Abstract

Drawing on a decade of investment data (2015–2025), this article offers a meso-level analysis of funding for Australian videogame companies by corporate and financial sector stakeholders. Findings reveal geographically concentrated investment in east coast urban centres, primarily driven by North American and Asian venture capital firms. In contrast to public funding from federal and state screen and arts agencies – which at least, nominally, emphasise cultural value – corporate and financial sector investment targets high-growth, high-risk ventures, particularly those aligned with emerging technologies. Situating these findings within recent debates on media financialisation, the article shows how investment flows and financial actors in the Australian videogame industry materially shape its industrial composition.

Introduction

Accounts of project financing in the Australian videogame industry are typically framed through two dominant narratives: public sector support via screen and arts funding agencies at both federal and state levels (e.g. Darbas, 2024; Keogh, 2021), and partnerships between local development studios and larger international publishers (e.g. Apperley, 2008; Banks and Cunningham, 2016). While these accounts highlight important financial dynamics that have shaped the industry, they provide only a partial picture. Less attention has been paid to what Science and Technology Studies scholar Kean Birch (2023) describes as ‘innovation financing’ – a form of investment activity driven by corporate investors or firms within the financial sector. This type of financing typically targets early-stage or privately held companies and often involves equity-linked investments.

To be clear, the relationship between finance capital and videogames is not new. Commercial videogames have always been underpinned by forms of financial investment, from early venture capital (VC) financing of Atari in the 1970s (by the American VC giant Sequoia Capital, see Sequoia Capital, n.d.) to the role of Silicon Valley VCs in shaping smaller firms (including in Australia) throughout the 1990s ICT boom (Stuckey and Harkin, 2025). What has changed in the past decade, however, is the extent and character of financial sector involvement. Rather than episodic injections of venture funding into individual studios, we now see sustained participation by VC, private equity (PE) and large technology firms treating games as an investable asset class. This shift reflects what deWaard (2024) sees as a wider financialised logic of contemporary media industries, where the vast surplus capital generated elsewhere in the economy seeks outlets for reinvestment – even in sectors historically regarded as volatile or hit-driven. In this context, the influx of financial capital into games is less an anomaly than a symptom of broader structural pressures in the global economy: as the rate of profit declines in other sectors, investors seek returns wherever they can be found, including cultural industries once considered too uncertain. At the same time, the industry's rapid growth has made games appear increasingly stable and lucrative to investors (Ball, 2025).

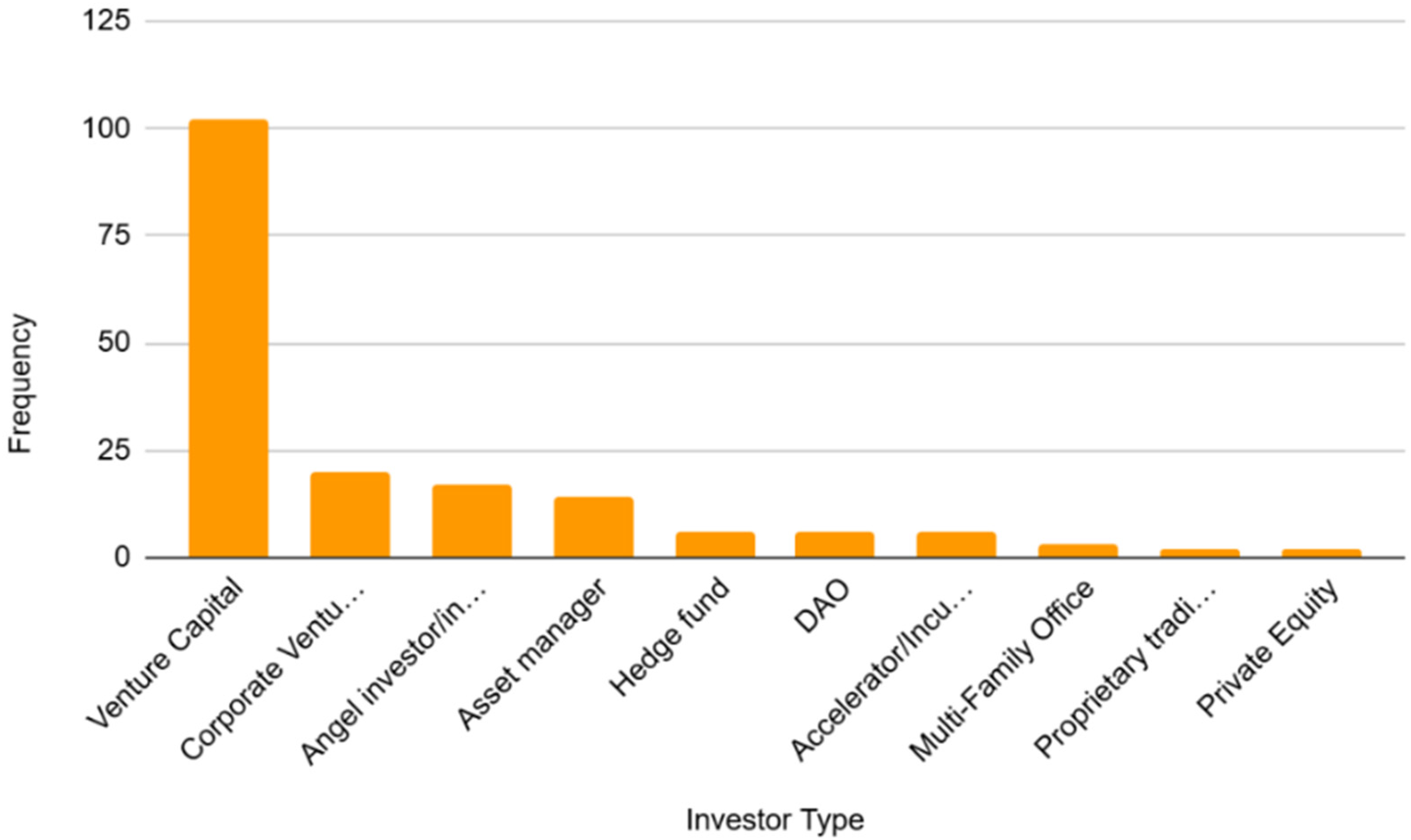

Frequency of investor types in Australian game development financing from corporate and financial sector stakeholders.

