Abstract

The predominant view of the role of business in society is that the objective of business is to maximize profit. Some argue that it ought to be something different. Others argue that for many firms it already is something different. However, the “something different” has not been fully fleshed out in its various versions. To address this gap, we define different relationship types between variables in an objective function and develop and present the resulting range of 10 alternative objective functions for firms. We then discuss how their development contributes to conceptual, empirical, and normative debates about organizational purpose. Removing the conventional assumption of profit maximization as the sole management principle opens up the possibility of new, more nuanced theoretical approaches to management. This article lays the groundwork for such theory development through the systematic and analytical identification of alternative objective functions that represent different specifications of firm purpose.

Keywords

Introduction

The question about the role of business in society may be as old as the field of management itself. Economic theory suggests that the objective of firms is to maximize profit in order to create wealth for owners. 1 Currently the dominant perspective on the objective of corporate activities (Jones & Felps, 2013a), this view is strongly institutionalized: It is a powerful social norm among managers (Rose, 2007; Smith & Rönnegard, 2016), it permeates management education (Galbreath, 2006), and it is even legislated in some countries. 2 The profit maximization requirement is grounded in welfare economics and utilitarian moral philosophy—welfare of society is said to be maximized when firms maximize their profit (Jones & Felps, 2013b; Windsor, 2006).

Some, however, argue that the objective of business ought to be something other than profit maximization, calling the view of profit maximization as the sole business objective into question by arguments based in the very theory from which it was developed (see Jones & Felps, 2013b, for a detailed utilitarian critique of the presumed existence of a link between shareholder wealth maximization and social welfare). That profit maximization leads to social welfare maximization—the “invisible hand” argument of Adam Smith—rests on “untenable assumptions” which have gone largely unnoticed in management theory (see Donna Wood in Agle et al., 2008, p. 159). These assumptions are of course not unknown to economic theorists. Jensen (2002, p. 239) admits that “[w]hen monopolies or externalities exist, the value-maximizing criterion does not maximize social welfare.” The theoretical response of economics to the question of externalities and monopolies, however, is optimal government intervention, not firms undertaking other objectives besides profit maximization (Jensen, 2002).

Economics as a social science is primarily concerned with efficiency and remains relatively silent on equity considerations such as distributional impacts. Accordingly, the claim that profit maximization leads to social welfare maximization rests not on the Pareto principle (that at least some are made better off while no one is made worse off), but on the more relaxed Kaldor–Hicks compensation principle: truly, some may in fact be made worse off, but at the same time some others are made so much more better off that they could compensate those that are made worse off and still be better off themselves.

Crucially, management is a social science that operates in the real world where externalities and other market failures are present and distributional impacts do matter. For profit maximization to maximize social welfare in practice, it should be accompanied by optimal government intervention and by Kaldor–Hicks-style compensation payments. Like the two oars of a rowboat, profit maximization by firms and these corrective measures are supposed to work simultaneously and in tandem. In practice, however, there are formidable obstacles to implementing the corrective measures. A rowboat will not go in a straight line if you row more strongly with one oar than the other.

Still others contend that for many firms, the objective already is something other than profit maximization. Research shows that entrepreneurs do have other objectives besides profit maximization (e.g., Amit, MacCrimmon, & Zietsma, 2000; Cohen, Smith, & Mitchell, 2008; Douglas & Shepherd, 2000; Spence & Rutherfoord, 2001). In particular, social enterprises or hybrid organizations now exist in many countries and across a variety of economic sectors (e.g., Santos, 2012; articles in a 2015 special issue of California Management Review on hybrid organizations), as well as giving rise to new institutional forms such as Benefit Corporation statutes (Clark & Babson, 2012; Haigh, Walker, Bacq, & Kickul, 2015; Jones & Felps, 2013a). These are enterprises with an explicit dual purpose: to promote some common good—such as employment, poverty alleviation, environmental quality, or improved health—and to do so in a profitable manner. Famous examples include the 2006 Nobel laureate Grameen Bank and outdoor clothing company Patagonia, a benefit corporation (for more, see Dorado, 2006, and Thompson & Doherty, 2006). Regardless of the arguments for and against the profit-maximization paradigm, it remains a fact that enterprises exist where profit maximization is not the sole management principle. 3

In sum, the current predominant view is that the objective of business is to maximize profit; some argue that it ought to be something different, while others argue that for many firms it already is something different. Whatever one’s take on this, the debate is hampered by the fact that the “something different” has not been fully fleshed out in its various versions.

The basic idea in the “something different” approach is that social welfare, which in the profit-maximization view is an implicit objective, would be made an explicit objective. Some say that such formulations are not possible. While Mitchell, Weaver, Agle, Bailey, and Carlson (2016) argue that letting go of the single-objective requirement is not only possible but even desirable (also see balanced scorecard advocates), Jensen (2002) famously argued that it is “logically impossible to maximize in more than one dimension at the same time unless the dimensions are monotone transformations of one another” (p. 238). Arguments against multiple objectives have been taken up by many as proof that the development of objective functions containing social welfare needs to be rejected. We disagree. Incorporating social welfare in the objective function does not have to mean maximizing in more than one dimension, and having a single-valued objective function does not require that the objective function contain only a single variable. Neither does having multiple objectives equal having multiple objective functions, as implied by Sundaram and Inkpen (2004a). It is entirely possible to build objective functions that do contain both profit and social welfare if the relationships between those variables are clearly specified, and in this article we do just that.

We develop in two steps a range of objective functions that contain profit and the firm’s contribution to social welfare. 4 First we define different relationship types that can exist between variables in an objective function. From that basis, we then develop and present the range of alternative objective functions for firms. While our article thus revolves around normative stakeholder theory (Donaldson & Preston, 1995), we do not advocate any particular version of it and the article can be viewed as a descriptive account of variants of normative stakeholder theory. Indeed, the article is intended to be analytical in its methodology and so does not, for example, form normative judgments about the desirability of different objective functions. Having outlined the alternative objective functions, we then discuss how their development contributes to the debate about organizational purpose on several levels and for different audiences. We conclude our article with a discussion of the strengths and limitations of our approach as well as directions for future research.

Types of Relationships Between Variables in the Objective Function

An objective function is an equation specifying which output the firm attempts to maximize or minimize, with which variables as inputs and under which constraints. It consists of two kinds of elements: the variables that are contained in the function, and the relationships through which the variables are connected to one another.

In this article, elaborating on the variables is not where our contribution lies. We approach the purpose of business from an overall perspective, and hence the two goals that we want to incorporate as variables in an objective function are, simply, profit and social welfare. As we will discuss later, we do not go into the individual elements within social welfare at this stage. In contrast, identifying the relationships between these variables is key to our approach and forms the basis for structuring and systematizing the objective functions. We show that there are a number of possible relationship types, and through these, the two variables of profit and social welfare may be combined in complex ways to form distinct objective functions.

