Abstract

In this article, we elicit the assumptions needed for an assessment of a joint reform of personal income and indirect taxes in a consistent conceptual framework. One often lacks an encompassing model for both labor supply decisions in real world tax and benefit contexts and the allocation of disposable income to commodities. We characterize households’ labor supply decisions by a random utility random opportunity model of job choice. We illustrate the framework with a Belgian tax reform proposal that shifts the burden away from labor taxes to indirect taxation. We find substantial empirical evidence that, both from a distributional and from a budgetary perspective, it is important to account for the impact of indirect taxes on the labor supply decision of households. The cost recovery effects of the tax shift are negative. This is, among other things, explained by the income effect in our job choice model.

Introduction

In this article, we offer a framework that allows us to make a micro-based budgetary and a distributional evaluation of a joint reform in both the personal tax and benefit system and the indirect tax system. Such joint tax reforms are initiated by governments worldwide in an attempt to shift part of the tax burden from labor to consumption, which is considered to be less detrimental to economic growth (see Myles, 2009a,b,c for a review). However, there is not so much literature on micro-based empirical policy evaluations of these kinds of joint reforms. 1 Exceptions are Bach et al. (2006), Capéau et al. (2009), Pestel and Sommer (2017), and Savage (2017). From these studies, it can be inferred that such reforms may have substantial distributional effects. These papers, however, all proceed without an encompassing model for the labor market participation decision and the allocation of disposable income to commodities, which, at first sight, would seem a necessary tool for a consistent analysis of these distributional effects.

The reason for this gap is that such an encompassing model which at the same time sufficiently keeps track of the existing intricacies of the direct and indirect tax-benefit system, often becomes theoretically intractable, let alone useful for empirical implementation. And even if such a model did exist, few available datasets would allow for the estimation of such a model, as detailed information is required on households’ gross incomes, their labor market participation, and their expenditures. Therefore, the papers cited above make use of existing disconnected microsimulation models of direct taxes and benefits on the one hand, and of indirect taxes on the other. The former are often connected with a behavioral model of labor supply, the latter with a demand system that allocates expenditures. The cited papers then glue these model pieces together in a rather ad hoc fashion, to arrive at an evaluation toolbox for the joint tax reform.

What the present article offers is a framework that allows one to underpin how these model pieces can fit one into another in a consistent way. Thereto, we rely on a two-stage budgeting approach. 2 The first stage models the labor supply decision, which determines households’ disposable income. The second stage models the allocation of this disposable income to commodities and savings. It is known that such a two-stage budgeting approach requires the assumption of weak separability between leisure and consumption goods (Gorman, 1971). One of our main contributions is to exploit the fact that such a two-stage approach still entails the necessity of including commodity prices in the first stage decision.

Building on Bach et al. (2006), Capéau et al. (2009), and Pestel and Sommer (2017), we formalize the implementation of a joint tax reform in a microsimulation model with both labor supply reactions, and commodity demand reactions. Our framework allows us to assess the labor supply effect stemming from solely the change in consumer prices as a consequence of an indirect tax reform. Similar to Bach et al. (2006), Capéau et al. (2009), and Pestel and Sommer (2017), the change in consumer prices is taken into account in the labor supply decision by estimating and simulating the model with a real disposable income concept. However, whereas the deflation of income in those cited papers was chosen somewhat arbitrarily, we provide a theoretical underpinning of a household-specific deflator of disposable income. Instead of subtracting indirect taxes from expenditures in the estimation of their labor supply model, we argue that the inclusion of commodity prices in the first stage of the decision process with such a household-specific price index is sufficient to assess the budgetary effects of, behavioral reactions to, and distributional implications of a joint tax reform.

Note that also in previous papers, some heterogeneity has been incorporated in studies that link reforms in indirect taxation with labor supply decisions. But this has often been done in a quite ad hoc manner (Bach et al., 2006; Capéau et al., 2009; Pestel and Sommer, 2017). Often, it is unclear how expenditure heterogeneity plays a role in the estimation of the job choice model, and what the rationale is behind the real income concept used. In this respect, our main contribution is not the use of household-specific price deflators, but to provide a tractable and consistent modeling strategy for the labor supply effects of joint direct and indirect tax reforms. Indeed, the framework we propose can also be used with a general price deflator instead of a household-specific deflator. Of course, this would alter both the estimated model, and the simulated labor supply responses, and the distributional impact of a joint direct and indirect tax reform. The empirical importance of including heterogeneity depends mostly on the chosen simulated reform: it will matter more for changes in indirect taxation for specific goods, of which consumption is very unequally distributed across the population, and it will matter less for general changes in the value-added tax (VAT) rate.

As far as the first stage is concerned, we use a random utility random opportunity (RURO) discrete choice model of job choice (see e.g., Aaberge and Colombino, 2014; Dagsvik et al., 2014). 3 Contrary to classical discrete choice models of labor supply (e.g., Van Soest, 1995), this model considers a job to consist of a package of attributes: the labor time regime, the wage paid, and other pecuniary and non-pecuniary attributes. As such, offered wages become an aspect of the elements in the choice set. This allows us to capture a number of behavioral reactions which have hitherto received little attention in the literature on tax reforms. For example, in our framework, jobs with lower gross wages may become more attractive after a reform in the tax-benefit schedule. As will be shown in the empirical application, this might have important second-order effects on the taxable base, and hence on government revenues.

We deliberately kept the modeling of the second step simple. We impute income shares for each commodity group, and then assume Cobb–Douglas preferences characterized by these estimated shares. Given the Cobb–Douglas assumption together with the two-stage budgeting approach, we then treat the estimated budget shares as parameters, and keep them fixed throughout our simulations. The constant shares assumption could be relaxed and/or replaced by more complex demand models, but the added value of doing so will depend on the specificity of the change in indirect taxation in the joint tax reform to be evaluated. Indeed, despite its restrictive character, this specification allows us to capture the real income effect of an indirect tax reform on the labor supply decision in a convenient fashion, and this might well be quantitatively the most important impact.

To illustrate the framework proposed in this article, we perform policy simulations that are inspired by a tax shift proposed in Belgium in 2023. The reform’s principal aim is to lower tax on labor incomes through a higher tax-free amount in the personal income tax, and it is partly financed by increases in VAT rates. We simulate a revenue neutral reform in which the increase of VAT rates covers the financing necessary for the proposed increase in the tax-free amount.

We limit our analysis in the empirical illustration to the budgetary and employment effects of the simulated reform and their distribution across households. We refrain from performing a proper normative analysis. To analyze the budgetary effect of the joint reform, we decompose the total effect into mechanical and behavioral components. The former measures the impact of the reform on government revenues when there is no change in individual behavior. That is, individuals are not allowed to adapt their bundle of commodities nor their job choice. The behavioral component, by contrast, collects the change in revenues that can only be ascribed to changes in individual behavior. To be able to assess the added value of our framework, we further decompose the behavioral effect in the impact of changes in commodity demand, of changes in labor supply due to the change in nominal disposable income, and changes in labor supply due to the change in consumer prices.

The article is organized as follows. In “The Piecemeal Modeling Framework” section, we present the piecemeal modeling framework. First, we present in the “Two-Stage Budgeting Approach” section, the main components and explain how these components are linked through two-stage budgeting. Second, the “Job Choice Model” section introduces our implementation of the job offer model. Third, the “Measuring the Effects of a Joint Tax Reform” section explains how to measure budgetary effects and how to decompose them into mechanical and behavioral effects. In the “Empirical Illustration” section, we illustrate the presented framework with an empirical application. First, we discuss our empirical modeling strategy in the “Data and Simulated Reforms” section, whereafter we present the simulation results in the “Results” section. The “Conclusion” section concludes the article. The appendices contain more detailed information on the construction of the subsample on which the RURO model operates (Supplemental Appendix A.1), on the estimated parameters of the RURO model, the simulated labor supply elasticities and the model fit (Supplemental Appendices A.2 and A.3), on the procedure we used to simulate with the RURO model (Supplemental Appendix A.4), and on additional simulation results (Supplemental Appendix A.5).

