Abstract

Climate change poses a significant threat to future social and economic activities. This article seeks to understand how corporations respond to climate uncertainties and threats through the performance of different ‘risks’, including market, reputational, regulatory and physical risks. In doing this, we demonstrate how these risks are performative and political. Based on interviews and document analysis, we show how climate change risks are naturalized within market conventions through processes of reiterating climate change as risk, codifying the risk in monetary value, entangling the risk in market conventions and cementing the frame through political activities. We also show how these risk frames have political effects in that they fail to fully account for, or represent, the complexities of climate change. Indeed, the social and natural consequences of climate change undermine the risk models that seek to explain and predict these events. The consequences of these ‘misfires’ highlight the political nature of risk frames in that their effects are unequally distributed among less powerful actors. Importantly, however, these misfires also have the potential to provide space for new interventions in responding to climate change.

Introduction

Climate change has rapidly escalated within public consciousness as arguably the most pressing concern facing humanity (IPCC, 2014; Stern, 2007). Climate change is a critical issue for corporations considering that their carbon emissions are principally fuelling anthropogenic climate change and that they are called upon for solutions to mitigate catastrophic futures. The concept of ‘risk’ is a central construct for how businesses respond to and ‘manage’ climate change (Hoffman, 2005; Lash and Wellington, 2007). Risk is used to understand and order the threats and uncertainties around climate change. Importantly, however, these risk evaluations are not reflections or representations of climate change but performative and political frames influencing how societies should respond. Corporations thus play a critical role in forming our climate-changed future.

In this article, we investigate how corporations develop risk frames and their effects in five large Australian corporations. Our analysis is based on interviews with key actors engaging with climate change in these corporations, including environmental and sustainability managers, as well as corporate documents. In the empirical material, we first identify how corporations frame climate change into different forms of risk, such as ‘regulatory risk’, ‘market risk’, ‘reputational risk’ and ‘physical risk’. Second, we show how these frames are naturalized through processes of reiterating climate change as risk, codifying the risk in monetary value, entangling the risk in the market and cementing the frame through political activities. Finally, our analysis suggests that these performative risk frames ‘misfire’ (Austin, 1962), in that forces and relations excluded in risk framing ultimately undermine the risk configurations.

The highly variable and complex nature of climate change provides an ideal context within which to examine corporate productions of risk. In doing this, our study makes several contributions. First, we further develop a performative theory of risk to explain how risk frames shape present and future climate change responses. Beyond mapping different types of climate change risks, we theorize how the frames bring certain realities into being, that is, the ontological effect of corporate risk frames. Performativity is the ongoing material-discursive making of the world and corporations take part in shaping the possibilities to act in the future. Second, by studying the performative acts of framing, each cut or carving of the frame suggests inclusions and exclusions. This allows us to develop a typology to argue that the naturalization of particular risk frames is political in that it engages a narrow range of actors, favours certain conventions and demands particular actions (and/or inactions) by specific actors. Third, we illustrate how misfires happen through the inability of risk constructions to account for the represented phenomenon. The consequences of these ‘misfires’ further highlight the political nature of risk frames in that their effects are unequally distributed among less powerful or marginalized actors. Importantly, however, these misfires also have the potential to provide space for new interventions in responding to climate change.

The construction of risk

Theoretical discussion surrounding risk in organization and management theory (OMT) largely adopts a cognitive-scientific perspective, where organizations are ontologically separated from the risk they act upon. Organizations are perceived to be exposed to a variety of risks as objective facts that need to be ‘managed’ through rational decision making, employing, for example, cost–benefit analysis based on probabilities and consequences (Andersen and Schrøder, 2010; Randall, 2011). The core assumption underlying risk management is that risk is ‘out there’ and it just has to be ‘found’ and ‘captured’ by professional experts using statistical tools and analysis. Disciplines such as finance, economics, statistics and accounting have professionalized this approach by codifying risks into calculable entities, such as insurance costs and credit ratings, to determine the probability and consequences of events (Ailon, 2012; Lupton, 1999).

The concept of risk was translated into management in the 1990s following the catastrophes and scandals associated with, for example, the collapse of Barings Bank and the Brent Spar crisis at Shell (Power, 2004). The calculability of risk was, of course, challenged by the financial crisis of 2008, an event few management scholars and business practitioners predicted, despite their faith in calculable rationality. Beyond the confessional embarrassment of business schools in the aftermath of the global financial crisis (Podolny, 2009), this event highlighted the folly of acting with certainty on uncertainties. It also highlighted that the very belief in risk management constituted these events as scandals and crises (Ailon, 2012: 252); if we did not assume predictability and regularity, these events would likely have been interpreted very differently.

By contrast, a social constructionist perspective on risk suggests that the meaning of what a risk is, and how it should be dealt with, is dependent on pre-existing knowledge and discourses (Lupton, 1999). Risk constructs are open to social definitions and contestation. This perspective on risk pays greater attention to how cultural and political frameworks, and powerful institutions, influence how we understand dangers and uncertainties as ‘risk’ (Lupton, 1999). While there are many dangers and hazards to deal with in society, only a few are constructed as ‘risks’ (Lupton, 2006). In an influential text, Ewald (1991) explains, ‘Nothing is a risk in itself; there is no risk in reality. But on the other hand, anything can be a risk; it all depends on how one analyses the danger, considers the event’ (p. 199).

Within OMT, there is an emerging literature that has focused on organizations as places where risks are constructed and processed (Gephart, et al., 2009; Hutter and Power, 2005; Maguire and Hardy, 2013); that is, organizations by identifying, measuring and assessing risks are taking part in constructing the phenomena they are responding to. The emphasis here is on how the meaning of risk becomes stabilized and is shared through organizing processes. For example, Maguire and Hardy (2013) have examined how chemicals became ‘risky’ or ‘safe’ dependent on the discursive work of organizations. The meaning of the chemicals was socially constructed and (temporarily) stabilized through risk assessments and management processes. This suggests that the meanings of risk are shaped by the very organizational processes used to assess and manage them.

The constructionist perspective on risk in OMT counters the positivism of the regular risk literature by enriching our understanding of how organizational constructs and representations are understood and stabilized. This perspective also draws our attention to the underlying mechanisms of these constructions. However, in understanding how groups are struggling to impose a particular point of view, the constructionist perspective tends to neglect the material aspects of the represented (Butler, 2010; Callon, 2009). While the naïve realism of the cognitive-scientific perspective on risk omits important social factors, the social constructionist perspective has traditionally excluded natural factors or agencies (Çalışkan and Callon, 2010). Both these dominant approaches to risk thus face the dangers of upholding the nature/culture divide in understanding risks. Arguably, a performative approach can assist us here by shifting the focus from the meaning (social, symbolic, cultural) of risks to the ontological effects of risk productions, that is, the realities these constructions bring into being (Butler, 2010).

Risk as a performative construct

We suggest that risks are performative in that they are dependent on the way in which they are enacted and reiterated, which is a description beyond both essences and pure constructions (Cochoy, et al., 2010). Indeed, risks perform and order future uncertainties, making them manageable in achieving certain goals (Dean, 1999). This point has been argued by Callon (1998b: 2) in reference to how economics ‘performs, shapes, and formats the economy, rather than observing how it functions’. There is thus a joint movement of the discipline and the object of discussion. Callon (1998b) further suggests that this is applicable to any theory or model in that these constructs actively participate in shaping the very phenomena they are supposed to describe. This has been demonstrated by MacKenzie (2006) in showing how theoretical models of risk management have been incorporated into financial markets and used by finance professionals in shaping the practices that these models aim at predicting.

