Abstract

With the emergence of blockchain technology, many firms have approached cryptocurrency by allowing their customers to use it as a form of payment. However, little research has examined firms’ acceptance of cryptocurrency, the unique strategies that have been undertaken, or the impact on firm-level outcomes. Drawing on signaling theory, the author applies the event study methodology to learn how firm value (i.e., stock price) is impacted by firms’ announcement of cryptocurrency acceptance. The author finds that, on average, firms have lost 2.73% in firm value as a result of announcing cryptocurrency acceptance. However, a moderation analysis reveals that firms that have chosen to accept Bitcoin (as opposed to focusing exclusively on alternative cryptocurrencies) and firms that have approached cryptocurrency acceptance in more recent years experience financial gains. The geographical location (i.e., domestic or international) of cryptocurrency acceptance is not found to have a moderating impact.

Keywords

Blockchain technology (Stallone et al. 2024) is altering the way consumers make financial transactions (Soilen and Benhayoun 2022), as cryptocurrency has emerged as a new store of value and medium of exchange. Since Bitcoin's introduction in 2009, the cryptocurrency market has grown tremendously, with a market capitalization exceeding $3 trillion (CoinMarketCap 2025). Over 562 million people own cryptocurrency (Helms 2024), with millions of daily transactions (Sangari and Mashatan 2024).

Cryptocurrency presents firms with an opportunity to achieve financial service innovation by leveraging blockchain technology to allow their customers to pay with this digital currency. Such innovation can reduce firms’ costs and address customers’ needs in unique ways. Firms such as Google, Ralph Lauren, and Chipotle have announced their acceptance of cryptocurrency as a payment method. By doing so, they can improve customer centricity as they enhance their interactions with customers (Stallone et al. 2024). Customers shopping in-store and online can benefit from a faster, more convenient, and more secure checkout process (Pasirayi and Fennell 2023) as they access their cryptocurrency through their existing mobile devices, while customers shopping through newer, immersive channels (e.g., metaverse) can purchase new (e.g., NFTs) and existing digital products seamlessly.

