Abstract

Digitalization has the potential to disrupt many service industries. This is already evident in industries offering standardized business-to-consumer services. Even knowledge-intensive business-to-business (B2B) services have increasingly blended digital technologies. Yet, little is known about how this type of service and its associated service work has changed, as tasks are being increasingly performed by robots or through artificial intelligence. This study fills this void by exploring how frontline workers in two highly knowledge-intensive B2B service industries—auditing and public relations/communication (PR/C) consulting—enact their service work in response to digitalization. Building on an interview study with 50 professionals and taking an interdisciplinary stance we find—contrary to the findings in previous research—that auditing firms embrace digitalization to a larger extent than PR/C firms. Further, we find that the frontline workers’ enactment of their service work is influenced by the fit between technological innovations and the type of intelligence their services are built on, as well as their occupational identities and the service climate within the firms. We conclude the article by developing propositions and a conceptual model, and outline how service firms can support their frontline workers’ infusion of digital technologies in their service work.

Introduction

New digital technologies related to automation, robots, and artificial intelligence (AI) enable innovations that could potentially transform and disrupt the service sector (Keating, McColl-Kennedy, and Solnet 2018). This has led scholars to describe the service industry to be “at an inflection point” (Wirtz et al. 2018, p. 908) and predict that many service industries will need to undergo fundamental changes to meet the potential threat of disruption (Ostrom et al. 2015; van Doorn et al. 2017). Thus far, extant service research has mainly focused on how new technologies affect standardized business-to-consumer (B2C) services, performed, for instance, by cashiers and travel agents, and how that in turn, is perceived by customers (Okhuysen et al. 2015; Wirtz et al. 2018). Today, new technological developments allow even knowledge-intensive business-to-business (B2B) services, which—due to their complexity and reliance on human expertise and interaction—were hitherto shielded from digitalization (Susskind and Susskind 2015; Wirtz et al. 2018) to become increasingly blended and augmented (Davenport and Kirby 2015; Keating et al. 2018). However, the infusion of digital technologies in this kind of service work “is an unchartered area of frontline research, where theory and research lag the technological advances that continue to be deployed in practice” (Singh et al. 2017 p. 8). Therefore, more empirical studies are needed.

A prime example of knowledge-intensive B2B services is professional services such as auditing and consulting services (von Nordenflycht 2010). The professional service industry has grown rapidly over the last few decades and is today an important driver of the knowledge economy (Okhuysen et al. 2015). Professional services are highly complex, tailored, and creative, leveraging the employees’ strong expertise, interpersonal skills, and close client interaction (Singh et al. 2017). The vast majority of the employees in professional service firms (PSFs) are frontline workers who interact frequently with clients (Singh et al. 2017). Further, the employees tend to belong to a specific occupation (e.g., lawyers in law firms) whose identity (Pratt et al. 2006) forms the basis for the PSF’s reputation as providing premium services (Bévort and Suddaby 2016). However, recent technological innovations such as IBM’s Watson and Ross can now perform complex analyses and tasks previously reserved for human experts in PSFs (Brynjolfsson and McAfee 2014). This has led to contradictory predictions on how digitalization may affect the professional service industry—one claiming that professional services are not likely to be automated in the coming decades since they require social skills and creativity (Wirtz et al. 2018), and the other that such services are on the verge of disruption, as new technologies will make them obsolete (Keating et al. 2018; Susskind and Susskind 2015). It has further been predicted that frontline workers in the professional service industry will increasingly use digital technologies to augment their services (Davenport and Kirby 2015), to work in human-robot or human-AI teams (Wirtz et al. 2018), and to change their client interfaces and interactions (Singh et al. 2017). Due to the novelty of the phenomenon, empirical studies on how the predictions unfold in practice are however still lacking (Smets et al. 2017). Yet exploring it is central, as it may yield important theoretical insights into how frontline workers providing knowledge-intensive B2B services enact contextual changes related to technological developments in their daily service work (Keating et al. 2018; Singh et al. 2017), and what new roles they take on (Bowen 2016). It is also important from a practical perspective, as PSFs act as knowledge brokers among organizations and advise them on how to address strategic issues such as digitalization (Reihlen and Werr 2012). This study, therefore, addresses the question: How do frontline workers in PSFs enact their service work in times of digitalization and potential disruption?

To answer the research question, we build on an explorative interview study with 50 professionals in four auditing and six public relation/communication (PR/C) consulting firms in Sweden. Inspired by Subramony and Pugh (2015), we take a multilevel and interdisciplinary stance and draw on an analytical framework that combines insights from the literature on service intelligences (Huang and Rust 2018), service climate (Bowen and Schneider 2014; Schneider and Bowen 2019), and service work at the frontlines (Singh et al. 2017), with insights from the literature on occupational identity (Nelson and Irwin 2014; Pratt et al. 2006).

In contrast to predictions made in previous research, we find that auditing firms embrace digitalization to a larger extent than PR/C firms. Based on our findings, we contribute to the theorizing on how frontline workers in knowledge-intensive B2B service firms enact their service work in times of digitalization and potential disruption (Keating et al. 2018; Singh et al. 2017; Wirtz et al. 2018). We do so by showing first how the technology-service intelligence fit (Huang and Rust 2018) influences the PSF’s markets, competition, and client demands and creates a high/low sense of urgency among the frontline workers. Second, we show how frontline workers’ responses to the high/low sense of urgency are shaped by their occupational identity, providing them with a perceived “room to manoeuver” (Nelson and Irwin 2014; Pratt et al. 2006), and how the service climate in the PSFs (dis-)incentivizes them to adopt digital technologies in their work (Bowen and Schneider 2014; Schneider and Bowen 2019). Third, we find that the frontline workers can respond to digitalization through taking on two new service roles (Bowen 2016), creating blended services (Davenport and Kirby 2015), and developing new forms of client interfaces and interactions (Singh et al. 2017). Lastly, we summarize our findings into propositions and a conceptual model, thereby providing an answer to the first question of how macro-level changes such as digitalization are enacted by individual frontline workers in their service work (Singh et al. 2017; Subramony and Pugh 2015).

The remainder of the article is organized as follows: We provide a brief introduction to the literature on professional services, followed by a section discussing our analytical framework. We then present our methodology and empirical findings. In the concluding section, we outline the contributions of our findings, develop propositions and a conceptual model, and discuss the theoretical and managerial implications of our study.

Professional Services

The key characteristic for PSFs is that a majority of their employees are frontline workers who provide tailored, creative, and expertise-based advisory services and interact frequently with clients (Singh et al. 2017). Doing so demands high levels of social and analytical skills, flexibility, and out-of-the-box thinking (Wirtz et al. 2018). As these capabilities are difficult to imitate, they are often regarded as a key source of sustainable competitive advantage in PSFs (von Nordenflycht, 2010; Wirtz and Lovelock, 2016). These capabilities are built through careful recruitment from top schools and extensive internal training (Wirtz and Jerger 2016).

As PSFs build their reputation and relevance on providing “state-of-the-art” expertise, they need to be abreast with recent developments in management, technology, legislations, and industries (Reihlen and Werr 2012). While the need to stay relevant spurs PSFs to engage in service innovation (Barrett and Hinings 2015), they are conservative regarding their internal organization including processes, competencies, and business models (Anand, Gardner, and Morris 2007). This can be explained by the fact that PSFs act in a reputation- and relationship-based market, which makes it important for them not to deviate too much from what has made them successful in the past, because that might threaten their brand name and client relations (Reihlen and Werr 2012). Further, PSFs tend to be “mono-occupational,” implying that an overwhelming majority of the employees belong to a certain occupation, such as lawyers in law firms (von Nordenflycht 2010). In these firms, the occupational identity is strong and forms the foundation for the recruitment and promotion of the frontline workers as well as for the clients’ willingness to avail of their services (Bévort and Suddaby 2016). Due to their reliance on human expertise and interpersonal skills, and the lack of suitable technologies, professional service firms have traditionally been slow to incorporate new technologies in their work (von Nordenflycht 2010). However, as mentioned above, the recent advancements in digital technologies mean that professional services are no longer shielded from digitalization (Susskind and Susskind 2015). Rather, PSFs, as well as their frontline workers, will need to consider how to respond to remain competitive and relevant to their clients (Wirtz et al. 2018).

