Abstract

Background:

Additional billing is commonly and legally practiced in some countries for patients covered by health insurance. However, knowledge and understanding of the additional billings are limited. This study reviews evidence on additional billing practices including definition, scope of practice, regulations and their effects on insured patients.

Methods:

A systematic search of the full-text papers that provided the details of balance billing for health services, written in English, and published between 2000 and 2021 was carried out in Scopus, MEDLINE, EMBASE and Web of Science. Articles were screened independently by at least 2 reviewers for eligibility. Thematic analysis was applied.

Results:

In total, 94 studies were selected for the final analysis. Most of the included articles (83%) reported findings from the United States (US). Numerous terms of additional billings were used across countries such as balance billing, surprise billing, extra billing, supplements and out-of-pocket (OOP) spending. The range of services incurred these additional bills also varied across countries, insurance plans, and healthcare facilities; the frequently reported were emergency services, surgeries, and specialist consultation. There were a few positive though more studies reported negative effects of the substantial additional bills which undermined universal health coverage (UHC) goals by causing financial hardship and reducing access to care. A range of government measures had been applied to mitigate these adverse effects, but some difficulties still exist.

Conclusion:

Additional billings varied in terms of terminology, definitions, practices, profiles, regulations, and outcomes. There were a set of policy tools aimed to control substantial billing to insured patients despite some limitations and challenges. Governments should apply multiple policy measures to improve financial risk protection to the insured population.

Keywords

Introduction

The right to health where all people can receive health services they need without financial burden is a fundamental rights for all. 1 However, not all populations have access to health services despite being insured. Universal Health Coverage, a global commitment under the Sustainable Development Goals (SDGs) comprises of three dimensions including population coverage, service coverage, and financial protection. 2 To track progress towards UHC, relevant data were monitored. The percentage of population covered by health insurance can be easily measured and is already reported by many countries along with the SGD indicator 3.8.1 on service coverage and SDG 3.8.2 on proportion of population with large household expenditures on health as a share of total household expenditure (or income); with the standardised measurements.3,4 However, the details of cost coverage, that is, the size of a financial safety net that an insurance provides to its insured members has not been widely captured and whether the essential services have sufficient financial protection is also not well understood.

Health systems around the world present different forms of financing basis, ranging from tax-based financing, social insurance schemes, private mandatory or voluntary insurance to out-of-pocket payment. 5 In most countries, insured people are required to share certain cost at the point of service. This can be in the forms of a fixed rate or a percentage of medical bills with or without ceiling as agreed between insurers, providers, and patients known as copayment, deductible, or coinsurance. 6 For example, in England where healthcare are mostly funded by general tax, people are required to pay a small fixed amount per prescription; the German sickness funds require a small fixed amount per admission day and 10% of prescription price; the US’s systems use a mixed of fixed rate copayment, deductible, and 10% to 20% coinsurance depending on schemes and types of service. 7 The Japanese people pay 10% to 30% of total amount of health care costs. 8 However, additional billings to patients beyond the agreed cost-sharing rate are also legally and commonly practiced in many countries. Such instance occurs when the provider’s charges are higher than the amount covered by health insurance. 9 There are several terms used to call these additional payments – for example, balance billing, extra billing, and surprise billing. This might be expected or unexpected payment but has becoming a barrier among the insured people who cannot afford to pay resulting in either unmet needs or catastrophic health spending, similar to the negative effects of user fees in low- and middle-income countries. 10 In some States of the United States where additional billings are generally practiced, around two-thirds of insured adults are worried about their affordability to pay for unpredictable size of additional bills. 11

Legislative measures to regulate balance billing were introduced in some countries. For example, in January 2019, California Supreme Court ruled that additional billing by emergency physicians is unlawful. 12 However, regulating additional billings requires information such as size of additional billing, services prone to extra charge, and impacts on patients and health systems.

The review questions include (1) what are the definition of balance billings? (2) How are balance billings practiced? (3) Did the government or insurance fund control the level of balance billing if it legally permitted? and (4) what are the impacts of balance billing? To address the knowledge gap, this study seeks to comprehend the terminology, scope, definition, practice, effects, and regulations of additional billings. The scoping review was applied by this study as it matched the purpose of the study in providing the overview of balance billing from the related documents. Evidence from this study may inform policies to better regulate and mitigate its negative consequences on insured patients.

