Abstract

Markets and finance have long attracted ethnographic interest but the nature of their activity – opaque, secretive and increasingly placeless – precludes traditional ethnographic fieldwork. In this article, we propose documents as an alternative access point to these organisations as an ethnographic object of enquiry. Documents do not only present a written record, but they also enact relationships and encode tacit understandings. We develop Geertz’s work on the bazaar by taking an indirect route to access the field site – collateralised debt obligation – through documents. In reading these documents, we assume the position of investors who, in the absence of alternative publicly available information, are dependent on the documentary accounts made available to them by the sellers. These media act in ways that are similar to tourist guidebooks, a comparison we use to reframe the exchange as one that builds upon sociocultural relations rather than the abstract market relationships described by mainstream economists. We propose that these documents are not merely representational artefacts of the organisation but serve to establish and maintain social relationships between buyers and sellers through the management, standardisation and ritualisation of information disclosed to the investor.

Finance as dilemma for fieldwork-based ethnography

Markets and finance have long attracted ethnographic interest but certain qualities of their activity – opacity, secrecy, specialised argot – erect barriers to traditional ethnographic fieldwork. There are two fundamental problems for traditional ethnographic work related to access and place.

In terms of access, there has been a small number of high-profile ethnographies of financial markets, actors and places over the past two decades – Abolafia’s (1996) seminal Making Markets, Riles’ (2001, 2011) The Network Inside Out and Collateral Knowledge, Ho’s (2009) Liquidated and Luyendijk’s (2015) Swimming with Sharks, to name a few. However, gaining access is notoriously difficult in ethnographic fieldwork and involves the careful negotiation of complex and sensitive access issues with gatekeepers (Amit, 2000; Reeves, 2010). In finance, this may become even harder as the examples of tax avoidance, market manipulation and mis-selling grow.

Second, there is a more fundamental problem when locating the place of finance. All of the aforementioned ethnographies are located in the well-recognised spaces of banks in the City of London or Wall Street or in central banks or (stock) exchanges. The existence of the observable and bounded place solidifies a specific financial activity’s culture through its ‘commonality of use’ which ultimately has a homogenising effect on how people think about and interact with that place and the activity (Lefebvre, 1991: 56, 287). This gives these activities their cultural identity, a certain rootedness (Arefi, 1999) pronounced through common cultural references and states of belonging. These are commonly captured by ethnographers: working at Goldman Sachs, trading on Wall Street, having a client lunch and so on. This may have promoted the idea of financial activity as in situ, as place-bound and exclusive to spaces like the trading floor or the securitisation desk. In other words, these ethnographies encourage an understanding of finance as having a spatial fixity.

But finance is not fixed; it is also a discrete entity where closure is ‘imaginary’ and cultural, rather than physical, through the formation of a ‘new form of collective identity’ (Palan, 1999: 56). We are interested in finance’s relations to hidden financial worlds – its fluidity and its looser, assemblage-like structure – where finance is an abstract space that can be defined by complexity, tacit agreements, internal logics and reciprocity (Lefebvre, 1991: 56). In this abstract space of finance, there is an emphasis on socio-technical relations, as illustrated by Beunza and Stark’s (2004: 370) work on the ‘quantitative revolution of finance’ or Knorr-Cetina and Bruegger (2002a) on the emergence of global virtual societies – activity is facilitated by connectivity, knowledge flows and computing technologies, where relations are ‘entirely exteriorised and embodied on computer screens’ creating ‘postsocial relationships’ (Knorr-Cetina and Bruegger, 2002b: 162). These accounts draw a picture of finance as global and disconnected to a particular physical space, as replaced by virtual markets that enable exchange, and provide a new medium for observation. Yet, finance is best understood as non-modal, it is neither ‘one mode […n]or another’ (Maurer, 2012: 415): it has a certain fluidity about it, both in space and time. It both requires and does not require a place of production; it both requires and does not require physical transport to fulfil its destined impact. Finance needs the back office and the exchange in and as places, and the physical movement of assets and ownership. These physical locations format and limit the field because of enablements or constraints of spatially demarcated legal jurisdiction and the facilitation of face-to-face interpersonal relationships. Yet at the same time, the places and the spatio-temporal origins and destinations are insufficient referents for financial activity that ramifies through social and virtual networks and that is subtended by a whole other network of infrastructures, documents, proprietary recipes and formulae (Lepinay, 2011).

This problematic becomes obvious once we travel into the opaque and secretive world of complex and private financial activity that purposefully exists outside of the public realm and regulatory space, hidden behind obscure and non-physical walls of jargon and claims of expertise, and also often in far-away places, at least ostensibly so. Again, the place is both required and not required; transport matters and does not matter. One of us (Maurer) has done conventional ethnographic fieldwork in this world: sometimes physical walls and mirrored glass doors kept him out; but other times, he got ‘in’, even if through roundabout ways – at the bar, on a run, at court, or best of all, accompanying dog-walkers. Still, there are limitations. The offshore is a place where the homo economicus is both existent and obsolete, local and global (Knorr-Cetina and Bruegger, 2002a). For example, the commanding rise of new non-physical spaces of finance over the past three decades – the emergence of over-the-counter (OTC) derivatives and financial technologies – changes how we engage with traditional places of finance, such as the British Virgin Islands (BVI; Maurer, 2000). What is more, spaces of activity are ubiquitous and non-specific, or as Appadurai (1990) puts it finance is a ‘mysterious (…) and difficult landscape to follow’ (pp. 298, 302). These ‘shadowy realities’ are both a known entity – shadow banking, shadow rules, unregulated markets are the stuff of the business pages, after all, but at the same time, they remain unknown, out of sight, except for occasions where extreme events break down walls and shine light onto this particularly murky world of finance (O’Doherty et al., 2013).

Rethinking the collateralised debt obligation: from ideal to actual market

Collateralised debt obligations (CDOs), the object of study in this article, are a prime example of this increasing opaqueness of financial services, despite talk about transparency and accountability (Bernanke, 2010; Issing, 2005; Pina et al., 2007). The obfuscation created by the term ‘CDO’ itself as noted by Lanchester (2014) is, however, more than smoke and mirror; it echoes the underlying complicated realities of the CDO product, its organisation and the associated activities.

Both prior and following the financial crisis, financial economists tended to frame CDO activity within the context of the market (see, for example, ECB, 2004; Greenlaw et al., 2008; Haensel and Krahnen, 2007; Hull, 2009; Hull and White, 2004; Longstaff, 2010). But the very idea of a ‘CDO market’ is problematic because in the absence of detailed descriptions of how the market functions and organises, it invites us to think of these markets as exchange markets (we might call them ‘economists’ markets’): a transparent interface used by buyers and sellers to discover and adjust market prices depending on supply and demand (Knorr-Cetina, 2006: 553f.). In these types of markets, relationships between actors are assumed to be arm’s-length, non-repetitive and price-driven, and freely available, transparent information is crucial to pricing mechanisms in exchange markets (Bloomfield and O’Hara, 1999; Fama, 1969; Malkiel, 2003).

But CDOs do not neatly fit this imagery of the ideal market. They are organised on the basis of private exchanges between two sophisticated (counter-)parties, where one agrees, given the information documented, to engage in a transaction with the other, through the medium of a legally binding contract (D’Souza et al., 2009; Heckinger et al., 2014). The private nature of these deals, that is, for example, the withholding of price details that are a known quantity in an exchange-traded markets, means that these trades are secret and remain outside of the public realm. Indeed, Huault and Rainelli-Weiss (2014: 182) estimate that only 11% of derivative trades go through public exchanges, while the remaining 89% are ‘traded’ OTC. Thus, transparency rules and regulatory oversight only apply to a fraction of activity in this market and this limits access to information (Huault and Rainelli-Weiss, 2014).

This is not to say that the activity we observe for CDOs is not ‘a market’; it is simply a different type of market from that described by economists. By considering a broader definition, we can acknowledge that markets may take on various forms and have an inbuilt plasticity, that is, ‘the capacity to take and retain form’ (Nenonen et al., 2014). Hence, empirical markets, in particular financial markets, seldom conform to the economists’ ideal-type; instead, their form and functionality is enabled and shaped by different cultural and interactional patterns (Knorr-Cetina, 2006). They can be understood as collective responses to a particular problem or opportunity, and as such present a compromise reached between multiple actors with divergent interests (Callon and Muniesa, 2005). This need to compromise can, for example, be illustrated following White’s (1981a) model of actors as ‘tangible cliques’. These cliques signal and feed back to each other which induces an order – the ‘terms of trade’ – which sustain (or change) this particular structure, the markets initial form, over a period of time (Baker, 1984; White, 1981a: 571). Over time, these interactions diffuse and homogenise norms and behaviours across networks resulting in shared behavioural expectations (Baker, 1984; Dyer and Nebeoka, 2000; Rowley et al., 2000). The relationships therefore create a ‘social structure sustained by the self-interested choices of its constituent actors’ (White, 1981b: 2), stability-inducing mechanisms that allow the market to retain its form (Nenonen et al., 2014) where ‘reputation, trust, reciprocity, and mutual interdependence’ are necessary preconditions (Larson, 1992).

