Abstract

This study investigates the impact of Brexit uncertainty on the UK's services sector trade from 2016 to 2019 revealing a statistically significant negative impact that varied across sectors and destinations. Using the OECD-WTO Balanced Trade in Services dataset and synthetic difference in differences methodology, the findings indicate an annual shortfall of US$23.7/£18.5 billion in UK services exports compared to a scenario where the UK remained in the EU, translating to a 5.65 percent reduction. The bilateral data suggests an 8.5 percent average decline, with larger exports to countries like Germany and the US being less affected than smaller bilateral exports. The UK bilateral exports to the EU declined by 6.21 percent, while Ireland’s exports expanded by 21.4 percent. The study highlights that small firms were disproportionately impacted, leading to a decline in trade openness and export activities. Methodological sensitivity is underscored, with various approaches estimating Brexit’s impact differently. Sectoral analysis shows significant declines in Travel, Insurance, Finance, Telecom, Business and Cultural Services. Ireland notably benefited post-Brexit, experiencing a 14.75 percent annual increase in services exports due to business relocations. The study emphasizes the critical yet underexplored consequences of economic disintegration on international trade in services, providing essential evidence for future UK-EU trade relations post-Brexit.

Introduction

The Brexit referendum on June 23, 2016, signifying the UK’s decision to leave the European Union (EU), disrupted the deeply integrated services markets between the UK and EU developed over 45 years. This departure raised intricate questions about the future of services trade, affecting both domestic and international landscapes. Following the referendum, a prolonged period of policy uncertainty ensued, misaligning with the UK’s services sector strengths (Hall and Heneghan 2021). Understanding Brexit’s implications, including the introduced uncertainty, is crucial for evaluating economic disintegration’s real costs (Sampson 2017). Yet, precise assessments of Brexit’s impact on services trade are scarce because of the rarity of such disintegrations. Our study aims to address this, focusing on how UK services trade with the EU and globally has been affected.

As the world’s second-largest service market and the largest in Europe, the UK stands as a major services-based economy, with services’ value-added share of GDP more than 70 percent between 2012 and 2019. UK services sectors, notably professional, business, and financial services, contributes significantly through in terms of gross output, value-added, and job creation (Douch et al. 2020). Together with “other business services,” including research and development, professional and management consulting services, technical and trade-related services, these sectors generate a significant trade surplus for the UK, compensating for the large trade deficit in goods. In 2019, services exports accounted for 48 percent of all UK exports, generating a £112 billion surplus in services trade (ONS 2024).

Assessing the impact of Brexit uncertainty on UK aggregate exports and bilateral exports with the EU is complex. The existing literature on the role of policy uncertainty in services trade is limited. Economists generally agree that the UK’s exit from the EU’s customs union and single market may have more significant impacts on services than goods, especially on regulated services. This is due to the challenges in liberalizing services trade and the unparalleled trade liberalization achieved by the EU’s single market. As Lowe (2018, 2021) note, it is unlikely that future FTAs will achieve similar market access. Liberalizing services trade is challenging due to unique regulatory requirements and the intangible nature of services, necessitating close interaction between providers and recipients. This complexity is compounded by the industry’s heterogeneity, encompassing a wide range of sectors each with distinct business models and regulatory issues. The cost of trading services is higher than goods due to extensive regulations (OECD 2024), slow liberalization progress attributed to technological changes, and concerns over regulatory sovereignty (Hoekman and Mattoo 2011).

Services regulation is complex due to market failures, caused by imperfect competition, natural monopoly, and asymmetric information between customers and providers, as well as equity concerns, making services trade liberalization more challenging than goods trade one (Hoekman, Mattoo, and Sapir 2007). These characteristics impact trade, regulation, and necessitates unique management and delivery approaches and regulation heterogeneity (Francois and Hoekman 2010; Hoekman and Mattoo 2011; Mattoo et al. 2008). The rise of digital platforms introduces new regulatory challenges, including jurisdiction and data protection issues, emphasizing the need for a balanced regulatory approach.

Services, with their diverse range of industries from construction to health, exhibit greater heterogeneity than goods, featuring distinct business models and regulatory challenges. This diversity also applies to delivery modes, from non-tradable to digitally delivered services, including cross-border supply and the presence of natural persons. Brexit poses unique challenges for services trade, which relies on intangibility, perishability, and direct interactions. Restrictions on provider-consumer proximity and information flow could severely impact international services trade, especially under the WTO’s General Agreement on Trade in Services (GATS) modes like Cross-border (Mode 1) and Presence of natural persons (Mode 4). The UK’s exit from the EU’s customs union and single market risks greater consequences for services than for goods, due to the sector’s reliance on these factors. Technological advancements further blur the lines between tradable and non-tradable services, complicating the landscape. The UK’s previous integration in the EU’s service networks indicates potential significant shifts post-Brexit, potentially leading to at least a 16 percent reduction in bilateral services trade with the EU in optimistic scenarios (Mulabdic, Osnago, and Ruta 2017). Consequently, Brexit’s impact on services trade with the EU could be more severe than on goods trade.

The General Agreement on Trade in Services (GATS) within the WTO, implemented in 1995, aims to reduce trade barriers and ensure equal treatment for foreign service providers, although it allows for exemptions and flexible arrangements for economic and labor market integration, but the progress was very slow (UNCTAD 2020). On the other hand, the EU's internal market for services is more liberalized than the GATS principles, offering fewer restrictions and facilitating labor movement, highlighting the challenges UK service providers face post-Brexit. 1 The UK's exit from the EU marked a significant step back in service trade liberalization with EU countries, with anticipated substantial economic impacts, particularly in sectors like financial services, due to increased trade barriers and the loss of mutual recognition and free movement (Borchert 2016; Jozepa, Ward, and Harari 2019).

However, the other side of the argument points to the conspicuous absence of tangible alterations in rules and regulations governing UK-EU services trade during this timeframe (2017–2019). Consequently, not only is it challenging to identify evident causes for any potential impacts on UK-EU trade, but also establishing causality in this relationship presents a formidable challenge. Some argue that expectations varied by sector, with some fearing loss of EU market access, like Transport services, while others anticipated benefits from deregulation, especially in the financial sector, that could foster growth. Additionally, technological advances have lessened the reliance on face-to-face interactions, potentially facilitating access to non-EU markets, especially for digital services. These viewpoints suggest that Brexit uncertainty may not have significantly hindered UK services trade. Existing evidence shows that the Brexit uncertainty has hurt the UK trade as a whole in some significant way (Castelnuovo 2023). However, that evidence is mostly based on goods, with the evidence on trade in services being very limited (Ahmad, Limão, and Shikher 2020; Douch and Edwards 2021).

Empirically determining the impact of the Brexit referendum on the UK’s services trade is challenging, requiring constructing a counterfactual. We employ the synthetic difference-in-differences (SDID) method to identify the causal impact. Treating the 2016 referendum as a quasi-experiment, we estimate its impact on the services exports of the UK compared with other major services exporters, examining the heterogeneous effects across sectors.

This paper contributes to the literature in four ways. Firstly, we address the fundamental question of whether and to what extent Brexit uncertainty impacted UK trade in services during the period 2016–2019. Through the presentation of robust and innovative evidence grounded in rigorous causal analysis, we definitively resolve this debate. We find that UK aggregate services exports have declined by 5.65 percent, and bilateral exports to the EU have decreased by 6.21 percent following the Brexit referendum. This decline is contrasted by a significant rise of Ireland as a service economy, increasing its aggregate services exports by 14.7 percent and its bilateral exports to the EU by 21.4 percent. The significance of services within the UK’s economic landscape underscores the substantial costs associated with Brexit uncertainty. It is worth noting the intriguing aspect that service sectors were notably under-represented in the Brexit negotiations throughout this period, a phenomenon that continues to prompt speculation and inquiry.

Beyond the scope of this paper lies the exploration of whether this “price” to be paid for Brexit was a consciously anticipated and voluntary choice or an underestimated strategic misstep. Nevertheless, the evidence presented here serves as a catalyst for contemplation regarding the future of service industries in the post-Brexit era and in the face of potentially heightened uncertainty in future scenarios. Our second contribution is to show the importance of heterogeneity within services with the new evidence of the uneven impact across service sectors. The paucity of the research on the services trade is not only due to the lack of detailed and reliable sectoral, bilateral data, but also because of the general lack of research on the services trade and its policies (Buckley and Majumdar 2018). It is particularly challenging to study services because of the large heterogeneity of sectoral characteristics. In this case, the large variation of the impacts we identify among different service types shows that it is important to investigate sectoral differences to obtain a full picture.