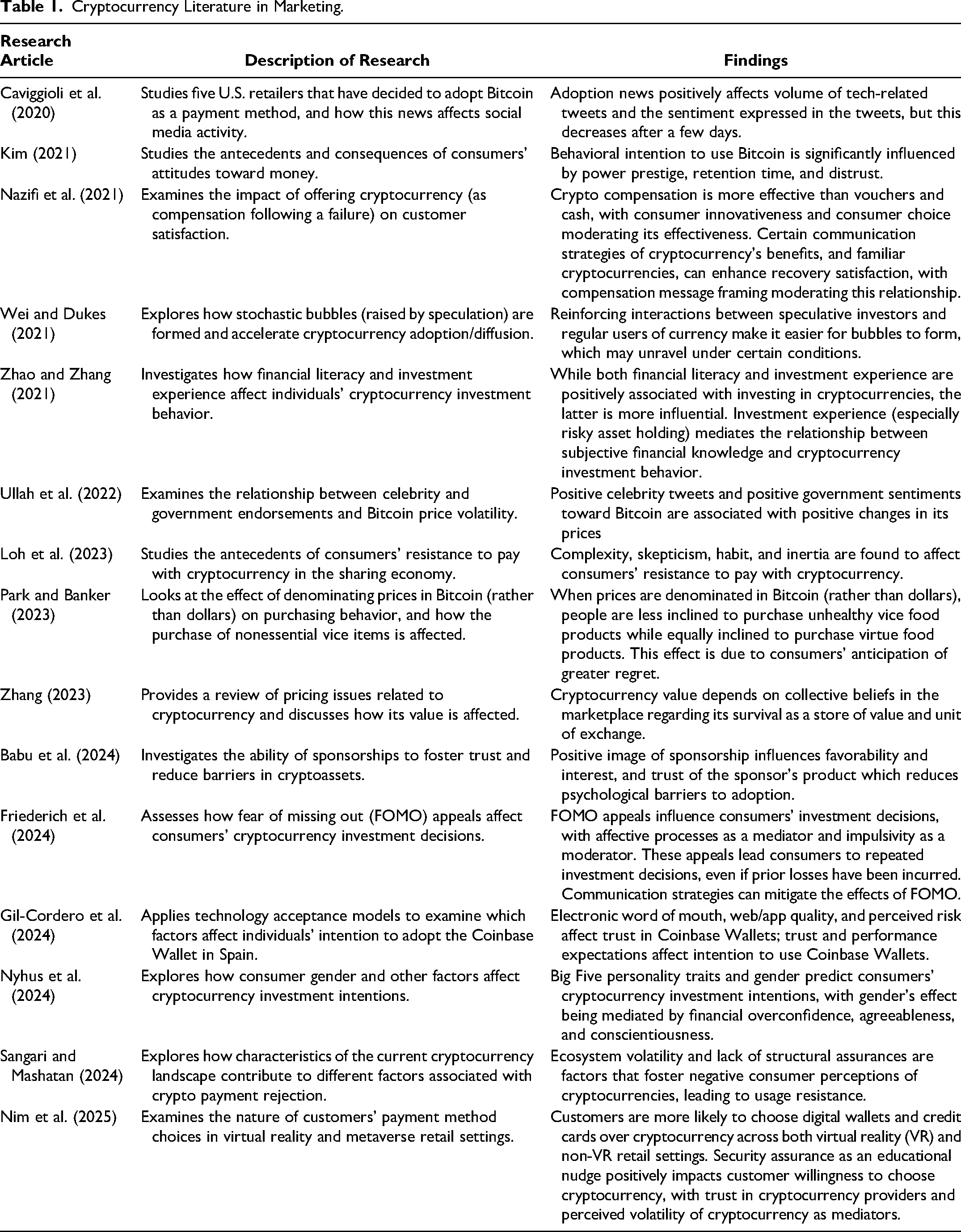

While some firms that have approached cryptocurrency acceptance (CA) have experienced positive outcomes (Deloitte 2021), this may not be the case for all firms; Expedia ended CA in 2018 with little explanation, and Dell ended CA in 2017 due to low demand (Whateley 2021). The market has continued to operate without an accurate understanding of the value of CA and how firms should approach CA strategically. Cryptocurrency research in marketing (see Table 1) has mostly focused on consumer-level outcomes (e.g., satisfaction, behavioral intention) rather than firm-level outcomes, although calls for such research have been raised (Hakkarainen and Colicev 2023).

Cryptocurrency Literature in Marketing.

To this end, the current research applies the event study methodology (Pasirayi and Fennell 2023) to assess the implications that CA has for firm value (i.e., stock price). Firms’ investors represent one of the first external stakeholder groups to assess the implications of innovations that firms announce to the public, and they either reward or penalize firms by buying or selling their stock (Sorescu, Warren, and Ertekin 2017). This feedback can provide strategic guidance to firms and allow managers to understand the conditions under which investors are receptive to CA. The current study's comprehensive dataset consists of all publicly traded U.S. firms that have announced CA, spanning from 2013 through 2023. The main effect of CA announcements on firm value is investigated, followed by a moderation analysis that explores the impact of unique firm decisions (i.e., which cryptocurrencies to accept, where to accept cryptocurrency, and when to accept cryptocurrency).

Conceptual Framework

With blockchain technology growing amid the fourth industrial revolution, which consists of additional new technologies such as the Internet of Things, virtual reality, and digital assistants (Krafft, Sajtos, and Haenlein 2020), CA has emerged as a new financial service innovation opportunity. Innovation is “the process of bringing new products and services to market” (Hauser et al. 2006), and its application to financial services can reduce firms’ costs, better address consumers’ needs, and allow firms to differentiate themselves (Nejad 2016, 2022). It can also enhance customer loyalty and advocacy, as consumers and their changing preferences are addressed (Nejad 2022; Sharma, Saboo, and Kumar 2018).

After innovations are conceptualized, tested, and refined, firms often announce them to the public, to share (previously) private information and generate interest. According to signaling theory, these announcements allow firms to convey credible information about unobservable product/service quality (Shin et al. 2024). One of firms’ initial external stakeholder groups to collect this information is their investors, who consistently monitor firms’ ability to effectively provide value to consumers (Bahmani, Bhatnagar, and Gauri 2022). Firms’ announcements reduce the informational asymmetry that investors experience (Bhagwat et al. 2020) by allowing them to better understand firms’ innovations and their implications for both consumers and firms themselves. In turn, investors’ perceptions may lead them to buy or sell stock, thereby affecting firm value (Bahmani, Bhatnagar, and Gauri 2022).

While firms explicitly reveal financial service innovation through their CA announcements, the implicit signal being transmitted to investors is firms’ strategic interest in blockchain technology. Although this technology was developed in 2009, firms gradually (and privately) took their time to assess how it could be properly leveraged. In the meantime, investors experienced informational asymmetry, as they waited to see if (and how) firms would recognize the value of this technology and ultimately adopt it. CA announcements therefore reduce this informational asymmetry and allow investors to more accurately evaluate blockchain technology (i.e., through a specific marketing application) and its accompanying characteristics—an evaluation that investors may shift onto the announcing firms (Caviggioli et al. 2020; Hou et al. 2018).

