Abstract

This article asks how sustainable investing contributes to societal goals, conducting a literature review on investor impact—that is, the change investors trigger in companies’ environmental and social impact. We distinguish three impact mechanisms: shareholder engagement, capital allocation, and indirect impacts, concluding that the impact of shareholder engagement is well supported in the literature, the impact of capital allocation only partially, and indirect impacts lack empirical support. Our results suggest that investors who seek impact should pursue shareholder engagement throughout their portfolio, allocate capital to sustainable companies whose growth is limited by external financing conditions, and screen out companies based on the absence of specific environmental, social, and governance practices that can be adopted at reasonable costs. For rating agencies, we outline steps to develop investor impact metrics. For policy makers, we highlight that sustainable investing helps diffuse good business practices, but is unlikely to drive a deeper transformation without additional policy measures.

Introduction

There are growing expectations that sustainable investing (SI)—that is, investing that takes environmental, social, and governance (ESG) information into account—will contribute to the achievement of societal goals. Historically, the Quakers divested to avoid supporting the slave trade, and colleges divested to challenge the South African apartheid regime (Molthan, 2003). Today too, many investors are attracted to SI due to their altruistic motives (Hartzmark & Sussman, 2017; Riedl & Smeets, 2017), expecting that SI will allow them to make a positive impact. Banks and asset managers are catering to these expectations by offering more and more investment products that emphasize sustainability, responsibility, and—increasingly—impact (Global Sustainable Investment Alliance [GSIA], 2018). Policy makers too are discussing SI as a potential mechanism for mitigating climate change (International Panel on Climate Change, 2018) and for helping us realize the United Nations’ Sustainable Development Goals (SDGs; Betti et al., 2018).

Yet, in spite of these high expectations, little is known about the actual impact investors make through SI. We define investor impact as the change that investor activities achieve in company impact, and company impact as the change that company activities achieve in social and environmental parameters. These definitions are consistent with prior academic literature (Brest et al., 2018) as well as with the view of leading institutions in the field of impact evaluation (International Finance Corporation [IFC], 2019).

The concept of investor impact is only beginning to take root in the SI industry. Currently, most SI funds either exclude firms operating in harmful industries or focus on companies that have in the past performed well on metrics of ESG performance. This is a static approach, which ignores that impact is fundamentally about change. Companies can and do change over time, and investors make an impact by triggering or accelerating such change. Due to a lack of suitable metrics for investor impact, however, very few investors analyze how their activities cause companies to change. As a result, the majority of the US$ 30 billion that are deployed in SI today (GSIA, 2018) is invested in ways that promise only modest and perhaps even negligible investor impact.

To date, academic literature on SI has also neglected the concept of investor impact. Many studies rely in their analysis on ESG metrics, which can be interpreted as a proxy for company impact. 1 However, the vast majority of studies uses ESG metrics as an explanatory variable, very few analyzing ESG metrics as a dependent variable. As a result, little is known about what drives changes in company impact in general. This is true in particular for the literature on the financial performance of SI (e.g., Friede et al., 2015; Lins et al., 2017; Renneboog et al., 2008), which investigates how ESG metrics influence investment performance, but not how different ways of investing influence ESG metrics. As a consequence, there is a gap regarding the mechanisms of investor impact in the literature on SI.

While there are studies that deal in some way with investor impact, they often do so in a context that is not related to SI. Therefore, this article conducts a broad review of such literature to bring together findings regarding the mechanisms of and evidence for investor impact. We distinguish shareholder engagement, capital allocation, and indirect impacts as the three principal mechanisms of investor impact. For each mechanism, we evaluate the existing empirical evidence as reported in the literature and establish key determinants that increase or decrease investor impact. Shareholder engagement emerges as the most reliable mechanism for investors seeking impact, in the sense that it has been clearly demonstrated empirically. The impact of capital allocation is less reliable, since different parts of the mechanism have been studied empirically, but not yet in combination. Indirect impact mechanisms, which include stigmatization, endorsement, benchmarking, and demonstration, have hardly any empirical support in the literature so far.

The findings of this review have important implications for investors, ESG data providers, and policy makers. Investors who want to stimulate real-world impact based on evidence have three ways of pursuing this aim. First, roll out shareholder engagement throughout their portfolio, focusing on requests that have a good chance of success and yield substantial improvements in company impact. Second, allocate capital to companies that have positive company impact, under the condition that these firms are constrained in their growth by external financing conditions. This condition applies more likely for smaller firms operating in less mature financial markets. Third, screen out investments based on the absence of ESG practices, focusing on a few specific and transparently communicated practices that have a low “cost of reform” for companies. This should be pursued in a large coalition of investors and encompass stocks and bonds. ESG data providers, meanwhile, should consider developing metrics of investor impact. Most existing SI fund ratings provide a snapshot of the company impact of the portfolio constituents. This leaves a gap for ratings that reflect the change in company impact that the fund is driving through its investment activity. Finally, policy makers should be aware that while SI is a powerful mechanism for diffusing good business practices, SI alone is unlikely to transform industries without additional policy measures.

Key Concepts and Scope

Our literature review aims to gather the available scientific evidence for the different mechanisms of investor impact. To set the scope of the review, we provide a detailed explanation of the concept of investor impact and describe the mechanisms of investor impact, which are illustrated in Figure 1.

Key concepts and mechanisms.

Investor Impact

The notion of impact in an investment context originates from development finance, where funds are directed toward programs with the intention of improving livelihoods. The World Bank characterizes impact as “ . . . causal effects of a program on an outcome of interest” (Gertler et al., 2011, p. 8). There is a rich literature concerned with impact evaluation, mostly with applications to development finance, philanthropy, and foreign aid (Bamberger et al., 2012). In this literature, impact is consistently described as having three defining characteristics: (a) it describes a change against a baseline, (b) it relates to a clearly defined parameter, and (c) it implies causality in the sense that the change would not have occurred in the absence of the activity. The last requirement is also referred to as additionality (see, e.g., Greiner & Michaelowa, 2003). On this basis, we define impact as change in a specific social or environmental parameter that is caused by an activity.

In the context of SI, it is useful to distinguish between the impact of investors and the impact of companies. Investors do not have a direct impact on social and environmental parameters. Instead, investors have an impact on the companies they invest in, which in turn have an impact on social and environmental parameters (Brest & Born, 2013; Brest et al., 2018). Thus, as previously defined, we refer to investor impact as the change that investor activity achieves in company impact, and we refer to company impact as the change that a company’s activities achieve in a social or environmental parameter. This definition is in line with the recently released principles for impact management from the IFC, which stipulate that investors should establish a narrative that outlines how the investor contributed to the achievement of company impact (IFC, 2019).

