Abstract

I examine whether union membership affects individual foreign direct investment (FDI) preferences in ways that vary across investors’ country of origin. I argue that the country of FDI origin will bear upon how union members assess FDI, because it provides cues about what the economic prospects of (unionized) workers will look like under different foreign investors. I argue that the salient attribute of foreign investors is whether they originate from a country that is an important form of patient or impatient capital. Compared with non-members, members will be more supportive of FDI from countries embodying patient than impatient capital. Specifically, I expect the (positive) gap in support between FDI from patient and FDI from impatient capital countries to increase with union membership. Conversely, I expect the (positive) gap in support between FDI from impatient versus patient capital countries to decrease with membership. Evidence from original Swiss survey data corroborates my argument. Respondents were asked to evaluate FDI from China and Europe (entities embodying patient capital) and from the United States (a country embodying impatient capital). The results show that the gap in enthusiasm for European FDI versus American FDI increases with union membership, while the gap in enthusiasm for American FDI versus Chinese FDI decreases with membership. Complementary qualitative analysis of reports, documents, and testimonies by trade unions in continental Europe show that their views are in sync with those of their members, suggesting that unions shape their members’ FDI preferences. The findings have important implications for the politics of backlash against economic globalization.

Keywords

Introduction

Rising protectionism (e.g. export controls on advanced technologies; “friend-shoring” of supply chains) and the crisis of multilateral economic governance (e.g. the demise of the World Trade Organization dispute settlement system) amidst the resurgence of great power rivalry and geoeconomic competition have put the postwar liberal international order under tremendous strain. The full integration of China into the world economy after 2000 was a major shock and a catalyst for the long-run erosion in support for liberal trade and capital mobility in advanced economies (Broz et al., 2021). One manifestation of the current backlash against globalization is the expansion of governments’ investment screening policies (Bauerle Danzman and Meunier, 2023). Recent scholarship has linked new investment restrictions to the rise and politicization of Chinese foreign direct investment (FDI), suggesting that policymakers have used rationales related to national security and strategic concerns to justify these developments (Bauerle Danzman and Meunier, 2023; Chan and Meunier, 2022; Tingley et al., 2015).

As restricting Chinese investment entails costs, I am interested in whether political opposition to the backlash against Chinese FDI might be motivated by the material interests of the losers of such backlash. I focus on the political demand of the politics of Chinese versus other foreign investment by analyzing individual and group preferences of one major stakeholder in decision-making, namely, trade unions. The interests of unions and their members lie with bread-and-butter issues like jobs and working conditions and, I shall argue, dovetail with investment coming from countries characterized by state capitalism like China. Consequently, I ask whether dispositions of trade unions and rank-and-file members toward Chinese FDI mitigate negative sentiments related to ideational concerns (nationalism, national security, etc.) and therefore constitute, against the growing share of Chinese FDI in total FDI, a crucial pillar behind the societal acceptance of pro-inward FDI policies.

The literature offers conflicting expectations and evidence regarding the preferences of labor unions over generic inward FDI flows and policy (Owen, 2013, 2015; Pinto, 2013). The inconclusive results may be due to unions having heterogeneous FDI preferences. However, little is known about how unions assess various types and sources of inward FDI. As groups organized around the shared economic interests of their members, unions hold views on policies depending on whether they are economically harmful or beneficial to their members. Following an inductive, yet theoretically informed logic of research, I argue that the salient attribute of foreign investors that will influence unions’ FDI preferences is whether investors’ country of origin is an important form of patient or impatient capital. Patient capitalists are unresponsive to short-term market pressures to increase profitability and instead seek to capture benefits specific to long-term investments (Deeg and Hardie, 2016). Long-term investment strategies reduce economic insecurity associated with FDI. In short, patient (impatient) capital is in harmony with (inimical to) worker interests (Engelen et al., 2008; Hall and Soskice, 2001; see also Goyer, 2006).

Regarding mass attitudes, research has called into question that material self-interest explains individuals’ foreign economic policy preferences (Hainmueller and Hiscox, 2006; Jensen and Lindstädt, 2013; Mansfield and Mutz, 2009; Rho and Tomz, 2017). Many citizens have difficulties understanding the distributional consequences of trade, not to speak of the economic impact of FDI whose distributive implications are even more complex to grasp. In the absence of knowledge on the distributional effects of foreign economic policy, individuals are prone to take their cues from intermediate organizations to which they belong (Fordham and Kleinberg, 2012; Kim and Margalit, 2017). I argue that union members will be influenced by their organizations in how they think about FDI from different countries. For members, the nationality of investors will act as an information shortcut for varying distributive effects related to capital’s country of origin.

Individuals prefer FDI from culturally similar than from culturally dissimilar countries (Jensen and Lindstädt, 2013). Union members are unlikely to be entirely immune from holding such preferences. However, members will be more supportive of patient than impatient foreign capital relative to non-members. Consequently, I expect the gap in support between FDI from culturally similar and patient capital countries and FDI from culturally remote and impatient capital countries to increase with union membership. Similarly, the gap in support between FDI from culturally similar and impatient capital countries and FDI from culturally remote and patient capital countries will decrease with union membership.

Within the confines of observational studies, a major challenge to investigate individual preferences over inward FDI has been data related. National and cross-national surveys typically do not include questions that would allow for a systematic study of whether union membership affects attitudes toward FDI from a variety of countries or regions. I address this limitation by using original survey data from Switzerland. Responding to a call for proposals, I was able to design my own topical module on Swiss foreign economic relations, which was embedded in a nationally representative survey (Ernst Stähli et al., 2015). The data allow an analysis of the effect of union membership on individual support for inward FDI from major investing partners (China, Europe, and the United States (US)) that vary in the type of political economy (patient vs impatient forms of capitalism) and in cultural proximity vis-a-vis Switzerland while controlling for prominent alternative explanations.

I find robust evidence in support of my argument. Union membership does not have an unconditional statistically significant influence on Swiss individuals’ attitudes toward generic FDI. However, the impact of membership is conditional on whether the country/region of FDI origin is an important form of patient capitalism. When investors are culturally (relatively) similar but embody impatient capital, such as American investors, union membership tends to reduce support for FDI. Put differently, the support for American FDI tends to be lower among members than non-members. By contrast, when FDI embodies patient capital, irrespective of the investor’s cultural similarity or dissimilarity, as in the cases of European and Chinese investments, union membership increases support for FDI. That is, the levels of support for European FDI and Chinese FDI are higher among members than non-members. In all, I find that the gap in support for European versus American FDI is larger for members than non-members, while the gap in support for American versus Chinese FDI is smaller for members than non-members. Note that in these data, union members still have slightly more positive attitudes toward American than Chinese investment; it is merely the enthusiasm gap between the two that is smaller for members than non-members.

While the main construct of interest (patient/impatient capitalism) is not identified directly but only via variation in the home country of investors in the statistical analysis, I examine the causal mechanism—the role of unions in shaping members’ preferences—by other means. First, based on desk research, interviews with labor leaders, and analysis of union publications, I document for several continental European countries, particularly Germany and Switzerland, that unions differentiate between countries that embody patient capital models of investment (China, Europe) and those that do not (US). Moreover, I show that they provide information to their members on how to think about FDI from different countries. Second, the quantitative analysis explores alternative mechanisms related to individuals’ knowledge and employment experiences. None of the tests is conclusive.

This paper makes several contributions. First, to my knowledge, it is the first study on the impact of union membership on individual FDI preferences. Second, it is among the first studies to document how unions think about different types of FDI and how they influence their members’ FDI preferences, adding to the literature on unions’ role in educating their members’ preferences over economic policies (Ahlquist et al., 2014; Kim and Margalit, 2017; Mosimann and Pontusson, 2017). Overall, I identify consistent individual and group FDI preferences for a major interest group in advanced democracies, preferences that reflect notions of patient versus impatient capital and yield counterintuitive findings regarding the attitudes of unions and their members toward Chinese FDI and American FDI.

