Abstract

Despite the growing importance of servitization as a source of competitiveness for manufacturers, limited knowledge exists about organizational issues of servitization. Drawing on transaction cost economics theory and a configuration theoretical perspective, our study illuminates different organization architectures for servitization and how firms align such architectures with servitization approaches to achieve high financial performance. We analyze qualitative data based on interviews with 22 managers and quantitative data from a survey of 161 equipment manufacturers. The results indicate that manufacturers mostly opt for one of three organization architectures for servitization: internal product business unit, internal specialized service business unit, or external service provider. In addition, they reveal equifinal configurations of servitization characteristics to achieve high financial performance for each organization architecture. The internal specialized service business unit turns out as a flexible organization architecture to successfully provide smoothing, adapting, and substituting services. The use of an external service provider is less suited for the provision of adapting and substituting services, which require more knowledge specialization and coordination. All three organization architectures can be used to provide smoothing services. In summary, the results may serve as decision-making templates for aligning organization architecture, offering characteristics, and service provider integration to pursue servitization successfully.

Keywords

Introduction

Manufacturers across diverse industries use servitization, that is, the augmentation of a product offering by adding services, to address changing customer needs and improve their competitive position (Eggert et al. 2014; Gebauer et al. 2010; Josephson et al. 2016; Patel et al. 2019). For instance, Kornit, the producer of high-speed industrial inkjet printers and one of the world’s fastest-growing manufacturers, launched KornitX as a specialized subsidiary to offer customized industrial services to its business customers (Fortune 2021; Kornit 2022). Similarly, Kone, a leading escalator and elevator manufacturer, indicated in their recent annual report that modernization and predictive maintenance services made up 51% of sales in 2022 after adopting a strategy to become less dependent on core product sales (Kone 2022).

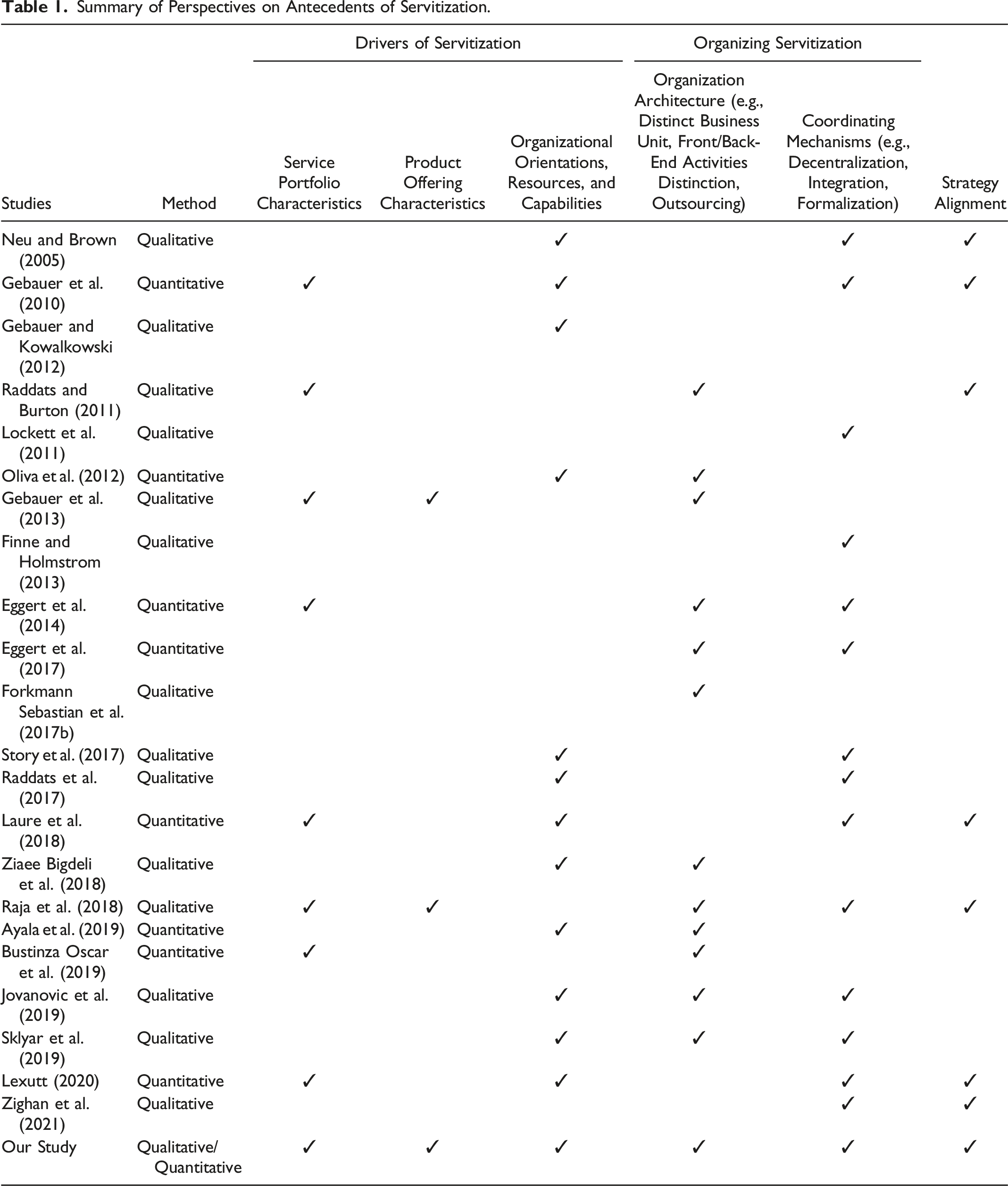

Summary of Perspectives on Antecedents of Servitization.

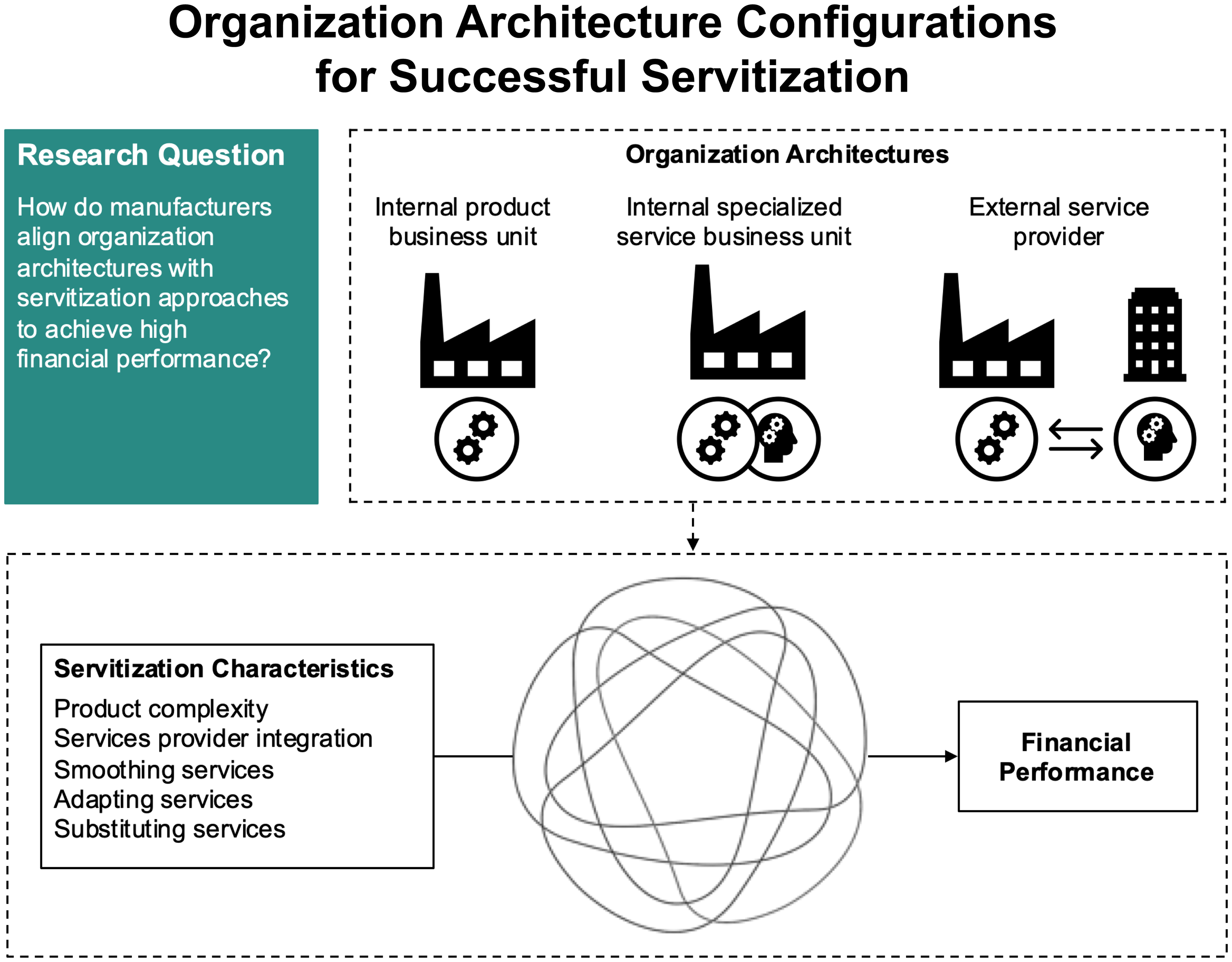

While prior research has contributed to the understanding of servitization, it provides limited guidance regarding the performance implications of the interplay between the organization architecture for servitization on the one hand, and servitization approaches on the other. Organization architecture refers to the formation of organizational elements of a system, the relationships between them and the environment, and the principles that guide its design and evolution (Fjeldstad et al. 2012). It helps understand how arrangements that may also span organizational boundaries affect the emergence and transformation of business activities (Fjeldstad and Snow 2018; Gulati et al. 2012). Servitization approaches can be classified as smoothing services (i.e., complementary services that facilitate product sales or usage), adapting services (i.e., services that significantly expand a product’s functionality), and substituting services (i.e., services that substitute a firm’s current product-centric orientation with a fully service-centric one) (Cusumano et al. 2015). The few existing studies that have examined servitization approaches from the perspective of the formation of organizational elements point to several distinct arrangements, including an internal organization where products and services are both managed by the manufacturer, and an external organization where a specialist service provider acts on behalf of the manufacturer, or a range of hybrid options (Oscar et al. 2019; Kowalkowski et al. 2011). Our study seeks to further illuminate such organizational issues for servitization and investigates the following research question: How do manufacturers align organization architectures for servitization with servitization approaches to achieve high financial performance?

