Abstract

We study the implications of an increase in the price of necessities, which disproportionally hurts the poor, for optimal income taxation. When the government is utilitarian and disutility from labor supply is linear, the optimal nominal taxes and transfers are unchanged as households supply more labor to secure their consumption expenditures. Quantitative analyses with convex disutility of labor supply reveal that, because of positive labor supply effects, keeping average tax rates constant suffices to optimally react to the asymmetric price shock. The poorest agents increase their labor supply the most. Thus, optimal income tax policy in response to asymmetric price changes does not prevent the disproportional decline in the indirect utility of poorer households.

Introduction

The expenditure share of necessities usually declines in household income. Hence, the relative price of necessities asymmetrically affects households across the income distribution 1 and a price increase of necessities may require to adapt redistributive policies in an optimal income tax setting. Yet, so far, the impact of relative price changes on optimal income tax policy has remained largely unexplored.

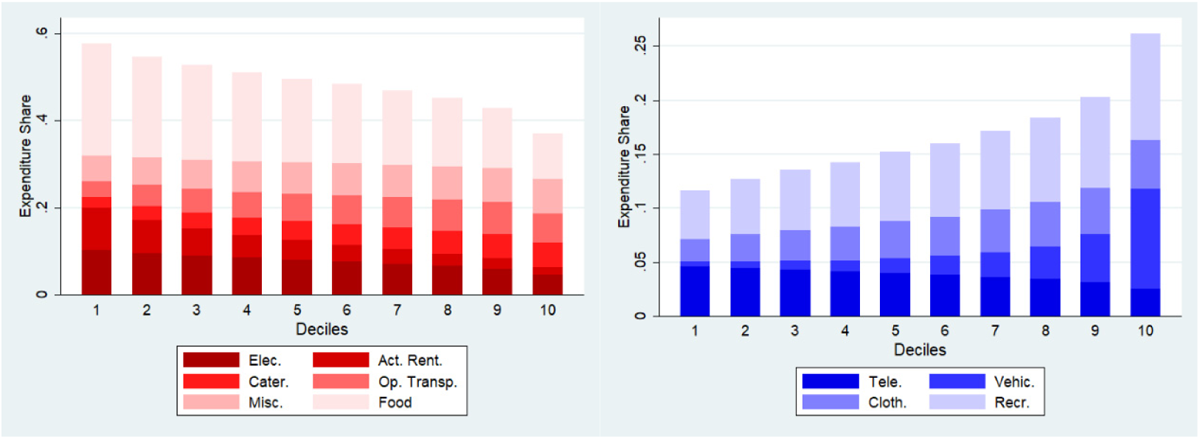

At the same time, implications of a systematic variation in expenditure shares and prices on income inequality have been widely discussed. 2 Figure 1, taken from Gürer and Weichenrieder (2020), highlights price developments in twenty five EU countries over the period of 2001–15 that had heterogeneous implications for differently affluent deciles of the population. 3 Items depicted in red (left panel) experienced a price increase above the average Consumer Price Index (CPI), whereas blue items (right panel) had a price increase below the CPI. The darker red (blue) the item, the higher (lower) the price increase has been. Items that can qualify as necessities, such as “Actual Rentals of Housing,” “Electricity, gas and other fuels,” and “Food,” constitute a significantly higher fraction of the total budget for the lower deciles and have been exposed to an above-average price increase. We label this phenomenon “pro-rich inflation.”

Pro-rich inflation in Europe. Notes: Based on unweighted averages across 25 EU countries between 2001 and 2015. Elec.: electricity, gas and other fuels.; Act. Rent.: actual rentals of housing; Cater.: catering services; Op. Transp.: operation of personal transport and equipment; Misc.: miscellaneous goods and services; Tele.: telephone and telefax services and equipment; Vehic.: purchase of vehicles; Cloth.: clothing; Recr.: recreation and culture. Source: Gürer and Weichenrieder (2020).

This study explores the implications of pro-rich inflation for optimal income tax policy. We use a model in which subsistence levels and therefore expenditure shares differ across rich and poor households. First, we derive the comparative statics of a basic model with a linear disutility of labor. Our analytical results show that an increase in the price of necessities increases households’ labor supply such that the price increase on the subsistence consumption can be covered out of the additional market income. Given our assumption of homogenous preferences and identical prices for households, the additional gross income requirement is the same for all households irrespective of their position in the income distribution. Price increases that fall on items with higher expenditure shares for the poor particularly harm low ability households because they must work more hours for the same additional income.

