Abstract

The traditional literature on fiscal federalism prescribes centralization of redistributive tasks to avoid welfare- or tax-induced migration. More recent work shows that even if the redistributive part of taxation, namely progressivity, is set by an upper-layer government and lower-layer governments only compete via a tax multiplier, income sorting can flatten effective tax progressivity. We argue that upper-layer governments anticipate the impact of local income sorting and strategically adjust their statutory tax schedules. The mobility of the income tax base sets limits to such strategic behavior. We apply causal machine learning methods to identify the effects of decentralization on the statutory tax structure in Switzerland. More decentralized cantons implement more redistributive statutory tax schedules for the least-mobile household types.

Introduction

It is often feared that fiscal decentralization and the resulting competitive pressure on local governments undermine welfare policies or, at least, lead to inefficiently low levels of redistribution. To preserve a certain level of redistribution, already the seminal normative contributions by Tiebout (1956), Stigler (1957), Musgrave (1971), and Oates (1972) argued that redistributive functions of the public sector should be centralized.

We study decentralized income taxation, whereby the redistributive parameter, namely the progressivity of the income tax schedule, is centralized at an upper-level government, while local governments compete with a tax multiplier (“tax shifter”) levied on said schedule. Previous research has shown that even if the primary redistributive parameter is centralized, income sorting can undermine effective redistribution in an otherwise decentralized income tax setting (e.g., Ellickson 1971; Westhoff 1977; Ross and Yinger 1999; Feld and Kirchgässner 2001; Epple and Nechyba 2004; Hodler and Schmidheiny 2006; Schmidheiny 2006a, 2006b; Schaltegger et al. 2011). If the tax base is mobile, high-income individuals with high statutory tax rates could sort into jurisdictions with an overall lower exploitation of the tax base. Hodler and Schmidheiny (2006) analyze such a setting in the canton of Zurich, Switzerland, whereby the cantonal level defines the tax schedule and local municipalities compete with a tax shifter. They document that the effective tax progression is lower than it is defined in the statutory tax schedule. As sorting is far from complete—even in the context of the metropolitan area of Zurich, in which mobility costs are low—the study shows that substantial redistribution is possible.

The flattening of the effective tax progression in comparison to the statutory tax schedule is an interesting stylized fact per se. However, it is difficult to interpret this flattening from a policy perspective. If the statutory tax schedule reflects the socially desired degree of redistribution, then decentralization undermines the redistributive goal. Such an assumption is, however, difficult to sustain as the definition of the tax schedule is itself a policy parameter. We argue that the definition of the statutory tax schedule is endogenous and that potential sorting is taken into account in the political process. From a traditional normative public economics perspective, policymakers in upper-level governments could internalize the effects of income sorting and the resulting flattening of the effective tax schedule. Accordingly, they could define statutory tax schedules, which are comparatively more redistributive than without income sorting. Alternatively, from a public choice perspective, the fact that high-income individuals can (partially) escape statutory progression by sorting into jurisdictions that exploit the tax base to a lower degree, might lead to less resistance to comparatively more progressive statutory rates. Governments could exploit this weakened opposition by high-income individuals and pander to the remaining electorate of low- to intermediate-income households.

Both mechanisms are constrained by the mobility of the tax base. They are feasible for intermediate levels of mobility but not for very high or very low levels of mobility. In case of very low mobility of the tax base, income sorting is not a great concern. In case of very high mobility, the tax base might react very strongly and decide to leave even the upper-level jurisdiction, which sets the tax scheme. This naturally limits the options to tax more progressively than relevant competitors.

We analyze the impact of different degrees of fiscal decentralization on the structure of statutory income taxes for different household types that differ in their degree of mobility. We take advantage of the Swiss institutional environment where 26 upper-layer governments (cantons) define the degree of fiscal autonomy provided to their local governments (municipalities). The cantons define the income tax schedule, while municipalities levy a tax shifter (tax multiplier) on that same tax schedule. Hence, it is the upper-layer government that decides on the redistributive part of taxation (progressivity), while local governments decide on a surcharge only (level). We estimate how the degrees of fiscal decentralization affect the statutory tax structure (level and progressivity) of different household types (singles, married couples, married couples with two children, retired).

We document two patterns. First, fiscal decentralization tends to reduce the relative statutory tax burdens overall for all household types except the retired. This overall level effect is consistent with the well-documented size effects of fiscal decentralization. The literature has long discussed whether and how decentralization affects the size of government, starting with efficiency arguments in the public economics tradition by Tiebout (1956), Oates (1972, 1999) and the public choice critique by Brennan and Buchanan (1980); or, later on, the tax competition literature initiated by Wilson (1986), Zodrow and Mieszkowski (1986) and Wildasin (1991); as well as the yardstick competition literature initiated by Besley and Case (1995). Empirically, a number of studies observe that fiscal decentralization is indeed associated with a smaller public sector in terms of expenditures and revenues (e.g., Oates 1985; Shadbegian 1999; Feld, Kirchgässner and Schaltegger 2010). 1

Second, and more interestingly in our context, decentralization reduces the statutory tax burden more strongly on the low- to intermediate-income groups of households with limited mobility (such as households with children). These results are consistent with our hypotheses that cantonal decision-makers either internalize potential income-sorting effects at the local level or pander to the low- to intermediate-income electorate. As a result, they implement more redistributive statutory tax schedules for the less-mobile taxpayer segments, where sorting occurs but remains incomplete.

The rest of the paper is structured as follows. Section “Redistributive effects of decentralized taxation” reviews the related literature. Section “Hypothesis” states the testable hypothesis. Section “Institutional setup” provides a description of the institutional environment with particular attention to Swiss fiscal federalism and the taxation of natural persons' income. Section “Empirical strategy” presents the empirical strategy. After the description of our dataset, we discuss our identification strategy and the empirical models. Section “Results and interpretation” presents the estimation results. To illustrate our findings, we use our estimation results to calculate the counterfactual tax schedule of a centralized region if it were to become–certeris paribus–more fiscally decentralized. Section “Conclusion” concludes.

Redistributive Effects of Decentralized Taxation

Fiscal decentralization may affect how governments define the structure of the tax schedule and social transfer programs. One of the main arguments is that tax competition induces governments to try to attract higher-income groups and discourage lower-income groups that might qualify for social transfers (e.g., Moffitt 1992; Kirchgässner and Pommerehne 1996). This argument depends crucially on the mobility of the tax base. Low mobility costs provide strong incentives for tax and welfare migration, undermining redistributive spending and taxation. By and large, the theoretical literature seems to reach a certain consensus in predicting that decentralization limits the implementation of decentralized redistribution (Inman and Rubinfeld 1996).

