Abstract

This article analyzes the effects of diversification and brand breadth on firm performance for professional service firms (PSFs). The research aim is two-fold. First, we test whether moving into products may put at risk the core resources that sustain PSFs’ competitive advantage. Second, we study which branding strategies best match their diversification attempts. Broad (narrow) brands characterize a branding strategy with scarce (plentiful) associations to specific product characteristics. We analyzed trademark portfolios of 47 U.S.-based management consulting firms in the 2000 to 2009 time period. Panel regression results suggest that (1) PSFs always benefit from diversification when they remain pure-service providers; (2) performance is positively related to a strategy of specialized narrow brands.

Is diversification a growth strategy that increases performance for professional service firms (PSFs)? As far as service firms are concerned, PSFs are at the extreme end of the intangibility range (Amonini et al. 2010) because their main input and output is knowledge (von Nordenflycht 2010). This knowledge is embedded in specialized services such as consultancy, usually developed and delivered by highly skilled employees. Thus, PSFs display typical service firm characteristics like high labor intensity, low capital investment, and customized offerings (Miles 1993), which correspond to low fixed and high marginal costs with scarce economies of scale and scaling-up incentives. Although we might expect an extreme fragmentation of offerings and markets dominated mostly by small firms, instead, we see the emergence of large companies in PSF sectors, such as in accountancy (Suddaby and Greenwood 2001), management consulting (Sarvary 1999), and advertising (von Nordenflycht 2011), as well as increases in market concentration. This evidence is puzzling and prompts the research question: what mechanisms are allowing some PSFs to grow successfully, despite the apparent lack of opportunities from economies of scale?

We tackle this question by combining theoretical insights from the resource-based view of the firm (Helfat and Eisenhardt 2004; Stiglitz 2000; Teece 1982) and information economics (Nayyar 1990). Our aim is to explain the growth path of diversified PSFs consistent with recent specialized business media debates on how some PSFs are able to exploit their intangibles through diversification. According to the resource-based view, the primary sources of a firm’s competitive advantage are intangible, unique, and difficult to imitate resources (Denrell, Fang, and Winter 2003; Foss, Lyngsie, and Zahra 2013). These resources are also often deployable in a wide range of end applications (Eggers 2012; Gruber, MacMillan, and Thompson 2008). For PSFs, an important step in diversification is moving from pure service to product diversification (Brivot 2011). As this move represents an important tilting point for PSFs with managerial relevance, we argue that this contingency is key when studying performance through diversification. In this context, the release of a physical product should be seen as the release of a software-related product that is coded and reproducible, implying a transition from a labor-intensive offering to a more capital intensive one. Christensen, Wang, and van Bever (2013) suggest that PSF sectors, in particular management consulting, are on the verge of a major “product” disruption due to the new possibilities offered by information and communication technologies; De Man, de Man, and Stoppelenburg (2016) describe the emergence of new business models where consulting firms are moving away from the traditional pure-service provision model. However, the performance implications of this diversification process are still unexplored.

The second aspect we discuss is how PSFs should brand their offerings during the diversification processes. The severe information asymmetries in PSF markets present opportunities for firms to strategically position and market their offerings with a strong reputational image (Kotler, Hayes, and Bloom 2002; Nayyar 1990). Consumers, unsure about the quality of an offer due to the lack of tangible attributes, will use the brand with its attached meaning as a decision anchor. When firms diversify, they choose a single broad brand or multiple narrow brands. On the one hand, the intangibility of services and their “credence” characteristics (Nayyar 1990) can push PSFs to focus on a single brand, that is, the company name that captures the firm’s overall reputation (De Chernatony and Riley 1999). On the other hand, PSFs can also successfully develop multiple subbrands to market diverse services (Rahman and Areni 2014). If reputation and trust are key variables, should PSFs employ the same broad brands to market different products and services? Or bet on various narrow brands that are product/service-specific? We argue that the distinction between PSFs offering pure services versus tangible products is key for solving this dilemma. Our two main research questions are therefore:

Empirically, we select a set of PSFs as our test sample, namely, 47 U.S.-based management consulting firms, and analyze their performance in the 2000 to 2009 time period. We capture these PSFs’ diversification and brand dimensions from their trademark portfolios. Trademarks are the legal counterparts of brands that firms can use to identify unique products or services and advertise in markets. Semadeni (2006) shows, for the specific case of management consulting, that trademarks contain information on firms’ marketing strategies.

Our first main finding is that PSFs always benefit from diversification if they merely add new services. The truly unrelated diversification that exposes the pitfalls of diversification is the addition of product offerings. We argue that this diversification to products undermines PSFs’ strategic positioning as providers of expert knowledge. This finding contributes to the diversification literature by showing the performance implications of diversification for service firms with a high level of intangibility in both input and market output. Compared to recent works on diversification, this article is closely aligned to the relatedness debate (see Neffke and Henning 2013).

As regards studies focusing on PSFs (Hitt et al. 2006, on law firms; Greenwood et al. 2005, on accountancy firms), we complement their tests on the impact of diversification by considering diversification into products as well as services. In terms of managerial importance, this article shows that for PSFs, the transition from service to products, given the different level of codification involved, could be a significant threshold that divides negative (or null) from positive performance outcomes. We suggest that the impact of diversification depends on a contingency (services vs. products) related to the codification and visibility of tangible attributes.

The second key finding is that a strategy of narrow brands fits pure-service PSFs better than a broad brand strategy. This result provides a novel take in the understanding of service marketing for diversified PSFs. While some authors (Amonini et al. 2010; Rahman and Areni 2014) acknowledge that brands are key in PSF contexts where customers run a high risk of making an incorrect decision (Hill and Neeley 1988), evidence on the effect of branding is still limited (Berry 2000). Our contribution relies on insights from the economics of information theory already applied in marketing studies (Zhang et al. 2015), but not yet to PSFs. Our finding that pure-service PSFs’ performance is enhanced by narrow brands somewhat contradicts the expectation from prior studies that reputation-driven markets favor one single broad brand (Amonini et al. 2010). Instead, we argue that pure-service PSFs have strategic incentives to provide targeted information signals to customers in new segments by using narrow brands.