Digitalization and Frontline Professional Service Work

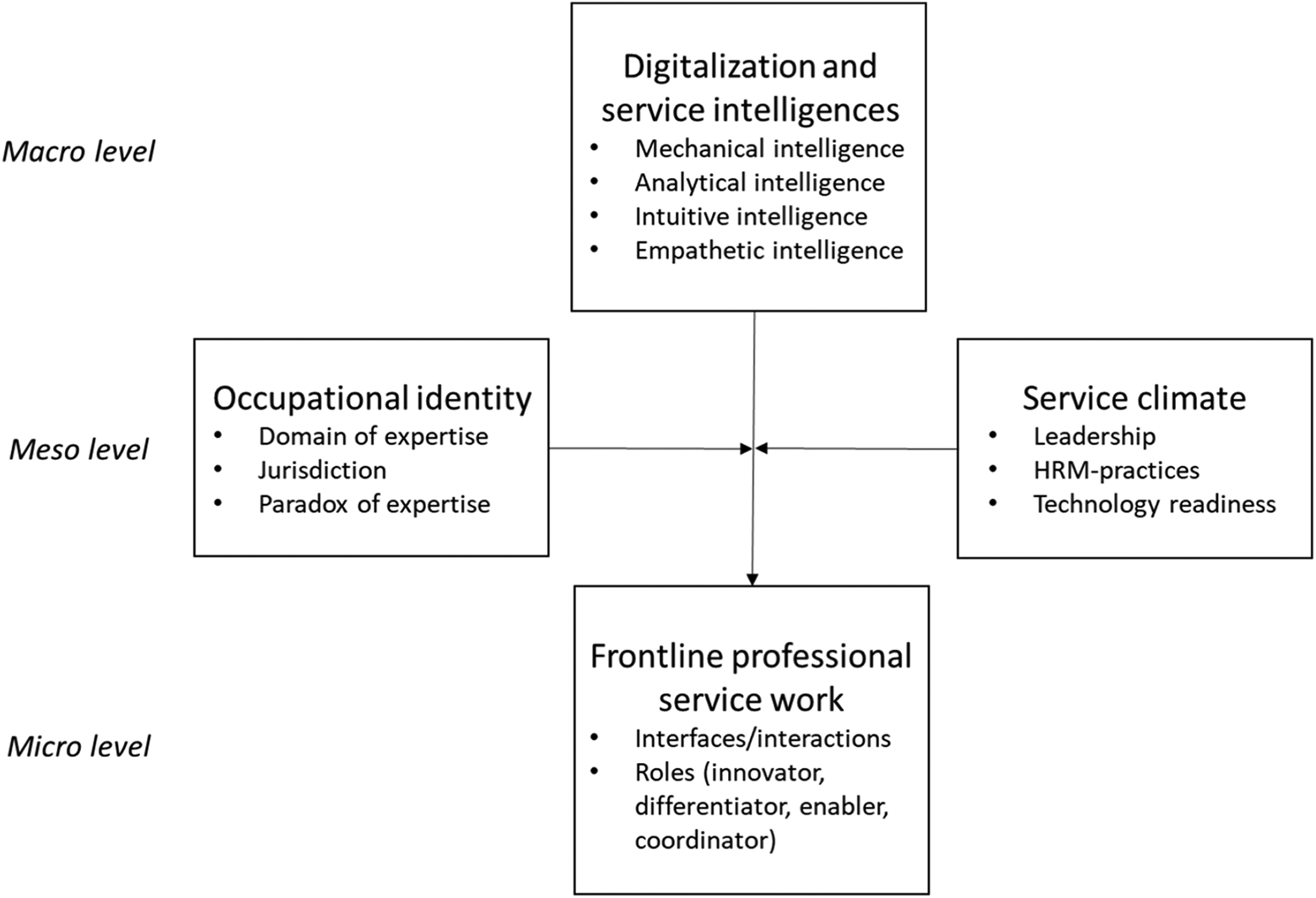

This study focuses on how frontline workers enact their service work in times of digitalization and potential disruption. 1 However, to fully grasp how and why frontline workers use digital technologies in their service work, we need to also understand the contextual setting they are embedded in Christensen, Wang, and Van Beaver (2013). Inspired by Subramony and Pugh (2015), we take a multilevel, interdisciplinary approach and combine the literature on service intelligence, occupational identity, service climate, and frontline service work into an analytical framework (see Figure 1).

The analytical framework illustrating how digitalization—a macro level phenomenon—is enacted by frontline workers at the micro level (illustrated by the vertical arrow), and how that in turn is shaped by meso-level phenomena, that is, the frontline workers’ occupational identities and service climates (illustrated by the horizontal arrows).

In brief, the analytical framework illustrates that the enactment of digitalization in frontline service work depends on what type of service intelligence (Huang and Rust 2018) the services build on, as that defines to what extent the new technologies are applicable to the services. Second, it also depends on the frontline workers’ occupational identity (Pratt et al. 2006), which is particularly salient in PSFs (Bévort and Suddaby 2016), and the service climate in their organizations (Schneider and Bowen 2019), as they define what is the legitimate use of digital technologies in frontline service work. Lastly, the literature on service work (Bowen 2016; Singh et al., 2017) shows the new roles and actions that the frontline workers can take on when enacting digitalization in their service work. Each part of the analytical framework will be discussed in detail below.

Digitalization and Service Intelligence

Digitalization refers to the use of digital technologies that are built on information and machine power and intelligent connected machines, potentially enhancing customer value and impacting competition in various industries (Brynjolfsson and McAfee 2014). It has been argued that digitalization may “dramatically change service industries” as such services are increasingly being performed by robots and through AI (Wirtz et al. 2018, p. 908). Although the interest in digitalization has grown in the service literature, it has tended to be dominated by a “humanistic paradigm” and focused on how humans, such as managers, customers, and policy makers, interact and cocreate value (Keating et al. 2018). Less attention has been given to the role of new technology in service work, even though “it is clear that recent technological developments, particularly in the areas of AI and autonomous systems, will have the potential to significantly alter the nature of service and the role of humans in service exchange” (Keating et al. 2018, p. 767). Thus, we need more knowledge on how digital technologies influence what we see as services, and how service workers reshape their work to meet potential disruption and exploit the new technologies (Ostrom et al. 2015).

A reflection of this is found in the article by Huang and Rust (2018), who describe the jobs as comprising back-end tasks and front-end tasks and argue that in services, job replacement will occur at task level rather than job level. The tasks, in turn, form activities that belong to an occupation (Huang and Rust 2018). By incorporating new service technologies, frontline workers can augment their work (Davenport and Kirby 2015), provide more customized, blended services, and increase their productivity (Huang and Rust 2018). The pace at which these developments take place is suggested to depend on what type of intelligence the services are built on. Huang and Rust (2018) define four types of intelligence and list them in the order of difficulty for technology to master: mechanical, analytical, intuitive, and empathetic intelligence. Mechanical intelligence relates to standardized tasks (e.g., routine tasks in a call center) that can be easily automated. Analytical intelligence relates to systematic and predictable analytical tasks that can be performed by AI, information processing, and machine learning (e.g., robot-advisory services). Intuitive intelligence relates to holistic thinking and the processing of complex information (e.g., using AI in medical diagnostics). Lastly, empathetic intelligence relates to understanding and responding appropriately to people’s emotions and needs. This is particularly important in professional services, which largely rely on social skills and creativity (Wirtz et al. 2018).

It is argued that in near future, service robots will be increasingly used to deliver services, building on the first three intelligences (Huang and Rust 2018), and that social skills will become increasingly important (Singh et al. 2017). Consequently, services that are traditionally built on service relationships might transition into more anonymous service encounters between humans and service robots (Gutek, Groth, and Cherry 2002). However, services built on empathetic intelligence will be more difficult for AI and robots to perform (Huang and Rust 2018; Wirtz et al. 2018). It is predicted that in these services, humans are likely to take care of and deliver emotional and relational tasks, while being supported by service robots doing analytical tasks (Wirtz et al. 2018). However, empirical studies on how the suggested transitioning of services from being human-based to technology-based is enacted by frontline workers, particularly in services that combine different types of intelligences, are however still lacking (Keating et al. 2018; Smets et al. 2017).

Occupational Identity

While the literature on service intelligence helps us understand to what extent service tasks can be performed by digital technologies, it says less about the willingness of frontline workers to include new technologies in their service work. It is the frontline workers’ occupational identity that guides how they make sense of situations (Bévort and Suddaby 2016), new technology (Nelson and Irwin 2014), and their actions (Pratt et al. 2006). The occupational identity builds on the occupational members’ perceptions of “who we are” and “what we do” (Pratt et al. 2006). In practice, this means that by performing certain tasks and practices, occupations construct their identities and jurisdictions (Anteby, Chan, and DiBenigno 2016), which are based on the members’ expertise in a specific area of work and provide boundaries for what constitutes legitimate practices and professional conduct (Nelson and Irwin 2014). Occupational identities are often defined in relation to other occupations, by distinguishing from them or engaging in negotiations over which domains of expertise, roles, and tasks the members should perform (Nelson and Irwin 2014). When new areas of competence and work emerge, as in the case of new technologies, they can be perceived as “vacant jurisdictions” and as open for competition among occupations wanting to claim ownership over them (Okhuysen et al. 2015; Verbaan and Cox 2014).

Recent research has highlighted that occupations are becoming increasingly dependent on technology to perform their work (Anteby et al. 2016). Thus far, a large part of this literature has shown how occupations—while still performing the same service—manage to change the meaning of the service, and thereby, also the occupational members’ perceptions of “who we are” 2 (Nelson and Irwin 2014). Less is however known about how changes in the service work—“what we do”—can reform occupational identities (Nelson and Irwin 2014). Yet, this is important to understand, as the adoption of new technologies may not only change how tasks are performed but also entire occupations, 3 so that “the people doing the work, the arrangements around the work, the technology used in the performance of the work, and even the purpose of the work may change” (Okhuysen et al. 2015, p. 7).

