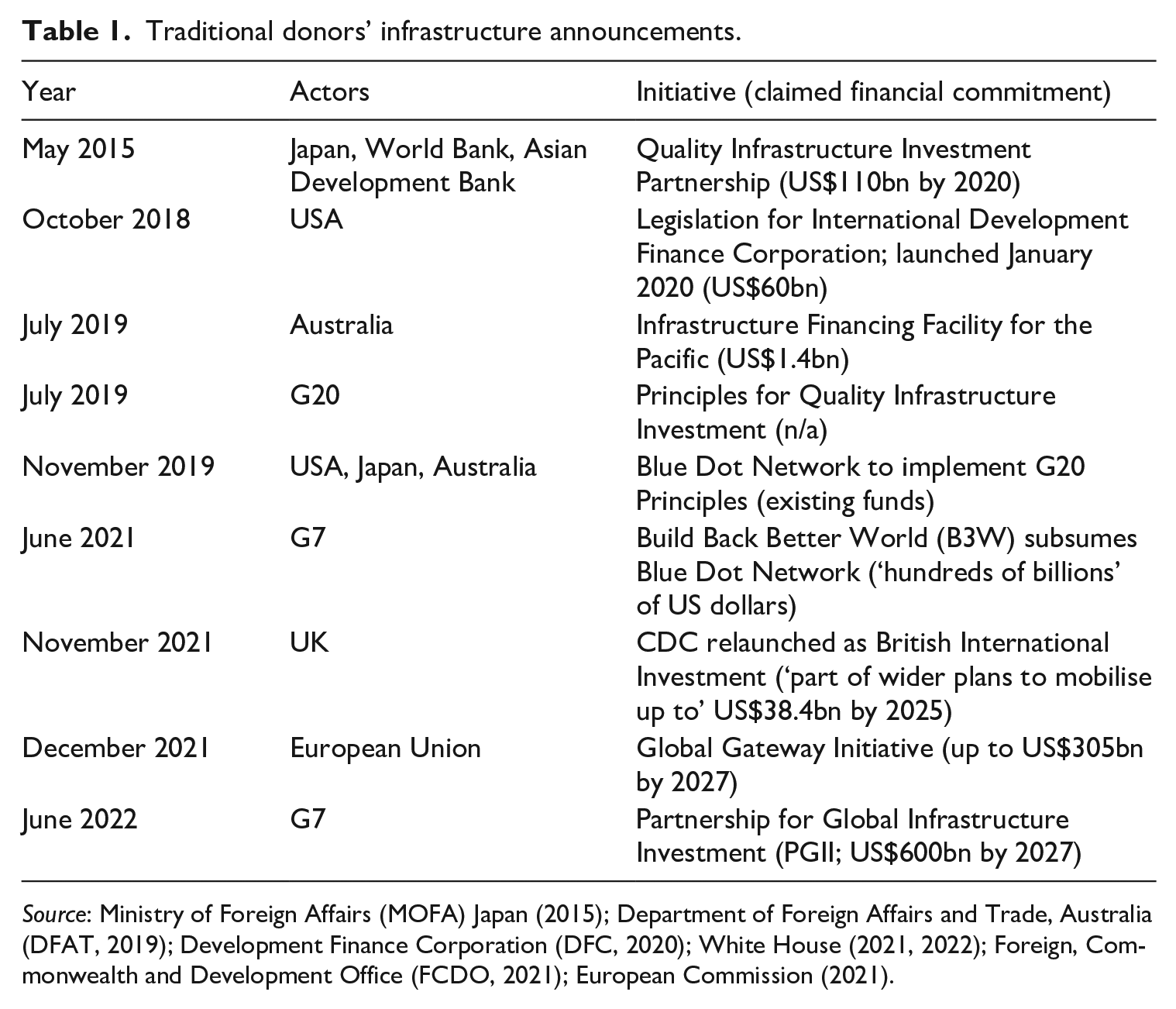

Since 2018, many traditional donor states have ostensibly reoriented their international development programmes to compete with China’s. This reflects their increasingly negative view of China as a strategic competitor that is advancing geopolitically by leveraging development financing through its Belt and Road Initiative (BRI), launched in 2013. Their return to financing ‘hard’ infrastructure is notable because, Japan aside, they had neglected this for decades, favouring ‘soft’ governance programming. Today, however, they announce new, big-budget initiatives with great fanfare (see Table 1).

Traditional donors’ infrastructure announcements.

However, the actual delivery of funds and projects has been remarkably underwhelming, especially compared to China’s BRI. This article focuses on the United States since, as the world’s wealthiest and most powerful country, with considerable fiscal and economic advantages compared to Europe, it is ostensibly best-placed to compete with China. Although relatively novel, US efforts lag China’s over a similar time frame and have very limited scope to improve. In the year following the BRI’s announcement, Chinese development financing surged by over US$30bn, from an already-high $60bn. Although disbursements peaked in 2016, 949 projects were recorded from 2013 to 2021, collectively worth US$170bn (Malik et al., 2021: 13, 61). Conversely, US infrastructure financing in 2019 was about US$1bn, down over three-quarters since 2005 (Organisation for Economic Co-operation and Development (OECD), n.d.). In its first year, B3W spent ‘a paltry US$6m’ on just two projects (Kenny and Morris, 2022). The US Development Finance Corporation (DFC), launched in January 2020 to compete with China, has a maximum capitalisation of just US$60bn; China Development Bank (CDB, 2021: 6) alone reported assets of US$2.54tr in 2020. From January 2020 to September 2022, the DFC made US$20.4bn in new commitments. However, only US$6.2bn was for projects that could conceivably be classified as ‘infrastructure’, and just US$253.9m was disbursed. Furthermore, with three-quarters of the DFC’s resources already committed (US$45.7bn), there is little scope for further growth (DFC, 2023). 1 Conversely, at the 2023 Belt and Road Forum, China committed another US$100bn for projects.

There is therefore a yawning – and ostensibly puzzling – gap between the West’s boldly stated resolve to compete with China on global infrastructure, and the actual delivery of projects and funds. Major Western states explicitly identify China as a strategic competitor threatening their security and prosperity and their cherished ‘rules-based order’. The BRI is widely seen as a nefarious grand strategy, challenging US hegemony by extending Chinese leverage (and, for some, military power). This is precisely why Western governments 2 decided to provide an alternative for developing countries. World order is ostensibly at stake. Why, then, are the status quo’s defenders mounting such a feeble defence? This makes little sense from traditional, state-centric approaches in International Relations (IR) and International Political Economy (IPE), which would expect the United States to mobilise sizable resources as part of its ‘economic statecraft’.

The answer, we argue, lies in the starkly different political economies underpinning and shaping the operation of the Chinese and US states. Our approach, based in Gramscian state theory and political economy, foregrounds the material constraints on ‘statecraft’ arising from the interests of dominant social forces, rooted in historically evolving, conflict-ridden capitalist development. States are not neutral instruments that political elites can simply repurpose at will. They are expressions of social power and interests, with past and current struggles shaping institutions, making them ‘strategically selective’: always more open to, and better at promoting, some forces’ interests and agendas over others’ (Jessop, 2008). States’ ability to compete geoeconomically depends on whether and how far state managers can mobilise the required productive forces and capital; this depends, in turn, on whether their agenda corresponds to the interests of the groups commanding these resources.

For China, the BRI was, in important part, a spatio-temporal fix to externalise industrial overcapacity and over-accumulated capital within state-owned firms and banks. These problems threaten China’s long-term growth model and hence dominant social forces’ survival, producing a powerful push for internationalisation through overseas infrastructure projects. These interests also shape the BRI’s implementation, generating blowback and retrenchment. Conversely, in the United States, after decades of deindustrialisation and defunding of public infrastructure, there are few productive forces to mobilise. To develop infrastructure, the United States depends heavily on mobilising private capital, which only deploys in limited, profitable areas. This model, which has failed domestically, has been internationalised to developing countries where prospects for success are even worse.

The limits of conventional perspectives on international economic competition

In mainstream IR and IPE, international economic competition is typically viewed through Luttwak’s (1990: 19) notion of ‘geoeconomics’: ‘the logic of war in the grammar of commerce’. Geoeconomics involves ‘the use of statecraft for economic ends; a focus on relative economic gain and power; a concern with gaining control of resources; the enmeshing of state and business sectors; and the primacy of economic over other forms of security’ (Youngs, 2011: 14). While approaches vary, all are limited by their implicit faith in states’ ability to mobilise ‘their’ economies’ resources, failing to appreciate how capitalist social relations shape state behaviour.

