Abstract

Asymmetric timber trade between least-developed countries with large forest resources but backward processing industries and emerging economies has led to an uneven distribution of value in international timber commodity chains. Selling their raw timber with no domestic value added contributes little to socio-economic development and is associated with high rates of deforestation. The Lao PDR has served as a raw timber frontier for advanced timber industries in neighboring countries, leading to forest loss and related environmental problems. In response, since 2015, the Lao government has adopted drastic policy measures to end forest degradation and upgrade its timber industry (e.g., log export ban). Using teak as an example, our study provides empirical ex-post evidence on the effectiveness of state-imposed timber industry upgrading policies. The study relies on expert interviews with key policy actors at national and local levels, as well as an enterprise survey and cluster analysis conducted in Xayyabouly province. These drastic policies had far-reaching implications for the structure of the timber industry and the configuration of the timber value chain and rural development.

Keywords

Introduction

The tropical timber trade pattern is generally, but not exclusively, characterized by a flow of wood and wood products from less-developed producer countries, often situated in the Global South, to more industrialized consumer countries. In this context, fast-growing emerging economies like China, Vietnam or Brazil have turned into flourishing wood processing hubs, exporting manufactured wood products to global markets. To satisfy their growing demand for raw material, they increasingly rely on timber imports in form of logs and sawn wood from tropical, highly forested countries, often from the least-developed countries, such as the Republic of Congo, Cameroon, Papua New Guinea or the Lao PDR (ITTO, 2021). In the absence of any well-developed wood processing industries, these latter countries sell off their valuable timber resources without much value added, which could benefit local economic development, while they see their natural forests disappear increasingly. Industry and value chain upgrading are considered to be an appropriate leverage with which to overcome such negative trade relations in global timber value chains (Bolwig et al., 2010; Ponte & Ewert, 2009). Drawing from Humphrey and Schmitz (2002), practical measures include (i) process upgrading: achieving more efficient production through reorganization; (ii) product upgrading: moving into products with increased unit value; and (iii) functional upgrading: increasing skill content.

In this context, there exist multiple examples of tropical countries that have enacted log export bans for the dual purpose of protecting their natural forests and promoting domestic timber processing, in order to strengthen exports of higher value-added wood products (Von, 1994). In Indonesia, for instance, a log export ban policy came into effect in the 1980s and 2000s with the aim of reducing illegal harvesting and strengthening domestic wood processing (Resosudarmo and Arief 2006). In Malaysia, where timber extraction for export was a vital source of revenue, the government has imposed log export bans and export quotas since the 1990s to enhance domestic downstream manufacturing (Tachibana, 2000). In Ghana, a major exporter of roundwood from Africa to Asia-Pacific, the government imposed a log export ban in the 1990s to stimulate growth and rural development via increased value added in wood manufacturing, instead of exporting raw timber (Amoah et al., 2008).

In 2015, the Lao PDR followed these examples. The background was a growing mismatch between rising timber exploitation rates and decreasing revenues from raw timber exports. As a response, the government pursued more control over the timber trade and wood processing for state-directed industry upgrades and forest protection, by enacting a log export ban in conjunction with an array of policies, including state-prescribed product standards for exports. By examining the case of teak, one of the country’s most valuable hardwood timber species, this study on ex-post policy effectiveness provides empirical insights into the ways in which the Lao wood processing industry has responded to this policy change. The case of Laos demonstrates how various types of wood processors, with different interests and strategies, respond differently to state-imposed upgrade policies.

Study Area and Background

Rich Forests, Poor Industry

With official figures that classify a proportion as high as 81% of the country’s land as being forests, 1 Laos ranks among the most forested countries in the Asia-Pacific region (FAO, 2015). Continuous loss and depletion of forests, nevertheless, have diminished forest cover gradually, from around 17 million hectares to 9.5 million, between 1960 and 2010 (Koch, 2017; Phompila et al., 2017). Forest conversion to agriculture and industrial tree plantations, such as rubber and eucalyptus, along with hydropower development and mining, are known to be the main direct drivers of forest loss in Laos (Lestrelin et al., 2013; Phompila et al., 2017). Illegal logging is the main cause of forest degradation, particularly in government-managed protected forests where natural high quality timber such as balau, keruing and in some rare locations teak (e.g., Luang Prabang) can still be found. (EIA 2015). The booming wood processing industries in neighboring Vietnam, Thailand and China, which are dependent on timber imports, provide lucrative and nearby outlets for raw timber exports from Laos (To & Canby, 2017). In recent decades, stricter forest protection laws in these countries, such as the logging ban in Thailand, have even spurred timber imports from Laos to meet growing demand for raw timber while conserving domestic forest resources (Hirsch, 2006). This refers both to (1) illegally harvested natural timber traded through powerful cross-boundary patronage networks, often controlled by foreign operators (To et al., 2014), and (2) legal timber from plantations, such as planted teak (Midgley et al., 2015). While raw timber outflow has been flourishing in recent decades (To & Canby, 2017), Lao’s domestic wood processing industry has been suffering from timber supply shortages (Barney & Canby, 2011).

The wood industry sector of Laos accounts for about 6% of national GDP and plays a critical role as a foreign exchange earner (Wanneng et al., 2021). Forest-related exports, including wood products, account for about 10% of all exported products (Lao Statistics Bureau, 2023). From 2000 to 2008, timber exports increased from 100 million USD to 250 million USD, the bulk of which (approximately 95%) ended up in neighboring Thailand (25%), Vietnam (50%) and China (20%) (Midgley et al., 2015). Whereas in the 2000s a great portion of wood exports comprised logs and semi-processed products (e.g., square logs, sawn wood), with only 1.7%–3.2% being manufactured, high-value wood products such as furniture and flooring played a marginal role in wood exports (Midgley et al., 2015). Although forest resources are abundant in Laos, downstream timber processing has remained far behind its potential, creating limited value-added to benefit local economic and rural development. End-product manufacturing is dominated by large foreign joint ventures, whereas intermediate production takes place in domestic micro and small enterprises. Apart from a few larger companies involving foreign capital, Laos’s wood processing industry consists of small, labor-intensive businesses based on outmoded technology with low wood recovery rates (Barney & Canby, 2011; Smith et al., 2018).

In 1998, there were approximately 1164 wood processing enterprises in operation in Laos (FAO, 2015). Since then, the sector has experienced modest, but continuous growth (Barney & Canby, 2011). According to figures by the Ministry of Industry and Commerce (MOIC), in 2016 the total number of officially registered wood processors increased to 1595 establishments, including 40 sawmills, 482 finished product processors (secondary processing) and 1073 furniture manufacturers (tertiary processing). In addition, there were an estimated 1154 micro-scale, household-based wood processing businesses (mainly tertiary processing), of which the majority (956 enterprises) operated informally without a license (Smith, 2021).

Teak in Laos

Teak (Tectona grandis) is endemic to Northern Laos and is one of the country’s most valuable hardwood timber species, supplying international and domestic markets (Midgley et al., 2015). While the natural teak stands of Laos have virtually disappeared due to over-logging since the colonial age, the area corresponding to plantation teak has expanded gradually since the late 1970s (Phimmavong et al., 2009), and it experienced a boom in the 1990s and early 2000s (Smith et al., 2018). The current extension of teak plantations for the whole of Laos remains opaque, with estimates ranging between 28,000 (Midgley et al., 2015) and 47,000 ha (DOF 2023). Although the government of Laos has developed and improved a legal framework to promote tree plantations, investment in such initiatives remains limited, mainly due to ineffective forestry policies, inconsistent laws and regulations, and high transaction costs (Smith et al., 2021). Unlike Acacia and Eucalyptus plantations, which were established mostly based on land concessions granted to private investors, 99% of Lao’s teak plantations are smallholder-based, with average woodlot sizes ranging from 0.5 to 3 ha (Smith et al., 2021).