A more formal statement of these definitions reveals that investor impact can be achieved in two different ways. Assume that a social or environmental parameter P depends among other variables on the level of company activity Ac. Company activity can refer both to a company’s operations and to its products and services. Then, company impact Ic is the marginal change in parameter P per unit of company activity Ac, integrated over the level of company activity.

To simplify, we define q, the social or environmental quality of a company’s activities, as the average change in parameter P per unit of company activity Ac. It follows that company impact is given by the product between the level and the quality of company activity.

As previously defined, investor impact Ii is the change in company impact Ic achieved by investor activity. Assuming Ic depends among other variables on the level of investor activity Ai, Ii is the marginal change in company impact Ic per unit of investor activity Ai integrated over the level of investor activity Ai.

Using Equation 2, we can provide a mathematical definition of investor impact in terms of changes in the level of company activity Ac and the quality of company activity q.

Equation 4 shows that there are two fundamentally different ways for investors to achieve investor impact. First, by growing the level of company activity; second, by improving the quality of company activity.

To give an example, consider a company that manufactures solar panels. We will look at impacts on global carbon dioxide emissions per year as the parameter of interest. The level of the company’s activity is measured in solar panels produced, and the quality of the company’s activity is given by the average carbon emission savings achieved with each panel produced. Let’s assume the company sells 10,000 panels per year, each of which, over its life cycle, avoids three tons of carbon emissions. Then the company impact is 30,000 tons of avoided carbon emissions per year.

Now consider an investment in this solar panel manufacturer. Investor activity can be measured in terms of dollars invested, and we will assume there is a US$ 10 million investment in the company’s equity. Let us assume that this investment allows the company to increase its level of activities, in this case the production of solar panels, by 10%. As a result, the company’s impact will increase by 10% yielding an investor impact of 3,000 tons of avoided carbon emissions. Alternatively, the investor behind this investment may use the influence that comes with his or her equity stake to improve the quality of the company’s activity. For example, the investor may convince the company’s management to recycle old solar panels, increasing the carbon emissions avoided per panel by 10%. Again, the company’s impact will increase by 10%, yielding an investor impact of 3,000 tons of avoided carbon emissions—simply by alternative means.

To illustrate how this example could be applied in practice, one might consider using a company’s ESG practices as a proxy for q and a company’s size as a proxy for Ac. Positive investor impact could be achieved by either improving the company’s ESG practices or by increasing the company’s size, provided that its ESG practices are above average.

Mechanisms of Investor Impact

There are various mechanisms of investor impact. In order to ensure that our review covers all the relevant mechanisms, we conducted a series of interviews with experts from the SI industry. Specifically, we asked industry experts for anecdotal evidence of when their activities or the activities of their organizations have triggered change at companies. In addition, we shared and obtained feedback on earlier versions of this article from asset managers, asset owners, and regulators in Switzerland and the United States during conferences and workshops. We focused on mechanisms that are available to investors alone, excluding mechanisms that are also available to other actors. For example, investors may have an influence by lobbying regulators. However, examining the impacts of lobbying activity would broaden the scope of this article far beyond investor impact.

Through these exchanges with industry experts and regulators, we identified three fundamental mechanisms of investor impact, as shown in Figure 1. Shareholder engagement refers to shareholder activities that are intended to change companies’ ESG practices, often referred to as “voice” (Hirschmann, 1970 ). These include the right to vote on shareholder proposals during annual general meetings, discussions during informal meetings with management, and criticizing corporate practices in news outlets, as well as threats of selling the companies’ assets (see, e.g., Admati & Pfleiderer, 2009; Amel-Zadeh & Serafeim, 2018; McCahery et al., 2016). Capital allocation refers to the investor activity of allocating capital to particular financial assets. Investors may either buy a company’s financial assets, implicitly backing the company with their capital, or sell a company’s financial assets, denying the company such backing. The latter is commonly referred to as “exit” (Hirschmann, 1970). Indirect impacts include a range of impact mechanisms where investor activities do not directly affect company activities, but where instead the activity of investors influences a third party, which in turn affects company activities. Stigmatization refers to an investor tainting a company’s image in public; endorsement refers to an investor endorsing and promoting a company’s sustainability performance; benchmarking refers to rating agencies measuring and benchmarking a company’s ESG performance; and demonstration refers to investors encouraging other investors to follow their lead.

Scope of the Literature Review

The scope of the review includes scholarly work that addresses the identified mechanisms of investor impact. For each mechanism, we queried academic databases with keywords describing the investor impact mechanisms, yielding an initial body of literature. We then extended the range of keywords by searching for central concepts and keywords drawn from the body of literature already identified. For example, the concept of “stock price elasticity” was identified as an important theoretical basis for capital allocation, leading us to include a body of literature dealing with stock price elasticity in our review. This approach ensured that we could identify all contributions that are important for the identified mechanisms, even if they use different terms to describe the mechanisms, or deal only with particular aspects of the mechanisms.

Using this approach, we identified a total of 64 relevant contributions from a range of different disciplines. Capital allocation is dealt with mostly in the financial economics literature, specifically asset pricing and corporate finance. Shareholder engagement is dealt with mostly in the corporate governance literature, as well as in management science. Indirect impacts are dealt with primarily in business ethics, management science, and sociology. We analyze this body of literature to assess the empirical evidence for each mechanism as well as known determinants affecting the effectiveness of the mechanisms.

