Abstract

Based on more than 7,000 shareholder proposals, this article argues that firms targeted by environmental, social, and governance (ESG)–related proposals subsequently improve their ESG performance. We reach the same conclusion in the climate change context. Surprisingly, we find no evidence that withdrawn proposals are more or less impactful than proposals that were omitted or those that were brought to a vote. This result suggests that the filing of the proposal itself has an agenda-setting effect. Yet, we find evidence that the more shareholder proposals a firm receives, the stronger the effect on ESG performance. By submitting proposals, shareholders signal what matters for them and this, in turn, may shape a firm’s strategy.

Introduction

Within management research, the role of shareholders on corporate outcomes and performance has received significant attention (e.g., Desender & Epure, 2021; Flammer et al., 2021; Johnson & Greening, 1999; Kochhar & David, 1996). Shareholders can try to induce a change in business conduct through a broad spectrum of activities, such as divesting (i.e., selling their shares), engaging in negotiations with management, or submitting shareholder proposals (McCahery et al., 2016). Yet, the extant literature on the effects of shareholder activism has mainly focused on corporate governance (e.g., Ertimur et al., 2010; Gillan & Starks, 2000) and financial implications (e.g., Becht et al., 2009; Flammer, 2015). Today, the requests and interests of shareholders frequently go beyond those aspects and incorporate issues from the environmental or social domains (Dikolli et al., 2022; Margaret et al., 2023).

In recent years, shareholder activism on environmental, social, and governance (ESG) issues has gained momentum (Dimson et al., 2015). For example, the percentage of ESG-related proposals of all proposals listed in the Institutional Shareholder Services (ISS) database increased from 29% in 2006 to 53% in 2020. Prior research on the effects of shareholder activism on target firms’ environmental and social performance leaves room for further investigations. Lee and Lounsbury (2011) show that environmental shareholder resolutions have a positive impact on corporate pollution practices—opening up research avenues for generalizing these findings to other ecological domains and social aspects. David et al. (2007) observe a negative effect of shareholder resolutions on corporate social performance (CSP). This rather counterintuitive finding is based on a Kinder, Lyndeberg, and Domini (KLD) rating score that combines strengths and weaknesses—a procedure that has been criticized as inappropriate (Mattingly & Berman, 2006). Furthermore, Flammer et al. (2021) and Reid and Toffel (2009) find that shareholder proposals can elicit greater disclosure of climate information, but the authors do not analyze the effects on the release of carbon emissions themselves. Thus, we ask if shareholder proposals in general can serve as an effective instrument that may lead companies to change their sustainability strategy. To answer this question, we examine the effect of ESG- and carbon-related shareholder proposals on different measures of firms’ ESG and carbon performance. Moreover, to identify possible determinants of the effects of shareholder proposals, we analyze whether the type of proposal sponsor (i.e., an investor focused on socially responsible investing (SRI) or a non-SRI investor), the proposal status (i.e., withdrawn, omitted, or final vote), or the number of proposals received influences firms’ performance.

We combine propensity score matching (PSM) with a difference-in-differences approach. This setting allows us to determine a differential effect in the ESG and carbon performance of target firms and matched nontarget firms, attributable to (not) receiving a respective shareholder proposal. Using the ISS database for U.S. firms, our baseline sample consists of 7,448 ESG- and carbon-related proposals submitted between 2006 and 2020. The dependent variables are different measures of ESG performance, including Refinitiv’s overall ESG Score and individual E, S, and G Pillar Scores, as well as different measures of carbon performance, including an Emissions Score, total carbon emissions, and carbon emission intensity. While the ESG and carbon performance is similar for target firms and matched nontarget firms in the year before the annual shareholders’ meeting takes place, after receiving a proposal, target firms improve their ESG performance on average by 8% and decrease their carbon intensity on average by 11% compared with nontarget firms in subsequent years. Interestingly, the positive effect of carbon-related proposals is limited to carbon emission intensity while total carbon emissions are unaffected. Furthermore, we find that the effects are more pronounced for proposals that are filed by investors that have no explicit sustainability agenda. As an important outcome, we find no evidence that the proposal status (i.e., withdrawn, omitted, or final vote) has a significant effect, yet we find that the number of prior proposals received has a significant effect.

Our findings contribute to the literature on shareholder activism and complement recent evidence on the growing influence of shareholder proposals in the ESG context (Flammer et al., 2021). Our results provide robust evidence that firms targeted by ESG-related shareholder proposals subsequently improve their ESG performance. Similarly, carbon-related proposals have a positive, albeit limited, effect on firms’ carbon performance. Interestingly, we find no evidence that withdrawn proposals are more or less impactful than proposals that were omitted or those that were brought to a vote. This result suggests that the procedural outcome of a proposal may be less important than its submission in driving change. While surprising, this finding can be explained by the nonbinding nature of most shareholder proposals, which limits their direct influence, but underscores their role in shaping managerial priorities. The act of filing itself signals dissatisfaction and raises awareness among stakeholders, compelling management to respond strategically. While procedural differences exist between these categories of proposals, their shared ability to set agendas remains central to understanding their impact. Furthermore, our study contributes to the growing body of literature on impact investing (Kölbel et al., 2020), which examines the extent to which investor activities can influence changes in corporate activities. Our results indicate that shareholder proposals are a promising approach for investors to induce improvements in firms’ ESG and carbon performance, but that the magnitude of the effect is driven by the proposal sponsor and the number of proposals filed. Proposals filed by less norm-constrained investors appear to have the largest effect regardless of whether the proposal is withdrawn, omitted, or brought to vote.

The results also have practical implications for both managers as well as capital market participants. We show that a shareholder proposal can be a sufficient instrument to influence the ESG and carbon performance of firms. As such, an early incorporation of issues raised in such a proposal and according adjustment of corporate strategy may be an important risk mitigation strategy. For investors a key question is whether investments in public equities can generate any impact at all. Our findings show that in fact investors can encourage firms to make improvements in ESG and carbon performance through shareholder proposals.

Background and Related Literature

Disapproval of the business conduct of an investee firm can prompt shareholders to raise concerns, whereby they can voice their opinions in different ways. Investors may (threaten to) sell their holdings, that is, divest (e.g., Admati & Pfleiderer, 2009; Rohleder et al., 2022). Alternately, they can privately engage with the firm’s management through meetings and discussions (e.g., Becht et al., 2009; Dimson et al., 2015) or they can express their opinions publicly by filing shareholder proposals.

Submitting a proposal and voting at general assemblies are essential rights given to shareholders. These are key mechanisms for investors to provide oversight of managerial behavior and communicate their views on how firms should be run (Prevost et al., 2016). Shareholder proposals pertain to a wide range of matters such as executive compensation or anti-takeover amendments (Dikolli et al., 2022). Over the years, shareholder activism on ESG issues has become increasingly prevalent (Dimson et al., 2015).

However, research shows that the majority of shareholders tend to vote against shareholder sponsored resolutions and, ultimately, only a few proposals pass (Li et al., 2021). In contrast to management-sponsored proposals, the resolutions of votes on shareholder sponsored proposals are nonbinding in the United States. Even if a proposal receives majority support from shareholders, the firm’s board can make its own determination of whether to adopt the proposal or not (Cuñat et al., 2012). As such, one might expect management to pay little attention to the demands of shareholders filing and supporting proposals (Flammer et al., 2021). Nevertheless, since the early 2000s, firms have taken the votes on shareholder proposals more and more seriously (Ertimur et al., 2010).

In the context of shareholder activism, one strand of literature examines the effect of shareholder activism on firms’ corporate governance performance, policies, and structures. Studies indicate that shareholder proposals can be impactful and induce management to adjust business practices to be in line with the aims of the proposals (Cuñat et al., 2012; Flammer, 2015). Specifically, prior research has shown that shareholder proposals on common corporate governance issues are a driver of governance change (Ertimur et al., 2011; Ertimur et al., 2010). Aggarwal et al. (2019) find that directors who receive low shareholder support in elections are more likely to leave the board within 1 year. Other studies indicate that shareholder proposals related to CEO compensation (“Say on Pay”) are followed by changes in the amount of CEO pay (Denis et al., 2020; Ferri & Sandino, 2009).

Another strand of literature investigates the effects of shareholder activism in an ESG context. Chen et al. (2020) indicate that institutional ownership drives firms’ environmental and social performance and that shareholder proposals are one possible channel for institutional investors to achieve this. In addition, Neubaum and Zahra (2006) reveal that shareholder activism is a significant moderator of the institutional ownership–CSP relationship. Flammer et al. (2021) and Reid and Toffel (2009) show that environment-related shareholder proposals increase firms’ voluntary disclosure of climate change risks. Moreover, they find that environmental shareholder activism is most effective if it is initiated by institutional investors (e.g., mutual funds or public pension funds). He et al. (2023) study mutual fund voting behavior on environment-related and social-related proposals. They show that the level of mutual fund support is informative about negative environmental and social incidents in the following one to 3 years. As such, the results indicate that mutual funds have information about firms’ environmental and social risks. Surprisingly, David et al. (2007) find a negative relationship between shareholder proposals and subsequent CSP using KLD ratings. This counterintuitive result may also be explained by the use of an aggregated KLD rating score, which is derived by summing all strengths and subtracting all weaknesses of a firm’s social action. Such a composite measure is viewed critically as it does not provide a reliable picture of a company’s actual CSP (Mattingly & Berman, 2006). Moreover, the data are rather old—they were collected in the 1990s—and ever since then shareholder activism on environmental and social issues has become more established (Goranova & Ryan, 2014). Using a similar time window as David et al. (2007), Lee and Lounsbury (2011) examine the influence of SRI investors on corporate pollution management practices. They find that environment-related shareholder resolutions filed by SRI investors increase the benzene internalization rate of target firms. While these are important contributions, there is room for further research to investigate the general effect of shareholder proposals across different investor groups on firms’ ESG and carbon performance in an empirical setting using more recent data.