In a next step, we use the price data for twelve consumption goods for the period 1996–2017 and calibrate our model to three European countries that empirically have been affected differently by pro-rich inflation: Germany, the United Kingdom and the Czech Republic. Unlike in our first part, this calibration allows for nonlinear disutility of labor. Our results show that the optimal government response is to increase net nominal taxation. Average taxes, on the other hand, hardly respond to asymmetric price changes. Given that taxes had been optimal before the relative price changes, the mere additional net nominal taxes (subsidies) on the rich (poor) that arise due to the increasing labor supplies (and gross incomes) suffice to respond optimally to the price changes. Still, poorer households increase their labor supply more and lose a higher percentage of their total indirect utility.

The literature on optimal income taxation as initiated by Mirrlees (1971) includes only very few contributions that consider the implications of introducing subsistence levels of consumption. Unlike our study, the existing literature primarily focuses on the heterogeneity of this subsistence level across individuals. Rowe and Woolley (1999) provide an example with four agents. Kaplow (2008) considers heterogeneity in many dimensions as well as subsistence levels. Judd et al. (2018) simulate optimal income tax schedules with households that differ with respect to up to five characteristics, including basic needs (subsistence levels).

Another feature of our paper is the attention on the prices of consumption goods. Again, the literature on this is sparse, but some examples exist. Albouy (2009) considers the implication of regional price levels on optimal income taxation. Kushnir and Zurbrickas (2019) build a general equilibrium model and discuss housing prices for the optimal income tax schedule. Kessing, Lipatov and Zoubek (2020) study productivity enhancing taxation with regions that vary in productivity and hence in the price of labor.

The next section introduces the features of the general framework used throughout the paper. Section “Analytical Results When Disutility of Labor is Linear” derives comparative statics over a basic version of the model. Section “Exemplary Model Simulations” calibrates the model to three European countries and presents the results. Finally, section “Discussion and Conclusion” concludes.

The Model

Consider an optimal income tax model with multiple consumption goods. There are discrete sets of agents and goods, indexed by

Individual preferences are homogeneous and separable between consumption goods and labor supply. Hence, the uniform commodity taxation theorem of Atkinson and Stiglitz (1976) holds 4 and optimal income taxation is sufficient to redistribute income. Differentiated consumption taxes are ignored.

An agent's budget constraint reads:

The government maximizes a utilitarian social welfare function W by assigning

It is intuitive to consider two separate stages. First, agents supply labor and earn gross income. Simultaneously, the government chooses an optimal nonlinear income tax schedule. Payment of the taxes determines the net incomes of individuals. In the second stage, agents decide on the amount of expenditure for each good.

To solve the model, we proceed backwards. Considering net incomes as given, we maximize the sub-utility of consumption (first term in (1)) with respect to the budget constraint (2). This yields good demands as functions of

In principle, a change of consumption prices might go along with wage changes for ability types. The following abstracts from this. A wage invariance may result if, for example, price changes derive from a foreign sourced input, say energy, leading to income increases abroad rather than in the country under consideration. Another justification is that optimal redistribution as a function of the wage structure is well understood in the literature and the policy discussion in many countries seems to monitor wage developments carefully. The same cannot be claimed for income dependent inflation effects.

Analytical Results When Disutility of Labor is Linear

To build intuition, this section derives comparative statics for a simple version of the above model. In the spirit of Stiglitz (1982), there are high and low productivity agents in the economy, that is,

Agent i 's utility function reads:

As mentioned, the solution starts with the second stage where households maximize the utility from consumption given the budget constraint

See Appendix section “Proof of Proposition 1” for the proof.