Today, firms in many industries tend to concentrate on core activities and outsource non-core activities to external partners in order to access diverse capabilities and expertise and capitalize on greater flexibility (Fjeldstad et al. 2012), thus changing the existing organization architectures and forming new ones that can include external partners. Understanding organization architectures for servitization is important as it relates to manufacturers’ make-or-buy decisions pertaining to service production and delivery (Oscar et al. 2019; Finne and Holmström 2013; Sebastian et al. 2017b). Such make-or-buy decisions can be understood by evaluating the transaction costs of different organization architectures (Walker and Weber 1984). In the context of servitization, these decisions may differ due to distinct infrastructures that connect actors involved in service production and delivery, protocols that define the code of conduct during service provision, and common resources available to the actors involved in servitization (Fjeldstad et al. 2012; Sebastian et al. 2017b).

Using transaction cost economics theory (TCE; Tadelis 2002; Williamson 1991), we characterize different organization architectures for servitization. In addition, based on a configuration theoretical approach (Misangyi et al. 2017), we examine the interplay between different servitization characteristics to explain firm performance for different organization architectures. Advancing research on servitization through these lenses addresses recent calls for more theoretically pluralistic inquiries (e.g., Oscar et al. 2019; Forkmann et al. 2017; Kohtamäki et al. 2019). Based on a multi-step research design, we analyze data from a qualitative study of 22 managers of equipment manufacturers and a quantitative survey of 161 equipment manufacturers.

Our findings reveal that for all organization architectures, the provision of smoothing services is part of the configurations to achieve high financial performance. Furthermore, manufacturers utilize internal product business units over organizational outsourcing options (i.e., an external service provider) when offering highly complex core products and adapting services, particularly when the production and delivery of integrated product-service bundles require greater degrees of knowledge specialization and coordination. When offering substituting services for highly complex products, manufacturers employ a specialized service business unit.

Our study contributes to the servitization literature in three ways. First, our results corroborate insights from previous studies that have outlined alternative organizational arrangements for servitization (Oscar et al. 2019; Ziaee Bigdeli et al. 2018). The results of our qualitative study indicate that manufacturers mostly opt for one of three organization architectures: They provide servitized offerings through an internal product business unit, an internal services business unit, or an external services provider. We advance the existing literature by showing that the success of such organization architecture decisions is associated with further factors, including offering characteristics (i.e., core product, service portfolio) and their strategic characteristics (i.e., product/service orientation, service provider integration).

Second, our findings extend the research on the alignment between different servitization approaches and organizational factors to achieve high performance (e.g., Eva et al. 2017; Neu and Brown 2005). The results of our quantitative study indicate that for each organization architecture, there are multiple sufficient configurations of factors to achieve high financial performance. Thus, we advance the extant literature (e.g., Finne and Holmstrom 2013; Gebauer and Kowalkowski 2012) by showing that there is no single optimal way for organizing servitization, but equifinality is demonstrated (i.e., alternative pathways to achieve the same high-performance outcome exist). In addition, these findings offer new insights into the connections between the organization architecture and servitization, which may guide managers to find ways to decrease the risk of failure (e.g., Kowalkowski et al. 2013; Raja et al. 2018).

Third, our findings indicate that organization architectures for servitization vary in terms of the TCE mechanisms (i.e., interaction and coordination costs, information asymmetry, knowledge specialization, and asset specificity) and the provision of different servitization approaches. Smoothing services are part of performance-enhancing configurations in all organization architectures, indicating that this servitization approach is less constrained by TCE mechanisms compared to other servitization approaches. However, our findings also suggest that asset specificity and knowledge specialization are more important than interaction or information aspects when providing substituting services.

Overall, our findings advance the understanding of servitization and its organization and allow for the development of potential templates for decision-makers. These templates may be useful in assessing a manufacturer’s existing servitization approach and organization architecture and in providing guidance when a manufacturer envisages a servitization trajectory, such as shifting from merely offering smoothing services to offering adapting and substituting services.

Conceptual Background

Perspectives on Servitization

Servitization is considered a strategic option for manufacturers to differentiate products from competing offerings and escape the product commoditization trap (Laure et al. 2018; Eggert et al. 2014; Enke et al. 2022). Over the last two decades, scholars have used different conceptualizations and classifications to describe manufacturers’ servitized offerings (e.g., Rabetino et al. 2018, 2021; Wang et al. 2018). Although servitization can be defined in manifold ways, prior work largely agrees that it involves a transformation process in manufacturing firms that involves a shift from a product-centric to a service-centric business approach (Kohtamäki et al. 2019; Kowalkowski et al. 2017; Rabetino et al. 2018; Wang et al. 2018). Thus, servitization may entail major changes in a manufacturer’s resources and capabilities, offering composition, or organization architecture (Forkmann et al. 2017a; Lexutt, 2020; Raja et al. 2018; Ulaga and Reinartz 2011).

Following Cusumano et al. (2015), our study distinguishes different types of servitized offerings, namely smoothing, adapting, and substituting services. Smoothing services facilitate product sales or usage without significantly altering a product’s functionality (e.g., delivery, installation, maintenance, helpdesk, training, finance, and warranty). These services can often be standardized and reused with slight adjustments for different customers (Laure et al. 2018). Adapting services significantly expand a product’s functionality or help the customer develop novel product usages (e.g., customization, upgrades, optimization, refurbishing, and technical consultancy). These services are tightly coupled with product characteristics as part of a customized solution for a specific customer and do not lend themselves easily to standardization (Laure et al. 2018). Finally, substituting services replace the purchase and use of a product by a customer and provide an integrated and outcome-related solution (e.g., fully managing product-related operations such as Rolls-Royce’s power-by-the-hour solution or complete outsourcing). Substituting services are about “reconfiguring the responsibilities within the value chain” (Gebauer et al. 2010, p. 201), where manufacturers retain full responsibility for (parts of) the customer’s operations (Laure et al. 2018; Cusumano et al. 2015).

The classification proposed by Cusumano et al. (2015) captures manufacturers’ options ranging from offering merely complementary services in addition to core products to substituting their current product-centric orientation with a fully service-centric one. In line with Laure et al. 2018; Raja et al. 2018, we view smoothing services as basic services that can be conceived as one end of the servitization spectrum, where basic services are added to a manufacturer’s products, possibly using the existing organization architecture without requiring too many transformational changes. Substituting services are at the other (most complex) end of the servitization spectrum and often require new organizational resources, capabilities, or organization architectures (Laure et al. 2018). Adapting services fall between smoothing and substituting services and reside in the middle of this spectrum (Cusumano et al. 2015).

Forms of Organization Architecture and Types of Servitized Offering

There is evidence that manufacturers utilize different organizational arrangements for servitization that sometimes even transcend their organization’s boundaries (Sebastian et al. 2017b; Kowalkowski et al. 2013). Potential reasons for collaborating with external partners include internal challenges in integrating new services into existing product-centered operations or aligning them with ossified product orientations, and thus to commercialize these services profitably (Gebauer et al. 2013). A manufacturer may remain principally a product provider but also possess additional service processes to offer smoothing services as add-ons to standalone products or as part of a service bundle (Laure et al. 2018; Cusumano et al. 2015). Such an initial servitization approach is less likely to necessitate any fundamental organization design changes on behalf of the manufacturer (Laure et al. 2018). Another approach includes the provision of adapting services with the manufacturer acting as both a product and service provider to offer tailored solutions to customers (Cusumano et al. 2015). Here manufacturers need to develop more advanced service-related capabilities and frequently revise the existing organization architecture accordingly (Laure et al. 2018). Manufacturers providing substituting services often manage a combination of multiple smoothing and/or adapting services together with products. However, the provision of substituting services is not simply an offering expansion strategy as it may require major revisions of the existing organization architectures (Laure et al. 2018; Forkmann et al. 2017; Raja et al. 2018).

Misalignment of a manufacturer’s servitization approach and its organization architecture can increase failure risks (Benedettini et al. 2015; Raja et al. 2018). Prior work suggests that firms can achieve servitization success through specific configurations of business model elements (e.g., service capabilities, pricing strategies, implementation processes) in relation to the chosen servitization characteristics (Forkmann et al. 2017a). Many studies show that different servitization approaches increase performance when other factors, such as service culture, customer interfaces, and service delivery systems, are present (Laure et al. 2018). Hence, the literature suggests compound effects of multiple interrelated factors that determine servitization success. In particular, servitization characteristics (i.e., type of servitized offering, core product characteristics), strategic characteristics (i.e., organizational capabilities), and environmental characteristics (i.e., competitive intensity, technological turbulence) are key drivers of servitization success. Based on these considerations, we posit that alignment between a manufacturer’s organization architecture for servitization with its servitization approach may be important for achieving superior performance. Our multi-step research design examines this interplay between servitization-related characteristics and unpacks configurations thereof to explain financial success across different organization architectures.

Organization Architectures for Servitization: A Make-or-Buy Consideration

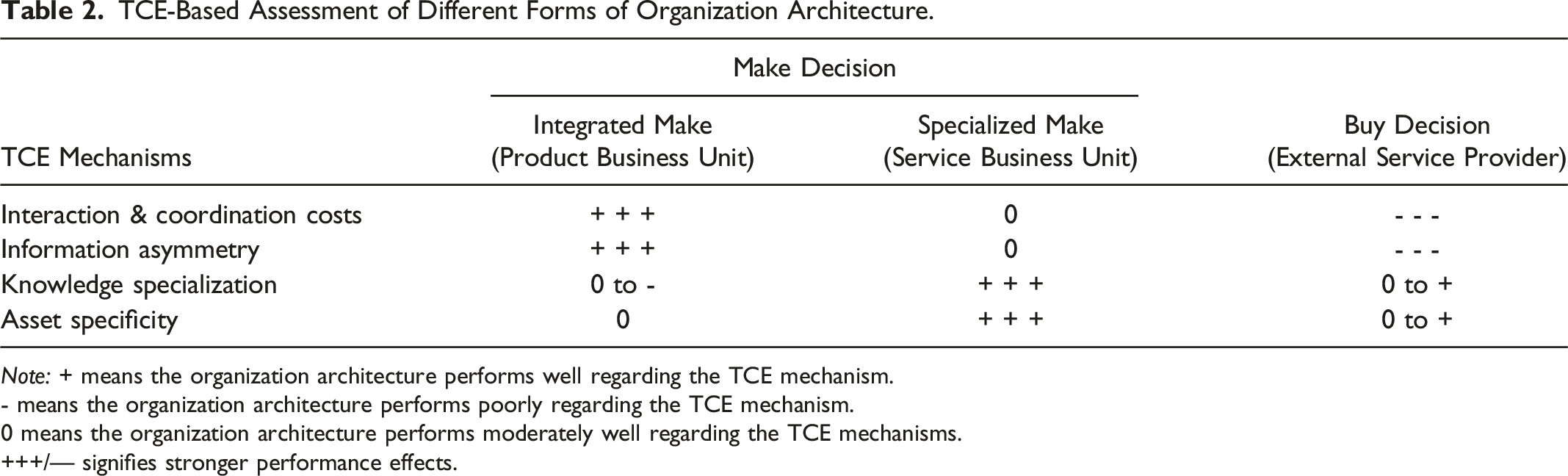

TCE serves as the theoretical lens to explain different forms of organization architectures for servitization, in particular the underlying make-or-buy decision that manufacturers must make (Tadelis 2002). TCE is often used to understand the efficacy of such make-or-buy decisions (Geyskens et al. 2006; Walker and Weber 1984) and illuminates the transaction costs associated with different forms of organization architecture. It considers the concepts of interaction and coordination costs, information asymmetry, knowledge specialization, and asset specificity (Williamson 1991). From a TCE perspective, firms tend to vertically integrate (make decision) when the internal transaction costs for achieving a strategic aim (such as providing servitized offerings) are low (Williamson 1991). Firms tend to outsource activities (buy decision) and thus form organization architectures that transcend the organization’s boundaries (Brusoni et al. 2001; Eggert et al. 2017), when internal control and coordination costs are higher than transaction costs with a third party.

