Abstract

The nature and extent of changes in management remain subject to debate, especially around the notion of post-bureaucracy. Most research concedes that there has been some change, but towards hybrid or neo-bureaucratic practices. However, the mechanisms through which these changes have occurred, and their precise forms and outcomes have received less attention. This article addresses these issues by focusing on an emerging group of managers that closely resembles images of new management (e.g. project-based, change focused, externally oriented and advisory in style). Drawing on interview-based research in the United Kingdom and Australia, it examines consulting practices and orientations adopted within management roles. It first constructs an ideal type of neo-bureaucracy and then explores different elements of management as consultancy empirically. It shows how they are inspired by anti-bureaucratic rationales but assume a hybrid neo-bureaucratic form. We also show that, far from resolving tensions between rational and post-bureaucratic forms, management as consultancy both reproduces and changes the tensions of management and organisation. Thus, rather than denying or heralding changes in management towards a ‘new spirit of capitalism’, we focus on a context in which such changes are occurring and demonstrate their wider implications for both management and consultancy.

Keywords

Introduction

Considerable attention has been given to the changing nature of managerial work and, in particular, the extent to which it has been transformed through post-bureaucratic ideas and practises of ‘change, flexibility, leadership and culture’ (Tengblad, 2006: 1438). Such a question is never likely to be resolved fully (e.g. Thomas and Linstead, 2002), but even sceptics acknowledge that some change in management has occurred (e.g. Hales, 2002; Harris et al., 2011). In particular, organisations and their management can take a hybrid, neo-bureaucratic form that combines elements of the old and the new. However, the precise nature of these changes—their mechanisms, forms and outcomes—have been neglected. Thus, rather than seek to establish the extent of change (O’Reilly and Reed, 2011; Poole et al., 2001), we pose the question of how neo-bureaucratic management has been achieved and with what effects? In particular, using an ‘extreme case’ (Blaikie, 2009), we explore the idea of management as consultancy through a study of managers taking on consulting roles and practices within organisations.

Others have explored emerging management practices in areas such as project and interim management and research and development (Hodgson, 2002; Inkson et al., 2001; Vie, 2010). However, the adoption and use of consultancy practices within organisations appear to be especially well suited to examine the changing nature of managerial work as both a medium and outcome of change. First, the traditional notion of a professional consultant using abstract expertise to advise on organisational change (e.g. David et al., 2013; Kitay and Wright, 2007; Kubr, 2002) has strong, although largely unacknowledged, parallels with images of the new manager. For example, while by no means synonymous, the post-bureaucratic manager is portrayed like a consultant, as a partner and catalyst of organisational change and/or an expert dispensing advice through project-based working—‘inspiration, expert advice … and proactive instigation of change’ (Hales, 2002: 55; also Tengblad, 2006). In some cases, the parallel is more explicit, with new managers seen as ‘adept with the language of MBA programmes and big league consultants, parachuting from one change assignment to the next’ (Grey, 1999: 574). In addition, consulting as a relatively mobile or insecure—‘up or out’—career resonates with the greater mobility and job insecurity of contemporary management under neo-bureaucratic regimes (Clegg, 2012; Farrell and Morris, 2013; Poole et al., 2003).

But consulting is also an appropriate context to explore contemporary management, as it is a key mechanism through which changes are introduced into management occupations. This is typically understood in terms of the traditional role of external management consulting in bringing management ideas into client organisations, including those associated with neo-bureaucracy (Clegg, 2012). We adopt a different focus—how consulting as a set of practices and orientations has been developed within organisations to help instil enterprise, manage change and reduce hierarchical boundaries. Clearly, changes in management have occurred through other mechanisms, not least through broader market and ideological changes, as well as the growth of management education and use of information technology (Poole et al., 2003; Thomas, 2003). Nevertheless, focussing on the practice of consultancy within organisations presents an opportunity to examine a specific context where core elements of neo-bureaucratic management are evident, one of the means through which it is introduced and, in particular, its perceived effects.

The article is organised as follows. First, we develop an ideal type of neo-bureaucratic organisation and management, introducing the importance of organisational tensions and dilemmas. We then outline our research study with its focus on management as consultancy. Based on our data, we explore four aspects of this phenomenon: (1) adopting an external focus by drawing on the pro-change orientations and knowledge of outsiders, (2) a strategic ‘value-added’ approach, (3) use of ‘non-hierarchical’ styles of interaction and (4) deploying formal methods of change management and cross-functional project work. We then discuss the implications of our study by engaging with debates in which traditional visions of management are reinterpreted within a ‘new spirit of capitalism’ (Boltanski and Chiapello, 2005). In particular, we argue that management as consultancy epitomises much of the popular image of the ‘new’ management, in part by co-opting criticism of bureaucracy. However, rather than fundamentally challenging traditional forms of organisation and management, or resolving tensions between these and recent post-bureaucratic ideals, neo-bureaucracy reproduces and reshapes many of the broader tensions of management and organisation. In short, our analysis sets out an ideal type of neo-bureaucratic management and illustrates how such practices can be achieved while also reinforcing the broader ‘causal powers’ of managerial control and its accompanying contradictions (Tsoukas, 1994).

