Abstract

In this article, we examine the theoretically constructed case of private equity in the UK anno 2007. The theory at play is the theoretical edifice Luc Boltanski has been developing for more than two decades and which concerns the underlying architectonics of how social reality is constituted, challenged and stabilized. We thus interweave the story of private equity with the evolution of Boltanski’s work: from the six-world model to the widening of the critical notion of ‘test’ and the outline of a new ‘connexionist’ capitalist logic, and finally to his most recent attempts at reconnecting his sociology of critical practices with a more traditional critical sociology. Now that Boltanski’s work from the 1990s is being increasingly used and critiqued in our field, we believe it is important to engage with his more recent writings which, while less easy to ‘apply’, have acquired more depth, complexity and a change in focus in response to some of the more pertinent critique. The case of private equity is of particular interest in that for a brief moment it became the ‘face’ of 21st century capitalism, something which is significant in the broadening of our discussion into the possibilities and the limits of critique under a financialized capitalism.

Introduction

The year 2007 was an eventful year for the private equity (PE) industry and its executives. Described as the Face of the New Capitalism (The Independent, 17/02/07), PE found itself splashed all over the front pages of the UK newspapers and the subject of various television documentaries. Media outrage reached fever pitch when Nicholas Ferguson, a key city investor, pilloried the tax arrangements of PE executives: ‘highly paid private equity executives are paying less tax than a cleaning lady … I have not heard anyone give a clear explanation of why it is justified’ (FT

1

05/06/07, emphasis added). Over the summer of 2007, PE executives were forced to testify in the UK Parliament as part of the Treasury Select Committee Inquiry into Private Equity, an event that was described in the press as ‘The Trial of Private Equity’ (FT 20/06/07). It would seem, then, that the case of PE in 2007 would qualify as a proper ‘affair’ in the sense Boltanski (2013) gives it: By this term, we mean … a big public debate, triggered by a case entailing uncertain features and involving a question of justice, of which the famous Dreyfus affair remains, up to our time, the paradigm. In the course of these affairs, a conflict, which is originally local, spreads and takes on a general significance. (p. 45)

In this article, the case of PE will function as a ‘theoretically constructed case’ (Bourdieu and Wacquant, 1992) that allows us to consider the evolution of ‘pragmatic sociology’ (or ‘sociology of critique/critical practices’ as Boltanski would refer to it later)—a theoretical edifice Luc Boltanski has been developing for more than two decades, at times in collaboration with co-authors (Boltanski, 2008, 2011b, 2013; Boltanski and Chiapello, 2005a; Boltanski and Thévenot, 1999, 2006). The emphasis of such a ‘sociology of critical practices’ is firmly on the description of the social world as if it were the scene of a trial, in the course of which actors, plunged in uncertain situations, implement inquiries, develop experiments, formalize their interpretations of the state of affairs into reports, determine qualifications, and subject one another to tests. (Boltanski, 2013: 46, emphasis in original)

The sociology of critique takes as its main object of research those situations in which people are producing criticisms and justifications in the public sphere. This stance entails treating the various versions of conflict in symmetrical fashion as people account for themselves and examining the sense of justice they thereby express. The approach was originally developed in contradistinction to the asymmetrical critical sociology, mainly associated with the work of Pierre Bourdieu (1990, 2005), which focuses on revealing otherwise hidden forms of oppression, a revelation which is only accessible from the external and superior viewpoint of the sociologist. However, in his latest writings, Boltanski (2011b, 2013, 2014) has sought to integrate elements from ‘pragmatic sociology’ and ‘critical sociology’ in his attempt to reveal certain hidden aspects of our social reality while still grounding his analyses in situated actions.

We believe the case of PE is particularly interesting in that for a brief moment 21st century capitalism really did acquire a ‘face’, and thus, the critique of capitalism acquired a ‘target’ and direction. This was explicitly acknowledged by Guy Hands of PE house Terra Firma who claimed that the top 10 large buyout firms risked becoming the ‘unacceptable and unaccountable face of capitalism’, adding for good measure, ‘there are 6bn of them out there and they are gunning for us, there are [only] 10,000 on our team’ (FT 01/03/2008). It is worth pointing out at this stage that the aim of our article is not to make a judgement about PE and its worth to society; we aim to treat the various sides in the debate (and that includes academic supporters and detractors) in symmetrical fashion when exploring their critiques and justifications. Indeed, what is not in doubt regardless of one’s position is that ‘private equity tends to have a polarizing effect on public discourse’ (Wright, 2013: 4) and that a lot of the critique of PE is ‘being driven more by a wider political debate than by the specifics of the private equity context’ (Bacon et al., 2010: 1366), in particular with respect to the societal effects of a new era of financial capitalism (Erturk et al., 2010). It is precisely the public significance of these debates that makes PE suitable to discuss the possibilities of critique.

An examination of Boltanski’s work and the sociology of critique more generally is timely, considering that it has taken on increasing significance now that various aspects of it have been recently criticized (Parker, 2013), discussed (du Gay and Morgan, 2013) and applied (Huault and Rainelli-Le Montagner, 2009; Nyberg and Wright, 2012; Patriotta et al., 2011; Reinecke, 2010) in a broadly conceived field of management and organization. By interweaving the stories of PE and the sociology of critique, we aim to use the PE case to critically examine the development of Boltanski’s work and, simultaneously, look at the unfolding story of PE through the theoretical lens provided by Boltanski. As such, we follow Alvesson and Sandberg’s (2013) call for ‘a more active construction of empirical material … not just waiting passively for data to show us the route to something interesting, as is typically the case in more conventional research’ (p. 146). Practically, this means that we refrain from dividing theory and empirical material and presenting them in distinct sections. As the story moves forward, so does the theory.

Our article is structured as follows. First, we briefly introduce the object of our initial analysis, PE, and the conceptual matrix organized around the six worlds which was first published in French by Boltanski and Thévenot (1991) in their 1991 book De La Justification and developed in later writings (e.g. Boltanski and Chiapello, 2005a; Boltanski and Thévenot, 1999, 2000). We use this matrix to structure our reading of the events, commentaries, critiques and justifications surrounding PE in 2007. We will then show in some detail how actors selected meanings from a range of possible interpretations and logics in constructing critiques and defences in putting to the test the ‘worth’ of PE. This reading of the PE story ultimately leaves us in an apparent dead end, theoretically as well as empirically. Yet, this deadlock we face in our initial analysis of PE also reveals something significant about the possibilities of critique under a financialized capitalism and the limitations of Boltanski’s earlier work. In his latest book, Boltanski (2014) admits that his original pragmatic sociology which observes individuals in specific situations has the disadvantage of blinding the researcher to the social world as a totality which always pre-exists action and which subjects individual action to a system of constraints and power effects. In recent work, he therefore imports elements from a more traditional critical sociology while giving them pragmatic twists. Thus, his notion of ‘complex domination’ is responsive to the web of power relations social actors always face, and the extension of his notion of critique to encompass ‘existential critique’ addresses the need to take the social totality into account.