A key aspect of performativity is that observed patterns can in fact undermine the model or construct that is supposed to predict or explain them (Butler, 2010). This produces overflows (Callon, 1998a), counter-performativities (MacKenzie, 2007) or misfires (Austin, 1962), given the lack of discursive closure in representing the represented. In Callon’s (2007b) and MacKenzie’s (2007) anthropology of markets, the misfires are analytically external to the performative act, a transgression of the framing device. The emphasis is on the actor or agencement—a sociotechnical arrangement of humans, tools and technical equipment with the capacity to act and give meaning to action—performing the model or theory (Callon, 2005). It is these agencements that ‘frame’ by creating and, simultaneously, managing how something is understood (Callon, 1998b). Overflows are transgressions of the particular frame and similar to what economists call externalities (Callon, 2007a). The ‘economic-centric’ assumption is rather that the overflow can be stabilized through quantification and monetization (Blok, 2011). For example, climate change, viewed as an externality, can be accounted for through carbon markets in the continuously evolving agencement of the market (Callon, 2007a, 2009).

Butler (2010) appears less surprised by overflows or misfires. In her analysis, that which is studied or modelled will often shape the calculations beyond what was predicted or assumed, and it is only under certain conditions that models or theories bring into being what they intended to describe. It is not the overflow or counter-performativity that challenges the performative act, the potential misfire is in the performative act itself. The misfire is potentially delayed by simultaneously drawing upon and covering up the conventions upon which the performative work is founded (Butler, 1997; Derrida, 1977). Thus, the frame works ‘best’ when not seen since it is less likely to be problematized or challenged. For example, the success of financial risk models is dependent on simultaneously enacting and hiding from view the assumptions of the market that the models acted on—assumptions that became glaringly clear after the financial crisis as a grand misfire. Thus, the threat to the model (MacKenzie, 2007), performation (Callon, 2007a) or speech-act (Austin, 1962) is not external, surrounding it like a ditch (Derrida, 1977: 17), but rather internal to the act of ‘breaking up’ or specifying a performance.

The metaphor of ‘frame’ is still useful to understand the agency of the performative act—how things become understandable and acted upon. Carving up frames suggests delineations, defining inside from outside. Focusing on the frame-making repositions agency in understanding performativity. This involves a shift from the agencement of risk frames to the doing of ‘cutting’ up the world, that is, the production of the agencement or framing. The analysis is thus moved ‘down’ to incorporate the politics of frame constructions. Butler (1993) evokes this in how gender performativity materializes sexed bodies ‘stabilized over time to produce the effect of boundary, fixity, and surface’ (p. 9). The discursive cuts produce material effects. However, with her focus on social forces, Butler gives less significance to materiality in conceptualizing the performative act and potential misfires (Barad, 2007; Callon, 2007a; Kirby, 2011).

Barad (2007) further develops Butler’s theory of performativity by reconceptualizing the nature of matter and discursive practices. With her neology ‘intra-action’, Barad (2007) signals the mutual and entangled constitution of discourse and matter: ‘[I]n contrast to the usual “interaction,” which assumes that there are separate individual agencies that precede their interaction, the notion of intra-action recognizes that distinct agencies do not precede, but rather emerge through, their intra-action’ (p. 33). It is through the material-discursive intra-actions that phenomena become meaningful. A specific intra-action then enacts an agential cut effecting a separation of, for example, ‘subject’ and ‘object’ suggesting a structure among these components (Barad, 2003). Agency is the dynamic and ongoing configuration of constituting boundaries through agential cuts (Barad, 2003; Nyberg, 2009).

By shifting the focus of performativity from agencement to the (re)configurations of phenomena through agential cuts, it is possible to open up discussions of power and politics. The performative acts forge (Butler, 1999) or cut (Barad, 2007) conventional understandings of a phenomenon, bringing about the effect of an entity or category. Intra-actively producing entities or categories constrain and enable what can be said and done. The cuts have regulative and normative effects (Barad, 2007; Butler, 1997). This productive understanding of power allows for studying the ongoing constitution of risk. The risk frames have both codifying effects regarding what can be known (‘effects of veridiction’) and prescriptive effects regarding what is to be done (‘effects of jurisdiction’) (Foucault, 1991: 75). This opens up questions of how risk frames serve some interests more than others, which also implies distribution of responsibilities, accountabilities and, most importantly, material effects.

The complex nature of climate change provides an ideal context within which to examine the performativity of corporate risk construction and framing. While the science of anthropogenic climate change has solidified around a rigorous consensus highlighting the dire consequences of our escalating greenhouse gas (GHG) emissions (Cook, et al., 2013; IPCC, 2013), the political debate about how to respond to the science has become a politically vexed and polarizing issue. Conservative political parties and the fossil-fuel industry have promoted a climate change denial movement which has been highly successful in delaying emissions regulation (Dunlap and McCright, 2011). These delays have resulted in dramatic increases in GHG concentrations with devastating material effects. Climate politics are thus volatile and uncertain in terms of how we understand the multifaceted nature of climate change impacts, how we should respond to them and who we should hold responsible for taking action. As central contributors to the production of GHG emissions and influential actors in the politics of climate change, corporations are central players in this contested political arena.

In investigating the performativity of corporate climate change categorizations, we developed three research questions. First, in understanding how climate change has been produced and segmented into manageable corporate components we are interested in (1) How corporations produce climate change risks? Second, in order for these particular cuts to have effect, certain conditions need to be in place. Developing the politics of performativity, we ask, (2) What are the processes of naturalizing climate risk frames? Finally, considering that these cuts produce inclusions and exclusions of what (and who) is taken into account, there will always be potential misfires. This led to our third research question: (3) How do climate risk misfires happen and how are their effects distributed?

This study

In responding to these questions, our investigation draws on a broader study of Australian business responses to climate change conducted during the period 2009–2013 (Wright and Nyberg, 2015). Climate change has been a subject of particular political and social contestation during this period which included the failed Copenhagen climate talks, the resurgence of climate change denial in media and public polling, and dramatic changes in the political leadership in Australia in large part due to climate change policy (Rootes, 2011). Like the United States and Canada, climate change in Australia has become a central feature of political contestation and corporations have been forced to develop more explicit approaches to this issue as a result of regulatory and political change (Hoffman, 2012; Nyberg, et al., 2013).