Tischer and Leaver (2017) make this point about the CDO market. They demonstrate that CDOs are not a product of one investment bank but are rather assemblages made possible through interactions between multiple, geographically dispersed actors with specific expertises which are brought to bear on the product. Their work highlights how each CDO can be understood as a network organisation where (1) any actors’ ability to generate income is interdependent, (2) power to affect outcomes is distributed and (3) norms are embedded in social relationships formed through repeated interaction. But unlike producer networks that endure through long-term supply chain agreements, clique membership is transient and variously recombinable: functional expertise may be offered to multiple producers of CDOs (i.e. investment banks).

But these market-configuring network relationships are difficult to discern for both insiders and outsiders for an additional reason: they occur in various jurisdictions scattered around the globe. They are translocal by design, made up of complex networks of organisations that ‘cross-cut and inter-mesh’ temporarily (to produce a CDO) before parting ways and reconfiguring their relations (Garstens, 2010). There is no specific space or locale where interaction takes ‘place’, rather, such assemblages are constructed through digital channels of communication. Under such circumstances, we ask whether it is possible to engage in traditional forms of ethnography to understand this kind of phenomena. Is it possible to produce an ethnography in these placeless places, or non-places (Auge, 1995), through the traces of the artefacts they leave behind? Is it possible, in other words, to advance a particular type of ethnography in studying finance through its documentary traces?

To state our methodological argument at the outset, we develop a type of ethnography based on the documents of CDOs, supplemented by background knowledge acquired by one of us in more conventional ethnographic fieldwork in an offshore jurisdiction, the BVI. The BVI research helps to situate the institutional space of the CDO market somewhat – but only to a point. As we noted earlier, physical, geographical space both is and is not a requisite of this market. We develop an ethnographic approach to those ramifying networks of expertise and the evidence they leave behind as documentary traces and deduce what we can from these documents in motion and in relation to one another and to physical spaces. But, as with physical space, the documents both do and do not matter: they are performative and obfuscatory, didactic and misleading. Nevertheless, we can ask questions of them, and with broader ethnographic context at our disposal, we get better at learning how to ask (Briggs, 1986). Fortunately also, every ethnography can also be supplemented by the entire ethnographic record, our own documentary traces, so to speak, left behind from others’ fieldwork.

In this case, we turn to Geertz’s (1978) ethnography of the bazaar and draw an analogy between the CDO market and the bazaar, which serves as our analytical framing device. We do this precisely because the idea of the bazaar offers insights into structures that are much less transparent and more opaque than the economists’ market, structures where relationships between actors rely on trust, repeated interaction, information sharing and information withholding, or secrets. We develop and expand the traditional idea of the bazaar as postulated by Geertz by taking into account recent changes in actually existing bazaars through alien influences: the introduction of tourists, for instance, may put strains on and alter how bazaars function, in particular, because of the limited ability of tourists to engage in a knowledgeable and sophisticated fashion in this setting. To the tourist, haggling is part of the show, and they glean tips on how to do it from guidebooks. The tourist’s haggling is not the same as the everyday reality for insider participants, which may rarely be objectified as a culturally specific mode of market engagement.

We argue that documents can help us to understand bazaar-like economic settings of the CDO ‘market’, where investors take on the persona of the tourist, reliant on documents, rather than learned experience, which ultimately puts them at the mercy of the information contained in these documents to make judgements about what constitutes a good deal. Maurer’s (2000) conventional fieldwork in the BVI shows that investors rarely have much understanding of what they are getting themselves into – they rely on networks of expertise contained in registered agents of trust companies and financial advisors, offshore legal and accountancy firms and, when they get into conflicts with one another, the courts. But even the experts rarely have a full view of what they themselves are proffering to these investors. Partly, of course, this is the point: complex offshore structures are made purposefully complex, to find a way around the letter of the law or to put up barriers between the investor and the regulatory authority, the business competitor or the estranged wife. CDO documents similarly operate through misdirection and purposefully produce knowledge gaps, as we discuss further below. Nevertheless, these documents are more than just documentation; they are produced for very specific reasons.They act as informants that guide and encourage participation and in doing so they present particular aspects of the deal that are seen as enabling a private exchange between buyer and seller. Documents thus become our respondent, in our own analytical foray into the CDO market: they act as ‘response to query’ (Riles, 2006: 6).

Known ignorances and maldistributed knowledge: the bazaar as analytic idea

We should state from the outset that we are not trying to claim that the ‘CDO market’ is like an actual bazaar: neither is it what Geertz (1978) calls penny capitalism nor is it an ‘institution so embedded in its sociocultural context as to escape the reach of modern economic analysis altogether’ (p. 28). Indeed, in some ways, CDOs are the opposite of such a view: they are highly complex, ‘exotic’ financial products that have, almost exclusively, been subject of modern economic and financial analysis (Crotty, 2009; Longstaff and Rajan, 2008).

Yet, in certain respects, beneath this veneer of CDOs as an economists’ market, CDOs transactions exhibit bazaar-like qualities because information is partial, ignorance is high and clientisation is a key trading mechanism to moderate the problems arising from the partiality of information and the low levels of understanding about the product on the part of the buyer. Similarly, the bazaar, as an institution, possesses specific structural characteristics, underlying rules of the game and cultural norms of exchange. Yet, as Geertz (1978) points out, the bazaar is more than that: it is an analytic idea, one that enables a more theoretical engagement of the economic activity observed, one that incorporates ‘sociocultural factors into the body of discussion rather than relegating them to the status of boundary matters’ (p. 28). It is in this metaphorical sense that we consider the CDO market to be like that of a bazaar.

For Geertz (1978), a bazaar is a multiple set of contextualised realities with commonalities across a set of core characteristics; yet, specific bazaar experience may not be generalisable beyond the specific setting in which it is observed (Keshavarzian, 2007: 68). As noted by McMillan (2002), bazaars are a distinct form of economic organisation which call into question the omnipresent framing of any economic activity as market, with its emphasis on the importance of perfect or near-perfect information and rational, calculating subjects.

Bazaars are different not only in terms of the processes by which they operate through a system of social relationships rather than rational, contractual obligations, but by the flow of information, or the privation thereof. Information in bazaars ‘is poor, scarce, maldistributed, inefficiently communicated, and intensely valued’ (Geertz, 1978: 29). This lack of information, however, is known and accepted as such by participants in this activity, or as Geertz puts it, a ‘known ignorance’ upon which trading activity is initiated and negotiated. Known ignorances are subject to degrees of knowing and/or the ability to accurately read and translate an activity. Knowing and not knowing are not diametrically opposed, but rather fluid descriptors with a large overlap. Thus, people move through their repeated interactions in the bazaar in a way that reflects their prior experiences. So rather than treating known ignorance and unknown ignorance as dichotomous variables, they should be considered along a multidimensional spectrum, one that describes a multiplex or multi-level phenomenon nested within known and unknown ignorance.

However, for such a known ignorance to exist, buyers require prior experience, or at least a conceptual understanding of basic functions of the bazaar, building upon which, a firsthand experience of trading activities and the processes involved will eventually enable the buyer to become accustomed to them, to establish sufficient knowledgeability. For Geertz (1978), two processes are important to establish knowledgeability: first, information search and second, clientisation. The former describes the key process of searching for signs that informs the buyer about the current state of the market in the absence of standardised and visible prices. These signs, if correctly translated, will give the buyer a better understanding of prices and quality of the product. To reduce the cost of information search, buyers of the same good also show a tendency to seek to establish relationships with particular sellers of these goods (Geertz, 1978: 30) in absence of random selection based on price. This clientisation is based on reciprocity rather than dependency; both parties acknowledge that alternative opportunities to seal a trade exist and utilise this to make a deal, which is seen as advantageous to both parties. Clientisation thus has an organising effect that partitions the bazaar into overlapping groups, within which insiders benefit from better information availability.

These features clearly highlight the bazaar as an institution that is much more dependent on social mechanisms to function than is assumed in economists’ markets associated with ad hoc, price-driven mechanisms co-ordinating parties in a transaction. Relationships between buyers and sellers in these settings are thus embedded; there is a common appreciation for price setting, prominence of products and people and behavioural etiquette (Geertz, 1978: 30). This knowledge, according to Geertz, renders these settings familiar, or ‘home’-like.

The curious case of the ‘tourist’ in Geertz’s account

It is, however, important to note that Geertz’s observations of the mechanisms of known ignorance and clientisation derive from his primary focus on the relationship between traders, justified by the empirical reality where participant actors oscillate between roles as buyer and seller (Fanselow, 1990: 251). And while this may indeed capture much of the market activity, there are other local or native actors who only act as buyers of goods. These actors are disadvantaged to some degree depending on the frequency in which they engage with (specific) traders in the bazaar, but they possess the sociocultural understanding gained from past experience to navigate the bazaar environment successfully.