The contribution of this article lies in a thorough ‘testing’ of the original model developed by Boltanski and Thévenot in the context of a very public controversy which seems to fit the ideal criteria of the model as outlined by Boltanski (2013). The limitation of its application points us to the need to engage with Boltanski’s latest work which tries to keep up with the ever-changing ‘spirit’ of capitalism, in particular in its latest incarnation of a financialized capitalism where ‘the ontology of the network has been largely established in such a way to liberate human beings from the constraints of justification on action’, and there seems little reason ‘to pose the question of justice’ (Boltanski and Chiapello, 2005: 106). In putting to work some of Boltanski’s recently developed notions (complex domination, existential critique), we aim to reveal significant aspects concerning the status and capability of critique under a financialized capitalism.

The PE story viewed through the lens of the ‘six-world’ conceptual matrix

PE is the name loosely given to an industry which pools capital from investors (pension funds, insurance companies, sovereign wealth funds, wealthy individuals) into specific funds, managed by the owner-managers of the PE fund. This ‘pooled capital’ is then used to purchase, usually with recourse to bank loans (in order to provide ‘leverage’ which could amount up to 75% of the purchase price in the case of large-cap PE houses in 2006 and 2007), a controlling interest in existing companies and then delisting them from the stock exchange. The purpose of the purchase is to resell the target company at a higher price after a limited period during which the company’s operations are restructured. The proceeds—a capital gain from resale plus dividend and other payouts prior to resale—are shared between the investors (or LP—limited partners) and the owner-managers of the PE fund (or GP—general partners). PE houses would typically receive management fees of 2% on the funds they utilized and also a proportion of the proceeds of the sale of companies in their portfolio (typically 20%), technically known as ‘carried interest’ (Erturk et al., 2010; Morgan, 2009; Watt, 2008).

PE emerged during the 1980s, although the industry was then labelled as ‘leveraged buyouts’ (LBOs). The LBO of RJR-Nabisco in 1989 was probably the culmination of that particular wave and was even turned into a 1990s comedy ‘Barbarians at the Gate’. 2 The controversy surrounding the industry at the time (particularly in the United States) led in part to its relabelling to PE (Wright, 2013). In the United Kingdom, the average company subject to LBO during the early 2000s was relatively small and generally had little public profile which explains the relative invisibility of PE prior to the mid-2000s (Folkman et al., 2009). Between 2005 and mid-2007 due to some audacious billion-pound takeovers by large PE players, the industry suddenly found itself subjected to a sustained labour movement campaign and regulatory inquiries. The privacy traditionally valued by PE to provide breathing space to restructure firms further contributed to public distrust (Bacon et al., 2013). PE faced an intense level of scrutiny in the mainstream media and was required to justify its activities in order to maintain legitimacy towards a rapidly growing group of interested parties.

The public justification of PE’s contribution to the common good makes it a pertinent case to use Boltanski and Thévenot’s (1991, 2006) key work On Justification to investigate the ways in which various actors in the controversy mobilized their arguments. 3 The main concern of the original model pertained to ‘the problem of evaluating people and things in relation to conceptions of the common good within a public regime of critique and justification’ (Thévenot, 2001: 58). Underpinning the model is the basic position that there always exists a radical uncertainty concerning the ways things are, about what matters and what has ‘worth’ in society. To anchor their model, Boltanski and Thévenot (2006) draw upon various conceptions of the ‘common good’ as found in classic works of political philosophy, considering the latter as grammatical enterprises that were intended to clarify and fix rules that are oriented towards justice. The ‘worlds’ informing judgements include the industrial world (judgement in terms of efficiency), the market world (evaluation in terms of market performance), the domestic world (evaluations concerning trust, loyalty and personal dependencies), the civic world (valuing the general interest and citizenship), the world of opinion (valuing renown, fame and recognition) and the world of inspiration (judgement in terms of creativity and insight). According to Boltanski and Thévenot, these six worlds correspond to the most common representations of justice that our societies have acquired throughout history and represent the base of social interactions in critical situations (Eulriet, 2008). Situating the arguments of various actors in different conceptions of the common good as reflected in the six-world model may help us to unpack and contextualize some of the hyperbole surrounding PE in 2007.

The claims to legitimation PE put forward in the public domain mainly through its industry bodies, the British Private Equity and Venture Capital Association (BVCA) and the European Private Equity and Venture Capital Association (EVCA), were threefold. First, PE contributed to the common good in the market world by providing returns on investment superior to those of publicly traded equity, returns which were only weakly correlated with stock market performance (Froud and Williams, 2007). Such claims were typically backed up by graphs in glossy publications. Many fund managers and pension managers therefore saw it as a sign of their forward-looking thinking to invest part of their portfolio in PE funds. Second, and even more accepted in the UK context, was the justification for PE in the industrial world. The basic argument here was that public companies faced agency problems that could be overcome by better ‘alignment’ of the interests of principals (owners) and agents (managers) by creating board structures that were more focused and more directly incentivized to increase the value of the firm. Indeed, this ‘better ownership’ line was even echoed in a formal report on PE by the Financial Services Authority (FSA—the industry regulator at the time), which insisted that ‘the control that private equity fund managers exercise as owners of the companies they invest in is what truly defines the private equity business model’ (FSA, 2006: 45). Finally, the relatively high fees charged by PE compared to other finance providers were justified to investors on the basis that these charges represented value because of the financial and managerial skills and expertise that the PE firm would bring (Bacon et al., 2008). We see the PE industry here drawing on the world of inspiration, portraying themselves as corporate saviours. The PE industry prided itself on taking over underperforming businesses with the aim of reorganizing management and relaunching the business. And the regulator accepted this justification too, stating that ‘private equity managers can add real value by bringing their expertise and insight to a firm’ (FSA, 2006: 45).

It has to be emphasized that these justifications were initially mainly aimed at policy makers, financial journalists and investors. There was little or no engagement with critique located in the civic world. This would include the concerns raised in public debate arising out of the perception that PE gains were at the cost of other members of society, rather than the reward for a positive contribution made to that society (Watt, 2008). Perhaps Philip Yea, then CEO of 3i, put into words what many PE executives were privately thinking when he suggested in an interview, ‘While it may seem unfair that the private equity model has the advantage, that surely is the point of capitalism—that those with the advantage win’ (FT 15/02/07). In the economic context of the United Kingdom, where organizational restructurings driven by the financial markets had been common for many years, the PE boom was supported by the City institutions, the regulators, the institutional investors and even the government, and simply seen as a new and effective variation in finance-driven change processes (Morgan, 2009).

