Abstract

Relational event models expand the analytical possibilities of existing statistical models for interorganizational networks by: (i) making efficient use of information contained in the sequential ordering of observed events connecting sending and receiving units; (ii) accounting for the intensity of the relation between exchange partners, and (iii) distinguishing between short- and long-term network effects. We introduce a recently developed relational event model (REM) for the analysis of continuously observed interorganizational exchange relations. The combination of efficient sampling algorithms and sender-based stratification makes the models that we present particularly useful for the analysis of very large samples of relational event data generated by interaction among heterogeneous actors. We demonstrate the empirical value of event-oriented network models in two different settings for interorganizational exchange relations—that is, high-frequency overnight transactions among European banks and patient-sharing relations within a community of Italian hospitals. We focus on patterns of direct and generalized reciprocity while accounting for more complex forms of dependence present in the data. Empirical results suggest that distinguishing between degree- and intensity-based network effects, and between short- and long-term effects is crucial to our understanding of the dynamics of interorganizational dependence and exchange relations. We discuss the general implications of these results for the analysis of social interaction data routinely collected in organizational research to examine the evolutionary dynamics of social networks within and between organizations.

Keywords

The increased availability of longitudinal data generated by observable continuous-time interaction among organizations is exposing—and at the same time helping to address some of the limitations of network models typically adopted in empirical studies of interorganizational exchange and dependence relations (Butts, 2008; Marcum et al., 2012; Perry & Wolfe, 2013; Vu et al., 2017).

The diffusion of data produced by technology-mediated communication is making continuous-time social interaction data in the form of digital footprints increasingly common (Golder & Macy, 2014). Similarly, the new possibilities to record social interaction and individual behavior in continuous-time offered by mobile technologies (Butts, 2008; Barrat et al., 2013), sensor networks (Stehlé et al., 2011), sociometric badges (Wu et al., 2008), radio-frequency identification devices (RFID) (Elmer & Stadtfeld, 2020), and video recordings (Pallotti et al., 2020), are raising new questions that traditional research designs—and models—adopted in organizational and management research are ill-suited to address (Gylfe et al., 2016; LeBaron et al., 2018). These new data collection and observation technologies are making data on social interaction available at an unprecedented level of detail and precision. Access to continuous-time social interaction data is becoming increasingly common in many well-established areas of organizational research such as, for example, team composition, productivity and performance (Leenders et al., 2016; Lerner & Lomi, 2019), and organizational routines (LeBaron et al., 2016), and socialization (Ingram & Morris, 2007). In this paper we want to suggest that research on interorganizational relations can similarly benefit from models developed for the analysis of continuous-time interaction (Kitts et al., 2017).

Time-stamped sequences of relational events connecting senders and receivers of action constitute the observable micro-relational structure of social networks. In fact, social networks are frequently derived from aggregation of sequences of relational events unfolding in continuous time into discrete network “ties” (Brandes et al., 2009; Stadtfeld & Block, 2017). Building directly on Butts (2008), our starting point in the current study is the observation that this aggregation involves the potential loss of relevant information about the temporal and relational microstructure of interorganizational exchange and dependence relations. During the last forty years, organizational and management theorists (Pfeffer & Salancik, 1978; Hillman et al., 2009) have systematically built on the classic theoretical vision of exchange as a fundamental social relation (Cook, 1977; Blau, 2017).

In modeling exchange processes, the risk of information loss is particularly severe when interaction is characterized by time-ordered, or sequential constraints like, for example, in the case of conversational sequences (Gibson, 2005), interorganizational coordination (Butts, 2008), and financial transactions (Finger & Lux, 2017). Available statistical models for social networks are not well suited to the analysis of continuous-time exchange, especially when observed interaction frequency is high (Butts, 2009). For example, in standard statistical models adopted in empirical research on interorganizational networks (Lomi & Pallotti, 2012), aggregation of relational event sequences into network ties assumes the presence of stable relations over more or less arbitrary time frames, and typically ignores information on the sequential order that defines even the most elementary relational mechanisms (Amati et al., 2019).

Consider reciprocity, for example, a relational mechanism of central importance in theories of exchange (Molm et al., 2003) and considerable substantive interest in empirical studies of interorganizational relations (Oliver, 1990; Baker & Faulkner, 1993; Uzzi, 1996; Ingram & Roberts, 2000). Reciprocity is not invariant with respect to the timing in the underlying acts of exchange between actors. The correct identification of who is initiating action and who is receiving and returning it—and when—matters precisely because sequential ordering in social interaction provides important information about status differences and dominance relations (Chase, 1982; Gibson, 2005), and plays a central role in governance (Larson, 1992) and in the allocation of organizational attention (Cohen, March, & Olsen, et al., 1972; March & Olsen, 1983). Without information on the timing of exchange events, and on the time elapsing between them, the notion of reciprocity remains theoretically important, but becomes empirically more difficult to identify.

Like other, more complex, relational mechanisms involving multiple actors and multiple exchange events (Nowak & Sigmund, 2005), direct reciprocity emerges over periods of variable length, where the time scale may vary from few minutes for communication in emergency situations (Butts, 2008), days for email communication (Perry & Wolfe, 2013), and months for complex interorganizational exchange (Kitts et al., 2017). Clearly, different rules for aggregating sequences of time-ordered and time-stamped relational events into network ties, might lead to different conclusions about tendencies toward reciprocity. In summary, to understand relational phenomena, including interorganizational networks, it is important to be able to identify who is giving to whom, when, and how much.

Representing network relations as flows connecting senders and receivers of action or resources does not exhaust all the empirical possibilities (Borgatti & Halgin, 2011). Data on social relations may come in many forms (Borgatti & Foster, 2003), and event data are only one of such forms (Borgatti et al., 2009). In consequence—and how is common in organizational and management research—different models are appropriate for different settings, and different research questions (Borgatti et al., 2009; Robins, 2015). For example, networks—and interorganizational networks in particular—are often generated by formal contractual arrangements between corporate actors (Jones et al., 1997; Lomi & Pattison, 2006). In such cases, networks do not accumulate flows, but, rather, enable them. The main purpose of this study is neither to compare different network models, nor to claim superiority for one specific class of models. Recent comparative research and critical assessments of different classes of network models—static versus dynamic, tie-oriented versus actor-oriented, structure-oriented versus change-oriented, etc.—are available elsewhere (see, e.g., Butts, 2017; Stadtfeld et al., 2017; Block et al., 2018, 2019a, 2019b).

The purpose of this study is to illustrate how recent refinements in the relational event modeling framework originally introduced by Butts (2008) may be adopted to address some of the core theoretical and methodological concerns routinely arising in empirical studies of interorganizational exchange taking the form of temporal sequences of interaction events (Vu et al., 2017; Amati et al., 2019). The model that we present combines an efficient approach to sampling (Lerner & Lomi, 2020b; Vu et al., 2011b) with sender-based stratification (Vu et al., 2015) as well as the possibility of distinguishing between short- and long-term network effects. The first feature (efficient sampling) allows the model to be easily scaled for the analysis of samples of relational event data characterized by a very large risk set, or space of possible events. The second feature (sender stratification) allows the model to control for unobserved heterogeneity—a problem that becomes particularly serious as the space of possible events increases, and varies over time. The third feature (short- and long-term network effects) is particularly salient in empirical settings where relational events occur at a very high-frequency, and/or are clustered within temporal frames of specific length.

The relational event model (REM) that we describe is broadly applicable to diverse levels of analysis that may be of interest to students of organizational behavior. Examples of research in organizational behavior where REMs have demonstrated their empirical value include studies of small group interaction (Pilny et al., 2016; Butts & Marcum, 2017), team dynamics (Quintane et al., 2013; Leenders et al., 2016; Schecter et al., 2018), organizational communication (Foucault Welles et al., 2014), problem solving (Quintane et al., 2014), learning (Vu et al., 2015), leadership and hierarchy formation (Lerner & Lomi, 2017), and collaboration and conflict (Lerner & Lomi, 2020a). In a recent study on coordination in surgery teams based on video-recordings Pallotti et al. (2020) advocate the adoption of event-oriented research designs and models like the one we discuss in this paper, as the best strategy for understanding continuous-time interaction in teams and small groups (Leenders et al., 2016).

While the advantages of event-oriented research designs have long been recognized (Tuma & Hannan, 1984), REMs for data with complex network-like dependencies have been proposed only relatively recently (Butts, 2008; Brandes et al., 2009; Perry & Wolfe, 2013; Vu, 2012). Building on these advances, in this paper we propose a relational event modeling framework for the longitudinal analysis of interorganizational exchange and dependence relations based on temporal point-process models for directed interaction data (Perry & Wolfe, 2013; Vu et al., 2017; Amati et al., 2019). We demonstrate the empirical value of the model in an analysis of direct and generalized reciprocity in financial transactions. The empirical case is based on data that we have collected on the complete set of interbank transactions recorded on a major European trading platform during the year 2006 (Finger et al., 2013; Fricke & Lux, 2015; Hatzopoulos et al., 2015; Finger & Lux, 2017). Because their recording is accurate to the second, financial transactions provide an almost ideal illustration of directed continuous-time interaction generating time-stamped sequences of relational events connecting sender (lenders) and receiver units (borrowers). By re-framing financial transactions as relational events, the analysis that we present clarifies how diverse forms of reciprocity operate differently over distinct time frames to affect the micro-relational structure of financial markets.

Financial markets show how relational concepts common in the study of interorganizational relations (see, e.g., Oliver, 1990; Baker et al., 1998; Smith & Chae, 2016; Bowers & Prato, 2018; Cuypers et al., 2020) may be extended to the analysis of continuous-time interaction between organizations. Yet, the high-frequency data produced by financial markets make financial transactions a relatively unusual—but not for this less theoretically interesting or empirically relevant—form of interorganizational exchange (MacKenzie & Millo, 2003; Knorr-Cetina & Preda, 2006). For this reason, we supplement our main illustrative empirical analysis with a replication study of interorganizational relations among health care organizations as a common example of an empirical setting where relational coordination among organizations has been extensively researched (Van de Ven & Walker, 1984; Hoffer Gittell, 2002; Gittell, 2012).