Methods

Search strategy

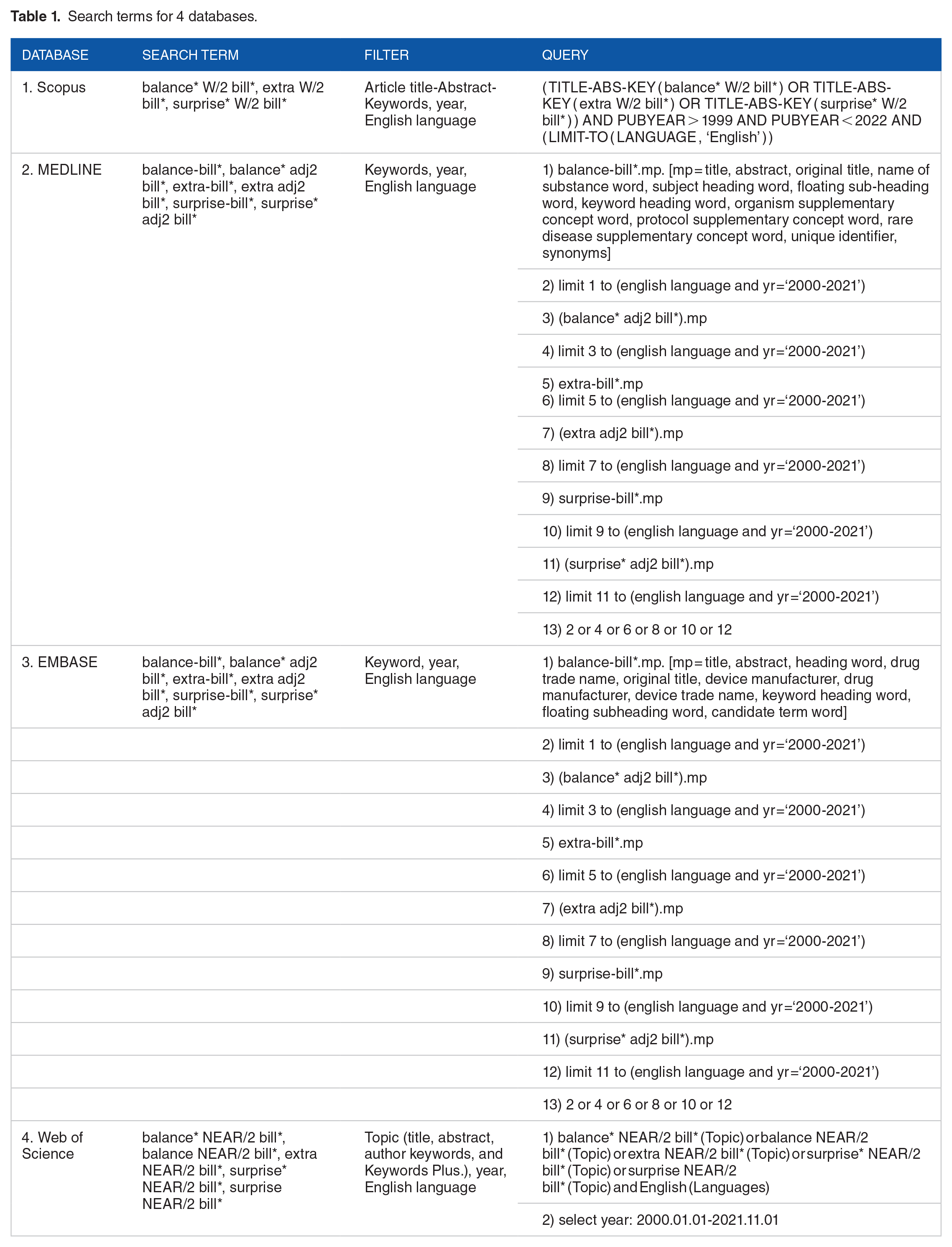

A systematic search was carried out in November 2021. Four electronic databases that cover medicine, public health, healthcare management, health financing and health policy including Scopus, MEDLINE, EMBASE and Web of Science were used for literature search. Hand searching was also employed to supplement the missing documents.

Search terms were developed from the research questions which seek to understand the definition and scope of balance billing. Hence, only 1 key domain related to balance billing and 2 related terms including ‘extra billing’ and ‘surprise billing’ was listed and used to search in the 4 databases with appropriate quote marks, truncation, and filtres defined in each database, see Table 1. An operator ‘OR’ was applied to all words listed in the key domain.

Search terms for 4 databases.

Inclusion and exclusion criteria

Full-text articles that reported the details with regard but not limited to the definitions, scope, profile, practice, impacts, and regulation of balance billing (and/or 2 related terms-extra- and surprise billing) for health services were included in the analysis. Only studies published in the English language between 1 January 2000 and 1 November 2021 were included. The clinical research studies and contents unrelated to our focuses were excluded. The uninsured people were also left out from the study. The searching operation was executed from 28 October to 2 November 2022.

Data screening and extraction

The search results from the 4 databases were exported to a reference manager software ‘Endnote’. After removing the duplications, the remaining papers were transferred to Rayyan (www.rayyan,ai), a free access online tool that facilitate review and assessment by review team members. We went through 2 screening steps (1) the balance billing and 2 related terms including ‘extra billing’ and ‘surprise billing’ were searched by title, abstract and keywords, (2) the included studies from the first step were screened by the full text. Screening in each stage was determined against the eligible criteria. Two authors were responsible for independently screening the title, abstract, and keywords of all records. Discrepancies were determined by the third reviewer. The articles that were agreed to be included by at least 2 reviewers were searched for full text. Each of the retrieved full text document was independently reviewed and extracted into a matrix by 2 authors; the disagreements were concluded by the third author.

Data analysis and synthesis

Data charting was proposed by an author. Then, it was discussed and finalised by the team members. Basic information including authors, published years, countries, research methods, study objectives, and all relevant details related to balance billing (and its related terms) covering definitions and scopes, impacts on patients and regulations were extracted. Then, coding of relevant contents was developed which was framed by review questions. All authors were involved in tracking and synthesising the data. Then, an author summarised and filled the data into the presented chart and tables.

Finally, 5 themes on additional billings emerged from the analysis: (1) term and definition, (2) balance billing in practice: what services incurred additional bills, (3) regulation, (4) impacts on insured patients, (5) measurements to address impacts, and (6) challenges and solutions. Several sub-categories emerged in these themes. We analyse themes by using Excel spreadsheet.

Scoping review is an appropriate tool to explore and provide an overview of knowledge gaps 13 related to balance billing. This method does not require a critical appraisal, 14 hence, we did not performed quality assessment of literatures.

We provided Preferred Reporting Items for Systematic reviews and Meta-Analyses extension for Scoping Reviews (PRISMA-ScR) Checklist in Supplemental Appendix A.

