Abstract

The study aimed to estimate the cost for developing and implementing 2 smoking cessation service delivery models that were evaluated in a 2-arm cluster randomized trial in Commune Health Centers (CHCs) in Vietnam. In the first model (4As) CHC providers were trained to ask about tobacco use, advise smokers to quit, assess readiness to quit, and assist with brief counseling. The second model included the 4As plus a referral to Village Health Workers (VHWs) who were trained to provide multisession home-based counseling (4As + R). An activity-based ingredients (ABC-I) costing approach with a healthcare provider perspective was applied to collect the costs for each intervention model. Opportunity costs were excluded. Costs during preparation and implementation phase were estimated. Sensitivity analysis of the cost per smoker with the included intervention’ activities were conducted. The cost per facility-based counseling session ranged from USD 9 to USD 11. Cost per home-based counseling session at 4As + R model was USD 4. The non-delivery cost attributed to supportive activities (eg, Monitoring, Logistic, Research, General training) was USD 107 per counseling session. Cost per smoker ranged from USD 6 to USD 451. The study analyzed and compared cost of implementing and scaling community-based smoking cessation service models in Vietnam.

Background

Tobacco use remains a major cause of the growing global epidemic of noncommunicable diseases.1,2 In 2010, the prevalence of tobacco smoking among adult males (aged 15 and older) remained high in Vietnam (56.1%).

3

In that same year, the Vietnamese government passed the

Methods

This paper presents costing analyses for interventions under the VQUIT’ programs. The data were managed in an Excel spreadsheet, and the analysis was carried out using Stata version 12. All costs were presented in US dollar (exchange rate as 1 USD = 22 000 Vietnam dong), and were adjusted to 2020 price using the Vietnamese Consumer Price Index (CPI) (www.gso.gov.vn). 14

The VQUIT program

From 2013 to 2018, a NIH-funded 2-arm cluster randomized controlled trial, Vietnam Quits Tobacco (VQUIT), was conducted in 26 CHCs located in Thai Nguyen Province, a rural area in the northern midland and mountainous region of Vietnam to investigate the feasibility of 2 smoking cessation services models “4As” and “4As + R”. The intervention is described in detail in previous publications.13,15 VQUIT compared 2 intervention models for increasing the delivery of evidence-based tobacco cessation services at the commune level. In the first model, the 4As, CHC health care providers attended a 2-day training on how to screen patients for tobacco use (Ask), offer advice to quit (Advise), assess readiness to quit (Assess), and offer brief counseling (Assist). The second model, 4As + R, added a system to Refer smokers to VHWs who received 4 days of training on how to offer 3 sessions of home-based cessation counseling. CHC patients who were identified as tobacco users were therefore offered either provider-delivered facility-based brief counseling (4As) or brief counseling plus more intensive home-based counseling delivered by VHWs (4As + R).

Data collection

The VQUIT program randomized 26 study sites into 3 waves; the first wave included 8 sites, the second 10, and the third 8. The delivery of services at both 4As and 4As + R models followed a standard of operation designed from VQUIT program which allowed us to shorten the cost data collection period within the first wave of the trial, from January 2014 to September 2016. The cost reported in this paper then were possibly represent the cost for other waves of the VQUIT program. During this period, 8 communes were randomized into 1 of 2 study arms: the 4As or 4As + R model. The cost data were collected from 2 sources: VQUIT program’s financial reports and interviews with relevant staffs, such as VQUIT program’s researchers, CHC staff, and VHWs. Relevant data were extracted from financial reports by the authors. Research team’s observations and interviews were conducted to collect additional information that were unavailable in financial reports and to validate the extracted data from these reports.

Costing approach

In this study, a healthcare provider perspective was applied to capture fiscal costs incurred in 2 fiscal years 2014-2015 and 2015-2016 during the first wave of the VQUIT program. This cost perspective was of both public healthcare providers’ (from provincial, district, and commune level) and of non-government providers’ (from the VQUIT program). Costs incurred by tobacco users were excluded. An activity-based ingredients (ABC-I) costing approach was adopted to capture the implementation costs of the 4As and 4As + R models. 16 First, all activities related to the VQUIT program during the first wave were listed and categorized into 5 groups as follow: (1) smoking cessation services, (2) training for care providers, (3) research, (4) monitoring, and (5) logistic and administration. Next, the cost of each activity was estimated using the ABC-I costing method, identifying the needed resources for the mentioned activities. We identified 6 categories of cost ingredients foreach activity that included: personnel, travel, material for Information, Education & Communication (IEC), office materials, operation and other recurrent expenses, and building and equipment expenses.