Lost in (Network) Translation

A major line of theoretical development in the study of organizations posits that organizations attempt to control uncertainty in their resource environments by actively establishing exchange and dependence relations with other organizations (Selznick, 1949; Aldrich & Pfeffer, 1976; Pfeffer & Salancik, 1978). The system of exchange relations generated by these control attempts has been routinely represented in terms of interorganizational networks (Laumann & Marsden, 1982; Galaskiewicz & Wasserman, 1989; Galaskiewicz & Burt, 1991; Davis & Greve, 1997; Gulati & Gargiulo, 1999; Lomi & Pattison, 2006). More or less explicitly, research based on network representations of interorganizational relations has been inspired by the theoretical intuition of Harrison C. White (White, 1992, Ch.9) according to whom: “Social (…) structures are traces from successions of control efforts.” Empirical studies inspired by this view typically focus on the analysis of “structure,” but cannot observe the “successions of control efforts” out of which “structure” ultimately emerges.

Contemporary research on interorganizational networks is frequently based on sophisticated statistical models for network ties representing directly structures of dependence relations among organizations (Van de Bunt & Groenewegen, 2007; Atouba & Shumate, 2010; Stadtfeld et al., 2016). The basic assumption of this line of research is that interaction between organizations takes the form of network ties, defined as relatively stable and enduring relations between organizations (Van de Bunt & Groenewegen, 2007). Interaction itself, however, is rarely examined directly. The analytical focus is on network ties that are typically derived from an aggregation—and, often, dichotomization of sequences of relational events connecting “sending” and “receiving” organizations (Lomi & Pallotti, 2012).

This way of representing interorganizational exchange and dependence relations is clearly appropriate when relations are produced by relatively stable forms of attachment subject to inertial forces like, for example, in the case of relational contracts that link organizations to their clients, suppliers, and competitors (Monteverde & Teece, 1982; Levinthal & Fichman, 1988; Uzzi, 1996; Baker et al. , 1998; Lomi & Pallotti, 2012). Yet, this approach becomes increasingly inadequate when organizations regulate their dependence relations through high-frequency interaction like, for example, in the case of financial transactions—where “buyers” and “sellers” manage their resources dependence through continuous-time exchange. In this case, essential information may be lost in the translation of sequences of time-stamped, instantaneous, and possibly repeated relational events into enduring network ties. Three kinds of information loss are particularly limiting for empirical studies of resource dependence relations between organizations.

The first type of information loss concerns the timing of the underlying relational events. Neglecting information about who initiates and who receives action makes it more difficult to adjudicate agency (Gibson, 2003; Stadtfeld et al., 2017; Tasselli & Kilduff, 2021). Identifying direction in the flow of action is obviously very important in research on task-oriented teams (Pallotti et al., 2020). In the study of interorganizational relations, the aggregation of individual exchange events into timeless network ties is particularly problematic because it involves the loss of information about the temporal order of individual acts of exchange out of which patterns of resource dependencies emerge (Pfeffer & Salancik, 1978). As it is clearly the case in the analysis of conversational turns (Gibson, 2005), the loss of information on the timing of exchange events between organizations would make the relation between them more ambiguous.

The second kind of information loss concerns the rates at which relational events are emitted by the source organization (or sender) toward its target (or receiver). Patterns of interorganizational exchange happen at rates whose speed is dependent on features both of the context and the relation. For example, financial transactions—the specific interorganizational events we study in the empirical part of the paper—typically happen at very high frequency, with a large number of actual events occurring at short time scales—daily, or even hourly. Strategic alliances, joint ventures and similar intercorporate relations involve episodic relational events with a duration that is sometime established by contract. These intercorporate events may be reasonably approximated by stable network ties (Gulati & Nickerson, 2008), or reconstructed in terms of aggregate counts of events (Stuart, 1998). The majority of interorganizational relations fall somewhat within these extreme cases—with streams of relational events connecting sender and receiver organizations that unfold at a variable rates (Amati et al., 2019).

Finally, network mechanisms do not operate instantaneously—that is, it takes time for configurations of networks ties to emerge and produce their effect. To illustrate consider reciprocity—a social mechanism commonly studied in organizational research (Larson, 1992; Dabos & Rousseau, 2004; Caimo & Lomi, 2015), and perhaps one of the most commonly recognized social mechanism in the study of human organization (Gouldner, 1960; Coleman, 1988; Fehr et al., 2002). Reciprocation, the process that produces reciprocity, takes time to operate. If actor

The observation that information may be lost in translation from relational “events” to network “ties” is not reported here for the first time (Borgatti & Halgin, 2011; Stadtfeld & Block, 2017). In fact, it maps onto the more general distinction between models for “event recurrences” and “state transitions” developed in the context of early event history models in organizational ecology and corporate demography (Hannan, 1989). As Marsden (1990) has clearly recognized, interpreting networks as units of analysis is possible only if assumptions are made about how to abstract “relationships or ties” from sequences of observed micro-level relational events connecting the actors. In the case of directed relational processes that we have discussed, the problem involves information loss due to aggregation of sequences of time-stamped relational events into ties. In the next section, we illustrate how newly derived REMs may be adopted to address this problem directly.

Recent Advances in Models for Relational Event Sequences

REMs afford representation of social relations at the same level of time resolution of the observed data—for example, months, days, minutes, seconds. Their closeness to observed data gives event-oriented models an obvious advantage over alternative longitudinal models based on various forms of temporal aggregation. Even when available, sequences of relational events observable in continuous time have been typically aggregated over time into binary cross-sectional network panels (Tuma & Hannan, 1984). The resulting data structures are conceived as enduring connections between social units and ultimately modeled using either Exponential Random Graph Models (ERGMs) (Lusher et al., 2013) or Stochastic Actor-Oriented Models (SAOMs) (Van de Bunt & Groenewegen, 2007; Snijders et al., 2010). The first attempt directly to model sequences of relational events without aggregating relational events into ties was proposed by Butts (2008) a decade ago – but the problematic distinction between relational events and relational states has a much longer history in the analysis of social networks (Freeman et al., 1987; Marsden, 1990; Doreian, 2002).

More recent studies have introduced specialized models for the analysis of relational event sequences. All REMs predict the occurrence of a relational event embedded in a sequence of time-ordered events. However, their specification may refer to distinct statistical traditions. Former REMs are closely related to event history analysis (e.g., Butts, 2008; Brandes et al., 2009; de Nooy, 2011; Quintane et al., 2013) and have been progressively extended to the analysis of large-scale networks (Vu et al., 2011a).

A more recent body of work links REMs to point-process models (Vu et al., 2011b; Perry & Wolfe, 2013; Vu et al., 2017; Amati et al., 2019) for repeatable data, then emphasizing the estimation of events’ occurrence rates rather than the duration between successive events (Hannan, 1989). As we discuss below, the REM that we propose in this paper builds on this more recent line of research.

A last body of methodological and empirical research on REMs is rooted in SAOMs, thus assuming that relational events are the product of utility-driven individual decisions (Stadtfeld & Geyer-Schulz, 2011; Stadtfeld et al., 2017). The central feature of this approach is the decoupling of temporal and social interdependence.

Specialized relational event models have been proposed for the analysis of two-mode (Quintane et al., 2014) and multiplex networks (Lerner & Lomi, 2017). Vu et al. (2011b) introduced a continuous-time regression model based on Cox (1972, 1975) for accommodating time-dependent network statistics. Contextually, the authors exploited nested case-control sampling (Borgan et al., 1995) for extending REMs to a more general relational setting where the counting process of relational events is placed on the edges rather than on the nodes (Vu et al., 2011b). For simplicity, the model is developed only for non-recurrent settings—that is, settings where the creation of an edge between two nodes only occurs at most once. Perry and Wolfe (2013) extended the model of Vu et al. (2011b) to recurrent settings and multicast interactions—that is, those involving a single sender and multiple simultaneous recipients—see the recent work of Lerner et al. (2021) for recent progress on this front.

In turn, this latter body of work has promoted further extensions. Vu et al. (2015), for instance, combined a flexible stratification method with nested case-control sampling to fit REMs with more complex data structures, and show the scalability of the approach to very large data sets.

More recently, Vu et al. (2017) implemented a marked point-process (Cressie, 1993) extension of Perry and Wolfe (2013). The main advantage of this approach is to control for critical micro-mechanisms that may connect the same nodes in a recurrent event network. The proposed model extension accomplishes this task by decomposing the whole sequence of relational events into two parts. The first involves event times modeled as counting processes. The second involves event destinations or “marks” which can be modeled via discrete-choice functions.

One innovative aspect of this newly derived framework for REMs is being less computationally intensive than other related approaches that have attempted to deal with the same issue (Butts, 2008; Vu et al., 2011b).

The more recent work of Lerner and Lomi (2020b) assessed the reliability of REMs parameters estimated under a nested case-control sampling that computes explanatory variables only for a random subset of events while aggregating all events into the network of past events. Their empirical results suggest that REMs can be reliably fitted to networks with more than 12 million nodes connected by more than 360 million dyadic events simply by analyzing a sample of some tens of thousands of events and a small number of controls per event.

Building on these recent experiences, in this paper we propose a point-process model for recurrent events that further develops the combination of stratification and nested case-control sampling. Specifically, we propose (i) a sender stratified REM that accounts for senders' heterogeneity defined on the composition of their receivers' sets, (ii) a nested case-control sampling scheme that updates, at each point in time, the risk set of each sender, and ultimately samples non observed events on the basis of senders' past interaction, and (iii) a classification procedure of time-dependent statistics that distinguishes between short- and long-term network effects.

A Model for Relational Event Sequences

The REM that we introduce in this work provides a novel analytical framework for studying time-ordered sequences of relational events in a “behavioral oriented framework” (Butts, 2008, p. 167).

In its current specification, the model represents an extension of Vu et al. (2015) and Lerner and Lomi (2020b) on the basis of Vu (2012, p. 110) and Perry and Wolfe (2013). This approach improves other parameterizations adopted in earlier studies—that is, Vu et al. (2011b), Perry and Wolfe (2013), Quintane et al. (2013), Vu et al. (2015), and Vu et al. (2017) by (i) incorporating intensity-based statistics—so that the strength of relations between senders and receivers can be modeled; (ii) allowing the predictive value of past events for future event to decay over time—so that events occurred in the more distant past have a weaker impact on future events; (iii) computing network effects over different time horizons—so that the model can distinguish between short- and long-term effects, and (iv) adopting a stratification procedure that alleviates concerns about how heterogeneity of the sender units may affect the empirical estimates—an issue that becomes particularly salient as sample size increases.