A way to avoid such dynamics would be to limit competition and centralize the redistributive decision at higher levels of government, across which mobility costs are higher and tax and welfare migration are less likely (e.g., Musgrave 1971, 1997; Sinn 2003). In the context of income taxation, this could consist of centralizing the redistributive parameter, namely the progressivity of the income tax schedule. However, decentralization might undermine effective redistribution via progressive taxation even when the definition of a redistributive tax schedule is centralized. The underlying assumption is that fiscal decentralization induces the sorting of individuals not only by their preferences for public goods but also by income and tax burden (e.g., Ellickson 1971; Westhoff 1977; Ross and Yinger 1999; Epple and Nechyba 2004; Schmidheiny 2006a, 2006b; Schaltegger, Somogyi and Sturm 2011). Hodler and Schmidheiny (2006) investigate the effect of income sorting on the progressivity of the effective tax schedule in the highly decentralized canton of Zurich. In the Swiss setting, the definition of the tax structure is centralized at the higher-level jurisdiction (cantons), while local jurisdictions compete with each other by setting a tax multiplier on the cantonal tax schedule to finance local public goods. Hence, tax competition among local governments cannot directly affect the statutory tax schedule. However, taxpayers are mobile and can sort into different local municipalities, which are able to set different tax multipliers. Hodler and Schmidheiny (2006) describe and model a mechanism of local income sorting, which depends on the trade-off between local taxation and housing prices. They show that if the preferences of taxpayers are homogenous, income sorting is complete and the statutory tax progression is de facto neutralized. Rich households (poor households) locate in local jurisdictions with low (high) tax shifters and high (low) housing prices, which undermines redistributive income taxation. However, heterogeneous preferences make sorting incomplete, and some level of redistribution through income taxes prevails. Empirically, they show that although the flattening of the effective income tax schedule is observable, an important degree of progressivity in effective tax rates is preserved. The study uses data from the metropolitan area of Zurich, in which decentralization—and, hence, local autonomy including the authority to define an income tax multiplier—is especially high and mobility costs are low.

Hypothesis

We argue that the upper-level governments anticipate that income sorting can undermine the redistributive goal set in the statutory tax schedule. Accordingly, from a traditional normative public economics perspective, a rational and benevolent upper-level government reacts to the sorting of the tax base. It mitigates the flattening effect through income sorting by strategically adapting the statutory tax schedule to achieve its distributional objective. Or, alternatively, from a public choice perspective, policymakers could pander to low and intermediate incomes with lower tax burdens and more redistributive statutory rates for higher incomes. Sorting within the upper-level jurisdiction reduces the effective progression for high-income individuals and, thus, limits the incentives to out-migrate and the associated loss in tax revenue.

Of course, such strategies can only be successful with either heterogeneous location preferences along the income dimension or—more intuitively in our application—limited mobility of the tax base, i.e., higher mobility costs. The natural limit of such strategies is set by the mobility costs to out-migrate of the upper-level jurisdiction. In an international context, this would require to move in another country. In the context of the present study, it requires moving to another canton. Clearly, mobility costs are much higher the further away—geographically, socially, or culturally—the tax base has to migrate to avoid higher tax burdens.

We test this hypothesis with data at the Swiss cantonal and local level. The data at our disposal allow us to observe the aggregate cantonal and municipal statutory tax schedules. We observe the statutory tax burden of the total of cantonal and local income taxes by income class and household type. The available data distinguish four types of taxpayers facing different mobility costs: singles, married couples, married couples with two children, and the retired. 2

Institutional Setup

Fiscal Federalism in Switzerland

Switzerland is a federal state with a highly decentralized political structure that consists of three hierarchical government layers: The Confederation (central government), the cantons (the equivalent of U.S. states), and the municipalities (the local governments). The country counts 26 cantons and 2,294 local municipalities (in January 2016). Looking at the relative importance of each layer of government, we note that the Confederation is responsible for about 34%, the cantons together for about 43% and the municipalities together for about 23% of public expenditures and revenues (own calculation based on FFA 2015).

The cantons are responsible for all tasks which are not jointly delegated to the federal government (bottom-up), and they can independently decide to delegate some to their municipalities (top-down). If not delegated to the municipal level, cantons are, for instance, in charge of education, public security, health services, cultural matters, the implementation of the federal legislation in specific areas, etc. In the present study, we focus on the distribution of competences between cantons and their municipalities. 3 Although the degree of local autonomy varies greatly, the general institutional environment is comparable. Overall, citizens enjoy an important degree of political participation rights via instruments of direct democracy, such as voter initiatives and different forms of referenda, as well as via the direct election of local officials. 4

The cantonal and municipal autonomy over spending decisions goes hand in hand with the responsibility to raise the necessary revenues. Financial transfers from one government layer to another represent only a small part of the respective revenues of the three government layers. For instance, less than 15% of the total annual current receipts of municipalities come from transfers from other layers of government (FFA 2015).

Redistributive policies can be implemented on both the revenue and expenditure sides. On the revenue side, redistribution is mainly achieved through progressive income taxes at all three levels. However, it is by far the cantonal and the municipal levels that redistribute the most in absolute terms. 5 On the expenditure side, the three layers are typically responsible for different public goods and services; however, they also share some competencies. For instance, whereas the pension system is mainly regulated by the Confederation, cantons provide, on a voluntary basis, supplementary pensions to their poor retirees. Cantons and municipalities are jointly responsible for the provision and the financing of social assistance. However, the assignment of tasks between the cantons and their municipalities is typically well defined in legal provisions at the statutory level in each canton. Feld (2000) concludes that the Swiss redistribution system can be considered as highly decentralized.

The Swiss Tax System

All three layers of government have clearly defined sources of revenue (FTA 2017). The cantonal and municipal governments rely most heavily on revenues from the taxation of incomes of natural persons as well as profits of legal entities. The second most important source of revenue is wealth and capital taxes. About 55% of the cantons’ annual current receipts stem from direct taxes on income and wealth of natural persons as well as on profits and capital of legal entities. The annual current receipts of municipalities mainly stem from direct taxes on natural persons’ income and wealth (about 45% together) and on legal entities (about 10%). Besides these main revenue sources, cantons and municipalities can not only tax inheritances, gifts, real estate, real estate transfers, motor vehicles but also dogs, lottery, water, entertainment, and casinos. All of these tax bases are exploited to various degrees across cantons (and municipalities) and time. Additional revenue is generated through user charges and fees.

The federal government is responsible for all major consumption taxes, most importantly the value-added tax (VAT) and excise taxes such as taxes on tobacco, alcohols, mineral oils, and automobiles. As the federal government also levies the federal direct income tax, it is worth noting that all three layers of government jointly tax incomes of natural persons and profits of legal entities. Obviously, there are various other sources of revenue at the federal level, such as customs duties or pay-roll taxes to fund social security systems.

The Natural Persons’ Income tax

Our empirical analysis focuses on the cantonal and municipal taxation of natural persons' annual income. Cantons individually define three parameters of the income tax scheme. First, they define the income tax base y (within a federal framework) by setting the amount of tax allowances (or tax deductions). Formally,

The analysis of the cantonal and municipal taxation together allows taking into account the systematic substitution effect among cantonal and municipal spending and taxation due to the varying division of responsibilities between both government layers (Eichenberger 1994). The cantonal and municipal tax burden

Online Appendix OA.1 presents the average statutory income tax schedules for incomes between CHF 20,000 and CHF 1,000,000 for each canton and household type. The figures in OA.1 present the mean of the average income tax schedules for the period 1983–2010, as well as the mean and the underlying range of municipal average rates for the first (1983) and last (2010) years in our dataset. As can be seen from these figures, cantonal tax schedules differ vastly across canton, household types, and time. In most cantons, tax schedules have become more progressive over time in that the tax burden has been reduced more strongly for the low-income classes than for intermediate to high-income classes. Note, however, that the general tendency over time to reduce tax rates is primarily due to inflation adjustments. Such adjustments are necessary to avoid that inflation drives up the progressivity of the tax scheme (a phenomenon usually referred to as “cold progression”).