Literature Review

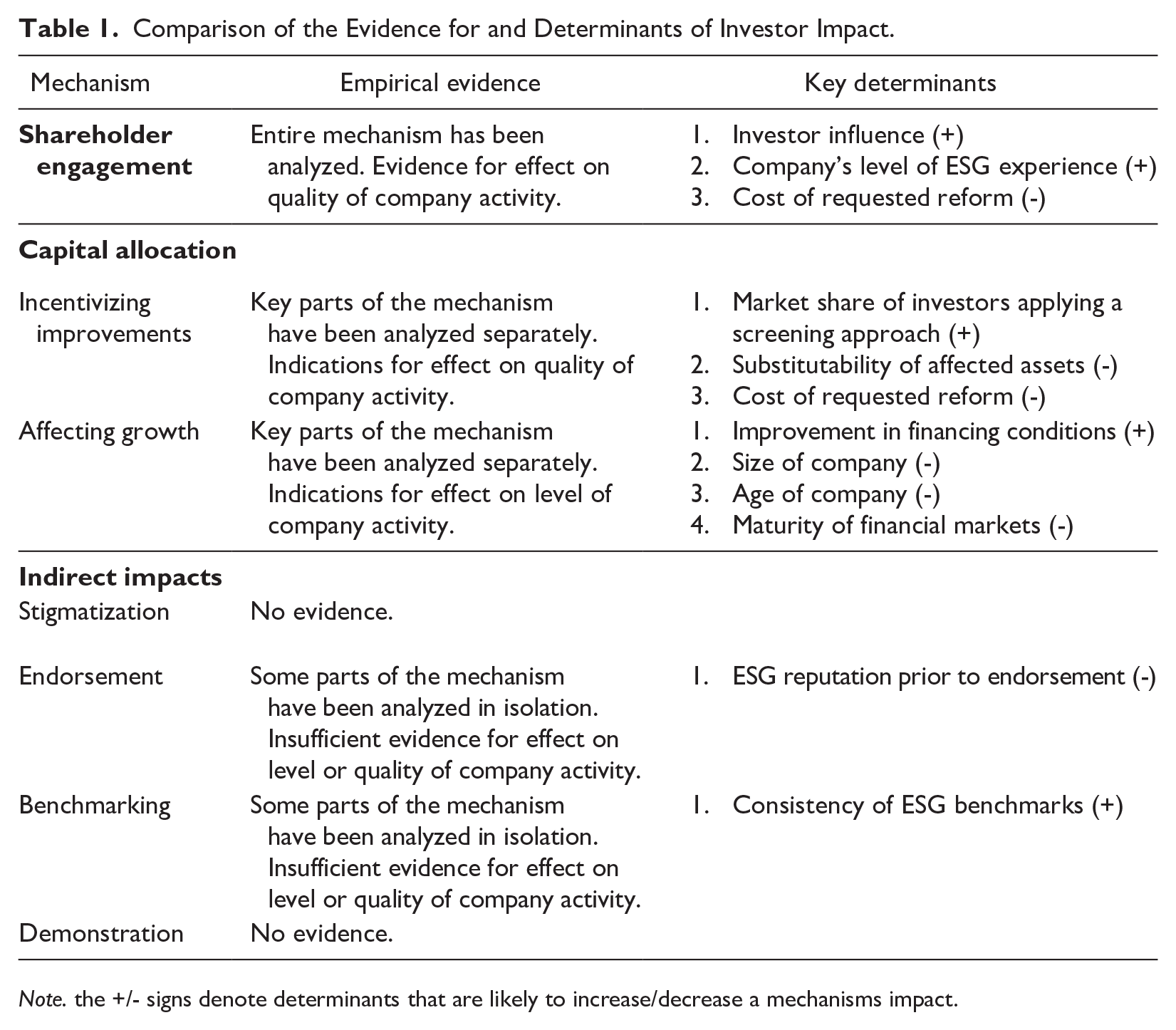

Table 1 provides a comparison of the level of empirical evidence for the mechanisms of investor impact, as well as the known determinants that are likely to influence the mechanisms’ effectiveness. Determinants that have a positive influence on effectiveness are denoted with a plus sign, those with a negative influence with a minus sign.

Comparison of the Evidence for and Determinants of Investor Impact.

Note. the +/- signs denote determinants that are likely to increase/decrease a mechanisms impact.

Shareholder Engagement

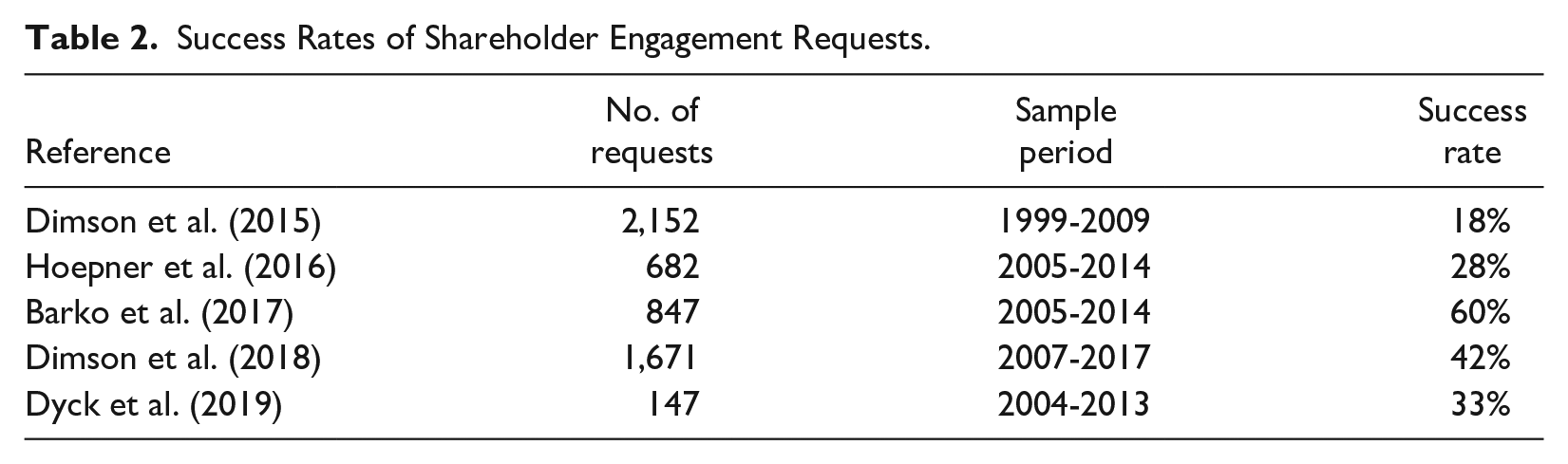

Active engagement of shareholders may cause companies to improve the quality of their activities. There are five empirical studies that analyze the extent to which companies comply with shareholder engagement requests (Barko et al., 2017; Dimson et al., 2015, 2018; Dyck et al., 2019; Hoepner et al., 2016). The key results of these studies are summarized in Table 2. Taking different approaches and relying on different data, each study reports the success rate of a given number of shareholder engagement requests as part of its analysis. The results show that while shareholder engagement requests do not always succeed, there is a reasonable probability that they do, ranging from 18% to 60%.