This problem was less prominent in prior studies of interorganizational exchange relations based on REMs where the analysis was limited to small and relatively isolated organizational communities (Kitts et al., 2017; Amati et al., 2019).

Model Definition

The model assumes that nodes join the network according to a stochastic process and create an edge every time a new relational event occurs. In other words, at its core, the model is defined in terms of a count process defined on network edges. Originally developed in survival and event history analysis, the counting process approach provides now the analytical framework for modeling streams of relational events.

The model that we present in the current paper places the counting process

In contrast to other similar modeling approaches (Butts, 2008; Vu et al., 2011, 2011?; Perry & Wolfe, 2013; Vu et al., 2015), the intensity function of our model

The Temporal Micro-Structure of Relational Event Sequences

Following a well-established practice in statistical modeling of networks, REMs statistics are defined in terms of local configurations of ties generated by temporal patterns of dependence linking successive relational events (Snijders et al., 2006; Snijders, 2011; Amati et al., 2018).

Temporal patterns of dependence may be generated by a number of mechanisms such as, for example, repetition, reciprocity, transitivity, and other kinds of triadic closure. In REMs, these temporal—rather than spatial—patterns of dependence emerge from—and at the same give rise to structured sequences of events that are then used to compute network-like statistics (Butts, 2008).

In REMs, the network statistics

Intuitively, this time-weighting scheme (Daley & Vere-Jones, 2003) implies that relational events close to the current time

To account for time-specific variations in network micro-mechanisms, our REM specification allows for two distinct classes of network statistics. First, degree-based statistics that count the number of sequences of directed relational events that crystallize into specific local structure of dependence. Second, intensity-based statistics that are normalized by the number of sequences of relational events involving the same pair or groups of nodes. While degree-based statistics unfold within short- and long-term temporal frameworks, their intensity based counterparts are time-weighted in order to remove the possible collinearity with degree-based counterparts and then reduce their correlation. Indeed, by design, network effects are nested one in the other, with more complex structures containing simpler ones. In our model, shorter and longer temporal frames for degree-based statistics are determined on the basis of a recency parameter expressed in number of days. Instead, the temporal decay of intensity-based statistics is driven by the parameter

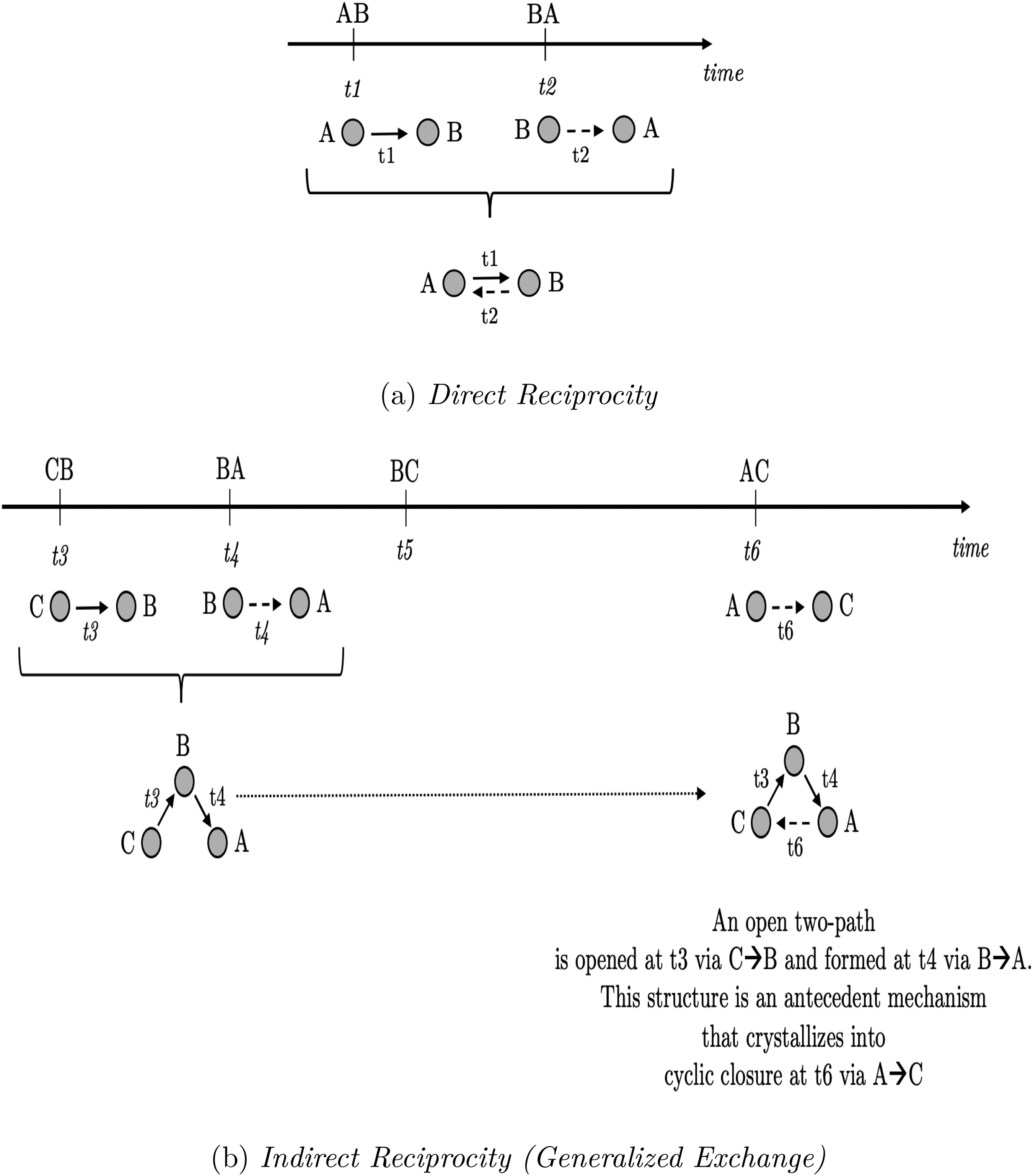

Figure 1 shows how local dependencies of interest may emerge from time-ordered sequences of relational events. On a solid line that represent time, we depict individual acts of exchange linking together three actors (A, B, and C) in a way that gives rise to direct and generalized reciprocity. Figure 1a shows how two time-ordered relational events that channel resources in opposite directions eventually crystallize in a sequence of reciprocal exchange. Figure 1b shows how a time-ordered sequence of three relational events may concatenate in a cyclic triadic structure that reveals actors’ preferences toward generalized exchange or generosity.

More specifically, in Figure 1a the resource transfer from

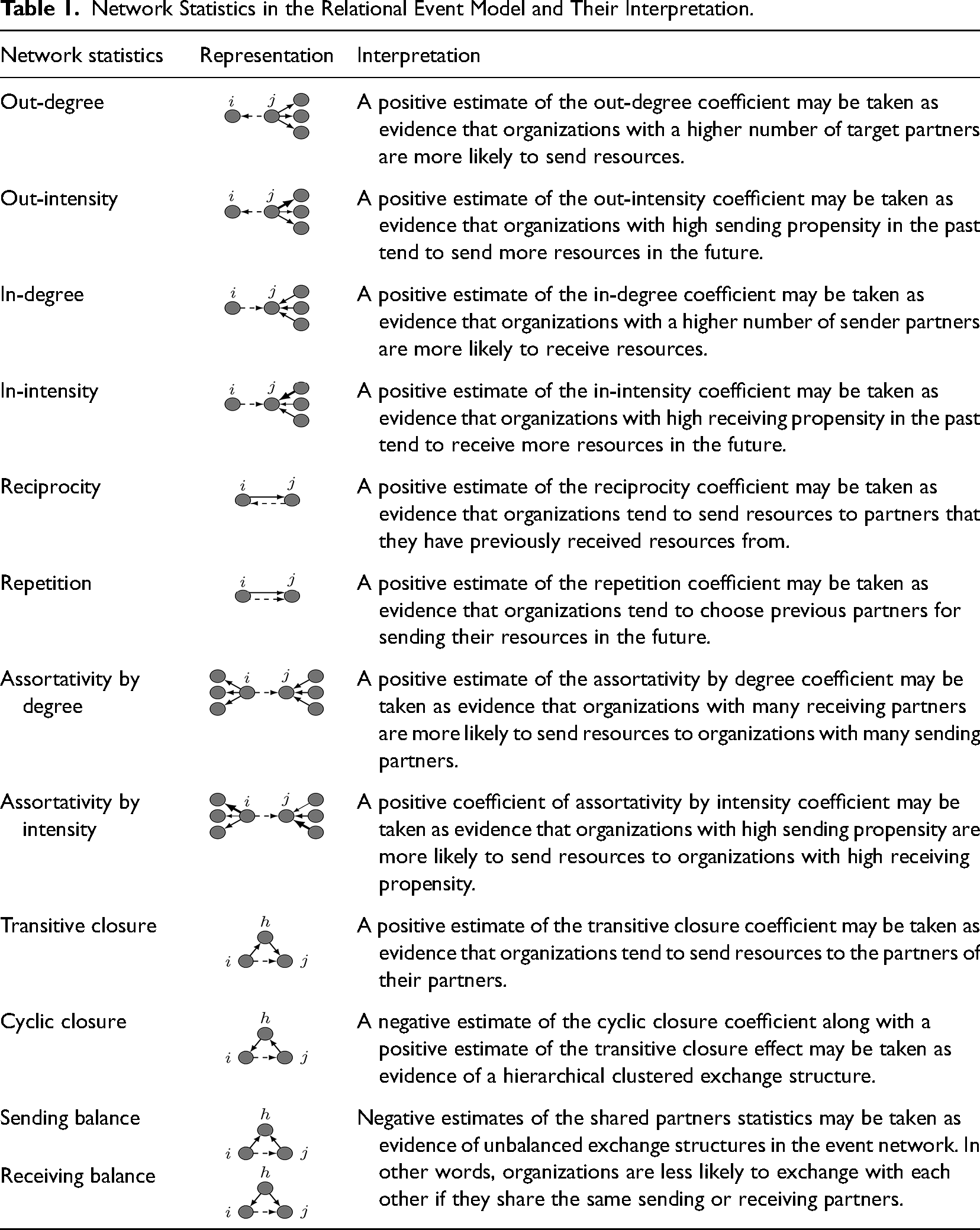

The discussion of some of the main local temporal structures that arise from relational event sequences is organized around Table 1, which provides an intuitive graphical representation and summary interpretation of the network statistics that we include in the empirical model specification discussed later in the paper. Mathematical formulas associated with those network statistics are reported in Appendix B.