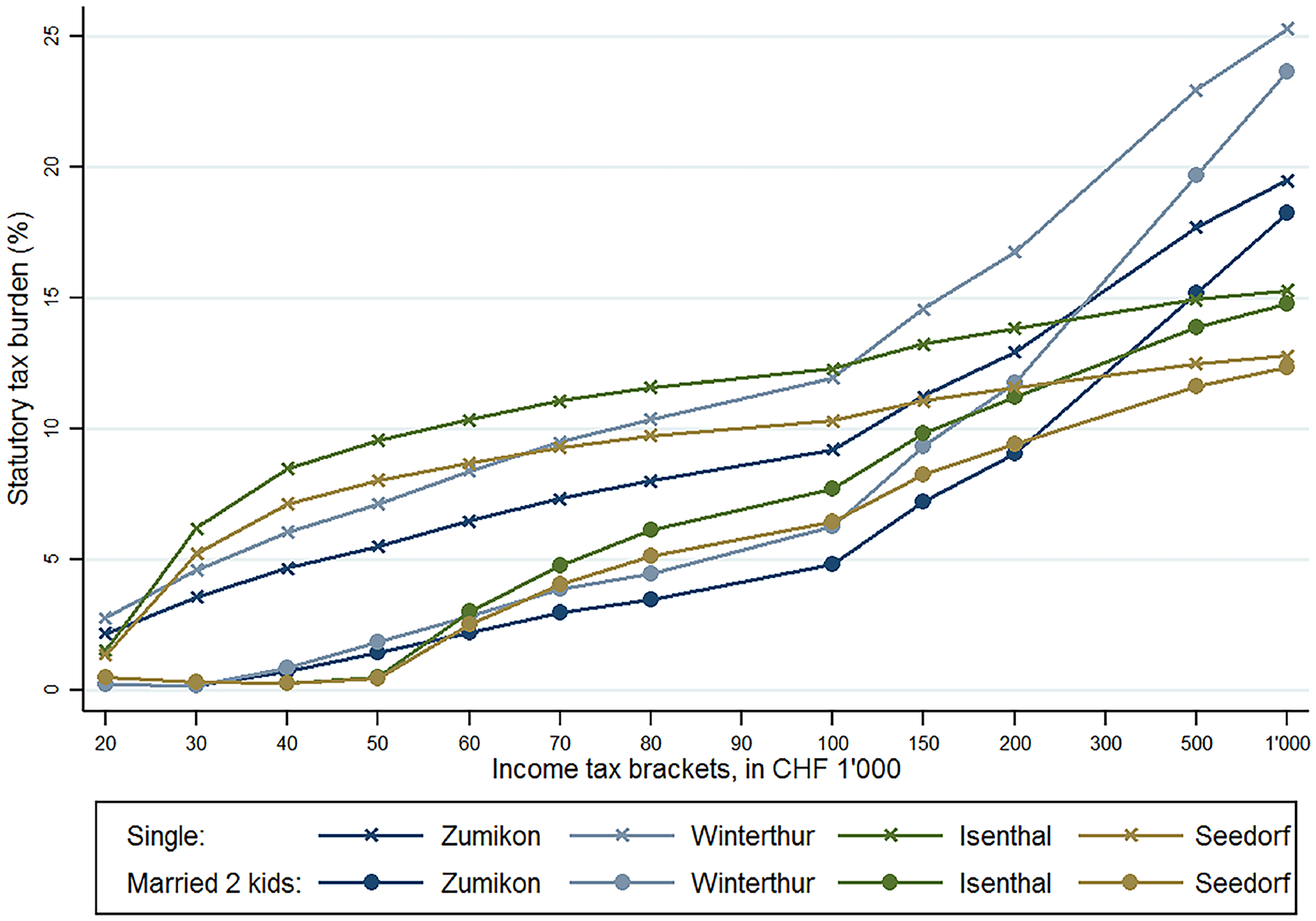

As an illustration at the municipal level of how the tax schedules vary across municipalities within cantons and how the municipal tax shifters affect taxation, Figure 1 plots the 2010 average statutory tax rate for two household types (single and married with two children) in four municipalities that belong to two different cantons. Zumikon and Winterthur belong to the canton of Zurich, where fiscal decentralization is highest. Isenthal and Seedorf (UR) are municipalities of the canton of Uri, one of the most centralized cantons. We note that different households face different tax schemes within and across cantons. Differences between household types emanate from differences in the municipal tax shifter, differences in the statutory tax schedule (i.e., single vs. married), and differences in applicable tax allowances.

Example of four tax schemes.

Empirical Strategy

Data

We build a panel dataset at the municipal level for the period 1983 to 2010. Because of the extensive decentralization in Switzerland, our database has to combine data from various sources, but it contains a wide range of economic, sociodemographic, and geographic municipal, as well as cantonal characteristics. Important covariates are further described in Subsection “Identification strategy”.

The amalgamation of municipalities over the years introduces the risk of attrition bias. In our case, Switzerland counted 3,023 municipalities in 1983 and 2,584 in 2010. We account for this problem by artificially merging the municipal data for periods prior to their amalgamation, thus simulating the universe of existing municipalities in our last period over the entire period. Dropping these observations does not change our results.

