Abstract

In this article, we use the critical theory literature to describe the processes of co-optation by which capitalism engages with its radical alternatives in order to subvert their emancipatory potential. We chose the global Islamic banking industry as our empirical context, which represents bold efforts to build a radical alternative embedded in Islamic moral precepts. However, we observed that the performative intent of capitalist discourse, reflected in a strong preoccupation with effectiveness and efficiency, has come to dominate all economic claims in the Islamic banking industry. The oppositional ideas that were intended to disturb the economic status quo now reproduce it along with its privileges, despite the vaulted rhetoric about establishing a genuine alternative. The article ends by mapping out some implications of re-introducing co-optation in the critical theory literature.

Keywords

In our advanced industrial society, tolerance of oppositional ideas serves, paradoxically, to strengthen and perpetuate the status quo.

Scholars have recently shown increased interest in the attempts to diagnose the ills affecting the global economy, especially against the backdrop of the financial crisis in 2008 (Dufour and Orhangazi, 2014). Some argue that this tendency is due to the inherent nature of neoliberal global capitalism which is ‘concerned only with money making money’ (Jackson and Carter, 1995: 883), diminishing the power of human-centered values and ethics. The regularity of the financial crises and the asymmetries and inequalities generated by capitalism were further highlighted in 2011 with the Occupy Wall Street movement (Shrivastava and Ivanova, 2015). This movement used aesthetics to critique the inequality of the economic system and the personal greed that it spawns. Such protests are manifestations of the growing legitimacy crisis of capitalism and are instrumental in dramatizing both the need and the possibility of thinking about alternatives (Adler, 2014). Some scholars believe that the resolution of systemic crises requires a major restructuring, and mere bailouts and temporary arrangements will not work (Wolff, 2013). This existing state of affairs has made economists and social scientists think hard about the non-capitalist socioeconomic formations with the aim of finding out if these alternatives can challenge and ultimately replace the dominant system. One can identify numerous alternative ways of contesting capitalism such as intentional communities, cooperatives, microfinance organizations, and alternative currencies (Meyer and Hudon, 2017), but it is not clear whether these alternatives disrupt or strengthen the capitalist system. As the quote of Marcuse shows, capitalism not only allows but even benefits from its critique. This capability of capitalism to restructure its alternatives, or co-opt them, without subsuming them into its core is the topic of this article. We present a theory of co-optation to show the processes by which neoliberal capitalism usurps anti-capitalist alternatives. This is followed by a detailed historical examination of Islamic banking (embedded in the ideology of Islam) as an empirical illustration of this theory and as a radical alternative of conventional banking (rooted in neoliberal capitalism).

Since ‘neoliberal capitalism’ is a polysemic and politically charged term (Ganti, 2014), there is no fixed closure of its exact meaning. However, what we can offer is a broad sense of orientation, which is sufficiently accurate to point out the main tenets of its philosophical system. Given the above, we define neoliberal capitalism as a socioeconomic order which privileges unrestrained market competition, minimal state intervention, and a self-regulating economy based on market relations where individuals with an entrepreneurial orientation maximize their material interests (Kotz, 2018). This order is rooted in a moral project of human liberation and freedom as well as an ideology (Fotaki and Prasad, 2015) of organizing society by valorizing the individual while destroying collective structures (Bourdieu, 1998). This stands in stark contrast to Islam with its theistic epistemology and belief in Allah (God) where human liberation means submission to the will of God (Ul-Haq and Westwood, 2012). In the capitalist system, individuals are modeled as self-interested rational maximizers with a competitive, hedonistic, winners-take-all mentality (Ferraro et al., 2005), while Islam assumes that individuals are focused on cooperation, empathy, love, and community with an altruistic mentality (Zaman, 2019). By treating all humans as rational egoists focused on maximization of material gains, neoliberal capitalism completely ignores the spiritual concerns that are central to an understanding of the purpose of life in Islam (Ul-Haq and Khan, 2018). Similarly, in the capitalist system, the basic problem of individuals is economic, that is, how to satisfy infinite wants with finite resources (Hussen, 1982) and the solution to this problem lies in accumulation of wealth through ever higher forms of efficiency. On the contrary, the problem of individuals in Islam is spiritual transformation, that is, how to control their desires for material goods while cultivating their spirit, and the solution to this problem lies in the love of God and the struggle to create a just society (Zaman, 2019). In this sense, any socioeconomic model emanating from Islam would ipso facto have an agency of liberation.

The above differences led us to study the Islamic banking industry as our empirical context since it claims to provide a radical alternative to the traditional banking system (Rudnyckyj, 2019). It is important to note, however, that this alternative does not claim to be a holistic challenger to neoliberal capitalism but only presents itself as a partial implementation of Islamic ideology in the banking arena—an important sphere of economic activity. We used the methodology of ‘narrative construction’ (Wadhwani and Decker, 2018) to study the Islamic banking industry in order to mark out events and processes constituting turning points in its evolution. This allows us to contribute to critical theory by first integrating existing literature into a coherent process theory of co-optation and then illustrating its empirical application in the Islamic banking context. In the next section of this article, we briefly present findings of existing literature on alternatives followed by our theory of co-optation. Then, we present a detailed historical narrative of important changes in the Islamic banking industry. Afterward, we show how this alternative was co-opted by capitalism using its agents and discourses. In the end, we map out some implications of re-introducing co-optation in the critical discourse especially in opening up the possibilities for formulating a transformative enterprise.

Anti-capitalist resistance and alternatives

Despite the hegemony of capitalist discourses, we do find instances of anti-capitalist movements as well as alternative forms of organizations (Gibson-Graham, 2008). These include social mobilizations ranging from the Zapatistas in Mexico to the Battle of Seattle among many others. Similarly, some examples of alternative economic practices and organizations include unpaid labor (household and volunteer work), online and virtual currencies, community-based indigenous enterprises, worker cooperatives, and barter networks. This implies that a variety of alternatives in different domains also exist alongside the market system of capitalism (Mitchell, 2002). However, we acknowledge that it is complex to neatly demarcate the boundaries of these alternatives as their critics can always point out some capitalist elements (Fisher, 2009). We resort to Martin Parker and his colleagues’ conceptualization who argue that what makes the alternatives unique or distinct from capitalism is their emphasis on alternative values which are geared toward social, human, and democratic goals (Bousalham and Vidaillet, 2018, Parker et al., 2014).

There are two ‘ideal’ types of such alternatives, incremental and radical, which can be conceptualized as two ends of a continuum. The objective of incremental alternatives is to first highlight a problematic aspect of the existing economic order and then to improve or correct it. These alternatives assume that there are situations where the market mechanism becomes unfair resulting in material disparities and power inequalities. The purpose of these alternatives is to improve the fairness of the system instead of subverting it. The response of capitalism to such alternatives is mostly to accept their critique and incorporate mechanisms that address legitimacy deficits as long as ‘the profit-based dynamic can continue to operate’ (Chiapello, 2013: 63). Hence, these alternatives actually contribute to the robustness of capitalism (Boltanski and Chiapello, 2005) owing to their therapeutic function. Consider, for example, the Bottom of the Pyramid (BOP) projects which attempt to use the market mechanism to not only generate profit but also alleviate poverty in developing countries. This image of private corporations harnessing the creative and entrepreneurial capacities of local communities while dispensing philanthropy has gained considerable attention within the business world (Simanis and Duke, 2014). However, scholars have argued that BOP projects represent, at best, an incremental improvement in development outcomes amid reproducing exploitation, dispossession, and marginalization of the indigenous communities (Arora and Romijn, 2012). The relation of BOP projects with private capital actually leads to a legitimation of consumerism and marketization (Chatterjee, 2014). This dense interconnection of incremental alternatives with capital has prompted some to question their ‘alternative’ status (Fisher, 2009) since they are different only in form and are driven by the same logic of capitalism. Yet, this difference helps us in disentangling the alternative from the normative (Maurer, 2005) and in maintaining the historicity and contingency of economic practices. Maintaining this difference, then, is a strategic move to sustain the desire of building alternatives and to continuously experiment with possibilities for the emergence of another world not undergirded by market relations.

The radical alternatives, on the contrary, have anti-capitalist objectives with a competing value system. The challenge is no longer to improve the status quo but to eliminate and replace it with a better one. In that sense, these alternatives do not simply represent a tweak to the dominant model of economic organization but a potential to reconfigure it on alternative lines. Thus, the radical alternatives, as compared to the incremental ones, are more complex and are more likely to challenge the dominant system. Some examples include grassroots self-management alternatives such as worker cooperatives and alternative currencies. The metanarrative built by these initiatives is irreconcilable with capitalist logics and therefore cannot be simply integrated into the existing system by eliminating some of its problematic aspects or by inserting another regulatory constraint.