Success Rates of Shareholder Engagement Requests.

Going into more detail, Barko et al. (2017) and Dyck et al. (2019) show that shareholder proposals are associated with subsequent increases in the ESG ratings of targeted companies. This is evidence that shareholder engagement can lead to changes in company activities that are detectable in data from sources other than engagement service providers themselves. Together, these studies provide strong evidence that shareholder engagement is an effective mechanism through which investors can trigger reforms that improve the quality of company activities.

The success rate of shareholder engagements depends on a host of determinants related to characteristics of the engagement request, the company engaged, the investor engaging, and the specific process of engagement (Goranova & Ryan, 2014). The studies cited above highlight three specific determinants that have an important influence on the average rate of success.

The first determinant is the cost of the reform that is associated with complying with the engagement request. A consistent finding of the reviewed studies is that requests in the environmental domain tend to have lower success rates compared with requests in the social domain, and that requests in the corporate governance domain have the highest rate of success. Dimson et al. (2015) attribute this to the fact that reforms in the environmental domain are likely to be costlier than those in the governance domain. More explicitly, Barko et al. (2017) show that requests that require some form of costly reorganization have lower success rates compared with requests that entail lower costs. Taken together, these findings indicate that the chances of success decrease as the costs of the requested reform rise.

The second determinant is investor influence. There is evidence that engagement requests are more likely to succeed when the shareholder engaging holds a larger share of the targeted company (Dimson et al., 2015, 2018). However, it is not only the presence of larger holdings that causes investor influence to increase. Dimson et al. (2018) find that a group of investors engaging has more influence when the engagement is spearheaded by an investor who is from the same country as the company being engaged, suggesting that linguistic and cultural elements may play a role as well. Additionally, the chances of success rise when asset managers that are large and internationally renowned are part of the group of investors engaging.

The third determinant is the company’s level of ESG experience. The success rate of engagement is higher with companies that have previously complied with engagement requests (Barko et al., 2017; Dimson et al., 2015). Furthermore, companies that had high ESG ratings prior to the engagement are more likely to comply with engagement requests (Barko et al., 2017).

Capital Allocation

While the impact of capital allocation on company activities may seem intuitive at first glance, it touches upon a rather fundamental question—namely, to what extent the decisions of investors influence the course of the real economy (see, e.g., Morck et al., 1989). From the reviewed literature, we identify two mechanisms governing how the capital allocation of sustainable investors may influence company impact: First by creating incentives to improve ESG practices and therefore the quality of company activities, and second by affecting growth and therefore the level of company activities. In the following, we review the available literature for each of these two mechanisms.

Incentivizing Improvements

Sustainable investors may shift asset prices by applying screening approaches. There are several different screening approaches in practice, including negative screening (excluding certain harmful industries), norm-based screening (excluding companies that do not adhere to widely accepted norms of business conduct), as well as best-in-class screening (allocating capital to companies that have the best ESG performance relative to their industry peers). ESG integration, where investors consider ESG metrics as part of the investment analysis, can be can regarded as a rather complex screening approach, which eventually results in some companies being over- or underweighted or excluded from the investment portfolio. All approaches have in common that they result in a portfolio allocation that differs from the market portfolio. Through this deviation, investors may create incentives for companies that do not fulfill inclusion criteria to enact reforms. Thus, investors may be able to trigger changes in ESG practices through screening approaches. However, there is no empirical evidence that explicitly links sustainable investors’ screening approaches to changes in ESG practices. There is some evidence that screening approaches affect asset prices, and theoretical models that predict an effect on ESG practices. There remains, however, considerable uncertainty as to whether the model assumptions hold in practice.

Several theoretical studies have modelled the consequences of screening approaches for asset prices. In their equilibrium model, Heinkel et al. (2001) argue that sustainability preferences of investors can influence asset prices. This is in line with findings of Fama and French (2007) as well as those of Luo and Balvers (2017), both pairs of authors showing—based on standard asset pricing models—that preference-neutral investors require a premium for balancing out the portfolio choices of investors who share a particular nonfinancial preference because this forces the preference–neutral investors to deviate from the market portfolio. Furthermore, Heinkel et al. (2001) predict that if the decrease in the stock prices of firms that do not conform to the requirements of sustainable investors’ screening approaches is significant enough, these firms will start to implement the reforms demanded by sustainable investors. This is in accordance with Edmans et al. (2012), who argue that when managerial incentives are tied to stock market value, managers will be sensitive to nonfundamental shifts in the share price of their corporation. Regarding the proportion of investors that needs to apply a screening approach in order to trigger corporate improvements, Heinkel et al. (2001) provide a numerical example in which at least 20% of investors need to apply a common screening approach to create the incentive for a company to implement reforms that cost 5% of its annual cash flow.

Similarly, the equilibrium model of Gollier and Pouget (2014) shows that by “voting with their feet”—that is, by consistently divesting from companies that do not fulfill certain criteria—investors can lower asset prices for these companies and with that incentivize firms to invest in order to fulfill these criteria. Based on the findings of the Stern Review (Stern, 2008), Gollier and Pouget (2014) estimate that 8% of investors applying the same screening approach is required to incentivize the investments in the new technologies required to mitigate climate change. However, both the quantitative estimates of Gollier and Pouget (2014) and those of Heinkel et al. (2001) must be considered with caution as they depend strongly on stylized assumptions. As a result, it remains unclear what share of SI investors is required to cause movements in asset prices sufficiently large to incentivize meaningful improvements.

A series of studies provide empirical evidence that screening approaches of sustainable investors can affect asset prices in stock and bond markets, as well as in markets for venture capital and private equity. The reviewed studies differ substantially, however, in terms of the reported effect size.

Two empirical studies that investigate sustainability preferences in stock markets come to opposing conclusions regarding the effect on share prices. Hong and Kacperczyk (2009) examine the effect of investors excluding “sin stocks,” such as tobacco, alcohol, and gambling, from their portfolios. They show that sin stocks have depressed prices and exhibit outperformance of 2.5% per year, relative to comparable stocks. This result implies that the moral aversion of investors for sin-stock companies has decreased the stock prices of these companies. At the same time, a related study focusing on the effects of divestment in the context of the South Africa boycotts in the 1980s concludes that these divestments had no discernible effects on asset prices (Teoh et al., 1999).