Third, the study speaks of debates about whether foreign economic policy preferences are egocentric (Hainmueller and Hiscox, 2006; Jensen and Lindstädt, 2013; Mansfield and Mutz, 2009; Rho and Tomz, 2017). The literature has focused on a narrow understanding of economic interest as self-interest, ignoring that group economic interests may influence attitudes (Fordham and Kleinberg, 2012). I show that material interests play a significant role in shaping FDI attitudes. Finally, the focus on egocentric economic interests helps to understand the drivers (and moderators) of the backlashes against Chinese acquisitions and economic globalization. Unions and their members moderate negative sentiments related to ideational concerns toward Chinese FDI, thereby helping to shore up pro-inward FDI policies. Meanwhile, their skepticism toward impatient capitalists makes them one of the staunchest critics of financial globalization.

Literature review

A modest literature has investigated the relationship between unions and FDI inflows or regulation. The theoretical expectations and the evidence are mixed. On one hand, in line with the idea that FDI reduces the power of workers and their representatives, Owen (2013) found a positive association between levels of unionization and restrictions on FDI inflows in an analysis of American industries over the period 1981–2000 (see also Owen, 2015). On the other hand, consistent with the view that FDI increases employment and wages, Pinto (2013) finds that pro-labor, left-leaning governments correlate with FDI inflows. In short, unions are likely to be ambivalent regarding the desirability of generic inward FDI. As a matter of fact, the international and comparative political economy literatures have largely neglected how unions perceive inward FDI and how perceptions may differ across the country of FDI origin. 1

Although these studies do not address individual FDI preferences directly, their findings suggest that the effect of union membership (positive or negative) on attitudes toward generic FDI might not be significantly different from zero. The literature on individual FDI preferences formation has ignored how membership influences attitudes toward inward FDI and how it may condition attitudes toward FDI across capital’s country of origin. Moreover, the cumulative evidence from this literature lends stronger support to nonmaterial rather than material explanations.

Building on the notion that individuals have little knowledge on the distributional effects of trade (Rho and Tomz, 2017) and a fortiori of FDI, Jensen and Lindstädt (2013) argue that individuals rely on heuristics to form preferences on FDI. Specifically, individuals will use non-economic contextual frames, in particular who the foreign investors are, to evaluate FDI. The cognitive frames tap into out-group differences and stereotypes. The upshot is that individuals will prefer FDI from countries that are culturally similar over FDI from countries that are culturally dissimilar. Drawing on survey experiments, Jensen and Lindstädt (2013) show that American and British citizens are more likely to say that German FDI is good for their respective countries compared with Saudi Arabia FDI, while American individuals are less likely to support Chinese FDI compared with generic FDI. Similarly, Feng et al. (2021) show that nationalist sentiment breeds skepticism of foreign and especially Chinese investment in the US. Focusing on the identity of the other country, Li and Zeng (2017) demonstrate that Chinese individuals are less supportive of FDI from Asian countries with which China has contentious political relations than FDI from other regions (for a similar argument related to a country being a security threat, see Chilton et al., 2020).

Turning to ideology/ideas, Pandya (2010) finds limited support for a correlation between right-leaning individuals and pro-FDI attitudes, while Chilton et al. (2020) show, using survey experiments in the US and China, that concerns about whether a country allows reciprocal investments, which reflects a sense of fairness, influence individual attitudes toward FDI (see also Jensen and Lindstädt, 2013).

Some accounts combine sociodemographic and ideational factors. Linsi (2022) shows that older British individuals, who grew up when the dominant public discourse toward foreign mergers & acquisitions (M&As) was “economic statism,” are hostile to foreign M&As, while younger individuals socialized in the neoliberal era are not. For a sample of developing countries, Lee and Shin (2020) argue and show that women are more likely to support inward FDI than men (or at least not less likely to do so), because multinational firms help diffuse norms about gender equality and women disproportionately benefit from service sector growth associated with FDI inflows.

Focusing on individuals’ economic interests, Pandya (2010) shows that skill level is associated with support for incoming FDI in 18 Latin American countries. Regarding job insecurity, an alternate channel of FDI’s income effects, the author finds some evidence for a negative correlation with the probability of a pro-FDI stance. Similarly, Jensen and Lindstädt (2013) show that priming respondents with a picture of a foreign investment that creates employment increases support for FDI. Based on experimental evidence from China, Li and Zeng (2017) find, contrary to economic theory, that low-skilled individuals do not prefer low-skilled, labor-intensive FDI over skill- or technology-intensive FDI while corroborating the influence of FDI projects’ impact on the local labor market on preference formation. Regarding economic contextual factors, Feng et al. (2021) find that the gap in support for generic business investment and Chinese/foreign business investment increases with local trade-related job losses (and that this relationship is further conditioned by nationalist sentiment).

Triggered by the sharp increase of Chinese outbound FDI in recent years, one strand of research has focused on the dispositions of political and economic elites toward Chinese FDI inflows (Raess, 2021; Tingley et al., 2015). However, little is known about how individual respondent characteristics affect attitudes toward Chinese inward FDI, and how it might vary across capital’s country of origin. An exception is Feng et al. (2021), even though that study does not compare attitudes toward FDI from different countries. In addition, many studies sample American citizens, which by definition precludes analysis of public attitudes toward American FDI and comparative analysis of attitudes toward Chinese and American investments. This is an important limitation as the US is the single largest foreign investing country and has a distinctive political economy (Hall and Soskice, 2001).

The argument

It consists of three steps in a causal chain. First, unions’ FDI views reflect their experiences with and considerations about the distributive consequences of different types of FDI. One of the main prisms through which unions assess the distributive effects is whether foreign investors are patient capitalists with a long-term horizon or impatient capitalists with a short-term horizon. Patient forms of capital align with worker interests and are preferred by unions. The nationality of foreign investors captures something deeper than cultural similarity, namely, whether foreign investor/capitalism in the country of FDI origin is a form of patient versus impatient capital.

Second, unions, as intermediate organizations organized around the shared economic interests of their members, shape their members’ preferences (Fordham and Kleinberg, 2012). The main channels of influence include the dissemination of information (e.g. facts, opinions) via general or internal communication (e.g. members’ magazines, direct mailings), meetings, mobilization drives and political campaigns. These activities allow unions to regularly communicate with rank-and-file members about the political–economic issues of the day (Ahlquist et al., 2014; Iversen and Soskice, 2015; Kim and Margalit, 2017). The information they distill is “likely to be biased in favor of the interests they represent,” and, accordingly, members “may come to hold specific attitudes about policies that are perceived as harmful (or beneficial) to the group” (Fordham and Kleinberg, 2012: 322).

Third, members view unions as the custodian of their economic interests and thus as a reliable source of information. They will turn to unions for cues on how to think about politics (Iversen and Soskice, 2015). The information will make members more sophisticated in their political choices in the sense that they become more aware of their (own group’s) material interests. The upshot is that members will take their cues on how to think about FDI from unions.

Individuals have difficulties in understanding their own egocentric policy preferences (Hainmueller and Hiscox, 2006; Rho and Tomz, 2017). Following Jensen and Lindstädt (2013), I expect cultural proximity among countries to influence individuals’ FDI preferences. Specifically, I expect the level of FDI support among Swiss individuals to be highest for European FDI, intermediate for American FDI, and lowest for Chinese FDI. Such rank order of preferences should hold not only for non-members, but also potentially for members as they tend to be less aware of their material interests than their leaders. Regardless, the argument focuses on the gap in support for FDI from different countries of origin between non-members and members, with the latter holding more sophisticated preferences than the former.

While the next subsection introduces the building block of the theory, the following two examine the stance of trade unions and the process by which they “educate” their members’ preferences, respectively. The qualitative analysis of union views and activities is based on desk research, analysis of publications by unions, and interviews with a dozen labor leaders conducted between 2012 and 2022 in four European countries. Section “Conclusion” presents the quantitative evidence on the effect of union membership.

Capitalism in the country of FDI origin as a form of patient versus impatient capital

I argue that whether capitalism in the investing firm’s country of origin is an important form of patient capital will condition the union’s enthusiasm for inward FDI. This feature of the investor’s political–economic system is likely to mitigate economic insecurities associated with FDI (Scheve and Slaughter, 2004). By contrast, impatient capitalists are likely to be the source of or exacerbate the (fears of) negative effects of inward FDI on jobs, job security, and working conditions. The patient versus impatient capital categories should influence how unions view FDI because they are primarily concerned about FDI’s income (i.e. labor market) effects. All else being equal, I expect unions to be more supportive of long-term than short-term investment projects and of FDI stemming from countries characterized by patient rather than impatient capital.

