Abstract

This study investigated young adults’ financial agency-building. In youth, agency-building entails becoming aware of capabilities possessed and structural conditions. Despite the agentic viewpoint being well-established in youth research, agency in financial issues is understudied. We conducted semi-structured interviews for 18 independently living young adults from Finland aged between 21 and 26 years. The transcribed interviews were narratively analysed. Participants shared events that represented their orientation towards financially independent adulthood. The narratives of ‘stepping up to adulthood’ and ‘leaning back on childhood’ demonstrate their differing tendencies to resort to parental support. Becoming aware of their parents’ financial socialization increased confidence to update their skills in the future. Our study suggests that parents’ financial socialization not only increases children’s financial capabilities but functions as a mirror surface for young adults, thus supporting financial agency-building. Complementing the theorization of financial socialization, this study presents the young adults’ perspective on financial agency-building.

The transition from childhood to adulthood occurs gradually. Children and youth become integrated into a consumer society through various socializing processes, including parents, friends, school and media culture. The path towards adulthood involves various milestones: leaving home, finishing school, beginning a job and starting a family (Berngruber, 2016), which intertwist financially independent orientation, such as residential independence (Xiao et al., 2014). Consequently, financial skills enhancements are stressed in importance with young people. In many developed countries, this transition is no longer linear but rather comprises complex processes and expected and unexpected events. For instance, young adults face challenges in securing stable employment due to economic volatility (Vosylis et al., 2022), and capricious life events can also impact their financial stability (Autio et al., 2009). In addition, changes in the economic and social environment influence on the lengthening of the transition to adulthood (Billari & Liefbroer, 2010; Côté & Bynner, 2008; Serido et al., 2020). In order to adapt to these changes, young people commonly engage in short-range planning. According to du Bois-Reymond (2009), this phenomenon can be characterized as yo-yo biographies-in-the-making, wherein young adults encounter various alternatives or constricting paths within their professional and educational spheres. This, in turn, prompts them to alter their plans multiple times, consequently leading to heightened financial skills requirements.

Young people transitioning into independent financial agents is a complex phenomenon, with parents acknowledged as one of the primary influencers shaping their upbringing (Gudmunson & Danes, 2011; LeBaron et al., 2022). Parenting styles have been recognized as influencing young adults’ financial behaviour, such as seeking advice (Fan et al., 2022). Parents are increasingly involved in their children’s financial lives also after they earn their own money, often offering advice on how to handle financial matters (Luhr, 2018). The sense of competence in managing one’s own finances (i.e. financial independence) has been identified as a milestone in the transition from parental financial support to self-sufficiency (Butterbaugh et al., 2020). However, there is limited research on how young adults view the transition to independent financial agents. Furthermore, young adults’ perceptions of skills improvements that support the adaptation to new financial situations have not gained academic interest.

The present study focuses on young adults’ path towards financially independent adulthood and the formation of their financial agency. Utilizing the framework of agency, the study to approach how young adults perceive their increasing financial participation. In the literature, agency is associated with acknowledging structural conditions, such as resources, social relations, cultural context and the interplay between the individual and the surrounding structures (Giddens, 1991). In addition, agency refers to an active participation and intentionality of actions (Coffey & Farrugia, 2014). In terms of financial issues, agency is associated with emerging subjectivity and sense of control over one’s financial future (Newcomb, 2018), as well as the interaction between financial resources and future-oriented thinking (Bermudez et al., 2022). Kortesalmi (2024) stresses the situational viewpoint of financial agency in the interaction of personal abilities (such as money management and informed consuming) and structural conditions (such as opportunities to utilize formal financial services and earn income). In this study, financial agency is defined as a sense of confidence in financial management (i.e. financial independence) and financial learning (i.e. achieving financial skills and knowledge in new situations). Consequently, financial agency is viewed as an ongoing process rather than a fixed state. The study explores on the intersection between childhood family and independent financial adulthood, and young adults’ perceptions of the formation of financial agency are examined by applying narrative practices in the analysis of young adults’ interviews. Despite the importance of economic conditions in young adults’ lives, there is a limited number of studies that illustrate individuals’ financial participation from the agentic viewpoint. This study aims to address the gap.

Literature Review

Agency-building in Youth

In the field of youth research, the concept of agency is currently prominent. While individualized notions of agency focus on psychological aspects (such as motivation), much of the literature on agency emphasize young people’s participation in society (e.g. Archer, 2003; Bolin, 2016; Bourdieu, 1990; Caetano, 2015). According to Coffey and Farrugia (2014), agency aims to account for differences in young people’s lives, making it a heuristic attribute. On the other hand, agency can also be seen as a developmental characteristic that individuals possess and enhance. This perspective highlights the unique position young adults occupy in society, as they typically create their own behavioural models rather than merely reproducing those that they were socialized to adopt. Consequently, the interplay between individual capabilities and structural conditions is particularly significant for young adults (O’Connor, 2014).

There are diverse emphases on the role of agency in illustrating social reproduction. For example, Bourdieu (1990) argues that young people’s subjectivities are largely shaped by structures, leading them to reproduce these structures through their actions. Consequently, reflexivity is not considered significant in shaping their identities. On the other hand, Giddens (1991) considers the construction of individual subjectivity as a reflexive project of the self, arguing that structural constraints are less significant. Reflexivity involves evaluatiing one’s identified capabilities against situational demands (O’Connor, 2014). Archer (2003, 2007) suggests that reflexivity functions as an emergent personal property that mediates between structure and agency. This mediation involves an internal dialogue where individuals plan their actions by aligning personal concerns with external conditions. Reflexivity not only mediates the influence of structures on individuals but also shapes their actions in specific situations. More specifically, Archer posits that structural properties shape the situations that agents encounter and exert power over them. As a result, social practices emerge from agents’ reflexive deliberations (Archer, 2003, p. 135; Caetano, 2015).