Measures

In this costing analysis, the VQUIT program’s 5 activity costs were divided into Direct and Indirect categories and by implementation phase (eg, start-up vs implementation). The cost ingredients were also classified to either variable or fixed costs. Definitions of these cost categories (direct vs indirect; start-up vs implementation, variable vs fixed cost) followed the World Health Organization’ guidance in estimating the cost of primary healthcare programs. 17

Activity groups

Direct costs can be defined as the costs that are directly involving in the services delivery process, 16 here are the cost of consultation for smoking cessation service to smoker and essential training for CHCs’ staff. Indirect costs, on the other hand, would be the costs that incurred during the services implementation but are not required to involve directly in the services delivery. All activities were categorized into 5 groups of direct and indirect activities as below.

Phases of implementation

Each activity was defined as occurring in either start-up or implementation phase. 18 The start-up phase (for the fiscal year of 2014) captured activities that required to establish the intervention and happened before the first service delivery (eg, development of curriculum and educational materials). The implementation phase (starting from fiscal year 2015) included activities and cost associated of running the program (eg, training for staffs and the delivery of counseling services).

Cost ingredients

Six cost ingredients adopted to identify the resources needed for each activity, were grouped into either variable or fixed costs. Variable costs, which would depend on the volume of delivered services, were personnel, travel, IEC materials, office materials, and operation and recurrent costs. Fixed costs, which would not depend on the volume of delivered services, were costs for building and equipment.

Analysis strategy

Total cost of the VQUIT project were annualized and unit costs including either cost per service or cost per fully intervened smoker were estimated. Difference scenarios of resources used were used to analyse the sensitivity of the cost per fully intervened smoker.

Annualization process

There were 2 part of the annualization process, the first one was to annualize the value of assets and the second one was to annualize the use of activities which were useful for long-term. First, assets (eg, building, furniture, equipment) were annualized at the item’s useful life-years (with 33 years for building and 10 years for equipment, according to Vietnam’s Ministry of Finance). Purchasing prices and/or current replacement prices were used for estimating annualization. Second, cost for activities which were useful for more than 1-year uses was also annualized. Research (ie, developing protocol/questionnaires/guidelines) and intervention preparation activities (ie, set up tobacco cessation counseling service at CHCs) costs that required across all 3 waves are annualized over a 3-year period which was the length of the study.

Shared cost allocation

Along with costs attributed directly to either the 4As or 4As + R model, the shared costs of both models were identified (eg, meetings, technical supports, supervising activities, etc.). These shared costs were allocated to each model using the proportion of the actual number of smokers that received the intervention. In the scope this study, the proportion of services delivered at each arm was used to allocating the shared costs. Particularly, the shared costs were allocated at 13.7% to 344 counseling sessions in the 4As model, and 86.3% of shared costs were allocated to 540 facility-based and 1619 home-based counseling sessions (a total of 2158 sessions) in the 4As + R model.

Unit cost calculation

The cost per counseling sessions was estimated separately for each intervention model. The cost per facility-based counseling session and cost per home-based session were calculated by dividing the total cost by the volume of delivered counseling sessions reported during the first wave of VQUIT program. The activity-based costing allowed to estimate total cost concluded of directly allocating cost to either facility-based or home-based counseling session and the shared cost allocating to each type of service. The cost per smoker for each model was calculated by multiplying the cost per session by the number of sessions per smoker, here are 01 facility-based session for smoker at both models and the addition of 03 home-based session for the 4As + R in each model.

Sensitivity analysis

A 1-way sensitivity analysis was conducted to assess how the cost per smoker differed by different scenarios. Three different scenarios were developed to provide insights about how program costs would vary depending on the range of activities included. Figure 1 summarises what cost activities were included in each scenario for the sensitivity analysis.

Costs included by scenarios for sensitivity analysis.

Scenario 1

This scenario included cost estimates for all 5 activity groups: costs associated with tobacco cessation services (training and counseling); research activities; logistics and administration, and monitoring. This scenario represents the potential cost to the national health care system of implementing, administering, and monitoring and evaluating the program.

Scenario 2

In this scenario, “Research” activity costs were excluded to represent the costs for replicating the intervention (ie, tobacco cessation services) when also including administration and monitoring costs.