Results

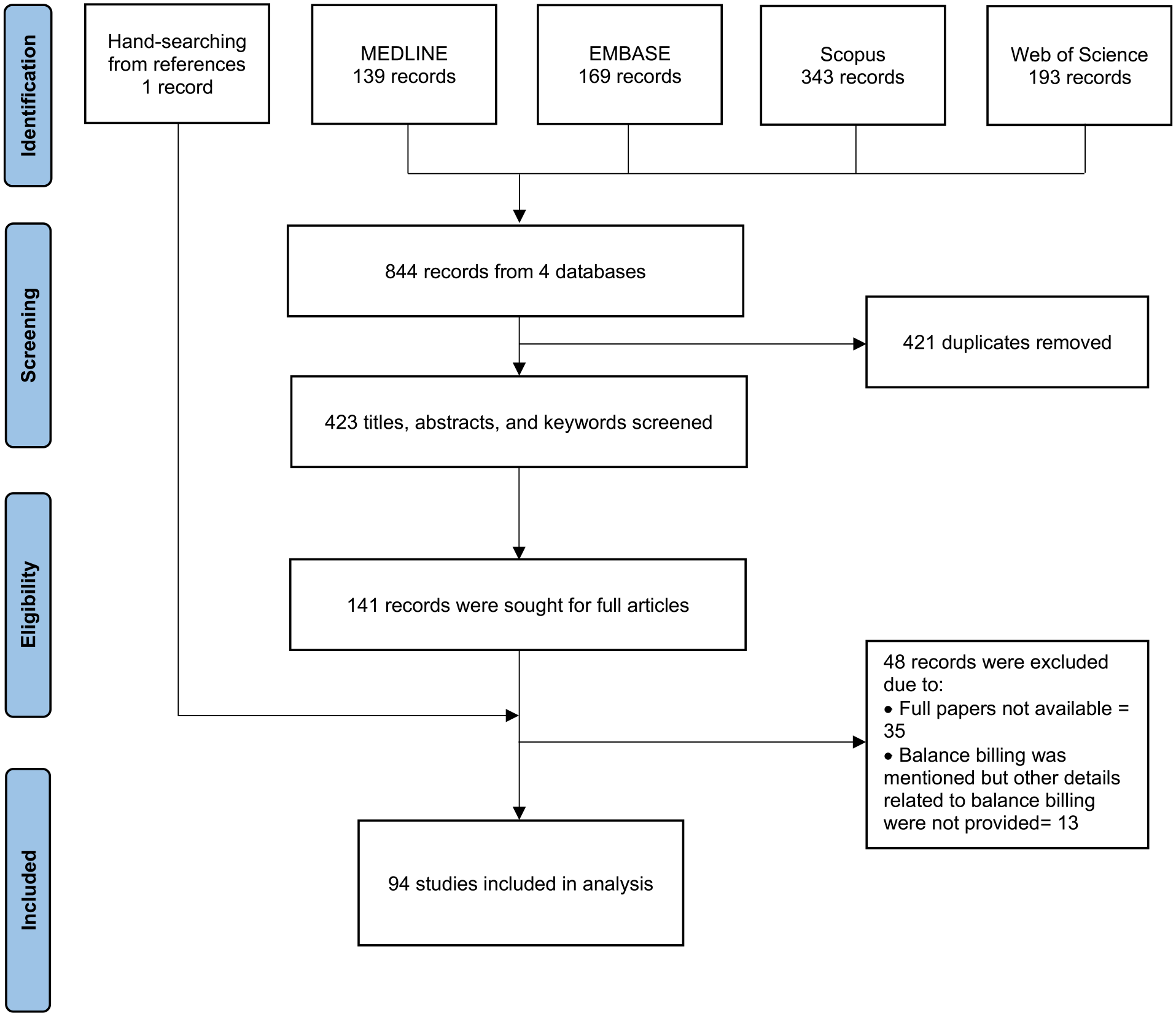

The systematic literature search from 4 databases found 844 records that almost half of them (421 records) were removed due to duplication. The remaining 423 articles were screened with the title, and abstract, and keywords to select publications that met the inclusion criteria. As a result, 141 documents and the additional article from hand-searching were retrieved to screen the full papers; 35 records were excluded because full papers could not be accessible after great efforts, and 13 records were removed as there were no details of balance billing. In total, 94 studies were selected to the final analysis. Figure 1 displays the number of studies at the different screening stages.

PRISMA flow diagram of the records form scoping reviews.

Characteristics of the included studies

Table 2 summarises the research setting of the included articles. More than one-third of the included papers (37 articles) were research studies; 11 articles were review papers; and 46 studies were other types such as commentary, perspective, news, and report.

Characteristics of the included studies.

A majority 83% of total studies (78 studies) were conducted in the United States. There were 4 studies from Canada, and 3 papers from Japan. Two studies are observed in 3 groups which were Belgium, multi-countries, and not-specify countries. Only one each was study in France, the Philippines, and Taiwan. Full characteristics of all included studies were provided in Supplemental Appendix B.

Terms and definition of additional billings

Different terms of additional payments made by insured people were used by different countries. The term ‘balance bill(ing)’ was commonly used by all countries except Belgium and Canada. Belgium was the only country that called ‘supplements’. The second common term, ‘extra-billing’, was utilised by Canada and Japan. The United States applied various specific words to reflect balance billing. Apart from the mostly used term ‘balance bill(ing)’ in various States of the US, ‘surprise bill(ing)’, ‘surprise (medical) bill’ or ‘surprise out-of-network bill(ing)’ were generally used not only for the differentiated meaning but also interchangeable with balance bill(ing) and surprise bill(ing). Out-of-Pocket in terms of coinsurance and copayment was used by a study in the US. 53 Other terms including ‘unexpected balance bill’, ‘unexpected medical bill’, and ‘billing practice’ were also found in the United States, see Table 3.

Terms used for additional billing in the included studies.

