Abstract

Policymakers implement regulations with limited capacity to register the unexpected. We argue that unexpected events do occur when regulations are implemented and we develop the concept of explication to account for the performative misfires that generate them. Explication is the organisational process that allows abstract ideas to be transposed into material realities and it allows us to identify how regulatory texts can carry signs and intentions in absence of their authors. We investigate the implementation of Markets in Financial Instruments Directive (MiFID), a regulatory package that generated a market context that was significantly different from what its economic programme sought to achieve. The competitive model underlying MiFID aimed to create a level-playing field among European financial markets but in reality its explication reduced transparency. We make four contributions to organisation studies. First, we show that explication is a source of contingency in implementation. Second, we shed light on the individual and collective hermeneutic performance as the source of counterperformativity. Third, explication brings intention back into the discussion: intention emerges from the unintended consequences borne by regulatory texts from the moment interpretation begins. Fourth, we show how explication can be a widely useful concept in organisation studies because it brings the performativity of language back into material semiotics whilst maintaining a place for contingency.

Introduction

In the past decade, performativity has become an important tool in organisation and management theory for making sense of how conceptual thinking affects reality and how, in this process, reality backfires or modifies theory (e.g. D’Adderio and Pollock, 2014; Ferraro et al., 2005). It is seldomly the case that theories straightforwardly perform their programme. On the contrary, performative processes based on abstract theories often contradict the promises contained by such theories (Callon, 2010; Muniesa, 2014). As Bamford and MacKenzie (2018: 99) have suggested: ‘abstraction and empiricism are intertwined in the very notion of counterperformativity, making it a particularly useful concept for [analysing] the curious ways in which models “fail”’. A model ‘can indeed be a powerful thing, but how it changes the world is inherently unpredictable’ (Bamford and MacKenzie, 2018: 121). Building on the idea that overflows always occur when theories are put into practice (D’Adderio et al., 2019), our study investigates how economic programmes, when translated into public management, lose the rationalisation they are otherwise assumed to have in economic theory, and as a result, generate counterperformative effects.

We use the term ‘economic programme’ to refer to two entwined realities. First, the term emerges from our empirical research. Specifically, ‘economic programme’ refers to those parts of economics and economic theories that underpin the deployment of the Markets in Financial Instruments Directive (MiFID): a programme of regulation intended to make European financial markets more competitive based on the pure model of perfect competition. 1 Second, we use the term ‘economic programme’ with reference to the literature on performativity – specifically the work of Muniesa (2014: 37), who suggests after Godelier, that ‘any sort of process, regardless of its particular point and scope, as soon as it is costly (and any process may be costly) is economic in nature’. Our use of ‘economic programmes’ captures a range of economic realities – theories, models or narratives – all of which have already been the subject of performativity studies (for instance in the social studies of finance tradition, see e.g. MacKenzie et al., 2007). The importance and value of this literature is that it ‘opens the black-box’ of such economic programmes. We build on this to provide an empirically informed illustration of the counterperformative effects of MiFID, before then exploring how this contributes to our understanding of counterperformativity in management and organisation studies.

How does an economic programme produce an altogether different organisational reality from the reality it depicts? In other words, how does performativity misfire rather than fail? This question is rarely taken as the starting point for inquiring into performative processes and performative failures (but see Callon, 2010 or Nyberg and Wright, 2016). As the logical opposite of successes, failures have too often been the default explanation for what happens when performativity goes awry (Butler, 2015; Fleming and Banerjee, 2016; King and Land, 2018). 2 Consequently, alternative explanations for economic utterances that fail to be realised have often been written out of analyses of performativity (Birch, 2011).

In what follows, we investigate what is realised when the economic programme underlying MiFID is transposed into the normative framework of a legal regulation. In so doing, our aim is to investigate how an abstract idea gave rise to a world that not only differs from what this idea suggests, but to an otherworldly reality from its suggestions. As we will see in subsequent sections, MiFID did not create the sought-after level-playing field that should have resulted from greater transparency (Finance Watch, 2011). On the contrary, MiFID created a situation where transparency was lost. As a result, the economic promises underlying MiFID – the achievement of competition bringing prices down – were not met, and prices went up because of a new environment created by the regulation itself (London Economics, 2010).

To make sense of this performative misfire we develop the concept of explication: the organisational process that allows abstract ideas to be transposed into material realities. Explication involves a movement of the implicit towards the explicit, revealing from within the abstract what is implied (i.e. contained, but not yet expressed). In a specific organisational setting, explication reveals the multiple necessary mediations partaking in the materialisation of ideas in reality. 3

Our article is structured as follows. The first section begins by reviewing the literature on performativity, highlighting the performative character of laws and regulations. Then, it develops an account of explication by describing how regulations are spelled out when transposed into specific organisations. The second section introduces the context for MiFID and the methodology for our study. The third section presents our analysis and identifies the counterperformative effects that result from the explication of MiFID. In the fourth and final section, we discuss our results and contribution to the literature on performativity and organisation theory.

Literature review

The literature on performativity developed extensively over the last 20 years. Following Gond et al. (2016: 444), who provide a mapping of discussions on performativity in organisation and management theory, our research can be located within a line of argument that understands performativity as ‘bringing theory into being’. To date, studies focus mostly on economic theories and managerial concepts instantiated within organisational contexts. For instance, this perspective has been used to describe rational decision-making (Cabantous and Gond, 2011), strategy theorising (Cabantous et al., 2018), but also to show how the language of economics shapes management practices (Ferraro et al., 2005), or how mainstream theories reinforce dominant approaches for instance in public policy (Henriksen, 2013; Marti and Scherer, 2016). In this perspective, ideas or theories materialise as social norms (Flyverbom and Reinecke, 2017), whether they originate in scientific literature (Roscoe and Chillas, 2014), or in specific managerial culture and practice (Aroles et al., 2021; Carton, 2020; Themsen and Skærbæk, 2018). However, a better understanding of how economic theory is brought into being through the vehicles of law and regulation is lacking. Our review therefore begins with the law, explaining in what ways it makes sense to see it as performative, before then showing how explication is the organisational process that allows abstract ideas to be transposed into material realities.

The performative ‘operations of the law’

Economic sociologists have for a long time studied the structuring effects of legal regulations on markets (Castelle et al., 2016; Pinsard and Tadjeddine, 2021; Schneiberg and Bartley, 2008), and they have shown that interactions between regulators and regulated actors are the locus of tensions that sometimes backfire on regulations. Funk and Hirschman (2014), for instance, have discussed how ambiguous innovations can undermine the categorical distinctions used by regulators. Similarly, Thiemann and Lepoutre (2017) have studied how financial actors creatively interact with regulations to evade their constraints, and how regulators may also react to such attempts. Other disciplines such as critical legal studies have discussed the performativity of legal regulations. For instance, Faulkner (2012) adopts a socio-legal studies perspective to analyse ‘the tension between standardisation and imprecision in the conceptual detailing’ of European laws, and makes the case that legal texts are sociolinguistic actors having performative agency. ‘[W]hile not autonomous’, Faulkner (2012) writes, the European regulation ‘accomplishes actions by virtue of its status as a legal document in the politico-legal system of the EU’ (p. 755). Similar perspectives on the enactive power of legal texts can be found in Mackenzie and Green (2008), who use the concept of ‘performative regulation’ to highlight the constitutive agency of regulation (Styhre, 2018).

These studies resonate with what Roman law historian Yan Thomas calls ‘the operations of the law’ (Thomas, 2021) – the techniques that were used in Roman law to construct and connect categories of ‘people’ and ‘things’, with a view to recovering the architecture of the social world. Simply put, looking into the performativity of legal regulations entails an analysis of how these regulations are operationalised to produce their outcomes, as this ‘can reveal circumstances and conditions in which the law is effective or counter-productive, especially since regulation can have unintended/unforeseen consequences’ (MacGregor, 2015: 52). By studying if a legal regulation ‘does what it says it does’ (Race, 2012: 330), we might indeed find reasons why MiFID misfired.