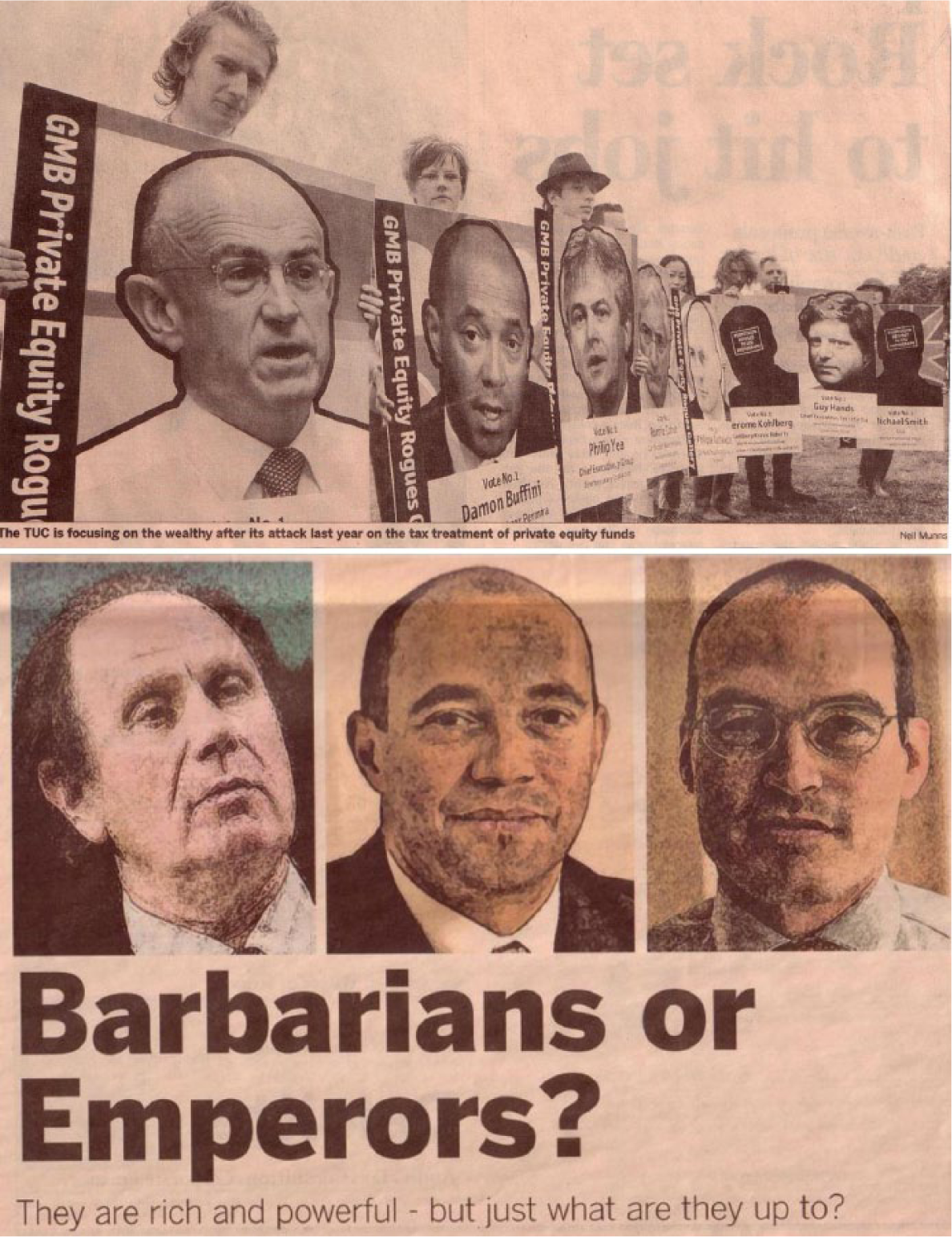

In 2005, the unions had started a campaign attacking the arguments PE put forward about itself to social actors it deemed important. This campaign was initially situated largely within the same market and industrial worlds in which PE had developed its arguments and eventually hit a nerve with politicians, the media and the public at large. The unions’ main concerns with PE were summarized by Watt (2008) as increased intensity of work and worsened working conditions in companies owned by PE; shortfalls in corporation tax revenues due to the high use of leverage (loans) and the tax deductibility of interest payments, thus creating an ‘unlevel’ playing field with other companies; and a reduction in the transparency of the corporate sector through taking publicly listed companies private, thus leading to a loss of socially valuable data. What seemed to rattle the industry most was the use the world of renown (Figure 1) as a platform to devalue PE’s societal role by singling out PE bosses as ‘rogues’ in highly personalized campaigns. For a brief moment, these PE bosses thus became ‘the poster boys of the immoral new financial sector’ (Froud et al., 2012: 20).

Locating critique in the world of renown/fame.

This pressure culminated in a full-blown media storm and a public hearing in front of the UK Treasury Select Committee in June 2007 which exposed the PE industry to a potential detrimental regulatory response for which it seemed underprepared (Bacon et al., 2013). The PE industry, increasingly worried about the public criticism, launched its own initiative on disclosure and transparency in an attempt to deflect calls for more regulation (Folkman et al., 2009). This review was chaired by Sir David Walker, a former Deputy Governor of the Bank of England as well as Chairman of the Securities and Investment Board (a precursor to the FSA), who would work with an advisory group of industry insiders. In Boltanski and Thévenot’s (2006) vocabulary, we can see the domestic world coming into play here: ‘Domestic relations are sometimes inserted into a market situation in compromise figures. In such cases a “gesture” is recommended … an accommodation with domestic reputation’ (p. 312). Many key PE figures ultimately now felt obliged to respond publicly (through speeches and interviews) and were of course required to provide testimony before the Parliamentary Committee. This is where we come close to the ideal situation of Boltanski and Thévenot’s justification model when different claims are put to the test in the public sphere.

PE put to the test?