Bureaucracy, post-bureaucracy and neo-bureaucracy

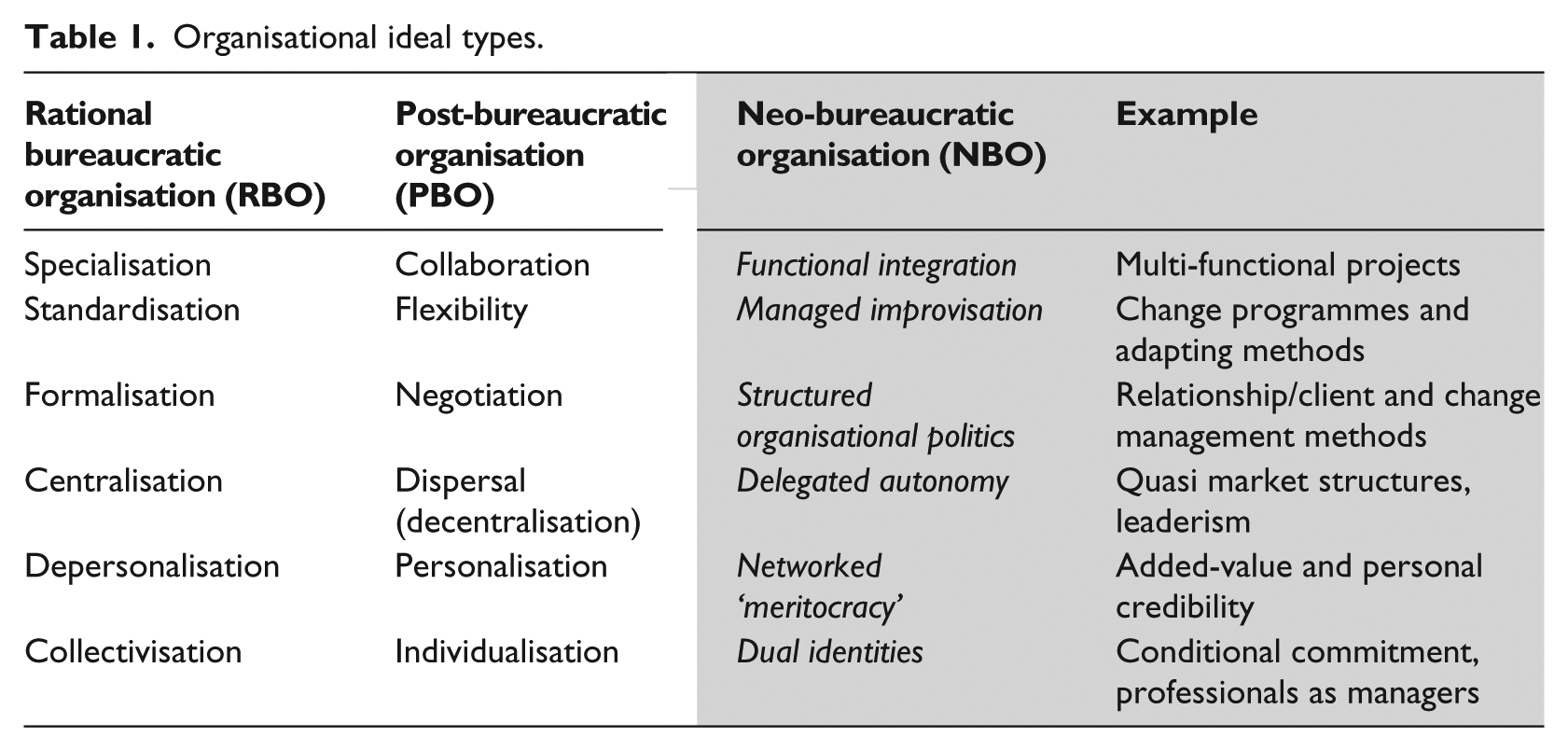

From the 1980s to date, much has been written about the move towards post-bureaucracy, where claimed organisational characteristics include ‘less rule-following, less hierarchical control, more flexibility, more coordination based on dialogue and trust, more self-organised units [e.g. projects], and more decentralised decision-making’ (Vie, 2010: 183). Reed (2011), for example, outlines an ideal type of the post-bureaucratic organisation (PBO) as comprising collaboration, flexibility, negotiation, dispersal (decentralisation), personalisation and individualisation. This is typical of other accounts of post-bureaucracy (e.g. Bolin and Härenstam, 2008), although the term ‘flexibility’ probably under-represents the importance of organisational change (Sturdy and Grey, 2003). Together, these dimensions are based upon an oppositional shift away from bureaucracy and the perceived rigidities of ‘organisation man’ (Whyte, 1956). Here, the familiar Weberian ideal type of the rational bureaucratic organisation (RBO) applies, made up of specialisation, standardisation, formalisation, centralisation, depersonalisation and collectivisation (Reed, 2011: 233).

However, how far rationalist and hierarchical traditions have been replaced by ‘support, consultation and inspiration’ (Vie, 2010: 183) has been hotly debated (Tengblad, 2012). There were those, especially advocates, who saw fundamental change in management and organisations towards post-bureaucracy (Kanter, 1989). But an even larger body of academic work has been devoted to challenging claims of bureaucracy’s demise (e.g. Clegg et al., 2011). This points to its persistence, dominance and even intensification in different forms. For example, Hales (2002) argues that organisations have long been subject to minor changes or ‘organic’ variations but still fundamentally retain ‘hierarchical forms of control, centrally-imposed rules and individual managerial responsibility and accountability’ (p. 52). Likewise, McSweeney (2006) and Harrison and Smith (2003), for example, identify an intensification of bureaucracy through the spread of measurement and regulation in the public sector.

Over time, a general recognition emerged in the literature, even among the most sceptical accounts, that while post-bureaucracy was barely evident beyond the hype, some change in organisations had indeed occurred (Harris et al., 2011), resulting in hybrid forms of bureaucracy (Tengblad, 2006). The labels attached to these vary hugely according to analytical focus such that bureaucracy became ‘soft’ (Courpasson, 2000), ‘lite’ (Hales, 2002), ‘selective’ (Alvesson and Thompson, 2005), ‘accessorized’ (Buchanan and Fitzgerald, 2011) and ‘customer-oriented’ (Korczynski, 2001). Following an emerging convention, and to avoid any implication that such changes necessarily reflect a reduction in bureaucracy, we use the term ‘neo-bureaucracy’. As Clegg (2012) observes, ‘whilst there can be little doubt that real and significant change is underway … what has emerged is not the “end” of bureaucracy, but a more complex and differentiated set of … neo-bureaucratic possibilities’ (p. 69). Likewise, Farrell and Morris (2013) identify neo-bureaucracy as a hybrid that combines market and bureaucracy, centralised and decentralised control or ‘new and more distributed modes of organisation juxtaposed with bureaucratic modes of co-ordination and control’ (p. 1389).

We, therefore, start from an assumption of the persistence of some features of bureaucracy, including various forms of rationality and hierarchical control, but also changes and differences resulting in hybrid organisational forms and practices, which could include some features of what has come under the label of ‘post-bureaucracy’ (Alvesson and Thompson, 2005). Of course, bureaucratic hybrids are not new (Adler and Borys, 1996; Ashcraft, 2001; Blau, 1955) and comprise different features. For example, Hales (2002) stresses networks and leadership alongside hierarchical control and accountability. Similarly, hybridity can be evident in the co-existence of bureaucratic and post-bureaucratic structures in different parts of the same organisation (Bolin and Härenstam, 2008; cf. Lawrence and Lorsch, 1967). Nevertheless, these studies can be drawn together by way of a summary of the key features of neo-bureaucratic organisations (NBOs):

Relatively few hierarchical levels (decentralisation) combined with centralisation of control (e.g. through information technology) (Reed, 2011); the traditional hierarchical career becomes more lateral and insecure (Morris et al., 2008).

Non-hierarchical styles of interaction (Diefenbach and Sillince, 2011) with control achieved through markets, self-discipline (e.g. enterprise culture) and/or peers as well as hierarchy (Reed, 2011; Styhre, 2008).

The use of project planning and cross-functional integrative teams which might result in parallel and temporary hierarchical structures (Clegg and Courpasson, 2004; Hodgson, 2002). Some fragmentation of organisations and relationships (e.g. through outsourcing, external networks and diffuse occupational boundaries), but not their dissolution (Alvesson and Thompson, 2005; Poole et al., 2003).

This list is useful, not least because detailed and comprehensive accounts of neo-bureaucracy are rare. Probably the most developed classification is by Reed (2011). However, his focus is different and quite specific—control logics, foci and modes. Thus, he points to employee participation through ‘delegated autonomy’ and how labour market competition disciplines workers as well as hierarchy. In other words, the core combinations of centralisation-decentralisation and hierarchy-market are evident but not the breadth of organisational characteristics such as those outlined above.

What then might an ideal type of the NBO look like as a hybrid of those of RBO and PBO (see Table 1)? First, both specialisation (RBO) and collaboration (PBO) can co-exist by not completely breaking down functional or occupational divisions but bringing specialisms together through multi-functional project teams for example—through ‘functional integration’ (Table 1, Row 1). Indeed, project management is a central theme of hybridised working more generally, with its focus on measurement, change and local accountability (Clegg and Courpasson, 2004). This is also reflected in the combination of standardisation and flexibility/change (Row 2) where change is managed in a structured way using, but also adapting, formal tools—what we have termed ‘managed improvisation’. Likewise, informal negotiation and political relations with others can be achieved through formal structures or practises, such as relationship and change management techniques and internal markets—a form of ‘structured organisational politics’ (Row 3). Market structures within organisations, where colleagues become clients or customers, for example, also form part of the discipline sought partly outside of traditional hierarchical control—‘delegated autonomy’. This is also evident in the emphasis placed on the leader or facilitator at the expense of the manager (O’Reilly and Reed, 2011) and, as noted already, can be partly achieved through distributed technologies (Reed, 2011) (Row 4). A hybrid form of depersonalisation and personalisation (Row 5) has not received the same attention in the literature as other aspects of the NBO. However, we will suggest that a form of this is evident in the practice of managers demonstrating how they objectively ‘add value’ to the organisation but in a way which is also based on personal relationship networks and credibility—what we have termed ‘networked meritocracy’. Finally, between the collective identification of ‘organisation man’ and the individualisation of PBO (Row 6) lies the prospect of conflicting or dual identities, such as that of the ‘professionals as managers’ (e.g. doctor managers) in many public-sector hybrids (Farrell and Morris, 2013), where organisational commitment may be partial or shifting.