Commenting on the work of Yan Thomas, Muniesa (2018: 204) notes that it is ‘through the performative technology of the juristic fiction, that parties are delineated, objects formulated, agencies attributed and properties ascribed. It is through jurisprudence [i.e. case law], widely understood, that human institutions can be shaped and made sense of’. Not only are the operations of the law fundamentally performative, they also generate eventful outcomes based on the deliberations and interpretations that they require. Indeed, reading the law is seldomly a straightforward undertaking, and legal regulations require a situated interpretation often taking the form of discussions of case law. This is why we can say with Deleuze (1995: 169) that it is ‘case law [jurisprudence, in French], ultimately, that creates law’. Case law is descriptive of practices and the related material uses of law because it ‘advances by working out from singularities’ (Deleuze, 1995: 153). Hence, ‘we don’t need an ethical committee of supposedly well-qualified wise men, but user-groups. This is where we move from law into politics’ (Deleuze, 1995: 170). Deleuze (1990: 146) is emphasising that meaning (of the law in abstracto) is defined by means of use (or what the law affords in concreto). Yet as we will see, MiFID, the economic programme we investigate, is the outcome of a lengthy process literally created by a ‘Committee of Wise Men’ (European Commission, 2001).

Spelling the regulation out: Of explication

While much has been written about how economic theories performatively shape organisations and markets (e.g. Callon, 1998; Geiger and Gross, 2018; MacKenzie et al., 2007; Ul-Haq et al., 2022), there are still few performativity studies adopting a legal or regulatory perspective (Henriksen, 2013). Relatedly, Beunza and Ferraro (2019: 535) have outlined the performative effects of what they call a ‘regulatory network’: an organisational assemblage that aims at changing regulation in practice. With this concept, they show how ‘regulatory processes can be assimilated in various “performative projects”, whether it is through enrolling, fundraising, lending facilities or sitting on boards’. While their study is informative for understanding how regulations can be used by market actors to change an economic field, the authors do not consider the performativity of the legislative and regulatory processes proper – that is, the specific type of performativity resulting from the normative character of regulation, the institution promoting it, and the material aspects of its transposition into organisation.

To advance our understanding of problems emerging from the enactment of regulatory texts into their material contexts, we need to turn to alternative sources, and to develop our conceptual tools further. Specifically, we want to understand how MiFID created a material landscape unlike what it proposed. We therefore need to attend to the performance going on when a regulation is materially put to practice, which we call an ‘explication’. We derive the term explication from the parent concept of ‘explicitness’ that Muniesa and Linhardt (2011) elaborate to describe what happens when a public reform is brought to life. According to them, when moving from an abstract description to a material setting, things happen. Their study of an administrative reform of the State in France ‘works out empirically the problem of implementation as an explicitness trial’ (Muniesa and Linhardt, 2011: 551), and describes the many conundrums resulting from the elucidation of the meaning of the reform. Adopting a pragmatist viewpoint, their study specifically looks into ‘moments of struggle and hesitation in which what is at stake within the implementation process needs being clarified’ (Muniesa and Linhardt, 2011: 564).

While their proposal is both seductive and informative, we believe it could benefit from a discussion of the textual character of reforms. 4 Indeed, reforms are most often formalised as normative texts – such as laws and regulations, in our case MiFID. The juristic force that comes with the text is what explicitly allows the performativity of the reform to be discussed, and to realign a pragmatist interest in materiality (in the manner of ANT) with the interpretive quality of language (in the manner of pragmatic linguistics). By paying attention to the specific vehicle that law is, we can further develop the concept of explication. First, by highlighting the content of such processes, we can shed light on the collective hermeneutic performance that is the very source of counterperformativity. Second, explication allows us to bring back the issue of intention that ANT scholars often dismiss – because it bears the sign of an asymmetry between ‘human intentional action and a material world of causal relations’ (Latour, 2005: 76). Third, by weaving a parallel between the organisational process of transposing abstract ideas in a material setting, we can unpack the concept of implementation which often conveys a false notion of immediacy: as we will see in our case, explication and implementation differ as processes. Explication takes time, it allows contingency to emerge and to generate material overflows during the movement of the implicit towards the explicit. Our use of explication therefore differs from that of Muniesa and Linhardt (2011) who do not emphasise this specific aspect of what they call a ‘trial of explicitness’. Fourth and finally, our case shows that by thinking of explication as an organisational process, we can bring the question of the pragmatics of interpretation back into the discussion.

How does explication work? Explication develops by way of multiple interpretations, not in the sense of the ‘solving of a riddle’, but rather in the sense of the ‘performance of a play’ (Connor, 2014: 185). It is not that a ‘truth’ contained in the regulatory text is ‘revealed’ as a solution, but rather that the very act of interpreting a regulatory text means putting into play, by appropriating, adapting, making fit for, the given regulation in a given context. Or, as Barthes (1977: 146) would put it: ‘a text is not a line of words releasing a single “theological” meaning (the “message” of the Author-God) but a multi-dimensional space in which a variety of writings, none of them original, blend and clash’. As with legal interpretation, explication builds systematically counter to what exists prior to its emergence. Sometimes, actants may seem to overinterpret the text, to favour their perspective, just as different readings can offer conflicting interpretations of, or interventions on, the text (Lecercle, 1999).

The normative character of regulatory texts does not change this possibility, inscribed in the very structure of texts. Once disseminated, a regulatory text, like all texts, escapes its author: only the ‘readers’ – whatever their quality – can develop their interpretation, thereby performing an explication of the text, giving rise to material realities that on the one hand might be implied by the text, but on the other hand, might never be expressed explicitly. Explication sheds light on how normative texts, in the very moment they materially unfold what they contain in reality, ‘break’ from their organisational contexts – the ‘determination [of which] is never certain or saturated’ (Derrida, 1982: 310). This operative, counterperformative force, derives from the ‘very structure of the written’ (Derrida, 1982: 317), which detaches the initially intended meaning of the author and allows it to exist graphically in the text.

In this respect, MiFID offers a paradigmatic example, consisting of distinct layers of texts, all of which contain their own potential explications. First, MiFID is made of different types of texts which we describe in more detail below: Level 1 ‘Directives’, and Level 2 ‘Implementing Directives’ and ‘Implementing Regulations’. Directives need to be transposed, which means both relocated and translated, whereas Regulations are directly copy-pasted, into local regulations. In other words, Directives are always subject to the pragmatics of legal interpretation. However, we will see that the apparent simplicity of this process does not turn into immediate material results. Second, and furthermore, both Directives and Regulations contain recitals which are bits of texts that often begin with ‘whereas’ clauses that are located in the front-end of the legal text. In the case of MiFID, they are usually understood as the trace of unfinished deliberations between member-countries. While they do not have legal value, they are supposed to be general statements. It remains that ‘the doctrine surrounding recitals in EC law is mystifying. It is either irrational or so complicated as to amount to the same thing’ (Klimas and Vaiciukaite, 2008: 62). The creation and dissemination of European regulations is never straightforward because of the complexity of the EU’s political organisation. The Union is made from several countries, with different legal histories and habits, different ways to make sense of the law, and multiple institutions involved in different capacities at different levels in the European legislative process (e.g. the European Commission or the European Parliament). Consequently, simple ideas such as the pure model of perfect competition, once transposed in regulatory texts, often create complex situations, even though it serves as a key pillar for developing regulations in Europe.