Growing teak was promoted in the wake of institutional reforms under the “New Economic Mechanism” policy starting in 1988, especially in the context of (forest) land allocation to households for productive use other than slash-and-burn agriculture, alongside state-initiated tree plantation promotion programs (Arvola et al., 2019; Phimmavong et al., 2009). In the 1990s planting teak became a convenient way for rural households to make bare land productive with little labor input and investment, mainly for the goal of obtaining land tenure rights (Maraseni et al., 2018; Smith et al., 2017). Due to the teak rotation cycle being long, ranging on average between 15 and 25 years, teak plays a rather marginal role in the daily livelihood considerations of smallholders. Typically, teak is considered to be an auxiliary financial asset to satisfy urgent cash needs (e.g., weddings, school fees) (Wanneng et al., 2021). Correspondingly, smallholders devote little time and effort to develop the adequate silviculture techniques, such as thinning, pruning and weeding (Midgley et al., 2007; Newby et al. 2012; Pachas et al., 2019). Smallholders have little bargaining power, and low prices discourage them from amplifying their efforts in plantation management (Smith et al., 2018). Among the reasons why the prices paid to smallholders are low is because there is no standardized and official grading system for plantation teak (Wanneng et al., 2021). It is a common practice for smallholders to sell standing trees to middlemen or sawmills on an individual basis (Ling et al., 2018). Teak prices vary across the country (Smith et al., 2018; Wanneng et al., 2021), depending on size, quality, logistic costs, and administrative costs, such as taxes and fees (e.g., harvesting inventory, plantation registration), and also due to unofficial charges along the value chain to bypass regulations on timber harvesting and trade (Maraseni et al., 2018).

Smith et al. (2018) estimate that 89% of all teak processors in Laos are small-scale and micro enterprises, while the remaining medium and large facilities comprise foreign-owned firms. There exists a wide spectrum of teak value chains in Laos in terms of length, level of integration and actors involved. In general, value chain governance is considered to be weak (Smith et al., 2018; Wanneng et al., 2021), with a low level of integration and cooperation among value chain actors (Maraseni et al., 2018).

The points made above, regarding wood processing in Laos in general, are equally true for teak. For long, gathering teak round logs, shaping them into square logs, and sending them across the border had been a popular and lucrative business model (Smith et al., 2018). In this context, Keonakhone (2006) estimated that about 95% of the plantation teak grown in Luang Prabang, the center of teak production in Laos, was exported as round or square logs. The great majority of all Lao teak exports ended up in regional markets, mostly in Thailand, China and Vietnam (Midgley et al., 2015).

Joinery products represent more than half of all teak products manufactured within Laos as Wanneng et al. (2021) recently found out. This includes ceiling and flooring products, walls and stairs, which are made from cheaper wood, mainly from immature trees with large portions of sapwood. Higher value products include doors, windows and frames, which make up about one quarter of all finished teak products, followed by furniture (Barney & Canby, 2011).

Material and Methods

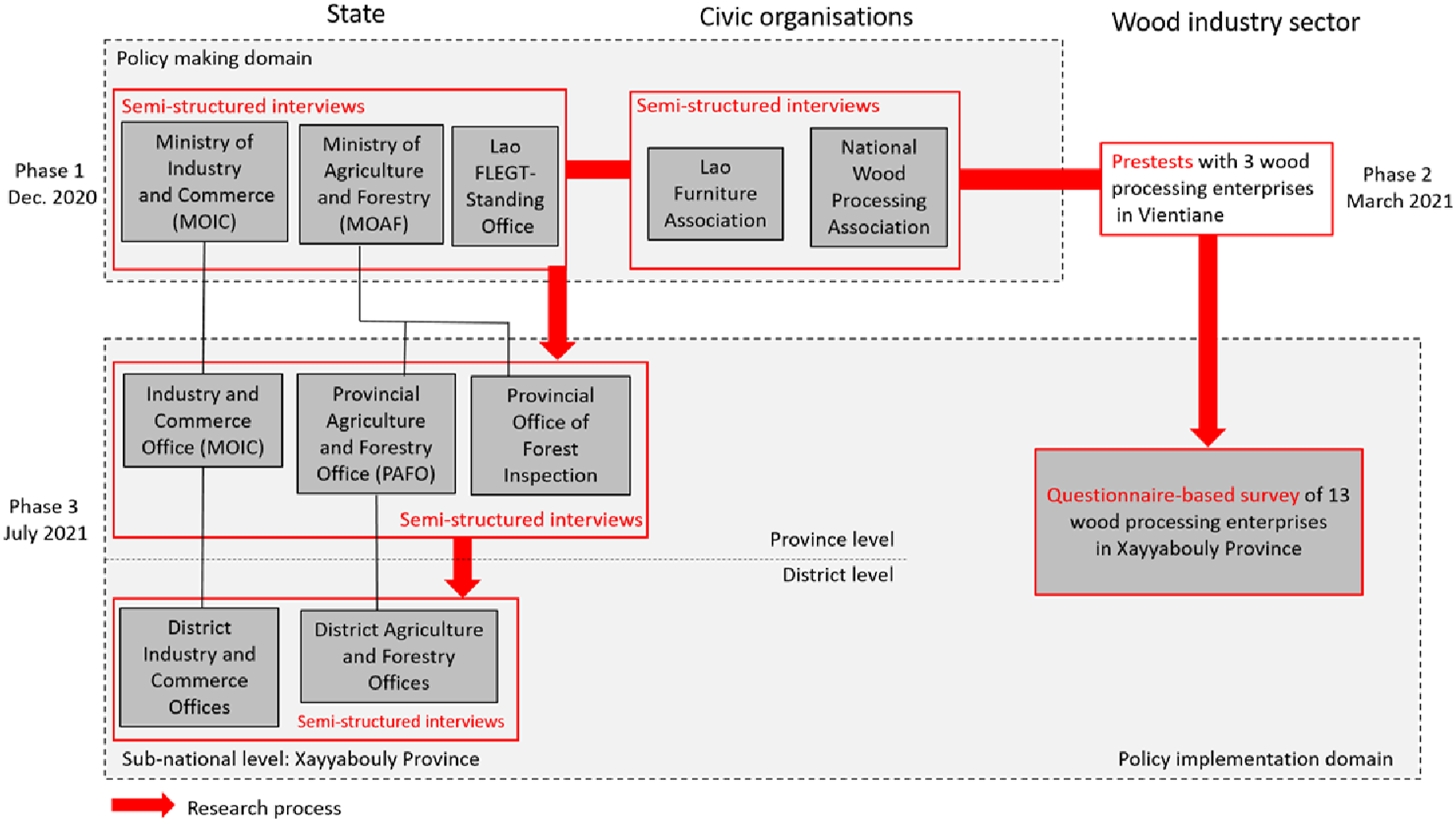

Our study adopts an ex-post perspective on recent state-imposed upgrading policies for wood processing industries in Laos. We seek to contrast policy objectives, as defined by the Lao government, with outcomes on the ground, drawing conclusions on policy effectiveness (Wollmann, 2007). Ex-post policy evaluation can involve quantitative and qualitative social science research. While the first is commonly used to assess policy performance based on quantitative indicators (Yang, 2007), qualitative methods allow for more nuanced interpretations of policy outcomes (Yanow, 2007). As both are relevant for our study, we deployed a dual method research design.

Laos is one of the few remaining post-socialist countries worldwide. As such, governance has remained unicentric, with policies being made solely at central-level state agencies. Sub-national and non-state actors (e.g., civil society organizations) are then charged with policy implementation in line with central provisions (Creak & Barney, 2018), and this applies to forest governance and policymaking (Mustalahti et al., 2017; Ramcilovic-Suominen et al., 2019). Hence, in the first phase of our study, concerned with agenda setting and policy formation, we focused on policy formation at the central state level. Apart from analyzing relevant policy documents, we also conducted semi-structured interviews with experts in the relevant line ministries: (1) The Ministry of Agriculture and Forestry (MAF) which is in charge of forestry and timber production; and (2) the Ministry of Industry and Commerce (MOIC) which is in charge of wood industries and wood products. Furthermore, we interviewed the Laos Furniture Association and the National Wood Processing Industry Association, the country’s two most prominent wood-related business associations. It is worth noting that since 2022, after our fieldwork was completed, numerous responsibilities tied to wood industries have been gradually shifted back from MOIC to the MAF.