Thirdly, this study makes a significant contribution to the expanding body of literature that investigates the effects of trade policy uncertainty, particularly in the context of Brexit (Handley and Limão 2022). Our research not only builds upon but also complements recent endeavors by scholars such as Bloom et al. (2019), Born et al. (2019), Douch and Edwards (2021), and Fernandes and Winters (2021), each employing various methodologies. While these studies collectively establish a negative impact of Brexit on UK trade, it is important to note that the estimated magnitudes vary considerably, and their primary focus has been on trade in goods.

Additionally, we demonstrate that the choice of methodology significantly influences the specific estimate of the magnitude of the Brexit impact. Our study underscores the multiple statistical advantages of the SDID method compared to the synthetic control (SC) method (Abadie, Diamond, and Hainmueller 2015; Abadie and Gardeazabal 2003) and several difference-in-difference (DID) approaches (Card and Krueger 1994), including modifications suggested by Doudchenko and Imbens (2016) and Ferman and Pinto (2019), particularly relevant when analyzing services trade as it delivers robust and efficient estimates of the effect for aggregated data.

The structure of this paper includes an overview of the contextual framework, an examination of factors influencing services trade under policy uncertainty, a discussion of the data and stylized facts about services exports, the methodology employed, the results of our analysis, a discussion of the findings, and a conclusion.

Background

Brexit and Policy Uncertainty

The Brexit referendum on June 23, 2016, marked the end of a 45-year era of close economic integration between the UK and the EU. This significant shift in the EU’s globalization efforts profoundly impacts the relationships among the UK, the EU, and the global economy. The unique aspect of this situation is that the UK did not immediately leave the EU. Instead, the 2016 referendum began a lengthy period of uncertainty, as the UK navigated the complexities of its EU departure.

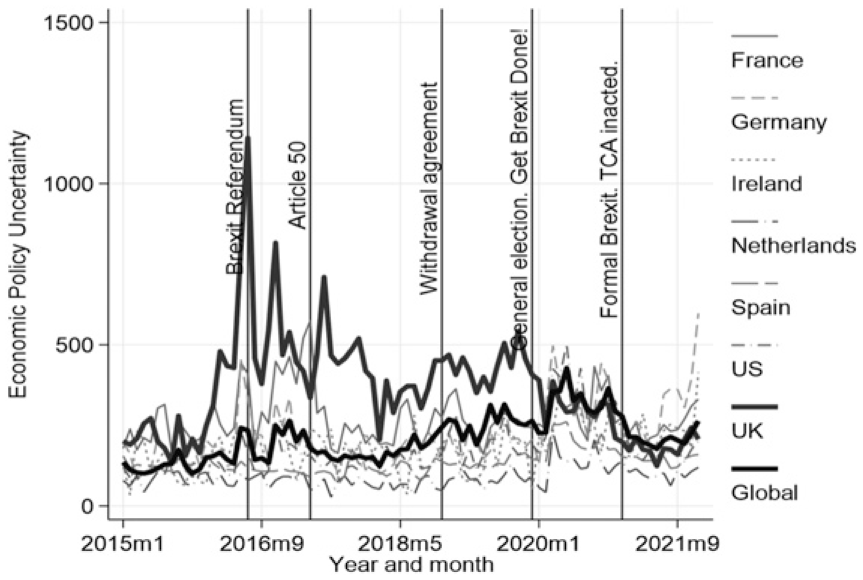

In 2016–2019, the UK policy uncertainty, measured by the economic policy uncertainty index (Baker, Bloom, and Davis 2016), was higher and more volatile than for other developed economies (Figure 1). Up until March 29, 2017, the primary source of uncertainty plaguing the UK services sector revolved around the formal triggering of Article 50 by the UK government to initiate the exit process. Over the subsequent two and a half years, an elevated level of uncertainty persisted, driven by the absence of a consensus on the specific form Brexit would assume. The political uncertainty eventually receded following the resounding electoral victory of the Conservative Party, championing the slogan “Get Brexit Done,” and the appointment of Boris Johnson as the new Prime Minister at the close of 2019. This marked the path for the UK's formal departure from the EU single market and customs union on January 31, 2020. Brexit uncertainty. Note: The figure shows the Economic Policy Uncertainty Index (Baker, Bloom, and Davis, 2016). Data are from https://www.policyuncertainty.com/.

Nonetheless, economic uncertainties concerning the future relationship with the EU endured during the Brexit transition period in 2020, as negotiations between the UK and the EU aimed to define the precise terms of the Brexit trade agreement between the two parties. The final agreement was ultimately reached on December 24, 2020. By this juncture, the extended period of enduring and widespread uncertainty across various facets of the EU-UK relationship had inflicted damage on the UK economy. It had led to diminished investment, weakened business and financial conditions, and a decline in household spending (Bank of England 2019).

Expectations About the Implications of Exiting EU: UK Falls to GATS Provisions

During the transition process, the implications of the UK exiting the EU and resorting to GATS provisions for its services trade were complex. Departing from the EU Single Market was expected to increase barriers to trade in services, a significant shift from the seamless trade within the EU. The Single Market has been instrumental in reducing administrative hurdles and allowing service providers to operate across member states with minimal friction (Borchert 2016; Jozepa, Ward, and Harari 2019).

A major change post-Brexit is the cessation of mutual recognition of professional qualifications between the UK and EU member states. This recognition enabled professionals to offer services across borders without needing requalification. Without it, UK professionals could face considerable barriers entering EU markets, navigating complex national regulations for authorization. The cessation of free movement between the UK and the EU impacts the mode 4 supply of services, which involves the temporary movement of workers. This restriction hinders UK firms’ ability to send employees to provide services in EU countries, affecting service trade dependent on physical presence.

Sector-specific impacts are significant. The financial services sector, which benefited from operating across the EU under a single license, could see a substantial reduction in exports to the EU. Studies suggest financial services exports to the EU could drop dramatically, risking billions in revenue (Borchet 2016).

Brexit’s implications extend beyond immediate trade barriers. The EU’s draft mandate for future trade relations suggests going beyond WTO commitments but with restrictions and exclusions, such as audio-visual services. Possible accommodations in areas like commercial presence (Mode 3) and temporary movement of workers (Mode 4) are unlikely to match current access. The concept of “equivalence” for financial services offers limited comfort due to its patchy composition and political uncertainties.

The shift to GATS provisions represents a significant step back in service trade liberalization. The loss of mutual recognition, free movement, and increased barriers across sectors highlight the challenges for UK service providers in accessing the EU market. The economic impact is anticipated to be substantial, with sectors like financial services facing significant changes, ultimately affecting the broader UK economy.

Theoretical Background and Research Questions

To address the dual-sided argument presented in the introduction, we engage with the complex question of Brexit uncertainty’s impact on services trade. The theoretical considerations will guide our empirical investigation and originates from economic theories detailing uncertainties’ effects on the economy and trade outcomes. MNEs play a crucial role, representing a significant portion of service-trading entities. Examining their motivations for investment and adaptive responses to uncertainty through international business theories is essential. Additionally, we integrate sector-specific insights to deepen our exploration.

Trade Policy Uncertainty and International Trade Dynamics

The field of international economics emphasizes the reliance of trade flows on the predictability and stability of trade policies and future trading frameworks. This dependency arises from the substantial initial investments required to embark on exporting activities, as highlighted by Anderson and Van Wincoop (2004). Trade Policy Uncertainty (TPU), characterized by ambiguity or unpredictability in future trade policies, undermines firms’ ability to make informed planning and investment decisions. TPU encompasses uncertainties surrounding tariff rates, trade agreements, and regulations impacting international trade.

The foundational theory of TPU in business and economics examines the impact of potential future changes in trade policies on investment decisions. Notably, Bloom (2009) has demonstrated that economic uncertainty leads to delayed investment. In the context of international markets, higher levels of TPU predicts that firms will likely delay entering new markets and respond less actively to tariff reductions (Handley and Limão 2015). Such conditions can deter firms from expanding or further investing in existing international ventures.