Nevertheless, the question remains as to why capitalism has not encountered more sustained and potent resistance from radical alternatives? In other words, the issue is not whether the alternatives exist inside or outside the market system or interact with it in some kind of transitional articulation, but why the radical alternatives are not able to replace capitalist values with their own. We argue in this article that this is because the alternatives can be co-opted before they can be fully explored in all of their potentiality. Hence, a phenomenal power of neoliberal capitalism lies in its ability to domesticate these alternatives. Despite their vulnerability, however, we still would like to treat them as alternatives due to their original radical intent, the alternative values they promote, and their significance in the realm of the potential.

Theory of co-optation

Herbert Marcuse, an influential member of the Frankfurt School of Critical Theory, used the term ‘repressive tolerance’ to express the idea that capitalism, as a hegemonic system, appears to relinquish some of its power and control which shows as if its challenger has gained some space. However, in reality, the alternative is only tolerated while being rendered impotent owing to its acceptance of the system’s ‘rules of the game’ (Marcuse, 1965: 83). Hence, it is possible that the apparent radical enterprises are actually reinforcing the system that they purport to resist. This is achieved when the system submits the emancipatory potential of these alternatives to capitalistic rationality and logics. Marcuse expressed this capacity of the system to ensure that the alternatives have no meaningful impact as ‘co-optation’. Following this line of thought, we define co-optation as the ability of the established economic order to respond to new radical challenges and challengers by altering their foundations. Capitalism allows emancipatory ideas to be voiced since the processes of co-optation can not only effectively paralyze their transformative possibilities but also monopolize them. In other words, the power to co-opt provides capitalism with a formidable apparatus of domination over revolutionary ideas while maintaining an illusion of tolerance for disruptive thinking. This produces a situation in which the alternatives are subverted and lose their emancipatory potential. However, Marcuse did not provide any detailed mechanism or process by which repressive tolerance leads to co-optation. In this section, we attempt to describe this process beginning with explicating the discursive nexus of knowledge and capital by using the idea of performative intent.

Performative intent

The capitalist discourse is governed by a performative intent defined as the ‘intent to develop and celebrate knowledge which contributes to the production of maximum output for minimum input’ (Fournier and Grey, 2000: 17). This intent portrays the endless search for efficiency and effectiveness following the mechanical logic of optimization while also influencing our thought categories. It generates a normative pre-commitment to efficiency (Maurer, 2005) as well as seemingly neutral categories of ‘risk’, ‘value’, ‘profit’, and ‘shareholder wealth maximization’, which are shown as inevitable, natural, and beneficial for every kind of economic activity (Engelen, 2002). However, these categories are not outside the economic reality that they purport to describe but actually constitute it (Callon, 2007), and hence will only make sense when the world they suppose has been actualized (MacKenzie, 2007). In that ‘actual’ world, the categories are transferrable across different domains with their connotative baggage intact and are then worked out and applied to create spaces of inclusion and co-optation (Fairclough, 2004). The discourse, thus, establishes its authority by shaping the identities of individuals who internalize this performative intent as well as the associated categories (Ferraro et al., 2005) and are ready to reproduce it using instrumental rationality. The vocabulary of performance sets the rules of the game and legitimizes the actions of agents working in tandem with its agenda. It also provides a hegemonic and dominant template for social and economic organization which is then available for mimicry.

Role of professionals

In order to assert their unique identity as emancipatory possibilities, the radical alternatives need to build up a non-performative intent (Fournier and Grey, 2000) geared toward, for example, the maximization of social justice or environmental sustainability or God’s will instead of efficiency. This also implies a challenge to the ‘naturalness’ of existing legitimate and reified economic arrangements. There are costs of these challenges, however, as the existing institutional players including the regulatory agencies, business councils, and international institutions such as the World Bank, International Monetary Fund (IMF), and World Trade Organization (WTO) exist to preserve, sustain, and reproduce capitalist relations (Peet, 2009). The coordinating mechanisms of capitalism are also protected by a wide range of social institutions, which appear as modes of economic control (Aglietta, 1998). As an example, consider market entry regulations, which place limits and persuade all players to conform to laws and norms of efficiency thereby acting as barriers to the development of non-performative alternatives.

Similarly, the economic space typically does not view unproven business archetypes as legitimate and, as a result, the initiators of these alternatives face significant resource constraints. They have to pay a heavy illegitimacy discount since they rank low when judged for economic appropriateness. In other words, the alternatives need to gain sociopolitical as well as economic legitimacy in an unfavorable ecosystem. For this purpose, some alternatives hire existing professionals (managers, engineers, scientists, lawyers, accountants, etc.) in the hope that they will act to establish some degree of stability by providing technical and organizational structures of control (Delbridge and Ezzamel, 2005) such as policies, rules, bureaucracy, formal incentives, double-entry accounting systems, information and communication technologies, and standardized work processes. These technologies and structures are characterized by accountability and attention to procedure in order to enable a nascent alternative to perform its activities in a predictable manner despite environmental uncertainties. Nevertheless, this requires some modifications in the alternatives based on the existing frames of reference to make them more comprehensible to the professionals.

Although the professionals might see their task as utilitarian in design, their quantification obsession creates an imaginary in which countable abstractions (of people and resources) become necessary for understanding and controlling the otherwise complex economic reality. Consider, for example, the institutionalized practices of accounting systems, which are considered fundamental for any ‘rational’ economic order and carry great symbolic significance (Miller and Rose, 1990). Highlighting activities and achievements in financial terms, as a form of rhetoric, legitimates performative practices (Cooper, 2015). International Accounting Standards (IAS), which have become globally ubiquitous, make it problematic for any country to attract investors or deal with international financial institutions without having them in place. These standards are set and overseen by organizations that are funded privately, which incline them to privilege interests and practices of businesses over societal obligations. The financialization of economy, through which financial markets are given the highest priority, is aided by accounting standard setters who ensure that issues, problems, and their solutions remain confined to serving the objective of global capital (Cooper, 2015). In this manner, the technologies act as systems to restructure the radical alternative on performative lines and play an important role in its mission drift.

In addition, most of these professionals have internalized the norms of behavior dictated by the ideology of managerialism that has infiltrated and colonized their minds (Dent and Whitehead, 2002). The lens of this ideology forces them to see the alternatives as inherently ‘risky’ due to non-conformity with their tacit knowledge and occupational socialization. The moral code inscribed in their identities motivates them to supply knowledge, which not only can reduce this risk (Beck, 1992) but also justify their professional existence. Hence, these professionals engage in constructing and spreading an argument of necessity. This argument is based on a principle of self-preservation that calls for deviations from initial values of the radical alternative for survival, effective competition, building trust of key resource providers, and for integration with the mainstream system. In summary, the professionals construct a need to inject some impurities in the alternative.

Impression management and dual discourses

The alternatives cannot relinquish their original mission since they defined themselves in oppositional terms to capitalism and this opposition was mobilized in their initial discourse to assert a fundamental difference. This difference now acquires a distinctive, central, and enduring feature of their identity and associates itself normatively to its emergent archetype. Therefore, the progenitors of these alternatives improvise and morph them into hybrids by preserving their distinctive form but accepting the performative intent. In order to protect and maintain the public image of the alternatives, however, these actors may resort to a variety of impression management techniques (Bolino et al., 2016). For example, the ‘fair trade’ movement, as an alternative to neoliberal free trade, has faced skepticism regarding its claim of a socially just international trade relationship between Southern producers and Northern consumers (Jaffee, 2007). However, in order to save its legitimacy as the protector of small agro-producers and a champion of solidarity and exchange equity, it resorted to an institutionalized certification system (such as FLOCert) to deflect this criticism and to gain mainstream visibility (Renard, 2005).

Impression management may simultaneously consist of multiple designs, including the emergence of dual discourses: one discourse for its sympathizers which highlights its differences with capitalism through elaborate ceremonial displays of confidence, while the other for economic consumption which highlights its integration and interoperability with the existing ecosystem. This allows the alternatives to send two separate signals to its different stakeholder groups. For example, it sends a signal of ‘distinctiveness’ to the stakeholders interested in its original mission while also sending a signal of ‘equivalence’ to the stakeholders interested in its performative character. The purpose of this duality is to obfuscate the compromises it has made.