Despite using the similar term for additional billing, the definitions and scopes differed even in the same country. In Belgium, 97 this additional payment called ‘supplements’ covered the extra payments for non-covered services which is more comprehensive than the copayment for covered services beyond the rates agreed upon between providers and insurance agencies 98 that was called ‘extra bill(ing)’ in Canada90,93 or ‘balance bill(ing)’ in Japan,95,96 France, 103 Philippines 104 and Taiwan. 105 Japan clearly defined the heterogenous scopes between ‘balance billing’ and ‘extra billing’. Balance billing was the additional fees on top of the prices set by the fee schedule, while an extra billing was the payment for uncovered services or medicine outside the fee schedule95,96 including the utilisation in the large hospitals without a referral from the primary care doctor. 94

Though various terms of balance billing were used in the US, diverse concepts emerged. In the US, the terms ‘balance bill(ing)’ and ‘surprise (medical) bill(ing)’ were used interchangeable in the same study. The magnitude of ‘balance bill(ing) was the difference between the (hospital) price chargeable for the services provided to insured patients and the reimbursement rate by health insurance36,42,43,55,78,89; this meaning was also aligned with ‘surprise (medical) bill(ing)’ indicated in some included studies.35,39,46,54,59,67,68 Another general scope of both balance billing31,38,84,106 and surprise billing34,44,45,47,50,64,70,73,76,80,81 was the ‘unexpected’ extra payment charged to patients who received treatments, medical transport or health services provided by the providers outside their insurance networks. Interchangeably use between balance billing and surprise billing of this scope was found in some papers.21,58,85 Also, some studies indicated that ‘surprise (medical) bill(ing)’ applied for out-of-networks physicians who provide services either at in-network or out-of-network facilities35,72,75,82 particularly the emergency services provided by out-of-network providers.35,75

For a more specific scope, ‘balance bill(ing)’ was defined as the extra amounts charged to patients who received services provided by out-of-network clinicians at their insurer’s provider network,17,18,38,70 however, this concept was mostly applied for ‘surprise (medical) bill(ing)’.16,25,28 -30,32,33,35,49,56,57,69,71,74

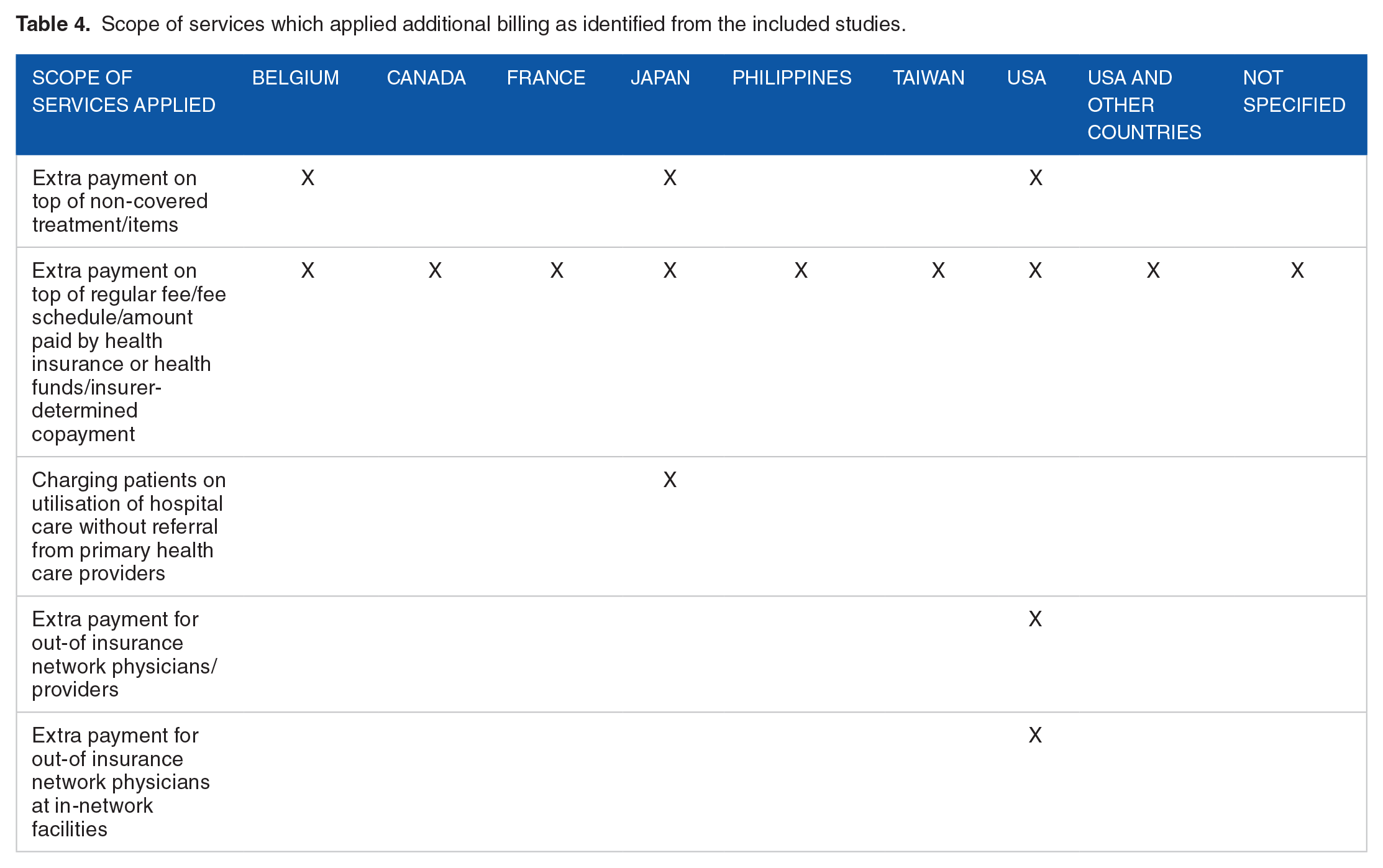

The differences between ‘balance bill(ing)’ and ‘surprise (medical) bill(ing)’ were emphasised in some papers.22,49,60,72 The surprise billing in these studies was the situation that patients received an extra bill for services provided by a physician at in-network facility, but the concepts of balance billing were not similar. Kelly, 22 Chhabra et al, 49 and Molyneux 72 referred the balance billing as an unavoidable payment for services provided by out-of-network physicians not covered by the health insurance plan, while Fuse Brown 60 defined a broader view of balance billing that was the remaining balance between the amount paid by the health insurance company and total hospital charges. Another term, ‘billing practice’, applied in the US, was an unexpected extra payment for the services provided by out-of-network physicians. 71 Table 4 summarises the key concepts of balance billing from the selected studies.