Volatile trade policies or future trade restrictions pose risks by disrupting supply chains, elevating costs, and narrowing market opportunities, thus affecting market expansion and efficiency. Firms might hesitate to invest in new markets or adjust supply chain strategies if the future trade policy landscape remains uncertain. Moreover, TPU differentially impacts firms’ trade engagement and performance, as explored by Limão and Maggi (2015), Handley and Limão (2017), and Pierce and Schott (2016). Trade policy uncertainty can effectively act as a tariff increase, with trade agreements serving as crucial mechanisms to mitigate policy uncertainty, as demonstrated in studies by Handley and Limão (2015) and Carballo, Handley, and Limão (2022).

Location Choice of Multinationals

Foreign-owned businesses are responsible for 56 percent of UK’s annual services exports (excluding financial, insurance and transport services) in the UK in 2019 (Lowe 2021). Understanding these firms’ motives and how they respond to economic uncertainty is critical.

Countries compete for inward investment, recognizing its potential to generate employment, contribute to GDP, facilitate direct technology transfers, and spur host country productivity, wage growth, and innovation (Blomström, Kokko, and Globerman 2001). Such investments can also significantly alter local industrial landscapes (Barry and Kearney 2006).

The factors attracting MNEs to specific locations are varied, driving interdisciplinary research across International Trade, International Business (IB), and Economic Geography (Iammarino and McCann 2013). Traditional trade theories describe FDI as a strategy for MNEs to optimize productivity and efficiency, with vertical FDI driven by cost differentials (e.g., labor, materials) from developed to developing nations, and horizontal FDI minimizing transport costs and capitalizing on brand recognition by establishing operations near consumer markets in developed countries (Krugman, Obstfeld, and Melitz 2018). Modern trends show MNEs investing in cost-effective, developed nations to support export platforms and foster innovation ecosystems (Dachs et al. 2024; Helpman 2006). Initially, IB strategy research emphasized macro-level country-specific advantages (CSAs) like natural resources, institutional quality, and market size (Dunning 1992). Although recent scholarship has shifted towards micro-level corporate strategies, CSAs remain crucial. Current theories suggest MNEs must leverage CSAs in host countries—such as labor availability, knowledge clusters, or large markets—to enhance their global efficiency (Mellahi et al. 2021).

Brexit has cast uncertainty on the UK’s ability to retain and attract FDI. Pre-Brexit, the UK’s liberal economic policies, substantial market size, and robust growth made it appealing for scaling investors (Driffield et al. 2013). Its open economy facilitated robust trade and FDI, ranking high globally and within Europe, particularly in service sectors. MNEs were attracted to the UK’s integration in global value chains, producing a diverse and knowledge-intensive range of products and services (Du and Shepotylo 2021). The UK’s institutional quality, expedient business setup processes, proactive investment policies, competitive corporate tax rates, and labor market flexibility further added to its allure (World Bank 2020). London’s prominence in global financial and business services and its talent pool underscored the UK’s status as an investment hub. However, the severance of EU ties has raised questions about the UK’s capacity to attract export-platform FDI. Multinationals previously saw the UK as a gateway to the EU, utilizing its advantages to serve the larger EU market (Tamberi 2024). The potential post-Brexit loss of passporting rights and restrictions on professional and business services are substantial deterrents. Concerns about market access, professional mobility, and impending divergences in data protection laws may redefine the UK's role as a service provider and investment destination (Breinlich et al. 2020). The relocation or redirection of future investments of UK multinationals to EU territories, anticipated during Brexit, could reduce economic outputs and exports from the UK (Dhingra and Sampson 2022; Douch, Du, and Vanino 2019).

Economic Policy Uncertainty and Market-Based Uncertainty

Economic policy uncertainty (EPU) and market-based uncertainty significantly influence business decision-making and operational frameworks, extending beyond trade policy uncertainty. EPU covers economic, regulatory, and market phenomena, shaping corporate strategies and growth patterns, and impacting the service industries (Baker, Bloom, and Davis 2016). Market-based uncertainty includes sudden changes in market sentiment, financial bubbles, or negative forecasts, which are unpredictable due to economic model limitations (Müller and Hornig 2020). These uncertainties interact and cascade, affecting the economy through identifiable channels.

One notable channel is the impact of economic and regulatory uncertainties on investment and expansion within service sectors. The significant capital required for technology, infrastructure, and human capital makes these uncertainties formidable barriers. Firms, faced with such uncertainties, delay or scale down long-term projects. Bloom (2009) highlights how economic and regulatory ambiguities corrode investor confidence, impeding resource flow towards growth-focused initiatives.

Uncertainty adversely impacts consumer and business confidence, curtailing discretionary spending in sectors like leisure, travel, and luxury goods Global supply chains, essential for service industries, are at risk from geopolitical uncertainties and trade disruptions, potentially fragmenting supply chains and increasing costs and complexity (Baldwin 2016; Majeed and Moore 2019).

Economic uncertainty also deters R&D and innovation investments, crucial for a competitive edge in service industries. Firms may scale back on R&D due to uncertain regulatory or market conditions, stifling innovation (Piva and Vivarelli 2018). Service industry labor markets are vulnerable to policy uncertainty, affecting hiring and wage practices, especially in skilled labor-dependent sectors, amid restrictive post-Brexit immigration policies (Acemoglu and Restrepo 2019).

Increased EPU levels correlate with reduced global credit availability, such as diminished stock market liquidity in G7 economies (Dash et al. 2019), challenging service industries’ access to capital. Persistent uncertainty hinders long-term strategic planning, potentially intensifying negative repercussions on the UK’s service trade with EU partners and diminishing its investment appeal, linked to the locational choices of multinationals.

