Abstract

This article examines the initial effect of Affordable Care Act (ACA) Health Insurance Marketplace (Exchange) insurance on access to care among employed beneficiaries in a highly populated US state. Does Exchange insurance lead to better/worse health care access for employed beneficiaries, compared with similar individuals covered through standard employer-sponsored insurance (ESI) coverage? This retrospective study uses data from the 2015 Ohio Medicaid Assessment Survey, a dual-frame and computer-assisted telephone survey administered by the Ohio Colleges of Medicine Graduate Resource Center, the Ohio Department of Medicaid, the Ohio Department of Health, and Ohio State University, in conjunction with RTI International. This study examines a sub-sample of employed adults (age 18-64) covered by either an Exchange plan or ESI, extracted from the full sample of n = 42 876. We use linear propensity score matching using Euclidean distance to balance treatment groups and logistic regression models to estimate the treatment effect of Exchange coverage on all outcome variables. McNemar tests, Rosenbaum sensitivity analysis, and Benjamini-Hochberg procedure adjustments are also conducted. Compared with ESI insurance, Exchange insurance has no significant effect on outcomes measuring either perceived access to care or, more specifically, perceived financial barriers to accessing care. Exchange plan viability remains a hot topic of debate across the United States, given the potential repeal of the individual mandate. We use risk-adjustment methods to demonstrate that Exchange plan beneficiaries do not experience worse access to care than ESI beneficiaries. That said, several key limitations are discussed.

Keywords

Introduction

In 2010, the Affordable Care Act (ACA) created the Health Insurance Marketplaces (also known as the Exchanges), thus establishing a new category of coverage to augment the non-group insurance market in the United States. The ACA Exchanges were operational in 2014, following the US Supreme Court’s June 2012 decision to uphold the constitutionality of the individual mandate in National Federation of Independent Business v. Sebelius, 567 U.S. 519. As of 2017, 34 states operate federally facilitated Exchanges, while there are also 12 state-based Exchanges and 5 state-based Exchanges on the federal platform. 1

The Exchanges allow individuals to compare and choose health insurance coverage options from an assortment of participating health plans. Notably, per ACA regulation, Exchange plans must be standardized as Qualified Health Plans (QHP). Each QHP must be licensed by the state in which it operates and provide essential health benefits, such as hospitalization, mental health services, prescription drugs, and pediatric services. The Exchanges also provide financial assistance via advance premium tax credit (APTC) and cost-sharing reduction (CSR) subsidies for individuals earning up to 400% of the federal poverty level (FPL) and 250% of the FPL, respectively. 2 In 2011, the Congressional Budget Office estimated that the APTC subsidies would help 20 million Americans afford health insurance. 3

Exchange enrollment has steadily increased over time. Across the United States, 12 216 003 individuals selected Exchange-based plans in 2017. 1 In Ohio, which operates a federally facilitated Exchange, Exchange enrollment increased from 173 000 enrollees in 2015 to 196 000 enrollees in 2017. 4 However, the ACA coverage mandate remains politically contentious, spurring efforts throughout 2017 to repeal the ACA in its entirety. Although ACA repeal efforts have been unsuccessful to date, the US Department of Health & Human Services (HHS) is acting to alter Exchange plan operations, for example, ruling that it would cease payment of Exchange CSR subsidies in October 2017. While the policy debate rages over the viability of the Exchanges, policymakers and health plans operating Exchange plans must continue to evaluate plan performance and meet the needs of their beneficiaries.

Background

As a result of the ACA Exchanges, non-group private insurance coverage grew from covering 3% of the total US population in 2013 to covering 7% of the population in 2016. 5 Historically, nearly three-quarters of the non-group insurance market are employed, and most non-group coverage enrollees are employed full-time. 6 In Ohio, a previous study shows that recent Exchange participants are mostly employed (68% of enrollees), almost exclusively White (89%), middle-aged (49 years old on average), and higher income earners than Medicaid expansion enrollees. 7