The notion of test … offers us a tool to understand the relation between pretensions that are expressed (which can be, obviously, fantasmatic or deceitful) and the realities inscribed in the texture of the world, in that, precisely, they are able to offer a resistance to these pretensions. (Boltanski, 2002: 284, our translation)

Integral to the six-world model introduced in On Justification is the concept of test/trial (épreuve in French). Indeed, the very possibility of the model rests on the existence of test formats particular to the ‘world’ under consideration, more or less codified and explicit, so that claims can eventually be confronted in specific situations. The first requirement for a test to be considered legitimate is thus to present itself as a test of something that is precisely defined beforehand (Boltanski and Chiapello, 2005). Second, for these tests of legitimacy to work, they have to be qualified, organized and categorized so that they yield a valid ‘proof’ (Boltanski and Thévenot, 2000). Sometimes, the qualification and categorization processes underpinning a test’s legitimacy will be clear and explicit (examples being political elections and international athletics events). However, in other cases, the qualification and categorization processes may be subject to challenge and refinement and extraneous forces may occur in the tests which make the outcomes inconclusive (Bourguignon and Chiapello, 2005).

In refuting PE’s claims, the unions, followed by the media and politicians, engaged the PE industry in reality tests applied in both the industrial and the market world. In terms of market tests, critics pointed to the short-termism and variability of return within and between PE funds, with overall average levels of return being far from exciting over a longer period (e.g. Erturk et al., 2010; Phalippou and Gottschalg, 2009). The PE industry countered with its own set of numbers showing clear evidence of value creation. Critics then proffered that even if PE on average added value to companies, the results did not show to what extent this was through genuine value creation rather than ‘value appropriation’ (from other stakeholders such as workers, taxpayers, the state—Watt, 2008). In terms of industrial tests, trade unions used specific cases to ‘prove’ PE was involved in asset stripping (especially property sales) and sacking workers to make profits for the benefit of the GP. The British and European PE industry bodies responded to public accusations of asset stripping and job destruction by commissioning surveys and academic research that demonstrated not only the superior profitability of PE sectors but also their record of social responsibility in creating jobs (Bacon et al., 2013). For example, an extensive study of 190 European PE-backed buyouts sponsored by EVCA (Bacon et al., 2010) suggested that the ‘buy it, strip it, flip it’ buyouts involving short-term ownership and focus on improving efficiencies only represented a very small share of their sample and tended to occur only at market peaks and with very large buyouts. Ultimately, the ‘outcome’ of the tests in those two worlds was mainly a plea for ‘a better analysis of private equity’, improving the test formats in other words, as antagonists agreed that arguments were relatively difficult to substantiate because of the problems associated with obtaining comparable data over time (Walker, 2007; Watt, 2008) and with the ‘aggregate evidence … mixed and ambiguous’ (Folkman et al., 2009: 518). Furthermore, several academic articles pointed to the ‘heterogeneity of the phenomenon’ (Wood and Wright, 2010: 1279) with both critics and supporters acknowledging that the effects of PE vary strongly depending on the sector they are in, the size of the deals, the stage of the business cycle (growth vs maturity) and the use of debt leverage (Folkman et al., 2009; Wright, 2013). Recent debates in finance journals add to the confused picture regarding the actual performance of PE with different authors claiming that the average buyout fund underperforms (Phalippou, 2014), roughly breaks even with (Franzoni et al., 2012; Sorensen et al., 2014) or significantly outperforms (Harris et al., 2014; Higson and Stucke, 2012) relevant stock market indices. 4

A third angle of critique grounded in the civic world seemed to get more traction. Evans and Habbard (2008: 68), for example, pointed out that PE funds were exempt from many of the regulations that apply to traditional collective investment schemes and therefore posed a clear transparency problem. They demanded that ‘these regulatory exemptions and gaps would need to be justified in the public debates’. Trade unions were also concerned with the increasing inequalities in society represented by the high earnings of PE partners and were vociferous in their campaign for reform of the taxation system (Morgan, 2009). This critique, quantified in a civic test, was succinctly summarized by Watt (2008): Much income of GPs is taxed as capital gains at much lower rates than earned income (typically 10–15% vs. 40%). Whatever the justification for the differentiation between rates of capital-gains and income tax, it is hard to see why it could be justified in this case. PE itself insists that carried interest is its reward for value creation. Why then should it be more favourably taxed than earned or dividend income? (p. 562, emphasis added)

It was a carefully lobbed verbal grenade from within the City elite by the chairman of SVG we already referred to in our introduction—‘highly paid private equity executives are paying less tax than a cleaning lady … I have not heard anyone give a clear explanation of why it is justified’ (FT 06/06/07)—that really gave impetus to this second line of critique. The quote was reported across UK broadsheets like the Guardian, the Times and the Financial Times, as well as the tabloid press like the Daily Mail and Express. The Times in particular highlighted that the inequity of a tax regime brought to light by Ferguson’s comments would enrage Middle England. And yet, as Montgomerie et al. (2008) noted with a certain degree of bemusement, ‘Despite losing the public argument, the Private Equity industry did not suffer any consequences’ (p. 2), and they sought the explanation for this in ‘… its successful mobilization of existing ideological and structural conditions, leaving to the government the task of justifying any regulatory or tax changes’. Perhaps this should not be too surprising an outcome as Boltanski and Thévenot (1999) already admitted that when people engage in a test of reality, they implicitly recognize what they call ‘the reality of reality’, that is to say the ‘network of pre-defined and more or less specialized entities, rules, test formats, conventions, and so on, that orient action by limiting the field of possible interpretations’ (Boltanski, 2014: 14).

While PE’s apparent shortcomings in the civic world, especially regarding its interpretation of corporate governance and tax rules as legitimate loopholes to be exploited, provoked a strong source of indignation, it still managed to weather the critique. On taxation, the government did scrap the taper relief system—which lowered tax on carried interest from 40% to 10% over 2 years—and introduced a flat rate of 18% in October 2007, while announcing it would make PE managers pay a fairer share of tax. On the issue of transparency, the Parliamentary Committee agreed to await the Walker Report recommendations to see whether the industry could sort itself out. The industry duly implemented recommendations that concentrated on the issue of transparency to the exclusion of almost everything else 5 (Morgan, 2009). One could argue that PE eventually managed to engage in the ‘civic’ test very much on its own terms, demonstrating it could put its house in order without any interference (e.g. in 2008 ‘voluntary disclosure’ reports were published by UK PE houses such as Permira and Terra Firma which caused them little or no difficulty). In the late summer of 2007, as the first signs of the Global Financial Crisis emerged, PE started its retreat into the shadows. As media attention shifted, the PE executives deliberately managed to cut their public exposure, while a much less beneficial financial climate meant that no longer could they be considered to be the ‘face of capitalism’. That mantle passed to investment bankers, but in a far less clear-cut way.

A critical deadlock?