It has further been argued that occupational members’ ideas of “who we are” and “what we do” influence their perceptions of what new technologies might “be” and “do” (Nelson and Irwin 2014). Members of an occupation can, due to their deep expertise, be unwilling to accept new technologies, particularly when these technologies do not support the way of performing tasks or give the kind of outcomes as the members’ expertise prescribes. In these cases, the occupational members may become subject to the paradox of expertise, and risk missing opportunities they recognize, because “their mastery of the existing approach encourages them to devalue solutions that do not match this approach” (Nelson and Irwin 2014, p. 919). The paradox of expertise is likely to arise when the task the technology performs is closely linked to the occupation’s identity, when the technology performs the task in a way that differs from the occupation members’ ideas of how it should be done, and when the occupational identity is strong and stable (Nelson and Irwin 2014).

Building on the above, we suggest that the frontline workers’ occupational identities influence how they enact their service work in times of digitalization and potential disruption (Nelson and Irwin 2014). Previous enactment research has however suggested that for new knowledge and technologies to be taken for granted and to become part of occupational members’ identities, thus bridging what they “do” with who they “are” (Nelson and Irwin 2014; Pratt et al. 2006), they need to first become embedded in formal organizational practices, roles, and behaviors (Bévort and Suddaby 2016). Therefore, for knowledge on how the organizational context influences the frontline workers enactment of digitalization, in the following section, we review the service climate literature (Bowen and Schneider 2014).

Service Climate

Thus far, a large part of extant service research has focused on either how macro-level phenomena influence aggregate customer outcomes or how microlevel phenomena influence individual customer outcomes (for an exquisite review of the field, see Subramony and Pugh 2015). Very few studies have explored how organizational phenomena at the meso level influence individual service workers and their customers at the micro level (Subramony and Pugh 2015). Yet, understanding the organizational context is important, as it is likely to impact how frontline workers adopt new technologies and change their service work accordingly (Schneider and Bowen 2019). The service climate is defined as the “employee perceptions of the practices, procedures, and behaviors that get rewarded, supported, and expected with regard to customer service and customer service quality” (Schneider, White, and Paul 1998, p. 151). A strong and service-focused climate has been shown to result in higher service quality and has been suggested to build interrelated practices such as leadership behaviors and human resource management (HRM), the knowledge and skills of employees, fair treatment, and the rewards and recognitions they receive (Bowen and Schneider 2014; Schneider and Bowen 2019). We suggest that the service climate also impacts the frontline workers’ “technology readiness,” that is, their propensity to adopt, embrace, and use new technologies in their service work (van Doorn et al. 2017).

Service Work at the Frontlines

Lastly, we direct our attention to the microlevel and the literature on organizational frontlines and frontline workers. Organizational frontline research can be defined as “the study of interactions and interfaces at the point of contact between an organization and its customers that promote, facilitate, or enable value creation and exchange” (Singh et al. 2017, p. 4). In the present study, we use the framework for organizational frontline inquiry developed by Singh et al. (2017) as a backdrop. In brief, the framework describes how frontline workers in service firms—depending on their services’ reliance on lean to rich technological interfaces and simple to complex knowledge-based problem-solving interactions—will use digital technologies differently (for an illustration of the framework, see Singh et al. 2017, p. 7, or Online Appendix A). We suggest that professional services can be regarded as highly complex, knowledge-based, and problem-solving services that build on rich, mainly human-to-human, client interfaces. This would, according to the framework, call for the use of digital technologies such as co-robots and human-AI teams (Singh et al. 2017; Wirtz et al. 2018).

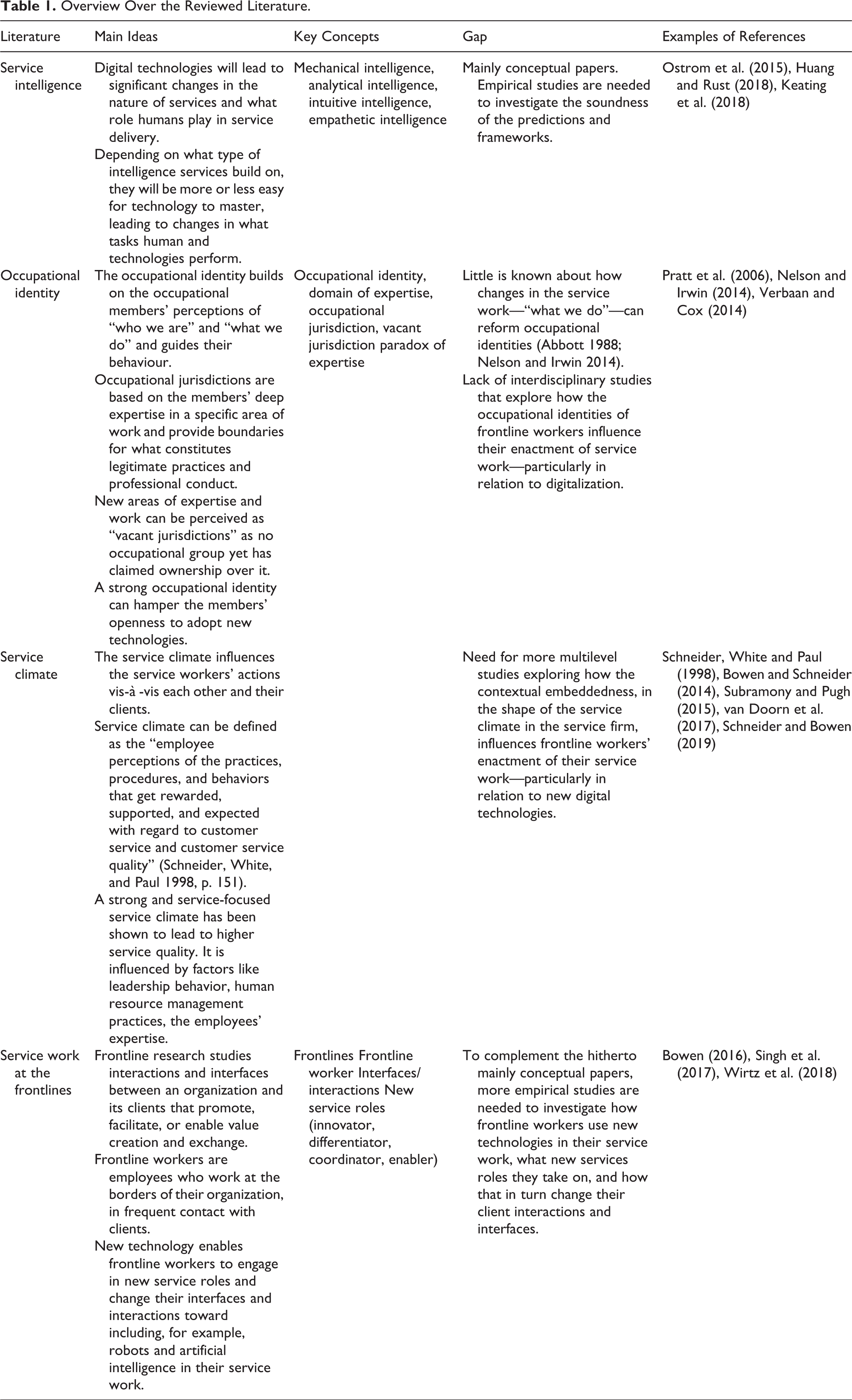

Extant studies in this field have argued that the nature of service work will change as organizations increasingly shift from manual work to knowledge-based work to remain competitive (Okhuysen et al. 2015). It has been suggested that digitalization will enable frontline workers to take on four new roles: innovators, differentiators, enablers, and coordinators (Bowen 2016). Innovators work in close interaction with clients, understand their needs, and innovate new ways of meeting them, for instance, with the help of technology. Differentiators increase service differentiation and avoid service commodification by adding a “human touch,” transforming a commercial transaction into a relationship. Enablers help other employees and clients adopt and interact with technology in service delivery. Coordinators manage the increasing interdependencies among frontline workers, back-office employees, and clients (Bowen 2016). As long as the service workers’ behaviors are aligned with the expectations clients have on their service roles, role congruency emerges, which in turn affects the clients’ evaluations positively (Wirtz et al. 2018). Whether the four roles described by Bowen (2016) will be salient even in knowledge-intensive B2B service work, such as professional services, is however not studied. For an overview of the reviewed literature, please see Table 1 below.

Overview Over the Reviewed Literature.

Method

Research Design

Based on the complexity and novelty of the phenomenon, we have used a qualitative, explorative methodology, well-suited for theory development (Gioia, Corley, and Hamilton 2013). The study has been performed in Sweden, which is a country characterized by high levels of digital maturity and innovation (see https://www.globalinnovationindex.org/analysis-indicator, retrieved September 28, 2018). Thus, it provides a rich context for exploring how frontline workers enact their service work in times of digitalization and potential disruption. As empirical examples, we have used two types of professional services: auditing and PR/C consulting. Auditing forms an illustrative example of “classic professions” as it is highly regulated and protected through, for instance, accreditations and strong professional norms (von Nordenflycht 2010). On the other hand, PR/C consulting forms an illustrative example of “neo-professions” as it lacks a well-defined domain of expertise, has fuzzy boundaries, and very low entry barriers (von Nordenflycht 2010).