To appraise how recent policies have unfolded on the ground, we selected Xayyabouly province as a case study (Figure 1). Located in Northern Laos, Xayyabouly is one of the country’s most important teak producing and processing regions. Apart from teak plantations, the province accommodates some of the few last natural teak stands in Laos, accounting for 300 ha in total (Panyasith et al., 2018). With previously over 100 formally registered wood-based companies, timber processing teak in particular, has played a vital role in the provincial economy. To understand policy implementation at the sub-national level, we conducted expert interviews with the provincial departments of the aforementioned line ministries (Department of Agriculture and Forestry, Department of Industry and Commerce) and their subordinate district offices. First-hand empirical insights on how recent policies have affected wood-based industries at the enterprise level were gained through a standardized survey with the 13 remaining wood processers in the province, encompassing all formally registered operators across Xayyabouly province at the time of the survey (July 2021) (Figure 2). Descriptive data on ownership, size, product portfolios, production volumes and other firm-characterizing indicators were collected, comparing the situation before and after policy changes came into force. In this regard, we referred to the year 2015 as a baseline and used 2021 as reference year for comparison. To draw a more nuanced picture, a cluster analysis approach was deployed to analyze the survey data according to three different enterprise types. Laos and Xayyabouly province. Source: Own drawing by the authors. Overview of the research design and research process.

Results

Policy Formation in the Laos Timber Trade and Processing Industry

After 2000, Laos experienced steadily increasing government efforts in the regulation, control and management of wood processing industries. This included measures to classify processors along manufacturing stages and to standardize wood products along legally defined product categories. Together, these measures aimed to upgrade domestic processing industries in order to increase value added in Laos, instead of exporting raw timber or sawn wood to obtain only meager benefits. At the same time, the government restricted natural timber use while promoting plantation timber as a substitute to natural timber, to be used as raw material for the domestic wood industry. The following section examines major policy changes.

From Natural Timber Extraction to Plantation Forestry

In 1999, Prime Minister Order (PMO) No. 11/1999 restricted the export of logs from natural forests. This policy shift was followed by PMO No. 10/2000 and PMO 15/2001 in the subsequent years, imposing export restrictions on unfinished wood products such as logs, sawn timber and semi-finished wood products from natural forests. Use restrictions on natural timber made plantation timber more attractive (Pimmavong et al., 2009). In the subsequent years, however, plantation forestry remained in an inchoate state (Smith et al., 2021), and thus was unable to close the timber supply gap. After 2000, the government promoted plantation forestry increasingly, through an open-door investment program meant to stimulate production-driven reforestation of bare and degraded forest land (Smith et al., 2021). Plantation timber was considered as a substitute to replace natural timber to be used for the national wood processing industry. In 2002, the government issued PMO (18/2002), which fully prohibited exporting logs and sawn timber from natural forests. This aimed to encouraged wood processors to invest in their own timber plantations to ensure a supply of raw material in the long run. Although the subsequent plantation boom was dominated by fast-growing species, eucalyptus and rubber in particular, sector liberalization also attracted foreign capital inflow in export-oriented hardwood timber processing and manufacturing, such as teak. In 2005, the Forest Strategy to the Year 2020 identified teak as a potential species for sustainable plantation development and input for export-oriented, high-value wood processing. In 2013, in response to the depletion of production forests, the government issued PMO 31 to temporarily close production forests to logging. As a result, the available commercial timber supply, which now comes mainly from plantations, continued to decline. In 2016, PMO 15 on Strengthening Strictness of Timber Harvest Management and Inspection Timber Transport and Business fully prohibited logging in natural forests. Hardwood timber such as natural rosewood and natural teak dropped out as a raw material for high-value wood products, making domestic processing increasingly reliant on plantation timber, mostly teak from smallholders. The 2019 Forest Law (article 95) strengthened additionally the transition towards plantation timber in wood processing, as it requested wood processors to ensure the exclusion of natural timber.

State Efforts to Control Domestic Wood Industries

In Laos, the first national policy initiatives targeting industrial wood processing date back to the 1990s. In 1999, the government promulgated the Industrial Processing Law (1999) which defines different types and sizes of businesses, including those involving wood processing and handicrafts. In the subsequent years, more legal amendments refined the wood industry classification system further (e.g., the revised Law on Industrial Processing, 2013). Most pivotal in this regard was Decision No. 0719 on Timber Processing Manufacture Standards, which was issued in 2009 by MOIC. Drawing on investment capital, mechanization levels, production capacity, number of staff and product portfolio as key defining criteria, it categorized the national wood industry in a tripartite system of enterprises: • Micro-processors and household-based manufactures, which produce semi-finished or finished wood products such as furniture, household and handicraft products; • Level I processors, comprising sawmills and manufactures of semi-finished products such as sawn wood, construction wood and other semi-processed wood; • Level II manufactures that produce finished timber products.

Business registration and sector-specific licensing became a major policy instrument to monitor and regulate wood processing operations, to enforce compliance with existing rules and to encourage processors to participate in the formal economy. Through stricter registration and documentation obligations, the state aimed to increase control over the sector and to enforce its policies. According to the Law on Enterprise (2013) all enterprises must be registered with the MOIC, or more precisely, its provincial departments. Regarding wood processing specifically, since 2007 Decision No. 1301/MOIC on Timber Processing Management requires timber processors to apply for licenses granted by the provincial departments of MOIC on an annual basis. With the promulgation of PMO 15, companies without registration and license were forced to shut down or temporarily suspend their businesses. This affected to a great extent those household-based and micro enterprises that were unable to match state-imposed standards on production and sourcing. Most recently, the 2019 Forest Law (Article 104) stipulates that any operations of forestry businesses require permission from MOIC (business registration) and MAF (technical approval).

After 2000 the government bundled wood processing enterprises organizationally into specific, state-affiliated business associations, with the aim to enhance cooperation within the business community and to create state-industry interfaces to facilitate exchange, sector promotion and policy implementation. In this context, in 2005, the National Wood Processing Industry Association (NWPIA) was established on the initiative of MAF. One year later it was transferred to MOIC, to then be handed over back to MAF in late 2022, in order to operate under the umbrella of the National Chamber of Commerce and Industry. With 128 members (2007) from across the country, NWPIA represents a major part of the national wood processing industry, mainly larger, export-oriented companies. In addition, in 2003 MOIC initiated the Lao Furniture Association (LFA) which is currently under the supervision of MAF.

State-Imposed Wood Product Standardization for Industry Upgrading

State-defined product standards that intend to increase quality to achieve greater value added within Laos have become a major policy instrument, deployed by the Lao government over the past two decades, for the purpose of upgrading the wood industry. In 2008, MOIC issued Decision No. 1415 on the Form and Size of Timber Products, stipulating uniform product standards across the country for three categories of timber products: (1) sawn timber, (2) semi-processed wood timber products (veneer, joinery products, wood for housing), and (3) finished timber products (plywood, flooring and parquet, furniture). In this context, product registration with state agencies was adopted to regulate exports, based on pre-defined forms, size and type standards. This qualified only high-value manufactured products for export. Processors became obliged to report on their activities on a quarterly basis, including input and output planning, while the provincial Departments of Industry and Commerce (DOIC) - now the Provincial Agriculture and Forestry Office (PAFO) – was meant to monitor and check the implementation at local level.

In 2015, Decision 2005/MOIC, replacing Decision 1415/MOIC, further defined categories of wood products, including their type, form and sizes (thickness, width and length). The goal was to facilitate the management of production, use and distribution of wood products. Processors were requested to list their products with the provincial DOIC quarterly, as a basis to control compliance with standards, and to control raw material inflows and product outflows of wood processors. In 2016, PMO 15 suspended the export of logs, sawn timber and any other (unfinished) wood product that did not comply with the standards set in Decision (2005)/MOIC and Decision 0002/MOIC, the latter of which was released in 2018 to provide even more detailed standards for export products, distinguishing between natural wood products and those made out of plantation timber.