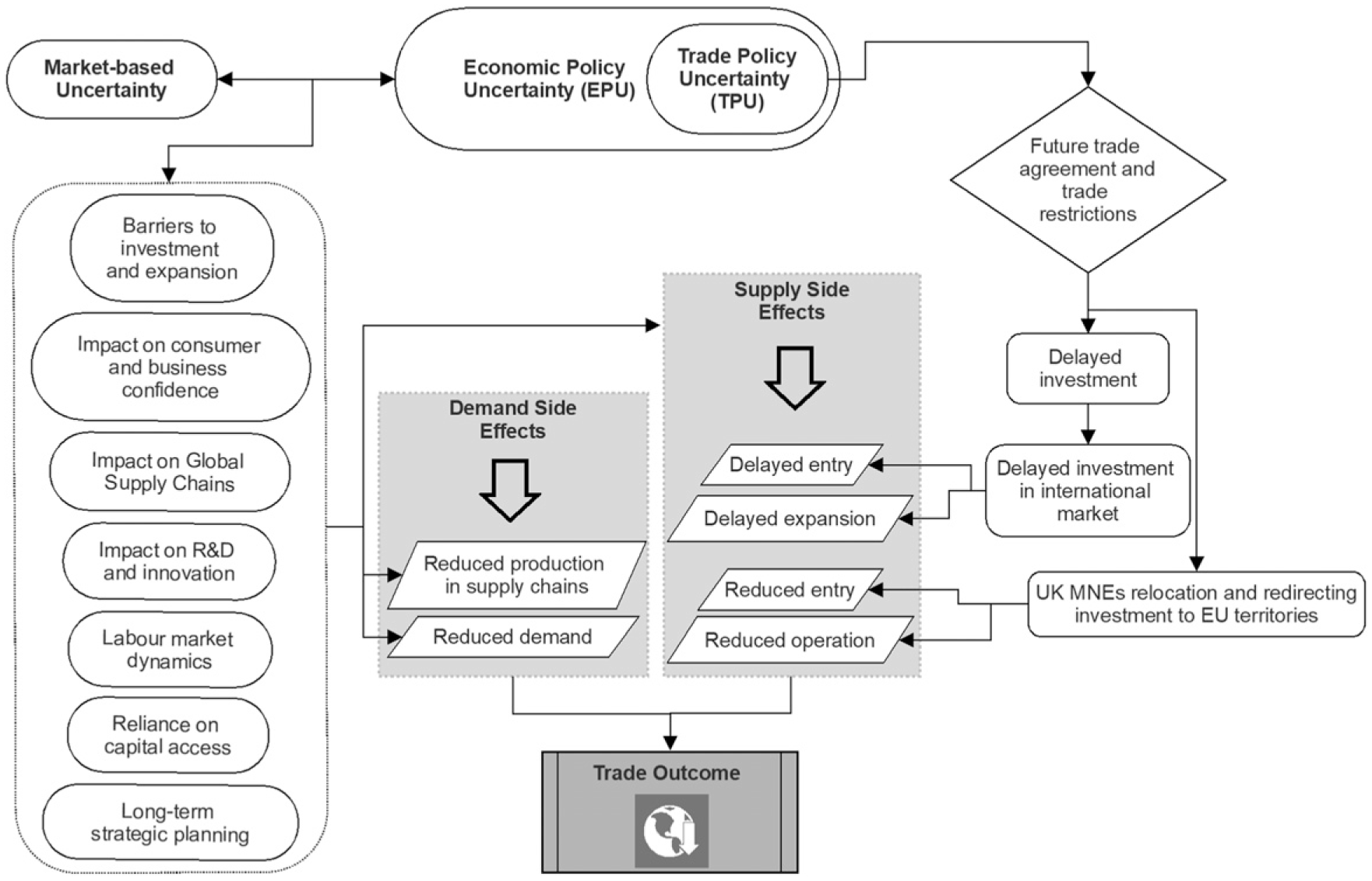

In summary, Brexit uncertainty—a confluence of various uncertainties—affects trade outcomes, highlighting the complexity of these impacts and the difficulties in predicting precise outcomes, as outlined in Figure 2. Empirical analysis is essential to understand the broad effects of these uncertainties on trade dynamics. This leads to our primary research question: Brexit uncertainty and trade outcomes: A conceptual framework.

How does Brexit uncertainty impact UK services trade?

Sectoral Differences in Response to Brexit Uncertainty

Analyzing how UK service sectors respond to Brexit uncertainty requires integrating theoretical insights and empirical data, acknowledging the diversity among sectors. Theoretical models provide a general framework, but unique sector attributes dictate specific reactions to uncertainty.

Potential shifts in country-specific advantages (CSAs) vary significantly across sectors. The Resource-Based View (RBV) of management highlights the importance of a firm's distinct resources and capabilities in securing a competitive edge (Barney 1991, 2001). MNEs often aim to enhance productivity and efficiency, driven by cost differences between countries. Horizontal FDI, aimed at market proximity and developing innovation ecosystems, predominantly occurs among developed nations. Consequently, the attractiveness of service sectors for multinational investments hinges on their ability to exploit host CSAs, such as global service networks, broad market access, regulatory frameworks, skilled labor, innovation capacities, and local knowledge spillovers.

The UK's exit from the EU single market and customs union was expected to significantly alter some of the UK’s location-specific advantages, especially affecting service sectors and supply chains. MNEs in the Financial, Insurance, and Professional services sectors faced pronounced challenges, such as the loss of “passporting” rights for cross-border financial services. Additionally, “national reservations” restrict EU market access for professional and business services, and data protection uncertainties could disadvantage UK-based firms in cross-border operations, affecting sectors like Telecom and Cultural services. These developments have prompted businesses to consider relocating to the EU for a more stable investment environment, diminishing the UK’s attractiveness for firms seeking EU market access. Alternatives like Ireland have become more appealing due to lower relocation costs for certain business functions, such as financial services, compared to more complex and costly relocations in sectors like transport.

The impact of Brexit varies across sectors due to differing levels of regulatory reliance (Scott 2013). Institutional Theory suggests that some sectors depend more on regulatory frameworks for effective functioning. For example, the Insurance sector, operating within a complex regulatory environment, faces challenges post-Brexit with potential regulatory divergence affecting competitiveness. Sectors like Travel and Transport, including Aviation and Shipping, are governed by extensive regulations. Anticipated trade barriers and reduced competitiveness disproportionately impact firms in these sectors engaging with EU customers.

In summary, Brexit’s impact is not uniform across sectors; certain ones are more adversely affected due to the loss of competitive advantages. This includes the Financial, Insurance, and Cultural sectors, while Travel, Transport, and Telecom face challenges from regulatory changes and potential divergences, hindering investment and growth. Recognizing these sectoral differences is essential for targeted and effective decision-making during these uncertain times.

How have different services sectors responded to the Brexit uncertainty?

Landscape of UK Trade in Services

Services trade data are not as readily available as data for the goods trade. The inherent complexity of recording services, especially when delivered in digital form (OECD 2019), results in only a handful of countries publishing (some) bilateral trade in services statistics, with asymmetric reporting by partner countries and service categories. This has made the analysis of the services trade challenging. To mitigate these problems, the OECD and the WTO have recently developed a global dataset of coherent bilateral trade in services statistics according to the main services categories, building upon the WTO-UNCTAD Trade in Services Database.

In this paper, we draw on the latest edition of the OECD-WTO Balanced Trade in Services dataset (BaTIS), which is currently the most comprehensive, consistent, and balanced data on bilateral trade in services, which in addition to the total bilateral trade between 201 countries, also includes data on trade at sectoral level for 12 main EBOPS 2010 services categories in 2005–2019. The advantages of this database lie in the fact that efforts have been made to resolve the unbalanced and missing services trade flows in the data, which considerably enhances the data quality (Liberatore and Wettstein 2021). The data are available for 2005–2019, but for most of our analysis we have chosen the period of 2012–2019 to deliberately exclude the financial crisis period of 2008–2009 and the European debt crisis in 2010–2011. The included period allows us to compare the period of 2016–2019, which covers the post-Brexit Referendum, with the previous 4-year period. Appendix A presents the data and gives background on the UK trade in services in detail.

Identification

The empirical analysis estimates the effect of the Brexit referendum and associated period of uncertainty, discussed in the background and conceptual framework sections, on the UK-EU bilateral services exports since 2016. Unlike several related papers that view Brexit as a natural experiment employing DID methodology (Crowley, Exton, and Han 2018), we argue that Brexit is not a randomized policy experiment and requires a carefully constructed counterfactual for comparison. The identifying assumption of parallel trends between treated and control units is compromised by the presence of unobservable, time-varying confounders. A prolonged period of dissatisfaction with the UK's economic performance since 2008 (Fetzer 2019) indicates that the demand for policy change was not random, challenging the parallel trend assumption, as further analysis will demonstrate. Additionally, the referendum's outcome was highly uncertain, with many observers initially predicting a victory for Brexit opponents (“For the vast majority of the campaign, both polls and markets had ‘remain’ with a solid lead” Economist 2016). Therefore, while the policy’s timing may seem clear post-results announcement, assuming the policy’s application to the UK as a random occurrence is likely flawed.

To construct a counterfactual scenario to identify the causal effect of Brexit is essentially to build a doppelganger, or a what-if scenario that never actually occurred. The field of causal inference has evolved significantly. It started with the simple Difference-in-Differences (DID) approach, as introduced by Card and Krueger (1994). The development of the Synthetic Control (SC) method introduced by Abadie and Gardeazabal (2003) was a significant improvement. SC is more reliable when these parallel trends are violated. However, it requires a significant amount of historical data for accurate pre-event analysis and does not easily facilitate standard statistical tests for hypothesis testing, as noted by Abadie, Diamond, and Hainmueller (2015). To derive a causal interpretation of Brexit’s impact, we model the unobserved counterfactual with observed data using the SDID estimator (Arkhangelsky et al. 2021).

Synthetic Difference-In-Difference Estimator

Synthetic Difference-In-Difference combines the advantages of the SC and the DID methods. SC usually performs well when the number of treated units is small and there are no or few comparable non-treated units. SC method matches pre-treatment outcomes, making the good pre-trend match as the criteria and provides weights for the control units, making the method transparent and available for further analysis and interpretation. At the same time, it is poorly suited to drawing statistical inferences about the properties of the estimator. DID, on the other hand, allows for estimating the treatment effect within a standard linear model with two-way fixed effects, but it requires the treated and non-treated units to follow parallel pre-trends. DID works well when the number of treated units is large. However, SDID relaxes the parallel trend requirements, works robustly when the number of treated units is small, and, more importantly, allows for drawing statistical inferences within the usual regression framework.