Diffusion of co-opted alternative

The early co-opted alternatives gain status, technical expertise, as well as power, and are increasingly seen as exemplars or models by later entrants. Narratives start circulating about the problems faced by these incumbents and the optimality of their solutions in order to trigger an imitative response resulting in more adoptions (Bartel and Garud, 2009). Although some might point out the hybrid and contested nature of these solutions thereby introducing uncertainty about their appropriateness, diffusion can still occur due to the sanctioning and framing efforts of powerful incumbents (Litrico and David, 2017). As these change-promoting agents and new entrants start building an industry, a need arises for Standard Setting Organizations (SSOs). These organizations ‘expose firms to industry knowledge and allow for conversations and debates with the joint objective of shaping the industry’s future’ (Vasudeva et al., 2015: 833). The SSOs attempt to set agreed upon premises, auditing systems, protocols, and standards of economic behavior by promoting industry ‘best practices’ (Brunsson and Jacobsson, 2000). Hence, new organizations emerging in this milieu are impinged upon by the norms of existing arrangements and find it convenient to simply adopt the co-opted solution.

The performative intent, role of professionals, argument of necessity, impression management and dual discourses, and the diffusion of co-opted alternatives are the principal processes, which inform our theory of co-optation. Nevertheless, this theory is not deterministic as there are conditions under which the success of a radical alternative might actually be legitimate. In other words, any alternative can be evaluated based on its original intent, objectives, and its emancipatory values and/or practices. The positive results of this evaluation would mean that the alternative can retain its radical credentials. For example, Susan Esper has argued that Argentinian Worker Recuperated Enterprises (WREs) are ‘one of the few ongoing large-scale successful attempts at performing an alternative form of organization within a capitalist system’ (Esper et al., 2017: 672). Hence, it is not necessary that every alternative will be co-opted, and we might find local instances where strategies of dissent are intact. Let us now turn to the case of Islamic banking to examine the validity of this theory.

Research context

Since the radical alternatives to capitalism and the resistance that they face is socially organized, it is important to study the turf on which these struggles take place. One such important domain is the commercial banking industry, which plays a vital role in providing mediation functions for accumulating capital and is thus considered a hallmark of capitalism. The fundamental model of this industry works on charging interest on debt and usurious lending. David Graeber has documented that interest and usury have been resented and forbidden for millennia by all major religions due to their affinity with greed, avarice, and injustice (Graeber, 2011). Nevertheless, a significant development in the evolution of capitalism is the enhanced access to various forms of interest-based debt, the development of financial markets, the resulting social insecurity, inequality and oppression, and the creation of an idle class of wealth owners (Dwyer, 2018).

Distinguishing characteristics of Islamic banking

Despite its structural injustices, interest and usury became institutionalized as part of normal commercial transactions due to the growing power of banks to not only lend but also create money by issuing debt (Niewdana, 2015). This institutionalization, however, was not fully accepted across various cultural contexts including Muslim-majority countries in which Islamic law (Shari’a) provided guidelines for an alternative system. Although there are many distinguishing characteristics of this system, the most significant is the Quranic injunction against interest (riba) and uncertainty (gharar). For instance, God says in the Quran: ‘Those who swallow usury cannot rise up save as he ariseth whom the devil hath prostrated by (his) touch. That is because they say: Trade is just like usury; whereas Allah permitteth trading and forbiddeth usury’ (2:275; quoted from Pickthall, 2006). Similarly, Prophet Muhammad (peace be upon him) has ordained: ‘[d]o not sell a dinar for two dinars and one dirham for two dirhams’ (Sahih Muslim, chapter 19, book 10: 3849; quoted from the translation of Siddiqui, 1973). Since there is a prohibition on predetermined interest rate, Islamic banks cannot function on fixed returns and have to emphasize risk-sharing as well as soundness of a project instead of credit worthiness of the entrepreneur (Iqbal and Molyneux, 2005). Moreover, there are prohibitions against using uncertain economic contracts (gharar), for example, future harvest of a farm, sale of items with unspecified quality and/or unspecified price (el-Gamal, 2001), wherein profitability is the result of a sheer matter of chance (Warde, 2000). In addition, Islamic banks cannot invest in certain unlawful (haram) products (e.g. alcohol, pork, gambling) and in interest-bearing financial assets or financial derivatives. The objective of these principles is to promote an economic system based on social justice, human welfare, and equity (Mir and Khan, 2015) undergirded by a divine framework that provides moral meanings to these principles. In the words of the vice-chairman of the International Association of Islamic Banks, . . . the Islamic financial system cannot be introduced by eliminating ‘riba’ (interest) but adopting the Islamic principles of social justice and introducing laws, practices, procedures and instruments which help in the maintenance of justice, equity, fairness, and human considerations. (Mohd, 1986: 100–101)

These unique features, especially the moral dimension, are incommensurable with the secular economizing spirit of capitalism (Mir and Khan, 2015), particularly reflected in the traditional banking system, and hence provide a radical disjuncture between Islamic and capitalistic worldviews. The former centers on the Divine and privileges the hereafter over this world, whereas the latter centers on the market and values economic growth (Zaman, 2019). In this sense, any economic system emanating from the Islamic worldview will be non-performative in its nature and hence present a radical alternative. Therefore, studying the evolution of Islamic banking industry can provide an empirical illustration of our theory of co-optation.

Research methodology

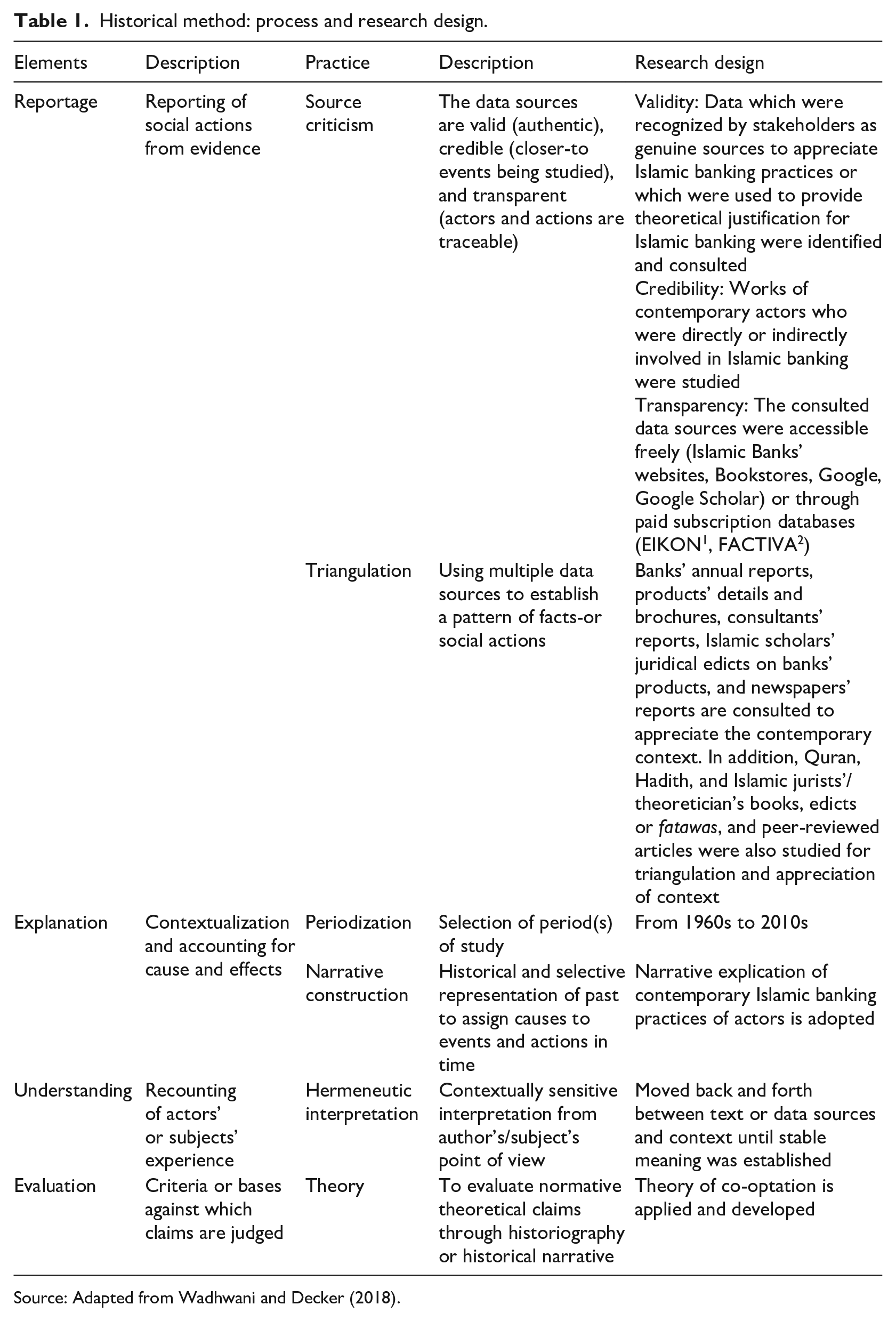

We employed the historical methodology (Wadhwani and Decker, 2018) in order to make sense of how the progenitors of Islamic banking understood this alternative and made decisions that shaped its emergence. More specifically, we followed the practice of narrative construction in order to structure the ‘evidence in ways that assign causes and consequences to events and actions through their organization in time’ (Wadhwani and Decker, 2018: 119). The objective of our analysis was ‘explicative’, which focuses on ‘applying and developing theory to reveal the operation of transformative social processes’ (Maclean et al., 2016: 613). This is a suitable objective since it not only allows us to approach the archival sources with our generalizable theoretical structure of co-optation but also reveals how people attached with Islamic Banking framed its problematics in order to generate support for organizational and industry-level changes.