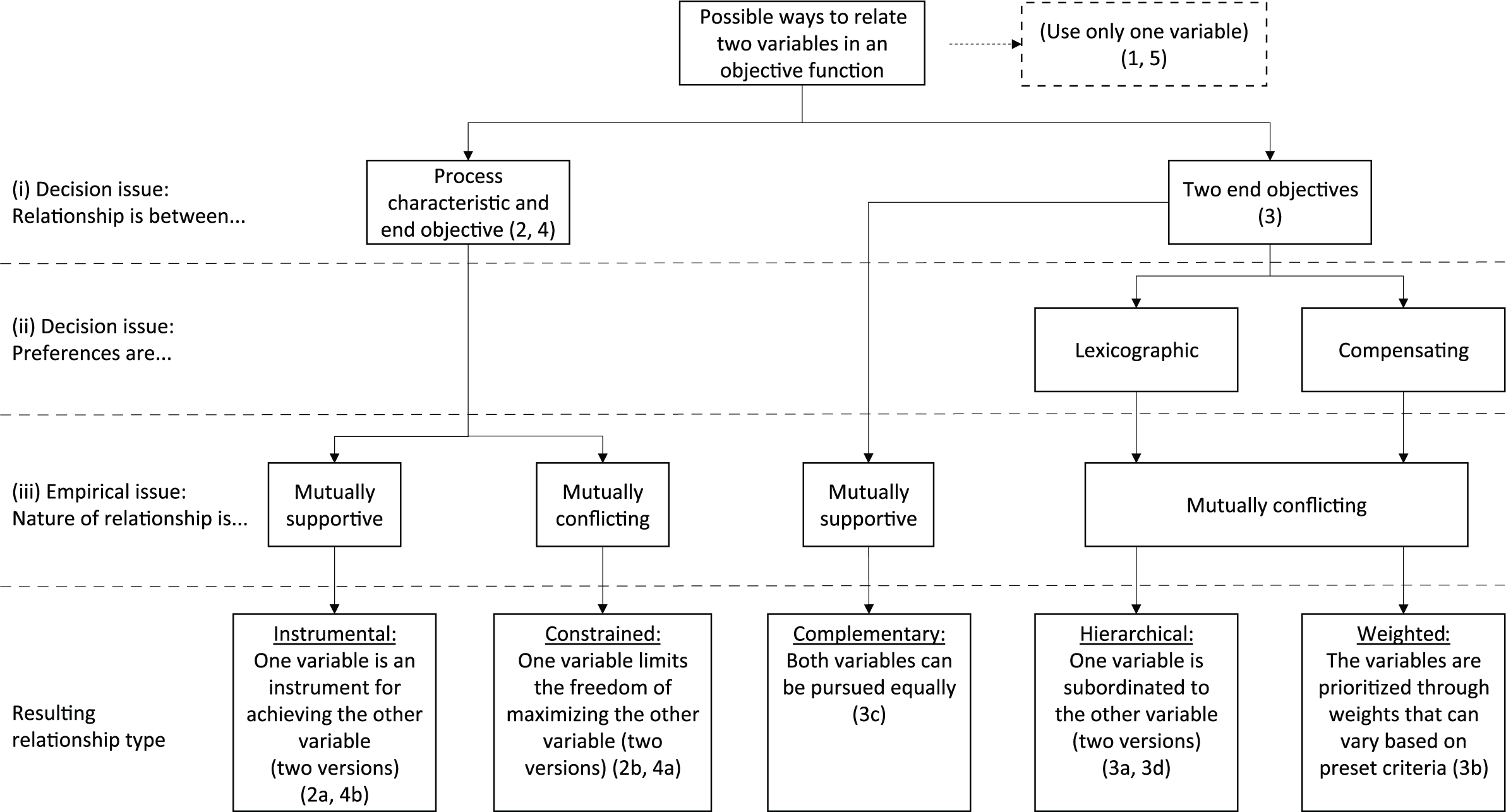

We develop the relationship types between the two variables based on three analytical dimensions: (1) whether the two variables are considered to be process characteristics or end objectives, (2) whether preferences between the two variables are lexicographic or compensating, and (3) whether the relationship between the two variables is mutually supportive or mutually conflicting. With these dimensions, we can capture the complex connections between the two variables (see Figure 1).

Objective functions theoretical decision tree (with numbering in Table 1 shown in parentheses).

The first two of these dimensions are decision issues. This means that managers or owners can decide how they want to conceive the relationship between the two variables in their firm. With regard to the first dimension, end objectives describe something the firm is striving for, and process characteristics qualify the process of striving for the end objectives. Thus, in the case of profit and social welfare, either one is a process characteristic and the other is an end objective, or they are both end objectives. As to the second dimension, if the business actors have lexicographic preferences toward the objectives they are not willing to trade off one objective for any amount of the other objective, and if they have compensating preferences there is substitutability between the objectives (see, e.g., van den Bergh, Ferrer-i-Carbonell, & Munda 2000; Wilkie, 1990).

The third analytical dimension differs from the two others in that it is not a decision issue but an empirical question. The nature of the relationship between two goals can be mutually supportive or it can be mutually conflicting. Goals are mutually supportive when pursuing one goal also serves the achievement of the other goal or, at least, does not harm it. In contrast, goals are mutually conflicting if the pursuit of one goal involves a trade-off with the other. In the case of profit and social welfare, the pursuit of profit can be beneficial for social welfare, but it can also be detrimental under many circumstances; in extreme cases, aggressive cost-cutting, for example, has been blamed for environmental disasters such as the BP Deepwater Horizon oil spill in the Gulf of Mexico (Feeley & Johnson, 2013), while the unbridled pursuit of profit in investment banking contributed substantially to the 2008 financial crisis, with many negative effects on social welfare, including large numbers of people losing their jobs and homes (Sorkin, 2009).

However, profit need not come at the expense of social welfare and may indeed increase social welfare and, thus, the goals of profit and social welfare can be mutually supportive. This is the premise of Porter and Kramer’s (2011, p. 67) idea of creating shared value: economic and social value created through “policies and operating practices that enhance the competitiveness of a company while simultaneously advancing the economic and social conditions in the communities in which it operates.” While it is beyond the scope of this article to identify the many possible ways by which the pursuit of profit can be beneficial for social welfare—or the pursuit of social welfare to profit—there is an extensive literature that explores the “business case” for company attention to social welfare and, thus, when the relationship between social welfare and profit is positive rather than negative (Aguinis & Glavas, 2012; Eccles, Ioannou, & Serafeim, 2014; Schreck, 2011). Even though it is difficult if not impossible to formulate a priori a generic set of rules to be followed, it is evident from the literature that there is support for a positive relationship between firm attention to social welfare and profit, albeit highly contingent; as Vogel (2005, p. 45) puts it: “CSR does make business sense for some firms in specific circumstances.” This means that in pursuing a given objective function, individual organizations will need to have an understanding of the particular mechanisms by which that firm’s actions in a given context create social welfare impacts on profit (and vice versa).