Scope of services which applied additional billing as identified from the included studies.

Balance billing in practice: What services incurred additional bills

Totally, 49 studies revealed that insured patients in the United States, Belgium, Japan, and Taiwan were charged with an additional bill for the broad range of un-covered healthcare services; for instance, services for emergency conditions, surgery and its related services, specialist consultant, medical investigation, medicines, and medical devices or premium healthcare services.

Patients who suffered from emergency conditions and required surgical procedures, to their surprises, had been frequently reported of balance billing payments. There were 20 (out of total 78) articles from the US that reported additional bills to patients visiting emergency department.15,31,33,36,39,40,45 -47,50,56,58,60,66,68,72 -74,76,81 Although insured patients visited the in-network facilities, their insurance did not always fully reimburse services provided by out-of-network emergency physicians.15,45,58,60,66 In addition, ambulance service, either vehicles or air lift, was another cause of additional billing to patients with emergency conditions.15,44,45,48,56,60,63,67,69,72,86 Surgery,32,49 -51,57 -60,63,67,69,72,86 anaesthesia-related services,27,50,56,60,66,69,72,76,79 and medical intervention were the second most common cause of balance billing.46,52,95,96

Balance billing on elective and ambulatory surgical procedures was commonly practiced in the US.46,49,51,57,63,67,86 These interventions included cataract surgery, total joint arthroplasty, arthroscopy, colonoscopy, and upper gastrointestinal procedures. Charge from surgical assistants became a common surprise billing for American surgical patients.50,60,69,72 Japanese insurance did not fully cover some high-tech procedures which were under trials or those not included in the fee schedule lists; thus, patients were balance billed.95,96

In the US, Belgium, Japan, and Taiwan, medical investigations, medicines, medical devices, specialist services, and hospitalisation were extra-billed for various purposes. For medical investigation, 12 articles from the US reported the additional bill for laboratory,52,81,106 radiology50,53,56,60,72,76,79,82 and pathological diagnosis.56,60,72,76,84 In terms of medicines and medical devices, some studies revealed their additional payments for chemotherapy, specialist medicines, and durable devices in the US, 52 while Japanese and Taiwanese patients paid for new medicines or medicines under trial, and medical devices not listed in the unified benefit package.96,105 Specialist services in the US, for instance, psychiatrists, gynaecologists, otolaryngologists or hospitalists also enforced additional payment.37 -39,41,52,79 In addition, Japanese insurance applied copayment on hospital consultation fees as a measure to control the overuse of ambulatory services in large hospitals. 96 Inpatients from Belgium and USA copaid for their hospitalisation,47,73,97 while Japanese insurance charged patients with long hospital stay beyond 180 days. 96 In Taiwan, Japan, and Belgium, additional payment also applied for premium hospital services including extra-charge rooms or private rooms95,96,98,105 or fast tract appointments. 96

On provider perspective, additional billing was the measure for financial recovery to maintain hospital services as insurance agencies neither cover their full cost and allow margin; nor the uncovered services.20,22,24

Regulations of additional billings

Totally, 47 publications showed that additionally billing was legal; with a wide range of regulatory measures in controlling balance bills in 9 countries. Additional billing was legally prohibited in the Canadian and Philippines public health insurance systems.90,92,104 On the contrary, balance billing for certain services was legal in Australia 99 and Germany 100 while some degrees of regulations on balance billing were reported for Japan, France, Taiwan, Belgium, and the US governments.

In Japan, balance billing for services listed and provision of unlisted services in the fee schedule was strictly prohibited; however, extra billing for uncovered services was allowed in a few cases44,94,95 which were similar to Taiwan where additional billing for special medical equipment was allowed. 105 In France, balance billing was allowed if it was agreed in the contractual arrangement between physicians and regulator. 103 A group of physicians, called ‘sector 2’, was allowed to set their own physician fee with a penalty for excessive extra billing which was defined as the payment beyond 150% of reference fee, 90 while the ‘sector 1’ physicians, who earned benefit from the tax deduction, were not allowed to balance bill. 103 The regulation of the additional bills for the specific room types in Belgium could benefit to the weaker socio-economic patients to access common wards for needed inpatient services97,98,101 but did not wish to pay extra.

Impacts of additional billings on insured patients

Our analysis found several negative consequences caused by additional billings to the insured patients and health systems. To individuals, additional billings incurred financial hardship, reduced access to needed care, and eroded trust between people and medical institutions.