Theory and Hypotheses Development

The submission of a shareholder proposal signals dissatisfaction with a corporation (David et al., 2001). In the context of shareholder activism, research suggests that shareholder proposals may have a signaling effect, where investors try to convey messages to firms (Back & Colombo, 2022). Investors exert pressure through shareholder activism to convey their opinions and expectations, thereby demanding managerial actions or corporate change (Flammer et al., 2021; Levit & Malenko, 2011; Shackleton et al., 2021). To alleviate the pressure put on firms through the spotlight of shareholder activism, corporate leaders may reevaluate and adjust business practices to avoid proxy fights, which might remove the current board from its position (Del Guercio & Hawkins, 1999). Indeed, prior research shows that firms are responsive to shareholder proposals and that they can influence corporate outcomes (Goranova & Ryan, 2014). Moreover, some ESG aspects can be financially material, which might be an additional motivation for management to react on ESG-related proposals. Hence, we expect firms to respond to these types of resolutions and demonstrate appropriate actions for their shareholders. Thus, we formulate the following hypothesis:

In the financial community there is growing recognition of the costs associated with climate change. Hence, many investors incorporate climate risks into their decision-making (Flammer et al., 2021; Krueger et al., 2020). It is, therefore, not surprising that shareholders file proposals pressuring investee firms to decrease carbon emissions. Rohleder et al. (2022) find that portfolio decarbonization contributes to the reduction of divested firms’ carbon emissions. Similarly, we presume that shareholder proposals, as another form of shareholder activism, may also change target firms’ carbon performance. Therefore, the second hypothesis is framed as follows:

Shareholders can differ considerably with regard to their investment styles and preferences (Barberis & Shleifer, 2003). These differences are likely to have an impact on portfolio choices and the interactions with portfolio firms. Hence, this raises the question of whether the sponsor type has an influence on the effectiveness of shareholder proposals.

SRI funds are expected to meet certain norms or ethical values that are in line with their investment styles. As can be seen in Panel B of Figure 1, these SRI preferences are also reflected in a high proportion of submitted proposals pertaining to ESG issues. In contrast, when non-SRI investors file a shareholder proposal, they are less likely to be driven by such norms or ethical values. Instead, it can be expected that they are more likely to raise certain ESG-related issues due to the conviction that these issues are of financial relevance. As such, ESG-related shareholder proposals filed by non-SRI investors could be perceived by management as more important from a financial point of view—and therefore more relevant as a whole. Thus, we formulate our third hypothesis:

Sample Composition.

Most shareholder proposals are precatory, that is, they recommend an action by the firm, but implementation is not mandatory. As such, the outcome of a vote is not binding. In addition, it is important to note that a large proportion of shareholder proposals do not even result in a shareholder vote because they are either withdrawn by the sponsor or omitted by the SEC (see Panel C of Figure 1). An omitted proposal has been actively challenged by the target firm for exclusion from the proxy materials. Under Act 14a-8 of the Securities Exchange Act, there are several reasons that justify an exclusion, such as matters dealing with the firm’s ordinary business operations or proposals that are regarded as improper. In each case, exclusion requests are reviewed by the US Securities and Exchange Commission (SEC) and must be sufficiently reasoned. Reputational concerns may be a key driver for firms seeking the omission of shareholder proposals. A proposal that is excluded will not appear in the proxy materials distributed to shareholders prior to the annual shareholders’ meeting. Therefore, firms may have an interest in ensuring that critical proposals regarding ESG issues are not made public. In contrast, withdrawn proposals signal some level of agreement or compromise between the sponsor and the target firm. Hence, prior studies suggest that withdrawals indicate successful negotiations (Bauer et al., 2021; Bauer et al., 2015). For this reason, we formulate our fourth hypothesis:

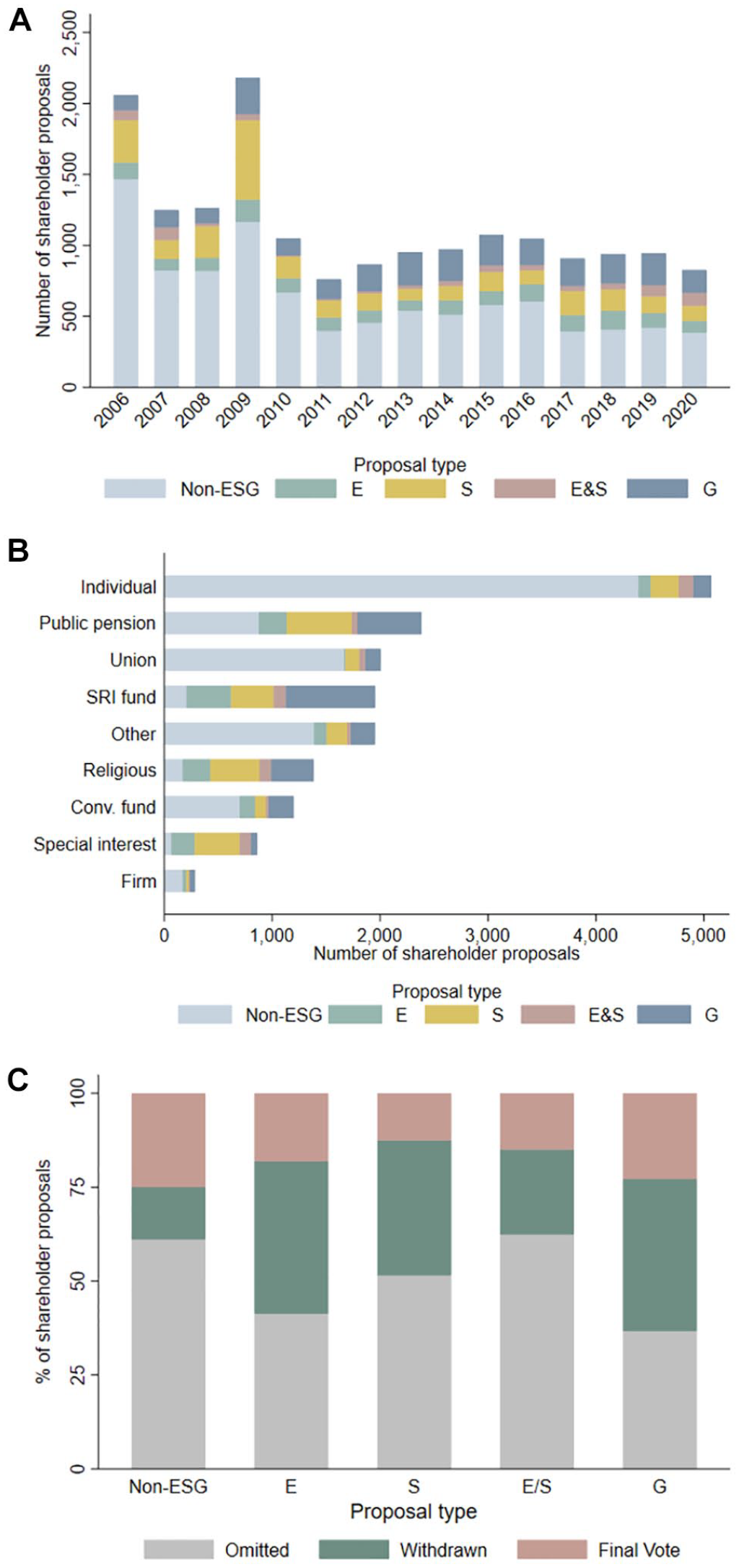

Over the years, the same firm usually receives multiple shareholder proposals. The data in Panel A of Figure 1 show that, on average, firms receive 4.3 ESG-related shareholder proposals over a 15-year period. However, some firms receive up to 150 ESG-related shareholder proposals. Consequently, the signal strength from shareholder proposals could vary with the cumulative effect of prior proposals a firm has received. The repeated exposure to such signals may enhance their impact, as the more present a signal is to the signal recipient, the stronger its effect may be (Gulati & Higgins, 2003). Therefore, we formulate our fifth hypothesis:

Data and Methodology

Sample

For our analyses, we collect data from different sources. Our primary data source is the ISS database. Over the period from 2006 to 2020, we obtain shareholder proposals for firms headquartered in the United States that are part of the S&P 1500 or the Russell 3000 index. Panel A of Figure 1 shows the initial sample of 17,090 shareholder proposals pertaining to 1,714 unique U.S. firms. For each resolution, ISS reports the meeting date that the proposal was voted on, a description of the proposal issue, 1 as well as the type of the person, firm, or organization sponsoring the proposal. In our analyses, we focus on the subset of shareholder proposals related to ESG and carbon issues, which comprises 7,448 resolutions pertaining to 1,068 firms. On average, 44% of the proposals address ESG issues. Among these, 398 shareholder proposals specifically targeted carbon emissions. In the first step, we focus on the first shareholder proposal a firm receives, that is, we exclude any subsequent proposals, as they may affect firms differently. In the next step, we consider the number of proposals filed in subsequent years to analyze the effect of multiple proposals.

Panel B of Figure 1 shows the number of total proposals and the proportion of ESG-related proposals by sponsor type. Over our sampling period, a large share (46%) of non ESG-related proposals are submitted by individuals, whereas SRI funds 2 mostly sponsor proposals related to ESG issues (23%). Non-SRI funds sponsor almost equal amounts of ESG-related (7%) and non-ESG-related (7%) proposals. Furthermore, Panel C of Figure 1 shows that 25% of non-ESG-related shareholder proposals are brought to vote, 14% are withdrawn and 61% are omitted—for ESG-related proposals, it is 22%, 23%, and 55%, respectively.

We use Refinitiv (formerly Thomson Reuters) as our source for financial, ESG, and carbon data. The Refinitiv database provides financial data for more than 100,000 publicly traded firms. Furthermore, Refinitiv processes publicly available sources, such as firm websites and annual and corporate social responsibility (CSR) reports, to compile more than 500 ESG metrics for approximately 11,000 firms, with time series data going back to 2002.

We also draw on Refinitiv’s industry classification system, which sorts firms into 33 business sectors. Using the International Securities Identification Number (ISIN) for each firm, we then combine the financial and ESG data from Refinitiv with the shareholder proposal information from the ISS database.

Matching

An empirical challenge in studying the effects of shareholder proposals on firms is that the submission of shareholder proposals is not random. Ideally, we would address this endogeneity concern by using an instrumental variable approach. However, we are not aware of such instrumental variables for the submissions of shareholder proposals. Instead, we use a matching approach to build a counterfactual of how firms’ ESG and carbon performance would have evolved if they had not received a respective shareholder proposal. Matching can alleviate concerns regarding selection bias, ensuring that treatment and control samples are as similar as possible before the treatment (Dehejia & Wahba, 1999). Therefore, we match our sample of firms that received a proposal (i.e., treated firms) to a group of firms that were not targeted by shareholders (i.e., control firms) by PSM.

For each treated firm, we apply PSM for the end-of-year firm characteristics (i.e., matching variables) from the year prior to the annual shareholders’ meeting for which a proposal was submitted. For potential control firms, we consider all publicly listed U.S. firms. We perform a one-to-one matching, which means that we assign one control to every treated firm, based on the nearest neighbor method. Matching is conducted without replacement, that is, a control firm can only be assigned to one treated firm in each year. However, the same control firm can be matched with different treated firms across years.