For realists, geoeconomics is intrinsic to IR. Unitary states, seeking survival under anarchy, use economic statecraft to pursue their national interests in endless, ‘zero-sum’ competition. States ‘act geo-economically simply because of what they are: territorially defined entities designed precisely to outdo each other’ (Luttwak, 1993: 64). Realists thus view the BRI as part of China’s geopolitical strategy, harnessing development financing to undermine US hegemony. They mainly debate how far China’s economic statecraft threatens US interests, and whether countermeasures should be forceful or exhibit ‘geoeconomic restraint’ (cf. Friedberg and Boustany, 2020; Kim, 2021).

Many liberals accept realists’ basic perspective but lament this shift from a ‘Neoliberal Order’ to a ‘Geoeconomic Order’, seeking to preserve cooperation through institutions that restrain competition and create ‘positive-sum’ outcomes (Roberts et al., 2019). Accordingly, liberals recommend responses to the BRI that strengthen existing multilateral institutions, rather than bilateral competition (e.g. Kenny and Morris, 2022).

These approaches have two weaknesses for our purposes. First, they would struggle to explain the yawning gap between the United States’ stated intentions and its actual performance. Why the world’s richest, most powerful state seems unable to mobilise the necessary resources to compete on global infrastructure with China – still a relatively poor, developing country – is mystifying from a traditional IR perspective. US defence spending vastly outstrips China’s. If geoeconomics is indeed war by economic means, why does the United States not dedicate similar resources to compete with the BRI, given the US/G7’s identification of infrastructure as a crucial focus for contesting Chinese influence?

A second, connected problem is the tendency to view states and markets as separate, externally related objects. Realists implicitly assume state control over the economy by treating economic indicators and resources as attributes of national power and neglecting to consider how markets shape state behaviour. Conversely, liberals ask whether states or markets are dominant, for example, describing a shift from a market-led to a state-led era. Such distinctions fail to recognise that markets necessarily emerge and operate through the transformation of states to establish and protect market processes and their distributional outcomes (Hameiri and Jones, 2020). Consequently, the real question is not whether markets or states dominate, but whose interests are advanced through different state forms in particular historical moments.

More promising, but still limited, are liberal approaches that explore how domestic political considerations shape policymaking. Solingen (1998), for example, argues that states’ external policies are shaped by struggles between ‘liberalizing’ and ‘backlash’ coalitions. Open Economy Politics scholars have developed this idea, attributing growing Sino-US economic competition to domestic rent-seekers’ demands for protection domestically and exclusivity abroad, fuelling rivalry ‘despite perhaps [the] best intentions of both states’ (Lake, 2018: 237). They thus credit Donald Trump’s rise and the US–China trade war to the anti-globalisation backlash from economic ‘losers’.

However, liberal approaches still struggle to explain the precise form and extent of states’ international economic competition, because of their assumption that ‘zero-sum’ contests necessarily reflect protectionist interests. There is little evidence that the undeniable ‘losers’ of US-led globalisation – manufacturing firms and workers – benefitted from Trump’s trade war (or his other policies). Trump’s focus on intellectual property and market access seemed instead to cater to globalisation’s winners. The same, we shall see, is true of US infrastructure competition with China, which caters not to ‘losers’ but to the chief winners: finance capital.

Explaining how, and how well, states compete

To surmount these limitations, we follow Babić et al.’s (2022) call for a ‘political economy of geopolitics’ that is not exclusively ‘state-centric’, but situates state power within social power relations and political economy dynamics. We argue that state managers cannot simply mobilise ‘their’ national resources to pursue their chosen policy goals; rather, their goals, and states’ ability to pursue them successfully, are conditioned by dominant social forces’ interests and agendas, which are materially embedded within evolving, conflict-ridden capitalist development.

Our approach is rooted in Gramscian state theory, which sees states not as unitary actors but as complex institutional ensembles reflecting and entrenching constellations of social, political and economic power (Jessop, 2008). The state’s form and operation are understood not simply to express political leaders’ will or strategy, but the interests, agendas and struggles of dominant social forces, spanning state and society (Gramsci, 1971; Poulantzas, 1978). States’ institutional arrangements, and policymaking and implementation, are shaped by socio-political conflict, principally among classes and class fractions but also potentially ethnic, religious and other groups. These forces struggle for power and control over resources, seeking to reshape the state to advance and entrench their own interests and agendas, while marginalising their opponents’ (Hameiri and Jones, 2020). Consequently, the state is never a neutral instrument that governments can simply use or repurpose at will. Its institutions always exhibit a ‘strategic selectivity’, systematically favouring some social forces’ interests and agendas over others (Jessop, 2008). IR – whether cooperative, competitive or conflictual – is therefore understood as the expression of states’ underpinning socio-political coalitions (Bieler and Morton, 2018; Chacko and Jayasuriya, 2018; Rolf, 2015).

Although state managers (policymakers) typically have some autonomy from individual business interests, capitalist states – including China’s – systematically advance the interests of dominant capitalist fractions. Structurally, state managers depend on capital for many desired social processes, including investment, production, employment and revenue generation, meaning the state’s very survival entails creating conditions necessary for capital accumulation (Block, 1987). Agentially, leading business interests are also far better organised and resourced than other groups to influence policymakers, dominating in lobbying and party financing, and enjoying high-level access through institutionalised and informal consultations, and a ‘revolving door’ with officialdom, compounding advantages arising from shared social backgrounds and networks (Blanes i Vidal et al., 2012). However, because states reflect socio-political contestation, organised business’ power can be challenged and attenuated under certain historical, social and geopolitical conditions. Notably, in the early post-WWII decades, capital was forced to compromise with organised labour to stabilise its dominance (Ruggie, 1982). However, where other forces are weak or absent, capital’s basic interests are particularly powerful.

Nonetheless, as this emphasis on contestation suggests, states do not simply do big business’ bidding. US leaders’ decision to compete with China on infrastructure clearly reflects their peculiar concerns, heavily conditioned by realist thinking: worries that the United States and traditional donors are losing influence and prestige in developing countries to Beijing, and about China’s growing impact on global norms and institutions. Nonetheless, as demonstrated below, exactly how US officials pursue competition with China reflects the US state’s transformation primarily to serve finance capital’s interests. Far from demanding competition with China on global infrastructure, Wall Street is largely disinterested – and this explains the limits of Washington’s competitiveness.

Indeed, how well states compete internationally depends upon how far state managers’ geoeconomic vision and policies jibe with dominant social forces’ interests. 3 To pursue geoeconomic agendas, state managers must mobilise the necessary capital and productive forces: commodities, machinery, labour, technical knowhow and so on. However, whether these even exist, let alone in the necessary quantities, and whether they can be ‘deployed’ for ‘statecraft’, are open questions. Resources and capital are highly unevenly distributed, thanks to uneven and combined capitalist development (Rolf, 2015). Obviously, one cannot build a bridge without the requisite cement, steel or engineering expertise, or the capital to purchase these. Realists appreciate this basic reality but wrongly assume that states can simply ‘wield’ domestic capital and resources as part of their ‘national power’. Conversely, we insist that state managers’ ability to mobilise productive forces and capital depends on whether their agenda corresponds with the interests of the social groups commanding these resources. In capitalist states, governments do not straightforwardly ‘command’ key resources. Even in China, state-owned enterprises (SOEs) and banks are quasi-autonomous actors, principally motivated by profit, not geopolitical gain; their activities are not directed by geostrategic policymakers (Jones and Zeng, 2019; Jones and Zou, 2017). If relevant forces are enthusiastic – supporting or even demanding a given geoeconomic initiative – we can expect forceful implementation of official agendas. Conversely, where they are indifferent or hostile, outcomes will be constrained. As Trump’s trade war indicates, state managers may have sufficient autonomy to develop policies that alienate dominant capitalist fractions. Nonetheless, unless they are prepared to compel businesses’ active participation, practical implementation will remain weak. Moreover, whether compulsion is even thinkable, let alone practicable, will itself depend on society’s balance of forces. The postwar settlement was not simply the result of forceful policymakers imposing their will, but of mass mobilisation through two world wars, the power of organised labour and affiliated political parties and the threat of communism. Absent wider struggles and transformations, decision-making and implementation will likely follow the grain of existing power relations.

In sum, to understand how, and how well, states compete geoeconomically, we must first identify the socio-political relations shaping their strategic selectivity, and then study whether these enable state managers to mobilise the requisite productive forces and capital. We now use this approach to explain China’s massive international infrastructure financing footprint, and the US’ underwhelming response.

Explaining China’s international infrastructure programme

Beijing’s impressive global infrastructure-building role is essentially an external expression of contradictions arising from China’s capitalist development. China’s export-oriented, investment-led growth model has resulted in enormous structural imbalances, including over-investment, vast surplus industrial capacity and capital overaccumulation. The BRI sought to ameliorate these problems by externalising them. Its explosive implementation reflected, and was powerfully shaped by, the industrial and financial cadre-capitalist interests that dominate China’s party-state.