Patient capitalists operate with a long-term horizon that dovetails with workers’ interests (Hall and Soskice, 2001). In patient capital models of investment, capital is not tied to short-term stock market valuations. Patient investors are willing and able to forego an immediate return on investment in anticipation of more substantial gains in the future. In firms infused by patient capital, short-term profitability is not the main let alone the sole benchmark determining corporate strategies and decisions. By contrast, in impatient models of investment, firms use financial instruments that tie them to quarterly earnings reports. The short-term horizon of impatient private capital implies that (offshore) outsourcing or firm restructuring and related job shedding are the default corporate response to short-term slumps in revenue or capital market pressures to outperform short-term industry benchmarks. In short, investors’ long-time (short-time) horizon moderates (reinforces) actual or perceived economic insecurities and job losses associated with FDI (Pendleton, 2019; Scheve and Slaughter, 2004).

The traditional form of patient capital, long dominant in coordinated market economies (CMEs), is linked to the “insider” system of corporate governance in which firms enjoy cooperative and close relationships with investors. In its heyday, the provision of patient capital was made possible through a combination of long-term capital through bank loans and cross-shareholdings among large firms. Bank lending, with or without extensive state involvement in the allocation of credit by financial institutions as in France and Germany, respectively, played a crucial role in the supply of patient capital (Zysman, 1983). This system of corporate finance is aligned with the “stakeholder model” of corporate governance, which provides voice to shareholders, banks, suppliers, and employees. The interests of the various stakeholders are to be balanced against each other in corporate decision-making (Vitols, 2001). CMEs, and thus patient forms of capitalism, are dominant across continental Europe (Hall and Soskice, 2001).

The emergence of state-owned capital is the latest manifestation of patient capital in the global economy. China’s state-led capitalism is a case in point (Kaplan, 2016, 2021). Through various entities within the Party and the state, the Party–state retains control of a large swath of the economy (aerospace, aviation, chemicals, energy, metals, minerals, nuclear, petroleum, power, railway, steel, shipbuilding, telecommunications, etc.) as well as the largest banks and thereby the allocation of financial resources (Wu, 2016). Consequently, Chinese firms, particularly state-owned enterprises (SOEs), operate with a long-term horizon. Just like state-owned creditors “are backed by their governments’ implicit guarantee of their loan portfolios, should their debtors encounter financial distress” (Kaplan, 2016: 649), SOEs can endure short-term losses due to state backing of their investment portfolios. The bulk of Chinese outward FDI is carried out by SOEs, 2 and in the case of transactions conducted by private investors, doubts often persist about the actual links to the Chinese government, as in the case of Huawei (Meunier, 2019). It should be noted that the internationalization of Chinese firms has followed a political logic: it was given initial impetus by the adoption of the government’s “go out” strategy at the turn of the millennium, and was reinforced with the launches of the “One Belt, One Road” policy in 2013 and the Made in China 2025 industrial policy in 2015.

Investors originating in liberal market economies (LMEs), such as the United Kingdom and the US, are considered to be impatient capitalists harboring a short-time horizon (Hall and Soskice, 2001). The dominant form of corporate financing is market-based through capital-raising on stock markets. LMEs are characterized by the “shareholder model” of corporate governance, in which the maximization of shareholder value is the firm’s primary goal. Firms are under the pressure of capital markets to produce above-average quarterly results to maintain high stock market valuation. Accordingly, workers’ interests take a backseat, being secondary to shareholder’s interests. Goyer (2006) shows how one type of impatient capitalists, hedge, and mutual funds primarily from Anglo-Saxon countries, invest in undervalued continental European firms, restructure the acquired firms to maximize assets under their management, a process that often involves labor shedding.

Trade unions’ views on inward FDI

How do union officials evaluate the quality of different types of FDI? First, unions tend to have a slightly more positive view of greenfield investments than M&As. Greenfield investments create jobs and unions typically seek out to establish social dialogue at the new plant to fix working conditions. However, building social partnership from scratch may be challenging, as the Huawei case in Germany shows. By contrast, M&As spark fears of job losses and worsening working conditions. A Swiss union leader told me that the former occurred mainly ex ante, using the metaphor of the bridge that is being made beautiful for the wedding, while the latter occurred ex post, when investors ask themselves whether to maintain existing working arrangements. That said, established union structures pre-M&A can facilitate continuity post-M&A.

Second, unions tend to prefer FDI by multinational companies (MNCs (greenfield and M&A)) over private equity (portfolio investment) because they readily associate the former with long-time horizons by investors and the latter with short-termism. In other words, private equity is impatient/financial, whereas FDI is patient/production. Private equity firms with long-term investment perspectives are welcome. Scholars suggest that unions in continental Europe express deep concerns about private equity and hedge funds (Engelen et al., 2008; see also Thatcher and Vlandas, 2016). During the 2005 national election campaign, Franz Müntefering, the Chairman of the Social Democratic Party, likened private equity firms and hedge funds to swarms of locusts sucking out firms and laying off employees, triggering the so-called locust debate (Heuschrecken-Debatte). At the time, the metalworking union IG Metall gave the title “US firms in Germany—The suctioners” to the May issue of its member magazine metall. 3 Note the slippage from short-term financial investors (Münterfering) to American firms (IG Metall), creating a link between the two and thereby blurring the line between American private equity and FDI.

Third, the patient/impatient dichotomy does not perfectly overlap with the motivation for investment: production or financial. Arguably, a new source of patient capital is overseas state equity purchases by Sovereign Wealth Funds (SWF) (Thatcher and Vlandas, 2016), which fits the patient/financial category. Prior to the financial crisis, German unions and international service unions such as UNI Global Union took a rather critical stance toward SWF investment, bundling together SWF, hedge funds, and private equity firms (Schäfer and Bläschke, 2009). It cannot be excluded that unions’ positions toward SWF subsequently evolved toward a more positive stance, in line with shifts in positions of major societal groups and policymakers in the post-crisis period (Thatcher and Vlandas, 2016).

Finally, union leaders I talked to claim that their attitudes toward FDI (or for portfolio investment, for that matter) do not depend on the capital’s country of origin. In other words, long (short) term investment is good (dangerous) in general, irrespective of whether investors come from China, the US, or elsewhere. Nonetheless, unions make experiences with investors from various nationalities, and they talk and think about the nationality of investors. What do they say?

German unions have actively responded to the surge of Chinese FDI, including by analyzing and writing about their experiences. IG Metall begun monitoring Chinese investment in the metal industry in 2012. Wolfgang Müller, then senior union official at the Bavaria office in Munich, coordinated a bottom-up process that led to the creation of a network of works councilors and union officials at Chinese invested firms. The goals are to foster dialogue and understanding through the sharing of experiences, coordinate actions, and enhance monitoring capacity. The network meets for a yearly workshop and runs a WhatsApp group.

Building on interviews conducted within the network, Müller (2017) published a study on the effect of Chinese FDI on industrial relations and economic development in 42 acquired firms with 150 or more employees, predominantly in the machine tools, automotive, logistics and service sectors. The findings are as follows: (1) works councils and collective bargaining arrangements were unaffected; (2) job loses did not occur; instead, there was employment growth; and (3) while know-how transfer to China occurred, production and R&D activities in the acquired firms expanded. According to the worker reps, the motivation for the investment is the acquisition of strategic assets, such as German know-how and quality, including scientific and practical knowledge embedded in skilled workers, managerial competence and production processes. Moreover, they view Chinese investors as taking a long-term interest in maintaining the German production location with its specific functions. When acquired firms face economic hardship, Chinese investors take a long-term perspective, typically continuing to invest in order to increase market share, as opposed to axing jobs to return to profitability.

Both Chinese SOEs and private firms are found to behave as patient capitalists (Müller, 2017: 19). However, the former epitomize patient capital as they pursue particularly sustainable investment strategies, especially with regard to job retention (Müller, 2017: 23). Chinese investors are favorably compared with financial investors: “The overall picture of the operational reality in Chinese-invested companies . . . is surprising—both in view of the widespread reservations especially against Chinese investments and because of the often negative experiences with company takeovers by financial investors” (Müller, 2017: 22). Importantly, worker reps see Chinese investors as patient capitalists: they stressed the long-term horizon of Chinese investors (Müller, 2017: 20) and “pointed out several times that the patience of Chinese investors was atypical” (Müller, 2017: 22). The conclusion is that “most worker representatives surveyed have therefore evaluated Chinese investors positively so far—especially in comparison to their experiences with other investors” (Müller, 2017: 22).