The process of historical method (Wadhwani and Decker, 2018) involves (1) reporting of social actions based on valid, credible, and transparent data sources; (2) contextual explanation of causes and effects; (3) understanding or hermeneutic interpretation of actors’ experiences; and (4) evaluating the theory (see Table 1 for details). We acknowledge the problem of researcher bias, which can result from selective observations and through imposition of theory on empirical data. We avoided this bias through a rigorous methodology and by remaining more reflexive in our inquiry (Stutz and Sachs, 2018). In other words, we followed an objective and systematic methodology and also self-reflected, especially during the data analysis phase, in order to recognize and ‘bracket’ (Tufford and Newman, 2012) our own influence on the research process in the form of assumptions, beliefs, interests, and experiences with Islamic banking.

Historical method: process and research design.

Source: Adapted from Wadhwani and Decker (2018).

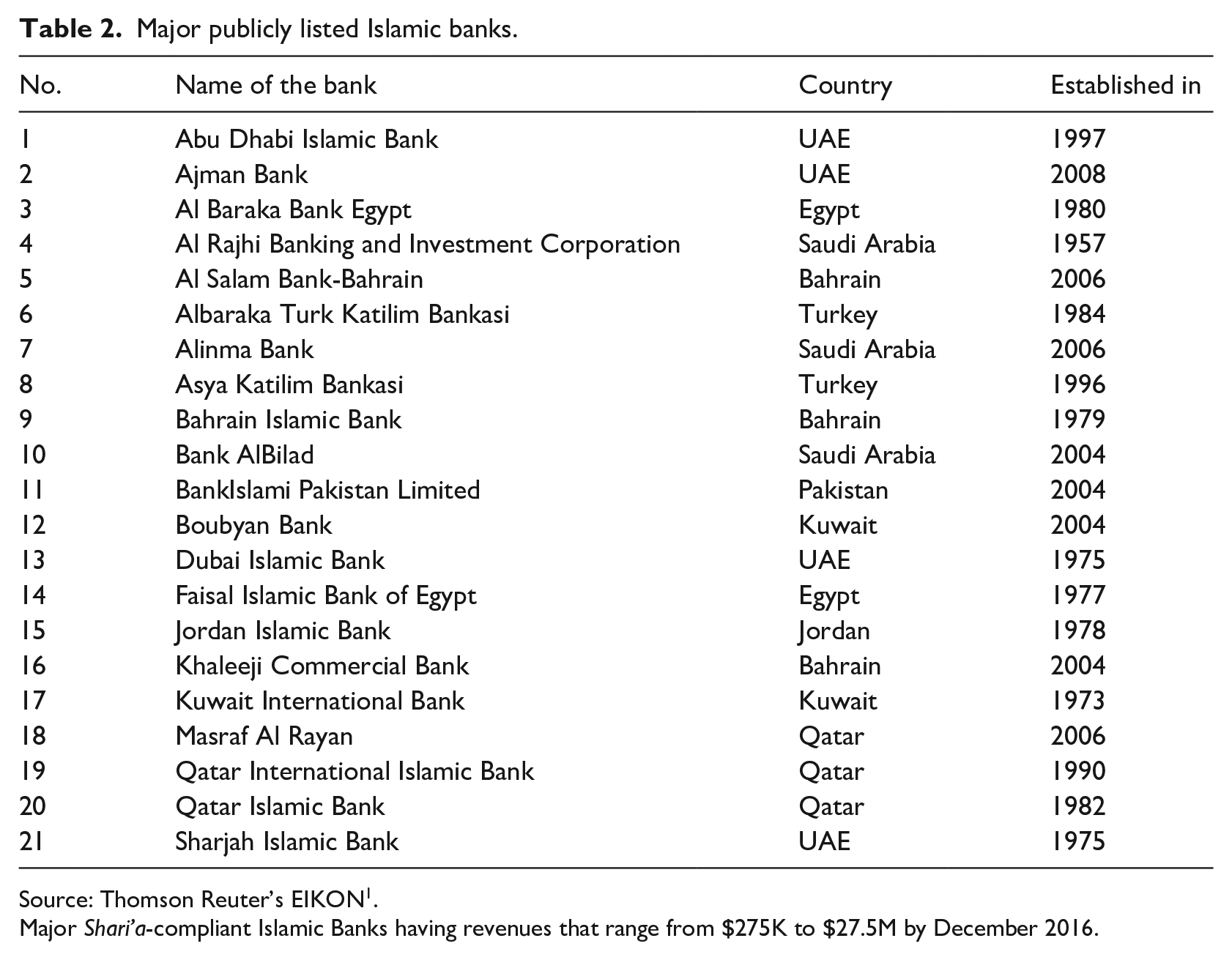

Following this historical method, we first selected the context—21 major publicly listed Islamic banks established by or in Islamic countries (see Table 2)—and period of study—from 1960s onward when the first Islamic bank was set up. The selected banks were dealing with the full range of Shari’a-compliant products and were located or had operations in major Muslim countries. We consulted the banks’ annual reports, products’ brochures and details, and edicts of Islamic scholars about Shari’a-compliance of banks’ products. This primary data were downloaded from the banks’ websites and the proprietary database of EIKON 1 . In addition, for hermeneutic interpretations and triangulation, we relied on secondary sources: Quran (scripture revealed to Prophet Muhammad (peace be upon him)), Hadith (sayings and deeds of the Prophet), consultants’ reports, newspaper articles, and Islamic scholars’ books and general edicts or fatawas for the industry. It was necessary to use an eclectic, yet carefully selected, collection of primary and secondary sources in order to produce a holistic narrative.

Major publicly listed Islamic banks.

Source: Thomson Reuter’s EIKON 1 .

Major Shari’a-compliant Islamic Banks having revenues that range from $275K to $27.5M by December 2016.

We looked for relevant consultants’ reports and newspaper stories through FACTIVA 2 using the keyword ‘Islamic bank*’ during the observation period. The resulting reports and newspaper stories were used to appreciate the context of Islamic banks’ practices, and the meanings ascribed to their practices by society and stakeholders. As frequent references were made to the injunctions of Quran and Hadith and the works of some scholars, al-Sadr (1982), Mawdudi (1947), Siddiqi (1983), and Usmani (1998), we consulted these sources for hermeneutic understanding of the banks’ practices and products’ justifications. The triangulation of sources also included books and peer-reviewed articles (listed in the ‘References’ section and identified with *). These books and articles were searched using the keyword ‘Islamic bank*’ through Google Scholar.

Based on a systematic interrogation of these sources, we construct a historical narrative, which provides a selective but adequate representation for highlighting important players (Islamic economists, bankers, Shari’a advisors, regulators), events, and actions. By following this procedure, we attempt to show the historical emergence of Islamic banking industry while uncovering the processes of its co-optation.