But Geertz’s account also notes ‘tourists’ as something fundamentally different to those who are native and knowingly ignorant. Tourists are viewed to be part of a setting they do not understand and which is alien to them (Geertz, 1978: 31). Unfortunately, Geertz does not go into any great detail about why tourists matter in the wider bazaar system. Tourists are simply viewed as not belonging to the bazaar with a different social and economic relationship with the traders relative to those who are knowingly ignorant. In the modern context, the bazaar is open to everyone; everyone can dip in and out, immerse themselves in it or spectate. But by definition of their status as aliens, tourists will find it more difficult, if not impossible to engage in the same manner as locals would. This is because tourists lack an understanding of the complex web of relations, the importance of information seeking and social etiquette that are key processes in the bazaar exchange. Clientisation of the trader–customer relationship commonly used to alleviate some of the information limitations does not apply to tourists. In his account of peddlers in an Indonesian village, Geertz (1963: 36) notes traders’ reputation for being unscrupulous and lacking ethics when dealing with (peasant) buyers that only travel to the market occasionally. But rather than arguing for these to be expressions of the traders’ normative dispositions, he argues that such devious behaviour can be explained by ‘role asymmetries’ between the alien buyer and the native seller. Buyers are constrained in their ability to act because their role places them outside of the bazaar. They lack the knowledge and information to engage effectively with traders, and what is more, their position as occasional buyers makes it difficult for them to overcome this disadvantage, to gain access to information. It is not simply a matter of the availability and quality of information that limits the buyer’s ability to accurately assess product quality and price, but a matter of their position. The bazaar tourist assumes a similar asymmetric position to that of the occasional peasant buyer and is thus equally likely to be subjected to seller’s mis-selling and poor practice.

For Boorstin (1961: 85), tourists search for experiences passively, and their quest is fundamentally opposed to the active nature of relationship building and information seeking described in Geertz’s accounts. Tourists, even when in possession of guidebooks, brochures and other information, are not in control; they are at the mercy of what they have been told and what they are presented and offered by the local. The local seller assumes power and sets the terms of the trade. If we follow Boorstin’s logic, even travellers, a more active and sophisticated version of the tourist, would be at a disadvantage in the bazaar-setting because of its distinctive character. The bazaar builds on long-term relationships and space specificity, that is, the true nature of each bazaar is different, yet subject to an overarching idea of the bazaar as an analytic concept. Thus, clientisation, the reciprocity of relationships in bazaars, is restricted to naturalised, repeat buyers, whereas one-off customers, such as tourists, either overpay for their product, as noted by Geertz, or are required to recall foreign yet similar experiences to guide them through the process. In particular, the tourists’ passivity becomes problematic given the absence of prices on display and the lack of quality assurances. Thus, tourists and traders alike must begin to rely on signalling systems to some degree. In short, the relationship between buyers and sellers is not a reciprocal one, but one of dependency of sellers on tourist buyers.

This returns us to Geertz’s claim that the bazaar is more than a physical place, it is an analytic idea. By treating the bazaar as an analytic construct, we are able to transpose key conceptual elements to our case, despite the aforementioned absence of a space. Instead, we use documents issued for each CDO to uncover the bazaar-like features of the relationship between investors in and sellers of CDOs with the aim to gain a more subtle understanding of relationships and interactions between investors in and sellers of CDOs in situations in which economic exchange occurs, but which are unlike mainstream markets. Investors, like participants in the bazaar economy, differ between those that oscillate between acting as buyer and seller, for example, big financial conglomerates that created and purchased CDOs, and those that solely acted as buyers of CDOs without any in-depth experience of the assemblage process itself. It is the latter we will explore in more detail. Doing so allows us to focus attention towards the private, secret and opaque facets of these activities which clearly speak to the information scarcity and social etiquette expressed in Geertz’s account of the bazaar.

Unravelling secrecy through the media of documents

Anthropology has a venerable history of engaging with its subjects’ secrets; indeed, in a recent review, Jones (2014) argues that ‘secrecy has a long-standing status as a paradigmatically anthropological topic’ (p. 52). From studies of secret societies and initiation rites (Beidelman, 1993) to an understanding of discretion and disclosure as central to small-scale and state-level political organisation alike (e.g. Herzfeld, 2009; Mahmud, 2014), the field of anthropology has provided numerous methods and theoretical objectives for the ethnography of opacity.

Markets are interesting institutions in the context of opacity and secrecy: modern, mainstream economics definitions of markets assume that they are transparent, that the free availability and flow of information is crucial to their pricing mechanism (Bloomfield and O’Hara, 1999; Fama, 1969; Malkiel, 2003). Yet, within bazaars, the norm is that a market participant’s advantage comes from insider knowledge. The question for an anthropology of financial markets is then how to gain access. Social studies of finance have taken different approaches, from apprenticeship (Maurer, 2000) to employment within an organisation (Lepinay, 2011) to multimodal engagements through documents, back offices and media accounts (Riles, 2011; Tett, 2009) or the historical and technical study of financial infrastructure (Knorr-Cetina and Bruegger, 2002; Pardo-Guerra, 2012).

In each of these cases, however, the social scientist can literally ‘go’ to some ‘place’ to observe finance in action. This is not the case for CDOs where assemblage is placeless: there is no central ‘place’ in which to observe this particular activity. CDOs are structured in corporate offices and domiciled in Caribbean offshore tax havens, listed in Ireland and managed by boutique firms. While each of these geographic spaces poses challenges of their own in terms of access, the trading of CDOs also occurs in secrecy.

We take insight from Jones’ (2014) work on secrecy. Rather than focusing on modes of hiding information and instead diving right into the fundamental paradox of opacity – that in fact a lot of people are often ‘in’ on the secret but lack the authority to speak about it (p. 55) – Jones seeks to reorient anthropology of secrecy towards the media of its enactment. By this he does not mean the traditional communications media (or at least, not these alone) but all the ‘signifying materialities that people use to establish and maintain social relatedness’:

Secrecy’s media are the vehicles through which relations of inclusion and exclusion or similarity and difference are modulated via communicative practices of concealment, revelation, revelation of concealment, and concealment of revelation. (Jones, 2014: 56)

For the strange case of the CDO market, we can in fact gain access to those media of enactment. Those media include offering circulars, term sheets and pitchbooks used to market CDOs to investors and, in fact, the CDO itself. These specific documents, while public, animate the CDO as a networked assemblage of obscure interrelationships. But more than this, it is also an actor – an agent in the enactment of its own secrets and its (economic, political) power as noted by Latour (1988): documents are ‘“immutable, presentable, readable and combinable” artefacts used to mobilise networks of ideas, persons, and technologies’ (p. 26).

While we cannot ‘go’ to the marketplace of CDOs, we can explore through its channels of action, through its network, how it makes a bizarre bazaar of its own. Documents have become a prominent artefact in ethnography, not least through Riles’ (2006) Documents, because they act as ‘point of entry into contemporary problems’, thus allowing for experimentation in making sense of modernity (p. 2). The use of documents in ethnography spans widely as highlighted by the cases in Riles’ (2006) edited book: it can focus on the formalism and aesthetics of the document; it can revolve around the act of ‘filling’ in forms (adding information, more or less transparent and codified); it can be a communiqué, a short statement with agential qualities for external parties, or it can be a more chronic publication with a specific purpose (to inform investors, staff etc. the future, thus creating a future).

Academic inquiries into documents often focus on specific aspects of ‘documentary practices, their strategic or instrumental character’ (Riles, 2006). Documents may also act as ‘organisational devices’ to create, maintain and manage relationships by providing stable temporal structures around networks (Preda, 2002). By encoding a world into a text, they help constitute that world. To take a familiar example, the things on a to-do list have no necessary relationship to one another until they are inscribed in that list. They can be of vastly different kind, order and scale (‘walk the dog; finish revisions to paper; write will’). The list then becomes a prescription for future action and ongoing relationships – until everything is ticked off. Thus, documents are performative in their own right, they produce new realities or reshape existing ones, they are temporally fixed yet also intertemporal and they are longitudinal iterations of an object. If ethnography is about people and cultures observed in situ to understand customs, exchanges and the mode of functioning of the observed space, then a document can assume a similar function when there is no ‘space’ within which to observe these exchanges. The document functions as a placeholder: it serves as an abstraction of the village, bazaar or organisation; it serves ‘as evidence of a wider “cultural logic”’ (Riles, 2006: 12). It also sets out the ‘terms of trade’ (White, 1981a: 517), the practices between actors that create a new social/economic reality where each actors has a specific function framed by cultural rules, pre-existing formatting, future orientations and so on.

Like the actual bazaar described by Geertz, CDO documents are in themselves a polymorphous set of relationships, disclosures, concealments, connections and articulations, tendrils reaching here and walls preventing views there. It seems unlikely that any one person actually reads these documents in their totality. Parts are read by different parties at different times and with differing degrees of expertise, sophistication or accreditation. Different actors contribute to the different pieces and connections of the documents, too, activating some relationships while quieting others. It is these qualities to which we draw attention below.