A firm can make its decisions regarding the first and second dimensions without knowing the outcome of the third dimension. However, when it comes to developing the objective function in full, the empirical dimension we have identified also becomes important since it determines whether certain approaches to combining profit and social welfare are in fact possible in the real world. The risks of not taking this dimension into account stem from possible misapprehensions or mistaken assumptions about the relationships between profit seeking and social welfare. This is evident in the debate on creating shared value. In their critique of creating shared value, Crane, Palazzo, Spence, and Matten (2014) suggest that Porter and Kramer (2011) ignore the tension between social and economic goals and engage in wishful thinking by cherry-picking supportive examples. Building on this critique, De los Reyes, Scholz, and Smith (2017) propose that in contrast to the “win-win” cases of Porter and Kramer, there are also potentially “win-lose” cases, where business wins and society loses (i.e., profit at the cost of societal welfare) and “lose-win” cases, where business loses out while society gains (societal welfare enhanced while profit suffers).

Combining the outcomes along our three analytical dimensions we obtain five possible relationship types between two variables in an objective function. The relationship type between a process characteristic and an end objective is instrumental for mutually supportive variables and constrained for mutually conflicting variables. There are two versions of each relationship type depending on which one of the two variables is the process characteristic and which one is the end objective. Between two mutually supportive end objectives the relationship is complementary. Between two conflicting end objectives, the relationship is hierarchical in the case of lexicographic preferences (again with two versions) and weighted in the case of compensating preferences. These alternative ways of relating two variables to one another are shown in Figure 1 and described in more detail below.

Instrumental Relationship

If the relationship between two variables is instrumental, one variable (the instrumental variable) is a means for achieving the other variable (the end objective). Thus, to what extent the instrumental variable is being pursued depends on the extent to which it serves satisfying the end objective. This describes well the win–win oriented approach of many firms to corporate responsibility, where corporate responsibility improvements are motivated by the beneficial impacts they might have on the economic success of the business. Indeed, the potential instrumental association between various aspects of social welfare and profit has been widely debated and researched since the 1970s (for a review, see, e.g., Margolis & Walsh, 2003).

Constrained Relationship

With a constraint-type relationship between the two variables, one variable (the objective) is maximized so that the value of the other variable (the constraint) stays within a preset range. Either one of our two variables can be regarded as a constraint by the firm. For example, a firm may decide on the social welfare impact it wishes to achieve; for a pharmaceutical company, this could be to provide at least a certain number of people with access to its product, and then it would maximize profit within these limits. Or, a firm may decide on the economic outcome it wishes to achieve—such as full cost recovery or a specific return on investment—and then maximize the social welfare impact within these limits.

Complementary Relationship

When there are two mutually supportive end objectives, their relationship may be called complementary. Both objectives are valuable in themselves, but since there is no trade-off involved, their mutual relationship is without problems. Both may be equally regarded as end objectives at the same time, and both may be maximized at the same time. Take the example of the newly developed food product “pulled oats,” a plant-based, convenient, and tasty protein source, where commercial success and promoting sustainable eating seem to be going hand-in-hand (Yle News, 2016).

Hierarchical Relationship

Another alternative for the firm is to decide that one variable has priority over the other, as in lexicographic ordering. In this case, the more important objective is satisfied first, after which the less important objective is satisfied to the extent possible without affecting the outcome of the first objective. For example, corporate responsibility is sometimes presented through Carroll’s (1991) pyramid where economic responsibilities enjoy the priority status and legal, ethical, and philanthropic responsibilities follow in a clear hierarchical order (though not everybody agrees with this ordering). A hierarchical approach to relationships between multiple objectives may fit with many “conventional” firms with strong corporate responsibility: Responsibility is a genuine business objective, but nevertheless one that is subordinated to the profit objective. However, the priority can run both ways, and a firm (e.g., a social enterprise) may also consider profit as only the secondary objective.

Weighted Relationship

When the approach to integrating multiple objectives is through compensating preferences, weights enter the picture. While it would be difficult to determine specific fixed weights for the multiple objectives a priori, such weights can be variable, meaning that the objective given priority varies from one decision-making situation to another based on preset criteria. For example, a firm whose preset criteria concern maximizing a broad concept of sustainability could prioritize environmental protection in a situation where the carrying capacity of nature is about to be irreversibly exceeded, philanthropy where there is an imminent humanitarian catastrophe, and profit when the firm is threatened by economic failure. Not only because of changing circumstances but also because of diminishing returns from any individual variables, the variable to be prioritized changes in a dynamic manner. Jones and Felps (2013b) refer to this same issue when they point out that the extent to which economic wealth contributes to social welfare depends on relative economic scarcity in the era and the society in question. Schad, Lewis, Raisch, and Smith (2016) depict such dynamic balancing through the image of tightrope walkers, where maintaining the desired balance requires consistent, ongoing microshifts. In effect, the approach of variable weights transforms the multiobjective problem into a new single-objective problem, where the new single objective to be maximized depends on the values of the other, multiple objectives. While this approach in a way “pushes the problem outside the formula,” in doing so it turns attention to a potential meta-objective, that is, a new single “umbrella” objective. Jones and Felps (2013a) propose such a meta-objective to be stakeholder happiness; a concept which depends on several elements, including but not limited to economic wealth (also see Lankoski, Smith, & Van Wassenhove, 2016).