Co-optation of the Islamic banking industry

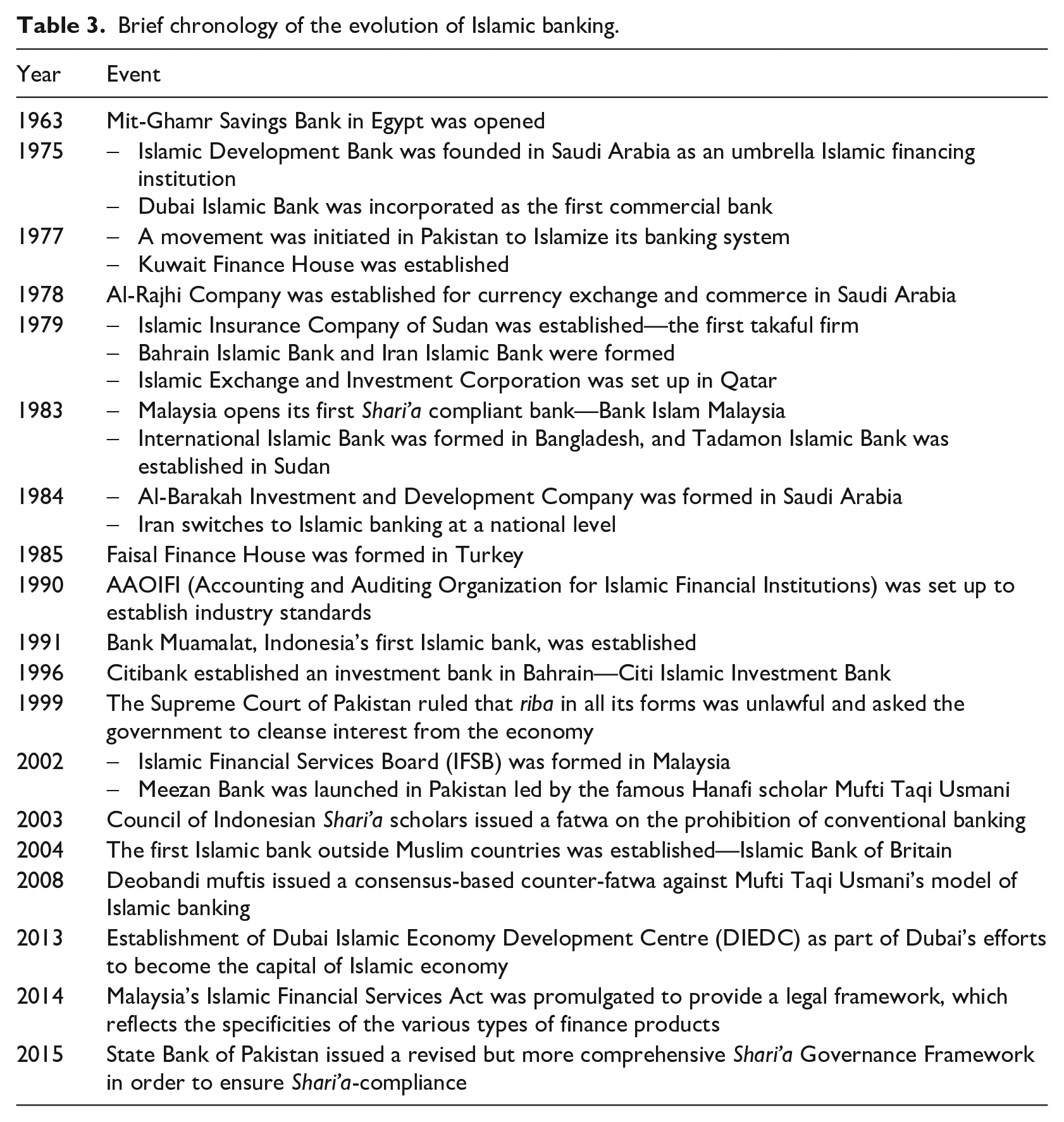

Islamic banking has expanded rapidly across the globe since its birth in Egypt in the 1970s and now more than 300 Islamic banks are functioning in 50 countries worldwide (see Table 3 for a chronology). From insignificant beginnings, the assets of Islamic banks have gone beyond $1.87 trillion in 2014 and are expected to reach $6.1 trillion by the end of this decade (Grewal, 2013). This phenomenal growth rate indicates that this industry is now an important part of the global financial system.

Brief chronology of the evolution of Islamic banking.

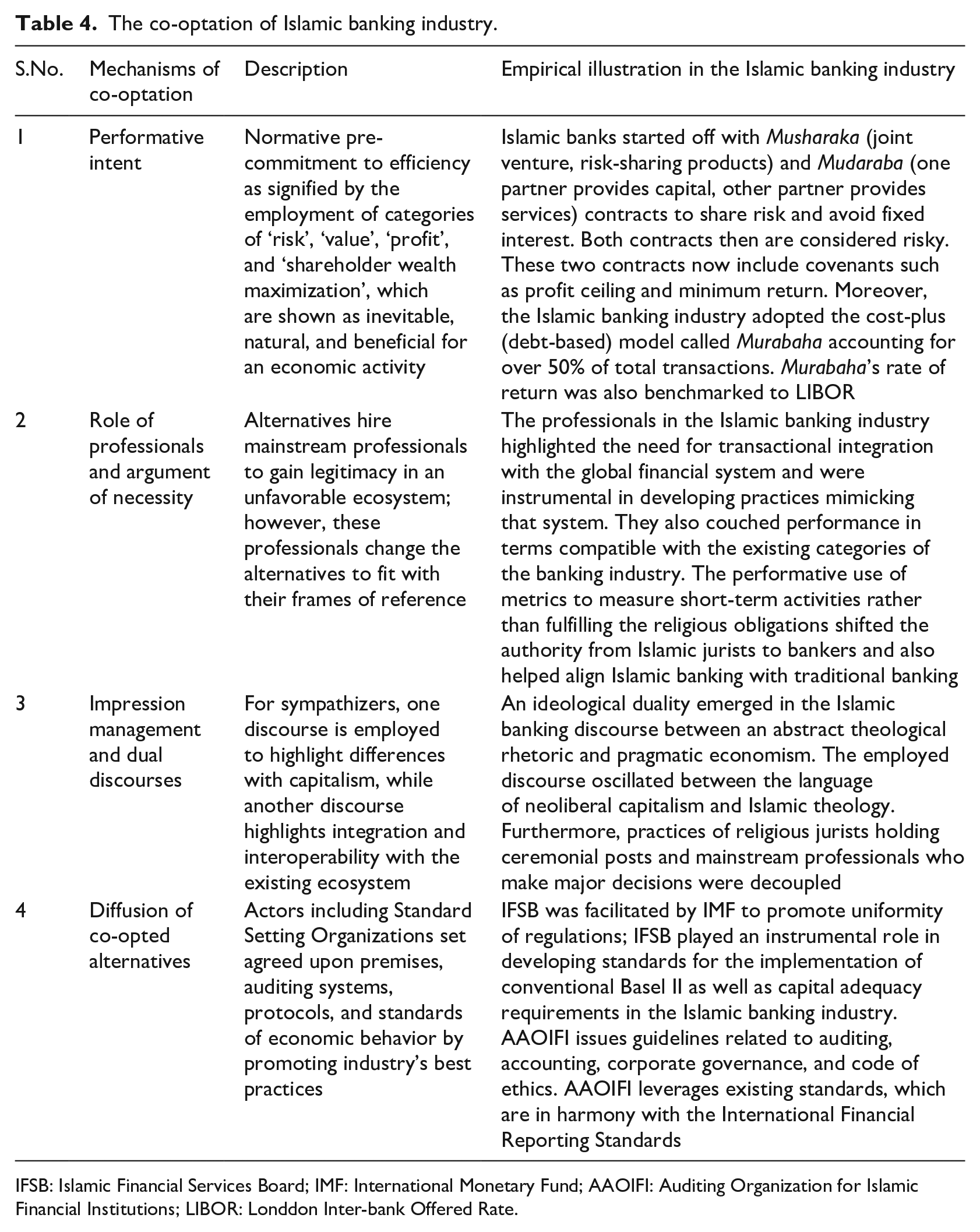

The Islamic revivalist thought of 20th century, generated in a post-colonial context, critiqued the ascendance of modern rationalism and argued for submission to divine sovereignty within the guidelines of Islamic law (Shari’a) as the legal superstructure (Lapidus, 1997). Thought leaders, for instance al-Sadr (1982), Mawdudi (1947), and Usmani (1998), of this revivalist movement challenged the desirability of both capitalism and socialism as secular systems bereft of ethical values and argued instead for a ‘spiritual economy’ (Rudnyckyj, 2010) grounded in Islamic moral principles. These scholars, besides Chapra (1992) and Siddiqui (1972), were instrumental in bringing Islamic economics as a radical alternative to the fore where it had to face the mainstream positivist economics with its powerful empiricist tenets, mathematical models, and laboratory experiments (Nasr, 1988, 1994). This encounter made many realize that it might be difficult to find an economic space to experiment with these ideas at the national economy level, and a better starting point might be the industry level (Farooq and Hunt-Ahmed, 2013). As work progressed in the field, Muslim thinkers turned their attention to a rediscovery or reinvention of classical business contracts offered as Shari’a-compliant alternatives to conventional banking products (Usmani, 1998). However, the mechanics of contracts and the instrumentalities of techniques with increased standardization came to dominate Islamic banking (see Table 4 for a summary), co-opting the efforts to produce a divinely sanctioned radical alternative (Usmani, 1998).

The co-optation of Islamic banking industry.

