Abstract

One key challenge for consumers at the base of the pyramid (BoP) is access to products that could transform their livelihood, leading to nonconsumption as the dominant pattern. Previous studies have claimed that nonconsumption could be addressed with services offering access to goods without ownership. Drawing on expected utility theory, we conduct two experimental studies in rural India that provide the first empirical support for the idea that the availability of access-based services reduces nonconsumption at the BoP. Additionally, we show that this effect is explained by BoP consumers’ expected utility assessment as reflected in their perception of access being more affordable and entailing less financial risk than ownership. We also demonstrate that access temporality, an important configurational variable for access-based service providers, affects the degree to which nonconsumption can be decreased. Compared to short-term access, BoP consumers perceive long-term access to be too similar to ownership in terms of affordability and financial risk, which causes them to refrain from purchasing. Overall, the results suggest that access-based services represent a viable alternative for addressing nonconsumption at the BoP. However, service providers should be aware that short-term access is required to gain acceptance among BoP consumers.

The idea of reducing poverty through economic exchange has received widespread attention. The so-called base of the pyramid (BoP) consists of the billions of people in the lowest income group, predominantly in emerging markets. Not only is this segment considered to be a promising target group (Prahalad 2010), but transformative services also intend to address the multitude of challenges faced by consumers at the BoP (Anderson and Ostrom 2015).

One challenge at the BoP are consumers’ restrictions (Hill, Martin, and Chaplin 2012) that make many goods unaffordable, leading to the dominance of nonconsumption (Ojomo 2016). BoP consumers are thus prevented from using products that could improve their livelihood, such as power generators (as a reliable power source) or air coolers (for prevention of excessive heat). Such products require high investments or long-term financing, neither of which BoP consumers can afford. Moreover, the risks and responsibilities of owning a product (i.e., the “burdens of ownership”; Moeller and Wittkowski 2010) foster nonconsumption, as poverty increases risk aversion (e.g., Haushofer and Fehr 2014). The BoP is thus characterized by significant unmet needs due to a lack of access (Hammond et al. 2007). Services that offer access to goods without ownership could increase utility for BoP consumers by addressing affordability challenges and ownership risks (Karnani 2007). As Lovelock and Gummesson (2004, p. 36) explain, “in developing economies, prospects for improved quality of life may revolve around finding creative ways of sharing access to goods […] in ways that bring the price down to affordable levels.”

Access-based services have attracted increasing attention as an alternative consumption mode (e.g., Bardhi and Eckhardt 2012; Schaefers et al. 2016). Prominent examples include car and bike sharing (e.g., Zipcar, Capital Bikeshare) and short-term rental of fashion items (e.g., Bag Borrow or Steal). Such services give multiple individuals temporary access to a product, in return for a fee that is substantially lower than the ownership price. However, despite the growing attention, research has focused only on developed economies (e.g., Bardhi and Eckhardt 2012; Baumeister, Scherer, and von Wangenheim 2015; Schaefers et al. 2016; Wittkowski, Moeller, and Wirtz 2013). For the BoP context, where access-based services may have a transformative impact, access has been mentioned only in conceptual papers and anecdotal evidence (e.g., Blocker et al. 2013; Karnani 2007). To the best of our knowledge, there remains no empirical evidence regarding the potential of access-based services in reducing nonconsumption at the BoP.

Addressing this research gap, we investigate the effects of offering access to BoP consumers as an alternative to ownership. Two experimental studies among consumers in rural India show that making access-based services available can reduce nonconsumption at the BoP. Based on expected utility theory (Oliver and Winer 1987), we show that different utility assessments of ownership and access explain BoP consumers’ access preference. We also investigate how access temporality, a key configurational variable for access-based service providers, influences utility assessments and choices. We find that, among BoP consumers, short-term access is required in order to reduce nonconsumption, as long-term access does not have greater expected utility than ownership.

The empirical evidence for the transformative potential of access-based services and the insights into the underlying expected utility assessment processes contribute to the existing literature on transformative services (e.g., Anderson and Ostrom 2015; Blocker et al. 2013) and on the use of market-based approaches to increase well-being at the BoP (e.g., Hammond et al. 2007). We further expand the current scope of research on access-based services by examining utility assessment differences between ownership and access and by investigating access temporality as a managerially relevant characteristic. The results of our study are relevant for service providers and public policy makers in evaluating the potential of access-based services at the BoP.

Nonconsumption at the Base of the Pyramid

The BoP comprises the lowest income segment of the world’s population, located predominantly in developing economies and in rural areas (e.g., London, Anupindi, and Sheth 2010). For these consumers, chronic restrictions impede consumption of goods that could improve living conditions. Hill and Stephens (1997) describe how these restrictions arise from a lack of income and impede access to products. As Blocker et al. (2013, p. 1196) state, “individuals facing chronic restrictions in the marketplace may be unable to consume many things that are needed for basic survival, not to mention objects of desire throughout life.” The BoP is thus characterized by a substantial amount of nonconsumption. As Ojomo (2016) describes: “If nonconsumption were a company in Nigeria, or in almost any other emerging market, it would have a monopoly in most industries.”

Despite the large share of nonconsumption, consumers at the BoP appear to desire many products. Hill and Stephens (1997) describe coping strategies that impoverished consumers use to obtain goods. Hill, Martin, and Chaplin (2012) found social comparison based on access to goods to be important for BoP consumers; their analysis shows that impoverished consumers, whose access to goods is more restricted than that of others within their societies, experience even less life satisfaction.

In order to better understand BoP consumers and the possibilities of reducing poverty, prior studies have examined, for instance, the psychological consequences of poverty (e.g., Haushofer and Fehr 2014), the determinants of BoP consumers’ purchase decisions (e.g., Chikweche and Fletcher 2010), the relationship between saving money and well-being (e.g., Martin and Hill 2015), and the long-term effects of different pricing strategies (Jones Christensen, Siemsen, and Balasubramanian 2015). However, to the best of our knowledge, the idea of reducing nonconsumption at the BoP has not been empirically investigated. Moreover, existing work has conceptualized reducing nonconsumption at the BoP by making ownership more affordable. Hart and Christensen (2002) describe how substantially reducing product features allows for lower purchase prices. Despite less functionality, BoP consumers may purchase “because nonconsumption is the alternative, and customers often prefer something to nothing, even if that something is not very good from a high-end market viewpoint” (Hart and Christensen 2002, p. 56). Similarly, Nakata and Weidner (2012) suggest that reduced features or smaller units would allow for lower prices, which should enhance BoP consumers’ product adoption. In contrast to these considerations of reducing ownership thresholds, we empirically test whether making shared access services available reduces nonconsumption.

Access-Based Services

In line with recent conceptualizations (Schaefers et al. 2016; Wittkowski, Moeller, and Wirtz 2013), we define access-based services as giving customers access to a good for a period of time in return for an access payment, thereby offering a certain degree of freedom in using this product while legal ownership remains with the service provider. Two key differences between ownership and access are specifically relevant with regard to BoP consumers.

First, the access price is a fraction of the price for obtaining ownership. Compared to ownership, access-based services only require a fee per usage unit (e.g., per hour or day). Although the accumulated fees for an access-based service can be higher over time than the purchase price (Durgee and O’Connor 1995), the individual payments are lower, making access more affordable than ownership (Blocker et al. 2013; Lovelock and Gummesson 2004).

The second difference pertains to the risks and responsibilities involved. The decision to own comes with financial risks (Kaplan, Szybillo, and Jacoby 1974), and ownership also includes the financial responsibility for maintenance and repair. These burdens of ownership, which are connected to potentially negative monetary impacts, 1 can be avoided with access-based services (Berry and Maricle 1973; Moeller and Wittkowski 2010; Schaefers, Lawson, and Kukar-Kinney 2016). Although there are also certain burdens of access (Hazée, Delcourt, and Van Vaerenbergh 2017), these barriers are predominantly nonmonetary, such as the potential contamination of products used by other customers.

In light of consumers’ resource restrictions at the BoP, the two outlined characteristics of access—affordable prices and avoiding the burdens of ownership—suggest that it may be a relevant consumption mode for BoP consumers. In the next section, we will hypothesize how these characteristics should allow for reducing nonconsumption at the BoP and how expected utility assessment should explain this effect.

Nonconsumption Reduction Via Access-Based Services

To develop hypotheses about the effects of access-based service availability on nonconsumption at the BoP, we draw on expected utility theory (Oliver and Winer 1987) and the underlying utility maximization principle. Consumers are assumed to choose among available alternatives by evaluating each subjective expected utility (Foxall, Oliveira-Castro, and Schrezenmaier 2004; Verma, Thompson, and Louviere 1999). Therefore, “individuals seek to maximize their subjective expected utility on the basis of an internal assessment of the future gains and losses” (Polo and Sese 2013, p. 140) associated with the available alternatives. As we outline below, utility maximization considerations can explain both BoP consumers’ nonconsumption and their reactions to access availability.

According to expected utility theory, nonconsumption results from a situation in which, among all available alternatives, the ratio of expected gains and expected losses is below the utility of maintaining the status quo (Dhar 1997). Thus, none of the available alternatives reaches the utility threshold (White, Hoffrage, and Reisen 2015), 2 and consumers refrain from purchasing. This is more likely to occur at lower income levels, as the ratio of expected costs of making a purchase and the available monetary resources is greater. Expected utility theory thus explains BoP consumers’ preference for nonconsumption over ownership when access is unavailable as evidenced by the predominance of nonconsumption at the BoP.