Archer (2012) acknowledges the challenging position of young individuals who face the lack of authoritative normative sources, thereby highlighting the significance of reflexivity. Concurrently, the real relations of young people with others constitute their socialization, with families playing a central role in facilitating their reflexivity. As young adults encounter new opportunities and unknown situations, reflexivity becomes imperative in their daily lives. Their reflexive practical reasoning—shaped by prioritization, accommodation, subordination and excluding matters—is influenced by their network of relations (Archer, 2012, p. 99). In essence, navigating opportunities in negotiation with parental recommendations while identifying valued matters in life establishes the reflexive process of reproducing and reformulating practices for young adults. However, according to Coffey and Farrugia (2014), more nuanced understanding is required to identify how practices are negotiated rather than labelling actions as agentic. Therefore, investigating young adults’ reflexive process of perceiving opportunities and enhancing capabilities in interdependence with their parents offers an opportunity to study their agency-building. Moreover, examining the reflexivity of young adults regarding their life course beyond expected social positions provides an avenue for studying their agency shaped by available resources.

Families’ Support in Young Adults’ Agency-building

The development of agency is a continuous process that takes place throughout one’s life, with a significant emphasis on the adolescent years spent at home. Children’s agency within the family is closely related to their age, with their participation in family decision-making increasing as they mature. According to Bertol et al. (2017), various influencing strategies are employed by children from a young age, such as bargaining and persuasion, in interaction with family members while incorporating their parents’ beliefs into their requests (Kerrane et al., 2012). The reflection between capabilities and desires is involved in agency-building, and it begins before possessing independent financial resources. Participating in family consumption decisions provides children with an opportunity to establish an autonomous agency through the reflection of their capabilities and requests (see du Bois-Reymond, 2009).

Parenting is viewed as a balance between directing and supporting children’s agency, which is achieved through inter-generational negotiations and mutual accounts of household chores (Aronsson & Cekaite, 2011). Parents lay the foundation for their children’s agency by assigning household duties that correspond to their capabilities, enabling them to recognize their potential and develop their subjectivity. As Curran et al. (2018) state, self-regulation and commitments are essential to constructing children’s agency through reciprocal and interactive processes that involve parental strategies and adolescents’ compliance and resistance against parental directives. In families, care is intertwined with parental support. For example, family consumption research approaches care as a central dimension of family consumption. According to Kastarinen et al. (2022), caring is closely associated with generativity—it changes and evolves over time, and caring produces more caring. From the young adults’ viewpoint, they interpret their parents’ worrying as caring, and they reciprocally avoid situations that would worry their parents (Lahelma & Gordon, 2008).

Daily family practices offer opportunities for family members to observe and interact with financial issues (Luhr, 2018). Parents model financial practices for their children, communicating values and expectations through their observations (LeBaron & Kelley, 2021; Serido & Deenanath, 2016). For example, parents talk with children about savings and credit card use, while at the same time, they model desired financial decision-making. However, parents should also provide experiential learning opportunities in addition to financial discussions and modelling financial behaviour, as suggested by LeBaron et al. (2022).

The topic of financial learning within families has been analysed through the framework of family financial socialization (Gudmunson & Danes, 2011). Financial learning occurs during discussions with parents regarding earning, spending, saving and borrowing while observing their parents’ positive and negative practices (Serido & Deenanath, 2016; Shim et al., 2009). For young adults, financial learning in families is particularly important because they not only develop necessary capabilities but also become increasingly conscious of their attitudes, values and norms, which ultimately affect their financial well-being (Serido & Deenanath, 2016). Studies show that adolescents are also actively involved in financial socialization (e.g. Jorgensen et al., 2017). However, the top-down approach of financial socialization— where parents impart knowledge, skills, and attitudes to their children—has been criticized (Guhin et al., 2021). Moreover, socialization tends to focus on social reproduction, which fails to account for situations where learning and applying new models of behaviour are essential, such as in financial matters.

In contrast to the individualization thesis, the significance of families in young adults’ lives has been discussed. Young adults are no longer viewed as individuals who need to separate themselves from traditional family ties. Instead, families are seen as integral to the transition into adulthood (Wyn et al., 2012). This perspective highlights the interdependence of young adults and their families. Lahelma and Gordon (2008) argue that different states of dependence and independence occur in various areas of life and are consistently negotiated. Family relationships are identified as two-way flows of material, emotional and economic resources (Wyn et al., 2012). As Aaltonen (2013) illustrates, young adults exercise their agency within families during their transition to adulthood. In summary, the construction of a young adult’s agency is a complex journey of moving forward and occasionally returning to their childhood home and family support. In youth research, agentic viewpoints have a long-standing tradition. However, the role of agency in financial issues has been understudied in these discussions. The present study adopts a relational perspective on agency. Agency is viewed as the constitution process of the subject (see Niemi, 2022). By examining the interviews of young adults, the study approaches financial agency-building in negotiations within the interdependent relationship with parents.