Data Collection

The present study builds on interviews with 50 partners and digital experts in four auditing firms and six PR/C firms in Sweden. Given that the partners and digital experts were expected to have a strong influence on service strategies and how digital technologies were used in their firms, exploring their views was deemed as particularly interesting. The studied PSFs were selected based on their position in the Swedish market. All studied firms had existed for more than 10 years, had a strong brand, and were among the largest firms in their industry. In general, the auditing firms were large and had an international presence, while the PR/C firms were smaller and more local. Thus, the number of interviews per firm varied with the size of the firm, so that more interviews were performed in the larger auditing firms than in the PR/C firms. Further, in three of the studied PR/C firms (PR/C 4, PR/C 5, and PR/C 6) only partners were interviewed, as there were no appointed digital experts in these firms. The interviews were performed in 2018, were semistructured, and lasted approximately 45–90 minutes. All interviews were recorded and transcribed (an overview of the studied firms and the interviewees is found in Online Appendix B and a copy of the interview guide in Online Appendix C).

Data Analysis

Following Pratt et al. (2006) and Gioia et al. (2013), the data analysis was performed in an iterative fashion and comprised three phases: First, we meticulously read all the transcripts to get an overview of the data. We then coded the data into inductively retrieved, informant-centric codes. As this resulted in a large number of codes, we organized them into first-order codes, in which codes relating to each other were classified together (Pratt et al. 2006). Second, we looked at the first-order codes, and inspired by Gioia et al. (2013, p. 20), asked “what is going on here, theoretically?” To answer this question, we used an abductive approach and compared our codes with our analytical framework (Gioia et al. 2013). By moving back-and-forth between theory and data, we could identify research-centric, theoretical categories (Gioia et al. 2013; Pratt et al. 2006). Lastly, we investigated whether we could distill our theoretical categories even further into aggregate, theoretical dimensions (Gioia et al. 2013; Pratt et al. 2006). This led us to identify four dimensions: close/weak technology-service intelligence fit, well-defined/fluid occupational identity, a service climate for digitalization, and frontline professional service work. The analysis resulted in the development of data structures (for the generic data structure, see Online Appendix D, for data structures for each dimension and industry, see Appendices E–L).

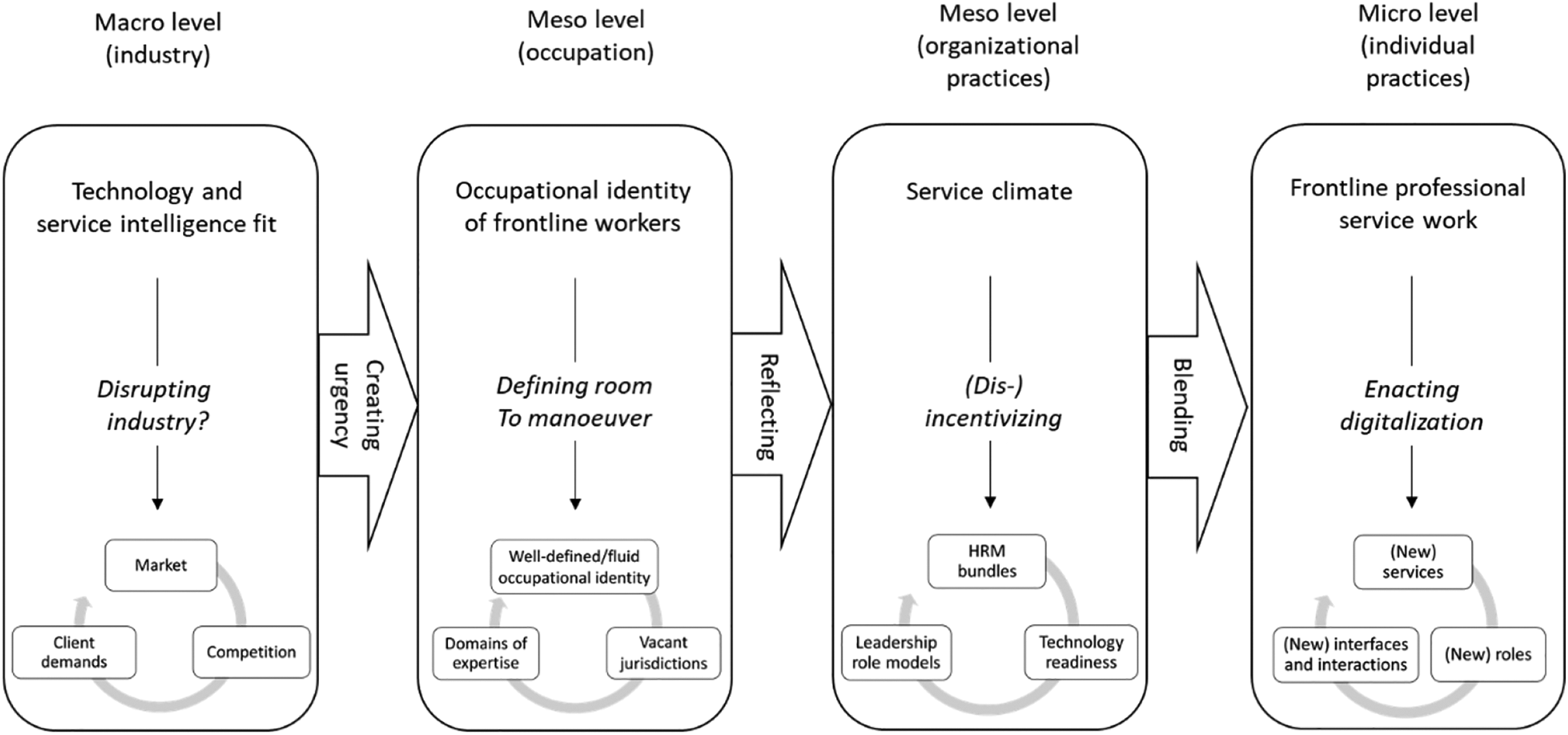

In the analysis, we were careful to take a stance of “well-intended ignorance” (Gehman et al. 2018, p. 291) and keep an open mind to the possibility that different and unexpected patterns could exist in the data. 4 However, we found very strong industry-specific patterns, meaning that the interviewees in auditing firms responded in very similar manner, while the interviewees in the PR/C firms responded in a different but internally coherent manner. We also found variations in how eager individuals were to learn about digital technologies, although the auditors witnessed a shared understanding in their firms of how important it was to develop new digital skills and services to respond to disruption. In the PR/C firms, however, digital expertise and services were not regarded as strategically important. Together, the results enabled us to develop research propositions and a conceptual model (see Figure 2).

Conceptual model of how the frontline workers’ enactment of their service work in times of digitalization and potential disruption is contextually embedded and shaped by the technology-service intelligence fit, occupational identity, and service climate.

Findings

In the following, we will present the results from the two analyses. For each dimension, we will first discuss the findings from the auditing firms and then the findings from the PR/C firms.

Digitalization as a (non)disruptive Force

The first dimension captures how the service workers’ views on digitalization as (non)disruptive are influenced by what type of intelligence (Huang and Rust 2018) their services are built on. We find that the views are derived from how digital technologies change the market for their services, the competitive landscape, and the clients’ demands (for data structures with illustrative quotes, see Appendices E and F).

Digitalization changes the market for traditional auditing services

All interviewed auditors described their industry as being on the verge of disruption, and that they had to digitalize their business to avoid becoming obsolete: “We cannot choose whether we want to digitalize or not—if we choose to be a traditional auditing firm that does not digitalize, we will be out of business” (Partner, Audit 4). The auditors also felt that as the digital technologies developed so fast, they had to respond very quickly: “In three years, lots of things will have changed, but in five years there will be dramatic changes” (Partner, Audit 3). The reason for this was that technological development has enabled automation of many analytical auditing tasks, through either robots or AI. This has reduced the need for human labor in the analysis process and created a need for the auditors to redefine their services. The auditors also feared that technological advancements would make the classic auditing role minuscule. For instance, the governments in the Nordic countries were jointly developing an initiative—the Nordic Smart Government initiative 5 —which aims at connecting organizations via robot process automation to oversee agencies such as the tax authorities. This would enable the authorities to retrieve financial information directly from the organizations, thus reducing the need for auditors to produce financial reports and act as middlemen.