The availability of an access-based service in addition to ownership allows consumers to obtain a product’s expected benefits at substantially lower costs (Lovelock and Gummesson 2004). Thus, an access-based service reduces the threshold for using a product while the product’s benefit remains largely the same. Under utility maximization assumptions, the availability of access should thus, in general, decrease nonconsumption. If consumer restrictions at the BoP are also taken into consideration, it becomes clear that these consumers should be especially receptive to maximizing their utility by obtaining a product’s benefits at reduced costs (Karnani 2007). Prior research, for instance, has found impoverished consumers to be more likely to use means that make products more affordable, such as coupons (Noble et al. 2017). As Blocker et al. (2013, p. 1199) describe, the idea of shared access to resources at lower cost per individual “aligns with the needs of poor consumers because the emphasis shifts from possession of products, which typically requires substantial income, to having ability to ‘access’ products and services.” Access-based services thus allow BoP consumers to use products they could not afford to own. We therefore assume that making an access-based service available in addition to ownership should encourage BoP consumers to choose access instead of nonconsumption, while this effect should be weaker for consumers whose income puts them outside the BoP, in the so-called mid-market segment (Hammond et al. 2007).

3

To test whether expected utility theory explains BoP consumers’ reactions to the availability of access, we also investigate three related concepts that determine expected utility. According to Oliver and Winer (1987), consumers’ utility assessment is based on currently available, immediate knowledge (i.e., “now” knowledge) as well as anticipatory or “future” knowledge. While the former describes available information on a product, the latter represents an apprehension about possible outcomes of a purchase decision. These two types of knowledge immediacy are related to the third concept, uncertainty, which describes the risk inherent in evaluating a decision’s future utility. We propose that these three concepts are reflected in consumers’ perceptions of the affordability, transaction utility, and financial risk of a purchase situation.

The information available when making a purchase decision includes a product’s price (Oliver and Winer 1987). This “now” knowledge is important for judging an offer’s affordability, which is a key determinant of purchase behavior (Notani 1997). In the BoP context specifically, due to resource restrictions affordability represents “one of the most critical features” (Nakata and Weidner 2012, p. 25). We propose that, because access-based services allow for prices at affordable levels (Lovelock and Gummesson 2004), the difference in perceived affordability between access and ownership is greater among BoP consumers than among mid-market consumers.

The “future” knowledge that consumers incorporate into their expected utility estimation is reflected in their assessment of the transactional utility (Thaler 1985), that is, the perception of an offer representing a “good deal.” Thus, in addition to immediately judging an offer based on its affordability (i.e., current knowledge about the difference between available and required resources), consumers will predict the future utility of a purchase. Compared to ownership, consumers may determine that access is a better deal because they are able to gain access to a product for considerably less than the reference price. Restrictions at the BoP again suggest that the difference between the access fee and the purchase price leads BoP consumers to perceive the former as a better deal than consumers who face fewer monetary restrictions. Therefore, we propose that BoP consumers’ perceived difference in transaction utility between access and ownership is greater than that of mid-market consumers.

Both the known data on a product and the anticipatory knowledge are connected to the uncertainty a consumer faces when making a purchase decision. This aspect of expected utility assessment is reflected in consumers’ perceived financial risk, 4 defined as the uncertainty regarding the likelihood and severity of a financial loss after a consumption decision (DelVecchio and Smith 2005). In the context of access-based services, because the ownership price is higher than the fee for obtaining access, ownership is characterized by a greater potentially negative outcome. Additionally, access entails lower opportunity costs than ownership due to its temporary nature. While access also entails different burdens (Hazée, Delcourt, and Van Vaerenbergh 2017), these are not as strongly related to potential financial losses because a wrong choice regarding an access-based service can be corrected with less financial harm. Although avoiding the burdens of ownership represents a general motive for access-based service use (e.g., Schaefers, Lawson, and Kukar-Kinney 2016), it appears to be especially relevant at the BoP. The differences in perceived financial risk between ownership and access should be greater for BoP consumers, as they risk a greater proportion of their income.

Taken together, the three concepts of expected utility theory, reflected in perceived affordability, transaction utility, and financial risk, should explain why BoP consumers prefer access over ownership when the former is also available.

Study 1

Method

Setting and Data Collection

To test the effects of access availability (Hypothesis 1) and the factors underlying access preference (Hypothesis 2), we conducted an experiment with one manipulated between-subjects factor (ownership only vs. ownership and access available) and one measured variable (monthly household income). For the context, it was important to select a product category relevant to BoP consumers regarding potential livelihood improvement. At the same time, it needed to be a product with affordability constraints. Based on these criteria, we chose solar-powered air coolers for the following reasons. First, annual mean temperatures in emerging markets such as India have been increasing for decades, raising the demand for products that reduce the detrimental effects of excessive heat (Dzieza 2017). Second, the product category addresses the vulnerability from excessive weather conditions, which is substantially higher among BoP consumers (Mazdiyasni et al. 2017). Third, it is a suitable product category due to the lack of access to electricity, which is a universal characteristic of the BoP (Hammond et al. 2007).

Our study was conducted in rural areas of the Indian state of Rajasthan. Data collection was based on paper-and-pencil questionnaires used in personal interviews. Scenario descriptions and the questionnaire were translated from English to Hindi by a professional translator and translated back into English by one of the authors to ensure consistency. The challenge of recruiting respondents was met by cooperating with a local nongovernmental organization (NGO) with experience in survey-based data collection. Support from the NGO also increased trust among respondents. The interviewers were instructed to randomly select one of the two questionnaire versions, explain it to respondents, and collect responses. To verify proper completion of the procedure, we conducted a 2-day pretest in the field. Subsequently, one of the authors held a feedback session with all interviewers. The interviewers then collected data for 30 days, accompanied by regular update sessions with one of the authors.

Complete questionnaires were obtained from 266 respondents. Following DiLalla and Dollinger (2006), invalid responses were excluded from the final analysis: Two respondents reported incomes 1.5 times and 2 times as high, respectively, as the next highest reported income; nine respondents were not involved in family purchase decisions for household goods; six cases exhibited straight-lining answering patterns (Menictas, Wang, and Fine 2011); and 13 respondents reported inconsistent scores in quality control items. The final analyzable sample thus consisted of 236 individuals (60.2% male; M age = 36.2 years, SD = 9.97), equally distributed across both experimental conditions.

Procedure and Manipulations

All surveys began by assessing respondents’ involvement in household purchase decisions and by capturing their general risk aversion. The second page contained a picture and brief description of a solar-powered air cooler as well as questions on the product’s expected livelihood impact and respondents’ attitude toward the product.

We manipulated access availability by describing two different offers (see Supplementary Appendix 1). In the first condition, where ownership was available and access was unavailable, respondents were informed that the product could be purchased for INR 9,000 (approximately US$ 140). This price was based on actual sales prices for similar products. Participants then evaluated the offer’s affordability, transaction utility, and financial risk before indicating whether they would purchase the product for the quoted price or whether they were not interested (i.e., nonconsumption). In the second experimental condition (i.e., both ownership and access available), respondents were informed that the product could either be purchased (for the same price as in the first condition) or rented for a monthly fee of INR 375 (approximately US$ 6). We selected this fee to ensure a moderate amount of time (i.e., 24 months) before accumulated access fees matched the purchase price. Respondents in the second experimental condition evaluated the affordability, transaction utility, and financial risk of both the ownership offer and the access offer. Finally, they indicated their preference for purchasing, renting, or neither. Both experimental conditions were thus equivalent by describing the same product and offering it for the same purchase price. The only difference was in the availability of access. Both conditions ended with questions on respondents’ gender, age, average monthly household income, and an evaluation of the survey.

Responses to the question on expected livelihood impact (“This product would make my life better”; 5-point scale) revealed a mean of 3.49 (SD = 1.17), which was significantly above the scale’s mid-point (t = 6.39, p < .001). This result shows that the selected product category is generally relevant for respondents. Importantly, responses did not differ across experimental groups (b = .37, t = 1.49, p = .14) nor across income (b = .00001, t = .67, p = .51; Experimental Group × Income interaction: b = −.00001, t = −.37, p = .72).

Respondents perceived both scenarios to be equally understandable: “The questionnaire was easy to understand”; 5-point scale; M unavailable = 3.92; M available = 3.99; F(1, 234) = .30; p = .56. Understanding was not influenced by income (b = .000001, t = .08, p = .94; Experimental Group × Income interaction: b = −.000003, t = −.20, p = .84). Moreover, understanding did not confound our results, as no differences existed across choice categories in each scenario (unavailable: F(1, 115) = 1.47, p = .23; available: F(2, 116) = 1.19, p = .31).

Measures

The dependent variable was respondents’ choice of nonconsumption, ownership, or access (when available). The mediating variables and covariates are listed in Appendix A, and a correlations table can be found in Supplementary Appendix 2. Single items were used to capture the affordability and transaction utility of ownership and access, respectively. Perceived financial risk of ownership and access were each assessed with 3 items based on DelVecchio and Smith (2005). As covariates, we captured respondents’ general risk aversion (Mandrik and Bao 2005) and their utilitarian attitude toward the product (Voss, Spangenberg, and Grohmann 2003).

Income Levels

In our sample, monthly household income ranged from INR 1,000 (approximately USD 15) to INR 50,000 (approximately USD 770), with a median of INR 10,000 (approximately USD 150), a mean of INR 11,004.23 (approximately USD 170), and an SD of INR 8,709.06 (approximately USD 134). The income distribution of our sample thus mirrors the income distribution in rural areas of Rajasthan (Labour Bureau 2016). Importantly, there were no income differences between the two experimental conditions (M unavailable = 10,284.62, SD = 8,502.54; M available = 11,711.75, SD = 8,886.31), F(1, 234) = 1.59, p = .21.

Common Method Bias

Because data were collected from the same respondents at the same point in time, we accounted for common method bias (Podsakoff et al. 2003). Respondents were encouraged to answer honestly and were informed that there were no right or wrong answers. Moreover, in order to prevent implicit theorizing, the underlying conceptual model was not disclosed.