Organisational ideal types.

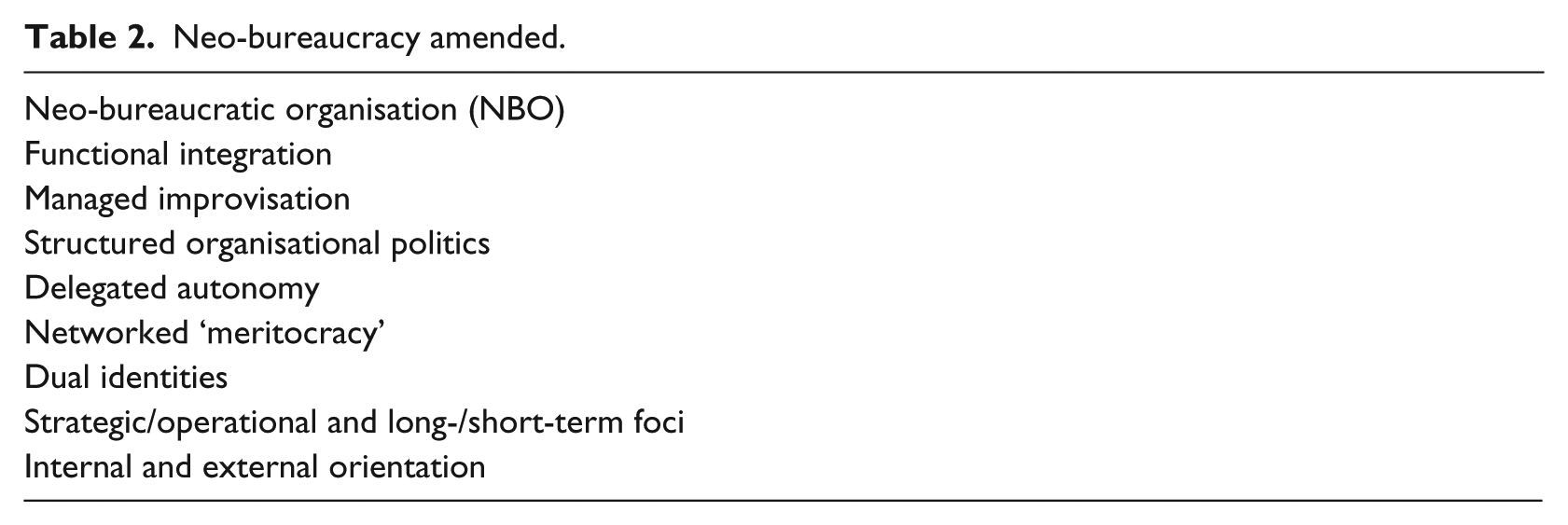

This ideal type of the NBO is clearly linked to the established models of the RBO and PBO, and this adds to its analytical value. However, its relative simplicity means that some issues are hidden from view. Indeed, the critiques of bureaucracy which helped inform changes in management practice extend into other areas. For example, Boltanski and Chiapello (2005) cited the following perceived problems of bureaucratic management as being static, hierarchical, internally focused, tactical, ‘excessively technical’, limiting of autonomy and authenticity, open-ended (ongoing) and lacking in commerciality or market discipline (p. 165; see also Du Gay, 2000). Most of these are covered in our ideal type, but we might add a greater external and strategic focus to PBO as well as the need to lose an ‘open-ended approach’ and introduce some form of periodic ‘closure’. This might translate into elements of a hybrid NBO form which combined internal and external orientations; short-term projects and long-term development and; attention to both the strategic and tactical or operational (see Table 2). Reed (2011), for example, also talks of ‘a deft combination of remote strategic leadership and detailed operational management’ (p. 243).

Neo-bureaucracy amended.

Ideal types are of course useful as analytical and comparative tools in that they simplify, synthesise and accentuate. However, they are not intended to reflect reality exactly (Hekman, 1983). For example, empirical research shows how new organisational forms are likely to vary significantly in practice, by sector or nation (Bolin and Härenstam, 2008; Johnson et al., 2009). Indeed, our concern is not with organisational forms per se but on what NBO means for management practices and outcomes. Before exploring this empirically, we briefly introduce the importance of tensions of management and organisation to the debate on bureaucracy and its hybrid forms.

Neo-bureaucracy as an organisational solution or problem?

We have seen how post-bureaucracy emerged in opposition to the bureaucratic organisation and as a potential solution to the various popular critiques of it (e.g. Heckscher and Donnellon, 1994; Kanter, 1989). The limitations of bureaucracy are, of course, very familiar within organisation theory but are typically presented not so much as problems but organisational design dilemmas or tensions. Thus, rather than prescribing a wholesale move away from one form to its opposite (e.g. post-bureaucracy), a seemingly more balanced (contingent) view can be taken where some value is recognised in each pole, such as that between specialist expertise and collaboration (Child, 1984). Likewise, others point to dilemmas within poles, such as between specialisation pursued through internal or external expertise (see Menon and Pfeffer, 2003) or change directed at short-term economic benefits (‘value add’) versus that focused on long-term development—‘Theory E Vs Theory O’ (Beer and Nohria, 2000).

So, where does neo-bureaucracy fit in? It has been suggested, tentatively at least, that the hybridity of neo-bureaucracy holds the potential to resolve classic organisation design dilemmas or, more specifically, the tensions between PBO and RBO. For example, Clegg (2012) observes that ‘neo-bureaucratic possibilities have had the effect of undermining some distinctions previously deemed incontestable (e.g. market vs. hierarchy; centralization vs. decentralization; public vs. private sectors) … domination and self-determination’ (pp. 69, 71). Similarly, Reed (2011) maintains that neo-bureaucratic regimes

attempt(s) to blend, even achieve a partial synthesis between, selected elements of ‘the cage’ (rational bureaucratic control) and ‘the gaze’ (post-bureaucratic control) in order to deliver a configuration of regulative mechanisms that can effectively facilitate the practice of contemporary governance. (p. 245; cf. Donnelly, 2009)

Of course, dialectical traditions of analysis, such as labour process theory (e.g. Marglin, 1979; Ramsay, 1977) as well as those which point to the hubris of modernity (Beck, 2009; Gabriel, 1999) would suggest that, far from solving problems, new structures and management practices are likely to generate new dilemmas. Indeed, dualities, contradictions and paradoxes are likely to be a ‘normal condition of organisational life, not an anomalous problem to be removed or resolved’ (Trethewey and Ashcraft, 2004: 81). These include both generic and particular tensions, notably various forms of resistance and other unintended consequences. Similarly, other types of opposition or adaptation can be expected, such as moulding new practices and ideas to improve or maintain one’s occupational or sectional status—conflict within capital (Armstrong, 1986).

Given the productive power of such tensions, it is not surprising that some theorists of neo-bureaucracy suggest that it does not simply bring the prospect of resolution but that also, ‘in such hybrid and often unclear situations, conflict and confrontation are inevitable’ (Clegg, 2012: 71). For example, tensions have been noted between empowerment and rationalisation or hierarchy (Watson, 1994; Webb, 2004), and leadership as both rational–legal (e.g. strategic) and charismatic (Grey, 1999). Likewise, Clegg and Courpasson (2004) note with regard to project management that

it neither abolishes control nor those tensions associated with it. Instead, it has distinct modalities of control, each of which generates quite specific tensions. These are not so much an innovation in organization form but a repositioning of some classic questions. (p. 545)

such as the design dilemmas outlined above. More generally, Bolin and Härenstam (2008) speculate that the combination of bureaucratic and post-bureaucratic structures puts a ‘particular strain and restrictions on … employees, who are controlled according to two principles’ (p. 559). Finally, Reed (2011) calls for the need to recognise that ‘the potential for resistance, incompetence, confusion and incoherence is very considerable and should never be underestimated in relation to any grounded assessment of how these hybridized control systems actually operate in practice’ (p. 243). It is to such an assessment that we now turn.

