Abstract

In a series of experiments, we investigate if lowering the income tax rate on pensions increases savings. Our results show that reducing the tax rate on pensions has minimal impact on saving behavior. However, when we manipulate the current tax rate for savings deduction, subjects adjust their savings accordingly. This suggests that individuals tend to overlook the impact of income taxes on pensions. Furthermore, our findings highlight that governments can raise after-tax pensions without altering tax revenues by shifting from deferred to immediate pension tax systems.

Introduction

Demographic changes, in the sense of low fertility on the one hand and increased life expectancy on the other, have a major impact on pension reforms and policies (OECD 2017). Although various countries offer a variety of incentives to save for retirement, many countries face an ongoing retirement savings crisis (Benartzi and Thaler 2013). For example, 50% of American households are at risk of not having sufficient funds to maintain their preretirement standard of living once they stop working (Munnell et al. 2021). Thus, it is particularly important to understand whether existing saving incentives are effective at all. This study examines the effectiveness of lower income tax rates on pensions to incentivize retirement saving using a series of experiments.

Due to both the progressivity of the income tax system and the special tax treatment of retirement income (e.g., through extra tax allowances or tax credits for older people), the income tax rate applied to pensions is often lower than that applied to working income (OECD 2017). Under the widely used deferred taxation of pensions, retirement contributions are tax deductible, returns on contributions are tax exempt, and pensions are taxed. Therefore, applying a tax rate to pension income that is lower than the tax rate at which contributions are deducted should create an incentive to save (OECD 2018b: 48). Suppose, for example, that an individual’s time preference rate equals the rate of return on his or her retirement savings, contributions are deductible at 30% and pensions are taxed at 15%; in this case, the return on a $1 contribution amounts to

In this vein, it has generally been argued that lower tax rates on capital income encourage saving (e.g., Summers 1984; Hausman and Poterba 1987). However, the economic theory is ambiguous. First, rational choice theory predicts that an opposing income effect may offset or even overcompensate for the substitution effect; thus, savings may also remain unchanged or even be reduced when the income tax rate on pensions (hereinafter the pension tax rate) decreases (e.g., Power and Rider 2002). Second, from a behavioral economics perspective, a reduction in pension tax rates may have no effect at all, representing a particularly ineffective and costly subsidy. This is because individuals may either ignore taxes altogether, using simple heuristics such as consistently saving the same percentage of pre-tax income (Beshears et al. 2017), or underweight only pension taxes due to myopia or confirmation bias; i.e., people may pay attention to information that confirms their saving intentions (their tax refunds) but underweight information that contradicts those intentions (pension taxes) (Feldman and Ruffle 2015; Feldman et al. 2018; Blaufus and Milde 2021).

Prior empirical evidence on the effect of tax incentives on overall private savings is inconclusive. Some studies find that overall savings increase, while other studies find that individuals only reallocate their savings in response to tax incentives (for an overview, see OECD 2018a: 85–91). However, it is almost impossible to clearly identify the effect of saving incentives with observational data (Engen et al. 1996). In contrast, using an experiment, (1) we are able to manipulate current and future tax rates, (2) we can provide individuals with information on tax rules in advance to ensure that the observed behavior is not due simply to a lack of tax knowledge, and (3) we can control for investment alternatives and thus prevent the problem of tax incentives, possibly resulting in simply a shift between tax-privileged investments and other investments. Thus, our study provides causal evidence on the effect of pension tax reductions. By definition, this benefit comes at the price of a certain degree of abstraction.

In total, more than 1,100 native German speakers, with an average age of 40, took part in our online experiment examining the impact of pension taxation on savings. The subjects had to make incentivized savings decisions in a life-cycle model containing seven saving periods with different income levels and three pension periods in which the subjects received income only from their previous savings. The pensions were subject to deferred taxation. In a between-subject design, we manipulated the incentive to save by either changing the pension tax rate while holding constant the tax rate at which contributions were deducted (hereinafter the tax refund rate) or by changing the tax refund rate while holding the pension tax rate constant.

Surprisingly, our findings show that reducing the pension tax rate has almost no significant effect on saving behavior, although we substantially increased the incentive to save from

Our study contributes to research on the effectiveness of tax incentives to encourage retirement saving (e.g., Beshears et al. 2017; Power and Rider 2002; Chetty et al. 2014; Tschinkl et al. 2021; Cuccia et al. 2022; Messacar 2023; Duffy and Li 2024). Regarding tax policy, our findings suggest that governments that aim to increase retirement savings should not rely on lower pension tax rates but should instead increase incentives that directly arise in the saving period. However, the effect of an increase in the tax refund rate is also modest. For example, even for a large increase in the tax refund rate from zero to 45% (with the pension tax rate held constant at 30%), the savings rate increases by only 5.3 percentage points. In contrast, we show that changing the tax treatment from deferred taxation to a theoretically equivalent immediate taxation that applies to retirement savings but not pensions significantly increases effective savings by 7.2 percentage points. The observed difference between immediate and deferred taxation is large. In our experiment, only if pension taxes are halved (from 30% to 15%) do the subjects receive the same level of after-tax pensions under immediate and deferred taxation. This suggests that governments could significantly increase the average after-tax pension without changing the level of tax revenue just by switching from a deferred to an immediate pension tax system, which is in line with the findings of Beshears et al. (2017), Blaufus and Milde (2021), and Tschinkl et al. (2021), but contradicts the recent findings of Bohr et al. (2023), who find no difference in savings between immediate and deferred taxed pension plans.

Hypothesis Development

The Effect of Pension Tax Rates on Retirement Savings

A reduction in the pension tax rate increases the return on savings and thus the incentive to save. If we assume that the return on savings is equal to an individual’s time preference rate

Rational choice theory, however, predicts an opposing income effect. Suppose that individuals maximize their lifetime utility

In the income phase, subjects earn an income

If we assume a constant level of relative risk aversion, it can be shown that a decrease in the pension tax rate increases (decreases) retirement savings when the level of relative risk aversion (RRA) is lower (higher) than one because in this case, the substitution effect is larger (smaller) than the income effect (for a proof, see Online Appendix A). Thus, rational choice theory predicts an increase in savings only for individuals with an

Behavioral economics offers different predictions. First, if individuals follow a simple heuristic where savings equal a fixed percentage of pre-tax income independent of the tax treatment of retirement savings (Beshears et al. 2017), a decrease in pension taxes would not affect retirement savings. In line with this, Beshears et al. (2017) find no evidence that individuals’ contribution rates differ between immediately taxed pension plans and deferred-tax pension plans, suggesting that many people indeed ignore and/or neglect these tax rules.

Second, due to confirmation bias, individuals may ignore or underweight information that contradicts their saving intentions (pension taxes) while considering information that is in line with their saving intentions (tax refunds). In this case, a change in the tax rate on pensions would also have no effect or only a small effect. Blaufus and Milde (2021) provide evidence that is consistent with the interpretation of a confirmation bias. Using lab experiments with university students, they find that even after informing their subjects about the tax rules, the subjects underweight the pension tax rate while perceiving the tax refund rate almost correctly. The authors derive their conclusions by comparing economically equivalent immediate and deferred pension taxation using a time-invariant tax rate and the provision of informational nudges on the pension tax rate, the tax refund rate, or both. However, the authors do not examine whether their subjects respond to changes in the tax rates. This is important because individuals may neglect taxes simply because the rates are the same for current and future income. This would be in line with prospect theory, which proposes that individuals simplify their choices during an editing phase in which they discard information that is common to two options (Kahneman and Tversky 1979). Thus, the observed tax ignorance may also stem from the application of the same tax rate to future and current income, and individuals may discard this information because it is common to future and current income. Moreover, prior behavioral research has shown that salience is important in terms of reducing tax misperceptions (e.g., Chetty et al. 2009; Finkelstein 2009; Taubinsky and Rees-Jones 2018). The use of deviating pension and tax refund rates should increase the salience of taxes and thus attract individuals’ attention, which might reduce potential confirmation bias.