The Piecemeal Modeling Framework

In this section, we introduce the piecemeal modeling framework to evaluate the labor supply effects of a joint direct and indirect tax reform. We present the link between consumer prices and the job choice in a general fashion by means of a two-stage budgeting approach in the “Two-Stage Budgeting Approach” section. The “Job Choice Model” section presents the discrete job choice model (RURO), and the “Measuring the Effects of a Joint Tax Reform” section explains how we can disentangle the effects of a joint tax reform with our framework.

Two-Stage Budgeting Approach

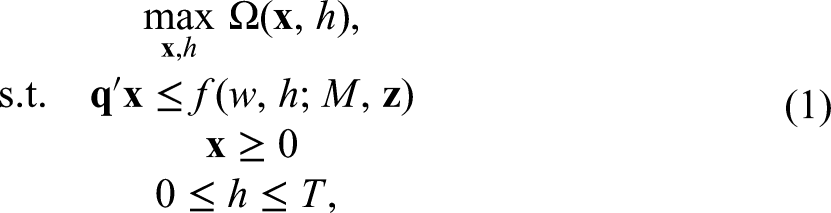

In its most general form, a (static) consumer decision model jointly treats the labor supply decision and the allocation of disposable income to commodities and savings. Formally, let

Such models of joint determination have been formulated and successfully empirically implemented in the literature (see e.g., Blundell and Walker, 1982, 1986; Browning, Deaton, and Irish, 1985; Browning and Meghir, 1991). These contributions, however, refrain from modeling the complexity of tax-transfer systems by assuming that labor income is simply the product of labor time and net wages. This renders these models less suitable for a more detailed assessment of the impact of the tax-benefit system on consumers’ behavior. However, introducing a more detailed description of the tax-benefit system poses a lot of intricate problems, as most existing tax-benefit systems cause the budget set

Many of these issues have been resolved by the introduction of discrete choice modeling into the empirical labor supply literature (popularized by Van Soest, 1995; for overviews, see Aaberge and Colombino, 2014; Blundell and MaCurdy, 1999; Creedy and Kalb, 2005; Blundell, MaCurdy, and Meghir, 2007; Keane, 2011; Keane, Todd, and Wolpin, 2011). In this approach, the budget constraint

However, the price to be paid for this increased realism on the side of labor supply modeling, is that one reverts to a simple tradeoff between disposable income and leisure, irrespective of the allocation of the former to different consumer goods. This independence between the labor supply decision on the one hand and the allocation of the income generated by it on the other, is only warranted if one assumes weak separability between consumer goods and leisure in the preference structure (Gorman, 1971). Unfortunately, this assumption was subject to much criticism when it comes to empirical applications (see e.g., Blundell and Walker, 1982; Browning and Meghir, 1991). Estimates of commodity demand functions can be severely biased when the erroneous assumption of separability between budget allocation and choice of leisure time is maintained.

So it seems as if one faces a tradeoff: either using a labor supply model in which real-world tax-benefit systems are integrated, but without indirect taxes and detailed consumption decisions integrated in the analysis; or modeling consumption decisions in great detail, but without the possibility to link this with a sufficiently realistic behavioral labor supply model. On top of this, even if a tractable general model for labor supply and the allocation of disposable income to commodities would be available, few datasets contain the information necessary to estimate such a model, as information on both gross labor income and disaggregated expenditures is generally not available.

In the absence of both a suitable encompassing model and the data to estimate such a model, we, therefore, propose a piecemeal modeling strategy to assess the impact of a joint tax reform at the micro-level. Given the limitations outlined above, our methodology proposes a consistent integration of different submodels, which are allowed to interact to the maximal extent. This interaction takes two forms. First, as will be explained in the “Data and Simulated Reforms” section, we rely on a statistical matching approach to impute expenditures into an income survey. Second, we advance a two-stage budgeting approach in which we allow (changes in) relative consumer prices to impact the labor supply decision as follows.

Under the assumption of weak separability, we can rewrite the overall utility function

The second stage of the two-stage budgeting approach consists in the allocation of the budget

Replacing

Notice that with this notation, the functional form of

In particular, we assume that

Job Choice Model

To model the first-stage labor supply decision, we employ a RURO framework (see Aaberge, Dagsvik, and Strøm, 1995; Aaberge, Colombino, and Strøm, 1999, and Dagsvik and Strøm, 2006; for surveys, see Aaberge and Colombino, 2014, and Dagsvik et al., 2014). The RURO model differs from the standard discrete choice multinomial logit model for labor supply (McFadden, 1973; Van Soest, 1995) in two ways. First, in contrast to the standard model, an individual chooses a job rather than optimal working hours. A job consists of a wage offer,

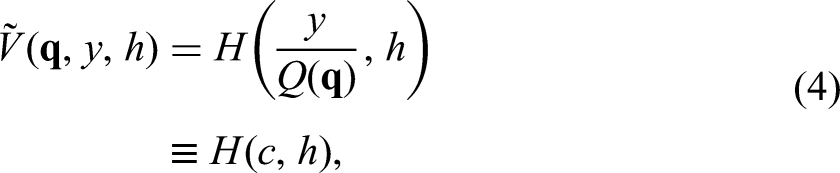

From the previous section, it turns out that the labor supply model should be specified in real terms, that is, deflating disposable incomes obtained from a particular job choice, by an individual-specific Divisia price index.

Formally, let

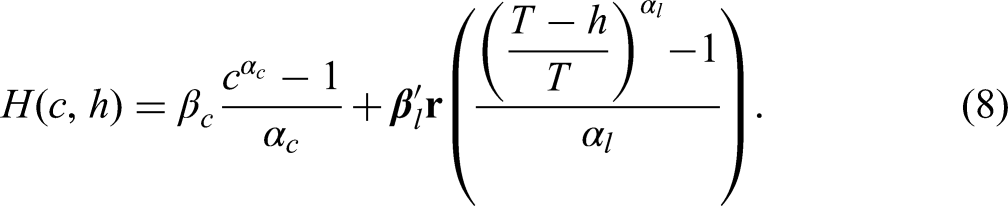

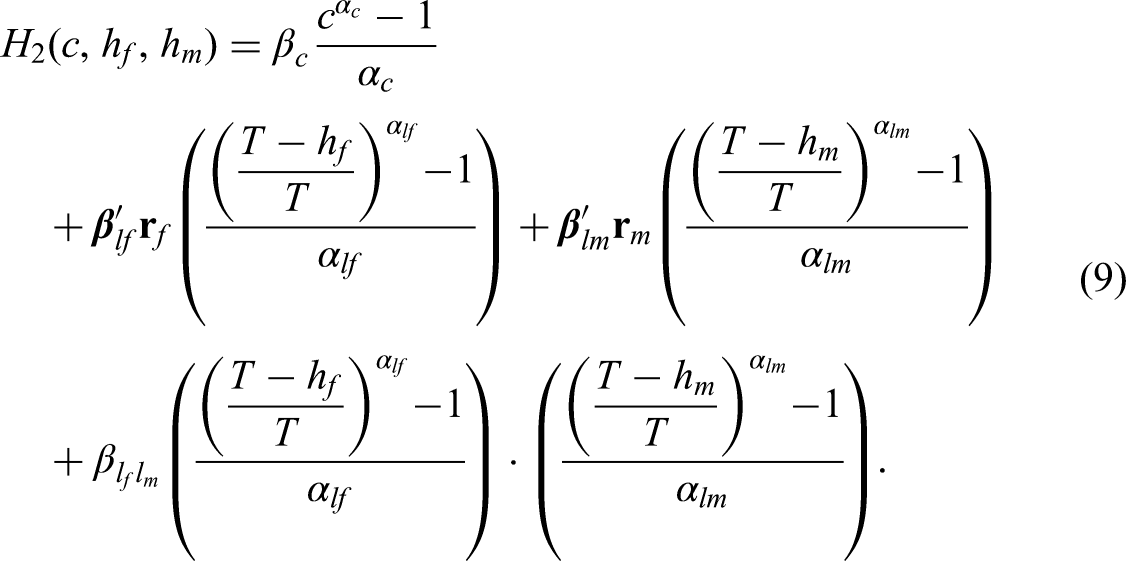

In our modeling strategy, we represent individuals’ opportunities and preferences by the following functional forms.