According to (i), the net tax (subsidy) on high (low) type in response to pro-rich inflation stays constant. (ii) clarifies the reason: agents compensate the price increase by working more. Both high and low type agents increase their labor supply to secure their subsistence consumption expenditure: this corresponds to an increase in net incomes of

Our results do not mean that pro-rich inflation is beneficial for the rich. Indeed, they face the same pressure (

Note that the optimal reaction of redistribution to a price increase of necessities is different from the reaction that derives from a wage change. One might be tempted to presume that as a price increase on necessities disproportionally hits the low ability type, it is similar in effect to a reduction in the real wage and the productivity of this type. The policy reaction is different, though, as an exogenous reduction of the real wage of the poor indeed would lead to a change in optimal policy. The reason is that a reduced productivity of the low ability type reduces the cost of distorting the labor supply of the poor. Hence, a further distortion becomes optimal to ease the self-selection constraint of the high ability type. The marginal tax rate of the low ability type increases and the absolute tax paid by high ability types goes up as well. In the above model, these effects are absent. Intuitively, the price increase may reduce the consumption value of a euro of redistribution, but does not affect the relative productivities.

Proposition 1 characterizes an extreme case in which the government does not change nominal redistribution. This is a result of a linear disutility of labor. When the disutility on total welfare is linear, the government is not concerned about the asymmetric changes in the labor supply behavior. What is the extent of governmental compensation in response to pro-rich inflation when disutility of labor is assumed to be convex? How would the resulting indirect utilities of different agents change? The next section offers quantitative evidence from simulation exercises to answer these questions.

Exemplary Model Simulations

This section simulates the model presented in section “The Model” for Germany, the United Kingdom, and the Czech Republic using 1996 and 2017 prices. According to Gürer and Weichenrieder (2020, Figure 6), pro-rich inflation was low to mid-range in Germany, mid to high range in the United Kingdom, and relatively high in the Czech Republic.

Our calibrations use the EU Household Budget Surveys (HBSs) of 2010 and the Harmonized Index of Consumer Prices (HICP) for the period 1996–2017. 9 Appendix section “Description of the Datasets” describes these datasets. Our analysis keeps everything constant, including wages and wage structure, and concentrates on price variations. Our results may be viewed as a worked-out example, based on real-world expenditure structures and price developments. Therefore, it is more realistic than the highly stylized model of the previous section.

Using the cross-section of the EU HBSs, we construct agents with different income levels in the three countries based on expenditure shares observed in 2010. Following this, we separately calibrate the model with the prices of 1996 and 2017.