To assess and control for possible common method bias, we employed the marker variable technique (Lindell and Whitney 2001; Podsakoff et al. 2003). As a theoretically unrelated marker variable, we used respondents’ enjoyment of research participation (“I enjoy participating in research studies,” 5-point scale). Bivariate correlations revealed very few significant relations between the marker variable and the other questionnaire items (significant correlations between −.19 [p = .03] and .21 [p < .01]); the average absolute correlation was very low (.10). We also included the marker variable in all estimations required for hypotheses testing and compared the results with and without the marker variable. As the results remained stable, common method variance does not account for the estimates obtained and thus does not bias our results.

Results

Effects of Access Availability

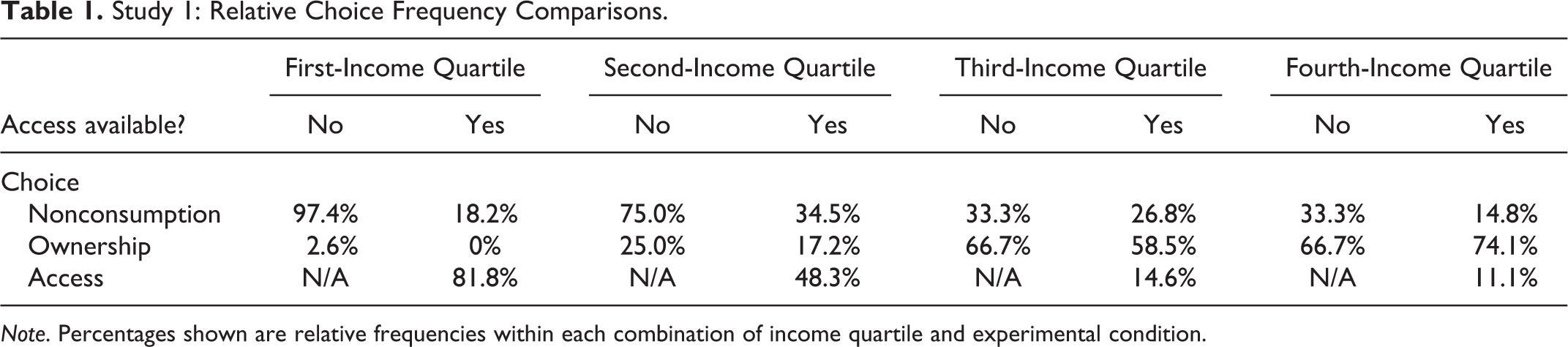

We first observed the relative choice frequencies across income levels by comparing our sample’s income quartiles (Table 1). Generally, access availability leads to a decreased frequency of nonconsumption, while the frequency of ownership remains relatively stable. Additionally, both the decrease in nonconsumption and the frequency of choosing access are greatest in the lowest income quartile.

Study 1: Relative Choice Frequency Comparisons.

Note. Percentages shown are relative frequencies within each combination of income quartile and experimental condition.

To test Hypothesis 1, we estimated a binary logistic regression that analyzed the effects of access availability and income on nonconsumption, with the remaining two decisions for ownership and access combined as a reference category. The independent variables in the regression equation were access availability, mean-centered income, and the Access Availability × Income interaction. Age, gender, risk aversion, attitude toward the product, and expected livelihood impact were included as covariates. The results show significant effects of access availability (b = −1.78, z = −5.13, p < .001), income (b = −.00014, z = −4.30, p < .001), and the Access Availability × Income interaction (b = .00011, z = 2.43, p < .05). 5 Of the covariates, a more positive attitude toward the product (b = −.41, z = −2.21, p < .05) and a greater expected livelihood impact (b = −.36, z = −2.18, p < .05) decrease the probability of nonconsumption, while greater risk aversion increases it (b = .38, z = 1.82, p < .10).

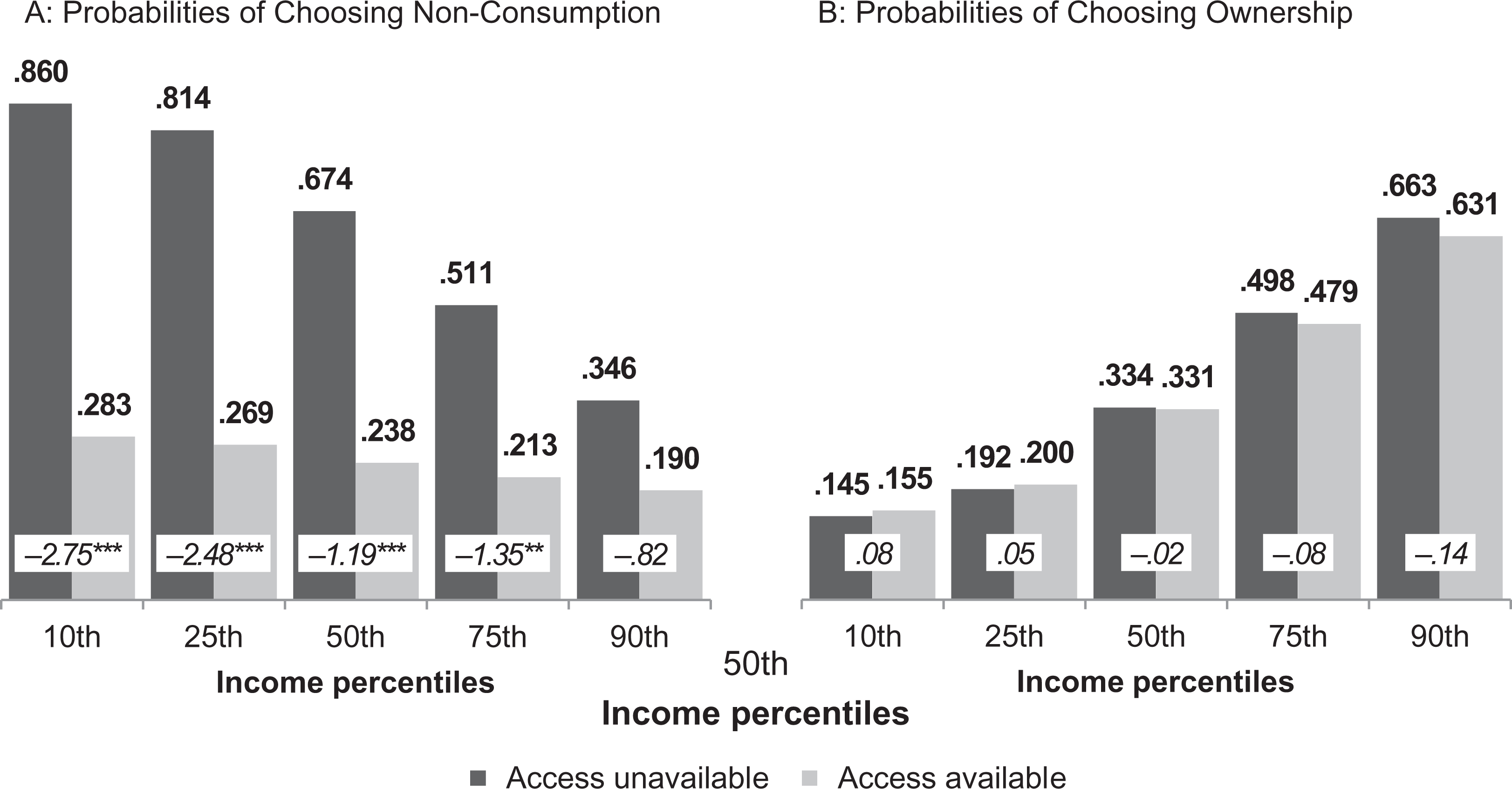

A spotlight analysis (Irwin and McClelland 2001) based on the 10th, 25th, 50th, 75th, and 90th income percentiles reveals that among lowest income respondents (10th percentile; INR 2,000; approximately USD 31), access availability significantly reduces nonconsumption (b = −2.75, z = −5.23, p < .001). At higher income levels, this effect is attenuated. For respondents in the 90th percentile (INR 20,000; approximately USD 310), no significant effect is observed (b = −.82, z = −1.54, p = .12). Based on the regression coefficient estimates, Figure 1A displays the estimated probability of nonconsumption by access availability at different income levels. In addition, we used the Johnson-Neyman technique (Johnson and Fay 1950) to determine the income at which the probability of nonconsumption is no longer reduced when access is available. This occurs at INR 18,710 (approximately USD 288), which is slightly above the threshold proposed by Hammond et al. (2007) for distinguishing BoP and mid-market consumers. In other words, the availability of access reduces nonconsumption at monthly household income levels below INR 18,710 but has no effect above this value.

Study 1: estimated choice probabilities and spotlight results. Note. Values in bold are estimated probabilities based on logistic regression results; covariates included are age, gender, risk aversion, attitude toward the product, and expected livelihood impact. Values in italics are spotlight analysis regression coefficients. ***p < .001, **p < .01.

To assess the robustness of our findings, we examined whether the decrease in nonconsumption was caused by an increase in ownership preference. We thus analyzed the influence of access availability on the likelihood of choosing ownership by conducting a logistic regression analysis on the decision to own, with the two decisions for access and nonconsumption as the reference category. There is only an effect of income (b = .00014, z = 4.33, p < .001) and the covariate attitude toward the product (b = .55, z = 2.76, p < .01). Figure 1B illustrates that the likelihood of choosing ownership is greater at higher income levels, but that access availability does not affect this decision, lending further support to our hypothesis. Overall, these results indicate that when access is available in addition to ownership, BoP consumers replace nonconsumption with access.