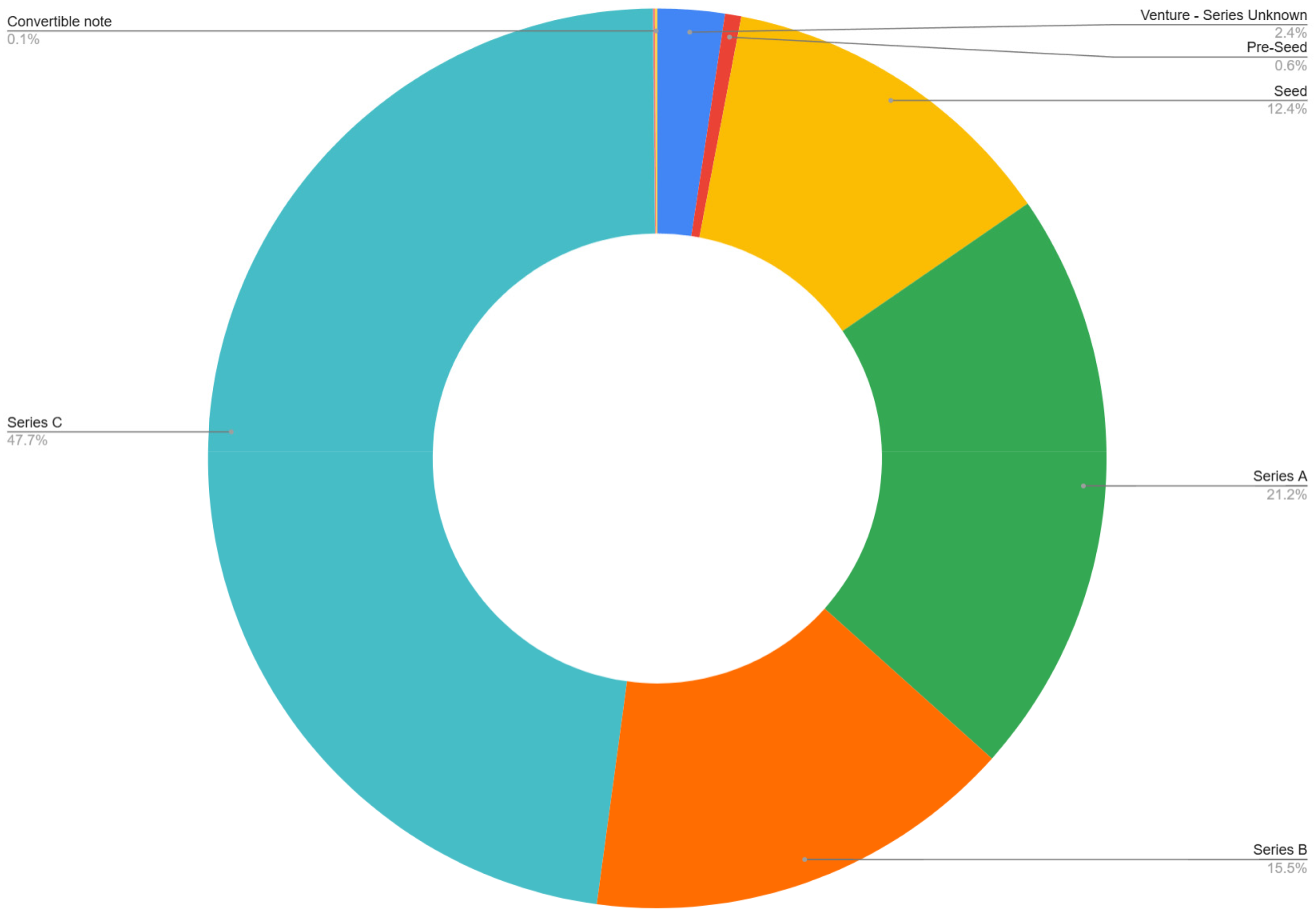

Industry investment by funding stage/type.

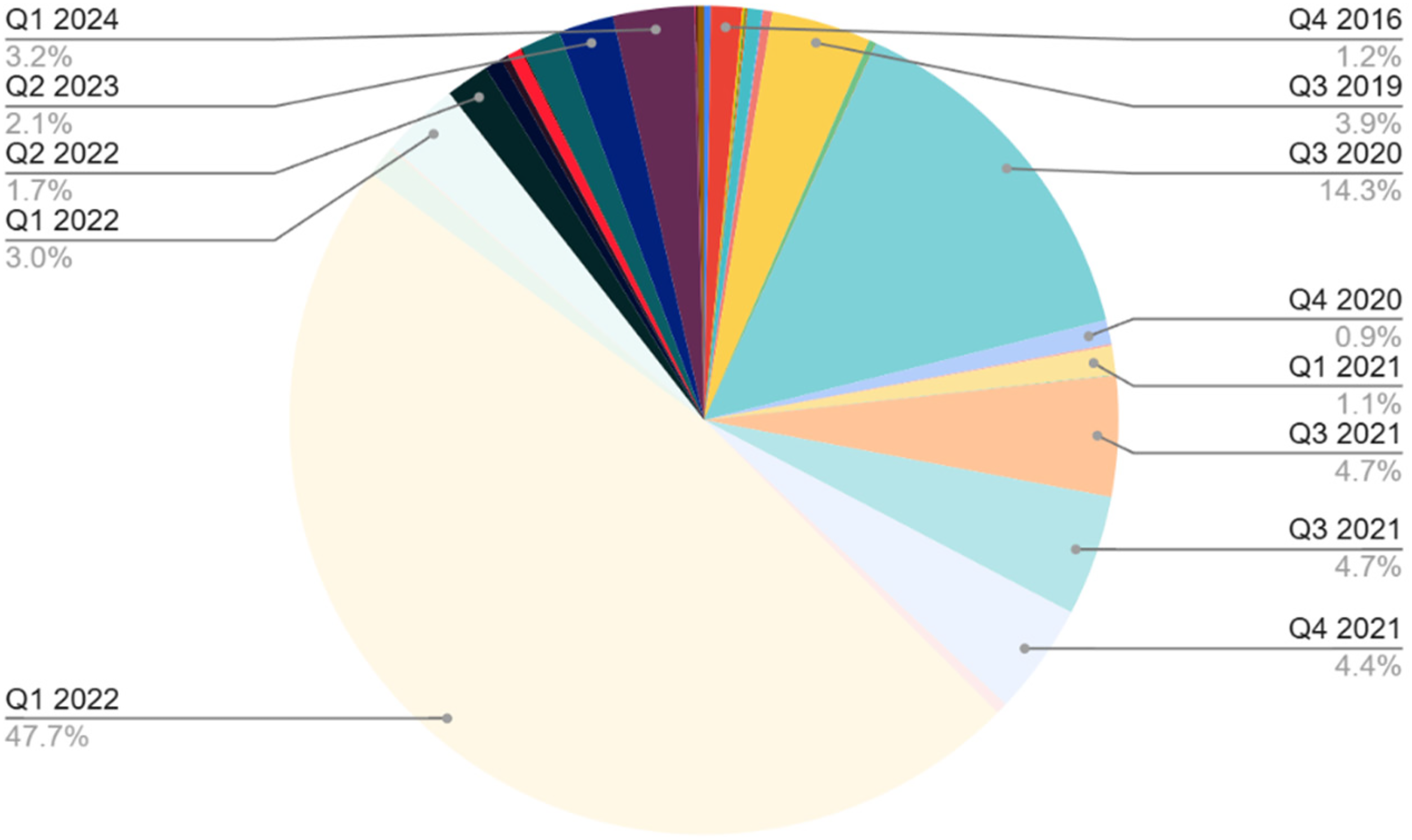

Allocation of capital over time.