We include matching variables that are known to have an influence on the possibility to receive the treatment, as well as the dependent variable (firms’ ESG and carbon performance). Drempetic et al. (2020) and Shackleton et al. (2021) show that firm size is associated with higher ESG Scores. Thus, we consider total revenue (Log Revenue) and total assets (Log Assets) given in natural logarithms as measures of firm size. We include a measure for financial risk, calculated as firms’ Debt-Equity-Ratio. Hong and Kacperczyk (2009) find that firms with lower ESG performance have higher leverage ratios. For our analysis of shareholder proposals related to carbon emissions, we add property, plant, and equipment (PPE) as a matching variable. The PPE Intensity, measured as the ratio of PPE to total assets, indicates the extent to which a firm relies on physical assets in its business activities. A high PPE intensity is typically associated with more carbon emissions compared with a firm that requires less PPE in its production processes (Trinks et al., 2020). We also include the respective firms’ ESG and carbon performance measures in the matching process. The reasoning behind this inclusion is that firms that already have high ESG ratings or carbon performances are less likely to achieve further improvements. Furthermore, it is likely that investors would submit ESG- or carbon-related proposals specifically to firms with low ESG or carbon performances, which would introduce a selection bias in our sample. Finally, we require exact matches on the calendar year and within industry sectors, following Refinitiv’s industry classification system, to control for year and industry characteristics.

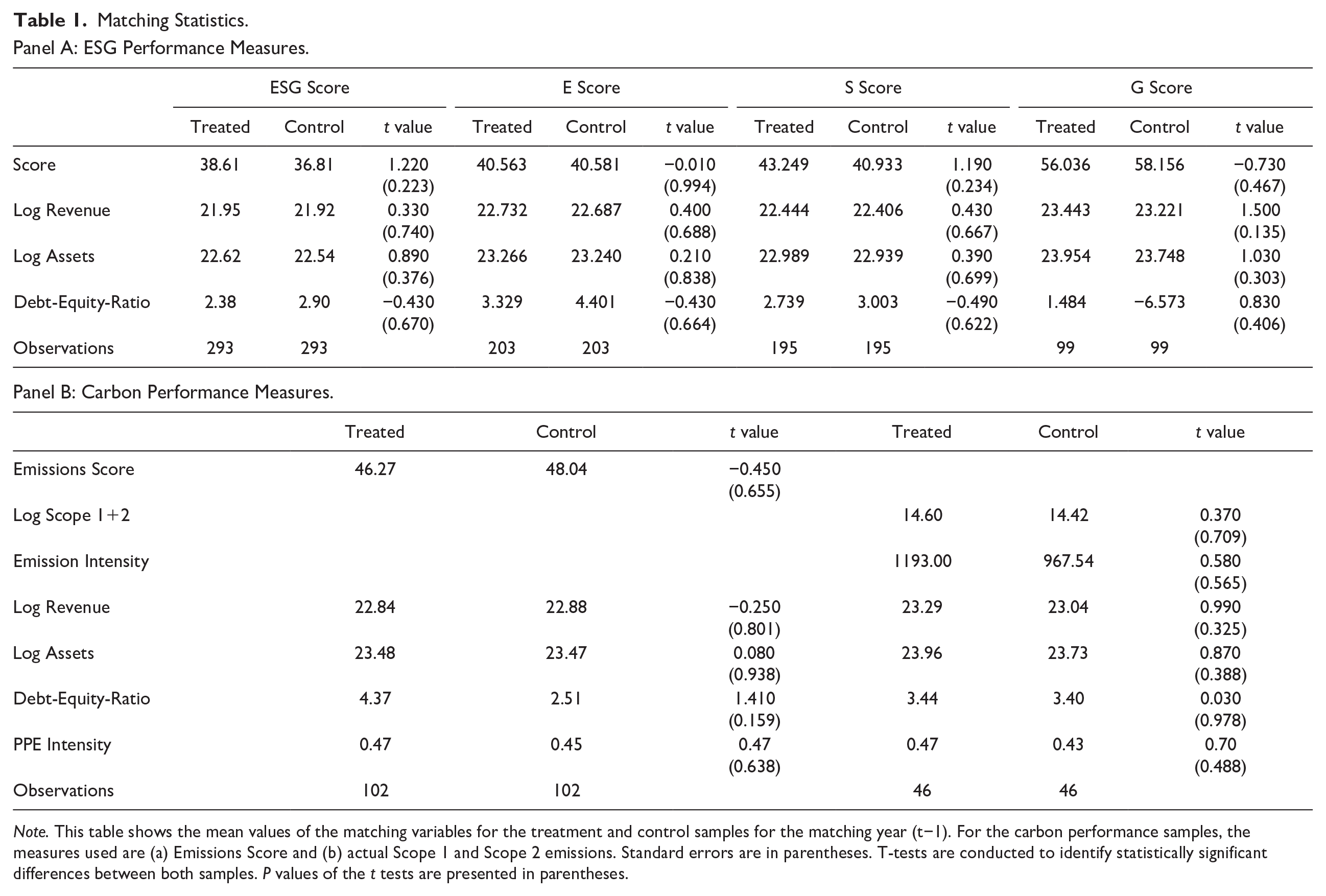

Table 1 contains the mean values of the matching variables for the treatment and control samples for the matching year (t−1). All differences are statistically insignificant. This indicates that the matching is successful.

Matching Statistics.

Panel A: ESG Performance Measures.

Note. This table shows the mean values of the matching variables for the treatment and control samples for the matching year (t−1). For the carbon performance samples, the measures used are (a) Emissions Score and (b) actual Scope 1 and Scope 2 emissions. Standard errors are in parentheses. T-tests are conducted to identify statistically significant differences between both samples. P values of the t tests are presented in parentheses.

We conduct an alternative matching approach to check the robustness of our results. Our decision to match on current levels of ESG and carbon performance could potentially neglect the trend of previous years. Therefore, we also match firms on the changes in ESG and carbon performance by summing up annual changes over the last 3 years prior to the proposal. This approach leads to similar results, allowing us to assume that our main analyses are not biased by the time path of ESG and carbon performance.

Variables

Our dependent variables are different measures of ESG performance provided by Refinitiv, including the Environmental Pillar Score (including themes such as resource use and environmental product innovation), the Social Pillar Score (including themes such as workforce, human rights, community, and product responsibility), the Governance Pillar Score (including themes such as management, shareholders, and CSR strategy), and the overall ESG Score (an aggregation of the individual E, S, and G Scores). 3 All scores are percentile rank scores, which range between 0 and 100. As a measure of carbon performance, we use the Emissions Score, 4 which tracks a firm’s commitment to and effectiveness in achieving environmental emission reductions. We also include direct and indirect carbon emissions as a dependent variable. Specifically, we focus on carbon emissions from sources that are owned or controlled by a firm (Scope 1) as well as emissions associated with the purchase of electricity, steam, heating, and cooling consumed by the firm (Scope 2). These are operationalized as total carbon emissions and carbon emission intensity. Total emissions are measured as the natural logarithm of a firm’s combined Scope 1 and Scope 2 carbon emissions (Log Scope 1+2). Taking the natural logarithm allows for better comparison between firms, since, for example, firms with high emissions can also reduce their emissions more in absolute terms. Scope 1+2 Intensity is calculated as total Scope 1 and Scope 2 carbon emissions (in metric tons) divided by a firm’s total revenue (in million U.S. dollars). This captures a firm’s efforts to reduce carbon emissions in its operations and energy consumption, while controlling for changes to the amount of its operations (Busch, Bassen, et al., 2022).

To estimate the effect of shareholder proposals on firms, we use a dummy variable Treat that equals 1 for firms that received a shareholder proposal and 0 for control firms. We create another dummy variable Post, which takes the value of 0 for years before the treatment and the value of 1 starting with the treatment year. For each firm in the treatment group, we define the treatment year as the year in which the annual shareholders’ meeting took place when the shareholder proposal was submitted. The interaction of Treat with Post allows us to measure the difference in the ESG and carbon performance between treated and control firms after the treatment. In addition, to control for other factors influencing firms’ ESG and carbon performance, we include the matching variables as control variables in our difference-in-differences approach.

Difference-in-Differences Model

To determine the differential effect of shareholder proposals on firms’ ESG and carbon performance, we estimate specifications of the following baseline difference-in-differences model in a panel structure:

where ESG is a measure for the ESG or carbon performance of firm i in year t. Post identifies the pre-treatment and treatment period, Treat indicates whether a firm received a shareholder proposal, and Post × Treat is the interaction term of interest. X’ contains firm-level control variables that might affect the ESG and carbon performance of firms, including Log Revenue, Log Assets, Debt-Equity-Ratio, and PPE Intensity. Firm-fixed effects (α) control for unobserved time-invariant firm characteristics. In other specifications of our baseline model, we also include year-fixed effects and industry-year-fixed effects that control for industry-specific unobserved effects in each year. ε is the error term. We calculate firm-clustered standard errors.

In the first specifications of our model, we analyze all ESG-related shareholder proposals on the aggregate ESG Score. In the following specifications, we explore environment-related (social-related or governance-related) proposals on the E Score (S Score, or G Score). We include up to 5 years before the treatment and up to 10 years after the treatment in our sample. The reason for the unbalanced time window and long post-treatment period is that sustainability efforts may require time (e.g., switching production operations) to translate into rating score or emission-level changes. Depending on the respective model specification, our panel datasets range from roughly 500 to more than 4,000 firm-year observations.