Firms’ CA announcements may be positively received by investors for a few reasons. First, investors may be receptive to the fact that firms can reach new customers, especially those with an innovative mindset who enjoy trying new things and tolerate uncertainty (Nazifi et al. 2021). This includes consumers who are becoming digitally connected with the metaverse (Hakkarainen and Colicev 2023) and are increasing the need for cryptocurrency as a transactional infrastructure for the purchase of virtual assets (e.g., property, apparel, NFTs) (Ooi et al. 2023). Over 80% of metaverse consumers pay primarily with cryptocurrency (Nim et al. 2025). Second, investors may recognize the cost savings that CA can produce for firms, which can also be passed down to consumers. Since cryptocurrency transactions are verified on the blockchain through predefined decentralized protocols, intermediaries (e.g., credit card companies, banks) are cut out (Komulainen and Natti 2023), which greatly reduces fees. Processing fees for credit cards can reach 3.5% (Forbes 2024), which can be reduced by 40% to 80% when cryptocurrency is used instead (Hakkarainen and Colicev 2023). Consumers may feel empowered when experiencing fewer fees (Nejad 2022), thus enhancing their usage likelihood (Gleim and Stevens 2021). Third, engagement with the blockchain may produce reputational benefits for firms, which investors value. Caviggioli et al. (2020) found that firms that added Bitcoin as a payment option experienced increases in volume (and positivity) of online word of mouth, as consumers perceive these firms as innovative. This could improve brand image and lead to enhanced sales, loyalty, and market share (Caviggioli et al. 2020). Finally, consumers may spend more when using cryptocurrency, which could further enhance firms’ cash flows. Noncash payment methods have been found to reduce consumers’ pain of payment, which can improve the shopping experience as consumers focus on the benefits afforded to them (Nim et al. 2025; Xu, Ghose, and Xiao 2023). In summary,

At the same time, investors may respond negatively to CA announcements. First, investors may worry that consumers may resist cryptocurrency adoption due to skepticism (i.e., doubting the benefits), complexity (i.e., usage difficulty), and habit (i.e., preferring existing payment options) (Loh et al. 2023). Effective firm-driven communication is needed to overcome these barriers (Babu et al. 2024), in addition to education regarding how to obtain cryptocurrency—an unfamiliar process that could result in errors (Ooi et al. 2023). Second, due to blockchain decentralization, regulation is limited and assurances cannot be provided. Consumers are not safeguarded if they make transactional mistakes or forget their blockchain passwords (Hakkarainen and Colicev 2023), which has cost them billions (Soilen and Benhayoun 2022). Malicious events (e.g., hacker theft) have also contributed to these losses (Komulainen and Natti 2023). The associated perceived risks may negatively affect consumers’ trust perceptions and likelihood of engaging with cryptocurrency (Babu et al. 2024; Sangari and Mashatan 2024; Zhao and Zhang 2021). Finally, cryptocurrency values are volatile (Belk, Humayun, and Brouard 2022), since demand factors affect them (Zhang 2023). This volatility poses two issues for firms. The first relates to the fact that the cryptocurrency market has been dominated by opportunists who seek cryptocurrency as a get-rich-quick opportunity (Anaza et al. 2022) rather than an alternative medium of exchange (Nazifi et al. 2021; Soilen and Benhayoun 2022). These speculators greatly impact cryptocurrency values (Wei and Dukes 2021), which could damage other individuals’ likelihood of regularly using cryptocurrency as a form of payment (Sangari and Mashatan 2024). The second issue relates to the fact that after customers’ cryptocurrency transactions take place, firms must monitor exchange rates and decide whether to exchange cryptocurrency for dollars right away (Wei and Dukes 2021) or retain it as a longer-term investment. Firms must recalculate prices regularly, which could become complicated and costly (Mkedder and Das 2024), thereby complicating investors’ expectations of positive cash flows. Thus,

