Abstract

The authors explore two important topics related to this special issue. One is how corporate social responsibility (CSR) activities impacts stakeholders, more specifically customers and shareholders/investors. Second is understanding customer recognition and demand for CSR activities. Insight into these topics is gained through the study of contextual differences in this value creation. Previous studies suggest that two important contextual differences have the potential to impact CSR-based value creation, the product versus service nature of the firm and whether the firm operates primarily in a business-to-business (B2B) versus business-to-consumer (B2C) channel. The lower innovative capabilities of service firms and the relative intangibility of services should hamper the impact of CSR activities in service versus product contexts. The impact should be higher, however, in a B2B versus B2C context based on the need for greater organizational alignment, adaptation, and relationship-specific investments. Results from a large-scale secondary dataset reinforce prior findings that CSR activities influence firm value through customer satisfaction. Moreover, the results reveal that this effect is weaker for service (vs. product) firms and stronger for B2B (vs. B2C) firms. The findings offer important implications for marketing theory and practice.

Keywords

The adoption of sustainable and socially responsible policies to address social and environmental issues has become a major topic in both research and practice. In this special issue of the Journal of Service Research, the important topics include how corporate social responsibility (CSR) activities impact stakeholders. A report by Aflac (2019) shows that 77 percent of customers are motivated to buy from firms that knowingly engage in socially responsible behavior, while 73 percent of investors consider firms’ efforts to improve the environment and society when making investment decisions. Another goal is to further our understanding of customers’ recognition and demand for CSR activities, where contextual differences stand to play a major role. This study takes closer look at customers and shareholders/investors, as two major stakeholders, and how CSR activities create value in different business contexts.

Previous research has shown that CSR directly influences customers’ perceptions of a firm (Luo and Bhattacharya 2006; Park et al. 2017), while investors appear to demand additional cues of the actual value of CSR (e.g., Awaysheh et al. 2020; Lenz et al. 2017; Luo and Bhattacharya 2006; Servaes and Tamayo 2013; Surroca et al. 2010), prompting arguments that CSR activities should be consistent with a firm’s overall corporate strategy (Porter and Kramer 2006; Rangan et al. 2015). From a marketing perspective, CSR activities should match what the company is trying to achieve in relation to customers (Du et al. 2007; Mishra and Modi 2016). In this sense, the impact of CSR activities on firm value should depend on customer evaluation (Luo and Bhattacharya 2006).

Previous research has largely focused on the overall impact of CSR without considering that there may differences across industry settings or contexts. Luo and Bhattacharya (2006) investigate the impact of CSR activities on customer satisfaction and financial performance assuming industries behave similarly. However, the strategic actions a firm pursues should, to some degree, depend on their industry context. Among the industry contexts considered fundamentally different and commonly researched is that between services versus products (Anderson et al. 1997; Lariviere et al. 2016). Although the service sector’s share of the GDP for any developed country is more than 70 percent (Ostrom et al. 2010) our knowledge of CSR performance in this sector is scant. We found only one study that compares how CSR “announcments”affect stock market reaction differently for service versus product firms. Casado-Díaz et al. (2014) argue that, because services are harder to evaluate than products, announcement of CSR activities have a greater impact on service (vs. product) firms’ abnormal stock returns, such that investors rely on these activities as a proxy for risk-reducing performance.

But this impact may be short lived. Previous research indicates that abnormal stock returns have non-significant impacts on future financial performance (Markovitch and Steckel 2012). Customers form their experience with a firm based on the whole value chain that a firm offers. Despite existence of CSR initiatives, firms struggle with communicating them to their customers/investors (Kramer 2018). Consequently, CSR announcements alone may fail to communicate the full performance of a company regarding CSR. In other words, CSR-related announcements necessarily include all CSR-related activities. Therefore, we focus on firms’ CSR activities and use firm value to study the longer-term effects of CSR on investors and firm financial performance.

Another important contextual difference in the marketing literature is whether firms compete in business-to-business (B2B) or business-to-consumer (B2C) channels. Prompting our focus on this contextual difference is the greater organizational alignment and adaptation between sellers and buyers in a B2B context (Anderson and Weitz 1992; Wathne et al. 2018), which has the potential to apply to CSR activities. Yet research on the impact of CSR activities on stakeholder perceptions in a B2B context is also very limited, where we know of only one other study that compares B2B with B2C (Homburg et al. 2013).

We argue that it is important to explore cross-industry comparisons as it helps firms to understand how to both act and communicate effectively in various environmental settings in relation with their stakeholders. In addition, cross-industry comparisons enable firms to learn from what is effective in other industries and, if possible, apply similar strategies. When it comes to CSR, understanding fundamental contextual differences is important for helping practitioners engage effectively in CSR activities, according to their operational setting. More precisely, this understanding can guide firms’ investments in organizational capabilities and communication strategies that increase the effectiveness of CSR. Service firms, for example, lag product firms in their investment in innovative capabilities (Biemans and Griffin 2018; Damanpour 1996), which may hinder them from engaging in “value-creating” CSR activities (Chen et al. 2018). By innovation capabilities, we refer to capability of the firm to “… continuously transform knowledge and ideas into new products, processes, and systems for the benefit of the firm and its stakeholders” (Lawson and Samson 2001, p. 384).

We draw upon the stakeholder theory and literatures involving customer satisfaction, innovation, services marketing, and B2B buyer–seller relationships, which we use to establish three predictions. First, following Luo and Bhattacharya (2006), we predict that customer satisfaction (i.e., customer perception) is a link from CSR activities to shareholder value (i.e., firm value). Second, we anticipate that the influence of CSR activities on stakeholders is weaker in a service versus product context. Third, we predict a stronger influence of CSR activities on stakeholders in a B2B versus B2C context. In presenting these predictions, we rely on a definition of CSR as firm performance in relation to its societal obligations (Brown and Dacin 1997; Sen and Bhattacharya 2001). We operationalize customer satisfaction as a cumulative evaluation of the customer’s experience to date with a product or service provider, which serves as a meaningful basis for cross-category comparisons (Fornell and Johnson 1993; Fornell et al. 1996).

By testing our predictions, we clarify relevant contextual effects involving products versus services and B2B versus B2C organizations. We posit that product firms possess more innovative capabilities (Biemans and Griffin 2018; Chauvin and Hirschey 1993; Damanpour 1996) and more tangible attributes (Fornell and Johnson 1993; Johnson et al. 2002), which allows their CSR activities to stand out in the marketplace and have a greater impact on satisfaction and firm value. We posit further that the need for greater alignment, adaptation, and relationship-specific investments in B2B contexts (Anderson and Weitz 1992; Dwyer et al. 1987; Wathne et al. 2018) increase the impact of CSR activities on customer satisfaction and firm value when compared to B2C contexts.

We rely on a novel and unique database, gathered from the Drucker Institute Corporate Effectiveness measurement system. The database is an aggregation of data from a large number of existing databases (including the ACSI). Among the available measures are CSR performance that incorporates measures related to the environmental, societal, and governance (ESG) aspects of firms’ activities as well as an aggregation of customer satisfaction. What makes the database unique is provision of indicators for CSR, customer satisfaction, and innovation capabilities for a large number of firms in various industry sectors. Significantly, the Drucker system is the first database that includes comparable measures of B2B and B2C firms (Crosby and Ghanbarpour 2023).

Accordingly, based on our analyses, we suggest that service sectors need to develop greater innovation capabilities to leverage their CSR efforts. At the same time, firms in B2C sectors need to better align their CSR activities with customers’ demand and/or better communicate the importance of those activities to improve their impact on firm value.

In the next section, we review the theoretical arguments that link CSR activities to customer satisfaction and firm value and predict how the relationship should differ for services versus products and B2B versus B2C firms. We then present our empirical study and results. Although CSR has positive impacts on customer satisfaction and subsequent firm value for products and services alike, the impact is weaker for services; the links are significantly stronger in a B2B context. These findings have important implications for the CSR strategies adopted by different service and physical product firms, as we detail in our conclusions.