Tech-based entrants increase the competition in the auditing industry

The technological developments also led to stronger competition from start-ups and tech-based firms offering automated auditing services. Although the auditors felt somewhat protected by the regulations, they still feared that large tech-firms would enter the auditing market and use their data and state-of-the-art technologies to outcompete the auditing firms. What will we do when big companies like Google and Apple start to move into new industries like ours? We have been discussing it for a while, and I guess it will only take 1-3 years before it happens in our local market. (Partner, Audit 3)

Clients demand digital auditing services

As a consequence of technological developments and new competition, the clients were changing their demands from classic to digital auditing services, and turned to the auditors for advice on how to digitalize their accounting functions. The auditors predicted this development to become even stronger in the future when the “digital natives” take control of the client firms. The auditors were also concerned that the changing client demands would pose a threat to the current business model in the auditing firms as well as to the regrowth of the auditing occupation. Traditionally, junior staff members would spend their first few years in the auditing firm performing data collection and data analysis. As these types of tasks were increasingly getting automated, the senior auditors were worried that the clients would not be interested in hiring junior auditors, and this, in turn, would lead to a reduced profitability in the auditing firms. Normally we have a lot of juniors in the firm, that’s where we earn money. But if we can automate all the juniors’ work, will the clients be interested in hiring juniors with little experience for more complex tasks? I doubt it. Then what will we do? Should we be just a bunch of senior partners? Then we will be extinct when all of us retire. (Partner, Audit 2)

Digitalization expands the market for traditional PR/C services

Turning to the PR/C industry, the PR/C consultants did not view digitalization as disruptive. Rather, they described their market as growing because digitalization provided them with new communication channels for their services: “There are more communication channels today, I mean, when I first started as a consultant in 1990, there were no mobile phones, no Internet. I had a fax machine and an old phone” (Partner, PR/C 5). The PR/C consultants also found their clients to regard communication as increasingly important. Although the client firms were expanding their communication functions, they still did not have all the skills they needed in-house. Therefore, they turned to PR/C firms for advice and extra resources.

Tech-based entrants do not increase the competition in the PR/C industry

Recently, many tech-based start-ups had entered the PR/C market. The PR/C consultants did not view them as a threat because the new entrants offered “unattractive” automated and standardized services. The PR/C consultants, on the other hand, offered tailored, strategic services that built on social skills and their “deep expertise and knowledge about the society, the international context, and developments” (Partner, PR/C 1). However, the PR/C consultants were worried about a new group of competitors: strategy consultancies. These had recently acquired creative agencies and were now seeking to include PR/C services into their service portfolios. Given that the strategy consultants approached the same kind of clients (top managers in large organizations) as the PR/C consultants and positioned themselves as offering premium services, this competition was perceived as more acute. In response, the PR/C consultants engaged in frequent communication with their clients and explained how they were different from other types of agencies including strategy consultants.

Clients demand classic PR/C services

The PR/C consultants described their clients as demanding mainly classic PR/C services, and as “lagging behind” in terms of digital skills. The clients therefore asked the PR/C consultants for “basic services,” such as helping them to “develop an app or get media training in social media channels” (Partner PR/C 4). This was said to be particularly salient in public organizations, which formed an important client sector for the PR/C firms but had limited budgets and experience of using digital technologies in their communication. Further, as public and private organizations increasingly relied on their websites for communicating with their clients, they turned to PR/C firms for help in crafting web-based communications. Taken together, this created a stable demand for PR/C services.

Occupational Identities as Defining the Room to Maneuver Digitalization

The second dimension captures how the occupational identity of the auditors and PR/C consultants influences their perceived room to maneuver, that is, what kind of responses to digitalization they can legitimately engage in without compromising the occupational ideas of “who they are” and “what they do.” We find that the room to manoeuver is shaped by three interrelated aspects: How clear the occupational identity is, what domain of expertise it relies on, and the boundaries of its jurisdiction. Surprisingly, we find a perceived larger room to manoeuver among the auditors than the PR/C consultants (for data structures with illustrative quotes, see Appendices G and H).

Auditing—A Conservative and Regulated Industry in Transition

The auditors described that due to the strong professional norms and accreditations in the industry, it was very clear to auditors, policy makers, clients, and candidates what kind of training an auditor had and what kind of tasks she or he could engage in. However, due to the perceived threat of disruption, the auditors felt a strong need to change. To do so, they were in close dialogue with the professional associations about the future of the auditing and sought support from them for their new ideas: “We try to work with the regulators, educate them and connect with them so that they understand what is happening in the industry and keep up with the developments, because if they would fall behind, we could end up in a very tricky situation” (Partner, Audit 1).

Expanding the auditors’ domain of expertise

To respond to disruption and take advantage of digitalization, an important issue in the auditing firms was to recruit and develop digital skills: Our most important focus right now, particularly in Sweden but also in the Nordics, is to recruit new [digital] competence to our firm. (Partner, Audit 4)

Entering new digital jurisdictions

The recruitment of new types of candidates to develop new tech-based auditing services enabled the auditors to expand their traditional domain of expertise to also include digital expertise. The appropriation of new digital technologies also enabled the auditors to perform auditing tasks in new ways, providing their clients “with auditing analyses, but the way they are performed look different from what they used to, since we can now pick up data from the [clients’] systems several times a year instead of doing random tests at the end of the year” (Partner, Audit 1). By partnering with new entrants in the industry, the auditing firms could also get access to new areas of tech-based auditing services: “Of course, we are in dialogue with the tech giants, but many of the smaller startups are extremely niched, which means that if they can collaborate with a firm like us, they get another sales channel, and we both have a win-win situation: we can solve client problems with their product and [they can access] our network and business expertise” (Partner Audit 1). Thus, by recruiting new candidates with digital expertise and partnering with new start-ups, the auditing firms could move into a similar but new market for digital-based auditing services.

PR/C consulting—an elusive industry

In contrast to the auditors, the PR/C consultants described their role as vague and difficult to explain, both to their clients and to themselves. This was due to the “secrecy” of the industry, and the consultants’ ambition to “work behind the scenes” and let their clients take credit for their work. However, it also contributed in making the consultants’ efforts “invisible” to the larger audience. The consulting industry was further described as undergoing changes related to mergers between PR/C firms, new competition from strategy consultants, and new entrants offering automated media services. This made it difficult for clients and PR/C firms to define “what competencies a PR/C consultant could be expected to have” (Partner, PR/C 1). Thus, the PR/C consultants had to spend considerable efforts on communicating to existing and prospective clients what services they offered and what kind of skills and expertise they possessed.

Defining the PR/C consultants’ domain of expertise

The PR/C consultants described the ability to build strong client relations and to have a deep understanding of their political landscapes and communication needs, as core PR/C skills. However, to keep up pace with digitalization and be trustworthy vis-à-vis the clients, they perceived it as necessary to have some digital skills in-house as a “hygiene factor.” Therefore, the PR/C firms had recently started appointing junior consultants with a “normal background” (traditionally, a degree from a business school) and an extra interest in digital technologies as “digital experts,” who were asked to take on the role of internal advisors to the other consultants in the firm and to “…look at AI and bots and develop new solutions for our clients that we will try to push out now, text message communication tools, apps, etc.” (Digital expert, PR/C 3).

The digital experts were also asked to create task forces comprising digital experts from different offices to develop new digital services. However, the number of digital experts in the firms was very small and lacked power. This was explained by the other consultants’ view on digital services as being less prestigious and profitable than classic PR/C services: “Because what happens now is that when we try to do digital stuff, we tend to move down the value chain” (Digital expert, PR/C 1). It was also reflected in the digital experts’ view of their role as temporary, and as a means to learn more about digital technologies: “After all, I am an economist, it’s not as if being a digital expert is my core competence or part of my career, I see it rather as a way of gaining deeper insights into the issues I am interested in” (Digital expert, PR/C 1). Interestingly, while the digital experts were eager to share their expertise with their colleagues, this was not encouraged by the senior partners. Rather, they regarded digital expertise as “not for everyone” in the PR/C firms, but something only a few consultants needed to possess: “One of our digital experts took the initiative to give all junior consultants a basic course in digital tools, but she was criticized for it because [the partners thought that] not everyone should know about or be able to work with that” (Digital expert, PR/C 1).

Demarcating the jurisdiction

The view of digital expertise being nonstrategic was reflected in the PR/C firms in several ways: First, innovative projects that did not align with the top management’s ideas of what the firm “was like” and “what it did” were not easy to accept. This restricted the consultants’ room to experiment with new types of digital tools or interact with new types of clients and actors, like influencers in social media. The PR/C consultants also made clear demarcations between their own and adjacent skills and services, such as advertising. This was explained as being partly due to historical boundaries between the industries and partly due to the culture in the PR/C firms, wherein the adjacent skills were regarded as less valuable and prestigious—a view which sometimes backfired: “We don’t respect our [acquired creative] agencies’ work, although it is becoming increasingly important, and then we get surprised when [name of advertising agency] wins a project we have bid for because they say the same thing as we do but in a much nicer and prettier way—we really have no self-awareness at all” (Digital expert, PR/C 1).

A Service Climate for Digitalization

The third dimension captures the views among the interviewees on how their organizations support and reward digital expertise. The views were derived from the service climate, which in turn builds on three interrelated aspects: the leaders as role models, the HRM practices, and the technology readiness in the firms. We find the service climate to incentivize digital expertise in the auditing firms but not in the PR/C firms (for data structures with illustrative quotes, see Appendices I and J).

Auditing partners act as role models in learning digital skills

To increase the level of digital expertise in their firms, the partners arranged internal seminars for demonstrating new digital tools, get trained in programming, and sharing experiences of using digital technologies in client projects. The seminars were open for everyone, regardless of seniority: “Last week, we had a seminar on coding in Python with 3–4 partners and 20 auditors—it was so great because everyone got involved” (Partner 2). The partners also made a point of attending the seminars, thereby signaling to their colleagues that it was important. At first, some of the partners had been reluctant to attend the seminars, as they felt uncomfortable to let their colleagues know that they were “beginners.” Over time, this changed, and by being open about their lack of experience in digital technologies, the partners made it easier for others in the organization to attend the training: “There is no fear of exposing oneself as a beginner anymore, and that is really important” (Partner, Audit 2). Consequently, attending the seminars was widely encouraged and had become “a natural part of work” (Partner, Audit 2).