Explaining Access Preference

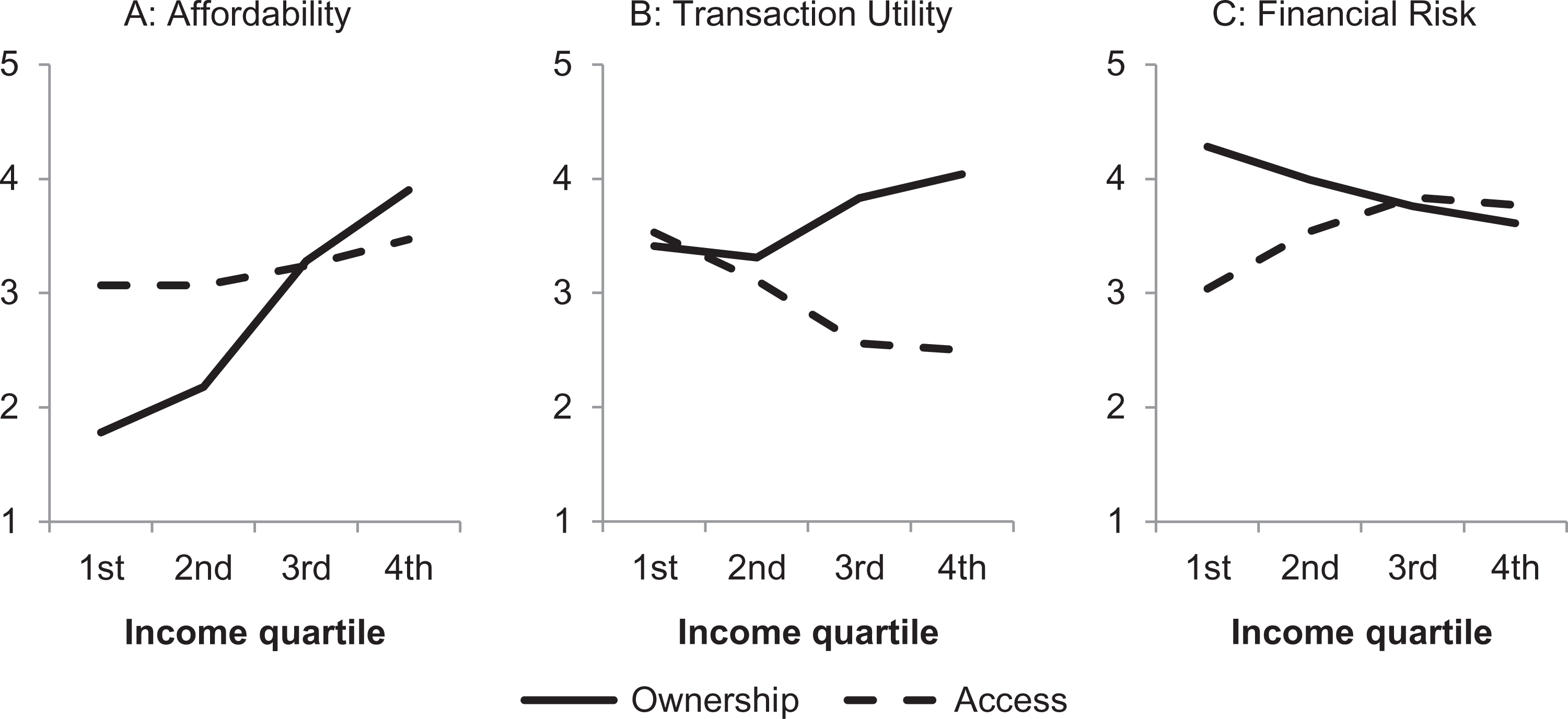

Analysis of the expected utility assessment underlying the reduction in nonconsumption (Hypothesis 2) was only possible for respondents who could choose access (i.e., the access available condition). We analyzed a repeated-measures analysis of covariance for affordability, transaction utility, and financial risk among these participants, using income quartiles as a between-subjects factor. For affordability, the interaction between consumption mode and income is significant, F(3, 110) = 8.20; p < .001. Similarly, an interaction is observed for financial risk, F(3, 110) = 10.65; p < .001. As illustrated in Figure 2A and C, respondents in the first- and second-income quartiles perceive access to be more affordable and to entail less financial risk than ownership (p < .01), while there are no differences among respondents in the third and fourth income quartiles, lending partial support to the assumption that BoP consumers assess the expected utility of access to be greater than that of ownership. For the within-subjects comparison of transaction utility, although the consumption Mode × Income interaction is significant, F(3, 110) = 4.65; p < .01, the estimated marginal means reveal a pattern opposite to the other two variables (Figure 2, panel B). Contrary to our assumption, perceptions do not differ in the first two income quartiles; among respondents in the third and fourth quartiles, access is perceived to have lower transaction utility than ownership (p < .001).

Study 1: Within-subjects comparisons by income. Note. Analysis performed with access available condition participants. Values are estimated marginal means; covariates included are age, gender, risk aversion, attitude toward the product, and expected livelihood impact.

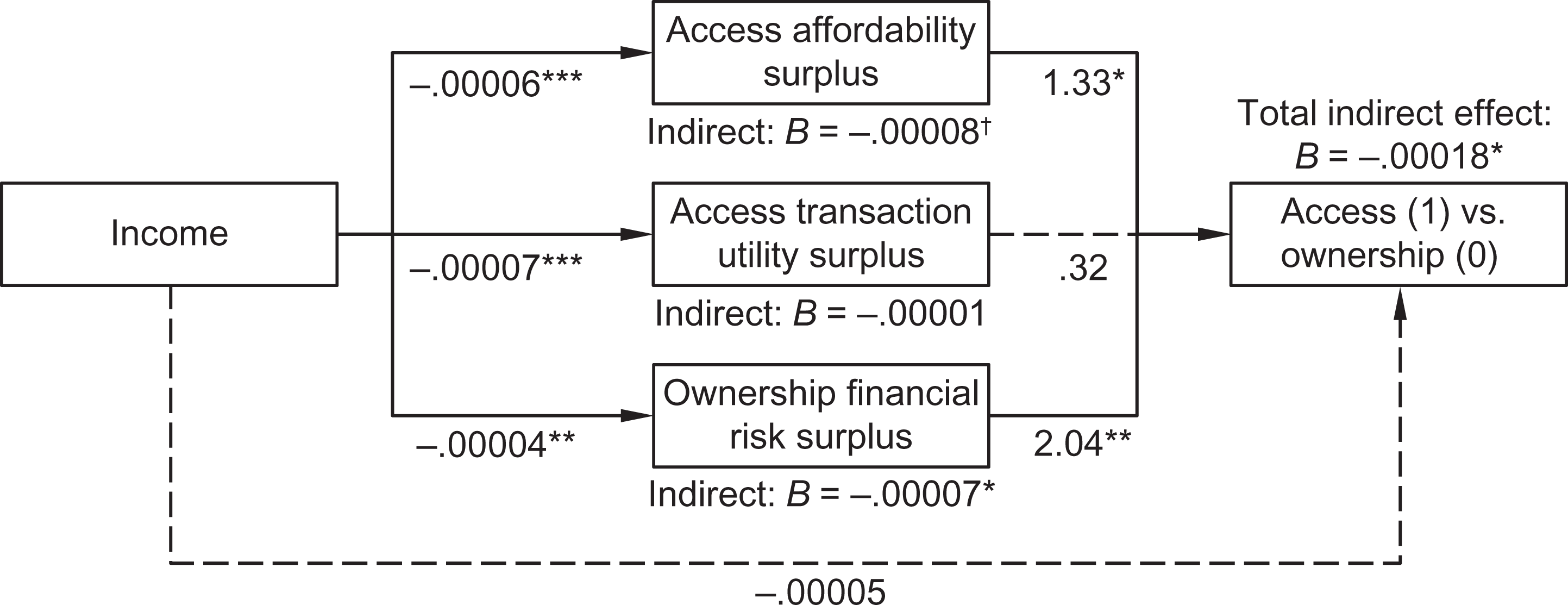

We examined whether the three expected utility variables explain the greater access preference among BoP consumers by estimating a mediation model using the PROCESS SPSS macro (Version 2.16, Model 4, 10,000 bootstrap samples; Hayes 2013). The dependent variable was again access preference (0 = ownership, 1 = access). To incorporate the within-subjects differences in expected utility assessment, we calculated difference scores for the three variables in question. By subtracting each respondent’s rating for ownership affordability from their rating for access affordability, we calculated the degree to which access is perceived to be more affordable than ownership, denoted as “access affordability surplus.” Similarly, we subtracted the transaction utility scores for ownership from the transaction utility scores for access to create a variable named “access utility surplus.” By subtracting financial risk perception of access from financial risk perception of ownership, we calculated a variable denoted as “ownership financial risk surplus,” which represents the extent to which perceived financial risk of ownership exceeds that of access. 6

The mediation results, illustrated in Figure 3, indicate two significant indirect paths, as the bootstrap confidence interval (CI) excludes zero: The effect of income on access preference is mediated by access affordability surplus (B = −.00008, standard error [SE] = .00012, 90% CI: [−.00014, −.00001]) and ownership financial risk surplus (B = −.00007, SE = .00008, 95% CI: [−.00020, −.00001]). Because the direct path from income to access preference becomes nonsignificant when the mediators are included (b = −.00005, z = −1.14, p = .26), there is complete mediation. Thus, compared to mid-market consumers, BoP consumers view access as more affordable and less risky than ownership, which explains their greater preference for access over ownership when the former is available.

Study 1: Mediation Analysis Results. Note. Analysis performed with access available condition participants. Access affordability surplus represents the difference between affordability of access and of ownership. Access transaction utility surplus represents the difference between the perceived transaction utility of access and of ownership. Ownership financial risk surplus represents the difference between perceived financial risk of ownership and of access. Covariates included are age, gender, risk aversion, attitude toward the product, and expected livelihood impact. ***p < .001, **p < .01, *p < .05, †p < .10.