Third, individuals often act myopically (e.g., Thaler et al. 1997; Benartzi and Thaler 1999). In this vein, behavioral life-cycle theory assumes that individuals behave as if they have a dual preference structure, namely, one dimension that is concerned with the short run (“the doer”) and one that is concerned with the long run (“the planner”) (Shefrin and Thaler 1988). In the current context, this means that the doer would focus primarily on the information associated with current consumption, i.e., the tax refund that rewards the doer, and underweight or even ignore the long-term tax consequences of savings, i.e., the income taxation of pensions. Accordingly, a reduction in the pension tax rate would have little or no impact.

Overall, the theory is ambiguous, so it is ultimately an empirical question whether a decrease in pension taxes increases savings. Prior empirical research that directly studies the effect of lower pension taxes is rare. Some studies examine the effect of changing tax rates, but this usually implies also changing the tax refund rate. These studies find some evidence that an increase in the tax price of future consumption 2 results in a decrease in the probability of contributing to pension plans and a decrease in retirement savings (e.g., Power and Rider 2002). Thus, a decrease in pension taxes should increase savings. Moreover, there is indirect evidence from research on the choice between immediately taxed and deferred-tax pension plans. In an experiment, Cuccia et al. (2022) find that an increase in pension tax rates increases the preference for immediately taxed pension plans, which implies that at least some individuals consider the effect of pension tax rates in their decisions and decrease their contributions to deferred pension plans when pension tax rates increase. Therefore, we test the following hypothesis:

A decrease in the income tax rate on pensions (the pension tax rate) increases the savings rate.

The Effect of Tax Refund Rates on Retirement Savings

Instead of reducing the pension tax rate, one could increase the tax refund rate to enhance intentions to save. Indeed, deferred-tax pension plans are often advertised with reference to the tax deductibility of savings. For example, Capital One tells its customers how they can maximize their tax savings by contributing to deferred-tax plans: “If you can save money on your taxes while saving for your future, you can feel good about your financial decisions on two fronts at once” (Capital One 2018). Moreover, Messacar (2023) shows that taxpayers actually exploit the tax deductibility of savings to change their final tax balances, suggesting that taxpayers are aware of the benefit of tax deductibility and should therefore respond to the tax refund rate.

In the case of an increase in the tax refund rate, rational choice theory unambiguously predicts an increase in savings (for a proof, see Online Appendix A). However, behavioral economics predicts either no effect at all if individuals use the heuristic of consistently saving the same percentage of their pre-tax income independent of the tax treatment of savings (Beshears et al. 2017) or increases in savings because the tax refund information that they receive confirms their saving intentions and is thus considered and not ignored (confirmation bias) (Blaufus and Milde 2021) or because the tax refund rewards the doer according to behavioral life-cycle theory (Shefrin and Thaler 1988). In line with the rational choice prediction, as well as the prediction from confirmation bias or behavioral life-cycle theory, we state our second hypothesis as follows:

An increase in the tax rate at which savings are deducted (the tax refund rate) increases the savings rate.

Comparing the Effect of Pension Tax Rates and Tax Refund Rates on Retirement Savings

Since both pension tax rates and tax refund rates separately increase the incentive to save, it is important to determine which of these alternatives is more effective in terms of encouraging retirement saving. Rational choice theory predicts ambiguous results that depend on individuals’ RRA. However, in the experimental life cycle used in this paper, an increase in the tax refund rate should be more effective if an individual’s RRA is less than one. Moreover, for individuals with an RRA greater than one, a reduction in the pension tax rate is never effective because it does not increase savings but rather reduces them (Section “The Effect of Pension Tax Rates on Retirement Savings”). Thus, for these individuals, an increase in the tax refund rate is always more effective than a decrease in the pension tax rate. 3

The implications derived from behavioral economics differ depending on which approach is used. Again, if we assume that individuals save the same percentage of their income regardless of the tax treatment of savings (Beshears et al. 2017), it should make no difference whether the tax refund rate or the pension tax rate is changed since both parameters are neglected or ignored. However, if individuals suffer from confirmation bias as proposed by Blaufus and Milde (2021), an increase in the tax refund rate would be more effective in terms of encouraging saving because the pension tax rate (but not the tax refund rate) is underweighted or ignored.

Moreover, some researchers even argue that tax refunds could be overweighted because a tax refund provides an “immediate reward for saving” (Thaler 1994: 189). The reasoning is based on behavioral life-cycle theory (Shefrin and Thaler 1988). In this vein, Bernheim (2002: 1204) also argues that the benefit of deferred taxation is that it “coopts impatient selves with the immediate reward of a current-year tax deduction”. As a result, increases in tax refund rates could be more effective than reductions in deferred income taxes on pensions.

In contrast, Cuccia et al. (2022) argue that people who contribute to a deferred-tax pension plan may perceive this as trading an immediate gain (the tax refund) for a future loss (the pension tax). Due to loss aversion (Kahneman and Tversky 1979) and the fact that the discount rates of losses are lower than those of gains (Thaler 1981), the effect of a pension tax rate reduction (loss reduction) should be greater than that of an increase in the tax refund rate (gain increase).

Due to these opposing arguments, it is unclear whether a change in the tax refund or a change in the pension tax rate is more effective. We follow the rational choice prediction, the prediction of confirmation bias and the short-term thinking argument of behavioral life-cycle theory, testing the following hypothesis:

Increasing the incentive to save by increasing the tax refund rate is more effective in terms of stimulating saving than decreasing the pension tax rate.

Experimental Design

Procedure and Treatments

To test our hypotheses, we conduct an online experiment with 1,143 subjects. The subjects make retirement savings decisions over a life cycle (Modigliani 1954) consisting of an income phase (seven periods) and a pension phase (three periods). During the income phase, subjects receive an increasing, certain income in each period to make savings decisions for the pension phase. 4 After each savings decision, subjects complete a tax return for the respective period, declaring pretax income and tax-deductible savings. In the pension phase, the subjects do not receive an exogenous income; rather, they receive a constant income depending on their savings during the income phase. To keep the experiment as simple as possible, we do not consider lifetime or income uncertainty or interest on savings. 5 The income received during the income phase is subject to a 30% withholding tax. Savings contributions, by contrast, are taxed on a deferred basis; i.e., the savings are tax deductible (resulting in a tax refund), while the pension is fully taxable. However, the pension tax rate and the tax deductibility of savings vary depending on the treatment (see below).