IFSB: Islamic Financial Services Board; IMF: International Monetary Fund; AAOIFI: Auditing Organization for Islamic Financial Institutions; LIBOR: Londdon Inter-bank Offered Rate.

Basic forms of financing used in Islamic banking

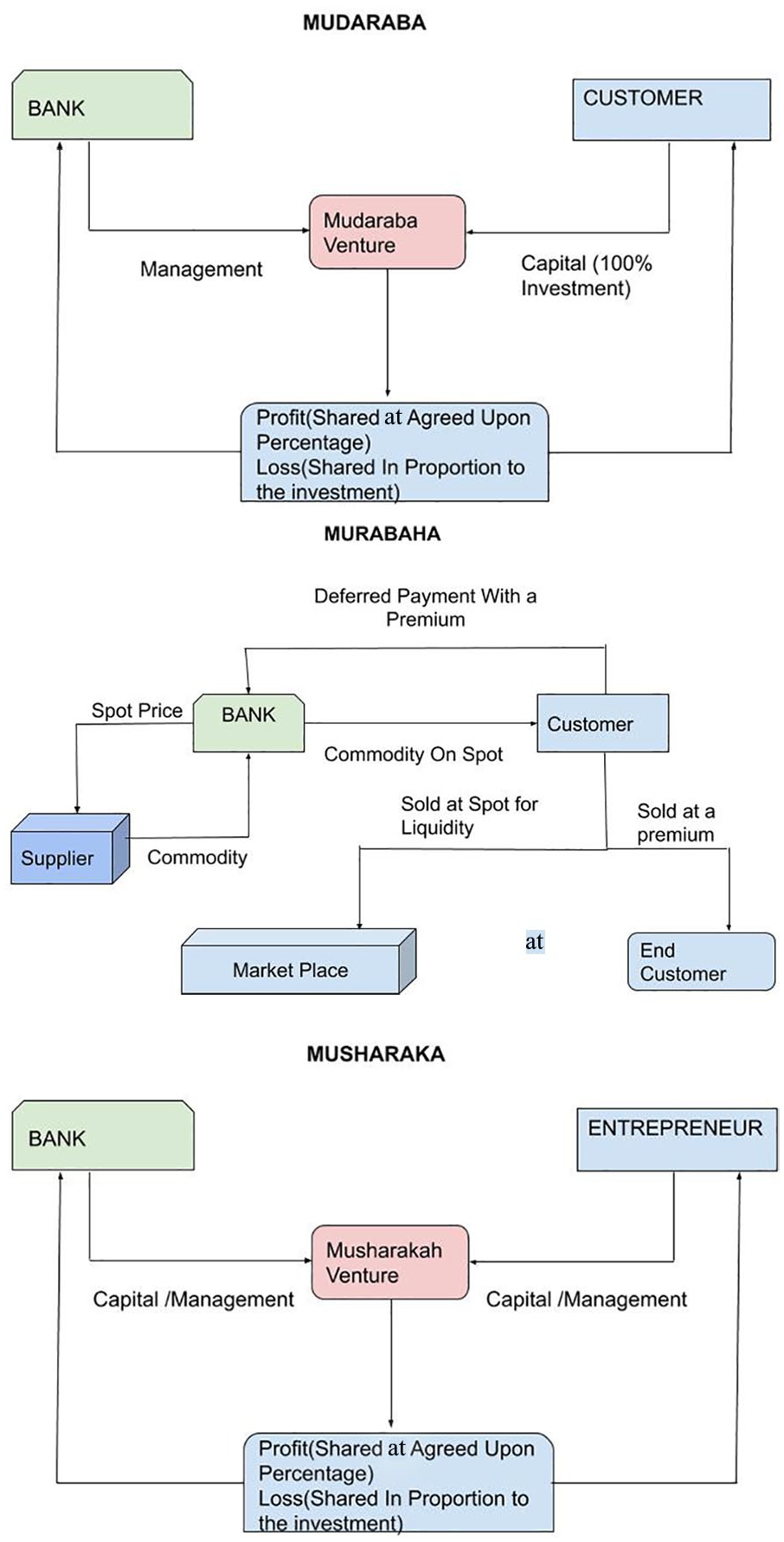

When money is invested by the Islamic bank, it is treated as potential capital (Askari et al., 2010). Hence, any return must reflect the profitability of the business being financed, which implies a sharing of profit and loss between the financier and the entrepreneur (Ayub, 2007). In this sense, Islamic banks have to share risk with their clients as they are co-investors in their business, and this can be achieved through equity-based modes of financing. This led jurists to argue, in the initial phases of the industry, that the ideal contract is either Musharaka (joint venture) or Mudaraba (limited partnership) (Kahf, 1982). Musharaka can be understood as a joint venture in which all the participants supply capital and also share in both gains and losses. On the contrary, Mudaraba is an investment partnership contract wherein the managing partner (mudarib) provides only services while the investors (rabbul-maal) provide capital for the venture. These two parties share profits generated from this business but only the investor bears the risk of losing the investment.

Nevertheless, when Musharaka and Mudaraba contracts were implemented, Islamic banks started including covenants such as profit ceiling and minimum return. They reasoned that the presence of asymmetric information in the partnership model makes it inherently risky for the bank to trust the borrower as financial statements might be falsified or creative accounting practices might be applied to manage profitability (Nienhaus, 1983). Consequently, complex administrative and legal mechanisms were needed in order to monitor and enforce these contracts (Adam et al., 2015). This led some to argue that debt-based modes of financing are more secure for the Islamic banking industry instead of joint ventures (Humud, 1976). However, this argument violated the profit and loss as well as collaborative risk-sharing spirit of Islamic contracts (Rudnyckyj, 2017), rendering them similar to the conventional long-term debt contracts. Both these contracts gradually came to be realized as risky products since the bank assumed all risks and had to rely on the entrepreneur to manage the venture.

The industry, then, adopted the cost-plus (debt-based) model called Murabaha, which became the most commonly used product for short-term financing accounting for over 50% of total transactions (Pollard and Samers, 2007). Murabaha as a mode of Islamic finance ‘. . . is predicated on the permissibility of charging a credit price that is higher than the spot price of a property’ (el-Gamal, 2006: 64). In a Murabaha transaction, the borrower pays back on a deferred basis and the bank holds ownership of the purchased products prior to the end of the contract. However, this deferred payment employs the time value of money since the Islamic bank ‘does not incur any real financial risk of ownership’ (Karim, 2010: 46). The flowcharts depicting the mechanics of these three contracts are shown in Figure 1.

Flowcharts of Islamic banking products.

This mode of financing, at least initially, faced skepticism as documented by el-Ashker in his study of Islamic banks in Egypt. In his own words: Murabaha is received with great caution . . . as it is feared that the method might open the back door for dealing on a fixed interest basis. (el-Ashker, 1987: 95)

Scholars also criticize the practice of benchmarking Murabaha’s rate of return to LIBOR arguing that tying pricing to a usurious banking metric is contrary to the profit and loss sharing principle (Karim, 2010). This linkage also forces the return to be homogeneous among all banks regardless of their profitability scale (Chong and Liu, 2009). Some studies also found the fluctuation in ‘profit shares’ of Islamic banks to closely follow market interest rates (Kuran, 1995), which implies that in practice the returns from Islamic banks are fixed just like conventional banks instead of being dependent on profits/losses. Even Mufti Taqi Usmani, who initially played an instrumental role in legitimizing these Islamic modes of financing, later admitted: Murabaha is only a device to escape from interest and not an ideal instrument for carrying out the real economic objectives of Islam. (Usmani, 1998: 72)

The argument of necessity

An important part of the process of co-optation was the argument of necessity, employed to sanction impurities in the Islamic banking industry. The argument of necessity stems from the nature and quantum of risks associated with Musharaka and Mudaraba, the ideal modes of financing. Asymmetric information, duplicitous practices of clients, and legal uncertainties were among the reasons that necessitated the widespread adoption of Murabaha, which, not being an ideal instrument, was tolerated ‘as a transitory step’ (Usmani, 1998: 72). Departing from the positions of early Islamic banking theorists, Usmani posits that there are two sets of rules, one that is ideal and applicable in normal situations (Shari’a-enabling) and another that affords concessions in the context of unusual circumstances (Shari’a-compliance), and ‘the Islamic banks are mostly relying on the second set of rules’ (Usmani, 1998: 16). Thus, a state of interim tolerance (Shari’a-compliance) was required to start scaling up the industry in order to reach the next stage where the industry could reach the stage of purity (Shari’a-enabling). However, it was not clear, in this later theorization, as to how the industry would move from Shari’a-compliance to Shari’a-enabling (Siddiqui, 2007). What started as an argument of necessity, tolerating interim impurity, actually gave rise to an Islamic banking industry grounded in and sustained by an alternative discourse of Shari’a-compliance only. For example, when asked about his views on the mission drift of Islamic banking industry due to the focus on compliance, the CEO of CIMB Islamic, Malaysia, said, . . . This debate is a waste of time. It doesn’t serve society, and it provides a dis-service to Islamic finance because it distracts it from doing what is needed. The customer is king, and the customer gets what the customer wants, as long as it is consistent with Shariah. (Wright, 2015, emphasis added)