Discussion

Study 1 investigated how access availability influences choice among BoP consumers and the process underlying their preferences. Supporting Hypothesis 1, BoP nonconsumption is reduced when an access-based service is available in addition to ownership. Moreover, their preference for access is explained by the expected utility assessment based on current knowledge (i.e., affordability) and uncertainty (i.e., financial risk), lending partial support to Hypothesis 2. However, BoP consumers do not evaluate access to have higher transaction utility than ownership. This result could indicate that under resource restrictions, expected utility assessment is not primarily based on future utility but rather on data-in-hand and uncertainty. Mid-market consumers, in contrast, focus more on future knowledge (i.e., transaction utility) and perceive access to have less transaction utility than ownership, which may indicate their focus on the possibility that over time, accumulated rental fees will exceed the purchase price (Durgee and O’Connor 1995).

Overall, the results support the assumption that access-based services are a viable alternative for BoP consumers due to greater affordability and less financial risk. Our findings provide novel insights into the general applicability of access in a BoP context. However, as Lovelock and Gummesson (2004) point out, it is important to gain a better understanding of the effects of various characteristics of access-based services that managers may use to address a target market.

Access Temporality

Access-based service providers can configure various characteristics of their offering. Prior research has, for instance, considered the accessed product’s brand, the level of service convenience, and the access price (e.g., Baumeister, Scherer, and von Wangenheim 2015; Schaefers et al. 2016). Another important characteristic is the temporality, meaning the minimum length of access required by a service provider (i.e., minimum rental period). Previous studies have investigated individual types of access temporality, such as car sharing, in which customers pay per minute of rental time (e.g., Baumeister, Scherer, and von Wangenheim 2015; Schaefers, Lawson, and Kukar-Kinney 2016). Other studies have addressed relatively short-term operating leasing (e.g., Wittkowski, Moeller, and Wirtz 2013) and long-term rental (e.g., Gullstrand Edbring, Lehner, and Mont 2016). However, to the best of our knowledge, no study has compared different levels of temporality. This is surprising, as temporality is considered one of the key dimensions of access (Bardhi and Eckhardt 2012).

In the BoP context, it is important to consider temporal aspects of access-based services for the following three reasons. First, an increase in access temporality increases the minimum rental fee. In light of BoP consumers’ resource restrictions, it is likely that greater access temporality affects the expected utility of an access-based service and reduces its attractiveness for this target group. Second, poverty was found to elicit a greater focus on the present than the future as evidenced by increased time-discounting (Haushofer and Fehr 2014) and a “short-term focus on continued existence” (Martin and Hill 2012, p. 1158). However, previous research has not sufficiently examined the effects of this temporal orientation on service consumption practices. Third, for service providers, access temporality represents an important managerial lever that affects asset utilization and revenues. However, due to the lack of broad experience with access-based services at the BoP, there remains no deeper understanding of how different levels of access temporality affect consumers’ service acceptance.

From the perspective of expected utility theory, greater levels of access temporality (e.g., long-term vs. short-term rental) increase the minimum rental fee and thus capital commitments (Klein and Leffler 1981), which should decrease utility. The difference in expected utility between access and ownership, as shown in Study 1, should therefore be reduced. For BoP consumers, an increase in access temporality is more likely to decrease expected utility below the utility threshold (White, Hoffrage, and Reisen 2015) or even make access unaffordable, which should be reflected in greater nonconsumption. In contrast, according to utility maximization, lower access temporality should lead to greater access preference, especially among BoP consumers.

As a core service characteristic, access temporality affects consumers’ expected utility assessment regarding knowledge immediacy (i.e., “now” and “future” knowledge) and uncertainty. Differences in the minimum usage period are thus likely to affect perceived affordability, transaction utility, and financial risk. First, as an increase in access temporality translates to a higher financial threshold, it reduces affordability. Second, because greater access temporality reduces flexibility and increases the likelihood of accumulated access fees exceeding the product’s purchase price, the offer represents less of a good deal than low temporality. Third, because greater temporality increases the consumer’s financial obligation, the risk of monetary loss because of a wrong purchase decision increases. Due to the financial restrictions, these differences in expected utility assessment should be greater for BoP consumers and should explain their access preference.

Study 2

Method

Setting and Data Collection

Study 2 comprised one manipulated between-subjects factor (short-term vs. long-term access) and household income as a measured variable. The context was identical to Study 1 (solar-powered air cooler). Data were again collected in rural areas of Rajasthan (India) in cooperation with the same NGO, using paper-and-pencil questionnaires.

Complete questionnaires were obtained from 280 different respondents than in Study 1. Based on quality checks (DiLalla and Dollinger 2006), invalid responses were excluded: Five participants were outliers in terms of household income, 21 were not involved in family purchase decisions, 4 questionnaires showed straight-lining in the answers, and 5 respondents failed quality control items. Thus, the final sample consisted of 245 responses (65.3% male, M age = 38.1 years, SD = 11.91), almost evenly split between the two experimental conditions (short-term access n = 109; long-term access n = 136).

Procedure and Manipulations

Surveys were identical to the access available condition of Study 1, with the only difference being the minimum required rental period (see Supplementary Appendix 1). In the short-term access condition, participants were informed that the product could be rented “for INR 12 per day/INR 360-372 per month (minimum rental period: 1 day).” In the long-term access scenario, the terms were stated as “INR 12 per day/INR 360-372 per month (minimum rental period: 6 months = INR 2,196).” Thus, both conditions differed only in temporality, while the rental fee remained constant. We stated the daily/monthly rental fee to prevent confounding effects of respondents’ ability to calculate the minimum required payment. A manipulation check question was included (“How do you evaluate the required minimum rental period?”; 5-point scale; 1 = short term, 5 = long term). As intended, responses in the short-term condition (M = 2.17) differed from those in the long-term condition, M = 3.36; F(1, 243) = 41.28; p < .001.

Both scenarios were equally understandable (M short-term = 3.60; M long term = 3.71), F(1, 243) = .47; p = .49, and understanding was not influenced by income (b = .000009, t = 1.17, p = .24; Experimental Group × Income interaction: b = −.000007, t = −.57, p = .57). Respondents’ understanding did not differ across the three choice categories, F(2, 242) = .29; p = .75.

Measures

The dependent variable was respondents’ choice between purchasing (ownership) or renting (access) the product or neither (nonconsumption). We used the same scales as in Study 1 to measure affordability, transaction utility, and financial risk of both ownership and access as well as general risk aversion, attitude toward the product, and expected livelihood improvement (see Appendix A and Supplementary Appendix 3).

Income Levels

Respondents’ monthly household income ranged from INR 950 (approximately USD 14) to INR 72,000 (approximately USD 1,100), with a median of INR 8,000 (approximately USD 123) and a mean of INR 13,143.47 (approximately USD 202; SD = INR 14,171.28). The income distribution of our sample is again representative for rural areas of Rajasthan (Labour Bureau 2016). No income differences existed between the experimental conditions (M short-term = 13,380.28, SD = 15,873.09; M long-term = 12,953.68, SD = 12,701.47), F(1, 243) = .06, p = .82.

Common Method Bias

We again tested and controlled for common method bias. The same remedies were used as in Study 1, and we again used respondents’ enjoyment of research participation as a marker variable. Correlations with the focal variables were small (r < .28), and inclusion of the marker variable did not change the results. Thus, common method bias was deemed negligible.

Results

Direct Effects of Access Temporality

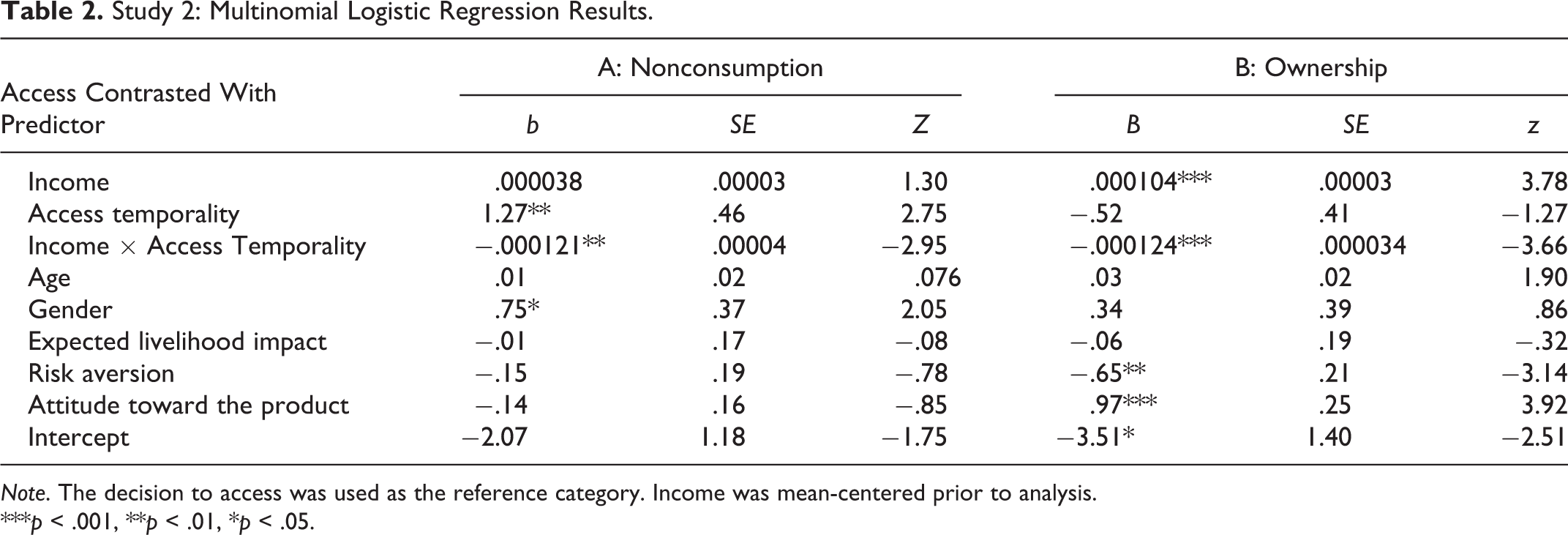

We conducted a multinomial logistic regression, with choice as the dependent variable, using the decision to access as the reference category. The independent variables were access temporality (0 = short term, 1 = long term), mean-centered income, and the Temporality × Income interaction. Covariates were age, gender, risk aversion, attitude toward the product, and expected livelihood impact. The significant likelihood ratio test for the overall model, χ2(16) = 98.50, p < .001, and a Nagelkerke’s R 2 of .379 indicate an adequate model fit. The likelihood ratio tests for the individual variables indicate significant effects for access temporality, χ2(2) = 12.94, p < .01; income, χ2(2) = 23.19, p < .001; the Temporality × Income interaction, χ2(2) = 22.16, p < .001; attitude toward the product, χ2(2) = 26.44, p < .001; and risk aversion, χ2(2) = 10.53, p < .01. Table 2 provides the parameter estimates of the two contrasts.