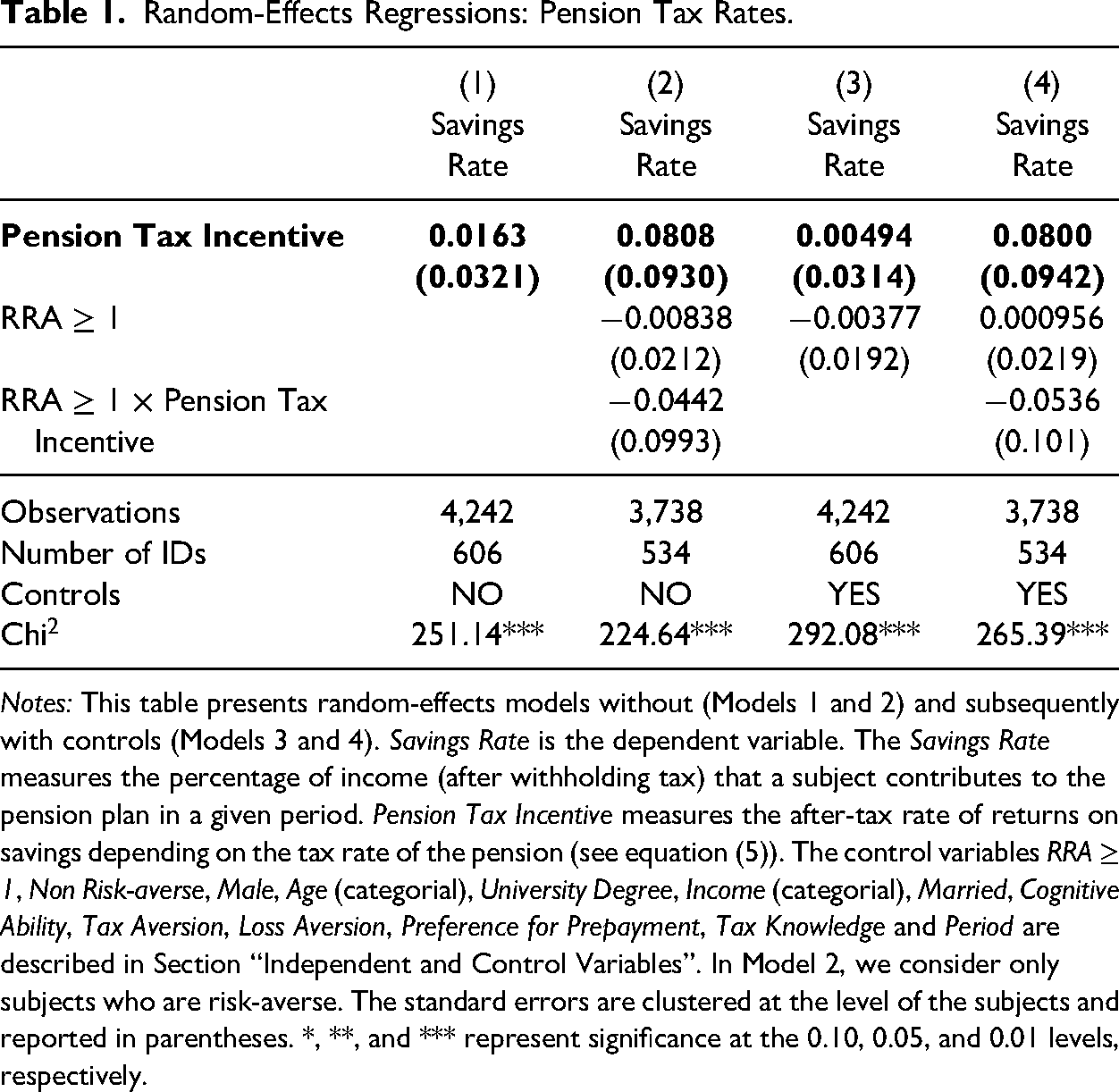

Random-Effects Regressions: Pension Tax Rates.

Notes: This table presents random-effects models without (Models 1 and 2) and subsequently with controls (Models 3 and 4). Savings Rate is the dependent variable. The Savings Rate measures the percentage of income (after withholding tax) that a subject contributes to the pension plan in a given period. Pension Tax Incentive measures the after-tax rate of returns on savings depending on the tax rate of the pension (see equation (5)). The control variables RRA

At the end of each period, the subjects receive an overview of their savings, the result of the tax return and the payoff for the period (income after withholding taxes

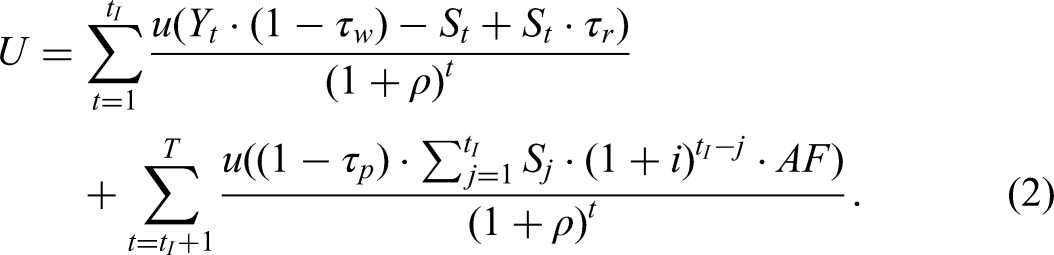

In some experimental life-cycle studies, researchers use induced utility functions, which provide the opportunity to test saving behavior against an optimal benchmark (e.g., Brown et al. 2009; Ballinger et al. 2011; Duffy and Li 2019). However, this also significantly increases the experimental complexity (Koehler et al. 2015). Since we are interested only in saving behavior under different saving incentives, it is not necessary to introduce a specific utility function, and we rely on the subjects’ own exogenous preferences. To motivate consumption smoothing and to adapt our experimental design to the underlying rational choice model with an additively separable utility function (see equation (1)), only one of the 10 periods is randomly assigned for payoff at the end of the experiment, as in Blaufus and Milde (2021).

6

Thus, subjects maximize their experimental wealth according to the following expected utility function:

In addition to receiving a fixed payoff of €2.00, the subjects receive a variable payoff. The latter consists of the payoff depending on the saving behavior during the life cycle and the payoff based on two postexperimental questions on loss aversion and risk-taking.

To study the effect of different saving incentives, subjects are randomly assigned to the two treatments Tax Refund Incentive and Pension Tax Incentive. In the Tax Refund Incentive treatment, the pension tax is constant at 30%. In this treatment, each subject is randomly assigned to one of the following tax refund rates: 0%, 15%, 30%, and 45%. To this end, subjects are informed that the savings are either not deductible or deductible at half, full or 1.5 times the amount saved. 7 In the Pension Tax Incentive treatment, the tax refund rate is constant at 30%, and each subject is randomly assigned to one of the following pension tax rates: 0%, 15%, 25%, 30%, 35%, and 50%. 8 In cases where both the tax refund rate and the pension tax are 30% (i.e., the incentive to save is zero), the overall experimental design is the same for both treatments, and we use these observations for both treatment groups.

In some analyses, we look separately at the subgroup with an incentive to save of zero, i.e., that with the same pension tax rate and tax refund rate of 30%. This subgroup is referred to as Deferred30. To test whether subjects simply save a certain percentage of their income after withholding taxes and fully neglect the tax treatment of savings, we conduct an additional treatment in which there is no tax (No Tax). We reduce the income in this treatment to make it economically equivalent to that in the previously mentioned subgroup Deferred30. We also conduct a treatment in which the savings contributions are taxed immediately at a rate of 30%, but pensions are tax-free (Immediate). From a rational choice perspective, this treatment is economically identical to No Tax and Deferred30.

We provide descriptive statistics depicting the average sociodemographic characteristics of the subjects in Table B1 in the appendix. To test whether there are no systematic differences in the sociodemographic characteristics of the subjects between treatments, we perform a joint Chi

Subjects and Data

The experiment was conducted in Germany and was programmed with oTree (Chen et al. 2016). All the subjects were native German speakers over 18 years old and were recruited from the survey platforms Clickworker, Prolific and Respondi. 9 A total of 1,247 subjects were randomly assigned to the following four treatments: Tax Refund Incentive (431 subjects), Pension Tax Incentive (606), 10 Immediate (110), and No Tax (100). A total of 47.6% of the subjects were male, and the subjects’ average age was 39.8 years (SD 15.8). Their mean earnings were €4.94 (SD €1.27), with a minimum of €1.10 and a maximum of €9.57. The median time to complete the experiment was 26 minutes, yielding a median hourly wage of €11.40.

To use reliable data in the analysis, we considered the following elements in the design: (1) At the beginning of the experiment, the subjects received detailed instructions on the experimental procedure and the tax rules (see Online Appendix B). These were written in neutral language. In this way, we kept the subjects from using individual scripts when interpreting the loaded terms. For example, we did not use the terms retirement or pension contributions but rather terms such as income phase, rest phase, savings decision, and payout. (2) Subjects participated in a training round in which taxes were not taken into account. 11 (3) The subjects had to complete two comprehension tests (one regarding the experimental design before the training round and one regarding the tax rules and the compensation). 12 (4) We included some attention checks during the experiment. The subjects were allowed to participate in the experiment only if they answered all the comprehension questions correctly and passed all the attention checks. 13

Measurement of Variables

Dependent Variable

We use

For the bivariate analyses, we compare the mean

Independent and Control Variables

As independent variables, we use the incentive to save (Incentive), which measures the after-tax rate of return on savings. The incentive to save is affected by the tax rate on tax-deductible savings

We distinguish the incentive to save arising from the tax refund rate (Tax Refund Incentive) and the incentive to save arising from the pension tax rate (Pension Tax Incentive). 14 We also use the independent variables Immediate, No Tax and Deferred30. Immediate and No Tax are dummy variables equal to one if the observation belongs to the respective treatment. Deferred30 is another dummy variable equal to one for observations belonging to the deferred taxation setting, where the current tax rate on income, the tax refund rate, and the pension tax rate are each 30%. Period is a metric variable denoting the periods of the income phase (from one to seven).