China’s post-Mao economy has been fuelled by export-oriented industrialisation, exploiting Western-led offshoring and trade liberalisation, and the direction of export revenues and domestic savings into state-led investments in industry and infrastructure. This has produced unprecedented growth, but also entailed the vast over-expansion of productive forces and infrastructure relative to effective demand. Today, China produces over half the world’s steel and cement, 10 and 6.5 times as much, respectively, as second-placed India (Statista, 2021; WSA, 2021). Its infrastructural development has been similarly staggering. China now has two-thirds of the world’s high-speed railways and generates three times the hydroelectricity of second-placed Brazil (International Hydropower Association (IHA), 2020: 10; State Council, 2021). However, over-investment has generated vast overcapacity and market saturation in everything from transportation to housing. Even before COVID-19, industrial overcapacity had reached almost 25 percent (National Bureau of Statistics, China (NBS), 2020). Skilled labour is also overproduced. China trains 22 percent of the world’s science and engineering graduates – versus the United States’ 10 percent – but most struggles to find work (American Institute of Physics (AIP), 2018).

These problems were compounded by the 2008 global financial crisis (GFC), which caused a sharp, sustained fall in Chinese exports and gross domestic product (GDP) growth, exacerbating industrial overcapacity. Profitability, which had already been falling due to over-investment, collapsed. Returns on SOEs’ domestic assets fell below the cost of capital, while every RMB5 of domestic investment now generated just RMB1 of economic growth. This meant even fewer profitable outlets for China’s financial sector, which, by 2014, had accumulated deposits of US$5.14tr, alongside US$4tr in foreign exchange reserves, much of it unprofitably invested in US gilts (Jones and Hameiri, 2020: 5).

Policymakers’ response to this crisis reflects the Chinese party-state’s strategic selectivity, which systematically favours state and state-linked capital’s interests over workers and households. Keynesian economists have long advocated cutting surplus capacity and rebalancing from investment to domestic consumption. However, this would require increased wages and welfare, plus austerity for cadre-capitalists in industry and construction. The latter are far more powerful and organised than politically repressed workers. They enjoy privileged access to decision-makers and finance, and are huge employers, making their continued viability essential for the Communist Party’s performance legitimation and wider socioeconomic goals. Construction alone accounts for a quarter of China’s economy, is linked to one-third of local government revenue and employs 16 percent of urban workers (Guo et al., 2022; McMahon, 2018: ch. 4). It is also China’s second-most corrupt sector, generating kickbacks for officials (Pei, 2016: ch. 4).

Reflecting these entrenched interests, state managers responded to China’s post-GFC crises through domestic stimulus and efforts to externalise surplus capacity and capital through the BRI. Domestically, RMB1.5tr of the government’s post-GFC RMB4tr (US$586bn) stimulus package was earmarked for infrastructure (Qin, 2016: 204). Externally, through the BRI, Beijing encouraged other states to borrow from Chinese banks to fund infrastructure projects implemented by Chinese contractors. Led by the National Development and Reform Commission, the BRI was an extension of industrial and spatial development planning, offshoring surplus capacity and outmoded industries, with provinces lobbying for support for their pet projects (Jones and Hameiri, 2020: 6; Jones and Zeng, 2019; Ni et al., 2020).

China’s BRI ‘succeeded’ because it jibed with the powerful state-linked interests that it is intended to serve. SOEs secured 96 percent of BRI construction contracts and 72 percent of investment projects from 2013 to 2018 (Jones and Hameiri, 2020: 7). Their interests also shaped practical implementation. Project documents revealed that ‘industrial overcapacities’ were ‘the main motivation behind projects and program’, which were ‘not regulated or guided’ by policy frameworks or geostrategic objectives (Ye, 2019: 707). Projects were as likely to be located outside of the BRI’s six official ‘corridors’ as inside, and investment grew fastest in non-BRI countries (Jones and Hameiri, 2020: 7). Provincial governments also appropriated much BRI financing to bail-out faltering domestic infrastructure schemes and ‘save loss-making SOEs’ (Ye, 2019: 708–709).

The BRI also ‘worked’ because it suited Chinese financial-sector interests, which are skewed towards supporting SOEs’ megaprojects, including high-risk projects shunned by traditional development financers. This reflects five structural features of China’s political economy. First, households are effectively forced to save in commercial banks, which are in turn driven to purchase policy banks’ bonds, generating huge capital inflows (Chen, 2021: 843). With domestic profitability collapsing, banks eagerly seek opportunities overseas. Second, perennial export surpluses have generated vast foreign currency reserves, which are directed to support overseas investment and lending, including through transfers to policy and commercial banks (Setser, 2023). Third, extensive state ownership and cadre-capitalist guanxi networks ease lending, particularly to SOEs, as lenders assume that state(-backed) entities will eventually repay (Breslin, 2014). Fourth, risk assessment and oversight among regulators and lenders is weak, particularly overseas, leaving them dependent on SOEs’ own (frequently over-optimistic) assessments (Jones and Hameiri, 2021: 177–178). Fifth, as international latecomers, Chinese firms and lenders are forced into higher-risk markets that established competitors shun (Jones and Zou, 2017: 750). These factors – coupled with apparatchiks’ incentive to support top leaders’ initiatives – meant that Chinese financial institutions enthusiastically embraced the BRI.

Nonetheless, Chinese SOEs and banks are quasi-autonomous, profit-seeking actors, and their desire to minimise risk and maximise profit also shapes BRI implementation. Infrastructure-related risks are twofold: pre- and post-completion (Klagge and Nweke Eze, 2020). Pre-completion risks include the costs and difficulties associated with feasibility studies, exploration, land acquisition, environmental and social impact assessment (ESIA) and mitigation, meeting other regulatory requirements, preparing and facilitating construction, project construction, site security and financial risks like currency fluctuations. Post-completion risks include political risks (e.g. violent instability endangering the project, nationalisation, policy or regulatory change) and uncertain returns (e.g. fluctuations in demand or user fees).

Chinese SOEs and lenders bargain hard to shift these risks onto BRI recipients while maximising their own profits. They have often succeeded due to factors shaping developing recipients’ decision-making. Host governments are often desperate for development financing, unable to attract more risk-averse investors, evaluate risk and returns poorly and/or are motivated by sectional political/ economic interests (Jones and Hameiri, 2020). Consequently, they have often signed lopsided contracts. Chinese SOEs typically demand that host states bear many pre-completion risks, either directly or through incorporating local firms as project partners, for example, to manage ESIAs, displacing communities from project sites and so on (Jones and Hameiri, 2021: ch. 4).

To minimise post-completion risks, Chinese SOEs prefer ‘turnkey’ projects, whereby they are paid (e.g. through a host-state loan from CDB or Eximbank) to construct a project and then transfer it to the recipient. This gives SOEs little incentive to ensure projects’ viability. Where recipients’ planning processes are weak, misguided or corrupted, this often generates ‘white elephant’ projects (Jones and Hameiri, 2020). Less ideal for SOEs is a Build-Operate-Transfer model, whereby the SOE owns and operates the infrastructure for a fixed period, during which it hopes to make a profit on its initial investment, before transferring the asset to the host state. This is feasible only for projects generating direct user fees, for example, electricity generation, telecommunications. Even then, SOEs typically seek to minimise their risks, for example, by insisting that host states guarantee income streams, regardless of demand, for example, with hydropower dams in Laos (Barney and Souksakoun, 2021). The riskiest approach is equity investment, which entails longer-term responsibility for a project’s viability. SOEs – and Chinese financiers involved in equity funds (see Moses et al., 2022) –pursue this only where post-completion risks are either low or are mitigated, for example, by long-term contracts maximising a profit-generation window, or by securing tradeable outputs, like oil. Where SOEs cannot secure favourable terms, they will not implement projects, even where they have notionally been agreed by Chinese and host-state leaders as ‘flagship BRI projects’ (Zhang, 2019).

Chinese banks and insurers strike similarly hard bargains. For lenders, the BRI is an opportunity to expand commercial-rate lending and, reflecting recipients’ risk profile, they typically charge interest rates of 4–6 percent, versus traditional multilateral lenders’ 0.5–1 percent (AidData, n.d.). To ensure repayment, they have used controversial methods, such as using oil sales or cash as collateral (Chen, 2021: 848). They have also stalled or scrapped projects considered unprofitable, even where they ostensibly enjoy high-level political backing (e.g. Global Energy Monitor, 2022).