Synthetic Difference-In-Difference is well suited to estimating the casual Brexit effect on services exports since the treatment occurred simultaneously for all treated units, and the number of the treated units is only 1. It may be argued that the treatment is primarily applied to the bilateral trade of the UK with its EU partners rather than with the rest of the world. This is a plausible hypothesis that we also explore. Detailed presentation of the method is given in Appendix B.

Results

We first present the results for aggregate services trade. We aggregate bilateral trade by exporter and time to demonstrate the SDID method in detail and discuss the main effects at the country level. We then advance our analysis to more granular data, considering both bilateral and sectoral levels of services trade and also consider effect on the UK trade with the EU.

Aggregate Analysis of UK Services Trade

We begin by analyzing the UK’s aggregate trade flows in comparison to those of other countries in the dataset, according to the following estimated equation:

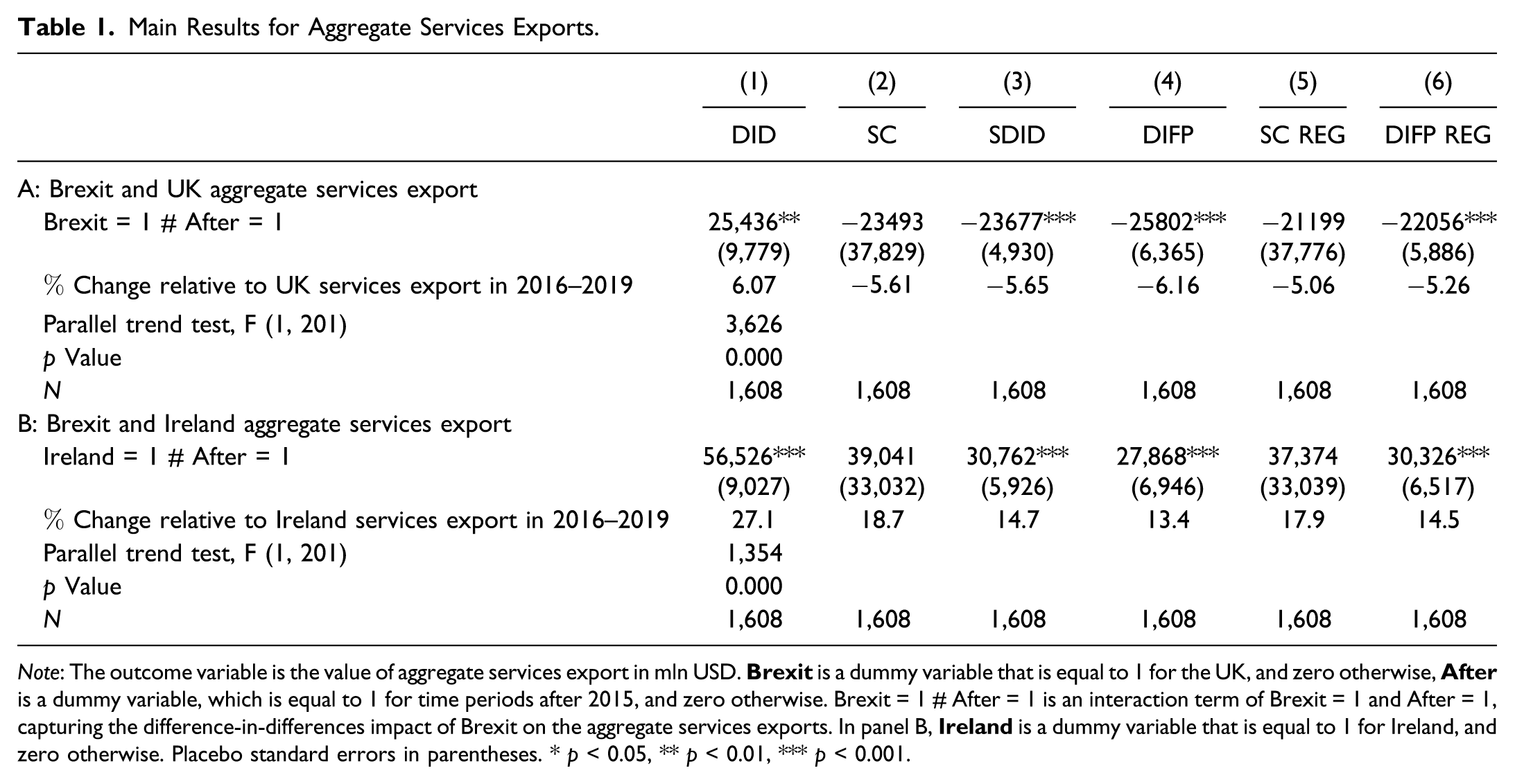

Main Results for Aggregate Services Exports.

Note: The outcome variable is the value of aggregate services export in mln USD.

Overall, we regard the estimate in column (3) as the most robust estimate of the impact of Brexit on the UK’s aggregate services exports. The estimate is negative, large, and statistically significant at 0.1 percent. The decision to exit the EU has resulted in US$23.7/£18.5 bln 3 lower services exports relative to what the figure would have been had the UK not exited from the EU. It translates into 5.65 percent lower services exports than the 2019 level of aggregate UK services exports. The other methods, with a noticeable exception of DID, agree on the magnitude of the effect in the range of 21.2–25.8 bln USD.

We further consider the impact of Brexit on the services exports of Ireland in panel B of Table 1, as that country has seen an unprecedented surge in services exports starting around 2015–2016. The estimated equation is the SDID estimator of the causal effect, which generates a positive and significant effect at 0.01 percent level. In 2016–2019 Ireland experienced US$30.8/£24 bln higher aggregate services exports annually, which is 14.7 percent of its 2019 services exports. As was the case for the UK, the DID estimate is not consistent due to the violation of the parallel trend assumption and it differs considerably from the other estimates. We present more detailed description of results, including diagnostic figures on weights as well as the results for Ireland in Appendix C.

Bilateral Sample Analysis of Overall and Sector-Level Services Flows

We further proceed with the analysis of more granular data considering the bilateral UK trade and the impact of uncertainty post-Brexit referendum on the UK bilateral services exports with the EU and the rest of the world.

Impact of Brexit on bilateral exports

After establishing the advantages of the SDID method in comparison with DID, SC, and their modifications, we proceed with our main analysis using bilateral trade data. The utilization of bilateral data offers several advantages: (a) enhanced control over the treated and control groups, enabling a more accurate estimation of the Brexit impact on overall UK exports and UK exports to the EU; (b) inclusion of multiple treated units, leading to improved precision in the estimates; and (c) selection of an appropriate method for calculating standard errors, such as bootstrapping, which is preferable to using placebo standard errors, as discussed by Arkhangelsky et al. (2021).

Employing a bilateral sample increases the sample size, although the expansion does not necessarily result in improved estimations and requires additional considerations on the choice of the estimated sample. Several reasons support the preference for a limited sample in our analysis. Firstly, the inclusion of very small services exporters and importers who engage in occasional trading, particularly when examining the analysis at the sectoral level, introduces a substantial noise in the data due to larger measurement error and intermittent nature of the less aggregate exports flow, reducing a signal to noise ratio, which is the crucial characteristic of the data when using SDID (Arkhangelsky et al. 2021). More granular data also makes it problematic to calculate export series when zero trade flows happen more often. Furthermore, the data quality for these countries is notably inferior compared to that of major exporters, resulting in a significant measurement error, particularly in relative terms. BATIS data set deals with quality of data and balancing to a great extent, but the information for small services exporters, especially in the sectors with low and irregular flows, is less reliable. This, in turn, leads to the attenuation bias and higher standard errors in the resulting estimates.

Secondly, the computational complexity of SDID methodology exhibits a non-linear increase in computation requirements and time, surpassing a growth rate of

To deal with computational complexity and noise in the data in the bilateral model, we consider a baseline sample of the top 27 services exporting countries and an extended sample of the top 67 services exporting countries in 2012–2019, which consequently represent 80 percent and 95 percent of services trade in 2012–2019. The remaining countries are combined into the Rest of the World group, so no information is lost as the result. Table A5 in the Appendix provides information about the sample composition for both samples.