A similar study in Austria based on an analysis of nine Chinese acquisitions corroborates the key findings of the German study (Adam and Eichmann, 2018). Moreover, the entry of Chinese firms was rated positively by all the stakeholders surveyed, including seven employee reps and two managers. In all cases, Chinese investors were seen as being in the business for the long haul.

What about investors from other countries? Anglo-Saxon, particularly American, investors are often singled out. Based on the experiences of German employee representatives, the following comparison is drawn: “Chinese investments are generally long-term, in contrast to the Anglo-Saxon quarterly approach” (Müller, 2017: 1). And one union rep from the metalworking union to quip: “Better ten Chinese than one American investor!” (cited in Müller, 2017: 10).

My interviews with union officials and works councilors corroborate the above findings regarding Chinese FDI and nuances the perspective on American FDI (for detailed interview information, see Annex 1 in Online Appendix). I interviewed six worker reps in France, Germany and the Netherlands in 2012 to probe their perceptions and practices in relation to Chinese FDI inflows. The findings suggest a surprising endorsement by European labor of Chinese investment. The interviewees expressed no worries concerning social dumping, confident in the unions’ ability to steer Chinese investment in directions that will further the diffusion and deepening of quality jobs for workers. If anything, the risk of hollowing out labor laws and practices is a function of short-term business planning. For the worker reps, the nationality of the investor per se is unimportant; rather, what matters is whether investors have a short versus a long investment time horizon.

The views of three Swiss union officials interviewed between 2018 and 2022 are overall consistent with those expressed by union reps elsewhere in Europe. Chinese investors pursue long-term projects, with investment driven by market- and strategic asset-seeking considerations. Moreover, Chinese firms are compliant with the law, attacks on or hollowing out of collective agreements have not happened. 4 The case of the Syngenta Monthey site of ChemChina in Lower Valais, Syngenta’s largest production site worldwide with 930 employees, is a case in point. The social partnership is dynamic and the latest collective agreement concluded in June 2022 even includes some social advances. 5

According to one interviewee, the Chinese are easier to deal with than the Anglo-American because they pursue long-term strategies while the latter, based on his experience, do not. There are different national cultures, pitting American versus European investors. Americans view workers as a cost factor and do not understand respect for workers’ rights, in line with the shareholder value model. British investors are similar to American investors albeit “not as bad,” while French, Italian and German investors are viewed favorably due to their long-term perspective. For another interviewee, however, American long-term investors, such as family-owned group Huntsman in Monthey, do not behave that differently than other long-term investors (corroborated in a follow-up interview with a German union official).

In sum, the country of FDI origin has a bearing on unions’ FDI preferences only inasmuch as it captures something deeper about the investor, namely, if it embodies patient capital or not. Chinese and European investors are viewed favorably as patient capitalists; (Anglo-) American investors are predominantly seen as impatient capitalists, although perceptions are not unanimously negative. To paraphrase Thatcher and Vlandas (2016), this time applied to unions, the patience and loyalty of capital is more important than its nationality.

Informed preferences?

I submit that union members’ exposure to information about how unions view the labor market effects of FDI will influence their FDI preferences. First, research suggests that unions generate and disseminate information that shapes members’ political attitudes, including ideological self-placement, support for redistribution or international trade (Ahlquist et al., 2014; Iversen and Soskice, 2015; Kim and Margalit, 2017; Mosimann and Pontusson, 2017). Second, these studies dismiss the possibility that selection effects drive members’ attitudes. Given that unionization is strongly shaped by economic and institutional factors related to employment and labor markets (Wallerstein, 1989; Western, 1997), the claim that political ideology or preferences motivate workers to join unions is far-fetched. The most convincing empirical strategy to disentangle treatment from selection effects finds that self-selection into unions accounts at most for a quarter of the union effect (Kim and Margalit, 2017). Finally, given that unions educate their members’ preferences on trade (Ahlquist et al., 2014; Kim and Margalit, 2017), it is plausible that they also do so regarding FDI.

Below, I show that unions provide information to their members on how they think about FDI. While there is nothing secret about the position of unions regarding FDI, the information is not just as available to non-members. Unions tend to convey the information via “private” communication channels reserved to members. When they go public, getting the message out still depends on union structures and therefore the target audience largely remains members.

I analyzed news reports in French and German languages dealing with Chinese FDI over the period 2010–2016 in the member magazines of the largest industrial unions affiliated with the peak associations Schweizerischer Gewerkschaftsbund (SGB) and Travail. Suisse, namely the Work and L’Evénement Syndical publications for Unia and the Syna Magazin and Syna Magazine publications for Syna, respectively. 6 The publication frequencies range from three times a month (L’Evénement Syndical), to monthly (Syna Magazin(e)) or bimonthly (Work). L’Evénement Syndical, for instance, has a circulation of more than 62,000 copies among French-speaking Unia members and sympathizers, allowing a wide dissemination of information related to the professional world, union campaigns in Switzerland and internationally. 7 I opted to focus on news reports, by which I mean a collection of articles on the same topic forming a “dossier,” since a single article is unlikely to focus readers’ attention in the same way as a special report.

Around the time of the data collection for this study, I found two news reports presenting facts and analysis of (the labor market impact of) Chinese FDI (Work, 2013, 2016). 8 The first report has a principal article with the title “The Chinese are here.” It maps about 60 Chinese investments across the country. A second article deals with the acquisition of Swissmetal by Chinese group Baoshida. The overall tone of the report is (moderately) positive. A key message from the first article is that Chinese investors are “deep pocket” investors as China sits on US$3.3 trillion of foreign reserves and seeks to invest a significant share of these reserves in Europe. The second article speaks about the rescue of a firm in a state of near-bankruptcy, the safeguarding of jobs, and the hope for a better future.

The main heading of the second report is “Better the Chinese than locusts.” It asks whether Chinese investors are better than German or American investors and claims to give answers. As the article is written in German and Swiss-German journalists (and people) typically follow the political life in neighboring Germany (just as French-speaking Swiss follow French news), it is not that surprising that reference is made to Germany. First, the title is a clear reference to the locust debate. Second, the report cites the conclusion of a study by the Confederation of German Trade Unions in North Rhine-Westphalia: “The workforces of acquired companies [by Chinese owners] are doing better than workforces with financial investors who are only interested in short-term returns” (Work, 2016: 8). 9 The core message is that Chinese investors are preferable over short-term financial investors (read: American investors). Other articles discuss Chinese takeovers: Swissmetal by Baoshida, mentioning the jobs safeguarded, an uncertain future, and six illegal Chinese workers found at one factory; and Saurer by Jinsheng, emphasizing of continuity in employment relations and playing down potential fears.

In Germany, unions also disseminated information on how they think about FDI. Recall the cover page of IG Metall’s member magazine of May 2005 conveying the unequivocal message both visually and in writing that American firms are looters. The study by Wolfgang Müller (2017) of IG Metall was commissioned by and published on the website of the Hans-Böckler-Stiftung—a foundation dealing with Co-determination and research on work-related issues on behalf of the Confederation of German Trade Unions. 10 While the study was made available to the general public, typical viewers of such websites are unionized workers and union sympathizers.

In short, the specific union views on Chinese and American investments have being quite extensively discussed and relayed within the German and Swiss labor movements, and their members exposed to these views. While the above suggests that unions may well play a role in educating their members’ FDI preferences, I do not wish to imply that the present analysis definitely settles the issue of causality. Coding trade union communication versus basic media analysis would add additional evidence for the claim that the variation in members’ preferences really can be considered to have emanated from different cues given by the unions. Doing so would go beyond the scope of this study.

In conclusion, I argue that unions provide information to members about patient versus impatient capital. Members will be more supportive of patient than impatient foreign capital relative to non-members. Specifically, I expect the gap in enthusiasm for American FDI and Chinese FDI (favor US > China) to decrease with union membership (Hypothesis 1). Similarly, the gap in support of European FDI and American FDI (favor EU > US) will be larger for members (Hypothesis 2).