Theoretical Background

Stakeholder Theory

Stakeholder theory applies to the observed relationships between CSR activities and stakeholder responses, suggesting that firms are not merely profit-seeking organizations but must satisfy the needs of their stakeholders, including efforts to achieve social support in their roles as corporate citizens (Cordeiro and Tewari 2015; Freeman 1984; Russo and Perrini 2010). In this view, CSR activities help alleviate conflicts between stakeholder needs and profit-seeking motives, which may enhance firm value. In general, extant literature suggests that CSR initiatives that are consistent with a firm’s business strategy, as it relates to customer satisfaction, should increase firm value (Aksoy et al. 2008; Ivanov et al. 2013; Luo and Bhattacharya 2006), whereas efforts less directly connected to its strategy might be only weakly linked to satisfaction and firm value.

Previous studies of the direct relationship between CSR and customer responses, such as customer satisfaction, offer several explanations for why CSR leads to more satisfied customers. Bhattacharya and Sen (2004) propose that it establishes a sense of connection between customers and the firm and increases positive attitudes toward the firm, which leads to customer–company identification. Customer–company identification then appears to mediate the effect of CSR on customer satisfaction (He and Li 2011; Pérez and Del Bosque 2015). Furthermore, engaging in CSR activities enables firms to develop and strengthen relationships with their customer base (Sen et al. 2006) and gain access to more customer-related knowledge, which they can leverage to offer greater personalization and valuable offerings to customers (Jansen et al. 2006; Jayachandran et al. 2005; Luo and Du 2015). Luo and Bhattacharya (2006) argue that a product offered by a socially responsible company provides added value, through the influence of positive social causes, which increase customers’ perceptions of value and satisfaction.

As stakeholders, shareholders also may be influenced by a firm’s CSR activities, and vast research has investigated this pathway for an effect of CSR on firm value. Initially, researchers reported contradictory results (i.e., positive, negative, neutral) for the CSR–financial performance relationship (see Margolis and Walsh 2003). In an effort to resolve this debate, Luo and Bhattacharya (2006) suggest using forward-looking financial performance metrics (i.e., firm value) and accounting for underlying processes or contingency conditions to explain the range of observed relationships. They conceptualize and test customer satisfaction as a mediator in the CSR–firm value relationship, which reveals that CSR exerts an insignificant direct effect on firm value. Rather, CSR influences firm value mainly through customer satisfaction. The underlying mechanism for this mediation is that CSR increases customer satisfaction, which is expected to create value for shareholders by increasing customers’ loyalty intentions, as well as predicted future cash flows for the firm (Gruca and Rego 2005; Olsen and Johnson 2003).

Considering previous findings, we do not expect a direct relationship from CSR to firm value. Similar to Luo and Bhattacharya (2006), we include customer satisfaction on the indirect path from CSR to firm value. Although this relationship has been tested, we offer a formal hypothesis due to the differences in our operationalization of constructs, the timeline of the studies, and our extension of the hypothesis to include B2B firms.

Services versus Products

We posit that inherent differences between services and products lead to a greater impact of CSR on customer satisfaction and firm value among product firms. Compared with services; firms that compete primarily on products/goods possess greater innovation capabilities (Biemans and Griffin 2018; Chauvin and Hirschey 1993; Damanpour 1996), as they develop well-structured processes and possess resources to create innovations (Damanpour 1996); and are easier to evaluate (Fornell and Johnson 1993). These differences explain why competitive product firms exhibit categorically higher customer satisfaction than competitive service firms 1 (Fornell et al. 1996), a difference that persists over time and across countries (Johnson et al. 2002). More specifically, Johnson et al. (2002), show that across national satisfaction indices, satisfaction is highest for competitive products, lower for competitive services and retailers, and lower still for government agencies (i.e., service firms with relative monopolies). Interestingly, the research also shows that satisfaction for comparable services is higher in more openly competitive economies. That competition, up to a point, fosters innovation is a natural explanation for differences between satisfaction level of service and product firms (Aghion et al. 2005).

The extant literature indicates that innovative capabilities are a necessary ingredient to increase the effectiveness of CSR on customer satisfaction and the subsequent impact on financial performance (e.g., Kuzma et al. 2020; Luo and Bhattacharya 2006). There are two possible explanations for this effect. Luo and Bhattacharya (2006) explain the underlying mechanism using institutional theory. They posit that stakeholders are more likely to perceive CSR as a positive firm activity if the firm also is meeting its main responsibilities well, such as offering high quality, innovative products that address customers’ needs. On the other hand, Chen et al. (2018) find that innovation capabilities help firms to engage in value-creating CSR activities by enabling firms to incorporate CSR strategies in their product innovations. Similarly, research found that innovation capabilities can increase the effect of CSR on new product innovations (Luo and Du 2015), which is expected to increase customer satisfaction. Since service firms (versus products) have a long tradition of weaker performance on innovative capabilities (Biemans and Griffin 2018; Damanpour 1996), we expect lower impact of CSR on customer satisfaction for these firms.

While both product and service firms embody degrees of tangibility and intangibility, including “back-of-house” activities, the relative intangibility of services compared with products makes services, in general, more difficult to evaluate (Casado-Díaz et al. 2014), display, and communicate (e.g., insurance and financial services; Johnson et al. 2002). Accordingly, research specific to CSR suggests that products exhibit and communicate more tangible and effective CSR activities than services. Service CSR activities are more likely to occur back-of-house and be less visible to customers (e.g., hiring diversity, governance practices; Casado-Díaz et al. 2014). In addition to the mentioned activities, physical goods have greater opportunities to engage in CSR activities that are directly in customers’ “line of sight” (e.g., eco-friendly materials, recyclability of physical goods). Therefore, customers can more easily recognize CSR activities related to physical goods (Aksoy et al. 2022; Peloza et al. 2012). Aksoy et al. (2022) empirically demonstrate that CSR activities are harder for service customers to perceive, because of the inherent intangibility. Considering the type of CSR activities that service and product firms engage in, the impact of CSR activities on customer satisfaction may be weaker for services than for products (Ghanbarpour and Gustafsson 2022; Park et al. 2017; Pérez and Del Bosque 2015).

Taken together, limited innovation capabilities and the relative intangibility of services explain why we expect lower effectiveness of CSR initiatives on customer satisfaction, which likely influences their financial performance (Hull and Rothenberg 2008; Porter 1996). Even if CSR activities have generally positive impacts for both product and service firms, the impact may be weaker for service firms. We hypothesize formally:

Given the potential importance of innovation to this prediction, we qualify H2a by positing that service firms with higher innovative capabilities should perform better than those with lower capabilities.

B2B versus B2C Relationships

As indicated in the introduction, there is limited research on CSR linked to stakeholder perceptions in a B2B context (Homburg et al. 2013). This research shows that “business practice” CSR activities (i.e., CSR activities within a firm’s core business operations) foster customers’ trust, while philanthropic CSR strengthens customer–company identification. The authors further highlight the competitive situation and CSR alignment as important moderators. We extend this research by comparing the impact of CSR activities between B2B and B2C firms.

B2B contexts, in contrast to B2C, reflect a greater need for alignment, adaptation, and relationship-specific investments in buyer–seller interactions. Relationships in B2B marketing channels tend to involve larger, more complex transactions; a range of people, products, and processes; and relational rather than transactional interactions (see, e.g., Hutt and Speh 2021; Johnston and Bonoma 1981; Kumar and Reinartz 2012; Saini et al. 2010). As a result, B2B relationships require greater organizational alignment, adaptation of physical assets and investments, and credible commitments (Anderson and Weitz 1992; Wathne et al. 2018). According to Anderson and Weitz (1992), idiosyncratic investments in channel relationships act as powerful signals of such commitment. Distributors perceive manufacturers as more committed to a relationship when they make distributor-specific investments, while manufacturers place more confidence in distributors who offer “non-redeployable” resources. From a transaction cost perspective, credible commitments “take shape as economic actors consciously agree upon mechanisms that provide added insurance” (Williamson 2010), which may create “hostages” in support of exchange relationships (Heide and Wathne 2006; Wathne et al. 2018; Williamson 2010).