Concerning the empirical side, using trademarks as a proxy of product/service and brand strategies enables us to present results from a panel data set, also accounting for some endogeneity issues. This advances the nascent research on trademarks as a valuable proxy in social science research (Mendonça, Pereira, and Godinho 2004; Schautschick and Greenhalgh 2016). Moreover, using trademark registrations means we can track companies’ actual actions. This responds to the call by Amonini et al. (2010) for more research on the competitive positioning of service firms relying on actual actions.

Theory and Hypotheses

Emergence and Consolidation of PSFs

PSFs are a quintessential example of organizations whose performance is driven by resource-based strategies. The resource-based view of the firm (Barney 1991; Grant 1996) dictates that firms’ intangible resources are often the major determinants of competitive advantage and performance potential. For PSFs, intangible resources in the form of knowledge are not only their major production input but also a main component of their, often intangible, output.

The emergence of PSFs is part of the structural transformation of industrialized economies to knowledge economies, where firms’ comparative advantage has come to lie around their ability to skillfully manage intangibles rather than tangible capital (Starbuck 1992). Service firms that rely significantly on knowledge and human capital are at the heart of this phenomenon (Miles 1993): Their output is intangible and can neither be stored nor easily transferred; service production is not capital intensive, whereas service output is often coproduced with clients’ interaction and thereby customized rather than standardized. Such properties explain why these firms typically rely less on traditional economies of scale from production (Miles 1993; von Nordenflycht 2010). While novel communication technologies have spurred major advances in the degree to which services can be standardized, codified, and also transferred (Miozzo and Soete 2001), high-end services, such as those offered by consulting firms, still strive to maintain personalization and customization while enjoying the efficiency benefits of codification and standardization (Hansen, Nohria, and Tierney 1999). All this reasoning suggests that PSFs have scarce incentives to scale-up operations (Christensen, Wang, and van Bever 2013). Moreover, there are additional constraints to performance when the production output is also intangible and it is difficult to evaluate ex ante due to uncertainty and asymmetric information (Denrell, Fang, and Winter 2003; Foss, Lyngsie, and Zahra 2013). Nevertheless, about 31% of the Top 500 in the 2016 INC. list of 5,000 fastest-growing private companies in the United States are classifiable as PSFs (http://www.inc.com/inc5000/list/2016/). This has fueled literature on the drivers of performance and growth for PSFs.

Diversification and PSF Performance

von Nordenflycht (2011) suggests that the growth of PSFs goes hand in hand with increasing diversification. He observes how a process of size matching between clients and suppliers characterizes the evolution of many knowledge-intensive industries, with large and diversified companies serving large clients and small companies serving small clients. The very large companies combine the ability to coordinate large projects and provide whole packages of diversified services that satisfy the complex needs of large clients. In this respect, diversification is important for PSFs’ performance mainly because of demand forces. Other studies in different contexts have also offered demand-based explanations of diversification benefits, including one-stop-shop considerations (Brush, Dangol, and O’Brien 2012; Greenwood et al. 2005), and in general economies of scope in consumer utility (Kuruzovich et al. 2013; Ye, Priem, and Alshwer 2012).

Compared to manufacturing companies, performance is linked to the ability of PSFs to create value, more than to capture it, because the benefits of diversification will be in sales volumes (more customers or higher prices) with scarce efficiency gains linked to economies of scope in production (Greenwood et al. 2005).

From a resource-based perspective, intangibles are sunk investments with redeployable characteristics that naturally lead to diversification (Gruber, MacMillan, and Thompson 2008; Helfat and Eisenhardt 2004; Teece 1982, 1986). Yet, for PSFs, intangible resources like human capital skills are often tacit because they are practice based and the outcome of a routinization process (Dougherty 2004). Thus, PSFs that aim to redeploy their intangible resources in other contexts must attempt codification because knowledge should be replicated in order to be transferred (Kogut and Zander 1992). The intensity of codification is therefore a strategic decision with several degrees of freedom; PSFs that scale up and apply knowledge resources to different markets will adjust codification strategies according to their optimal replication-based economies (Hansen, Nohria, and Tierney 1999). However, a crucial stage in PSFs’ codification efforts is when they decide to move from services to tangible products (Brivot 2011). Products with tangible attributes are, by nature, based on more codified and visible characteristics. For example, the Management Consulting Group has developed Ascertain®, a revenue management and process evaluation toolset: The software analyzes, monitors, and links data from different sources and networks within a firm across operational and business support systems and inventories. This product is the outcome of a codification process that allowed the company to move from a business model based on consultancy services to one based more on product licensing revenues.

If we focus on the input side, adding products to services represents a related diversification because firms replicate the same key knowledge for targeting (often) the same customers (Neffke and Henning 2013; von Nordenflycht 2011). However, the realization of tangible products forces firms to adopt a more formal codification that could generate trade-offs. The availability of tangible offerings renders information in the marketplace less asymmetric, which in turn diminishes PSFs’ ability to defend their source of sustainable comparative advantage. Tangible products that allow customers to produce their own solution can eventually cannibalize the professionals-embodied competencies (Roberts and McEvily 2005). This is a key point in our theory. For PSFs, diversification toward products could undermine the strategic resources that primarily define the value proposition of PSFs in the marketplace. Their reputation is precisely based on tacit professionals-embodied competencies that diversification could render more visible and codified (Neffke and Henning 2013), reducing their nonimitability and nonsubstitutability (Barney 1991) and their value creation potential accordingly.

We therefore propose the following hypothesis:

Branding and Performance

Services are the quintessential example of experience goods, whose quality can only be evaluated after consumption, and some services can even be credence goods, if their ex post evaluation is complex or even impossible (Dolfsma 2011; Nayyar 1990). In sum, information asymmetries are particularly high (Skagg and Snow 2004; Starbuck 1992). In this respect, PSFs face challenges when promoting, protecting, and leveraging their intangible resources. Consumers who cannot rely on previous experience for making an informed decision typically depend instead on a firm’s reputation (Fombrun and Shanley 1990). Brands are a classic tool on which a firm’s reputation rests (Brown and Dacin 1997); therefore, the information a brand conveys can be key to reducing uncertainty over the quality of a service and its provider (Bharadwaj, Varadarajan, and Fahy 1993).