Treating transaction parties as sophisticated assumes that the product is understood in its minute detail from the outset and that includes it upsides and downsides: the SEC (2014) assumes transaction parties have ‘sufficient knowledge and experience’ to evaluate ‘the merits and risks of the prospective investment’. Treating them as sophisticated also assumes that the intricate workings of the deal are known and understood by both parties, thus allowing for information disclosure to be limited. However, given the complexity of these financial products, this is an assumption that lacks empirical justification as Haldane (2009) highlights: to be able to fully assess the deal, an investor would need to read thousands of pages of documentation to understand its minute detail, its reference assets and how it is being put together. Such a task goes beyond any investor’s due diligence as well as capacity to cope prior or during the transaction process.

Offering circulars act to relieve the investor from reading such an unworkable amount of technical detail. They are largely produced by international law firms and contain standardised sections that are copied and pasted across offering circulars – notices to residents in various jurisdictions, risk factors, tax considerations and so on. However, segments that contain specific information pertinent to a particular CDO – the offering, descriptions of notes, securities and collateral managers – are produced in consultation with the structuring parties. As such, offering circulars exhibit an ‘architecture’ that is similar to Riles’ (2011) description of ISDA master agreements where the reader is drawn to schedules appended to the standardised document (p. 57). Riles (2011) notes how repeat users take the standardised sections for granted; they routinise their engagement with the document (p. 58). However, she also observes that many users ‘don’t even know what the rest of the document [the standardised sections] says in much detail – they just focus on the parts that need to be filled out’ (Riles, 2012).

In the case of CDOs, the pertinent details are even further summarised by sellers in glossy, client-facing pitchbooks and technical term sheets, and the investor is directed to focus on these key aspects only. But, it is clear from Haldane’s account that these documentations do not fully address the information misalignment between buyer and seller. More problematically, the documents reiterate the problem of assumed sophistication or knowledgeability of the investor; it is presumed that all investors know how to engage these documents. In fact, the acceptance of information provided through these documentations as incomplete but sufficient and therefore suitable to act upon provides a contemporary, high finance echo of Clifford Geertz’s (1978) idea of ‘known ignorances’.

In what follows, we will discuss key features and functions of these documents by focusing on five themes: (1) the duality of documenting for regulatory and promotional purposes; (2) simplification of complex reality; (3) incomplete, but sufficient provision of information; (4) standardisation and its regulating effect; and (5) the document as an organising agent.

The CDO documents: documentation, simplification and obfuscation

The duality of documenting for regulatory purposes and promoting the CDO product

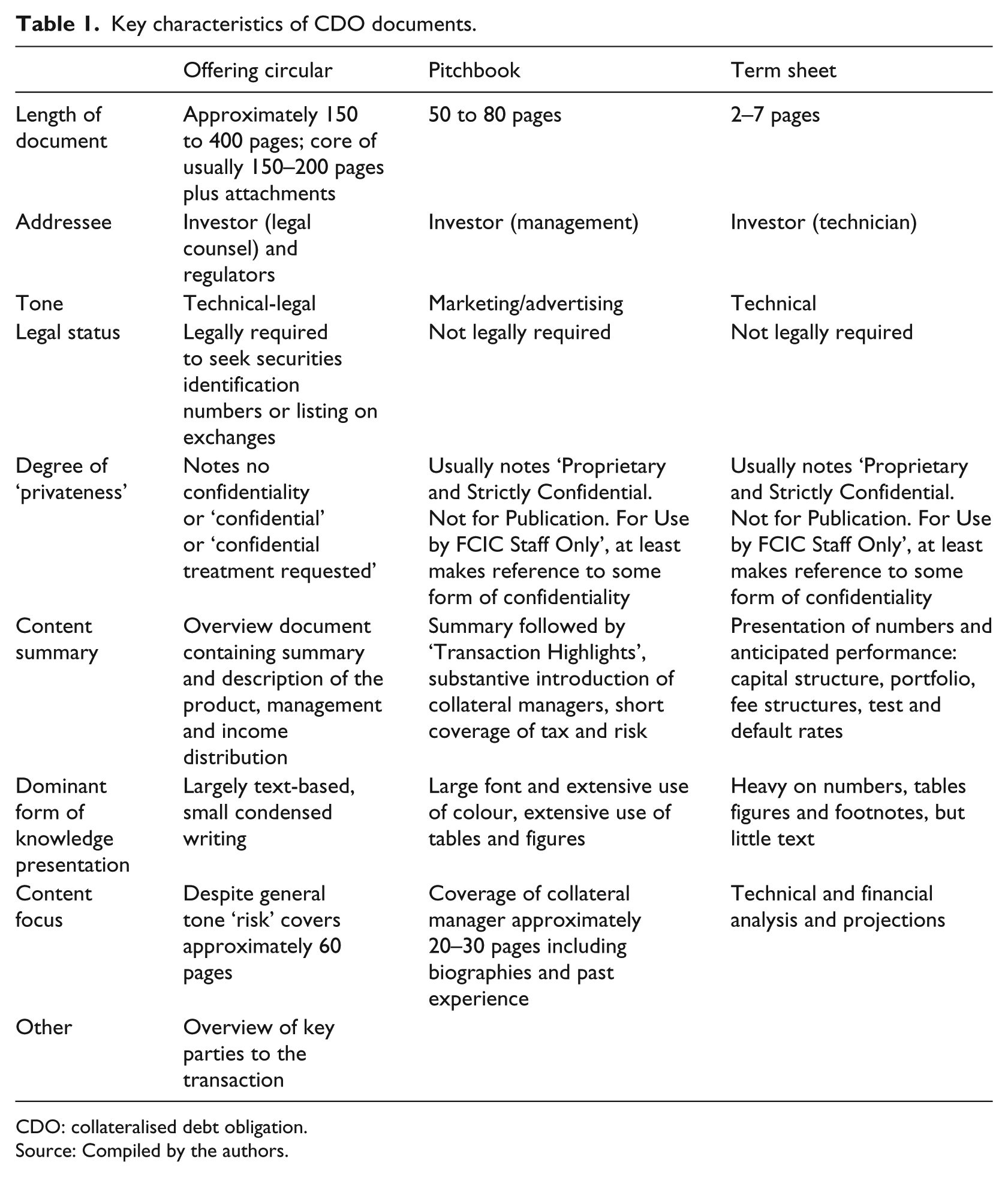

The overview presented in Table 1 illustrates that the three types of documents issued for each CDO have different purposes, target different audiences and communicate different aspects of the CDO. The knowledge presented in each document is targeted at particular groups of people. Featuring long and detailed descriptions, the offering circular is a largely text-based document that is aimed at satisfying legal requirements for seeking a listing on an exchange or applying for a securities identification number (‘SIN’ – an emerging global standard for trading, clearing and settlement purposes). Lengthy glossaries, disclaimers and tax considerations, alongside extensive discussion of risk, further underline the documents’ status as ‘technical legal’ artefacts (see Riles, 2011, for a detailed discussion). They are akin to the university strategic planning documents analysed by Marilyn Strathern (2006), which exist in part to show that the university can govern itself (p. 185). So, while they exist as a reference for investors, they are not written for them, but to fulfil legal requirements.

Key characteristics of CDO documents.

CDO: collateralised debt obligation.

Source: Compiled by the authors.