Calibration

In the simulations, we use four agents (set

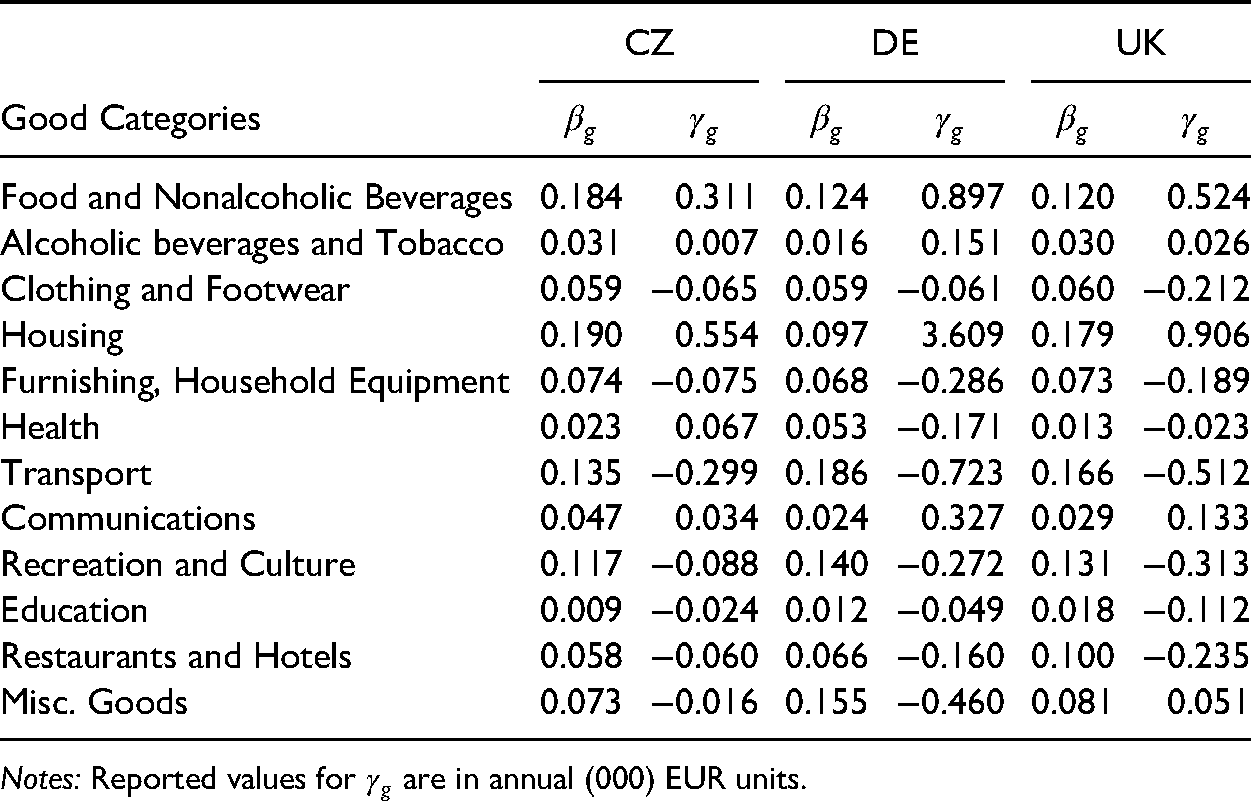

Results of the Parameter Estimation.

Notes: Reported values for

The utility function is specified as follows:

Using household data, we perform a linear expenditure system estimation for each of the three countries to recover marginal budget shares (

Table 1 presents the results of the estimations. Note that categories which can be naively classified as necessities such as “Food and Non-alcoholic Beverages” and “Housing” have higher subsistence parameters compared to the rest of the goods. These high subsistence levels are needed for expenditure shares that are declining in income levels. For some goods, there are negative subsistence levels. Pollak (1971) notes the possibility of obtaining negative values as a result of LES estimation. He mentions that interpreting