Branding, as a specific form of communication, fulfills different roles. It lowers transaction costs in the market by reducing uncertainty about some of the provider’s properties during an information search (Sappington and Wernerfelt 1985). It also works as an appropriation tool since it helps to distinguish and identify the product/service in the market. Thereby it forms barriers to entry (Lancaster 1990). Branding increases customer loyalty, thereby strengthening a company’s reputational assets. In terms of systematic empirical evidence, strong brand equity is related in the literature to higher consumer awareness, higher company performance, and higher financial returns (Keller and Lehmann 2006).

Branding research on PSFs is still in its infancy and there is no consistent evidence of how brands impact PSF performance (Rahman and Areni 2014). Feldman Barr and McNeilly (2003) show that not all PSFs are able to use branding strategically to create a competitive edge. From a strategic point of view, we expect reputation building to be a key driver of PSFs’ performance thanks to the inherent properties of their business: “Most service organizations will depend upon the associations stakeholders make with their corporate names” (Davies, Chun, and Kamins 2010, p. 530). This is crucial because if diversification is a common phenomenon for PSFs, we could ask how branding adapts and translates into actual strategies.

We can define PSFs’ branding strategies according to their brand breadth. On the one hand, PSFs may focus on one (or a few) consolidated brands that can be extended when diversification takes place, hence bet on broad brands. This strategy is usually realized through names and logos that identify an emotional awareness linked to firm name and image (Keller 1993; Krasnikov, Mishra, and Orozco 2009). On the other hand, PSFs can create brands that contain specific information on product/service attributes, generating a portfolio of specialized narrow brands. In practice, there will be a continuum of branding strategies to complement diversification.

Broad brands may be a tool to charge premium prices or boost demand: Companies that risk their name may be rewarded by customers who act on the belief that those companies would do their best to deliver the value that they promise. In fact, brand extension strategies tend to be positively evaluated by market analysts (Block, Fisch, and Sandner 2014).

However, broad brands might expose firms to more risks: firstly, in cases of negative publicity due to failures in diversification attempts. Termination, culls, and recalls of products/services marketed with brands used for other products/services backfire on brand image (Cleeren, van Heerde, and Dekimpe 2013). Secondly, by using the same brand, firms may apply some niche-specific resources to antagonist niches, creating negative externalities. For example, it could be very difficult to sell under the same brand a service directed at environmentally concerned customers and polluting companies. The extension of a brand to different markets might be beneficial for service firms, but only if it is considered “legitimate” by the market (Nayyar 1990), that is, there might be important market constraints to brand extensions. For the specific case of management consulting firms, Greenwood et al. (2005) even talk about “reputation stickiness”: Given the complex and abstract nature of services offered, corporate clients do not easily extend a firm’s reputation from one service to another. Semadeni (2006) argues that PSFs embed a tension between branding radically new offerings to differentiate themselves from competitors and sticking to their core mission to increase their legitimacy and alignment to the sector’s professional norms. When information asymmetries are strong, legitimacy is an important asset for firms. Hence, firms will prefer to have narrow brands that are very specific to the targeted product/service segment.

Clearly, the previous arguments apply to the specific conditions encountered by typical PSFs marketing their knowledge-intensive expert services. As soon as PSFs include products in their offerings, they are giving away tangible characteristics from which customers can extract clues on quality. Thereby consumers are also able to compare those clues with the firm’s reputation conveyed through brands. This reduces the asymmetric information in the market, relaxing the importance of brands as signals.

In sum, the final impact depends on how brands could be leveraged to support higher premium prices or an increasing demand in markets plagued by asymmetric information between firms and consumers. While a similar argumentation in terms of value creation applies to product firms, we argue that the information asymmetries are much stronger in the markets where PSFs are active, given the “credence” nature of PSFs (Nayyar 1990). Thus, we propose these two contrasting hypotheses:

Empirical Analysis

Sample

For our sample, we select public companies from Bureau van Dijk’s Osiris database within Standard Industrial Classification (SIC) code 874, 1 that is, management and public relations service firms. We choose U.S. companies to ensure comparability in terms of trademark numbers and cultural approaches (Giarratana and Torrisi 2010). We focus on the organic growth of these organizations, that is, excluding mergers and acquisitions, thus avoiding the confounding effects of financial mergers. Trademarks can change owner when sold or acquired by companies. The U.S. Patent and Trademark Office (USPTO) database details changes in ownership if the acquirer maintains a brand without a stand-alone subsidiary. If after acquisition, a subsidiary remains independent, it will maintain the ownership of the brand. We only consider the trademarks registered and owned by the companies in our sample without grouping for holding ownership. We further limit our analysis to public companies in order to have valid financial data; finally, we select companies that owned at least one live trademark during the sample period. It turns out that 47 firms fulfilled this condition. In other words, we fine-tune our sample in order to consider only PSFs with a high visibility, press coverage, and whose brands had reached a legitimacy level that needs formal trademark protection from potential imitators. These selection criteria are also in line with the conceptual focus of our article. We do not attempt to explain how PSFs build reputational assets, rather to understand how they use them to counteract the typical challenges of information asymmetry in their markets.

We use four accounting variables from the Osiris database: (a) the total number of employees, (b) turnover, (c) total assets, and (d) cost of goods sold. We take data for the years 2000 to 2009, thereby constructing a balanced panel data set. Wherever the Osiris variables for turnover and number of employees are missing, we drop the entire observation for that specific company and year and keep only the complete ones, resulting in a total of 172 observations.