New HRM practices reward digital expertise

The recruitment of new groups of candidates with digital expertise has also led the auditing firms to develop their recruitment practices: “We are not used to recruit this kind of profiles, so we had to update our talent management mindset a little and think about how we could reach out to this particular group of people” (Partner, Audit 1). As the auditing firms were not well-known among engineers and data scientists, they had to create new employer branding strategies. Undertaking these changes was described as important, as the number of recruits with technical background was expected to grow “We recruit about 60 students each year, and the proportion of engineering students is growing, so that will make our recruitment process look a bit different” (Partner, Audit 1). This development was also reflected in the performance management systems, which recently had been changed to also capture digital skills. “It has become like a competition in my team, to have the highest levels [of digital expertise] in as many areas as possible and that is very good, because it is part of the performance measurement systems and all of a sudden even our business people can discuss AI and analytics with our clients in a trustworthy fashion (Partner, Audit 1).” By making these skills visible and rewarding, the firms made it attractive for auditors across all levels to acquire them.

High levels of technology readiness

The auditors described their organizations as open to adopt new technologies: “It is really not easy to change in an industry like ours that is so regulated, but I think everyone is very aware that [digital disruption] is happening and the partners are quite positive to the changes” (Partner, Audit 1). Apart from acting as role models and implementing new HRM practices, the partners also supported local initiatives aiming to develop digital expertise, for example, by forming cross-sectional groups around a certain topic, and encouraged them to disseminate their knowledge internally through reports, seminars, visiting other offices, and acting as internal experts. For instance, in Audit 1, a small team started to explore how data visualization and analytics could be used in auditing and developed into a Nordic innovation team. Another example was found in Audit 2, where a partner set up an informal team to respond to new client demands for auditing services related to cryptocurrencies. The team eventually developed into a formal hub of expertise serving the Nordic countries.

PR/C partners act as role models and embrace traditional skills

In the PR/C firms, the situation was different. Through their actions, the partners signaled to the consultants that their main focus should be on classic PR/C services and skills and that it was legitimate not to be interested in learning about digital tools or social media: “Well, I don’t know anything about it, but there is this thing called advertising on social media” (Partner, PR/C 1). This attitude created a “knowledge gap” between the partners and the digital experts, which in turn made it difficult for the partners—who were responsible for client relations and for selling new projects—to know what kind of digital services they could offer or how to price them: “It happens that partners sell in [digitally oriented] assignments that they don’t really understand and then we [digital experts] need to fix it somehow” (Digital expert, PR/C 1).

Established HRM practices do not capture digital skills

In the PR/C firms, the performance measurement systems were attuned to classic PR/C services and did not capture the work performed by the digital experts, thus restricting their possibilities for promotion: “We need to have 80% billable hours—that is what determines your bonuses and career development—but I spend 80% of my time pitching, so I underperform constantly” (Digital expert, PR/C 1). In contrast to the auditing firms, the PR/C firms did not offer training in digital tools or technologies to their consultants. Instead, it was up to each consultant to decide what to learn and also to find time for it. This was described not only as difficult, due to the “high tempo” and demand for “billable hours,” but also as hampering the development of digital expertise among the consultants: “I think our philosophy is that all learning should take place at work, and while that is a good philosophy I think that for this type of brand new stuff, we also need to put aside some time for training that is more than just a one-hour webinar with someone from Silicon Valley who tells you about the features of a new digital tool” (Digital expert, PR/C 1).

Varying levels of technology readiness

Due to the “knowledge gap” and lack of training and rewards for digital expertise, the technology readiness varied between consultants and units in the PR/C firms. While the PR/C consultants, particularly the digital experts, wanted to raise the general level of digital expertise in their firms, it was not supported by the partners: “PR/C 6 started as an annual report agency, although report writing has become more digitalized, [top management] has decided to keep the annual report group isolated and not develop it digitally” (Partner, PR/C 6).

Digitalization in Frontline Professional Service Work

The last dimension captures how frontline service workers use digital technologies in their service work. This encompasses what type of services they provide, what roles they take on, and what kind of interfaces and interactions with the clients they use. We also find that in the auditing firms, the frontline workers used new services, roles, and interfaces/interactions in their service work. In the PR/C firms, the frontline workers relied mainly on classic PR/C services and interfaces/interactions but did take on a new service role (for data structures with illustrative quotes, see Appendices K and L).

Developing new digital auditing services

To meet the client demands and perceived threat of disruption, the auditors sought to incorporate digital technology in their service offerings. As a first step, they unbundled their “packages of services” into separate services and tasks to analyze tasks for which they could use digital technologies to augment or replace human work. In doing so, the auditors sought to keep the strategic tasks in-house, “giving away” while less important or profitable tasks to tech-based firms offering automated auditing. By focusing on the strategic services, the auditors hoped to maintain a strong brand and a position “high up in the value chain.” They also believed that automating analytical tasks would give them more time to engage in advanced value-creating tasks even at junior levels. Thus far, digital technologies had been implemented to perform traditional, standardized auditing tasks, such as using robots to process large quantities of client data and automated text analysis models building on machine learning to clean and analyze data in the clients’ accounting systems. This was said to lead to higher levels of efficiency and accuracy. The auditors therefore expected it to become more common in the future: “Well, the classic auditors who just sit around, look at numbers, compare, and check for mistakes, etc. it’s just a matter of time before they disappear—perhaps not totally, we probably need a human to hold accountable—but just apply some machine learning and it will find lots of mistakes in the accounting data that a normal auditor would never detect” (Partner Audit 1).

The auditors further explored how new technologies could be used to extend their service offerings into new, adjacent areas, such as using blockchain-based tracking models which client firms could use to collect data and improve risk assessments. The use of digital technologies further enabled the auditors to change the temporal focus of their services—from providing retrospective to predictive and prescriptive analyses: “I gave a client presentation last week on predictive analysis, in which one component was to use AI to predict which of the client’s contracts would yield losses” (Partner, Audit 2). The auditors described the development of new, technology-based services as central because they expected their classic business model to become less relevant: “In 5–10 years, [the classic business model] will only represent 50–60% of our total earnings globally and the other things we are supposed to earn money on are not invented yet” (Partner, Audit 1).

While infusing digital technologies in the auditing services was described as “imperative,” it also created anxiety regarding the pricing models. Traditionally, the auditing firms had used a price per hour or a fixed price model for their services. As tasks now could be increasingly automated, the auditors were worried that the clients would be less willing to pay for them. This was described as a key strategic question in the auditing firms, as changes in the pricing models shift toward “subscriptions,” “managed services,” or “risk and reward” which could have an impact on both the positioning of the firms—moving from premium to commoditized services—and their profitability: “So, we might have to use a different pricing model, but if we choose the wrong one, we might become bankrupt” (Digital expert, Audit 2)” Further, the auditors were experimenting with taking on new types of projects, which were related to digital transformation of the clients’ accounting functions and aimed at providing them with both new digital tools and new organizational processes and routines. These projects were described not only as increasingly important for the auditing firms but also as challenging, as they required their internal project teams to be cross-functional and include “auditors, tech-people, and consultants.”

New service roles in auditing firms—coordinators and translators

As being an expert in financial systems was no longer enough to succeed as an auditor, the partners tried to enhance the digital expertise among their junior auditors. This had resulted in the creation of a new role in the auditing firms: here referred to as translators. The role was developed in newly created training programs, which aimed to give junior auditors with a business degree a basic digital skillset: “We bring up juniors who will become really skilled auditors, and who will be the interface towards our group (of technological experts): they will understand the technological foundations of the analytic tools used in auditing, and they will also be able to see how we can deliver tailor-made services to our clients” (Partner, Audit 1). The translators were expected to act as “bilingual” auditors who could translate between different groups of experts in the auditing firms and help find technological solutions to business problems.

The auditing firms also sought to take on a new coordinating role. Instead of focusing on a single client, the auditors would now orchestrate several actors in the clients’ service ecosystem to deliver more multifaceted services. As an example, one of the studied auditing firms had helped its client develop a new technological solution that would enable the client to better monitor its supply chain, improve accuracy in the invoicing and accounting systems, and increase internal efficiency in the finance function. In doing so, the auditing firm had set up collaborations with start-ups, incumbent tech-firms, insurance agencies, supply chain specialists, and experts in organizational change, and managed the client’s relations with them as well as the entire project. This type of role was expected to become more important in the future: “We will have even more collaborations with other types of actors, collaborations that are more adjusted to the specific situation rather than long-term partnerships, the market will demand that we can collaborate with many different types of actors” (Digital expert, Audit 2).

New human-to-robot and robot-to-robot interfaces and interactions

Although the auditors relied on close human-to-human client relations for gaining new assignments, they were increasingly complementing these with human-to-robot and even robot-to-robot interfaces and interactions: “We have a pilot project where our robot speaks to the client’s robot, and when we ask for more information the client robot answers. It is automation on both ends” (Partner, Audit 1). Which interface and interaction were used, depended on the types of tasks that the services were built on. The initiatives to use robot-to-robot interactions were supported by both clients and policy makers.