Ultimately, our initial reading of the PE story leaves us with the rather uncomfortable ‘So what?’ question. We hope to have demonstrated that Boltanski and Thévenot’s model offers a useful structuring framework to describe the world as a site full of disputes and critiques and helps us see how actors select meaning among a large scale of possible interpretations. As such, the PE story echoes the findings of other engagements with Boltanski and Thévenot’s work in the field of organization and management studies where their model has been applied to bringing forward the underlying principles in determining a ‘fair’ price (Reinecke, 2010), mapping the logics of justification used in discourses of legitimacy in response to a nuclear accident (Patriotta et al., 2011) and justifying business responses to climate change (Nyberg and Wright, 2012). But ultimately, the notion of ‘test’ as originally developed by Boltanski and Thévenot leaves us in a critical and practical cul-de-sac. We find at best (from the critics’ perspective) inconclusive tests in the industrial and market worlds (focusing on employment effects and financial returns) and a displacement of the critique in the civic world. The tests proved inconclusive because arguments on employment effects tended to be based on incomparable data (Walker, 2007), with effects strongly depending on the sector, size of deals and the stage of the business cycle (Wright, 2013), and even in the field of finance, the performance of PE remains very much the subject of fierce debate as it appears that the type of dataset on which the analysis is performed leads to substantially different results (Phalippou, 2014). As we argued above, the displacement concerns the PE industry’s singular focus on the issue of transparency critics had put forward, making it easy for PE to address concerns in the civic world on its own terms. It is thus a moot point whether PE actually ‘lost’ any battles at all amid the media hyperbole in 2007.

Perhaps a hint of the limitations of the justification model was already provided by Boltanski and Chiapello’s (2005) introduction of a seventh, projective, world with its connexionist logic where the value system is articulated around the notions of project, network and permanent change. Huault and Rainelli-Weiss (2013) provide an up-to-date reading of this logic in the context of current financial markets where very mobile individuals have a disinclination for accountability, and it is ‘therefore tricky to identify references to justice specific to the connexionist logic’ (p. 196). This connexionist world ‘belongs to an ephemeral aggregate of experiences and interests, not to a charter of rights and obligations’ (p. 197). At the heart of this value system, they suggest, is a particular form of project, financial innovation, which aims to create pockets of profit and which organizes the relationship between people and objects. It is interesting to note in this context that Froud et al. (2012) in their interviews with senior PE executives found that those involved at the top levels of private equity (PE) must adhere to principles that depended heavily upon “absolute trust” between senior partners … Simultaneously, PE was represented as a brutal business that would not tolerate sub-standard performance: anyone falling short, either in personal integrity or in skills, was to be instantly discarded without exception and without any regard for notions of loyalty or friendship. (p. 2)

In a recent evaluation of the justification model, Boltanski (2013) furthermore suggested that it offers useful descriptive and analytical tools, but that is also limited in that it does not permit mounting a wider critique encompassing socio-economic reality regarded in its totality with different components systematically linked one to another. He also pointed to the fact that the situations associated with critique and justification refer to a fairly restrictive domain of the social. It presumes some outcome of consensus or settlement of the dispute where one party would withdraw the critique or the other party change its modus operandus in response to the critique. These situations assume a certain balance of power between the parties involved, which is becoming increasingly unrealistic as Boltanski (2011a: 372) conceded, especially in our era of a financialized capitalism. Wagner (1999), in a sympathetic review of De La Justification, already had pointed out that the sole focus on orders of justification overemphasizes the degree to which the social world is coherent and rational, the degree to which relations of equivalence between human beings prevail, and the degree to which human beings actually engage each other. (p. 349)

In order to address our critical and practical deadlock, we will turn to Boltanski’s most recent work in the final part of the article. In these writings, he attempts to reconnect the contributions of pragmatic sociology and its analyses of situated action to a Marxist view of history in which private and organizational lives are lived in confrontation with the deeper drama of what Marxism terms the ‘mode of production’, which refers to the manner and means of generating and distributing wealth on a social scale. The passions aroused by PE point to the underlying unease about this wealth generation and distribution under a financialized capitalism. One distinguishing feature of Boltanski’s late work is that in contrast to the argument developed in The New Spirit of Capitalism (Boltanski and Chiapello, 2005), he no longer necessarily sees critique as a motor for changes in capitalism itself. Indeed, he now emphasizes the ‘paradox of … a critique which is simultaneously very present, highly desirous of existing and making itself manifest, and yet very conscious of the difficulty of having the slightest purchase on reality’ (Boltanski, 2011b: 156). In the context of the financial world in particular, because of a hyper-instrumentalization through financial models and technology, critique becomes disoriented as it tries in vain to make sense of the permanent change and innovation in the sector. Huault and Rainelli-Weiss’ (2013) analysis of over-the-counter (OTC) financial markets, for example, emphasizes ‘the specific ability … to durably disarm the critique and escape, for the most part, the constraints of justification’ (pp. 202–203). Long before critique finally succeeds in making itself heard, it finds itself with little purchase on a financial world that has already moved on to ‘the next thing’. 6 So perhaps the deadlock we face in our analysis of PE may actually reveal something significant about the possibilities of critique under a financialized capitalism.

Existential critique, domination and the issue of class

Boltanski’s recent attempts at reconciliation between pragmatic and critical sociology suggest the ‘break’ was perhaps overemphasized in the first place. Indeed, the work of both Giddens and Bourdieu, with which scholars in organization studies are perhaps more familiar, already tried to overcome the dualism of invisible determining structures and its obverse, an individualist micro-sociology which relies on the vernacular of self-understanding of individual social actors. Structuration theory, for example, does not begin with either the individual or society, but its core concern is the mutually influencing processes between actions and structures (Giddens, 1991). Investigating structure meant for Giddens ‘delving into the subtle interplay between the intractability of social institutions and the options they offer for agents who have knowledge, but bounded discursive awareness of how those institutions work’ (Giddens, 1989: 298). Underpinning Bourdieu’s (2005) famous notion of habitus was a notion of action not simply as immediate reaction to a brute reality, ‘but an “intelligent” response to an actively selected aspect of the real’ (p. 212). Social actors set traces of past trajectories against the immediate forces that confront them which makes that their strategies cannot be deduced directly from either their immediate position or the immediate situation. Boltanski (2013, 2014) in his later work sets much store in this distinction between ‘the world’, conceived of as ‘everything that happens’, and ‘reality’, the construction of which makes it necessary to select, in the continuous flow of events, some elements that are treated as if they were the only relevant ones. Reality for Boltanski is always constructed, as in the commonplace ‘the social construction of reality’, and can be mapped in a quasi-cartographic way. ‘The world’ is what transcends this mapping, and which may produce events or phenomena that appear to contradict social reality, or at least cannot readily be integrated into the pictures generally used to give meaning to what is happening. Boltanski (2014), thus, summarized the distinction: Everything that happens emanates from the world, but in a sporadic and ontologically uncontrollable fashion, while reality, which is based on a selection and an organization of certain possibilities offered by the world at a given moment in time, can constitute an arrangement apt to be grasped synthetically by sociologists, historians and also local actors. (p. xvii)

Thus, reality is sustained by institutions that determine its shape through a framework of rules, procedures and test formats that purport to be generally applicable.