Research context and design

Mechanisms of change—towards management as consultancy?

Accounts of recent changes in management practices vary in the attention they give to the conditions and mechanisms of such change. For example, Alvesson and Thompson (2005) provide a list of ‘the usual suspects’ such as the rise of enterprise, leadership, knowledge work or shareholder/investor capitalism (p. 488; see also Morris et al., 2008). Our concern is at a lower level, with the specific mechanisms in which management might become more neo-bureaucratic. In many contexts, such ideas and practices have been shaped by agents such as external consultants, publishers, gurus and analysts (Madsen and Slåtten, 2013). Relatedly, managers have become increasingly ‘professionalised’, at least in the sense of being more formally educated and trained where change and service (customer/client) discourses are strong themes (Khurana, 2007). In the case of both change and project management, for example, relatively abstract management knowledge and mechanistic consulting tools have become commonplace (Caldwell, 2005). This process occurs through business schools, occupational/professional associations and in-house training (Mueller and Whittle, 2011). In addition, the parallel between new managers and management consultants is not entirely coincidental in that consulting firms themselves effectively act as training providers to those who subsequently leave consulting for management positions elsewhere either through choice—‘a work-life balance’—or as a result of consultancies’ ‘up or out’ policies (Meriläinen et al., 2004).

The adoption of consultancy practices in management has also been more explicit. In particular, management consultancy has been proactively colonised by particular external management occupations and professions, notably accountancy/audit and information technology (Galal et al., 2012; Greenwood et al., 2002). Our focus is slightly different—the more or less explicit move of management into the jurisdiction of consultancy within organisations. This development is evident in the transformation of management occupations such as human resource management (HRM) or internal auditing to include consultancy as an inherent part of their work activity (Selim et al., 2009; Wright, 2008). This relates both to a more general move into change management and the pursuit of a more ‘strategic’, less hierarchical, advisory role (Caldwell, 2001). Aside from such colonisation, consultancy is being brought into management, more generally, in the form of, what one practitioner-expert described as, individual ‘consultant managers’ (Czerniawska, 2011). These individuals are either former external consultants—a ‘consulting diaspora’ (Sturdy and Wright, 2008)—or are recruited from other specialisms and adopt management roles using consulting practices. For example, in a recent Harvard Business Review article on the consulting industry, it was claimed that ‘precise data are not publicly available, but we know that many companies have hired small armies of former consultants’ as managers (Christensen et al., 2013: 110).

At the same time, consulting groups or units have developed in large organisations to assist in the management of change projects and programmes. Internal consulting has, of course, existed for some time but was typically compared to its external counterpart and, as a result, seen as rather unfashionable (Armbrüster, 2006). Currently, therefore, combined with the fact that management consulting sometimes has a stigma associated with it, the title ‘consultant’ or ‘consulting’ may be absent from these units, even if many of the core characteristics are evident. Indeed, it has been argued that ‘internal consultancies have become major players; there are large numbers of managers who are, in fact, working as consultants … without even realizing it’ (Law, 2009: 63). As we shall argue, in its various forms, management as consultancy provides an illustration of the mechanism, forms and tensions of neo-bureaucratic management.

The research study

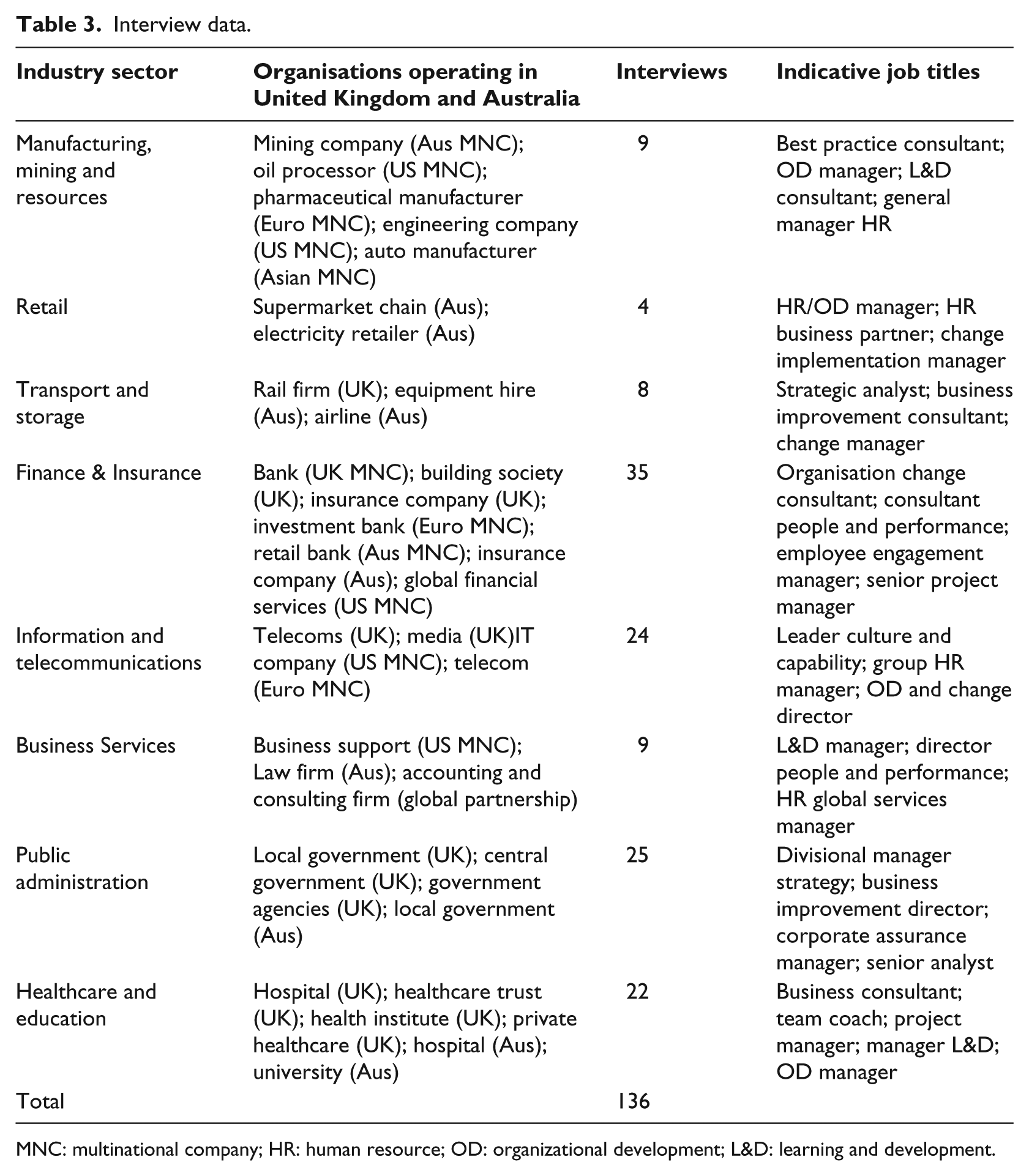

This article is based upon data from a research project looking into the role and impact of management as consulting within organisations. The research was conducted in the United Kingdom and Australia during 2007–2011 and involved an exploratory, qualitative approach investigating management groups and individuals operating in a ‘consulting role’ in large corporations and public-sector organisations. We undertook 136 semi-structured interviews of 45–120 minutes (91 in the United Kingdom and 45 in Australia) with consultant managers and others (e.g. clients, sponsors)—in over 50 organisations (24 in the United Kingdom and 30 in Australia). These included managers from a range of occupational and functional backgrounds, including operational efficiency, organisational development, strategy and HRM working in multinational corporations in financial services, telecommunications, manufacturing, government departments and healthcare organisations (see Table 3).

Interview data.

MNC: multinational company; HR: human resource; OD: organizational development; L&D: learning and development.