Providing traditional PR/C services with a digital twist

In contrast to the auditors, the PR/C consultants relied mainly on their classic services and regarded digital elements as an add-on to them: “I think that digital tools are pretty much seen as an add-on that can be used to spice up the offers that we make” (Digital expert, PR/C 1). For instance, when developing a campaign or providing media training—two examples of classic PR/C services—the PR/C consultants could add a 3D-printed element in the campaign and include training on how to respond to critique on Facebook. Thereby, they could rely on their classic skills while positioning themselves as “someone who knows digital channels, digital business intelligence, digital media, etc.” (Partner, PR/C 5). Although the consultants were adding digital technologies to their services, they did not use digital tools such as automation in their internal work processes. This was explained partly by the consultants’ feelings that it “would not be feasible” and partly that it would only be useful for a very small part of their tasks.

A new service role in PR/C firms—coordinator

The PR/C consultants also developed a new coordinating role that enabled them to maintain their positioning in the market as offering premium services to their clients, claiming that: “Coordinating large complex values is where we can add value” (Partner, PR/C 1). In this role, they took advantage of the fact that the number of agencies in the PR/C market had grown due to digitalization. Building on their existing client networks and experiences, the PR/C consultants helped their clients coordinate large communication projects and ensured that all the media agencies and technology-based start-ups that the client had hired for the project collaborated and completed the project on time.

Relying on human-to-human interfaces and interactions

Due to the strong reliance on traditional services and skills, the PR/C firms did not engage in developing new, technology-based client interfaces or interactions. Instead, they focused on creating strong personal human-to-human relationships with their clients.

Summary of the Findings

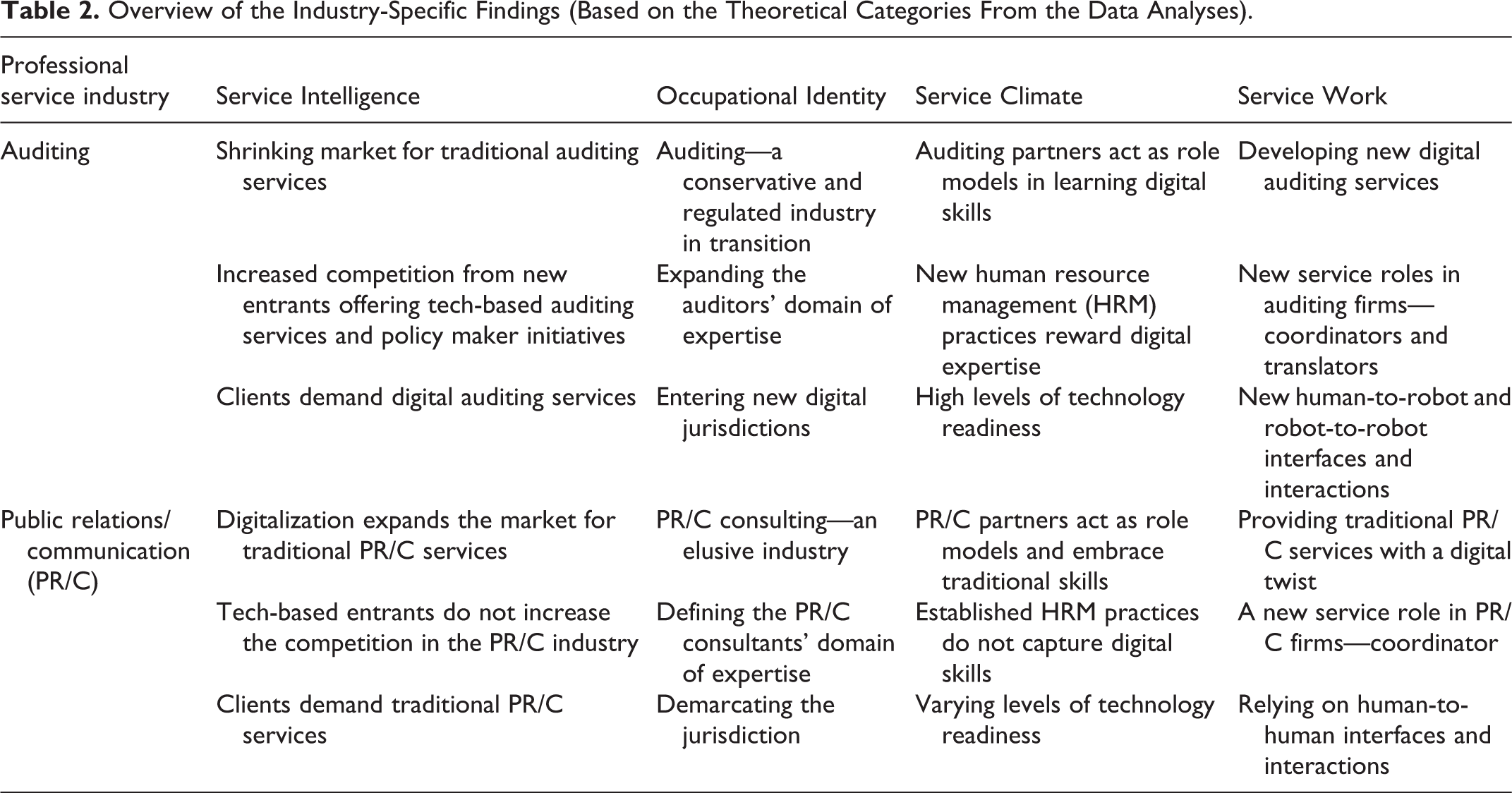

Summing up, while we find the dimensions of service intelligence, occupational identity, and service climate shaping how frontline workers’ enact their service work, we also find industry-specific differences. These are summarized in Table 2.

Overview of the Industry-Specific Findings (Based on the Theoretical Categories From the Data Analyses).

Concluding Discussion

This article set out to explore how frontline workers in PSFs enact their service work in times of digitalization and potential disruption (Ostrom et al. 2015; Singh et al. 2017; Subramony and Pugh 2015). Based on our findings, we make several, interrelated contributions that together help us answer our research question.

Fit Between Service Intelligence and Technology

First, we contribute by way of new insights into how changes at the macro level, that is, digitalization, is enacted in frontline professional service work (Subramony and Pugh 2015). Previous research has made contradictory predictions on how this may unfold—one claiming that knowledge-intensive services that require social skills and creativity are not likely to be automated in the coming decades (Wirtz et al. 2018), the other that such services, of which professional services is a prime example, is currently on the verge of disruption (Susskind and Susskind 2015). Our findings contribute to resolving the contradiction by providing empirical evidence for how the fit

6

between technological developments and the type of intelligence the services are built on (Huang and Rust 2018) influence how digitalization is enacted by frontline service workers in PSFs. As illustrated by the auditing firms, a close fit creates an image of digitalization as disruptive and a strong sense of urgency among their frontline workers. In contrast, and as illustrated in the PR/C firms, a weak fit creates an image of digitalization as nondisruptive, and thus a low sense of urgency among their frontline workers. We also extend the conceptual framework by Huang and Rust (2018) by identifying three interrelated channels through which the technology-service intelligence fit shapes the sense of urgency related to digitalization in PSFs: (i) the market for the PSFs’ traditional services, (ii) the competitive landscape, and (iii) the clients’ demands. We argue that a close technology-service intelligence fit may lead to a shrinking market for the PSFs’ traditional services,

7

as the new technologies enable new services to be developed, which may outperform traditional services and make them obsolete. Further, a close fit allows new entrants, such as start-ups and tech-giants, to enter the market and provide tech-based services. If successful, the entrants may change the competitive landscape in the industry and potentially disrupt it. Lastly, clients may respond to technological developments and new service offerings and entrants by changing their demands and asking for new types of services and service deliveries. Therefore, the three channels reinforce each other and create a momentum of change in the industry. Thus, we provide new insights into how the fit between technological developments and the service intelligence on which a firm’s services are built on (Huang and Rust 2018) influences to what extent the firm perceives digitalization as disruptive (Susskind and Susskind 2015; Wirtz et al. 2018) and propose:

We also extend Huang and Rust’s (2018) framework by identifying two responses to the technology-service intelligence fit: First, firms offering services composed of various types of service intelligence, such as auditing firms, respond by unbundling their services into tasks, applying digital technologies on tasks requiring analytical intelligence, and reserving tasks building on intuitive and empathetic intelligence for humans to perform. Second, firms offering services that build mostly on empathetic intelligence, such as PR/C firms, respond by continuing to rely on human service delivery, and are less likely to provide blended services. Together, these findings nuance the claims that professional services are being disrupted (Susskind and Susskind 2015) and more blended (Davenport and Kirby 2015), by providing an explanation for why this development unfolds differently in different professional service industries (Christensen et al. 2013). They also nuance the statement that this type of service will not be automated in the next decades by showing how they—depending on their technology-service intelligence fit—will gradually become more automated and blended (Wirtz et al. 2018). Thus, we provide an answer to how knowledge-intensive B2B services such as professional services transition into blended or technology-based services (Keating et al. 2018; Smets et al. 2017) and propose:

Occupational Identity and the Perceived Room to Manoeuver

Second, while technology-service intelligence fit helps explain why the auditors felt a stronger threat of disruption than the PR/C consultants, they give less insight into how they enacted their service work. To understand this, we need to explore how they perceived their room to manoeuver, that is, what new types of service work they could legitimately engage in (Nelson and Irwin 2014; Pratt et al. 2006; Verbaan and Cox 2014).