Scenario 3

This scenario included only the costs of delivering the intervention: (1) smoking cessation-counseling services (facility-based counseling session and VHW-delivered sessions) and (2) training (for facility staff and VHWs). This third scenario included only costs that were assumed to be necessary to sustain the intervention at the primary care system level.

Results

Table 1 shows costs during the start-up phase (September 2014-August 2015) and the 12-month implementation phase of the VQUIT program (September 2015-September 2016). The total cost of the VQUIT program for the 2 fiscal years 2014-2015 and 2015-2016 was USD 314 691. The allocation of costs between start-up and implementation phases were 64.32% and 35.68%, respectively. “Research” activities accounted for the largest share of the total expense at 64.88%, followed by costs of logistics activities at 18.07% of the total cost, and of smoking cessation services at 9.79%.

Costs by study phases for first wave of VQUIT program.

Fiscal year captured in the Start-up phase was from September 2014 to August 2015 and was from September 2015 to September 2016 for the Implementation phase.

Costs are presented in 2020 price.

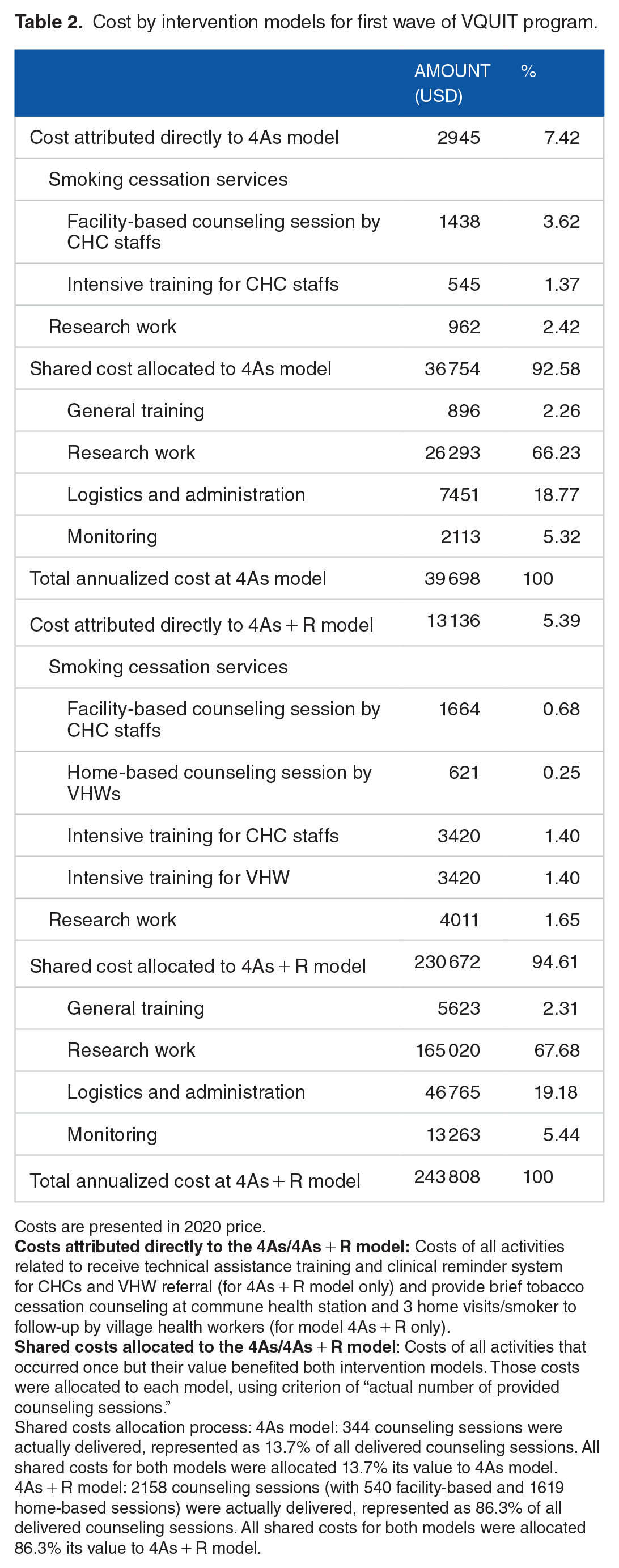

Table 2 shows the costs attributed to each intervention model, the 4As and 4As + R. A total of 2502 counseling sessions were delivered by the study sites during the implementation phase. The 4As CHCs provided 344 sessions of facility-based counseling (accounting for 13.7% of all delivered counseling sessions), and the 4As + R CHCs provided 2159 sessions of facility-based and home-based counseling (accounted for 86.3% of all delivered counseling sessions). The shared costs were allocated based on these proportions. This resulted in a total annualized cost of the 4As model of USD 39 698 for delivering 344 facility-based counseling sessions, and the 4As + R model of USD 243 808 for delivering 540 facility-based and 1619 home-based counseling sessions.