In multivariate analyses, we consider different sociodemographic control variables, such as Risk Attitude, Age, Male, University Degree, Income, Married, Tax Knowledge, Cognitive Ability, Tax Aversion, Loss Aversion and Preference for Prepayment. Detailed definitions of these variables are provided in Tables B2 and B3 in the appendix.

Estimation Strategy

We test our hypotheses using bivariate and multivariate analyses. In the bivariate analyses, we use Pearson’s tests to examine the relationship between the incentive to save and the subjects’ average savings rate. To control for various sociodemographic variables and the subjects’ incentives to save, we run random effects regressions that account for the dependence among the observations within each subject

Empirical Results

Saving Incentives from Differing Pension Tax Rates

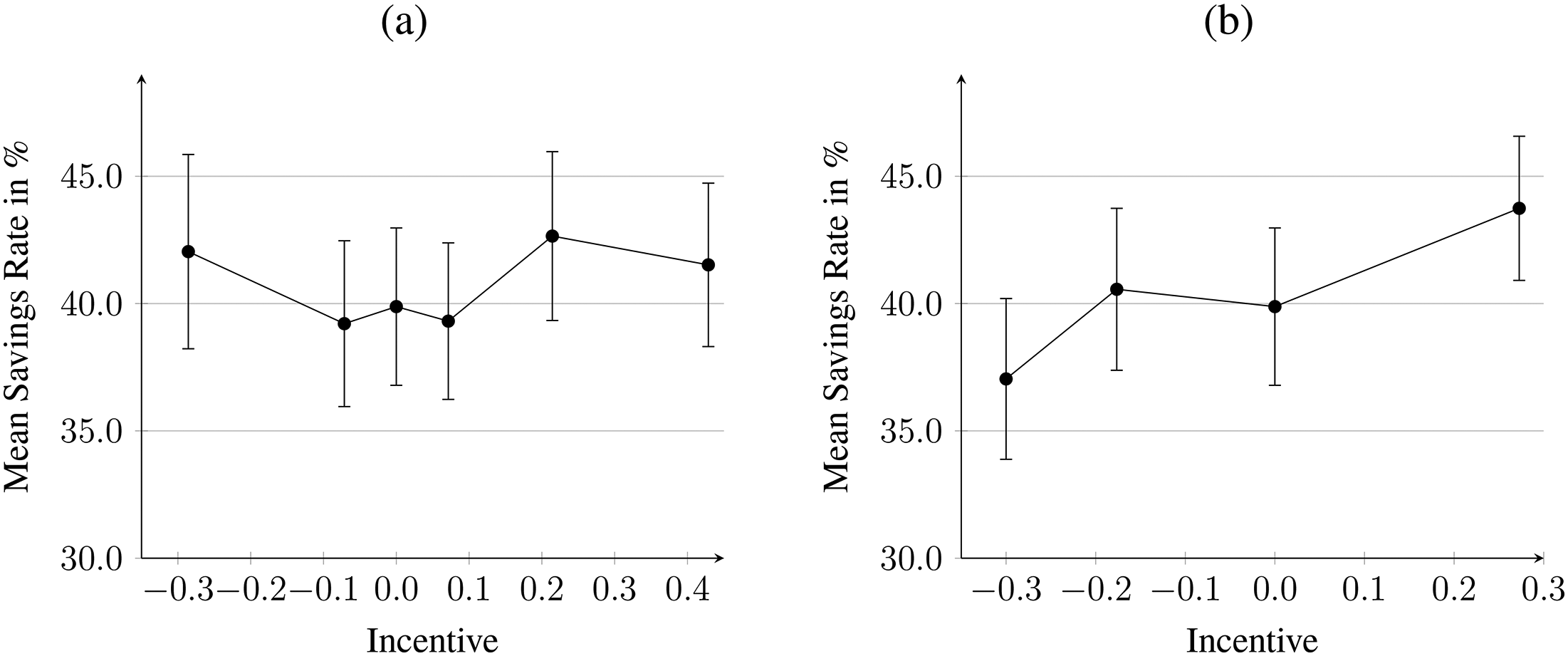

According to H1, we examine the extent to which different incentives to save due to changes in tax rates affect saving behavior. Figure 1(a) shows the average savings rate depending on the incentive to save. At first glance, one can see that the incentive has almost no impact on saving behavior. We also find no significant correlation between the level of the pension tax and saving behavior (

Incentive to Save. (a) Pension Tax Incentive; (b) Tax Refund Incentive. Notes: The two figures show the average savings of the subjects depending on the incentive to save. In Figure 1(a) [1(b)], the incentive to save is changed by varying the pension tax rate [tax refund rate]. The Savings Rate measures the percentage of income (after withholding tax) that a subject contributes to the pension plan in a given period. The incentive to save (Incentive) determines the after-tax rate of return on savings according to equation (5). Error bars show 95% confidence intervals.

Our multivariate analyses with and without control variables confirm our bivariate finding that the level of the incentive does not significantly impact saving behavior (see Models 1 and 3 in Table 1). We also consider that subjects in earlier and later periods might respond differently to varying pension tax rates. To test this, we run the same regressions separately for the first and last three periods of the income phase (not tabulated). The treatment effect is homogeneous across periods, with no effect of pension tax rates on saving in either the first or last three periods. Thus, we reject our first hypothesis.

However, this does not automatically mean that the incentive is completely neglected. According to rational choice theory, for risk-averse individuals with a relative risk aversion less (greater) than one, an increasing incentive to save due to lower pension tax rates should increase (decrease) savings. Consequently, our result could arise because the different saving behaviors of the two groups (

Despite the different pension tax rates ranging from 0% to 50%, individuals do not respond to these different incentives to save in their saving decisions. Since there is no tax to consider in the case of a 0% pension tax, we conclude that taxes are also ignored in the case of positive pension tax rates. This behavior is consistent with several explanations: myopic behavior, confirmation bias (where individuals ignore information, such as pension taxation, that undermines their saving intentions) (Blaufus and Milde 2021), or the use of heuristics. For example, individuals may save a fixed percentage of their income regardless of the tax treatment (Beshears et al. 2017) or save the same percentage of their after-tax income.