Opportunities

Preferences

The job choice model, in which unobserved characteristics of the job are present in the structural specification, allows to capture behavioral reactions that cannot be simulated within the standard random utility model (RUM) framework. For example, jobs with lower wages but with more attractive unobserved non-pecuniary characteristics might become more attractive after a reform in the tax-benefit schedule which lowers personal income taxes.

Measuring the Effects of a Joint Tax Reform

We decompose the budgetary effects of tax reforms into a mechanical and a behavioral component. The former measures the impact of the tax reform on government revenues when there is no change in individual behavior. That is, individuals are allowed to change neither their bundle of commodities nor their job choice. The behavioral component, by contrast, only collects the change in revenues that can be ascribed to those behavioral changes. This component consists of three elements: a change of consumed quantities, a change of labor supply due to changes in direct taxation, and a change in labor supply due to changes in consumer prices. Throughout, we indicate pre-reform variables by a subscript 0, while post-reform variables are subscripted by 1. Recall that we denote the chosen job by

Revenues from indirect taxation

We denote expenditures on good

First, we define the quantities following from applying the constant budget share assumption on the disposable income after the mechanical effect in the direct taxation, but before any labor supply adjustment,

Revenues from direct taxes and social security contributions

We define government revenues from personal income taxes and social security contributions as the difference between employer labor costs

Distributional effects

To assess the reform’s distributional impact, we subtract indirect taxes paid from disposable income. This concept acts as a measure for households’ real income and thus purchasing power. 14 In the cases where we assume constant quantities (the mechanical effect), it is a lower bound for a measure of welfare change based on the compensating variation (see Capéau et al., 2018).

Empirical Illustration

The framework proposed in “The Piecemeal Modeling Framework” section is illustrated by applying it to a joint tax reform scenario in Belgium. First, we discuss the data we use for the application, and explain the implemented joint tax reform in the simulations (the “Data and Simulated Reforms” section). Thereafter, we present the results (“Results” section) focusing first on the budgetary and employment effects (“Budgetary and Employment Effects” section) and then on the distributional impact of both the mechanical and behavioral effects (“Distributional Analysis” section).

Data and Simulated Reforms

We implement our approach on Belgian data. We argued that income should enter the utility of the RURO job choice model in real terms. To construct a real income concept we utilize the arithmetic tax and benefit microsimulation model EUROMOD, which incorporates both direct and indirect taxes (Sutherland and Figari, 2013). 15

EUROMOD runs on the Statistics on Income and Living Conditions (SILC) survey, which is a micro-level dataset that contains detailed information on income, poverty, social exclusion, and other living conditions. For Belgium, the survey’s reference population includes all private households and their current members residing in the country. Individuals living in collective households, such as hospitals, youth institutions, and old people’s homes are excluded from the reference population. All of our calculations in the simulation stage are performed on the Belgian SILC 2019, which contains 15,409 individuals who live in 6,762 households. The RURO model was estimated on pooled SILC’s of 2015, 2017, and 2019. 16

SILC does not contain data on expenditures, which is required to calculate indirect taxes paid by the households and to construct the household-specific Divisia price indices, needed to estimate the RURO model. We impute consumption income shares in SILC, based on a statistical match between SILC and the Household Budget Survey (HBS). We link SILC waves 2015, 2017, and 2019 with, respectively, HBS waves 2014, 2016, and 2018. The statistical match is based on predictive mean matching methodology, and is discussed in detail by Akoğuz et al. (2020). The imputation of budget shares is now standardized and implemented in EUROMOD as part of the indirect tax tool. 17

The RURO model was estimated on a subsample of the SILC data of waves 2015, 2017, and 2019, that only contains those households in which the reference person and their partner, if any, are available for the labor market. Supplemental Appendix A.1 contains more details on the composition of this subsample. In the “Job Choice Model” section, we presented our functional forms. Supplemental Appendices A.2 and A.3 present the estimated model parameters, the simulated aggregate wage elasticities of labor supply, and the model fit.

18

The elasticities of our model are low, and in this sense broadly in line with the abundant micro-econometric estimates for other countries (see Bargain, Orsini, and Peichl, 2014 and Mastrogiacomo et al., 2017 for overviews for several European countries and the United States). First, the total own wage elasticity of 0.19 for single females and 0.23 for single males is mainly determined by the participation elasticities. The total own wage elasticity of 0.13 for females in couples and 0.11 for males in couples is mainly determined by the intensive margin elasticities (see Supplemental Table A.4). Second and contrary to the cited literature, the elasticities are not declining with the level of the gross wage rate (see Supplemental Tables A.5 and A.6). Third, in couples we find substantial negative cross-wage elasticities (

After estimating the model parts, we use the model to simulate the effects of a tax reform inspired by a tax shift proposal in Belgium. 19 The tax reform constitutes primarily of an increase of the tax-free amount in the personal income tax, financed by an increase of the VAT rates. We bring all reduced rates (resp. 6 percent and 12 percent) to the standard rate of 21 percent. The revenues from the reform in indirect taxation determine the increase in the tax-free amount. However, we know that our model captures only half of all indirect taxes paid in the baseline. This can partly be explained by the under-reporting of alcohol and tobacco consumption, but is mainly due to our inability to observe VAT and excise-payments from transactions between firms. As a result, we multiply the indirect tax revenues registered in the model with the inverse of the partial coverage rate in the baseline to determine the additional VAT-revenues available. Moreover, the goal of the reform in direct taxation is to increase the net gain of working. Therefore, the increase in the tax-free amount is neutralized in the later stage of the personal income tax calculation for those receiving replacement incomes, proportional to the share of replacement income in taxable income. As a result, the tax-free amount increases from €9,050 to €14,955 (euros of 2019).

The (household specific) imputed income shares serve as parameters of the Cobb–Douglas preferences in our two-stage budgeting approach. They can thus be used to simulate the effects of indirect tax reforms on expenditures, indirect taxes paid, and the Divisia price indices. The weak separability assumption we exploit in the simulation stage implies that we do not allow the budget shares to change when labor market status alters as a consequence of a tax reform.

Next, using the new Divisia indices following from the indirect tax reform, and the possibility to simulate direct tax reforms with EUROMOD, the impact of a reform on households’ labor supply decisions can be simulated by our estimated RURO model. The simulation procedure is explained more in detail in Supplemental Appendix A.4. Note that households who do not belong to the subsample on which RURO was estimated, can alter their behavior only through the expenditures margin in our simulations.