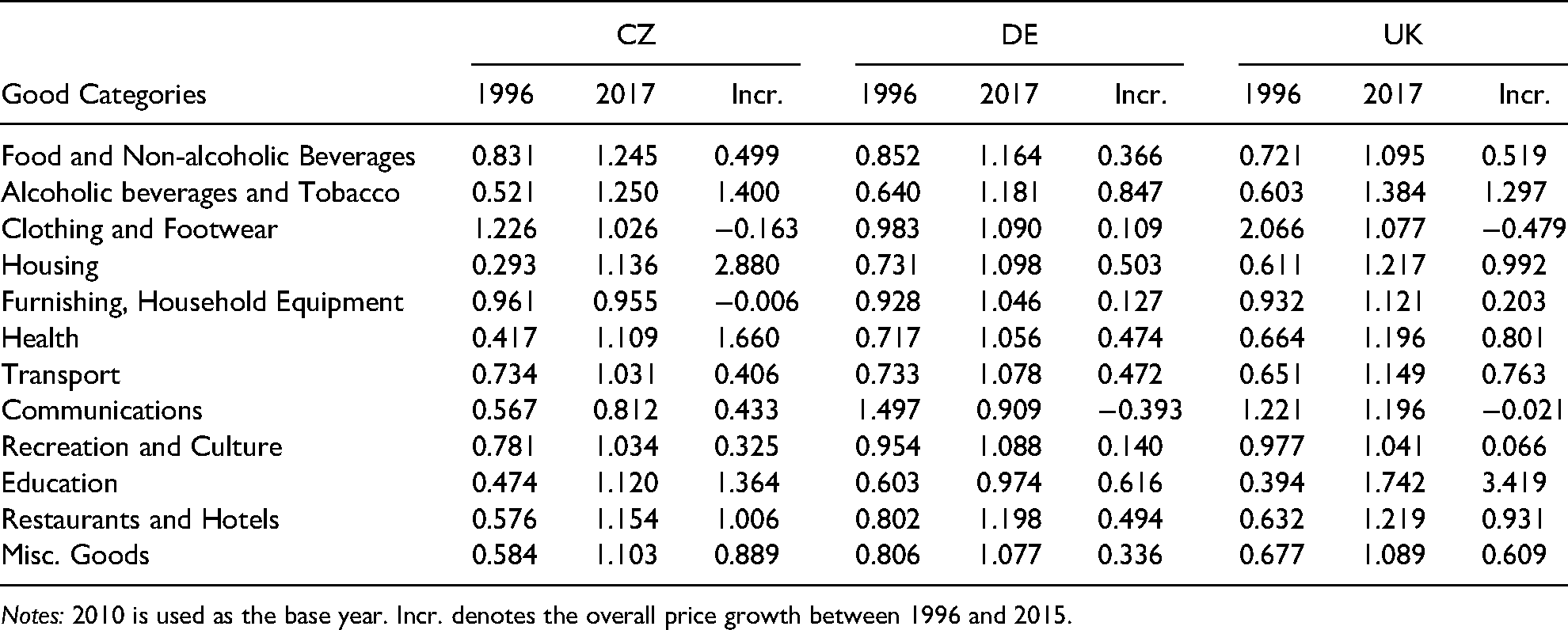

Simulations require price observations for each of the 12 categories in three countries in 1996 and 2017. Table 2 provides the prices (using 2010 as the base year) and their corresponding rates of increase over the period of interest.

Prices in 1996 and 2017.

Notes: 2010 is used as the base year. Incr. denotes the overall price growth between 1996 and 2015.

In our main specification, we set the Frisch elasticity of labor supply (

Next, we determine wage rates for four agents in each country. A common approach in the literature directly feeds the simulations with the empirically observed wage rate distributions. With this method, the net incomes that would be implied by the model are, ex ante, unknown. However, the estimation of

Another benefit of this approach is that, as mentioned in Saez (2001), once the assumptions regarding utility parameters change, implied wage rates change as well. This is particularly helpful for our purposes because, as robustness checks, we change our assumptions regarding the subsistence parameters and the labor supply elasticity.

Agents’ first-order condition with respect to labor supply reads (see Appendix section “Derivation of the Agents’ First Order Condition for the Generalized Utility Function”):

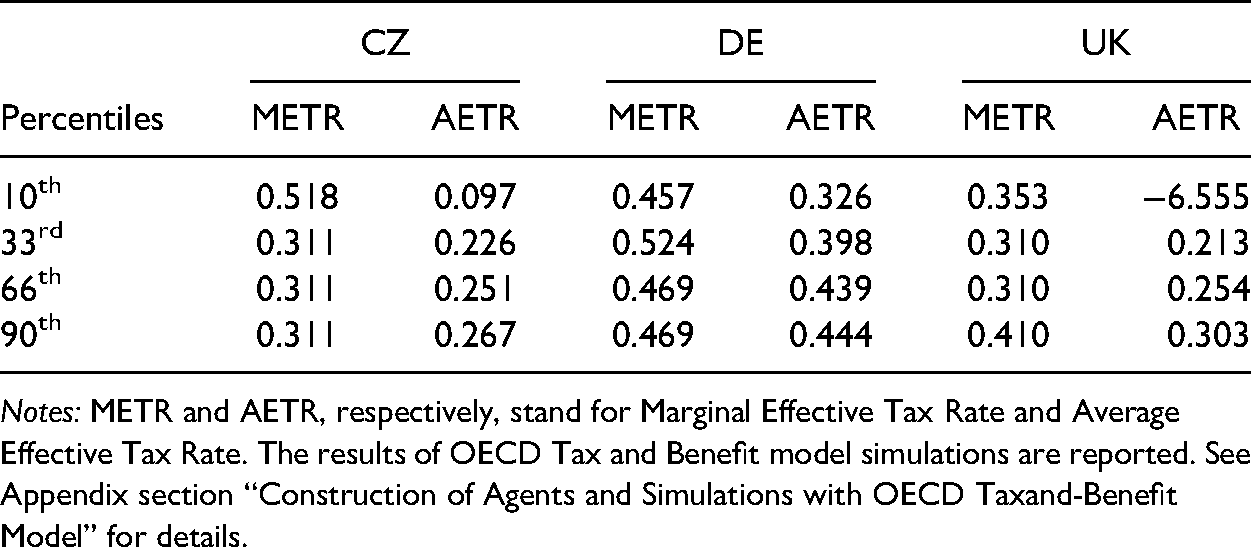

Actual Tax Schedules in 2010.