As policymakers increasingly turn to markets to deliver health insurance to the public, the efficacy of insurance competition will continue to be examined. Notably, despite ACA provisions to homogenize plan benefits and combat adverse selection in insurance markets, the Exchanges have demonstrated considerable volatility in pricing and plan offerings, 8 inciting concerns over selective contracting and provider network quality. In evaluating Massachusetts’ pioneer health insurance exchanges (Massachusetts Exchanges), a key model for the ACA Exchanges, Shepard 9 finds evidence of narrow networks arising from favorable selection: (a) Health plans excluded highly regarded academic hospitals from insurance beneficiaries’ provider networks, (b) reduced costs by routing patients to cheaper hospitals, and (c) limited access to top providers. Likewise, recent evidence from 8 states finds ACA Exchange plans pursued narrower hospital networks in an attempt to lower Exchange plan premiums, particularly among lowest- and second-lowest-price silver plans. 10

Narrower provider networks could become problematic for accessing care, as consumers often choose less generous coverage in Exchanges than in traditional employer-sponsored plans. 11 However, there is mixed evidence on how Exchange-based coverage affects access to care and health services utilization compared with standard employer-sponsored insurance (ESI). Evidence from the Massachusetts Exchanges suggests there are minor differences in access to care between Exchange coverage and private commercial insurance, although Exchange plan beneficiaries report greater difficulty identifying providers who accept their insurance. 12 More recently, Shih et al. 13 find no significant difference in radiation therapy use between post-breast-conserving-surgery patients with ACA Exchange coverage and comparable patients with employer-sponsored coverage.

Objective

The objective of this study is to examine the effect of Exchange insurance coverage on access to care among employed beneficiaries in Ohio, the United States’s seventh largest state by population. We identified our study cohort as employed Ohioans covered by either Exchange insurance or standard ESI. As such, this study is guided by a core causal question: Compared with standard ESI coverage, does Exchange insurance lead to better or worse health care access for employed Ohioans?

Hypotheses

This study considered 2 hypotheses in an attempt to answer our research question:

Methods

Data

The study used the 2015 Ohio Medicaid Assessment Survey (OMAS) public-use dataset. First implemented in 1998, the OMAS is a dual-frame (landline and cellular phone) and computer-assisted telephone survey administered by the Ohio Department of Medicaid, the Ohio Department of Health (ODH), the Ohio Colleges of Medicine Government Resource Center (GRC), the Ohio State University (OSU), and other State of Ohio health-associated agencies teamed with RTI International. Although the full OMAS data set contains responses from n = 42 876 individuals, to address our core causal question, we retrospectively examined a sub-sample of employed adults (age 18-64) enrolled in either Exchange coverage or ESI in 2015.

Data collection for the 2015 OMAS occurred from January to June 2015. Participants self-reported responses about insurance, health status, health care utilization, health behavior, and socioeconomic factors. The overall response rate for the 2015 OMAS was 24.1%. Notably, the dual-frame methodology allowed for more precise estimates for both younger and low-income households that increasingly rely solely on cell phone service. 7