Results

Budgetary and Employment Effects

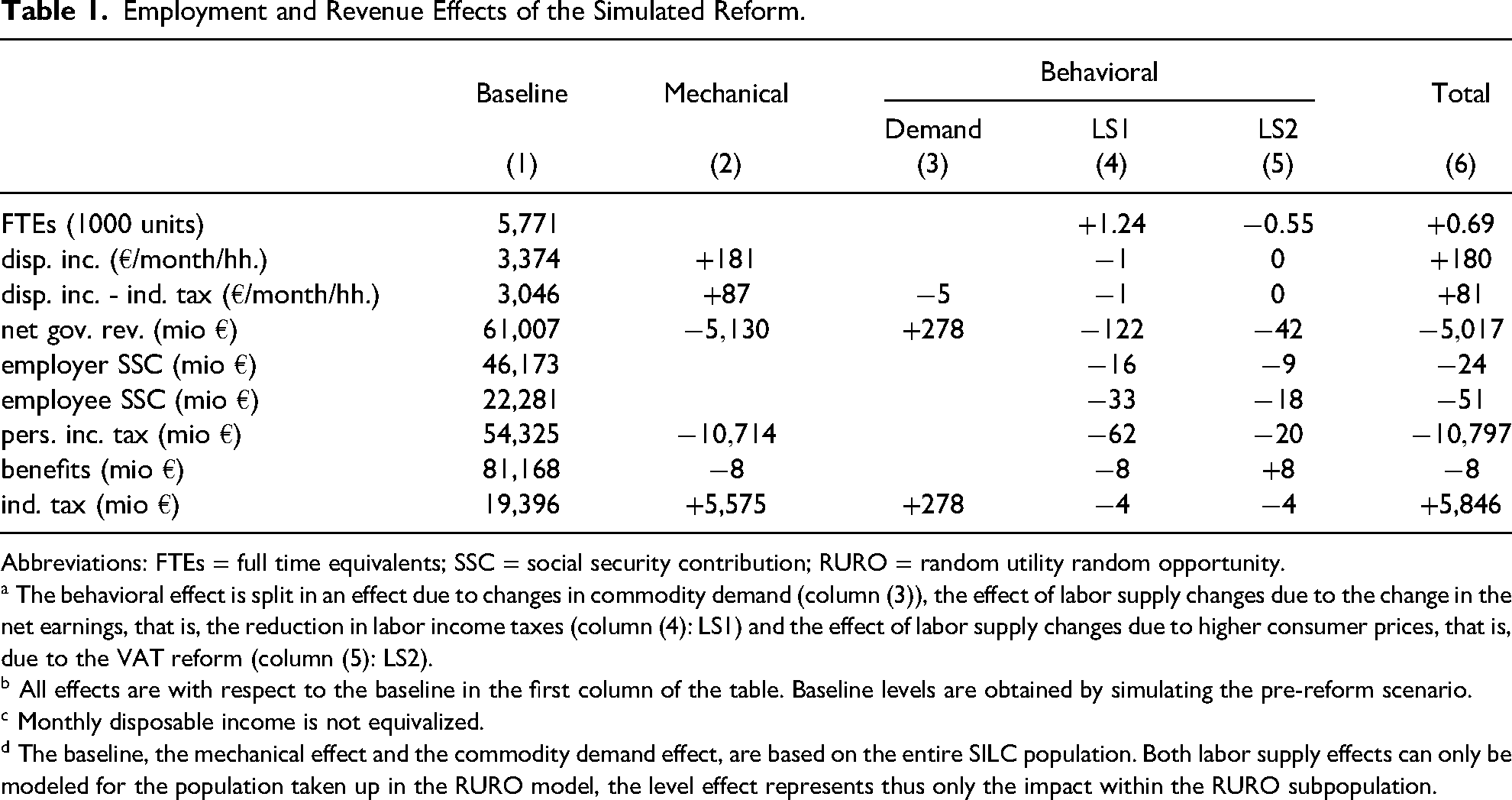

As discussed in the “Measuring the Effects of a Joint Tax Reform” section, we decompose the total budgetary effect of a tax shift into two distinct parts: a mechanical effect (or “impact” effect) and a behavioral effect. The former measures the effect when households could not alter their consumption bundle and their labor supply with respect to the baseline scenario. The latter, by contrast, exclusively captures the impact of these behavioral responses, and is further decomposed in a commodity demand effect, the labor supply effect of the direct tax reform, and the labor supply effect of the change in consumer prices. Changes in labor supply are predicted by the RURO model and we assume that households alter their consumption according to the constant income shares assumption, that is, assuming Cobb–Douglas preferences. Note that employment effects are by definition always behavioral effects. Unless otherwise stated, results are grossed up at population level by means of statistical weights.

Table 1 displays the absolute changes of the joint tax reform with respect to the simulated baseline. The first four rows show the employment effect, the effect on household disposable income, the effect on real disposable income defined as disposable income minus indirect taxes paid, and the effect on government revenue. The impact effect of the simulated reform is a loss in personal income tax revenue of €10.7bn, a considerable bill for the treasury. 20 The personal income tax reductions are immediately reflected in an increase in disposable income of households: it increases with €181 per month per household.

Employment and Revenue Effects of the Simulated Reform.

Abbreviations: FTEs = full time equivalents; SSC = social security contribution; RURO = random utility random opportunity.

The increase in VAT rates leads to additional revenues of €5.6bn, pushing down the initial cost from €10.7bn to €5.1bn. 21 This is also revealed in the third line in which we show the impact on disposable income minus indirect taxes paid at the household level. The impact effect goes down from €181 to €87 per month per household, implying an additional indirect tax bill of €94 per month.

The first line of table 1 shows the additional employment, expressed in full time equivalents (FTEs), triggered by the tax reform. 22 The rise in net earnings triggered by the reform induces an additional employment of 1,240 FTEs. Not unexpectedly, the diminution of the increase in disposable income net of indirect taxes comes with an erosion of the employment effect: due to the VAT increase almost one half of the newly created FTEs are lost, and additional employment due to the joint reform falls back to 690 FTEs.

The cost recovery effect of this additional employment is however negative. This cost recovery is the net effect of a decrease in benefits to be paid due to more employment, an increase in social security contributions paid by the employer and by the employee, and an increase in the personal income tax, as a result of increased labor supply, and finally, an increase in indirect tax payments following the increase in disposable income, and thus higher consumption. Surprisingly, the additional employment of 1,240 FTEs, due to the change in net earnings, is not translated into an increase of the taxable base of social security contributions and the personal income tax (column (4)). Contrary to the expectation, revenues from social security contributions drop with €49 million (€16 million paid by the employer and €33 million paid by the employee), and personal income tax revenues decrease with €62 million. Later in this section, we will show that the negative impact on government revenues of the labor supply reaction to higher net earnings can be attributed to a negative income effect. The income of new entrants is rather moderate, so they generate few additional tax revenues. At the same time, the tax reform allows persons already working to work less and to afford jobs with somewhat lower gross wages. Since the tax schedule is progressive, this effect excavates possible cost recovery effects, especially when individuals higher up in the income distribution are lowering their labor supply or are choosing jobs with a lower wage. Contrary to what is often raised in the public debate, viz. that a bill of €10.7bn in the personal income tax will finance itself through cost recovery, the final bill exceeds the initial one.

As expected, the impact of the increase in VAT rates (column (5)) leads to an additional deterioration of revenues from social security contributions and personal income tax, but to a lesser extent than the initial labor supply reaction to the reduction of personal income taxes.

The only positive element for cost recovery is the impact of higher indirect tax revenues due to a higher disposable income after the personal income tax reform (column (3)). In the first stage, without any labor supply reactions, the demand adjustment results in €278 million additional revenues. The labor supply reactions, which in general lower disposable income to be spent, deteriorate this effect slightly with €8 million (€4 million in both columns (4) and (5)). The final bill of €5.017 billion is still slightly lower than the initial bill of €5.13 billion.

Summing up these aggregate results, we conclude that the actual tax shift does indeed create additional employment, but that the numbers are very small overall. And due to the reaction on the intensive margin, both in hours and in wages, the cost recovery effects are negative. Moreover, revenue neutrality obtained by higher VAT rates, erodes the employment effect, and thus exacerbates the negative cost recovery effects. The final bill, after behavioral effects, is slightly lower than the initial bill, only due to the additional VAT paid after the increase in disposable income. To deepen our understanding of these aggregate effects, we first look at the employment effects in more detail.