Context and methods

The empirical setting: competition, pre- and post-trade transparency

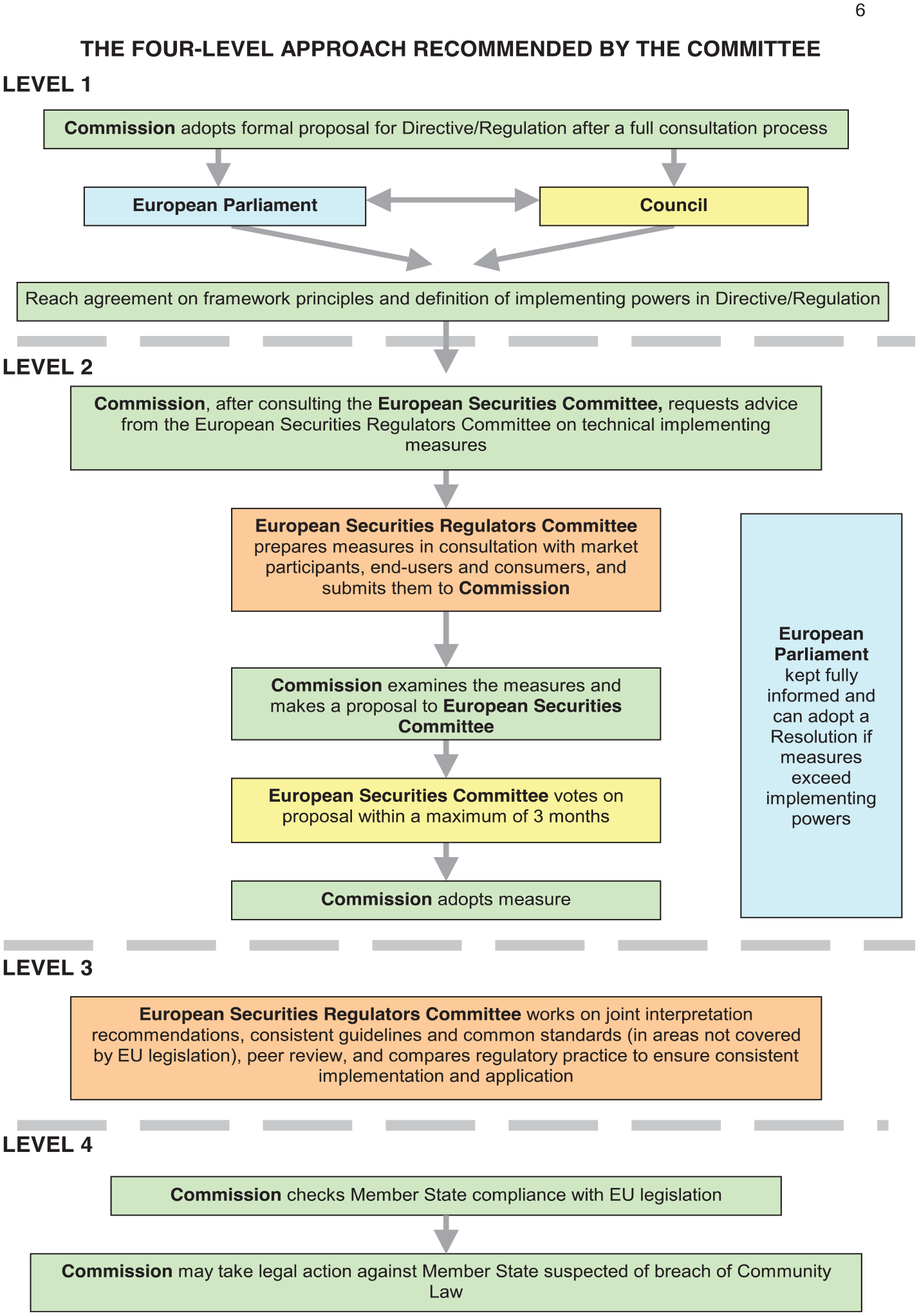

Learning from the failures of the 1993 Investment Services Directive, the EU’s finance ministers appointed a ‘Committee of Wise Men’ on 17 July 2000, to integrate European financial markets. This committee, chaired by Alexandre Lamfalussy, issued a report on 15 February 2001 proposing the rearrangement of European financial markets with a formal method (the ‘Lamfalussy process’). Figure 1 shows back and forth discussions between multiple stakeholders: the European Commission, the European Parliament, national regulators, market participants and end-users.

The Lamfalussy Process. This figure represents the organisation of the ‘Lamfalussy process’: it identifies four different levels (or stages in the cycle) and highlights the role of different institutions at each level: specifically, the European Commission (green colour), the European Parliament (blue colour), and the Committee of European Securities Regulators (also known as ‘CESR’, orange colour).

From the beginning, the Committee of Wise Men promoted an integrated financial market that would provide the Union with significant gains (Jabko, 2005). To substantiate the argument, the Lamfalussy report contained summaries of three academic papers published in the prominent journals the American Economic Review and the Journal of Financial Economics. Its minimal ‘literature review’ begins by noting that until the early 2000s, ‘little empirical evidence was made available to sustain the theoretical predictions’ made by models extolling the benefits of financial integration. It then argues that the papers presented in the report show ‘the validity of the positive predictions of the[se] theoretical models’ (European Commission, 2001: 110), indicating how financialisation is promoted by the application of an economic programme, transposed into a regulatory package aimed at changing the organisation of financial markets. 5

To achieve greater integration, a level-playing field was needed. Consequently, monopolies held by historical stock exchanges, still active in 21 of the 27 Member States, had to be removed. A comprehensive framework for a renewed organisation of European financial markets was developed by the Commission and on 21 April 2004 voted on by the European Parliament. The directive, MiFID, allowed private actors to create alternative trading venues and compete with regulated markets – the former national monopolies. However, developing competition between regulated markets and emerging alternative trading systems required further steps. According to neoclassical economic theory, a market needs to meet at least four conditions to qualify as ‘perfect’ (Ferguson and Gould, 1975: 222–225): prices are given to a large number of buyers and sellers, goods are homogenous, free entry and exit are granted, and the market is transparent (i.e. market participants should have perfect knowledge of quantity, quality and price). In a context where there is a monopoly and where only one trading venue is responsible for quoting prices and executed transactions, accessing price information is not an issue. Alternatively, in a context where many trading venues provide different prices for the same financial instrument, accessing price information (‘transparency’) turns into a critical issue for market participants.

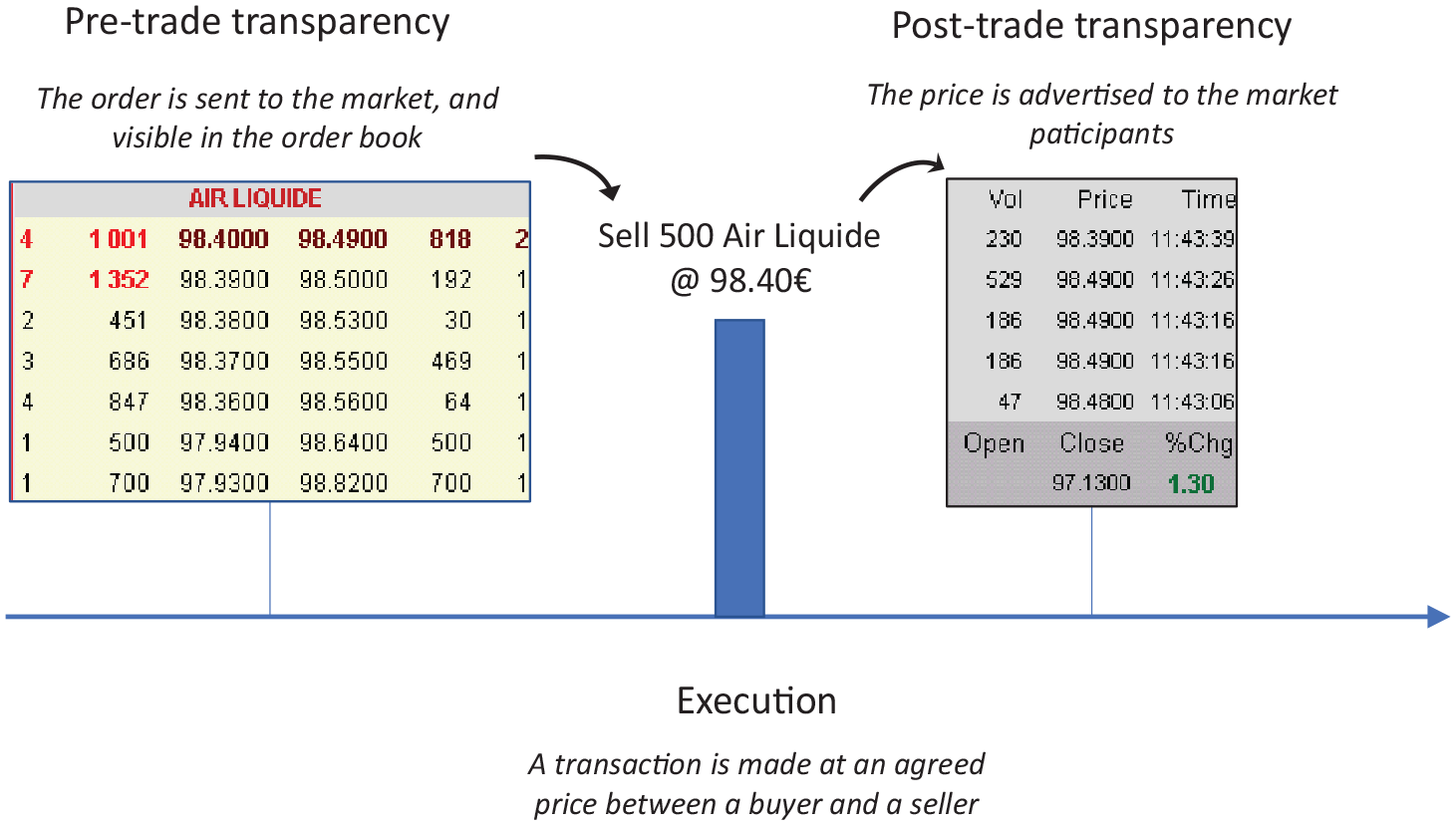

To enable competition in this new landscape, transparency rules were enacted: pre-trade transparency rules on the disclosure of prices and volumes available on the one hand, and post-trade transparency rules on completed transactions taking place on these platforms on the other hand (see Figure 2 hereafter). Principles were developed in the Implementing Directive and Regulation issued by the European Commission (European Commission, 2006a, 2006b). They remained one of the most disputed topics of MiFID because they dealt with the core of the financial market’s activity: the shaping and dissemination of information. Pre-trade and post-trade transparency contribute concomitantly to creating the typical level-playing field sought after by the European Commission, with a view to generating a competitive state within European financial markets. They provide market participants with information about transactions – either prices offered or asked prior to the execution in the case of pre-trade transparency, or effective prices executed on market platforms (or off-market) in the case of post-trade transparency. In both cases, prices are disseminated by way of advertising through an IT system, for example a Bloomberg or Reuters terminal.