Network Statistics in the Relational Event Model and Their Interpretation.

Preferential attachment refers to a generic positive feedback mechanism whereby highly connected nodes increase their connectivity faster than less connected nodes (Jeong et al., 2003). When the process of interest is directed— that is, it implies a flow of material or symbolic resources form a sender to a receiver—preferential attachment may be represented in terms of activity—the tendency of organizations to establish relations with partners—or popularity—the tendency of organizations to be selected as partners (Stuart, 1998; Stuart & Yim, 2010).

The main implication of preferential attachment is that network nodes establish new edges as a function of the number of edges that they have established in the past (Newman, 2001). For this reason, empirical studies on interorganizational networks interpret preferential attachment as a process that confers network nodes an accumulative advantage resulting in different logics of connectivity (Powell et al., 2005), or prominence in an organizational field (Rosenkopf & Padula, 2008).

We model preferential attachment by means of two distinct sets of network statistics. To model activity, we introduce “out-degree” and “out-intensity” statistics—both defined as functions of unique receivers for each sender. To model popularity, we introduce “in-degree” and “in-intensity” statistics—both defined as functions of senders for each receiver. While the out-degree statistic is a simple sum of the number of receivers per sender, the out-intensity statistic is a weighted sum of receivers per sender, in which the weights account for both the number of unique receivers per sender, and the temporal relevance of the relation flow of resources form a sender to a receiver. A similar distinction is made between the in-degree and in-intensity statistics.

Reciprocity refers to the tendency of organizations to establish symmetric relations with partners. Reciprocity involves role-switching within a dyad given that partners are simultaneously senders and receivers (Vu et al., 2017). In studies of interorganizational relations, reciprocity is often viewed as a stabilizing mechanism since non-reciprocated relations have an intrinsic tendency to become symmetric or, alternatively, to be dissolved (Rivera et al., 2010). Reciprocity is typically associated with strategies of uncertainty reduction or avoidance because of its capacity to sustain mutual expectations, obligations, and reputation (Laumann & Marsden, 1982; Coleman, 1988; Uzzi, 1997).

In REMs, repetition refers to the tendency of an observed relational event connecting a sender and a receiver to be repeated in the future (Vu et al., 2017). Repeated events within the same dyad is a key feature of relational systems (Freeman et al., 1987). Indeed, prior empirical studies of interorganizational networks have interpreted the tendency of network ties between partners to endure as a condition for developing trust between partners (Gulati & Nickerson, 2008) and as a response to uncertainty (Podolny, 1994; Beckman et al., 2004).

Assortativity refers to the tendency of network nodes to connect on the basis of their similarity or dissimilarity expressed in terms of degree (Snijders et al., 2010) or activity (Vu et al., 2017). Assortative networks are characterized by connections between nodes with similar number of partners or levels of activity. Disassortative networks, in contrast, are characterized by connections between nodes of dissimilar degree (Newman, 2002) or activity (Lomi et al., 2014). Empirical evidence of assortativity is mixed. Whereas interorganizational networks have been usually found to be assortative, recent studies have occasionally found evidence of disassortative mixing (Zhao et al., 2010).

In directed systems of exchange relations, closure may present itself in a number of distinct forms, such as transitivity and generalized exchange (Robins et al., 2009; Lomi & Pallotti, 2013). In general, closure is associated with path-shortening—the behavioral tendency of organizations connected to the same partners to become directly connected (Uzzi, 1997; Kogut & Walker, 2001). In our empirical application we initiate four distinct types of closure-related network statistics—that is, “transitive closure,” “cyclic closure,” “sending” and “receiving balance.” The network statistics associated with the mechanisms of preferential attachment, reciprocity, repetition, assortativity, and closure are illustrated and explained in Table 1. Throughout the paper we keep our focus on the dynamics of direct and indirect reciprocity—here operationalized through a cyclic type of closure.

Model Estimation and Interpretation

Following Cox (1975), we treat the conditional intensity function as a nuisance parameter and estimate the vector of network statistics

To discuss our inference approach, let us consider a general form of partial likelihood—that is,

In many empirical applications, large networks of events produce correspondingly large risk sets. Even if sparsity can be exploited to make computations more efficient, (Vu et al., 2011b and Perry & Wolfe, 2013), the presence of temporal network statistics requires an appropriate approach. To make the partial likelihood inference feasible, we combine stratification (Vu et al., 2015) and nested case-control sampling (Borgan et al., 1995).

Introducing stratification alters the partial likelihood in (3). For the sender-stratified model, parameters in

Under the sampling-based inference approach, for each event or case we randomly sample a subset of nonevents or controls from the current risk set to compute the denominator sum in the partial likelihood (3a). In other words,

Thanks to the sparsity of network statistic changes, a small number of controls is sampled on the basis of Lerner and Lomi (2020b). In the sender-stratified approach that we implement in this paper,

The outcome variable associated with the observed relational event takes value 1 for cases or events and 0 for controls or nonevents, while the explanatory variables are the network statistics

We developed an ad-hoc Java package to produce the nested case-control datasets that feed Cox proportional hazard procedures for the estimation of network effects. An examples of such routines is clogit in R. More details on the sampling steps are discussed in Appendix C.

Even if our REM is defined in terms of a conditional logistic regression, interpreting parameter estimates requires particular care. Quantities of interest like odds ratios can only be interpreted heuristically as the fundamental interdependence among network statistics makes ceteris paribus assumptions particularly implausible. In discussing the results, we provide an interpretation of parameter estimates that is based on the sign and the odds ratios of the parameters. Positive values of parameter estimates reveal an increase in the likelihood of observing the corresponding micro-mechanisms.

A significant and positive value for direct reciprocity, for example, would be taken as evidence that organizations are more likely to select as partners other organizations with which they have exchanged resources in the past. Similarly, a significant and positive value for transitive closure would be taken as evidence that resource exchange is more likely to be observed between organizations sharing the same partners.

Empirical Setting: The European Interbank Market

Banks are required by central financial authorities to hold an appropriate amount of liquid assets as reserves needed to face sudden and unexpected liquidity shortages. However, in the course of their activities, banks do not always manage to satisfy these liquidity constraints. Borrowing liquidity of suitable maturities on the interbank market is a legitimate way to cover liquidity shortfalls. The interbank market allows banks facing contingent liquidity constraints and banks willing to invest excess liquidity to manage their mutual resource dependencies through a technology-based market interface.

The European interbank money market is a specialized market for liquidity that is designed to facilitate exchange of cash equivalent assets through dedicated credit lines. Funds are transferred via high-frequency bank-to-bank transactions that commonly involve the purchase and sale of highly liquid short-term debt securities. These instruments are typically issued in units of at least 0.05 millions and tend to have overnight maturities.

Regarding overnight transactions, we can say that for each market participant liquidity requirements vary continuously during the trading period, and market roles are fluid in the sense that participants may, at any time, decide to buy or sell liquidity.

No single transaction is sufficient to satisfy liquidity requirements once and for all. Banks may participate in the market as sellers when their liquidity requirements are temporarily satisfied and have excess liquid assets.

Several studies have examined the network of credit relations between European banks. In the typical empirical paper, the network of trading relations is reconstructed by aggregation of events into network ties, which is done by considering individual transactions as expressions of durable trading relationships. De Masi et al. (2006) and Iori et al. (2007), for example, examined the presence of clustering in the aggregate network of interbank transactions. Iori et al. (2008) and Finger et al. (2013) showed that the interbank market exhibits random network qualities at the daily scale, with systematic structures emerging over longer periods like months or quarters. In this regard, Bianchi et al. (2020) have recently shown that quarterly-based patterns of reciprocal exchange are sensitive to exogenous shocks induced by changes in the global economic scenario. However, in these studies doubts linger that the empirical regularities reported could in fact be the product of aggregating sequences of transactions—at the daily level in the case of Iori et al. (2008), or according to “various horizons of time aggregation” in the case of Finger et al. (2013). This point is illustrated and discussed in a recent study comparing estimates of REMs and SAOMs on data of the interbank money market collected between 2006 and 2009 for the specific purpose of documenting changes in market micro-structure brought about by the financial crisis (Zappa & Vu, 2021).

By avoiding time aggregation, REMs afford exploration of potential differences between short- and long-term patterns of interaction—without treating the latter as a necessary consequence of the former. In available studies on the European interbank market the focus on market efficiency encourages an interpretation of short-term variations as random fluctuations around a long-term equilibrium rather than structural signals requiring autonomous interpretation.

In the context of the present study, the interbank money market provides a particularly useful and stringent testing ground for models of interorganizational exchange based on relational events. Useful, because REMs help to reveal the micro-organizational structure of the market starting from individual transactions. Stringent, because the high-frequency of the transactions allows us to test the model under extreme empirical conditions. The purpose of the replication study that follows the main empirical illustration is to explore the extent to which the REMs may be specified and estimated on more conventional interorganizational settings—that is, settings characterized by more durable collaborative relations produced by more complex and less intermittent coordination requirements among health care organizations (Provan & Milward, 1995). The replication study is particularly useful also for testing the properties of a model explicitly designed for the analysis of samples of hundreds of thousands—perhaps even millions of observations (Lerner & Lomi, 2020a)—when “scaled down” to analyze much smaller samples containing few thousands—or even only few hundreds—of observations (Breiger, 2015).

Data

The data that we use in the main empirical illustration contain information on time-stamped unsecured interbank transactions recorded on the e-MID trading platform in 2006. The e-MID electronic interface serves as the reference marketplace to trade interbank liquidity in Europe. Thanks to its special real-time gross settlement system, e-MID guarantees that liquidity is available at a low price and managed flexibly. Availability of liquidity and its low price are assured by the reserve maintenance system operated by the European Central Bank. The e-MID trading platform is open every day from Monday to Friday and from 9 am to 5 pm. During the 30 min that anticipate the opening and follow the closure, it is also possible to exchange liquidity, and occasionally banks trade liquidity before 9 am and after 5 pm. So, every day, the trading activity is concentrated within 9 hours. Demand and supply of liquidity are updated every few minutes or seconds in high-frequency markets like e-MID. For instance, during the year 2006, within the typical trading day, the inter-arrival time between two consecutive transactions is, on average, 89.4 seconds.