The log export ban, in conjunction with the rigid standardization of export products, pursued the following policy objectives: • To shut down small processors that operate illegally without license beyond the state radar. • To discourage small and household-based enterprises from wood processing (sawing and cutting timber for commercial use), or, alternatively, to integrate them into wood clusters to adopt higher quality standards and process timber into final products. • To shut down registered, legal companies that are unable to match manufacturing standards stipulated by the government, and to increase pressure on the remaining enterprises to upgrade and manufacture according to the standards for more value added to be created in Laos.

To a certain extent, these policy changes unfolded under the growing influence of global forestry policy ideas. These were widespread in Laos, along with intensified engagement by international organizations and development agencies. Most recently, the FLEGT has played a pivotal role regarding wood processing and trade since 2012, when the Lao government indicated its interest in joining the Voluntary Partnership Agreement (VPA). Therefore, it is not a coincidence that Decision 2005/MOIC and PMO 15 were released when Laos intensified its FLEGT engagement with the European Union through concrete projects on legal reforms and provincial pilot programs.

Macro-Level Observations on Policy Effects in Wood Processing

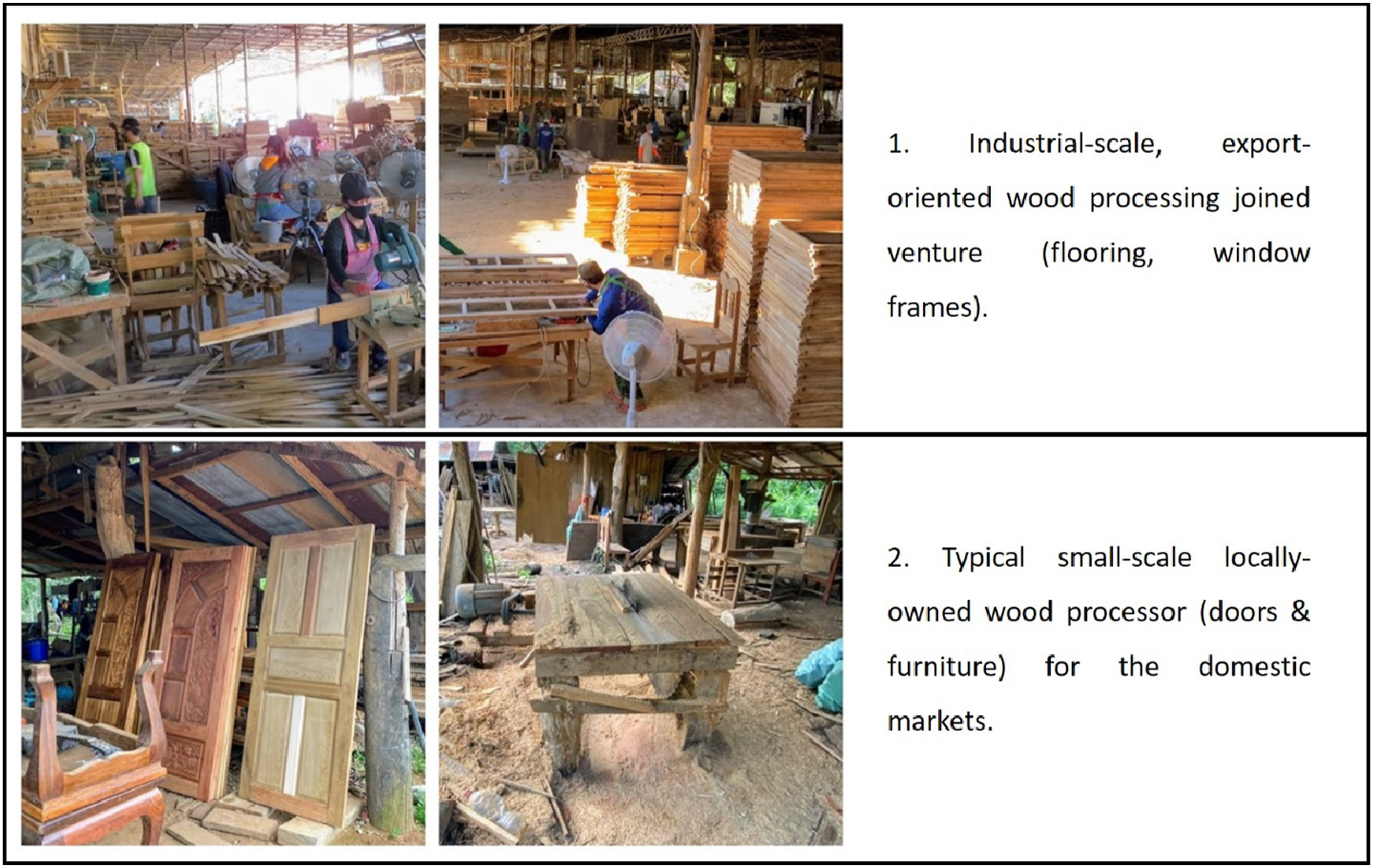

Before Decision 2005/MOIC and PMO 15 came into force in 2016, figures from provincial authorities listed 111 wood processing establishments in the Xayyabouly province, with a wide spectrum of operational scales. Thereafter, the changing policy environment forced 98 of them to shut down or to temporarily suspend their operations. (Figure 3) Consequently, when our survey was carried out in July 2021 the remaining wood processing companies accounted for only 13 establishments throughout the entire province. According to the provincial authorities, the majority of the dissolved companies comprised small-scale processors with no capacity to adapt to the challenging quality standards stipulated by the government. Others fully relied on natural timber harvested in the course of the implementation of projects involving hydropower dams, mining and infrastructure, and development, and thus they lost their sourcing base overnight. Teak processors in Xayyabouly. Source: Photos taken by the authors in 2021.

Micro-level Perspective: Policy Responses of Different Wood Processors in Xayyabouly Province