Study 2: Multinomial Logistic Regression Results.

Note. The decision to access was used as the reference category. Income was mean-centered prior to analysis.

***p < .001, **p < .01, *p < .05.

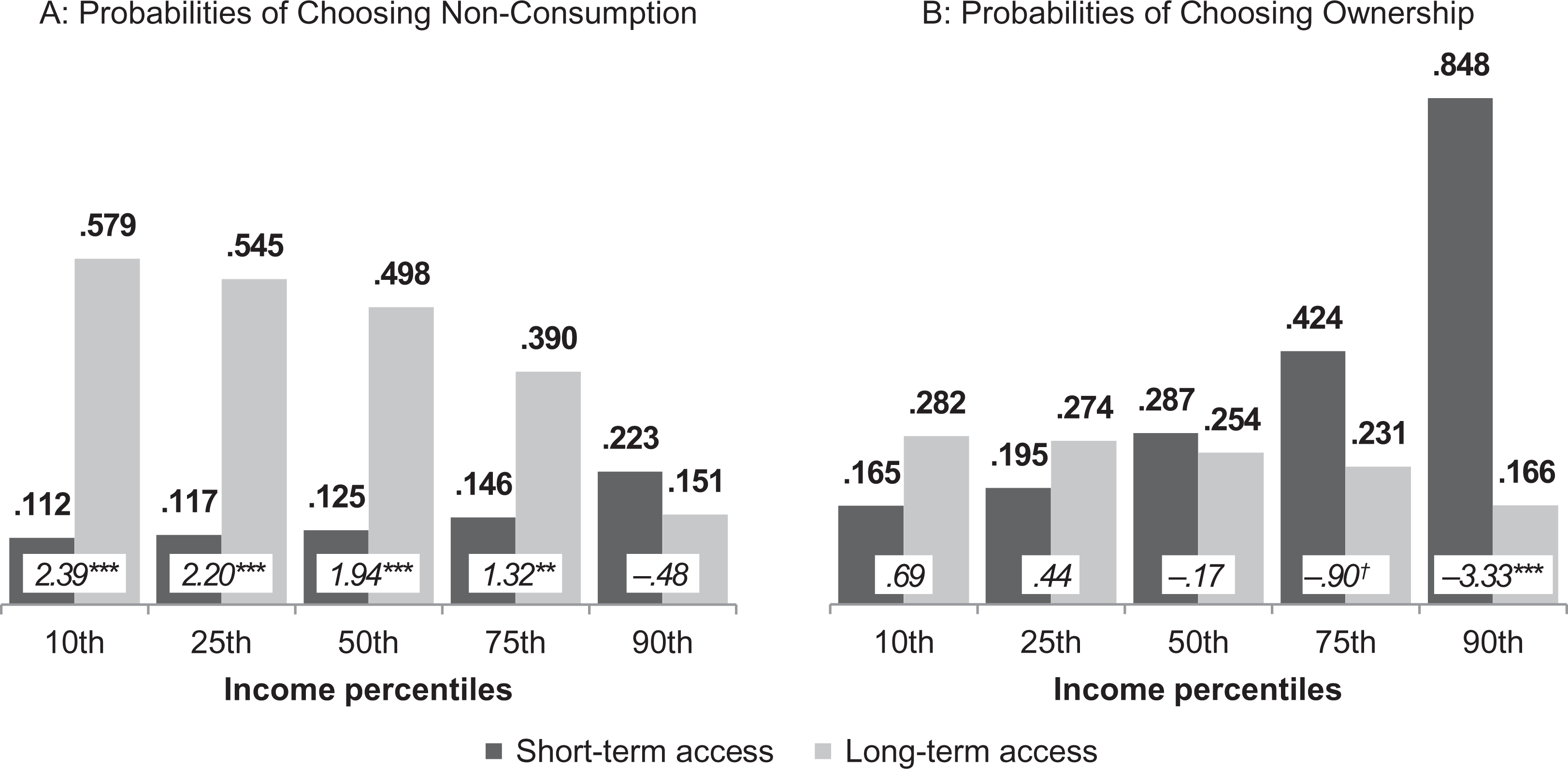

The comparison between access preference and nonconsumption (Table 2A) showed no significant impact of income (p = .20). As hypothesized, compared to short-term access, long-term access increases the likelihood of respondents’ nonconsumption. Moreover, the significant interaction indicates that this effect is stronger at lower income levels. We again used the Johnson-Neyman technique (Johnson and Fay 1950) to spotlight differences in respondents’ reactions to access temporality depending on income. For an income below INR 18,063 (approximately USD 278), again close to the BoP threshold (Hammond et al. 2007), long-term access reduces preference for access and increases the probability of nonconsumption. For respondents at or above this threshold, access temporality does not influence choice. Figure 4A shows the estimated probability of preferring nonconsumption over access by temporality at different income levels.

Study 2: Estimated choice probabilities and spotlight results. Note. Values in bold are estimated probabilities based on logistic regression results; covariates included are age, gender, risk aversion, attitude toward the product, and expected livelihood impact. Values in italics are spotlight analysis regression coefficients. ***p < .001, **p < .01, † p < .10.

Second, although there was no hypothesis in this regard, we contrasted the decision to access with the decision to own (Table 2B). Preference for the latter is positively influenced by income and attitude toward the product and negatively influenced by risk aversion. Access temporality does not affect preference for ownership over access (p = .20). However, a negative interaction effect is present, indicating that the effect of access temporality on ownership preference differs across income levels. The Johnson-Neyman technique shows that among respondents with an income of up to INR 16,070 (approximately USD 247), access temporality does not affect choice. Above this value, long-term access leads to a decrease in the likelihood of preferring ownership over access, which we found surprising. To better understand this result, Figure 4B displays the estimated probability of preferring ownership over access. Interestingly, greater access temporality increases access preference among respondents in the 90th income percentile.

Overall, in line with our assumptions, a large share of BoP respondents opts for nonconsumption if long-term access is offered. Mid-market respondents, in contrast, substitute access for ownership if the former is offered with a long-term policy, which represents an intriguing result.

Temporality Effect Mediation

We first analyzed a repeated-measures analysis of covariance for the three mediating variables to examine whether the differences across income levels are affected by access temporality. For affordability, the interaction between the within-subjects factor, income, and temporality is not significant, F(3,232) = 1.85, p = .14. For transaction utility, F(3,232) = 4.11, p < .01, and financial risk, F(3,232) = 6.04, p < .001, the three-way interactions are significant. Closer examination revealed that for affordability and financial risk, in line with Study 1, short-term access is perceived to be superior to ownership among BoP consumers. This difference is attenuated for long-term access. For transaction utility, the results again show a mixed picture. In line with the counterintuitive findings of Study 1, among mid-market consumers, short-term access is perceived to be inferior to ownership. Long-term access, however, is viewed by respondents in the fourth income quartile to have greater transaction utility than ownership.