Notes: METR and AETR, respectively, stand for Marginal Effective Tax Rate and Average Effective Tax Rate. The results of OECD Tax and Benefit model simulations are reported. See Appendix section “Construction of Agents and Simulations with OECD Taxand-Benefit Model” for details.

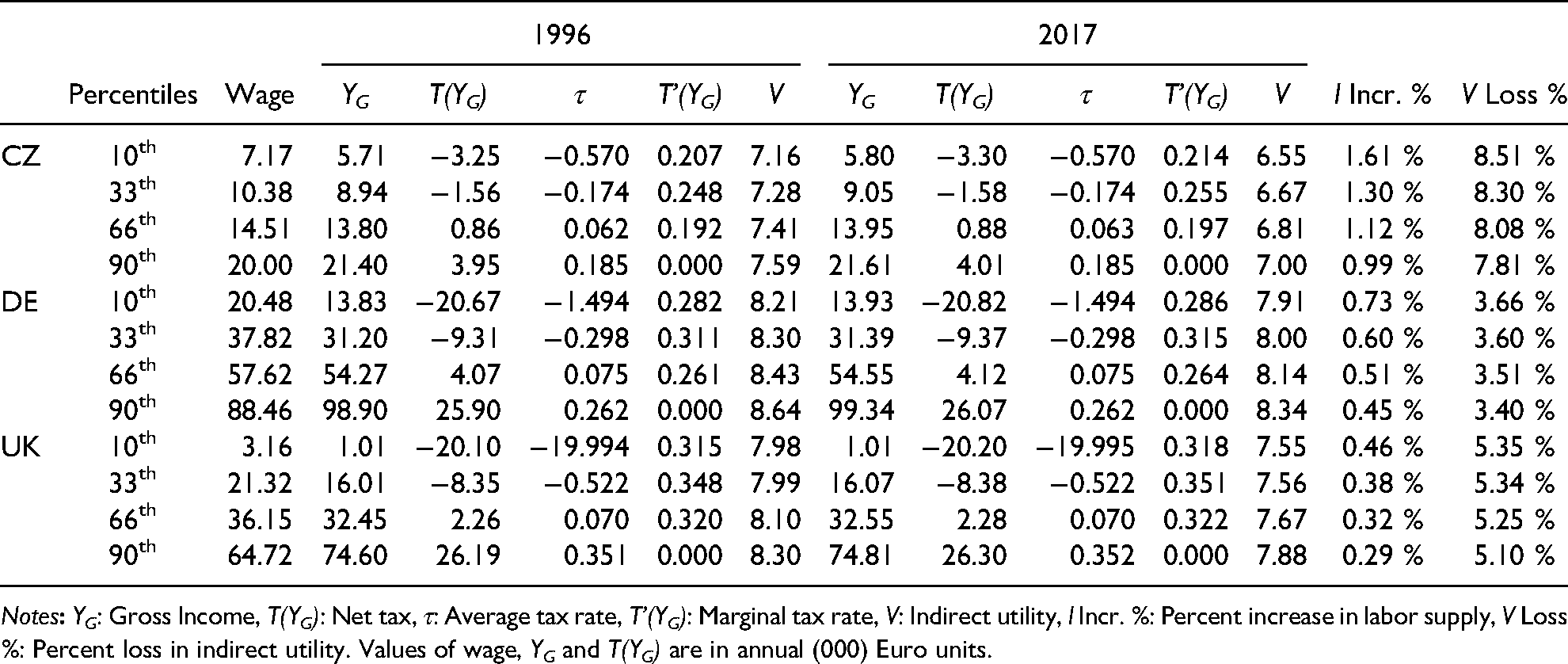

Optimal Policies for 1996 and 2017 Prices.

Notes

Results

We now compute the optimal policies for 1996 and 2017 prices. The first and second panels of table 4 present the optimal policies in 1996 and 2017 for each country.

Table 4 presents the optimal policies before (1996) and after (2017) asymmetric price changes for the four agents in three countries. A comparison of the two panels reveals that, after asymmetric price changes, net nominal taxes (subsidies),

Judging by the increased labor supply behavior of, for example, the 10th percentiles, we can infer that the increased net nominal subsidies do not fully insure poorer households against price increases. Note that labor supply responses are still asymmetric. Agents with lower ability increase their supply more in response to price increases. Moreover, the indirect utility of low ability agents declines disproportionately. Hence, even an optimal redesign of the income tax schedule leaves poorer households disproportionally harmed.