But how do such commitments apply to CSR activities? Hoejmose et al. (2012) suggest that greater, more explicit expectations, and even requirements, exist for the alignment of CSR activities and policies in B2B buyer–seller relationships, which are critical to consistent relationships. These differences suggest a greater need for “fit” between buyers and sellers in a B2B context, which leads to increased realization of the seller’s activities by buyers. According to Ozdora-Aksak and Atakan-Duman (2016), B2B and B2C firms also engage in different types of CSR activities: B2B firms link their CSR activities to their core business functions (i.e., value-creating CSR), whereas B2C firms tend to adopt more discretionary, varied, and philanthropic CSR initiatives. Engaging in value-creating CSR activities that are integrated into firms’ core business agenda likely leads to greater customer satisfaction (Chen et al. 2018). Du et al. (2007) also suggest customer responses may be more positive to CSR initiatives integrated into a firm’s or brand’s core positioning, whereas CSR activities that merely contribute to broad social well-being or are less specific to the firm’s core value and activities have less positive influences on customer satisfaction. Finally, CSR is an inherently cross-functional activity. The parties in a B2B buyer–seller relationship tend to be already aligned around other elements of the value-creation process, so a supplier should be more successful when implementing CSR activities that receive positive stakeholder reactions (Du et al. 2010; Hoejmose et al. 2012). Taken together, prior literature suggests that CSR activities in a B2B context have greater impacts on customers and subsequent shareholder value. We formally hypothesize:

Conceptual Model

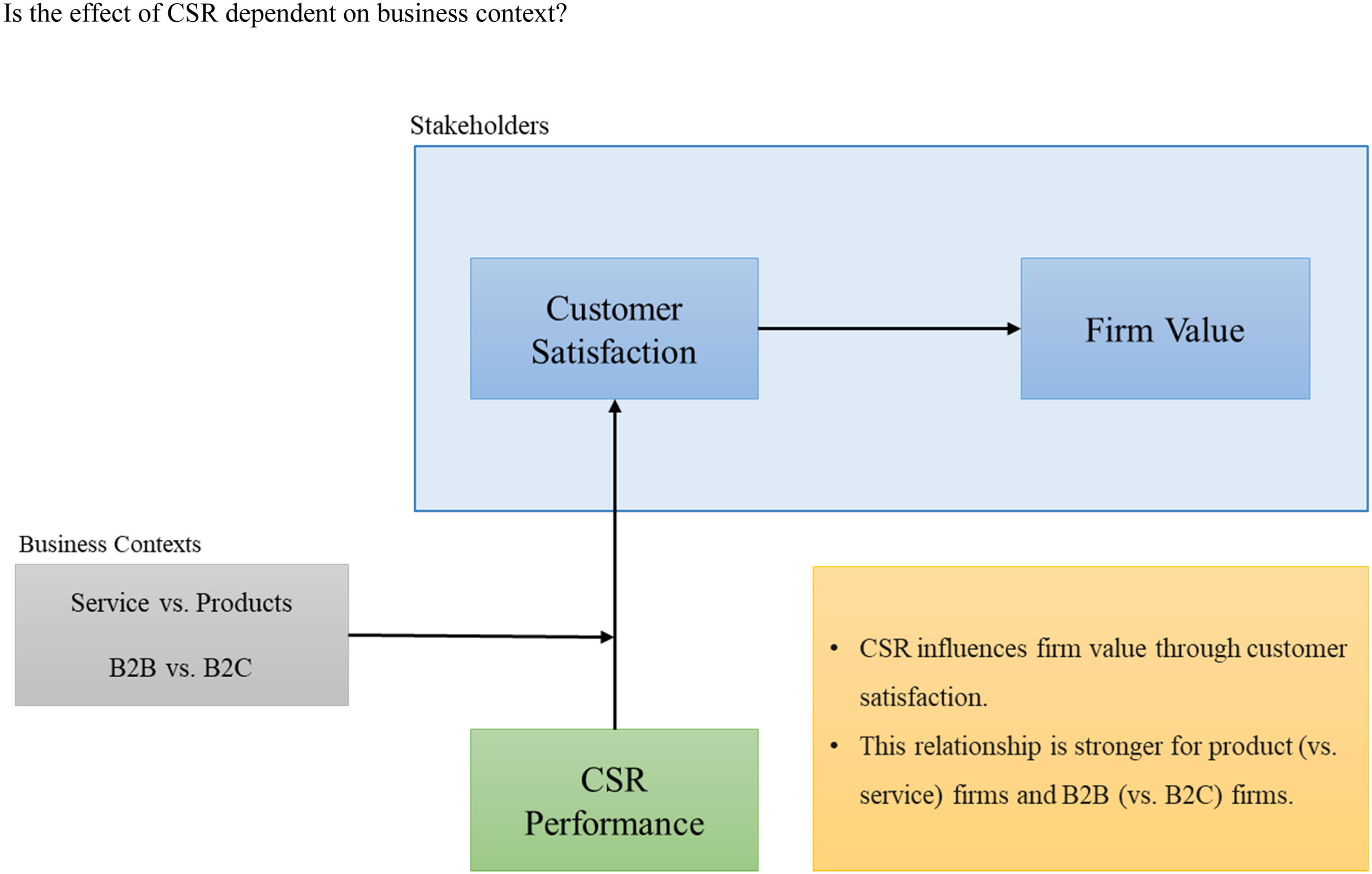

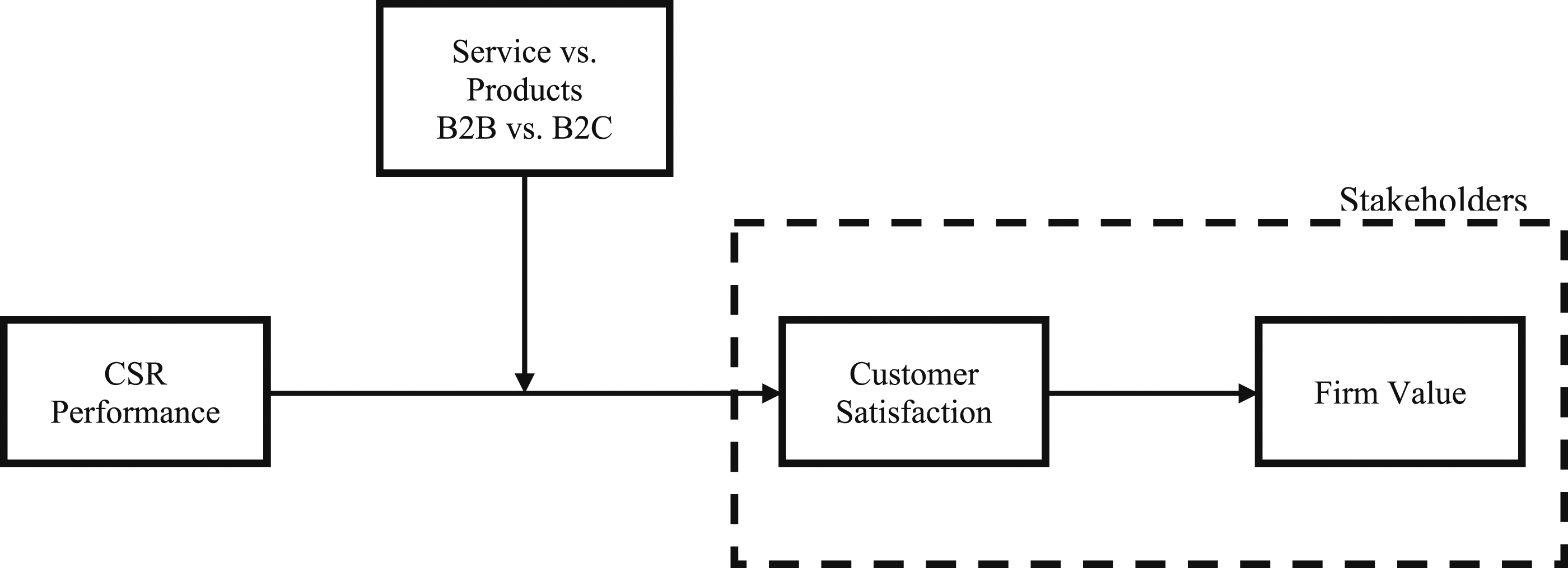

To address these issues, we propose a framework, similar to Luo and Bhattacharya (2006), in which CSR affects firm value through customer satisfaction (Figure 1). We build on their findings to examine this relationship specifically in service versus product firms and B2B versus B2C contexts. Furthermore, we add evidence from the CSR literature to predict that CSR positively influences customer satisfaction and firm value across contexts, but the positive impact should be weaker for service firms, albeit relatively higher for B2B service firms. Conceptual framework.