Variables

Outcome variables

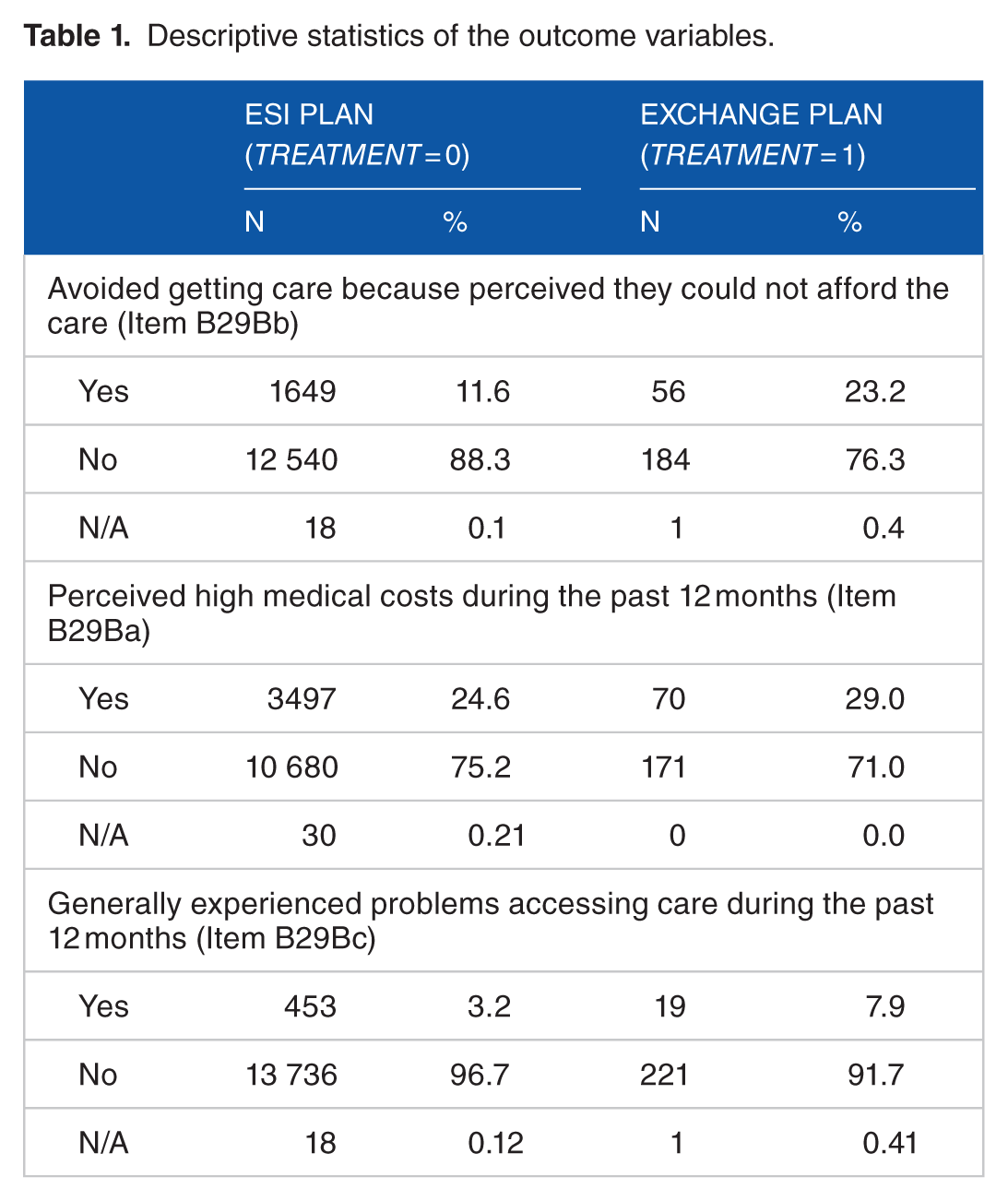

There were 3 outcome variables. To test Hypothesis 1, our first outcome variable measured the survey participants’ general perceptions about difficulty accessing care within the last 12 months: (a) OMAS item B29bC, “Did you have any problems getting the care you needed?” To test Hypoth-esis 2, our second and third outcome variables specifically measured cost-related difficulties with accessing care, including (b) OMAS item B29bB, “Did you delay or avoid getting care that you felt you needed but could not afford?” and (c) OMAS item B29bA, “Did you have any major medical costs?” All outcome variables were binary with possible “yes” or “no” responses. All “don’t know” and “refuse to answer” responses were recoded as missing data. Table 1 summarizes the 3 outcome variables.

Descriptive statistics of the outcome variables.

Treatment variable

The primary treatment variable, Treatment, was a measure of Exchange insurance coverage among currently employed Ohioans. Treatment = 1 if a participant reported both having Exchange plan coverage, OMAS item B4I = 1, and being currently employed, OMAS item g71 = 1. In comparison, the control group, Treatment = 0, was comprised of individuals who reported having ESI, OMAS item B4A = 1, and current employment, OMAS item g71 = 1.

ESI covers many privately insured individuals in the United States. 14 In studying the effects of Exchange insurance on access to care among employed Ohioans, it would be improper to compare Exchange coverage, Treatment = 1, to an uninsured or Medicaid-covered cohort because of potential selection bias. 14 Notable favorable selection exists in private insurance markets, as employed individuals tend to be healthier and more productive. 14 Therefore, to mitigate potential endogeneity caused by favorable selection, we estimated the causal effect of Exchange insurance on access to care in comparison to the effect of standard ESI on access to care.