Outcome Variables: Average Statutory Tax Rates

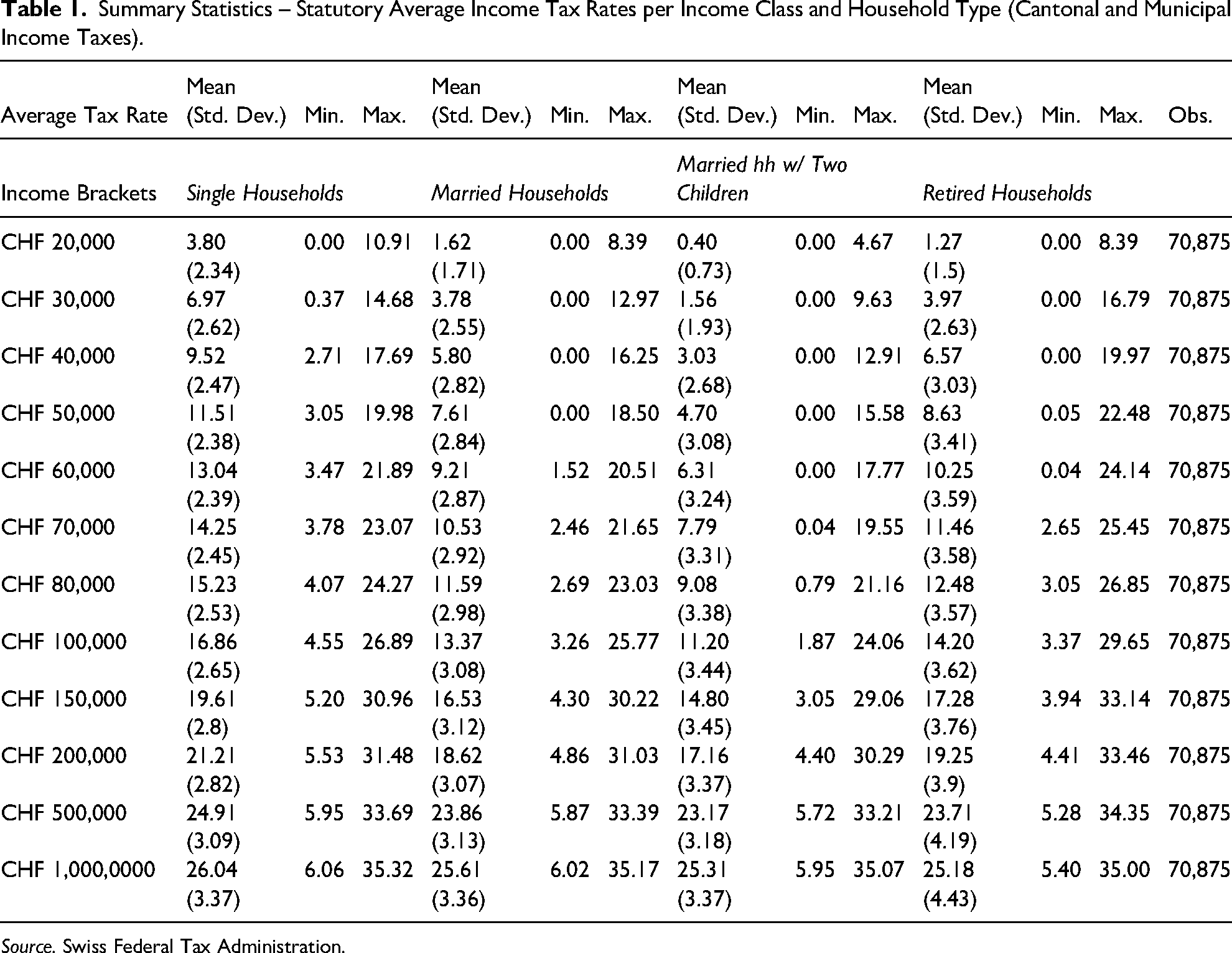

We are interested in the impact of fiscal decentralization on natural persons’ statutory tax schemes. The dependent variables used in each of our empirical specifications consist of the municipality-specific average tax rates. These tax rates correspond to the aggregated cantonal and municipal statutory tax burden relative to gross income. The tax rates are available for different income brackets going from CHF 20,000 to CHF 1,000,000 and for different household types. Table 1 provides summary statistics for each income bracket and household type. 6

Summary Statistics – Statutory Average Income Tax Rates per Income Class and Household Type (Cantonal and Municipal Income Taxes).

Source. Swiss Federal Tax Administration.

The distinction between household types allows accounting for cantonal differences in tax allowances, which affect the statutory tax progression. In addition, different household types are likely to reflect different degrees of mobility. Mobility tends to be correlated with income, household size, the number of children, or age. Households with higher incomes and younger individuals are more mobile, while larger household and those with children are less so. We speculate that single households are the most mobile, followed by married couples without children, married couples with children, and the retired. In comparison to married households, single households can optimize on average over fewer persons. Households with children must consider various additional child-specific constraints, such as childcare and schooling, which differ across cantons and increase the costs of relocation, especially across cantonal borders.

Data from the Swiss Household Panel (SHP) confirm this intuitive mobility ranking. Looking at the occurrences of relocation within the SHP between 1999 and 2014, we observe higher mobility within cantonal borders than across. The comparison of the probability of moving of each type of household shows that the category “single, no children” has the highest degree of mobility with a probability of moving (within cantonal borders) of 16.13% in a specific year. Then comes the category “married, no children” (7.22%), “married, with children” (5.48%), and “retired, married” (2.67%). The same ranking, yet with substantially lower values, is obtained when focusing only on relocations across cantonal borders.

The same data do not reveal clearcut differences in the probability of moving, depending on income. The observed probability of moving within, as well as across cantons, is relatively homogenous across income classes. One noticeable observation is that lower-income households are more likely to move within the cantonal borders, while higher-income households are more likely to move across cantonal borders.

Variable of Interest: Fiscal Decentralization

Measuring fiscal decentralization is not trivial. To proxy the degree of decentralization within the Swiss cantons, we use, like most studies, a measure taking a budgetary perspective. 7 We calculate the expenditure decentralization ratio, which is obtained by taking the municipal total expenditures divided by the total of municipal and cantonal expenditures. This provides us with an annual measure of fiscal decentralization for each canton. A score of 1 would indicate complete fiscal decentralization, whereas 0 would be equivalent to complete centralization.

Note that such a measure is often fraught with problems, as it may fall short of providing a complete picture of the degree of local autonomy (Rodden 2004; Stegarescu 2005; Wilson and Janeba 2005; or Martinez-Vazquez, Lago-Peñas and Sacchi 2017). Rodden (2004) and Martinez-Vazquez, Lago-Peñas and Sacchi (2017) point out that there are various dimensions to the question of autonomy, of which the budgetary perspective (and the resulting decentralization ratio) is just one. Following these authors, the other two are policy decentralization—that is, how and to what degree upper-level governments can override local decisions—and political decentralization—that is, how local policymakers assume office. Within Switzerland, these three dimensions are very strongly correlated. Policy autonomy comes typically with the implied budgetary responsibilities and upper-level governments cannot easily override decisions made at the local level. The allocation of tasks is spelled out explicitly in cantonal statutes. Political decentralization is guaranteed in all local governments across cantons and local decision-makers are all directly elected within the local jurisdiction.

Moreover, one of the main characteristics, in contrast to other countries, is that fiscal equivalence and institutional congruence are well established and well respected by and large. Vertical transfers make up only a minor part of local revenues, and local expenditures have to be financed in principle by local revenue sources. Intertemporal fiscal balance is strong and protected by a credible no-bailout clause. This no-bailout clause has been contested and confirmed in a case before the Federal Court in 2003.

Overall, we argue that the decentralization ratio is a good measure of decentralization in the context of the Swiss cantons. In contrast to cross-country studies, cantonal decentralization decisions are made within a rather homogenous institutional environment. Laws, rules, and measures are comparable across Switzerland. The decentralization ratio presents the obvious advantage of being easily comparable and consistent across cantons and over time. Note also that the expenditure decentralization ratio is highly correlated with alternative measures. 8

Identification Strategy

Endogeneity is obviously an important concern. It could be that cantonal governments simultaneously decide on decentralization and taxation based on some other factor or that issues related to the tax structure drive decentralization in a reverse causal direction. 9 In our specific case, in which we focus on the statutory tax burden (instead of the effective tax burden), reverse causality might be a lesser concern than simultaneity. We see at least three potentially important channels of endogeneity that have to be addressed.

First, the pressure of intercantonal tax competition might affect how cantons define the relationship with their municipalities and, ultimately, the degree of fiscal decentralization. Intercantonal competition pushes cantons to be efficient, and, depending on how cantons perceive the ability of their municipalities to provide public goods efficiently, fiscal decentralization could be more or less pronounced. The degree to which intercantonal tax competition puts pressure on cantonal governments depends on the mobility cost across cantonal borders. If the mobility of taxpayers or certain groups of taxpayers is high, intercantonal tax competition is a restriction that policymakers must consider. We argue that the mobility of taxpayers is correlated with geographical distance. The further away an individual has to relocate to avoid the reach of some cantonal tax schedule, the higher the mobility costs. Therefore, we control for the average travel time by public and private transportation from each municipality to the next municipality in a different canton. Data on bilateral municipal travel time between 1980 and 2010 were generously provided by Axhausen et al. (2015) and by the Federal Office for Spatial Development. We compute a measure corresponding to the average bilateral travel time using private transportation from one specific municipality to the nearest municipalities of the neighboring cantons. For instance, in 2010, it took an average of 50.75 min to drive from the municipality of Bulle to the nearest municipalities of the neighboring cantons (Bern, Vaud, and Neuchâtel).

Secondly, a particularly salient mechanism in the Swiss context is the instruments of direct democracy. They might be a source of endogeneity affecting the degree of fiscal decentralization, as they restrict cantonal centralization tendencies (Matsusaka 1995; Feld, Schaltegger and Schnellenbach 2008; Funk and Gathmann 2011). To account for potential endogeneity channeled through direct democracy, we include a dummy variable that equals 1 for cantons that feature a mandatory budget referendum (0 otherwise). It is a standard measure of direct democracy when fiscal policy is concerned (Feld and Matsusaka 2003; Funk and Gathmann 2011).