The effect of union membership on FDI preferences

Study design and data

To test my argument, I use original Swiss survey data. I designed my own topical module titled “Attitudes of Swiss citizens toward China as a source of investment and trade,” which went through a competitive bid process and was accepted for insertion in the Measurement and Observation of Social Attitudes in Switzerland (MOSAiCH) survey in 2015 (Ernst Stähli et al., 2015). Owing to space constraints, only a limited number of questions could be asked and implementing a survey experiment was not an option. While this survey data presents the advantage of being based on a representative sample, the major drawback, reflecting the constraints just described, is that it does not allow me to directly test the causal mechanism.

MOSAiCH is a biannual cross-sectional representative survey that includes standard questions on the sociodemographic characteristics of respondents and, in 2015, thematic modules on “Citizenship” and “Work orientations,” providing several variables used in the analysis, including union membership. While the survey was administered using the computer-assisted personal interviewing technique, my module was inserted in a drop-off questionnaire delivered to all respondents of the face-to-face survey and submitted in paper-and-pencil format. The response rate was 77 percent. The data allow for a systematic comparison of the attitudes of Swiss union members vis-a-vis non-members toward inward FDI from China, Europe, and the US at a point in time when Chinese FDI was salient.

While the decision to focus on Switzerland is data-related, the research design is suitable to explore a question introduced in a more general way. China, Europe, and the US not only capture variation in the cultural dimension (similarity/dissimilarity between themselves and from the viewpoint of the Swiss), but also in the economic dimension (patient/impatient capital). While the former dimension should provide cues regarding FDI preferences to individuals, the latter should inform members’ preferences. Crucially, the two dimensions are cross-cutting in the cases at hand, providing the necessary leverage to test my argument. China is culturally dissimilar but has patient capital; Europe is culturally similar and has patient capital; the US is culturally similar or dissimilar to Switzerland depending on whether it is compared with China (H1) or Europe (H2) and has impatient capital. Moreover, Switzerland has good political relations with all three, thereby excluding alternative explanations based on ally/adversary dynamics. Switzerland and the People’s Republic of China have maintained diplomatic bilateral relations since 1950 and signed a trade agreement in 2013, while the Swiss have not banned China’s tech giant Huawei from their 5G network.

In comparative perspective, Switzerland receives, relative to its size, average amounts of Chinese FDI (Ministry of Commerce of the People’s Republic of China (MOFCOM), 2016). Just like in other advanced economies, Chinese FDI sharply increased since the late 2000s. A record-breaking deal (at the time of the transaction) significantly raised the salience of Chinese FDI: Sinopec’s acquisition of Geneva-based Addax Petroleum for US$7.2 billion in 2009. 11 Approximately 50 Chinese firms had a foothold in the Alpine country in 2013–2014, mainly SMEs active in a wide range of industries and regions (Kessler et al., 2014). Concomitantly, there has been a fair amount of media coverage of Chinese acquisitions in the French and German speaking regions both in the digital and print media (e.g. Jacolet, 2013; RTS, 2015; Städeli, 2015; Tanda, 2014). The EU and the US often rank at the top of the list of investors in advanced economies. This is no different for Switzerland: the EU is by far the largest foreign investor, accounting for nearly 80 percent of FDI stocks in 2015, followed by the US with just over 10 percent (Swiss National Bank (SNB), 2016).

Finally, while the Swiss political economy leans toward the CME model, including with regard to corporate governance and inter-firm relations, its labor market exhibits liberal traits (Mach and Trampusch, 2011). The Swiss work long hours and have low employment protection in the context of union fragmentation, intermediate/low levels of unionization and collective bargaining coverage, and weak workplace employee representation (Emmenegger, 2011; Oesch, 2011). Accordingly, the potential negative labor market effects associated with incoming impatient investors and thus the skepticism of unions to such investment is likely to be attenuated in liberal Switzerland and, if anything, more pronounced in “pure” CMEs. In other words, the Swiss case represents a conservative case.

Dependent variable

I use the following survey questions to generate the variables Pro-Chinese FDI, pro-European FDI and pro-American FDI: “Some foreign companies invest in Switzerland, for example by creating or buying companies. Do you think it is a good or bad thing for Switzerland that [Chinese (Q28a)] [European (Q28b)] [American (Q28c)] companies invest in Switzerland?” The questions encompass both mergers & acquisitions and greenfield FDI. They measure whether Swiss individuals think inward FDI by country of origin is good or bad for the country as a whole. Given the focus on the union effect, these are more appropriate than more narrow questions measuring self-interested attitudes. Unions not only represent but also provide information concerning the interests of wage earners, which constitute the vast majority of the working population. The answers on each item are recorded on a 5-point scale, with the highest score of 5 assigned to individuals who believe that [Chinese] [European] [American] investment is very good for Switzerland and the lowest score of 1 to those who believe it is very bad. 12

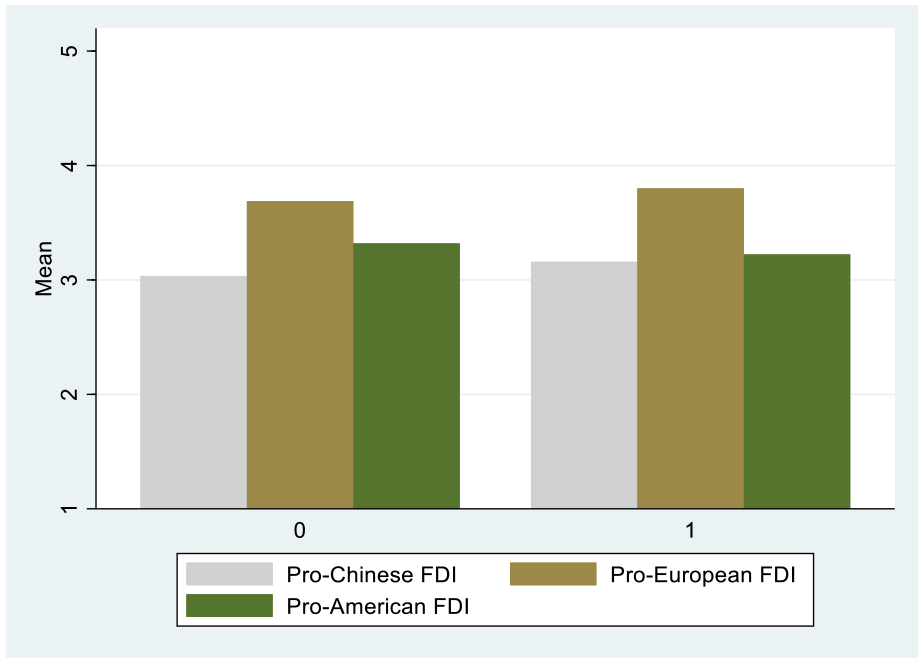

Among Swiss respondents, support is highest for European FDI, lowest for Chinese FDI, and somewhere in-between for American FDI, a rank order that holds for non-members and members alike, even though support for American FDI is only slightly higher than support for Chinese FDI among union members (Figure 1). Interestingly, the support for Chinese FDI and for European FDI is higher among members than non-members, whereas support for American FDI is lower for members relative to non-members. This provides prima facie evidence for my theory. I stack the data for the three survey questions to obtain the main dependent variable Pro-FDI.

Average support for FDI from China, Europe, and America by non-union members (0) and members (1).

Independent variables

To generate the union membership variable, I use a survey question that asks “Are you or have you ever been a member of a trade union, an employees’ association or an employers’ association” (D39). By way of a statement placed before the set of answers, respondents are prompted to respond by excluding their membership in professional associations. Union membership is a dummy that equals 1 if respondents are or have been a member of a trade union or an employees’ association (0 otherwise). I recoded to 0 reported (past and present) membership by high-level managers as they are likely to be members of an employers’ association rather than a trade union/employees’ association. 13 I focus on present and past membership because unions encourage a particular worldview that persists beyond union membership. 14

A first piece of evidence regarding the sophistication level of union members vis-a-vis non-members comes from the response patterns to the survey questions on different investors. Non-members are about twice as likely than members to indicate “don’t know” to the three questions. 15 Non-members also tend to be significantly more likely to answer “neither good/nor bad” to the questions. This suggests that exposure to union information by way of union membership is a significant channel through which individuals acquire sophisticated views on incoming FDI.