Recent studies on green bonds—that is, bonds that are issued to finance projects with environmental benefits—indicate that the sustainability preferences of investors can influence bond prices. Baker et al. (2018) find that at issue, the yields of green bonds are on average 0.06% below the yields of comparable bonds. They present supporting evidence that the observed differences are caused by nonfinancial preferences of investors. Similarly, Zerbib (2019) shows that sustainability preferences of investors result in a negative yield premium of 0.02% for green bonds. Hachenberg and Schiereck (2018) too, confirm that green bonds are traded with a negative yield premium, while Tang and Zhang (2018) do not find evidence of such a premium.

Studies on the role of demand in public equity markets confirm that shifts in investor demand can influence stock prices, even when fundamental values remain unchanged. A large set of studies makes use of the fact that, due to passive investors, the inclusion or exclusion of companies in or from popular indexes, such as the S&P 500 index, triggers substantial investments in or divestments from these firms (Beneish & Wahley, 1996; Chang et al., 2015; Kaul et al., 2000; Lynch & Mendenhall, 1997; Shleifer, 1986; Wurgler & Zhuravskaya, 2002). All in all, these studies find that the observed sudden changes in demand do affect stock prices. Studies that make use of order books (Ahern, 2014), announcements of equity issues (Loderer et al., 1991), or auction repurchases (Bagwell, 1992) come to similar conclusions.

There is, however, no consensus on how strongly changes in demand affect share prices. A useful measure for the influence of demand on prices is the price elasticity of demand. 2 Highly negative elasticity values indicate little influence of changes in demand, whereas less negative values indicate a stronger influence of demand on prices. The results presented by Loderer et al. (1991), Kaul et al. (2000), and Wurgler and Zhuravskaya (2002), as well as Ahern (2014), indicate elasticities of around -5 to -10. The studies by Bagwell (1992), Chang et al. (2015), and Shleifer (1986) indicate lower elasticities, of between -1 and -1.5.

Only a few studies investigate demand effects in private markets such as markets for private equity and venture capital. Gompers and Lerner (2000) show that a doubling of inflows of capital increases the valuation of new investments of venture capital funds by between 7% and 21%, corresponding to an elasticity of -5 to -14. This is in line with the findings of Diller and Kaserer (2009), who find that demand effects influence private equity funds’ returns.

Taken together, the literature provides evidence that the capital allocation of sustainable investors can affect asset prices. However, it leaves open two important questions. First, there is no agreement on the size of the effect sustainable investors have on asset prices, making it difficult to judge whether the effect is material. Second, while there is evidence that the capital allocation of sustainable investors has affected asset prices in some cases, there is so far no evidence that such changes in asset prices have translated into changes in ESG practices. Nevertheless, the literature reviewed above highlights three specific determinants that increase the likelihood that sustainable investors’ screening approaches lead to improvements in the quality of companies’ activities.

First, the effect of an investor’s screening approach is likely to be higher if a large proportion of investors apply the same approach. The equilibrium models of Heinkel et al. (2001), Fama and French (2007), Gollier and Pouget (2014), and Luo and Balvers (2017) indicate that the total effect of screening approaches on asset prices, as well as the marginal effect per additional dollar involved, increases with the fraction of wealth commanded by investors that apply the same screening approach. Hence, the effect of an individual investor’s decisions depends on how many other investors apply the same screening approach.

Second, the effect of investors’ screening approaches is likely to be higher for companies whose assets are not easily substitutable. The models of Heinkel et al. (2001) and Fama and French (2007) show that the capital allocation of sustainable investors has a stronger effect on the prices of assets whose returns are only weakly correlated with the market portfolio—that is, assets that are not easily substitutable. Counterbalancing sustainable investors’ demand for these assets requires a higher deviation from an optimally diversified portfolio from neutral investors than is the case for stocks that have very close substitutes. Accordingly, both Wurgler and Zhuravskaya (2002) and Ahern (2014) find empirical evidence that stocks with low substitutability exhibit a lower price elasticity.

Third, a screening approach is more likely to cause companies to improve their ESG practices if the costs for a company to implement the reforms required to conform to the requirements embodied in the screening are low. The models of Heinkel et al. (2001) and Gollier and Pouget (2014) point out that whether changes in asset prices induced by SI provide an incentive for companies to improve their ESG practices depends on the cost of the necessary reforms.

Affecting Growth

The capital allocation of sustainable investors may also affect the growth of companies by changing the financing conditions these companies face. In this way, sustainable investors may be able to alter the levels of activity of particularly sustainable or unsustainable companies. The literature studies two ways in which investors can change financing conditions for companies and highlights that the impact depends on further characteristics, such as company size, company age, and market maturity.

A direct way in which sustainable investors may enhance a company’s financing conditions is by providing capital on concessionary terms. Subsidizing companies that are deemed beneficial for development by providing them with financing more attractive than that available at market conditions is widely practiced by development finance institutions and other public sector actors and has been shown to enhance corporate investment (see, e.g., Cravo & Piza, 2016; Kersten et al., 2017; Yaron & Schreiner, 2001). Brest and Born (2013) and Brest et al. (2018), as well as Chowdhry et al. (2019), argue that private investors too can promote sustainable companies by providing them with capital on concessionary terms—that is, with better conditions than these companies would obtain from preference-neutral investors. 3

A more indirect way for sustainable investors to alter financing conditions is by affecting the prices of a company’s financial assets for the entire market. As discussed in the previous section, the capital allocation of sustainable investors can affect asset prices under specific conditions, most notably the condition that sustainable investors represent a substantial market share. In this way, capital allocation may not only create managerial incentives to change but also change the cost at which affected companies raise capital from other investors (see, e.g., Fischer & Merton, 1984). In an equilibrium model, Beltratti (2005) shows that if investors underweight unsustainable companies, this can increase the cost of capital for these companies, reduce their investment activity, and thus decrease their market share. 4 However, while effects of capital allocation on asset prices and the cost of capital are supported in the empirical literature, associated changes in growth are not.

Regardless of how investors alter a company’s financing conditions, the literature points to several company characteristics that determine whether a change in financing conditions translates into accelerated growth of company activities. A nonfundamental movement in stock prices, such as the one created by the demand of sustainable investors, only translates into corporate investment activity when the company depends on external capital to finance these investments (Baker et al., 2003).