Given the ambiguous and dynamic nature of consulting in general, the absence of any formal occupational classification and the exploratory nature of our approach, we adopted a broad definition of ‘management as consultancy’. This included staff in management positions who provided advice, facilitation and expertise to operational managers, typically on a project basis, and who recognised their skills and activities as consulting-related (Scott, 2000). Following the tradition of organisational or ‘staff professionals’ more generally (Dalton, 1950; Daudigeos, 2013), they typically did not have a formal line responsibility for changes as some other managers in the organisations might have done. Of course, such a group could be classified as simply traditional internal consultants, but this would be misleading for various reasons. First, at a general level, the common distinction between (external) consultants and managers is problematic or at least blurred (Sturdy et al., 2009). Not only have process approaches to consulting long been equated with regular management practice (Schein, 1969), but even expert traditions can be seen as a form of management, especially with the recent emergence of consultant managers in HRM and elsewhere. Fincham (2012), for example, sees external consultants as a special, expert or ‘extruded’ form of management, while Ruef (2002) describes them as ‘externalized management’ (p. 81). Second, in our particular contexts, individuals or units would not have a consulting label nor define themselves primarily in such terms. For example, unit titles included ‘transformation delivery’, ‘corporate assurance’ and ‘performance improvement’ and individuals used labels such as ‘project manager’, ‘business analyst’, ‘leader’ or some other standard management title (see Table 3). Furthermore, individual respondents could be considered as conventional managers in terms of

Being continuing salaried employees who sometimes saw consultancy as part of their managerial role;

Being mostly based within operational divisions and cost centre structures, not working with a purely free-floating or market-based approach;

Sometimes acting in a quasi-policing (hierarchical) role, ensuring change objectives were met, including through involvement in implementation.

Although we focus mostly on common features, there was variation in the extent to which consulting was a central part of job/unit roles and identities and the assumption of hierarchical responsibility for organisational change. Likewise, there were differences in terms of whether units were set up explicitly in line with external consulting models, and whether individuals had previously worked as external consultants or simply saw consultancy as a convenient way to start, extend or end a managerial career.

In analysing the interview and documentary data, we began by coding transcripts and fieldwork notes, focusing particularly on the interviewees’ perceptions of their role. Later stages of coding involved a more iterative interrogation of the data (Crowley et al., 2002). Following an initial stage of open coding, where we identified a broad number of concepts, we then organised these into (1) drawing from and partnering external consultants, (2) a strategic and enterprise occupational focus, (3) adopting an advisory style and relationship management and (4) the use of structured change and project methods in an integrating role. These became organising themes within our analysis of the data. In seeking construct validity, we reviewed each other’s coding choices and our interpretation of organisational cases was fed back to key informants. Although there were some contextual differences in the data from the United Kingdom and Australia, no significant variation was evident in relation to our focus of analysis, perhaps because of our emphasis on large and, often, international organisations. In the sections that follow, given the wide scope of our empirical coverage, we use only illustrative quotes (preserving organisational and individual anonymity) to provide insight into some of the ways in which new forms and tensions of neo-bureaucratic management occur.

Management as consultancy

Drawing from and partnering external consultants

As noted earlier, one mechanism through which consultancy is diffused into management is the high staff turnover in consulting firms. This is partly the result of the proactive recruitment of external consultants into management positions. Many of our respondents (the majority in Australia and especially in private-sector contexts) were brought to their roles specifically on the basis of having worked as external management consultants, often in major global firms. The assumption was that they had a greater enthusiasm for, and skills in, change management and an anti-bureaucratic, pro-change and pro-market orientation:

I think there is a consulting mindset, a consulting skills set, that is somebody that can go in, can diagnose problems, can diagnose issues, work with solutions, and work with different people to drive an outcome … It [a consulting background] gives you a commercial edge because you definitely think in terms of, ‘is this adding value; they are paying for me; is this worth it?’ There is an element of service which is a really good thing to have.

However, the ability of these former consultants to embed their consulting skills and anti-bureaucratic ethos could be constrained. In part, this related to the potential dissonance of these characteristics in different organisational settings, as well as the perishability of their status as former external consultants. Indeed, paradoxically we found it was often through the loss or softening of their novel, enterprising appearance and the adaptation of formal methods associated with external consultancy that change was facilitated—by ‘going native’ or at least by diluting or adding to their outsider identity. As one senior manager explained,

One of my guys is an ex-external consultant and in the first few months we had to wean him off going in with a presentation pack and (saying) ‘these are the three different ways you could do it’.

Such enforced adjustment was experienced by some former external consultants as undermining their expertise and identity, making them more likely to be perceived in relation to traditional bureaucratic hierarchies than as ‘professional managers’. However, and in keeping with the hybridity of neo-bureaucracy, many sought to maintain a dual identity as an ‘outsider within’ (see also Meyerson and Scully, 1995: 589).

The influence of external consultants in changing management practice towards neo-bureaucracy extended beyond their direct recruitment into the management ranks of organisations. In particular, consultant managers were often a contact point for external consultants. Here, they would play a cosmopolitan, externally oriented role as knowledge intermediaries, looking outside the organisation as well as working with internal colleagues. Of course, such external relationships carried occupationally competitive risks, not least being associated with failed projects or being substituted by the external firms, leading to inequity in knowledge exchange—‘we are training them (the external consultancy)’. Overall, however, whether through recruitment and/or ongoing partnerships, external consultants had a direct influence bringing change to managers’ practices and orientations that extended beyond their conventional influence through client projects.

A focus on strategy and enterprise

It is important to highlight that many of the consultant managers in our study did not have any formal consulting experience, especially those in the public sector. They were appointed from within the organisation, based on their operational experience as traditional managers. This meant consulting roles could attract both those at the end of their managerial careers (‘old and bold’ individuals as one respondent referred to them), as well as those who were part of a ‘fast-track’ or graduate system. In some cases, adopting a more explicit consultancy role was considered to be an extension of existing managerial responsibilities towards more strategic concerns. For example, in one UK local authority, a performance review team was tasked with a new role of delivering an organisation-wide change programme, thus representing a hybrid of the operational and the strategic.

In such cases, the initiative was largely organisationally led, with consulting practices being used to build a change and project/programme management capacity. In other instances, however, management as consulting emerged from individuals or functional management groups where the high status and market success of external consultants, with their seemingly anti-bureaucratic ethos, was a reference point and aspiration. As noted earlier, this entry into the occupational jurisdiction of consulting has occurred in HRM in particular and was evident with HR managers in our study. Different parts of the consulting role were emphasised, such as challenging ‘clients’ and becoming project-based:

I’m not sitting behind a desk in an ivory tower, hidden … I’m very mobile, so if I need to be in another location, the car is under the building and I move, so I’m mobile and truly like a consultant.

A recurring theme in this occupational shift for the HR function was that, once again, consultancy represented a mechanism for moving from a transactional (operational) relationship to a more strategic and proactive or enterprising role. The hope was that traditional HR tasks would be decentralised to business divisions or outsourced, although this was not always the case, with hybrid roles being the result. In addition, and in keeping with wider processes of ‘corporate professionalization’ (Muzio et al., 2011), there was a concern to ‘add value’, to demonstrate a clear, ‘objective’ financial contribution to the organisation. This was pursued and demonstrated in various ways such as seeking external fee-paying clients, diversification away from operational activities and through social networking internally (see also below). As one change unit manager said,

It’s very, very important that the business perceives us as value adding, and that’s something we work really, really hard at, to make sure that the business constantly thinks ‘yeah, these are good guys to have around’.

Again, such developments came with risks. In the case of HRM, for example, these included consultant managers often having to overcome pre-existing negative perceptions of both HRM and consulting. As we noted before, many units did not use the term ‘consulting’ or ‘consultant’ for precisely these reasons. It was as if they wanted the strategic orientation (and integrative function) of the role without the consulting label. As a senior ‘client’ manager in a global company commented of one consulting unit:

Let’s not call them ‘internal consulting’ anymore … call them that loose layer of people that bring together different people from all parts of the organisation as and when we want to solve something … the word ‘consultancy’ also becomes synonymous with estate agency or double-glazing sales person!