Heterogeneity in labor market effects

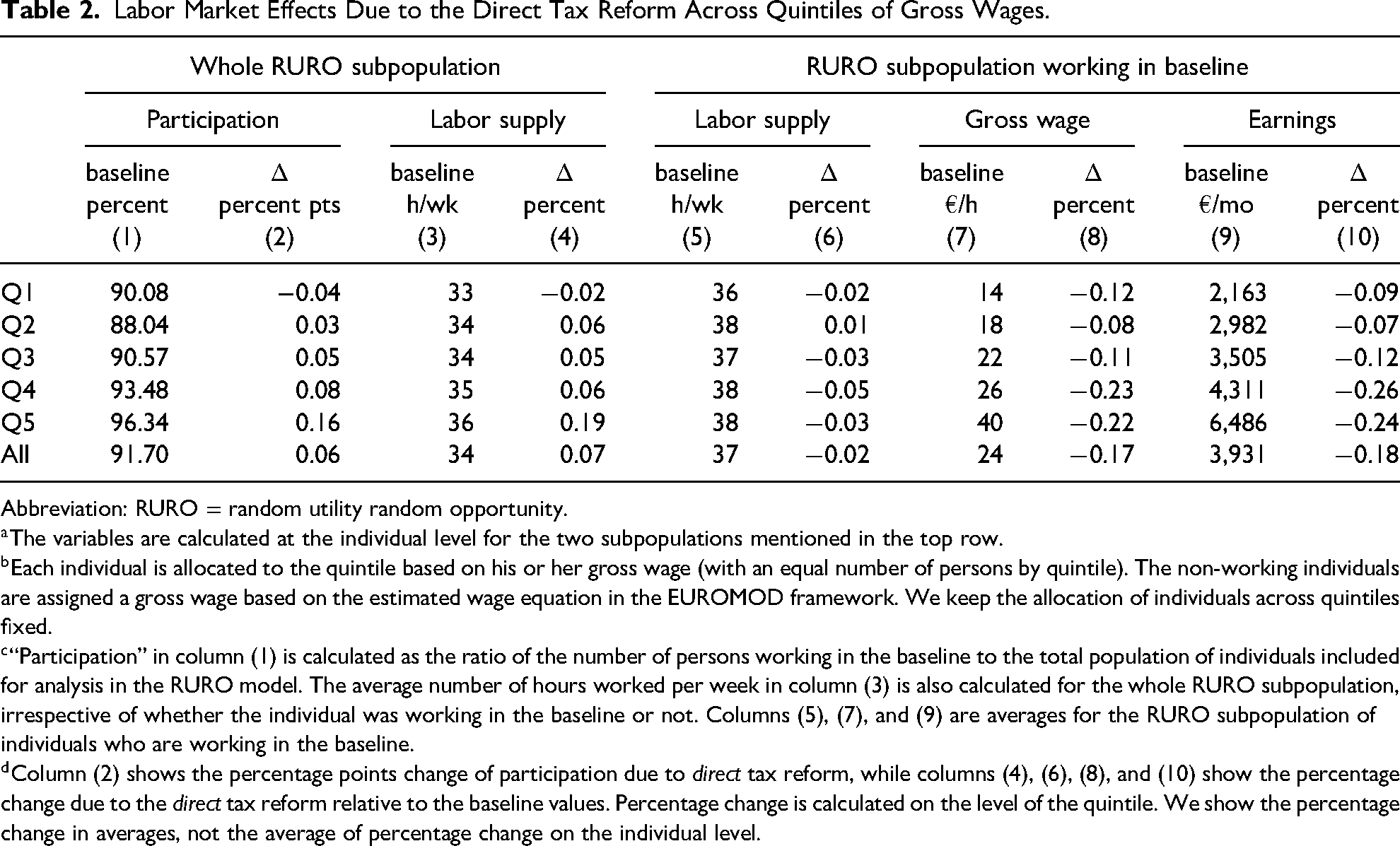

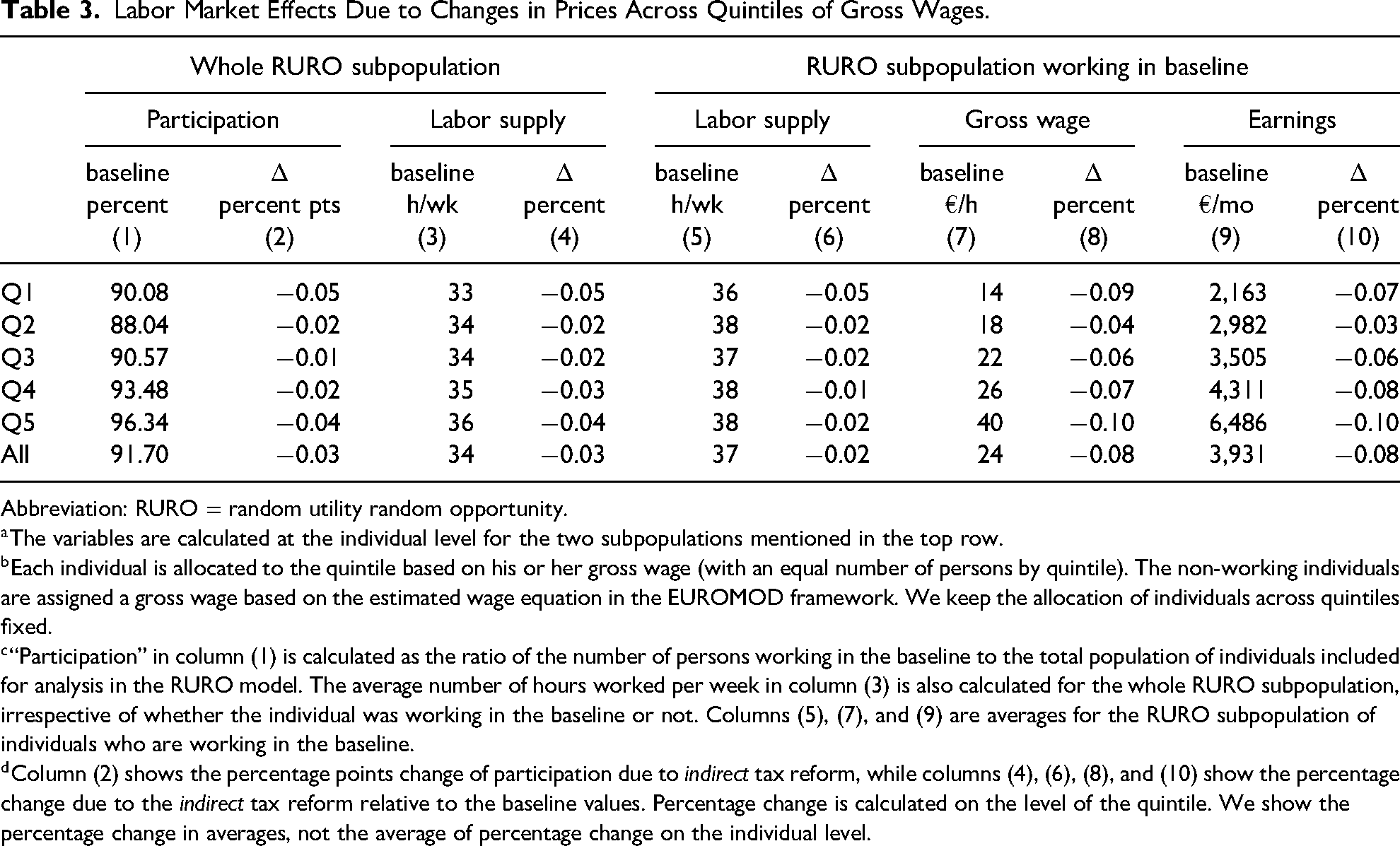

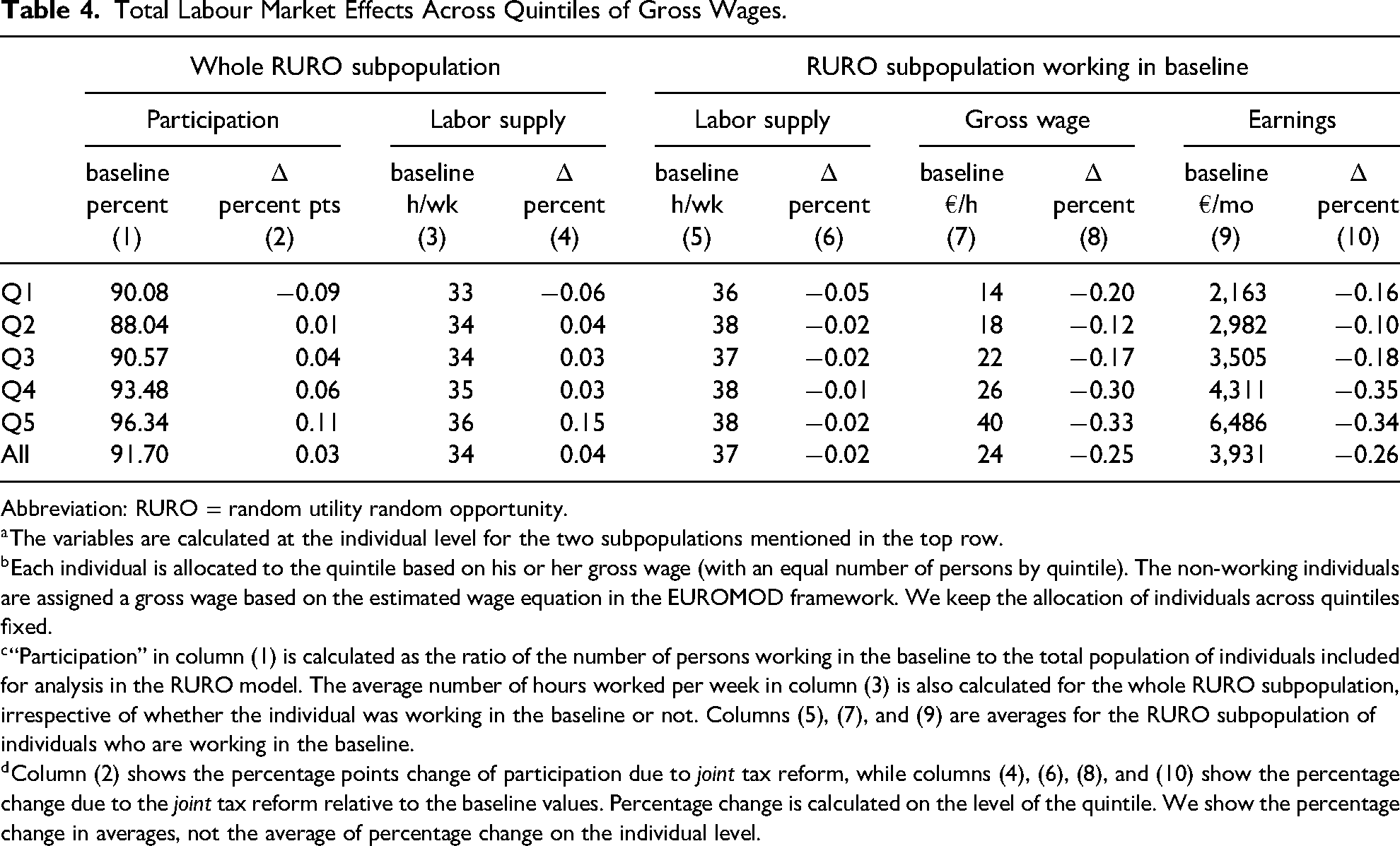

In tables 2–4, we summarize the labor market effects of the simulated reform. The tables present the effects of the reform on job choice for the population of individuals included for analysis in our job choice model (“Job Choice Model” section), across quintiles of the gross wage. Table 2 shows the labor market effects due to the reform in the personal income tax system. Table 3 shows the additional labor market effects due to the higher consumer prices, which follows from the indirect tax reform. Finally, table 4 summarizes the total labor market effects of the joint reform. To order the individuals, we use the gross wage rate observed in the job choice of the baseline for those individuals who work in the baseline. For the non-participating individuals, we impute a gross wage based on their observable characteristics and the wage equation used in the EUROMOD framework. Columns (1)–(4) describe the effects for the whole RURO population, both on the extensive (working or not, labeled here as “participation”) and on the intensive (number of hours worked per week) margin. Gross wage being a characteristic of the job, changes in job choice may also trigger an additional effect on earnings, which are the product of gross wage and hours worked. This is presented in the right part of tables 2–4 (columns (5)–(10)). In that part of the tables, we limit ourselves to the population being employed in the baseline. The reason is that wages of non-working individuals are not observed. Hence we cannot calculate the percentage change in wages and earnings for these individuals. 23

Labor Market Effects Due to the Direct Tax Reform Across Quintiles of Gross Wages.

Abbreviation: RURO = random utility random opportunity.

Labor Market Effects Due to Changes in Prices Across Quintiles of Gross Wages.

Abbreviation: RURO = random utility random opportunity.

Total Labour Market Effects Across Quintiles of Gross Wages.

Abbreviation: RURO = random utility random opportunity.

Column (2) of table 2 shows that the increase in employment of 1,240 FTE’s, discussed in the “Budgetary and Employment Effects” section, mainly results from an increase in participation of individuals characterized by a high gross wage. The increase of participation is most outspoken in the top quintile of the gross wage distribution (an increase of 0.16 percentage points from a baseline level of 96.34 percent). There is a negative impact on participation