A Range of Alternative Objective Functions

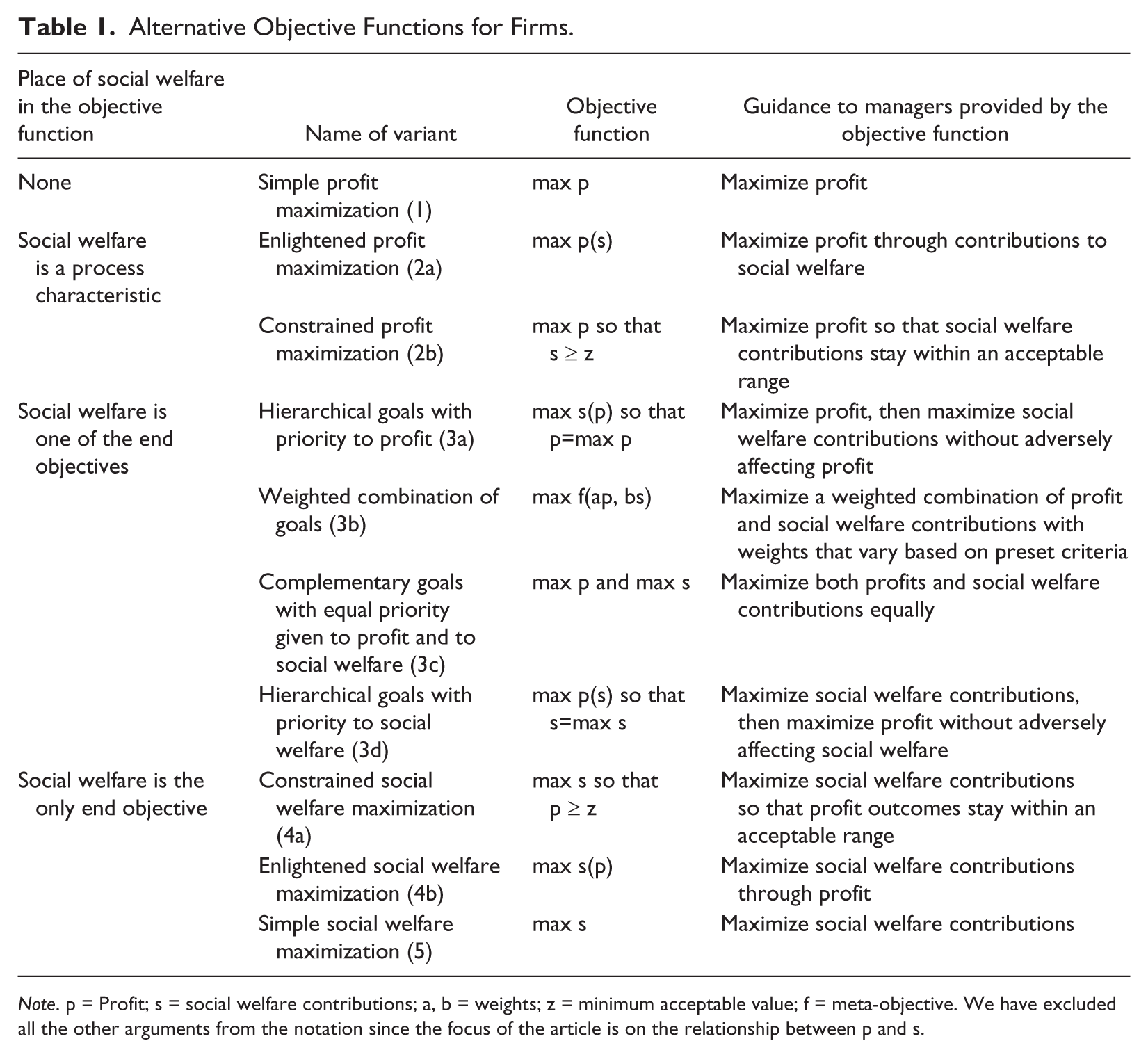

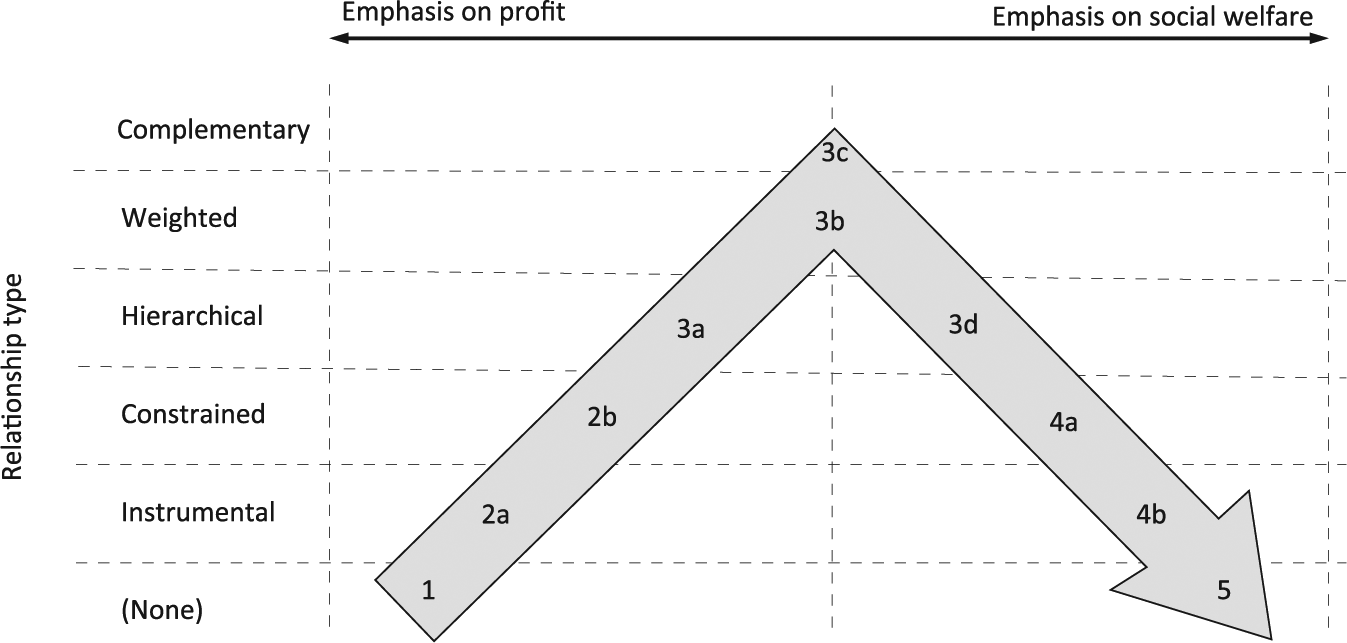

Through these relationships between variables we obtain a spectrum of possible objective functions for firms. In these “ideal types” the role of social welfare in the objective function ranges from total exclusion to being the only purpose of the firm through a number of intermediate options. There are several conceptually distinct cases: variants of profit maximization, where social welfare is not an end objective; variants of multi-objective firms where social welfare is one of the end objectives; and variants of social welfare maximization, where social welfare is the only end objective. In total, we identify 10 different objective functions for business, 1 excluding and 9 including social welfare. Table 1 lists them in the order of increasing centrality of social welfare among the firm’s objectives, and Figure 2 shows this continuum of objective functions schematically.

Alternative Objective Functions for Firms.

Note. p = Profit; s = social welfare contributions; a, b = weights; z = minimum acceptable value; f = meta-objective. We have excluded all the other arguments from the notation since the focus of the article is on the relationship between p and s.

The range of alternative objective functions in the order of increasing centrality for social welfare.

The numbering logic assembles the objective functions into five groups according to increasing centrality of social welfare: social welfare can be (1) entirely absent from the objective function, (2) a process characteristic, (3) one of the end objectives, (4) the only end objective, adjusted by profit as a process characteristic, and (5) the only variable in the objective function. This numbering scheme reflects the decisions made in the first stage of the decision tree in Figure 1. It is further refined by the additional labels a, b, c, and d to take into account the remaining stages in the decision tree. Thus, the objective functions are numbered 1 to 5 before taking into account whether the preferences between the variables are lexicographic or compensatory (i.e., the second analytical dimension) and the empirical relationship between profit and social welfare (the third analytical dimension). The numbers plus the additional letter labels represent the 10 variants that result.