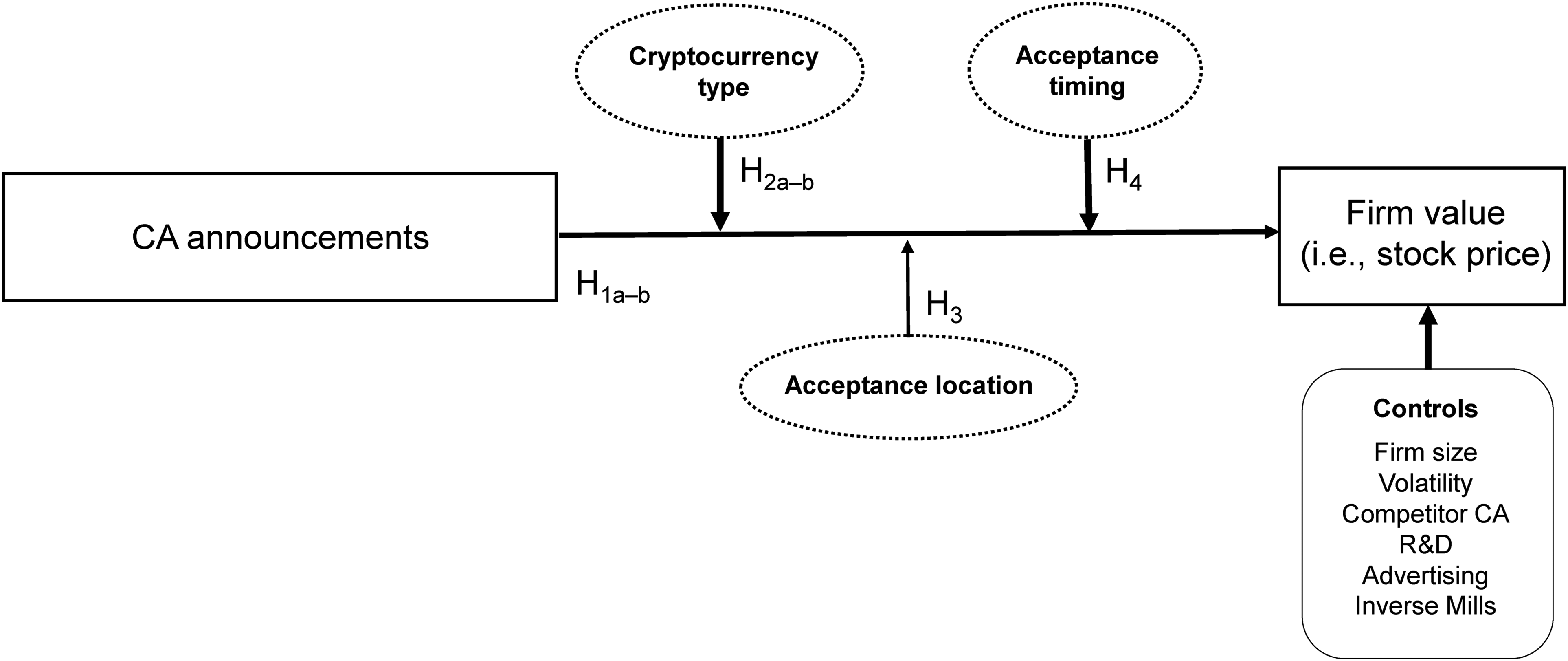

Although CA is expected to affect firm value, firms’ strategies do not follow a uniform path. As these strategies are revealed through firms’ CA announcements, additional signaling cues may lead investors to scrutinize firms for suboptimal decisions, thereby producing varying financial effects (Bhagwat et al. 2020). Next, these cues are explored more specifically, to understand how they may moderate firm value. The conceptual model is depicted in Figure 1.

Conceptual Model.

Cryptocurrency Type

A key decision relates to which types of cryptocurrency firms will accept, thereby signaling which ones they believe consumers are more likely to engage with. Currently, there are over 9,000 cryptocurrencies available (Statista 2024). Firms have taken one of three possible approaches thus far. Firms such as AT&T have chosen to exclusively accept Bitcoin (the original cryptocurrency), Fleetcor (now Corpay) has decided to focus exclusively on newer alternative cryptocurrencies (e.g., XRP), and AutoNation has chosen to accept both Bitcoin and alternative cryptocurrencies.

Although cryptocurrencies do not differ much in terms of volatility, they differ greatly in price (Flitter 2022). For example, at the time of this writing, one Bitcoin costs over $100,000, while alternatives such as Dogecoin cost less than $.50 (CoinMarketCap 2025). Because of this, firms may perceive alternative cryptocurrencies as more accessible, which could increase usage. However, cryptocurrency exchanges allow consumers to purchase any fraction of a cryptocurrency they desire (e.g., .05 units of Ether, equivalent to $100). Furthermore, when consumers connect their cryptocurrency wallets, product/service prices are displayed in fractional values (i.e., a $100 item is listed as .05 Ether). Therefore, consumers are unlikely to experience true accessibility concerns.

Since the primary difference between cryptocurrencies (i.e., price) is resolved through fractional purchasing, firms that avoid Bitcoin and decide to accept only alternative cryptocurrencies may be penalized by investors. First, alternative cryptocurrencies have made the market larger and more complex, which can complicate consumer adoption (Zhao and Zhang 2021). In addition, the increasing number of cryptocurrencies has diverted from the possibility of having an ideal, universal option that could better enrich consumers’ experiences (Mkedder and Das 2024). Second, consumer research has long posited that familiarity (i.e., the amount of exposure an individual has had to a stimulus) positively affects attitudes and preferences and allows consumers to better handle new product information (Nazifi et al. 2021). Consumers’ higher levels of familiarity with Bitcoin can aid their perceptions of its value and use cases, enhance perceptions of trustworthiness, and increase satisfaction (Nazifi et al. 2021), leading to positive word of mouth and repurchase—drivers of future cash flow that investors value (Luo, Homburg, and Wieseke 2010). In addition, Bitcoin has consistently remained the most popular cryptocurrency since its inception in 2009 (Zhang 2023), presenting an uphill battle for less popular alternatives.

In summary, avoiding Bitcoin and focusing exclusively on alternative cryptocurrencies may be a poor choice for firms, as this could signal a lack of properly understanding factors that guide consumers’ cryptocurrency preferences. As a result, these firms may witness negative financial effects as compared with firms that accept both Bitcoin and alternative cryptocurrencies. However, firms that focus exclusively on Bitcoin are expected to witness similar financial effects as firms that accept both Bitcoin and alternative cryptocurrencies, as offering both options is not likely to have negative consumer effects. Thus,

Acceptance Location

Next, firms have decided where to accept cryptocurrency. While many firms have decided to accept it primarily in the United States, nearly 20% have focused on other countries. For example, Pizza Hut announced CA in Venezuela, Burger King did so in Russia, and McDonald's did so in El Salvador. After all, cryptocurrency is a global currency that can facilitate cross-border transactions (Soilen and Benhayoun 2022).