Pre-trade and post-trade transparency explained.

During fieldwork, we observed two distinct types of behaviours from market actors. Pre-trade transparency was fought by some financial intermediaries who deliberately tried to circumvent MiFID by creating non-transparent markets (now known as ‘dark pools of liquidity’, see Patterson, 2012). They played with categories and definitions provided by the regulatory text. By pushing their interpretation of the regulation and by seeking to waive obligations attached to the pre-trade reporting principles set by MiFID, some actors created competitive advantage. The second type of behaviour, post-trade transparency, was not fought by market actors. The issue was more about what to do, or, what rule was to be followed, rather than trying to circumvent an already clearly identified rule. In the present study, we do not discuss the actions resulting from the first type of behaviour which is a deliberate intention to push the text to the limit and to indulge in ‘creative compliance’ (Black, 2012; Thiemann and Lepoutre, 2017). We instead focus our research question on explication as evidenced in the post-trade transparency issue to demonstrate that explication is not gaming by other means.

Data collection

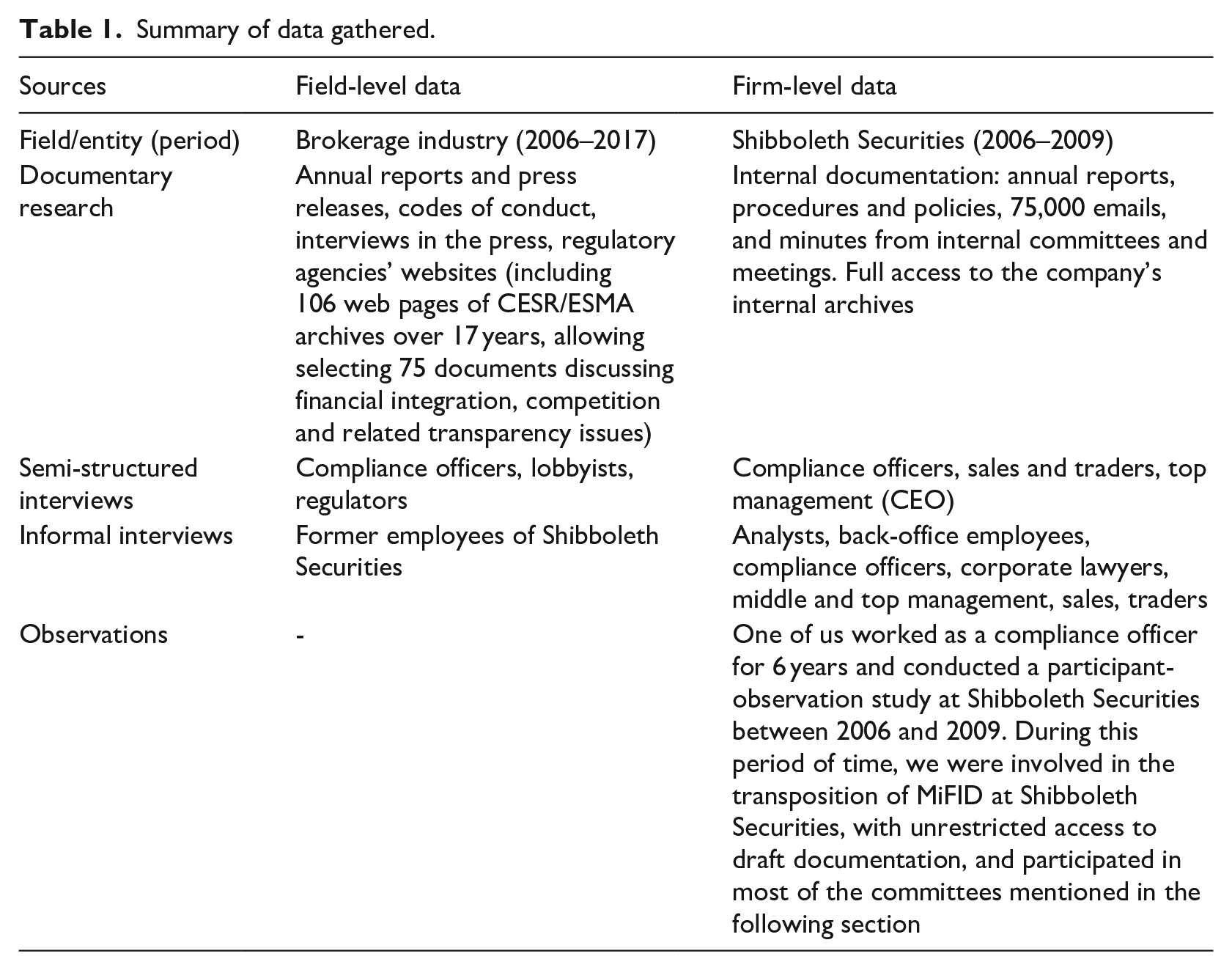

Our case focuses on the compliance department of Shibboleth Securities, 6 a European brokerage company headquartered in Paris, operating in 13 countries across Europe, the United States, Asia and the Middle East. Its 750 employees catered to more than 1200 institutional clients by providing investment services such as financial analysis, equity sales and execution services. We describe how the compliance department tackled transparency in the renewed market environment, offering a unique perspective on the transposition of MiFID (see Table 1). This compliance department played a pivotal role in the local transposition of MiFID. As an active member of the French Association of Investment Firms (AFEI), the lobbying arm of financial intermediaries in France, the compliance department contributed to discussions on ‘implementation measures’, involving different market actors and institutions. These contributions were often discussed at department meetings.

Summary of data gathered.

Between September 2006 and October 2009, one of us worked as a compliance officer in the compliance department of Shibboleth Securities. During this period, and despite turbulence from the 2007 to 2008 financial crisis, we maintained access to people involved in several different areas of the company (from commercial roles such as sales, analysts and traders, to support functions such as middle- and back-office, IT and organisation). Fieldnotes, observations and discussions on the trading floor were supplemented by analysis of internal documents such as codes of conduct and procedures, and a corpus of approximately 75,000 emails. This privileged position in the company’s trading floor afforded us access to regular meetings involving discussions with consultants, representatives of national and international regulatory agencies and professional bodies. Between June 2007 and January 2008, we attended 28 meetings concerning the transposition of MiFID into internal policies and procedures. These meetings provided a forum for discussing the new transparency regime and required changes to the information system, the organisation of reporting and related procedures, and other adjustments necessary to comply with the new regulation. To complete our sources, field-level data were gathered between 2006 and 2017 with a view to fact-checking the accuracy of firm-level data gathered some time ago. Library research was subsequently conducted until mid-2022, to gather further evidence from published sources to support the ongoing relevance of our present discussion.

Data analysis

We address our research questions on counterperformativity and how explication works via three interrelated analytic moments. The first moment involved a discussion of fieldnotes. The first author was an insider, taking part in the experiences described in the findings section. The second and third authors were interlocutors in the analysis, able to take the role of the Devil’s advocate (as in, Rerup and Feldman, 2011). In so doing, these two authors were in a position to discuss, criticise and ask for more details on the empirical materials gathered, thereby ‘challenging [. . .] emerging explanations’ provided by the first author (D’Adderio and Pollock, 2014: 1820). For instance, descriptions provided by the first author were often hagiographic due to the time spent on the trading floor; they also derived from the perspective of a compliance officer – the position held during fieldwork. While this was important for discussing how MiFID was locally received and interpreted, it also put the emphasis on officiating compliance as well as the interpretation contained within this department. Challenging this interpretation, by questioning the localised reading of particular aspects of the regulation with its existence elsewhere was necessary to develop an explanation of the phenomenon we describe in this article.