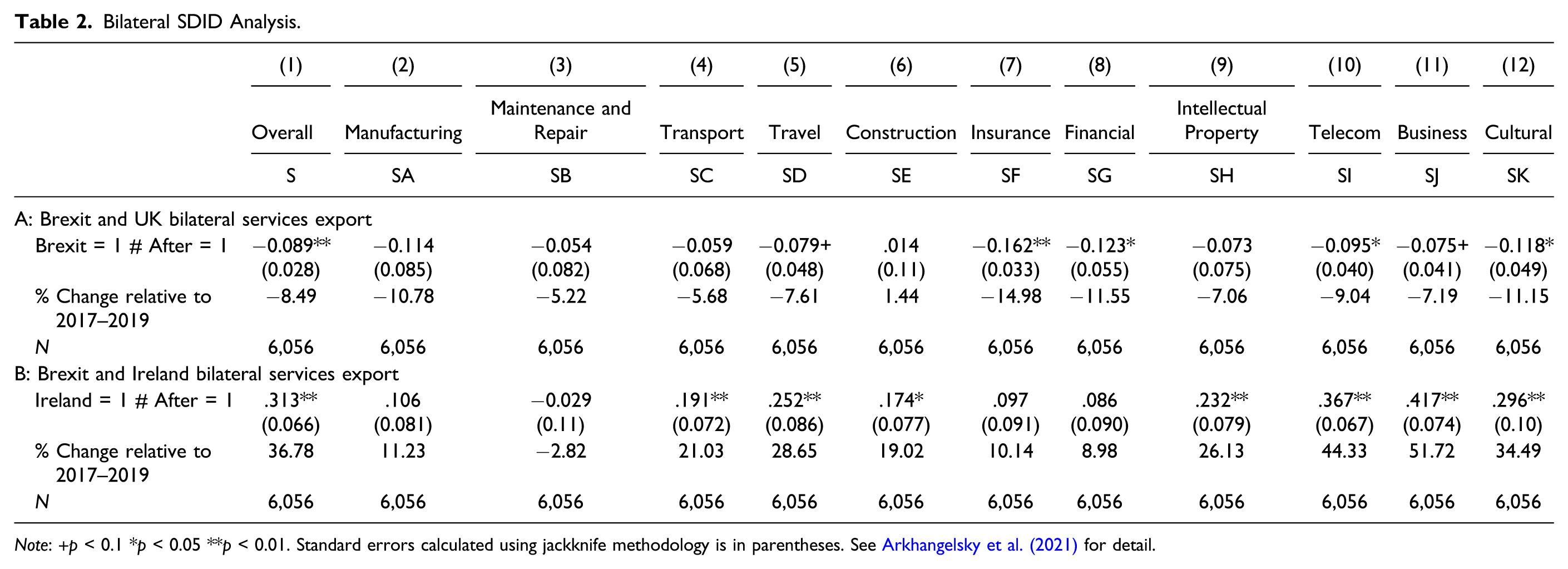

Bilateral SDID Analysis.

Note: + p < 0.1 *p < 0.05 **p < 0.01. Standard errors calculated using jackknife methodology is in parentheses. See Arkhangelsky et al. (2021) for detail.

There is a negative and significant impact of Brexit on the UK services exports of 8.5 percent, which is above the 5.7 percent impact estimated on the aggregate export flows. It indicates that the smaller bilateral pairs were affected relatively more strongly than the major trade partner flows. Among different services subsectors, the impact is robustly negative and significant for Insurance, Financial, Telecom, Cultural and Travel services. In percentage terms, Insurance and Finance, which are traditionally the services where the UK has a comparative advantage, experienced the strongest decline of 15 percent and 11.6 percent consequently. At the same time, Ireland has experienced surge in services exports, increasing those by 37 percent, which is much higher than the estimates for the aggregate flows. It can be explained that Ireland has increased its services exports to the smaller services users very substantially. The major expansion are observed in Telecom (44 percent growth) and Business services (52 percent), but also having a very strong performance in Transport, Travel, Intellectual Property and Cultural services. To conclude, analysis of the bilateral flows confirms our results for the aggregate flows and reinforces them in the following sense: while UK has been unable to expand its services exports to medium and small countries, while Ireland successfully grew its services exports across the wide range of partner countries. Overall, the bilateral results are consistent with the results at the aggregate.

The reported results are also robust to extending the sample to a larger pool of the major 67 exporters, representing 95 percent of the services exports, which are presented in Table A6 in the appendix. The impact of Brexit for the extended sample is estimated to be −7.3 percent lower exports for the UK and 29.8 percent higher trade for Ireland, which is also moving the bilateral estimates closer towards the aggregate sample estimates. The sectoral results are also very consistent across the baseline and extended samples.

Is Trade With EU Affected More?

As the most immediate effect of Brexit was the expected change in the trade policy of the EU and the UK in terms of goods and services, it is natural to assume that exports from the UK to the EU countries should be affected more negatively than the UK’s exports to the non-EU countries. At the same time, while the effect on trade in goods is better understood and easier to measure, as tariffs and non-tariff measures are readily available for all UK trading partners and at highly detailed product level, the effect of Brexit on services trade costs and services trade is less clear. Moreover, since UK multinationals may respond to the expected increase in barriers to trade with the EU by moving some parts of their business to the EU countries, it may be argued that the impact of Brexit on trade in services with the EU countries is ambiguous.

Although the actual changes occurred only when the UK left in 2021, in a situation when the required adjustments are costly, incur fixed costs, and take time to adjust, businesses will find it optimal to adjust prior to the policy changes. For example, the policy uncertainty around international trade since the 2016 Brexit referendum reduced firms’ export participation (Crowley, Exton, and Han 2018) and aggregate trade flow (Douch, Du, and Vanino 2019; Graziano, Handley, and Limão 2020). UK firms, especially smaller ones, have already responded to the Brexit uncertainty by redirecting their trade away from the close, rich, and previously frictionless EU neighboring markets to places further afield (Douch, Du, and Vanino 2019). Some of the effects were detectable even before 2016, when the anticipation of future trade shocks led to tangible changes in trade dynamics (Douch, Du, and Vanino 2019; Handley and Limão 2017). This is known as the anticipation effect. Brexit was not the first occasion when such an effect was observed. Freund and McLaren (1999) show a rise in trade before the EU trade agreement came into force. The primary reason for the anticipation effect to take effect in a policy uncertainty situation is the inherent sunk costs associated with trade. Firms would have to bear certain costs to export, most notably when entering a new market (Eaton, Kortum, and Kramarz 2011; Melitz 2003). The costs of searching for partners, developing local knowledge and reputation, marketing, and following legal procedures, cannot be recouped if the firm subsequently withdraws from exporting, and hence would become sunk costs.