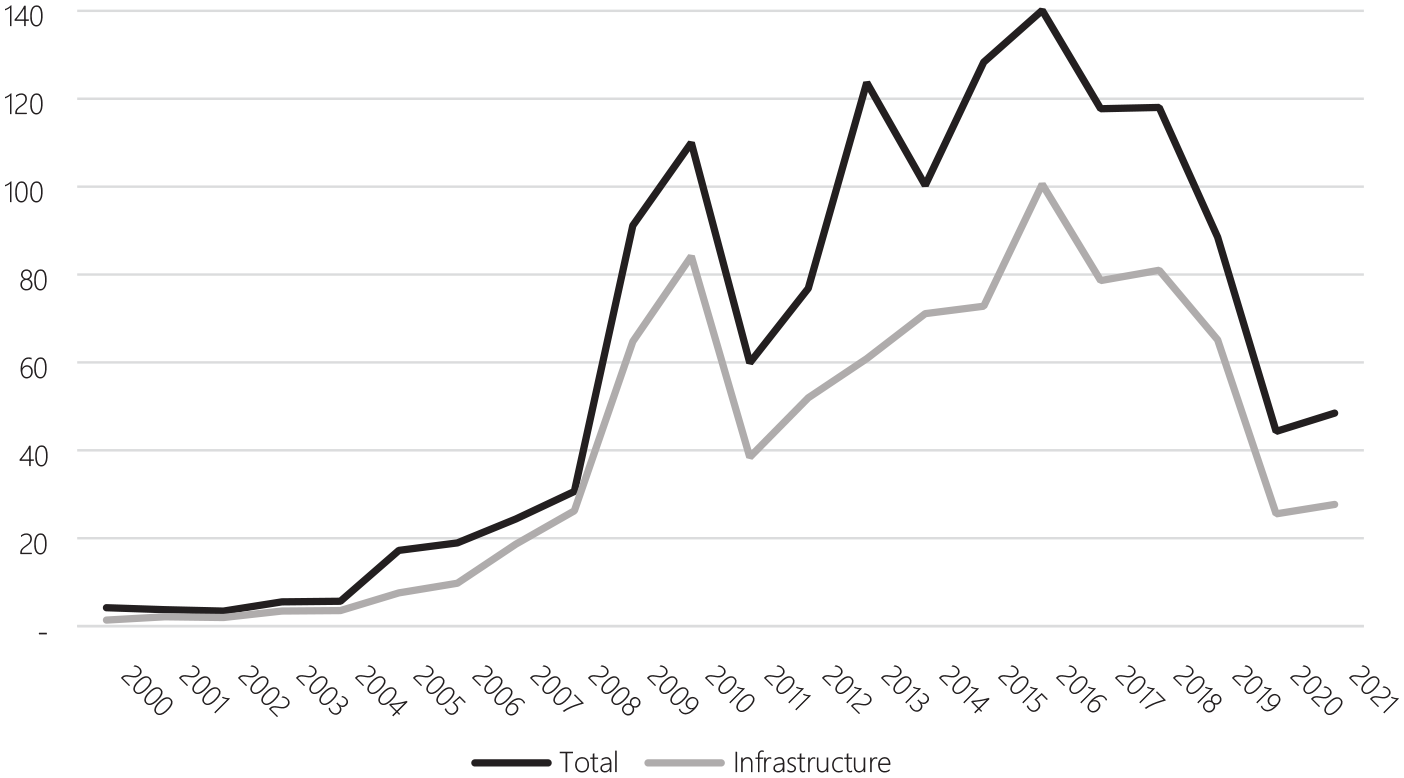

The BRI’s initiation and implementation have thus been powerfully shaped by forces within China’s political economy; they do not simply reflect state managers’ ‘geoeconomic statecraft’, as realist or liberal accounts suggest. Scaling up earlier initiatives, the BRI internationalised China’s development model in response to contradictions within its domestic economy. Because it served the interests of powerful state(-linked) firms and banks, it secured their enthusiastic participation, resulting in a massive surge of projects (see Figure 1). However, these actors’ profiteering objectives also powerfully shaped the BRI’s implementation. Contrary to state managers’ ‘win-win’ rhetoric, SOEs and lenders arguably exploited recipient governments’ weaknesses to secure terms that often benefitted them disproportionately. One estimate finds that half of BRI projects generate no economic value while only one-tenth will break even (Lane, 2020). Controversies mounted over environmental damage, labour abuses, community displacement, white elephant projects and unsustainable debt, dampening recipients’ appetite and damaging China’s global reputation (Malik et al., 2021).

Chinese overseas development financing – grants and loans (Constant 2021 US$bn).

This reaction drove policy changes that reined-in the BRI. In 2017, in response to growing international blowback, Chinese regulators and banks tightened rules to prevent firms exploiting the BRI for unintended, controversial projects. Commission for Discipline Inspection teams also began investigating some projects for corruption. At the 2019 Belt and Road Forum, Xi Jinping implicitly acknowledged various shortcomings, promising higher-quality projects and a ‘clean and green’ BRI. Combined with prospective recipients’ greater hesitancy, regulatory tightening suppressed BRI financing (see Figure 1), even before COVID-19 lockdowns plunged many developing countries into debt distress.

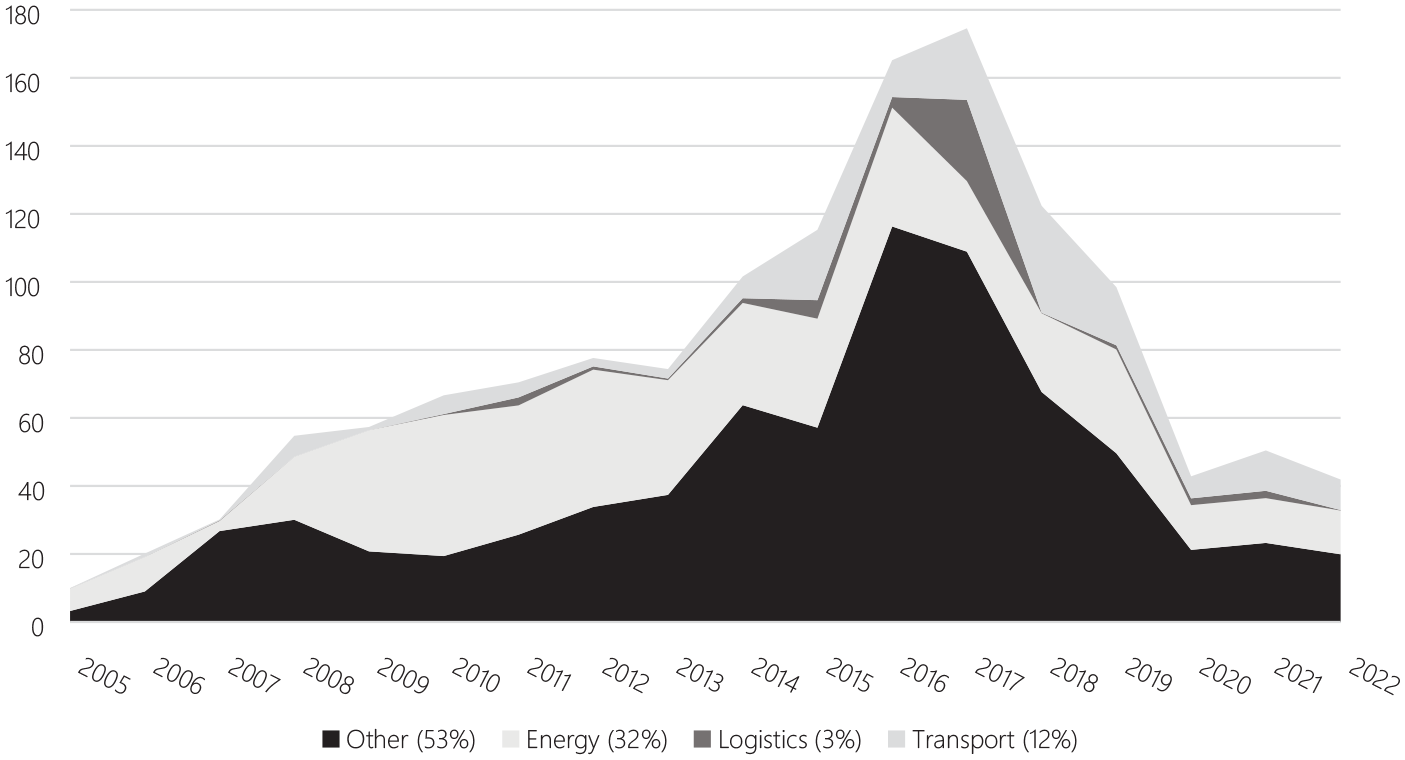

To adapt, Chinese policymakers are experimenting with special-purpose funds and involving more private and multilateral finance – through syndication, multilateralisation and public–private partnerships (PPPs) – to reduce policy banks’ risk exposure and dependence on sovereign lending (Liu and Dixon, 2022; Moses et al., 2022; Parks et al., 2023; Van Wieringen and Zajontz, 2023). China’s involvement in global infrastructure may therefore pivot from megaprojects framed by intergovernmental agreements, back towards state-supported investment, whose quantity and infrastructure focus remain substantial (see Figure 2). To kickstart demand, China is also beginning to provide grants to help develop a bankable pipeline of projects (see Liu et al., 2023). Beijing is also emphasising non-infrastructural development assistance, suggesting further convergence with traditional donors (Carmody et al., 2022).