We follow prior studies based on the same data source (see, e.g., Finger et al., 2013; Fricke & Lux, 2015; Bianchi et al., 2020) and restrict the analysis to the set of transactions taking place in the overnight segment of the European interbank money market, where credit extensions need to be paid back by the beginning of the next trading day. The e-MID overnight market offers a comprehensive view of interbank lending, and represents about 85% of the total volume of loan contracts exchanged on the market (Beaupain & Durré, 2008).

Besides its importance in terms of size, the analysis of the overnight segment is relevant also to the understanding of trading dynamics in the European interbank market. Thanks to high-frequency transactions, the overnight market absorbs short-term liquidity shocks and progressively adjusts the liquidity positions of credit institutions. Moreover, and more substantially, in short-term loans utilitarian motivations to trade prevail over speculative ones, thus reinforcing the relationships among credit institutions. Both these features make the overnight segment of the European interbank market an ideal empirical setting to investigate the emergence and development of distinct micro-mechanisms of exchange that emerge from the collection of time-stamped relational events.

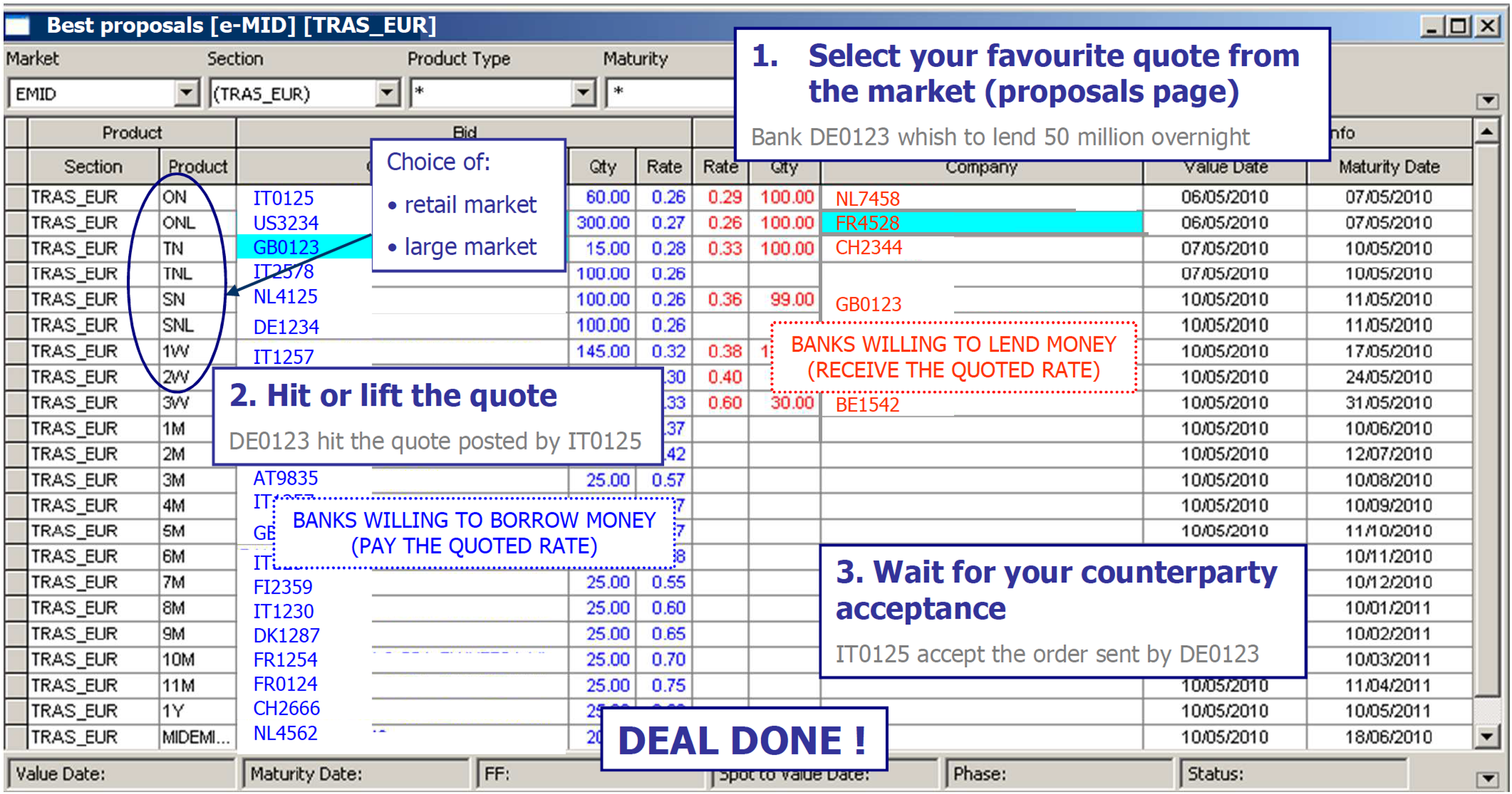

The e-MID market takes the form of a multilateral screen-based trading platform where registered banks can electronically transfer interbank deposits by adhering to the market regulation. Trades are public in terms of duration, amount, rate, and time. The e-MID trading system is quote-driven. Market participants that are willing to trade can reveal their intentions to the market by posting a quote (direct order) specifying the setting of the credit contract. The market operator in this position is called quoter. If the deal is attractive for another market actor, this can actively hit the pending quote, disclose the identity of its potential trading counterpart, and eventually send the order back to close the deal. The market operator is this position is called aggressor. A snapshot of the e-MID trading mechanism is illustrated in Figure 2. On the e-MID market, banks know, at each instant in time, what banks are available to trade and what banks have reached a market deal. In other words, banks receives real-time updates on who trades with whom, then revealing social motivations to trade with direct and indirect counterparts.

The emergence of local dependence structures from time-ordered sequences of relational events.

Trading mechanism on the e-MID platform.

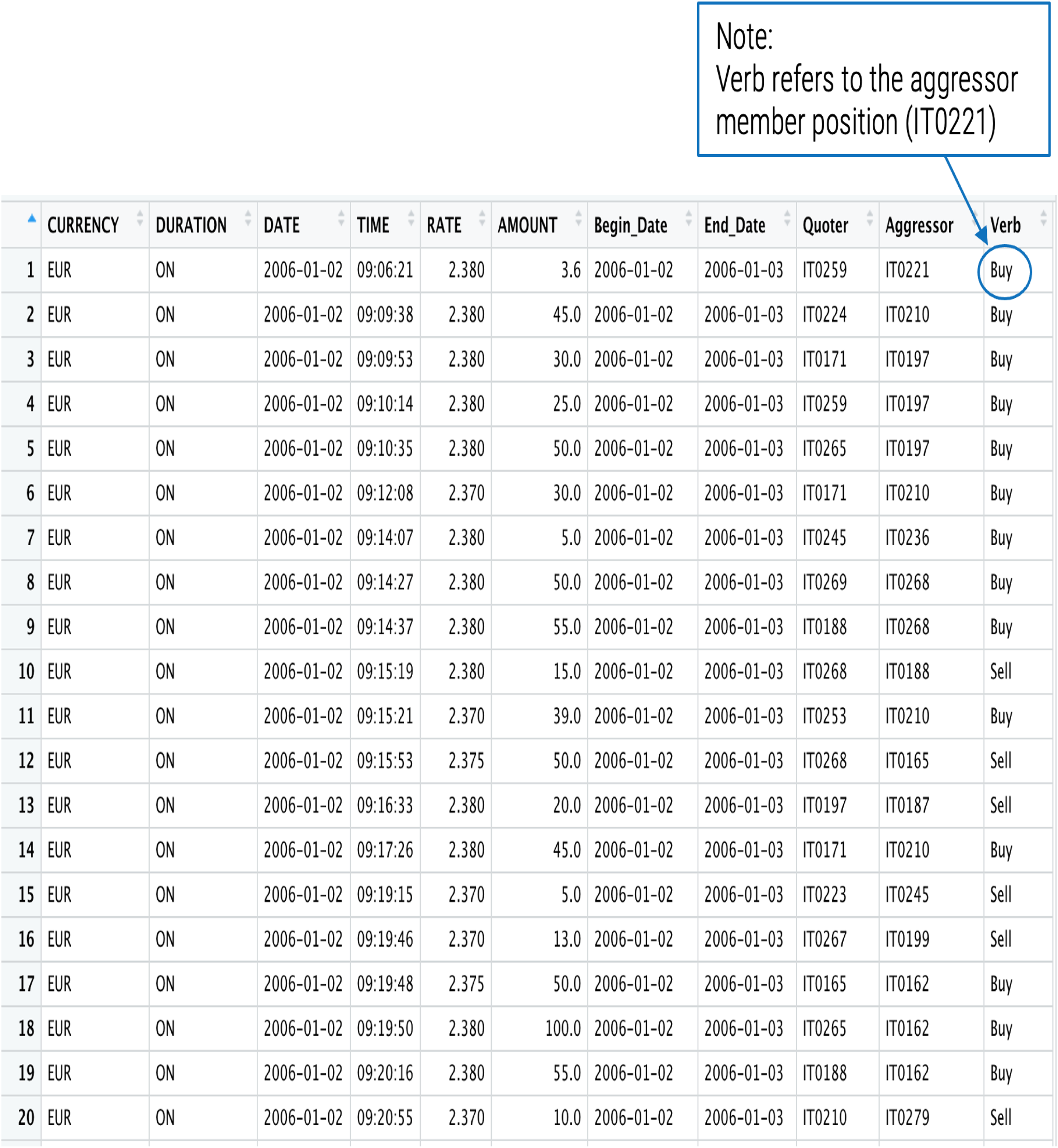

The output of e-MID trading is a time-stamped dataset like that depicted in Figure 3. Each row in the dataset is a transaction that is public in terms of duration, time (precise to the second), amount (in millions of EUR), and rate. The identity of the banks involved in the trading of overnight funds is provided by unique identification codes that reveal banks’ country of origin and their role. Lenders and borrowers of liquidity are identified on the basis of aggressors’ side of the market. Banks that lend liquidity have a sell label, while banks that are in need of borrowing liquidity have a buy label.

Distinctive features of e-MID transactions. Quoters and aggressor are market roles of e-MID market participants. Senders are liquidity lenders and receivers are liquidity borrowers. By design, pay back transactions are not reported in the available dataset.