By revealing this information, firms signal where they believe CA will initially be most beneficial and well-received. Investors may reward CA outside of the United States for a few reasons. First, non-Western financial markets are growing quickly, offering firms more robust financial returns (Nejad 2022). Such markets are highly interested in digital payment systems, with the average nation's share of cash transactions expected to decrease from 29% to just 17% by 2026 (Anaza et al. 2022). Finland is even planning to become completely cashless (Anaza et al. 2022), while El Salvador and the Central African Republic have adopted cryptocurrency as their national currency (Belk, Humayun, and Brouard 2022; Park and Banker 2023). Second, investors are becoming increasingly interested in developing economies due to an absence of legacy systems and young, growing populations (Nejad 2022). Some even have favorable government policies toward firms aiming to assist unbanked and underbanked consumers (Nejad 2016, 2022). Therefore,

Acceptance Timing

Finally, firms have decided when to begin CA. Overstock announced CA as early as 2013, while Honda waited until 2023 to do so. Through their CA announcements, firms implicitly signal their belief in when an entry into the cryptocurrency market will be most beneficial.

Firms that enter early can enjoy expansion effects and resulting consumer demand, with investors rewarding them as they establish first-mover advantages (Geyskens, Gielens, and Dekimpe 2002). These firms mainly target innovators (Babu et al. 2024), who may spread positive word of mouth and attract more consumers. However, following this, firms may experience high (and unexpected) time and monetary costs, as new technologies such as blockchain present a challenging learning curve (Geyskens, Gielens, and Dekimpe 2002) and the potential for failure (Komulainen and Natti 2023). Moreover, these firms must work to boost consumer adoption through marketing activities (e.g., advertising, sales promotion) whose effectiveness can take time to develop (Nejad 2016). In summary, firms in early stages of the market may experience positive, then negative, financial effects.

However, firms that enter later may again reap rewards, for two reasons. First, consumers’ benefit of adopting cryptocurrency increases as the number of firms accepting cryptocurrency rises (Wei and Dukes 2021), which could lead to a larger base of adopting consumers and greater usage. Thus, firms that announce CA in later periods of time are presented with more experienced consumers. Second, due to social pressures, consumers who hesitate to adopt cryptocurrency may decide to adopt it only after receiving approval from their peers (Kim 2021). Since individuals assess whether certain behaviors are socially and culturally approved (Kim 2021), they may wait for others to validate cryptocurrency before adopting it themselves.

In summary, investors’ response to CA is expected to follow a U-shaped pattern, as the benefits of CA shift over time.

Methodology

Collection of Data

Business news databases and other newswire services were used to search for and collect all CA announcements made by publicly traded U.S. firms (consisting of 4,000+ firms). Verification of whether any announcements were made in close time proximity to major firm events (e.g., quarterly earnings announcements, leadership changes) was conducted, since such events can produce confounding financial effects (Sorescu, Warren, and Ertekin 2017). None were found. The final dataset consists of 50 CA announcements occurring between 2013 and 2023—a sample size similar to prior event studies (e.g., Boyd, Chandy, and Cunha 2010).