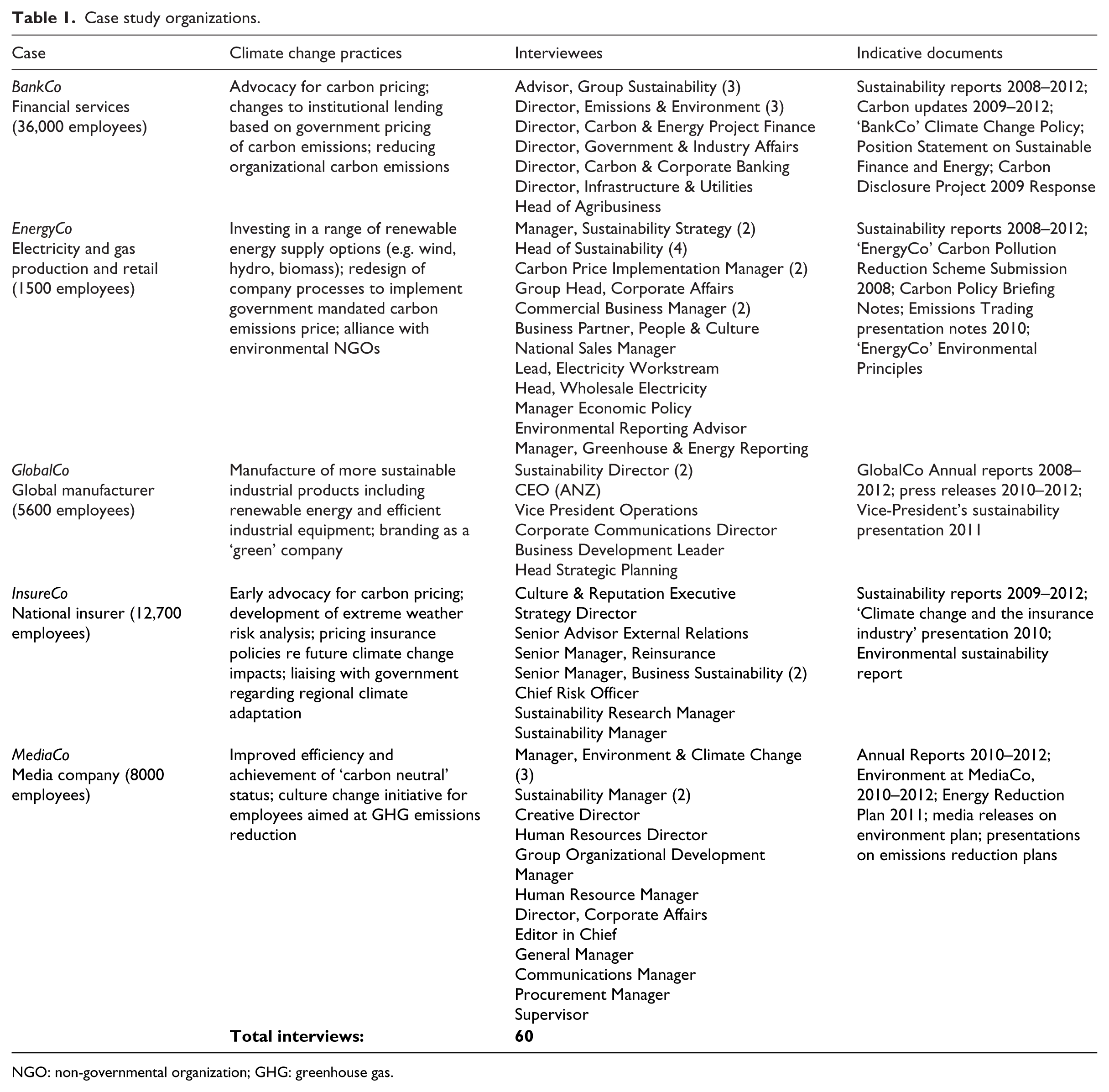

In this article, we draw on data derived from five case study corporations. As outlined in Table 1, these five corporations included the following: a leading energy producer which was supplementing fossil-fuel generation with renewable energy sources, a large insurer that was measuring the financial risks of extreme weather events, a major bank which was factoring in a ‘price on carbon’ in its lending to corporate clients, a global manufacturer which was reinventing itself as a ‘green’ company producing more efficient industrial equipment and renewable energy technologies and a global media company that had embarked on a major eco-efficiency drive to become ‘carbon neutral’. Our empirical data include a total of 60 interviews with senior and operational managers from the five companies as well as an extensive range of documentation including sustainability and annual reports, submissions to government, shareholder briefings, climate change presentations and policy documents. The interviewees were chosen on the basis of their direct involvement in their organization’s response to climate change and involved a range of questions exploring these practices. The interviewees lasted on average 90 minutes and were all transcribed verbatim.

Case study organizations.

NGO: non-governmental organization; GHG: greenhouse gas.

While the initial aim of our research was not to study risk per se, the concept of ‘risk’ emerged early on in our data analysis as a key discourse for managers and corporations in their engagement with climate change. Indeed, the centrality of risk in our data echoes accounts in the business literature (Hoffman, 2005; Lash and Wellington, 2007), surveys by consultancies (Center for Climate and Energy Solutions (C2ES), 2013; Enkvist and Vanthournout, 2008) and other empirical studies (Loechel, et al., 2013; Mills, 2009). Thus, our theoretical engagement with risk followed from our initial analysis of the empirical data.