Recognition of this permissible impurity also gave rise to many corrective mechanisms that were applied when a banking transaction was deemed unlawful. For example, if some interest was charged on a particular contract, it could be doled out as charity in order to sanitize the transaction (Maurer, 2005). Shari’a Supervisory Board (SSB) of Al Salam Bank’s recommendation, in its annual report of 2017, is ‘to ward-off the Shari’a non-compliant income from the transactions executed during the year and have it spent on charity’ (p. 67). 3 These cleansing mechanisms, however, are totally unfamiliar concepts in Islamic law (Saeed, 2011) as the mathematical equivalence between charity and impure interest income is akin to creating a formula between permissible (halal) and impermissible (haram). Despite this, the purification procedures had to be institutionalized in order to force the transactions to become moral. Other such methods include misuse of technical juristic terms, reliance on weak opinions, and acceptance of ‘. . . the practice of using [rules from] another school (madhhab ghayr) in a single transaction without completing Sharı’a conditions’ (Ghias, 2013: 109). Due to widespread acceptability of the argument of necessity, the problem set changed from the development of Shari’a-based financial contracts to the application of Shari’a principles to complex financial transactions in the interest-based system. In essence, although a language of alternative values exists in Islamic banking, it is rendered ineffectual by the hegemony of the performative discourse.

Response of the existing banking experts: defenders of the status quo

The Islamic banking industry, in its development stage, faced the challenge of hiring qualified professionals with knowledge of Western banking and Shari’a. They had to rely on traditional banking professionals who were able to control and manipulate the nascent industry’s landscape by focusing attention on comparisons with the capitalist-inspired financial architecture (Irfan, 2014). The professionals, most of whom were graduates of Western institutions, highlighted the need for transactional integration with the global financial system and were instrumental in developing practices mimicking that system. For example, the Chairman of Bahrain’s First Islamic Investment Bank said in a conference, . . . Our aim is to create credit-rated medium-to-long term investment tools with returns compatible with existing conventional products, so that financial advisors the world over can advise their clients to invest with us on the basis of returns, rather than because they are Islamic. (Tripathi, 1997)

Similarly, on the issue of benchmarking with LIBOR, the Head of Global Islamic Finance at Citigroup remarked, . . . If you come up with your own benchmark different from LIBOR or US treasury, then you won’t be able to integrate this product in the overall financial sector. (Asiamoney, 2002)

Although the knowledge generated by Muslim jurists was new, the implementation of this new knowledge depended on its generalization and abstraction by means of pedagogic devices provided by the professionals. As head of Islamic investment banking at United Bank of Kuwait remarked, The religious aspects of Islamic banking should be looked after by the Shariah experts; the commercial implementation should be handled by the bankers. (Reuters, 1994)

The bankers applauded Islamic banking as long as it was profitable, thereby assuming that efficiency somehow possesses divine sanction which does not need any further justification. Another manifestation of this thinking is visible in selecting the most appropriate governance structure for Islamic banks. In the initial days of the industry, many suggested adopting a mutually owned thrift institutional structure in which depositors are shareholders (el-Gamal, 2007). However, the bankers favored the conventional shareholder-controlled management and board structure, which created a ‘fundamental conflict of interest between Islamic depositors and shareholders’ (Nienhaus, 2007: 130). In this way, they not only reproduced the competitive logic of capitalism but also reconfigured the Islamic discourse insofar as it was compatible with this logic.

In addition, these experts emphasized the high symbolic value of rationality, which is signaled through numbers and calculations. This ‘trust in numbers’ (Porter, 1995) was supposed to help in the generation and strengthening of perceptions of objectivity and neutrality in the Islamic banking system. Quantified measures were also required to ensure transparency, accountability, and performance evaluation. The common language of numbers simplified a messy reality that helped in organizing the decision processes toward costs, profits, financial ratios, return on capital, and the like. The same financial measures allowed comparisons between Islamic and traditional banking that are otherwise, at least theoretically, different. These analogical comparisons (Ariff et al., 2011) forced the professionals to couch their performance in terms compatible with the existing categories of the banking industry. However, the same terms then started guiding their thinking and validating particular accounts without them realizing the traps of co-optation. Focused on playing the numbers game with traditional banks, Islamic bankers never measured their impact on social justice or social welfare. In summary, the performative use of metrics to measure short-term activities rather than fulfill religious or social obligations produced a governmentality that not only shifted authority from ulama to bankers but also helped align Islamic banking with traditional banking.

However, despite their embeddedness in the global financial architecture, the professionals needed to take care of the demands of their main customers, that is, Muslims, who are concerned with the genuineness of Islamic banking. For instance, the Chairman of the International Association of Islamic Banks commented, We had been living with a schizophrenic type of arrangement. On the one hand, we knew we were doing something wrong in accepting interest and on the other we didn’t admit it. (The Globe and Mail, 1980)

These Muslims represent a niche set of consumers who are averse to interest and can be conceptualized as a new category of financial subjects—the homo Islamicus (Pollard and Samers, 2007). In order to satisfy these stakeholders, an ideological duality emerged in Islamic banking discourse (e.g. annual reports of banks) between an abstract theological rhetoric and pragmatic economism. For example, after declaring a 245.60% growth rate in profits after tax, the CEO of BankIslami in its annual report of 2017 stated that ‘By the grace of Allah . . ., BankIslami completed another year with growth in key areas despite all the challenges’ (p. 13). 4 This dual discourse is significant as it shows how an Islamic banker oscillates between the language of neoliberal capitalism and Islamic theology or moves back and forth between homo economicus and homo Islamicus.

Role of Shari’a advisors

The initial Islamic commercial banks such as the Dubai Islamic Bank or Kuwait Finance House did not have religious scholars to guide their operations (Kahf, 2004). However, in order to increase the industry’s trust and legitimacy for common public, the banking regulators recommended constitution of an SSB as an additional body comprising Islamic scholars with specialized training in Islamic commercial jurisprudence. By the early 1990s, most of the Islamic banks were operating with a board of Shari’a experts (Nienhaus, 2007). The role of SSB was to oversee the activities of Islamic banks so as to ensure compliance with Shari’a tenets. It is important to note that formulation of a knowledge configuration for addressing the objectives of social justice and welfare is simply not given any consideration. In addition, the board of directors of an Islamic bank appoints and determines the emolument of advisors serving on the SSB which creates a conflict of interest.

These advisors come from Islamic seminaries—Madrassahs—and are generally not well versed in the complexities of the Western financial system (Nienhaus, 2007). This problem was resolved by Islamic banks through decoupling the governance and the product development mechanisms from the grant of religious approval. They hired Western-trained finance professionals for the former and Islamic scholars for the latter. This led industry analysts to remark: There are two forces moving in an Islamic bank: the financially educated and the religiously educated. Management is having to blend these two forces. (Khalaf, 1995: 2)

In this sense, maintenance of a strict structural organizational boundary becomes an important mechanism of co-optation. Nevertheless, both types of professionals played their part since the Shari’a advisors were instrumental in convincing the general public of the ability of Islamic banking to cater to their financial needs in a religiously responsible manner. Gradually, the intellectual flexibility of these advisors resulted in their popularity and multiple memberships in different supervisory boards (Nienhaus, 2007).

Role of SSOs

Initially, Islamic banks used to set their own accounting standards in consultation with their Shari’a advisory boards and keeping in view their national norms and interests (Abdel Karim, 1990). It was argued, however, that this fragmentation would generate problems of consistency and high risk for an industry that crosses geographic, doctrinal, and cultural lines. For example, Dr. Rodney Wilson, Professor of Economics, remarked, With Islamic banking the products are similar but there are no central standards. Different banks in different countries have different regulations. Malaysia, for example, is known to be more adventurous than the Gulf. (Bank Marketing International, 1997)

Even regulators from traditional banking pressed the need for uniform accounting standards to allow Islamic managers to allocate resources effectively and to cultivate an efficient market in this process (Maurer, 2002). In addition, it was not possible to earn network benefits without agreement on a uniform mechanism of a financial transaction. An official of ANZ International Merchant Banking argued, ‘The lack of central Sharia authority means you cannot have standardization across the market. Without standardization, you cannot have a market’ (Khalaf, 1995: 2).