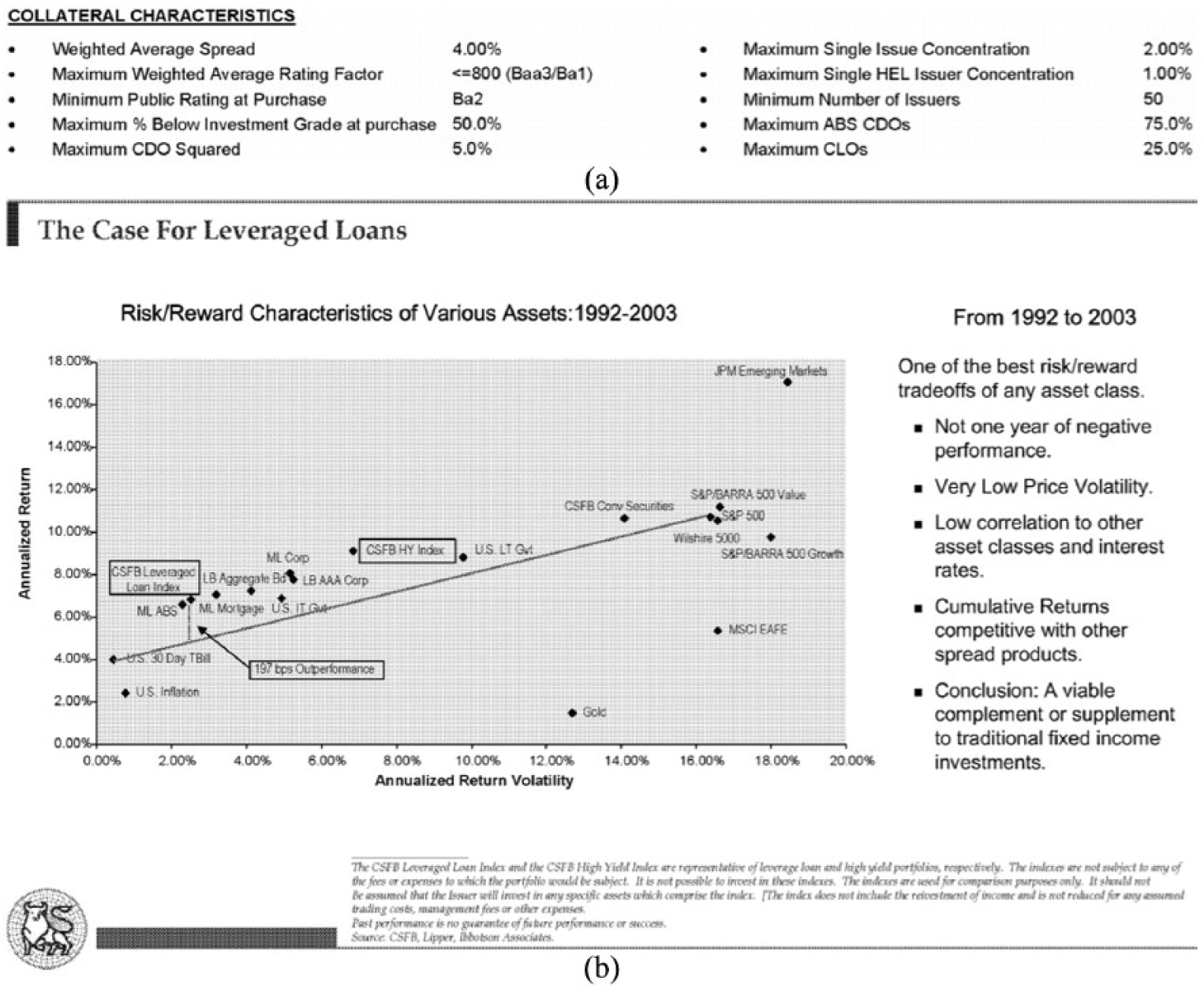

Documents produced solely for the purposes of investors – pitchbooks and term sheets – provide easily digestible snippets of information through bullet points, tables and figures. However, layout and information density per page differ substantially: the layout of pitchbooks mirrors PowerPoint presentations and contains only concise and limited information on each page/slide; term sheets provide densely populated graphs and tables arranged to fit on as few ‘sheets’ of paper as possible. Pitchbooks clearly target investors, in particular, those making investment decisions. They are glossy brochures, stacked with exhibits and tables, where bullet points rather than extensive blocks of text are key features. They take on a promotional function through a lengthy description of the collateral manager, as experienced and independent actor with the principal task of ensuring that investor interests are met; thus, they are actively used to promote the product. The term sheet is the technical equivalent to the pitchbook – it offers very condensed insights concerning key performance indicators, fees structures and characteristics. These are presented in highly technical jargon and use numbers aimed at technical experts, such as coverage tests, weighted averages, minima and maxima criteria (see Figure 1(a)).

(a) Use of bullet points and technical jargon in CDO term sheets and (b) bullet points and use of data to support the narrative in CDO pitchbooks.

By producing different documents, the sellers of CDOs appeal to the specific interests of investors and there expertises. The investor is not a solitary figure after all. The investor represents a group of people made up of decision makers, technical experts and legal counsel. The different types of documents appeal to these different readerships (Table 1); they speak directly to their audience and provide each expert with a familiarly formatted description of the activity. Pitchbooks appeal to the decision makers interest in risk, its management and returns; term sheets provide technical staff with key data and assumptions to guide them when assessing the deal; and the architecture of offering circulars provides a familiarity to legal counsel to focus on sections that matter to them, rather than the whole document.

Simplifications of complex realities: diagrams, bullets and numbers

The widespread use of bullet points in pitchbooks and term sheets shown in Figure 1(b) promotes specific narratives and to summarise long text for investors. These informational bullets are supported by data in support of the claim made. As Strathern puts it, the surfeit of lists and bullet points in these documents is itself part of the organisation’s ‘bullet-proofing’ of itself from outside interference. The effect is that of a picture produced both ‘to impress others’ and show ‘how impressed we are with ourselves’ (Strathern, 2006: 188) – it warrants expertise and demonstrates sophistication. It also compels a mirroring of that sophistication in the regulator and in the investor, too.

But, bullets, numbers and graphs do not only advertise the product to the investor but they also serve to translate the products complexity into an abridged, simplified version of the truth to instil confidence in the investor to make decisions. In pitchbooks and term sheets, the legal jargon of offering circulars is transformed into diagrams and numbers, and combinations thereof, ‘which are easier to handle than words or silhouettes’ (Latour, 1988). But it is not only the simplification of complexity that is important; what matters is how this guides investors’ decision-making. By illustrating complex realities in diagrams or summarising them in single numbers, uncertainty is removed from the process. The investor feels reassured that the product is safe and sound, not least because they are constantly reminded of the products riskless nature expressed through the dominance of AAA-rated assets and barely existent default rates, often expressed as long-term averages – ABS, CMBS and RMBS default rates are ~0.1%, ~0.2% and~0.2% for the period 1978–2004 – and compared to other asset classes, such as corporate bonds (Lexington Capital Funding, 2005: 9).

The proactive provision of incomplete, but sufficient information to preserve investor’s passive status as seekers of information

Pitchbooks and term sheets are instructional in the sense that they provide the investor reader with what is considered key information. As such they represent a technique used to obstruct readers from engaging with content more vigorously (Strathern, 2006). This happens by over-emphasising a point’s simplicity to make it tautological and self-evidencing, but sometimes these can also be nonsensical:

Better performance of Structured Finance Securities (including RMBS, CMBS, ABS and CDOs) has led to better performance of CDOs backed by those assets. (Crystal Cove, 2004: 13) One step further – looking into additional aspects. (Camber 3, 2005: 23) Focus on best execution, monitoring and administration practices. (GSC CDO, 2006: 40)

Statements of the kind provided by GSC CDO (2006) are analogous to statements about ‘research excellence’ in the university strategic planning documents analysed by Strathern (2006), which state objectives like ‘to encourage and pursue research of the highest quality across the full range of subjects studies in the University’ (p. 183). Strathern (2006) wryly notes the absurdity of the statement, for the ‘highest quality of any institution’s research will be its highest’ (original emphasis).

These statements fill an otherwise empty page in such a way that speaks to potential investors, to assure them of a certain familiarity with the product. In other words, investors are fed the knowledge that is seen to serve the function of promoting the product. The small print provided in the heavily text-based offering circulars serves the opposite function. It overwhelms readers unfamiliar with these documents, making the task of deciphering important information a laborious one. These documents have no logical entrance point for the novice reader: a summary page up front is followed by a series of notices to various potential investors to cover all eventualities before providing the reader with a table of contents to break down the information in more digestible chunks. These documents are reporting in nature. They do not serve a clear function beyond details that require discussion for legal and regulatory purposes.

The proactive provision of incomplete, but sufficient information acts to preserve investors’ passive status as seekers of information. The act of volunteering details about the product is more than just a part of the transaction process. Obviously, parties to the transaction need to be informed, but at the same time, the provision of incomplete information serves to control the information out there. The main purpose of the disclosed analytics is to provide investors with information that comforts their expectations about the high returns and low risks of CDOs and hence are not presented in a way that encourages interpretation. The pitchbook and term sheet act as distraction from the more detailed offering circular: they act as noisemakers (Jones, 2014: 56), to drown out any potential signal that could be conceived of as stimuli for unwanted discussion. By providing the target audience with information exclusively, the sellers of CDOs (1) maintain control over the knowledge that is out there and (2) curb investors from seeking their own information to pre-empt them from asking questions that may require a difficult answer.

Standardisation and its regulating effect on contents and omission of information

These functions are, at least in part, dependent on some standardisation, not for reasons of familiarity but in a regulatory sense. That is, standardisation limits the kind of information that is collectively produced by sellers across the markets, thus legitimising the content itself as truth. The knowledge out there in the interface between buyer and seller is therefore a product of the story told in the documents. And this story is carefully crafted, not just by what is included, but perhaps more importantly, by what is excluded or cut-off.

CDO documents are both standardised and standardising. They share a blueprint – the document architecture – both in terms of their layout and content (Riles, 2006). In fact, many sections appear as though they are copied and pasted from one CDO to the next. Cover pages include a selection of similarly arranged features (overview of key parties, tranches and certain conditions). These are followed by a long list of notices for key investor jurisdictions, followed by yet another overview of key terms. Of course, certain information (technical data, names of reference assets etc.) is specific to each CDO, but the document architecture leads readers to specific focal points which in turn standardises how we think about and how we engage with CDOs in the real world (Riles, 2006). Standardisation thus pushes investors to think about CDOs as a homogeneous set of products with similar features and risks; ignoring the fact that CDOs can be distinguished by type, purpose, maturity, collateral and domination (SIFMA, 2016). Standardisation facilitates coordination between parties and reduces transaction costs as parties become familiar with the products, but the ‘truths’ told by these documents also distract from other knowledge that would benefit investors. For example, the effort spent in establishing a collateral manager’s suitability to manage CDO collateral masks the absence of any information on how the collateral manager has been selected.