Cost by intervention models for first wave of VQUIT program.

Costs are presented in 2020 price.

Shared costs allocation process: 4As model: 344 counseling sessions were actually delivered, represented as 13.7% of all delivered counseling sessions. All shared costs for both models were allocated 13.7% its value to 4As model.

4As + R model: 2158 counseling sessions (with 540 facility-based and 1619 home-based sessions) were actually delivered, represented as 86.3% of all delivered counseling sessions. All shared costs for both models were allocated 86.3% its value to 4As + R model.

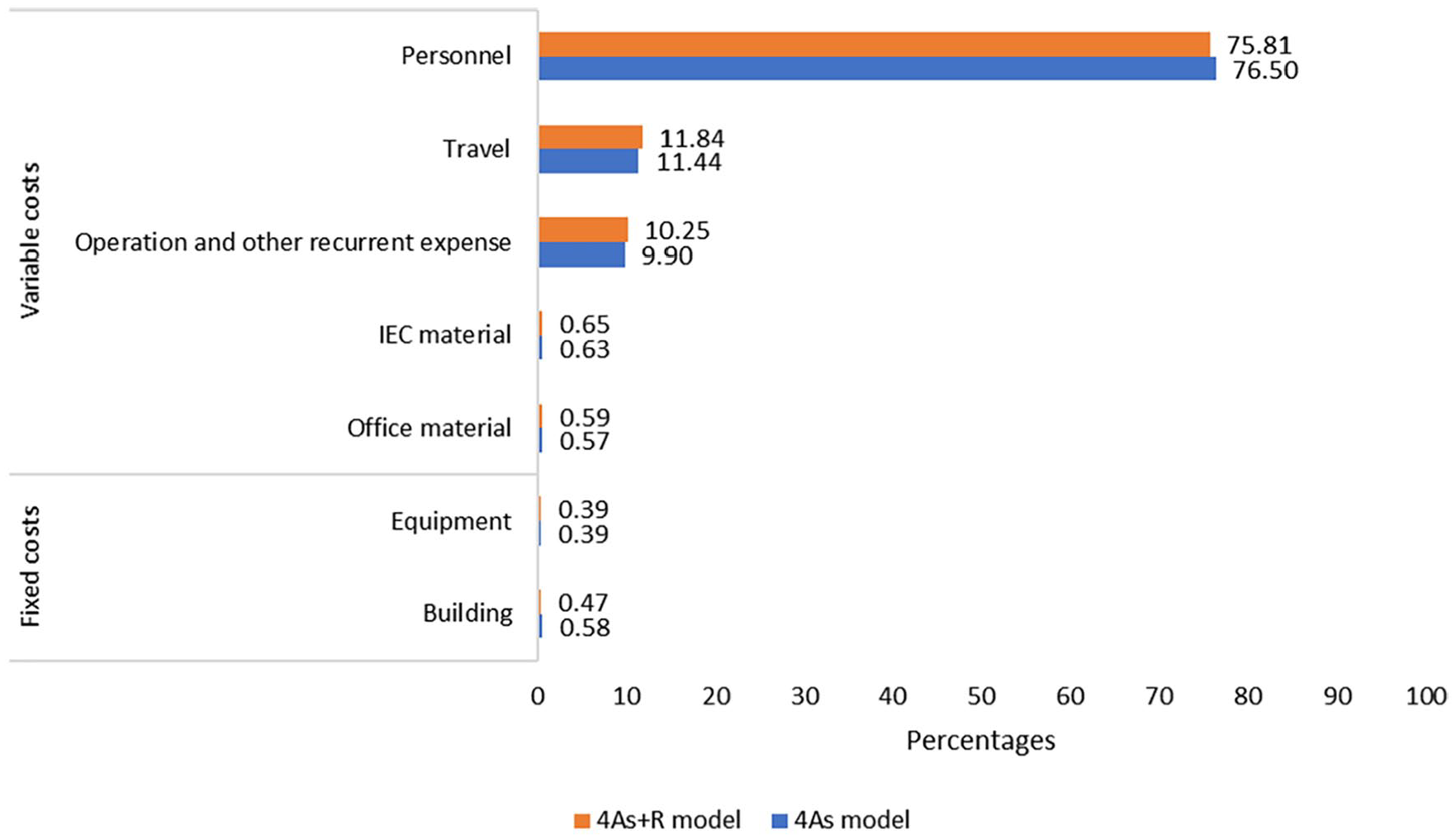

Figure 2 shows the overall cost of ingredients across all activities (eg, Research, Training) for each of the models. There was a similar pattern for these costs between the 2 intervention models. More than 75% of costs was for personnel, followed by about 11% for traveling, and about 10% for operation costs. The costs for IEC materials, office materials, building, and equipment were small, with each ingredient being less than 1% of the program’s costs. Moreover, variable costs accounted for about 99% of the total cost, and the rest were fixed costs.

Percentages of costs by ingredients for the first wave of VQUIT program.

Table 3 shows the unit cost per counseling session and per smoker for each model. The cost per facility-based counseling session was USD 9 and USD 11 for the 4As and 4As + R models, respectively. The cost per home-based counseling session of the 4As + R model was USD 4. Other non-delivery costs attributed to supportive activities (eg, Monitoring, Logistic, Research, General training) were estimated at USD 107 per session for both models. The cost per smoker in the 4As model (using 1 facility-based counseling session) was USD 116, and the cost per smoker in the 4As + R model (using 1 facility-based and 3 home-based counseling sessions) was USD 451.

Unit cost by intervention models for the first wave of VQUIT program (USD).

Costs are presented in 2020 price.

Figure 3 presents the sensitivity analysis of the cost per smoker using 3 different scenarios. The 4As model was less costly in all scenarios. For example, in scenario 1 (Full costs), cost per smoker in the 4As was USD 335 higher than the 4As + R model. Similarly, in Scenario 2, when research-related costs were excluded, the cost per smoker at 4As and 4As + R model, respectively, was USD 36 and USD 135, a difference of USD 99. The cost per smoker showed in Scenario 3 included only those costs associated with delivering cessation services and were USD 6 and USD 15 for 4As and 4As + R model, respectively. Details of the total cost and unit cost at different scenarios were in Supplemental Tables S2a and S3a.