For both customers and manufacturers, servitization represents such a make-or-buy decision (Oscar et al. 2019; Eggert et al. 2017; Bigdeli et al. 2018). For example, a customer needs to decide if they will perform the maintenance services for a machine themselves (make decision), or if they want the manufacturer or a third party to take on this service task (buy decision). From the perspective of the manufacturer, providing such maintenance services could be done in their name through a third-party services provider (buy decision) or in-house (make decision) (Gebauer et al. 2010). For “making,” manufacturers have additional choices: integrating the production and delivery of products and services in one organizational entity, usually the product business unit (i.e., an “integrated make decision”) or differentiating the production and delivery of products from that of services, and consequently forming a separate, more specialized service business unit (in addition to a product unit) with responsibility for service provision (i.e., a “specialized make decision”) (Brusoni et al. 2001; Zhou 2013).

Manufacturers that use an internal product business unit to provide servitized offerings (integrated make decision) have the advantages of full control, high integration, and low information asymmetry (between product and service elements of the offering). However, the product business unit often does not possess specialized service knowledge and capabilities (Raja et al. 2018). Hence, some manufacturers may develop a dedicated internal service business unit (specialized make decision) equipped with the necessary knowledge to provide servitized offerings (Gebauer and Kowalkowski 2012; Raja et al. 2018). This organization architecture, however, can come with major costs (e.g., due to developing service-related knowledge capabilities in-house and creating internal transaction costs). Consequently, some manufacturers work with external service providers (buy decision) that are specialized in service provision.

TCE-Based Assessment of Different Forms of Organization Architecture.

Note: + means the organization architecture performs well regarding the TCE mechanism.

- means the organization architecture performs poorly regarding the TCE mechanism.

0 means the organization architecture performs moderately well regarding the TCE mechanisms.

+++/--- signifies stronger performance effects.

Interaction and coordination costs relate to the efforts necessary to ensure that the services offered provide value to customers by being specific to and integrated with the particular underlying product (e.g., Buvik and John 2000; Ellram et al. 2008). With an integrated make decision, all product- and service-related activities are subsumed within a manufacturer’s product business unit, which suggests low (internal) interaction costs. This high degree of integration is partially abandoned with a specialized make decision for the organization architecture, that is, when separate business units (i.e., a product unit and a service unit) within the manufacturer contribute to the development and provision of servitized offerings. The interactions of these internal units might be affected by distinct unit cultures, budgets, or operating procedures, and (internal) interaction and coordination costs will increase due to organizational differentiation. Finally, a buy decision may cause even higher interaction and coordination costs as relational governance mechanisms must be established to balance interests (Geyskens et al. 2006) and safeguard against opportunistic behaviors by the external service provider (e.g., misuse of proprietary information).

Information asymmetry, which relates to the (different) information states that parties to a transaction hold (Tadelis 2002), can also be used to characterize the forms of organization architecture. Information asymmetry ought to be lowest for an integrated make decision since the product and service offering is developed and delivered in an integrated manner via one (product) business unit. For a specialized make decision, some information asymmetries may exist as two different business units within the manufacturer need to integrate their partial offering components vis-à-vis an organizational buyer (Zhou 2013). In such a situation, information slippages, delays, or miscommunications may interfere with the seamless provision of servitized offerings. Finally, for a buy decision via an external service provider, information asymmetry should be highest as intentions and behaviors of external service providers may be even more difficult to perceive, predict, and evaluate.

Knowledge specialization considers resource specialization issues, particularly around knowledge, in the context of TCE (Brusoni et al. 2001). Choosing an integrated make decision as the organization architecture often does not allow for specialized servitization knowledge to develop. Product units charged with servitization tasks often struggle to develop sufficient service orientation and are thus hampered when deploying more complex services (Gebauer and Kowalkowski 2012; Oliva et al. 2012; Raja et al. 2018). Specialized make decisions remove such barriers since a dedicated in-house service unit can develop the necessary servitization expertise. Similar considerations are also at play in the buy decision case as the third organization architecture form: the external service provider is specialized and thus can develop some proprietary service-focused knowledge (Eggert et al. 2017).

Asset specificity, referring to the underlying resources and the resulting capabilities (Williamson 1991), can also be associated with organization architectures. Asset specificity for servitization affects the delivered quality of the servitized offering to the customers. In an integrated make decision, the service aspect of the offering is often in jeopardy as the competition for resources in the product business unit (and its likely preference for product-centric investments) may suppress service-specific assets. This may hinder the manufacturer from developing the required service capabilities or hiring the required service specialists for the product business unit (Oliva et al. 2012; Raja et al. 2018). Using an external service provider as part of a buy decision can, to some extent, counteract this issue and ensure service-centered asset specificity. However, similar to the arguments relating to knowledge specialization, the external service provider may have to “hedge their bets” and work with assets they can use in conjunction with multiple different manufacturers. Alternatively, their assets may have limited specificity due to information gaps relating to the underlying characteristics of the manufacturer’s product. The highest level of asset specificity is expected in a specialized make decision via a dedicated service business unit that can use its superior knowledge of the underlying product, combined with its relative independence from product-centric management decisions, to develop specific assets and thereby ensure the highest degree of delivered value of a servitized offering.

Based on these considerations, we conclude that no form of organization architecture is per se more appropriate for servitization from a TCE perspective. To understand the contingencies of when specific organization architectures allow successful servitization, we employ a multi-step approach to unpack how firms align organization architectures for servitization and servitization approaches to achieve high financial performance.

Overview of Studies

We conducted a qualitative pre-study to explore the possible forms of organization architecture of servitization (as outlined in the literature) and to ascertain with which servitization characteristics such architectures interact. Based on the insights obtained in the qualitative study, we then conducted a quantitative study to investigate the interplay between relevant servitization characteristics to achieve high financial performance for different organization architectures.

Qualitative Pre-study

Overview

We conducted semi-structured interviews with 22 executives across 17 equipment manufacturers in diverse sectors. The studied firms include medium and large multinational manufacturers to better understand any possible variances of organization architecture in different settings. The interviewees were senior executives in charge of key account management and services across business units that provide servitized offerings. We sampled firms with varied characteristics in terms of market experience (i.e., the number of years present in the market) or servitization strategy (i.e., types of services offered). The selected equipment manufacturers are innovation champions and among the leading players in their sectors. All studied firms offer products and services to international markets. Data collection ceased when theoretical saturation was reached, that is, when later interviews corroborated earlier interviews and no additional insights were found (Strauss and Corbin 1990). We coded and analyzed the interview transcripts using thematic analysis (Gioia et al. 2013) based on the theoretical themes and antecedents of servitization derived from the literature. Online Appendix I outlines the sample composition and the details of coding and thematic analysis.

Findings and Discussion

In line with the extant literature (Oscar et al. 2019; Eggert et al. 2017; Finne and Holmström 2013; Sebastian et al. 2017b), we found that the studied manufacturers use mainly three forms of organization architectures for servitization: a) an internal product business unit, b) an internal specialized service business unit (often newly created), or c) an external service provider. We also discovered that manufacturers do not necessarily employ only one organization architecture when pursuing different types of servitization. The studied manufacturers choose either a single organization architecture (e.g., only an internal product business unit) or a combination of organization architectures (e.g., both a product business unit and external service providers). The interviews also revealed that manufacturers’ decisions regarding organization architectures are affected by other servitization conditions (i.e., service characteristics, service provider integration). For instance, many manufacturers offer smoothing services through external service providers to minimize operation costs for standardized services across diverse geographical areas. These manufacturers often use a “certified supplier” program (i.e., a comprehensive training and monitoring program for external service providers) to ensure that external service providers follow their standards when interacting with customers. By contrast, when the level of product complexity and service customization is high, many manufacturers choose to deliver services internally through either their product or their service business unit.

Some manufacturers reduce reliance on external service providers and employ internal service business units to interact with customers more closely to develop customized product-service offerings. Many respondents also considered developing a specialized service business unit to reduce “knowledge leakages,” avoid “opportunistic behavior” by external service providers, and have more “control over interactions” with customers. The findings also show that the degree of integration and shared objectives between the focal firm and external service provider is critical for offering more sophisticated core products or servitized offerings. We also found that while firms’ strategic characteristics (e.g., service and product orientations) and environmental characteristics (e.g., technological turbulence) affect servitization, these characteristics seem less connected to issues relating to organization architecture decisions.

In sum, the findings point to servitized offering characteristics, product complexity, and service provider integration as important conditions of servitization that somehow interact. Together with a manufacturer’s organization architecture for servitization, these factors may predict servitization success and are therefore considered in our quantitative study.