Data and Methodology

Data

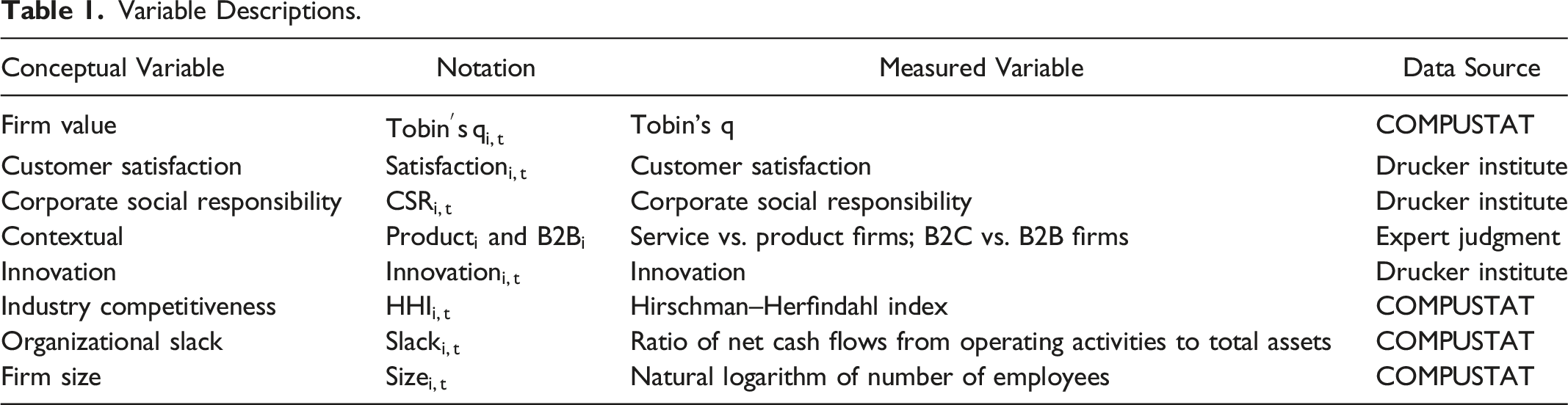

Variable Descriptions.

A recent comprehensive review of the Drucker measurement system (Crosby and Ghanbarpour, 2023) details how the system was developed, the annual data capture and aggregation processes, the data sources and specific metrics (i.e., years included, where they fit in the nomological nets of the constructs, prior use in the literature, etc.), model fit statistics, factor loadings, and an appraisal of the content and construct validity of the measures. The authors conclude that the Drucker system of measures is suitable for academic research and that it adequately addresses data and method limitations identified by previous research.

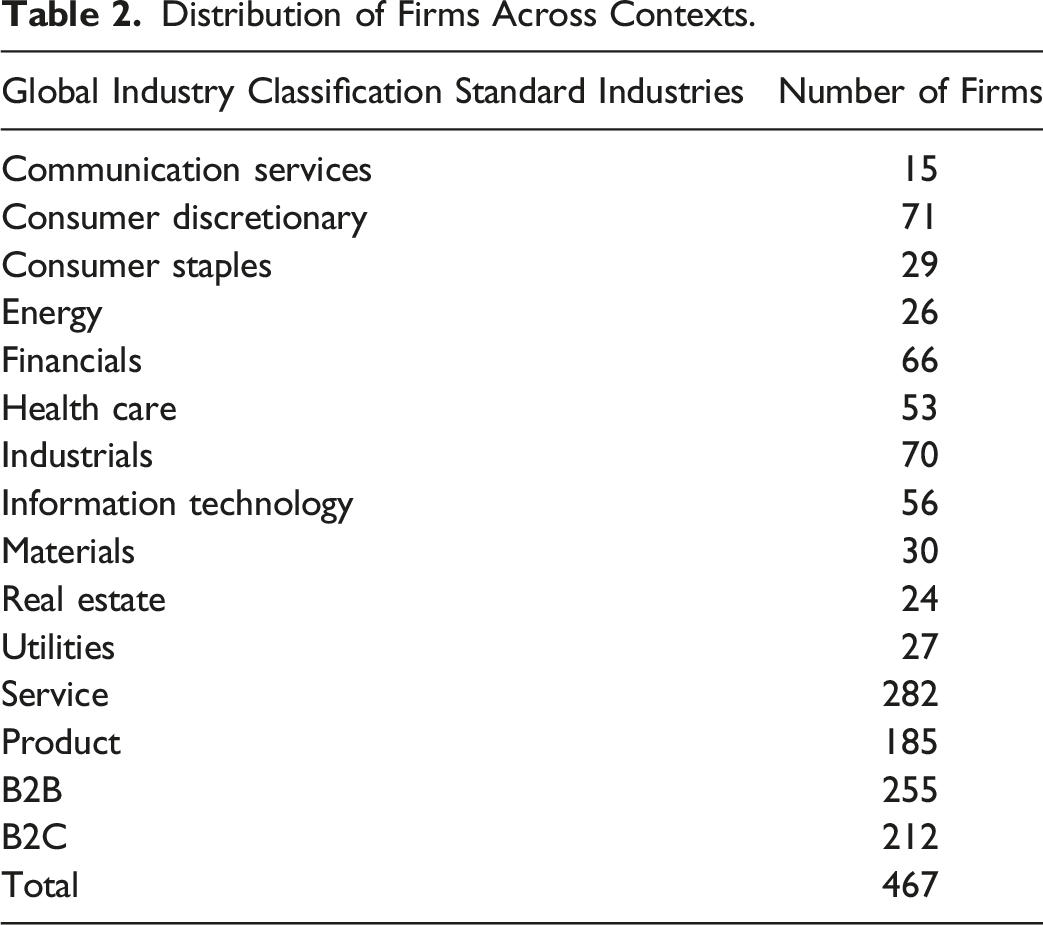

Distribution of Firms Across Contexts.

CSR

From an empirical standpoint, our interest is less focused on the social obligations of firms and more linked to how they perform, relative to the social obligations. Previous research tends to rely on KLD measures of CSR, but Berg et al. (2022) determine that averaging different ratings offers more reliable insights than relying on a single rating to measure CSR. The Drucker composite CSR measure draws on five different, comprehensive ESG rating systems, from which it extracts seven metrics (eight in 2021) to capture overall CSR performance. Two metrics are expressed in both absolute and industry relativized terms. In creating the composite score, the institute standardizes the input metrics, computes an average, and then re-standardizes the result. Although they are independently produced using different methods, the ESG metrics in the Drucker system have an average factor loading of 0.82 and an acceptable level of convergent validity with an average variance extracted (AVE) score of 0.70 (Hair et al., 1998). 6 The Drucker approach to measuring CSR thus addresses potential issues associated with using a single rating of CSR, as well as the concerns related to KLD scores. See Crosby and Ghanbarpour (2023) for further discussion.

Customer Satisfaction

Marketing literature related to customer satisfaction primarily uses data from the American Customer Satisfaction Index (ACSI). Although ACSI data are well-established, reliable measures of customer satisfaction, the index is limited to B2C firms. Therefore, we use ratings provided by the Drucker Institute to operationalize customer satisfaction. Similar to CSR, the Drucker Institute’s customer satisfaction scores are based on multiple indicators. From 2014 to 2021, those indicators included the ACSI, CSRHub’s Product Rating, JD Power’s Net Promoter Score, and wRatings’ Quality Gap Score. From 2014 to 2018, the measure also included the Temkin Index Score, which was replaced in 2019–2021 by the JD Power Customer Satisfaction Index. Initially the ACSI, Temkin, and Net Promoter scores were expressed in both absolute and relative terms, but the relative metrics were eventually dropped, as redundant. This customer satisfaction measure is the average of the underlying indicators, which is re-standardized. The metrics have an average factor loading of 0.69 and an acceptable AVE score of 0.54 (Hair et al. 1998). Given these results and other details summarized by Crosby and Ghanbarpour (2023), we argue that this measure is a valid reflection of the firm’s cumulative level of customer satisfaction.