Previous research has argued that occupations with a clear identity, low infusion of new types of workers, and few identity crises are highly susceptible to the paradox of expertise and thus less open to adopt new technologies than neo-professions (Nelson and Irwin 2014). Yet, while auditing fulfills these criteria, the studied auditors were indeed experimenting with new types of services, roles, recruitments, and competencies, whereas the PR/C firms were less inclined to do so. A possible explanation to this finding is that the high perceived threat of disruption trumped the occupational identity and caused the auditing firms to engage in innovation to remain competitive. However, extant literature has repeatedly shown how incumbent firms in similar positions fail to reform and adapt to new technological and societal changes (Okhuysen et al. 2015). So why were the auditors, despite belonging to a well-defined occupation, more apt to experiment (von Nordenflycht 2010)? We propose, in contrast to the perception in previous literature (Nelson and Irwin 2014), that members of occupations with well-defined occupational identities and jurisdictions might paradoxically have more room to manoeuver as it is clear to both the occupational members—their clients and their stakeholders—“who they are” and “what they do” (Pratt et al. 2006). Thus, they can afford to experiment with new ways of performing tasks (e.g., using robots rather than manual work to analyze financial data), as long as the service role they perform is congruent (Wirtz et al. 2018) with more overarching occupational ideas on what type of service work their members “do” (e.g., providing advisory services related to auditing). Members of occupations lacking well-defined occupational identities, on the other hand, cannot rely on shared assumptions of “who they are” or “what they do” (Pratt et al. 2006: Nelson and Irwin 2014). Instead, they need to constantly reinforce their roles vis-à-vis their clients, stakeholders, competitors, and themselves to maintain their occupational identity. Thus, experimenting with new services and pushing the jurisdictional boundaries is a risky endeavor, as it may adversely impact their clients’ perceptions about them and their reputation (Reihlen and Werr 2012).

Further, we find that by appropriating vacant jurisdictions like cryptocurrencies and predictive and prescriptive analyses, it is possible for occupations to stretch the boundaries of their domain of expertise and associate themselves with digitalization (Verbaan and Cox 2014). Our findings illustrate how the auditors, by performing new types of service work, could enable a transition from providers of “classic” auditing services and experts in accounting to providers of tech-based auditing services and digital experts. In contrast, the PR/C consultants sought to maintain their traditional occupational identity and domain of expertise by contrasting themselves from new agencies offering digital services, claiming that digital expertise was not for everyone, and dissociating themselves from the roles as digital experts. As the use of digital technologies was not aligned with consultants’ occupational norms on how the service work should be performed, for instance, with a high degree of human touch, or what the outcomes should be (Nelson and Irwin 2014), it was valued as less important and useful. This indicates that, in contrast to claims in previous literature, the fluidity of occupational identity is not necessarily an enabler but may well be a liability when it comes to technology adoption and service innovation (Nelson and Irwin 2014). Thus, by taking an interdisciplinary stance (Subramony and Pugh 2015), we are able to unveil how frontline service workers’ occupational identity might facilitate or impede the adoption of digital technologies in their service work. In doing so, we also add to the scant but growing literature on how changes in what occupational members “do” influence their perceptions of “who they are” (Nelson and Irwin 2014).

Service Climate as (dis-)incentivizing the Enactment of Digitalization in Frontline Service Work

Third, we contribute new insights into the literature on service climate (Subramony and Pugh 2015). We add to Bowen and Schneider’s (2014, p. 6) service climate framework, which focuses on the internal aspects of the service firm and its customers, by showing how external macro-level phenomena such as digitalization, and meso-level phenomena such as the employees’ occupational identities, contribute to shaping the service climate. We also find that the service climate (dis-)incentivizes frontline service workers to enact digitalization in their service work, depending on the leadership role models (Bowen and Schneider 2014; Schneider and Bowen 2019), the HRM practices (Subramony and Pugh 2015), and the technology readiness (van Doorn et al. 2017) in the organization.

Previous research has indicated that leaders can build a strong service climate by being role models, setting high standards for service, and allocating resources to develop it (Bowen and Schneider 2014). Our findings support and extend this by showing how it plays out in the setting of digitalization. In brief, we find that in the auditing firms, the partners and senior managers acted as role models by providing resources for internal training, attending seminars on digital technologies, and supporting initiatives directed at developing digital expertise. In the PR/C firms, the partners and senior managers acted as role models for traditional PR/C service work and did not provide resources for or engage in training related to digitalization.

Further, our study responds to the calls for more multilevel studies exploring the link between HRM practices and service worker customer-relevant skills and expertise (Subramony and Pugh 2015). We find that bundles of HRM practices can contribute to create a service climate that promotes and rewards the development of digital expertise among the frontline service workers and new digital services (Schneider and Bowen 2019). In the auditing firms, new talent management practices, internal trainings, and performance measures were developed to stimulate the employees to learn about digital technologies, and to develop new digitally informed work practices and services. By allowing the employees to post on the intranet the digital skills that they possessed, the auditing firms increased transparency in the organization and enabled the human resource functions to track and reward those skills. In the PR/C firms, on the other hand, digital skills were not captured or rewarded by the HRM systems. This created a feeling of being unfairly treated among the digital experts and stifled the development of a service climate in which digital expertise was promoted. Thus, we extend extant research on the roles of HRM practices and perceived fairness for service climate (Bowen and Schneider 2014) by showing how they can (dis-) incentivize the embracement of new technology.

We also contribute to the literature on service climate (Bowen and Schneider 2014; Schneider and Bowen 2019) by highlighting technology readiness (van Doorn et al. 2017) as its important aspect, particularly in relation to the enactment of digitalization in frontline professional service work. Based on our findings, we suggest that a close technology-service intelligence fit stimulates an increased technology readiness in service firms, which in turn allows their employees to embrace new technologies in their service work. For instance, while the auditing firms were populated by service workers with training in business or law, the view of digitalization as potentially disrupting their industry led them to incorporate new digital technologies in their services and to increase the digital expertise of their workforce. In the PR/C firms, the weak technology-service intelligence fit and the association of digitalization with commodification led to a low level of technology readiness, particularly among the partners and senior managers. Thus, we wish to add technology readiness as an important service climate antecedent (Bowen and Schneider 2014), particularly related to digitalization. Based on the above, we propose:

Enacting Knowledge-Intensive Service Work at the Frontlines

Due to the novelty of the phenomenon, previous research on how digital technologies are infused in frontline service work has mainly been conceptual (Singh et al. 2017; van Doorn et al. 2017; Wirtz et al. 2018). We provide the first empirical study on how this is materialized in professional services, thereby heeding the calls for more empirical research on the topic (Singh et al. 2017; Smets et al. 2017).

Previous research has suggested that the use of digital technologies will enable service workers to engage in value-adding tasks, such as service innovation (Marinova et al. 2017), and that professional services will become more blended (Davenport and Kirby 2015). We provide new detail to these claims, by showing how the technology-service intelligence fit, occupational identity, and service climate contribute to (dis-)incentivize the frontline service worker to engage in service innovation and blend their services. We also contribute new insights into what kind of new blended services are developed (Davenport and Kirby 2015). In the auditing firms, we found that the frontline service workers innovated new tech-based services such as predictive and prescriptive analyses, which expanded their service portfolio as well as their services’ time horizon from being retrospective to becoming future-oriented. The PR/C firms, on the other hand, relied on their traditional services and treated digital elements as “add-ons.”

With empirical support and detail, we further contribute to the framework developed by Wirtz et al. (2018) by showing how firms offering services that build on complex cognitive-analytical and emotional-social tasks, increasingly develop new types of blended teams. While Wirtz et al. (2018) argue that these services will be performed by human-robot teams, our findings show that firms will use different combinations of human and robot constellations for various tasks in their services. For instance, the studied auditing firms increasingly used robots to perform analytical tasks, while humans performed emotional, relationship-building tasks. Consequently, the client-auditor interaction and interface were also transforming: from relying on human-to-human service relationships, to also include human-to-robot, and even robot-to-robot service encounters (Gutek et al. 2002; Singh et al. 2017). The PR/C firms, on the other hand, relied on human teams and on human-to-human client interactions and interfaces, as the services mainly built on emotional-social tasks. This finding highlights the need for organizations to be able to organize and manage a plethora of team constellations, and client interactions and interfaces. It also advances the conceptual framework by Singh et al. (2017) by showing how service firms traditionally providing highly complex, knowledge-based problem-solving services with rich client interfaces, through the adoption of new technologies can extend their frontlines to also encompass less complex services with rich interfaces (e.g., using robots in auditing). Thus, we provide a dynamic angle to the framework and complement it by offering an explanation for why service firms use technology (or not) to develop new client interfaces and interactions (Singh et al. 2017).