Quantitative Study

Overview

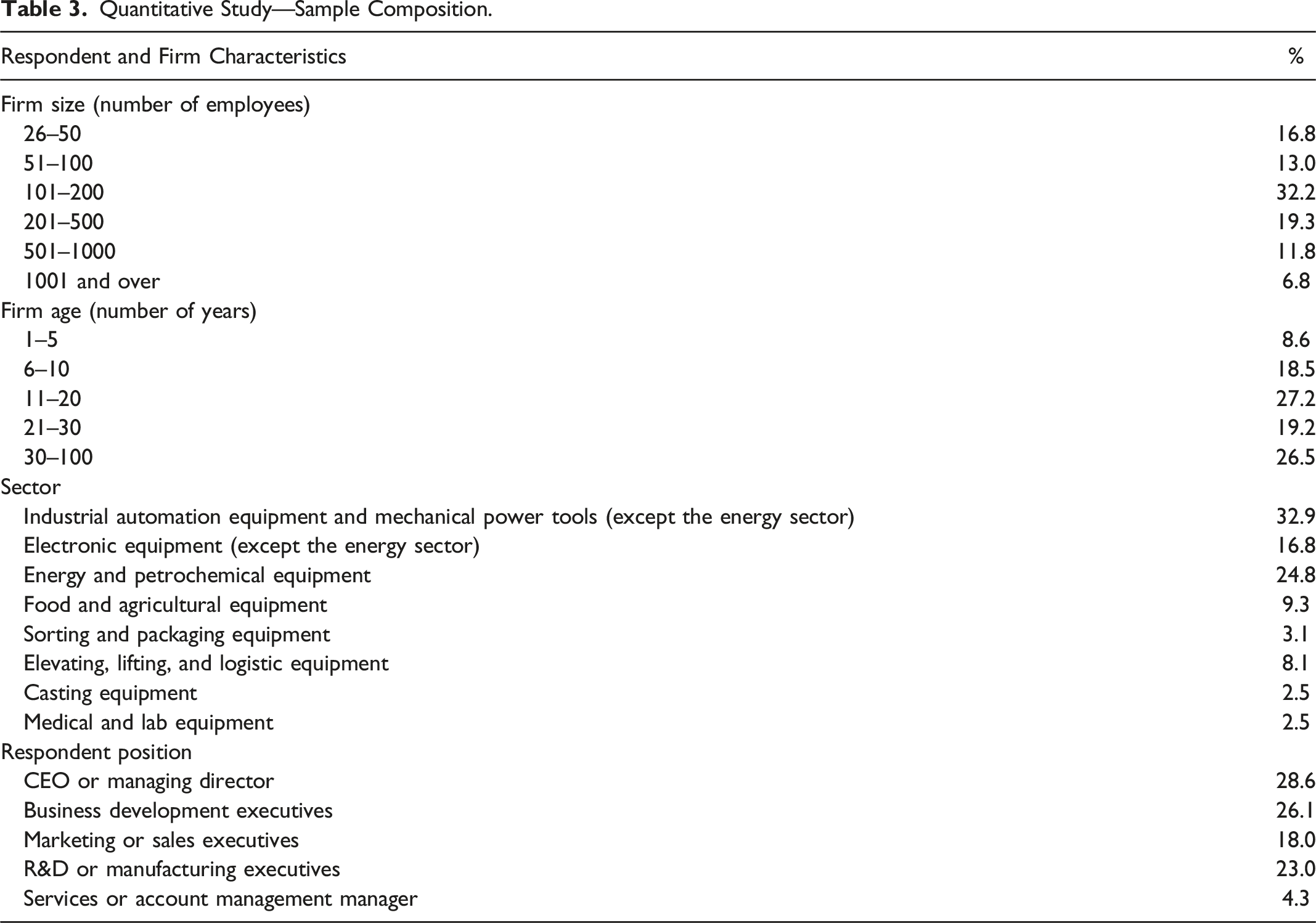

We used a standardized questionnaire as the data collection instrument and surveyed managers from equipment manufacturers in Iran. We selected this research setting for several reasons. First, Iran is one of the “Next Eleven” emerging economies, that is, a fast-growing market with the potential to become a large economy (Barker 2012). Although international sanctions have affected Iran’s economic growth, its economy bounced back in 2016 at an annual growth rate of 6.4% (World Bank 2017). We collected the data during this period of economic development in 2017. Iran represents one of the most industrialized economies in the Middle East with over 40 major industry sectors, including automotive, chemicals, and consumer durables. Using a sample from an emerging economy also counterbalances the existing bias in the servitization literature, which has mainly focused on firms in developed countries (Subramaniam et al. 2015).

We collected data from equipment manufacturers operating in diverse sectors, including casting, industrial automation, electrical, and energy and petrochemical equipment. The sampling frame consisted of a random list of 400 manufacturers, which we obtained from the business directory of two Iranian universities. We collected data using an online survey. Key informants received an invitation email including a link to the online questionnaire. The email explained the purpose of the study and it assured anonymity and confidentiality.

Quantitative Study—Sample Composition.

Measurement Instruments and Validation Procedure

We measured all but one construct with established measures (see Online Appendix II for an overview of the construct measures). We measured product complexity using five items from Wang et al. (2017). We used eight items from Flynn et al. (2010) to capture service provider integration. Technological turbulence and competitive intensity were measured using three items each from Gerald et al. 2015. We adapted four items each from Vorhies and Morgan (2005) to measure firms’ product and service orientations. To capture the type of servitized offerings, we developed self-typing descriptions based on previous studies (Laure et al. 2018; Cusumano et al. 2015; Windahl and Lakemond 2010). Specifically, we pre-tested three paragraphs describing different services that firms could provide in combination with core products. For each of these services, we also gave different examples. Respondents were asked to assess each of the services regarding their importance as part of the manufacturer’s offering to customers. We employed a seven-point Likert-type importance scale anchored from 1 = “not important at all” to 7 = “extremely important.” Based on insights from the qualitative study, we also asked respondents to indicate who has mostly been responsible for providing these services to main customers for the last 2 years using three choices for distinct organization architectures: a) an internal product business unit, b) an internal service business unit, or c) an external service provider. Finally, we adopted five items to capture firm performance compared to their main competitors (Zhou et al. 2005). We also captured firm size (the number of full-time employees) and firm age (the number of years since the firm was founded). We developed the questionnaire in English and professionally translated it into Persian following the back-translation procedure to ensure comprehensibility and equivalence between the target and the source versions of the questionnaire (Brislin 1970). We pre-tested the questionnaire with eight managers to identify and revise unclear terms and ambiguous questions and simplify sentence structures where needed.

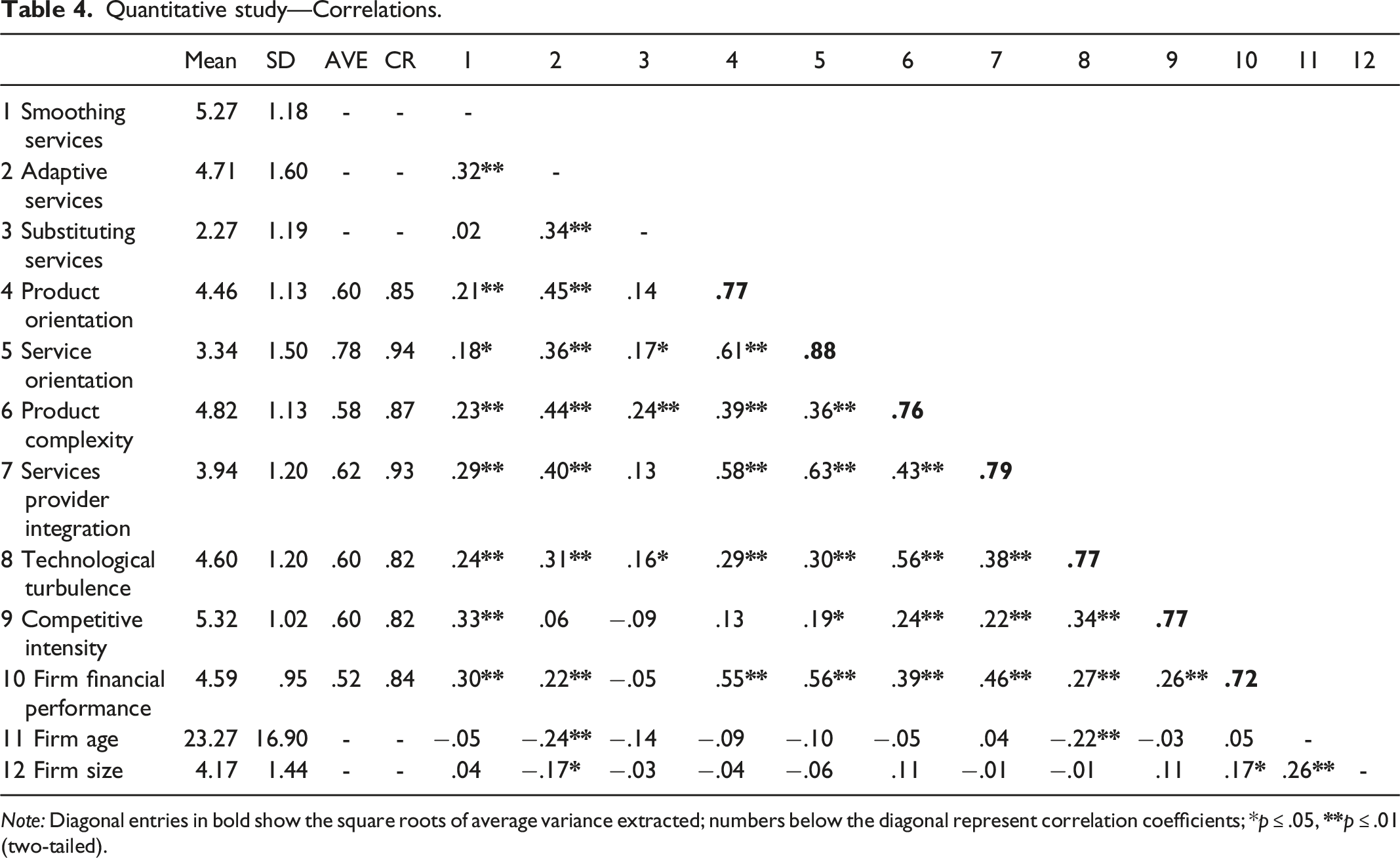

Quantitative study—Correlations.

Note: Diagonal entries in bold show the square roots of average variance extracted; numbers below the diagonal represent correlation coefficients; *p ≤ .05,

We examined non-response bias by comparing early and late respondents (Armstrong and Overton 1977). The results of a series of t-tests showed no significant differences between the two samples (p > .05). We used procedural and statistical remedies to control for common method variance (CMV) (MacKenzie and Podsakoff 2012; Podsakoff et al. 2003). Procedural controls included measures to ensure sufficient levels of knowledgeability to answer the questions. In addition, we reduced the potential for social desirability by providing informants with explicit instructions to reflect the actual situation in their organization when answering the questions and by promising anonymity and confidentiality to the respondents when we invited them to participate in the study.

Besides procedural controls, we assessed possible common method bias using the latent common method factor approach (Podsakoff et al. 2003). We built a second measurement model that included a latent common method factor. In addition to their respective factors, in this model, all items are loaded on the common method factor. Following Büttgen et al. (2012), we forced the factor loadings of the common method factor to be equal as a differential impact of the common method factor on different items can be ruled out by definition. The comparison of the measurement model without the common method factor with the measurement model that includes the method factor (χ2 = 680.17, df = 432, CFI = .92; TLI = .91; RMSEA = .06) show no significant difference. Online Appendix II presents the confirmatory factor analysis with and without the method factor. The results indicate that overall fit statistics indicate that both measurement models fit the data reasonably well and provide sufficient evidence of discriminant and convergent validity. As shown in Online Appendix II, the standardized loadings slightly decreased with the inclusion of the method factor. Therefore, the results indicate no evidence of CMV.