Notice that the notation we use in Table 1 does not specify any particular form for the objective functions, equally allowing linear or other functional forms. Note also that, contrary to some studies, this is not meant to be a stage model (on stage models, see, e.g., Kolk & Mauser, 2002): These are not stages that companies travel through but different specifications of the purpose of the firm or strategic business unit (even if it is possible for a firm/strategic business unit to migrate to a different objective function). We now introduce each objective function, with supporting literature and illustrations.

Variants of Profit Maximization

Our first group, Alternatives 1 to 2b, contains objective functions where profit remains the sole end objective for the firm.

Simple Profit Maximization (No

1). When the objective of business is simple profit maximization, there is no place for social welfare in the objective function of the firm. This view was famously articulated by Friedman (1962): There is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition, without deception or fraud. (p. 133)

This specification clearly and simply instructs managers to maximize profit.

Enlightened Profit Maximization (No

2a). Under this alternative, social welfare does enter the objective function as an instrument for firms to pursue their goal of profit maximization. Even if social welfare does get an explicit role, the end objective of the firm is not changed, and managers are supposed to improve social welfare only to the extent that this can contribute to the process of profit maximization. This is a widespread view. For example, Jensen (2002) directly proposes enlightened value maximization as the appropriate way of specifying a firm’s objective. Similarly, most of the influential work by Porter falls under this view, with the idea of shared value presented as “integral to profit maximization” (Porter & Kramer, 2011, p. 76). Enlightened profit maximization is echoed also in firms, for example: “It is fundamental that a company such as Nestlé plays a positive role in society. Indeed, we believe that we will create long-term value for our shareholders only if we connect positively with society at large.” (Nestlé, 2012, p. 5).

Constrained Profit Maximization (No

2b). With constrained profit maximization, profit remains the sole end objective for the firm, but social welfare becomes a constraint on the process of making profit. In other words, the freedom to maximize profit is limited by the requirement that social welfare outcomes remain within an acceptable range. Note that constrained profit maximization refers here to self-imposed, endogenous constraints (Rönnegard & Smith, 2013), not to the firm obeying exogenous constraints set, for example, through regulations. The necessity to obey such external constraints is already captured by their instrumental impact on profit. Graafland (2002) calls a variant like this the license-to-operate perspective, the point being that the acceptable minimum level of social welfare is that which is required by society for the firm to maintain its license to operate. However, the required social welfare outcome level under constrained profit maximization may also be internally set by the firm to be higher than the minimum determined by a license-to-operate perspective. In other words, to differentiate between enlightened profit maximization and constrained profit maximization, we envisage a firm’s managers constraining profit maximization because keeping social welfare within the acceptable range is in part determined by some sense of acceptability that is broader than that which in its absence might result in a threat to reputation or, more generally, license to operate. For instance, companies often have plant safety processes that protect workers and well exceed legal requirements because they care about worker safety and a determination has been made of a potential if unlikely risk that could, all the same, conceivably materialize.

Variants of Multiobjective Firms

This group, Alternatives 3a to 3d, contains alternatives where both social welfare and profit are end objectives, relating to each other differently depending on whether the actors have lexicographic or compensating preferences toward these objectives or, as in Alternative 3c, whether they are complementary goals and both profit and social welfare are sought equally.

Hierarchical Goals With Priority To Profit (No

3a). When the relationship between two business objectives is hierarchical and priority in the hierarchy is given to profit, this means that the firm first maximizes profit and then improves social welfare as much as possible without adversely affecting profit. This makes social welfare a real but secondary objective for the firm. For example, a food company might want to undertake as many animal welfare–improving measures as possible, as long as they do not harm profit. The difference between this alternative and enlightened profit maximization (No. 2a) is that the resulting level of social welfare is higher under this variant because social welfare is a genuine end objective: Under No. 2a, the food company would implement only those animal welfare measures that contribute to profit, under this variant are all those measures that do not take away from profit. Although the distinction may in practice often be subtle, the underlying difference in the approach is nevertheless clear.

Weighted Combination of Goals (No

3b). When business actors have compensating preferences, the form of the objective function instructs managers to maximize a weighted combination of profit and social welfare. For example, Jones and Felps (2013a, p. 358) propose that the objective of a corporation should be “to enhance the aggregate happiness of its normatively legitimate stakeholders over the foreseeable future,” an objective function that calls for assigning variable weights for profit and social welfare and thus falls within this category.

Complementary Goals With Equal Priority to Profit and Social Welfare (No

3c). Under this variant the objectives are mutually supportive, and the firm gives equal priority to profit and social welfare. In the case of “pulled oats” cited earlier, promoting sustainable eating and making profit from the product are complementary objectives. Similarly, for example, contributing to sustainability through the replacement of nonrenewable energy, and running a profitable business, could be complementary objectives for a solar panel firm. In such cases, it is possible for the company to treat these as equal end objectives. At the level of rhetoric at least, treating profit and social welfare as equal objectives is not uncommon. The Danone Manifesto by the French dairy product company, for example, is meant to “carry forward . . . our dual project for business success and social progress” (Danone, 2017).

Hierarchical Goals With Priority to Social Welfare (No

3d). This variant is the mirror image of the one where hierarchical priority was given to profit. Here, the firm first maximizes social welfare and then makes as much profit as possible without adversely affecting social welfare. Profit is a real but secondary objective for the firm. For example, Grant (2011, p. 9) describes an Aristotelian business model where the ultimate purpose of a firm is “firstly to serve society’s demands and the public good and secondly, to be rewarded for doing so.” Many social enterprises operate according to this model (Santos, 2012).

Variants of Social Welfare Maximization

In the objective functions of this group (Alternatives 4a to 5) social welfare is the only end objective; we can distinguish three variants just as we did with profit maximization, in Alternatives 1 to 2b.

Constrained Social Welfare Maximization (No

4a). Under this variant, the objective function instructs managers to maximize social welfare under the constraint that profit outcomes must stay within an acceptable range. This is consistent with how Drucker, as described in Smith (2009), argues that while economic responsibility is the first responsibility of a business, it is not its only responsibility. Often acceptable profit means enough profit for firm survival (e.g., Berger, Cunningham, & Drumwright, 2007; Graafland, 2002), but the profit threshold can also be set higher than this by a firm’s owners.

Enlightened Social Welfare Maximization (No

4b). Here the objective of the firm is to contribute to social welfare, but it is recognized that making profit is an instrument for this process. Consider for example the following statement by the pharmaceutical company Merck: “Our ability to meet our responsibilities depends on maintaining a financial position that invites investment in leading-edge research and that makes possible effective delivery of research results” . . . In other words, achieving a fair rate of return for its shareholders is the sine qua non for companies such as Merck to fund the investments required to make the world a better place for all its stakeholders (as quoted in Sundaram & Inkpen, 2004b, p. 371)

Or, as discovered by Berger et al. (2007, p. 142): The firms that were led by social values had to do well economically “so as to prosper and advance [their] noneconomic mission. As one values-led CEO asserted, ‘The more we prosper, the more society prospers.’”