Event Study Methodology

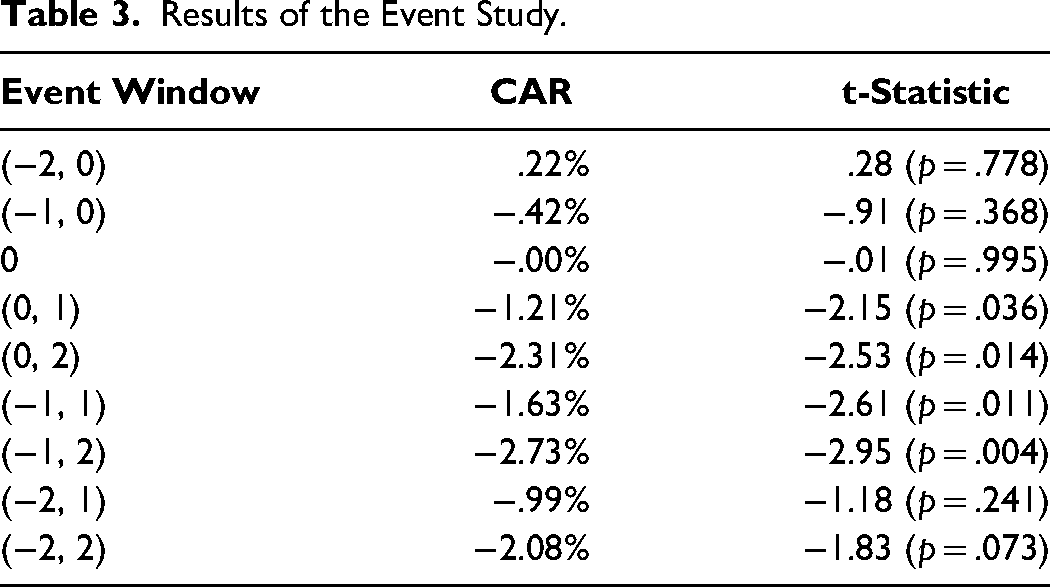

To assess the impact of CA announcements on firm value (i.e., stock price), this research incorporates an event study (Pasirayi and Fennell 2023). According to financial theory, the current price of a firm's stock reflects investors’ expectations regarding the discounted value of all future flows of cash that are expected to be amassed by the firm (Bahmani, Bhatnagar, and Gauri 2022), and reflects all information that is currently available. Since CA announcements reveal new information to the public on the day they are made (i.e., the event day), investors collect this information, recalibrate their perceptions of firms and their activities, and respond by buying or selling stock. This process can result in a novel effect on firms’ stock prices (i.e., abnormal return), which is commonly estimated with the market-adjusted model (Sorescu, Warren, and Ertekin 2017). Since an event's effects may manifest before the event day due to informational leakage, or afterwards due to media coverage delays or persistence effects (Bahmani, Bhatnagar, and Gauri 2022), abnormal returns are typically aggregated over several days (an event window) and termed cumulative abnormal return (CAR). CAR is estimated across a variety of event windows, with the most statistically significant window selected for analysis (Sorescu, Warren, and Ertekin 2017).

Independent and Control Variables

Values for several independent variables were assigned. First, AltCryptos (1 = a firm mentions that it is exclusively accepting cryptocurrencies that serve as alternatives to Bitcoin) and OnlyBitcoin (1 = a firm mentions that it is exclusively accepting Bitcoin) were created. Next, NonUSA (1 = a firm mentions that it is accepting cryptocurrency in a specific country outside of the United States) was developed. Finally, Timing (an index variable beginning with 1) tracks CA announcements chronologically. A quadratic term, Timing2, was also created.

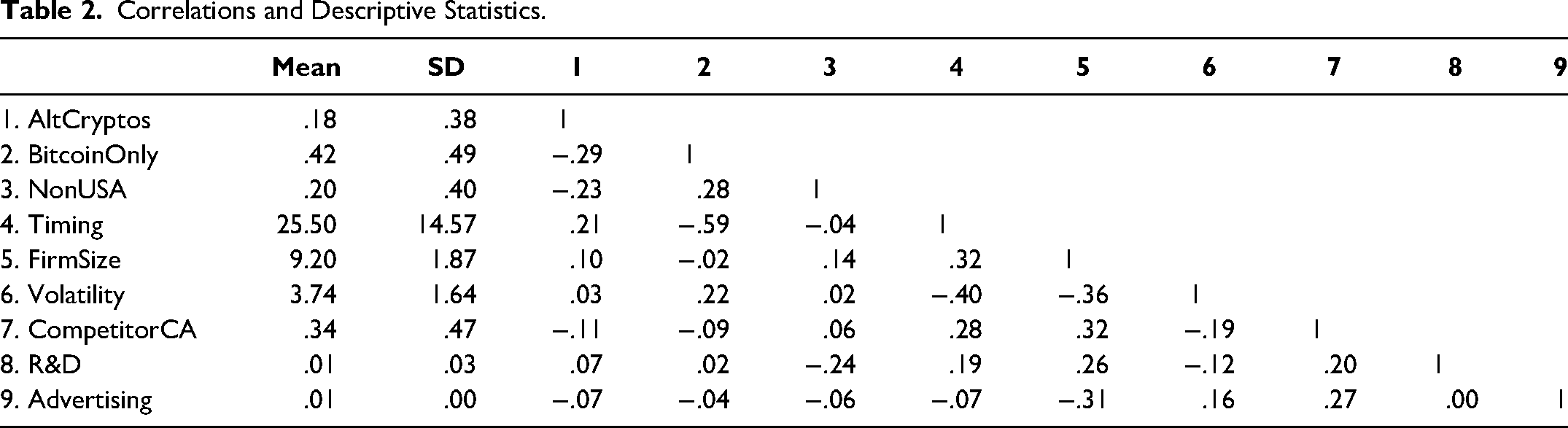

Several control variables were developed as well. FirmSize is calculated as the natural log of a firm's assets (Sorescu, Warren, and Ertekin 2017). Volatility represents the 30-day value (in %) of the cryptocurrency market's volatility (Newhedge 2025) at the time of a firm's CA announcement. CompetitorCA (a dummy variable) identifies whether a competitor within a firm's Standard Industrial Classification (SIC) industry has already announced CA. R&D is measured as the average five-year ratio of research and development expense to sales revenue for a firm's SIC industry (Hanson and Yun 2018). Advertising is estimated as the average five-year ratio of advertising expense to sales revenue for a firm's SIC industry (Bahmani, Bhatnagar, and Gauri 2022). Financial data were gathered from Compustat and the Center for Research in Security Prices database. Correlations and descriptive statistics are detailed in Table 2.

Correlations and Descriptive Statistics.