Boltanski (2011b, 2013, 2014) realized that the dynamic of critique, justification and the reality tests involved in establishing the validity of claims, as discussed in the earlier part of this article, actually reinforces the ‘reality of reality’, the forms of organization that are at once guaranteed and reproduced by the established test formats. He therefore introduced the notion of ‘existential test’ which links explicitly to what ‘affects’ people in their diverse everyday situation. Existential tests are based on experiences, like those of injustice or humiliation, and draw heterodox elements from these experiences that do not conform to existing formats. While tests of reality rest on a pre-defined format (e.g. codified in financial and accounting conventions or employment statistics), existential tests thus connect to the flux of ‘the world’ without them being easy to formulate or thematize. They involve the ‘search of explanations which lie outside the situation itself’ (Boltanski, 2011a: 366) and lean on ‘lived’ experiences rather than ‘instituted’ reality. Considered from the standpoint of the existing order, these existential tests have an aberrant character. They are often said to be ‘subjective’, and this allows those whom the tests aim to challenge to deny their reality (e.g. claiming that those who base their critique on them are paranoid or that they have misinterpreted the situation). It can be argued that the notion of ‘test’ loses much of its original potency and specificity in this development, but Boltanski (2014) believes it is a price worth paying in his recent quest to problematize ‘the question of where reality stands, what holds it together, what argumentative structures and what systems of proof are available to grant credibility to one particular picture of reality rather than some other’ (p. 36). 7 A critique based on existential tests sets itself as task somehow to reveal what is fundamentally at play. Inevitably, it will enter into controversies focused on the value—that is, the truth and social utility—of the world picture we are presented with. Drawing events from all that is happening in the world, existential critique contradicts or challenges the logic of the arrangements which constitute and organize our reality and aims at revealing its arbitrary character (Boltanski, 2008).

The PE ‘affair’ as it exploded in 2007 unexpectedly provided a focal point for people to express their concerns about the financialized economy they found themselves living in, with the involvement of PE funds in buying, restructuring and selling companies perhaps the most visible form of financialization in the first half of 2007 (Watt and Galgóczi, 2009). This was clearly perceived by the PE titans themselves, as is evidenced in the interview Stephen Schwarzman, co-founder and Chairman of Blackstone, gave to the Financial Times: ‘The recent unremittingly hostile treatment of buy-out firms is driven by myths and fears that have more to do with anxiety about changes in the global economy and in [people’s] own lives than with private equity itself’ (FT 27/11/2007). Yet, these existential concerns, namely, that the rise of PE was symptomatic of the new centrality of the financial sector within the structure of Western capitalism (Gowan, 2009), were always implicit but never clearly formulated in the campaign that challenged the legitimacy of PE. As such, a case could be made that at a surface level the singling out of PE was ‘unfair’ to some of the organizations and individuals involved as much of the resentment levelled at PE simply reflected a widespread feeling of injustice ‘that most of the fruits of economic growth are being swept up by a handful of rich folk, especially in finance, who enjoy huge fiscal advantages relative to the rest of the population’ (FT 23/1/2012). Under this increasingly financialized capitalism, certain contemporary financial intermediaries seem to function as a dominant group whose activities are aimed at capturing substantial shares of turnover and profits (Erturk et al., 2010). While there is some debate as to the historical novelty of the phenomenon, this delineation is seen to have some merit in that it ‘draws together a distinct group of actors who perform in a, for lack of a better term, behaviourally broadly similar fashion … and accumulate vast amounts of wealth for themselves’ (Beck, 2010: 1030). Boltanski (2008) explicitly reaches back to the Marxist vocabulary of ‘class’ when describing this group of actors: Recognising that they make up a class would mean to recognise that the worth accorded to each of the members of the elite, taken individually, is not related to their merits or capacities, but to a power they derive from their association with others of their kind. (p. 128)

These elites have of course no need or interest to define themselves as a class nor to proclaim the ties that unite them. They would stress, like, for example, Alan Greenspan (former chairman of the Fed), that ‘capitalism’s inequality of wealth, of course, reflects the variations of economic talent among our population’ (quoted in Holmes, 2014: 30). And yet, this is precisely the ‘hidden’ reality—the relations of force which make that ‘the relative weight of a small number can weigh more heavily than that of a big number’ (Boltanski, 2008: 40)—Boltanski believes existential tests and critique are aimed at revealing. He fully embraces the fact that these suspicions about the exercise of power (Where does it really lie? Who really holds it?) are the thematic of conspiracy theories and admits that the inclination to attribute intentionality and capacity to a dominant group of financial intermediaries indicates certain characteristics of the paranoiac 8 (Boltanski, 2014).

This reference to class and elites leads us to the concept of domination which is such a key feature of critical sociology. But the ‘domination’ that concerns Boltanski is more complex than traditional conceptualizations in critical sociology—one much more flighty and difficult to read and therefore more efficacious. He distinguishes between traditional or ‘simple’ modes of domination which are ‘obsessively orientated towards preserving a ready-made reality, which must be sheltered from disturbances that might be provoked by consideration of experiences in touch with the world’ (Boltanski, 2011b: 125), and complex modes of domination which he sees as typical of contemporary democratic–capitalist societies and their connexionist logic. These modes of domination avoid to resorting to repression if at all possible, at least when it comes to what is made visible to the public. Indeed, the latter explicitly allow for the incorporation of critique in the routines of socio-economic life, without that critique necessarily having any effect. Under such complex modes of domination, everything can be made discussable by any social actor deemed ‘legitimate’. For Boltanski, then, domination has to be thought of not as a factual condition that is imposed once and for all, but as a series of processes that have the effect of concealing key features of the world and thus restrict the field of critique. What distinguishes these complex processes of domination is that tests almost always seem to have prejudicial outcomes for certain groups of actors, and those whose expectations constantly meet with tests that discourage them end up endowing these processes with intentionality and considering it as a conspiracy (Boltanski, 2011b). Leaning on Bourdieu’s (1990) work on habitus, Boltanski (2014) does not see the dominant group of financial intermediaries as an objective totality but rather as a group of social actors who have internalized a set of generative schemes which makes that those who fill this class have in common certain behaviours, interpretations and even feelings. Of course, any mode of domination presupposes some coordination, but the spirit of ‘connivance’ the dominants express to one another when it is a matter of defending their privileges takes the fluid form of ‘an orchestration without conductor’ (orchestration sans chef d’orchestre in French), an intentionality without seeming intent and strategies devoid of clear strategic design. Consider Goldman Sachs’ Lloyd Blankfein’s recent comment on future market conditions, for example: ‘I would say with complete and utter confidence that nobody knows anything’ (FT 17/5/2014). It thus becomes virtually impossible to evaluate objectively the degree of solidarity that links the individual actors that make up this financial ‘class’ and to hold them to account as a class.