Notably, the Asia-Pacific region is now the world's third-largest market for PE deals in the videogame industry (Volckmann, 2024: 6–7). Yet despite this, little research has examined the role of corporate and financial sector investment in local industrial contexts like Australia. This article addresses that gap by exploring how financialisation – the growing influence of financial actors, practices, and institutions across social and cultural domains (van der Zwan, 2014) – influences the structure and composition of the Australian videogame industry. In this article, I ask: what do the investment practices of corporate and financial sector investors in the Australian game industry look like, and how have they shaped the industry's structure?

To answer this research question, I present findings from a content analysis of a decade of investment data (2015–2025) using the Crunchbase database. Doing so, I map corporate and financial sector investment in Australia's videogame industry – defined here as videogame companies headquartered in Australia. I focus particularly on early-stage ventures, taken as companies that have not undergone an initial public offering and are not listed on a stock exchange. I explore the allocation of innovation financing in the Australian videogame industry by identifying the top investors, the companies they invest in, the geographical origins of capital flows, as well as the frequency and value of investments. Through this analysis, I aim to highlight the structural implications of corporate and financial sector capital allocation within the industry. By doing so, the article contributes to ongoing debates on how innovation financing practices (and how specific forms and structures of finance capital) shape game production norms (see e.g. Egliston, 2025, forthcoming).

The findings reveal that investment in the Australian videogame industry is predominantly geographically concentrated in east coast urban centres (and indeed, predominantly in Sydney, rather than Australian game development ‘capitals’ of Brisbane and Melbourne) and largely driven by international sources, particularly VC firms based in North America and Asia. Unlike public funding from federal and state screen agencies – which tends to, at least nominally, emphasise cultural value – private investment is oriented toward high-risk, high-growth ventures, especially those aligned with emerging technologies. Over the past decade, this has been most visible in the speculative domain of blockchain gaming and spatial computing (e.g. virtual and augmented reality), which attracted significant capital during the subdued macroeconomic climate of the COVID-19 pandemic – where cheap money could finance speculative moonshots. The findings of this article brings into view a segment of the Australian games industry that has largely escaped the focus of academic research, government policy and media representation – an industry whose scale, scope and geography differ sharply from the familiar narratives of indie or creative game development.

The intervention here is that while research has become increasingly attentive to the variegated nature of both Australian and global videogame industries – encompassing studios of different sizes, forms of labour and organisational structures (e.g. Keogh, 2021, 2023) – finance must also be understood as a key axis around which power, legitimacy and production are organised. Rather than treating videogame production simply as another expression of ‘late capitalism', this article calls for a more precise account of the specific structures and flows of financial capital that shape the industry's composition, decision-making processes, and ultimately, the kinds of games that are made. In doing so, it offers a necessary complement to existing analyses of the industry's political economy, including work on platformisation (Nieborg et al., 2020) and globalisation (Kerr, 2017), by foregrounding how financial logics and infrastructures actively organise contemporary videogame production.

In what follows, I situate the study within broader literature on media financialisation, discussing how innovation financing has shaped other media industries and how these dynamics intersect with game production. Following this, I outline the historical trajectory of financing in the Australian videogame industry, with a focus on the relationship between public funding, international capital, and the shifting dynamics of innovation financing investment. The approach section details the Crunchbase dataset and content analysis used to study investment practices and impacts. I then present the study's findings, followed by a discussion – focussing particularly on the overarching theme of concentration. The article ends with some conclusions, an acknowledgment of limitations and directions for future work.

Related work

Media financialisation

The way that the interests of financial stakeholders influence the media industries, particularly film and television, has been a critical area of study within the political economy of media and communication. Early work by Janet Wasko (1982), for instance, has examined the ties between the film industry and its financiers (e.g. banks) throughout the twentieth century. Over the subsequent decades, significant research in fields like ‘media industries studies’ has paid attention to questions of media economics (e.g. Havens and Lotz, 2016; Holt and Perren, 2009), exploring the underlying financing practices and financial logics of stakeholders in the in film (deWaard, 2024), television (Lotz, 2019) and music (Galuszka and Legiedz, 2024) industries at the meso and micro levels. Further, work has examined the interplay between media production, financial practices, and wider macroeconomic conditions (e.g. media production and its relation to post-GFC monetary policy; see Papadimitriou, 2017). In this article, I am particularly interested in the influence of finance and the financial sector on media production – a question that has been taken up in a body of recent work, exploring the relationship between the media and technology industries and financial sector stakeholders (such as venture capitalists, PE firms and asset managers; see de Waard, 2024; Shestakofsky, 2024). Collectively, institutional investors and large media corporations are increasingly capitalising on the media industries, viewing cultural production as an ‘investment and profit-extraction opportunit[y]’ (de Waard, 2024: 107).

Game production and finance

Despite significant attention in other sectors, finance and financialisation have received relatively little attention in studies of the videogame industry. Foundational work in production studies, such as Kerr (2006) has pointed out the role of private and public investment across the value chain in project financing. More recent research on the videogame industry has focused on game development within the system of shareholder capitalism, highlighting the influence of shareholder primacy on corporate governance (e.g. Egliston and Padua, 2023; Nieborg, 2021) as well as labour relations and possibilities for collective action (Legault and Weststar, 2021). Others point out how financialised logics of investment and risk are materialised in the development practices of industry – for instance, the adoption of calculative, metrics-driven approaches to mitigate risk and appease investors (Egliston, 2024; Whitson, 2019). Elsewhere, studies have focused on the speculative financial investments by videogame companies (either directly or through their own corporate venture arms) in emerging markets – such as blockchain (Egliston and Carter, 2024a) and spatial computing (Egliston and Carter, 2024b). Beyond this, work to date has examined entrepreneurial financing – the process of securing funds to start, grow, or sustain a business venture – for instance, government funding (Sotamaa et al., 2020), publisher-developer licensing agreements (Whitson et al., 2021) and crowdfunding (Smith, 2015).

A growing but still nascent body of literature examines the role of financial sector intermediaries in the videogame industry. Recent meso-level analyses across business studies and media studies have used investment data to examine the influence of financial intermediaries, such as VC and PE, on the composition of the videogame industry (e.g. Egliston, 2025; Niculaescu et al., 2023; Volckmann, 2024). At the micro level, ethnographic accounts highlight the relationships – and often tensions – between the logics, aims, and values of investors and the practices of developers (Styhre, 2020; Whitson, 2019). The present article contributes to understanding the meso-level impacts of financialisation by exploring how different forms of investment capital press upon the Australian videogame industry, each with distinct investment logics that shape industry practices (Cooiman, 2024: 2). Investment logics – particular to certain forms of capital investment – shape the types of companies that investors support and have structural implications for the fields in which they invest.

Financing the Australian video game industry: Historical context

The Australian videogame industry, relative to its global counterparts in Asia, North America, and Europe, is a relatively small one. During the 1980s, amidst a nascent yet booming global videogame industry, Australian game development evolved from hobbyist production into a more professionalised sector. By the 1990s and into the 2000s, the industry became increasingly reliant on foreign (often American) investment. For example, writing on the history of Brilliant Digital – an Australian company that developed interactive 3D animated software – Stuckey and Harkin (2025) note the company as a beneficiary of American VC investment during the ‘Siliwood’ boom of full-motion video (pp. 5–7), amidst a wider Silicon Valley ICT boom (Crain, 2014).