Simple Social Welfare Maximization (No

5). Finally, when the objective function takes the form of simple social welfare maximization, there is no place for profit in it. However, this does not prevent a well-managed firm from making profit, as Freeman, Wicks, and Parmar (2004, p. 364) argue that “[c]ertainly shareholders are an important constituent and profits are a critical feature of this activity, but concern for profits is the result rather than the driver in the process of value creation.” This is perhaps illustrated by Yvon Chouinard’s (2016) business philosophy. He is the founder and owner of Patagonia, a company famous for making business decisions on product design and content that eschew profit in favor of the environment.

All 10 variants of the objective function in principle lead to different outcomes with regard to where the firm ends up in the decision space about profit and social welfare—or, should they lead to the same outcome, they may arrive there along different routes. Interestingly, Graafland (2002) found in a single report by Shell (1998) text corresponding to four different specifications: enlightened profit maximization, constrained profit maximization, weighted combination of goals, and constrained social welfare maximization, according to our terminology.

Alternative Objective Functions and Debates About Organizational Purpose

Developing and delineating the range of alternative objective functions for firms, as we have done in this article, has the potential to advance discussion by various audiences of organizational purpose. It can help these audiences see how there are more options to organizational purpose than have been currently articulated, what these options are, and how these options can be better communicated, taught, implemented, and tested.

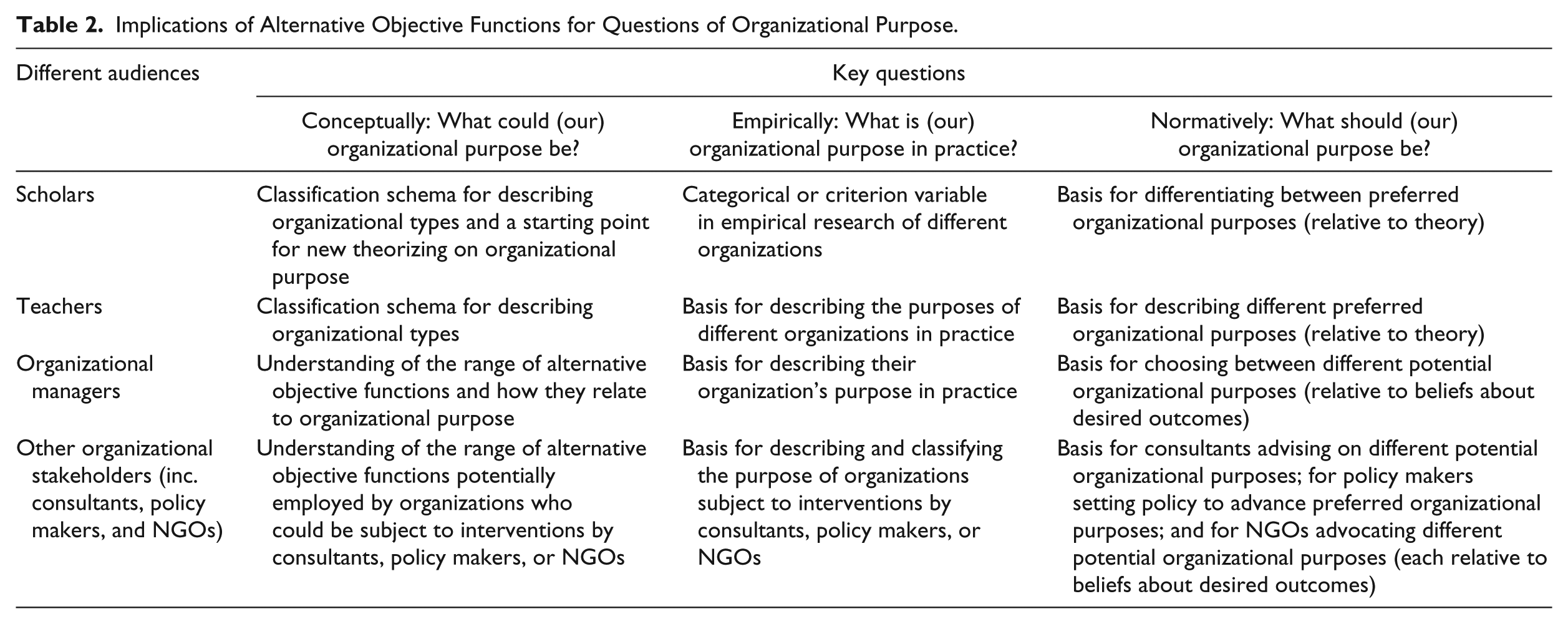

Adapting the key questions of corporate social responsibility from Hay, Stavins, and Vietor (2005)—may they, can they, do they, should they?—we show how fleshing out in detail the alternative objective functions can contribute to three kinds of debate on organizational purpose: The conceptual debate on what organizational purpose could be in principle, the empirical debate about what it is in practice, and the normative debate on what it ought to be. While our primary goal has been to address the conceptual debate on what organizational purpose could be, this article also informs the empirical and normative debates and with different implications for the different audiences. We now examine these implications for the various audiences, as we summarize in Table 2.

Implications of Alternative Objective Functions for Questions of Organizational Purpose.

Conceptually: The Debate on What Organizational Purpose Could Be

Organizational purpose is often framed as being about “shareholders vs. stakeholders.” Indeed, Rönnegard and Smith (2013) refer to this as the “basic debate” in the field of business ethics. However, we suggest that such a binary formulation is too simplistic for academic discourse. We bring nuance to the debate by providing scholars with 10 shades of gray in perceiving the role of business. Developing a systematic and comprehensive overview of variants of objective functions for business—albeit as ideal types—offers a fine-tuned view of the possible approaches to organizational purpose. This can serve as a classification schema for scholars describing organizational types in both their research and in their teaching. In so doing, we add specificity to the debate by developing for each variant a precise specification in the form of an objective function, as shown in Table 1. This can replace previous, ambiguous calls to “integrate” or “balance” objectives, and thus advance the discussion between competing paradigms.

This framework can also serve managers and their consultants in better understanding and articulating organizational purpose. Here, the goal is not to inform academic discourse but rather to get beyond simplistic notions of purpose that might be characterized as starkly as profit maximizing versus “do-gooding.” At the very least, it suggests different ways of thinking about “do-gooding.” For example, Objective Function 3a provides for social welfare maximizing only after profit is maximized, whereas 4a provides for social welfare maximizing while achieving a given level of profit, which might be less than profit maximizing. Profit is important to both organization types, but in 4a managers could turn their attention to social welfare as soon as the target level of profit has been achieved.

Policy makers and NGOs should also be interested in understanding organizational purpose and how alternative objective functions can influence outcomes relevant to public policy or NGO agendas. Thus, the framework is a way for both to better understand the landscape within which they are operating. For example, agencies tasked with protecting the environment might look differently at the incentives required for organizations pursuing simple profit maximization, that is, Type 1, as opposed to organizations that are also pursuing social welfare. NGOs could similarly identify different strategies for use with target organizations according to the type of objective function.