Data Analyses and Findings

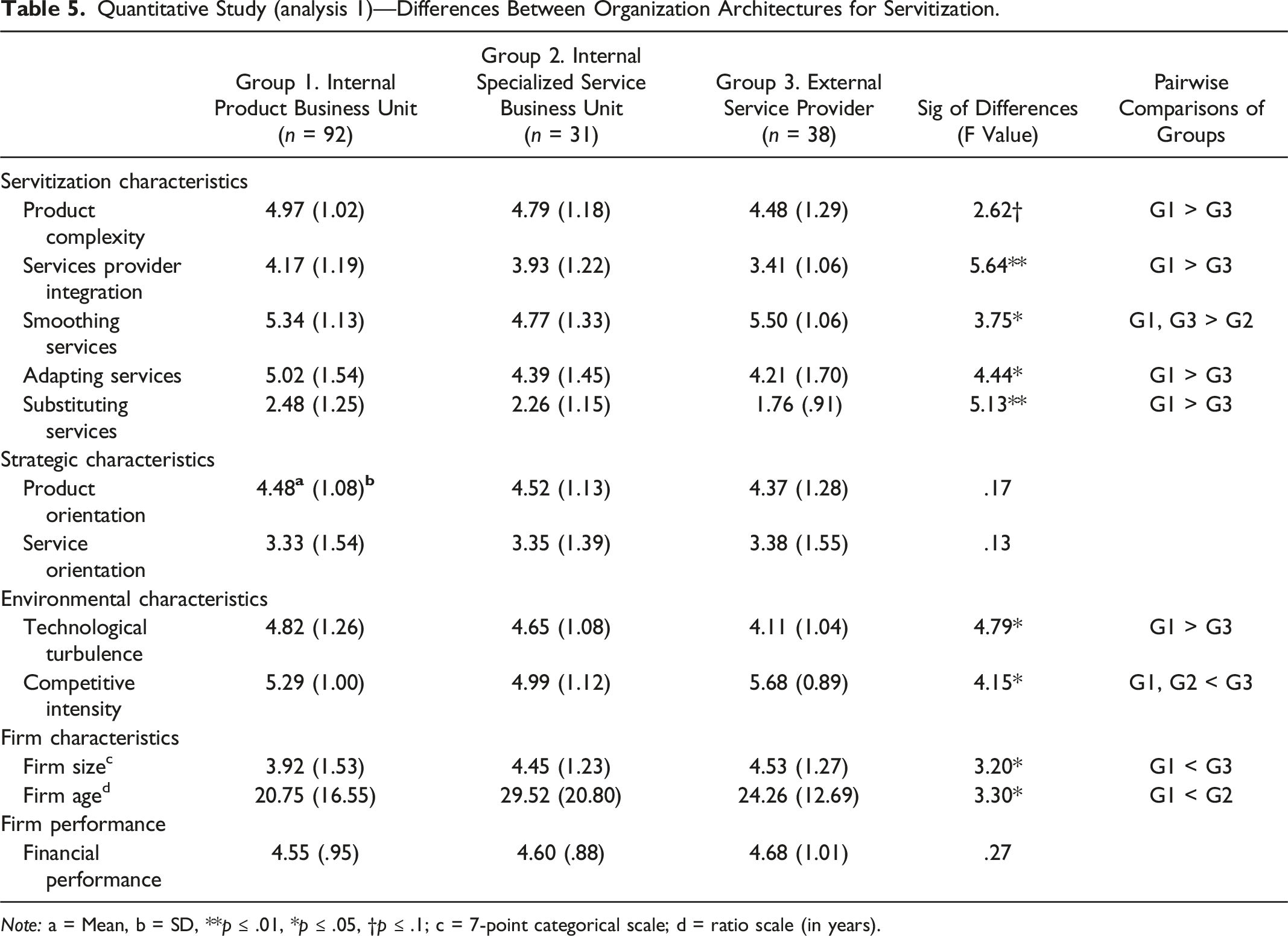

To understand how servitization is configured to achieve high performance, we analyzed the data via a two-step approach. First, we conducted an analysis of variance and pairwise comparisons to examine the differences between the three organization architectures for servitization pertaining to the firm’s strategic characteristics, offering characteristics, structural parameters, and environmental characteristics (Analysis 1). Second, we conducted a fuzzy-set qualitative comparative analysis (fsQCA) to examine the interplay between servitization-related characteristics and unpack configurations thereof to explain financial success for each of the three organization architectures (Analysis 2).

Analysis 1

Quantitative Study (analysis 1)—Differences Between Organization Architectures for Servitization.

Note: a = Mean, b = SD, **p ≤ .01, *p ≤ .05, †p ≤ .1; c = 7-point categorical scale; d = ratio scale (in years).

Analysis 2

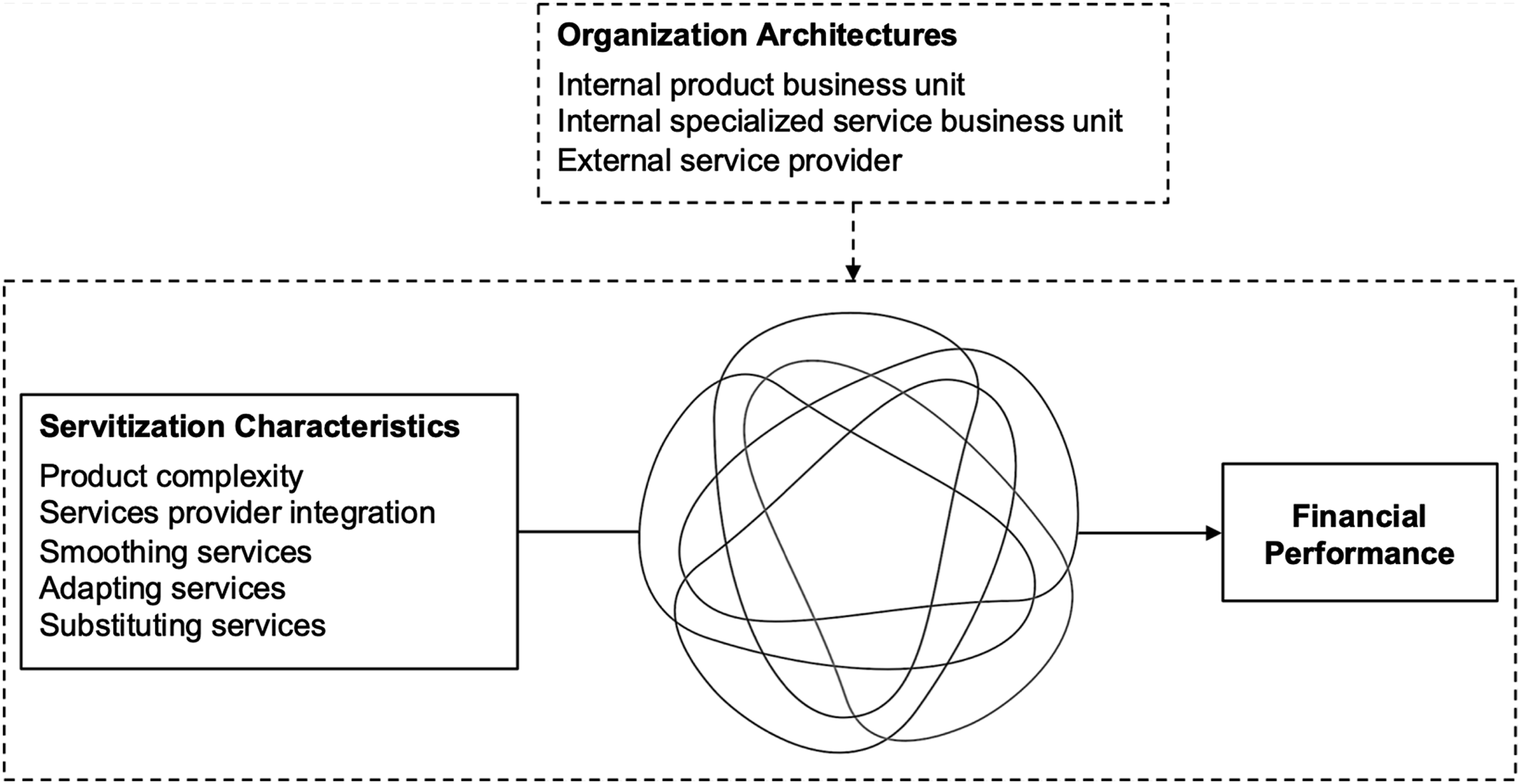

Based on insights from Analysis 1, we developed a theoretical framework (Figure 1) to unpack the configurations of conditions that manufacturers use to achieve high financial performance with servitization. In this analysis, we focus on those variables that characterize a manufacturer’s servitization approach. We excluded conditions that are not under a firm’s volitional control (i.e., environmental factors). In addition, we excluded conditions that did not show significant differences across the organization architectures in analysis 1 (i.e., product and service orientations). Theoretical framework for quantitative study—Analysis 2. Note: The Venn diagram illustrates configurations of servitization characteristics (antecedents) to accomplish high financial performance (outcome). We examined the configurations for each organization architecture separately.

Our theoretical framework is based on the configuration theoretical perspective, which has received considerable attention in recent years (e.g., Furnari et al. 2021; Misangyi et al. 2017). Configuration theory is based on the notion that “organizational phenomena can best be understood by identifying distinct, internally consistent sets of firms and their relationships to their environments and performance outcomes over time rather than by seeking to uncover one universal set of relationships that hold across all organizations” (Ketchen et al. 1997, p. 224). From this perspective, firms are systems of interdependent elements, and configurations are patterns of these elements that commonly occur together and are orchestrated and connected by a unifying theme (Meyer et al. 1993). Configuration theory holds that for sets of elements there co-exists a (limited) number of configurations that enable organizations to achieve superior performance (Ketchen et al. 1997). Configuration theory thus accommodates causal complexity, defined as “a situation in which a given outcome may follow from several different combinations of causal conditions” (Ragin Charles 2008, p. 124).

We used a configurational approach based on fsQCA to describe how the membership of cases (here firms) in sets of antecedent conditions (or combinations thereof) is linked to membership in the outcome set (financial performance). FsQCA examines the explicit connections between conditions in terms of necessity and sufficiency (Charles, 2008) and has been used to better understand servitization (e.g., Forkmann et al. 2017a; Salonen et al. 2020).