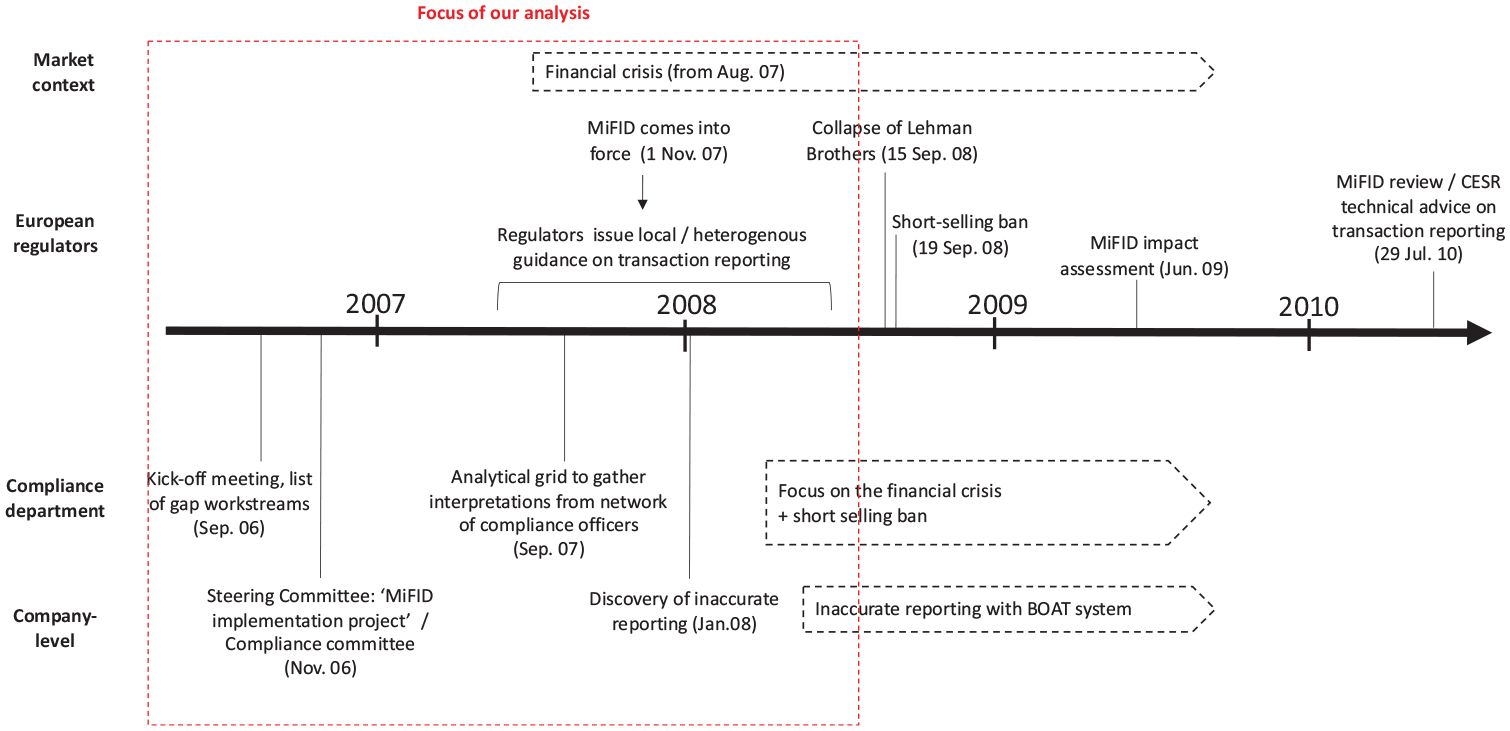

Following these discussions, we entered a second moment in the analysis. We reconstructed a chronology of field-configuring events (Lampel and Meyer, 2008), documented in the press and through data collection so that we could situate the time spent doing fieldwork on the trading floor inside this timeline (Figure 3). The timeline allowed us to identify important events in relation with our inquiry (for instance, the kick-off meetings and steering committees where MiFID was discussed internally, but also the regulatory announcements) that, taken together, resituate a thread of events that literally ‘make’ and unfold the explication of MiFID. This chronology was important to relate events with processes; for instance, news about the developing financial crisis and the collapse of Lehman Brothers.

Chronology of field-configuring events. This timeline displays field-configuring events, and was used to specify the focus of our analysis within the larger chronology.

In the third analytic moment, we returned to the research question and focused the empirical section of our article on the first 2 years of observations, starting in September 2006 before the enforcement of the directive (November 2007) and ending 6 months later (June 2008). 7 Fieldnotes from the 28 meetings attended between June 2007 and January 2008, proved crucial for identifying the issue of transparency. They also allowed us to analyse the different illustrations we provide under categories that pointed at recurring topics within the meetings. Access to on-going discussions in the industry and within Shibboleth Securities provided a window for identifying through subsequent library research how our analysis of the explication of this economic programme contributes to organisation theory.

Spelling MiFID out, putting MiFID to practice: A case study in counterperformativity

Anticipating MiFID at Shibboleth Securities (Sept. 2006–Aug. 2007)

At a meeting convened by the Head of Compliance and Internal Control, the four members of the compliance department (the front and back offices, the IT, the legal and the compliance departments) discussed a presentation identifying activities that would be affected by MiFID. A list of ‘gap workstreams’ was set with assignments. The task was to carefully read the regulatory package and identify business-relevant issues, with a view to making necessary adjustments before the new regulation came into force. The new MiFID environment had to be understood and the organisation prepared for what was later described as a ‘big bang’ (Skinner, 2007: 146). Three examples (organisational, normative and linguistic) illustrate the issues faced by market participants from the point of view of workstreams relating to the execution of orders at Shibboleth Securities, one of which focused on reporting transactions.

Organisational issues

A steering committee set by top management in November 2006 was swiftly renamed the ‘MiFID implementation project’ and met weekly. Dedicated sub-committees were created to work on the internal transposition of MiFID. The Compliance sub-committee was comprised of representatives from the compliance department in Paris and local compliance managers from the European subsidiaries. At their first meeting, it was clarified that updating procedures would be necessary and that transaction reporting requirements would be prioritised. The pan-European business model adopted by Shibboleth Securities also required coordination with a dozen subsidiaries and branches in Europe, the Middle East, the US and Japan. It soon became evident that MiFID was not clear enough when read in light of Shibboleth Securities’ organisation. One important issue relating to transaction reporting was about defining ‘scenarios for reporting to the authorities, taking into account the multi-local model of Shibboleth’ (meeting minutes from 18 June 2007). Shibboleth Securities was implanted in different places in Europe, so making sure that each local entity shared a similar understanding of MiFID requirements seemed paramount. At the same time, each local compliance officer had to maintain discussion with their local regulators and as we will see, this generated new problems when it came to making sense of the regulatory package.

Normative issues

Beyond firm-level interrogations, discussions involving local Parliaments and market regulators created other transposition issues for the directive. Locally, some institutions were unwilling to lose their own regulatory framework, and began ‘gold-plating’ MiFID. Rather than replacing their existing rules with European rules, they added the new rules to their existing framework at the cost of a loss of clarity and undue over-regulation (e.g. although in another context, see Haynes, 2009). Deciding where to report completed transactions soon became the subject of discussions between regulators and participants. In every country, local regulators and market participants were struggling to make sense of the regulation, as explicit guidance was not available on 1 November 2007. 8 At Shibboleth, the early days of September 2007 signalled that it was high time for the compliance business line to reach a shared understanding of the requirements. An analytical grid was sent by the head office in Paris to each compliance officer in charge of a local implantation.