Enterprise Characteristics and Types

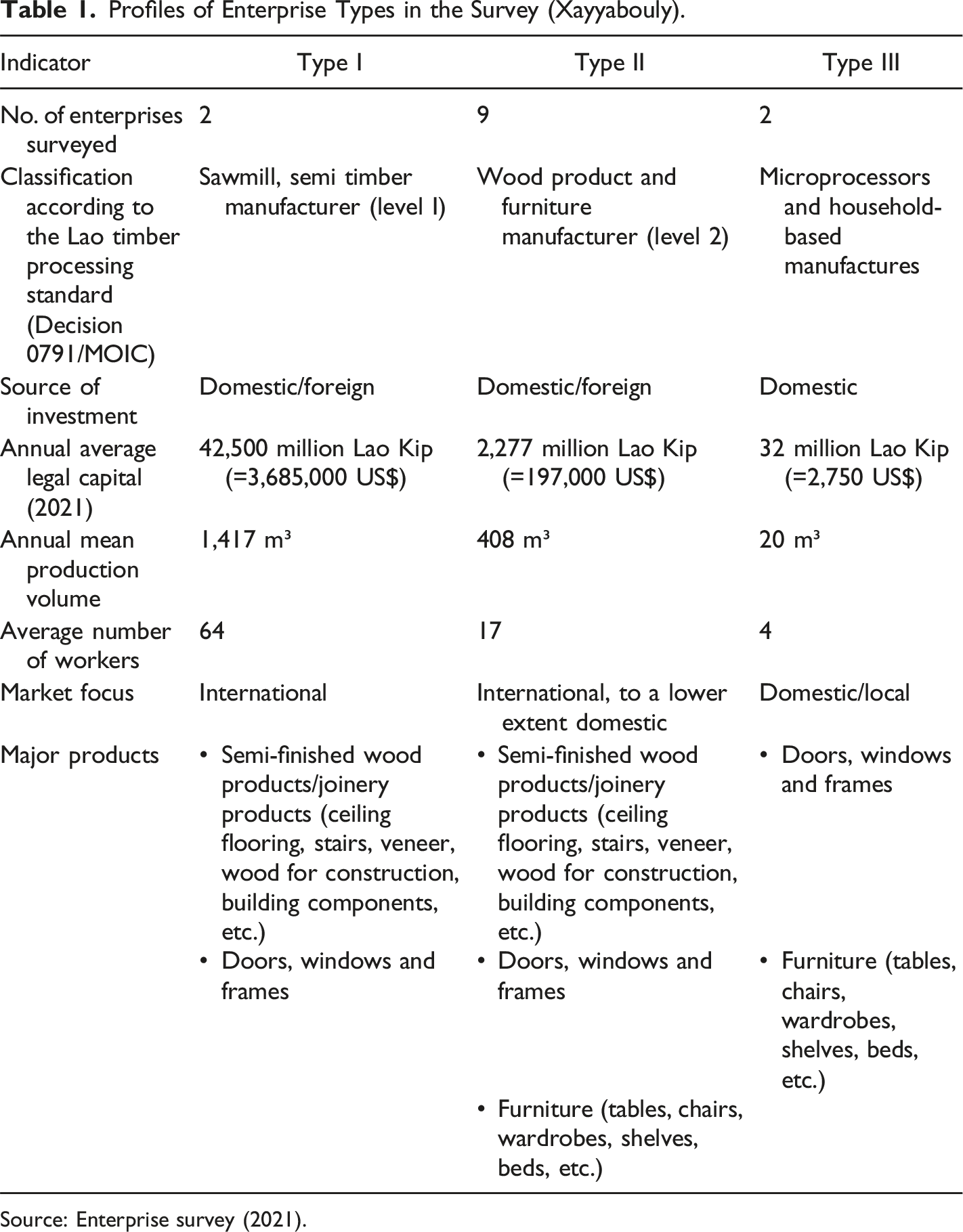

Profiles of Enterprise Types in the Survey (Xayyabouly).

Source: Enterprise survey (2021).

We found type I companies to consist of larger sawmills, mostly involving foreign capital. These companies integrate several processing steps and have rather diverse product portfolios, consisting of semi-finished, joinery wood products such as ceiling, flooring and stairs, and also doors, windows and frames. With 90% of these products being sold abroad, type I companies pursue export-oriented business strategies. Type II processors are much smaller in size and, by tendency, have a more nuanced product portfolio, ranging from semi-finished, joinery products (the same as with type I companies) to different kinds of furniture. With 73% of their revenues on average generated abroad, their focus is on international markets, whereas domestic markets play a secondary role. In both type I and II companies we found foreign capital involvement, stemming mainly from Thailand, which is also the main export market for these companies. In contrast, type III enterprises are rather small in size and comprise household-based microprocessors operating with rudimentary technology and producing small quantities solely for domestic markets. Their major finished products are doors, windows and frames, as well as different kinds of furniture.

Raw Material Sourcing

Teak Demand of Enterprises (n = 12). 3

Source: Enterprise survey (2021).

Although timber sourcing strategies appeared to be diverse across the enterprise sample, all companies emphasized the vital role of middlemen and traders. As for type I companies, state-run timber auctions are most critical, followed by sourcing through middlemen and traders, with whom they often sustain long-lasting relationships on the basis of oral agreements, and in some cases formal contracts. Occasional purchases from unacquainted suppliers were also mentioned, but seem to be less common in the sourcing strategies of larger companies. Buying directly from smallholders appears not to be an option for them due to the insufficient quantities offered by single teak growers and the correspondingly high transaction costs.

Type II enterprises indicated a large variety of sourcing strategies, including buying through traders and other sawmills, their own teak plantations and purchasing directly from smallholders. Fixed suppliers seem to be common, with transactions based on both oral agreements and formal contracts. This is complemented by occasional purchases from infrequent suppliers, most likely directly from smallholders.

As for type III enterprises, buying directly from smallholders appears to be common practice, mostly in form of ad-hoc, one-off transactions. Long-term relationships with single smallholders, however, appear to be exceptional, most likely due to the long rotation cycles and infrequent harvesting patterns common among smallholders.

Notably, all enterprises claimed to source their raw teak solely within the Xayyabouly province, referring to complicated and costly administrative procedures (e.g., taxes, permits) as key obstacles to cross-provincial timber trade in Laos. While supply is short, the demand for teak has also recently dropped for most processors.

In recent years, government policies encouraged wood processors to invest in their own timber plantations, and 6 out of the 13 enterprises stated that they possessed their own teak plantations. The size ranges between 115 ha, owned by a type I enterprise, and 1 ha owned by type II and type III enterprises. Four of these investments are more than 20 years old, dating back to when the government began promoting plantation forestry. The age of these plantations ranges from 8 to 35 years. Securing (future) timber supplies and complying with government policies were mentioned as the main motivators for growing teak in their own estates.

The logging and export ban imposed by the Lao government has had strong impacts on the domestic teak sourcing markets. The majority of companies (10) experienced rising prices for plantation teak, and at the same time complained about the dwindling (6) and stagnating supply (3) they have experienced over the past 5 years. Supply shortage was raised as the main challenge in raw material sourcing. The reasons behind this, as stated by the companies, are the increasing demand for plantation teak due to the logging ban. Consequently, timber supply has decreased, entailing increasing prices and harsher competition in the wake of PMO 15. At the same time, the willingness of smallholders to replant teak decreased, in light of increased market demand for agricultural cash crops such as cassava, bananas or grazing land for livestock. Rising plantation teak prices largely affects processors, as timber sourcing on average accounts for 43% of their production costs, a figure which in the case of smaller enterprises goes up even to 50%.

Social Capital and Value Chain Collaboration

Cooperation among chain actors, both vertically and horizontally, can be instrumental for value chain and industry upgrading (Mitchell and Coles, 2011). This includes collaboration in loose producer networks or more structured organizational arrangements, like cooperatives and associations at different scales. This facilitates sourcing, processing, marketing and sales (Kilelu et al., 2017; Mesquitta and Lazzarini 2008). The NWPIA and the LFA, both operating under the umbrella of the Lao National Chamber of Commerce and Industry, are the two most important business associations representing the wood processing industry. Membership in at least one of the two associations appears to be more likely the larger a company is. While type I enterprises indicated membership in both associations, the majority of type II enterprises declared membership in at least one of both associations. In contrast, none of the type III enterprises held membership in any association. Enterprises stated that the benefits derived from these memberships were moderate, and included mainly improved access to information (on laws and policies, markets, sourcing, technologies, etc.), partial training and capacity building, and the exchange of experiences among members.

When it comes to horizontal cooperation among wood processors, collaboration seems to be relatively common among type I and III enterprises, but less so among type II enterprises. The ability to join forces in the marketization of products, raw material sourcing as well as the exchange of technology were stated as the main reasons for companies to seek strategic cooperation with one another. Maintaining long-term, stable customer relations was most pronounced among type I enterprises, particularly regarding international customers in foreign markets. In type III and II enterprises, the precise number of clients was unknown and much more in flux.

Policy Response at Enterprise Level

The literature shows a wide spectrum of approaches that target value chain upgrading strategies, focusing on processes, products and functions, with the aim of facilitating the shift from lower-to-higher-value economic activities (Gereffi, 1999; Gibbon et al., 2008). This includes adopting new technologies, adding new or improved products to the portfolio or accessing new markets (Humphrey and Schmitz 2002; Trienekens & van Dijk, 2012). As outlined earlier, upgrading policies in Laos leveraged mainly industry and product standardization measures. These policies had the aim of forcing companies to invest in new technologies and to improve existing products, or to develop new ones. These actions would achieve greater value added in Laos and enhance competitiveness in international markets.