The stacking of the data creates three dummies, one for each of the FDI survey questions (Q28a-c). I label these variables Chinese FDI, European FDI, and American FDI, respectively. In the empirical analysis, the omitted category (reference group) is American FDI. In the model without interactions, the expectations from Jensen and Lindstädt (2013) are that the coefficients for Chinese FDI and European FDI are negative and positive, respectively, and statistically significant. In the interacted models, I expect the coefficients for the interaction terms Union membership*Chinese FDI and Union membership*European FDI to be positive and significant.

Controls

The baseline model controls for the socioeconomic position of respondents, including Education, Income, Job insecurity, Female, Age, and Urban residence. Regarding individuals’ ideological and symbolic dispositions, I control for Right ideology, belonging to the Swiss-German cultural group (as opposed to the Swiss–French or Swiss–Italian), and Nationalism. Differences in FDI opinions and stereotypes of country of FDI origin may be rooted in different Swiss cultures, which partly overlap with different ideologies of political economy (Armingeon et al., 2004). The measure of nationalism (opinions on “Increased exposure to foreign films, music and books is damaging our own culture”) captures cultural nationalism, including aspects of anti-Americanism, given the hegemony of Hollywood and American culture and the fabric of Swiss multi-culturalism—few Swiss would claim that reading Molière or Goethe is damaging to Swiss culture.

Attitudes toward European FDI might be driven by opinions on the European Union. I therefore control for Trust in EU, a proxy for pro-EU attitudes. Similarly, attitudes toward Chinese investment might be influenced by views on China’s rise as a trading partner and the (perceived) impact of the “China Shock” (Feng et al., 2021). Research suggests that trade with China has negatively impacted jobs and working conditions in advanced economies (Thewissen and Van Vliet, 2019). I control for opinions on whether trade deteriorates working conditions (Trade worsens conditions), which is likely to (partly) capture negative views respondents may have about trade with China, Switzerland’s third-largest trading partner. Finally, I control for individuals’ political information, measured as the frequency with which respondents use the media to get political news (Media exposure). This proxy for cognitive capacity adjusts for variation that may exist in media coverage and framing regarding (investment from) particular countries of origin.

I also estimate an extended model where I additionally control for living with a Partner, Home ownership, belief that the Economy is in good shape, opinion on trade’s impact on consumer prices (Trade lowers prices), and self-reported Economic knowledge.

Industry characteristics are likely to correlate with industry-level openness to FDI. Therefore, in all models I control for the respondents’ sector of employment by including 10 Industry dummies. I restrict the sample to the working age population. I use an ordered probit specification to analyze the ordinal dependent variable. The results are robust to using an ordered logistic model instead. All tests of statistical significance are based on robust standard errors clustered by industry. Annex 2 provides the definition and expected sign for the controls while Annex 3 provides summary statistics.

Results

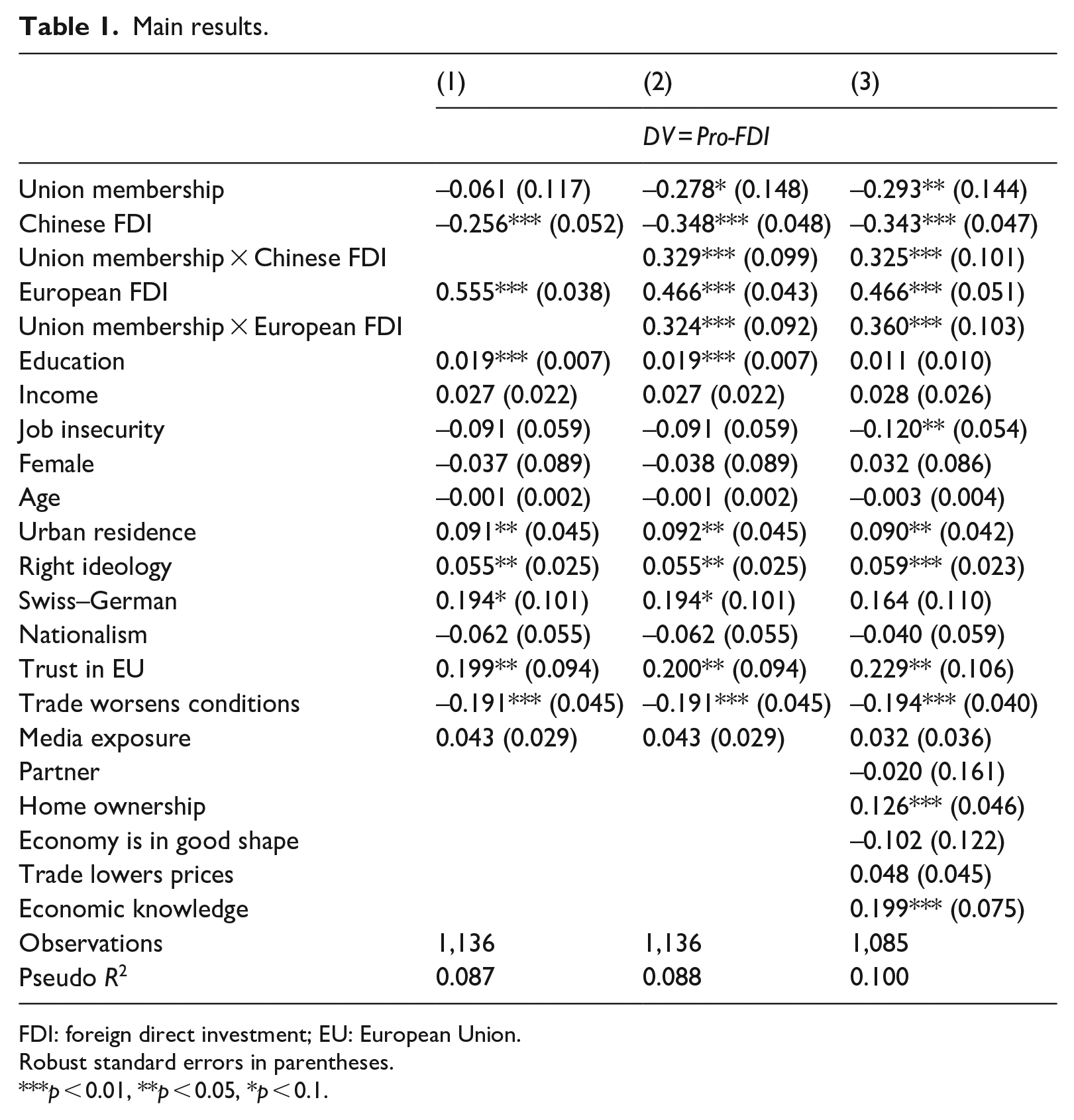

I begin with the baseline model without interaction terms (Model 1, Table 1). The coefficient for Union membership is negative and statistically insignificant, indicating that members are neither more nor less likely to support inward FDI than non-members. While this finding comports with the literature’s competing expectations regarding the relationship between unions and FDI policy, it may hide heterogeneity in how unions/members perceive FDI from different countries of origin. The coefficient for Chinese FDI is negative and statistically significant at the 99 percent level, implying that, all else being equal, the level of support for Chinese FDI among individuals is lower than for American FDI (the reference group). Conversely, the coefficient for European FDI is positive and highly statistically significant, suggesting that individuals’ support for inward FDI is higher when investment originates in Europe compared with the US. Swiss individuals’ rank order of FDI preferences is thus: favor Europe FDI > US FDI > China FDI. This comports with the argument that individuals use the non-economic contextual frames of cultural similarity/dissimilarity as cognitive shortcuts to form their FDI preferences. The control variables also comport with theoretical expectations, thereby increasing the confidence in the model. The statistically significant controls are Education, Urban residence, Right ideology, Swiss-German, Trust in EU, and Trade worsens conditions.

Main results.

FDI: foreign direct investment; EU: European Union.

Robust standard errors in parentheses.

p < 0.01, **p < 0.05, *p < 0.1.

I proceed with the baseline model including the two interaction terms Union membership × Chinese FDI and Union membership × European FDI (Model 2). The coefficient for Union membership is negative and statistically significant at the 90 percent level. In the presence of interaction terms, this coefficient captures the impact of union membership on attitudes toward American FDI (as Chinese FDI = 0 and European FDI = 0). Union membership reduces the support for American FDI. In other words, the level of support for American FDI is lower among members than non-members. This result is consistent with the notion that members interpret American FDI as impatient capital that is detrimental to workers’ interests and therefore arouses skepticism.