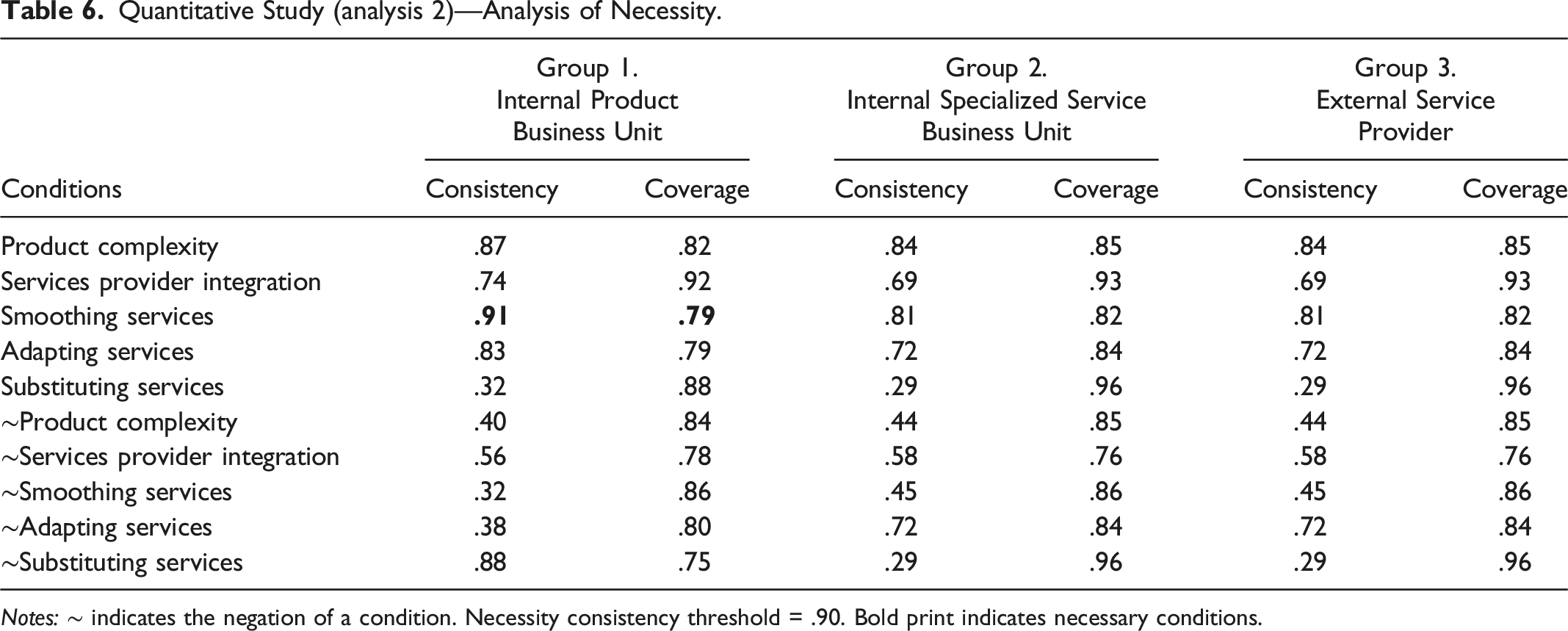

We performed the analyses in multiple steps following the procedures outlined in the QCA literature (e.g., Fiss, 2011; Ragin Charles, 2008). First, we calibrated the construct measures to obtain the fuzzy-set membership scores for each of the cases in the sets of antecedent conditions and the outcome set. We used the direct method of calibration to obtain the fuzzy-set scores for all conditions. We calibrated the fuzzy-set using the scale anchors. All scales were Likert-type rating scales ranging from 1 to 7. The calibration approach ties fuzzy-set membership scores to the scale descriptors and thus a respondent’s degree of (dis)agreement with, or relevance attached to, the items for a construct. We set the threshold for full membership in a fuzzy set at value 7 and for full non-membership at value 1. We used value 4 for the crossover point. This calibration approach is in line with prior QCA literature (e.g., Salonen et al. 2020). In the next step, we performed an analysis of necessity to examine whether any of the antecedent conditions or their negations are necessary for the outcome. Finally, we ran an analysis of sufficiency to identify consistently sufficient configurations of conditions for high financial performance.

Quantitative Study (analysis 2)—Analysis of Necessity.

Notes: ∼ indicates the negation of a condition. Necessity consistency threshold = .90. Bold print indicates necessary conditions.

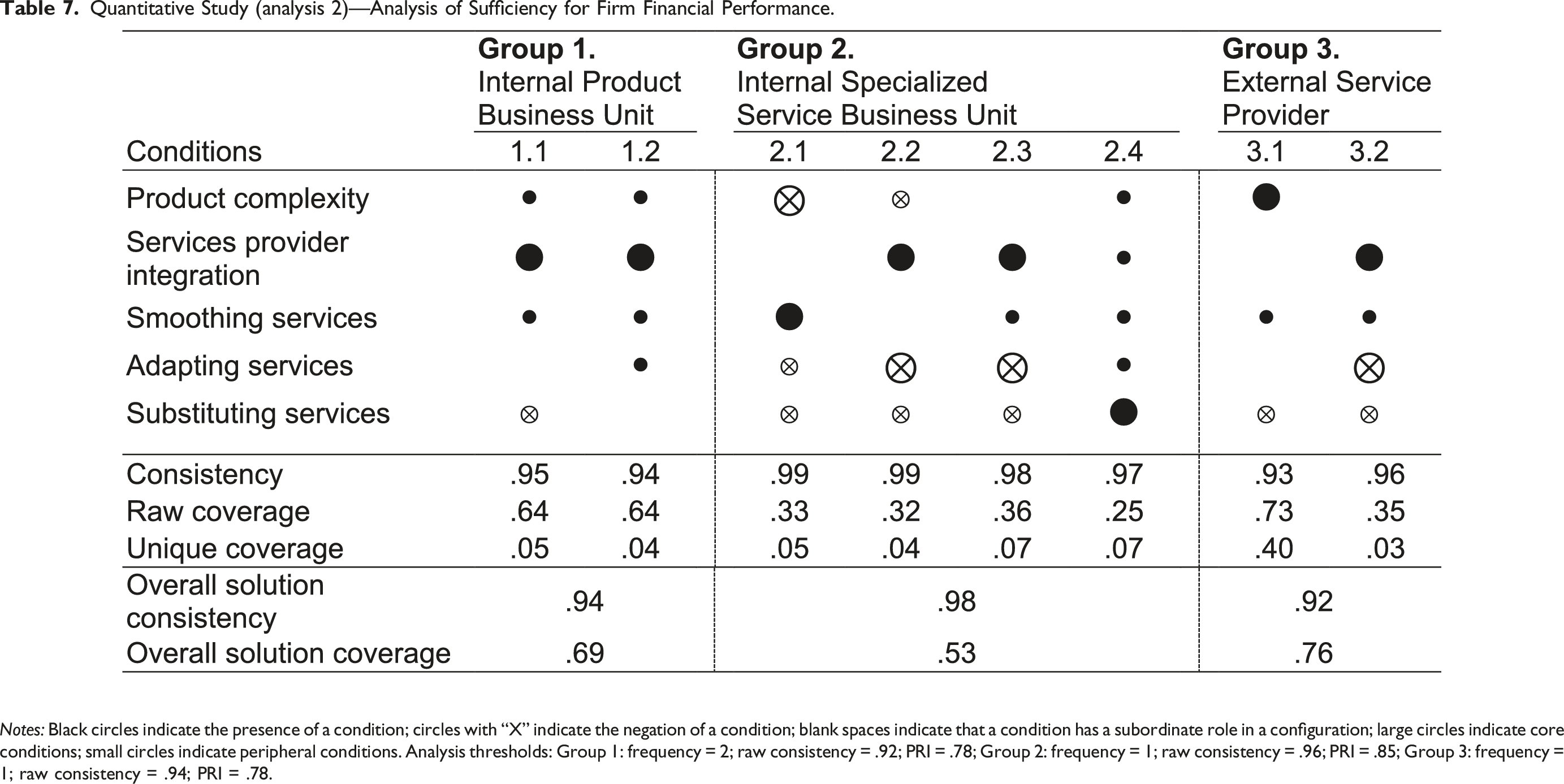

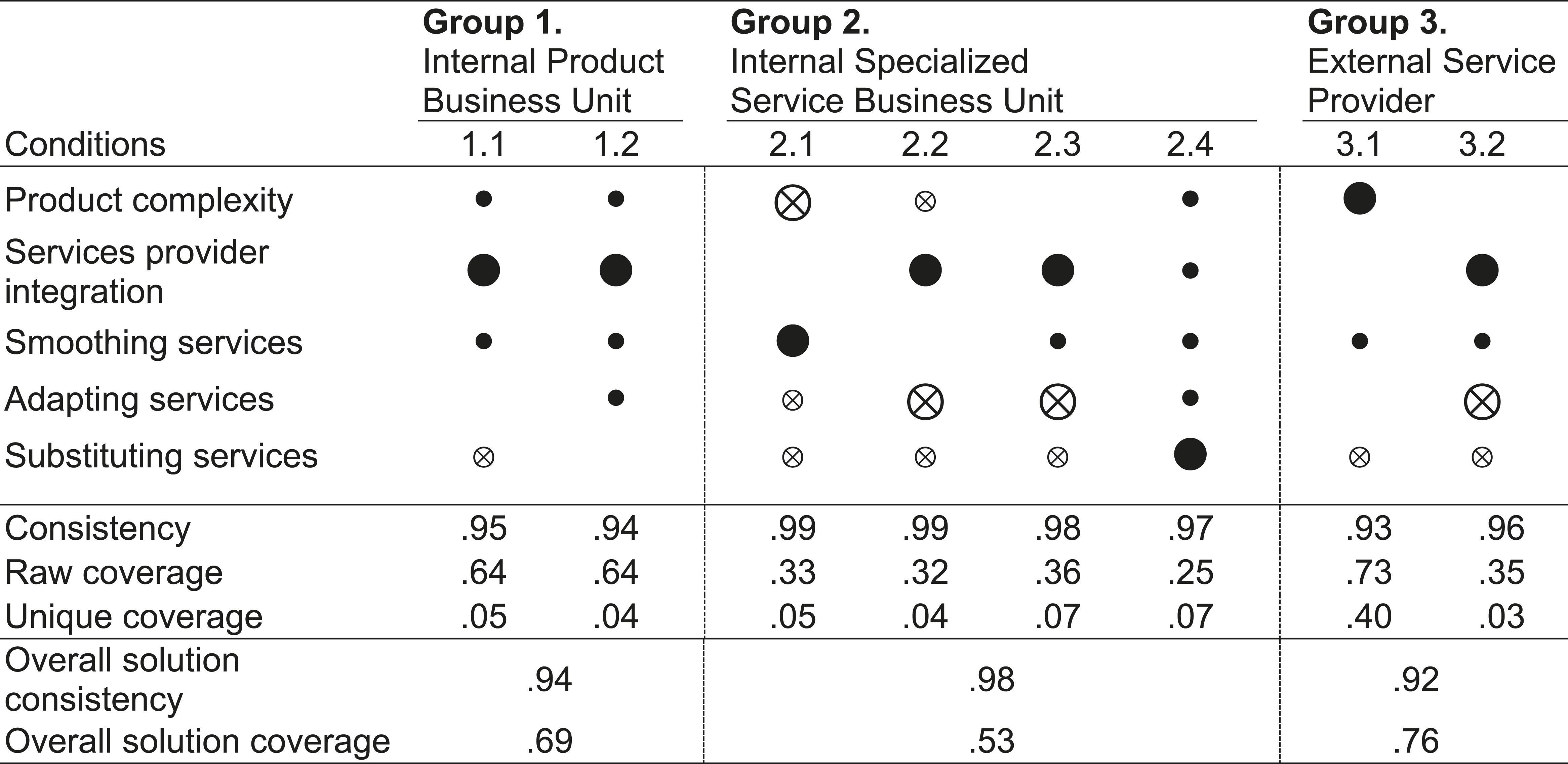

Quantitative Study (analysis 2)—Analysis of Sufficiency for Firm Financial Performance.