Contextual Variables

We classify firms in the data set into two categories: service versus product (i.e., durable and non-durable goods) and B2B versus B2C. We assigned firms to these categories on the basis of expert judgments. This categorization explicitly recognizes that any given offering is likely to be some combination of intangible services and physical goods (or B2C and B2B), but one or the other will be more central to a firm’s value proposition. This common classification system is used by government agencies to define gross domestic product (e.g., https://www.bea.gov/), as well as by researchers to explain categorical differences in satisfaction across industries (Bennett and Rundle-Thiele 2004; Fornell et al. 1996; Johnson et al. 2002). Two expert judges, with academic and business backgrounds, independently classified the firms in the Drucker population, using information from different resources, such as the companies’ websites, ACSI (for B2C firms), and alternative classification schemes (i.e., GICS, SIC, NAICS, Capital IQ platform). The agreement rates the judges achieved were 90.4 percent for services versus products and 89.2 percent for the B2B versus B2C classification (Perreault Jr and Leigh 1989). A third judge cast a vote in any cases in which the main judges could not achieve a common decision. A consensus determination then followed, through discussion among all three judges. In the end, two dummy variables identify product (vs. service) and B2B (vs. B2C) firms.

Innovation

The Drucker system measures innovation as an enduring, trait-like capabilitiy of a firm. As such, its 11 indicators of innovation include shorter-term inputs (i.e., R&D expenditures) and outputs (e.g., patents, trademarks) but also longer-term investments in talent (e.g., hiring in cutting-edge fields) and innovation-supporting channel relationships. Also included is a metric related to innovation reputation.

Firm Value

Following previous research, we use Tobin’s q to measure shareholder and firm value (Anderson et al. 2004; Grewal et al. 2010; Rubera and Kirca 2017). This measure is appropriate as it is widely used in prior literature and provides the grounds to compare the results with previous studies. Following Sorescu and Spanjol (2008), we compute year-end measures of Tobin’s q as the ratio of the market-to-book value of firm assets. We estimate the market value of assets as the book value of assets plus the market value of common stock, less the book value of common stock, less the amount of deferred taxes. We obtain these financial data from the COMPUSTAT database.

We should note that Drucker measurement system offers a financial measure as well. However, we believe the multidimensional Drucker financial measure is not appropriate for the purpose of this study (i.e., assessing firm value), as it mainly relies on profitability and accounting measures of performance.

Control Variables

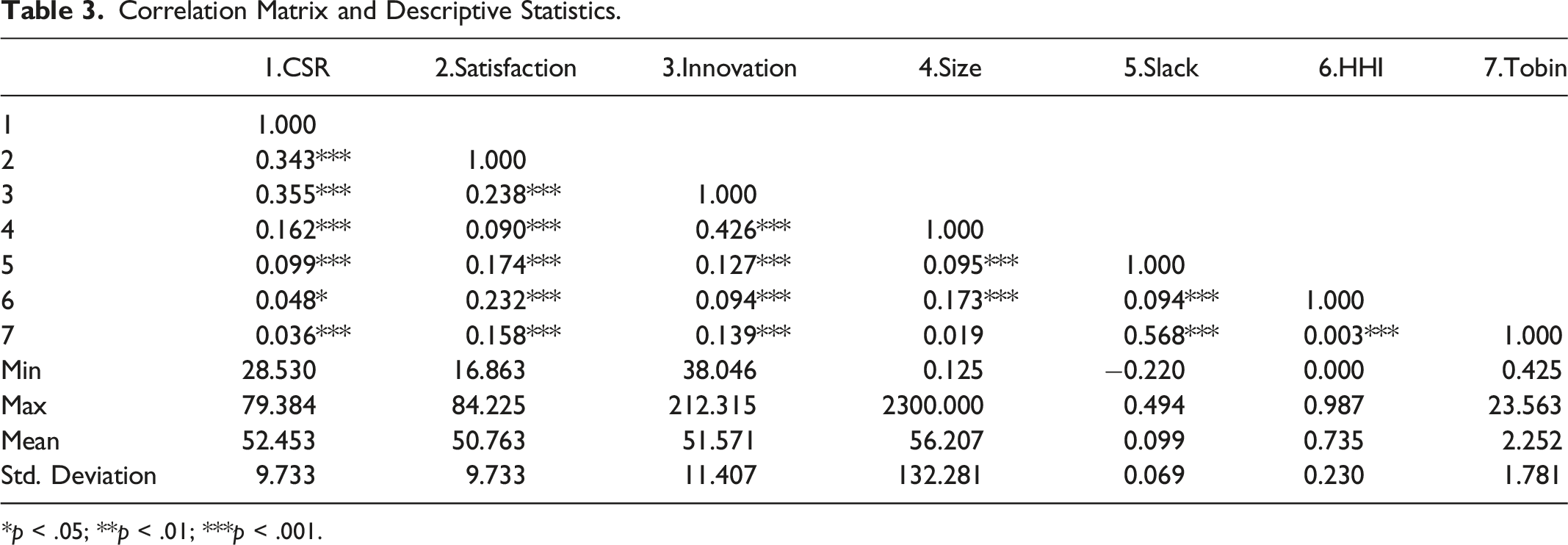

Correlation Matrix and Descriptive Statistics.

*p < .05; **p < .01; ***p < .001.

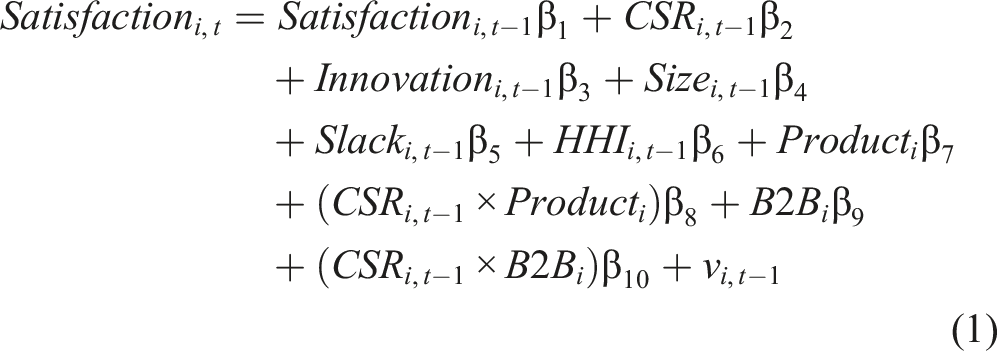

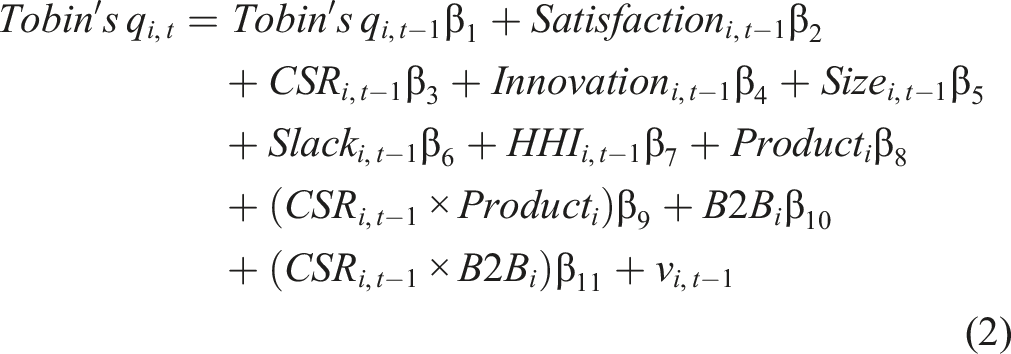

Model Specification

We use a dynamic panel data model, the generalized method of moments (GMM) (Arellano and Bover 1995; Blundell and Bond 1998), which is appropriate when the number of available periods (T) is fewer than the number of units of analysis (N). This method controls for common statistical issues such as endogeneity, heteroscedasticity, and serial correlation (Roodman 2009). With the GMM, we include two-period (t – 2) or earlier lagged independent variables in the estimation as instrumental variables to account for endogeneity concerns, then incorporate the first lag (t – 1) of the dependent variable to control for omitted variable bias and autocorrelation issues (Roodman 2009). In addition, we include dummy variables by year to account for unobserved time-specific effects and heteroscedasticity. We incorporate first-lagged versions of the independent variables in our models, because investors might need time to react to evidence of CSR and customer satisfaction, and they rely on past performance, as it becomes available, to make investment decisions (Rego et al. 2013; Srinivasan et al. 2009).