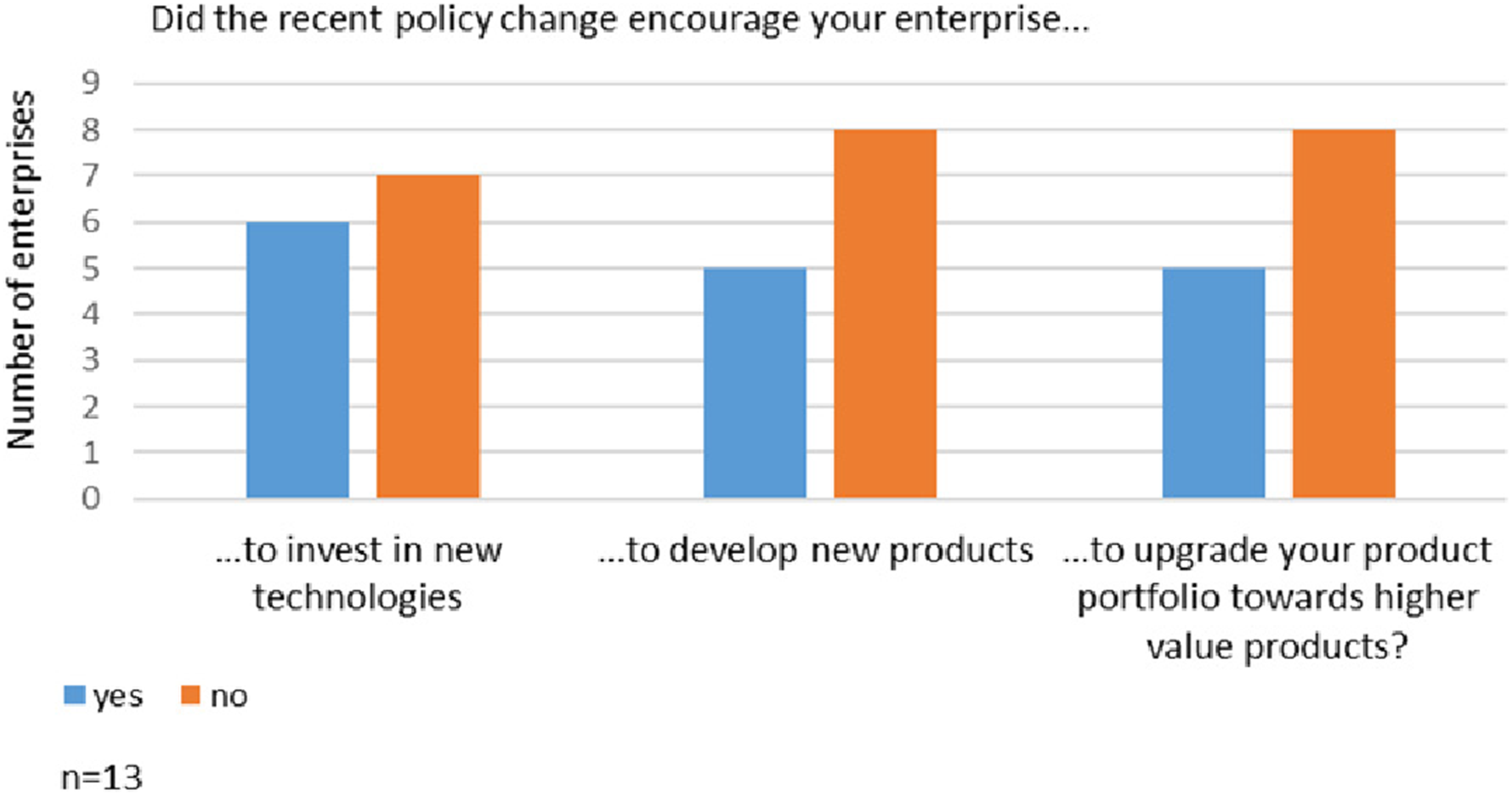

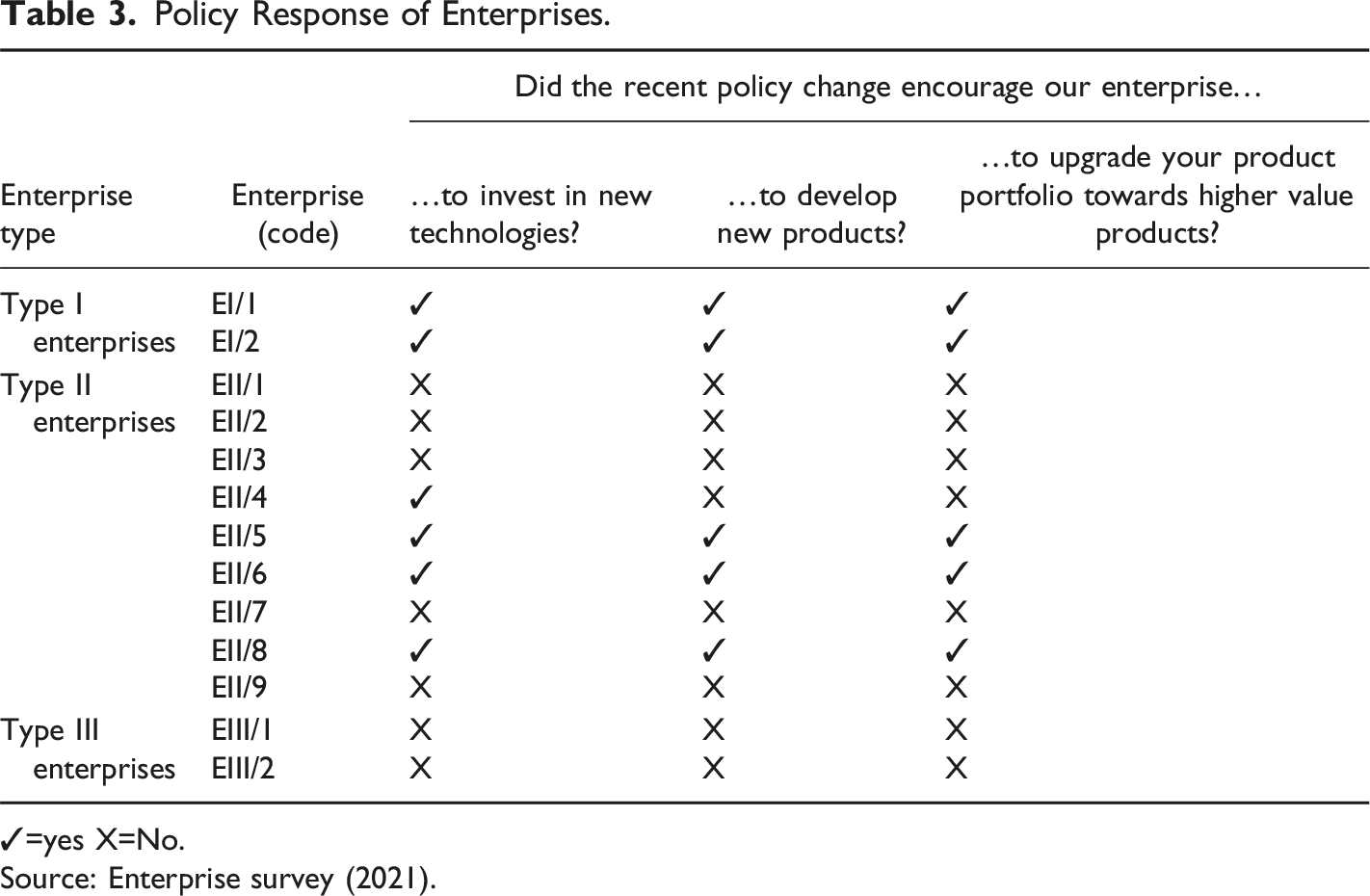

Figure 4 shows that only a minority of the companies that survived the drastic policy interventions invested in new technologies or product upgrading measures as envisaged by the government. Table 3 indicates that policy responsiveness was high among type I enterprises and, to a more limited extent, among type II enterprises. This manifests itself in technology and product upgrading investments, mainly for the purpose of expanding their business scope towards export markets and the necessary legal compliance. Furniture manufacturing was mentioned in this context most frequently. In contrast, policy response among type III enterprises was totally absent. Enterprise response to state-directed upgrading measures. Source: Enterprise survey (2021). Policy Response of Enterprises. ✓=yes X=No. Source: Enterprise survey (2021).