Standardisation has thus a purifying effect on documents (Riles, 2011: 59). The produced knowledge mirrors that of public inquiry reports as argued by Brown (2003): it produces hegemonic and verisimilitudinous realities. A new authority is created on a subject matter that was previously non-existent to perform the important tasks in reshaping the public market discourse that emerges from coordination among parties (Riles, 2011: 57). In other words, the emergence and proliferation of standardised documents disclose a homogenising and self-reinforcing network effect: the parameters set out in these documents strengthen a particular understanding of the market that allows the market to retain its form (Nenonen et al., 2014).

The document as organising agent

At the point of production, it is unlikely that any of these documents were even considered to attract an academic audience, never mind one that would critically and analytically engage with them. Thus, as academics, our reading of and the knowledge we can derive from these documents add to our understanding of these complex and exotic financial products. In that sense, documents are not just organisational devices but also organising devices; they act as reference point for numerous types of readers – supply side, investors, regulators and exchanges – and connect these actors across time and space (Preda, 2002). As such these documents enact certain behaviours and knowledges related to the product themselves; yet, at the same time, and given the scale of CDOs issued, these documents also tell us something about the larger picture because of the relationships between buyers and sellers formed within this noisy and non-transparent setting.

The collective endeavour that ultimately forms the product is, however, documented within a particular document – the offering circular – which delineates, as required by law, the product’s details, characteristics, its specifics. Documents can help us understand the CDO market not necessarily or only because of their content, but because of their agential qualities. In this sense, documents do more than just documenting an activity, they are organising artefacts. The document creates an image of the activity as a coherent whole; it brings together otherwise disconnected actors. It anchors actors’ relationships and it brings them formally into existence: states, corporations and other entities, including the CDO, exist because they are summed up somewhere using a selection of multiple sources (Latour, 1988: 27). Both the lack of place and the hugely disparate experiences and expertise held by these actors are overcome and united through these documents who act as witness to the complex arrangements required to create opaque financial activity. Norms and standards are therefore key marking stones to guide participants, yet they also characterise the markets to the outsider as noted by Strathern (2004 [1991]):

By organization I refer both to how they [materials] are collated and systemized by the observer and how collation and systemization already appear accomplished in the way that actors [in our case, documents, but also their authors and readers] present their lives. (p. XIII)

When stripping away the complex story told in those documents, organisation becomes visible within them. This act of simplifying, which both Riles (2011) and Strathern (2004 [1991]) discuss at length, is thus a way to unveil the secrets within documents, secrets that reveal how actors engage with one another, in particular when taking into account the investor’s position as an outsider. The assemblage of these products utilises complexity as a shield, to protect itself from aggressors and unwanted meddling, and documents act as devices to express this.

Documents are seldom stand-alone objects that are disconnected from each other. Indeed, the opposite is true. Documents relate to each other, they are combinable and products of combination. Documents, when combined, or when considered next to one another, can map higher order organisations that enable us to access and assess structures and patterns that otherwise remain hidden and secretive (Latour, 1988). The ability to combine documents is now more than ever propelled by technical and methodological advances. For example, by focusing on network connections, Tischer and Leaver (2017) show how CDOs are products of supply-side arrangements that are constantly reconfigured at the product level, yet repeated at the industry-level. By making these repeated relationships between supply-side actors visible, they provide an alternative map of the patterns and structures that are assumed by experts. The market takes on a different form; it becomes more stable and bazaar-like. Thus, the document in its singular format gains analytic power when considered alongside other, yet related documents.

Documents as investors’ guidebooks to the bizarre bazaar

The similarities between Geertz’s description of the Moroccan bazaar and modern financial practices, such as observed in this study of CDOs, are unexpected but striking, and clearly contrarian in character to widely accepted understandings of financial activity as being organised in markets. The documents both in their individual form and collectively allow us to gain insights into processes of knowledge production, their organising purpose and interaction between that organisation and those outside of it.

When considered within the context of the bazaar, the individual CDO acts as face to an entity that represents complex arrangements otherwise unobservable from the outside. Remember that CDOs are traded outside of exchanges, ‘OTC’ between the counterparties, and where regulation only exists in the form of elaborate ‘enter at your own risk’ signs. The bazaar helps us to illuminate the complex social interactions that organise collectively around rules and standards upon which cultural institutions emerge telling participants how to act, what to do, and crucially, what not to do. As outlined by Geertz (1978), in theory, conformity in bazaar activity is pursued through normative sanctions and the threat of reputational damage. And indeed, to the outsider, CDO norms and rules appear market-like through their promise of transparency and accountability – the pitchbook for the Jupiter High Grade CDO II (2004b: 25) even makes claims that its collateral manager, Maxim Advisory LLC, had ‘no traditional ties to Investment Banking’. Yet, only the insider has access to the information that allow for a more accurate assessment of actual behaviours within this setting orchestrated by a series of shadow norms (Lampel, 2004). For example, unbeknown to investors, State Street initially decided not to participate in a Magnetar-sponsored CDO citing the potential reputational risk, but this decision was later reversed following pressure from Magnetar (Eisinger and Bernstein, 2010; Koszeg, 2012). These shadow rules are spread and reinforced through clique-like behaviour via preferential relationship formation between sellers and their suppliers. For example, Rabobank, an investor in the Norma CDO, claimed that the relationship between NIR (a collateral manager) and Merrill Lynch did not resemble the arm’s-length relationship advertised, but in fact was much closer knit and that NIR was ‘beholden’ to Merrill Lynch for generating business for NIR (Koszeg, 2012, also see WSJ, 2007). In fact, Tischer and Leaver (2017) highlight that repeat interactions between supply-side actors was the norm. But none of this is visible to the outsiders, these shadowy relationships are hidden through a veil of secrecy that proves immensely difficult to lift.

Taking the point of view of the investor, before they enter the CDO bazaar they have to meet a set of formulaic criteria set by regulators, after which they are considered sophisticated or accredited: investors in CDOs must be banks and other financial intermediaries, non-financial firms and individuals with a net worth above US$1 million. Yet, such a definition says little about the actual state of sophistication with regard to knowledge or cultural understanding beyond a requirement for ‘sufficient knowledge and experience in financial and business matters to make them capable of evaluating the merits and risks of the prospective investment’ (SEC, 2014). This is another nonsensical statement. Investors are deemed sophisticated enough to handle CDOs if they are well capitalised; if they are well capitalised, they must have been sophisticated in order to get that way. Indeed, investors will exhibit varying degrees of sophistication when it comes to understanding the intricacies of the complex financial product they are about to engage within the same way that tourists and travellers do. Yet, even when experienced in similar settings – other derivative markets and exotic financial transactions – most investors will fall far short of the status of being native to this particular bazaar. As noted by Haldane (2009), highly complex and opaque interactions between products were barely recognised by the producers of CDOs, investment banks, themselves. If that is the case, how could investors be expected to do better given the limited access to information?

The forms of engagement within the bazaar setting that are assumed by the tourist/traveller and the CDO investor are comparable as both suffer from role asymmetries. The investor remains a tourist, or at best takes on the role of a traveller when involved in these transactions repeatedly, because investors are also unable to become knowingly ignorant, to use Geertz’s terms. ‘Insider’ information will remain inside and the availability of information and its use for signalling purposes by producers of CDOs is carefully managed in a collective endeavour to provide the outside world with one convincing account of the bazaar.

Because of this, we should not confuse these role asymmetries with the information asymmetry noted in Akerlof’s (1970) Markets for Lemons. Because CDOs are private contracts between two parties, the investor is precluded from accessing information unless provided by the sellers and thus is subject to traders’ account of product quality. This absence of external sources makes it difficult, if not impossible, to assess the quality of the product through alternative means such as Karpik’s (2010) judgement devices: labels, brands, guides, critics and rankings. Ultimately there is one source of information: the sell-side. The information may take different forms in different formats – pitchbooks, term sheets, offering circular – and they may be displayed using different tools – text, diagrams, numbers and so on. But they lack the diversifying effect that the coexistence of multiple judgement devices can have as they represent different combinations of actors and practices (Chiapello and Godefroy, 2017).

Of course, we argue that pitchbooks act as guidebooks to the bizarre bazaar, but here the guiding is solely performed by the sell-side and lacks an independent account. There is no diversity, documents and information therein are standardised and each pitchbook, despite some variation in content, makes use of overly similar judgement devices. Information is carefully selected and arranged with the sole purpose of selling the product to the investor. Investors, suffering from role asymmetry due to their position on the outside, lack the ability to critically engage and, instead, readily buy into what is presented to them. Notwithstanding, product quality in this market was assessed externally by independent credit rating agencies (CRAs). But these ratings did not constitute independent advice – CRAs were eager to produce AAA ratings to maximise fee income from investment banks, who sold AAA-rated products to willing investors. These CRAs employed credible calculative technologies that reduced complex problems to simple solutions (MacKenzie, 2011: 1784), abridged versions of truth, by ascribing ratings. For investors, these ratings (see Figure 2) offer a convenient way into CDOs; it allows them to ignore the complex realities inscribed in the ratings. And it is this ability to simplify complexity, the ability to offer some tangible assurance of product quality that makes these ratings a powerful tool for the sellers.