The test of the stationarity of the dependent variables relies on a Dickey–Fuller test procedure (Enders and Lee 2012), which shows that both customer satisfaction and Tobin’s q are stationary, suggesting estimation at levels (versus first differences). Accordingly, we estimate the following equations to test the presented hypotheses, where i stands for the firm and t for the time (year)

We winsorize the data at the 1 percent level and log-transform the variables with skewed distributions to prevent extreme observations from driving the results. By using standardized values (z-scores), we can facilitate the comparison of effect sizes (e.g., Rego et al. 2013; Tuli et al. 2010). To obtain reliable, robust results, we follow three steps suggested by prior literature. With Sargan–Hansen statistics, we test for the validity of our instrumental variables; a valid set of instruments would not reject the null hypothesis for Sargan–Hansen statistics (Roodman 2009). We also evaluate AR(1) and AR(2) statistics to test for serial correlation in the error terms. The null hypotheses (i.e., there is no k-order serial correlation) should be rejected for AR(1) and not rejected for AR(2), because the dynamic panel GMM expects first-order serial correlation in the data but not second-order serial correlation. Finally, we check the robustness of models by estimating them using ordinary least squares (OLS) and fixed effect estimators. The main effect of the lagged dependent variable for GMM should lie between the OLS and fixed effect estimations (Bond and Windmeijer 2002).

Results

In this section, we present the estimation results for the proposed models. First, we describe the main effect of CSR on customer satisfaction and Tobin’s q, to show how customers’ and investors’ responses to a firm’s CSR performance differ based on the service/product and B2B/B2C contexts. Second, we assess service firms independently, to evaluate the influence of CSR on customer satisfaction and Tobin’s q in B2C versus B2B firms.

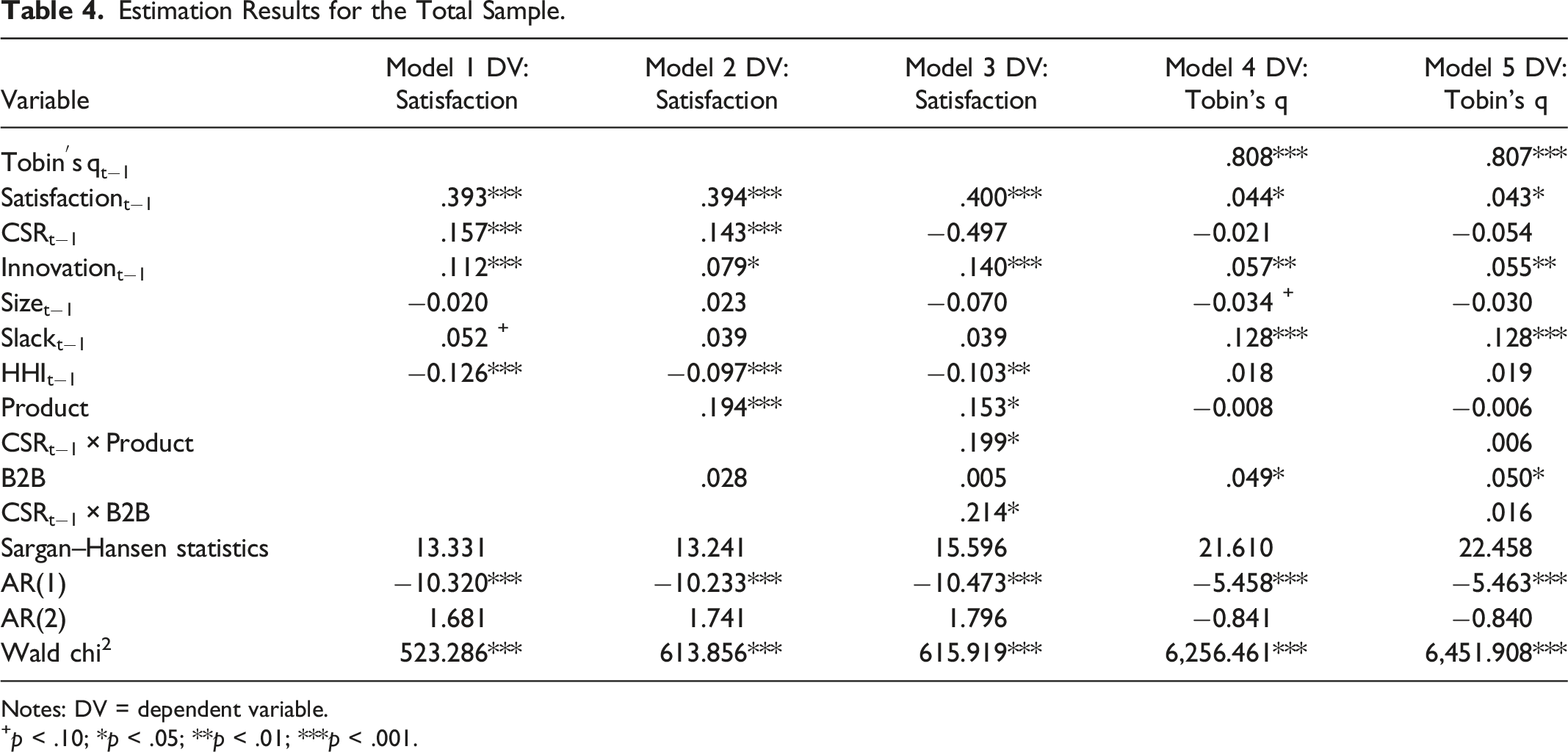

Estimation Results for the Total Sample.

Notes: DV = dependent variable.

+p < .10; *p < .05; **p < .01; ***p < .001.

In addition, as predicted by H1, CSR in Model 4 does not directly influence firm value (b = −0.021, p = .129) but instead does so through customer satisfaction (b = 0.044, p < .05). This result is in line with previous research that reveals insignificant direct effects of CSR on firm value (e.g., Luo and Bhattacharya 2006). Although not hypothesized, we checked for the moderation effect of business contexts in the direct relationship between CSR and firm value to test for the robustness of the results in regard with previous findings. The Model 5 indicates that the non-significant effect of CSR on Tobin’s q is robust to service or product firms (b = 0.006, p = .783), as well as to B2C or B2B firms (b = 0.016, p = .490).