More broadly, throughout the 1990s and 2000s global (largely American) publishing firms sought to capitalise on the weak Australian dollar and the local English-speaking talent pool, viewing Australia as a cost-effective destination to outsource labour (Keogh and Tulloch, 2024). This led to a dynamic where the local industry was heavily reliant on licensing deals with major American publishers, with companies like THQ and Electronic Arts distributing games made by Australian studios. A dependency on foreign (predominantly American) capital, however, left the industry vulnerable to macroeconomic downturns. In 2008, the GFC saw the Australian dollar hit parity with the US Dollar. Outsourcing production work to Australia was no longer cheap – leading to widespread studio closures as international investment dried up. In the wake of the Great Recession, the rise of digital distribution platforms (e.g. Steam), alongside the growth of mobile gaming and app stores, enabled smaller teams to publish games directly to consumers (see van Dreunen, 2024). As Keogh (2019) has argued, in the period post financial crash, the Australian industry can be characterised as ‘intensely informalized’, composed of a heterogeneous mixture of commercial studios – recently bolstered by the re-entry of multinational companies like Riot Games and EA (as well as by tax breaks for large, commercial developers) – alongside independent developers of various sizes.

Production studies research highlights how game production is shaped by geography, including local labour markets, and national policy frameworks (Kerr and Cawley, 2012; O’Donnell, 2014). In Australia, public funding – at both state and federal levels – has played a central role in shaping the industry. Federal support for games (formally introduced in 2012 through the Interactive Games Fund under the Gillard Labor government) has been inconsistent, marked by shifts in political will (Reilly, 2014). National funding for videogame production has more recently re-emerged as part of the Albanese Labor government's 2023 Revive National Cultural Policy – providing funding and tax incentives aimed at stimulating growth in the cultural and creative industries (including videogames). State governments, by contrast, have often provided more sustained and targeted support, though this varies by jurisdiction. Victoria, for instance, has positioned itself as a national leader through long-term investment in game development, while other states offer more modest or project-specific support (and others – such as South Australia – offer no direct game funding at all at time of writing).

Although public funding has supported globally recognised titles – such as House House's Untitled Goose Game (backed by Film Victoria, now ScreenVic) and Witch Beam's Unpacking (supported by Screen Queensland) – and these successes are often highlighted in industry and policy discourse, the majority of financial investment in Australian game development does not come from public funding schemes. Rather, as I show in what follows, corporate and financial sector investment are the largest source of funds in the Australian games industry. Key investors include game, entertainment, media, and technology corporations, as well as financial sector investors. Financing from corporate and financial sector investors tends to operate according to aims and logics distinct from ‘traditional’ modes of financing in the games industry, such as publishing deals. When a game developer enters into a relationship with a publisher, funding is tied to specific projects and often recouped through revenue-sharing arrangements. In contrast, investment in startups and other early-stage ventures from the corporate and financial sector tend to prioritise equity-linked stakes in companies that have the potential to grow, introducing different, and highly speculative logics of risk and investment.

Approach

This article draws on investment data about innovation financing in the Australian games industry. I focus on privately held companies 1 that received investment either from corporate venture or investment arms of larger corporate entities (e.g. of game or entertainment conglomerates), or from stakeholders in the financial sector. Data was sourced through Crunchbase, a financial database, using a Crunchbase Pro account. Crunchbase aggregates publicly available information on corporate and investment activity, sourcing data from press releases, interviews, and regulatory filings (e.g. earnings reports). It is widely used by investors for due diligence and portfolio scouting, and increasingly by researchers studying corporate financialisation.

While Crunchbase provides default search configurations (e.g. company industry, investor type, investment stage, etc.). I refined my search parameters to focus on videogame companies headquartered in Australia and used the following search terms ‘Videogames’, ‘video games’, ‘Online Games’, ‘PC Games’, ‘Mobile and Casual Games’. Given the lack of corporate and financial sector financing in the Australian games industry, relative to the broader global games industry, I adopted a broad approach, drawing on data covering the period from 1 January 2015, to 1 January 2025. 2 After an initial search, I manually reviewed results to remove misclassified entries, those that did not fit the sampling criteria, and those with insufficient investor information. This process resulted in a final sample comprising 37 investment rounds across 28 unique companies and 145 unique investors (with 178 total investors – that is, including investors who contributed to multiple rounds). I exported the dataset into Excel for analysis. 3

The data analysis was guided by critical scholarship on financing in the technology sector that employs quantitative analysis of investment data. This includes studies of investment in energy (Baker, 2023) and education technology (Komljenovic et al., 2023), as well as research on investor identities – such as educational background, geographic location, and gender (Mkalama and Ouma, 2024). Following these approaches, I undertook a quantitative content analysis of Crunchbase data. I categorised the data using both Crunchbase's default classifications – such as investment type, geographic location, and funding stage (e.g. seed, Series A) – and a supplementary coding schema developed through inductive analysis of the dataset. I added additional categories not captured by the default Crunchbase search features – including the technological focus of investment recipient companies (e.g. mobile casual games, PC/console development, VR/AR applications) and investor type (e.g. VC, asset management, etc.). I verified company-level information through Crunchbase profiles and triangulated this data with external sources, including official company websites.

Innovation financing in the Australian video game industry

In what follows, I present findings from my analysis of investment data in the Australian games industry, spanning the decade of 2015 to 2025. I examine key sources of funding – including VC, PE and corporate venture financing – and their role in shaping production priorities. I analyse how investment flows across different funding stages, from early seed rounds to later-stage funding. Finally, I consider the scope and geography of investment, highlighting the dominance of blockchain gaming, the geographic concentration of funded projects (largely in Sydney), and the significant role of international capital in driving industry growth.

Investor type

Funds – professionally managed pools of capital – were the most frequent source of investment in the dataset (see Figure 1). The most common were generalist equity funds, that is, funds that buy equity-linked stakes in a company. Amongst these, most frequent were VC funds (n = 102). VCs are professionally managed funds that typically invest in privately held, high-growth companies, aiming to acquire equity stakes in promising startups, helping them scale, and eventually exiting through public stock offerings or acquisitions (see Birch, 2023). American technology VC Andreessen Horowitz (one that has funded the likes of Facebook), and boutique videogame VC Bitkraft were amongst the most frequent lead investors. This reflects these firms’ wider, rhetorical framing of an investment strategy in investing in the global games industry (see Chen et al., 2022. See also Egliston, forthcoming). Other – less frequent – sources of investment included private equity (PE) funds (n = 2) which acquire, often restructure, and sell companies for profit (and while PE typically focuses on later stage companies, the sole company with any PE investment was a seed-stage company). Other funds included hedge funds (n = 6), which use investor money in often risky investments that outperform average market returns. This included an investment by Three Arrows Capital, embroiled in controversy after a high-profile bankruptcy due to sizeable leverage investments in cryptocurrency during the 2022 crypto crash.