Covariates

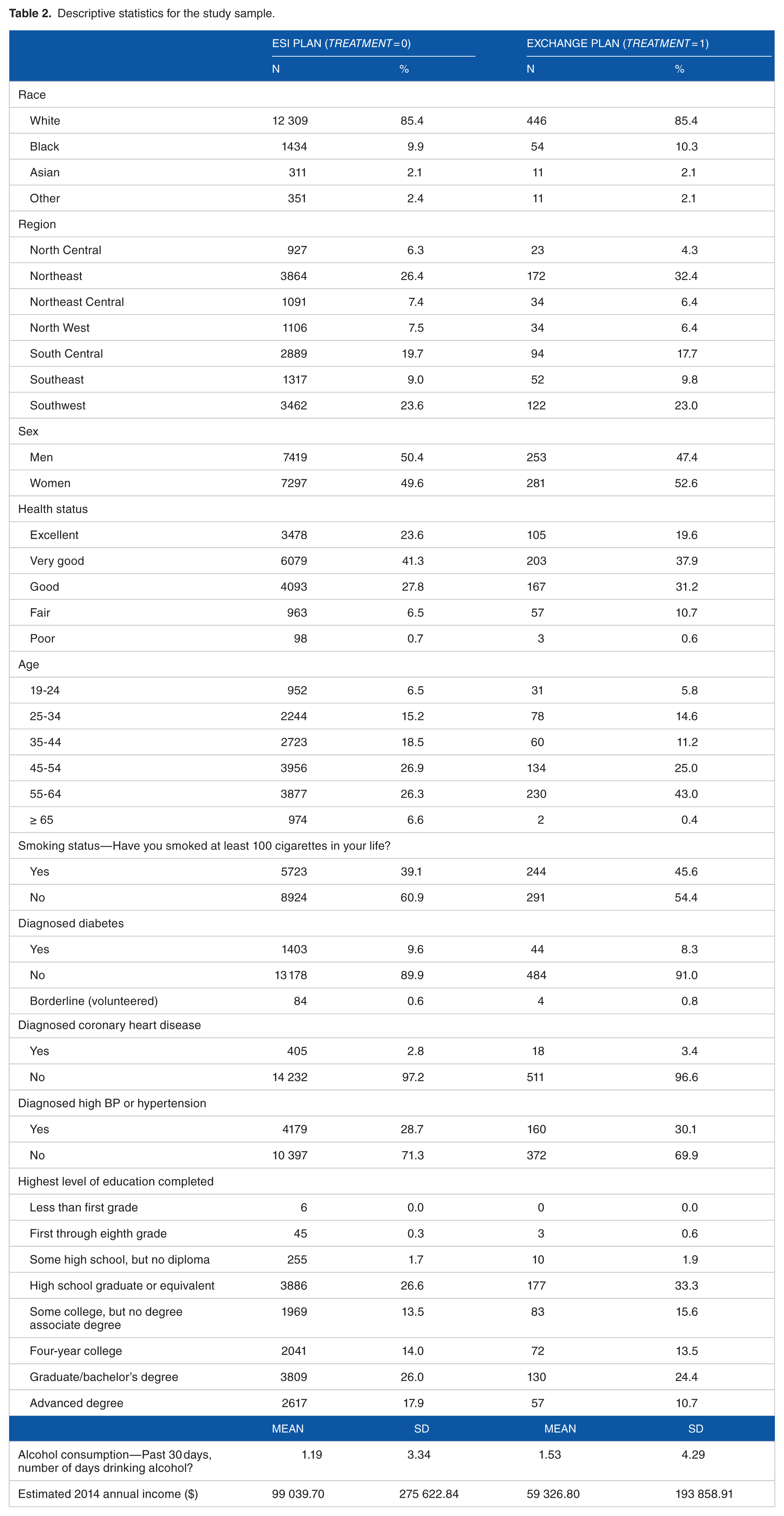

To control for potential confounding, we also included following health- and socioeconomic-related covariates, as summarized in Table 2: sex, age, region of residence, race, income, education, health status, chronic disease (diabetes, coronary heart disease, and high blood pressure or hypertension), and health behaviors (smoking and drinking). Andersen et al’s 15 Behavioral Model of Health Services Use (access framework) provides conceptual rationale for considering these covariates. The access framework describes how (a) contextual characteristics, (b) individual characteristics, and (c) health status can influence potential access to care and subsequent health care utilization. Both contextual characteristics and individual characteristics include predisposing factors and enabling factors. Enabling factors include income and education. Predisposing factors define the demographic covariates, including age, race, region of residence, and sex, as well as our health-status-related variables. We specifically consider common chronic diseases, including diabetes, coronary heart disease, and hypertension, to represent chronic illness status. 16 No multicollinearity was detected among the covariates.

Descriptive statistics for the study sample.