For each company, we collect the trademarks registered at the USPTO. Trademarks are combinations of “words, phrases, symbols, or designs that identify and distinguish the source of the goods or services” (USPTO Documentation, http://tess.uspto.gov). Firms can register as a trademark a new firm name, a name of a product, a jingle, a slogan, a new image, or a logo. In this way, they secure legal protection for their investment in marketing and reputation (World Intellectual Property Organization 2013). Even though trademarks do not protect against the imitation of the product per se, they do help to create a barrier to imitation because they prevent a similar product with a similar name or brand being sold in the same market. Trademark owners pay different fees for each class of goods or services for which a trademark is registered, and they have to prove periodically that they are using the trademark in the relevant market; even if the owner is willing to pay the fees, a trademark is canceled if it is not commercially used for 5 consecutive years after registration. Academic interest in trademarks has only recently emerged. Previous studies show that trademarks represent a good proxy for the products and markets in which a firm operates and that they are correlated with performance measurements and stock market value (Fosfuri and Giarratana 2009; Krasnikov, Mishra, and Orozco 2009). While trademarks are clearly related to advertising investments, they do not capture marketing strategies equally well across different sectors (Flikkema, De Man, and Castaldi 2014). Information available on a trademark is the extent to which firms decide to register names, logos, words, or phrases; the product categories protected; and the registration/filing and cancellation/abandon dates.

We collect data from USPTO’s Trademark Electronic Search System database. Trademarks are assigned to 45 international classes (ICs) and 60 U.S. product classes. For each trademark, the IC tends to be unique (one class per trademark) and identifies the primary product category where the product or service is marketed. The U.S. classification is an older system that represents the product categories to which the brand could be extended and is still kept by the USPTO as a secondary system next to the international one (Graham et al. 2013). Each trademark is usually linked to several U.S. classes starting with the goods and service description provided by the applicant. The more complex the good and service description, the more U.S. classes that are assigned to a trademark. IC and U.S. classes thus provide different information: The unique IC code identifies the type of product/service underlying the trademark, whereas the multiple U.S. codes indicate the breadth of the trademarks, that is, the product/service classes potentially covered by the same trademark. 2 It is also important to mention that the U.S. classification is not independently produced by the USPTO office. It is a classification constructed from the analysis of the standardized key words that trademark applicants at the USPTO have to use to describe the goods and services covered by the trademark. 3 Thereby, U.S. classes capture information directly provided by companies on the breadth of their trademark.

Dependent Variables

To test our hypotheses, we aim to fit a model with performance as the key dependent variable and a vector of independent variables related to diversification and brand breadth. We measure performance with the ratio of total sales and employees as in Greenwood et al. (2005):

Given that PSFs rely strongly on their human capital as their main intangible asset, considering sales per employee is a good indicator of their potential performance (Lorsch and Tierney 2002). Our measurement is also in line with the diversification literature, where the typical dependent variable concerns measurements of sales, to avoid confounding effects due to efficiency gains at corporate level (Zahavi and Lavie 2013). We also check the correlation of our measurement with two classic indicators of profitability, returns on sales (ROS) and capital turnover (CT). ROS and CT are the two components of the return on investment (ROI = ROS × CT), in which ROS is more of a measure of value capture and efficiency, while CT is more of a measure of value creation [CT = sales/(fixed assets + working capital)]. We find that our dependent variable is significantly correlated (p value = .006) to CT, but not to ROS (p value = .287); this means that, consistently with our theory on PSFs, our dependent variable captures more value creation processes than value capture and efficiency.

Independent Variables of Theoretical Interest

Diversification

The USPTO usually assigns each trademark to a unique IC product/service class that determines the goods or services on which the mark is used. There are 34 product categories and 11 service categories. For each firm, we know how many live trademarks in the different ICs the firm owned in a certain year, i. We then calculate a Herfindahl index for each firm at time, t. Such a concentration index takes a maximum value of 1 when all trademarks are registered in the same IC and a minimum value of 1/N, with N equal to the number of ICs available, when each class is covered by one trademark. Nineteen ICs appear in our sample, and given the problem of small sample bias, we follow the standardization suggested by Hall (2005), adopting the following formula:

Note that for a straightforward interpretation, we insert a negative sign at the beginning so that a higher diversification variable means a firm’s diversification is higher.

Brand breadth

Even if assigned to a unique IC product/service class, each trademark is classified by the USPTO into one or more of 60 different U.S. product and service classes. U.S. classification is based on the detailed description of the products and services that trademark applicants are asked to file at each trademark application. The more U.S. classes of a trademark, the more the underlying brand can potentially be extended to different product and service domains. We then calculate a Herfindahl index of concentration for the U.S. classes covered by the portfolio of live trademarks for each firm in each year. We standardize it according to Hall (2005) to avoid small sample bias, given that the number of U.S. classes in our sample is M = 39. Thus, our measurement reads

Note that we insert a negative sign at the beginning so that the broader the brand, the higher the potential extensions of a firm’s brand portfolio. Sandner and Block (2011) use a similar measurement as a proxy for the value of trademarks: The higher the breadth, the higher the costs, which implies that the company is investing more in protecting that trademark. This is confirmed by Melnyk, Giarratana, and Torres (2014), who show that broader brands are less likely to be abandoned.

Controls

A common concern when estimating firm-level models is that samples might include firms with very different strategic positions. To allow for this heterogeneity, we include several firm-level controls and rely on estimations including firm-fixed effects.

The first control is the firm’s lagged performance, which accounts for autocorrelation in firm-specific processes:

Firms in our sample also have different strategies when it comes to trademark filing. We count the number of live trademarks owned by each firm in each year and standardize them by firm size, proxied by the number of employees. The stock of trademarks changes annually because some trademarks “die” and new ones are registered. This variable allows controlling for brand proliferation according to the size of the firm. We take the logarithm of this ratio and define it in such a way that the brand intensity i,t is 0 if the company does not own any live trademarks in that year:

We further control for the size of the company by controlling for its total assets.

We also control for the total costs to avoid the following potential bias: If firms with higher growth rates have to pay higher costs in terms of wages for better skilled employees, the implied growth strategy is not sustainable in the long term. We also include the squared costs to control for nonlinear effects.

Given the many missing values in the data on costs (382 of the 470 data points are missing), we turn missing values into 0s and add a dummy for missing costs.