Beyond funds, other financial sector sources support the games industry. One is asset management firms (n = 14), often passive investors which manage pooled investments on behalf of clients, and hold very large, diversified portfolios. Another is multi-family offices (MFOs, n = 3), which oversee the wealth of high-net-worth families. Unlike more ‘active’ venture capitalists, these investors typically take a longer-term, less hands-on approach. Their holdings in game companies often form just one part of a much larger portfolio.

Independent and angel investors – high-net-worth individuals investing, often in exchange for equity – also play a role (n = 17), either operating alone or forming syndicates to pool capital. Some angel syndicates in the dataset emphasised specific social objectives – for instance, Eleanor Ventures, an angel investor syndicate that centred goals of diversity, equity, and inclusion, prioritising game startups led by women founders. Accelerators and incubators (n = 6) contribute to early-stage funding, providing startups with capital, mentorship, and business development support (e.g. one run and backed by the University of Melbourne). These programs typically help startups refine their prototypes and business strategies before seeking larger investment rounds from VC firms or corporate investors. Additionally, proprietary trading and investment firms (n = 2) – firms that invest their own funds (rather than investing on behalf clients) – have strategically invested in Australian gaming startups. This includes Alameda Research – the trading firm of defunct crypto exchange FTX – which had illegally invested customer funds.

Distinct from ‘traditional’ forms of financing, another trend was the rise of investments from crypto focused investors, particularly in the blockchain gaming space (n = 6). This included crypto investor funds, which function similarly to traditional investment funds but focus on digital assets and blockchain-based companies. Additionally, some of these crypto asset investors came in the form of decentralised autonomous organisations (DAOs) – community-governed investment pools that allocate capital through on-chain governance mechanisms. Notably, while DAOs often invest in crypto assets and ventures, they can invest in ‘traditional’ assets (such as equity-linked stakes in a company) if a DAO is registered as a company (where ownership and governance of investments is handled by the DAO).

Corporate investors in this dataset include the corporate venture capital (CVC) arms of large technology, media, and gaming companies (n = 20). These investors differ from traditional VCs in that they are often motivated by strategic efforts to consolidate competing firms (see Chesbrough, 2002). Strategic goals could include a company investing in game studios to secure exclusive content for their platforms or to expand their gaming ecosystems. Notably, few of these investors were themselves game companies, which contrasts with global trends where major international game firms are active in both venture financing and broader investment and consolidation (see e.g. the likes of Embracer, Tencent). Instead, the most active investors were a mix of crypto companies or the corporate VC arms of non-gaming firms. For some of these investors, the motivation is likely one of vertical integration – that is, investing in projects that can support or extend their existing business operations. For instance, Solana Ventures – the venture arm of Solana Labs (the developer of the Solana blockchain) – invested in games that integrate with the Solana blockchain, reflecting a wider industry perception of alignment between blockchain infrastructure and game development (Egliston, 2025). For others, such as companies already operating within the videogame industry, investment strategies appear motivated by a desire for horizontal integration, with companies seeking to expand their portfolio across adjacent or emerging sectors of the games industry. The most frequent corporates investor in the dataset was Animoca Brands, a Hong Kong-based game software company that also operates a corporate VC arm (participating in five deals across the dataset, three of which were as lead investor).

Investment stage and value

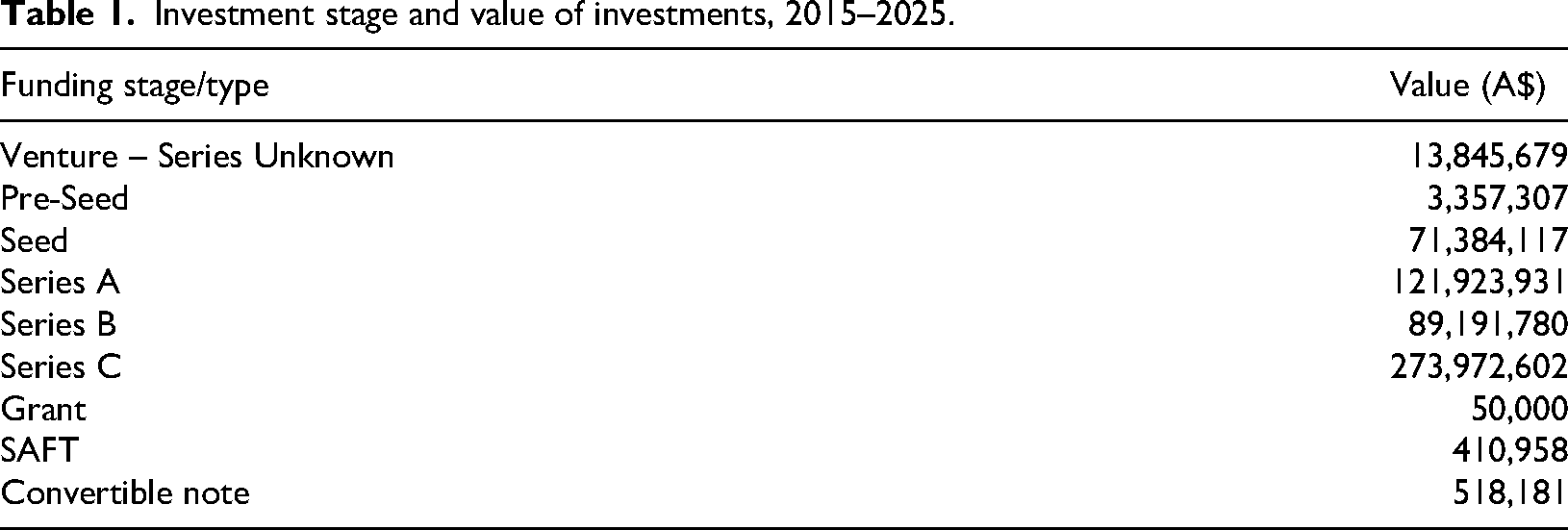

Investments – which totalled A$574.6 M over the decade – were spread across companies at different stages of maturity (see Figure 2). Funding for startups and privately held companies typically follows a structured process involving multiple stages, each with distinct expectations. At the earliest stage is pre-seed funding, financing what is often little more than an idea. Next is seed funding, which could support a more developed idea or prototype. Valuation at this stage is based primarily on the potential of the idea and the capabilities of the founding team rather than concrete performance. In the Australian games industry, pre-seed (n = 8) and seed stage (n = 14) funding was relatively low in value, with only A$3.3 M and A$71.4 M across each stage respectively, despite being the most frequent form of investment. Once a company gains traction with a working product or service, it may seek Series A funding, where investors look for signs of market demand, scalability, and a viable business model. Valuation at this stage considers revenue, growth projections, market size and competition. In the dataset, Series A funding amounted to A$121.9 M yet was less frequent than seed rounds (n = 7). As companies continue to grow and refine their operations, they may progress to Series B funding, which is typically aimed at expanding market reach, increasing production capacity, or enhancing product offerings. In this stage, funding reached A$89 M (n = 2). Series C investments are often even larger, and are focused on companies with proven business models seeking to control their market or expand internationally. Series C funding in Australia attracted A$273.9 M – and while least frequent (n = 1), was the highest value investment stage.