Statistical analysis

The causal effect of Exchange coverage on access to care can only be determined with knowledge of both potential outcomes (or counterfactuals) for each study participant under both Exchange coverage and standard ESI coverage. 17 However, while we cannot simultaneously observe both potential outcomes, statistical methods can be used to estimate the potential outcomes, comparing the effect of Exchange coverage and the effect of standard ESI on access to care. To strengthen our analysis and causal inference we conducted one-to-one nearest neighbor linear propensity score matching using Euclidean distance to balance the 2 treatment groups by sex, age, region of residence, race, income, education, overall health status, diabetes status, coronary heart disease status, high blood pressure or hypertension status, smoking status, and alcohol use, and we repeated the one-to-one matching process until no additional participant pairs could be formed.18-20 We then used logistic regression to model Treatment = 1, the event of having Exchange insurance coverage, using all observed covariates as propensity model predictors.

Participant responses to the 3 outcome variables were coded as dichotomous choices. Thus, for all outcome models, we used logistic regression to estimate the treatment effect of Exchange coverage on both the general access to care and the cost-related access to care outcomes. Using the OMAS survey weights, we conducted all regression analysis using survey logistic regression coding in SAS version 9.2.

Results

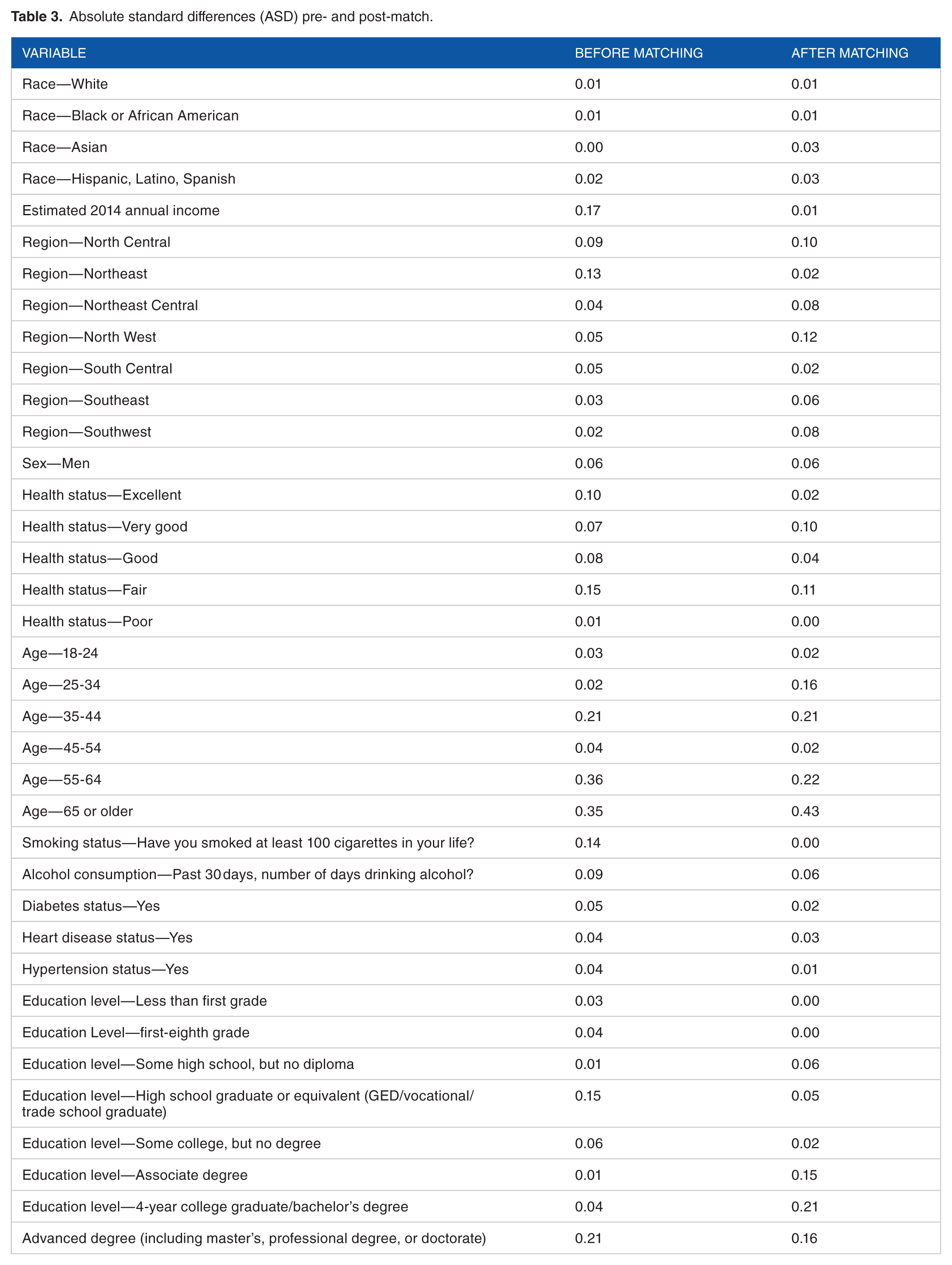

A total of 534 Exchange beneficiaries and 14 716 traditional ESI enrollees met our initial inclusion criteria. To assess whether the covariates were balanced between treatment group and control groups, we calculated absolute standardized differences (ASDs) before and after matching. A rule of <0.20 was used to determine an acceptable match. Overall, the matching method was effective, and after excluding missing data, 251 Exchange beneficiaries were matched one-to-one with comparable ESI enrollees. As depicted in Table 3, nearly all of the 37 covariate categories were ASD < 0.20 post-match and most were ASD < 0.10, thus ensuring comparable treatment groups prior to the outcome model analysis. 21 Of note, most of the covariate categories decreased ASD from pre- to post-match, and the matching method eliminated significant pre-match differences that emerged between the 2 treatment groups across income, smoking status, and health status categories.

Absolute standard differences (ASD) pre- and post-match.

Multivariate results