Results

Descriptive Statistics

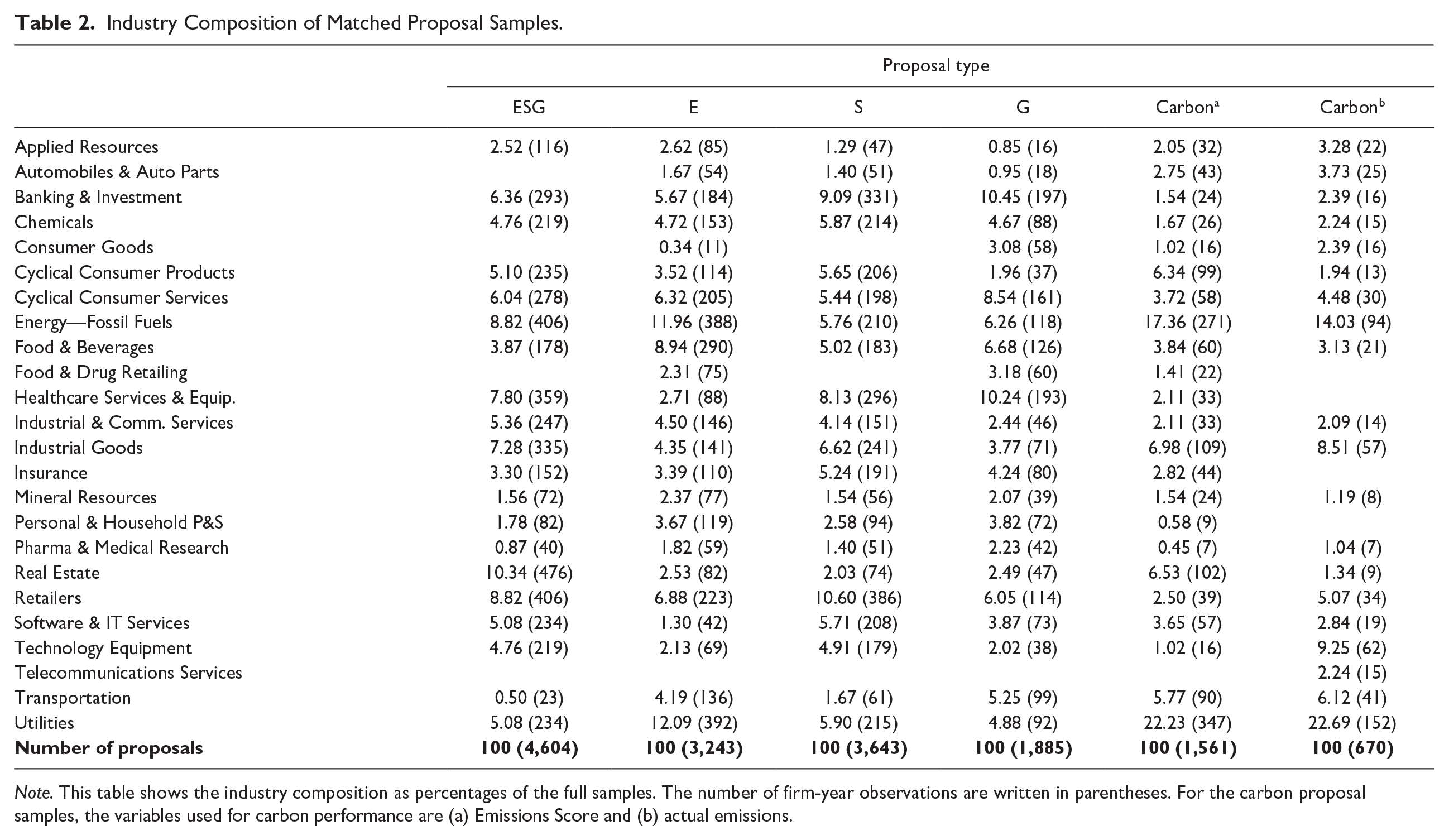

Table 2 highlights the industry composition of our sample. Depending on the variables for ESG and carbon performance and the type of proposal, the models include between 20 and 23 different industries. The samples on environment- and carbon-related proposals mainly include energy and utility firms. For social proposals, we find an increased share of retailers, while financial institutions are frequently included in the sample for governance-related proposals.

Industry Composition of Matched Proposal Samples.

Note. This table shows the industry composition as percentages of the full samples. The number of firm-year observations are written in parentheses. For the carbon proposal samples, the variables used for carbon performance are (a) Emissions Score and (b) actual emissions.

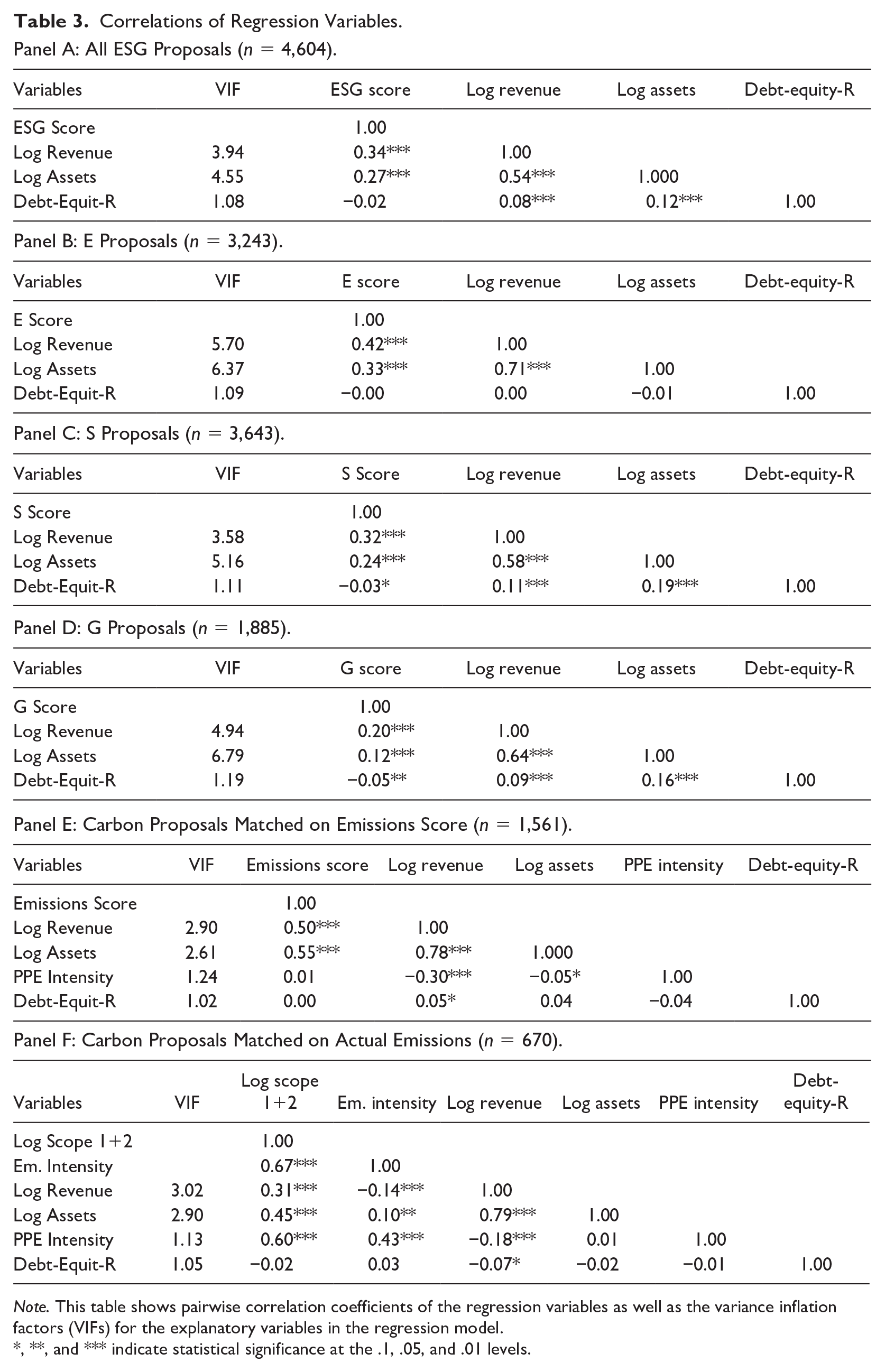

Table 3 reports the Pearson correlation coefficients of our variables. While the coefficients are statistically significant at p < .01, they are mostly low and usually do not exceed 0.7, except for Log Assets and Log Revenue. Therefore, we compute variance inflation factors (VIFs) for all explanatory variables in our regression models. Values greater than 10 indicate the presence of multicollinearity and issues in estimation (Chatterjee & Hadi, 2006). We find VIFs below 10 that suggest only very moderate correlation. Hence, we do not expect any issues with multicollinearity.

Correlations of Regression Variables.

Panel A: All ESG Proposals (n = 4,604).

Note. This table shows pairwise correlation coefficients of the regression variables as well as the variance inflation factors (VIFs) for the explanatory variables in the regression model.

, **, and *** indicate statistical significance at the .1, .05, and .01 levels.