For investors in early-stage entrepreneurial financing, there is often an imperative to create an exponential growth curve in valuations to signal that their portfolio companies – especially startups – are on a successful trajectory, thereby attracting additional investors. In the dataset, 22 firms received only a single round of funding, the majority of which was a single round of Seed funding (n = 15). This is not an uncommon dynamic in innovation financing and reflects broader trends in global games industry venture financing (see Egliston, forthcoming). A total of 4 companies secured two rounds of funding, 1 company received three rounds, and 1 had received four rounds of funding. In some cases, this can be explained by a company securing a single but substantial round of funding in the period under study (e.g. Zed Run or Virtually Human Studio – both of which a single round of A$27 M of Series A funding), or in other cases, where funding was from other single ‘round’ sources (e.g. grants). However, in most instances, it reflects the reality that many early-stage startups fail to meet investor demands and expectations.

Beyond venture stages (such as Series A, B and C rounds), the dataset includes several additional forms of financing. First are unspecified venture rounds (n = 2), which may represent growth equity investments not formally labelled within the standard Series convention. Second, one cryptogame company raised capital via a SAFT (Simple Agreements for Future Tokens) – a contractual arrangement often used in blockchain and crypto startups, where investors provide capital in exchange for rights to future tokens once a crypto platform or network is launched. Third, one company received a grant (the terms of which were not clear from publicly available information) from British-Australian mining company Rio Tinto (to produce an educational game for primary and high school students in Australia). Finally, the data captures financing through convertible notes, which are short-term debt instruments that convert into equity, typically during a future investment round.

Investment frequency and value over time

Investment in Australian game development has fluctuated significantly over the past decade, shaped by broader economic cycles and shifting investor priorities (see Figure 3). Between 2015 and 2019, funding levels remained relatively low, with annual totals ranging from approximately A$1.5 M to A$22.4 M (with a mean of A$7.9 M). This reflects broader global trends – the videogame industry has historically not been a major site of investment, particularly for the financial sector. This is largely because game development does not easily translate into scalable, rent-bearing technology, which the financial sector tends to prioritise.

However, investment activity changed markedly from 2020 onward, as global trends in digital media and technology financing spurred greater interest in game development. The COVID-19 pandemic – and the subdued macroeconomic environment accompanying it – played a significant role in this shift, with investment surging to A$89 M in 2020 and A$88 M in 2021. The peak year was 2022, when total funding reached A$326 M, driven by a mix of later-stage investments and speculative financing in emerging technologies such as cryptocurrency and spatial computing. A substantial portion of this capital flowed into a small handful of companies – namely, Sydney-based blockchain service and game developer Immutable, the Sydney-based blockchain-based game developer Illuvium, and the Melbourne-based VR company Zero Latency.

Market contractions – following rising interest rates post-COVID – saw investor exuberance for speculative projects wane. In 2023, investment totalled A$12 M and in 2024, sat at A$20 M. This volatility underscores how investment in the Australian videogame industry is shaped by global financial trends and macroeconomic conditions, with financing proving highly sensitive to fluctuations in interest rates and shifting investor sentiment toward technology and media.

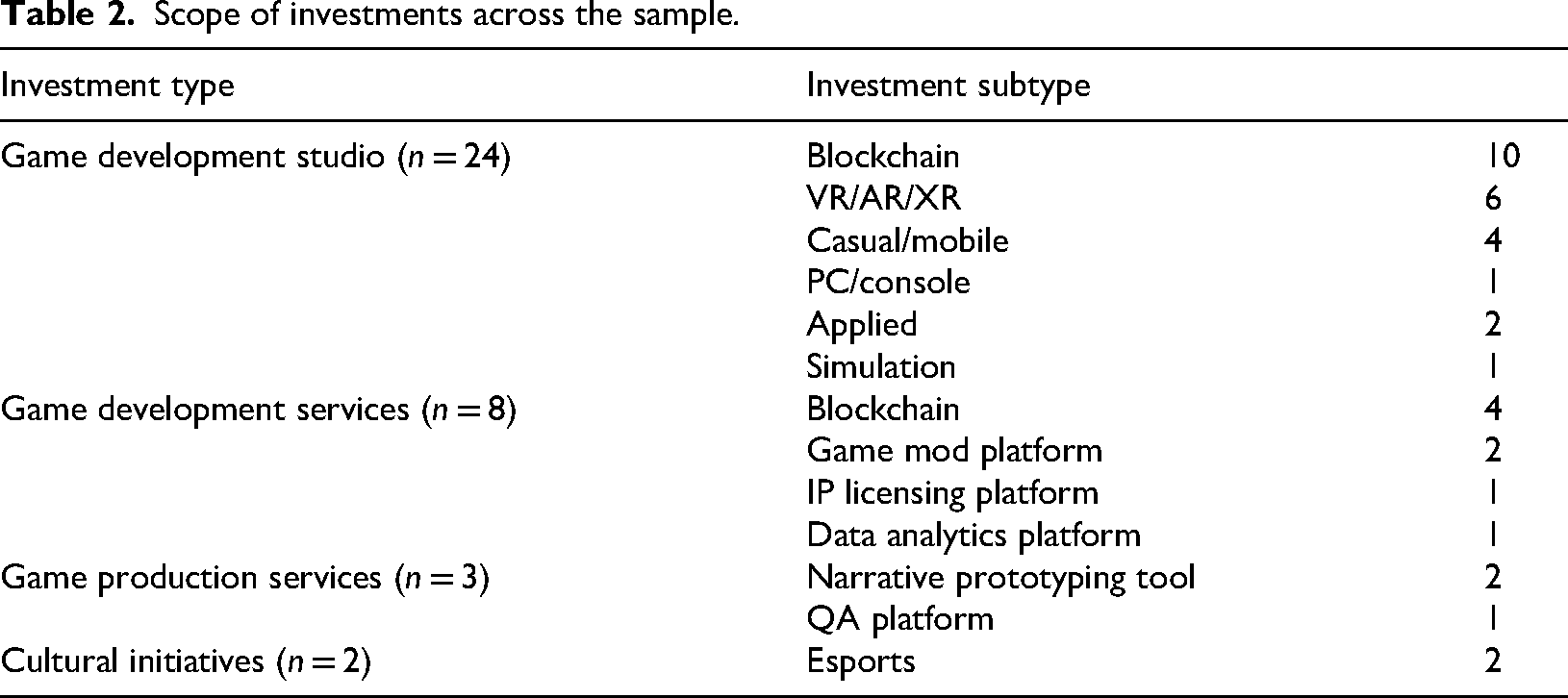

Investment scope

Investments fell into four broad areas: game development, services, production, and cultural initiatives (see Table 2). The majority of investments (n = 24; A$178.7 M) were in game development, with funding directed toward studios creating digital games, particularly those building original IP or scaling up existing titles. Service providers (n = 8; A$393 M), while less frequent, attracted the largest share of capital, reflecting strong investor interest in tools, infrastructure, and platforms that support the wider game ecosystem – such as backend technologies and blockchain infrastructure. An even smaller number of investments (n = 3; A$844 K) supported production focused investments (e.g. technologies for QA, prototyping). Finally, cultural initiatives (n = 2; A$2.1 M) accounted for the smallest share of funding, solely directed toward esports-related organisations.