Analysis of the Service Context

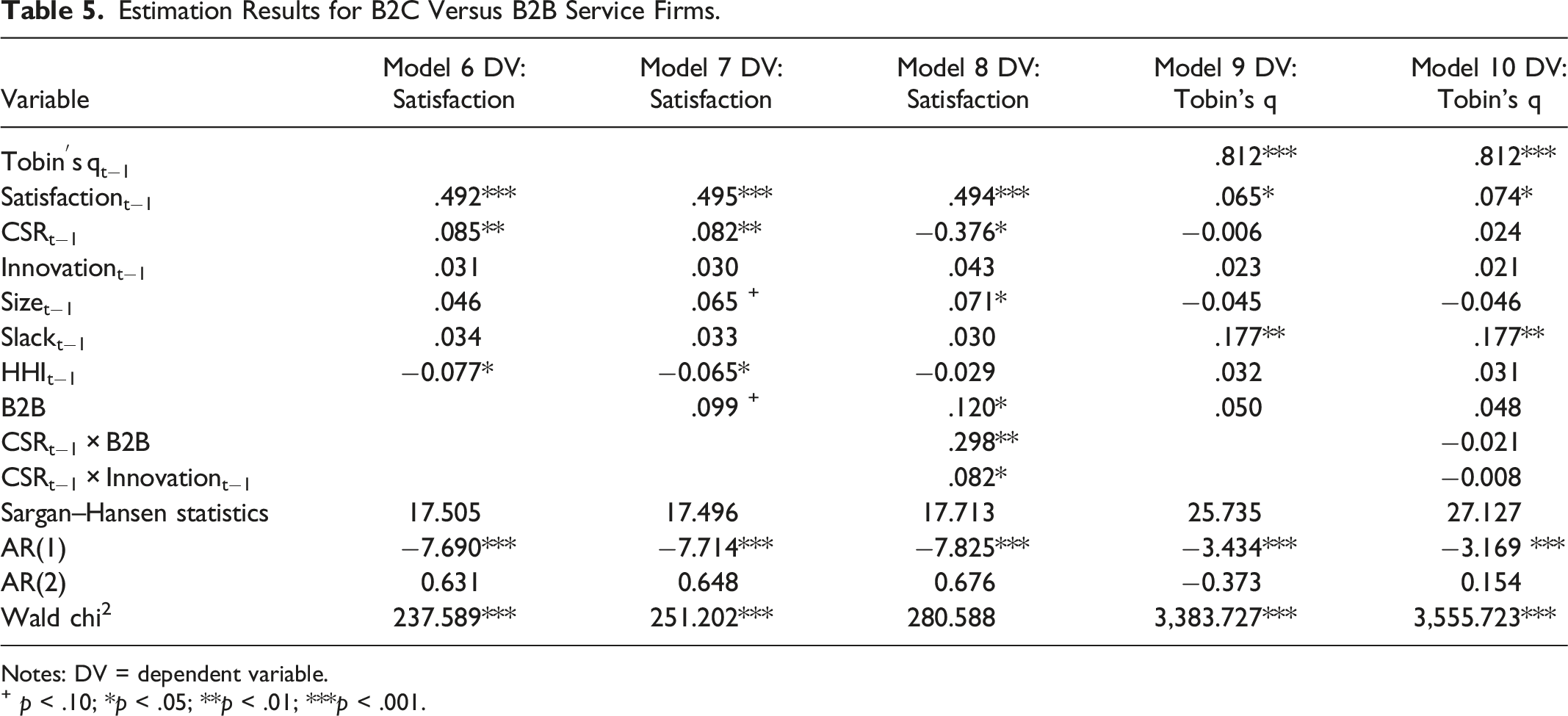

Estimation Results for B2C Versus B2B Service Firms.

Notes: DV = dependent variable.

+ p < .10; *p < .05; **p < .01; ***p < .001.

Despite the significant positive effect of innovation on both measures in a general context (i.e., total sample) (Table 4), innovation appears to exert non-significant effects on both customer satisfaction (b = 0.030, p = .322) and Tobin’s q (b = 0.023, p = .401) for service firms. We propose two potential explanations for these effects. First, innovation in service contexts is easier for competitors to replicate, so it has a weaker influence in the market. The competitive advantages in service settings relate more to networks of linked activities than to the innovativeness of individual service activities that are more replicable (Gustafsson and Johnson 2003; Porter 1996). Second, innovation in a service context may simply be harder for both customers and investors to perceive due to the intangible nature of services (Gustafsson and Johnson 2003).

Additional Analyses

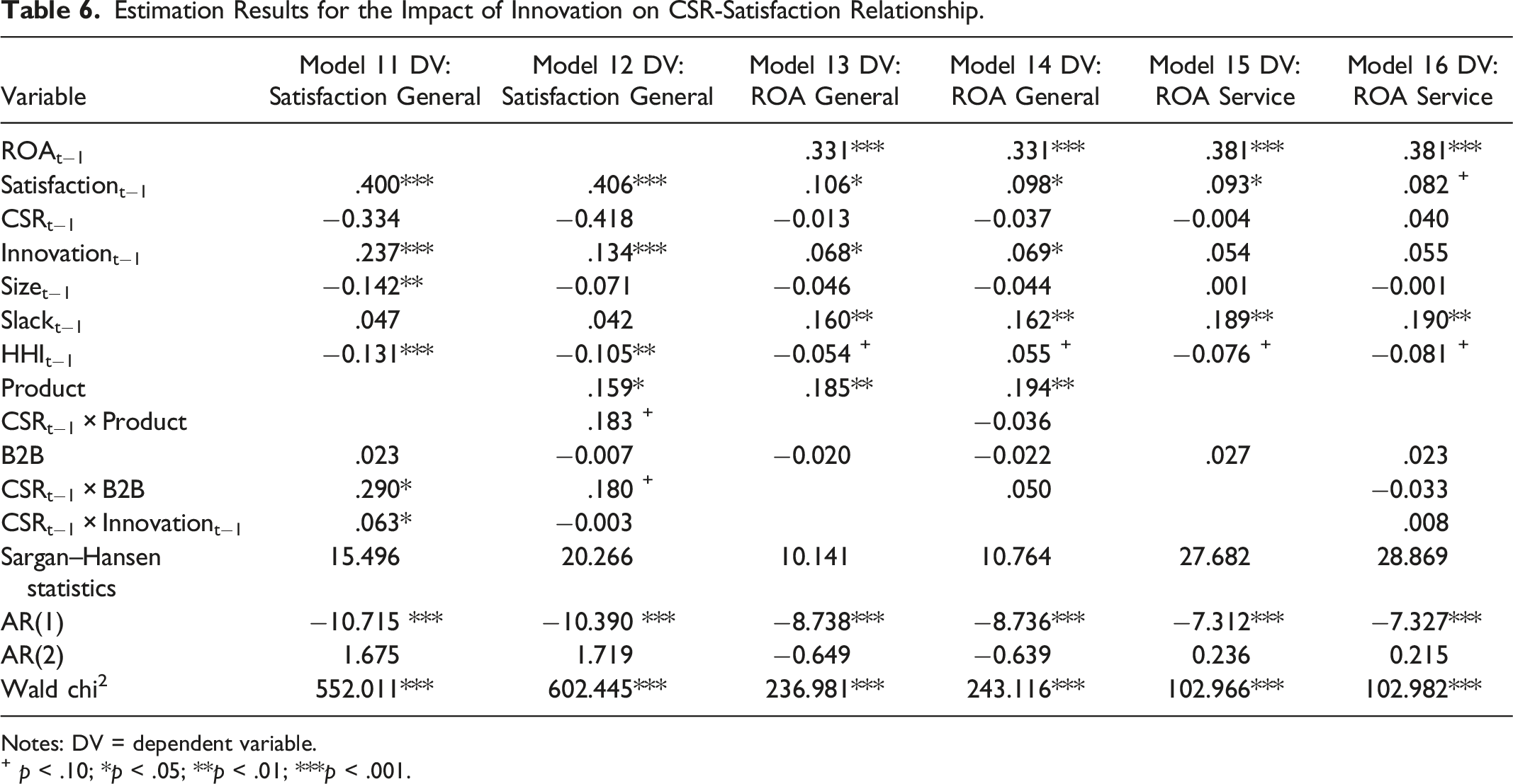

Estimation Results for the Impact of Innovation on CSR-Satisfaction Relationship.

Notes: DV = dependent variable.

+ p < .10; *p < .05; **p < .01; ***p < .001.

Second, we test for the effects on return on assets (ROA), instead of Tobin’s q, to confirm if the hypothesized effects are robust to other financial performance indicators (Table 6). Overall, our findings remain unchanged (Model 13–16). For the overall sample of all firms, customer satisfaction exerts significant effects on ROA (b = 0.106, p < .05), whereas the effect of CSR is non-significant (b = −0.013, p = .658). Similar relationships exist for the service subsample: Customer satisfaction affects ROA significantly for service (b = 0.094, p < .05), while the effect of CSR is insignificant (b = −0.002, p = .95). The moderating effects also show non-significant impacts on ROA.