Main Results

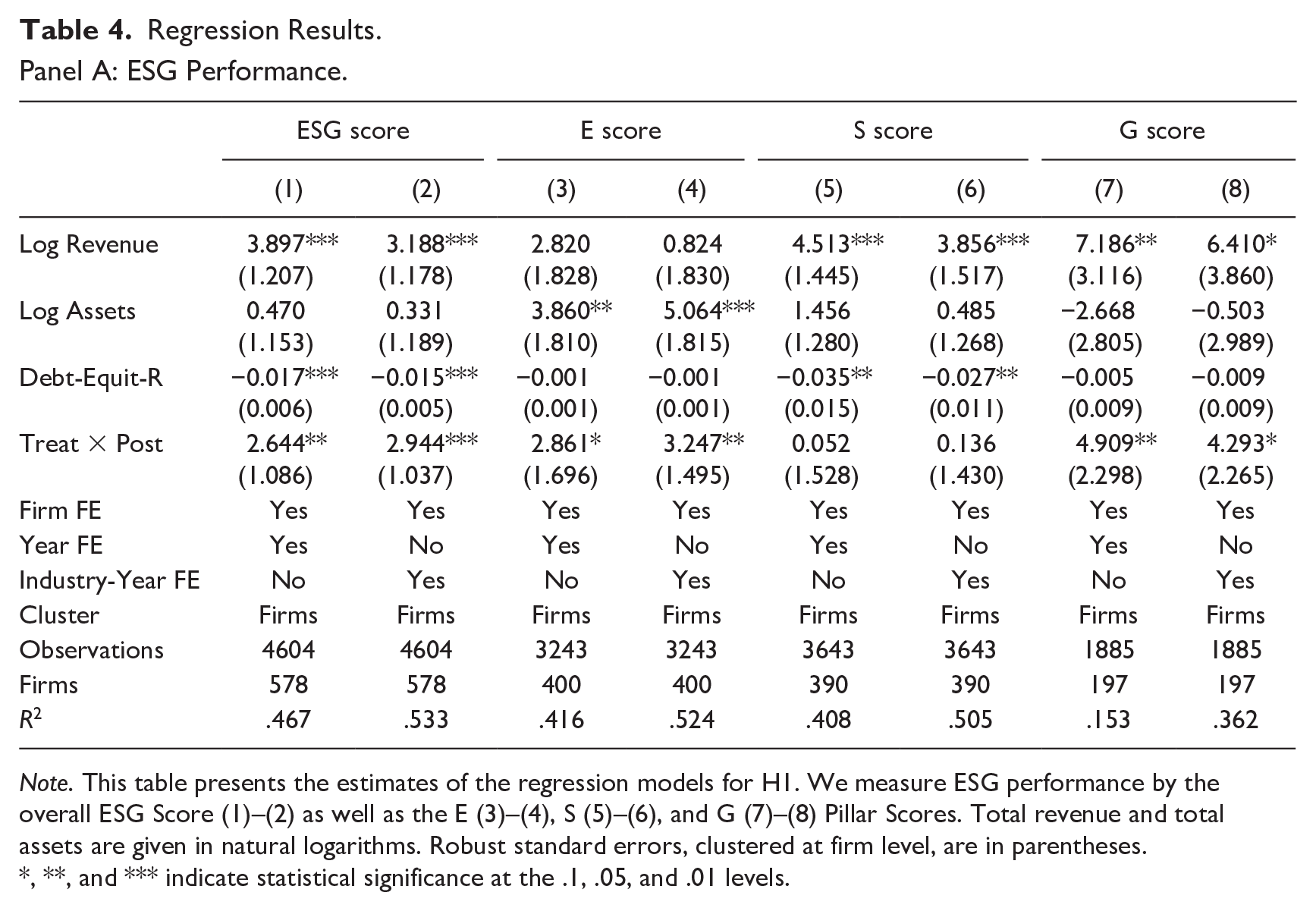

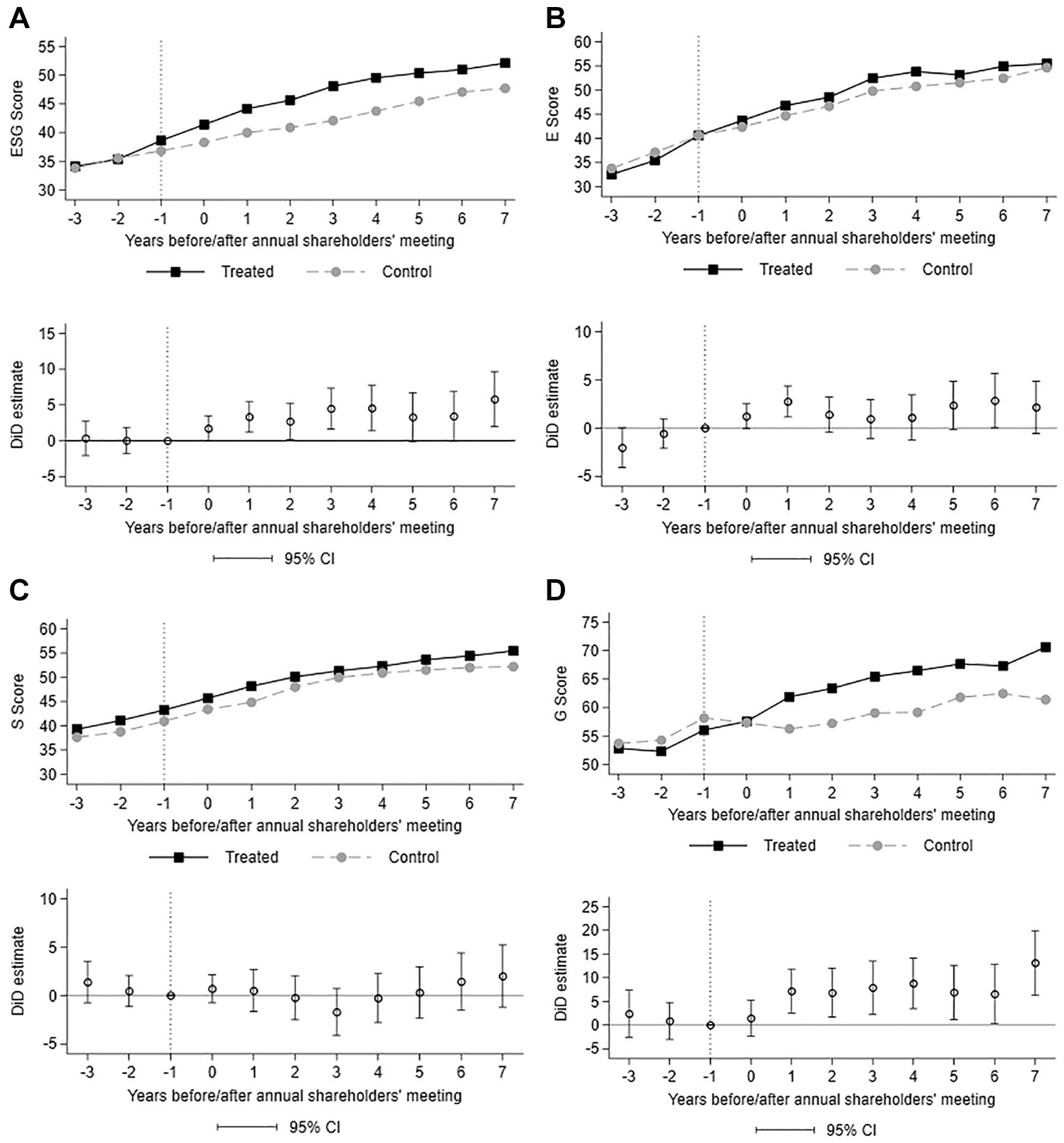

To test for H1a-d, we create two model specifications for each ESG-related proposal type and measure of ESG performance, respectively. The columns in Panel A of Table 4 contain the estimates of the panel regressions for the specifications. Columns (1) and (2) show positive and statistically significant interaction term coefficients for the ESG Score (2.644, resp. 2.944, p = .015, resp. p = .005). For treated firms, this corresponds to an increase by 6.8% to 7.6% in the ESG Score following the proposal submission (given the mean of 38.61 from Table 1). Similarly, we find positive and statistically significant estimates for the E Score (2.861, resp. 3.247, p = .092, resp. p = .033) and the G Score (4.909, resp. 4.293, p = .034, resp. p = .060). This corresponds to an increase by 7.1% to 8.0% in the E Score (given the mean of 40.56 from Table 1) and 7.7% to 8.8% in the G Score (given the mean of 56.04 from Table 1), respectively. However, these observations do not hold for the S Score of firms since the interaction term coefficients in columns (5) and (6) are close to zero and statistically insignificant. Figure 2 demonstrates the parallel trend in the different ESG performance measures of treated and control firms prior to the event, which is followed by a differential shift in the time after the proposal, except for the S Score. Moreover, it demonstrates that the observed differential shifts are mainly based on an increase in the ESG performance of treated firms, while control firms remain close to their previous levels. Overall, we see strong support for H1a and H1c-d.

Regression Results.

Panel A: ESG Performance.

Note. This table presents the estimates of the regression models for H1. We measure ESG performance by the overall ESG Score (1)–(2) as well as the E (3)–(4), S (5)–(6), and G (7)–(8) Pillar Scores. Total revenue and total assets are given in natural logarithms. Robust standard errors, clustered at firm level, are in parentheses.

, **, and *** indicate statistical significance at the .1, .05, and .01 levels.

Panel B: Carbon Performance.

Note. This table presents the estimates of the regression models for H2. We measure carbon performance by the Emissions Score (1)–(2) as well as total Scope 1 and Scope 2 carbon emissions (3)–(4) and carbon emission intensity (5)–(6). Total revenue, total assets, and total carbon emissions are given in natural logarithms. Robust standard errors, clustered at firm level, are in parentheses.

, **, and *** indicate statistical significance at the .1, .05, and .01 levels.

Panel C: Sponsor Types and Proposal Status.

Note. This table presents the estimates of the regression models for H3 and H4. We use the ESG Score as the dependent variable and explore the treatment effect across sponsor types and proposal status. We analyze SRI funds (1) and non-SRI funds (2), and we cluster different proposal sponsors according to whether they primarily pursue SRI preferences (3) or non-SRI preferences (4). Furthermore, we analyze proposals that were voted on (5), withdrawn (6), or omitted (7). Robust standard errors, clustered at firm level, are in parentheses.

, **, and *** indicate statistical significance at the .1, .05, and .01 levels.

Panel D: Number of Prior Proposals.

Note. This table presents the estimates of the regression models for H5. We measure ESG and carbon performance by the overall ESG Score (1) as well as the E Pillar Score (2), S Pillar Score (3), G Pillar Score (4), Emissions Score (5), total carbon emissions (6), and carbon emission intensity (7). For the ESG Score, we examine the treatment effect with regard to the total number of ESG-related proposals filed during the observation period. For the Pillar Scores, we consider the total number of E-, S-, and G-related proposals separately. For the Emissions Score and carbon emissions, we consider the total number of carbon-related proposals. Robust standard errors, clustered at firm level, are in parentheses.

, **, and *** indicate statistical significance at the .1, .05, and .01 levels.

ESG Performance Effects Over Time.