Methodological Approach

Context, Participants and Procedures

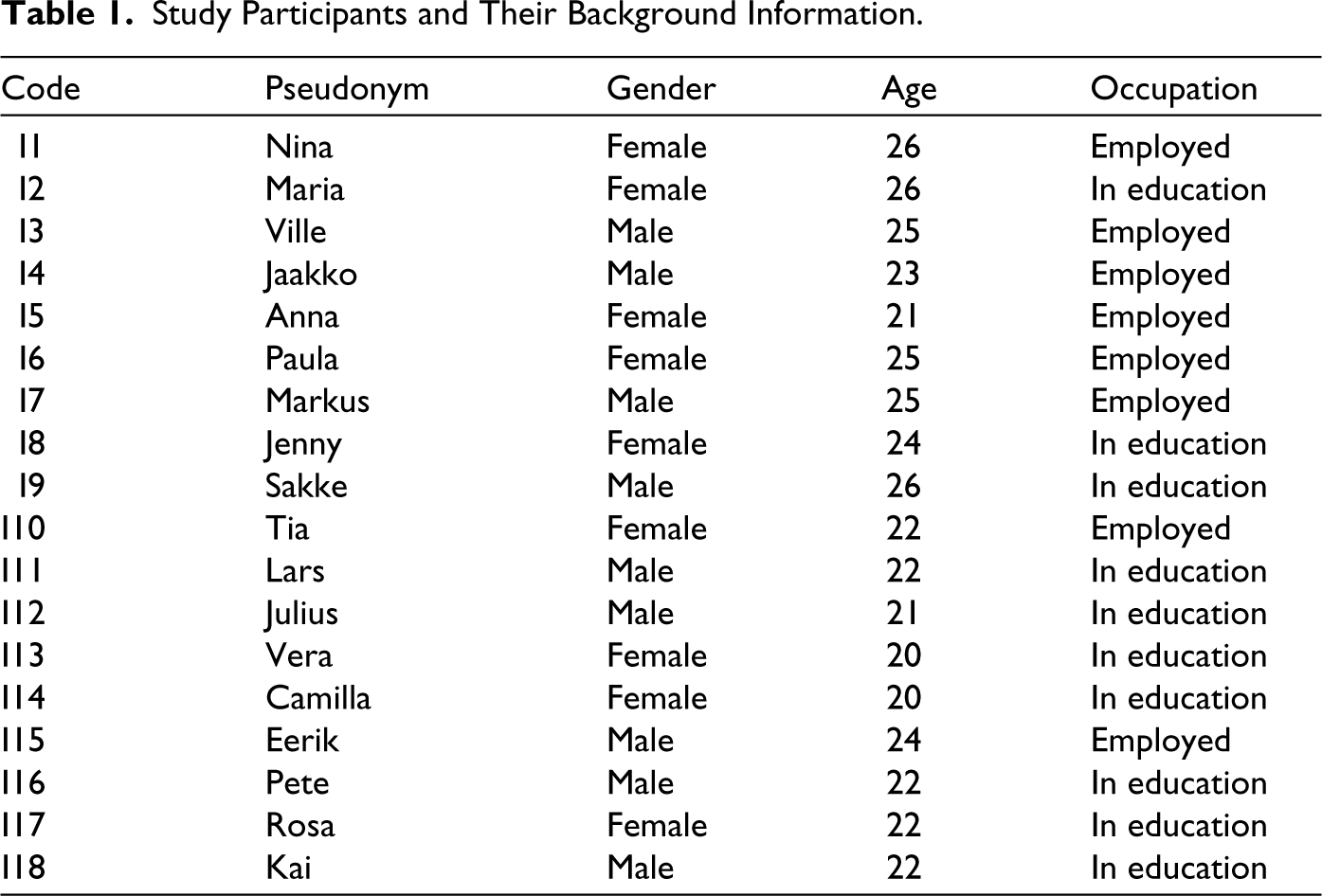

Participants in our study, all Finnish young adults, were on the verge of financially independent adulthood. Finland provides a context for examining young adults’ financial agency-building. First, the state supports the transition to financial independence through various means, such as financial aid for students and tuition-free education. Second, the housing and labour markets enable young adults to leave their childhood homes relatively early (Majamaa, 2015). In Finland, it is common for young people to start living independently from their families at a young age (Ranta & Raijas, 2020). Despite this trend, 26% of students in Finland receive direct financial support from their parents, and 15% of students share their bills with parents (Saari et al., 2020), indicating that parental involvement in young adults’ financial lives persists longer than their living arrangements would suggest.

Interviewees in this study were young adults aged 20–26 years (Table 1) who had been living independently for at least one year. While all were accustomed to managing their household expenses, their reliance on parental support varied. Participants were recruited through the networks of two interviewers, with several invitations sent out, resulting in a total of 18 interviews. The recruitment process aimed to balance in two categories: gender (nine females, nine males) and occupation (eight employed, 10 students) to ensure the variety of participants. However, socioeconomic backgrounds were not explicitly addressed during the interviews. For us, it was crucial that participants possessed abilities to discuss about their financial practices and skills enhancements to capture their perceptions and conceptualization of the phenomenon. Participants were informed that their participation was voluntary, no personal data would be collected, and they could withdraw at any time without explanation, in accordance with good scientific practice. The interviews were conducted in two parts: the first with nine pants in winter 2019–2020, and the second in summer 2020. Interviews were held both face-to-face and online via the Teams application, with each interview lasting about one hour. The online format facilitated remote participation, as the participants were from six different municipalities across Finland.

Study Participants and Their Background Information.