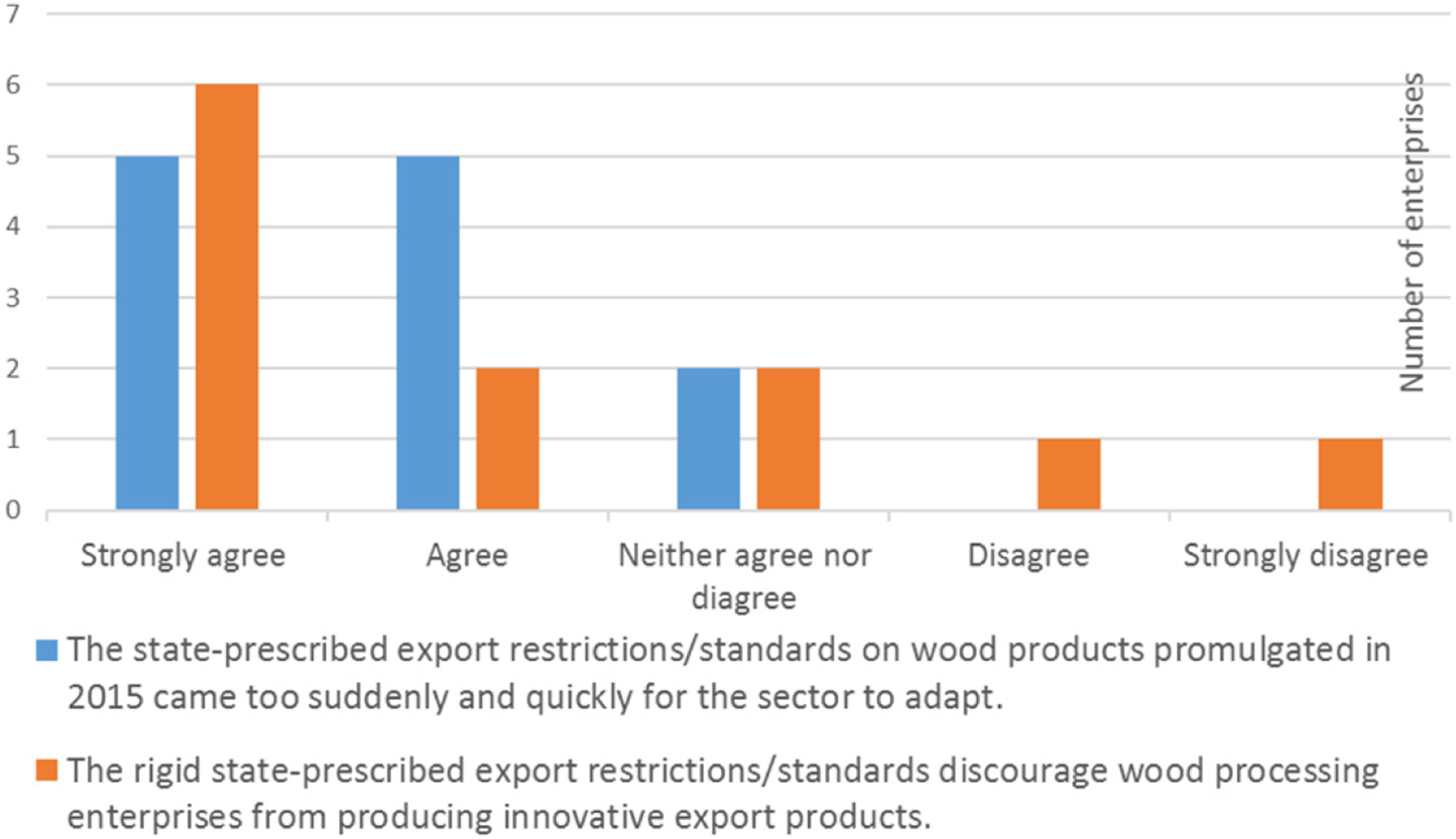

When asked about the positive effects they may have observed in light of recent policy changes, companies mentioned the efforts made to halt timber speculation and the export of unprocessed timber. They also believed to have observed positive trends in forest protection, but in part they lamented the banning of natural timber for sourcing. Efforts regarding the processing upgrade and the modernization policies were also viewed favorably. The regulations, however, were seen as being too general and too imprecise, and companies also complained that said regulations were too sudden, leaving insufficient time for them to adapt properly. The strict state-prescribed export restrictions in the form of product standards were considered to be too narrow, leaving only a limited space for companies to come up with new, innovative products (Figure 5). In this context, processors also complained that the narrow standards did not correspond to export market demands. Enterprises’ perception of policies (n = 12).

4

Source: Enterprise survey (2021).

State-Enterprise Interfaces

The state is increasingly tightening its control over timber trade and processing to strengthen policy enforcement and ensure legal compliance. All enterprises surveyed in Xayyabouly reported increased numbers of state inspections during recent years. This includes visits by the local authorities in charge of forestry, the environment, taxes and social/labor requirements. Apart from safety and tax issues, inspections included raw material sourcing and product standards. State control increased, but wood processors were offered very limited state support to expedite and ease business upgrading and legal compliance. When asked about public support schemes, access to market information and trade fairs were the main support mentioned by the companies surveyed.

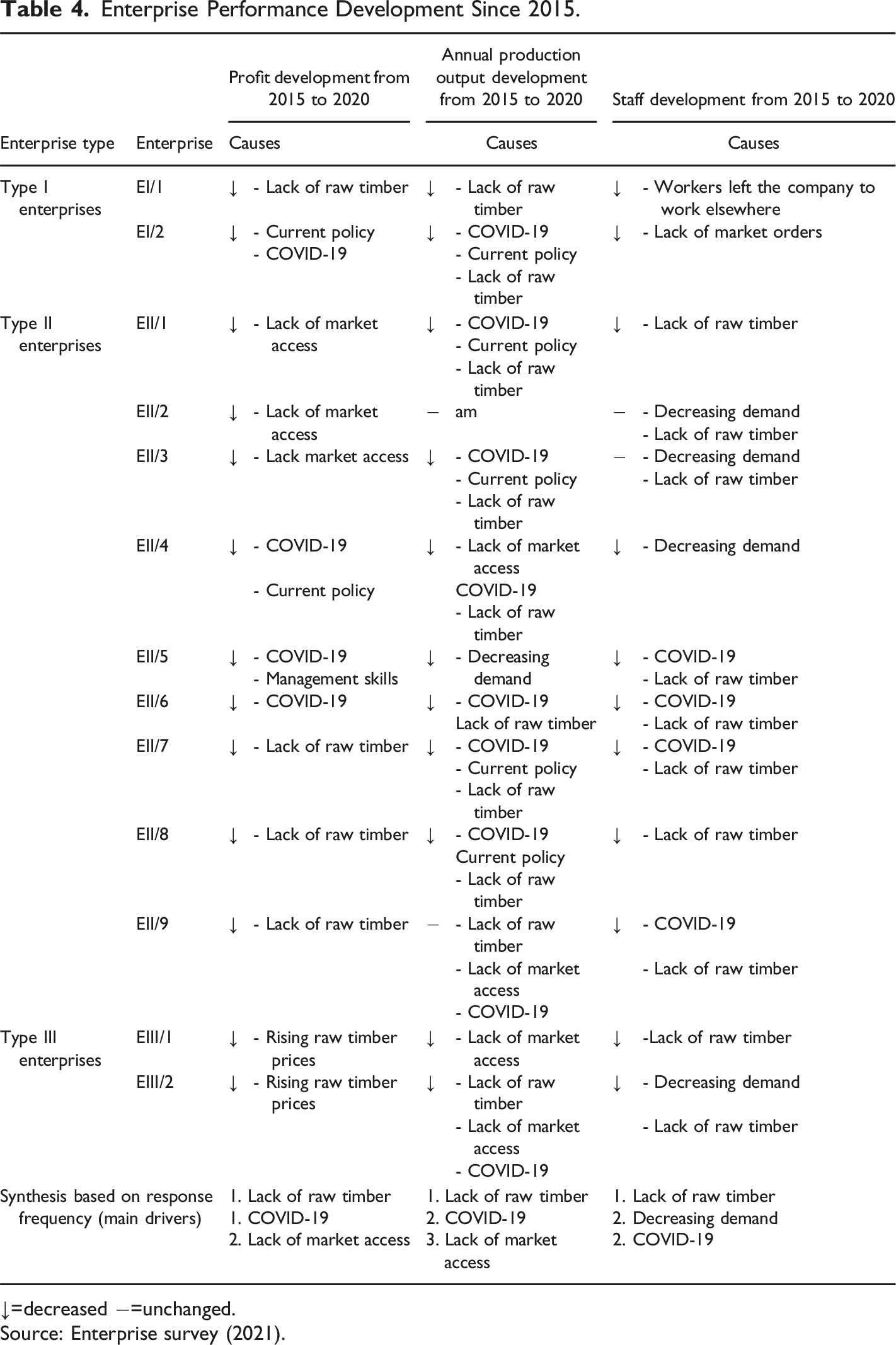

Enterprise Performance since 2015

Enterprise Performance Development Since 2015.