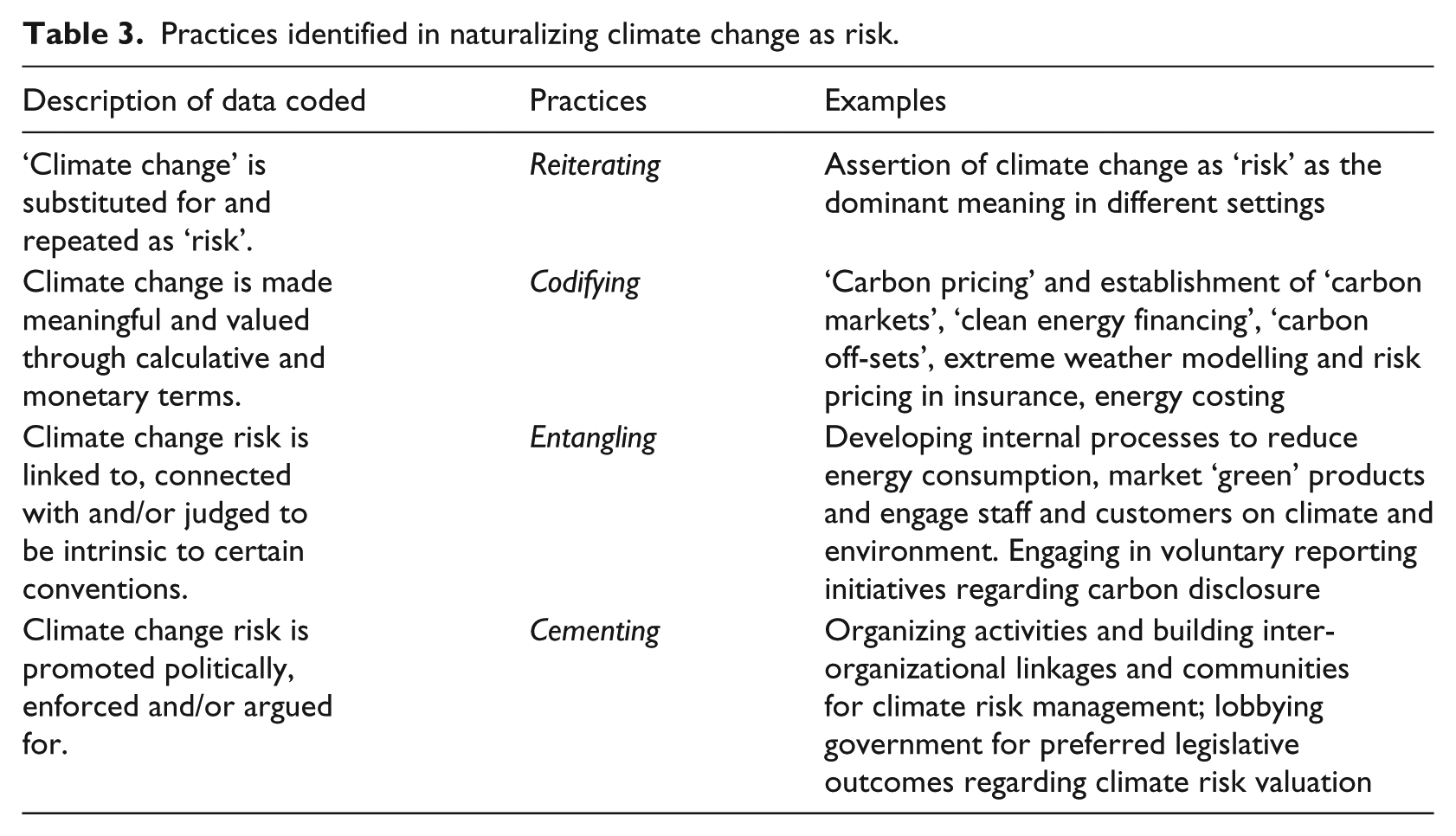

Having identified risk as important empirically, we then undertook a more specific coding of our data around this concept. First, we identified how corporations engaged with risk. Based on this coding, we identified three frames of risk developed and repeated in response to climate change: ‘physical’, ‘regulatory’, and ‘market’ and/or ‘reputational’ risks. Second, we coded for the different corporate practices, policies, rules, techniques and technologies through which these frames were enacted and expanded both internally and externally. Third, we re-analyzed our data in terms of how these particular frames became meaningful and were enacted, that is, their performativity. In our analysis, we identified four interrelated processes of naturalization: (1) reiterating climate change as risk, (2) codifying the risk in monetary value, (3) entangling the risk in the market and (4) cementing the frame through political activities. However, despite naturalization of these risk frames, we found such predictions were often surprised by discursive-material events. This led us to the final aspect of the data analysis: trying to understand how misfires happen. Here, we examined how unforeseen social relations and physical forces surprised corporate actors’ previous risk delineations and framings. These were instances when corporate framings could not account for events.

From climate change to risk management

Climate change is far from a recent concern for business. Indeed, managers in all five case studies related long histories of how their organizations accepted the mainstream science of anthropogenic climate change and had identified it as an emerging business issue. As noted by one respondent, this business acceptance of climate change contrasted with the public debate about climate change in the media and political arenas: … there is a bit of disconnect in terms of public perception around the newness of climate change and business understanding of where some of those impacts and issues are … [Climate change] is an issue that’s been ticking around for a while and has been considered an emerging business risk for quite a while. I mean I’m talking ten years. (Sustainability manager, BankCo)

Another respondent pinpointed the exact year (1995) that their organization started to incorporate a price on carbon in their investment decisions, some 17 years before carbon pricing was eventually introduced in Australia.

Importantly, corporations’ understanding and action in response to climate change were rationalized as a business decision aimed at improving profitability. As a manager at EnergyCo stated, ‘it’s not ideological—it’s purely a business case’. Well aware of the emotive and politically charged public debate surrounding climate change, interviewees and corporate documents sought to frame this issue around what they saw as the more ‘neutral’ terminology of ‘risk’ and ‘risk management’. This change of terminology happened both internally within organizations and externally towards customers, investors and other interest groups. For instance, as the sustainability manager at InsureCo noted, ‘climate change just polarises people. Whereas if we internally talk about “weather risk” … people tend to kind of keep listening, rather than shutting off’. Turning climate change into risk was then a deliberate decision to delineate risk from climate change to ensure that the corporation or industry could ‘manage’ the issue. As another manager at InsureCo noted, ‘Businesses get risk so I think we’ve got to—I don’t know how, but somehow reframe’. This reframing was often referred to in terms of the uncertainties surrounding climate change: So maybe we don’t exactly know what the impacts of climate change are, but surely most people would agree that there is enough of a potential risk around that maybe we should do something about managing it. It is just risk management! (Sustainability manager, EnergyCo)

The framing of climate change into risk management was well articulated by a director in BankCo, ‘… the whole greenhouse effect—is a global environmental risk, which turns into a global economic risk, which turns into a business risk for our customers. So it’s a risk’. Indeed, through reframing it as ‘risk’ companies and managers were then able to engage with this frame with greater confidence and certainty. This even allowed space for identifying business opportunities that might exist in a changing future. As the CEO of GlobalCo outlined, Climate change has been caused by man-made activities, that’s in excess of 90 per cent. When was the last time you made a business decision with that degree of certainty? So I think you’re foolish if you’re not starting to take action around, first of all, how do I mitigate the risk of how this is going to impact my business? Secondly how do I create an opportunity out of this issue?

As another GlobalCo manager emphasized, ‘We see [climate change] as a business risk on the one hand. But also there’s a business opportunity there perhaps if you can reposition’.