Discussion

With this research, we investigate the impact of firms’ CSR performance on two key stakeholders, customers, and shareholders, in service versus product and B2C versus B2B contexts. Understanding the impact of CSR on stakeholders and its mechanisms can help managers develop effective and efficient strategies to increase performance. Our results indicate that CSR positively influences shareholders (firm value) through an indirect path of customer satisfaction, in multiple contexts. This positive relationship is weaker, though still positive, for service and B2C firms. Furthermore, different types of service firms benefit more or less from CSR initiatives: CSR offers more positive performance benefits for B2B service firms.

Theoretical Contributions

We extend knowledge about the impact of CSR on firm stakeholders and contribute to related literature in four ways. First, we establish the positive role of CSR in creating value for both customers and shareholders in different business contexts. At a general level customer satisfaction is critical for creating value for shareholders through CSR activities, regardless of the business context. This is in line with previous research that implies CSR needs to be noticed and valued to evoke positive outcomes (Ghanbarpour and Gustafsson 2022; Luo and Bhattacharya 2006).

Second, we find that the effect of CSR on satisfaction is stronger for both products versus services and B2B versus B2C firms. This suggests previous finding showing that CSR announcements exert a greater impact on short-term stock returns for service firms may be short-lived (Casado-Díaz et al. 2014). Taking a longer-term perspective, our results show that the impacts of CSR activities on customer satisfaction and firm value is lower for service firms. Because it is harder for customers and investors to perceive firms’ CSR activities in service contexts, the positive effect of CSR on firm value through customer satisfaction is not as powerful in this setting (Ettlie and Rosenthal 2011; Prajogo 2006). Our results also extend previous research on CSR activities to both a B2C and B2B firms. B2B relationships involve larger, more complex, and relational transactions that require greater organizational alignment and adaptation (Anderson and Weitz 1992; Wathne et al. 2018). Our results support the notion that greater, more explicit expectations and requirements exist for the alignment of CSR activities and policies in B2B relationships (Hoejmose et al. 2012).

Third, we highlight the influential role of innovation in the relationship between CSR and stakeholders in service contexts, such that CSR exerts stronger effects on customer satisfaction for service firms that possess higher innovation capabilities. Although previous studies have found a similar relationship without considering the business context (e.g., Hull and Rothenberg 2008; Luo and Bhattacharya 2006), we show that interactive effect of CSR and innovation is context dependent—rather than a general effect. Fourth, we determine that innovation is an insignificant predictor of satisfaction and firm value for service firms. This finding suggests previous findings that position innovation as a mediator of the CSR–performance relationship (Surroca et al. 2010; Vishwanathan et al. 2020) may not hold in a service context. Rather, innovation is a necessary firm capability when working with CSR, as CSR coupled with innovation can be more effective for service firms. In short, innovative capabilities require a focus (in this case CSR) to make a difference for customers.

Managerial Contributions

CSR signals to different stakeholders that a firm is a positive force in society. Another study by Aflac (2016) indicates that 61 percent of investors consider CSR a sign of ethical corporate behavior, which reduces investment risk, while customers prefer to buy from firms that are making the world a better place (Aflac 2019). But not all firms are created equal with respect to their ability to engage in and communicate CSR activities that enhance customer satisfaction and firm value. This study reveals fundamental differences between products and services and between B2B and B2C firms, which lead to real differences in customer satisfaction and firm value derived from the contributions of CSR activities. Overall, to gain these benefits, the CSR activities should be customer oriented, because customer satisfaction is a key determinant of how investors view firms’ activites.

Our results raise some unique challenges for service firms regarding the impact of their CSR activities. It is possible that customers' perceptions of the CSR behavior of service firms do not reflect what the firms actually do. In a similar vein, Aksoy et al. (2022) assert the lesser capability of service firms for engaging in CSR activities that are recognized and valued by customers. This disconnect could be due to a higher degree of intangibility; lacking concrete evidence of CSR, customers might judge CSR performance on the basis of their general image impressions or the firm’s reputation or perhaps the CSR supplied by service firms does not match the CSR that customers demand (Kuokkanen and Sun 2020).

The distinction between product versus service firms is not absolute; product firms have service components (and the other way around). Making services more like products is not necessarily the answer. Rather, it makes signaling and communication through tangible clues more effective. A possible solution is that service firm develop effective communication strategies to enhance the awareness of the customers regarding their CSR activities and increase the tangibility of those activities for their customers (Du et al. 2010). For example, human trafficking has become a more salient social issue for customer and shareholders alike. Marriott International is training its employees to identify and report possible incidences of human trafficking on their properties, which is having an impact that is prominently featured in their annual report (Marriott 2022). A proper communication of this initiative by Marriott might increase the positive responses of customers.

The greater relative tangibility of product firms gives them a natural advantage when increasing the awareness of CSR activities, as when it comes to reducing the negative impacts of their products on the environment in the face of persistent climate change. Consider a firm such as IKEA, whose value proposition includes a large inventory of branded products, within a service process that directly involves the customer. In response to negative reports about the durability of its wood-based furniture products and their impact on the environment, IKEA developed and communicated an effective process to facilitate the recycling of those materials. It also devotes great effort to communicating the sustainable nature of its forestry products. But the intangible nature of service offerings requires an even more concerted effort to engage in more customer-relevant CSR activities. For example, our results suggest that CSR can increase customer satisfaction and firm value, if it can contribute to differentiating the firm.

Because no firm has endless resources, CSR efforts always involve an optimization problem. Firms must consider how they can establish CSR activities that both align with their strategy (Chen et al. 2018; Porter and Kramer 2006) and resonate well with stakeholders (Luo and Bhattacharya 2006). We recommend that, to increase the positive impact of CSR, firms might invest more in innovation capabilities and combine them with CSR activities, which would enable them to generate greater value. This issue appears especially relevant for service firms. Innovative capability is a necessary requirement for CSR performance and it has been long recognized that service organizations simply lag behind product companies. Service organizations need to invest more in structure and capabilities for their CSR activities to pay off.

Moreover, our results suggest that B2C firms can learn important lessons from B2B firms. Although creating closer partnerships with customers is more commonplace in B2B firms, B2C firms stand to gain more positive responses to their CSR activities if their focus is on value-creating CSR, as might be manifest in customer-oriented marketing, product innovations, and customer-value marketing (for details see Chen et al. 2018). Because B2B firms are more closely aligned with customers, reflecting the people, products, processes, and relationships they entail, they stand to be more successful with implementing value-creating CSR activities. Even B2B firms can learn from best practices based on alignment; B2C firms should look well outside their industries, or further up their supply chains, to benchmark and learn. Despite these recommendations, we do not measure alignment directly in this study, so continued research is needed to better understand the role of alignment in the CSR–satisfaction–value creation process.

Limitations and Further Research

It is important to test the impacts of CSR activities on customers and subsequent firm value continuously, to reflect how customers’ and shareholders’ perceptions of the value of these activities continue to evolve. Similar to Luo and Bhattacharya (2006), our study relies on an overall index of CSR performance, but various types of CSR might differentially affect product versus service firms and B2B versus B2C firms. For service and B2C firms, for which the impact is lower, a better understanding of how to redeploy resources from lower impact to higher impact activities would be especially pertinent. In addition, Du et al. (2010) indicate that effective CSR communication can increase the financial outcomes of CSR. To increase those outcomes for service and B2C firms, future research can investigate the effective communication means and attributes. Although our sample comprises many firms representing different contexts, the number observations in sub-samples (i.e., B2C-product, B2C-service, B2B-product, and B2B-service) is limited, which prevents us from analyzing and comparing firms in those sub-samples in details. Additional research might compare all four groups, using more equivalent sample sizes. As previous research on CSR–performance indicates (e.g., Hull and Rothenberg 2008), other firm- and industry-related factors, such as advertising activities, might moderate the investigated relationships. Future research can extend our knowledge on the impacts of CSR by taking different moderators into account.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.