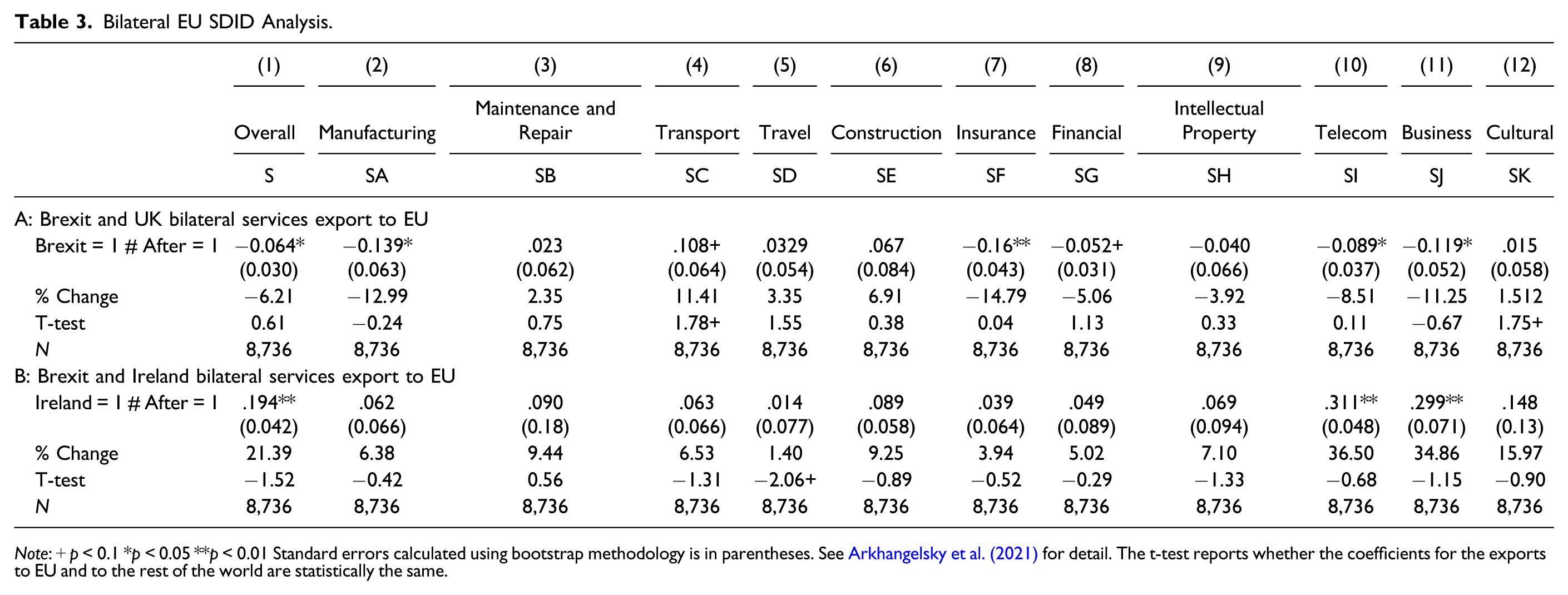

We further investigate whether the EU trade (a) has been significantly affected and (b) affected more strongly than the trade with all countries in the sample. To test the hypothesis of whether the UK services exports to the EU are affected more than that with the rest of the world, we redefine the pool of treated bilateral flows as the UK exports to the EU countries only, while the donor pool for the SDID counterfactual are all other countries trade with the EU countries. For this exercise, we continue using the pool of 27 major services exporters to which we add all remaining EU countries. The treated units are considered as UK and Irish exports to the EU countries, while the control group includes the trade of all other major exporters to the EU countries. The significant coefficient would indicate that post 2016 trade of the treated countries with EU countries have been statistically and significantly impacted. The further t-test for the equality of the coefficients with the coefficients from Table 2 would indicate that exports to EU responded differently than exports to all countries.

Bilateral EU SDID Analysis.

Note: + p < 0.1 *p < 0.05 **p < 0.01 Standard errors calculated using bootstrap methodology is in parentheses. See Arkhangelsky et al. (2021) for detail. The t-test reports whether the coefficients for the exports to EU and to the rest of the world are statistically the same.

Robustness Checks for Bilateral Sample.

Standard errors in parentheses.

Note: + p < .1 *p < .05 **p < .01.

Anticipation and Type II Error

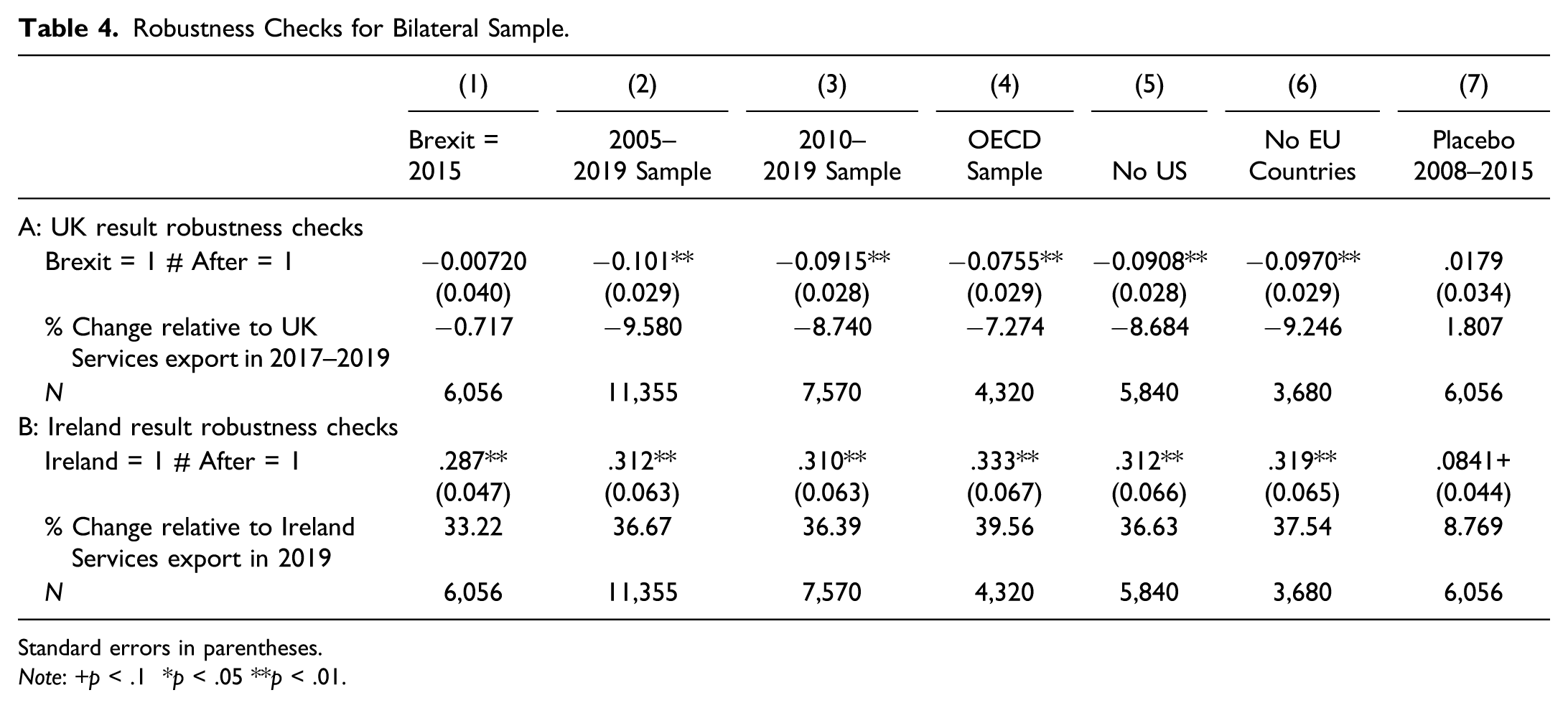

Focusing on the significance of the results ignores the important issue of the ability of the model to detect false negatives and to account for any anticipation effect that may bias the results, we produce the estimation when we backdating Brexit referendum to 2015, which produces expected nonsignificant result, indicating that the Brexit referendum results are actually driving the decline in the services exports in the UK. However, the results for Ireland indicate that the positive effect on the Irish services export has started prior to the Brexit referendum and is likely to be driven by other motives as well, such as more liberal tax policy, expansion of Irish IT and Intellectual Property services which may be the driving force in other services that are highly impacted by non-tradable component, such as Real Estate and Construction.

Extending the Sample

Synthetic control analysis benefits from expanding the sample to extend the pre-treatment period, which gives more confidence in the similar dynamics of the treated and synthetic units. Column (2) demonstrates that extending our sample to include data starting from 2005 does not change our conclusion, but only make them stronger. The estimated negative and significant impact on the UK services is −9.6 percent for the UK and positive and significant 31.2 percent for Ireland. Extending the sample to include 2010, but exclude the financial crisis episode, presented in column (3) also does not alter our conclusions.

Selection of the Pool of Donor Countries

Results of the estimation might be sensitive to the selection of the pool of countries from which the synthetic counterfactual is constructed. In particular, the donor pool should represent countries that are similar to the UK, but not affected by the Brexit shock. The fact that Brexit shock in 2016–2019 has mostly affected expectations and generated uncertainty about the future of the UK, rather than leading to actual changes in the trading rules and regulations helps us to identify us the effect, as the damage was mostly contained in the UK. Still, forward-looking agents would start acting in advance and make changes that may have impact on other countries.

We first limit the pool to the countries that are most similar to the UK and Ireland in the level of development, reliance on services and sharing similar policies, such as OECD countries. The results are presented in column (4), which slightly increase the estimated effect for the UK, but it remains negative and significant. In column (5), we remove US from the pool of donors, as it a much larger economy that expands its economic policy to wider pool of global economic agents. That does not change our results.