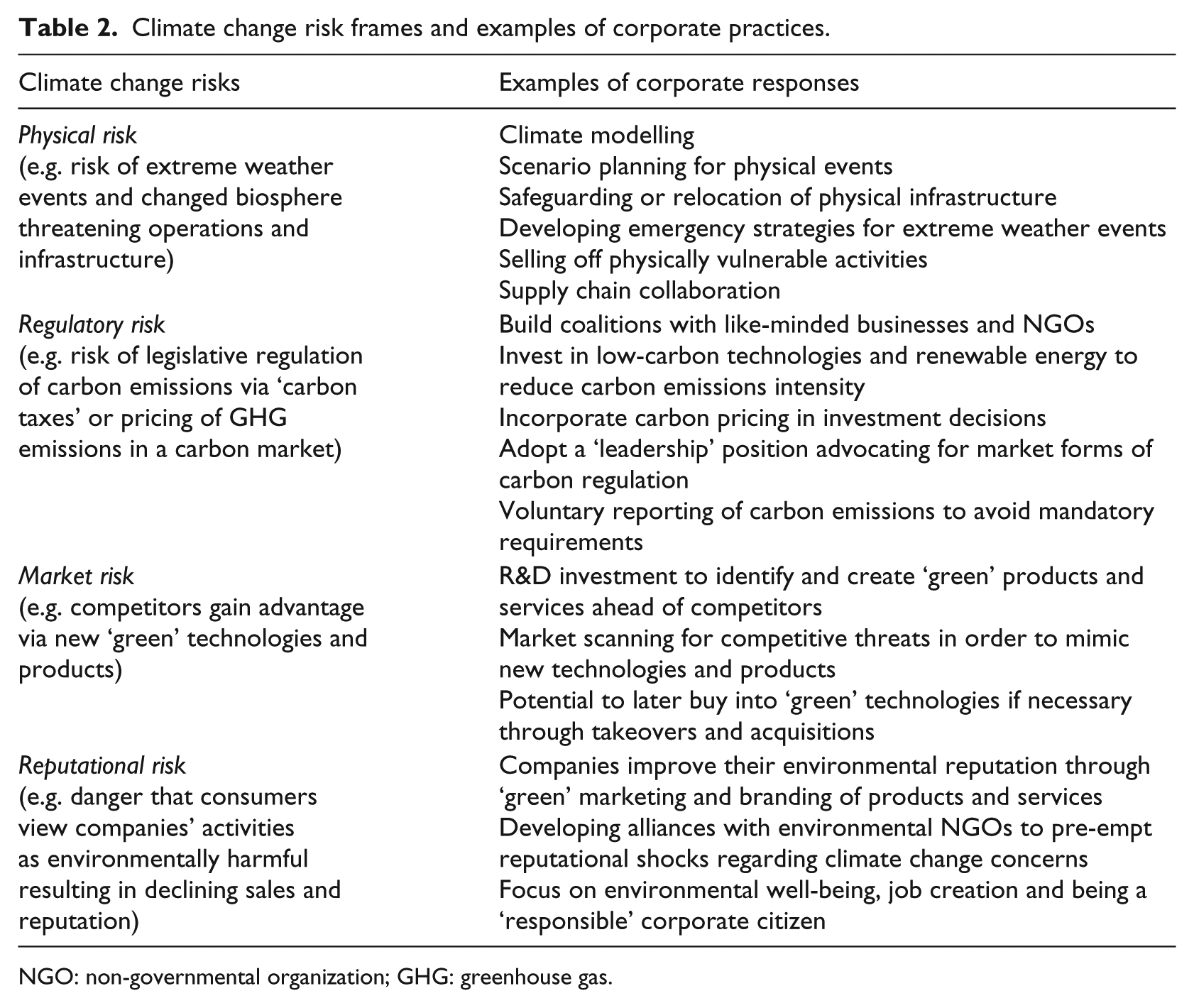

In order to ‘manage’ the risks surrounding climate change, the corporations in our study commonly framed climate change in three specific risk categories: physical, regulatory and market or reputational risk (see Table 2). Considering the consensus of this terminology with other studies (e.g. Lash and Wellington, 2007), this frame represents a standardization of climate change and could be reiterated in a range of circumstances. Repeating climate change as risk also gave climate change a somewhat positive light. While challenging, the risks were seen as preventable.

Climate change risk frames and examples of corporate practices.

NGO: non-governmental organization; GHG: greenhouse gas.

Physical risk

The physical risk frame emphasized the direct and indirect effects of changes in the environment on business activities. For example, at EnergyCo, the physical risk framing was evident in managers emphasizing the role of increasingly hot summers, droughts and bushfires resulting in increasing demands on peak power generation, threats to facilities such as large coal-fired power plants unable to source adequate cooling water and complications for the distribution of electricity (e.g. arcing from power transmission lines in heatwaves as a source of bushfires).

Physical risk frames were also evident in the banking and insurance industry as a way in which climate change was made meaningful. At BankCo, for instance, senior managers explained how physical risks to investments were an increasing focus in trying to make sense of climate change: is where it is located going to be of concern over the life of the asset in terms of storm damage or is it in an area that is likely to become a cyclone zone in the next 20 years? You know, are there adequate insurance or business continuity plans in place to be able to deal with that?

At InsureCo, a series of unprecedented storms and bushfires during the 1990s and 2000s surprised the risk models and led to a growing awareness of the company’s financial exposure to extreme weather events. This prompted the company to develop specialist groups of experts to account for changing weather patterns and a much closer analysis of the company’s exposure to regions likely to be hit by future storms and fires. As a former executive related, you’ve had this build up of weather events, extraordinary flooding in northern New South Wales and southern Queensland of the kind we’ve never seen. Like just flood on flood on flood. We’ve had the Victorian bushfires, just extraordinary and a number of things happening offshore that will go to the cost of reinsurance that will then impact the domestic general insurance market that are weather related. Much bigger hurricanes, more intense rain falls … So the (insurance) industry, both at the Australian level and globally, is re-forecasting all the time based on these much bigger impacts of weather events which the more enlightened people in the industry see are directly linked to changes in our climate.

The performative work of physical risks thus included reframing their response to climate change by modelling for weather events, safeguarding infrastructure, collaborating with the supply chain and developing emergency strategies.

Regulatory risk

The second risk frame evident in the case studies related to what was termed ‘regulatory risk’ and focused on the perceived uncertainty over future government regulation of GHG emissions and the potential for legislated ‘carbon pricing’, a topic of ongoing political discussion. For example, corporations with high levels of GHG emissions viewed future changes to emission regulation as having the potential to make their operations increasingly costly and uneconomic. One response was to improve energy efficiency and reduce their reliance on fossil fuels. For instance, EnergyCo, which was one of the country’s leading energy retailers, had diversified its energy production by investing in renewable energy sources such as wind, solar and geothermal power. As a senior sales manager outlined, ‘I think as an energy company you’ve got to have a balanced portfolio. Anyone that tries to back one horse—that’s a very high risk strategy’. MediaCo, although a less significant emitter of GHGs, had also undertaken an extensive organizational change programme focused on radically reducing its carbon emissions, in part focused on reducing its exposure to a future world of carbon pricing.

In seeking to inform regulatory changes, firms also articulated a ‘leadership position’ in policy debates by advocating for their preferred market-based forms of carbon trading and defined reduction targets. Hence, BankCo had been prominent for some years in promoting the virtues of a legislated price on carbon and the movement towards a fully fledged ‘carbon market’ in which emissions could be traded as a commodity. As one senior BankCo manager explained, ‘as a business we already incorporate climate change or carbon risk into our lending and lending investment’. Not only was this risk frame seen as opening up future business opportunities, but it was claimed that such a market approach was the most effective and cost-efficient way to reduce GHG emissions.

All of the cases also engaged in framing the discussion of regulatory risks by producing various voluntary reporting documents. Such voluntary actions were seen by many managers as a preferable alternative to government-mandated action. Thus, the performative work on the regulatory risk of climate change produced political activities and attempts to shape climate legislation and changed production practices, incorporation of carbon pricing in investment decisions and involvement in voluntary reporting which signalled firms’ environmental engagement.

Market and reputational risk

The third framing of business risk related to the market and reputational implications of climate change. This included the potential for new disruptive, ‘low-carbon’ technologies to challenge established business models, as well as the threat of changing stakeholder perceptions of companies’ environmental impact. In terms of market risks, a key issue expressed by our respondents was the potential for other companies to gain a competitive advantage through the early adoption of ‘green’ technologies and products which were better suited to a carbon-constrained world. One response was to invest in research and development in order to identify, create and bring to market these new technologies ahead of competitors. So, for example, GlobalCo had become a leader in the design and development of the so-called green technology and now produced wind turbines, fuel-efficient jet engines and electric vehicle infrastructure. Senior managers argued this positioned them as future leaders in a ‘green’ economy.

Increasing public awareness of climate change through media reporting and non-governmental organization (NGO) campaigns also resulted in a corporate realization of the reputational risk that flows from an association with GHG pollution. A common response for corporations was to use marketing and branding to promote their environmental and ‘green’ credentials. For example, MediaCo’s organizational change programme emphasized employee and customer involvement in reducing carbon emissions. As the programme branding emphasized, ‘Climate change is about all of us. Everyone can contribute by changing what we do by one degree, in lots of ways every day. Together these actions will help us change the future of the planet’. Such marketing offered the potential to manage public awareness of climate change by presenting companies as ‘taking action’ and ‘leading’ on this issue.

Beyond external branding, another way of managing reputational risk was to form alliances with environmental NGOs. Managers at EnergyCo stressed how having a relationship with selected NGOs allowed them to better frame their external messaging and lobbying of government. As one manager pointed out, We engage a lot with different green NGOs and some of them are more constructive than others … WWF and the Climate Institute and ACF, they are a lot more practical. They will work with business. They understand that business still has to make money. We are still going to be emitting greenhouse gas emissions, end of story. Of course we are. We are still going to be using resources. But they can kind of work with you to help you get better policy positions that also meet their end goals.