Investment stage and value of investments, 2015–2025.

Scope of investments across the sample.

Beyond these broad categories, more specific trends emerged within the investment landscape. Most investments – both by value and frequency – were directed toward games that incorporated blockchain technology, that is, a decentralised ledger system used to manage crypto assets and tokens. Cryptogames were positioned during this period as a natural test case for blockchain's broader promises of decentralisation and financial innovation (see e.g. Egliston, 2025). Between 2018 and 2022, blockchain-related game projects received substantial backing, with A$492.9 million raised across 14 deals. Notably, a significant portion of this went to just two firms: Immutable and Illuvium. This concentration of capital in cryptogames reflects a wider global boom in the area, driven by the popularity of early blockchain titles such as CryptoKitties (released in 2017; see Serada et al., 2021) and a wave of investor enthusiasm for ‘Web3’ technologies (Sadowski and Beegle, 2023).

Outside of blockchain, investment levels across other ‘emerging’ technologies were more modest. Spatial computing technology, like Virtual and Augmented Reality, attracted A$26.7 million across 6 investments. VR's appeal to investors appears linked to location-based entertainment and enterprise applications, rather than mass-market consumer adoption. Simulation games received A$27 million from a single large deal, indicating interest in games with training, educational, or applied uses beyond entertainment. Notably, investment in staples of the Australian games industry, such as casual and mobile games, accounted for just 4 investments (A$14.5 million).

Spatiality of investment

Geographically, investment is highly concentrated in NSW, specifically Sydney (n = 22), exceeding A$500 million over the 10 year period (although the majority of which flowed to a single firm – Immutable). While Victoria (and Melbourne in particular) has a strong game development output, offers the highest state-level funding and attracts the most federal funding (Darbas, 2024), investment from corporate and financial sector stakeholders in the state's videogame industry remains comparatively low (Victoria – predominantly Melbourne – received A$38 M over 8 investments). Western Australia received A$12.4 M in investment. Other states and territories saw little to no investment from the corporate and financial sectors, reinforcing existing geographic imbalances in game financing opportunities (Williams, 2025) and geographic concentration of production (Darchen, 2016).

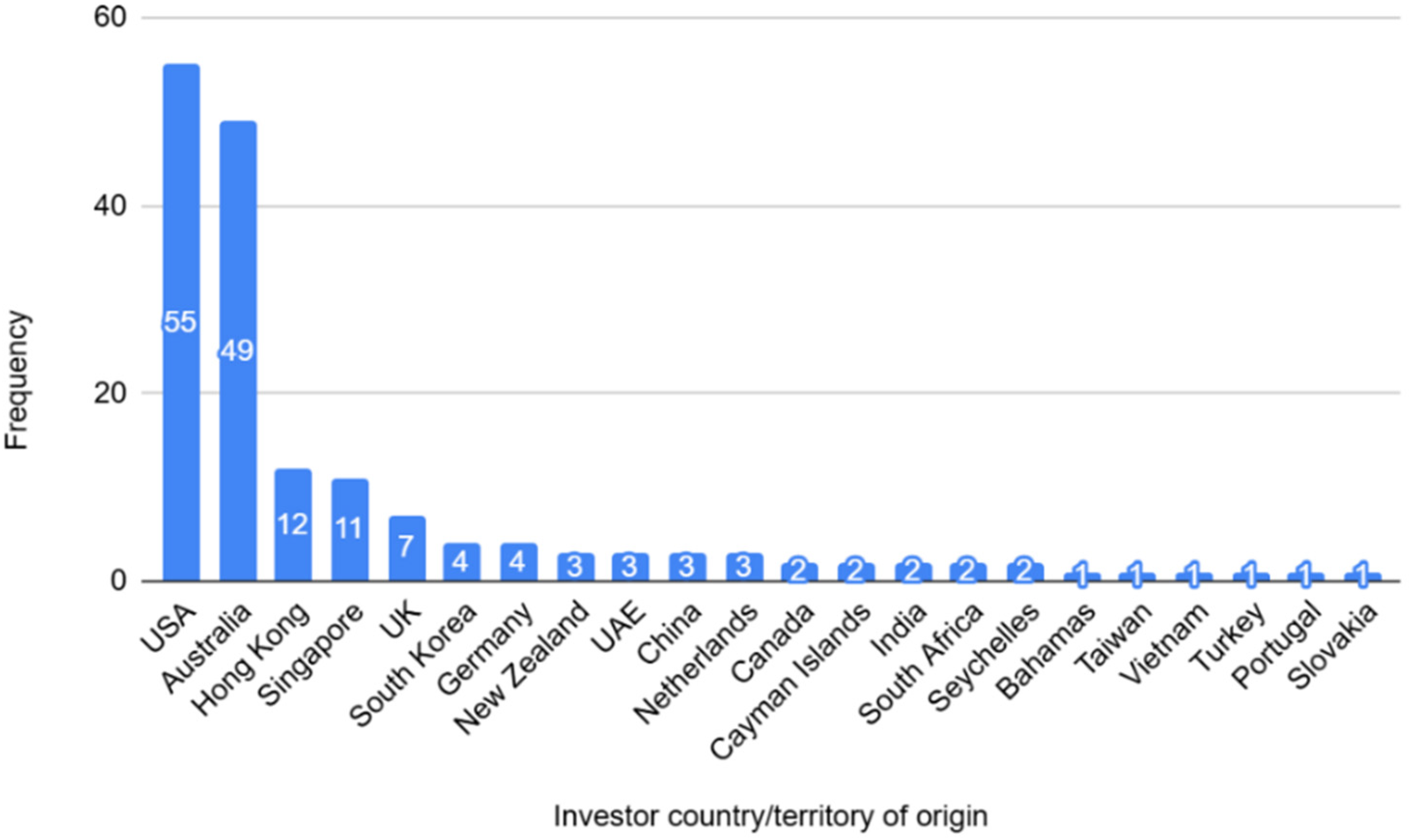

Financing for the Australian videogame industry primarily flows from international sources (see Figure 4), particularly financial hubs in Asia (such as Hong Kong and Singapore) and the United States, especially California – a longstanding source of media and technology investment capital (see Harris, 2023). This strong presence of international capital highlights how investment in Australian game development is driven in significant part by global financial priorities than by domestic policy or industry-led initiatives. While Australian investors were active participants (n = 49, ranking second by country of origin for total investment), their role was secondary to that of major international backers. Notable domestic investors included Carthona Capital, a Sydney-based VC firm that led several rounds, and the Telstra-backed accelerator Muru-D, which was among the most frequent contributors. A small portion of investment came from organisations with no fixed location, such as DAOs, reflecting the growing influence of crypto-based models of distributed governance in game financing.

Investor frequency by country/territory of origin.