Accounting for Endogeneity

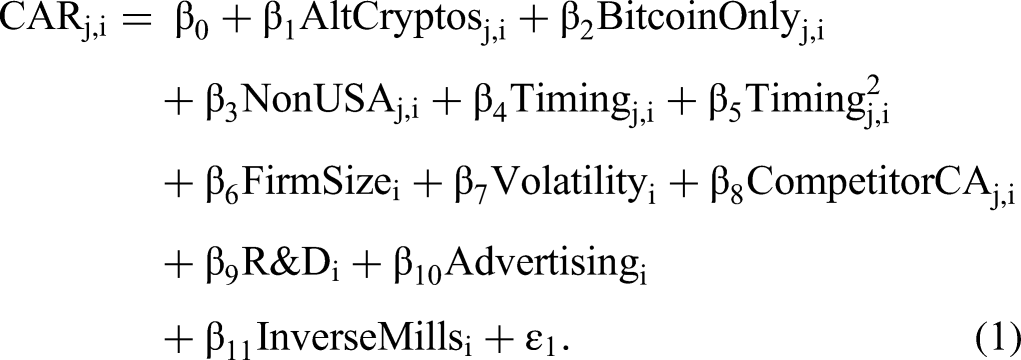

As this dataset consists of firms that have engaged in a similar type of activity, selection bias may be present (Pasirayi and Fennell 2023). In other words, unobserved factors may implicitly impact a firm's propensity to announce CA. This would signify systematic differences between announcing and nonannouncing firms and confound analyses of abnormal returns (Sorescu, Warren, and Ertekin 2017). Therefore, the Heckman procedure was employed (Bhagwat et al. 2020), which is explained in Web Appendix A. This procedure models a firm's likelihood of announcing CA and produces the inverse Mills ratio, which controls for selection bias. The current study's main model includes this variable and the independent and control variables to assess their joint impact on firm i's abnormal return as a result of CA announcement j, as follows:

Results

Event Study and Main Model

CAR was calculated over several event windows (see Table 3). Following Sorescu, Warren, and Ertekin (2017), the most statistically significant event window was selected for subsequent analysis, which spans one day before the event day through two days after [i.e., (−1, 2)]. This window reveals that, on average, firms have experienced a 2.73% decrease in firm value from announcing CA (t = −2.95, p = .004), in support of H1b. However, while 60% of the CA announcements in the dataset produced negative firm value effects, the remainder (40%) resulted in positive ones. Firms that made these announcements experienced, on average, a 2.01% increase in firm value. This stresses the importance of moderation analysis (i.e., the main model), which uncovers the strategic factors that lead certain firms to experience financial gains rather than losses.

Results of the Event Study.