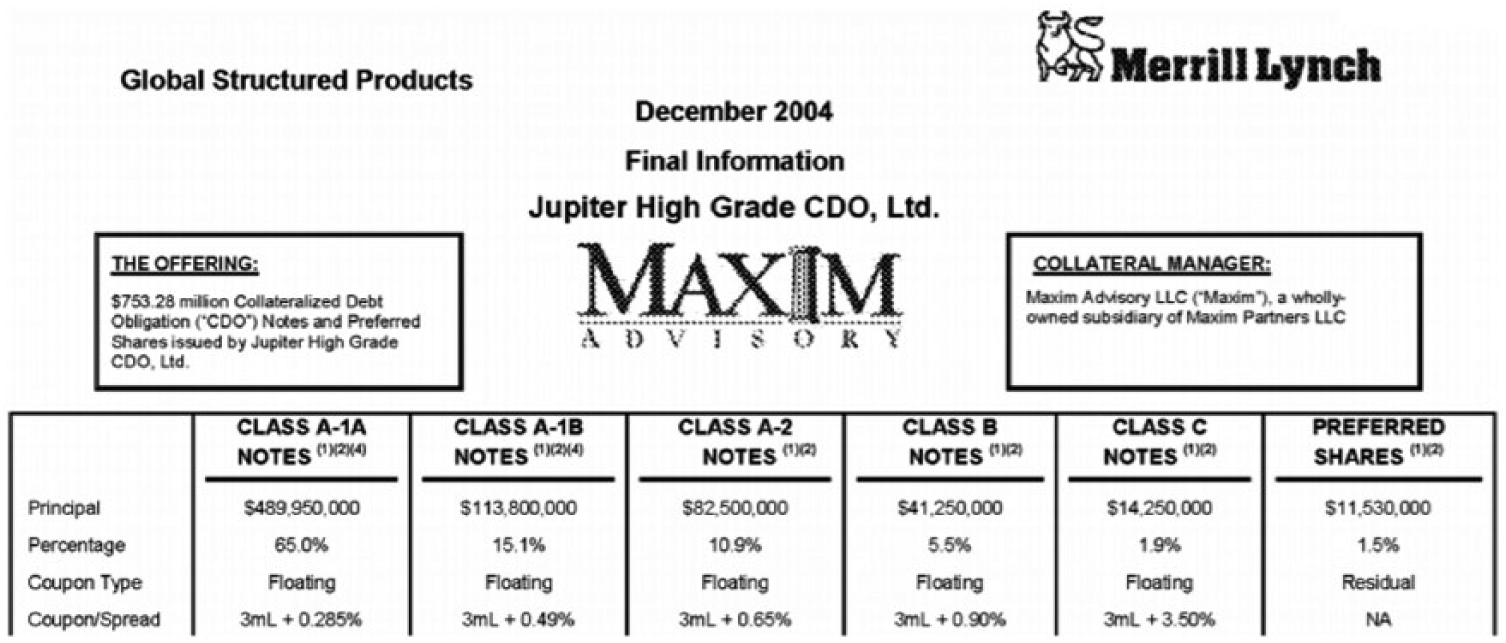

Prominent advertisement of Maxim Advisory, a collateral manager, in term sheet.

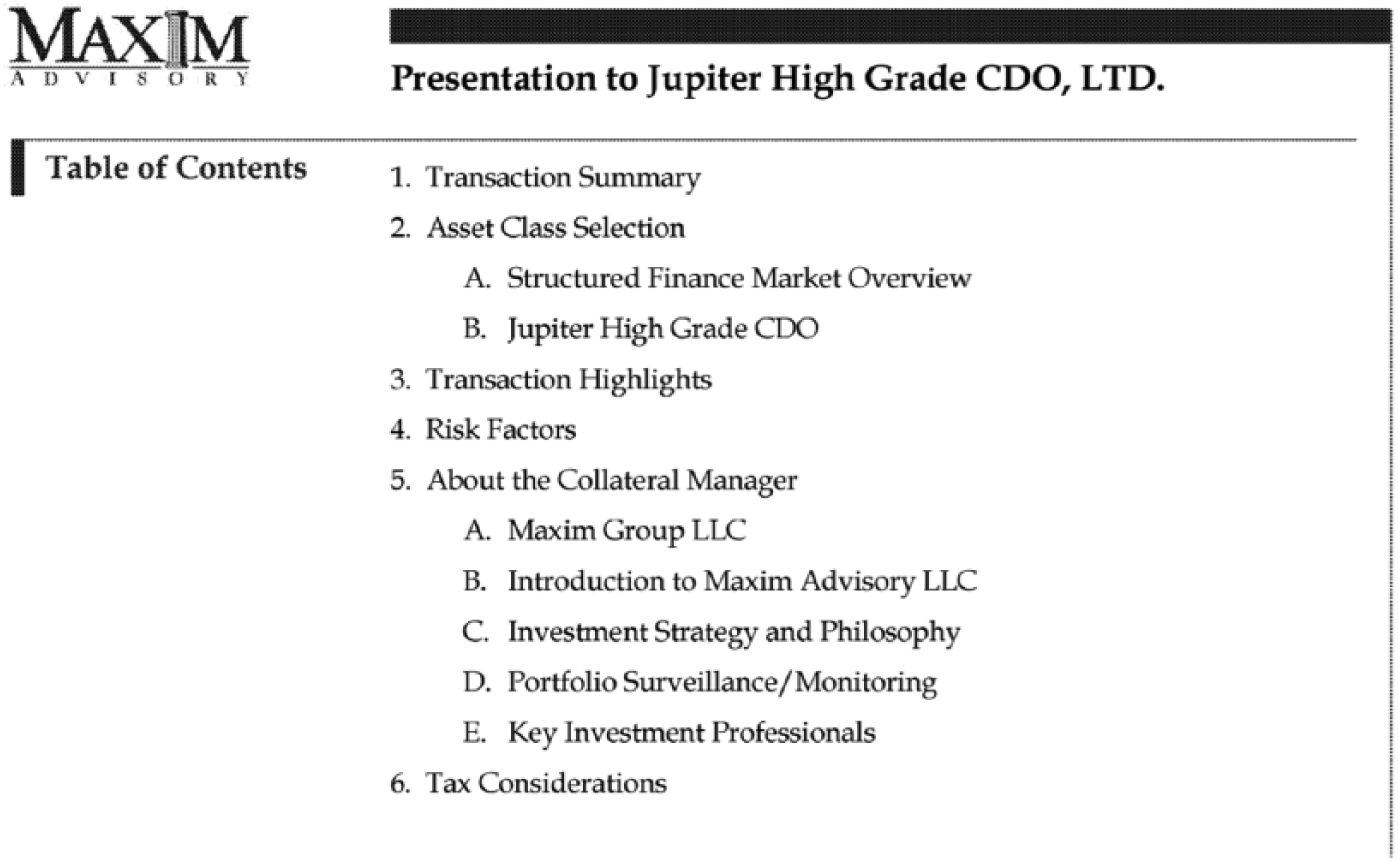

A second example is the prominent advertising of collateral managers in investor-facing documents: the Jupiter High Grade CDO pitchbook dedicates over 50% of its space – 34 out of 64 pages – to describing the collateral manager (Figures 2 and 3). This focus on collateral managers seeks to assure investors that these products are managed in their interests, to promote quality of processes and expertise. For example, Maxim Advisory LLC promotes its ability to ‘efficiently manage client’s risk’, their ‘exceptional execution services’, ‘… investment professionals with extensive backgrounds and experience in Structured Finance’ (Jupiter High Grade CDO, 2004b: 23, 26). This is even more relevant given that there is no mentioning of conflicts of interest in the pitchbook, whereas there is a four-page discussion of potential conflicts of interest of collateral managers in the offering circular (Jupiter High Grade CDO, 2004c: 15–18).

Collateral managers’ central role in a pitchbook as per table of contents.

However, the collateral managers’ ability to act and manage assets indiscriminately is ultimately constrained by product specifications set by the investment bank. Even when CDOs are static – when reference assets are fixed at the date the deal closes and cannot be altered – collateral managers are viewed as important marketing vehicles. This was the case with Goldman Sachs’ infamous Abacus 2007-AC1 CDO which involved ‘Fabulous Fab’ Tourre who explained the importance of selecting ACA Management, a leading CDO collateral manager, in an internal email:

One thing that we need to make sure ACA understands is that we want their name on this transaction. This is a transaction for which they are acting as portfolio selection agent, this will be important that we can use ACA’s branding to help distribute the bonds. (SEC, 2010: 8)

And this view is confirmed by an internal memorandum to the Goldman Sachs Mortgage Capital Committee (MCC):

We expect the strong brand-name of ACA as well as our market-leading position in synthetic CDOs of structured products to result in a successful offering. (SEC, 2010)

Thus, the prominent featuring of collateral management acts as noisemaker (Jones, 2014: 56) to promote the CDOs as independently managed and of low risk, high quality. Meanwhile, auxiliary information that does not advance the deal is collectively kept under wraps: in bazaars, there is no formal rule or law that makes it ‘illegal’ to set prices through price tags, but at the same time it is understood collectively that one person doing so would undermine, if not deconstruct the bazaar as an institution.