Chinese outbound investments >US$100m, by sector, 2005–2022 (US$bn).

The United States’ feeble competition

Whatever the woes of Chinese development financing, the United States remains unable to mobilise comparable productive forces or capital to compete, thanks to its radically different political economy. In the post-1970s neoliberal era, industrial hollowing-out and under-investment in infrastructure have eroded relevant productive forces, generating no comparable impetus from industry to internationalise. Reflecting the dominance of finance capital, US state managers primarily pursue domestic infrastructure construction by incentivising and ‘de-risking’ private investment. This has largely failed because private-sector appetite is weak, given the limited opportunities to extract profit. Recent changes – reflecting populist upheavals arising from contradictions within globalising US capitalism – are significant but remain constrained by neoliberal legacies. Crucially for our purposes, US external policy remains entirely premised on ‘escorting’ private capital into infrastructure, scaling up an approach that has already failed domestically and abroad.

State transformation and the rise and fall of US infrastructure

Since the 1930s, reflecting different configurations of social forces and struggle, and changes within global capitalism, the US political economy has evolved through three periods, with contrasting implications for infrastructure development.

The New Deal era (mid-1930s–mid-1970s) saw rapid industrial growth and infrastructural development. This reflected organised labour’s growing power and state managers’ efforts to stabilise capitalism and defeat fascist and communist rivals, which required significant concessions from an endangered capitalist class (Katznelson, 2013). The new class compromise of ‘embedded liberalism’ entailed Keynesian and Fordist arrangements which, coupled with massive military investments, vastly expanded America’s industrial base (Ruggie, 1982; Tassinari, 2019). While the military–industrial complex remained central, stimulating wider consumption and growth (Tassinari, 2019), civilian industry and suburbanisation also flourished, supported by federal investment in public infrastructure, which surged from the 1950s, peaking at over 2 percent of GDP in the late 1970s (Levy, 2021; Tomer et al., 2021).

The neoliberal era (1970s–late 2010s) saw the US state reconfigured around the interests of globalising fractions of capital, entailing industrial hollowing-out and infrastructural decline. This development stemmed from a global crisis of postwar capitalism, with rising energy prices and labour costs and militancy squeezing profitability, provoking a counter-offensive from capital and the ‘new right’ (Harvey, 2005). Under Reagan, rising popular expectations were crushed through attacks on organised labour, while profitability was restored by dismantling New Deal protections, pursuing pro-business deregulation and combining industrial subsidies to high-tech, military-linked industries with aggressive trade policies to hobble foreign competitors (Block, 2008; Hacker and Pierson, 2010; Tassinari, 2019).

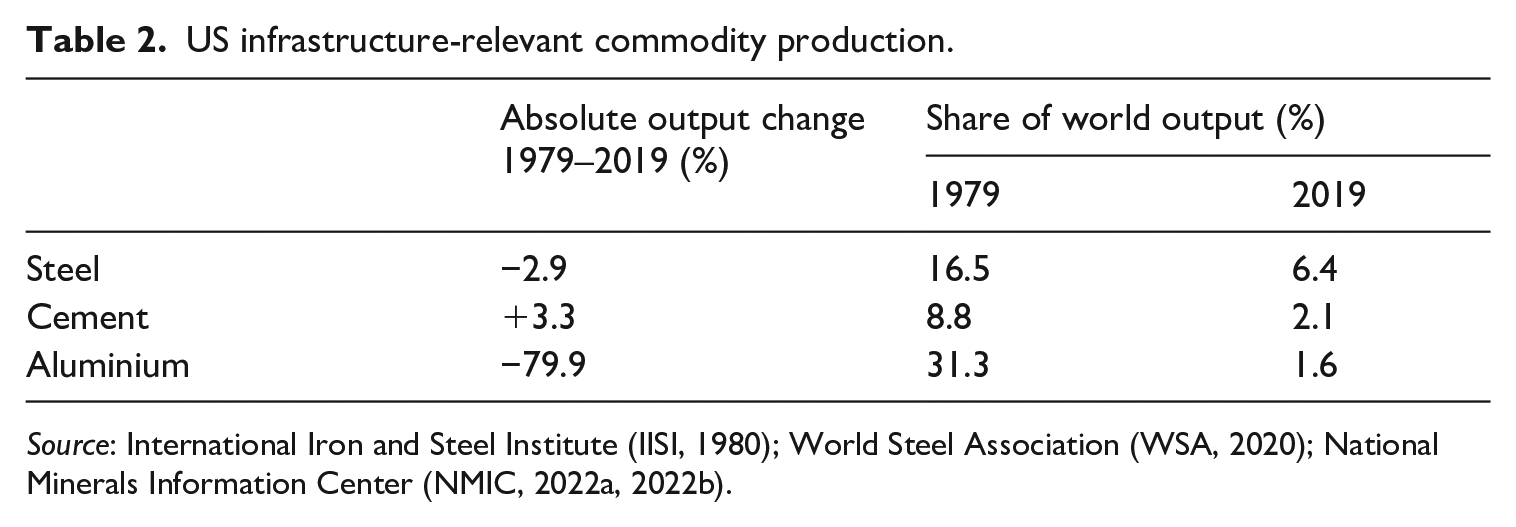

The US political economy fundamentally transformed in this period, realigning domestic socio-political dynamics. Offshoring to low-wage economies, including China, corroded the US industrial base. While the US population and GDP grew by 46 and 713 percent, respectively, over 1979–2019 (DataCommons, 2021), infrastructure-relevant productive output has stagnated or collapsed (see Table 2). Leading US firms have become heavily financialised and rentierist, deriving profit primarily from financial transactions and controlling ‘intangibles’ like intellectual property rights (Schwartz, 2022; Van der Zwan, 2014). Even notionally industrial firms have moved in this direction, focusing on maximising short-term ‘shareholder value’, often by cutting capital investment (Lazonick and Shin, 2019). Coupled with financial liberalisation, the result has been vast over-accumulation of capital in the sphere of circulation (financial transactions and asset management) rather than production (Christophers, 2023; Tooze, 2018). Inequality of wealth and power has sharply increased as real wages have stagnated, with consumer demand buoyed only by burgeoning household debt (Klein and Pettis, 2020). Concentration of asset wealth in richer, high-saving households has further reinforced the rise of asset management firms (Christophers, 2023).

US infrastructure-relevant commodity production.

This neoliberal transformation entailed sharp deterioration in US infrastructure. This does not reflect declining fiscal capacity per se. State managers have borrowed heavily for other purposes: federal debt tripled from 1980 to 2012 to over 100 percent of GDP, peaking at 135 percent during COVID-19 (U.S. Office of Management and Budget (OMB) and Federal Reserve Bank of St. Louis (FRBSL), n.d.). However, reflecting the US state’s strategic selectivity, spending prioritised the interests of finance capital and the military–industrial complex. Trillions of dollars were spent on post-GFC financial sector bailouts, demonstrating finance capital’s structural power (‘too big to fail’) and the ‘revolving door’ with officialdom (Tooze, 2018). Moreover, the state has continuously subsidised firms in security-related sectors, notably information communications technology, energy and semi-conductors. However, given the decline of justifications for the ‘public good’ under neoliberalism, this ‘hidden developmental state’ has been limited to correcting ‘market failures’ in areas deemed essential for ‘national security’ (Block, 2008; Block et al., 2023; Tassinari, 2019). This reflects the continued power of military–industrial interests, often connected to Congressional pork-barrelling.

Conversely, with few powerful corporate interests demanding support and subordinate groups disorganised and weakened, public investment in infrastructure languished. From 1980 to 2020, federal infrastructure funding more than halved, to around 0.8 percent of GDP (Tomer et al., 2023). From 2007 to 2017, it fell by almost US$10bn annually, with more going to maintenance than new projects (Siripurapu and Masters, 2021). In 2013, for example, just 6 percent of federal transportation spending went to new road and bridges (Petroski, 2016: ch. 2). Meanwhile, subnational governments’ budgets have been squeezed by years of economic crisis and austerity. US states are forbidden to undertake deficit spending and, although allowed to issue bonds to finance infrastructure, they are reluctant to do so because repayments count as current expenditure. Consequently, unlike China’s spendthrift, quasi-bankrupt provinces, states’ debt-servicing costs have flatlined since the 1970s, comprising just 3.3 percent of total expenditure (Siripurapu and Masters, 2021). Accordingly, states’ total capital expenditure fell from 3 percent of GDP in the 1960s to just 2 percent by 2017 (McNichol, 2019).

With public financing constrained, state managers have looked to private investors to fill the gap, by turning infrastructure into an investment asset. Successive governments have promoted PPPs, based on the notion that small sums of public money can ‘mobilise’ or ‘escort’ vastly larger private investments by supporting the development of ‘bankable’ (profitable) projects, and by incentivising and ‘de-risking’ investment (Gabor, 2021). Obama’s Moving Ahead for Progress in the 21st Century Act 2012 adopted this approach, as did Trump’s infrastructure plan, which sought to galvanise US$1.5tr of private investment through just US$200bn of public expenditure (McNichol, 2019).