Empirically: The Debate on What Organizational Purpose Is

Beyond a conceptualization of the range of alternative objective functions is the possibility of applying that framework to understanding the purpose of real-life companies in practice. With the help of the more systematic, comprehensive, and precise approach presented in this article, we can identify more clearly these alternative types of firms and understand their differences in the face of trade-offs between profit and social welfare.

For scholars conducting research, this characterization of firms according to organizational purpose might be relatively qualitative—a descriptive classification schema for different organizations. Conceivably, however, the alternative objective functions could take the form of a categorical (or nominal) variable in quantitative analysis such as regression or possibly serve as the criterion (or dependent) variable predicted by independent variables (e.g., a study to test whether companies with founding family influences, such as family members on the board, are more likely to have social welfare as the only business objective; i.e., Types 4a, 4b, or 5). While in teaching there might be less need to so sharply delineate different real-world organizations, there might be merit in drawing distinctions relative to operant objective functions in comparing different real-world organizations or in discussing case studies.

In the “Introduction” section, we noted that firms already exist that do not have maximizing profit as their objective. The managers of these organizations are likely aware of this, but may not fully appreciate, in an abstract sense, the various alternative forms that not-profit–maximizing organizations can take (Types 3-5). Equally, profit-maximizing managers might not be able to fully articulate the variants they might pursue (1, 2a, and 2b). Consultants could advise clients on these alternatives and on how different objective functions might translate into particular strategies. For example, Variant 2b, where the profit-maximizing firm wants to ensure a minimum level of social welfare, likely calls for different strategies relative to Variant 3a, where the organization would strive to create as much social welfare as possible after having satisfied its profit maximization goal. More generally, increased specificity on organizational purpose should help firms and their advisers to better understand and respond to stakeholder pressures to “take into account” other objectives besides profit.

Policy makers and NGOs will also likely be questioning the organizational purpose of real-world organizations. Policy makers should be interested in classifying organizations as a basis for possible policy interventions, particularly in regard to how they will likely respond to different incentives. NGOs will be thinking in terms of how they respond to different strategies. For example, with organizations for which social welfare is a business objective or the only business objective (Types 3-5), strategies of cooperation or partnerships could be justified as serving those social welfare objectives. In contrast, more coercive strategies might be required with Type 1 organizations.

Normatively: The Debate on What Organizational Purpose Should Be

The normative debate on what organizational purpose ought to be is an enormous topic, especially as regards the roles profit and social welfare should play in it. Suffice to note here, it is an enormous topic for all our different audiences, not just scholars. Scholars, relative to various theories of how business activity can generate social welfare might argue normatively for a preferred objective function. For an easy example in illustration, some scholars could present arguments that reject simple social welfare maximization (Type 5) because they believe it is not financially viable in the long term, and reject simple profit maximization (Type 1) because it precludes any intent to create social welfare, which might, in turn, have various undesirable consequences, including opportunistic behavior.

Preferred objective functions might also be advanced in teaching, again relative to theories of how business activity can generate social welfare. That said, Smith and Rönnegard (2016) are critical of business schools for focusing too heavily on shareholder value maximization as the purpose of business. They suggest that business schools should teach a plurality of conceptions of organizational purpose. This would be consistent with a range of objective functions, as we propose.

While intriguing for academics, the question of organizational purpose is of profound importance for managers (including business founders and owners) as well as for the consultants who advise them. It is fundamental to the business in so many ways, from why it exists through to how it functions. Beliefs about desired outcomes and how those outcomes can be realized are likely to drive choices among alternative objective functions. Santos (2012), for example, explains how social entrepreneurs differ from commercial entrepreneurs by focusing more on value creation than value capture as they address some of the most pressing problems in modern society. Nonetheless, while social entrepreneurs might have a clearer sense than most managers of their social purpose, even they must operate with regard to an objective function that specifies some relationship between profit and social welfare. This must also apply to benefit corporations that, by definition, have an explicit purpose “to create a material positive impact on society and the environment” (Clark & Babson, 2012, p. 838; also see Hiller, 2013). 5

Finally, both policy makers and NGOs are likely to have preferred organizational purposes relative to beliefs about how alternative objective functions might lead to desired outcomes. These preferences are likely to be reflected in policy interventions by policy makers and advocacy by NGOs. For example, NGOs might believe that organizations giving priority to social welfare are more deserving of their support or, conversely, more likely to comply with demands if targeted for not giving sufficient attention to a social welfare issue. Equally, companies that are constituted as benefit corporations and must report their social and environmental performance relative to credible independent standards (Clark & Babson, 2012) can expect to be scrutinized by NGOs—and possibly some policy makers—on the adequacy of their reporting and the performance itself.

Discussion and Conclusion

That profit maximization alone does not lead to social welfare maximization in the real world is generally understood by many proponents and opponents of the profit-maximization paradigm. Where these camps largely differ is the suggested solution: whether it should be optimal government intervention or the modification of organizational purpose to more explicitly contain social welfare. Management theory should at least examine carefully the modification approach, not least because management is a field with strong links to practice and real-world impacts. Indeed, several authors have argued that the discussion on how to combine multiple objectives in management needs to be broadened, including the question of an explicit role for social welfare in management theory (Mackey, Mackey, & Barney, 2007; Windsor, 2001; Young & Tilley, 2006). Donaldson and Walsh (2015, p. 198) argue that the purpose of business is to optimize collective value; in terms of the purpose of a firm, this means that firms with different purposes may rightfully exist, but it is “incumbent on a firm to be clear about its purpose and its effects on others”. In their recent article, Jones et al. (2016, p. 220) directly invite management scholarship to examine what could be “possible single-valued corporate objectives that include a stronger social welfare orientation.”

To address this issue, we set out to investigate what forms such alternative objective functions could take. We first identified five potential relationship types between profit and social welfare, and then examined how profit and social welfare could be combined in different ways to build distinct objective functions. In doing this, our contribution lies not in widening the range of possible objective functions but in systematizing and specifying that range. As a result of our analysis, we advance the idea that there are 10 specific “ideal types” of organizational purpose and describe these ideal types. As we explained at the outset, given our purely analytical approach, we do not take any normative standpoint about the objective functions in this article. However, now that the alternative objective functions have been laid out in detail, they can be better examined in further research against the criteria of how effective they are in securing social welfare outcomes, how efficient they are in the use of society’s resources in achieving those outcomes, as well as how feasible their implementation is in practice.

There are two important advantages in our approach. The first is that we use language and terminology that is similar to that in the profit-maximizing approach. Normative stakeholder theory may be considered the most fully articulated alternative to shareholder wealth maximization (Jones & Felps, 2013b). However, because it has not been articulated with comparable terminology and the specificity of the profit-maximizing view, a prominent criticism nevertheless goes that it is “incomplete as a specification for the corporate purpose or objective function” (Jensen, 2002, p. 236) and cannot therefore be viewed as a real contender to the profit-maximization paradigm (see also, Phillips, Freeman, & Wicks, 2003). Referring to the fact that shareholder value is expressed as a single-valued objective function, Raynor (2009, p. 6) goes as far as to argue that “shareholder value holds the upper hand over stakeholder theory for this reason more than any other.” To advance the discussion between competing paradigms it is important to be able to express those paradigms in comparable terms; this means expressing variants of stakeholder theory as objective functions.