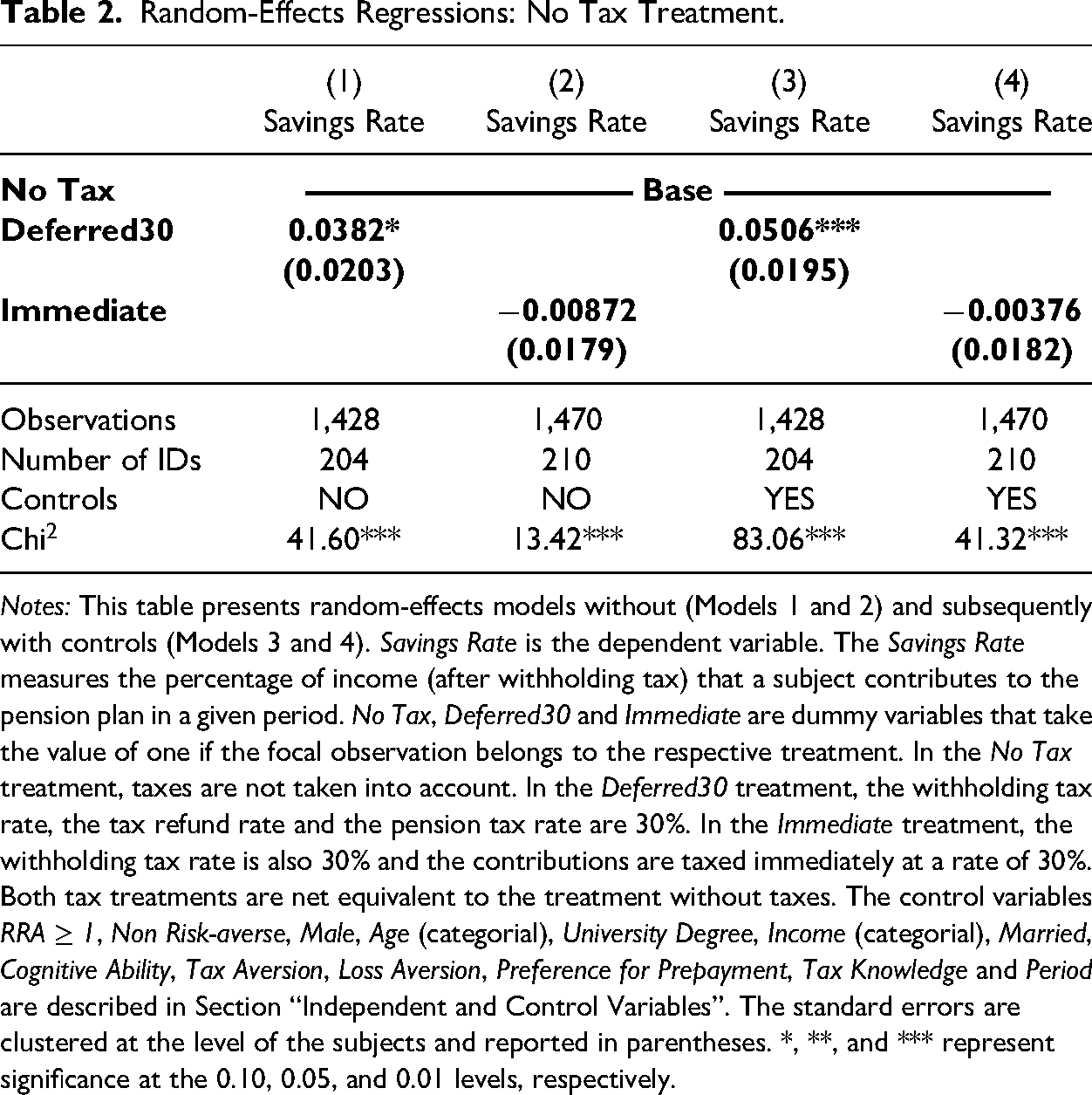

To examine the latter explanation, we compare the Savings Rate under deferred taxation with a tax refund rate and a pension tax rate amounting to 30% (Deferred30) with that under a net equivalent no-tax treatment (No Tax). We find that nominal savings are significantly higher in the case of deferred taxation than in the case without taxation (see Models 1 and 3 in Table 2). Thus, we can rule out the possibility that subjects simply save the same percentage of their income after withholding taxes.

Random-Effects Regressions: No Tax Treatment.

Notes: This table presents random-effects models without (Models 1 and 2) and subsequently with controls (Models 3 and 4). Savings Rate is the dependent variable. The Savings Rate measures the percentage of income (after withholding tax) that a subject contributes to the pension plan in a given period. No Tax, Deferred30 and Immediate are dummy variables that take the value of one if the focal observation belongs to the respective treatment. In the No Tax treatment, taxes are not taken into account. In the Deferred30 treatment, the withholding tax rate, the tax refund rate and the pension tax rate are 30%. In the Immediate treatment, the withholding tax rate is also 30% and the contributions are taxed immediately at a rate of 30%. Both tax treatments are net equivalent to the treatment without taxes. The control variables RRA

Next, we examine the explanation that subjects always save the same percentage of their pretax income, i.e., that they fully neglect taxes (Beshears et al. 2017). For this purpose, we compare two economically equivalent treatments, No Tax and Immediate. In the Immediate treatment, the pre-tax income is greater than the income in the No Tax treatment, while the after-tax income is identical to the income in the No Tax treatment. If subjects always save the same percentage of their pre-tax income, we would expect subjects to save more in the Immediate treatment. However, we find that subjects save the same amount in both treatments (see Models 2 and 4 in Table 2) and conclude that subjects are not anchored to pretax income when making the decision to save. In the next section, we examine the extent to which the level of a tax refund affects saving behavior.

Saving Incentives from Tax Refunds

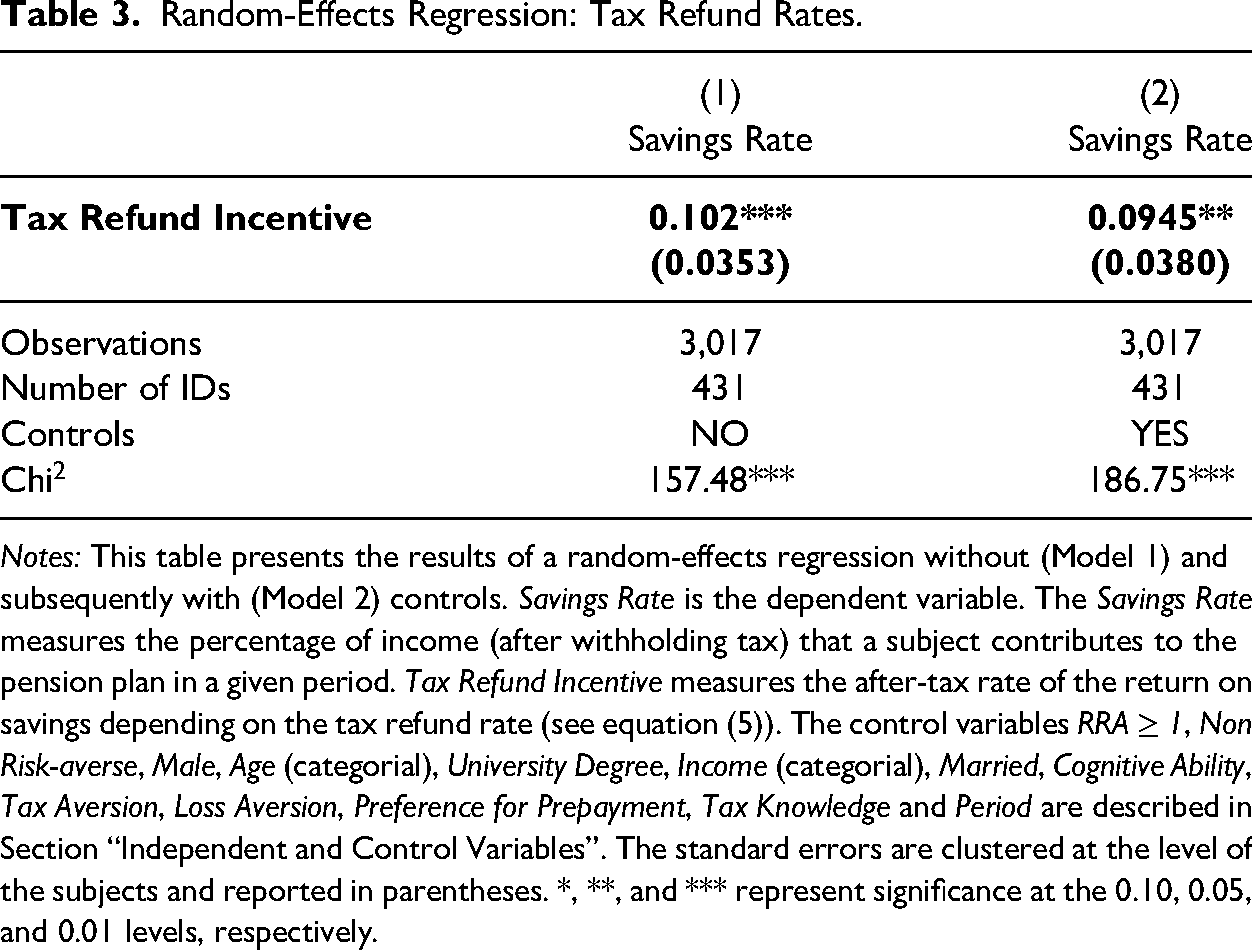

In this section, we examine the effect of tax refund incentives on pension saving behavior (Hypothesis 2). Figure 1(b) provides an initial impression of the results. Unlike the incentive from lowering the pension tax rate, increasing the tax refund has a significant positive effect on saving behavior (

Models 1 and 2 in Table 3 show that this relation is highly significant. If we vary the tax refund rate such that the incentive to save increases by 10 percentage points, the savings rate increases by 0.95 percentage points. This implies that a 10-percentage-point increase in the tax refund rate leads to a 1.18-percentage-point increase in the savings rate. 16 In summary, our results provide support for Hypothesis 2. An increase in the tax rate at which savings are deducted increases the savings rate.