One of the characteristics of complex domination regimes is that they offer less purchase to critique than a simple regime of repression (Boltanski, 2008). They do not aim to maintain the status quo at any cost but rather fully embrace a change agenda. This allows for a continuous unmaking of the social reality in which critical collectives may have managed to inscribe themselves. It is precisely the injunction to obey ‘the rules’ (‘laws of the market’, economic conjunctures, globalization) that guarantees the perpetual change that keeps people in a state of fragmentation, thus making it difficult for them to find some salient points that allow them to have a real purchase on reality. These operations are not secretive. Yet, they are opaque precisely because of their fragmented and technical character which makes them very difficult to describe and hence to critique in a way that is precise and that will capture attention, especially when personal interests do not seem to be immediately affected by measures adopted. As both Langley (2008) and Huault and Rainelli-Weiss (2013) pointed out, when everything becomes discursively recast as uncertain and complex technical issues to be solved, this reduces the space of the political and limits the possibility for any disagreement and public debate. Beck (2010) in this context referred to the ‘decentralised and seemingly chaotic elements’ (p. 1035) within finance capital that ‘co-exist with intense concentrations of monetary wealth’.

If we briefly fast-forward the story of PE from 2007 onwards, we see how it bears out Boltanski’s (2011b: 156) fear that critique is ‘exhausting itself in a permanent race with reality … even before it has arrived at a clear understanding of where it is going’. The new conjuncture that started with the global financial crisis mid-2007 suddenly created ‘different dealing opportunities for the distributional coalition of financial intermediaries in and around private equity’ (Folkman et al., 2009: 519). For example, in 2008, PE houses seem to have engaged mainly in buying up cheap debt from investment banks, often debt of companies they themselves owned, in seeking out different sources of gain (FT 24/10/2008). Credit market turmoil also put a cap on the biggest buyouts which had captured the public imagination. In the United States, the initial public offerings (IPOs) by Fortress, Blackstone and eventually KKR also marked the point when the business models of US and European PE groups openly started to diverge, with the newly listed US groups branching out from their PE roots, becoming asset managers. 9 By 2014, they actually preferred to use the new label ‘alternative asset managers’ as they fully focused on financial arbitrage, with remuneration for bosses at the top companies reported to outstrip that at investment banks by a factor of five (FT 13/2/2014). In short, one could say that the PE of 2007 which was the target of critique simply did not exist any longer from 2008 onwards, and in that in constantly transforming itself, PE managed to disarm, be it intentionally or not, the critique aimed at it. It is interesting to note that while PE was reported to experience a new boom from 2013 onwards, returning an unprecedented US$471b to their investors that year and with unspent cash in PE funds at a record US$1.07t(FT 16/05/2014), we witnessed no critique of the kind we saw in 2007.

It is a moot point whether the picture of a monolithic industry which underpinned much of the critique in 2006–2007 was accurate in the first place, 10 although the term ‘private equity’ was used in a very broad and sweeping sense by both proponents of the industry and its critics (Bacon et al., 2013; Wood and Wright, 2010). It is also worth pointing out that ‘the people’ the unions and politicians claimed to speak for, and protect from the effects of a financialized economy, were far from homogeneous either. As Langley and Leyshon (2012) have pointed out, financial subjects are summoned up and assembled in the cultural and material production of contemporary financial markets in many complex and multiple ways. For example, through their pensions and needs to finance their housing, people have become increasingly integrated into a process of subjectification in our financialized economy. Thus, the claim from the BVCA that ownership benefits accrued to pensioners because pension funds were the main investors in PE does not seem as far-fetched as Erturk et al. (2010) seem to suggest. This is not to say of course that there do not exist profound asymmetries in the way fruits of financialization processes are distributed or that we should not pay attention to what might interrupt or disturb the smooth insertion into these financial subject positions.

Conclusion: Lessons from the PE case anno 2007 and a postscript

I can’t be the only person to have noticed that, quite simply, you never hear or see a banker anymore, on any broadcast medium. A TV bigshot told me that this is a known fact: ‘They won’t do accountability interviews’ … The banks will no longer defend or explain themselves in public, and a big part of that is their conviction that they can get what they want by lobbying for it in private. Their history and experience teaches them so. (Lanchester, 2013: 7)

The case of PE in the United Kingdom is interesting when considered in the light of Boltanski’s later theoretical work as it shows how significant changes in the UK economic landscape were carried out without major announcements, and it was assumed that the ‘managerial’ character of the interventions initially made unnecessary their scrutiny by the public at large. In obliging PE to justify itself, critics certainly compelled it to refer to certain kinds of common good in whose service it claimed to be placed. As Boltanski (2008) pointed out, insofar as collective entities claim legitimacy, it is not possible endlessly to ignore the observations made about them. If they are to remain legitimate, the spokespeople for these entities must respond in some way to the disquiet expressed about them (e.g. in pointing to ‘value creation’ which supports the wider economy). Indeed, we have seen in the furore surrounding the tax treatment of PE executives that a major source of the sentiment of injustice was caused by the existence of advantages that were wholly detached from tests that could justify them. Yet, such a claim that they serve some common good in a general way falls still short of submitting to a legitimacy test. For such tests of legitimacy to work ‘properly’, participants in the test must be able to remain within a single world and they must avoid any elements that might introduce distortions (Boltanski and Thévenot, 2006). This espouses perhaps too naïve a view of the social world, something Boltanski is all too aware of as he returns to concepts of a more traditional critical sociology. To follow an orthodox pragmatist sociology is to submit to rules and formats where the odds of successfully holding the financial elites to account are very low. That much the PE case has shown us. 11