Sensitivity analysis of the cost per smoker during the first wave of VQUIT program.

Discussions

This cost analysis provides additional knowledge on potential resources needed for tobacco cessation services at community level. This study provided the costs of 2 intervention models; 1 to improve facility-based provider-delivered tobacco dependence treatment, and a second model that added referral to a VHW for 3 follow-up counseling sessions. 11 Adding the VHW counseling component increased the cost of sustaining the delivery of tobacco use treatment from USD 6 for the facility-based provider counseling alone to USD 15. However, the addition of the VHW counseling doubled quit rates compared with provider counseling alone. 13 This is consistent with studies showing that multisession cessation counseling can increase quit rates beyond brief health care provider counseling and adds to literature demonstrating that the central role that trained VHWs can play in effectively delivering preventive care, including smoking cessation interventions.19-21 It is important to note that these costs represent scenario 3 and therefore do not include the full costs (ie, research, logistics, monitoring, training) required to establish and implement the program.

Our findings are consistent with pre-existing studies that investigated the cost per face-to-face counseling session done by healthcare staff.22,23 Comparing our findings a study conducted at rural managed care organizations in the United States in 2006, our costs per facility-based session was significantly lower (USD 6-USD 13), however, as for total intervention cost per smoker, our cost in Scenario 2 of 4As model was slightly lower, USD 36 to USD 42. 22 All the costs are converted to 2020 prices and the selected scenario seemed to similar to the compared study settings as they both demonstrated the costs related to the delivery the service. In another study conducted in the Netherlands, an even higher cost for consultation service per smoker was reported at USD 55 (converted to present price and Euro to USD).23,24 Similar tobacco cessation interventions in Germany and India found the full costs were USD 24 and USD 14, respectively12,19 (converted to 2020 price 25 ), which were also more costly than the cost of counseling sessions per smoker in Scenario 3 of the 4As + R model at USD 15, as we provided 2 sessions per smoker (1 facility-based and 1 home-based) and counseling sessions provided by VHWs were known to cost even less. Findings from a Bangladesh study found that the unit cost of a counseling session by VHWs was about USD 3, 26 which was similar to USD 2 per home-based counseling session in the 4As + R model shown in scenario 3 of the sensitivity analysis.