Discussion

The findings of this study point to a defining feature of innovation financing in the Australian videogame industry: concentration. Ownership and concentration are foundational concerns in the political economy of media and communication, central to understanding how power operates within media and cultural industries (see e.g. Mosco, 2009). The concentration of media ownership has implications for the kinds of media that get produced and the form they take. This concern extends beyond visible ownership structures (such as, in the context of games industry, big publishing conglomerates like Electronic Arts or Ubisoft) to include the often opaque and behind-the-scenes role of financiers, whose influence, as both the present study and the current literature on media financialisation attests (see e.g. deWaard, 2024; Wasko, 1982), increasingly shapes the direction of media production. Financial actors – whether venture capitalists, asset managers or corporate investors – exert structural force over what gets produced and by whom.

Investment in Australia's game industry is concentrated in scope. While most investments were in game development companies (i.e. companies who produce game software), contrary to wider investment trends, this was not in mobile or casual games (see Egliston, forthcoming). Rather, much of the focus was on speculative, ‘tech-first’ ventures – particularly blockchain gaming and spatial computing (e.g. VR) – across both development and service layers. These investments follow global hype cycles around Web3 and the metaverse, driven largely by VC firms seeking rapid scaling and high returns (Cooiman, 2024). Tech-focused VCs – the most frequent investor in the sample – treat games as scalable technologies with infrastructural potential; those with the imagined capability to grow and become widely embedded in daily life – notably, blockchain and spatial computing. In the dataset, companies like Immutable, Illuvium, and Zero Latency attracted the largest deals (and most of the funding across the 28 companies in the sample), reflecting investor priorities around scalable emerging technology rather than the cultural or artistic value in games.

Second, the data reveals a clear spatial concentration of investment. Corporate and financial sector funding in Australian game development is overwhelmingly focused on firms in Sydney and Melbourne, with capital largely originating from international investors – primarily VC firms in North America (especially the US) and Asia. While New South Wales receives less funding for games from federal arts and cultural industry schemes (Williams, 2025), it attracts the highest levels of corporate and financial sector investment, suggesting that proximity to financial infrastructure and tech-aligned investor networks plays a greater role in securing corporate and financial investment than proximity to established game development ecosystems, such as those in Melbourne or Brisbane (Darchen, 2016). This concentration of funding in coastal urban centres mirrors broader public funding patterns, further centralising industrial and cultural production.

This dual pattern of concentration identified in the study has important implications for understanding the financialisation of Australia's game industry. Empirically, it builds on existing accounts of the sector. As Keogh (2021, 2023) argues, the Australian games industry operates as a Bourdieusian field – a structured social space composed of actors, oriented toward each other, with differing degrees of social, cultural, and economic capital – manoeuvring in pursuit of desirable resources (Bourdieu and Nice, 1980). Keogh's intervention, via Bourdieu, highlights the uneven distribution of power among game makers – which in turn affects the kinds of games that are made, and under what conditions – allowing for a more nuanced understanding of the industry's heterogeneity. Indeed, accounting for finance capital in the field further complicates an already messy picture of game production. Distinctions between AAA studios, ‘commercial indies’, and DIY developers are even further blurred when independent studios secure multi-million-dollar seed rounds (such as an A$9.7 million seed investment in Melbourne indie developer Lumi Interactive), or when companies like Immutable grow into tech unicorns (that is, exceeding a $1 billion valuation). If we are to take seriously Keogh's call to understand the industry as a variegated field, then finance must be recognised as a key axis around which power, legitimacy, and production are organised.

The picture of an industry dominated by American finance capital likewise has important implications for thinking about the relationships between capital and geography, and underscores how national industries remain conditioned by the structures of transnational capital even amid local narratives of creative independence. The results highlight a structural continuity in the geography of investment that has defined the Australian games industry since prior to the Great Recession (see Keogh and Tulloch, 2024; Stuckey and Harkin, 2025) – that is, one reliant on US finance capital. What is striking in the present data is that, despite a decade of cultural policy intervention in further cultivating an Australian games industry (see e.g. Darbas, 2024), the United States remains the dominant source of capital. This suggests a persistent subordination of Australian game development to US financial power, a dynamic which we can understand in terms of recent accounts of digital imperialism (Joseph et al., 2023; Nieborg et al., 2020). From this perspective, and contrary to existing work on the sector (e.g. Keogh, 2023), the Australian industry functions less as an autonomous creative ecosystem and more as a node within global circuits of value extraction (flowing upward to largely US investors).

The second implication is normative. A significant portion of capital flowing into Australia's game industry has been directed toward high-tech, speculative ventures – particularly in blockchain and spatial computing. These are often single-stage investments, which may indicate a lack of long-term commitment or belief in sustained growth. While public data via Crunchbase is limited in what it can reveal about the performance of privately held startups, this pattern of single stage investment is consistent with wider patterns of high failure rates that characterise innovation financing (Cooiman, 2024). But is this not a misallocation of resources – prioritising hype-driven projects over sustainable or culturally valuable forms of production? Crypto-based games, in particular, raise further concerns, from their environmental impact (as some Australian game developers have noted, see e.g. Sinclair, 2022), to their ties with volatile and extractive financial models (see e.g. Egliston, 2025; Zaucha, 2024), and their entanglement with scams and fraud (see White, n.d.). Ultimately, if the future of Australian game development is to be more equitable, diverse, and sustainable, public policy must actively counterbalance the highly speculative focus of innovation financing from the corporate and financial sector.

Conclusion

This article has examined the role of innovation financing in the Australian videogame industry. Drawing on a decade of investment data, I have explored its meso-level implications for the structure of the industry – tracing where capital flows and which actors are involved. The broader intervention here is that financialisation should be a key axis around which game production research is oriented, especially when considering how games are made, and which games get made. While finance – what economic sociologists Knorr Cetina and Preda (2004) describe as operating at a ‘second-order’ level – often appears abstract or detached from questions of consumption and production, its effects are anything but immaterial. Financialised logics materially reshape the industry: influencing what kinds of games are produced, who gets to produce them, and where investment is directed.

In concluding, several limitations must be acknowledged. This study maps structures and flows of capital rather than outcomes. It cannot assess whether specific investments were successful or how capital was deployed within companies (cf. Volckmann, 2024). Nor does it capture the on-the-ground realities of how game companies work with investors, and how relationships with investors may affect every day industrial norms. Future research could extend the analysis in this article by examining investor-developer dynamics more closely, or by triangulating investment data with interviews and ethnographic fieldwork. Further meso-level inquiry might adopt a more granular lens to explore how capital flows intersect with identity and privilege (cf. Mkalama and Ouma, 2024). Ultimately, integrating meso-level analyses of financialisation with micro-level perspectives will be essential for building a more comprehensive understanding of how financial capital shapes the videogame industry across multiple scales.

Footnotes

Acknowledgements

The author would like to acknowledge Taylor Hardwick and Tianyi Zhangshao for their helpful comments on earlier versions of the manuscript.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Australian Research Council DECRA Fellowship, ‘Paying and Playing: Assessing and Regulating Digital Games-as-a-Service’ (DE240101275).

Conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

Not applicable.