For seasoned publicly listed companies, stock prices seem not to have a substantial effect on corporate investment activity (Blanchard et al., 1993; Morck et al., 1989). Accordingly, Hadlock and Pierce (2010) find that financing constraints decrease with increasing size and age of companies. While a number of studies show that large companies with good ESG ratings enjoy a lower cost of capital (e.g., Chava, 2014 ), it is ambiguous whether this is due to investor demand—and, thus, an investor impact—or to the superior risk characteristics of those companies.

In contrast, a series of empirical studies show that small firms and young firms as well as firms operating in less mature financial markets with weak institutions are more likely to be restricted in terms of their growth by the cost of external financing (Beck et al., 2006; Beck et al., 2008; Bloom et al., 2010; Rajan & Zingales, 1996). Especially in developing countries, many small- and medium-sized companies lack any access to external financing (Beck & Demirguc-Kunt, 2006). The finding that many small firms are restricted by the cost of capital or even access to capital is consistent with the finding that most small companies use retained earnings, insider finance, and trade credit to finance their investments (Berger & Udell, 1998; Carpenter & Petersen, 2002). Financing constraints seem to have a particularly strong inhibiting effect on entrepreneurial activities. Evans and Jovanovic (1989), as well as Holtz-Eakin et al. (1994), show that wealthy individuals are much more likely to become successful entrepreneurs.

Taken together, there is only partial empirical evidence that capital allocation by sustainable investors can enhance the growth of sustainable companies. Nevertheless, the literature points to determinants on which such an impact likely depends. The first determinant is whether the investor changes the company’s financing conditions, either by lowering the cost of capital or improving access to finance. Additional determinants arise from the fact that a change in financing conditions only affects the level of company activity when the company’s growth is constrained by external financing conditions. Company size and age and the maturity of the financial market in which the company’s financial assets are traded all tend to reduce the degree to which growth is constrained in this way. Thus, capital allocation is more likely to affect growth for young, small firms in immature markets than for large, established firms in mature financial markets.

Indirect Impacts

Stigmatization

Investors can stigmatize a company by divesting that company’s assets or categorically excluding it from their portfolio. Apart from the impact through capital allocation this might have, the action can also impact other relevant stakeholders of the company. For example, people might be deterred from working at a company that is excluded by investors. Literature on the impact of such stigmatization, however, is thin. In a detailed assessment of the carbon divestment movement, Ansar et al. (2013) postulate that one of its most important impacts might be the stigmatization of the fossil fuel industry. For the antiapartheid divestment campaign, there is anecdotal evidence that the campaign helped elevate the issue of apartheid on the political agenda. Desmond Tutu, South African archbishop and an important figure in the struggle against the apartheid regime, commented that the disinvestment campaign in the United States added punch to the political struggle (Knight, 1990). However, we were not able to find studies that analyze to what extent exclusion decisions made by sustainable investors have led to stigmatization.

Endorsement

Investors can endorse companies for their social or environmental performance by including them in their portfolio or sustainability index. Such endorsement may help increase the visibility and improve the reputation of a company, indirectly helping it gain customers or motivate employees. We were not able to identify studies that analyze to what extent company reputation and sales were improved as a consequence of investor endorsement. There are two studies, however, that investigate whether companies that were included in a sustainability index decided subsequently to communicate their inclusion to stakeholders (Carlos & Lewis, 2018; Searcy & Elkhawas, 2012). The fact that companies communicate index inclusion suggests that such inclusion helps improve reputation. The studies show, however, that nearly half of the companies that were included in the Dow Jones Sustainability Index chose not to communicate their inclusion publicly. Carlos and Lewis (2018) find that companies are more likely to remain silent about their index membership when they have a strong reputation for ESG performance already. Thus, one important determinant of the endorsement effect seems to be a company’s prior ESG reputation.

Benchmarking

SI is feeding a growing industry of ESG rating agencies (Eccles & Stroehle, 2018). These rating agencies develop standards, create ESG benchmarks, and request increasing amounts of data from companies. The growth of this industry may encourage companies to report on their ESG practices in order to satisfy these increasing demands for data. Measuring and reporting may, then, also induce companies to improve their performance, for example, because companies are benchmarked against peers, or simply because measuring ESG performance indicators also enables companies to manage their ESG performance.

The literature provides no evidence of investors’ indirect impact exercised via their support for ESG rating agencies. This because even though it is fairly obvious that ESG rating agencies exist due to demand from sustainable investors, it is not clear whether additional investors buying or using ESG ratings will further strengthen the impact of these agencies’ benchmarking activities.

However, a number of studies have investigated the direct impact of ESG ratings and ESG reporting standards on companies’ social and environmental performance. Regarding standards, one study concludes that the introduction of the voluntary ISO 14000 standard for environmental management has led firms to improve their environmental outcomes (Melnyk et al., 2003). Another study, however, concludes that the adoption of this standard had no discernible effect on environmental outcomes (Hertin et al., 2008). Thus, the mere existence of ESG standards may not suffice to improve outcomes, even though it must be borne in mind that ISO 14000 is just one of many different standards in the ESG domain.

Studying ESG ratings, Chatterji and Toffel (2010) provide evidence that companies improve environmental performance in response to receiving a low ranking in an environmental benchmark. They find this to be especially the case when the cost of the necessary reforms is low, and when the company operates in a highly regulated industry. A problem with this effect, however, is that there are remarkable differences between the ESG benchmarks compiled by different agencies (Chatterji et al., 2016). Due to these differences, Chatterji et al. (2016, p. 1609) conclude that “SRI ratings will have a limited impact on driving rated firms toward any particular shared behaviors.” One determinant of the effectiveness of the impact of benchmarking is thus the consistency of ESG benchmarks—the more consistent ESG benchmarks are, the greater is their effect on company activities.

Demonstration

Besides affecting companies’ impact through their own activity, SI investors may also encourage other investors to do the same. We identify two mechanisms via which sustainable investors may be able to do so.

First, sustainable investors may help establish SI as a social norm (see, e.g., Cialdini & Trost, 1998). Research on charitable giving has shown that potential donors are more likely to give if they learn that others give as well (DellaVigna et al., 2012; Frey & Meier, 2004; Shang & Croson, 2009). Whether this mechanism applies in the context of SI, however, has not been investigated.