Random-Effects Regression: Tax Refund Rates.

Notes: This table presents the results of a random-effects regression without (Model 1) and subsequently with (Model 2) controls. Savings Rate is the dependent variable. The Savings Rate measures the percentage of income (after withholding tax) that a subject contributes to the pension plan in a given period. Tax Refund Incentive measures the after-tax rate of the return on savings depending on the tax refund rate (see equation (5)). The control variables RRA

Comparison of Saving Incentives from Pension Tax Rates and Tax Refund Rates

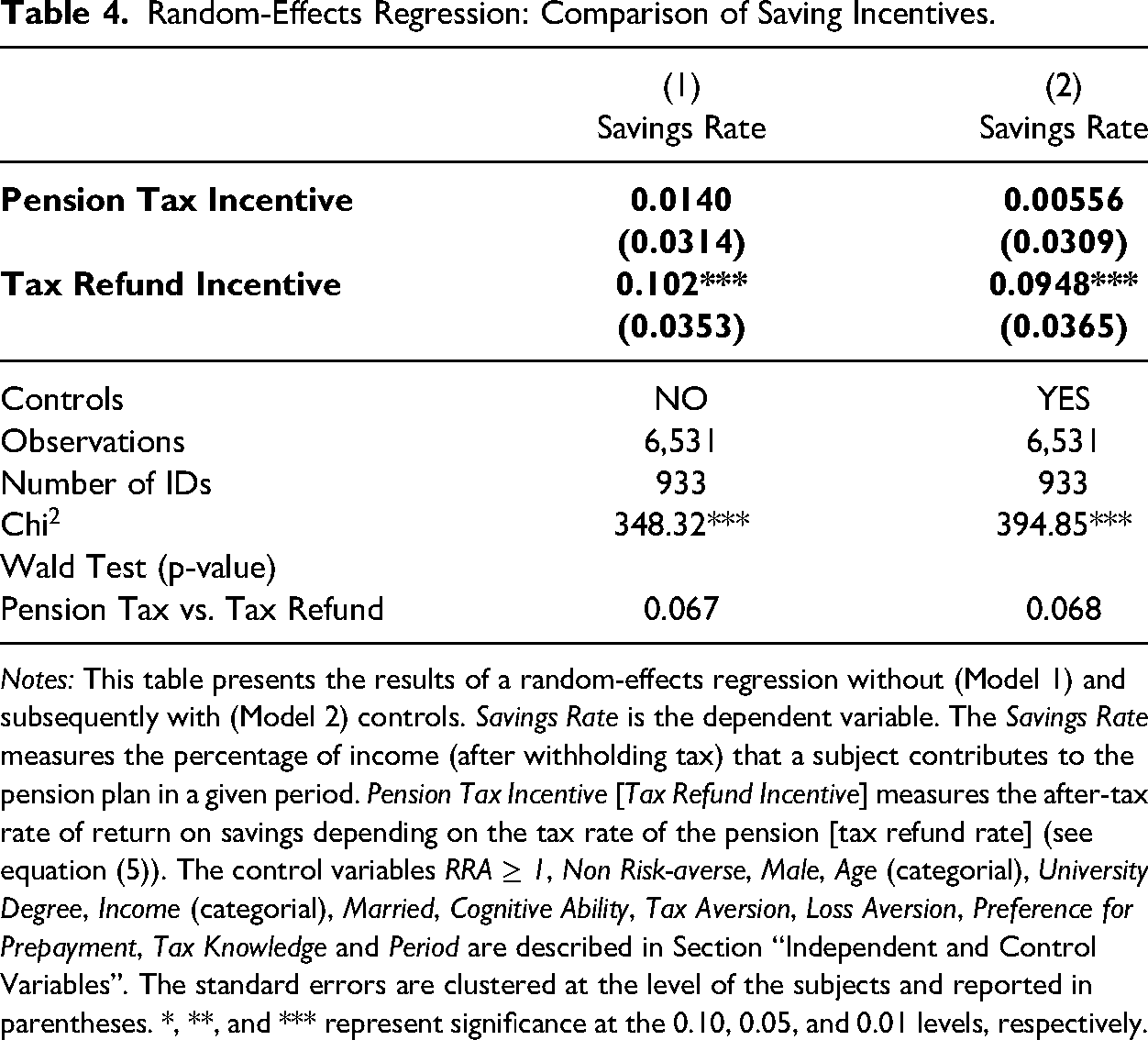

We have already shown that pension tax reductions are ineffective in encouraging higher savings, while higher tax refunds effectively increase savings. Models 1 and 2 in Table 4 show that this result is significant (Wald tests;

Random-Effects Regression: Comparison of Saving Incentives.

Notes: This table presents the results of a random-effects regression without (Model 1) and subsequently with (Model 2) controls. Savings Rate is the dependent variable. The Savings Rate measures the percentage of income (after withholding tax) that a subject contributes to the pension plan in a given period. Pension Tax Incentive [Tax Refund Incentive] measures the after-tax rate of return on savings depending on the tax rate of the pension [tax refund rate] (see equation (5)). The control variables RRA

However, the question arises why individuals respond to tax refunds but not to pension taxes. One reason could be that the pension tax is less salient than the tax refund and therefore not considered during the decision. Supporting this conjecture, subjects receive feedback on the tax refund’s consequences after each savings decision via the tax return, whereas the pension tax’s impact is only experienced during the pension phase. However, we find no evidence for this. First, we assume that subjects are aware of both the tax refund and the pension tax. This is ensured by the instructions and the associated comprehension test, as well as by the repeated presentation of the tax rules at each saving decision. Second, we conduct the analyses only for the first period, in which there is no feedback on the tax refund (untabulated). Even in the first period, the tax refund rate has a significant effect on saving behavior (

We suggest, however, that this result is consistent with confirmation bias, as individuals consider information consistent with their saving intentions (tax refund) but underweight contradictory information (pension tax). Importantly, our operationalization reflects real-world conditions where individuals receive feedback on tax refunds but little to no feedback on future pension taxation, as exact future tax rates are unknown, and pension information letters or digital pension dashboards are often infrequent and not highly salient. This lack of feedback is likely to amplify the observed confirmation bias, and the neglect of pension taxation may be even more pronounced in reality. Additionally, myopic behavior could explain this finding. According to behavioral life-cycle theory (Shefrin and Thaler 1988), individuals focus on tax refunds because the immediate benefit rewards the doer ,reducing opposition to saving. However, Blaufus and Milde (2021) find that individuals respond to a matching contribution paid directly into the pension fund, increasing their future pension. If individuals ignore all future benefits due to myopic behavior, they should also ignore matching contributions. Since individuals acknowledge future benefits aligned with saving intentions but ignore pension tax burdens contradicting these intentions, we argue that our results are best explained by confirmation bias, which has also been shown to explain tax effects on consumption behavior (Feldman and Ruffle 2015; Feldman et al. 2018). However, our design does not allow a definite answer, so myopic behavior cannot be clearly ruled out as an explanation.