Evidence from the US indicated that the out-of-network billing caused catastrophic debts to insured patients; reduced living standard of the patients and their families including cutting spending on food and essential consumption; forced patients to take on the second job; or even pushed them into asset loss and bankruptcy.18,19,21,31,75 These bills were frequently reported from the use of emergency services15,21,26 and specialised services49,58,75 not available in network which often required ambulance transfers; or services were provided by out-of-network physicians. In such unexpected, emergency, or life-threatening circumstances, patients or relatives usually had limited capacity to avoid out-of-network treatment,15,21,48,58 let alone their abilities to negotiate the expense incurred.55,65,71 In the US, out-of-network billing happened more frequently among for-profit hospitals. 66

The impacts of balance billing varied across countries. Some positive consequences of balance billing were reported by studies in the United States. Balance billing provided patients with choices of their preferred health services. 15 A study in Belgium suggested extra billing could increase quality of care which otherwise might be reduced when extra billing was prohibited. 97 The balance billing policy was applied as an instrument to contain public health spending 101 and recover the cost of providers.75,102

However, the increased patients’ choices from balance billing could lead to a 2-tier system, as only patients who could afford balance billing had access out-of-network services. As a result, inequitable access across income groups was reported by some studies, 101 while financial hardship to patients became the common impact of the additional bills.15,19,21,25,31,43,48,49,57,66,72,75,85,97,100 -102,105

Balance billing reduced access to care for patients who could not afford to pay. 101 Forgone care and limited access to health services due to extra bills had been reported by studies in Canada, France, and the US especially when the amount of fee was large.58,66,91,103 In Canada, the extra fees were the cause of unmet needs for the services outside the insurance benefits package. 91 Forego treatment was twice for people without private health insurance or top-up health insurance plans in France. Also, the amount of balance billing in France which had increased by double between 1990 and 2010 101 had resulted in limited access to services provided by specialists. 103 In the US, balance billing for out-of-network billing particularly the air ambulance transfers was either a major barrier in access to these emergencies and life threatening services for those who could not pay, or financial hardship for those who paid.58,66 In 2017, 69% of the extra billings were for transports to use services provided by out-of-network facilities. 66 Unexpected billing also lowered patient satisfaction, created distrust in physicians and hospitals,21,59 increased lawsuits and conflicts between patients and providers.59,65 Other impacts of the additional bills such as price discrimination by different physicians, 101 lack of billing transparency,71,102 untimely access to health services, 66 inequitable power of negotiation between patients and healthcare providers, 71 incentive for physicians to provide services in out-of-network health facilities, 49 and increase health spending 100 are shown in Table 5.

Positive and negative impacts of the additional bills, synthesis from literatures.

Negative consequence went beyond patients to broader healthcare systems. It undermined universality by disproportionately affecting poorer population. They experienced limited access to physicians and sometimes had to forego treatment because they were unable to afford the extra bills.91,101 In addition, such billing practice compromised transparency and fairness of medical fee. Magnitude of billing amount varied significantly across provider networks36,63,97 leading to distorted pricing and uncertainty of cost-sharing level.21,102 Out-of-network services appeared to be more costly and prices were rising over times.15,26,43,57 An oligopolistic service with limited supply of providers such as air ambulances had been a significant concern as these providers lacked incentives to become in-network resulting in aggressive price increase.43,58,66,85 There was a lack of standardised, transparent, and fair price list to serve as a reference for dispute settlement.21,31

Nevertheless, prohibiting balance billing could lead to some undesirable health care providers’ behaviour particularly reduced quantity and quality of care 100 resulting in the overcrowded emergency departments as speciality physicians might no longer accept the emergency calls that cannot be extra-billed. 24 This could result in limited choices for patients. 100

Measures to address detrimental effects of additional billings

This review identified 9 measures applied to mitigate negative effects from unfavourable billing practices including their limitations. First, governments imposed a total ban through legislative (federal and state) and administrative measures. It prevented all forms of additional billings to patients beyond what was previously agreed on cost-sharing rates (ie, deductibles or coinsurance); this prevented insured patients from unexpected financial burdens and catastrophe.23,24,69 Prohibition against additional bills might necessitate larger government budget to maintain good quality service.19,22 In Canada, government budgetary constraints was the main counterargument against banning because fiscal space did not allow full funding for all needed healthcare . 91 Studies in the US reported that overall patient welfare would be limited if balance billing was prohibited. 23 The situation of already beleaguered emergency departments would be even worse from overcrowding and long waiting time if out-of-network physicians refused to lend a hand in times of need when they felt underpaid.12,24

Second, the governments legislated measures to control prices of out-of-network services.16,18,25 In the US, over half of states implemented regulations to resolve surprise billing.58,66 A study in Florida found that the law successfully reduced price of out-of-network anaesthesiologists with positive effects to in-network services. It benefited more to fully-insured plans than self-funded plans. 16 However, concern was raise that this would cause a premium rise in subsequent years. 79

Third, an annual per capita ceiling for balance billing was introduced. 42 It had resulted in a reduction of household’s out-of-pocket spending on medicines without observed declines in service utilisation among Medicare beneficiaries during 1984 to 1996 in the US. 42

Fourth, developing fair billing methodologies to enhance price transparency of out-of-network payment rates through publicly available information, could be used to enhance fairness of payments between insurers and providers.12,22,31,84 The US had been facing a challenge to agree on service reimbursement rates between insurers and providers.36,51,79 An attempt to establish a credible data source for fair reimbursement rates was used by the New York state.12,84 Alternatively, such billing database might be used for benchmarking of which effects varied across markets depending on magnitude of difference between price and the benchmark.63,82 It should be mindful that insurers and providers might altogether be reluctant to share data 80 and benchmarking value could disrupt good-faith negotiations between insurers and providers. 82

Fifth, supplementary insurance could be used to cover extra fees. In Belgium, both sickness funds and private insurers offered supplementary insurance to cover the extra costs beyond the usual agreed co payments. However, this posed an additional concern over universality since not everyone could afford these additional protection. 98

Sixth, seeking informed financial consent from patients before providing out-of-network care could be another solution though difficulties in practice especially patients under life-threatening conditions. 46 In California, cost-sharing for all non-emergency physician services including out-of-network physicians at in-network facilities was restricted unless patient provided financial consent for additional billing 24-hour prior to service provisions. 38

Seventh, establishing a dispute resolution platform and mechanisms where patients and providers could negotiate offered another solution in promoting transparency, patient protection, good collaboration. 82 When the payment standard was not available, dispute resolutions operated in the US would be a platform for health insurance companies and providers to set the acceptable fee for out-of-network services.19,25 Unsuccessful dispute settlement could be deferred to an independent mediator to make a final decision on rates. 66