Thus, in framing climate change as a market and reputational risk, corporations produced new products and services and engaged in new collaborations to be included in managing the risk of climate change.

The performative work of risk

By framing and dividing climate change into different types of risk, corporations played a central role in bringing particular realities into existence. For instance, the division of climate change into physical, regulatory and market risk broke up a complex and amorphous concept into smaller components. This replaced the complexities of climate change and shortened the time frame of decades of scientific projection. As the sustainability advisor at BankCo acknowledged, … the long term risk of climate change activities impacting on business are far greater than any risk from an emissions trading scheme. But that is not the sort of thing that fits into your normal three year strategic planning project cycle!

Climate change was thus alienated from the environment and reframed as a calculative probability. As a senior manager at InsureCo explained, his business depended upon such assertions in the daily calculation of insurance premiums and future extreme weather events: ‘we are just picking out the risk at the end once all these decisions are made … all we’re doing is just measuring the risk once it’s established’. The framing thus produced a clear ontological argument of what climate change is and how it can be codified. The risk frames emerged entangled with market conventions to ensure that the frames had a grip, that is, became meaningful and were enacted. These conventions placed a value on the risk calculations and provided the conditions to enact the valuation. To support the conditions of the frames, corporations also cemented these within political activities.

The codification of climate change

An important measure of corporate engagement in framing climate change was to make it meaningful in a business sense, that is, codify climate change as calculative and valued in monetary terms. This involved a process of commodification where risk management assigned values to constructs, such as ‘carbon’, which could then be perceived as measurable, comparable and exchangeable. For instance, the former head of strategy at InsureCo referred to the critical practice of ‘pricing risks’ in order for his business to be able to deal with climate change. Through codification of climate change, uncertainty became epistemologically stable and risks could be known and incorporated into decision making.

This codification was performative in that risks became calculative and comparable, often using forms of cost–benefit analysis which allowed for risk distribution. For example, in terms of regulatory risk, the calculated cost of legislation on climate change could be compared with the cost of other outcomes, such as job losses or gains, curtailed or new investment. As one manager explained, ‘Underpinning this change are the regulatory responses that will put a price on carbon, stimulate investments in “green” energy and technologies’. Hence, the valuation of risk allowed climate change to become an economic opportunity, appealing to a range of powerful interest groups. This was particularly the case for financial services such as banking and insurance. As the director of carbon and energy finance at BankCo argued, ‘pricing carbon’ facilitated new markets and opportunities: ‘the easiest thing to do is go carbon trading—there’s a way to make money!’ By doing this, the risk could be embedded within the company’s policies and practices, as well as ensuring corporate customers were also acting on the particular risk framing. As BankCo’s environmental director explained, [customers] need price risk management tools in terms of carbon trading but they may also need additional working capital, in terms of upgrading technology or systems to reduce energy consumption, so energy efficiency or clean technology or investing in biodiversity offset projects as a way of managing their future carbon price exposure.

Indeed as this manager went on to explain, if corporate customers were not managing their climate change risks then, ‘… we will price that risk higher and then we may not do the deal because it’s no longer economic’. The commodification and valuation of climate change thus became part of the business model, and it was through this codification that new customers and opportunities were identified. For the insurance industry, the work of pricing climate change risk was presented as part of their business model. As InsureCo’s former CEO explained, ‘We’re in the business of understanding and pricing risk and weather-related events’. The risks were naturalized and supported by normal business practices.

The codification of climate change thus qualified the risk frames to be commensurable with a range of market responses, such as creating carbon pricing and trading mechanisms, developing new capabilities to better estimate and price changing climate risks, as well as upgrading technology and internal expertise. With monetary value, the risk frames became naturalized as ‘real’.

Entangling climate change risks with the market

The codification of climate change ensured commensurability between the valuation of climate change and a system that supports valuation. The climate change risks were reiterated and entangled through the activities of sustainability departments and managers who developed internal practices and policies which furthered risk commodification, modelling and adherence to risk management procedures. For instance, as the environment manager at MediaCo outlined, ‘my job is to keep their risk as low as possible and possibly to zero, on all aspects of environment, from regulatory right through to perception and reputation’. The assumption was that certainty, zero risk, could be produced through measuring and pricing climate change risks. At BankCo, a specialized team had been established to deal with climate change risks. According to the environment director, this team’s role included, ‘… talking to all the clients, developing all the products, seeing what product demand is emerging, working with the different product and relationship management teams to respond, training up all the relationship managers and the risk guys’.

How risks were handled could then be evaluated both internally, through practices of risk and performance management, and externally through economizing the risk frames. For instance at InsureCo, as the Chief Risk Officer explained, risk was a central indicator of both corporate and individual performance: ‘risk culture was also one of the key performance indicators for bonus for managers’. The entanglement of risk was also evident in other firms and industries. At MediaCo and GlobalCo, sustainability specialists stressed how innovation in internal processes (such as improved energy efficiency, waste reduction, ‘green’ marketing and employee involvement activities) not only offered to reduce costs and improve productivity but also helped to stave off the likely market and regulatory risks associated with climate change.

A good example of how risk frames were entangled in corporate practices and activities was evident at EnergyCo. As one of the country’s major electricity producers, EnergyCo was a significant emitter of carbon pollution and subject to the government’s newly introduced ‘carbon tax’. Within this changed regulatory framework, EnergyCo faced commercial pressure to ensure it passed on the cost of carbon pricing to consumers. As one senior manager explained, ‘The largest risk is not being able to pass through to the end users the costs we’re incurring upstream’. However, this also brought with it reputational risk of growing consumer hostility to increasing electricity prices. As a senior sales manager at EnergyCo explained, ‘I think one of the biggest risks is just the organisational reputation and brand risk. What’s this going to do to the [EnergyCo] brand in the broader market context?’ In order to manage this risk, the company established internal project teams to redesign billing processes and also communicate with customers about the ‘carbon tax’ and changes in billing in order to avoid the perception of ‘price gouging’. Climate change risk then became entangled with market valuations, roles and models, which served to further naturalize the conception of climate change as involving defined forms of risk.

This continuous codification and entanglement of climate change risks was further expanded globally through taking part in and supporting national and international emission-trading schemes. Given the process of commodification of climate change risk, the only sphere that can adequately deal with commodities is, of course, the market.

The politics of cementing climate change risk

In framing climate change as different forms of risk, corporations also needed to ensure these frames were socially binding. While the reiteration of climate change as different forms of risk was not necessarily politically motivated (indeed, this is how corporations commonly deal with uncertainty), the management of these risk conditions involved corporate political strategies. In the businesses we studied, managers sought to strategically influence the broader conditions within which risk constructions were debated by influencing other corporations, the government and the public.

Cementing climate change as risk and the valuation of these risks often involved inter-organizational collaboration. So, for example, in seeking to manage the carbon pricing risks it envisaged in future government regulation, BankCo organized seminars, workshops and conferences which involved senior managers from other corporations, government officials and other key climate change ‘thought-leaders’. As a senior manager explained, these events helped to emphasize the risk framing that the organization had adopted to climate change. Moreover, this risk framing spilled out across the broader community of sustainability professionals both in work and in more informal settings and shaped an occupational discussion of climate change as risk. As the environment manager at BankCo noted, The reason I know all the guys from the other companies is also because we obviously do a lot of client engagement around carbon and so you tend to meet the treasurer or the CFO who’s managing the risk and the sustainability or environment person who’s reducing the risk. So in terms of all the advocacy activities, we all tend to be on the same forums and so forth. So that’s probably why it’s a bit of a club.