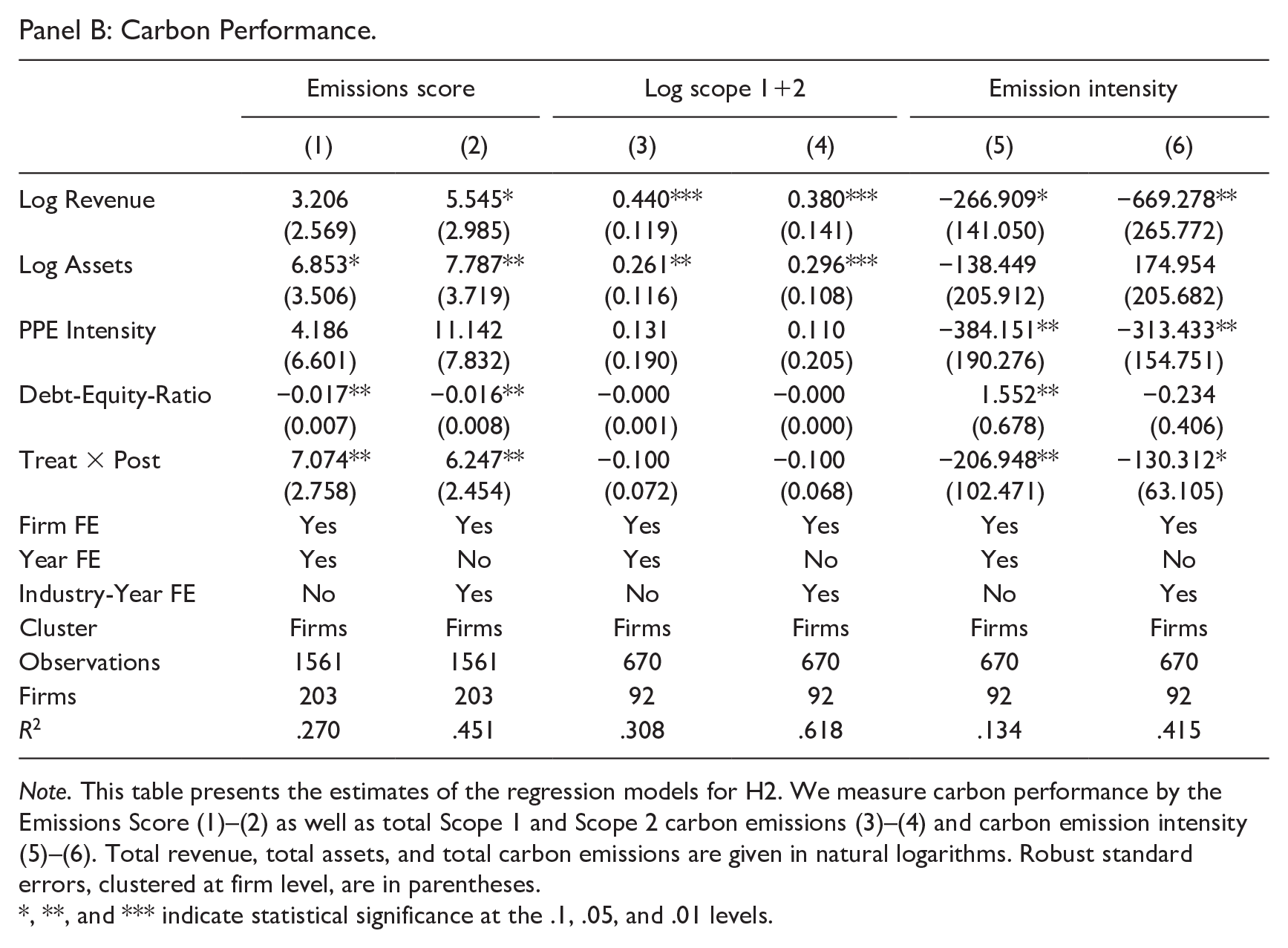

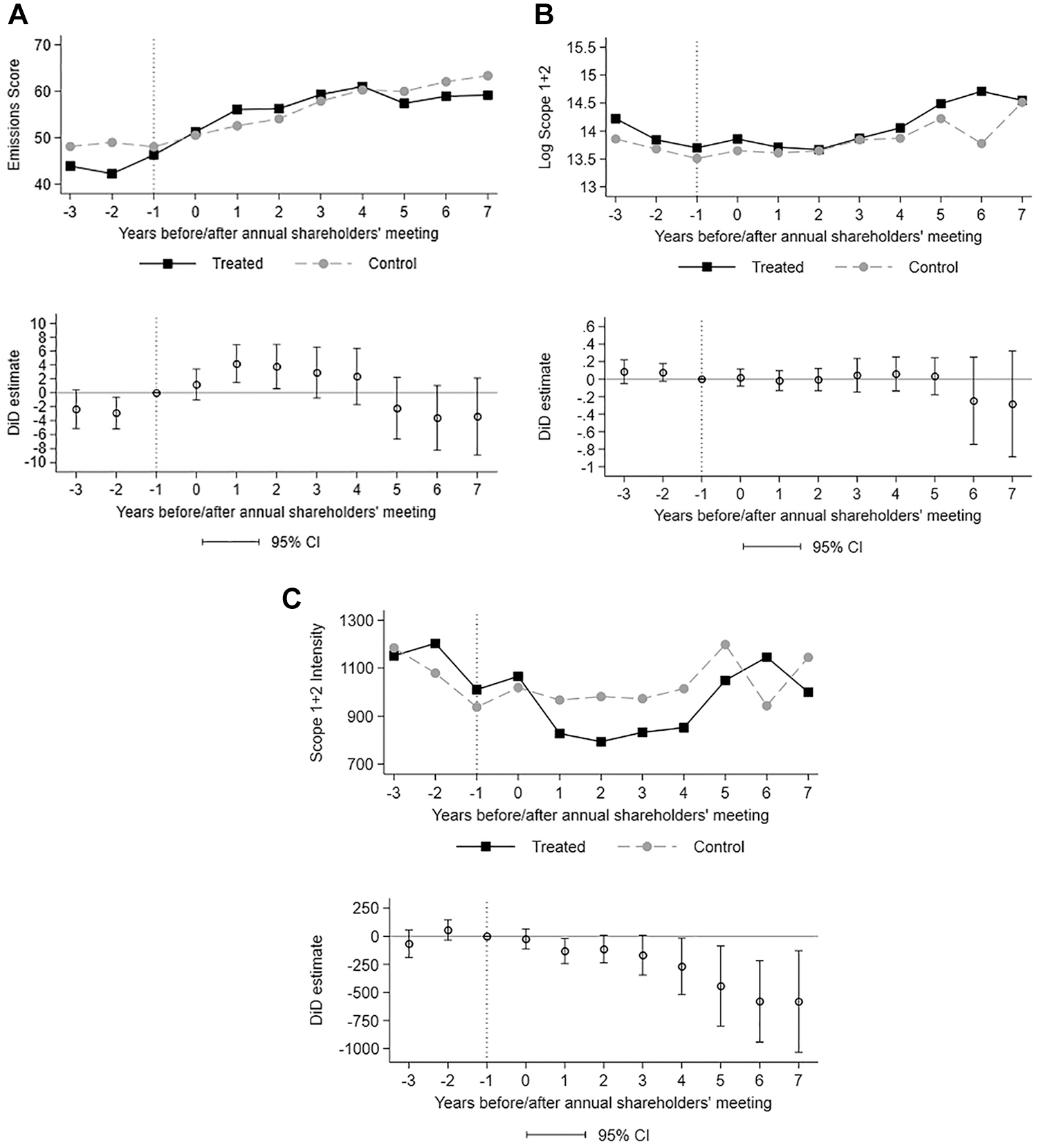

With H2, we also investigate whether the submission of a carbon-related proposal has an effect on firms’ carbon performance. Hence, we conduct the model specifications for the different measures of carbon performance, namely the Emissions Score, total carbon emissions (Log Scope 1+2), and carbon emission intensity (Scope 1+2 Intensity). In columns (1) and (2) of Panel B of Table 4, the coefficients of the interaction term Post × Treat for the Emissions Score are positive and statistically significant for both model specifications (7.074, resp. 6.247, p = .011, resp. p = .012). For treated firms, this corresponds to an increase by 13.5% to 15.3% in the Emissions Score following the proposal submission (given the mean of 46.27 from Table 1). Thus, treated firms show a significantly higher commitment towards reducing carbon emissions in their production and operational processes after receiving a carbon-related proposal as compared with control firms. Moreover, for Scope 1+2 Intensity, we find that the interaction term Post × Treat in columns (5) and (6) has a negative and statistically significant coefficient (-206.948, resp. -130.312, p = .043, resp. p = .059). Thus, despite a substantial decrease in observations for our carbon performance regressions compared with our ESG performance, we find evidence that treated firms reduce their carbon emissions by 130.3 metric tons per million U.S. dollars in revenue, or 10.9% (given the mean of 1,193.00 from Table 1), respectively. However, these observations do not hold for firms’ total carbon emissions, as the coefficients of the interaction term in columns (3) and (4) are close to zero and statistically insignificant. Thus, treated firms seem to concentrate on improving their operational carbon efficiency instead of reducing total carbon emissions. Our findings are reinforced by Figure 3, which shows the development of the average Emissions Score, total carbon emissions, and carbon emissions intensity of the treated and control samples before and after the treatment. Altogether, we find support for H2, except in the context of total carbon emissions.

Carbon Performance Effects Over Time.

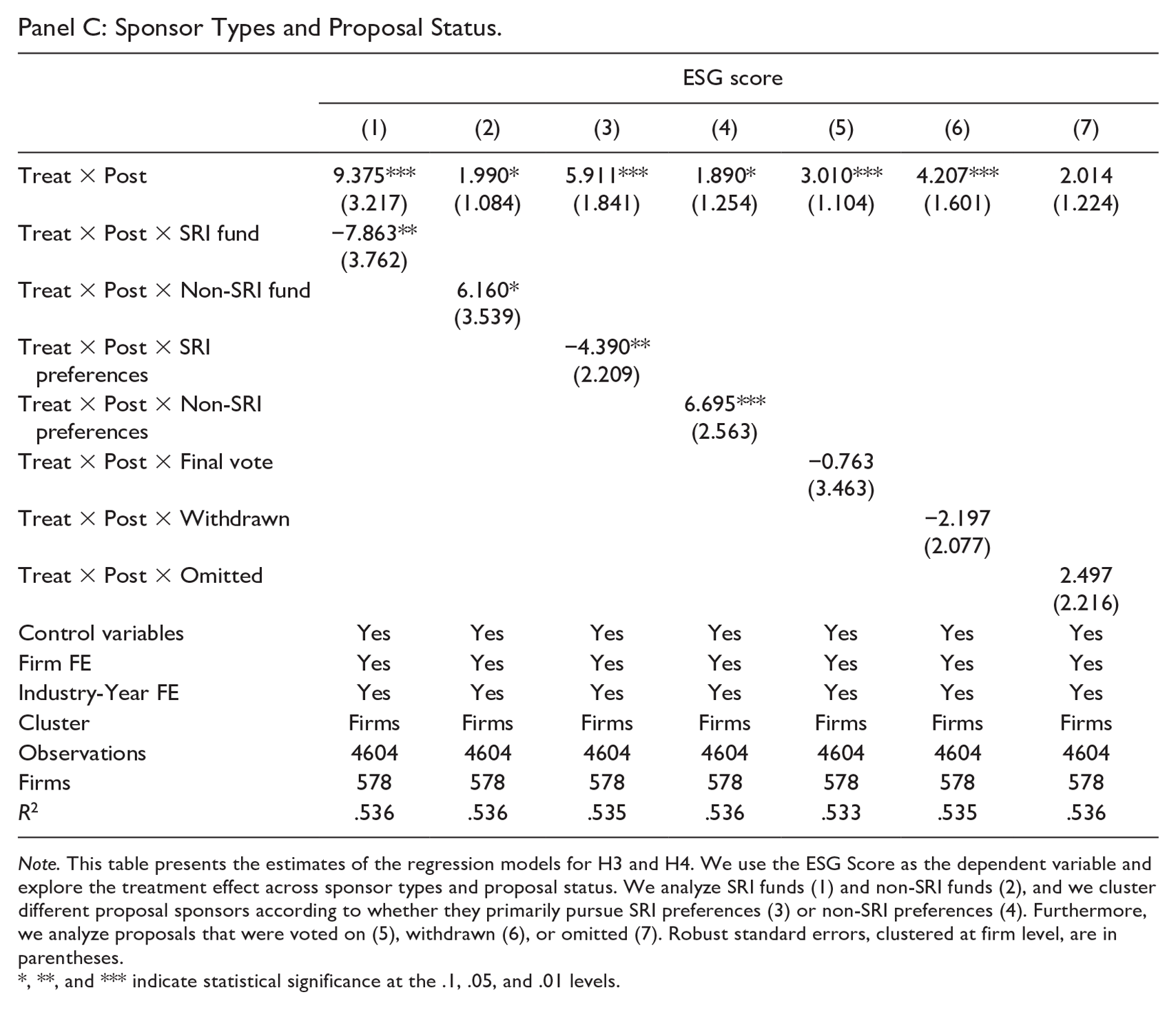

With H3, we explore the effect of ESG-related proposals on firms’ ESG performance for different proposal sponsors. Thus, we extend the baseline model into a triple difference-in-differences model to add another layer of heterogeneous treatment effect (i.e., the heterogeneity across proposal sponsors). Column (1) in Panel C of Table 4 shows a negative and statistically significant coefficient for the triple interaction term Treat × Post × SRI fund. While firms targeted by proposals from shareholders other than SRI funds improve their ESG Scores by an average of 9.375 points (p = .038), firms targeted by SRI funds only improve their ESG Scores by 1.512 points (9.375 – 7.863, p = .038). For non-SRI funds in column (2), on the other hand, the effect is 6.160 points larger (p = .082) than for other sponsors (1.990 points). A similar pattern emerges, when we categorize all sponsors as investors with SRI preferences (–4.390 points compared with all other shareholders, p = .047) in column (3), or non-SRI investors with financial preferences (+6.695 points compared with all other shareholders, p = .009) in column (4), respectively. We infer that firms are more responsive to shareholder proposals that are sponsored by investors who are most focused on shareholder value. Hence, we confirm H3.