Regression Methods

We perform panel regression estimations. A major issue to bear in mind is that the two main variables of theoretical interest (diversification and brand breadth) are highly correlated. We then resort to regression models with instrumental variables (IVs). IV estimators exist also for panel data models and can be estimated in Stata version 11 by relying on the xtivreg and xtivreg2 routines (Baum, Schaffer, and Stillman 2007; Schaffer 2010). The main idea behind instrumentation is to find exogenous variables that act as proxies for the endogenous regressors and are at the same time not correlated with other variables (Campa and Kedia 2002). In our case, we choose to instrument firm brand breadthi,t with three additional variables: These three instruments are expected to correlate with brand breadth but not with diversification.

The first instrument is prestige i,t . This variable is constructed from information compiled by market research company Vault. Rankings of the most prestigious U.S. consulting companies are available for the years 2006 to 2010 (http://www.vault.com/company-rankings/consulting/best-consulting-firms-prestige/). Vault bases its rankings on evaluations by consultants, not customers, which ensures they are independent of typical brand value measurements. Given that the list includes 50 firms, our variable is defined as 50-rank+1. The variable is set at 0 if the company does not appear at all on the list that year. Nine companies in our sample appear at least once in the ranking. The instrument captures the part of firm performance directly influenced by brand awareness, with no connection to product strategies.

The second instrument is patents i ,t . This variable is constructed by collecting information from the USPTO on patents filed by the companies in the years considered. Fourteen companies in our sample applied for at least one patent. The idea behind this instrument is that filing patents signals a greater ability by firms to manage the formal protection of their intangible assets (i.e., also trademarks), with all the associated legal requirements.

The third instrument is trademark age i,t : this variable is calculated as the average age of live trademarks in each firm’s portfolio in each year. Older trademarks might have a greater chance of being used for several products/services. If a company’s portfolio includes older trademarks, this might correlate with its reliance on the same names, thus affecting brand breadth, but not diversification. As mentioned above, to account for cross-firm heterogeneity, we include firm-level controls and firm-fixed effects. 4

To take into account the different effects of diversification within service sectors as compared to physical products, we run two additional regressions after dividing the data into two subsamples. The first regression accounts for the firms that have not released at each time t any physical product (pure-service cases). We do so by selecting cases where the entire portfolio of live trademarks owned by firm i in year t only covers service ICs, that is, in the 35 to 45 range. The second additional regression covers firms that at time t had already released a physical product in the market. Operationally, their trademarks cover at least one product class, that is, one class in the 1 to 34 range. We should note that the Nice Agreement, which produced the international Nice Classification, states, “A service is any activity or benefit that one party can offer to another that is intangible and does not result in the transfer of ownership of any physical object” (European Union Intellectual Property Office 2014, p. 8). This definition matches our definition of services as intangible products.

Finally, IV panel regression estimates can be tested for the validity of instrumentation using two main postestimation statistics (Baum, Schaffer, and Stillman 2007). The first test addresses concerns of weak identification, that is, for situations where the excluded instruments are only weakly correlated with the endogenous regressors. If the Cragg Donald Wald test produces F statistics higher than 10, the null hypothesis of weak identification can be rejected. The second postestimation test checks the validity of instrumentation by testing for overidentifying restrictions. If the Sargan-Hansen statistic is significant, the null hypothesis that the instruments are valid (i.e., uncorrelated with the error terms and correctly excluded instruments) can be rejected.