Eighth, bundled payment method combining hospital and professional fees was proposed as an effective solution to remove an incentive to balance bill rooted from the fee-for-service system.17,50,51 This proposal, however, was challenged by the fact that providers could end up refusing to join the service networks. 17

Ninth, a reform towards a single payer system in which all providers entered into contractual agreement of service provision would eliminate out-of-network surprise billing effectively. This means, de facto, there would be no out-of-network service or provider. 19

Common challenges in formulating policies to resolve additional billings

There were a few common challenges identified from the included literatures. An attempt to legislate against additional billings could be interfered and retarded by promotional campaigns of vested interest groups, policy lobbying, and regulatory capture as seen in the case of the US’ No Surprise Act.60,66,69

In decentralised or multisectoral contexts, there were required policy coherence to ensure universality of health safety net to every citizen. For instance, in the US before the No Surprise Act was passed in 2020, there was no federal law despite various state legislations.32,72,73 State protection did not cover people under employer-based insurance.21,75 Notwithstanding different degrees of effectiveness across all government measures, a common challenge was a limited ability to regulate private insurers and private service provision. 58 Evidence shows that restriction of private insurance was less comprehensive than public insurance. 15

Discussion

Balance billing could lead to increase the financial burdens and limited access to health services of households. It is the result of financial and service coverage decisions. Although balance billing is designed to discourage unnecessary use of services by patients; the imperfect nature of healthcare market, especially asymmetry of information where healthcare professionals have more technical information, hampers achievement of this goal. Over treatment and prescription is not uncommon, especially when professionals’ incomes are determined by frequency and volume of treatment such as fee-for-service through ‘supplier induced demand’. 107

A study among American doctors reported that 20.6% of overall medical care was unnecessary, caused by fear of malpractice, patient pressure or request, and difficulty accessing medical records, suggesting that de-emphasising fee-for-service physician compensation would impact on reduction health care use and costs of health services. 108 On the contrary, capitation payment where reimbursement was unlinked from volume of services provided, could result in under provision of services or lower quality. 109

This scoping review of 94 studies including research, reviews, and non-research papers that met the eligible criteria identifies basic knowledge of additional billing covering terms used, definitions and scopes, effects, regulations, and challenges. Balance billing had been practiced in various countries with different concepts and interpretations. Most literatures were from the United States where the health system relied mostly on private health insurance. 110

Our findings reveal that balance billing commonly referred to the extra payment by insured patients on top of the amount paid by health insurance plans. The concept covered the unavoidable payment that patients needed to pay when they received services provided by out-of-network physicians or providers; or used of services in the network but provided by physicians from out-of-network facilities. This problem was frequently raised by the US health system because of the skinny network 19 which means the healthcare facilities in the network cannot provide all services needed by the patients and shallow benefit package giving large room for non-covered services.

This study acknowledges the fact that health insurance funds can neither reimburse the full cost of services nor cover every service for everyone except with a very high premium which can be unaffordable by people who needs the protections from the insurance policy. However, the balance billing posed financial risk when patients faced balance billing even they used services from in-network hospitals, but these treatments were provided by out-of-network clinicians. Meanwhile, the surprise billing, another general term used in the US, created problems to accident or emergency cases35,75 as the patients had no choice and needed to use the most nearby services which were out-of-network facilities. The harmful effects of the surprise medical bills were confirmed by a study using a nationally representative sample of medical claims for obstetric services in the United States. 28 The results showed that patients possibly switched hospital for the second delivery after receiving their unexpected bills even the services provided by the in-network hospital in their first delivery. A review literature by Long et al 111 also reported that patients were vulnerable to experiencing surprise bills in their in-network facilities for hand surgery due to the multidisciplinary nature of hand care, the speciality emergency department, and other related required services. The unanticipated medical bills not only became financially devastating but also reduced patients’ trust and satisfaction with their physicians.

The tremendous negative impacts of the additional payments from this review, notably financial burdens and unmet needs as reported by Canada, France and the US,58,66,91,103 warrants restrictions or total ban, but measures were both supported and opposed by different stakeholders. To achieve UHC goals, balance billings require appropriate and effective regulation to protect financial hardship and minimise foregone care.

Balance billing and 2 related terms including ‘extra billing’ and ‘surprise billing’ are a part of out-of-pocket (OOP) payment. The higher could lead to catastrophic health spending, defined as the household health spending being greater than 10% (or 25% depending on the threshold applied in the calculation) of the total household consumption expenditure (or income), 112 and impoverishment which means additional households pushed to falling below the poverty line after paying the medical bills. 113 The reported health spending data of countries listed by the included studies from the World Health Organization reflects that current health expenditure (CHE) as a proportion of the Gross Domestic Product (GDP) in the United States (17%) was the highest share among all high-income countries including Belgium, Canada, France and Japan. These countries had policies to limit balance billing90,92,96,103 when it was allowed for certain conditions or healthcare providers. However, balance billing in the US was only legally prohibited or regulated in emergency departments or in-network hospitals in 21 States and the protections did not safeguard other services from balance billing; only 6 states – California, Connecticut, Florida, Illinois, Maryland and New York provided a comprehensive approach to safeguarding patients. 21

The unaffordable price from the balance billing could hinder access to health services resulting in unmet health needs. Despite a not high percentage of OOP (11% of CHE) and quite a low level of catastrophic health spending which less than 1% of total households in America in 2019 (25% threshold), 114 the evidence shows that the adjusted proportion of insured adults who are unable to see a physician due to the cost of healthcare rose by 3.6 percentage points between 1998 and 2017 (7.1%-11%, unadjusted) 115 In addition, among members of Organization for Economic Co-operation and Development, the United States reported the highest share of people, 18% of population skipped prescribed medicine because of the unaffordable cost which was 11% points higher than 7.1% average of OECD countries reported unmet health need in 2016 (or nearest year); 43% of the low-income adults in the US also experienced the unmet need due to the cost of health services. 116

Due to the adverse consequences of the additional bills, regulating additional payment should be implemented to protect the right to health of people. However, on the flip side from the provider’s perspective, controlling extra payments without government stepping in to provide significant budget subsidies, could lead to overcrowding health facilities, particularly in the emergency departments,12,24 and affect the quality of care. 100 Hence, adequate payment which recovers cost of provision can effectively ban additional billing. Extension of the provider network will prevent extra-billing from out-of-network facilities and physicians. Comprehensive benefit package will minimise the un-covered services.