The interview transcriptions were recorded with no personal identification details and resulted in a vast body of data totalling 112 pages. The citations used throughout the study have been anonymized to ensure confidentiality. The sensitivity surrounding the discussion of finances was carefully considered during the interview process. Special attention was given to creating an environment of mutual trust to facilitate the collection of accurate and reliable data. Interviewees were informed about their anonymity, and they could stop the interview at any time. The interviews began with narrative-based questions designed to elicit childhood memories and perceptions of themselves as consumers. This was followed by a series of semi-structured questions that focused on the themes of becoming a consumer and acquiring financial skills during adolescence. The selected methodology provided a platform for the interviewees to express their views and offer descriptions of their lived experiences, which facilitated the interpretation in a data-driven manner.

Data Analysis

The analysis of this study employs a narrative practice. Differing from the analysis of narratives, where the data are usually in story form, narrative practices focus on producing a coherent storyline or chain of events from the data (Polkinghorne, 1995). Events are approached as descriptions of intentional acts that the characters initiate. Further, events are interpreted as situational representations that introduce a sort of disruption in the normality (Herman, 2009). In other words, by illustrating the events, participants draw attention to their perceptions of what is disrupting their normal flow of activities. The narrative practice of analysis is piece together the data, making the invisible apparent and deciding on what is significant and insignificant (Josselson, 2011). Data elements are organized into a coherent developmental account. That is, narrative analysis is merely the synthesizing of the data rather than separating it into parts (Polkinghorne, 1995). The semi-structured questions used in this study facilitated the participants’ perspectives on their childhood families and their gradual move towards financially independent adulthood. The interviews allowed participants to retrospectively describe the events that represented the steps in this path. Although the semi-structured questions enabled participants to elaborate on their experiences related to the selected topics, the data is read and interpreted as a whole. Interviews were viewed contextually and explored as an entity rather than as fragmented units (Josselson, 2011).

Our analysis focused on young adults’ perceptions of their skills enhancement process. That is, we approach the study participants, young adults on the verge of financially independent adulthood, as narrators of that process. Our research interests targeted on what characterizes that process, and therefore, our analysis is not addressing the socioeconomic background of participating individuals. Initially, we directed our attention towards the significant events recounted by the participants as illustrative of their journey towards financial adulthood. These events played a pivotal role in facilitating the participants’ reflexivity, which involved an evaluation of their possessed capabilities vis-à-vis the situational requirements. Furthermore, the events served as milestones in their increasing involvement in the financial domain. In this stage of analysis, our examination was executed with a guiding question of ‘what events characterize young adults’ paths towards financially independent adulthood’. The events shared similarities and were defined and categorized based on the theoretical background of young people’s financial independence attainments (Drever et al., 2015; Serido & Deenanath, 2016; Xiao et al., 2014). From this, we formed a chain of events illustrating the path towards financially independent adulthood.