Results

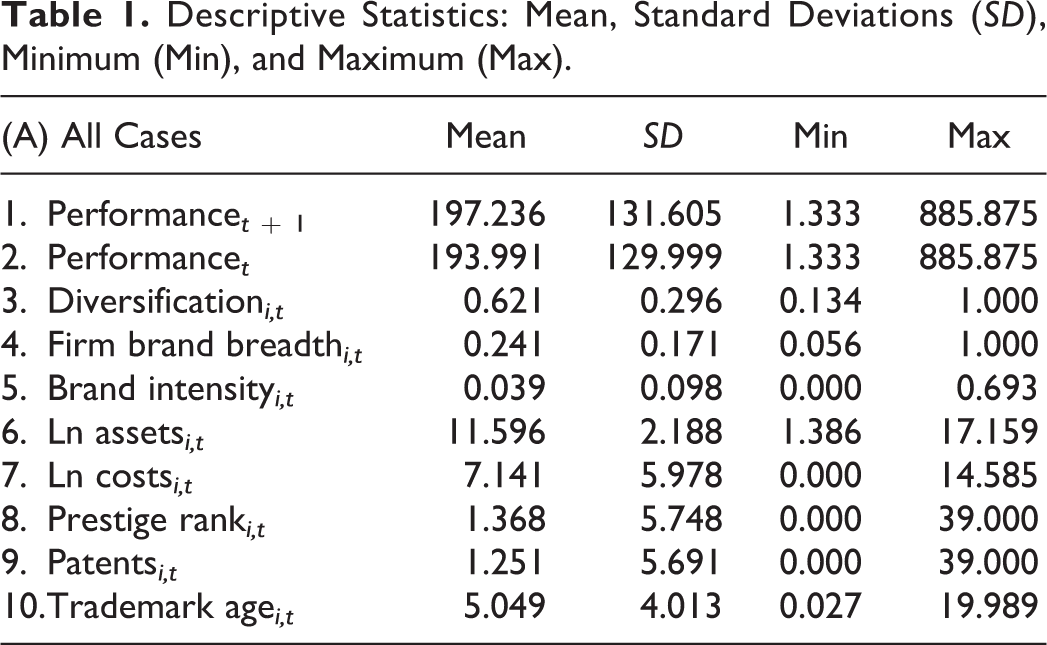

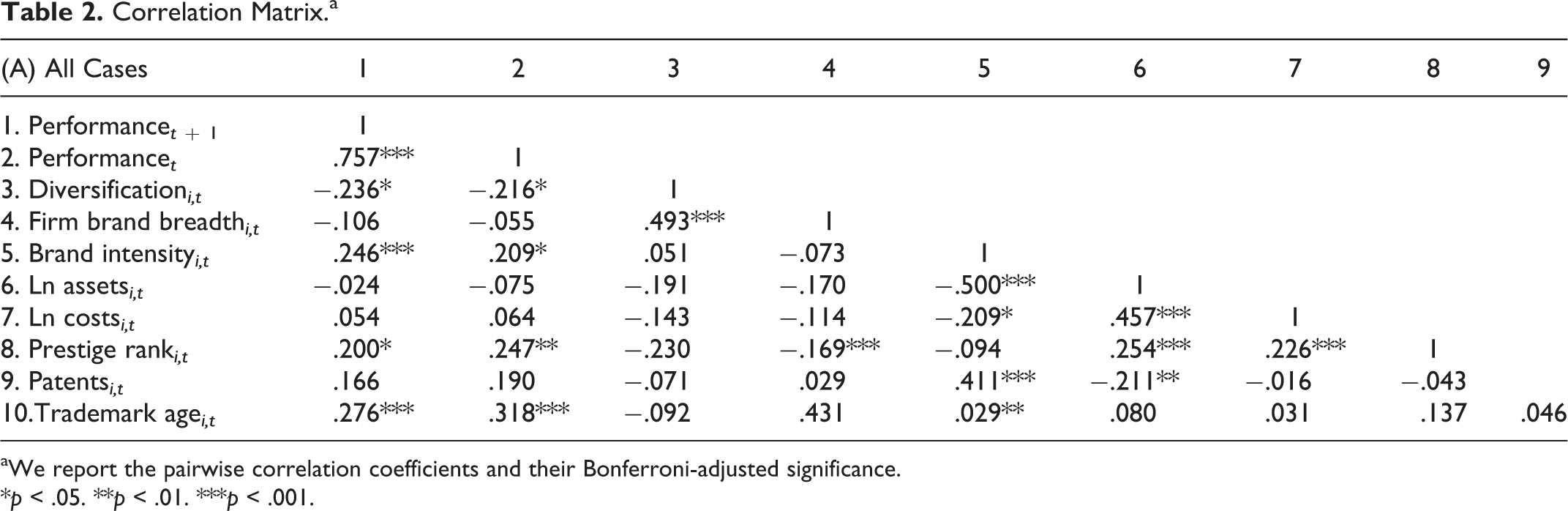

Table 1 shows the basic overall descriptive statistics for our variables and Table 2 reports the pairwise correlation coefficients, together with their significance. It is worth noting that apart from the diversification discussed above, no other variable of theoretical interest significantly correlates with firm brand breadth i,t above 20%.

Descriptive Statistics: Mean, Standard Deviations (SD), Minimum (Min), and Maximum (Max).

Correlation Matrix.a

aWe report the pairwise correlation coefficients and their Bonferroni-adjusted significance.

*p < .05. **p < .01. ***p < .001.

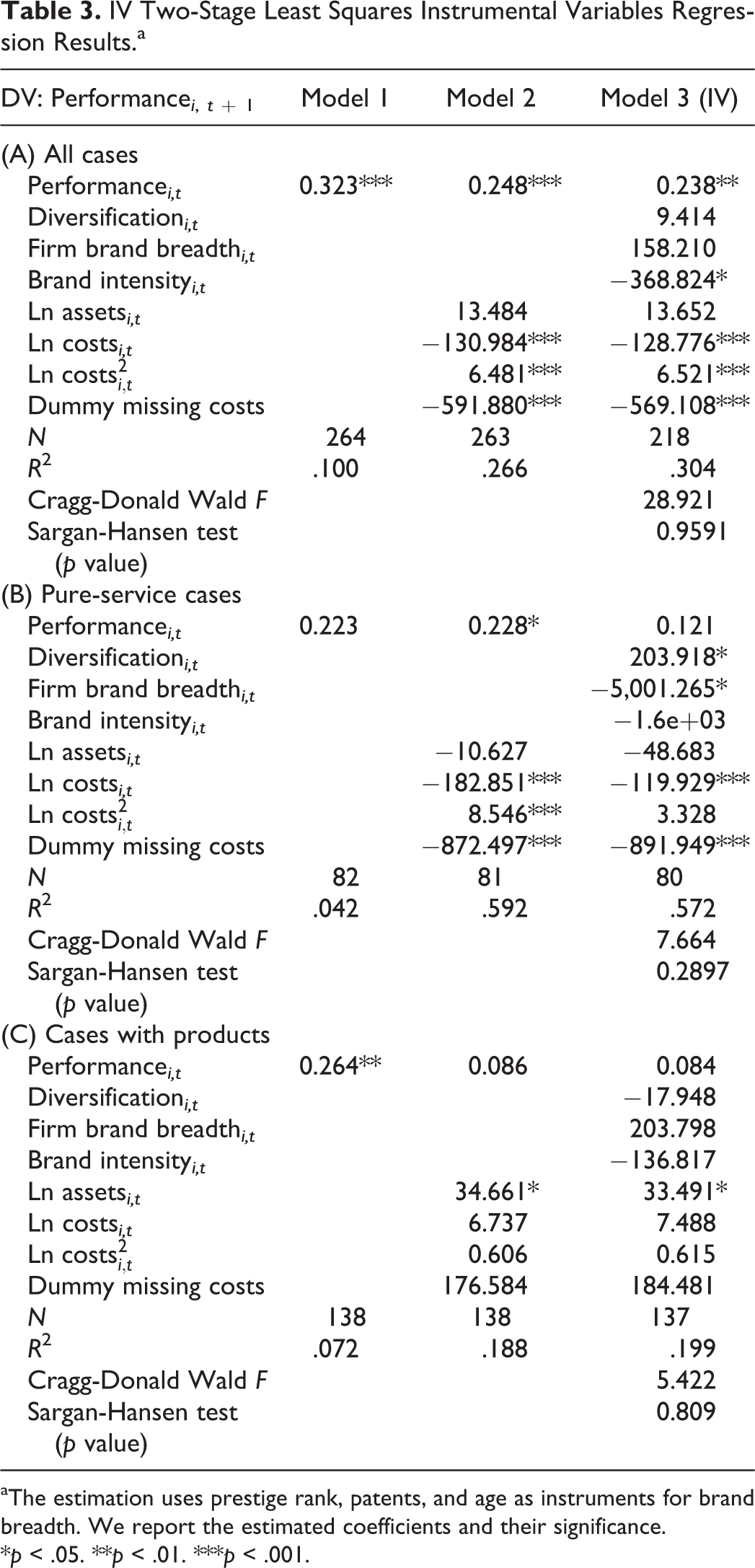

Table 3 shows the results of the IV estimates, which we perform for all cases (A), pure-service cases (B), and cases with products (C). Model 1 is the baseline model where performance only depends on past performance. Model 2 includes several control variables and Model 3 is the full model, with all the variables of theoretical interest.