With H4, we investigate whether the effect of ESG-related proposals on firms’ ESG performance hinges on the proposal status. As such, we interact the difference-in-differences variable with dummy variables that indicate if a proposal was withdrawn, omitted, or voted on. The coefficients for the triple interaction terms in columns (5) to (7) in Panel C of Table 4 are statistically insignificant. Hence, we find no evidence that withdrawn proposals are more effective than proposals that are omitted or voted on. Hence, we cannot confirm H4.

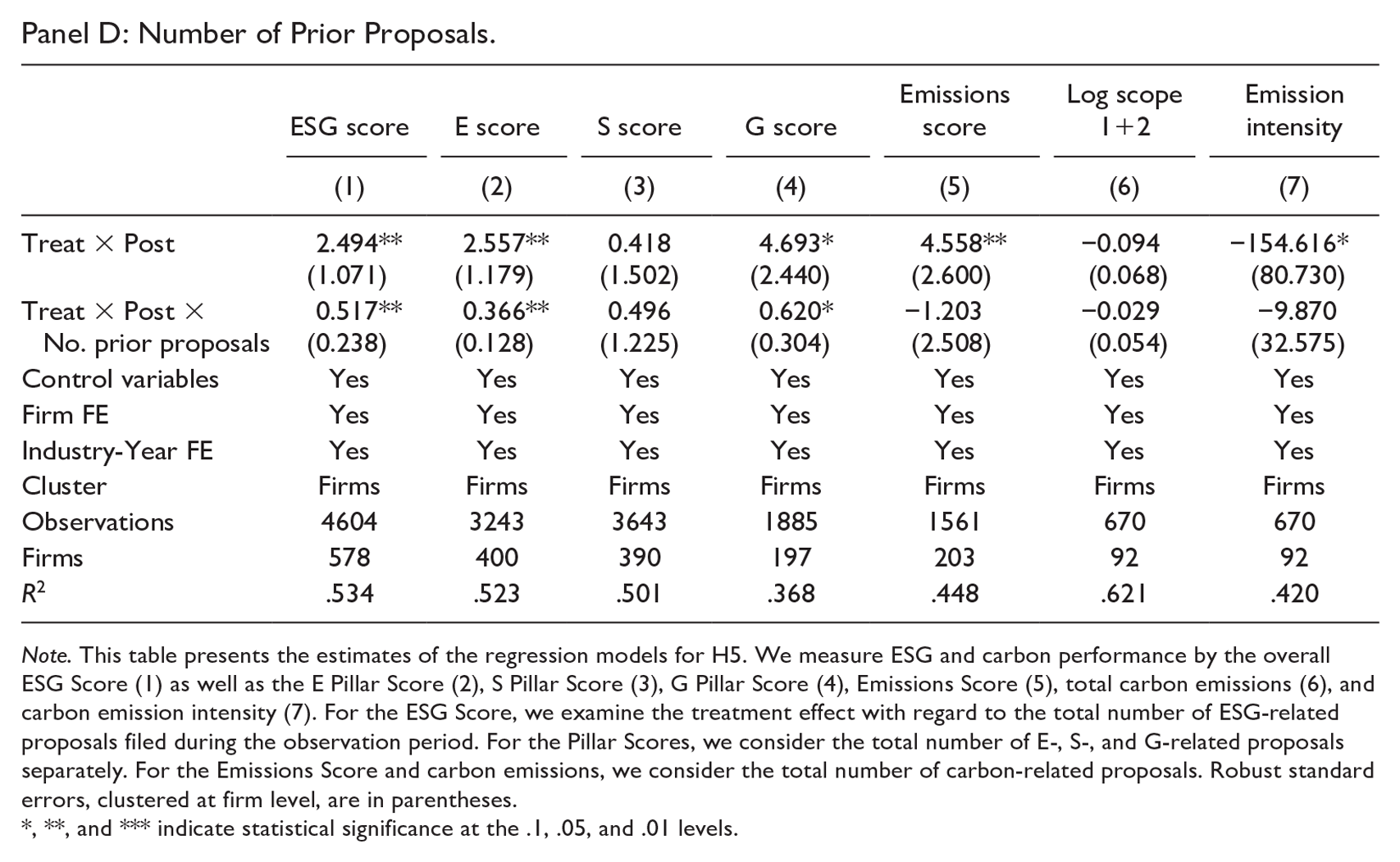

With H5, we examine whether the effect of ESG-related proposals on firms’ ESG performance is affected by the cumulative effect of prior proposals submitted to these firms. Therefore, we interact the difference-in-differences variable with the number of prior ESG-related proposals received by these firms over time. For the Pillar Scores, Emissions Score, and carbon emissions, we consider the number of prior E-, S-, G-, and carbon-related proposals separately. The coefficients of the triple interaction terms in columns (1), (2), and (4) in Panel D of Table 4 are statistically significant. For both the ESG Score (0.517, p = .037), E Score (0.366, p = .024), and G Score (0.620, p = .085), the ESG performance improves as the number of prior shareholder proposals increase. These observations do not hold for firms’ social and carbon performance, as the coefficients of the triple interaction terms in columns (3) and (5) to (7) are statistically insignificant. Hence, we find support for H5, except in the context of social- and carbon-related proposals.

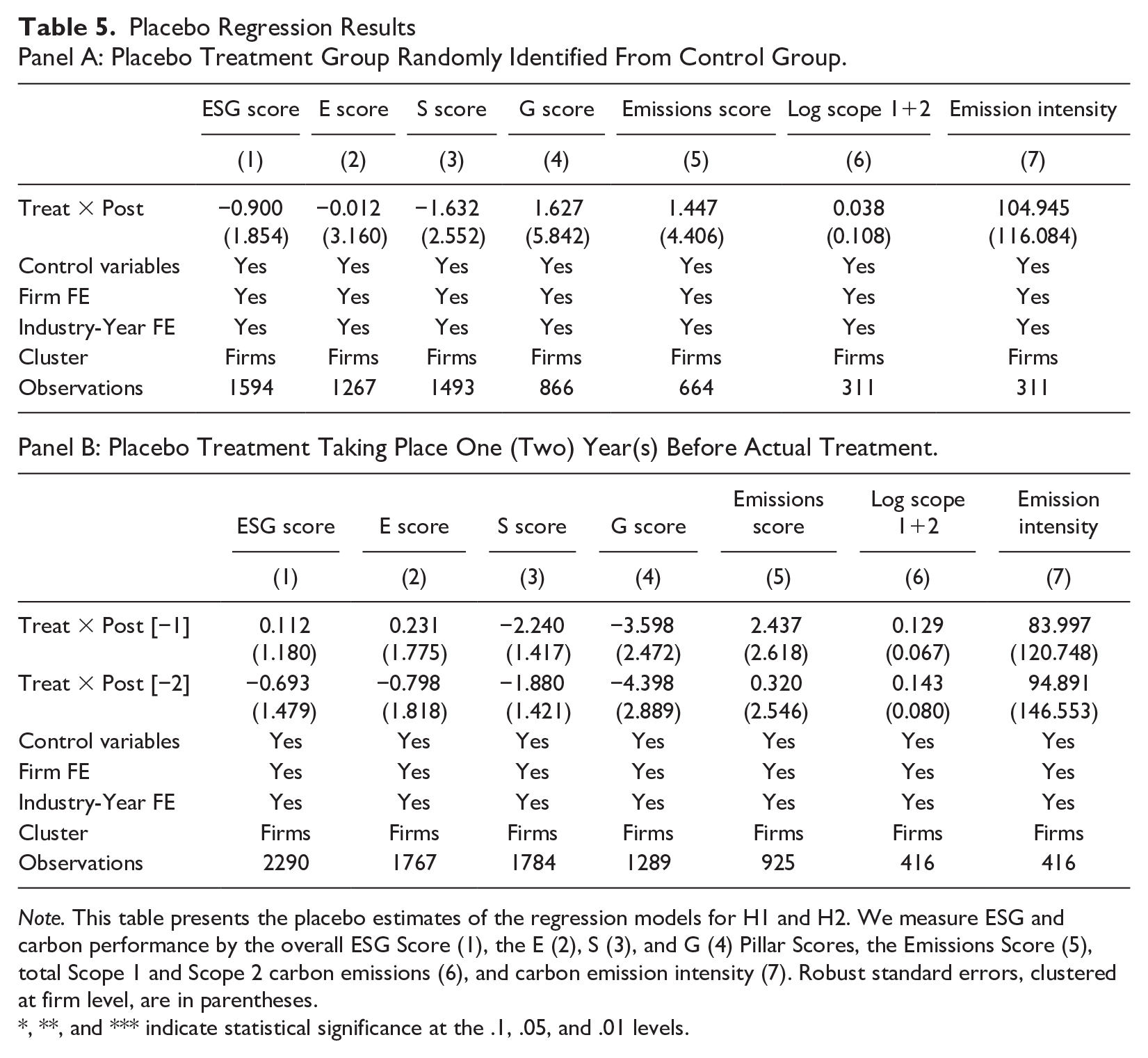

Finally, we perform several robustness checks to evaluate the validity of our results. First, we estimate variations of the baseline model without control variables and/or fixed effects to see if our results hold. All of these tests show similar results to our base analysis (unreported results). Second, we perform placebo tests to establish validity of inference in our difference-in-differences model (Bertrand et al., 2004; Hagemann, 2019). We drop the treatment group and randomly assign firms of the control group to a placebo treatment group. As can be seen from Panel A of Table 5, the placebo estimates do not show any significant treatment effects. Then, using the pretreatment data, we choose different years [t–1 and t–2] as placebo treatment dates prior to the actual treatment event. Similarly, as can be seen from Panel B of Table 5, the analysis of the placebo intervention does not show significant coefficient estimates, which implies that the treatment effect we find in our baseline model can be attributed to the shareholder intervention. In sum, this suggests that the assumptions underlying the identification strategy hold and that our difference-in-differences analysis is valid.