Although effective in some settings, this approach is inherently problematic with respect to infrastructure, because many projects are incompatible with finance capital’s demand for reliable profits. Governments investing in public infrastructure rarely expect projects to yield direct returns that cover the cost. Rather, they hope that, by supporting wider capitalist accumulation, projects will indirectly generate long-term tax revenues, or they may accept loss-making projects because they are valuable public goods. Private investors, however, only invest where they believe they can derive a direct, profitable return. Investors’ profit-seeking, risk aversion and frequent short-termism are simply incompatible with many kinds of infrastructure projects, which may take decades to generate returns, and often do so only indirectly (Arun, 2023).

US states have tried to address these problems by catering to investor interests (Gabor, 2021). First, they have sought to ‘de-risk’ direct investment by essentially guaranteeing profitable revenues through tax breaks, subsidies and lopsided contracts shifting risk from private investors onto public bodies (McNichol, 2019; Petroski, 2016: ch. 20). Second, complex financial arrangements are cultivated to facilitate indirect infrastructure investment, backstopped by public money. For example, states can issue bonds for infrastructure projects, which are repackaged into securities that, being more liquid, are more attractive to investors.

Nonetheless, infrastructure PPPs have never taken off in the United States. From 1985 to 2016 there were just 498 PPPs, collectively worth US$116.5bn (Geddes and Reeves, 2017). Investors have typically only engaged where projects generate profitable user fees – largely limited to energy and telecommunications, which, therefore, comprise over 80 percent of private infrastructure investments (McNichol, 2019) – or where state-backed arrangements guarantee their profits (Griffiths and Romero, 2018: 4). However, unlike the Chinese party-state, where moral hazard abounds, US states have often baulked at investors’ demands (Petroski, 2016: ch. 20). Furthermore, as we elaborate below, investors often avoid infrastructure due to portfolio-level incentives and constraints, even when governments pursue extensive project-level de-risking (Arun, 2023).

The result is severe decline in US infrastructure and associated productive capacity. The American Society of Civil Engineers (ASCE, 2021) grades US infrastructure at ‘C-’ and estimates that US$2.9tr would be needed over 10 years merely to achieve a ‘B’ grade, up from US$2.1tr 10 years ago. Relevant productive output has stagnated or collapsed, especially relative to global output (see Table 2), and serious shortages of skilled labour (Kane and Puentes, 2015). Consequently, unlike in China, there is no impetus from industry to internationalise domestic productive capacities.

The third, and current period might, following Gramsci (1971), be characterised as an ‘interregnum’, or perhaps simply a prolonged crisis of neoliberalism. Some observers talk of ‘post-neoliberalism’, which captures the sense of reaction against neoliberalism but arguably exaggerates the extent of a transition to a new political economy model (Babić et al., 2022: 9). Today’s conditions reflect the GFC’s long-term fallout and the political contradictions of neoliberal capitalism, expressed in both collapsing political engagement and populist rebellions across advanced capitalist states.

Like ‘national populism’ elsewhere, Trumpism is fuelled principally by disaffected middle- and working-class citizens who are the ‘losers’ of globalisation (Eatwell and Goodwin, 2018). State managers’ need to respond to and contain this rebellion is driving significant political and state transformation, including growing emphasis on ‘security’ over openness and an apparent revival of interventionist/protectionist economic policy (Chryssogelos, 2018; Gerbaudo, 2021). Attempts to re-legitimise the US state through ‘Bidenomics’ is the most significant global exemplar. Concessions remain limited, however, by the disorganised, weakened nature of the subaltern challenge which, moreover, is not linked in elite calculations to a systemic challenger to liberal capitalism – unlike organised labour and the political left during the Cold War.

Notwithstanding the difficulty in assessing very recent changes, substantial continuities with existing neoliberal practices should temper any judgement about a ‘New Deal’ redux. Biden’s Inflation Reduction Act 2022 leans heavily on subsidies (tax credits) and de-risking (loan guarantees) to stimulate private firms to invest in sustainable energy and semiconductors (Gabor, 2023; see also Christophers, 2023; Tomer et al., 2023). The Infrastructure Investment and Jobs Act 2021 (IIJA) involves more substantial public investment in infrastructure – US$863.7bn in federal spending (Tomer et al., 2022) – but even this is inadequate, and its results will likely be heavily constrained by the neoliberal era’s entrenched legacies.

While IIJA’s budget sounds impressive, it will not even cover the backlog of unmet infrastructure needs. For example, although 42 percent of total IIJA funding is allocated to roadways and bridges, this will only cover 46 percent of the backlog in this area; coverage in other areas will be lower still (Zhang and Batjargal, 2022: 4). Reflecting finance capital’s enduring power, IIJA still relies heavily on mobilising private finance, delighting BlackRock (2022) by extending opportunities for private ownership and PPPs, accompanied by tax breaks and subsidised loans. Due to neoliberal deindustrialisation and associated skills shortages, toughened requirements to use US-sourced construction inputs will radically delay implementation, even with the loopholes IIJA necessarily allows (American Association of State Highway and Transportation Officials (AASHTO), 2022; Tomer et al., 2023). Wider macroeconomic conditions are also unfavourable. High inflation will substantially erode the IIJA’s budget’s purchasing power and is forecast to cause the US construction sector to contract from 2023 to 2026, by 7 percent in 2023 alone (Tomer et al., 2023; Wood, 2023). High interest rates are also suppressing state bond issuances, limiting their capacity to co-finance projects, a requirement to access federal IIJA funds (Tomer et al., 2023). There are also serious doubts about the state’s ability to deliver such large-scale infrastructural programmes after decades of hollowing out of bureaucratic capacity (AASHTO, 2022: 9–10; Durand, 2023). Similar problems implementing the CHIPS Act (see Xu, 2023) underscore that, much like industry itself, state capacities hollowed out under neoliberalism cannot quickly be rebuilt.

Although the extent of structural change in the US political economy will continue to be debated, this is not immediately relevant for our purposes. As the next section shows, although domestic policy may be changing in response to populist challenges, internationally, US (and other Western governments’) infrastructure financing remains firmly aligned with its earlier, failed domestic approach to mobilising private finance.

Internationalising financialisation, failing to compete with China

In moving to compete with China on global infrastructure, Western states are internationalising approaches that have already failed domestically and face even stiffer challenges in the Global South. Their pledges on global infrastructure replicate an approach to development financing that has itself already failed to deliver: the so-called ‘billions to trillions’ (BTT) agenda.

Western states’ schemes to compete with China clearly internationalise their own domestic approach to infrastructure, much as China did with the BRI. They are all based around using small amounts of public money to ‘mobilise’ vastly larger private financial investments into infrastructure in developing countries. As the announcement for B3W put it, for example, to address ‘the $40+ trillion infrastructure need in the developing world’, the G7 will ‘coordinate in mobilizing private-sector capital’, with ‘investments from our respective development finance institutions . . . catalyz[ing] hundreds of billions of dollars of infrastructure investment for low- and middle-income countries’ (White House, 2021). The PGII is likewise based on ‘leveraging private sector investments’, with claims that ‘millions of [public] dollars can mobilize tens or hundreds of millions in further [private] investments and tens or hundreds of millions can mobilize billions’ (White House, 2022). This is why Western pledges feature total commitments of ‘up to x’: they depend entirely upon the uncertain participation of private finance. Whatever changes Western governments are making domestically in response to populist challenges, they are not committing large sums of public money to international projects, because populist pressures do not extend to (indeed, would likely oppose) such disbursements. Nor are many such projects plausibly vital for ‘national security’, the only other claim capable of justifying funding since the neoliberal onslaught. 4

This approach to global development is not new; it merely extends an earlier shift in neoliberal development financing, itself reflecting the scaling up of domestic state dependence on finance capital: the BTT agenda. The idea that development agencies should focus on catalysing private investment in the Global South originated in the early 2000s with the World Bank’s International Financial Corporation (Carroll, 2012). It became global policy in 2015 when the International Monetary Fund (IMF) and all the major multilateral development banks (MDBs) jointly issued their BTT policy framework (African Development Bank (AfDB) et al., 2015; see Mawdsley, 2018). This document recognised that existing flows of official development assistance (ODA) – the external equivalent of domestic public spending – could not possibly finance the 2030 Sustainable Development Goals (SDGs). While ODA had reached US$135bn by 2015, US$1.4tr more was required to implement the SDGs in low- and lower-middle-income countries alone (AfDB et al., 2015: iii; Mawdsley, 2018: 192). Just as taxing wealth to facilitate domestic spending has become increasingly unthinkable under neoliberalism, so there was little prospect of ODA filling this gap. However, the MDBs noted ‘large amounts of investable resources, mostly private’, accumulated within the global financial system, particularly among institutional investors, which will control an expected US$147.4tr by 2025 (AfDB et al., 2015: 2; PwC, 2020). To advance the SDGs, therefore, the MDBs hoped that billions of ODA dollars could ‘crowd in’ trillions in private financing: hence ‘billions to trillions’ (AfDB et al., 2015: 2). Noting that private investors are not ‘programmable by – or responsive to – policymaking bodies or conferences’ but are motivated by ‘risk-reward considerations’, public bodies would ‘need either to decrease perceived risk or increase anticipated returns’ so that ‘private business can deliver profit’ (AfDB et al., 2015: 2, 12, 13). The IMF and MDBs’ role should therefore shift to mitigating risks, ‘escorting’ private capital into developing countries.