Table 4 depicts logistic regression estimates with nonlinear coefficients converted to odds ratios (ORs), including the 95% confidence intervals of the ORs. According to the parametric model, our general access to care outcome was statistically significant (OR = 3.93, P = .019). In general, the odds that employed Ohioans with Exchanged coverage (Treatment = 1) experience problems accessing care were 3.93 times greater than the odds employed Ohioans with ESI (Treatment = 0) experience problems accessing care. However, compared with ESI insurance, Exchange insurance was not significantly associated with either experiencing prohibitively high medical costs or avoiding care because of cost. Compared with employed individuals covered through ESI, employed individuals covered through the Exchange did not experience statistically significantly different access to care due to cost-related issues.

Predicted probability coefficient estimates and corresponding odds ratios.

Source: Authors’ estimates from the 2015 Ohio Medicaid Assessment Survey data.

P < .05; **P < .01.

Robustness checks: Benjamini-Hochberg procedure adjustment, sensitivity analysis, and multivariate regression with covariate adjustment

The multivariate results supported Hypothesis 1, rejecting the null hypothesis at the α = .05 level that there is no difference between the 2 treatment groups’ general ability to access care. We conducted several robustness checks in attempt to confirm this result ahead of drawing our conclusions. We first tested multivariate regression models with covariate adjustment on the pre-match treatment groups. As expected, the models yielded estimates similar to our main model estimates in magnitude and significance. We next conducted a Benjamini-Hochberg (BH) procedure adjustment to control the false discovery rate such that among tests declared significant, the proportion of true null hypotheses will be lower than the specified α threshold. Errors in hypothesis test conclusions depend on the frequency of the truth of null hypotheses being tested. 22 The BH adjustment is more conservative than simply rejecting tests by comparing P values with α, and it is more powerful than the Bonferroni procedure which would compare all 3 P values with .05 / n. Per Glickman et al, 22 we conduct the BH procedure adjustment as follows:

We sort our n = 3 P values in ascending order;

We let k denote the largest index i = 3 (ie, 1 for each of our 3 hypothesis tests) for which pi < d × i / n, assuming a maximum false discovery rate of d = 0.05;

We declare all tests with P values p1, p2, … ,pk significant.

All 3 P values derived from the multivariate statistical analysis were greater than their corresponding d × i / n values (ie, .016, .033, and .05, provided in Table 4) and we declare all 3 tests insignificant at the .05 false discovery rate. We ultimately fail to reject the null hypothesis that that there is no difference between the 2 treatment groups’ general ability to access care.

Finally, intending to conduct Rosenbaum sensitivity analyses, we ran McNemar tests as an additional robustness check. For all 3 outcomes, the McNemar test results failed to reject the null. Yet again, despite the original parametric model estimates, we cannot confidently conclude that employed Ohioans with Exchange coverage experience worse access to care than Ohioans covered through standard ESI.