Similarly, the fact that using consulting services was often discretionary (subject to an internal market discipline and/or informal senior management patronage) meant aspirations to secure individual or unit credibility through strategic and financial contributions were by no means guaranteed. For example, one unit in a government department was prevented from becoming more strategic. As their manager complained,

[I argued] that I should be used to help deliver the board’s management plan … And they debated this for twenty minutes came back with the answer, ‘no, you please crack on and do what you keep doing’.

This unit was subsequently disbanded for being too tactical. At the other extreme, a bank’s consulting group was closed for being ‘too entrepreneurial’ in seeking external clients at the expense of internal needs. Whether led by individuals or units pursuing careers and credibility, or as part of wider organisational initiatives, the consulting label and its organisation as a discretionary service in an internal market, therefore, presented vulnerabilities as well as opportunities.

‘Non-hierarchical’ interaction and ‘relationship management’

We saw earlier how, in keeping with neo-bureaucracy, consultant managers placed emphasis on external relationships and knowledge (as well as internal ones), partly through partnerships with external consultants. Similarly, both consultancy and neo-bureaucracy are consistent with a playing down (not a removal) of hierarchy and an emphasis on advice-based interaction, persuasion or facilitation. This is partly because engagement with change is often seen as impeded by top–down approaches (Hartley et al., 1997), but also, once again, fits with a client-based (market) relationship. For example, in a large transport company in our sample, it was claimed that policing by the HR function had given way to an explicit ‘consulting’ approach—‘the way that you approach your everyday job is (by) influence first, power second … it’s a fundamental shift’. Even the crudest forms of rationalisation can be re-packaged as a ‘partnership’, as one consultant manager in a multinational financial services organisation outlined:

[We used to be] seen as the auditors coming … we were like the ‘head choppers’ and people thought we had a little bit of an agenda from senior management, looking for a percentage (of cuts) which really wasn’t the case … What we (have) tried to do is build up—make it like a partnership approach with the business area and also involve them in the decision making around the recommendations … Now we make that a joint approach.

In addition to advice or partnership-based interactions, consulting practice within management was reflected in the emphasis placed upon relationship management, especially laterally across the organisation. Here, again, it is the market-based discourse of both neo-bureaucracy and the ‘internal client’ which is important, even though, as noted earlier, almost all the units we saw actually operated as cost, not profit, centres in conventional hierarchies. Consultant managers adopted similar practices to those of external consultants (Karantinou and Hogg, 2001) in seeking to understand, anticipate and actively shape the current and future needs of client managers and departments. This meant formalising relationships such as aligning individual consultants to different business areas. For example, in one business services organisation, a consultant manager explained how they had

… looked at working in a consultancy cycle … things like negotiation, influencing as a really key part of the role. Relationship-building as well—they (consultant managers) need to be able to do that.

These formal practices had variable outcomes, but even when partially successful, they could raise client expectations without the prospect of meeting them, or fail to guarantee a flow of work of sufficient quality and/or quantity from the consultant managers’ perspective. Indeed, the market-based discourse often rendered consultant managers and units insecure in their roles, resulting in a greater emphasis on the need to establish credibility with client colleagues and sustain senior sponsorship through both formal and informal means.

Such political practices are not, however, peculiar to neo-bureaucracy (see also Pettigrew, 1975). What was more significant in our context was the contestation of hierarchical relations. We found significant variability, fluidity, ambiguity and contestation over managerial responsibility for change, even within a single organisation. For instance, consultant managers sometimes acted as regulators—akin to traditional line managers—in large change programmes, for example. In one communications organisation, an example was given where this approach remained necessary even though it had more negative long-term implications:

We took the decision that we were going to use a compliance-based approach around the first phase (of change). And we basically forced people to do it, because if I’d have given them the choice it would never have happened … So that has create(ed) a degree of alienation, and as a team we did … lose quite a lot of trust with those people.

In the same firm, a client was quite sure that it was she who took the lead or management role and responsibility, not the consultant managers, who she saw largely as a management ‘body shop’:

So we’re short of the analysts, the programme managers, the programme directors, the project managers. So ‘you give me the people’. I know I applaud the people, but don’t tell me [the consulting unit] is delivering my transformation, it isn’t, we are.

Such issues highlight how tensions and ambiguity can arise in neo-bureaucracy and not simply from a weak masking of hierarchy behind a facade of advisory, consultative and participative intra-organisational relations. Rather, hierarchical tensions can also be substituted by those of client and service provider and roles within this relationship can themselves be contested and variable.

An integrating role and project/change tools

The focus on external and lateral relationships combined with strategic aspirations ran in parallel with a wider integrative and neo-bureaucratic role performed, to varying degrees by all our interviewees. Indeed, consultant managers often had a unique position in their organisations in operating across traditional functional divisions to work on discrete projects using formal project management methods. Programme management could also be part of this, but even where integration was not formalised, it was widely recognised by clients. This was the case in a financial services organisation where a client commented that the consulting group:

… played a hugely instrumental role in co-ordinating the technology, the operations, the countries (offices), the underlying project streams falling through and all the rest of it and it has become a reality and is phenomenal, it’s so powerful, it’s absolutely unbelievable.

At the same time, consultant managers brought specific tools and models into the management of change across their organisations. In general, the approach to change that was most evident was highly structured and standardised (bureaucratic), such as the use of Six Sigma, process reengineering or continuous improvement. Thus, change and standardisation were combined. For example, one respondent reflected on his role in educating other managers:

[In] the final phase, which I call the ‘teach to fish phase’, we’ll have created a new set of processes, so we’ll have process consistency across our organisation. We will have put in place a set of tools which will allow us to measure that process consistency and we’ll have … trained and empowered people to continuously improve.

Whether or not the aim was to transfer expertise in methods, their use could enhance the status of the consultant manager or unit, although this was sometimes short-lived. For example, through the use of a methodology aimed at enhancing inter-team communication (i.e. functional integration), a change unit within a healthcare organisation had developed a positive reputation. However, there was also the feeling that the methodology had become overly familiar to client managers, resulting in a gradual loss of status for the unit overall. Similar issues occurred elsewhere such that consultants sought to conceal the particular label of their change tools, in case it was seen as overly standardised or no longer fashionable. One team jokingly called itself the ‘secret Six Sigma society’. In other words, the use of such approaches, along with integrative project management tools, was sometimes contested and often adapted or improvised.