IV Two-Stage Least Squares Instrumental Variables Regression Results.a

aThe estimation uses prestige rank, patents, and age as instruments for brand breadth. We report the estimated coefficients and their significance.

*p < .05. **p < .01. ***p < .001.

At first glance, the significant differences between the three models (A, B, and C) confirm our theory that PSFs’ transition from service to products should be treated separately, since it accounts for different dynamics and impacts on main variables.

Diversification i,t is significantly positively related to performance for pure-service firms (coefficient = 203.918, p value = .025), which provides empirical support for Hypothesis 1. We also check whether this positive relationship with productivity is also thanks to labor-saving effects, by running separate regressions for sales and employees. We find that the changes in our variables are only significantly related to changes in employment at pure-service firms. This is in line with the notion that the PSF business model is biased toward a balance between marginal revenues versus marginal costs without capital fixed investments and traditional economies of scale. For the two competing hypotheses, we find support for Hypothesis 2a: The narrower the brand strategy, the higher the performance in pure-service firms (coefficient = −5,001.265, p value = .015). PSFs that exploit economies of scope from their intangibles, managing a specialized portfolio of brands within services, achieve a higher performance.

In terms of our controls, brand intensity tends to exert a negative effect, meaning that the stock of brands is limited by the firm’s ability to spur growth in size; in fact, the brand proliferation should demonstrate a lower growth rate than the PSF’s increase in size for the intensity variable to have a positive impact on performance. This suggests fine-tuning brand strategies with the firm’s potential to extend its market share. Note also that costs are not significant for the mixed case. We think that this is a confirmation on the importance of value creation effects compared to value capture arguments based on efficiency.

The postestimation tests reassure us that the models have been correctly identified, except for weak identification in the cases with products (when the Cragg-Donald Wald F-test is 5.422, hence too small to reject the hypothesis of weak identification). In all the other models, the F statistics for the Cragg-Donald test are high enough to reject the null hypothesis of weak identification. The Sargan test results are consistent across all models, indicating that the null hypothesis of valid instruments cannot be rejected. Models have an explanatory power, measured by R 2 of about 20% for the product case, 50% for the service, and 30% overall. This power is in line with previous studies on diversification and performance like Campa and Kedia (2002), reporting an R 2 of about 15% with IV estimation (p. 1751), or Hashai (2015), reporting an R 2 of about 20% (p. 1393).