The effort of managing information in the CDO setting to such a degree gives rise to it as a bizarre bazaar, not a market. Social relationships matter, efficiency is at best second ranked, and the economic exchange is as much a theatrical performance as it is good business practice. Any outsiders encountering the bazaar (i.e. those who are not themselves actively involved in producing CDOs) require the knowledge to navigate this institution to successfully engage with its customs and modus operandi as performance. For that purpose, the unknowingly ignorant tourist requires an introduction to the bazaar, and this is provided in form of guidebooks. Guidebooks, like the documents available for CDOs, are highly stylised and provide information in an instructive, simplified way (Adler, 1989). The noise is stripped away from the descriptions offered to focus attention on key aspects seen as important by the authors and appreciated by the users. Guidebooks are also decidedly standardised with respect to structure and content; they can be understood as a ‘master script’ which encourages readers to seek ‘directed performances’ (Edensor, 2001). Tourists therefore understand the place in one way, as told by the guidebook, and it is only those that know the bazaar from experience and regular engagement, from being an insider rather than a remote participant, that recognise the discrepancies in this account.

To ‘guide’ means more than just to give directions, it is also about managing access and asserting control over the tourist. The guidebook has an organising function: it discloses attractions and creates demand for these attractions, in particular, where other reliable sources of information are unavailable (Cohen, 1985). This function is also demonstrable in CDO documentation: (1) they contain lists, short descriptions, visual illustrations and warnings for each product and for key aspects within it and (2) they instruct investors in how to think about CDOs in a very specific manner, where highlights point towards the most crucial or salient elements: transaction highlights, ratings, diversification (see Figure 3). They feature ‘maps’ or summaries to make key features available to readers and anticipated questions are dealt with upfront. However, in the absence of (critical) public accounts of CDOs at the time, documents are the only point of access for investors (and academics) to begin to develop an understanding this exotic product. While there is of course the possibility of chatter among investors to exchange ideas, this is kept out of the public domain. The absence of a public platform such as TripAdvisor, which gives access to alternative accounts/ratings for these destinations and thus materially influence how future consumers engage with the products (see Scott and Orlikowski, 2012), means that information remains subject to sellers’ accounts, where outside conversations are discouraged. Even in the presence of such a platform, there were very few, if any, accounts of negative experiences of the CDO product at the height of the market in 2006/2007 as the housing market remained buoyant and the product itself offered a long-term investment experience rather than instantaneous gratification.

Conclusion: documents, ethnography and organisation

This article sets out to address how documents present an opportunity to engage with finance ethnographically, especially where barriers of access, secrecy and the lack of physical space present difficulties for traditional fieldwork-based ethnography.

Despite its attraction and notable results, we have argued that conventional ethnographic fieldwork in finance is the exception rather than the norm. This is not necessarily because gaining access to sites is notoriously difficult, but because, increasingly so, modern financial activity does not take place in a specific locale or within a particular organisation; rather, it is a product of complex structures and relations in the non-physical world of global finance (Garstens, 2010; Palan, 1999). Even if we were able to access sites, we would skew the observation towards the activity manifested in that particular place. We would therefore fail to account for the entirety of the activity vital to the assemblage of modern financial products as networked products, one that goes beyond organisational boundaries (Tischer and Leaver, 2017). In any case, this access problem of ethnographic fieldwork in finance is unlikely to be resolved in the near future as technological advances and jurisdictional arbitrage will continue to favour finance as a global activity. Nor will finance be particularly welcoming of outsiders in light of the continuous set of crises and scandals, for example, the 2007–2008 crises or the Panama Papers; finance as an industry is likely to remain secretive.

But, finance’s secrecy and opacity must not lead to the expiration of ethnographic engagement with finance. Building on ethnography as a creative and explorative process (Humphreys et al., 2003), we propose that some of the frictions between access to field sites and organisational secrets can be resolved through indirect routes via organisational documents that act as media of enactment of secrecy. In doing so, and following Jones (2014), we have argued that applying an ethnographic gaze to documents can help us reveal objects, actors and relations that otherwise would remain secret. Different types of media can shed light on the secretive organisation of financial activity because they seek to simultaneously signal and make noise, to reveal and conceal secrets, and in doing so reveal acts of noisemaking and concealments. And documents, in all their different formats and target audiences, are not only a key source of organisational information with respect to the practices of documenting and representing but they are also organisational devices: they create, maintain and manage relationships, both within the organisation and between those organisations and the outside world (Jones, 2014; Preda, 2002).

The use of documents as sources of knowledge reveals practices and relationships between investors in and sellers of CDOs otherwise shielded from outsiders due to the private nature of this particular activity. Importantly, we found that neither the organisation of its assemblage nor distribution of CDOs resembles perfect markets. Instead, patterns of behaviours and structures disclosed in these documents are akin to the bazaar Geertz (1978) describes: information are mal-distributed, and processes of clientisation shape and enact the relationships between investors and sellers of these financial products. These documents simultaneously describe the product and persuade investors to trust its creators and the product itself. They act as shields to deflect regulators’ attention and investors’ scrutiny, but they do so by reflecting back at them their own ‘sophistication’ by merely being in the presence of these documents (Strathern, 2006).

However, the availability of information, both with respect to audience and content, is controlled in such a way that secrets are safeguarded, thus maintaining conditions in which investors remain only in possession of incomplete and imperfect information. In the absence of other, public sources of information, investors are continuously dependent on what, given the completion of the transactions, they may consider sufficient information to engage in this transaction. At the same time, the information made available to them remains incomplete and only partially discloses details. Sellers control information availability to manage expectations through standardisation and replication, where transparency and forthcoming disclosure of attractive ‘facts’ become a form of noise to distract from other information. Investors accept and act upon their perceived status as being knowingly ignorant: they make judgements based upon information that offers a supposedly independent account of product quality. Still, they remain unknowingly ignorant and are manipulated by sellers through the purposeful revealing of secret information in documents.

But sellers’ choices about what remains concealed, and what is reveal – to whom and at what time – are far from unique to financial market settings. In fact, Karpik (2010) highlights how this is a common feature in markets where product quality is opaque and prices present no meaningful shortcut to access the value of a product. Although judgement devices can be, and are, used by buyers of products, overly similar judgement devices may also have a standardising effect (Chiapello and Godefroy, 2017). But more problematically, the deployment of judgement devices – risk ratings and guides to collateral managers – disguise the fact that all information stem from, or are organised by, the same source: the sellers. And, sellers use these devices to misrepresent product quality by concealing products risks vis-à-vis uncertainty to make the product more palatable to buyers. Of course, experienced buyers may be aware of this concealment, but occasional buyers may misinterpret these signals and take them at face value because their role as tourists precludes them from becoming knowledgeable or knowingly ignorant.

And hence, the persona of the ‘tourist’ is not unique to this setting; rather, it potentially speaks to many situations in which (buying) decisions are made on the basis of limited and asymmetric information. Drawing a difference between the repeat costumer–stakeholder and the market outsider (the tourist) may allow for more nuanced analyses of the interactions between buyers and sellers of goods across diverse sectors. Akerlof’s (1970) market for lemons eludes to the fact that consumers are seldom experts and that they make decisions on the basis of available information published by the sellers. But we can take this idea further: recent scandals – from ‘dieselgate’ to mis-selling of Payment Protection Insurance products – and instances of misleading information being used to sell insurance products, real estate investments and so on, point towards the tourist vis-à-vis market outsider as a pervasive construct to understand (one-off) buyer–seller transactions. We encourage further research into the idea of the tourist/market outsider stakeholder from an ethnographic and organisation studies perspective.

By taking an indirect route to access this field site through documents – necessitated by the lack of access, the placeless activity of CDO assemblage and the private nature of the transaction – we assume the position of tourists, which we have argued is precisely how potential investors approach this ‘market’-place: by treating circular offerings, pitchbooks and term sheets as guidebooks. So, in the end, our method does in fact mirror ethnography in that we mimic the actions and assume the same position vis-à-vis knowledge as buyers in the CDO market, as well as some of the market participants who like us proceed without total knowledge, merely extending or ramifying one piece of the market instrument.

The ethnographic engagement with documents represents a suitable alternative to the more traditional fieldwork approach in a setting like organisational ethnography. Apart from being a convenient and pragmatic response to the challenges of access, documents are also a ready-made and widely available, yet often ignored, source of information that benefits from the type of new requirements for organisations to disclose information in an audit society (Power, 1997). And it is precisely the fact that these disclosures are not made directly to academics but to other readerships that make these documents intriguing artefacts for organisational ethnographers through which the acts of revealing and concealing the organisation’s secrets become an object of ethnographic concern.

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.