Our sample consists of 90,368 overnight transactions occurred in year 2006 among 172 banks. Transactions are not uniformly distributed within the 255 trading days. The daily number of observed transactions ranges from 135 to 570, with an average of 354.38 transactions per day. Among the 172 organizations that are active on the e-MID market, only 158 credit institutions act as lenders of overnight liquidity. Transactions are not uniformly distributed among lenders. The trading activity of the 25 most active lenders is 56.22% of the whole credit extensions and this percentage increases to 78.31% when considering the first 50 most active lenders. The distribution of overnight transactions per sender is then very skewed to the right, with few credit institutions having many more transactions than the average value.

Orienting Questions

The empirical analysis is guided by the general idea that temporal configurations of event sequences have predictive value for future events. The focus of the empirical analysis narrows on configurations of event sequences that extant studies of interorganizational dependence and exchange relations have connected to social mechanisms of theoretical relevance. More specifically, we ask three questions of broad theoretical relevance and contextual empirical interest. The first is: To what extent are exchange relations between banks reciprocated? In other words, how stable are the institutionally defined roles of “lender” and “borrower” that make market transactions possible? This question is important because the stability of market roles is a core feature of markets as institutions designed to facilitate exchange (White, 1981; Leifer, 1988; Podolny, 1994; Leifer & White, 2004). The answer to this question depends on the propensity of the banks to reciprocate lending relations or, in other words, the propensity of borrowers to lend liquidity to their lenders. When this happens, reciprocity erodes the boundaries defined around market roles.

The second question is: To what extent is reciprocity restricted to the parties directly involved in a financial transaction? Generalized reciprocity—also known as generalized exchange (Bearman, 1997)—emerges when direct reciprocity transcends the boundaries of the parties involved in a specific transaction, and gives rise to a cyclical sequence of events. This question is important because: “In generalized exchange, the rewards that an actor receives usually are not directly contingent on the resources provided by that actor; therefore free riding can occur” (Yamagishi & Cook, 1993, p. 235). The answer to questions about generalized exchange depends on the possibility to identify transactions that “flow through all parties in a cycle before a giver can become a taker” (Bearman, 1997, p. 1389).

Finally, we ask: To what extent are future transactions embedded in transitive sequences of past transactions? In other words, to what extent sharing partners is predictive of direct exchange? This question is important because triadic closure of this kind is frequently associated with the presence of trust (Coleman, 1988) and hierarchical order (Lerner & Lomi, 2017)—all essential elements that support market exchange by diffusing reputation and curbing opportunistic behavior (Williamson, 1979; Bradach & Eccles, 1989; Powell, 1990). The answer to questions about transitivity depends on the possibility to identify sequences of transactions between banks sharing the same transaction partners.

The tendency of interorganizational exchange events to become more or less likely when embedded in reciprocated, cyclic, and transitive sequences of past exchange events is what we examine in the empirical parts of the paper that follows. These forms of historical embedding are important not only for their predictive value, but also because they may sustain role fluidity (direct reciprocity), generalized exchange (indirect reciprocity), and cohesion (transitive closure). These are fundamental mechanisms underlying market exchange when the trustworthiness of potential exchange partners must be assessed, but cannot be directly observed. This is a theme of general importance in the study of exchange relations between organizations operating in financial markets (Podolny, 1994). A number of studies are available that demonstrate the direct relevance of these questions also for organizations operating in a considerable variety of different environments (Shipilov & Gawer, 2020), including organizations in the field of healthcare (Scott, Ruef, Mendel & Caronna, 2000)—the field that provides the context for our replication study.

Empirical Illustration

We estimated two models, both including degree- and intensity-based effects. Degree-based network statistics are computed by counting the number of local structures induced by time-ordered sequences of relational events as shown in Figure 1. Their intensity-based counterparts are computed by weighting the network effects through a temporal decay parameter

We add to our model specifications a monadic covariate indexing the nationality of each bank to control for home bias in exchange partner selection—a well-known tendency in financial markets (Strong & Xu, 2003).

In the baseline model (M0) the effects of interest are computed over the entire observation period. In the full model (M1), the same effects are computed over two distinct temporal frames to capture the trading dynamics in the short- and long-term, respectively. In our empirical application, short-term effects are computed by counting the network configurations of interest within a temporal frame of one trading day—that is, approximately 9 hours (8:30 am–5:30 pm). The corresponding long-term counterparts are computed with respect to the whole trading year 2006. In an empirical setting where trading occurs on a high-frequency scale and loan contracts have overnight duration, setting the short-term framework equal to one business day is a natural choice.

For the purposes of our illustration, the decay parameter

Best empirical practice suggests choosing recency and decay parameters with reference to the empirical setting that is being examined (see e.g., Amati et al., 2019), and using heuristic methods based, for instance, on grid search (Daley & Vere-Jones, 2003).

In the current section, we discuss empirical results that refer to direct reciprocity, generalized exchange, and transitivity because of their substantial relevance in generating more complex micro-mechanisms of connectivity as well as desirable systemic outputs like, for instance, cooperation, cohesion, and trust. We also comment briefly on the analysis of repetition, the core social mechanism in sequences of relational events.

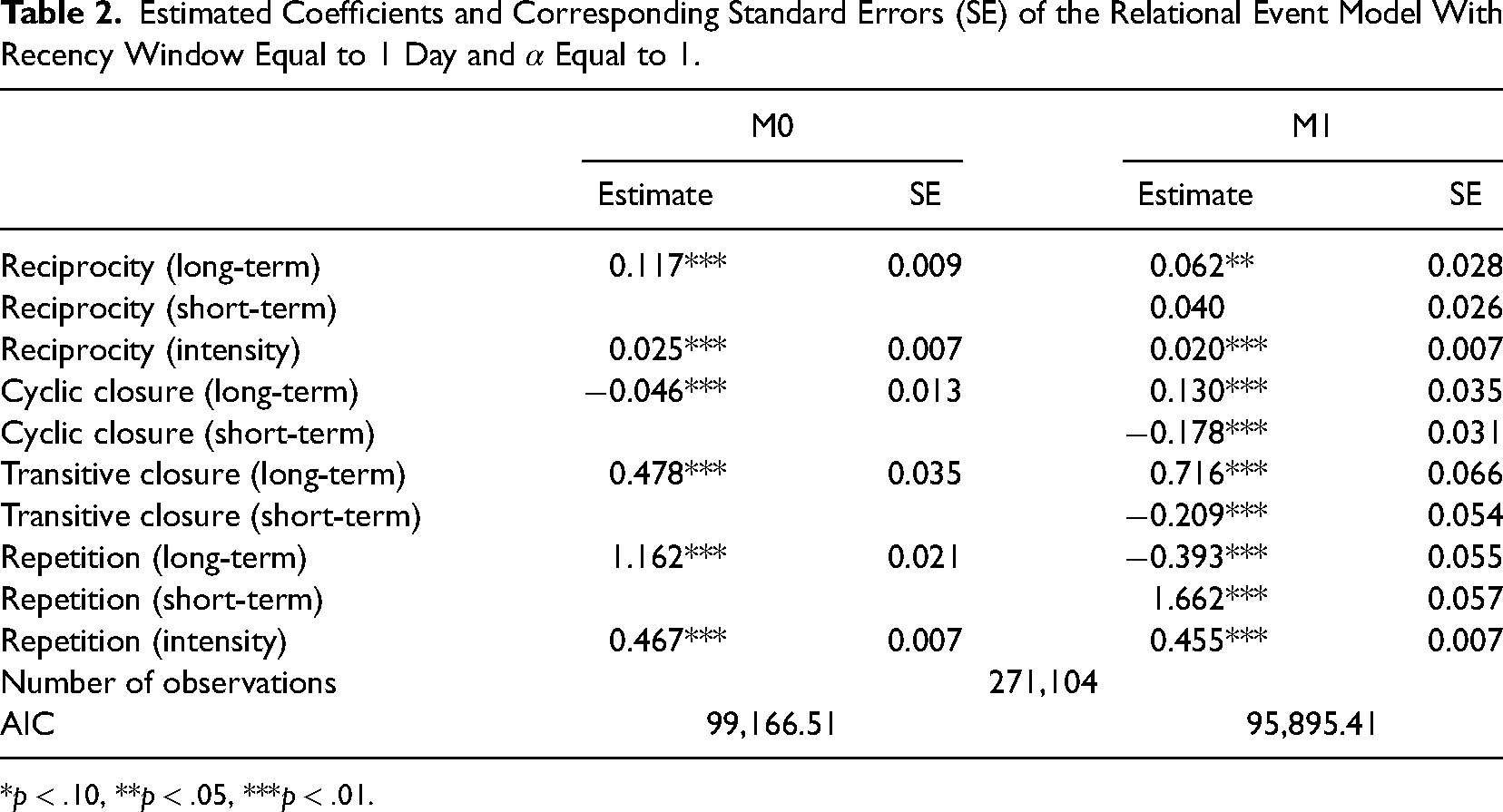

The full empirical estimates, and the complete commentary to all the degree- and intensity-based effects included in both models M0 and M1 are reported in Appendix A in Table A1. Details on the estimation procedure and on the nested case-control sampling scheme in particular may be found in Appendix C. In line with our orienting questions, below we focus on the effects of direct theoretical interest related to direct and generalized reciprocity, transitivity, and repetition. While commenting empirical results that are reported in Table 2, we emphasize the differences between short- and long-term effects, and between degree- and intensity-based patterns of reciprocated exchange.

Estimated Coefficients and Corresponding Standard Errors (SE) of the Relational Event Model With Recency Window Equal to 1 Day and

*

We propose a heuristic interpretation based on odds ratios since our REM has been ultimately defined as a conditional logistic regression for matched case-control data. For parameter estimates associated with network effects of specific theoretical interest, we also report what we call the “odds for high values”—a term that refers to the odds computed at two standard deviations above the mean of the value of the corresponding network statistic. We do so to provide a sense of the range of the strength of the effects implied by the empirical estimates.