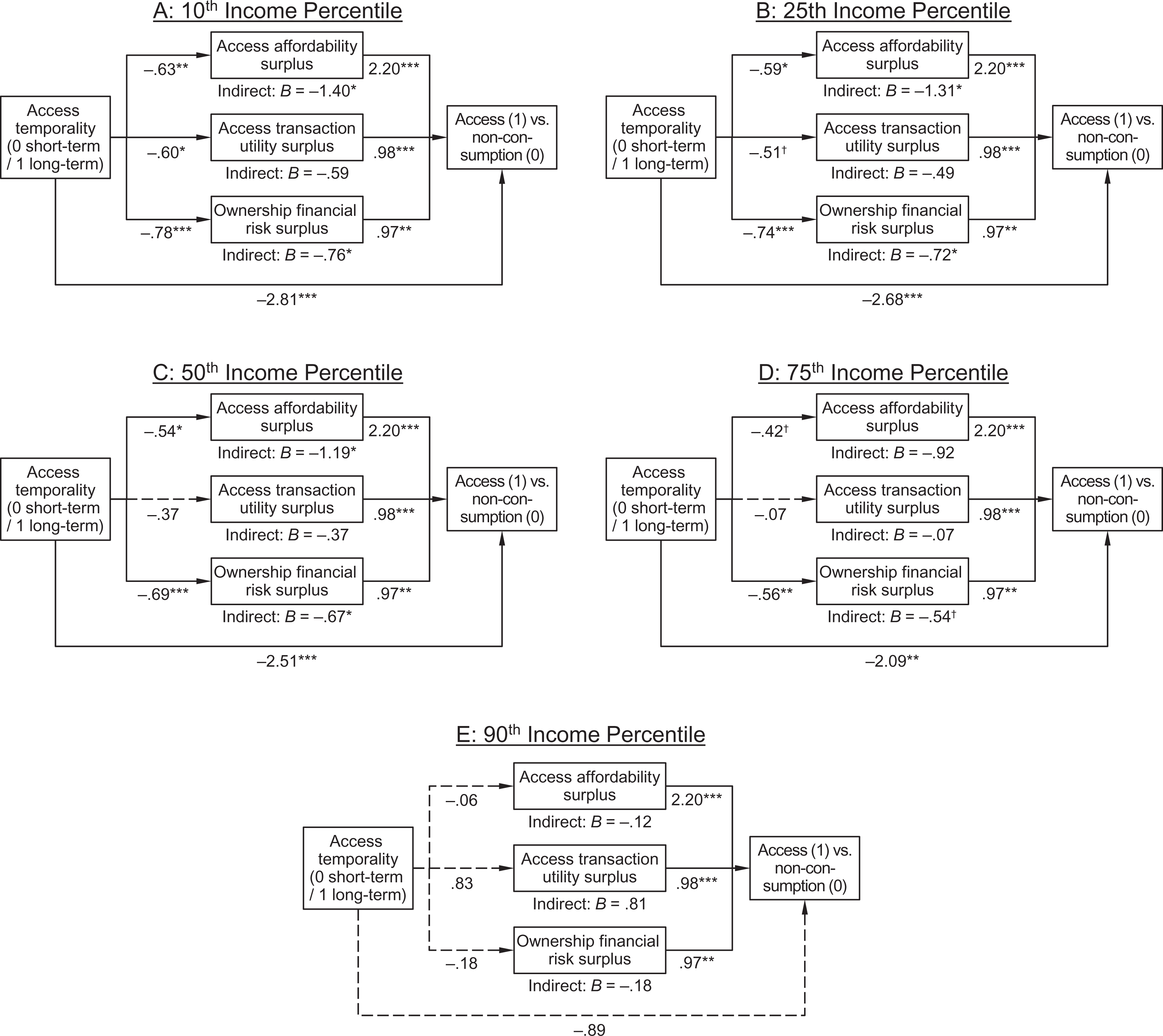

Second, to test the hypothesized moderated mediation, we analyzed a conditional process model (PROCESS model 8; 10,000 bootstrap samples; Hayes 2013). As in Study 1, we calculated access affordability and transaction utility surplus and ownership financial risk surplus for each respondent. 7 To explain differences in the reduction of preference for access over nonconsumption caused by greater access temporality at different income levels, we contrasted the two corresponding choice categories (access = 1; nonconsumption = 0). In line with the repeated measures results, significant interactions emerged for affordability (b = .00002, t = 1.73, p < .10), transaction utility (b = .00004, t = 1.96, p = .05), and financial risk (b = .000018, t = 1.82, p < .10).

Figure 5 illustrates spotlights of the mediations at different income levels. In the 10th (INR 2,800; approximately USD 44) and 25th income percentiles (INR 5,000; approximately USD 78), long-term access is perceived to have less of an expected utility advantage over ownership, as reflected in greater affordability and transaction utility, and lower financial risk. Consumers in the 50th percentile (INR 8,000; approximately USD 125) do not perceive short-term and long-term access to differ in transaction utility relative to ownership. For affordability and financial risk, the difference between the two access temporality conditions becomes nonsignificant in the 90th income percentile (INR 35,400; approximately USD 546). When comparing the indirect effects across income levels, it is important to note that the mediation via transaction utility does not reach the level of statistical significance. In contrast, affordability and financial risk mediate the effect of access temporality on access preference in the 10th through 75th income percentile (INR 15,000; approximately USD 232). Just as the direct effect decreases in magnitude at higher income levels, these indirect effects are attenuated. However, for both variables, the index of moderated mediation (Hayes 2015) is not statistically significant (affordability: index = −.000039; SE = .00004; 90% CI: [−.0001, .00003]/financial risk: index = −.000018; SE = .00002; 90% CI: [−.00005, .000006]). We thus only cautiously interpret the findings as evidence that the greater share of BoP consumers who opt for nonconsumption when long-term access is offered can be explained by longer temporality having less expected utility in terms of affordability and financial risk.

Study 2: Indirect effects of access temporality on access preference at different income levels. Note. Access affordability surplus represents the difference between affordability of access and of ownership. Access transaction utility surplus represents the difference between the perceived transaction utility of access and of ownership. Ownership financial risk surplus represents the difference between perceived financial risk of ownership and of access. Covariates included are age, gender, risk aversion, attitude toward the product, and expected livelihood impact. ***p < .001, **p < .01, *p < .05, † p < .1.

Discussion

Study 2 investigated BoP consumers’ reactions to access temporality. The results support the assumption that among BoP consumers, greater temporality reduces the preference for access and thus impedes its potential for reducing nonconsumption (Hypothesis 3). The hypothesized underlying process of long-term access reducing the expected utility advantage of access over ownership (Hypothesis 4) is only partially supported. We find that, among BoP consumers, the reduction in access preference caused by high temporality is explained by the perception that long-term access reduces the affordability of access compared to ownership and increases the financial risk.

Additionally, Study 2 provides intriguing insights into choice behavior among mid-market consumers. The exploratory analyses found that among these consumers, long-term access increases the probability of preferring access over ownership. This may indicate that, in contrast to BoP consumers, mid-market consumers value the reliability that comes with longer minimum rental periods.

General Discussion

Financial restrictions are one of the many challenges BoP consumers face, leading to a large share of nonconsumption. This especially applies to durables, due to their high price and the burdens of ownership. At the same time, many of these products may have a transformative impact. In this context, we have investigated whether access-based services are an acceptable option for BoP consumers to reduce nonconsumption.

Study 1 provides evidence that the availability of access-based services as an alternative to ownership reduces nonconsumption among BoP consumers. Moreover, we demonstrate that BoP consumers’ choice can be explained by utility maximization, reflected in greater affordability and lower financial risk of access relative to ownership. Interestingly, and in contrast to our assumption (H2c), BoP consumers do not consider access to provide greater transaction utility than ownership, which calls for more detailed investigations to better understand how “future” knowledge shapes expected utility at the BoP.

After establishing that access-based services can be transformative, Study 2 examined how such services should be designed to cater to BoP consumers’ needs. We found access temporality to be a determinant of nonconsumption reduction. In contrast to short-term access, long-term access elicits a similar propensity for nonconsumption among BoP consumers to that seen when only ownership is available. These reactions are again explained by differences in expected utility, as BoP consumers perceive long-term access to be more similar to ownership in terms of affordability and financial risk.

Additionally, the results for mid-market consumers provide interesting insights. Study 1 indicated that for these consumers, ownership offers greater transaction utility than access. This may indicate that, without severe resource restrictions, the benefits of freely using an owned product are valued more highly than when there are resource restrictions. Additionally, Study 2 showed that greater access temporality makes mid-market consumers replace ownership with access, which may indicate a desire for flexible but reliable ways of using a product, as supported by prior studies in industrialized markets (Lamberton and Rose 2012).

Theoretical and Methodological Contributions

Our work offers at least five main contributions. First, by investigating access-based services in a BoP context, we provide empirical evidence for the idea of reducing nonconsumption at the BoP. Although this link had been conceptualized (e.g., Karnani 2007; Lovelock and Gummesson 2004), existing studies have considered ownership as the only alternative to nonconsumption (e.g., Christensen, Johnson, and Rigby 2002; Ojomo 2016). To the best of our knowledge, our investigation provides the first evidence that shortcomings in well-being, exemplified by high rates of nonconsumption, may also be addressed by offering temporary access to goods. We thereby contribute to the BoP literature, specifically regarding poverty-related resource restrictions (e.g., Hill and Stephens 1997), which has predominantly focused on ownership and possessions (e.g., Hart and Christensen 2002; Nakata and Weidner 2012).

Second, by examining the underlying process of expected utility assessment and utility maximization, our results expand the knowledge of the decision processes of BoP consumers. Although utility maximization has periodically been used to explain individuals’ behavior at the BoP (e.g., Bekele and Drake 2003), our investigation of knowledge immediacy and uncertainty provides a more detailed understanding of expected utility assessment processes.

Third, the investigation of access temporality provides empirical findings for one of the key distinctions between ownership and access (Bardhi and Eckhardt 2012), which had been overlooked in prior studies. Our investigation shows that temporality directly affects consumers’ perceptions of access-based services and their subsequent choices.

Fourth, we do not assign consumers to the BoP based on a single, fixed income threshold but rather examine effects across different income levels. In light of the ongoing discussion about arbitrary thresholds (London, Anupindi, and Sheth 2010), we thus offer a more nuanced examination.

Fifth, by conducting an experimental study at the BoP in rural areas of India, our research goes beyond existing methodological approaches, as most previous studies in this context have drawn samples from metropolitan areas or focused on qualitative methods (e.g., case studies).

Managerial Implications

Enabling access to goods represents a key strategy for companies to successfully target BoP consumers (Hammond et al. 2007). By examining the potential demand for access-based services at the BoP, our findings contain implications for companies and for public policy makers.

It is frequently suggested that companies targeting the BoP should seek ways to compete against nonconsumption (e.g., Hart and Christensen 2002). Our findings show that offering access-based services instead of trying to sell ownership is one way to tap into BoP markets. Additionally, such strategies may also be economically viable, as shared access to a good should increase the revenue per dollar of investment in the underlying asset (Prahalad and Hammond 2002).

Furthermore, our findings are relevant for service providers and public policy makers evaluating the applicability of access-based services for livelihood improvement. Access-based services may reduce budget constraints, thereby making monetary resources available for expenses that add to better living conditions, such as education or medical care.

The finding that long-term access is not successful in reducing nonconsumption has direct implications for service providers. Specifically, from the standpoint of BoP consumer perceptions, companies should offer short-term access. However, for service providers, the decision to offer shorter minimum rental periods reduces the predictability of asset usage and thus needs to be made in conjunction with cost considerations in order to create a sustainable business model. It is also important to note that a short-term focus reduces acceptance among mid-market consumers.

Finally, our results indicate how BoP consumers evaluate access and ownership when making purchase decisions. When addressing this market segment, service providers should thus consider their services’ superiority over ownership in terms of affordability and financial risk and should clearly communicate this.