Discussion

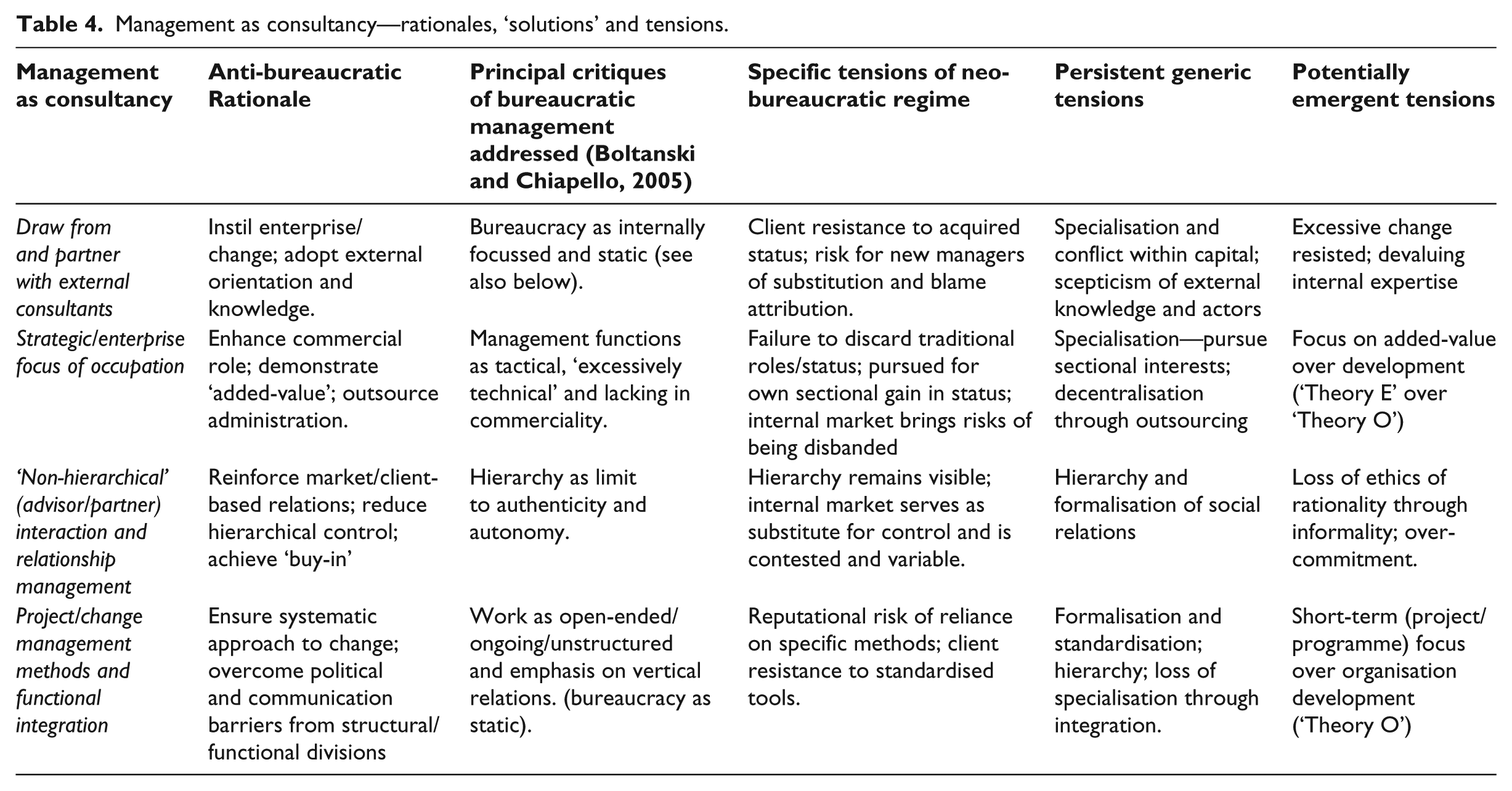

In this article, we have explored an emergent form of management—management as consultancy—which closely matches images of a new role claimed for managers more widely. Furthermore, the managerial rationales for the four interrelated elements of management as consulting we identified can be closely linked to some of the key critiques of bureaucratic management made by those pursuing a ‘new spirit of capitalism’ (Boltanski and Chiapello, 2005) (see Table 4, Columns 1–3).

Management as consultancy—rationales, ‘solutions’ and tensions.

The first element involved drawing from and partnering external consultants as a way to instil enterprise and adopt external ‘best practices’. Here, the new manager as consultant would adopt a more flexible and dynamic approach, less focused on internal systems and processes and more open to external knowledge to lead change. The second element was a more commercial and strategic focus to counter the tactical and ‘excessively technical’ approach associated with bureaucratic management. This was reflected in management occupations, such as HRM, and individuals or units embracing consulting models in order to legitimate their strategic role and ‘add value’, while other activities are downgraded or outsourced. The third element, we focused on was the adoption by managers of advisory or partnership styles of interaction and relationship management. This approach de-emphasised vertical, hierarchical control and mimicked market-based (customer/client) relations, thereby absorbing the critique of hierarchy as a limit to autonomy and change within organisations. Finally, the fourth feature involved the promotion of cross-functional project- and methods-based working. This aimed to unsettle or fragment traditional boundaries and stressed the importance of change and horizontal integration, as opposed to an emphasis on routinised or ongoing work practices based on vertical lines of authority, communication and interests.

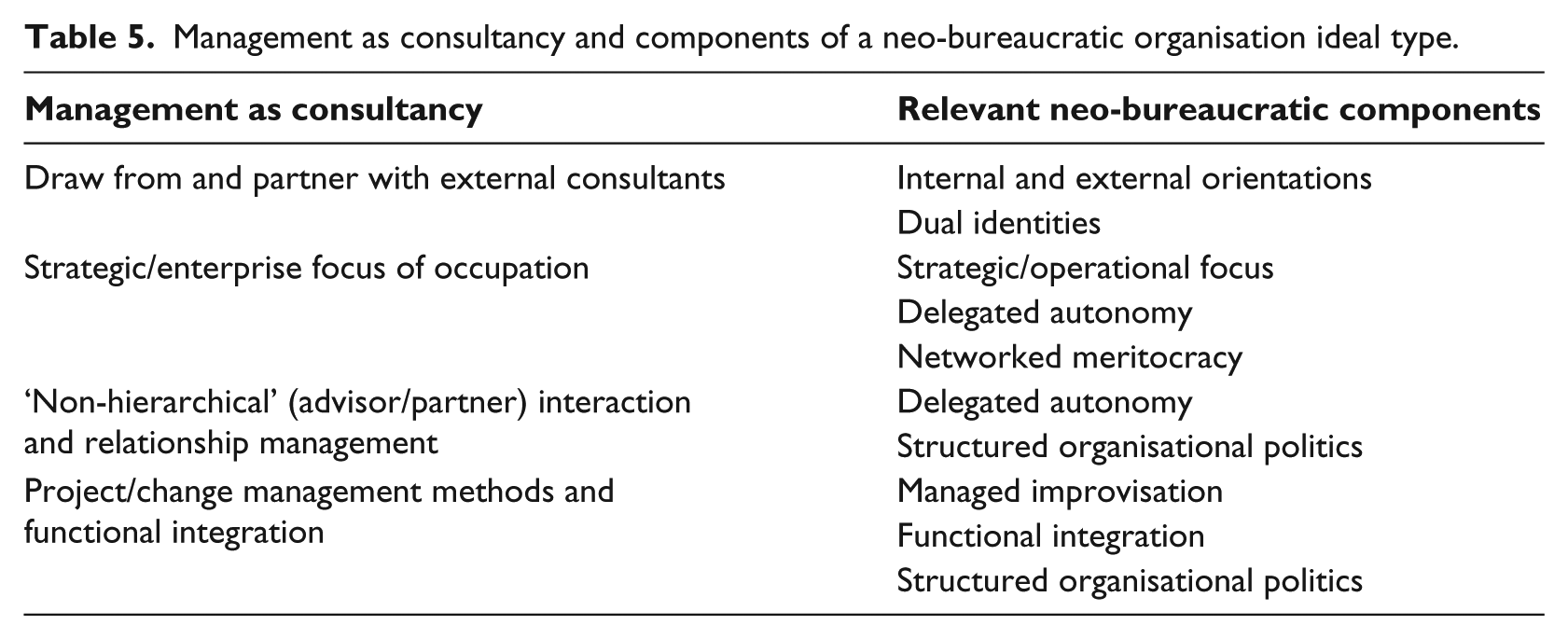

However, despite being informed by such anti-bureaucratic rationales, management as consultancy is by no means post-bureaucratic. Rather, it reflects a neo-bureaucratic hybrid. Indeed, if we return to the ideal type of NBOs outlined earlier (see Table 5), we can see many of the components reflected in the four sets of practices we have discussed, although, as with all ideal types, there will not be an precise match. First, drawing from and partnering with external consultants as well as colleagues illustrates the combination of internal and external orientations and can also be associated with the idea of dual identities—the ‘outsider within’. Second, the strategic/enterprise focus of consultant managers addresses only one side of the strategic/operational component. However, we saw how strategic work not only emerged from operational activities but was sometimes more of an aspiration than a core practise. An enterprise focus can also be linked to delegated autonomy in terms of the discipline of market and quasi-market structures that ran alongside sometimes opaque organisation hierarchies. And there is a connection with networked meritocracy as well, in the practice of seeking to demonstrate added-value in a formal but unreliable way, although this was less evident from our data. Third and more clearly, ‘non-hierarchical’ (advisor/partner) interaction and relationship management methods resonated strongly with delegated autonomy and the structured organisational politics components respectively. The latter is also reflected in the fourth practise—the use and adaptation of project and change management methods. But this most directly matches the idea of managed improvisation and directly duplicates the functional integration component of our neo-bureaucratic ideal type.