in the first quintile of observed wages, and only small effects in the second and third wage quintiles. This negative income effect also pops up in column (4), where we find that for the bottom quintile of the gross wage distribution, the average number of hours worked decreases. Overall, the average number of hours worked per week increases with 0.07 percent due to the increase in net earnings.

The negative effect on labor supply of a significant increase in disposable income following a tax reduction does not come as a surprise. It has been documented frequently in other assessments of tax reforms based on modeling behavior with a standard discrete choice approach (e.g., Blundell et al., 2000). However, the RURO model is uniquely equipped to unveil a potentially more important, additional, “income effect.” It shows up in column (8) as a considerable reduction in gross wages, itself the result of the switch by some individuals to the choice of a wage-hours package with lower gross wages than before the reform. On average, gross wages, following from the choice of jobs after the direct tax reform, are 0.17 percent lower than the gross wages of the jobs chosen in the baseline. This effect is mainly driven by the upper half of the gross wage distribution. 24 Combined with the decrease in labor supply this trickles down in a reduction of the taxable base of both social security contributions and personal income taxes: gross earnings decrease by 0.18 percent. Since this effect is predominantly found in the upper half of the distribution (earnings go down by 0.24 percent in the top quintile of gross wages, whereas they decrease by only 0.09 percent in the bottom quintile), this explains why the negative revenue effect in the progressive personal income tax is larger than the negative revenue effect in the proportional social security contributions.

The crux here is not whether we can produce the right amount of cost recovery. But the structural model of job choice unveils a mechanism which might at least partially explain the often disappointing revenue figures following tax reductions in the form of increases of household disposable incomes. Lowering of personal income taxes allows some individuals to afford a new job choice which comes with a lower gross wage, but with less hours to work and preferred unobserved characteristics (less stress, lower commuting time, etc.). Using a structural model which allows for this additional behavioral channel shows that a good empirical estimate of this additional “income” effect is crucial to produce credible revenue predictions.