Placebo Regression ResultsPanel A: Placebo Treatment Group Randomly Identified From Control Group.

Note. This table presents the placebo estimates of the regression models for H1 and H2. We measure ESG and carbon performance by the overall ESG Score (1), the E (2), S (3), and G (4) Pillar Scores, the Emissions Score (5), total Scope 1 and Scope 2 carbon emissions (6), and carbon emission intensity (7). Robust standard errors, clustered at firm level, are in parentheses.

, **, and *** indicate statistical significance at the .1, .05, and .01 levels.

Discussion and Conclusion

Investors are increasingly exercising their shareholder rights to influence corporate strategies on how to address ESG issues (Dimson et al., 2015). As such, shareholders have intensified their efforts to voice their opinions by divesting, engaging with firms, or filing proposals (Li et al., 2021). This is the first study examining whether shareholders can actually influence firms’ ESG and carbon performance by submitting shareholder proposals. As such, our findings contribute to the literature on shareholder activism. Our results suggest that target firms are associated with higher ESG Scores as well as individual E Scores and G Scores after they receive a respective shareholder proposal. Therefore, our study complements previous findings on shareholder activism by showing that firms can be induced to change their environmental or governance-related performance in response to shareholder proposals. Surprisingly, we find no statistically significant effect for the S Score, which leaves room for further investigations. One reason might be the range of data covered in the data aggregation process. The S Score captures a wide range of data points across different socially relevant topics, for instance information regarding the workforce, customers, human rights, and society. It is possible that changes to a specific social aspect might barely change the overall score. We come to an interesting finding by exploring whether the treatment effect is conditional on the proposal status. Surprisingly, we find no evidence that withdrawn proposals are more or less impactful than proposals that were omitted or those that were brought to a vote. This result suggests that the procedural outcome of a proposal may be less important than its submission in driving change. When shareholders address sustainability issues by submitting proposals, they signal dissatisfaction and highlight the importance of these issues to stakeholders. This act of filing itself raises awareness and compels management to respond strategically, regardless of whether the proposal is ultimately withdrawn, omitted, or voted on. As a consequence, the firm’s management is likely to conduct an internal review of the issue to determine its relevance to the firm’s operations. This review process can lead to greater awareness and understanding of the issue, potentially triggering internal discussions and even changes in the firm’s strategy. Moreover, it is possible that the firm’s management may decide to implement changes preemptively to avoid escalation or to demonstrate responsiveness to shareholders’ concerns. This could explain why the outcome of the proposal (withdrawal, omission, or voting) does not significantly alter the firm’s subsequent ESG performance; the crucial effect was already achieved by the proposal entering the firm’s decision-making space. The broader pattern supports the interpretation that the filing of a proposal itself introduces pressure and elevates the perceived importance of sustainability issues. Thus, while procedural outcomes differ, all types of proposals appear to contribute meaningfully to shaping corporate agendas. We also show that shareholders can demonstrate signal strength by filing multiple proposals over time. Our results indicate that the cumulative effect of prior shareholder proposals enhances their impact, as firms tend to exhibit greater improvements in ESG performance when they have a larger number of prior proposals. In this way, investors may indirectly shape a firm’s strategy as we find empirical evidence that the proposals are considered and implemented and corporate performance changes accordingly.

There is a growing body of literature on impact investing (Kölbel et al., 2020). We contribute to this literature by demonstrating that shareholder proposals are a promising approach for investors to induce improvements in firms’ ESG and carbon performance. As an important insight we show that the type of the proposal sponsor influences the effect of ESG-related proposals on firms’ ESG performance. Proposals that are sponsored by less norm-constrained investors, for example, non-SRI mutual funds, are associated with higher improvements in ESG performance than proposals submitted by sponsors that have a socially responsible agenda. One explanation for this outcome might be that firms give greater weight to shareholder proposals from non-SRI investors because they usually hold more stakes and they can exert greater pressure. The exit of a large investor could potentially drive down the share price (Admati & Pfleiderer, 2009), so firms might prefer to bow to the request of shareholder proposals and change their business conduct.

Our findings have practical implications for both managers as well as capital market participants. The results show that shareholder proposals can be a sufficient instrument for influencing the ESG and carbon performance of firms. Hence, managers seem to have recognized the relevance of such proposals for their strategy making. Independently of the circumstance if investors actually exercise their shareholder rights on ESG topics, proposals may serve as an important indication of relevant issues that investors expect firms to adequately address. An early incorporation of such issues and according adjustment of corporate strategy may be an important risk mitigation strategy. Furthermore, our findings are also relevant for investors that intend to generate impact with their investments. There is frequent discussion of whether investments in certain assets classes, notably public equities, can generate any impact at all. While several equilibrium models, such as those by Heinkel et al. (2001), Pástor et al. (2021), Pedersen et al. (2021), and Zerbib (2022), suggest a negative relationship between a firm’s corporate environmental performance and its expected stock returns (and consequently the firm’s cost of capital), empirical evidence on this matter remains scarce. Our findings show that investors can have an impact: Shareholders can encourage firms to make improvements in ESG and carbon performance through shareholder proposals.

With respect to global climate efforts, our results show that while carbon-related proposals have an effect on emission intensities, they do not have an effect on total emissions. The reason for this could be that the achieved carbon emission improvements are overcompensated for by respective growth effects. Thus, firms are either unable to decouple their emissions from production or the incentive to do so is not great enough (Bauckloh et al., 2022). However, to meet the Paris Agreement’s temperature goal of limiting global warming to 1.5°C, total emission reductions are essential, globally as well as for individual firms. As such, this finding constitutes clear limitations of the effects of shareholder proposals: they do not, yet, lead to total emission reductions.

Our study has some limitations, primarily due to the use of empirical data. First, achieving a perfect experimental setting is challenging in this context, which means that the submission of shareholder proposals to firms may not be randomly assigned, but rather endogenous. For example, shareholders might preferentially target firms that are already on a trajectory of improving their ESG performance, as these firms are more likely to consider the proposals. To mitigate this limitation, we employ a rigorous matching procedure—namely, PSM—to minimize differences between treated and control firms, thereby reducing bias attributable to observable confounders. PSM is a useful approach for addressing selection bias as it creates a quasi-experimental design where treated and control firms are matched on their likelihood of receiving a proposal based on observable characteristics. As such, this matching process helps control for pre-existing differences between the groups in various firm characteristics, such as the level and change in ESG performance. In addition, we incorporate the matching variables as control variables in our regression analysis, further adjusting for any remaining differences. While these steps cannot completely eliminate the possibility of confounding factors, they significantly strengthen the validity of our findings. Nonetheless, selection bias remains a potential concern. Firms may become targets for shareholder proposals precisely when they exhibit a greater willingness to integrate such demands into their operations. This could mean that observed improvements in ESG performance following proposals are at least partially attributable to pre-existing managerial openness rather than the proposals themselves. While we address this issue through our matching and regression framework, we acknowledge that these methods cannot fully account for unobservable factors driving both proposal submission and subsequent ESG improvements. One methodological approach that has been suggested to address selection bias is a regression discontinuity (RD) design based on close-call voting outcomes. Flammer (2015) employs this approach to isolate causal effects by comparing firms where shareholder proposals narrowly passed versus narrowly failed. While RD designs have clear advantages in establishing causality under certain conditions, they also come with significant limitations that make them less suitable for our study. Specifically, Flammer’s (2015) analysis relies on only 61 close-call proposals out of 2,729 total proposals—approximately 2.2% of her sample—raising concerns about external validity and generalizability. These close-call proposals are disproportionately concentrated in specific categories (e.g., labor and environmental issues), which may not represent the broader spectrum of shareholder activism. In contrast, our study examines a much larger dataset of over 7,000 shareholder proposals, including 4,604 ESG-related proposals spanning diverse topics and contexts. Adopting an RD approach in our case would likely result in an even smaller subset of close-call observations due to the relatively low number of proposals brought to a vote and the narrow margin required for RD identification. This would severely limit our ability to draw conclusions about the broader agenda-setting effects of shareholder proposals. Finally, while RD designs are powerful tools for causal inference in narrowly defined settings, they do not address broader questions about how all types of proposals—regardless of voting outcomes—contribute to shaping corporate agendas. Thus, while we acknowledge the strengths of Flammer’s (2015) approach in identifying causal effects under specific conditions, its limitations make it less applicable to our research question and dataset. Instead, we focus on leveraging robust matching techniques and comprehensive regression analyses.

Second, we base our analysis on firm-reported carbon emissions and, thus, rely on firms’ abilities to correctly measure, collect, and report their carbon emissions. However, it is a well-documented limitation that self-reported carbon emission data can be flawed (Busch, Johnson, & Pioch, 2022). While our analysis includes both direct emissions (Scope 1) and indirect emissions from purchased energy (Scope 2), it is important to note that reductions in these emissions may not fully capture shifts in carbon-intensive processes. For example, firms may outsource carbon-intensive activities to external suppliers, which would increase Scope 3 emissions—emissions that are often unreliable due to estimation by data providers and, therefore, excluded from our analysis. Future research could expand on this by examining how shareholder proposals influence firms’ carbon emissions across all scopes, including upstream or downstream impacts within the supply chain. Moreover, further research could evaluate which forms of shareholder activism are most effective. With shareholder proposals, we have considered a public form of shareholder activism, and it would be worthwhile to assess whether private engagement via meetings and discussions have a similar effect.

Third, at the point when we started writing this article, we were not aware of the fact that Refinitiv is rewriting its data (Berg et al., 2021) and, accordingly, some of the utilized ESG Scores may have changed over time. At this point, we can only acknowledge this limitation of the dataset and cannot assess to what extent data rewritings affect our measures of ESG performance and, thus, our empirical outcomes. In case any data rewritings took place within our sample, we cannot judge whether the previous or the new data reflects the true reality. However, we note that Bauckloh et al. (2021) show in a similar empirical setting that the rewriting history bias has no significant influence on the results.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We acknowledge the financial support provided by the Evangelische Bank eG and EB—Sustainable Investment Management GmbH, ISS Germany AG, and the Mercator Foundation through the project “Rahmenprogramm Sustainable Finance” (grant number 19026202). We are thankful for the comments and suggestions from the participants of the GRONEN 2022 Conference in Amsterdam, the 5th Annual GRASFI Conference in Zurich, the WK-NaMa Conference 2022 in Nuremberg, and the Annual Meeting of the Academy of Management 2023 in Boston.