↓=decreased −=unchanged.

Source: Enterprise survey (2021).

Discussion and Conclusion

Our study investigated how increased state control over timber trade and processing in Laos aimed to transform the national forest sector from a raw timber supplier to an export-oriented wood processing cluster with higher value products. Policies aimed at reducing raw timber exports date back to the 1990s. Since 2015, these policies have intensified, as exemplified by PMO 15, which not only prohibits the harvesting of natural timber, but also bans the export of unprocessed timber. In addition, strict product standards have been enforced on export-oriented manufacturers. However, the upgrading policy should not be misinterpreted as merely a proactive policy measure to modernize wood processing for greater value addition in Laos. It was also a necessary response to the reality of reduced commercial timber supply resulting from the closure of the national production forest estate and protected natural forests several years earlier. Given the small amount of exploitable timber remaining, mainly from plantations, the government increasingly recognized the need to downsize and rationalize the sector to operate more efficiently.

These policy changes brought about profound implications for the entire wood processing sector. A recent countrywide study (GIZ 2021a) revealed that, as envisioned in PMO 15 and related regulations, exports of finished wood products have indeed increased, while those of unprocessed products dropped. Though this policy change is likely to have decreased raw timber exports and to a certain extent prevented further forest degradation (Forest Trends, 2021), it came at a high socio-economic cost. A considerable number of wood operators did not survive the intended transition from unfinished to finished wood products due to their inability to adapt to the changing regulatory environment. Our results from Xayyabouly province mirror this trend. By mid-2021, the number of operators had dropped sharply across the province. It was particularly the small and micro-level processors, many with a focus on sawmilling, that stopped operating. We found two main causes behind this mass closure. First, natural timber intake increased competition for the remaining legal sources of wood (e.g., plantation teak) and, according to the companies surveyed, has resulted in higher prices of raw wood. This is critical, as raw material costs make up a great portion of total enterprise expenditures in the Lao wood industry (Maraseni et al., 2018). Second, the rigid and narrow product standards, in conjunction with the log export ban, forced a great number of operators, small-scale sawmills in particular, to shut down. These findings correspond with other studies documenting massive shutdowns, in particular in the Northern part of Laos (GIZ 2021a). Consequently, according to government figures, the sector as a whole experienced a sharp decrease, from 2788 wood operators in 2016 to 1157 as of December 2020, across all of Laos (GIZ 2021b). Official government figures indicate 947 wood processing enterprises in Laos for the year 2023, including 4 sawmills, 367 finished product processors and 567 furniture manufacturers (DOF, 2023).

Regarding industry upgrading, which was promulgated as a major policy objective, our cluster analysis in Xayyabouly revealed that, among the remaining companies, only larger processors made cautious upgrading and modernization efforts, including investment in technologies and product upgrades for more value added. Large investments in their own teak plantations to secure wood supply through integrated sourcing have also only been made by large operators. The few remaining smaller operators we encountered, however, were not responsive to any of the recent command and control interventions by the central government. State support schemes, providing critical incentives and guidance for enterprise upgrading such as trainings, subsidy and loan programs, technology transfer schemes (Kaplinsky et al., 2003; Trienekens & van Dijk, 2012), are still inadequate to facilitate the transition towards higher value products in Laos. Rather than the current top-down policy approach, an equal partnership between government and business would be needed for effective policy-making, as demonstrated in the case of Malaysia’s furniture industry (Boon-Kwee and Thiruchelvam, 2012). Furthermore, the scarce support provided through the two main wood-related business associations only reached those larger operators who are their members, but miss to reach smaller, partly informal operators. In sum, the case of Laos shows that a policy approach based solely on coercion and without sufficient incentives appears to be rather inappropriate.

Based on our findings in Xayyabouly and studies confirming the same trend elsewhere in Laos (GIZ, 2021a; 2021b), we found the wood processing sector to be undergoing a severe crisis, manifested in dwindling annual profits, decreasing production outputs and shrinking staff numbers in all surveyed enterprises. As this downturn occurred in the middle of the COVID-19 pandemic, however, it is rather difficult to attribute it solely to the changing regulatory environment. Processors mentioned both COVID-19 and PMO 15 as having a significant impact on their businesses. Now that the pandemic is over and international trade gradually recovers, further research would help to better understand the magnitude of the effects that policies have had on the sector. Moreover, including those wood processors that shut down in any future research would be beneficial to our understanding of the precise reasons for company closures.

Recognizing the drastic impact on domestic wood industries, only three years after PMO 15 was promulgated, the government revised its policy course again. Whereas exports of natural timber in any form remains strictly banned, plantation wood products, which includes teak, can now be exported again in any size, regardless of whether they are processed or unprocessed. Although processors raised concerns about the recent abrogation of the export ban on logs, fearing a further reduction in raw timber availability, they welcomed the reintroduced flexibility on export product standards. In this context, the Lao government issued Decision 1044 in 2023, which further refined the country’s wood processing industry categorization system into a more nuanced four-tier system. Under the new regulatory environment, small manufacturers and even family-based furniture processors are now formally considered an integrated part of the country’s wood industry. This provides the basis for more precise, targeted policy-making, at least for those small enterprises that are willing and able to modernize their operations.

Our study revealed that the Lao wood industry comprises a diverse spectrum of businesses, many of which are entangled within domestic and international timber value chains, but follow these different and specific business strategies. Yet state-directed upgrading policies have focused solely on larger operators with the potential to modernize and upgrade, often supported by foreign investment, and they have largely ignored the need of small and micro, informal, domestic enterprises in policymaking. Seemingly, the government deemed the latter to be economically inapt, stigmatized them in the context of illegal logging, and finally sacrificed them. The critical role of small-scale, informal value chain actors in the wood industry, and for rural development and livelihood security in rural Laos, however, has been emphasized in a recent study by Smith (2021). Hence, a more holistic perspective is required when it comes to policymaking in wood industry upgrading, not only to create added-value, but also to boost rural development in the Global South.

Research on business strategies in the rural Global South underscores the preference among small-scale and micro entrepreneurs for livelihood security over growth orientation. This makes them rather reluctant to invest in large-scale business upgrading and expansion, which comes with high risk (Berner et al., 2012; Mead & Liedholm, 1998). Following this rationale, the case of Lao PDR exemplifies the need for more nuanced policy measures when dealing with wood industry upgrading. Instead of imposing one-size-fits-all policy approaches on the sector as a whole, tailor-made interventions that consider the diversity of value chain actors and take into account their specific needs may yield better results. Promoting industry clusters through upgrading policies that allow for vertical and horizontal value chain integration could be an option to create benefits for all potential value chain actors. Auch and Pretzsch (2020) have shown for forest-based products that so-called participatory innovation platforms (PIPs) can be instrumental in exploring integrative and long-term upgrading strategies with chain actors as a basis for policy-making. Further research would be needed to determine whether PIPs could also be considered as an entry point for the four-tier industrial system in Laos. A facilitator role to initiate and facilitate the whole process could be played by the two national wood industry associations.

Footnotes

Acknowledgments

We are grateful to the experts from the Government of Laos and the local authorities in Xayyabouli Province for their active support to this study. We especially thank all the wood processing enterprises we interviewed for their willingness and efforts to participate in this study. Further, we are grateful to the two anonymous reviewers for their critical and constructive feedback.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Bundesministerium für Umwelt, Naturschutz und Reaktorsicherheit [18_III_085_Southeast Asia_A_FLR_Partnership]. The funding agency was not involved in this research.