Second, investors pioneering novel investment projects, for example, financing pioneering renewable energy projects in a developing country, may increase the subsequent flow of capital into such projects. For example, Egli et al. (2018) show that learning and associated efficiency gains within the renewable energy finance industry have reduced the cost of capital for renewable energy projects over time. Geddes et al. (2018) argue that enabling financial sector learning is an important way in which development banks encourage private investments in low-carbon energy generation. Thus, early investors in novel approaches or markets may have an impact not only through their own investment but also through subsequent investments that they facilitate. Since in these cases investors are one player in an evolving ecosystem involving technology providers, service providers, and regulators, it is very difficult to separate investor impact from contemporaneous factors.

Discussion

Table 1 provides an overview of the reviewed mechanisms of investor impact. Shareholder engagement emerges as most reliable in the sense that an effect of investor activity on company activity has been demonstrated empirically. Several studies show that shareholder engagement can lead to measurable improvements in companies’ ESG practices. The impact of shareholder engagement increases with the influence of the investor engaging and the ESG experience of the company engaged. It decreases as the cost of the requested reforms rises, meaning that shareholder engagement is more likely to trigger incremental improvements rather than transformative change.

Capital allocation has not been studied in its entirety, but important parts of the mechanism are empirically demonstrated, both for incentivizing improvements and for affecting growth. Capital allocation emerges from the literature review as a somewhat less reliable mechanism since we found no study that establishes a direct link between capital allocation by SI investors and a change in company activities. However, key parts of the mechanism have been studied and the results indicate that capital allocation could bring about investor impact in two different ways.

First, screening approaches may incentivize companies to adapt their practices. There is evidence that screening can affect asset prices; there is, however, no evidence to date that such a change in asset prices has indeed led companies to improve the quality of their activities. The likelihood that screening approaches have such an effect increases with the market share of the investors applying the same screening approach, and decreases with the substitutability of the securities that are excluded. A further determinant is the cost of the reform that is required if a company is to evade the screen.

Second, investing in sustainable companies may increase the level of company activity. There is evidence that improved financing conditions can accelerate a firm’s growth, but only when financing is a limiting factor. The likelihood of this impact increases with the improvement in financing conditions that the investor provides to the company compared with the status quo. It decreases with the age and size of the company, as well as with the maturity of the financial market in which the company’s financial assets are traded.

Indirect impacts are mostly unproven due to a lack of empirical studies that indicate their effectiveness. While there is anecdotal evidence for indirect impacts, none of the indirect impact mechanisms has been analyzed comprehensively—in the sense that investor activities have been related to a change in company activities. There is no empirical evidence for the effects of stigmatization and demonstration. There is some empirical evidence, however, for endorsement and benchmarking, yet it covers only part of the mechanisms, so that the extent of investor impact remains a matter for speculation. In terms of determinants, there are indications that an investor’s endorsement is more valuable when the endorsed company has a poor prior ESG reputation. Benchmarking would likely be more effective were different ESG benchmarks consistent—that is, if they identified the same laggards and leaders. It is important to note that a lack of evidence for indirect impacts does not imply that indirect impacts are irrelevant. Indirect impacts could be important under the right circumstances, but so far the academic literature does not provide evidence for their effectiveness.

Applying these findings to today’s US$ 30 billion market for SI (GSIA, 2018) suggests that the bulk of SI assets are invested in ways that promise rather modest and perhaps even negligible investor impact. Shareholder engagement, identified as the most reliable mechanism, is practiced for only 18% 5 of global SI assets, and for a mere 10% in the United States. About 50% of assets are invested in screening approaches, and 32% rely on ESG integration. However, there is a lot of diversity in the screening approaches, and there is inconsistency between different ESG ratings. This diversity means that even though the combined market share of these approaches is substantial, the effective market shares behind specific approaches are small. This dilutes any effect on asset prices and with it the incentives for companies to implement reforms. In addition, some of the most popular screening approaches exclude industries rather than practices, meaning that companies in affected industries are barely incentivized to improve at all as even if they were to improve, they would not have the opportunity to conform to the investment screen.

According to GSIA (2018), a mere 1% of global SI assets is invested in so-called impact investing, where accelerating the growth of sustainable companies is a key objective. Such investments often include concessions to the investee, and are placed in companies that have limited access to financing. Other SI approaches may also have an impact on the growth of sustainable companies; this is, however, less likely due to the fact that over 80% of SI assets are invested in publicly listed firms, where financing is usually a less important constraint for growth.

In addition, SI may have indirect impacts. For example, it may be that the fossil fuel divestment campaign stirs political and societal debate around fossil fuel consumption, and perhaps ultimately leads to less fossil fuel consumption. Similarly, it may be that ESG ratings drive companies to implement more ESG practices. Most promising, perhaps, demonstrating the feasibility of investments in novel approaches or technologies may trigger subsequent investments. So far, though, there is no empirical evidence that investor activity is actually driving such developments.

Implications

Taken together, our results suggest that the investor impact of SI as it is practiced today is rather modest. At the same time, they hold a number of implications for investors, rating agencies, and policy makers with regard to how investor impact can be increased.

For Investors

First, investors who want to stimulate real-world impact can roll out shareholder engagement throughout their portfolio. Ideally, investors should focus on requests that have a good chance of success and yield substantial improvements in company impact. In addition, investors can pool their shareholder rights with like-minded investors to increase their influence, and outsource the engagement mandate to specialized firms.

Second, investors can allocate capital to companies with a positive company impact that are constrained in terms of their growth by external financing conditions. While financing constraints are less likely for large, well-established companies, many small and young companies are constrained by external financing conditions, especially in less mature financial markets—for example, in developing countries. By easing the financing constraints of such companies, investors can support the growth of sustainable businesses.

Third, investors can screen out investments based on the absence of ESG practices, focusing on a few specific and transparently communicated practices. The most promising practices can be implemented by companies at a low cost and result in substantial improvements in company impact. The incentives for companies to adopt the demanded ESG practices increase with the share of investors applying the same screening approach. Hence, screening approaches should be pursued in a large coalition of investors and encompass stocks and bonds. The way in which the Institutional Investor Coalition on Climate Change communicates its members’ expectations for specific sectors may constitute a step in this direction.

Fourth, investors who are convinced that they can have indirect impacts should attempt to demonstrate them. SI funds could provide examples or look at intermediate proxies that make indirect impacts more tangible. For instance, investors could measure the level and the tone of media attention in response to an exclusion announcement as a proxy for stigmatization. Similarly, fund managers who launch an innovative product could track the uptake of their innovation as a proxy for demonstration.