Through the collaboration with other, often competing, corporations and industries, the corporations ensured a hegemonic dominance of the risk frames entangled with market conventions.

The political strategies to manage the conditions of the risk frames also included lobbying government for legislative outcomes that best suited particular corporate strategic positions. As the external relations manager in BankCo explained, ‘There’s a lot of interplay between what the business does and … how that’s communicated to government and also how we position ourselves in relation to regulatory and reputational risk’.

This political engagement extended to rival political parties given the likelihood of a change in government and the need to accommodate to shifting regulatory frameworks. While all of our case study companies were supportive of the need for ‘action on climate change’, there were differences in perceptions of how this could be best achieved. Hence, the environment manager at MediaCo stated his company’s opposition to the ‘carbon tax’ and emphasized an alternative model of voluntary corporate efforts to become ‘carbon neutral’. In contrast, senior managers at BankCo supported the government’s introduction of carbon pricing as this facilitated carbon trading as ‘a way to make money’, and for individual managers to feel they were playing a part in responding to an urgent social and environmental issue.

This political work by corporations was thus seen as critical in cementing climate change as both a regulatory and market/reputational risk. Whether for or against specific government policy, the corporations codified climate change as an economic risk valuation, often far divorced from the material consequences of climate change as a natural hazard. The performative risk framings were thus political, with corporations favouring particular descriptions of reality that corresponded to their economic interests. Indeed, there is arguably no direct benefit for a bank or insurance industry to mitigate climate change, such as floods, when the possibility of pricing the risk exists. As the BankCo environment manager outlined, ‘If they are managing it really well, no matter how “dirty” an industry they are, but if they’re managing their risk really well, we will lend to them. That is our position’.

Indeed, by hedging and spreading their risks through risk management, corporations were able to manage plural futures and distribute future effects to other actors who were not part of the discursive negotiations. Critically, the distribution of codification is far from equal in that not all can take part in risk framing. The market entanglement ensured that market institutions and actors were favoured in configuring climate change. However, the narrow framing of climate change in business risks produced misfires, where unaccounted factors upset risk calculations.

Misfires

The cuts or delineations of climate change into different forms of business risk simultaneously produce an ‘inside’ that was accounted for and an ‘outside’ that was hidden or marginalized. Thus, the performative cuts produced a particular reality. However, the conventions and political strategies only ‘hid’ how reality had been broken up. Moreover, these risk frames only accounted for calculable and linear natural effects, market actors and self-interested aspects of consumers. As a result, the excluded forces and relations continuously surprised the performed ‘reality’ in a variety of ways.

First, the narrow risk frame of climate change, codified in terms of measurements of carbon dioxide (CO2) emissions, meant that many aspects of the natural environment were not accounted for and often resulted in misfires in risk calculation. For example, EnergyCo’s recent investments in coal-seam gas production were promoted publicly as a ‘cleaner’ fossil fuel for electricity production contributing around 60% of the CO2 emissions of comparative coal-fired power generation. However, while ‘carbon’ in terms of CO2 emissions has become marketized and priced as risk, fugitive emissions from these activities of the far more powerful GHG methane (CH4) were notably downplayed. Moreover, the reiteration of climate change as risk excluded non-linear aspects of natural forces. This meant that corporate representations were ultimately unable to fully account for climate change complexities, such as extreme weather events and other unforeseeable realities. As the senior risk officer at InsureCo acknowledged, I mean most people didn’t think it hailed in Melbourne until last year. There was another one in Perth, you know it was classic. It was known in the industry as ‘un-modelled risk’, which means there isn’t a detailed model of the risk that you can use to price it. Perth—hail in Perth was unknown. I mean completely unknown.

Second, non-market actors were excluded from the risk codification and often later intervened in ways that wrong-footed corporate risk modelling. So, critiques of corporate climate initiatives continued to surprise their creators most often in allegations of ‘greenwashing’ and hypocrisy. For instance, despite BankCo’s claims to reducing its own carbon emissions and encouraging its corporate clients to adopt more climate-friendly practices, NGOs criticized the company and its competitors as the major source of investment for fossil-fuel-based energy production. Similarly, MediaCo and GlobalCo’s reputational claims to climate responsibility were often subject to public criticism as forms of ‘greenwashing’ by NGOs and the media. In the case of MediaCo, the internal focus on emissions’ reduction stood in marked contrast to the editorial line of the company’s newspapers which were prominent in their climate scepticism and promotion of climate change denial. At GlobalCo, public critics contrasted the company’s claims to producing ‘green’ future technologies with its involvement in coal, oil and nuclear technologies.

Finally, only certain aspects or subject positions are taken into account in framing risk. For example, market and reputational risk frames exclude aspects of consumption or consumer identification that are not based on market conventions. So, for instance, EnergyCo’s promotion of ‘cleaner’ coal-seam gas resulted in a vehement and ongoing public relations battle with agricultural landholders and communities which objected to gas ‘fracking’ as environmentally harmful (endangering groundwater aquifers), threatening to their health and well-being, and destroying the nature of rural life. Here, non-market conventions of community, aesthetics and the natural environment impinged on the risk calculus of lower carbon emissions and increasing commodity prices for ‘natural’ gas. Images on the nightly news of farmers and protestors locking themselves to bulldozers and angry protests outside the company’s city headquarters provided vivid examples of such a misfire.

However, considering the grip of market conventions, these misfires appeared to have a limited impact on the corporations themselves. Claims from non-market actors or marginalized consumer voices could be countered by corporate strategies of drawing new lines of risk (with potentially new misfires). Indeed, the framing of climate change risk was continuously reiterated and adapted. This ensures that corporations distribute the consequences of risk framing to those actors with least political and economic voice and agency: the environment, local communities and vulnerable actors. For instance, at InsureCo the costs of risk framing misfires fell on local communities. As the senior risk officer acknowledged, ‘ultimately the insurer can always put his prices up and cover himself … but that just means the community’s paying for the risk at the end of the day’.

Similar to the consequences of the global financial crisis, with assemblages of market actors ‘protecting’ their frames, the assumed predictability of risks ensures that these actors are not accountable for such misfires. However, unlike the financial crisis, in the case of climate change, governments appear unwilling to take on the social and financial costs. Thus, eventually it appears citizens and local communities will bear the consequences through higher insurance prices or indeed a lack of insurance altogether.

Discussion

In this section, we return to our three research questions and discuss their theoretical implications. In responding to the first question how corporations produce climate change risks?, our analysis illustrates how risk frames bring the present to bear on the future by providing ‘conditions of possibility’ for future actions (Maguire and Hardy, 2013: 249). The formation of climate change risks establishes particular framings of the future, that is, the meaning and understanding of climate change fabricate the possible ways to act on it (Yusoff and Gabrys, 2011). Producing climate change risk in particular ways justifies certain actions and it is the performative acts that give the future presence. Corporate claims surrounding climate change are performative in that they change the present and, at the same time, colonize the future through acting upon particular conceptualizations of climate change. Risk constructions have ontological effects in leading to certain social conditions and consequences. These agential cuts of particular risk frames can be used strategically to create both certainty and uncertainty in how the future will look in order to compose specific risk domains to suite corporate interests (Gephart, et al., 2009).