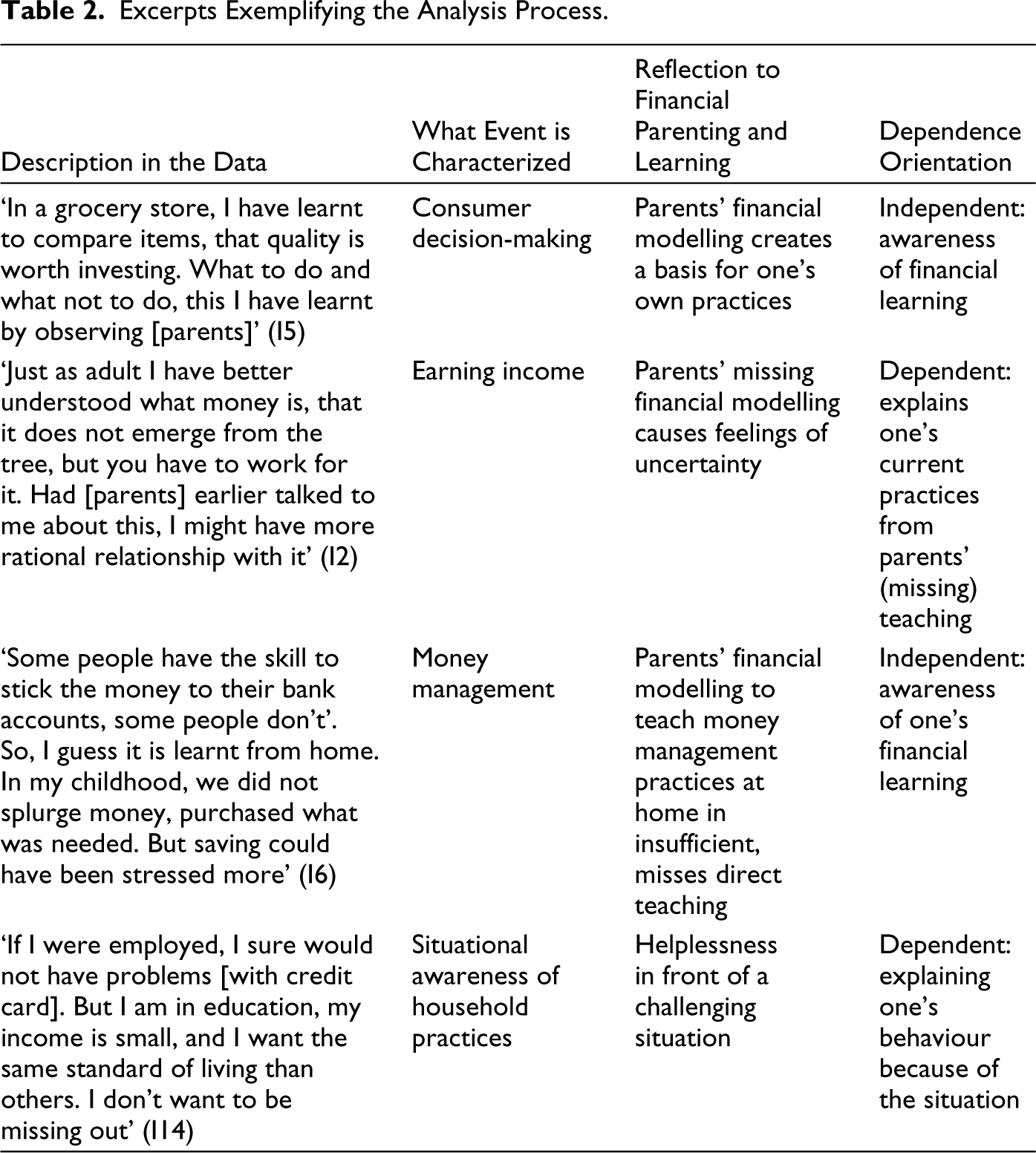

In the second stage, we interpreted the denotations of the categorized events, guided by the question of ‘how participants reflect the events to their financial learning’. Table 2 exemplifies how the leading questions facilitated the interpretation of the excerpts.

Excerpts Exemplifying the Analysis Process.

Despite events being sequenced, the participants’ transitions were not linear but intricate, characterized by diverse tendencies of financial independence and dependence of parental support. Subsequently, in the second phase, we delved into these two orientations. First, participants’ illustrations were independently oriented, that is, they were aware of their own subjectivity in financial actions and in the skills enhancement process. Second, participants’ descriptions were dependence-oriented, that is, participants’ subjectivity in financial actions was blurred. When focusing on these two orientations, we interpreted the data in terms of construction of young adults’ financial agency. This examination led to the emergence of two distinct narratives: (1) the independence-supporting narrative, referred to as ‘stepping up to financially independent adulthood’ [‘stepping up’], which highlighted the participants’ inclination towards independent financial actions; and (2) the dependence-oriented narrative, known as ‘leaning back on childhood’ [‘leaning back’], which traced the trajectories that compelled them to rely on parental support.

Findings

Findings are presented in two parts. The first part of the findings focuses on the significant events that participants perceived in their path towards financially independent adulthood. The second part of the findings focuses the two narratives that illustrate the two-folded dependence orientation. These two parts enable us to approach the characteristics of young adults’ financial agency-building.

Significant Events in the Transition to Adulthood

The participants displayed similarities in their descriptions of significant events that marked their progression towards financial maturity. These events brought about an awareness of necessary financial practices, knowledge and objectives. The participants’ initial financial engagements were attached to their families’ consumption practices, gradually increasing their independent engagements. We classified these events by reflecting on the theoretical framework of consumer decision-making (adapted from Drever et al., 2015; Serido & Deenanath, 2016), earning income and money management (Xiao et al., 2014), and situational awareness in household practices.

Establishing consumer decision-making habits began while the participants were still living at home. They recounted specific situations, such as standing in line for the cashier and interacting with shop assistants, which made them realize their ability to carry out shopping independently. The participants also started making independent consuming decisions, distancing their desires from those of their parents or siblings. Julius, for example, recognized his parents’ financial model (‘this is what my parents used to do’) and evaluated it (‘sometimes good, sometimes bad’), ultimately establishing his own approach (‘I do things differently’).

The most influential has been family and the models I got from home, the teaching model. For example, in grocery shopping, I have seen what to buy, how to buy, and how much there is this spare, so to say, spare that is sometimes expensive. It (the family model) has influenced me in two ways. You can learn about responsible money management. Or, on the other hand, you can learn to have not-so-savvy ways. I myself do it differently. I pay attention. (I12) (Julius, 21 years, in education)

When they were still living at home, they were able to allocate their income to the purchases they retrospectively considered unnecessary.

Before receiving a salary, they started making independent consumption decisions. But once they started earning money, they became more nuanced in their approach. The participants evaluated how their income affected their financial behaviour and how their newfound position as consumers was perceived within their families. They acknowledged the ability to make autonomous decisions regarding consumption, which provided them with a sense of freedom that was primarily used to purchase items deemed unnecessary. However, earning a salary also increased their sense of financial responsibility. They began to scrutinize different consumption options when spending their hard-earned money. By making independent consumption decisions, young adults gained insight into their own attitudes and values as consumers and built their financial subjectivity.

The descriptions of earning one’s own income were closely intertwined with a sense of responsibility towards financial behaviour, particularly consumption decisions. Participants’ personal income allowed them to distance themselves from parental oversight and the family’s financial situation, as Rosa explains in the following excerpt.

I started working relatively young and wanted to be independent, and coming from a big family, I wanted that (the parents) would not spend money on me. It had been discussed how tight (the family’s) financial situation was, so I didn’t want money spent on me. (I17) (Rosa, 22 years, in education)

With this, Rosa not only acknowledged her financial subjectivity in manifesting the independence that the income brought her, but it also differentiated herself from her parents and family by making individual consumption decisions while still living in her childhood home.

The data presented reveals that participants’ illustrations were indicative of the intermingling of money management and situational awareness of household practices. Participants placed significant importance on their ability to manage their finances within the given income level, as this established a sense of confidence in their abilities. Moreover, financial independence was not limited to being able to make a living but was also extended to gaining confidence to manage any situation. The act of balancing daily finances was found to be negotiated in situations that were coloured by various challenges. Specifically, young adults recalled instances where they initially struggled with balancing their finances but eventually succeeded. They also acknowledged the need to adjust their household practices in different financial situations, such as cooking cheaper meals, resisting eating out and postponing larger purchases when low on funds.