Notes: Black circles indicate the presence of a condition; circles with “X” indicate the negation of a condition; blank spaces indicate that a condition has a subordinate role in a configuration; large circles indicate core conditions; small circles indicate peripheral conditions. Analysis thresholds: Group 1: frequency = 2; raw consistency = .92; PRI = .78; Group 2: frequency = 1; raw consistency = .96; PRI = .85; Group 3: frequency = 1; raw consistency = .94; PRI = .78.

For manufacturers that pursue servitization internally through a specialized service business unit, Configuration 2.1 indicates that smoothing services represent a sufficient condition in the absence of product complexity and other servitized offerings to achieve high performance. Configurations 2.2 and 2.3, however, identify service provider integration as a sufficient condition in the absence of product complexity (2.2) and the absence of adapting and substituting services (2.2 and 2.3) to achieve high performance. These results further substantiate the findings from the qualitative pre-study, where manufacturers indicated that they often develop a new service business unit to offer smoothing services but encourage the collaboration (integration) between product development and service development teams to address customer needs. Finally, Configuration 2.4 reveals substituting services as a sufficient condition when the remaining conditions (i.e., product complexity, service provider integration, other servitized offerings) are present but have subordinate roles for achieving superior performance. This result corroborates findings from the qualitative pre-study indicating the need to develop a new specialized service business unit for more complex servitized offerings (vs. smoothing services), predicated on the integration between product development and service development teams as well as the mitigation of knowledge leakage risks.

For manufacturers that pursue servitization with an external service provider, Configurations 3.1 and 3.2 show that this organization architecture allows firms to achieve high performance when providing smoothing services only (i.e., in the absence of substituting services in 3.1 and in the absence of adapting and substituting services in 3.2). While Configuration 3.1 indicates product complexity is part of the sufficient configuration, Configuration 3.2 reveals service provider integration is an element of a sufficient configuration for high financial performance. These configurations are in line with the qualitative pre-study findings regarding the need to minimize operation costs for standardized services across diverse geographical areas using a certified external suppliers program.

The overall solution consistencies for all configurations are over .92, thus exceeding the commonly used threshold of .80 (Fiss 2011). In addition, the overall solution coverage scores of all configurations range between .53 and .76, indicating that the identified configurations cover the majority of the outcome set.

Discussion

Findings and Theoretical Contributions

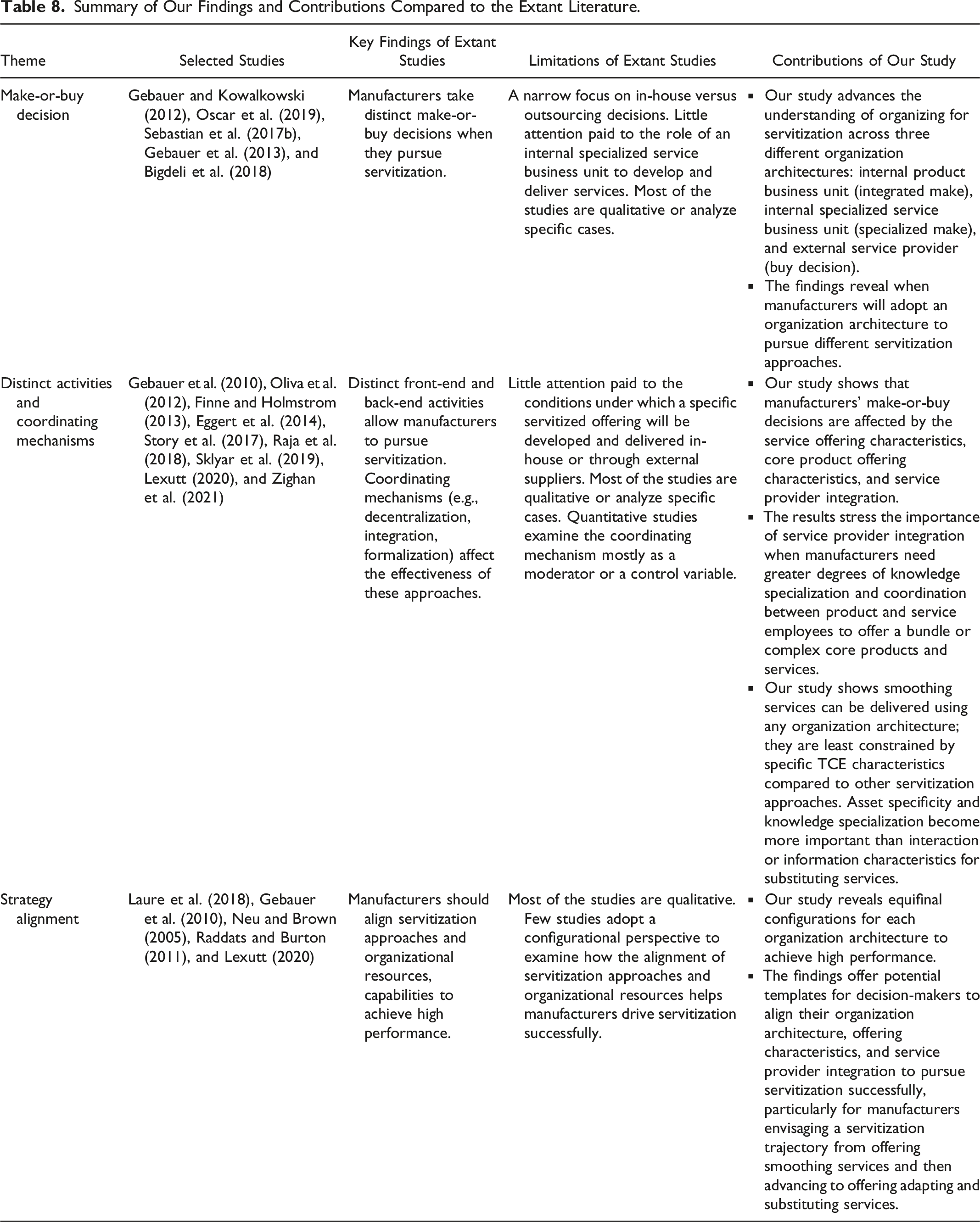

Summary of Our Findings and Contributions Compared to the Extant Literature.

First, we show that while organization architecture “matters” to explain servitization success, its impact is more complex (due to its interplay with other conditions) and more wide-ranging (due to manifold well-performing options) than indicated by the extant literature. Our findings advance existing studies that suggest servitization represents a make-or-buy decision, where manufacturers decide between providing servitized offerings in-house or via an external partner (e.g., Oscar et al. 2019; Gebauer et al. 2010; Kowalkowski et al. 2011; Ziaee Bigdeli et al. 2018). We investigate configurations of different aspects of servitization characteristics for achieving high financial performance in the context of manufacturers’ make-or-buy decisions. We thereby consider distinct make decisions (on top of buy decisions) through either an internal product business unit or an internal specialized service business unit. We show which organization architecture helps manufacturers with different degrees of core product complexity and service provider integration to achieve high financial performance when pursuing one or more specific types of servitized offerings. Therefore, the empirical findings from our qualitative and quantitative studies provide guidance for different organization architectures to successfully pursue distinct servitization approaches. We also detail the specific situations that require organizational integration of service provision with the core product business. We thus extend Oliva et al. (2012) by showing that an organization architecture integrating both service and product businesses can also contribute to financial performance as part of specific configurations.

In particular, we demonstrate that there is no single optimal way to organizing servitization, but there are equifinal pathways to achieve the same high-performance outcome. While all three identified organization architectures could be used to successfully pursue smoothing services (e.g., Configurations 1.1., 2.1, and 3.1), adapting and substituting services unleash their performance-enhancing effects only with specific organization architectures. These findings extend the extant body of work that suggests advanced services (vs. basic services) are likely to be offered in-house (vs. outsourced; Oscar et al. 2019). Internal specialized service business units turn out to be a flexible organization architecture as they can be used to successfully pursue all three servitization approaches, while employing an external service provider is less suited for delivering adapting and substituting services. Our findings show that smoothing and adapting services can be provided in different organization architectures and in different configurations of servitization approaches. However, for the most complex servitization approach (i.e., substituting services), such organizational variety does not exist. Rather, its performance-enhancing effect is realized in a configuration of factors that is specific to a specialized internal service business unit (Configuration 2.4). This finding has implications for manufacturers envisaging a servitization trajectory (i.e., usually starting with the provision of smoothing services and then advancing through adapting services to substituting services).

In this context, our findings also point to the issue that “more is not always better”: a firm that successfully uses smoothing services via an external service provider and has achieved an integration of that service provider with its product business unit can achieve financial success without offering adapting or substituting services (e.g., expressed by the negations in Configuration 3.2). Adding adapting and/or substitution services could increase interaction and coordination costs with the external service provider. The higher costs associated with more complex servitized offerings may render this organization architecture less efficient. Thus, when considering a development trajectory for servitization (Gebauer and Kowalkowski 2012), manufacturers that aim to advance servitized offerings over time should reassess their organization architecture.

Second, our results add to the servitization literature by providing insights into important organizational decisions that manufacturers make and how they translate into performance gains. We advance the extant studies that stress the importance of a configuration theoretical perspective to investigate antecedents of servitization success (e.g., Forkmann et al. 2017a; Kohtamäki et al. 2019). Our findings highlight the importance of the core product characteristics and service provider integration when organizing servitization for each of the three organization architectures. Manufacturers tend to opt for an integrated-make decision (i.e., product business unit) when offering highly sophisticated core products and services (e.g., adapting services). The production and delivery of such sophisticated product-service bundles require greater degrees of knowledge specialization and coordination between product design/delivery and service design/delivery teams. Therefore, neither forming a new specialized service business unit nor outsourcing are recommended options for adapting services when the degrees of product complexity and service provider integration are high. Manufacturers should consider the specialized make decision (i.e., a specialized service business unit) when offering substituting services beyond smoothing and adapting services for their highly complex products. This finding is in line with studies that suggest substituting services are likely to transform the manufacturer’s organization architecture (Cusumano et al. 2015; Sebastian et al. 2017b). The new specialized business unit should be responsible for developing fully managed product-service offerings that represent the most advanced form of servitization. The importance of such a new specialized service business unit becomes more important when fully managed product-service offerings are the main source of revenue for a manufacturer.