Additional Analyses

Uncertainty of Future Tax Rates

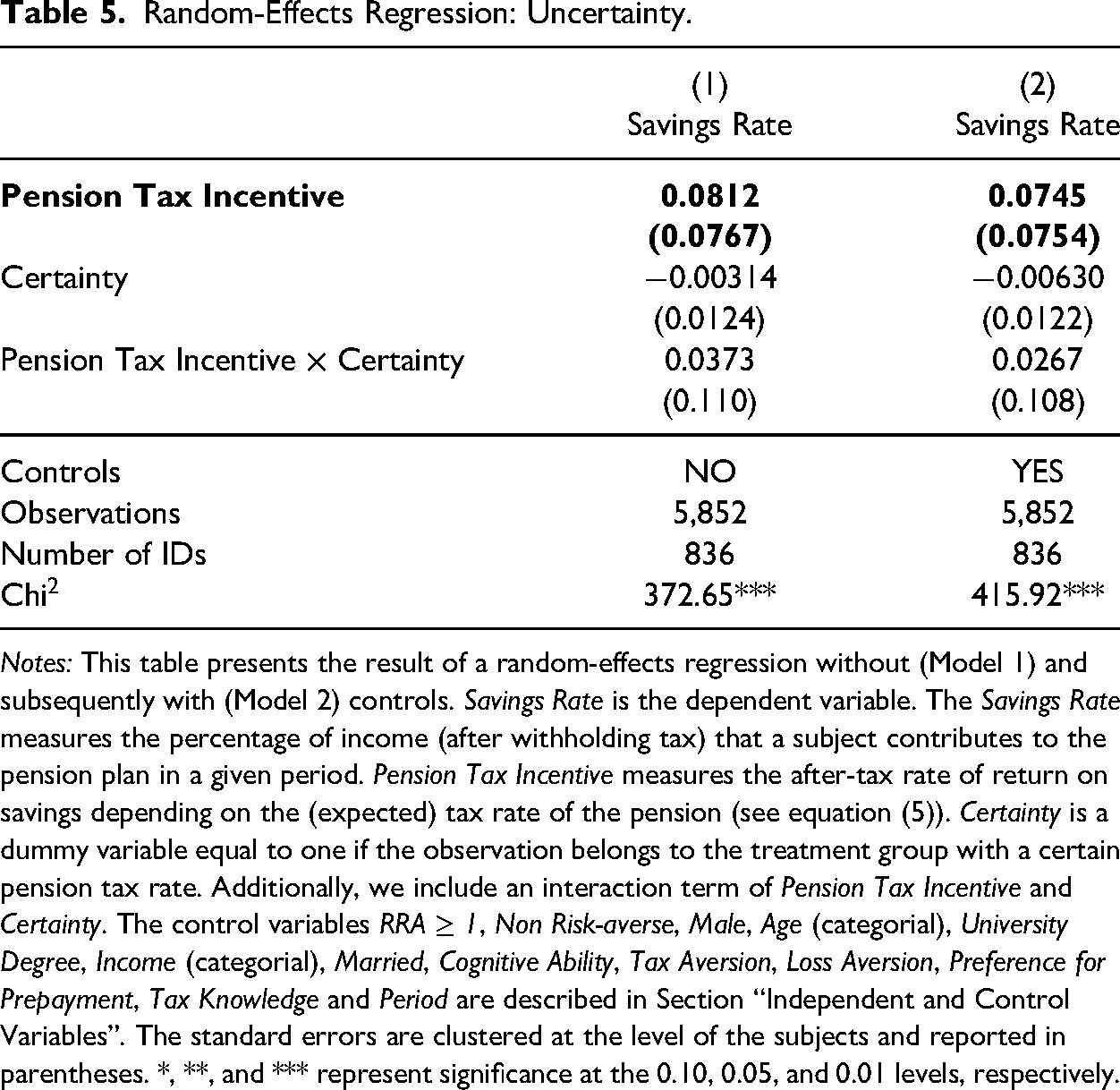

We have shown that pension taxes are neglected on average. In this context, we want to investigate the extent to which increasing salience can counteract this neglect of pension taxes. Chetty et al. (2009) and Taubinsky and Rees-Jones (2018) demonstrate, for example, that consumers do not react as strongly to nonsalient taxes, and Fochmann and Weimann (2013) show that increasing tax salience can reduce tax misperceptions. Uncertain pension tax rates should thereby increase the salience of the pension tax rate and thus attract individuals’ attention. 18

To test the effect of tax rate uncertainty, we conducted another experiment with a new treatment, Pension Tax Uncertainty. We implemented uncertainty as a mean-preserving spread (Rothschild 1978), allowing for a higher or lower pension tax rate with equal probability. Under uncertainty, the pension tax rates differ by

A total of 417 additional individuals participated in the experiment. The timing of data collection for this experiment was the same as for the other treatments, and there were no significant sociodemographic differences in terms of gender, age, education level or school degree between this treatment and the Pension Tax Incentive treatment (unreported).

Models 1 and 2 in Table 5 show the results of our analysis. In the regressions, we include a dummy variable, Certainty, which equals one if the subject is not in the Pension Tax Uncertainty treatment. Finally, using the interaction of incentives and salience (certain versus uncertain tax rates), we examine the effect of increasing salience. However, the interaction term is not significant. Moreover, in the treatment with an uncertain pension tax rate (main effect of Pension Tax Incentive), we do not find a significant effect of decreasing pension tax rates. Thus, we find that the taxation of pensions is neglected despite increasing salience. 19

Random-Effects Regression: Uncertainty.

Notes: This table presents the result of a random-effects regression without (Model 1) and subsequently with (Model 2) controls. Savings Rate is the dependent variable. The Savings Rate measures the percentage of income (after withholding tax) that a subject contributes to the pension plan in a given period. Pension Tax Incentive measures the after-tax rate of return on savings depending on the (expected) tax rate of the pension (see equation (5)). Certainty is a dummy variable equal to one if the observation belongs to the treatment group with a certain pension tax rate. Additionally, we include an interaction term of Pension Tax Incentive and Certainty. The control variables RRA

Immediate Taxation

We have shown that saving behavior is subject to significant tax misperceptions under deferred taxation. This is mainly due to the neglect of the pension tax. These tax misperceptions are unlikely to exist under immediate taxation, where savings are not tax deductible while future pensions are tax free.

To shed light on this issue, we again consider the Immediate treatment, where savings contributions are taxed immediately at a rate of 30%. In contrast to deferred taxation (equation (2)), lifetime utility

A comparison between equations 2 and 7 shows that immediate and deferred taxation are economically equivalent if the pension tax rate equals the tax refund rate (