As a result, in nominating or naming climate change as risk, corporations not only engage in cultural framing or construction but this process also has material effects. While risk discourses are familiar framing devices in a Goffmanesque sense (see, for example, Howard-Grenville and Hoffman, 2003), the corporate performance of producing risks also does something in the world (Austin, 1962). Our analysis demonstrates that risks are performative; they contribute to the reality they describe. This challenges any division between discursive constructions and materiality (Hardy and Thomas, 2014). The risk frames are materialized in their performance (Orlikowski and Scott, 2015). The production of risk is thus an action that shapes the world and its response to climate change. Enacting certain cuts over others produces interventions, which open up options for particular actions and close down others. The materialization of corporate delineations thus has performative consequences.

The production of risk frames is, however, dependent on appropriate circumstances; to produce a meaningful risk frame requires risk conventions. With this, we do not separate the performative acts, or cuts, from the discursive-material surroundings. The norms or rules of the discourse only exist in their performance (Wittgenstein, 1953); hence, ‘there is no language; there are only acts of language’ (Callon, 2007b: 318). The conventional procedures supporting the performative acts are also performative acts. Thus, rather than separating performative acts into categories of linguistic and non-linguistic, or discursive and material, in order to understand their sincerity or truth (Searle, 1969), our investigation suggests an alternative typology. As outlined below, this typology rests on the necessary conditions for performative acts to be performative (Derrida, 1977). Considering this, the answer to the first question is corporations produce climate change risk by framing ‘what is’ (climate change is risk) and ensuring that the conditions exist for the frame to have effect, that is, performing the ‘what is-ness’ of the frame.

Unpacking the underlying processes of this answer leads us to the second research question: what are the processes of naturalizing climate change? Our empirical analysis developed a typology of processes naturalizing climate change as corporate risk: reiterating, codifying, entangling and cementing (see Table 3). For a performative act or cut to have an effect, the act needs to make sense. This is not due to the transmission of meaning (a cultural form of analysis) but rather the possibility for the act to be reiterated in other circumstances. For example, in configuring climate change as risk, the sign or expression of risk needs to make sense beyond equating risk with climate change. Thus, in saying that ‘climate change is risk’, the idea of risk can be repeated in other circumstances without including ‘climate change’. Risk is simultaneously substituting for, and different to, climate change.

Practices identified in naturalizing climate change as risk.

However, equating climate change to risk is a narrow substitution, useful only to particular settings and circumstances. As a risk, ‘climate change’ takes on different qualities; it is codified. Through the codification of risk, climate change becomes a particular being: calculable, comparable and exchangeable, that is, a commodity. This codification of climate change into monetary value ensures that there are performed conditions for the cut to be performative. Thus, there are conventions that ensure that valuating climate change will have an effect, that is, climate change can be exchanged and become tradable.

There are already market conventions performed to ensure that the reiteration of climate change, codified in monetary terms, is enacted. The entanglement of climate change and the market suggests that the construction of these two constructs is shaping each other or intra-acting. Furthermore, the intra-action produces new constructs and meanings, such as, carbon markets. Following the codification of climate change to a monetary value, the alienation from the environment is complete with the entanglement producing solutions solely based on the marketization of climate change.

Finally, with a plurality of possibility to reiterate and codify climate change, the particular frame can be challenged by alternative imaginings of climate change (Levy and Spicer, 2013). Thus, to ensure continuous reiteration, the frame needs to be cemented in public and political conventions. As we have seen, the five corporations’ political activities worked to establish the conditions for climate change as risk. Interestingly, the reiteration and cementing of climate change as risk included both corporations supporting and opposing regulatory actions on climate change. Thus, the naturalizing effect of climate change is dependent on four different types of performative acts or cuts to produce the ontological effects: reiterating, codifying, entangling and cementing.

However, despite the robustness of the naturalized risk frames, our analysis showed how these constructs can often misfire. This leads to the third and final question: how do climate risk misfires happen and how are their effects distributed? Beginning with the first half of the question, the misfires of the risk constructions were not due to externalities overflowing the frames. Rather, the misfires came from within. The frames could not uphold the complexities of the discursive-material world and the crumbling frames were laid bare, showing the narrow agential cuts of inclusion/exclusion as well as the politics of the supporting conventions. This performative account of risk thus suggests a continuous and pluralistic process of producing a future that surprises its predictions.

By shifting the focus of performativity from agencement (with symmetry between humans and nonhumans) to the (re)configurations of phenomena through agential cuts, it is possible to open up the discussions of power and politics, which is sought after by both proponents (Callon, 2007a) and critics (Whittle and Spicer, 2008) of the anthropology of the market. Performativity is then itself a political activity, in that the enactment of risk frames involves the distribution of resources and power both within organizations and society more generally. The agential cuts open up questions of how risk frames serve some interests more than others.

The performativity thesis can thus provide a basis for critique in terms of understanding corporate domination. The plural ontological possibilities of a performativity perspective provide a space for interrogating the processes of how a particular reality is brought into being with particular effects (Butler, 2010). The political processes of stabilization are opened up in order to pay attention to the continuous performance of keeping constructs, theories and models ‘alive’ (Butler, 1997). However, every process of iteration holds the possibility of failure or misfire. That things could be different can be recognized without any access to reality beyond our historically and culturally dependent meanings. The unequal power in processes of framing risks and the unequal distribution of effects provide ample ground for critique of domination. A performative theory of risk thus allows us to understand the possibility for corporations to take part in producing a construct, as well as the consequences or effects of this construction.

Conclusion

Corporate risk framings are performative in that they have material effects in turning climate change complexities into narrow risk frames. Through corporations’ performative work in disentangling the risk of climate change from the natural or environmental sphere, a shift in focus is achieved in which mitigating climate change becomes the mitigation of corporate risk and the identification of corporate opportunities. Climate change as a pattern of long-term changes in weather is dislocated from the decision to act, with only economic cost–benefit analyses taken into account. The decision to ‘act on climate change’ then becomes an economic decision to increase profit, rather than keeping CO2 emissions out of the atmosphere. This corporate performative work has ensured that climate change is addressed solely through market decisions.

This suggests that by calculating and pricing risk, turning uncertainty into certainties, alternative political actions in mitigating climate change are marginalized. While some of the corporate practices described above can have mitigating effects, their primary aim is not mitigation per se but rather navigating changed regulations, maintaining market reputation, reducing costs and increasing profitability. Thus, the performative effects of risk construction mean that businesses are not so much responding to climate change, but rather seeking to absorb climate change within existing business activities. As a result, climate change is not acted upon as ‘the greatest example of market failure we have ever seen’ (Stern, 2007: 1). To the contrary, both the misfire of the market resulting in climate change and the uncertainty surrounding climate change provide space for even greater market expansion.

Finally, any construction of risk will of course be challenged by the materiality of climate change events and current discursive formations will continue to adapt in attempting to incorporate these events. This is an area that clearly needs further investigation. Specifically, understanding the continuous intra-actions between the performative constructs of climate change risk and the materiality of climate change (Barad, 2007) will become an increasingly complex issue. While recent extreme weather events have failed to result in a groundswell of public activism around climate change, future storms and crises may well challenge the narrow frames we cling to in engaging with this issue. Misfires make room for alternative representations of climate change and different political interventions and experimentation. We can thus expect that the narrow corporate theories and models dominating current responses to climate change will fail to produce the predicted effects. The complexity of climate change will ensure continuous epistemological politics in terms of what we know, what we should do and who should be responsible.