Our model does not take into account changes in wage rates. While these rates are held constant in the model, they certainly have changed during the period 1996–2017. Recent trends in income inequality suggest that wage dispersion has increased over time in most countries. In addition, labor market reactions may trigger endogenous wage changes, if the need to work more (following an increase in necessity prices) faces a less than perfectly elastic labor demand.

Pro-rich inflation implies higher price increases for items with high subsistence levels (such as food and housing). This increases the additional market income requirement. This said, it should be noted that it is difficult to make cross-country comparisons with regards to pro-rich inflation. This is because any result, for example, the magnitudes of declines in indirect utilities, depends on three characteristics of a country: agents’ preferences (

Discussion and Conclusion

This study investigates the implications of an above average increase in the price of necessity goods (labelled as pro-rich inflation) on the design of tax policies.

Assuming a utilitarian government and linear disutility of labor, tax policies are not affected by asymmetric increases in the labor supply across households. In this simplified case, our comparative statics suggest that each agent increases its labor supply such that he or she can secure the subsistence consumption expenditure. Since the households in a given country are assumed to have the same price changes and preferences, the additional net income required is identical for each agent. The increase in labor supply particularly hurts the indirect utility of low ability agents because they must increase their labor supply more compared to the others in order to provide the same additional income. At the same time, a utilitarian government does not intervene when the disutility of labor is linear and is thus indifferent to who bears this utility cost.

Next, using the EU Household Budget Surveys and Harmonized Index of Consumer Prices, we numerically study the effect of an exogenous increase in prices on tax policies for three European countries (Germany, the United Kingdom, and the Czech Republic) while allowing a convex disutility of labor. In this setting, pro-rich inflation increases net nominal taxes on the rich. At the same time, the average tax rates remain almost unchanged irrespective of the country of interest. Hence, increased gross incomes arising from increased labor supply largely suffice to provide the optimal response to asymmetric price changes when average taxes are kept constant. However, the optimal policy does not fully compensate poorer households. As in the highly stylized model of section “Analytical Results When Disutility of Labor Is Linear,” the poorest agents are the ones who must increase their labor supply the most. As a result, the optimal response of the government in income taxation does not suffice to prevent poorer households from being disproportionally hurt by such price increases.

It is worthwhile to highlight possible limitations of our analysis. One assumption is that worktime can be chosen individually. Conversely, a more active tax policy may be required in inflexible labor markets, in which individual changes in hours worked are difficult. While our Mirrleesian framework assumes that wages are private information, some contributions have argued that not only gross incomes but also wage rates are observable by the government. If this is true, the government can design wage rate specific lump-sum taxes/transfers and restrict distortions to the intensity of labor supply, which should provide for a reduced equity-efficiency trade-off. Relatedly, as in almost all Mirrleesian studies, we assume that the labor supply elasticity is homogeneous across the distribution to avoid double screening. A further simplification that we use is that tax distortions apply to the intensive margin only. Usually, adding the extensive margin via a fixed cost of taking up a job leads to some downward shift in marginal tax rates, but we expect no significant change of the message from introducing the extensive margin in our setting.

Price increases may also feed into higher profits and income, which is not discussed in this study. Gürer (2021) shows that higher prices, if triggered by higher markups, justify greater corporate taxes and lower income taxes. At the same time, Gürer (2021) abstract from asymmetric price changes, which is the main contribution of this study.

Our analysis has excluded further, potentially interesting aspects. What are the market mechanisms that generate pro-rich inflation? How important would it be to allow for endogenously changing wage rates in a general equilibrium framework? Investigating these issues may be fruitful for future work in this field.

Footnotes

Acknowledgments

We thank Eurostat for granting access to the microdata on European Household Budget Surveys and Harmonized Index of Consumer Prices data and participants of 2019 ZEW Public Finance Conference for providing valuable comments. None of the conclusions of this paper may be attributed to Eurostat, the European Commission, or to any of the national statistical authorities whose data have been used.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.