The dummy for the China FDI question is negative and highly significant. In the presence of the interaction terms, this indicates that non-union members view Chinese FDI less favorably than American FDI. Importantly, the interaction term Union membership × Chinese FDI is positive and statistically significant at the 99 percent level. This means that the gap in support for American versus Chinese FDI (favor US > China) is smaller among union members than non-members. The narrowing gap is due to both a lower support for American FDI among members compared with non-members (see above) and a higher support for Chinese FDI among members vis-a-vis non-members. These results are consistent with the notion that patient or impatient capital mediates union members’ assessment of FDI. In all, they provide support for Hypothesis 1.

Turning to the second interaction term, the constitutive term European FDI is positive and highly significant, implying that non-members view European FDI more favorably than American FDI. Crucially, the interaction term Union membership × European FDI is positive and statistically significant at the 99 percent level. This suggests that the gap in support for European versus American FDI (favor EU > US) is larger for members than non-members. This rising gap is driven by both a lower support for American FDI among members compared with non-members (see above) and a higher support for European FDI among members vis-a-vis non-members. These results are, again, in line with my theoretical expectations, providing support for Hypothesis 2.

In the extended model, the main results hold up (Model 3). The additional controls are correctly signed, with the statistically significant coefficients being Home ownership and Economic knowledge. Education is picking up exposure to economic ideas/information rather than skill level, as it turns insignificant with the inclusion of Economic knowledge. In this model, Job insecurity is statistically significant.

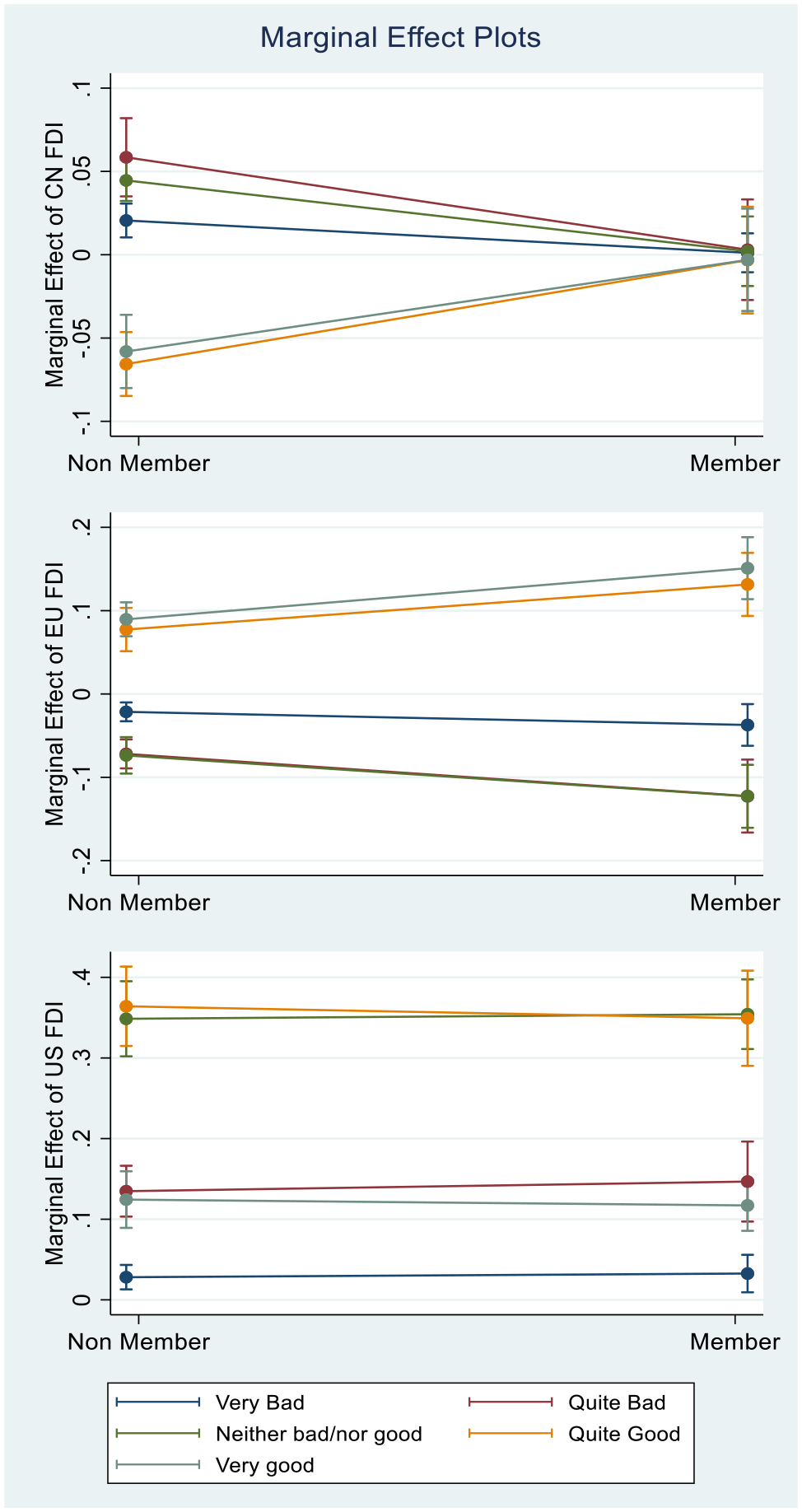

The effects are substantively meaningful. Based on the baseline model (Model 2), union members are 40 percent and 20 percent more likely than non-members to think that Chinese FDI and European FDI, respectively, is very good for the country. Meanwhile, members are 6 percent less likely than non-members to think that American FDI is very good for the country. Figure 2 plots the marginal effects of Chinese, American, and European FDI for non-members and members. By comparing effects across the first and second plots and across the second and third plots, we have confirmation for Hypotheses 1 and 2, respectively.

The marginal effect of Chinese, American, and European FDI, conditional on membership.

Alternative mechanisms

Within the constraints of the observational data, I consider alternative mechanisms. It might be the case that the observed, variegated attitudes toward FDI from various countries is a function of individuals’ level of sophistication derived from employment experiences or knowledge acquisition through education, rather than information provided by unions. In Annex 4, I rerun the baseline model substituting in the interaction terms union membership with variables related to employment experience or knowledge. I am interested in seeing whether we obtain similar results than with union membership, which would indicate other channels leading to sophistication.

Individuals covered by union-bargained collective wage agreements might see unions as important guarantors for their own or workers’ economic well-being (Iversen and Soskice, 2015). This might provide a work-related vantage point from which to assess the distributional issues surrounding investors from different countries. Interestingly, measured by the rate of non-responses to the survey questions on the different investors, the sophistication level of individuals who are and are not covered by collective agreements does not differ. 16 Moreover, individuals covered by collective agreements are significantly more likely to indicate “don’t know” than union members. The regression results confirm that being covered by a collective agreement is not associated with sophisticated views on FDI that factor in differentiated labor market effects depending on patient or impatient capital’s country of origin (Model 4). The results show that individual-level collective bargaining coverage does not affect how individuals assess the quality of inward FDI from China versus Europe versus the US, as can be seen by the statistically insignificant coefficients for Collective agreement, Collective agreement × Chinese FDI and Collective agreement × European FDI.

I next examine whether sophisticated FDI attitudes are not rather the product of job insecurity (Model 5). While individuals who perceive their job to be insecure are less likely to support impatient capital, such as American FDI, patient capital (Chinese or European FDI) does not condition the effect of job insecurity on FDI preferences as one would have expected as the coefficients for the interaction terms are negative as opposed to positive. In any case, the coefficients of interest are all statistically insignificant.

What about holding sophisticated FDI attitudes as a result of education? First, looking at the interacted model with education (Model 6), the positive and statistically significant coefficient for Education indicates that educated individuals are more (not less) likely to favor American FDI than less educated individuals. Simultaneously, they do not view Chinese FDI and European FDI differently from American FDI, as seen by the statistically insignificant interaction terms. Second, moving to the interaction model with the measure of self-reported economic knowledge (Model 7), the constitutive term Economic knowledge and the interaction term Economic knowledge × Chinese FDI are wrongly signed and insignificant, while the interaction Economic knowledge × European FDI is correctly signed but only weakly significant. Given the mostly insignificant results, we should not read too much into these results. Nonetheless, they are consistent with the views that economic knowledge reinforces stereotypes rooted in cultural similarity/dissimilarity (rather implausible) or that American and European FDI are seen as skill- or technology-intensive FDI, whereas Chinese FDI is seen as low-skilled, labor-intensive FDI (more plausible).