Table 3 shows the impact on labor supply due to the increase in VAT rates, and thus the decrease in real disposable income triggered by the increase in consumer prices. The decrease in additional FTEs due to joint tax reform as discussed in the “Budgetary and Employment Effects” section is due to a reaction on both the extensive margin and the intensive margin across the wage distribution. This is the result of a positive income effect, real disposable income has dropped, and a negative substitution effect between leisure and consumption. Indeed, the real gain of working is now lower. On all margins, the income effect does not compensate the substitution effect. Participation (column (2)) drops with 0.03 percentage points, driven by changes across the entire gross wage distribution. Also total labor supply decreases across the entire wage distribution, amounting to a total decrease of 0.03 percent, relative to the baseline level of labor supply. Focusing on only those working in the baseline, we additionally find that the increase in VAT rates has a similar effect on the wages resulting from the job choice as the decrease of the personal income tax, albeit less outspoken. Overall, wages drop by 0.08 percent. The decrease of worked hours, and of gross wages, results in an additional deterioration of the taxable base of personal income tax and social security contributions, gross earnings.

Table 4 combines both labor supply reactions, and shows the overall reactions for the joint tax reform. Regarding the extensive margin, the initial effect of the increase in net earnings dominates the impact of the increased VAT rates. Participation increases with 0.03 percentage points due to the joint tax reform. The same is true for the overall hours, which increases with 0.04 percent. The impact of both the direct and indirect tax reform on wages has the same direction. The initial negative impact on wages, mainly driven by the top gross wage quintiles, is exacerbated by the indirect tax reform, leading to an overall drop in gross wages of 0.25 percent. The gross earnings decrease due to the joint reform with 0.26 percent.

Distributional analysis

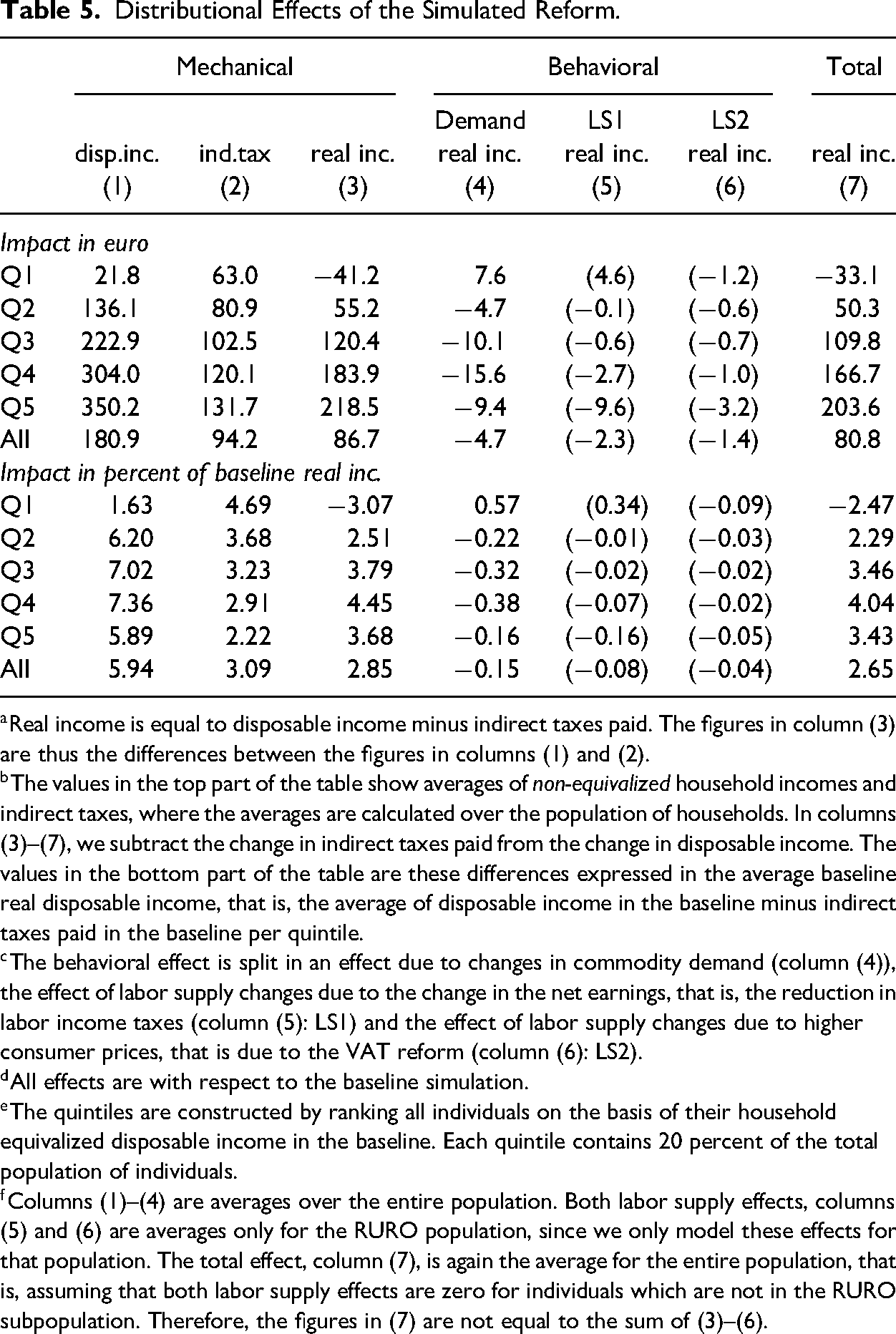

A comprehensive distributional analysis should incorporate all three elements of the reform: (1) the change in disposable incomes, due to the higher tax-free amount in the personal income tax for individuals active on the labor market, (2) increases in indirect taxes to be paid, which are also to be borne by non-active persons, affected by a commodity demand adjustment, and finally, (3) the changes in real disposable income and leisure time induced by changes in behavior. As mentioned above, in this article, we abstract from the effect of changed leisure time on individual welfare. 25 The results are summarized in table 5.

Distributional Effects of the Simulated Reform.

Contrary to the results in tables 2–4, where we only used the subpopulation modeled in the behavioral labor supply model, we now present results for the whole population. Each quintile of table 5 contains 20 percent of the number of persons in the population (including children, pensioners, etc.). The position in the ordering is determined by equivalized baseline disposable income of the household the person belongs to. In the top part of the table, we show the effect on monthly household disposable income net of indirect taxes paid. The amounts in the top part of the table are non-equivalized. They should be read as the averages of household incomes or of indirect taxes paid by the household. The bottom part of table 5 expresses the changes in percent of baseline real disposable income, that is, disposable income net of indirect taxes paid.

The first observation to be inferred from table 5 is the important impact of the financing through indirect taxes on the distributional assessment of the reform. Column (1) shows that the mechanical change in disposable income is broadly regressive. The mechanical effect increases up to the fourth quintile, both in euro and relative to baseline real income (bottom part of table 5). Only the impact for the top quintile, although still larger in absolute amounts, is smaller than the impact of the fourth quintile relative to baseline real disposable income. The increase in indirect taxes is more proportional to baseline real disposable income. This again leads to a regressive pattern: with the exception of the bottom quintile, expressed in percent of baseline real income, the indirect tax hike declines across the income distribution. For the bottom quintile, the indirect tax increase turns an already modest impact of disposable income into a substantial loss of

The second message from table 5 is the impact of the behavioral changes on the distributional assessment. First, given the mechanical impact on disposable income and indirect taxes, the expenditure model with constant income shares makes households in the bottom quintile reduce quantities. In the top four quintiles, households spend more, since the mechanical impact on disposable income is larger than the mechanical impact on indirect taxes paid. The effect on real income of this demand reaction is displayed in column (4) of table 5 by tabulating the additional change in real income stemming from moving from constant quantities to constant income shares. 26 It shows that the impact of the reaction in commodity demand counteracts the distributional picture of the mechanical impact. As in the previous sections, our framework also allows to disentangle the labor supply effect of the increase in net earnings due to the direct tax reform (displayed in column (5) of table 5) from the labor supply effect of the increase in consumer prices due to the indirect tax reform (displayed in column (6) of table 5). The labor supply effects are shown between brackets, since these figures represent the average effect for only those individuals belonging to the subpopulation taken up in the job-choice model. Both labor supply responses have distinct, albeit small, impacts on the distributional picture. First, column (5) reveals that the increase of the tax-free amount corrects the regressive mechanical distributional picture further, at least in monetary terms. The reasons are that (1) in the lowest equivalized disposable income quintile households start working, or work more, leading to additional disposable income, and (2) that households in the top part of the distribution will work less or will accept lower wages, leading to a decrease in disposable income. 27 Second, the labor supply effect due to the price change in column (6) is very different, with a decrease in disposable income for all quintiles. As discussed in the “Budgetary and Employment Effects” section, the increase in VAT rates leads to a decrease of labor supply across the gross wage distribution. Even though the behavioral effects slightly counteract the regressive nature of the joint tax reform, overall, the reform does lead to a regressive change in real disposable income, with the bottom quintile losing 2.5 percent of real disposable income (€33 per month), while the top three quintiles gain more than 3.4 percent (resp. €110, €167, and €204 per month).