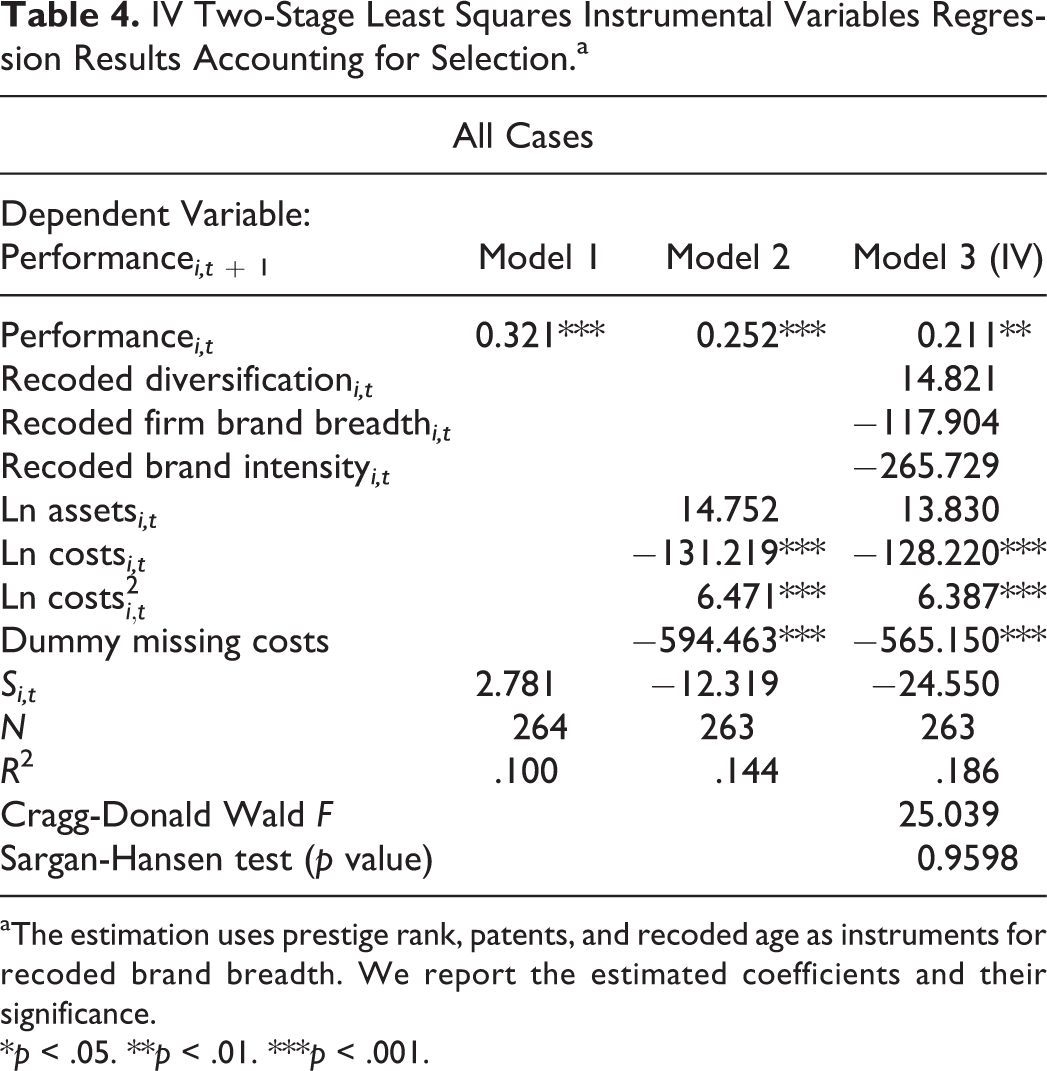

As a robustness check, we tackle the issue of potential selection bias. Despite only focusing on firms owning trademarks, our choice could be related to variables that we also include in our model. Since it is very arduous to find an instrument that affects trademark registration but not performance, we opt for an indirect test. We define a selection dummy Si,t which is 1 if a firm own trademarks in that year and 0 otherwise. We also recode all our trademark-based variables into new variables where missing values (corresponding to Si,t = 0) are set at 0. We then reestimate all our regression models using the recoded independent variables and add the selection dummy as an additional control. If the selection dummy proves insignificant and the other variables have qualitatively similar effects on the models, then a bias from selection can be safely disregarded. For all our model specifications, this turns out to be the case (see Table 4 for the entire sample). This evidence suggests there is no significant selection bias in our estimates.

IV Two-Stage Least Squares Instrumental Variables Regression Results Accounting for Selection.a

aThe estimation uses prestige rank, patents, and recoded age as instruments for recoded brand breadth. We report the estimated coefficients and their significance.

*p < .05. **p < .01. ***p < .001.

Conclusions

This article analyzes diversification and branding strategies as performance determinants for PSFs. Drawing on a sample of management consulting firms, we find that diversification combined with product-specific narrow brands enhances firm performance. However, these results only apply if PSFs do not extend diversification into tangible products like software packages. These results are a novel complement to the extant literature (Greenwood et al. 2005; Hitt et al. 2006)

This study has the following implications for academics and practitioners. First, diversification is an important avenue for increasing performance, but it should be coherently managed and fine-tuned with branding strategies (Hui 2004). Managers should focus on their firm’s intangible knowledge stock that could be extended into different service niches by customizing their offer accordingly. Given that the core competences of PSFs lie in their human resources, this task should probably be accomplished with a modularity approach that combines teams with different skills (Greenwood et al. 2005). Thus, the two necessary conditions to achieve this objective are a reliable map of all the skills in a focal PSF (Criscuolo, Salter, and Sheehan 2007) and the ability to form different combinations of expertise according to the demand requirements. Novel research could dig deeper in this area, proposing empirical evidence to match diversification and performance data with some measure of the modularization and team rotation.

Second, we show that moving from services to products requires competencies that are difficult to nurture within the boundaries of a company. These range from managing radically different client relations to the complexity of controlling different distribution channels for off-the-shelf products (Brivot 2011). More generally, besides exploiting the modularity of skilled personnel, other variables should account for the relationship between performance and diversification when PSFs include products. Diversification through mergers and acquisitions could be an important aspect when PSFs enter the realm of physical products as suggested by von Nordenflycht (2011); future studies could test if, when, and how acquisitions are the real means of increasing performance when PSFs enter the product domain.

Third, in terms of brand strategies, we confirm that PSF markets have particularly strong information asymmetries. Brands are classical anchors for channeling and protecting reputations. In the case of pure-service PSFs, given their extreme level of intangibility, the risks of diluting firm legitimacy by extending the same brand to different niches could be too high (Davies, Chun, and Kamins 2010). For example, a failure in a new product niche tapped with a consolidated brand could compromise the reputation of the same brand in the traditional market. Moreover, extending the same brand to new clients with different social values or behaviors could be a detrimental move if brand reputation is particularly meaningful for the original group of customers (Brush, Dangol, and O’Brien 2012).

In this respect, our main recommendation to managers is to develop narrow brands along with diversification rather than extend consolidated brands when tapping into a new service niche. Consequently, high coordination between the marketing division and “production” side of a company is advisable in order to understand the role of brands in a particular niche. Needless to say, a more fine-grained analysis could shed light on the real differences across brands trademarked by PSFs. Even though firms register multiple brands, the actual differences (names, colors, logos) may not be significant.

Fourth, further studies could address how customer perception is linked to actual trademarked brands, given that customer-based measurements of performance are particularly relevant for services (Bowen and Ford 2002). Direct consumer surveys or laboratory research could indeed achieve a two-fold aim. On the one hand, it is key to measure how brand extension to different sectors lowers customers’ perception of uniqueness. On the other hand, these approaches could decompose the evaluation of a global portfolio of PSF brands into the values of single brands, testing also whether or not the value of the brand portfolio is equal to the sum of the single parts. An important direction of this line of reasoning will shed light on how customer perceptions change when PSFs brands are extended to product-based business models. As rightly stressed by Greenwood et al. (2005, p. 670), “the benefits of diversification for PSFs are socially constructed.”

This article is not without limitations. Our empirical results draw only on a specific set of PSFs represented by management consulting firms with a coarse headquarter-based measure of performance. Further empirical research could test the validity of our conclusions in other PSF settings, for example, the more technology-intensive ones like engineering consultancies with performance measures for every niche in the firm portfolio. Another important test could be to see if our results apply to other industries that share with PSFs a high level of tacitness and asymmetric information. Finally, we do not have any proxy for the sunk investments that firms make on a registered trademark nor its actual market value. This is a common limitation of firm-level studies on the economic effect of brands (Sandner and Block 2011). Clearly, if our results remain valid, brands with higher costs and value should be subject to more restraints in terms of potential extensions.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.