This approach – which clearly scales up approaches developed domestically in neoliberal states like the United States – has delivered even poorer results in developing economies than in developed ones. As Bernards (2023) notes, finance capital has not cooperated with state managers’ efforts to draw it into development projects. International financial institution-escorted private financing actually declined after BTT was launched, from an annual average of US$37bn from 2008 to 2014 to just US$13bn from 2015 to 2017 (Tyson, 2018: 15). By comparison, the OECD estimates annual global infrastructure investment needs at US$6.3tr to meet development requirements, or US$6.9tr if climate goals are included (Mirablie et al., 2017: 15). The estimated ratio of public-to-private dollars required to address global infrastructure needs is between 1:4 and 1:6, but the average rate has been 1:0.7 (Tyson, 2018: 15). Institutional investors have shown virtually no interest, accounting for just 0.67 percent of all private participation by 2018 (Griffiths and Romero, 2018: 13). Declining private investment under BTT reflects the pro-cyclical nature of market-based financing and the dominance of international investors’ interests. From 2008 to 2014, central banks’ quantitative easing encouraged substantial flows to developing countries, including unusually high private infrastructure investment, but as monetary policy tightened, investors turned away from Southern economies (Tyson, 2018: 12).

The BTT approach has failed because ‘de-risking’ private infrastructure investment is even more challenging in the Global South than in the Global North. Without denying comparable problems in the North, on average, all the aforementioned pre- and post-completion risks are heightened in developing countries (Arun, 2023). States’ capacity to assess projects’ feasibility is weaker. Confused legal regimes and socio-political conflict can plague land acquisition. ESIAs may lack rigour and governments may be disinterested in or unable to afford adequate mitigation. Regulation is often inadequate, cumbersome or corrupted. Socio-political conflict can disrupt planning, construction and operations. Abrupt governmental changes can entail projects being downsized or scrapped. Relatively weak legal protections entail greater risk that governments may renege on revenue agreements or be unable to collect user fees. Currency and interest rate fluctuations can preclude even willing governments servicing their debts. Chinese infrastructure firms and lenders have been willing to engage under such conditions – albeit with extensive mitigations – because their interests entail substantial risk appetite. Western finance capital is far more risk-averse.

Alongside such project-level risks, institutional investors also face portfolio-level disincentives (Arun, 2023). Unlike government bonds or mortgages, infrastructure projects are heterogeneous, making them more illiquid and difficult to bundle and securitise, increasing investors’ risk. Fund managers must also meet profitability or earning quality thresholds, typically set independently of economic conditions or the cost of capital, which prevent fund managers from investing even in profitable projects. Furthermore, many fund managers shun assets with low credit ratings. They either do not invest or divest rapidly when countries are downgraded by ratings agencies. Institutional investors’ liability management strategies also tend to make infrastructure investments in the Global South highly speculative. Infrastructure assets, whose value is denominated in local currencies, are placed in funds’ higher risk ‘growth portfolios’, designed to generate quick returns rather than being held to maturity. Investor demand for these assets is therefore volatile and often unrelated to host-country economic conditions. This is amplified by investment firms’ short-termism, encouraged by linking managers’ bonuses to quick returns.

MDBs can only do so much to mitigate these problems. They can focus on specific projects, funding feasibility studies, helping with ESIAs and so on, to try to create ‘bankable’ prospectuses. But the wider socio-political context – which inevitably conditions investors’ risk assessments – will remain challenging, while portfolio-level constraints remain untouched. This is why the BTT agenda doubles down on promoting pro-market governance reforms in developing countries (AfDB et al., 2015). This includes traditional regulatory reforms but also developing local bond and securities markets to encourage foreign involvement (Gabor, 2021). But this working ‘on, through and around the state’ to promote neoliberal development has been attempted for decades (Carroll, 2012), and progress has been slow. This is because, as Gramscians would expect, reforms remain conditioned by socio-political struggles for power and resources, with dominant groups resisting changes contrary to their interests.

Furthermore, ‘de-risking’ is really a misnomer; the bulk of risk can only be shifted, not eliminated. What MDBs really mean is that risk should be shifted from private investors to host-states. As in the North, this entails structuring projects to guarantee revenue streams for investors and/or developing financial instruments that either provide a guaranteed return regardless of the project’s fate (bonds) or are sufficiently liquid to allow investors to divest quickly if things turn sour (securities) (Gabor, 2021: 446). However, many projects are not amenable to such engineering, many governments are leery of making or cannot afford such commitments and local capital markets are insufficiently developed. The countries best able to reduce infrastructure investors’ risk are typically larger, middle-income countries in Asia and Latin America – those already receiving most private investment (Arun, 2023).

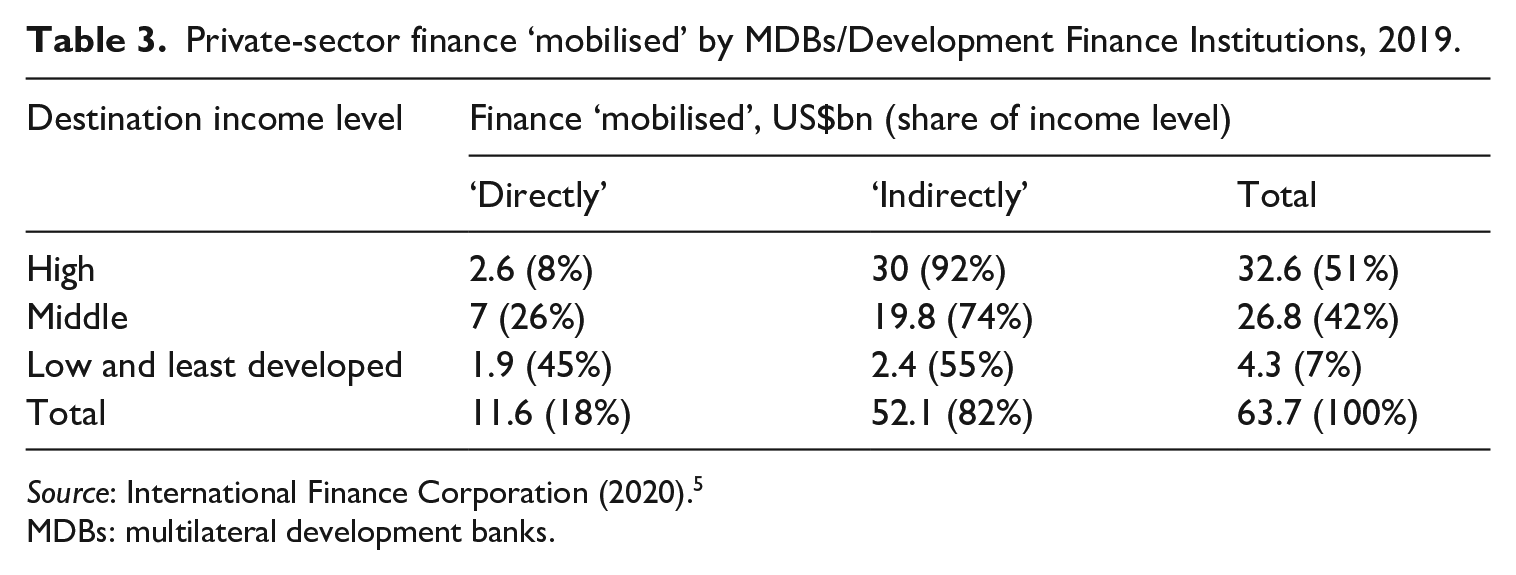

This explains why the limited private investment that exists in developing-country infrastructure is concentrated, as in the North, in lower-risk territories and in sectors where revenue streams can be guaranteed. In 2019, the latest year on record, 27 MDBs and development finance institutions claim to have ‘mobilised’ US$62bn of private finance into infrastructure (see Table 3). This is obviously grossly inadequate given the scale of need. Moreover, investment was heavily skewed towards richer, lower-risk countries, with just 7 percent flowing to the low/least-developed countries that should notionally be a key battleground for influence with China. Furthermore, even these achievements are questionable. The MDBs’ figures include not only the small minority of sums ‘directly’ mobilised as ‘a result of [their] “active and direct” involvement’, where ‘causality is much clearer’, but also ‘the remainder of private financing’ flowing to projects, all of which is ‘attributed’ to MDB involvement in ‘project design, de-risking and initial financing’, despite the ‘less concrete’ causality (International Finance Corporation (IFC), 2020: 12). MDBs are thus almost certainly claiming excessive credit for ‘mobilising’ funds. Moreover, the poorer (and hence riskier) the territory, the greater the share of ‘direct’ mobilisation – that is, the MDBs must work far harder to actively assemble consortia, rather than simply committing small sums that ‘crowd in’ eager investors.