Two Narratives Describing the Dependence-orientation in the Events

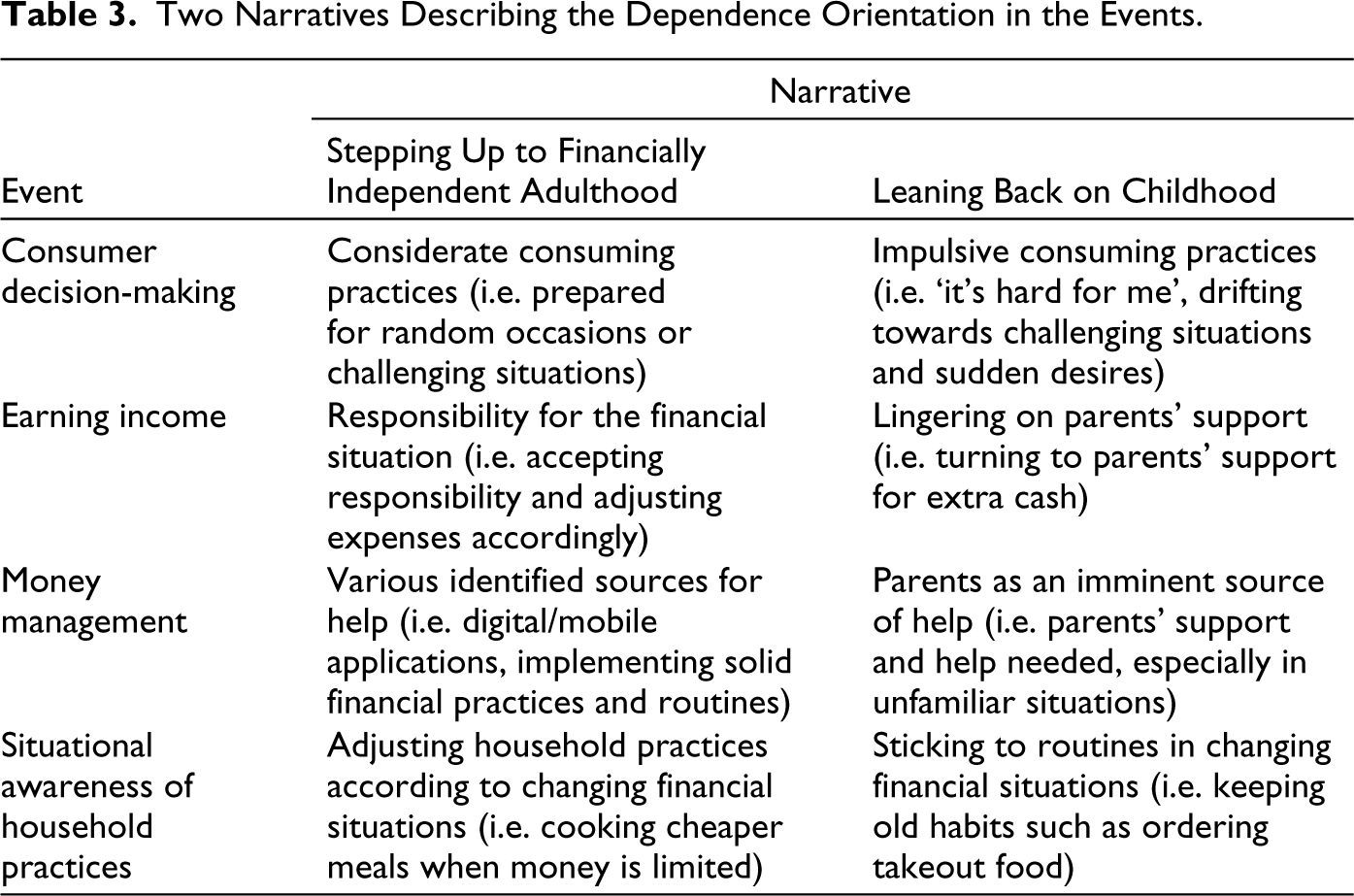

When examining how participants reflected on financial learning in these events, two narratives were created to illustrate the diverse tendencies in young adults’ descriptions. In the narrative ‘Stepping up to financially independent adulthood’, young adults acknowledged their agency, current position and future orientation as independent and financially capable individuals while accepting the possibility of parental support among other possible sources of help. In the ‘Leaning back on childhood’ narrative, the young adults’ definitions of their subjectivity leaned towards parental support in various forms. For instance, when confronted with a novel financial situation, the parlance either demonstrated the different sources of assistance to utilize (stepping up) or was associated with parents’ help (leaning back) in the situations. The events and narratives are presented in Table 3.

Two Narratives Describing the Dependence Orientation in the Events.

When describing themselves as consumers, narratives differed on how the subjectivity was perceived. In the ‘stepping up’ narrative, the everyday consumer habits as well as the challenges were acknowledged. Moreover, the narrative demonstrated that these challenges were anticipated and prepared to face to. For instance, the need to spend extra money around the holidays was covered by saving beforehand or afterwards. In the ‘leaning back’ narrative, the challenging consumer situations were perceived as succumbing to unavoidable situations. Sudden desires and tempting situations were acknowledged but they were referred as a reaction beyond controlling. Weak acceptance of responsibility over one’s financial behaviour indicated a stronger dependence on parental support. Conversely, ‘stepping up’ narrative indicated the participants’ responsibility over their consumer decision-making and higher level of readiness for financial independence.