Third, we contribute to a better understanding of organizing servitization using a TCE lens. Organization architectures for servitization vary in terms of TCE mechanisms (i.e., interaction and coordination costs, information asymmetry, knowledge specialization, and asset specificity) and their alignment with different servitization approaches. For substituting services, asset specificity and knowledge specialization aspects (i.e., service quality-related issues) appear to outweigh interaction or information aspects (i.e., cost-related issues), as reflected by Configuration 2.4 for the specialized make decision. For adapting services, the TCE mechanisms are more ambivalent. High financial performance can be achieved with an organization architecture based on cost-related issues (Configuration 1.2) or service quality-related issues (Configuration 2.4). Smoothing services have the highest degree of freedom regarding the associated organization architecture. They can be offered in all three organization architectures and are least constrained by the TCE mechanisms. These findings suggest that TCE mechanisms may become more pronounced and restraining for achieving high performance when manufacturers move up on a servitization trajectory (i.e., when they shift from smoothing services to adapting and substituting services). TCE mechanisms do not constrain make-or-buy decision-making for simple servitization offerings, while for more complex servitization approaches (e.g., adapting services) the TCE mechanisms necessitate specific organization architectures to achieve superior financial performance. For the most complex servitization approach (e.g., substituting services), quality-related TCE mechanisms become pivotal and thus seemingly allow only one choice of organization architecture for financial performance.

Managerial Implications

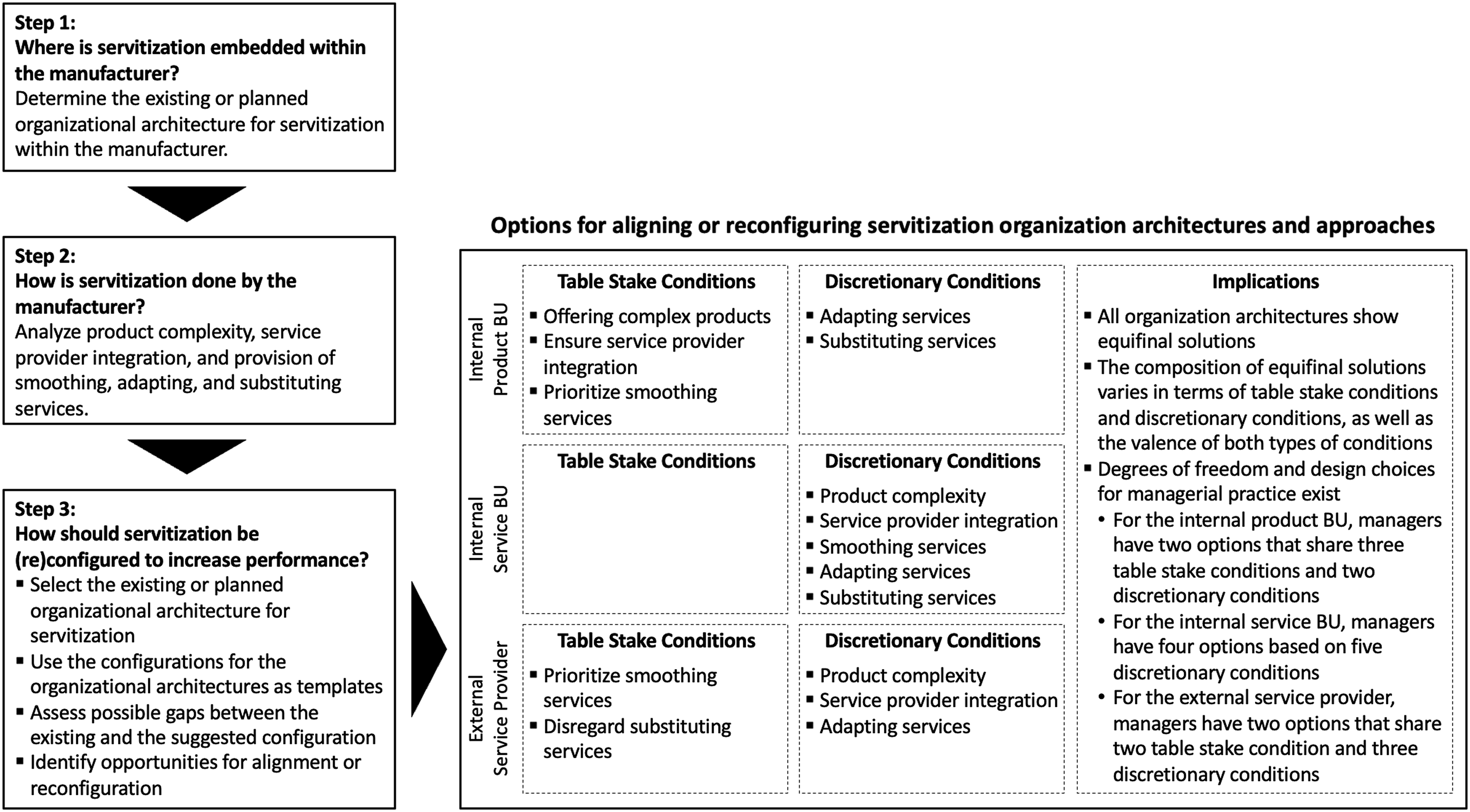

Servitization encompasses a transformation process for manufacturers that can come with major challenges. Our study provides guidance for addressing some of these challenges, in particular its organization architecture. More specifically, our findings suggest a three-step approach (see Figure 2) that can be used both for servitization audits and trajectory planning. Guidelines for organizing servitization.

A servitization audit starts with an analysis of a manufacturer’s already existing organization architecture for servitization in order to develop an understanding of the embedding of servitization within the organization (Step 1 in Figure 2). Next, manufacturers should assess their servitization approach, which includes an analysis of the types of services offered as well as an assessment of product complexity and service provider integration (Step 2). Once these analyses have been completed, a servitization audit can be done in terms of a gap analysis between the identified company characteristics (servitization approach, organization architecture, etc.) and the successful configurations identified in our study. If the company’s status quo does not match any of these configurations, an alignment need has been identified. The configurations identified in our analysis may consequently serve as templates for aligning servitization approaches and organization architectures in such a way that they unleash their performance-enhancing effects (Step 3 and alignment options). Thus, our findings allow managers to assess their current organization architecture within the firm and benchmark it against the configurations identified in our research.

As the findings of our studies show, alternative configurations of servitization approaches co-exist for the three investigated organization architectures, which vary in terms of table stake and discretionary conditions. Table stake conditions are those conditions that are present in (or absent from) all configurations for a specific organization architecture. Discretionary conditions are those conditions that are present in (or absent from) some, but not all configurations for an organization architecture. The distinction between table stake and discretionary conditions refers to manufacturers’ degrees of freedom in aligning their servitization approach with organization architectures (i.e., design options). The findings thus guide managers about what adaptations are necessary and/or possible. Comparing the firm’s current situation and different successful options via a gap analysis can show them what kind of change management activities they need to implement regarding organization architecture, product complexity, and service provider integration.

An extension of the servitization audit is servitization trajectory planning, which refers to the strategic development of a manufacturer’s servitized offering. Complex servitized offerings (based on adapting or substituting services) usually promise higher margins or better customer lock-in (Cusumano et al. 2015; Raja et al. 2018). Hence, manufacturers may want to move up on the servitization trajectory by offering more complex servitized offerings. Such strategic offering changes require planning in terms of the servitization approach and organization architecture. Our findings provide options for such trajectories as well as the possible need to change the organization architecture for servitization. In summary, the template may serve as the foundation for static assessments (in a servitization audit analysis) and dynamic planning (in a servitization trajectory analysis). Our findings provide guidance for defining, fine-tuning, and revising servitization strategies. They also guide managers to consider possible alternative performance-enhancing servitization configurations, and thus steer them away from mono-causal, single-lever solutions that only optimize one aspect of servitization in isolation.

Limitations and Avenues for Future Research

Due to design choices, this study is not without limitations. We acknowledge these and highlight potential avenues for future research. First, we adopted the conceptualization and classification of servitized offerings by Cusumano et al. (2015), which captures the development from offering complementary services in addition to core products to substituting their current product-centric orientation with a fully service-centered orientation. Future research could investigate the interplay between organization architectures and other classifications of servitization. For example, scholars may consider the classification of servitization based on service recipient (Antioco et al. 2008) or investigate how changing the degree of product-service ownership between the manufacturer and the customer across different servitization classifications can affect the manufacturer’s organization architecture.

Second, we investigated the configurations of three forms of organization architecture with other conditions that are sufficient to successfully pursue servitization. Future research may investigate differences between more fine-grained specialized service business units (e.g., separated business units for smoothing vs. adapting services) or external service providers (e.g., a certified external supplier program vs. an alliance with specialized third parties). Further, an understanding of the micro-foundations of how different organization architectures bring about servitization success and firm performance in the interplay with other servitization characteristics, thus unpacking and detailing the processes and components underlying this interplay, needs further study. This could include investigating more fine-grained analyses of the setup and routines associated with different organization architecture choices.

Third, our findings associating organization architectures with certain TCE mechanisms need further detailing. In particular, it is important to uncover the micro-foundations with regard to how certain mechanisms become more (or less) important in the context of different organization architectures and servitization approaches. For example, it is essential to understand that using different servitized offerings, including substituting ones, requires a specific organization architecture, namely a specialized service business unit. For this, in-depth qualitative research of the identified configurations would allow for a more fine-grained understanding of the modes of action resulting in financial performance.

Finally, future research could conduct longitudinal studies and investigate whether and how firms’ organization architectures and their servitization approaches change over time as part of a developmental trajectory. Such longitudinal studies might offer an understanding of tipping points, that is, critical events that require a manufacturer to adapt its organization architecture for effective service provision. In a similar vein, future studies could investigate how firms that run different servitization approaches simultaneously cope with situations of ambidexterity.

Supplemental Material

Supplemental Material - Organization Architecture Configurations for Successful Servitization

Supplemental Material for Organization Architecture Configurations for Successful Servitization by Nima Heirati, Alexander Leischnig, and Stephan C. Henneberg in Journal of Service Research

Supplemental Material

Supplemental Material - Organization Architecture Configurations for Successful Servitization

Supplemental Material for Organization Architecture Configurations for Successful Servitization by Nima Heirati, Alexander Leischnig, and Stephan C. Henneberg in Journal of Service Research

Footnotes

Acknowledgments

We thank the Editor, the Associate Editor, and the Reviewers of the Journal of Service Research for their thoughtful comments and guidance throughout the review process. We also thank Kati Kasper-Brauer, Marko Kohtamäki, and the participants of the 2019 Servitization Conference for their insightful feedback on previous versions of the paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.