Third, changes in the decentralization of tasks might be masked by changes in vertical fiscal flows. Even though vertical grants only play a minor role, they could potentially affect the measurement over time. Primarily, we address this issue by including cross-section and year-fixed effects and by flexibly controlling for municipality-specific time trends (linear and quadratic). However, we also estimated empirical models controlling for vertical transfer flows between the cantons and their municipalities for the period 1990 to 2010. In all of our specifications, our covariate selection method based on LASSO never selects the vertical grants variable (see below). Qualitatively, the results do not change. As the transfer variable only becomes available starting in 1990 and in order not to lose the time periods between 1983 and 1990, we abstain from including this covariate in our empirical models presented in the results section.

The traditional solution to such endogeneity issues consists of applying instrument variable (IV) techniques. In the literature, we find previous attempts at instrumenting fiscal decentralization. For instance, Canavire-Bacarreza et al. (2017) used geographic diversity as an IV, and La Porta et al. (1999) focused on country's legal origin. Unfortunately, none of these IVs are good candidates in our case, as they are time fixed and thus absorbed by the fixed effects and because the exclusion restriction is violated for obvious reasons. Martinez-Vazquez et al. (2017) summarize the various instrumental variable approaches and conclude that none of the approaches are entirely convincing.

For these reasons, our identification is based on advanced covariate selection algorithms using modern machine learning approaches and ultimately relies on a conditional independence assumption (e.g., Wooldridge 2002). We make progress over the previous literature in that we consider a much larger number of covariates. Controlling for as many observable factors as possible reduces the risk of omitted variables bias but increases the risk of overfitting. Therefore, we resort to causal machine learning methods in which we leverage the fact that we dispose of a large number of covariates characterizing our municipalities. To avoid choosing arbitrarily between one or the other, we use the post-double-selection LASSO method (Belloni, Chernozhukov and Hansen 2014) based on the LASSO estimator (Tibshirani 1996). This machine learning method consists of a data-driven process of covariate selection. The LASSO is a variable shrinkage algorithm that selects the relevant controls among a large pool of potential covariates. 10 In the first step, the algorithm selects the covariates that best predict the outcome variable. The second step is similar but selects the best predictors of the causal variable, that is, our fiscal decentralization ratio. In the third step, we estimate the full model using the union of the selected covariates from the two previous steps in an ordinary least squares (OLS) regression.

Although the covariate selection is based on LASSO, one must pay attention to the set of potential covariates that are made available to avoid the inclusion of bad controls (Angrist and Pischke 2009). A good example of a bad control would be a measure of income inequality such as the Gini coefficient. Our theoretical mechanism implies that fiscal decentralization affects income distribution through income sorting. Hence, the Gini coefficient is itself an outcome of the causal mechanism of fiscal decentralization and should not be included in the set of available covariates.

Table OA2.1 in the Online Appendix presents the descriptive statistics of the set of potential covariates. It includes a wide range of municipal covariates, ranging from geographic information, demographic characteristics, socioeconomic covariates, and municipality-specific time trends. To account for time- as well as cross section-invariant unobserved heterogeneity, our identification relies on the within canton variation, and, thus, we chose never to penalize municipal and year-fixed effects. All estimations include robust standard errors clustered at the municipal level (Moulton 1986, 1990; Bertrand et al. 2004).

Estimated Models

To estimate the impact of fiscal decentralization on the cantonal and municipal statutory income tax schemes, we estimate a series of tax reaction functions using the cantonal decentralization ratio as our main explanatory variable. We regress the municipal and cantonal average statutory tax burden on the cantonal decentralization ratio and relevant control variables selected by post-double LASSO.

We are interested in whether or not the statutory tax schedules are adapted to compensate for potential sorting effects. Our hypothesis posits that for different levels of mobility, policymakers may choose a corresponding statutory tax scheme to counteract the distributive effects due to income sorting.

Instead of regressing on one single measure of progressivity, we take full advantage of our data and estimate the effect of fiscal decentralization on all income classes and household types individually. We run one regression for each income class (10 classes from CHF 40,000 to CHF 1,000,000)

11

and household type (single, married, married with two children, and retired-married). This presents two main advantages: Firstly, it is not trivial to define a single progressivity measure that captures adequately the shape of the tax scheme. Secondly, given that there are not only differences in marginal tax rates across income classes and household types but also differences in tax allowances and deductions, we want to use all available information and avoid smoothing over such differences. Formally, we estimate the following model for each income class c and household type h:

Results and Interpretation

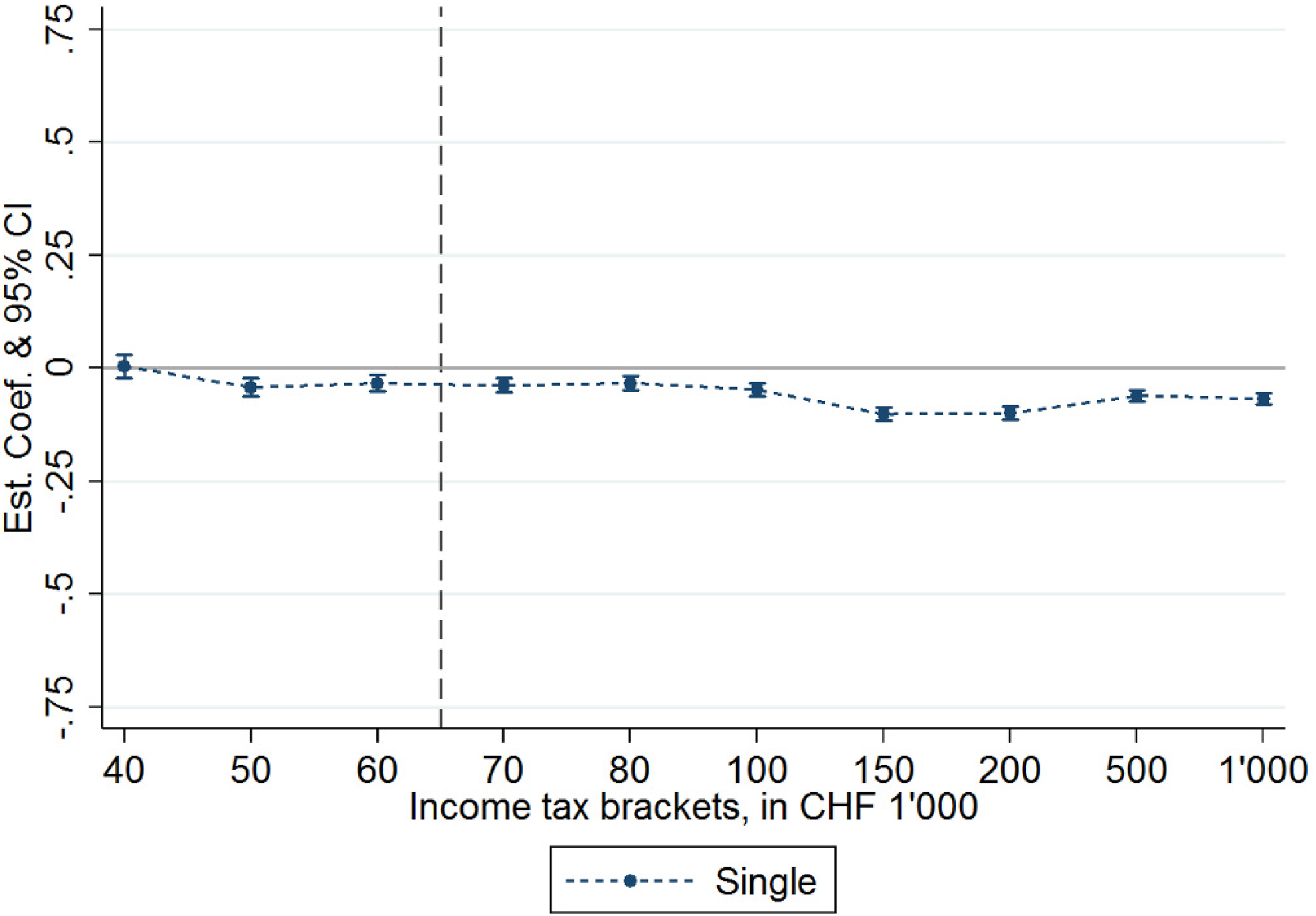

We are interested in knowing how fiscal decentralization affects the statutory tax structure. The estimated effects of fiscal decentralization on the tax rate of each income class and each household type (

The effect of fiscal decentralization on the statutory tax structure: single households.