The two narratives differed in their perception of how young adults interpret earning income. In the ‘stepping up’ narrative, earning one’s income translated to complete financial responsibility. That is, expenses were described to be adjusted according to income. If expenses increased, it was responded by looking for extra income options or reducing expenses. This adjustment demonstrated of being responsible for making changes when financial circumstances changed. Conversely, in the ‘leaning back’ narrative, personal responsibility was less defined and turning to parental support was more apparent. When interpreting the perception of balancing daily finances, the difference was in the understanding of money management. In the ‘stepping up’ narrative, daily money management was illustrated as a ‘job to be done’, unlike the ‘leaning back’ narrative, where money management was described as challenging and time-consuming.

The two narratives diverged in how participants employed strategies to support their daily finances. ‘Stepping up’ narrative indicated the usage of mobile applications or banking-provided budgeting tools. In addition, supportive practices such as budgeting, planning, bargaining and prioritizing quality over quantity were described to be implemented. These practices enabled to navigate through various financial situations successfully. On the other hand, in the ‘leaning back’ narrative, parents were mentioned as the primary source of help in new situations and difficulties. Daily money management was perceived as challenging, and the reasons for these challenges were perceived as beyond the participants’ control, such as being a student. Similarly, in the ‘leaning back’ narrative, adjusting household practices was not identified as a response to react in the financial situation or improve it. Certain habits, such as eating out with friends when unable to afford it, were considered inevitable events that ‘just happened’.

The reflexivity of the possessed capabilities led to the recognition of the process of acquiring these capabilities, including their parents’ financial socialization. An excerpt from Vera’s testimony serves as an example of this.

I have learned to control myself. I have learned that if I want something, I have to work for it, that you can’t just buy everything. When I was a kid, I didn’t get everything I wanted. But if I did enough household duties, I was able to get what I wanted. (I13) (Vera, 20 years, in education)

In this regard, the two narratives exhibited dissimilarities. The ‘leaning back’ narrative portrayed the achievement of financial capabilities as an unstructured and unidentified process. Financial skills and behavioural traits, such as saving habits, were believed to have emerged during childhood or were passively ‘inherited’. This implies that capabilities and solid financial behaviour were not perceived as being the result of a learning process. The insecurity regarding their capabilities led young adults to stand on the cusp of adulthood instead of being supported in taking the step into it. Furthermore, parents’ socialization was perceived as being inadequate, with parents refusing to discuss their financial situation or certain financial practices, such as saving and investing. This created uncertainty for young adults. Not only was there an absence of an objective evaluation of the family’s financial status but also a lack of evaluation of their opportunities to attain the same status. Additionally, young adults were in a difficult position when attempting to enhance their financial independence without understanding what they needed to be independent of. Two quotes exemplify this.

I think it has been good to notice that I will never attain the same income level that my father has had. Or you never know (laughs) but not at least at this young age. I consider it remarkable that I have grasped that. (I10) (Tia, 22 years, employed)

He (father) won’t tell me what he earns. And then, I can’t so fluently evaluate how much money my family has. Sometimes it is tight. But I am not sure, really, if it is tight. We have a fancy home, but I have no idea what kind of salaries my parents earn. Do they have a big bank loan or what. I really do not know anything about their salaries. And that influences my thinking about different professions and their salaries I know that I have no idea what a normal salary would be. (I14) (Camilla, 20 years, in education)

In the first quote, Tia congratulated herself for being able to (1) figure out her childhood family’s financial position, (2) evaluate that position with respect to her opportunities to attain the same level and (3) construct a financial status that she is satisfied with. In this last endeavour (3), Camilla expressed her frustration at not being able to evaluate her opportunities against the family background because of the lack of communication at home.

Discussion

For participants, financial agency-building was a process consisting of recognizable events. The events mark the points where young adults became aware of structural conditions, reflected on their capabilities, and anticipated learning in the future. This finding echoes those of Coffey and Farrugia (2014) and O’Connor (2014). For young adults, reflecting on their parents’ capabilities and financial socialization, were stressed in importance. First, when evaluating their parents’ capabilities, they acknowledged the quantity and quality of their own capabilities. Second, acknowledging parents’ financial socialization enabled them to recognize the attainment of these capabilities. Participants reproduced their parents’ financial practices, and gradually increased their independence. For instance, initial independent purchases at grocery stores progressed to individual consumption decisions and eventually to independent control of expenses and income.

In socialization, individuals adjust to attitudes, values, and norms and learn new abilities to harmonize themselves with the environment. In family financial socialization, the learning of financial behaviour and knowledge takes place in the family context (LeBaron et al., 2022; Luhr, 2018). Consistent with this study, parents socialized their upbringing, the study participants. Demonstrating this, participants reproduced their parents’ financial practices and designed their own practices. Previous research has emphasized the significance of positive parent–child relationships in family financial socialization (LeBaron et al., 2022; Luhr, 2018; Serido & Deenanath, 2016). In this study, good relationships supported young adults in creating interdependence with family members.