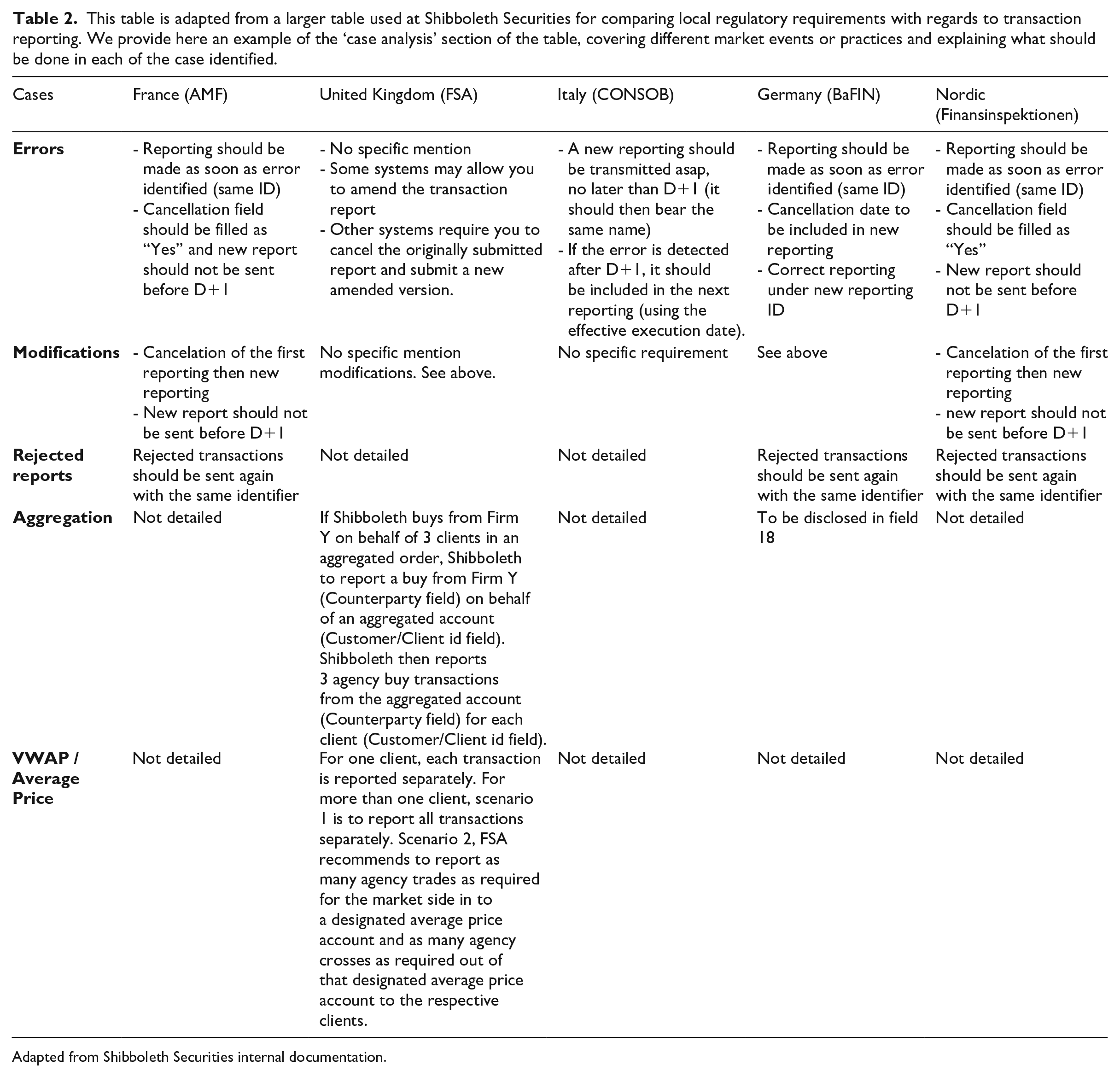

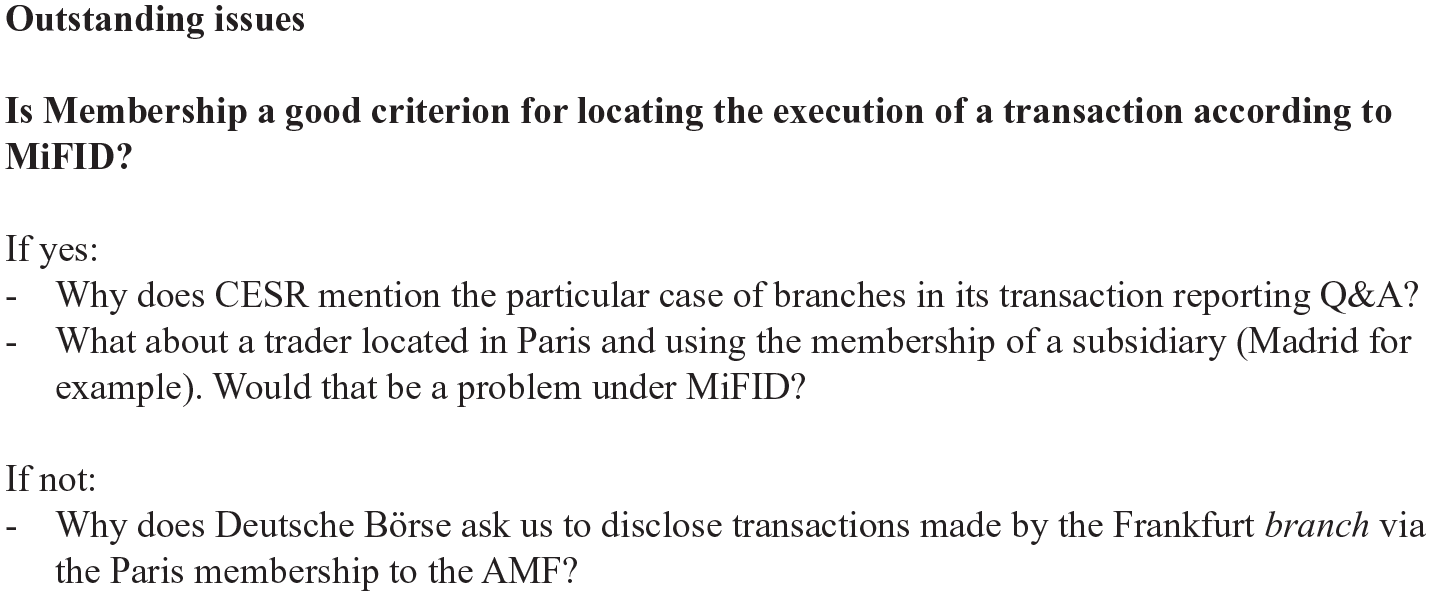

The grid was structured in three different parts, all of which differed from one country to another: the regulatory analysis; the case analysis (as shown on Table 2); and finally, the technical specifications. The case analysis detailed 12 different situations, such as the handling of errors or how to report an order that would be executed in multiple sequences, for instance over several days. Some countries decided to add more requirements whereas others did not bother and just cut-and-pasted the text published by the Commission. Some countries were giving market participants options for using either international norms (e.g. the International Securities Identification Number, or ‘ISIN code’, used as a single financial instrument identifier) or their local identifier. The Lamfalussy process afforded significant interpretive slack to the regulatory package. For instance, Figure 4 shows how two different institutions – CESR (a regulatory body) and Deutsche Börse (a market platform) – provided different understandings of ‘where’ to locate a transaction, a crucial element for developing the transparency regime necessary to the deployment of competition in European financial markets.

This table is adapted from a larger table used at Shibboleth Securities for comparing local regulatory requirements with regards to transaction reporting. We provide here an example of the ‘case analysis’ section of the table, covering different market events or practices and explaining what should be done in each of the case identified.

Adapted from Shibboleth Securities internal documentation.

This slide, extracted from minutes of the Compliance committee at Shibboleth Securities, provides an example of questions with no clear answer that MiFID opened: specifically, the issue here is about ‘where’ transactions are located, with a view to identifying to whom they should be reported.

During the gap analysis, multiple discrepancies appeared between the regulation written at European level and its local transpositions. Each country was a source of discrepancy. A survey conducted by the MiFID joint working group, a task force led by data vendors lobbying for their IT solutions, 9 shows that in June 2007, some European countries had very limited and often incomplete requirements about transaction reporting despite ISO standards.

Linguistic issues

In France, and likely elsewhere, there were issues with the translations produced by the local regulator. Documents circulated by the French regulator (the AMF) lacked clarity because of linguistic issues: [15 June 2007] – Mail from COO to Director in charge of lobbying at bank level

I have a number of comments to make on the AMF docs concerning the trade report

1/ First I think that there is in the French version of Regulation n°1287 art 12§.2 a very misleading translation (or even erroneous, with potentially a lot of confusion and the related consequences) of the term “Trade matching” which appears in the English version. [. . .] One could hastily conclude from the translation that a crossing engine (that is, a system allowing for confronting orders) must be approved by the competent authority before operating – even though this point is absolutely not made in the English version – a “trade” in English is equivalent to “executed order”, so a “trade matching system” is a post-trade system. It would be good if the AMF transposition did not make the same mistake.