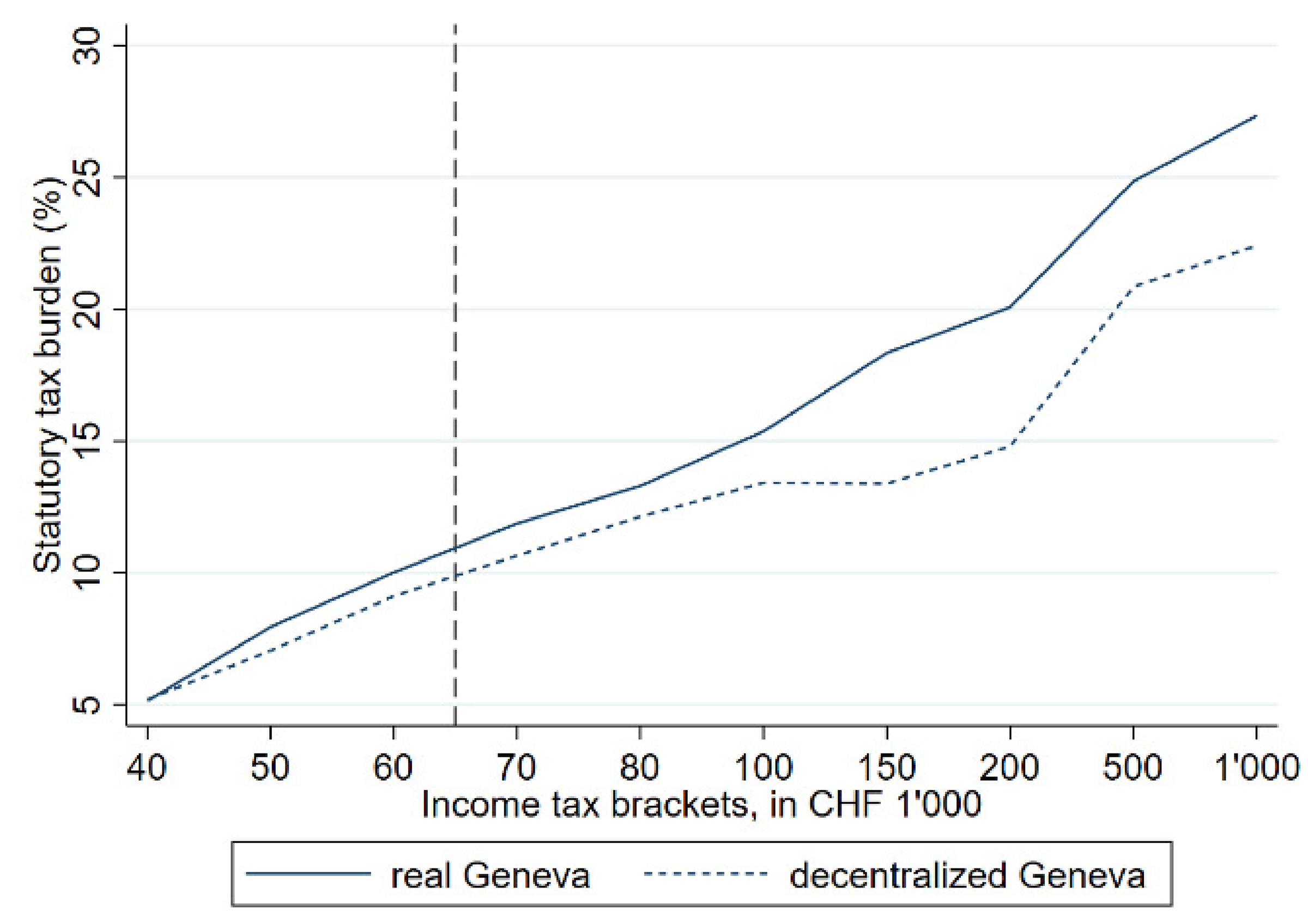

Real Geneva vs. counterfactual decentralized Geneva: single households.

The effect of fiscal decentralization on the statutory tax structure: married households, no children. (A) Decentralization and statutory tax structure. (B) Geneva vs. decentralized Geneva.

The effect of fiscal decentralization on the statutory tax structure: married households, two children. (A) Decentralization and statutory tax structure. (B) Geneva vs. decentralized Geneva.

The effect of fiscal decentralization on the statutory tax structure: retired households. (A) Decentralization and statutory tax structure. (B) Geneva vs. decentralized Geneva.

Single Households

In Figure 2 we plot the estimated coefficients and 95% confidence intervals from regressions across all income classes of the statutory average income tax rate of single households on our decentralization measure (decentralization ratio). We observe small negative and typically statistically significant effects across all income classes. The negative effects become slightly more pronounced for income classes with annual gross incomes above CHF 100,000. Beyond a general level effect, we do not observe huge differences in the tax structure for this most-mobile household type. These estimation results are well in line with the second part of our hypothesis which states that mobility costs set some natural limits to redistribute income (also) at the statutory level (in comparison with other cantons). Note that the overall negative level effect is in line with previous empirical evidence (e.g., Feld, Kirchgässner and Schaltegger 2010).

To exemplify and illustrate the overall impact of decentralization on the statutory tax scheme, we plot the actual statutory tax schedule of the relatively centralized canton of Geneva against its counterfactual tax schedule as if it were as decentralized as the canton of Zurich. While Geneva is the second-least decentralized canton in Switzerland (decentralization ratio in 2010: 0.19), Zurich is the most decentralized canton of the country (decentralization ratio in 2010: 0.50). Specifically, we use the tax schedule of the city of Geneva and calculate—ceteris paribus—the counterfactual statutory tax schedule for a decentralized city of Geneva in 2010. Obviously, this serves only as an illustration based on a back-of-the-envelope calculation with a strong ceteris paribus assumption.

According to this illustration, tax progression evolves more slowly in counterfactual decentralized Geneva for smaller incomes up to CHF 100,000 annual gross income, flattens out between CHF 100,000 and 150,000 and, then, progresses more strongly up to CHF 500,000, to flatten somewhat in comparison for incomes above that threshold. Mechanically, due to the progressive tax regime and the relatively stable effects across income classes (Figure 2), the overall differences become more pronounced as income increases.