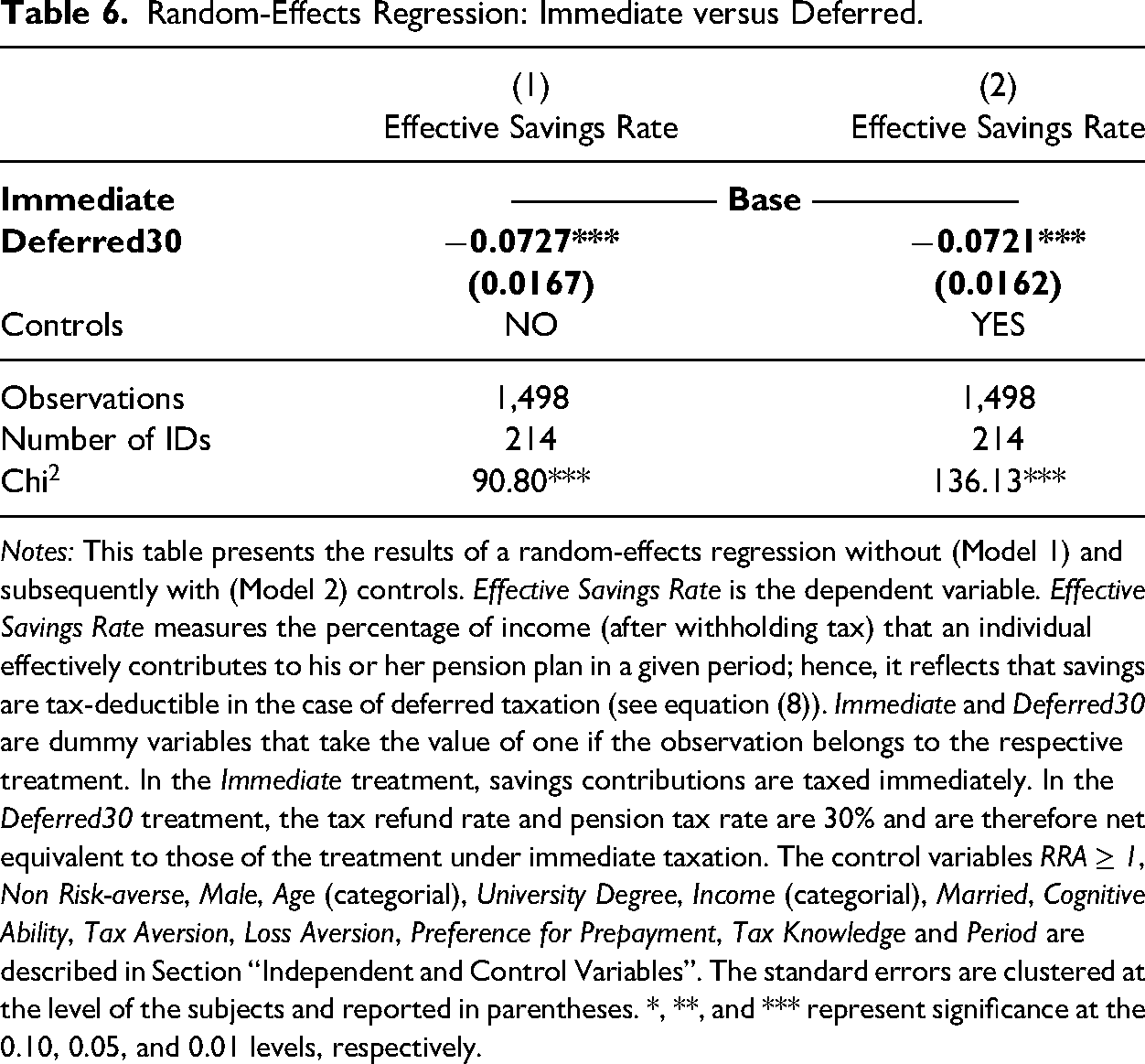

Therefore, we compare the saving behavior in this Immediate treatment with that in the deferred-tax treatment where the tax rate of both the tax refund and the pension is 30% (Deferred30). To make the savings rate of the deferred taxation treatment comparable to that of the Immediate treatment, we use

Random-Effects Regression: Immediate versus Deferred.

Notes: This table presents the results of a random-effects regression without (Model 1) and subsequently with (Model 2) controls. Effective Savings Rate is the dependent variable. Effective Savings Rate measures the percentage of income (after withholding tax) that an individual effectively contributes to his or her pension plan in a given period; hence, it reflects that savings are tax-deductible in the case of deferred taxation (see equation (8)). Immediate and Deferred30 are dummy variables that take the value of one if the observation belongs to the respective treatment. In the Immediate treatment, savings contributions are taxed immediately. In the Deferred30 treatment, the tax refund rate and pension tax rate are 30% and are therefore net equivalent to those of the treatment under immediate taxation. The control variables RRA

We find that in the case of deferred taxation—despite the economic equivalence—the effective savings rate is significantly lower than that in the case of immediate taxation. This confirms the finding of Blaufus and Milde (2021) and shows that their result generalizes from a laboratory environment with students to an online experiment with the general public as subjects (see also Bachmann et al. 2023). These results demonstrate that by introducing immediately taxed pension plans, a government can significantly increase effective retirement savings and thus after-tax pensions without changing the level of tax revenue. Notwithstanding the advantages of immediate over deferred taxation in incentivizing retirement savings, some research suggests that offering both immediate and deferred tax plans simultaneously may, in fact, be even more effective in this regard (Blaufus and Milde 2025).

Conclusion

Many countries use tax incentives to promote retirement savings. However, the effectiveness of these incentives is unclear (e.g., Chetty et al. 2014). Using a series of experiments, we find that decreasing pension tax rates does not encourage retirement savings. Even if we greatly reduce the pension tax rate from 50% to 0%, we do not observe any significant change in peoples’ saving behavior. Thus, a policy of reducing pension tax rates, for example, by providing extra tax allowances for older people, may be ineffective and costly.

In contrast, an increase in the tax refund rate, i.e., the rate at which individuals can deduct their retirement savings, increases savings. This finding is in line with myopic behavior (Thaler et al. 1997; Benartzi and Thaler 1999) or confirmation bias (Feldman and Ruffle 2015; Feldman et al. 2018; Blaufus and Milde 2021); i.e., individuals pay attention to information (tax refunds) that confirms their saving intentions but underweight information that contradicts such intentions (pension taxes).

In the experiment, all subjects were fully informed about the tax rules and passed comprehension tests on these rules. Nevertheless, we observe significant misperceptions regarding taxes on pension income. Thus, with respect to tax policy, our results indicate that policies that rely on providing people with additional information to promote retirement savings, while helpful in principle (e.g., Duflo and Saez 2003; Goda et al. 2014; Dolls et al. 2018), are insufficient. Moreover, our findings suggest that, in general, an instrument that increases current tax benefits is more effective than one that decreases future tax burdens even if both instruments are economically equivalent. This result is relevant for tax incentives designed to promote retirement savings but should also carry over to other contexts. For example, building on our results, one could predict that granting an immediate write-off of assets is more effective than exempting future investment income if the government aims to promote investment activity. Moreover, if people focus on their future pretax pensions (instead of their after-tax income) while making their savings decisions, it seems reasonable to expect that they also focus on nominal pensions (instead of real pensions). Research has already used experiments to examine money illusion (e.g., Büsing et al. 2023). Using similar experiments, future research may thus examine whether people who suffer from tax illusion also suffer from money illusion.

Furthermore, although prior research has shown that accounting for pension tax uncertainty is economically important for investors from a rational choice perspective (Brown et al. 2017), our findings suggest that people tend to ignore tax uncertainty, as we demonstrate that it does not change their savings. Thus, one should be very cautious when deriving policy implications from models that rely on the correct perception of uncertain tax rates.

However, our findings also speak to the limited potential of even tax refund rates to promote retirement savings. An increase of 10 percentage points in the tax refund rate leads to only a 1.2-percentage-point increase in the savings rate. In contrast, we show that substituting deferred taxation with economically equivalent immediate taxation increases the (effective) savings rate by 7.2 percentage points without changing tax revenue. Thus, policy makers may consider providing immediately taxed pension plans to encourage retirement savings more effectively.

Supplemental Material

sj-pdf-1-pfr-10.1177_10911421251335100 - Supplemental material for Does a Decrease in Pension Taxes Increase Retirement Savings? An Experimental Analysis

Supplemental material, sj-pdf-1-pfr-10.1177_10911421251335100 for Does a Decrease in Pension Taxes Increase Retirement Savings? An Experimental Analysis by Kay Blaufus, Michael Milde and Alexandra Spaeth in Public Finance Review

Footnotes

Appendix

Acknowledgements

We thank the participants at the 2021 arqus-conference as well as the 2022 conference of the German Association for Experimental Economic Research for their helpful comments and suggestions.

Data Availability Statement

Data are available from the authors upon request.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Kay Blaufus expresses appreciation for the receipt of financial resources through the Fund to Support Experimental Research at the School of Economics and Management at Leibniz University Hannover.

Ethical Statement

The experiment was approved by the Institutional Review Board of the German Association for Experimental Economic Research (No. G6qu3MUL).

Notes

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.