Vietnam launched a Quitline in 2015 that provides another resource for smokers to receive tobacco cessation counseling. However, the WHO guidelines recommend a multilevel approach to ensuring access to tobacco cessation treatment that includes integrating tobacco use treatment into primary care settings. With the advantage of lower personnel cost and proven effectiveness of integrating VHWs into the referral system, especially in rural and remoted settings,13,27 the 2 evaluated models (the 4As or 4As + R), if implemented widely, have the potential to build community-based capacity to promote smoking cessation, provide cessation services, and expand the access to tobacco use treatments in Vietnam.

Vietnam is now becoming a middle-income country, therefore, external financial support is likely to decline. The Ministry of Health (MOH) may need to plan for other sources of revenue (eg, fee based for counseling services) in order to sustain health promotion and diseases prevention programs like tobacco cessation. The current analyses, including different cost scenarios in the sensitivity analysis, offers local healthcare planners the full range of costs to consider when planning and budgeting community-level health care services and provide a possible roadmap to sustain such interventions in Vietnam. Specifically, the full cost estimated in scenario 1 can inform total financing needed to launch the VQUIT program (including research activities within the preparation phase). Similarly, costs summarized in scenario 2 provide a guide for financing implementation (mostly included activities in the implementation phase). Finally, the costs in scenario 3 provide information on the costs associated with sustaining the 2 different models for delivering cessation counseling services.

Regarding the applicability of these cost evidence, provinces in Vietnam may use such evidence to develop appropriate plan(s) for implementing community-based smoking cessation services. In addition, a brief cost effectiveness analysis between the implementation of intervention (either 4As or 4As + R) and standard of care had been conducted using the cost evidence in the present study and 10.5% and 25.7% of smoking abstinence rates from 4As and 4As + R model found from previous study, 13 respectively. The incremental cost effectiveness ration—ICER had been calculated as the ratio between difference in cost (intervention cost vs doing nothing—zero cost) and the difference in effectiveness (abstinence rates at post intervention vs percentage of natural quit smoking). Due to the lack of consistent information on the percentage of natural quit smoking, a sensitivity of ICER from both models and from 3 scenarios of cost had been done to solve the uncertainty (Supplemental Figure S3a). Overall, the investment on interventions at 4As + R model worth the money more than it was in the model 4As. Hence, provinces may also consider this factor when selecting an appropriate plan of implementing community-based smoking cessation services. There were several study limitations. The findings were estimated based on data from a study conducted in one province in the North of Vietnam and were estimated based on only the first wave of the intervention. In addition, some economic costs, such as voluntarily personnel cost, or cost of preventing related diseases due to smoking were not covered in this study. Nevertheless, results showed in this study were consistent with previous studies.12,27 Furthermore, evidence on long-term cost-effectiveness of the interventions in both models is still needed further research.

Conclusions

The findings offer the cost estimation for implementing 2 types of community-based smoking cessation services delivery in Vietnam and different scenario of cost included, providing supportive evidence to policymakers in developing smoking cessation programs in Vietnam.

Supplemental Material

sj-docx-1-his-10.1177_11786329211030932 – Supplemental material for Cost Analysis of Community-Based Smoking Cessation Services in Vietnam: A Cluster-Randomized Trial

Supplemental material, sj-docx-1-his-10.1177_11786329211030932 for Cost Analysis of Community-Based Smoking Cessation Services in Vietnam: A Cluster-Randomized Trial by Vu Quynh Mai, Hoang Van Minh, Nguyen Truong Nam, Hoang Thao Anh, Nguyen Minh Van, Nguyen Thi Trang and Donna Shelley in Health Services Insights

Footnotes

Acknowledgements

The research team in Hanoi University of Public Health has done the study with support from the Institute of Social and Medical Studies. We would like to thank both the researchers and financial staffs of the Institute of Social and Medical Studies for providing data and the local health staff in Thai Nguyen for data validation. There is no copyrighted material was used.

Funding:

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project is supported by National Cancer Institute [grant number R01CA175329-01], awarded to DS/NN.

Declaration of conflicting interests:

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Author Contributions

All authors have contributed equally to this work.

Research Ethics

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.