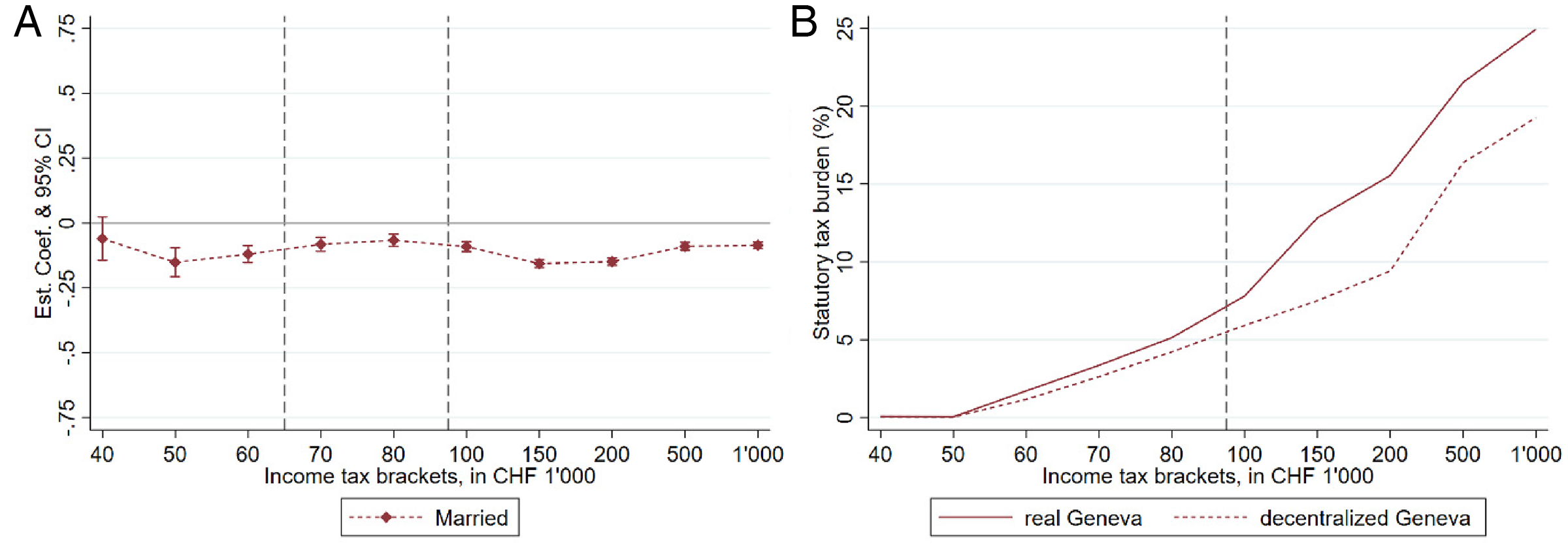

Married Households, No Children

Figure 4A illustrates that the overall dynamics of the estimated coefficients across income classes are similar but slightly more pronounced compared to single households (Figure 2). Figure 4B indicates that counterfactual decentralized Geneva would keep the tax burden lower and less progressive up to gross incomes of about CHF 200,000, at which point stronger progression kicks in up to CHF 500,000. As this household type is expected to be still fairly mobile—but less so than single households—these more pronounced patterns of delayed but then somewhat stronger progressivity up to the second highest incomes seem to be well in line with our hypothesis.

Married Households, Two Children

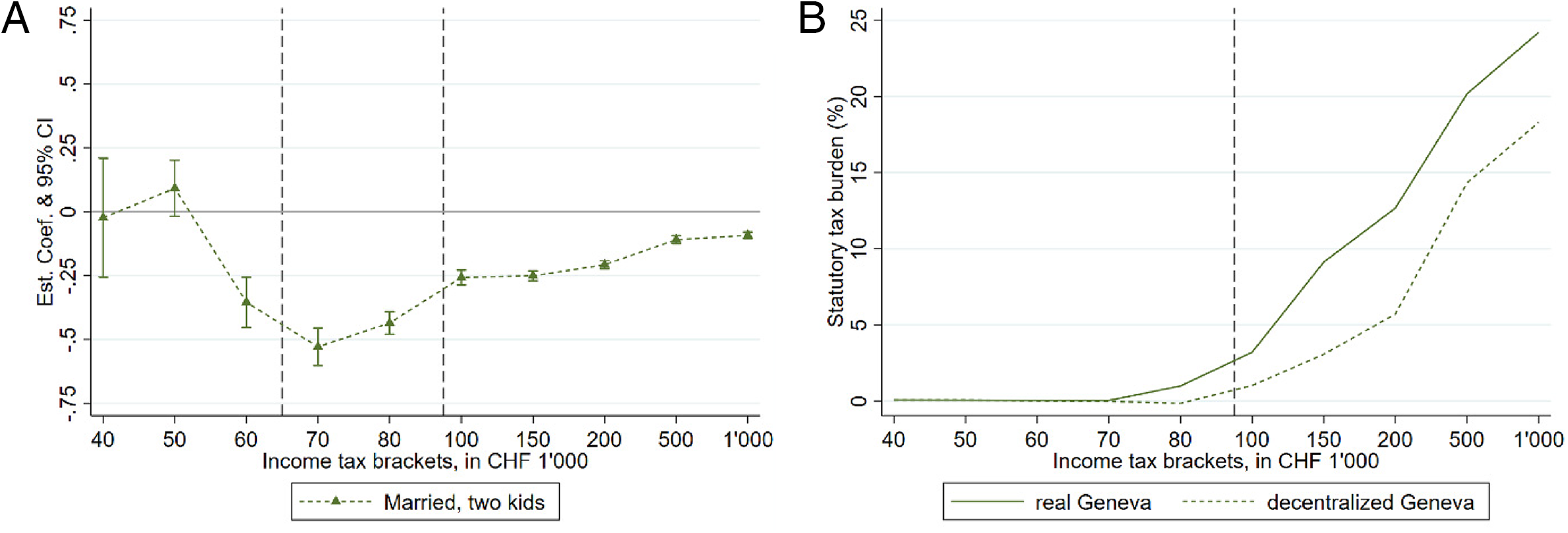

Most obvious is the relatively different evolution in the tax structure between centralized and decentralized cantons in the income classes up to CHF 100,000 gross annual income in Figure 5A. Below CHF 60,000, when the tax burden for families is close to zero in any case, decentralization does not matter much, and the estimated coefficients are insignificant and close to zero. However, there appear to be marked differences in gross incomes from CHF 60,000 onward. There are relatively large negative coefficients for incomes between CHF 60,000 and 100,000 which phase out for gross annual incomes beyond CHF 100,000. The estimated effects converge toward those for married households without children with incomes beyond CHF 200,000. The convergence of the effects concerning married households with and without children for higher-income classes reflects that the underlying statutory tax rates are the same, but child-related deductions are offered to one group only.

When focusing on the comparison of the actual and counterfactual tax schedule for Geneva (Figure 5B), we observe again that tax progression remains lower up to a gross income of CHF 200,000 in counterfactual decentralized Geneva. The larger negative effects for low-income classes observed in Figure 5B affect only very small tax rates and, mechanically, have a limited absolute effect on tax burdens in this example. Decentralization extends the extremely low-income tax burdens beyond annual incomes of CHF 70,000. Progression picks up much more slowly in comparison to actual and more centralized Geneva and only accelerates beyond CHF 200,000.

In comparison to the two previous household types of single and married households, this particular household type of married couples with two children is—according to our conjectures and suggestive evidence from the mobility patterns in the SHP—the least-mobile group and features the clearest evidence in line with our hypothesis. We observe relatively stronger effects for lower incomes, which delay the increase in tax burdens up to the intermediate to higher incomes (CHF 200,000), after which the progression increases and converges toward the previously observed difference for the other more-mobile household types. Again, the highest income classes tend to be the most mobile across cantonal borders, which might limit the extent to which differences can be sustained.