The odds implied by degree-based direct reciprocity (

The tendency toward reciprocity emerges also when considering intensity-based reciprocity—that is, reciprocation of transactions occurred within recurrently trading dyads. While degree-based reciprocity captures the simple propensity of European banks to switch their roles of buyers and sellers, intensity-based reciprocity reveals the tendency towards reciprocation within well-established trading partners. The odds for intensity-based direct reciprocity (

Jointly interpreted, the estimates of direct reciprocity parameters suggest that European banks participate in e-MID trading platform both as buyers and sellers. The tendency toward direct reciprocity is particularly notable with occasional trading partners, and in the presence of high levels of interaction, thus revealing that being active members on both sides of the market interface is a strong signal of creditworthiness. However, the estimates of intensity-based direct reciprocity reveal that, with well-established trading partners, European banks usually stick to either market roles, then suggesting that direct reciprocity works as a resolution mechanism aimed at satisfying unexpected liquidity needs. In summary, the estimates reveal that market roles tend to be stabilized by repeated transactions with the same partner.

When analyzing the temporal dynamics of generalized reciprocity, we narrow our focus on cyclic closure, or generalized exchange. Model M0 suggests evidence against the presence of generalized exchange during the whole period of observation. We notice that the odds of observing a direct transfer of liquidity from the former borrower

M0 reveals a general tendency of e-MID traders toward transitive relations. The odds implied by transitive closure (

Finally, we comment on the results related to the baseline tendency toward repeated events or “repetition.” The odds for degree- and intensity-based repetition are both positive and reveal the overall tendency towards repetition of past trades with the same partner. More specifically, for any pair of trading banks

In M1, we compute degree-based effects over different time frames that define short- and long-term network statistics. Long-term statistics count the number of configurations of interest during the full observation period, while short-term statistics evaluate the same configurations during one trading day.

A likelihood ratio test for nested models suggests that introducing short- and long-term network effects in M1 (log-likelihood =

As empirical results in M1 document, distinguishing between short- and long-term effects is crucial to highlight that the micro-mechanisms that bring buyers and sellers together on the trading floor do not evolve uniformly over time.

Past reciprocated transactions have a positive impact on future transactions both in the short- and in the long-run, thus signaling that reciprocity operates to support and facilitate resource exchange over multiple temporal frameworks. Interestingly, a positive parameter estimate associated with short-term repetition suggests that the tendency of current transactions to affect future transactions plays out over a single trading day. Surprisingly, within the same dyad, the stream of transactions is not uniformly distributed over longer terms, then suggesting that liquidity needs are usually adjusted within shorter temporal horizons by linking with either occasional or well-established trading partners—as the positive but weaker intensity-based repetition parameter shows.

Empirical results supported by M0 and M1 provide clear answers to our orienting questions. First, direct reciprocity emerges quickly in exchange relations. Its influence remains detectable over longer time periods and operates regardless of trading partners. However, generalized exchange takes longer time to emerge. Indeed, in the long-run, the positive tendency towards generalized reciprocity emerges contextually with weaker tendencies towards direct reciprocity—a result supporting the idea that actors receive a reward that is contingent on its network of direct and indirect borrowers, rather than on the resources in the exchange system. These findings are coherent with the dynamics of transitive closure emerging in the longer run as a stabilizing maket form.

Replication Study

Financial markets are not unusual empirical settings for management and organizational research (Baker, 1984; Abolafia & Kilduff, 1988; Podolny, 1994; Park & Podolny, 2000). Because of their very high frequency, intermittency, and volatility, however, financial transactions are rarely considered representative examples of interorganizational relations despite considerable research arguing—and demonstrating—the opposite (Knorr-Cetina & Bruegger, 2002; Knorr-Cetina & Preda, 2006; Abolafia, 2020). Does the model we have discussed apply only to high-frequency exchange like financial transactions?

To address this question, we now replicate the model estimated in the prior section on data on low-frequency collaborative patient-sharing relations among health care organizations. Patient-sharing is a well-recognized and extensively studied collaborative relation connecting organizations in the field of healthcare (Iwashyna et al., 2009; Veinot et al., 2012; Herrigel et al., 2016). Patient-sharing happens when a hospital decides to involve a partner hospital in the resolution of a clinical case (Lomi & Pallotti, 2012). As such, patient-sharing is almost an archetypical form of interorganizational collaboration involving significant levels of explicit communication and coordination between partners (Provan & Milward, 1995). Interhospital patient-sharing and transfer relations are frequently represented as interorganizational networks (Amati et al., 2021; Iwashyna et al., 2009).

The data we analyze in the replication study is extracted from a larger comprehensive database that has supported prior studies of inter-hospital coordination and patient-sharing. For detailed information on the empirical context, we refer readers to published articles based on the original data (Lomi et al., 2014; Stadtfeld et al., 2016; Mascia et al., 2017; Kitts et al., 2017; Amati et al., 2019).

The dataset consists of 3,264 patient-sharing events occurred over a period of 2 years among 31 hospitals located in a regional community located in Southern Europe. Each hospital is associated with a nodal covariate known as “Local Health Unit” (LHU) indicating the membership of each hospital to one of the administrative/territorial units in which the region is partitioned. The analysis is developed specifically for this paper for the purpose of demonstrating the flexibility of the model, and establishing its analytical value across empirical settings. More specifically, in this replication study we seek to (i) establish the general empirical value of differentiating between degree- and intensity-based effects and especially between short- and long-term network effects in conventional interorganizational settings; (ii) demonstrate that the insights of the model are not dependent on the underlying event rate, and (iii) show that the sender-stratified nested case-control sampling scheme can be flexibly adapted to samples with an event space of very different size. In particular, the replication study demonstrates that the model scales up, and just as easily “scales down” to event networks with a small number of nodes connected by low-frequency events (Breiger, 2015).

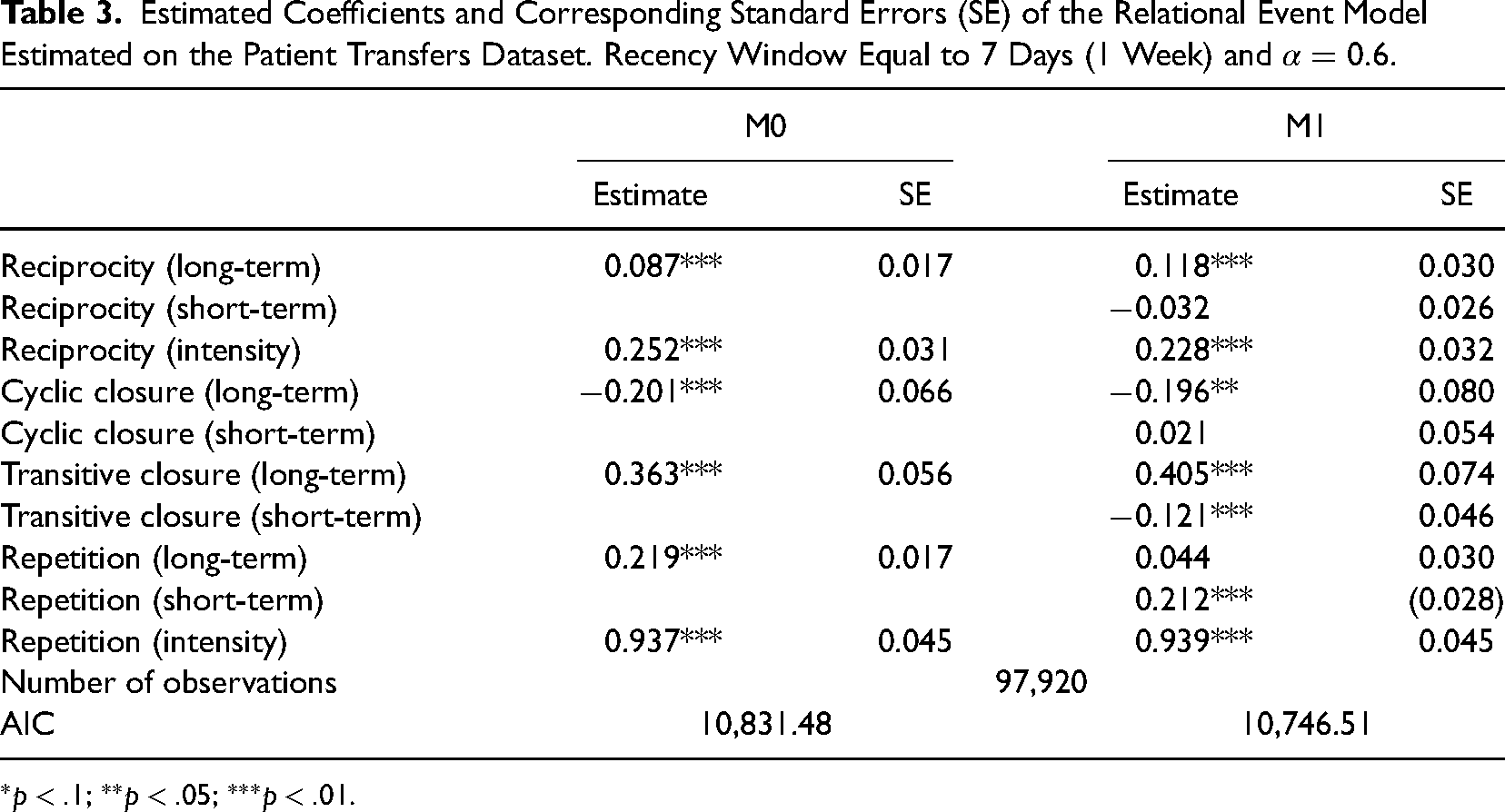

In the replication study we keep the same model specification as in M0 and M1 to make the two analyses directly comparable. However, because the granularity of patient-sharing events is much lower than high-frequency trading—few patient-sharing events versus thousands of credit extension per day—we differently tuned recency and temporal decay parameters. In this regard, the current empirical illustration provides some guidelines on how to parameterize recency and decay parameters from statistical as well as empirical considerations.

Following prior empirical studies (Amati et al., 2019), we set the recency parameter for short-term statistics equal to 7 days and the decay parameter equal to 0.6—that is, the value of

Differences in the event rates provide a unique opportunity to test the flexibility of our sampling scheme based on sender-stratified, nested case-control sampling. Given that the network has only 31 nodes, for each observed event, we sample the whole set of nonevents. For each observed patient-sharing event we sample all the 29 possible nonevents that could have occurred between the sender and all its 29 potential counterparts. It is straightforward to adapt our case-control sampling strategy to cases where sampling is not needed as all the possible nonevents may be considered.