The challenges to the disagreement on the reimbursement rate between insurers and health facilities can be resolved by reliable costing data, 117 while the concern on the budgetary constraints of the government to absorb the healthcare cost, if the additional bills are limited, should be addressed by applying the adequate payment rates which reflect providers’ cost. Some countries can control their health budget by applying blended payment methods for example China 118 and Thailand. 119

Restricting additional billing becomes more complex especially in a laissez-fair capitalist system and the context of private insurance dominates healthcare financing systems, and private for-profit providers dominate healthcare market.

To address balance billing, interventions need to address the insurance market which, from this review, seems to be the major root cause of balance billing. This requires transparency of premium rates collected from consumers, medical loss ratio, fair payment to healthcare providers, and profit margin of insurance firms. An Act of Congress requested insurance companies to spend at least 85% of premiums on medical claims and efforts to improve the quality of care and allow 15% administration, marketing, and profits.120,121 UnitedHealth, one of the largest US insurance companies, offered more than US$5 billion dividends to its shareholders. 122 Fair payment to providers reflecting their cost and margin can significantly minimise the balance billing. Appropriate profit margin allows benefit package more comprehensive which minimises non-covered services. Expansion of provider network will minimise balance billing from out-of-network providers. Interventions addressing healthcare providers, mostly applied by the included studies in this review, would not be effective unless the reimbursement rate reflect their cost and certain margin.

This review has some limitations. First, it is possible that some relevant studies were missed out because only English publication covered by the 4 databases were included in the analysis. The grey literature resources were not counted in this review.

Second, the key domain was developed from 3 specific terms. Although they were commonly used for naming the additional billing to insured people, there might be other specialised terms than those included in the searching strategy.

Third, our findings are largely influenced by studies from the US health systems and financing contexts. The US literatures consist of 83% out of the total 94 included studies. Therefore, interpretation of balance billing practice needs to be careful of this influence.

Fourth, we acknowledge that the root cause, effects, and regulations of additional billing are subject to local settings of each study such as social development, health systems ideologies, sources of finance, provider payment mechanisms, degree of public-private mix, and healthcare seeking behaviour. Further, the study objectives and corresponding search strategy yielded the results which did not allow us to assess the impacts of balance billing. In addition, background information such as financing sources and provider payment methods were not provided in the included papers. Also, the evidence is inadequate to indentify the size of balance billing relative to household incomes and its catastrophic impacts; and the differential impacts across rich and poor countries. Future research should focus on effects of balance billing in different country context.

Last, there might be some residual non-uniformity during data extraction due to multiple researchers’ extraction. The team tried to triangulate the extracted data with cross-checking by at least 2 researchers and revisiting the original paper when necessary.

Conclusion

Understanding the comprehensive knowledge of the on-top healthcare costs paid by insured patients is important to address the negative impacts of these practices which hamper achievement of financial protection goals of universal health coverage. Despite the different terms used, their consequences directly increased financial barrier, reduced access to health services or increase the proportion of population who have high out-of-pocket health expenditure. Consequently, the government in some countries introduced various measures from very strict to lenient measures to limit and control billing practices. However, the additional billing was commonly operated in some settings; those that limited extra payment for the medical bills still experienced a set of challenges such as law enforcement, resistance from the stakeholders, and limited resources to provide comprehensive benefit package. Examining the complex determinants, profiles and impacts of extra payment practices would unfold the knowledge gaps and inform the policymakers to discourage extra billings, increase access, and provide financial risk protection to all.

Supplemental Material

sj-docx-1-his-10.1177_11786329231178766 – Supplemental material for Definition, Practice, Regulations, and Effects of Balance Billing: A Scoping Review

Supplemental material, sj-docx-1-his-10.1177_11786329231178766 for Definition, Practice, Regulations, and Effects of Balance Billing: A Scoping Review by Shaheda Viriyathorn, Woranan Witthayapipopsakul, Anond Kulthanmanusorn, Salisa Rittimanomai, Sarayuth Khuntha, Walaiporn Patcharanarumol and Viroj Tangcharoensathien in Health Services Insights

Supplemental Material

sj-docx-2-his-10.1177_11786329231178766 – Supplemental material for Definition, Practice, Regulations, and Effects of Balance Billing: A Scoping Review

Supplemental material, sj-docx-2-his-10.1177_11786329231178766 for Definition, Practice, Regulations, and Effects of Balance Billing: A Scoping Review by Shaheda Viriyathorn, Woranan Witthayapipopsakul, Anond Kulthanmanusorn, Salisa Rittimanomai, Sarayuth Khuntha, Walaiporn Patcharanarumol and Viroj Tangcharoensathien in Health Services Insights

Footnotes

Funding:

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the World Health Organization Centre for Health Development.

Declaration of Conflicting Interests:

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Author Contributions

VT, WP, WW and SV developed the conceptual framework. SV and WW designed a searching strategy. The screening process was carried out by all authors. SV, WW and AK synthesised findings. SV, WW, AK and SR wrote the first draft of the manuscript. VT edited and revised the draft. All authors contributed to approving the final manuscript.

Ethics Approval

Not applicable

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.