It is undeniable that media hyperbole played a big part in the 2007 PE controversy. In anecdotal stories, the abstract collective entity of PE was represented by very concrete persons of flesh and blood according to storylines borrowed from the eternal register of fairy tales: bad guys, suspense, punishment, reward, vengeance and so on. Of course, this ‘trial by media’ was a poor substitute for critical inquiry in that the press stories elided measures that actually modified socio-economic reality in a significant way and focused instead on spectacular fairy-tale themes with pantomime villains. But what could such critical inquiry entail? Boltanski (2014: 234) suggests the simplest way to consider entities with a collective character is to borrow them from the stock of recognized entities that have achieved legal qualification or that are found in the media. The problem is, however, that this way of constructing collective entities ‘conceals reality while appearing to describe it’. Boltanski believes critical researchers ‘must thus forge their own entities and establish their validity with the means of inquiry at their disposal (interviews, statistical analysis). They must also give these entities specific names’ (Boltanski, 2014). Boltanski is well aware that such a construction of our objects of analysis will lead to the accusation of simply dealing with imaginary entities, or, when trying to put a human face to such entities, that one partakes in ‘the resentment of “losers,” the envious, and the insane’ (Boltanski, 2014). Such seem to be the risks of an existential critique. And yet, now that the question of knowing who the dominant are in our democratic–capitalist societies has become so problematic, there is something appealing in singling out individuals who stand for certain collective entities and their interests. The currently popular appreciation which sees ‘power’ as distributed among assemblages of human beings and machines which elude any actor taken separately empties the idea of domination of much of its substance (and thus severely undermines the possibilities of critique). Indeed, we learnt from Marx (1976) the importance of focusing our analysis on structures rather than on individuals, but he also reminded us it is still important to identify individuals as precisely personifications of certain interests and modes of domination. 12 The first step in solidarity between groups is the sense that, however different their subject positions under a financialized capitalism may be, they all face a common situation dictated by what used to be called ‘the ruling class’. As such, an important strategic move in any critique may be to give capitalism, that totality we cannot conceivably represent, an actual human face, thus exploiting the ‘breach’ that is presented by the faceless institutions of capitalism needing somehow to be represented by embodied actors (Boltanski, 2011b). The Lanchester quote at the start of this section indicates that perhaps even here critique may already be one step behind reality again. The point remains, though, that as critics we should be actively engaged in the construction of the collective objects of critique, even if this implies a homogeneity that is not there in reality (as we found in our case of PE), and that we should impute some will and intentionality to these collective entities without sinking into the temptation of conspiracy thinking. We believe that this is a key contribution of our article in terms of both diagnosis and a tentative practical suggestion.

Given that our case of PE mainly focuses on events taking place in 2007, we feel it is incumbent on us in concluding this article to make some connections to a more recent public controversy which pertains to critique under a financialized capitalism. As we were rewriting this article, a fierce debate arose around Piketty’s (2014a) Capital in the Twenty-First Century when the Financial Times dropped a front-page bombshell suggesting that key data Piketty had placed on-line appeared to be ‘constructed out of thin air’ (FT 23/05/2014). One of its journalists (Giles, 2014), when going through the numbers, found ‘no obvious upward trend’ in inequality and suggested that the conclusions of the book—that rising inequality is capitalism’s ‘guilty secret’—‘do not appear to be backed up by the book’s own resources’. In turn, Giles was then accused of making serious errors in his analysis (e.g. Elliott, 2014), and Piketty (2014b) also offered a robust defence. The interesting point from our perspective is not an evaluation of whose analysis was ‘right’ or ’wrong’, but the fact there was a real public controversy. The FT was reported, for example, to be ‘surprised by the furore caused by its attack on Piketty’ (Elliott, 2014). Piketty’s critique deserves the label ‘existential’ in that through the use of simple line charts, he tried to reveal a certain ‘hidden reality’—rising inequality—and thus bring to light some fundamental dynamics of capitalism. In doing so, he questioned the value (in terms of truth, social utility) of the world picture we are presented with and certainly found a receptive audience.

13

We find echoes of the PE debate in that ‘tests’ did not allow the parties to settle their claims in the public sphere. Both Giles and Piketty, for example, agreed that the US and UK data on which their interpretation rests become incoherent after 1970. This meant that Piketty had to combine disparate data sources and perform smoothing calculations. In a recent interview, Piketty (2014c: 115) bemoaned the absence of ‘the right tools’ which would enable the production of ‘commonly accepted facts’ and talked about ‘the willed blindness to the logic of contemporary dynamics’ (p. 111). The key point here is that the opaqueness about levels of wealth concentration undermines the possibility of having an informed and democratic debate, and one does need to stray too far into conspiracy theory territory to wonder why official data are so confusing. Is it perhaps an outcome of the ‘intentionality without seeming intent’ of a certain dominant class we referred to when discussing complex modes of domination? Mason (2014) pointed out in this respect that in the United Kingdom, the HMRC currently estimates that the top 10% of the population own 70% of the wealth, while the Office for National Statistics thinks they own just 44%. The discrepancy occurs because, of course, there is neither requirement nor desire to record actual market wealth at all. (Emphasis added)

Under conditions of complex domination, we therefore perhaps need a different mode of revelation than that of traditional critique—not so much an exposure of the secret but a revelation that does justice to it. The idea here is that the secret (in this particular case wealth inequality generated by capitalism) is not hidden as under a blanket; rather, the secret makes up the very lineaments our social reality (Taussig, 2000).

In conclusion, then, an existential critique should force us to reconsider relevant platforms and modes of expression that ensure that views that are critical of the logic and discourse of the prevailing system get a proper hearing and more importantly are able to make a difference in reality. In that sense, our identification of a critical deadlock is significant in itself. It suggests that critique under a financialized capitalism requires somehow configuring our present conditions into a constellation in which we are able to intervene—under complex regimes of domination we can no longer simply take straightforward intervention for granted. The extent to which Boltanski’s ‘tests’, as they featured in his work from the 1990s, are able to do this is perhaps questionable. Yet, they can serve at the very least as a reminder of the limits of traditional modes of critique: If we simply accept the ‘reality of reality’, then we have always-already lost Boltanski’s later work seems to suggest. Thus, for ‘late’ Boltanski critique is about finding new ways of problematizing our social reality: this involves the active construction of the objects of our critique and requires a certain aesthetic of revelation. Such a mode of revelation requires an ‘uncommon knowledge of the lineaments of reality’ and entails ‘creating a gap between apparent reality and real reality’ (Boltanski, 2014: 30, emphasis in original). Piketty’s simple but exhaustively researched line graphs are perhaps an example of this. The movement in the approach to critique between early and late Boltanski can be captured in a passage from his latest book where he compares the approach of the policeman and the detective. Becoming an effective critical scholar involves emulating the detective, Boltanski (2014) suggests, A policeman knows reality only in its officially determined form. He believes naively in its unity and sturdiness. The detective, in contrast, possessing the same type of intelligence and the same perversity as the great criminal, also knows how to dig into the crevasses and interstices of reality so as to exploit its inconsistencies, which perhaps means also unveiling its incoherence. (p. 31)