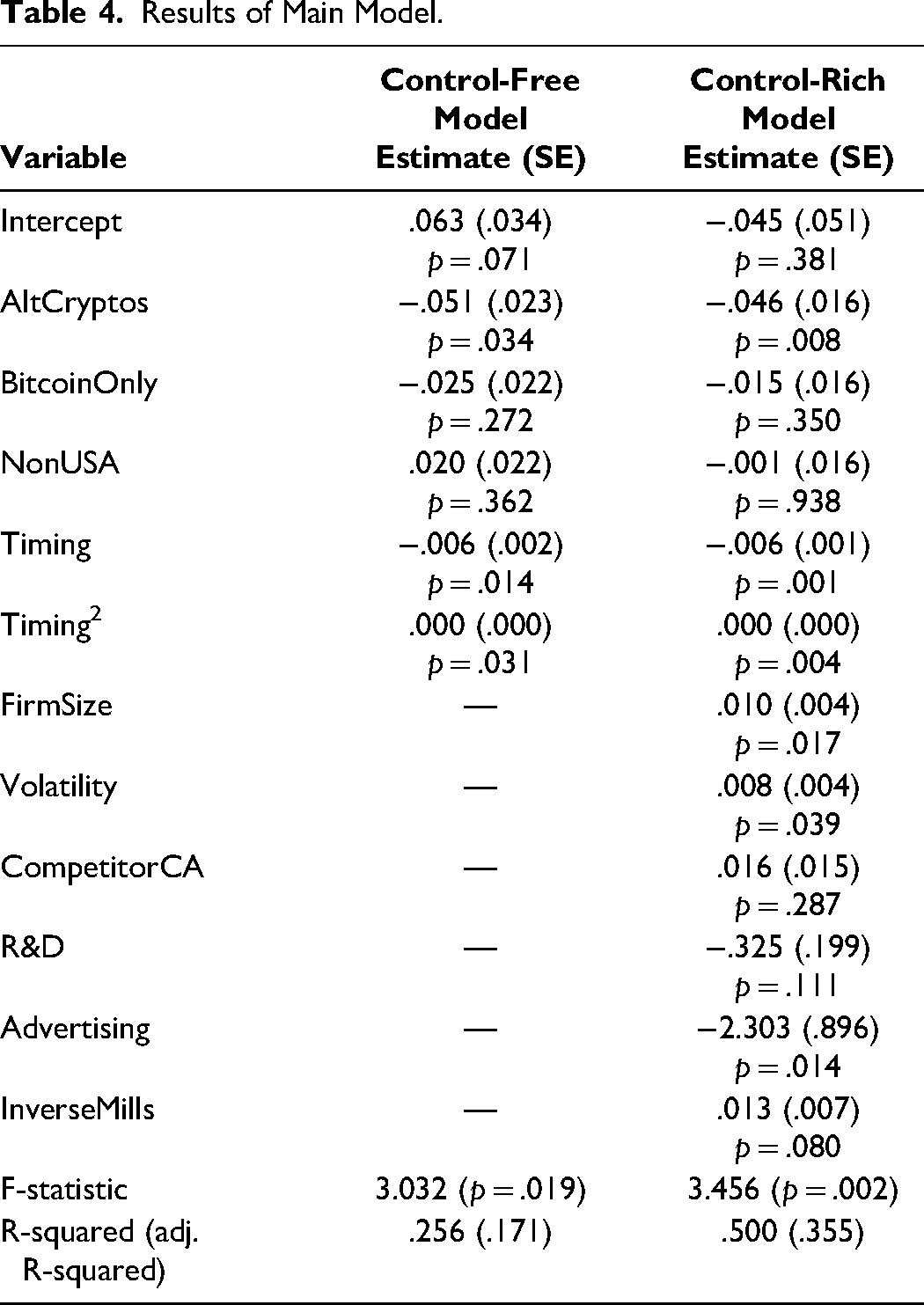

Next, Equation 1 was estimated to assess H2a through H4. The model fit is statistically significant (F = 3.45, p = .002), and multicollinearity tests reveal no concerns (variance inflation factors < 2). The results are provided in the third column of Table 4, with control-free evidence available in the second column. In support of H2a, AltCryptos has a significant, negative moderating impact on firm value (t = −2.77, p = .008). Investors penalize firms for exclusively focusing on alternative cryptocurrencies and not accepting Bitcoin. Regarding H2b, BitcoinOnly does not have a significant moderating impact on firm value (t = −.95, p = .350). Thus, firms that exclusively focus on Bitcoin are not treated differently than firms that accept both Bitcoin and alternative cryptocurrencies. In evaluation of H3, NonUSA is not found to have a significant moderating impact on firm value (t = −.08, p = .938). This suggests that investors are not concerned with whether firms choose to accept cryptocurrency domestically or in specific countries outside of the United States. Finally, in support of H4, the timing of firms’ CA has a nonlinear impact on firm value. With Timing carrying a significant negative coefficient (t = −3.40, p = .001) and Timing2 carrying a significant positive coefficient (t = 3.04, p = .004), a U-shaped relationship exists between announcement timing and firm value. In other words, investors’ response to firms’ CA began positive, then declined before improving again in recent years.

Results of Main Model.

Robustness Checks and Additional Analyses

The results are robust against outliers and across alternative event study calculation methods. Also, additional analyses revealed that (1) the effects of AltCryptos and Timing are unique and do not interact with each other, and (2) investors’ reactions to CA announcements are not industry dependent. Further details are available in Web Appendix B.

Discussion

With cryptocurrency promising consumers several benefits, many firms have approached CA. The current study's findings suggest that most firms have in fact been penalized by their investors for doing so. However, under certain conditions, firms are rewarded for CA. Next, the implications of this research and several avenues for future research are discussed.

Implications

From a theoretical perspective, this research supports signaling theory, as CA announcements stimulate significant reactions from firms’ investors. While these announcements explicitly reveal financial service innovation that firms have engaged in, they also implicitly signal firms’ strategic interest in blockchain technology. Thus, for the first time, investors are able to price their perceptions of both CA and blockchain technology into the market—perceptions that this event study reveals to be negative, on average.

Nevertheless, support is found for the notion that firms’ CA announcements carry multiple signaling cues, which investors closely assess to form more precise perceptions (Bhagwat et al. 2020) and treat firms differently based on the strategies they undertake. From a managerial perspective, this research presents a cautionary yet optimistic tale for firms. The moderation analysis reveals specific factors that lead investors to reward certain firms over others. First, it is found that the approach of exclusively accepting newer, alternative cryptocurrencies (e.g., Ether, Dogecoin) is negatively received by investors. In comparison, firms that accept Bitcoin (whether alone or in unison with alternative cryptocurrencies), the world's most popular cryptocurrency, experience firm value gains as a result. Second, the strategy of accepting cryptocurrency in countries outside of the United States is found to have no differential effect than accepting it domestically. This suggests that the firm value impact of CA is not improved or worsened by location strategy. Finally, as a U-shaped relationship between acceptance timing and firm value is discovered, firms can rest assured that the market is still ripe with opportunity. After an initially positive and then negative reception, in recent years, investors have again warmed up to CA and are willing to reward firms.

Avenues for Future Research

Several important avenues for future research are summarized in Table 5.

Future Research Avenues.

Footnotes

Editor

Beth Fossen

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.