Retired Households

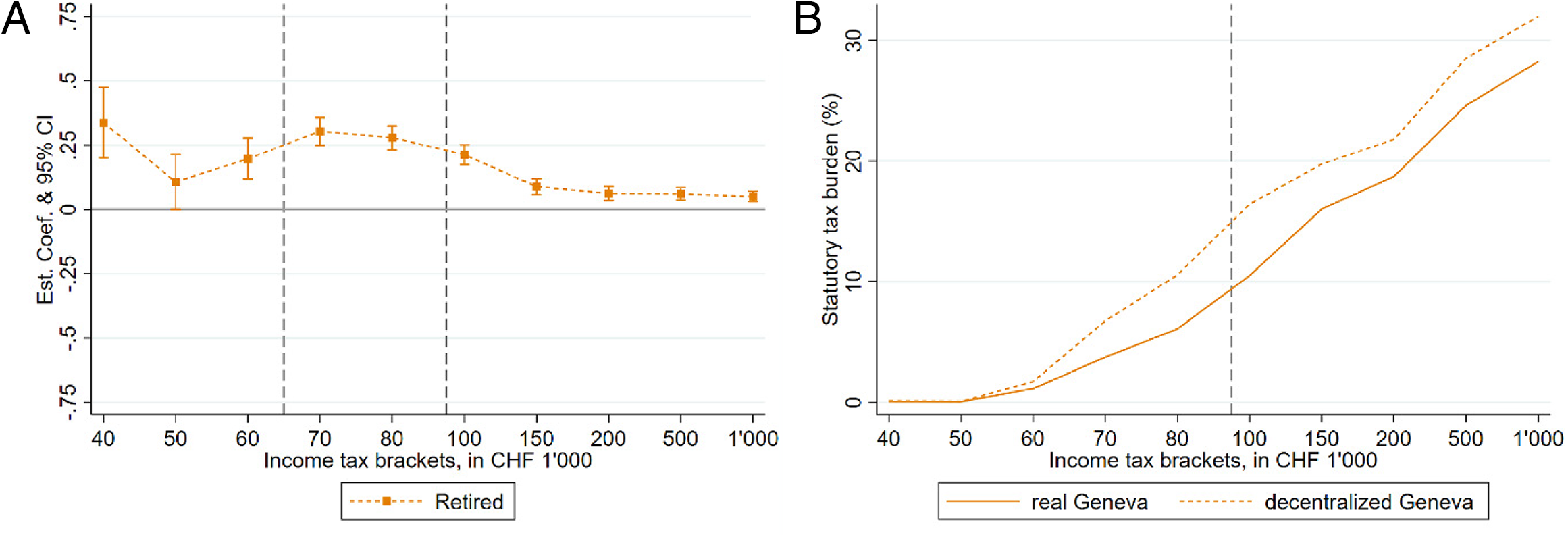

The pattern for retired households looks very different. The underlying tax schedule of this household type is based on the marginal tax rates applied to married couples. The big difference for this category is the missing deductions for job-related activities. For retired households, there are only very few deduction possibilities remaining (primarily for donations and debt service). With respect to retired households, decentralized cantons tend to define more progressive tax schedules for income classes up to CHF 100,000. Beyond that point, the differences fade out, and tax schedules become fairly similar, which could be a phenomenon driven—again—by the higher mobility of richer households.

Summary and Interpretations

There are two main takeaways. First, the estimated differences become smaller for income classes above the intermediate to a higher range of CHF 150,000 gross annual income. The relative convergence in terms of effect dynamics for the upper-income classes could be due to the relatively higher mobility of richer households across cantonal borders. 12 This would induce direct competition between cantons for these individuals and limit the potential statutory tax differences across cantons, decentralized or not. Second, the lower incomes—with the exception of retired households—are taxed more moderately and less progressively in more decentralized cantons up to intermediate to higher income levels, beyond which stronger progression kicks in. The patterns are more pronounced for the least-mobile household types. 13 More-mobile household types (e.g., single households) show fewer differences in estimated coefficients across income classes compared to less-mobile ones (e.g., married households with children). Note that most of the observed differences are driven by differences in deductions rather than marginal rates.

Our hypothesis states that more decentralized cantons adapt their statutory tax schedules to either internalize the effects of income sorting or to pander to the low- to intermediate-income electorate. Such strategies are only feasible for relatively immobile tax bases. The patterns of our results tend to be in line with such conjectures. The statutory tax schedules are similar (i.e., the estimated difference is constant) for the most-mobile household type (single) and for the highest-income groups (beyond CHF 500,000). The redistributive effects of decentralization are largest for the seemingly least-mobile household types in the lower- to intermediate-income classes.

Conclusion

The motivation for this paper comes from the theoretical ambiguity surrounding the relationship between fiscal decentralization and redistributive tax policies. The traditional literature on fiscal federalism argues that the centralization of redistributive policies allows the implementation of targeted rates of progression. However, more recent evidence shows that even in such a setup, effective redistribution might be undermined by income sorting at the local level.

We argue that rational policymakers anticipate the flattening of the effective income tax schedule through income sorting in decentralized jurisdictions and adjust the statutory tax schedule accordingly. From a normative public economics perspective, welfare-maximizing policymakers internalize the sorting effect by adapting their statutory tax schedule to achieve their distributional objectives. From a public choice perspective, policymakers realize that higher incomes can avoid higher statutory rates by sorting into jurisdictions that exploit the tax base to a lesser extent; thereby reducing the resistance against more statutory progressivity. Policymakers exploit this lower resistance and pander to the low- to intermediate-income electorate with more progressive statutory schedules for the higher incomes. Such behavior is constrained by the mobility of the tax base across upper-level jurisdictions’ borders.

We take advantage of the varying degrees of fiscal decentralization among the cantons of Switzerland. We test our conjecture by focusing on the taxation of natural persons’ incomes. Cantons define the tax schedule and municipalities levy a tax shifter. In this setup, we empirically investigate whether, and to what extent, cantonal policymakers—in charge of the definition of statutory tax structures—internalize income sorting at the local level and adapt the statutory tax schedule accordingly. We use panel data from the Swiss cantons from 1983 to 2010 and apply causal machine learning methods to estimate the impact of decentralization on the income tax burden across income classes and several household types (singles, married couples, married couples with two children, retired). These households distinguish themselves in their mobility cost and their propensity to migrate. We find evidence consistent with this interpretation: Decentralization is associated with comparatively lower tax burdens for low- to intermediate-income classes of the least-mobile household types such as married households with two children. The impact of decentralization is much less pronounced for the most-mobile household type of singles without children.

Supplemental Material

sj-pdf-1-pfr-10.1177_10911421221121029 - Supplemental material for Decentralization and Progressive Taxation

Supplemental material, sj-pdf-1-pfr-10.1177_10911421221121029 for Decentralization and Progressive Taxation by Simon Berset and Mark Schelker in Public Finance Review

Footnotes

Acknowledgments

The authors thank Raphaël Parchet as well as Kay Axhausen and his team for providing data. The authors are grateful for helpful comments and suggestions by Jim Alt, Reiner Eichenberger, Lars Feld, and Jon Fiva on an early version of this manuscript and Sonia Paty, Christoph Schaltegger, Andreas Kyriacou, Kim Hyuna, Gary Wagner (the editor), and the participants in the seminars and conferences at University of Fribourg, EPCS (Cambridge), IIPF (Lugano), SSES (Basle), Bodensee Forum, Assistentenkonferenz (Freiburg), Colloque Réseau finances publiques locales (Paris), ISNIE (Cambridge, MA) on the current version of this paper. This study has been realized using the data collected by the Swiss Household Panel, which is based at the Swiss Centre of Expertise in the Social Sciences FORS. The project is financed by the Swiss National Science Foundation.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.