Management as consultancy and components of a neo-bureaucratic organisation ideal type.

Indeed, while attention is invariably given to what appears new or unconventional, there is much about management as consultancy that reinforces and extends traditional managerial and bureaucratic concerns. So for instance, the focus upon demonstrating the contribution of management to ‘value creation’ or efficiency resonates with what Tsoukas (1994) refers to as its ‘causal powers’. Similarly, the focus upon ‘influencing’ and ‘relationship management’ reflect the perennial need to secure the cooperation of employees in pursuing managerial goals (Willmott, 1996). Indeed, through the reframing of ‘change’ as a universal, participative and manageable phenomenon, the potential to question broader organisational logics can be obscured—control as ‘consultancy’ not ‘management’. Some would even argue that, as part of a broader recalibration of the ‘new spirit of capitalism’ (Boltanski and Chiapello, 2005), it serves not only to absorb resistance and criticism but also to encourage employee or ‘client’ commitment to various forms of rationalisation. As we have seen, however, while potentially effective as an abstract ideology, in daily practice it was problematic.

This is in keeping with the views of those who identified, but also questioned, the potential of neo-bureaucratic hybrids to resolve organisational governance problems (e.g. Reed, 2011). Indeed, we have seen how various tensions emerged. These can be identified as both specific to the new regime of management as consultancy, but also as echoing classic organisational dilemmas. Furthermore, we can speculate on the potential for other tensions to emerge which might also form the basis for further research (see Table 2, Columns 4–6). First, in terms of drawing on, and working with, external consultants and knowledge, consultant managers risked client resistance on the basis of the stigma attached to externals as well as direct competition with them. Managers could also become a target for blame when their own or external partners’ projects failed to satisfy ‘client’ expectations. This also replays traditional conflicts between specialist management groups and concerns over outsiders and externally sourced knowledge. Furthermore, in terms of potential tensions, it is likely that the persistent emphasis on innovation might result in ‘change fatigue’ among staff, much as the external focus could lead to a devaluing of local or internal knowledge.

The second element—the adoption of a strategic, enterprise orientation with a particular focus on ‘added-value’—runs the risk of neglecting the qualitative development of the organisation (‘Theory O’). When pursued as part of individual, unit or occupational advancement (combined with outsourcing of administrative activities), it also reinforces traditional concerns with both specialisation and decentralisation. More specifically, we saw how former roles and statuses could not always be easily discarded (e.g. HRM). Even when they were, we saw how the internal market structures brought new insecurities from being ‘too’ entrepreneurial or ‘insufficiently’ so.

Tensions were perhaps most evident with regard to the third element of management as consultancy. Here, hierarchy was superficially downplayed but remained visible and/or competed with control through market relations. Similarly, informal partnership or ‘non-hierarchical’ advisory styles of interaction with clients ran alongside formalised relationship management. One can also imagine that difficulties might arise through the sanctioning of informal relations, in that the ethical protection provided by rational rules (e.g. against patronage) would be lost, bringing an additional risk of over-commitment, to change for example. However, it is precisely through such informal relations that external consultancy mostly operates, with considerable economic success (O’Mahoney, 2011).

At the same time, management as consultancy also matches its external counterpart’s focus on change and project management methods—our fourth element. Here, we saw some specific tensions around managers being associated with practices whose status was perishable, combined with familiar concerns with standardisation and formalisation. Also, the role of consultant managers as integrating different functions or ‘silos’ through project and programme-based working, can undermine organisational strengths derived from specialisation and potentially impede a longer term or ongoing developmental orientation (‘Theory O’).

How then might we summarise these observed and potential tensions and point to lessons concerning a wider dysfunctionality of neo-bureaucracy? Put simply, neo-bureaucracy moves management away from a situation in which its accountability and value to the organisation was relatively visible and bounded to specific contexts and senior managers (i.e. by hierarchy). In this ‘new spirit of capitalism’, the value of management shifts from project to project, and its ability to impact upon other parts of the organisation becomes more discretionary and client-based. Whereas previous measures of managerial contribution might have been be more easily quantified or, at least, were implied in the production process (e.g. cost-minimisation), neo-bureaucratic management relies upon perceptions of ‘added-value’ and market-based mechanisms. Hence, while the contradictory nature of management has been a recurring theme in critical studies, the application of neo-bureaucracy through practises, such as management as consultancy, suggests that it may serve to further de-value management in the long-term, as managers’ work becomes more ambiguous and less tied to the relative certainties of traditional patterns of control, much like external consultancy.

Conclusion

Our concern has not been to establish the extent of change in management, but rather to explore a particular case of neo-bureaucratic management and thereby also add to empirically based work on the ‘new spirit of capitalism’ at local levels. In doing so, we have sought to maintain a conception of management that acknowledges its day-to-day activities and its wider control function within capitalism, including how those activities themselves legitimate control. Such a position has helped in drawing attention to both continuity and change in the tensions and contradictions of organising more generally. Thus, our focus has been less on whether the hybridity of neo-bureaucracy can reconcile bureaucratic and post-bureaucratic models and rather to confirm that it is more problematic, outlining how this occurs in practice and with what effects. Of course, various questions remain over the mechanisms and directions of change, such as whether neo-bureaucracy is best seen as the result of purposive action or as ‘epiphenomenal’? Similarly, by using a subgroup of managers within organisations as an extreme case, it remains unclear as to whether neo-bureaucratic management can assume a more general, less specialist role.

Nevertheless, our findings have wider implications for the management of change and management occupations. For example, until recently, consultancy has largely been appropriated by a limited range of occupational groups and those who typically act as organisational outsiders with relatively high status (e.g. accounting, information technology). This has preserved a distinctive role and cosmopolitan identity for the consulting occupation, a mystique even (see also Kitay and Wright, 2007), which is typically reproduced in much of the academic literature. However, the changes we have pointed to suggest that consultancy is becoming internalised and, perhaps, further commodified (Armbrüster, 2006). If management consultancy is simply a form of ‘externalized management’ (Ruef, 2002: 81), then its substitution by consultant managers becomes a distinct possibility. This has significant implications for external management consultants who may experience the need to rely even more on their outsider and/or legitimation roles and on esoteric or novel expertise. As change management and explicit methodologies become more commonplace among management ranks, external consultants are unlikely to constitute a sufficiently attractive/distinctive service for clients. Furthermore, we have highlighted how it is mostly a particular, somewhat mechanistic, bureaucratic approach to change, which has been adopted within organisations. This, combined with similar forms of project management methodologies, may marginalise or silence possibilities for alternative, less hierarchical, masculine and planned, forms of organising change, consultancy or advice more generally (Buchanan et al., 2007; Marsh, 2009). This echoes a broader argument about the spread of management which ‘closes off alternative conceptions of coordination, most notably those of community’ (Grey, 1999: 579). Such alternatives would not be free from the dilemmas and tensions of organising but highlight how management, by contrast, remains firmly tied to capitalism and its own tensions, even if a new spirit is evident.

Footnotes

Funding

The research reported here was partly funded by the UK Economic and Social Research Council (ESRC—RES 000 22 1980A).