These reasons paved the way for some SSOs to evolve alongside the banking industry including the Islamic Financial Services Board (IFSB) and Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), although compliance to their standards is voluntary in most cases. The IFSB started its operations in 2003 with the aim of helping the Islamic financial services industry by promoting uniformity of regulations. Interestingly, the creation of IFSB was facilitated by the IMF, which is a platform for the institutionalization of a global financial architecture for capitalism (Venardos, 2010). Therefore, the notions of what constitutes ‘good governance’ at IMF are heavily influenced by the neoliberal capitalist discourse and are used to support the ‘free market’ ideology. Hence, the standards promoted by IMF are an effort to ‘reform’ alternatives so that they can be subjected to the hegemonic international capital (Taylor, 2004). It is no wonder then that IFSB was instrumental in developing standards for the implementation of conventional Basle II as well as capital adequacy requirements. For example, under Basle II, it is mandatory for Islamic banks to disclose risk factors to the financial markets, which consequently requires accounting techniques and terminologies (Bianchi, 2007). The financial regulators in Bahrain and Malaysia, for instance, have largely adopted the capital adequacy guidelines of IFSB.

Another important body responsible for transnational standard setting is AAOIFI (Warde, 2000), which has issued numerous best practices related to auditing, accounting, corporate governance, and code of ethics (Bassens et al., 2011). Interestingly, this autonomous standard setting body decided to leverage the existing standards instead of developing completely new Islamic standards. Therefore, many of its standards are in harmony with International Financial Reporting Standards with just some additional disclosure requirements (Levy and Rezgui, 2015). It was argued that Islamic banks needed to follow certain uniform accounting standards in line with international standards in order to create the impression of technical precision for regulators and investors. However, this uniformity and harmony came with a price since traditional accounting practices and the associated discourses are squarely embedded in the capitalist logics. In summary, Islamic bankers simply imported all the conventional accounting ideas and never questioned their value neutrality and relevance to Islam (Lewis, 2001).

The above discussion informs us that engaging in Islamic banking is no longer about commitment to divine commandments or social justice, but about performing at the most efficient level in comparison with traditional banks—a clear diversion from the original radical intent.

Discussion

In this article, we were interested in analyzing the processes by which capitalism engages with radical alternatives in order to thwart their revolutionary potential. For this analysis, we traced the development of Islamic banking industry, which emerged from bold but determined efforts to build such an alternative by partially reconciling modern economics with Islamic moral tenets. However, we observed that due to its reliance on existing capitalist discourse and techniques, the more the industry increased in size and economic significance, the more it resembled a conventional banking industry focused on economic efficiency instead of the original mission of social justice and redistribution. The entanglements with capital ultimately challenged Islamic banking’s proffered boundaries and solidarities as a radical alternative, which now presents a compromised situation of coexistence. The compromises made by the industry eventually drew a response from a section of Pakistani Muslim scholars in the form of a collective fatwa (edict; Ghias, 2013) against modern Islamic Banking. The fatwa revealed a cleavage within the community of Shari’a scholars, with one side arguing that ‘Islamic banks are not following the theoretical foundations of Islamic finance’ (Ghias, 2013: 104) and are therefore not distinct in their current form from conventional banks. In the fatwa proponents of Islamic banking are criticized for their reliance on devious interpretative methods such as cutting and pasting of juristic terms and fusing legal opinions of different schools of law. It lists several instances of mistakes and errors committed due to the violation of principles of jurisprudence. Focusing, for example, on Murabaha, it ventures into details of how Murabaha is used as a hila (stratagem) in Islamic banks and is not ‘an agreed upon Islamic financing instrument’ (Ghias, 2013, 109). It is argued that the manner in which Murabaha is executed not only falls short of the actual juristic procedure but even disqualifies it as a kind of sale. The practice of forced charity, which Islamic banks levy in lieu of penalty for late payment of rent, is also seen as a fallacious attempt to render interest permissible. What this fatwa exhibits, despite being more concerned with juristic and pedantic fault-finding, is an appreciation of the inadequacy of the enterprise in remaining true to its own radical ideals.

As the realm of the co-opted alternatives expands into society, it likely sparks a counter movement with the aim of protecting the sanctity of the original mission. These counter movements can take a specific cultural form depending on the peculiar nature of the radical alternative and can construct a moral frame through which the co-opted alternative can be problematized and stigmatized. Through this moral frame, the counter movements might call for a boycott of the products or services as a form of resistance tactic. Hence, the alternative exists in perpetual tension with its counter-logic. The edict against Islamic banking can also be recognized as a form of textual resistance against co-optation, which serves to dismantle the illusion of the industry offering any kind of radical alternative to the existing system. Although it is hard for the Islamic banking industry to now modify its course owing to its huge scale and scope of activities spread all over the world, we still want to point out how it can remain compliant with the letter and spirit of Islamic guidelines. First, it would need to reject the instrumental means-end rationality of performance goals and shareholder wealth maximization, and construct a non-performative intent. In other words, it needs to engage with the rich Islamic tradition to generate a radical imaginary focused on improving social justice, reducing inequality, and asserting non-market values. Unless there is a change in representations, there is a high chance that their efforts will be co-opted. Subsequently, the industry might decide to go ‘beyond debt’ (Rudnyckyj, 2019) and revert back to the original equity-based modes of financing and partnership models with a mutually owned thrift governance structure for the banks. This line of action requires many experiments and is a good avenue for future research.

Moreover, in order for an alternative to become a transformative force, it needs to develop new discursive strategies adept at subverting the entrenched symbolic order of mathematical commodity relations. The only viable way forward is to stop playing the game of the capitalist and focus our energies on reframing the discourse from efficiency and competition to other spheres of civil society. Consider, for example, worker cooperatives as an alternative organizational form and how competition with capitalist firms resulted in marginalization of its original values of self-help, democracy, solidarity, and equality (Cheney et al., 2014). This mission drift led scholars to formulate a ‘degeneration’ thesis (Storey et al., 2014) to argue that most cooperatives transmogrify into a capitalist enterprise when employees are excluded from ownership, when pursuit of profitability supersedes the original values, and/or when management hierarchy is introduced producing inequalities.

Extending the earlier works (Ibarra-Colado, 2006), we can also conceptualize the project of Islamic banking as based on a Southern alternative imaginary with some revolutionary potential. Capitalism, however, exerted its control over this imaginary not by repressing or imposing constraints but by channeling its forces to reproduce and extend itself. In this sense, co-optation is a subtle form of ‘epistemic violence’ of the Global North which ‘involves silencing, subjugating, diluting and distorting Global South voices’ (Khan and Naguib, 2019: 91). In this particular distortion, the opposition is not negated or vilified but embraced as the Other and then channeled into a productive form. Even the antagonistic vocabulary is tolerated because its essence has been trivialized. In other words, the subalterns can now speak for themselves as even their most flamboyant speeches will only reflect the acceptance of their subjugation.

This dire situation demands an urgent ethical response in terms of ‘epistemic healing’ (Khan and Naguib, 2019) whereby the marginalized knowledge systems such as Islam are brought back in discussion with their unique theological commitments. We also need to rethink the problematics of liberating agency in order to resist co-optation. To that end, we echo the position of Khan and Koshul (2011), who argue that ‘[a]gency can also arise from maneuvering with and within the self’ (p. 317). The realization of the nature and characteristics of one’s selfhood can generate higher forms of intellection, which can provide a frame of reference where subversion starts making sense.

Our saviors could be academics, intellectuals, and scholars (Esper et al., 2017), whose critique can play an active role in reframing existing representations and producing new identities (Cabantous et al., 2016); creating alternative organizational models, forms, and archetypes (Leca et al., 2014); and finally linking these identities and models to contemporary social movements (Willmott, 2013). These scholars as ‘progressive educators’ (Esper et al., 2017) can embed the alternative in a moral sphere where it would be easy to specify the ethical principles for evaluating new economic models. This is important for critical theory as it focuses on emancipatory possibilities instead of a simple deconstruction of the world. Indeed, if the theory and practice of action and resistance loses its prominence in the critical discourse, it would be, quite ironically, imperiled by the same co-optation it seeks to expose. We thus invite future researchers to extend our work by explicating how co-optation can be resisted.

An engagement with history and literature might be of use here since this will show us that the economy was not always the center of attention and will provide us a radical imaginary of a humane world, which can help us in not only generating a non-performative intent but also reinvigorating the emancipatory commitments of critical theory. Hence, we do not wish to leave our readers with disappointment but with a principle of hope, to use Ernst Bloch’s term, which permeates every man’s consciousness and to say that another world is possible.

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.