For Rating Agencies

Rating agencies and ESG data providers could play an important role in changing the SI industry by developing investor impact metrics. Lately, several ESG data providers have released company impact metrics, which is an important step towards understanding better how company activity can support the achievement of the SDGs. However, these metrics are often used to indicate the impact an investor has when investing in a certain fund, which is misleading. For example, a fund that holds companies that have implemented best practices regarding their greenhouse gas emissions would receive a top rating based on company impact metrics. However, a fund that holds companies with mediocre practices and drives them to upgrade these practices would receive only a mediocre rating.

Investor impact metrics should reflect the temporal change in company impact that investors can expect to cause. There is some activity in this direction, 6 and the need for investor impact metrics is also recognized by regulators. This article provides an overview of the mechanisms and determinants of investor impact and thus provides a blueprint on how investor impact metrics might look.

For Policy Makers

Policy makers should be aware that without additional policy measures SI is unlikely to result in the dramatic transformation that is required, for example, for the decarbonization of the economy. SI seems to be well suited to diffusing ESG practices throughout industries, ensuring that all low-hanging fruit are harvested. SI can also support innovation by promoting the growth of young and small sustainable businesses. Yet more fundamental changes also require policies that directly change the viability of economic activities, such as taxes on pollution or minimum standards. Rather than making such policies unnecessary, SI may be a suitable complement in that it incentivizes companies to adopt ESG practices and explore business models made viable by these policies.

There can be a positive feedback loop by which regulators enact policies that make certain ESG practices superior in terms of financial performance and investors encourage ESG practices that anticipate future regulation. Many SI proponents argue that material ESG aspects, where doing good coincides with superior returns, will drive positive change. However, materiality ultimately rests on the argument that ESG practices result in superior financial performance, which often depends on policy. For example, investment in water-saving technology is not a “material ESG practice” in a situation where water tariffs are too low to justify the investment. But it can become material once regulators begin to raise tariffs to appropriate levels.

Limitations

We acknowledge that investors may have a variety of motivations to engage in SI, and that the motivation to make an impact may not be important for all SI investors. For example, investors may have a desire to be morally aligned with their portfolio. If so, excluding certain industries that are perceived as “dirty” may be perfectly consistent with an investor’s motivation, even if it has no impact on the excluded industries (see, e.g., Haidt, 2007). Other investors may engage in SI out of a financial motivation—expecting less risk for example. If so, integrating certain ESG factors into investment decisions is perfectly consistent with that motivation (see, e.g., Friede et al., 2015). In both of these cases, investor impact is irrelevant to investor motivation. However, we argue that from a societal perspective investor impact is the essential feature of SI. If SI does not make a difference, policy makers would have no reason to foster it, and academics would have little reason to study it.

This review is limited to published academic results, which may not fully capture all relevant aspects of investor impact. The academic literature is biased toward publicly listed corporations and stock markets, due to data availability. Accordingly, this literature review is also somewhat biased toward public stock markets. And there are, potentially, further relevant impact mechanisms in specific financial markets—such as corporate debt, private equity, bank lending, and real estate—which are not reflected here. Also, aspects that are difficult to measure or are currently unfolding may not be represented appropriately. For example, there are increasing numbers of alliances of asset owners promoting sustainable finance, such as the Investor Coalition on Climate Change. The effects of these alliances have not yet been researched. Also, novel ideas such as blended finance, where private and public investors combine funds, may bring about significant investor impact, but have not yet been researched. Thus, a key limitation of this study is that there may be important investor impact mechanisms that have not yet been covered by academic research.

Future Research

This article concludes that shareholder engagement is a promising way to ensure investor impact. An important question that remains, however, is how to quantify the impact of engagement activities in a comparable way. Existing studies have quantified the success rate of engagement requests, but it is also necessary to quantify how substantial an engagement request is (Barko et al., 2017). One substantial request may have a greater impact than several superficial requests. Combining the aforementioned success rate with a measure of how substantial a request is could yield a comparable measure. Such a standard for reporting the impacts of engagement activities could make shareholder engagements comparable and also more visible and marketable.

Regarding the impact of capital allocation, one critical knowledge gap is that there is currently no empirical study that relates capital allocation decisions made by sustainable investors to corporate growth or to improvements in corporate practices. Hong and Kacperczyk (2009) point out that while their study demonstrates an effect on the share prices of tobacco companies, it does not investigate the effects on the activities of tobacco companies. Studies that not only relate SI to asset prices but also investigate the response of affected companies in terms of management and investment decisions would advance understanding of investor impact decisively. Such studies would be a first essential step toward developing a metric for the impact of capital allocation.

Regarding indirect impacts, there is a need for studies that either investigate the entire causal chain of indirect impacts or inform critical pieces that are currently missing. It would be valuable to conduct, for example, a case study of the Fossil Free divestment campaign, to establish the consequences of the campaign in terms of media attention, investor behavior, and corporate decisions, as well as to relate it to broader economic, political, and cultural dynamics around the fossil fuel industry. Such a study would close important gaps in the scientific understanding of the investor impact of stigmatization and would provide guidance as to how and when to pursue it.

Conclusion

SI is increasingly thought of as a mechanism for achieving societal goals such as the United Nation’s SDGs. We observe, however, that both in research and practice the notion of investor impact is neglected, and conduct a literature review on the mechanisms of investor impact. We conclude that shareholder engagement is a relatively reliable mechanism. Capital allocation can either accelerate the growth of companies, or incentivize companies to implement ESG practices, but there remain gaps in the evidence. Indirect impacts remain unproven regarding their effectiveness. Our results suggest that the current practice of SI has only a modest investor impact, and call for the development of investor impact metrics that reflect the contribution of SI to societal goals.

Footnotes

Acknowledgements

We thank James Gifford, Jonathan Krakow, Vincent Wolf, Alex Barkawi, Britta Rendlen, Emilio Marti, Raj Thamoteram, Tillmann Lang, Julia Meyer, David Wood, Florian Berg, Ola Mahmoud, Bert Scholtens, and Paul Smeets for valuable input and discussions. We would also like to thank participants of the Luc Hoffmann Institute workshop “Shareholder Activism for Sustainability” on May 28, 2018, and of the Yale Initiative on Sustainable Finance Symposium 2018.

Authors’ Note

The first two authors contributed equally.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge financial support from the BMW Foundation Herbert Quandt, the Luc Hoffmann Institute, and the European Union’s EIT Climate KIC under the SGA2019.