Conclusion

In this article, we propose a piecemeal modeling strategy to establish a micro-based budgetary and distributional evaluation of a joint reform in the direct and indirect tax systems. Using a two-stage budgeting approach, we allow (changes in) commodity prices to interact with households’ labor supply, and even more general, job choice decision. Assuming a Cobb–Douglas subutility of consumption, we show that deflation of disposable income with the household specific Divisa price index bridges the commodity prices with the labor supply decision. We employ this approach to a RURO model of labor supply. This enables us to highlight an additional margin on the labor market, the accepted wage in the job choice.

We illustrate the framework with an empirical application of a proposed Belgian tax shift. An increase in the tax-free amount in the personal income tax for working individuals is financed by an increase of reduced VAT rates of 6 percent and 12 percent to the standard rate of 21 percent. We find substantial evidence that it is important to account for indirect taxes in the assessment of the distributional and budgetary evaluation of a joint tax reforms. Our results show that, despite an overall increase in labor supply, cost recovery effects from personal income taxes and employee and employer social security contributions are negative. This lack of cost recovery is partly explained by the negative employment effect at the intensive margin, due to the income effect after the personal income tax reform. Jobs with on average less working hours are chosen, a behavioral reaction which is in line with the literature. However, the erosion of government revenues due to the behavioral impact is enhanced by an additional mechanism, unveiled by the use of the rich structural specification of the RURO model. Indeed, the RURO model predicts that the personal income tax reform might induce some individuals to choose jobs with lower gross wages, especially at the top of the gross wage distribution. Since lower gross wages trickle down into a negative effect on the taxable base for both PIT and social security contributions, our job choice model might point to an important new explanation for the low cost recovery of this kind of reforms.

Our framework also allows us to disentangle the overall employment effects from those stemming from the indirect tax reform, namely from the impact of changed commodity prices. The negative cost recovery effects worsen considerably due to the impact of increasing VAT rates on labor supply. Higher consumption prices means that the net marginal gain of working decreases. As a result, part of the positive impact of the direct tax reform on participation is deteriorated, and more households choose to work less hours and accept a lower wage in their job choice. Our simulations indicate that a revenue neutral reform would destroy almost one-half of the newly created FTEs, compared to the impact of solely the personal income tax reform, and the employment effect of increased prices accounts for one-fourth of the negative cost recovery effects of the overall tax reform.

Also the distributional picture of the simulated reform is affected by the behavioral changes we model in our framework. If we keep households’ consumption bundle and labor supply fixed, our results show that the poorest gain the least from the reform. The gain in percentage of disposable income increases up to the fourth quintile. The bottom quintile incurs a loss. If we allow households to alter their behavior the pictures slightly changes. The poorest decile now loses less due to more employment income. From the second to the fifth quintile, the mechanical gain deteriorates after taking into account behavioral changes, with the largest impact in the top two quintiles. This is mainly due to change in commodity demand, and change in job choice which entails on average less hours and a smaller gross wage.

We argue that the piecemeal modeling framework is an attractive set-up for the evaluation of joint tax reforms. Even though it is well known that the job choice is based on the real return to hours worked, often in empirical applications, or policy evaluations, any change in indirect taxation is assumed to have no employment effect. The proposed framework is an alternative to a comprehensive model of the labor supply decision and the consumption allocation decision.

Nevertheless, the piecemeal modeling framework is built on some strong assumptions, and it does not take into account all feedback effects of a joint tax reform. First, the two-stage budgeting approach is based on the assumption of weak separability of utility between leisure and consumption. Second, our proposal to deflate disposable income in the labor supply decision with the Divisia price index, stems from the Cobb–Douglas functional form of subutility of consumption. We acknowledge this is a strong assumption, but only use it as a tractable way to focus on the issue of incorporating consumer price changes in the labor supply decision. Moreover, this strong assumption allows us to use the full heterogeneity in expenditure patterns. We might of course introduce more involved demand systems to model the changes in the income shares following the change in income and in consumer prices. Yet, we conjecture that, given that we already modeled a large amount of household heterogeneity in the baseline spending patterns, the effect of additional changes in budget shares on the labor supply decision would be minor (compared to the current modeling strategy with constant income shares). Anyhow, the piecemeal modeling framework allows to link such more involved modeling of the consumption allocation with the labor supply decision. Especially in the case of evaluation of the labor supply effect of a very specific indirect tax reform, of which incidence is very unevenly spread in the population, or where non-standard commodity demand reactions are expected, for example, related to the green transition, such an extension of the piecemeal modeling framework is advised. Finally, the framework only allows to evaluate the feedback effects of a joint tax reform that stem from the employment decision of households. There is no endogenous impact of the joint tax reform on labor demand, or on the wage formation, nor are there general equilibrium effects on commodity prices and wage rates. However, also in this case, the piecemeal modeling set-up is suitable to be extended with such general equilibrium effects. For example, exogenously determined labor demand reactions can be taken up by the RURO model, by shifting the distribution of opportunities of households. The proposed framework, which links commodity demand models with models of labor supply, certainly does not prevent the modeling of other important feedback effects of policy reform.

Supplemental Material

sj-pdf-1-pfr-10.1177_10911421231198738 - Supplemental material for Piecemeal Modeling of the Effects of Joint Direct and Indirect Tax Reforms

Supplemental material, sj-pdf-1-pfr-10.1177_10911421231198738 for Piecemeal Modeling of the Effects of Joint Direct and Indirect Tax Reforms by Bart Capéau, André Decoster and Stijn Van Houtven in Public Finance Review

Footnotes

Acknowledgments

We are grateful to Sebastiaan Maes, Toon Vanheukelom, Rolf Aaberge, Ugo Colombino, John Creedy, John Dagsvik, Norman Gemmell, Zhiyang Jia, Tom Strengs, and Tom Wennemo, as well as workshop participants at the University of Essex, the World Bank and the New Zealand Treasury for comments on and help with earlier versions of the paper. The results presented here are based on EUROMOD version I4.0+. EUROMOD is maintained, developed and managed by the Joint Research Centre of the European Commission, in collaboration with national teams from the EU member states. We are indebted to the many peaople who have contributed to the development of EUROMOD. We make use of microdata from the EU Statistics on Income and Living Conditions (EU-SILC) and the Household Budget Survey (HBS) made available by Statbel (contract 2022-026 (HBS-SILC)). The results and their interpretation are the authors’ sole responsibility.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article benefited from financial support from the National Bank of Belgium (project 3H170248), the Belgian Federal Science Policy Office BELSPO (project BR/132/A4/BEL-Ageing and project P2/223/P3/E4BEL), the Joint Research Centre Sevilla (Contract No. 198961-2015 A10-UK) and FWO (Grant G0732020N).

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.