In all, these tests do not yield evidence that any individual characteristics of sophistication other than union membership are associated with sophisticated views of FDI that differentiate between the more or less negative labor market effects of patient versus impatient capital’s country of origin (or that fit any other theoretical expectations about differentiated distributional effects of FDI from various countries of origin, for that matter).

Robustness checks

I show the results for the robustness checks in Annex 5. To begin with, I reran the baseline model using alternative dependent variables. First, I generated Pro-FDI alternate where I assigned to the neither good/nor bad category (score of 3) individuals who indicated “don’t know” or provided no answer (Model 8). Second, I generated Pro-FDI trichotomous by collapsing the “very bad” and “quite bad” answers, on one hand, and the “quite good” and “very good” answers, on the other (Model 9). Finally, Pro-FDI dummy is a binary variable where the value of 1 is given to positive assessments of FDI (scores of 4 and 5) (Model 10).

Next, I ran alternate model specifications. 17 First, I ran a stripped-down specification where I exclude variables that arguably are post-treatment and obscure the effect of unionization (Model 11). Second, following Pandya (2010), I included a dummy for Private employee. This model excludes the industry dummies (Model 12). Third, I tested the sensitivity of the results to the use of other measures of education and symbolic dispositions (Model 13). Education alternate is a categorical variable with higher values indicating more educated individuals. Nationalism alternate is an alternative measure of cultural nationalism capturing threats to national culture posed by open borders and the intermingling of populations. Fourth, I added Pro PTA with EU, Pro PTA with China, Foreign business share, and Mobility to the extended model (Model 14). These variables control for attitudes toward deep trade integration with the EU, the Sino–Swiss trade agreement, (the extent of) firm engagement in foreign activities (i.e. within-industry firm heterogeneity), and worker mobility, respectively. Finally, I ran the baseline model including retirees (Model 15). Across all these models, the hypotheses are corroborated. It is worth stressing that in two models, the coefficient for union membership, to be interpreted as the effect of membership on attitudes toward American FDI, is no longer statistically significant. Arguably, this reflects some ambivalence of trade unions regarding American FDI (see above).

Conclusion

This paper investigates whether different countries of FDI origin impact people’s evaluation of whether FDI is good or bad for their country, differently depending on whether they are union members or not. I argue that unions shape the preferences of their members as the distributional consequences of FDI are not well known and consequently, individuals turn to intermediate organizations for cues. The explanation has to do with the treatment of investors’ country of origin as an important form of patient or impatient capital. Unions have a specific stance on this issue that will have observable implications on FDI preferences of their members vis-a-vis non-members. Members will prefer patient over impatient capital relative to non-members. Specifically, I argue that the gap in enthusiasm for patient and impatient foreign capital will increase with union membership. Conversely, the gap in support for impatient and patient capital will decrease with membership.

Using original Swiss survey data, I find strong support for my argument. Respondents were asked to assess FDI from China and Europe (country and region embodying patient capital) and from the US (embodying impatient capital). The results suggest that union membership increases support for European FDI and Chinese FDI and tends to decrease support for American FDI. More importantly, I demonstrate, as expected, that the difference in support for European FDI versus American FDI increases and the difference in support for American FDI versus Chinese FDI decreases with union membership. Members’ preferences thus reflect insightful views about the likely differentiated labor market effects associated with FDI from patient or impatient capital countries, and as such display more sophisticated FDI preferences than non-members. Additional statistical tests exclude prominent alternative explanations.

While the statistical analysis based on observational data does not allow for a definitive conclusion regarding the influence of unions on their members’ FDI preferences, the qualitative analysis provides evidence for the two-pronged mechanism underlying the theory. First, studies on the experiences and perceptions of worker representatives with Chinese investors in Austria and Germany, analysis of trade union internal communication in Switzerland, and my interviews with union officials in France, Germany, the Netherlands, and Switzerland confirm that unions view Chinese and continental European investors as patient capitalists and therefore in a positive light while the opposite holds for American investors. Second, I show that union members in Germany and Switzerland have been exposed in various ways to such ideas.

Future research directions include testing directly whether patience of capital drives union members’ FDI preferences using survey experiments and addressing possible limitations to the generalizability of the findings. For instance, do the results travel to countries where unionization rates are very low, such as France and the US, and/or where Chinese FDI is resource extracting rather than knowledge seeking? If anything, Switzerland, with its flexible labor market and weak union structures, resembles France and the US. It could be that unionization impacts perceptions of investors because collective bargaining can obtain more guarantees from investors. As bargaining coverage is higher than unionization due to extension clauses, the observed effects would be amplified and reach a broader swath of the population than just union members. My analysis suggests that collective bargaining does not impact FDI attitudes. Meanwhile, in “pure” CMEs like Germany, where impatient capital represents stronger threats to industrial relations arrangements, opposition of unions to impatient foreign investors is likely to be strongest. German union leaders’ entrenched skepticism toward American FDI suggests just that. In any case, despite dwindling membership in advanced economies, unions still represent large and often politically active portions of the electorate, capable of swaying political decisions to their own benefit.

Regarding the broader implications, first, the study strongly suggests that the economic interests of the groups to which individuals belong matter for FDI policy preference formation, even after controlling for individuals’ ideational and symbolic predispositions. In other words, the determinants of attitudes toward inward FDI are substantially material. Second, it clarifies the drivers of the backlashes against Chinese acquisitions and economic globalization more generally. While confirming that individuals are more opposed to Chinese FDI than other foreign investment, they become less averse to it when they are members of a union. While Chinese investors as patient capitalists are not unique, in the context of dwindling traditional forms of patient capital, they stand out as a (the) major contemporary form of patient capital in the global economy (Kaplan, 2021), potentially helping to nurture new pro-FDI coalitions. In contrast to political and business elites that have grown increasingly vocal in their calls to clamp down on Chinese acquisitions based on concerns with technology transfer and to tighten investment screening mechanisms (Chan and Meunier, 2022; Raess, 2021), union organizations have been more reluctant to rally around such causes because they see the interests of Chinese investors to be aligned with those of their members. Concurrently, their skepticism of American/impatient investors prevents them from being the flag bearer of pro-inward FDI policies, while suggesting that they belong to the most outspoken critics of financial globalization. In the new context of the US–China trade war and the Russia–Ukraine war, with changing perceptions of the security risks and benefits associated with economic cooperation with China (Chinese investment being less about jobs and patient capital, and more about geoeconomic competition) and of the US (more of a vital ally for Western democracies), it remains to be seen whether unions will reappraise some of their stances.

Supplemental Material

sj-docx-1-ejt-10.1177_13540661231186382 – Supplemental material for Disentangling public opposition to Chinese FDI: trade unions, patient capital, and members’ preferences over FDI inflows

Supplemental material, sj-docx-1-ejt-10.1177_13540661231186382 for Disentangling public opposition to Chinese FDI: trade unions, patient capital, and members’ preferences over FDI inflows by Damian Raess in European Journal of International Relations

Footnotes

Acknowledgements

Earlier versions of this paper were presented at the University of Reading (June 2017); the Congress of the Swiss Sociological Association in Zurich (June 2017); FORS—the Swiss Centre of Expertise in the Social Sciences in Lausanne (December 2017); the Annual Convention of the International Studies Association in San Francisco (April 2018); the University of Bern (March 2019), the World Trade Forum in Bern (October 2019), and the Congress of the Swiss Political Science Association in Lucerne (February 2020). For valuable feedback and suggestions, I thank participants and colleagues, especially Joseph Bommarito, Jonas Bunte, Céline Carrère, Nana De Graaff, Valentino Desilvestro, Manfred Elsig, Jonathan Golub, Lukas Linsi, Marcelo Olarreaga, Alexandre Pollien, Wanlin Ren, Tim Vlandas, Patrick Wagner, Aydin Yildirim, and Patrick Ziltener.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Swiss National Science Foundation (grant no. PP00P1_163745).

Supplemental material

Supplemental material for this article is available online.

Notes

Author biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.