The same message makes it clear that many aspects of the translated document, aimed at explaining how and what to report, remained unclear: 2 / What do we have to report? It’s not clear enough: the customer side or the market side? [. . .]

3 / art 2 3 ° The translation is not clear at all and no one here could understand exactly what this could mean: “the service provider who is negotiating for its own account on a trading platform, by entrusting the execution of its transaction. . .”

As we don’t understand what the regulator means, we are not in a position to suggest a new wording.

Summary

There are multiple gaps in the understanding of MiFID. While market actors prepared for MiFID, multiple readings and interpretations of the regulation were generated at the micro level (within actors like Shibboleth Securities), the meso level (whether by market professionals associations, or by consulting and law firms), and the macro level (during discussions between the European Commission and governments, or through the joint meetings of ministries of economy and finance). At the same time, these discussions expressed different interpretations in the multi-layered controversies surrounding MiFID. They result from the inner workings of the process created by the Wise Men of the Lamfalussy group – an expert group consistent with the regulatory logic of the European Union but not a user-group (as advocated by Deleuze, 1995).

Market participants were caught between multiple requirements resulting from local interpretations produced by local regulators. For companies like Shibboleth Securities, becoming a pan-European organisation with offices in many other countries had created more discrepancies and gaps that needed to be filled, and it created space for unintended, contingent, interpretations to emerge. Profound indeterminacy characterised the situation prior to November 1, 2007, contradicting the apparent simplicity of the theoretical model underlying the directive. By having to spell things out (Connor, 2014), market participants produced interpretations and created technical, material, solutions, whether in the form of new routines or new operating systems. Each market actor developed their own explication of the regulatory text, while not knowing precisely what the forthcoming market environment would look like in a very near future. While the issue of post-trade transparency had been identified early as one crucial element for achieving market competition, anticipations of MiFID requirements proved much trickier once confronted with the types of material questions that were generated by the multi-layered organisational context.

The concept of explication allows us to understand how and why the transposition of the regulatory package was not as straightforward as the Lamfalussy process could have initially suggested. By revealing the multiple mediations resulting from a given organisational process, whereby abstract ideas are inscribed in specific realities, unexpected material contingencies appear. MiFID was not yet enforced but it had already derailed from its tracks. Explicating the regulatory package led the implicit (what the ‘Wise Men’ could not think in advance) to materialise into explicit issues that blurred organisation.

Making things explicit (Sept. 2007–June 2008)

After summer 2007, decisions needed to be made, as a feeling of urgency began to crystallise. Overnight, between October 31 and November 1, 2007, the organisation of European financial markets shifted. Despite months of reading the regulatory package, the first weeks were challenging for compliance officers at Shibboleth Securities, who were constantly consulted by market operators in need of answers they could not provide. For the team, it felt like trying to drain a flooding river. This feeling endured but eventually subsided. We illustrate this with three series of examples of market participants seeking answers to their problems, how they translated those answers into scenarios, and finally how they addressed the resulting issues.

Searching for answers

Faced with uncertainty, market participants would request official advice from local regulators who were unwilling to provide it in writing. Once written, official advice formalised an official interpretation of the rules which was a deterrent. This would expose regulators locally and prevent them from keeping a margin of appreciation for forthcoming enforcement measures on market participants. In response, local regulators generated their own explication of the directive, making market operators develop practices complying with their local interpretation. On occasion, regulators pushed their interests, sometimes conflicting or even contradicting those of the European Commission. Existing IT processes and local procedures for reporting transactions that were retained could not be easily monitored at the European level. There was no guarantee that regulators in other countries would share local interpretations from elsewhere. These discussions took time, sometimes weeks, if not months, before regulatory advice was finally made public at a higher institutional level (usually, European). In the interim, a status quo allowed Shibboleth Securities and other competitors to continue working while developing their own explications when the regulatory package lacked clarity. There were many market situations for which there was no text available to address the contingency of market events.

Numerous and conflicting interpretations emerged because of this inability of market actors to understand or to get quick, consistent, answers from their regulators. Some market participants tried to take advantage of this ambiguity when developing their own interpretation. The competition sought after by the Commission began to emerge between market participants who could now confront each other on multiple execution venues. For instance, one of Shibboleth’s competitors decided to report both legs of every transaction (i.e. the ‘buying’ and the ‘selling’ side of the same transaction), thereby artificially doubling their traded volumes. First this made information on volumes irrelevant for other market participants. Second, it provided a distorted representation of the relative power among market participants, as traded volumes were used as a proxy to estimate the market share of each market participant. Even if unacceptable and severely harming the quality of transparency, such practices were accepted because the regulatory package was interpreted.

Writing down scenarios

The gap between the economic programme underlying the regulation and the reality it brought about was widening. Tackling discrepancies daily proved difficult. As late as February 2008 (3 months after MiFID came into force), weekly discussions with the French regulator AMF took place. Painstaking technical debates involving the consultants and compliance officers at Shibboleth’s head office and European subsidiaries produced a list of possible scenarios considering local transpositions of MiFID. The list was supplemented with precise identifications of ‘where’ the electronic information relating to a trade would come from and flow to. Transactions could be located in a country where Shibboleth Securities had a registered office (a separate legal entity such as a subsidiary, but not a branch) as well as a country where the trader actually received an order before processing it.

Initially intended to provide guidance for other departments of Shibboleth Securities, this document soon turned into an object of contention beyond the front office, between the IT, the legal and the compliance department, as nobody was willing to take full responsibility for writing down once and for all how the document would later serve as reference. The ambiguities of MiFID were many, and the stakes high. Finding a good balance between interpreting what the regulation seemed to say on the one hand, and what the internal IT system could afford on the other, was not simple. Navigating this grey zone, Shibboleth management had to decide on a reporting option, doing their best to choose a reporting option that they thought was close enough to the model put forward by the regulation, while at the same time simple enough not to generate further IT costs.

Addressing IT issues

Grey areas became fixed in response to the profusion of issues. For instance, the IT department was not willing to make radical changes to the IT system and continued to prioritise front office-related IT matters over the development of the back-office system. Eventually, this generated bugs in the reporting system. At the end of January 2008, Shibboleth discovered it was not reporting transactions correctly: approximately 5,000,000 executions that should have been reported as ‘agent’ were reported as ‘principal’. This incorrect reporting represented two-thirds of transactions executed between November 2007 and February 2008. Most of the data was reported but with an inaccurate identifier. This might look like a minor bug but it means that two-thirds of the transactions were flagged as if they were done on behalf of Shibboleth – whereas they were indeed processed by Shibboleth on behalf of its clientele. On the market side, the representation resulting from this bug hampered the effects sought by MiFID. The information sent to the market was inaccurate and the transparency principle at the core of MiFID was undermined. This outcome results from the complexity of an environment where the regulation requires system changes, with routine upgrades not being correctly performed, rather than intentional wrongdoing.

Summary

The level-playing field that implementation would require was not created. Nine months after MiFID came into effect, routines were put in place, and despite unresolved issues, market participants like Shibboleth Securities were reporting their transactions. Throughout 2007, a creeping crisis had developed, which culminated in September 2008 with the collapse of Lehman Brothers. The 2007–2008 financial crisis was an exogenous shock and had nothing to do with MiFID. It had developed in another country (the US), on a market segment that was not even considered by MiFID (subprime mortgages). Despite this missing link between MiFID and the 2007–2008 crisis, the magnitude of the event soon shifted the priorities of market participants.

Faced with unaddressed situations generated by the everchanging market context, operators requested official advice from the European Commission, which created a list of Q&As addressing a growing number of questions and let opposing views between the Commission and national regulators appear. The Q&A, among other initiatives – industry meetings, public hearings and consultations – showed that attempts to make issues arising in the course of MiFID’s transposition explicit was close to impossible. Dissimilarities emerged between the normative framework underlying the regulatory package and the way that framework was put to practice considering the broader organisational context. While MiFID was intended to homogenise financial market structures and related practices, its explication created a series of unintended consequences that meant it counterperformed its underlying economic programme. Earlier, after 1 November 2007, regulated markets had faced the fierce competition of alternative trading systems, as planned by the Commission. However, the assurance that information on prices was sufficiently accurate for market participants to make decisions about their investments was lost. The transaction reporting system was marred at the Commission level by insufficient anticipation of material quandaries resulting from the transposition of a regulatory text into a market context, as well as a lack of consistency across local explications. The multiplicity of interpretations generated massive overflows of an initial model based on the pure model of perfect competition.