To address the issue of potential spillovers from the negative UK shock to other countries, which may bias the estimated causal impact of Brexit, we remove the EU countries, which are mostly affected by Brexit referendum outside of the UK. Regarding to the spillover effect, the causal impact interpretation of the estimated effect relies on the comparison of the treated unit (UK) vs comparison/control—UK in absence of Brexit, which is approximated by the weighted average of the trajectories of other countries. Those other countries should not be impacted by Brexit, which makes the EU countries suspects for the exclusion from the pool of donors. It is unclear whether the UK shock spillover to the EU countries is positive because the services firms relocate from UK (overestimated impact, due to synthetic peers start growing quicker leading to large distance between UK and synthetic UK) or negative due to EU is hurt by disruption of trade with UK (underestimated effect, due to synthetic peers start growing slower). Column (6) presents the results that remain strongly negative and significant.

Placebo Test

Finally, we present a classical placebo test, where we assume that the referendum had been actually held in 2012 and remove observations for 2016–2019 from the sample. The results indicate that there is no significant effect on the UK services trade, as we expect. For Ireland the results are also not significant, but only marginally, indicating that the export boom in Ireland has been triggered by a combination of different factors, which were only re-enforced but the Brexit referendum outcome.

Discussion

The Overall Effects

Our SDID estimates indicate that the Brexit Referendum resulted in the UK experiencing a shortfall of £18.5 billion (US$23.7 billion) in services exports annually between 2016 and 2019, relative to a scenario where the UK remained in the EU. This represents a 5.65 percent reduction in aggregate UK services exports. Bilateral data shows an average 8.5 percent decline in bilateral services exports, suggesting larger bilateral exports (e.g., UK-Germany or UK-US) were less affected than smaller bilateral exports. This aligns with Melitz (2003), which shows trade adjusts more along the extensive margins (number of trade links) than intensive margins (trade value per link). Smaller firms, more impacted by uncertainty and trade barriers, exit exporting, while larger firms maintain or increase exports due to reduced competition.

The impact estimates vary with methodologies. For instance, Douch and Edwards (2021) estimate a 7–8 percent decline using the SC method, while Du and Shepotylo (2021) estimate a 9.2 percent reduction using a pool of OECD countries. These findings align with studies reporting significant negative effects of Brexit on trade, FDI relocation (Breinlich et al. 2020), GDP effects (Born et al. 2019), and consumer sentiment shifts (Douch and Edwards 2021). In the long term, trade loss translates into productivity loss, further eroding UK competitiveness (Van Reenen 2016).

Ireland benefited significantly from Brexit, with services exports expanding by £24 billion (US$30.8 billion) annually over 2016–2019, a 14.75 percent increase in Ireland’s 2019 level. Ireland’s favorable conditions, such as low corporate tax, global connectivity, and a young, English-speaking workforce, have attracted firms seeking EU market access post-Brexit. This success cannot be solely attributed to economic policy but reflects substantial heterogeneity in performance across sectors. While Ireland’s success in expanding its services economy over the examined period of this study feeds on its overall liberal economic policy and tax advantages, this success cannot be solely attributed to economic policy but reflects substantial heterogeneity in performance across sectors.

There is no evidence that the UK’s services exporters redirected their exports from the EU to countries outside of the EU, unlike goods exporters. This suggests limited scope for UK businesses to find alternative markets outside the EU during this examined period.

Overall, Brexit has imposed a “price” on UK services trade. This analysis prompts questions about whether this cost was a conscious choice anticipated by policymakers or an underestimated strategic misstep. The findings serve as a catalyst for considering the future of service industries in the post-Brexit era amid potential heightened uncertainty.

Sectoral Effects

Sectoral heterogeneity is crucial in understanding Brexit's unequal impact across various sectors. Limited sector-level research hindered effective debates during Brexit negotiations. While most sectors experienced negative impacts due to Brexit uncertainty, the extent varied. Notably, Insurance, Finance, Telecoms, Cultural, and Travel services saw significant declines leading up to 2020.

The

On the other hand, there are also reasons to expect the UK Financial sectors to be unaffected by Brexit uncertainty, which makes it an intriguing hypothesis. The historical account of the international financial centers shows that they have long-term trajectories and tend to be very stable over time (Cassis 2010). London has strong comparative advantages in financial services, which are hard to replace, even if the City is no longer Europe’s de facto financial center. The UK’s financial market activities not only outsize its EU peers in terms of its domestic financial system, but also have almost total dominance in certain wholesale market sectors, hedge fund management, FX trading, over-the-counter (OTC) derivatives, and private equity management (Armour 2017). The agglomeration effects enjoyed by the sectors allow businesses to benefit from a deep and liquid pool of human capital and tacit knowledge in a way that is unparalleled in Europe. Thus, the City’s dominance is expected to be fairly secure.

Our findings underscore a paradox: the UK's financial sector, despite its formidable strength, has not been impervious to the disruptive forces of Brexit uncertainty. This revelation is of paramount significance, considering the sector's exceptional role within the UK economy. Amid the prevailing optimism regarding the prospect of greater regulatory autonomy for the UK’s financial sector after Brexit, with the aim of fostering growth, a prudent approach becomes imperative. There is a pressing need to exercise caution, lest the cost of this divergence results in the unintended consequence of eroding the sector’s competitiveness.

There is little surprise that

Conclusion

This paper aims to investigate the extent to which Brexit uncertainty impacted UK services sector trade from 2016 to 2019. We establish a conceptual framework in which uncertainty about the operational conditions of services sectors is expected to significantly influence business decision-making, thus affecting daily operations, reshaping their operational paradigms, growth trajectories, and broader economic contributions. Due to varying degrees of reliance on country-specific advantages and regulatory alignments with trade partners, certain sectors are disproportionately affected.

Utilizing the most current OECD-WTO Balanced Trade in Services dataset (BaTIS) and Arkhangelsky et al.’s (2021) SDID methodology, our empirical analysis confirms that Brexit has indeed had a substantial negative impact on UK trade. Impacts vary significantly across sectors. Following the Brexit referendum, we observe a statistically significant decline in the exports of Travel, Insurance, Finance, Telecom, Business and Cultural services leading up to 2020. Conversely, Construction services did not exhibit a significant decline. Notably, Ireland emerges as the sole European country to substantially benefit from the Brexit referendum. Ireland experienced an annual growth of US$30.8/£24 billion in total services exports from 2016 to 2019 compared to a counterfactual scenario without Brexit. This growth accounts for an impressive 14.7 percent of Ireland's total services exports in 2019.

Economic disintegration, such as Brexit, introduces significant changes to international trade in services. This paper addresses a critical yet underexplored issue that has not received the attention it deserves in both the public sphere and research communities, particularly when compared to international trade in goods. One reason for this relative neglect is the scarcity of reliable data and rigorous analysis. The factual knowledge provided by this study regarding the prevalence and severity of Brexit's impact on UK competitiveness in global services offers essential evidence. It represents a vital step in the ongoing discussion about the future services trade relationship between the UK and the EU following the EU-UK Trade and Cooperation Agreement.

Supplemental Material

Supplemental Material - Brexit and the Services Trade—A Longitudinal Analysis

Supplemental Material for Brexit and the Services Trade—A Longitudinal Analysis by Jun Du1 and Oleksandr Shepotylo in Journal of Service Research

Supplemental Material

Supplemental Material - Brexit and the Services Trade—A Longitudinal Analysis

Supplemental Material for Brexit and the Services Trade—A Longitudinal Analysis by Jun Du1 and Oleksandr Shepotylo in Journal of Service Research

Footnotes

Acknowledgments

We thank Dr Martina Magli for the constructive comments and suggestions given at the Trade & Investment in Services Associates (TIIS) Conference (November 2021) and Professor Sarah Hall for her valuable comments on the earlier draft. We are also thankful for the stimulating discussions with Peter Foster and Laura Noonan of the Financial Times on an earlier version of the paper. We appreciate the comments from the participants of the Centre for Business Prosperity seminar. We thank editors and anonymous referees for constructive comments. The financial support of Lloyds Banking Group is greatly appreciated. The views expressed in this paper are those of the authors alone.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported Lloyds Banking Group.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.