Private-sector finance ‘mobilised’ by MDBs/Development Finance Institutions, 2019.

MDBs: multilateral development banks.

As in the United States, private financing has also been concentrated in sectors where user fees can generate profitable revenue flows: energy (37% from 2008 to 2017) and information and communication technology (30%); conversely, vital infrastructures like water, sanitation and roads have been neglected (Tyson, 2018: 12). This is reflected in the US DFC’s own disbursements, which rarely compete directly with Chinese-style megaprojects but concentrate on energy and finance (predominantly microfinance), where steady revenue flows can be secured (Roberts and Schaefer, 2021). Indeed, the small supply of ‘bankable’ projects means that Northern financers have mainly been competing with one another, not with Beijing, in a ‘zero-sum’ game with few new opportunities (Tyson, 2018: 25).

An example of such dynamics is provided by Klagge and Nweke-Eze’s (2020) case study of two renewable energy projects in Kenya: the €623m Lake Turkana Wind Park (LTWP) and the US$518.1m Menengai Geothermal Project (MGP). MGP was riskier, given high costs and risks associated with exploration for suitable steam drilling sites, and higher up-front capital costs. Unsurprisingly, private investors were disinterested. Financing was provided by the Kenyan state (55% equity stake) and a consortium of MDBs and development finance institutions (42% loans and 3% grants). Private firms did take a modest equity stake in LTWP (€85.5m, 68% of the total €125m equity), but they were all project developers, equipment suppliers or geographical information firms – not financial institutions. Again, MDBs and development finance institutions had to provide the remainder of the equity and almost all the €498m debt financing, with just €6m provided by a boutique private investor. This was despite enormous ‘de-risking’, including a power purchase agreement from the Kenyan state that guaranteed revenue flows and government financing for a 400 km-plus transmission line to connect LTWP to the national grid. Klagge and Nweke-Eze (2020: 76, 62) conclude that, although the MDBs/DFIs pursued de-risking to ‘serve the interests of private firms’, there was ‘no evidence’ that they had successfully converted developing-country infrastructure ‘into assets available for speculative investment’, with the ‘complex risk structure’ deterring most ‘private and especially institutional investor participation’.

Risk aversion also explains investors’ preferences for MDB bonds over direct involvement in infrastructure projects. Kenny and Morris (2022) argue that the United States should work through the World Bank rather than competing directly with Chinese infrastructure-financing because the Bank ‘leverages as much as $46 of private-sector backed financing for each dollar of public funding supplied by governments’. Morris (July 13, 2022, personal communication) clarifies that this multiplier relates to the World Bank’s ‘overall capital’ relative to ‘shareholder-provided capital and the [Bank’s] bond market borrowing’ and not ‘project-level private capital participation’. Risk-averse institutional investors prefer highly rated bonds, especially those issued by developed countries, despite relatively low yields (Griffiths and Romero, 2018: 13). World Bank bonds are similar. They offer a guaranteed return and low risk because the Bank is governed according to pro-business principles, making its lending profit-oriented and cautious, its borrowers rarely (if ever) default and it is ultimately backstopped by Northern governments. Therefore, although MDBs’ bond sales can raise funds to invest in infrastructure, private investors avoid direct risk-taking, and MDBs’ own investments will remain cautious, to guarantee repayment and continue servicing their own creditors.

In sum, although Western international infrastructure financing initiatives has been shaped by finance capital’s interests and worldviews, investors are disinterested, leaving their plans in disarray. With central banks’ interest rates likely to remain high for years to come, private investors’ interest in developing countries’ infrastructure will likely decline even further.

Conclusion

Although Western states have boldly proclaimed that they would compete with China’s BRI on global infrastructure financing, implementation has been underwhelming. Existing IR/IPE frameworks would struggle to explain this discrepancy because they would see international development financing as an instrument of economic statecraft, which governments deploy to pursue their geopolitical agendas. Conversely, we have argued, international ‘geo-economic’ competition is profoundly shaped by states’ political economy foundations. China’s BRI was a spatio-temporal fix to a serious challenge to the powerful cadre-capitalist class, stemming from contradictions within China’s growth model. It internationalised China’s domestic development model, involving large-scale investment in fixed assets financed by loans from state-owned banks and delivered by SOEs. This has often generated in recipient countries the same problems of excess capacity and bad loans plaguing China. In the United States, policymakers’ desire to compete with China for geostrategic reasons is not backed by supportive interests in industry or finance. After decades of under-investment in domestic infrastructure and deindustrialisation, no excess capacities exist to be exported. The US state has been reoriented around finance capitalists’ interests. Domestic infrastructure programmes aim to serve these interests, seeking to ‘crowd in’ private investment with various incentives. But private investors only engage in limited areas where profit flows can be guaranteed. Although it is being revised domestically in response to populist challenges, this failed approach has already been globalised and remains the dominant Western policy tool. Facing even greater challenges in Southern contexts, it has failed internationally, too. Although Western efforts to compete with China on global infrastructure remain in their infancy, given these structural weaknesses, we can reasonably expect them to continue failing in the future.

Our study has several implications for further research and practice. We have argued that existing theories of ‘geoeconomic’ behaviour cannot explain our empirical puzzle, but Gramscian state theory can. However, an explicit Gramscian theory of ‘geoeconomics’ itself remains to be developed. Further research could also explore why policymakers persist with – indeed, double-down on – flawed policies like PPPs and BTT. Gramscian theory provides a hypothesis: reflecting the balance of social power and the attendant ideology of neoliberalism, ‘there is no alternative’. It is simply unthinkable to tax wealth and profits to develop state capacities that could be authoritatively directed for political ends. This taboo is only just beginning to soften in the United States, and arguably only because centrist state managers and their supporters see it as essential to contain populism, and because the dollar’s ‘exorbitant privilege’ permits vast fiscal expenditure without taxing wealth and profits. Other states have no such luxury, and even the United States shows no sign of deploying significant fiscal resources internationally. BTT remains the dominant model, used across an increasing range of policy domains, from Ukrainian reconstruction to promoting ‘just’ energy transition and climate adaptation in the Global South. Given the structural constraints at work, it seems policymakers cannot even recognise openly BTT’s failure, let alone devise alternatives. For anyone seriously interested in addressing the problems to which BTT is proposed as a solution, rather than hollow geopolitical posturing, this is a tremendous political challenge.

Finally, our argument demonstrates what Marxists have long argued: that conflict and competition between states are not predetermined by the international states-system; it is powerfully shaped by the evolving, contradictory capitalist social relations within which that system is embedded. Western states are trying to compete on global infrastructure not because they have any strategic advantage in this area, but because China initiated the BRI – largely to address its own economic contradictions – prompting panicked Western state managers to compete on this terrain. The idea that states with crumbling domestic infrastructure and hollowed-out industries could do so successfully is scarcely ‘realistic’. At a minimum, Western state managers must be more selective about whether, where and how to compete with China. Rather than vainly pushing them to reject Chinese engagement wholesale in favour of an ephemeral alternative, Western efforts may be better spent in helping developing countries’ governments, political elites, civil society and media to better understand, evaluate and manage it. More broadly, Western state managers should recognise and reflect upon the limitations arising from decades of neoliberal ‘statecraft’, which is responsible both for the economic rise of China and for their own states’ miserable debilitation.

Footnotes

Acknowledgements

The authors would like to thank Tom Chodor, Kanishka Jayasuriya, Adam Morton and Jason Sharman for their comments on earlier versions of this paper, though responsibility for the final output remains solely with the authors. They are also grateful to Monica DiLeo and Chang Shin for excellent research assistance. For their many helpful comments, they also thank the journal’s reviewers and colleagues at events where earlier versions of this paper were presented: Humboldt University of Berlin (November 2022), the Political Studies Association’s British and Comparative Political Economy specialist group (December 2022), the Australian International Political Economy Network (February 2023), the annual convention of the International Studies Association (March 2023), the Oceanic Conference on International Studies (July 2023), the European Workshop on International Studies (July 2023) and the Griffith Asia Institute (August 2023).

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: Research for this article was supported by Australian Research Council Future Fellowship FT200100613, The Politics of Development Financing Competition in Asia and the Pacific.