In January 2009, Adam Kinsley, the Director of Regulation at the London Stock Exchange, wrote a letter to Carlo Comporti, the Secretary General of CESR, in answer to the Call for evidence on the impact of MiFID on secondary markets functioning (CESR/08-872). His diagnosis ‘that an excessive focus on competition between venues may overlook some other, more interesting, dynamics in the market such as the apparent decrease in competition between firms (broker/dealers and liquidity providers)’ is decisive and illuminating.

Similar critiques were raised by other organisations representing the interests of lay investors (e.g. Finance Watch, 2011). The Lamfalussy process, created by the Committee of Wise Men, and the framework offered by MiFID, made room for interpretation, and inevitably led to local adaptations during the process of its explication. As the principles diffused through the organisational field, they contributed to create counterperformative ripples that differed substantially from the effects sought after by the underlying economic model of pure and perfect competition. It is a model that cannot work correctly without the transparency resulting from the consistent reporting of transactions. Interestingly enough, the issue of information related with transaction reporting had been identified right from the beginning as one pivotal element of the contemplated regime, but the overall process of regulatory dissemination, together with the intrinsic character of legal texts creating interpretive slack when being spelled out, generated adverse effects and contributed to counterperforming the promises made by the economic programme.

Discussion and conclusion

In this study, we provide empirical evidence for how an economic programme based on the pure model of perfect competition is brought into existence and how its operation can be undermined by a process we have described as explication. Building on previous work by Muniesa and Linhardt (2011), we refine the concept of explication as an organisational process involving a movement of the implicit towards the explicit that allows the transposition of abstract ideas into organisational realities. Notably, our analysis has allowed us to redeploy the concept of explication and apply it to regulatory texts.

First, we have shown how organisations appropriate what is implied from within the abstract, and as a result, generate contingent realities that may veer or differ from the assumptions of an underlying model. Explication therefore reminds us that, in reality, materialising rules involves lengthy mediations that inevitably disrupt the false perception of immediacy conveyed by the often-used concept of implementation. Mediations are required for a regulatory text to deliver its normative force. Explication is real, whereas implementation remains an abstraction that will always require explication. To suggest a regulation is only ever implemented is to misinform policy and organisation theory about the material quandaries typical of explication.

Second, our case highlights the type of performance inside such processes. We shed light on the individual and collective hermeneutic performance that is the very source of counterperformativity. Performativity studies originated with the theoretical choice to extract intellectual pursuits from classical Oxfordian debates on the performativity of language. This decision has proven very useful for shedding light on the performative effects of theories, models and other related devices affecting organisation. Concurrently, performativity studies lost the ability to pinpoint the role that language continues to play in performative processes (Piekkari et al., 2020). As we have seen, regulatory packages, because they take the form of texts, bring us back to the material reality of texts doing things. Every actant is an interpreter (Barthes, 1977), performing its own reading of the regulatory text by ‘spelling it out’ in a unique play (Connor, 2014), thereby giving birth to series of contingent effects. These material effects, while implicitly contained in the regulatory text supported by its underlying economic programme – in the case of MiFID, the pure model of perfect competition – can never be fully anticipated, and as a result, counterperformativity always appears. While performativity originated within a discussion on ordinary language (Austin, 1962), and was later applied to more abstract elements (concepts, theories and models), there are still very few studies on the textual, material, character of law and regulation in organisation. Explication makes this possible by developing our understanding of the performative operations of the law, specific to it, and how norms and regulations get inscribed into the materiality of things.

Third, explication brings intention into the discussion. Intention emerges from the unintended consequences borne by regulatory texts from the moment interpretation begins. While our remarks might seem to state the obvious – that theories, when transposed in reality, very often ‘fail’ to achieve what they promise – it is also often the case that governing bodies prevaricate this. The assumption that regulations and their underlying models are working with a singular, mechanistically-derived reality (Holm Olsen, 2006), is profoundly incorrect. Regulations are always in reality explicated and explication is always open to contingent events that can escape any model. Subject to the rules of mechanical systems, implementation is therefore assumed to bring about change without generating unintended consequences of the kind we have detailed in the empirical section of this article. If policymakers do not incorporate the counterperformative effects of economic theory at the organisational level when they use it as a basis for developing regulation, they then enact rules and regulations that are too often understood as being (easily) ‘implementable’. This renders policymaking into a practice that is unable to account for the contingency of reality – always already contained, though implicitly, in the abstract and not necessarily external to a situation.

Fourth and finally, by bringing the performativity of language back into material semiotics whilst maintaining a place for contingency, explication can be a widely useful concept in organisation studies. Our case sheds light on the material, written, character of the regulatory text and its ability to carry signs and intentions in absence of their authors, which creates the conditions for counterperformativity to emerge. Organisational scholars can use explication to account for seldom considered but highly consequential counterperformative effects in which things are unexpectedly undone. Explication can be used between the material semiotics of ANT and the emphasis on textual formations in discourse analysis to understand the mediating role of the move from the implicit to the explicit.

For instance, scholars interested in economisation could pay more attention to laws and regulations as specific actors of the process of explication, where technical language plays a pivotal role as a translative, interpretive, actor. With explication pointing to an identifiable organisational process, unexpected events that are otherwise assumed to be exogenous can be shown to be endogenous when they can be attributed through explication to the counterperformative effects of specific models and associated laws and regulations. Explication also opens important avenues for the study of new technologies in organisations by drawing attention away from the impossible pursuit of technical perfection or abstractions about the implementation of these technologies, towards the actual contingencies they introduce into the coordination of work, a problem that is increasingly important with artificial intelligence technologies. Regulating these technologies is a challenge precisely because of what we are calling explication with the law and regulation itself and with the regulatory characteristics of these technologies. As well as assisting policymakers to better register the unexpected, explication can therefore also help us understand undesirable consequences resulting from the outputs of these technologies, much as normal accident theory or routines helped us understand issues and processes associated with mechanical technologies. Similarly, studies of finance and society can highlight the central role of organisations in the explication of regulatory texts where previously they have not. Even if organisational scholars might not have sufficiently recognised that ‘the law accounts for a richer reality than [they] have granted it’ (Bencherki and Bourgoin, 2019), this richer reality materialises during the organisational process of explication – for example, MiFID regulation now appears full of potential counterperformative outcomes.

Mainstream management theory, while focusing on implementation processes, very often ends up developing macro-level perspectives, which fail to provide sufficiently detailed granularity of the phenomenon they claim to study. By nurturing the capacity of organisation theory to hold both these two layers of analysis in tension, in this study we have been able to register movement in both directions. Here, organisation theory is attuned to mediations between the abstract and the material. Our article shows that it is possible to make sense of what happens when regulatory problems are dealt with at the macro-level (typically, at the level of institutions such as the European Commission), and result in developing top-down approaches that fail when they meet reality. Management theory that accepts explication, rather than implementation, as its starting point, expands the capacity of organisations to respond to contradictions generated by the tensions between these different layers, perspectives, and levels.

To conclude, explication underlines the gaps between, on the one hand, the abstract ideations developed by a Committee of Wise Men, and on the other hand, the manifold explicit realisations fixed in reality by market practitioners (‘user-groups’, as Deleuze would put it). This confrontation emerges as the performance, or the ‘putting into play’ of the regulatory package. Since explication is itself an organisational process, it is organisation theory that allows us to deal with both the counterperformative effects of theory on the one hand, and the textual materiality of regulation on the other hand. Organisation theory helps shed light on the numerous bottom-up initiatives that can be nurtured in a given organisational environment. By studying how an economic programme, translated into public management, generated adverse effects (typically, the creation of a market landscape devoid of the level-playing field sought after by its underlying theory), we have provided an illustration of the work of explication, and accounted for the gap between economic models on the one hand, and ex post facto emergent realities on the other hand. Traditionally, critics of such gaps between abstract theories and material realities emphasise ignorance in economics, focusing on issues of ‘non-knowledge’ (e.g. see Arnsperger and Varoufakis, 2005; or Gross and McGoey, 2015), acknowledging that ‘ignorance in markets in endemic and ineradicable’ (Mirowski, 2019: 528). Adding to this view, our study reinforces the notion that the ineradicably ignorant quality of the market is also generated by the legal-material configuration of market regulation in organisations.

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.