Participants also criticized their parents’ practices. For instance, parents’ habit to ‘continuously start new projects’ (that is, to purchase commodities with instalments) was criticized by their upbringing and commented that he himself ‘would not tie the cashflow with that many fixed payments, but rather enjoy the flexibility’. Ponderings between the acceptance and criticism of their parents’ financial practices demonstrate the negotiations that were attached to a financial agency-building. In the study, negotiating situations were mainly related to consumer practices, as exemplified by the quote from Julius. Coffey and Farrugia (2014) underline the role of parental negotiations in the agency-building process. However, we propose that these negotiations are not only conversations but also mental reflections on parents’ financial practices and models. Young adults were especially critical when perceiving parents’ financial modelling as missing. This left them uncertain of their current positions. That is, to attain financial independence, it was necessary to become aware of where to be independent before taking directions towards it. These findings are in line with O’Connor (2014), who states that going beyond social expectations requires becoming aware of those expectations (also, Bolin, 2016).

In the ‘stepping up’ narrative, several elements demonstrated its orientation towards financial independence. First, the parlance echoed the assumed responsibility for financial decisions. Second, although unfamiliar financial situations in the future were anticipated, expressions of confidence in capabilities and abilities to acquire new financial skills, when necessary, lightened concerns. In the ‘leaning back’ narrative, the accepted responsibility of financial decisions was more conditional. Expressions showed limited confidence in learning new skills and parents were mentioned as the most imminent source of help. Phrases of uncertainty and vulnerability, such as ‘If only would I have known’ or ‘I just couldn’t figure out [what to do]’, were related to future anticipations and evaluation of skills. Tones of confidence illustrated ‘stepping up’ narrative, while tones of uncertainty were more common in ‘leaning back’ narrative. The tones indicate the distinctive orientations of these narratives.

However, the study approached narratives as characterizing participants’ distinctive independence orientations as a whole, not as addressed to a specific subgroup. Participants’ descriptions illustrated both narratives simultaneously. For instance, a participant described her/his income-earning attempts that demonstrated financial independence orientation, while descriptions of her/his household practice adjustments demonstrated dependence orientation. This indicates that financial agency is not a binary concept but encompasses distinctive orientations. Accordingly, participants did not differ in being less or more agentic. Instead, their agency varied in being more and less independence-oriented, as illustrated by the two narratives. In this study, these orientations were interpreted in the context of financial independence and in relation to the childhood family. The study obtained to illustrate the phenomenon of financial agency-building, and participants’ demographic characteristics were not the focus. The deviation in the gender of participants (50% female, 50% male) represents the gender deviation in Finland. The occupation status of study participants was 44% employed and 56% in education, representing the occupation status of young adults in Finland. According to the OECD (2023), the status of young adults aged between 18 and 24 years in 2022 is 30% employed and 59% in education; however, the study is missing young adults not in employment nor education or training (NEET). Future studies should focus on the financial agency-building of that group.

The path to financially independent adulthood is not always straightforward and may involve utilizing parental support, as stated by Billari and Liefbroer (2010) and du Bois-Reymond (2009). The results indicate that even when living independently, parents’ caretaking has reached the youth (see Kastarinen et al., 2022). The support of parents was viewed not as specific answers to their requests but rather as a form of overall care. Study participants were offered opportunities to earn extra cash by doing domestic tasks and parents supported them with joint grocery shopping at parents’ costs. However, the participants’ depictions of this support were ambivalent, as they struggled with relying on their parents for guidance (Ranta & Raijas, 2020; Xiao et al., 2014). When parents’ support was voluntary and perceived as a gift, confidence was instilled. Conversely, when young adults were obligated to seek their parents’ assistance, they felt a sense of dependence that eroded their confidence in their abilities.

In this study, young adults illustrated disruptions to their routine financial practices. These disruptions were interpreted as exceptions to routinely executed practices, whereas smooth activities in everyday life did not occur. These disruptions served as catalysts for reflexivity and agency-building. In line with Archer (2012), reflexivity merges in situations of concern, forcing internal dialogue and articulation. While these situations can be emotionally challenging, they enable individuals to recognize their capabilities and construct agency (O’Connor, 2014). However, not all structural conditions are recognized and reflected at the same time; hence, agency-building is a lifelong process.

Conclusion

Young adults’ journeys into adulthood encompass complex financial situations that require them to learn to navigate without their parents’ guidance. The study findings illustrate the procedural and multifaceted characteristics of agency-building, as well as the interdependence of young adults with their parents. For the study participants, growth towards independent financial adulthood was a process that incorporated significant events. Events mark the points that they became aware of both their financial models as well as their parents’ models and financial socialization. We argue that incremental financial engagements are not merely a product of parents’ financial teachings but also a result of young adults actively designing their own financial models and strategies, which contribute to the construction of a financial agency. This study contributes to the literature on agency by proposing that in financial agency-building, negotiations with parents are also mental reflections on parents’ financial practices and models. Furthermore, the study contributes to the theoretical understanding of family financial socialization by suggesting that parents’ financial teachings not only enhance their children’s financial capabilities but also serve as a frame of reference for young adults to recognize the process of attaining these capabilities.

It is important to note that the study has certain limitations. Although the study sampling served its purpose, future research should consider employing different recruitment strategies, such as focusing on young adults still living at home. Additionally, utilizing quantitative methods could help to hypothesize the characteristics of the phenomenon of financial agency. The study was conducted in Finland, and while the transition to adulthood for young adults may share similarities in other Western countries, there may be country-specific enablers and trajectories that influence the results. Therefore, further studies should explore the financial agency in other countries as well. The semi-structured interviews focused on young adults’ viewpoints of consuming and financial learning in families. However, the study indicates that financial matters are intertwined with overall life management issues. Thus, including the elements of young adults settling into the labour market and self-defined life events (such as finding a partner and having children) in the viewpoint of financial agency-building would be beneficial for expanding our understanding.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.