Empirical estimates are reported in Table 3. To facilitate the comparison of results between the two empirical examples, we focus on the dynamics of direct and indirect reciprocity when discussing the new empirical estimates. As in the prior analysis, it is important to keep in mind that the interpretation of the estimates is essentially heuristic. Comparative assessment of statistical significance of parameter estimates is only qualitative, and has to be understood in the context of samples containing a very different number of observations.

Estimated Coefficients and Corresponding Standard Errors (SE) of the Relational Event Model Estimated on the Patient Transfers Dataset. Recency Window Equal to 7 Days (1 Week) and

The odds implied by long-term degree-based reciprocity in model specification M0 (

Patient-sharing is not significantly shaped by generalized exchange. The odds implied by cyclic closure (

The absence of cyclic structures in the patient-sharing network is balanced by a strong preference toward transitive closure. The odds implied by transitive closure (

Predictably, the parameter associated with the repetition of patient-sharing is considerably smaller than its counterpart for bank transactions. The parameters associated with repetition of patient-sharing—in its degree- and intensity-based forms—are both positive, thus singling the overall tendency of hospitals to share patients with specific partners. The odds implied by long-term repetition (

The distinction between short- and long-term effects in M1 reveals crucial insights on variations in the internal time structure of network mechanisms. While short-term reciprocity is not significant in both empirical settings, the magnitude of long-term degree-based reciprocity for hospital data is twice as large as its counterpart for overnight bank transactions. The odds implied by long-term degree-based reciprocity (

The positive effect of transitive closure is present in both empirical settings in the long-run. Patient-sharing events tend to be organized around clusters of organizations that preferably share resources with the partners of their partners. In contrast, transitive closure does not emerge across shorter temporal frames, thus suggesting that, in the short-term, two-paths do not tend to generate transitive triads.

Discussion and Conclusions

Exchange relations between organizations are frequently reconstructed as networks of interdependent network ties (Lomi & Pattison, 2006). This analytical strategy has sustained important theoretical progress and considerable empirical success in studies of interorganizational exchange and dependence relations (Galaskiewicz & Wasserman, 1989; Galaskiewicz & Burt, 1991; Mizruchi & Galaskiewicz, 1993), and in the analysis of social networks more generally (Borgatti et al., 2009; Brass et al., 2004; Butts, 2009; Robins & Kashima, 2008; Snijders, 2011). Theoretical progress and empirical success have contributed to cast aside problems inherent in the aggregation of time-ordered sequences of relational events into network ties (Freeman et al., 1987; Marsden, 1990). The point-process variant of the REM that we have introduced, discussed, and illustrated in this paper is an attempt to establish a principled analytical framework to address this issue by avoiding the information loss implied by time aggregation in the analysis of interorganizational relations (Vu et al., 2017).

What makes relational event models “social” is their focus on complex temporal dependencies arising from flows of events linking senders and receivers of action, and their ability to connect these dependencies to specific social mechanisms of theoretical interest (Butts, 2008). In this sense—and despite the distinctive differences that we have discussed—the purpose of REMs is broadly consistent with that of other statistical models for the analysis of social networks based on assumptions of dependence about network ties (Pattison & Robins, 2002; Snijders et al., 2006; Snijders, 2011).

While summarizing the current methodological debate on statistical models for network dynamics (Stadtfeld et al., 2017), we have emphasized three distinctive advantages of event-oriented models for networks. The first is that REMs maintain all the information available about the natural time-order of events. This happens because relational events are directly observable, while network ties typically are not. This feature makes REMs particularly appropriate to study dependence and exchange because who depends on whom ultimately depend on the order of exchange events over time. The second advantage of event-oriented models is that they facilitate the inclusion of information on the intensity—and not just the presence or absence of a relation linking senders and receivers. This feature makes REMs particularly useful in the empirical analysis of connected organizational systems with a skew distribution of relational intensity—that is, systems where a limited number of organizations account for a disproportionate share of the overall volume, or flow of resources being exchanged. The third advantage of event-oriented models is the possibility they offer of distinguishing between short- and long-term effects of past events on the probability to observe future events. This feature makes REMs uniquely useful in examining how the contextual effects of generic theoretical network mechanisms—such as, for example, direct and generalized reciprocity, and transitivity—operate differently over time.

An additional advantage that we have not stressed enough in this paper, but not for this less important, is computational. The case-control sampling approach that Vu et al. (2015) and Lerner and Lomi (2020b) proposed and that we have re-implemented in the context of a sender-stratified REM, allows the analysis of connected systems at a level of scale that is not currently accessible to more established statistical models for network ties—but see Stivala et al. (2020) for important progress on this front. The possibility of scaling up the model to sample sizes typically beyond the reach of more conventional statistical models for networks, brings to the fore the problem of unobserved heterogeneity. The sender-stratified specification that we have implemented is designed to address this issue.

The purpose of this work is neither comparing competing models for relational events, nor claiming superiority for one specific class of statistical models for networks over models based on alternative representations. Within the class of REMs, we think the stratification and sampling procedures that we have outlined may have considerable analytical advantages when the focus is on exchange processes and mechanisms. Readers interested in the current discussion on comparing competing statistical models for networks can refer to the recent specialized literature on the topic (Butts, 2017; Stadtfeld et al., 2017; Block et al., 2018, 2019b, 2019a). For the less ambitious purposes of this paper, we recognize that different definitions of network “ties” and different models are not only possible (Borgatti & Halgin, 2011), but are differently appropriate depending on the research questions being asked—and on the understanding of the core structural features of underlying social and organizational setting that is being observed (Borgatti & Foster, 2003; Borgatti et al., 2009). Narrowing this general discussion to event-oriented network models, we think readers would be well advised to refer to the classic works of Freeman et al. (1987) and Marsden (1990) for foundational statements on the relation between social “events” and social “ties.” We believe the case studies that we have developed illustrate well the empirical value of the model we propose. In an analysis of a large number of transactions linking buyers and sellers of liquidity on the electronic market for interbank deposit (e-MID), we have found that direct reciprocity works in the short- but not in the long-term. In other words, direct reciprocity stabilizes transactions between lenders and borrowers only in the shorter term. The reverse is true for generalized reciprocity—that is, transactions embedded in cyclic sequences are unlikely to be observed in the short term—but significantly more likely to be observed in the long term. In other words, generalized reciprocity stabilizes transactions between lenders and borrowers only in the longer-term—a result that models where relations are represented as timeless are likely to hide. In the replication study, differences in event rates provide a unique opportunity to test the flexibility of our model and the generality of our sampling scheme. We have found that mutual patient-sharing operates more strongly in health care organizations, while generalized reciprocity does not appear to affect patient-sharing among hospitals in the community. Transitivity emerges only in the long-term. Even if to a lesser extent, patient-sharing events tend to be organized around clusters of organizations that preferably share resources with partners of their partners.

In more general terms, the results supported by both empirical illustrations are consistent with a theoretical view of network effects as results of collective learning processes where actor slowly discover—while at the same time construct the structural features of their social environment. The fact that network mechanisms do not work instantaneously simply reflects this learning process. Clearly, certain structures are more difficult to learn than others—a view that is perfectly consistent with classic behavioral theories of expectation formation and search (Cyert et al., 1958; Levinthal & March, 1981). We think that this area of research at the intersection of network and behavioral theories of organizations is completely open.

How do the methodological advances that our model forwards might be usefully applied to areas of organizational and management research other than the analysis of interorganizational exchange relations? As an example of specific answer that may be provided to this general question consider Ingram & Morris, 2007 study of socialization at a “mixer party” attended by business executives. Analysis of socialization during the social event reveals that social selection based on homophily—that is, the tendency of individuals to select partners similar to themselves—did not operate homogeneously over the “life of the party.” For example, gender-based homophily operated in the early stages of the social gathering, but not later. Physical attractiveness produced opposite time-dependent patterns of social selection—that is, tended to operate later in the party rather than earlier. This study provides solid evidence that social selection mechanisms do not operate homogeneously over time. The study also demonstrates with unique clarity the risks of modeling social mechanisms and social relations as timeless rather than as contingent on specific times (when) and places (where) people meet (Abbott, 2007). Without information on the exact timing of individual social encounters, the authors would have concluded that tendencies toward homophily were absent during the party. The availability of continuous-time data made possible by electronic tags worn by participants revealed that this average conclusion would have masked the time structure of social events. The empirical case studies that we have presented support similar conclusions—and provide solutions that are generally applicable.

The REM that we have introduced in this paper makes full use of the information contained in the timing of relational events. These models may be specified, for example, to test hypotheses about what social selection mechanism operates faster, and what mechanism is likely to emerge in the longer term. How network mechanisms change over time is an active area of research that relational event models are opening (Amati et al., 2019). The specification of the time decay parameter facilitates the exploration of the link between broad theoretical predictions about how network mechanisms operate, and contextual features of the data or the institutional setting (Kitts et al., 2017). More generally, the possibility of distinguishing between short-term and long-term effects and between degree-based and intensity-based effects considerably increases the accuracy and expressiveness of REMs (Lomi & Larsen, 2001, pp. 11-12).

The comparative empirical experience that we have discussed suggests that longitudinal studies of interorganizational networks will have to pay particular attention to the internal time structure of the core phenomena under observation. Given a fixed observation period, settings characterized by high-frequency events—for example, financial markets—will produce a larger number of observations than settings associated with lower frequency events—for example, interorganizational fields. This minimalist implication of our comparative empirical analysis has far reaching consequences for future studies of dynamic networks. Differences in the number of observations will result in differences in statistical power—and hence differences in the ability of empirical models to detect significant variations in the data. The same model fitted to samples of events produced by data-generating processes working at different speed will produce results that may not be directly comparable. What we have called the minimalist implication of our study is important also because network mechanisms sustained by different forms of local dependence—for example, “reciprocity,” “transitive closure,” or “generalized exchange”—are likely to be characterized by different internal time structures—with simpler mechanisms generating events at faster rates. If this is the case, the time aggregation imposed by discrete-time observation schemes is likely to induce forms of time-heterogeneity whose effects on estimates of models for panel data may then be difficult to identify. The problems posed by time aggregation are not new (Tuma & Hannan, 1984). However, we are not aware of studies that have examined systematically the implications of time-aggregation in the context of dynamic models for networks.

Much work remains to be done in order to increase the appeal of REMs which are derived from event history analysis with which they share advantages and limitations (Blossfeld et al., 2019). At the moment, we see three main constraints on the widespread adoption of REMs in organizational research.