Limitations and Future Research

When interpreting the empirical results, certain limitations should be considered. First, both studies employed written scenario techniques and were based on self-reported data and stated choices and perceptions. Future research should examine BoP consumers’ behavior with regard to access-based services.

Second, we used income as a measured variable, which only allows for correlational interpretations. For instance, expected and actual income increases may affect BoP consumers’ decision between nonconsumption, access, and ownership, which should be considered in future studies.

Third, for our investigation of the underlying process and the examined variable of access temporality, we considered only elements related to financial aspects of access-based service use. At the same time, however, Hazée, Delcourt and Van Vaerenbergh (2017) show that various nonmonetary aspects may prevent consumers from using such services as well. Future studies should thus examine how these burdens of access affect BoP consumers.

Fourth, our studies did not account for the long-term livelihood improvement effects of access and ownership. The prolonged use of an access-based service might cause the accumulated fees to exceed the purchase price of the accessed product (Durgee and O’Connor 1995), which may explain why access is not perceived to have greater transaction utility than ownership. Future studies should thus consider possible detrimental effects of access.

Supplemental Material

Supplemental Material, ABS_for_the_BoP_-_Executive_Summary - Access-Based Services for the Base of the Pyramid

Supplemental Material, ABS_for_the_BoP_-_Executive_Summary for Access-Based Services for the Base of the Pyramid by Tobias Schaefers, Roger Moser, and Gopalakrishnan Narayanamurthy in Journal of Service Research

Supplemental Material

Supplemental Material, Access-Based_Services_for_the_BoP_-_Web_Appendix - Access-Based Services for the Base of the Pyramid

Supplemental Material, Access-Based_Services_for_the_BoP_-_Web_Appendix for Access-Based Services for the Base of the Pyramid by Tobias Schaefers, Roger Moser, and Gopalakrishnan Narayanamurthy in Journal of Service Research

Footnotes

Appendix A

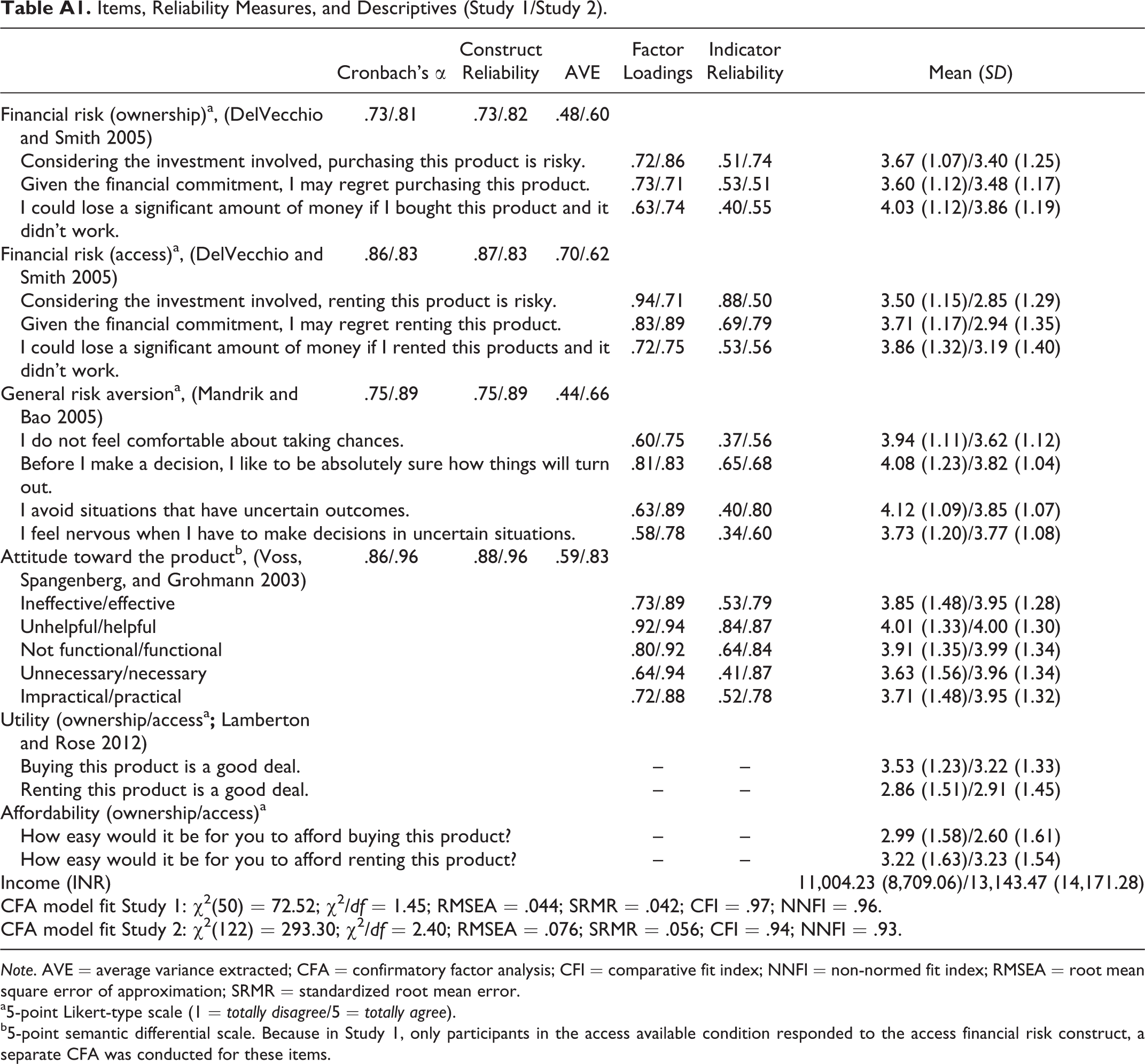

Items, Reliability Measures, and Descriptives (Study 1/Study 2).

| Cronbach’s α | Construct Reliability | AVE | Factor Loadings | Indicator Reliability | Mean (SD) | |

|---|---|---|---|---|---|---|

| Financial risk (ownership)a, (DelVecchio and Smith 2005) | .73/.81 | .73/.82 | .48/.60 | |||

| Considering the investment involved, purchasing this product is risky. | .72/.86 | .51/.74 | 3.67 (1.07)/3.40 (1.25) | |||

| Given the financial commitment, I may regret purchasing this product. | .73/.71 | .53/.51 | 3.60 (1.12)/3.48 (1.17) | |||

| I could lose a significant amount of money if I bought this product and it didn’t work. | .63/.74 | .40/.55 | 4.03 (1.12)/3.86 (1.19) | |||

| Financial risk (access)a, (DelVecchio and Smith 2005) | .86/.83 | .87/.83 | .70/.62 | |||

| Considering the investment involved, renting this product is risky. | .94/.71 | .88/.50 | 3.50 (1.15)/2.85 (1.29) | |||

| Given the financial commitment, I may regret renting this product. | .83/.89 | .69/.79 | 3.71 (1.17)/2.94 (1.35) | |||

| I could lose a significant amount of money if I rented this products and it didn’t work. | .72/.75 | .53/.56 | 3.86 (1.32)/3.19 (1.40) | |||

| General risk aversiona, (Mandrik and Bao 2005) | .75/.89 | .75/.89 | .44/.66 | |||

| I do not feel comfortable about taking chances. | .60/.75 | .37/.56 | 3.94 (1.11)/3.62 (1.12) | |||

| Before I make a decision, I like to be absolutely sure how things will turn out. | .81/.83 | .65/.68 | 4.08 (1.23)/3.82 (1.04) | |||

| I avoid situations that have uncertain outcomes. | .63/.89 | .40/.80 | 4.12 (1.09)/3.85 (1.07) | |||

| I feel nervous when I have to make decisions in uncertain situations. | .58/.78 | .34/.60 | 3.73 (1.20)/3.77 (1.08) | |||

| Attitude toward the productb, (Voss, Spangenberg, and Grohmann 2003) | .86/.96 | .88/.96 | .59/.83 | |||

| Ineffective/effective | .73/.89 | .53/.79 | 3.85 (1.48)/3.95 (1.28) | |||

| Unhelpful/helpful | .92/.94 | .84/.87 | 4.01 (1.33)/4.00 (1.30) | |||

| Not functional/functional | .80/.92 | .64/.84 | 3.91 (1.35)/3.99 (1.34) | |||

| Unnecessary/necessary | .64/.94 | .41/.87 | 3.63 (1.56)/3.96 (1.34) | |||

| Impractical/practical | .72/.88 | .52/.78 | 3.71 (1.48)/3.95 (1.32) | |||

| Utility (ownership/accessa

|

||||||

| Buying this product is a good deal. | – | – | 3.53 (1.23)/3.22 (1.33) | |||

| Renting this product is a good deal. | – | – | 2.86 (1.51)/2.91 (1.45) | |||

| Affordability (ownership/access)a | ||||||

| How easy would it be for you to afford buying this product? | – | – | 2.99 (1.58)/2.60 (1.61) | |||

| How easy would it be for you to afford renting this product? | – | – | 3.22 (1.63)/3.23 (1.54) | |||

| Income (INR) | 11,004.23 (8,709.06)/13,143.47 (14,171.28) | |||||

| CFA model fit Study 1: χ2(50) = 72.52; χ2/df = 1.45; RMSEA = .044; SRMR = .042; CFI = .97; NNFI = .96. CFA model fit Study 2: χ2(122) = 293.30; χ2/df = 2.40; RMSEA = .076; SRMR = .056; CFI = .94; NNFI = .93. | ||||||

Note. AVE = average variance extracted; CFA = confirmatory factor analysis; CFI = comparative fit index; NNFI = non-normed fit index; RMSEA = root mean square error of approximation; SRMR = standardized root mean error.

a5-point Likert-type scale (1 = totally disagree/5 = totally agree).

b5-point semantic differential scale. Because in Study 1, only participants in the access available condition responded to the access financial risk construct, a separate CFA was conducted for these items.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.