The second advantage is that using objective functions and their accompanying mathematical notation adds structure, forces one to be precise, and offers a parsimonious, yet accurate way of articulating relationships (Lévesque, 2004). Indeed, according to Adner, Pólos, Ryall, and Sorenson (2009), much of the value of using formal methods stems exactly from the fact that they force the researcher to undertake the task of thinking thoroughly through the concepts they invoke in order to be able to translate verbal argumentation in natural language into statements in symbolic logic. This is a task which is challenging and requires a deep understanding of the issues and concepts, but which ensures precision and transparency. Without such attention to precision, researchers may end up duplicating effort by forwarding equivalent ideas with different names (Adner et al., 2009), or end up perceiving consensus where in fact none exists (Jones & Felps, 2013a)—both highly relevant concerns in the context of social welfare and management theory where, according to Jones and Felps (2013a), lack of specificity has been a major concern.

As we discussed in the previous section, our article can contribute to conceptual, empirical, and normative debates about organizational purpose and benefit different audiences. Removing the conventional assumption of profit maximization as the sole management principle opens up new horizons for the development of new, more nuanced theoretical approaches to management. The contribution of this article is in the groundwork it lays for such theory development through the systematic and analytical identification of alternative objective functions for firms. Studies exist that have divided approaches to organizational purpose into three groups: profit-driven at one extreme, “social welfare-driven” at the other extreme, and some kind of integrative approach in the middle (see, e.g., Berger et al., 2007; Windsor, 2006), but our work attempts to go still further in the amount of detail and specificity it provides. Moreover, because the article outlines a range of alternative objective functions, future work is not locked into one path but can continue across a wide spectrum. This is in line with Freeman et al. (2004) who write: Unlike the narrow view of shareholder theory that ascribes one objective function to all corporations, stakeholder theory admits a wide range of answers. In this view, there is not just one stakeholder theory, but many possible normative cores . . . that make up the genre of stakeholder theory. (p. 368)

Our article also lays the ground for future empirical research. In particular, different types of firms may have similar-looking outcomes, while the boundaries across categories have been somewhat blurred (see, e.g., Peredo & McLean, 2006): “conventional” enterprises may have strong environmental responsibility, social enterprises may pollute, nonprofit organizations may have an income-creating leg, profit-maximizing organizations may undertake serious philanthropic activities, and the products of “conventional” firms may satisfy important social needs. This article, however, is not based on such external, manifest characteristics but on the underlying logic of the firm that is driving decision-making and management and is captured in its objective function. Even if there are instances where two firms arrive at similar outcomes, below the surface the firms may still be quite different. With the help of this article, we can bring some precision to these blurred boundaries.

Of course, the objective functions themselves are not directly observable from the outside, so we are not claiming that the identification of firms into these 10 variants would be empirically straightforward. Here one option is to ask the companies themselves, either inviting them to explain their choices along the decision tree in Figure 1, or to directly state which objective function they most closely identify with. Furthermore, the variants we present represent ideal types, and the extent to which they find direct correspondence in real-life firms is also an open question. Nevertheless, interesting empirical questions arise: How common is each variant, and are some variants missing in practice? Do firms tend to consistently follow one of the alternatives, or can different objective functions be operative in different parts of the company at the same time? What are the antecedents of choosing a particular objective function, and are the profit and social welfare outcomes indeed different for firms following different objective functions?

We acknowledge as a limitation of our article that we only address social welfare at a general level. Social welfare is a multifaceted construct, and there may be trade-offs and complementarities among the various individual “harms” and “goods” resulting from organizational activities. Examining such internal linkages within social welfare and how they can be taken into account in the objective function is beyond the scope of this article and should be undertaken by future work. Freeman, Harrison, Wicks, Parmar, and de Colle (2010, p. 289) solicit richer descriptions of stakeholder theory, asking: “What does it mean to balance stakeholder interests? Are there different types of balance and compromise?” We have provided descriptions for the relationship between profit maximization and social welfare but not addressed the relationships between individual elements of social welfare. Consequently, we do not enter into discussions on what exactly social welfare consists of, how tensions between components of social welfare should be addressed to produce the greatest good for society, and whether and how managers can know this.

This article is about the first step in strategy formulation as it articulates different ways of defining corporate purpose in general. Already with this step, however, tensions are present—in fact, our entire analysis revolves around fitting together contradictory but interdependent elements. This is a topic at the core of the emerging literature using a tension or paradox perspective (see, Hahn, Pinkse, Preuss, & Figge, 2015; Hahn, Preuss, Pinkse, & Figge, 2014; Schad et al., 2016; Van der Byl & Slawinski, 2015). Proceeding further to cover individual elements of social welfare and to the actual implementation of an objective function, the investigation is likely to run deeper into questions of tensions and conflicts and could potentially benefit from this body of literature.

Related to the above limitation, our objective functions contain the variable “social welfare” as one of the targets of managerial decision making. Compared with profit, this variable is likely to be less practical for day-to-day management. Profit or some measure of financial return is a meaningful yardstick for practicing managers because it can be measured with reasonable effort with information that is internally available to the firm. Although it must be noted that while measures of profit are not necessarily straightforward—consider revenue recognition, for example—to measure social welfare is a hugely difficult if not impossible task for any single firm, at least if we are looking at overall contributions to social welfare and beyond measures of its individual elements. Easily observed metrics are also required to monitor and measure agent performance; a factor which has so far tended to speak in favor of shareholder primacy in the debate about firm purpose (Stout, 2002). Some proxy or proxies for social welfare in the objective function is therefore needed for managers to facilitate their decision making, and this is an important area for future work.

To conclude, according to Walsh, Weber, and Margolis (2003), management was originally, in part, about contributing to the good of society, but this feature has largely been lost along the way (also see, Stout, 2012). Yet firms often find that their stakeholders have not abandoned this idea, and firms are increasingly demanded by their stakeholders to embrace other objectives besides profit maximization. In this article, we offer an analysis of alternative objective functions for firms that can help in the rediscovery of the role of business in contributing to social welfare.

Footnotes

Acknowledgements

The authors would like to thank Marc Le Menestrel and Pauli Lappi for useful discussions on an earlier draft, as well as participants in the GRONEN Research Conference held at the University of Hamburg in May 2016 and the ARCS Research Conference held at Rotterdam School of Management in June 2017, Editor Timo Busch, and the two anonymous reviewers for their valuable comments. While conducting this research, Leena Lankoski was on the faculty of University of Helsinki.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Craig Smith gratefully acknowledges Dreyfus Sons & Co. Ltd., Banquiers for research support on this project. No other financial support was received.