Discussion

Since the enactment and implementation of the ACA, policymakers and the public have steadily voiced their concerns about the Health Insurance Marketplaces. Choice in access remains a crucial point of apprehension. 23 Many Americans continue to question the Obama administration for its promise that the new law would not impede Americans from keeping their doctors of choice. 24 To date, the Exchanges have demonstrated volatility in pricing and plan offerings in some states, 8 while evidence from the early Massachusetts health insurance exchanges demonstrated limited access to top providers. 9 Consistent with that evidence, our multivariate results initially supported Hypothesis 1 (ie, B29Bc). However, on conducting a series of robustness checks, the main model results disappeared. As such, we cannot confidently conclude that employed individuals with Exchange coverage generally experience greater problems accessing care compared with individuals covered through standard ESI. Whereas recent evidence from 8 states finds ACA Exchange plans pursued narrower hospital networks in an attempt to lower Exchange plan premiums, 10 our evidence intimates a different experience in Ohio in 2015. Indeed, our data precluded the direct evaluation of network breadth or provider exclusions; however, the experience of employed Ohioan beneficiaries suggests that Exchange coverage is not independently associated with systematically better or worse access to providers of preference, compared with similar individuals covered through standard ESI.

To that end, the financial viability of the Exchange plans remains a particularly hot topic of debate. However, political narratives and public perceptions notwithstanding, our findings suggest that Exchange plan coverage may be no more financially prohibitive to accessing care than standard ESI coverage among employed Ohioans. Hypothesis 2 was not supported by the results (ie, B29Bb). Under the current law, and after the initial year of Exchange plan coverage in Ohio, employed Exchange beneficiaries did not seem to experience greater medical debt than their peers covered through standard ESI. Moreover, employed Exchange beneficiaries did not appear to forgo care for financial reasons more than their ESI-covered peers. That result may change over time. Our data set prevents us from estimating the independent effects of federal Exchange premium and cost-sharing subsidy support on health plan affordability and health care utilization. Undeniably, the end of CSR payments and the potential repeal of the individual mandate or premium subsidies could bring stark changes to health plans and beneficiaries alike, including narrower provider networks and higher premium rate increases. Further evaluation will be warranted, given the current scrutiny of the Exchange plans by policymakers and health plan beneficiaries.

This study has limitations that must be discussed. First, this was a cross-sectional study that could not account for time variation, raising concerns about endogeneity caused by unobserved factors. Our propensity score matching methods helped ensure a fairer comparison between the 2 treatment groups based on observable health- and socio-economic-related covariates. For example, the 2 treatment groups were matched on income, education, health status, and other variables, which helped mitigate potential selection bias. However, we could not account for unmeasured differences and potential omitted variable bias, although we did conduct sensitivity analysis in an attempt to identify the potential impact of an unobserved variable. Second, this study does not assess actual utilization; rather, the outcomes were self-reported measures of perceptions on access to care. Third, decreasing responses rates are a concern for telephone-based surveys. Response rates for nonfederal household telephone surveys generally range from 5% to 30%. 25 The 2015 OMAS had a response rate of 24.1%. Moreover, to mitigate sampling bias, the OMAS oversamples key demographic groups and weights responses to match Ohio’s demographics in the American Community Survey. 7

Fourth, we were unable to distinguish among different Exchange plan organizations or Exchange plan tiers. It is possible that some health plans, such as the state Medicaid managed care firms, offer systematically better or worse provider network coverage and access to care; it is also possible that an Exchange plan from one tier (ie, bronze) may offer significantly better or worse provider network opportunities than an Exchange plan from a different tier (ie, gold). Fifth, it is possible that the opportunity to purchase subsidized Exchange coverage could cause ESI-coverage crowd-out. It is possible the opportunity to enroll in Exchange coverage incentivized employed individuals to systematically forfeit their employment, thus potentially causing study sample selection issues. As our data are cross-sectional, we could not conduct historical time trend analysis. That said, our data do not support evidence of systematic ESI crowd-out. The majority (54%) of the employed individuals with Exchange coverage in 2015 were previously uninsured in 2014. Of those individuals who did switch into Exchange coverage in 2015, just one-third were previously covered through an employer-sponsored health plan. Finally, our results only reflect the experience of Ohioans. Although the results are not generalizable to other states representing different sociodemographic population characteristics, the results are representative of the seventh largest US state by population.

Footnotes

Funding:

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests:

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Author Contributions

All three authors contributed to the data analysis and manuscript preparation.