Abstract

Numerous studies argue that corporate social responsibility (CSR) helps companies build strong and positive relationships with consumers. However, it is not well understood why certain companies are more effective in their CSR activities than others. Some studies have attributed this difference to the country setting, but results are inconclusive. Building on signaling theory, this study explores corporate transparency as a boundary condition of the effects of CSR activities on the consumer–brand relationship. Three experiments and one large survey across three countries examine how a lack of corporate transparency undermines firms’ CSR efforts. Importantly, the authors theorize that country environments differ in terms of transparency, which is then reflected in different levels of corporate transparency. Different country levels of transparency help explain the discrepancies of CSR effectiveness for increasing brand attachment and building consumer behavior. Finally, the authors tie the diminishing effect of CSR in the case of low corporate transparency to an increase in consumer skepticism.

Prior research has suggested that companies’ successes with corporate social responsibility (CSR) are mixed when it comes to the influence of CSR efforts on consumer behavior (e.g., Sen and Bhattacharya 2001). Consumer doubt, for instance, is known to disrupt CSR effectiveness (e.g., Skarmeas and Leonidou 2013), and we argue that mixed CSR success may be explained by differences in additional corporate signals consumers use to alleviate skepticism. According to Julie Sweet, chief executive officer of Accenture, “Transparency builds trust and it’s critical in a crisis” (Financial Times 2020). If so, firms may find corporate transparency a suitable facilitator to enhance CSR effectiveness. Building on Liu et al. (2015), we consider corporate transparency as a firm trait that determines whether the information provided is objective and accessible to its stakeholders. The importance of corporate transparency has been emphasized in recent business studies in contexts such as accounting (e.g., Bushman, Piotroski, and Smith 2004), corporate management (Bernstein 2017), and service offerings (Liu et al. 2015). However, despite the increased attention to transparency in business research, to the best of our knowledge, transparency has been connected to CSR only as a prerequisite in CSR reporting (Dubbink, Graafland, and Van Liedekerke 2008; Fernandez-Feijoo, Romero, and Ruiz 2014). The general influence of corporate transparency as a boundary condition of CSR effectiveness remains less understood. In particular, it is unclear whether corporate transparency moderates the central link between CSR and the consumer–brand relationship (or brand attachment, our proxy for the latter variable; Kull and Heath 2016).

The international marketing literature has discussed different moderators to CSR effectiveness but produced inconclusive results (see Web Appendix 1). Importantly, country environments differ in terms of their transparency, which sets a framework for different levels of corporate transparency (for a literature review of country-level antecedents of corporate transparency, see Web Appendix 2). Thus, different levels of corporate transparency by country may help resolve the puzzle of why there are discrepancies in CSR effectiveness between countries. Given the rising importance of CSR among today’s businesses, with CSR spending at approximately $20 billion a year for Fortune Global 500 firms alone (Meier and Cassar 2018), we believe that it is important to examine whether and how corporate transparency serves as a condition for CSR effectiveness.

This study makes several contributions to the current marketing literature. First, it contributes to the literature on corporate social responsibility. Specifically, we find that transparency is an important boundary condition of CSR practices, thus enriching the understanding of when and why CSR benefits a company. While the marketing literature suggests that both company-specific factors (e.g., CSR issues, product quality) and individual-specific factors (e.g., consumers’ personal support for the CSR issues, their general beliefs about CSR) interplay with CSR effectiveness (Sen and Bhattacharya 2001), the variable of corporate transparency has not been identified as a moderator to CSR effectiveness.

Second, we examine potential reasons for a decrease in CSR effectiveness from the perspective of consumer information processing. In today’s world, there is a greater risk that consumers will experience information overload than that they will have insufficient information. Thus, it is important to understand how consumers process corporate signals such as transparency and CSR. Extant studies have established that consumers may become skeptical about companies’ CSR motivations and intentions (e.g., Skarmeas and Leonidou 2013). Consumer skepticism, in turn, inhibits the consumer’s relationship with the brand, decreasing brand attachment. According to our findings, a reason for the negative moderating effect of corporate transparency is that it stirs consumers’ skepticism and thus inhibits the usefulness of the signaling effect of CSR.

Finally, the study examines implications of the corporate transparency moderator for international marketing research. Corporate transparency has recently been identified as a key trend of international brand building and management (Steenkamp 2020); however, there is only limited knowledge on how corporate transparency interacts with CSR on an international level. The international marketing literature that examines the causes of differing degrees of CSR effectiveness between countries is confined to arguments related to either the state of economic development or culture (e.g., Becker-Ohlsen et al. 2011; Choi et al 2016; Web Appendix 1 provides a more detailed discussion), and results are inconclusive (e.g., Auger et al. 2010; Eisingerich and Rubera 2010; Jean et al. 2016; Kim and Choi 2013). Thus, there is a need to consider other potential moderators that explain differences in CSR effectiveness. Research has shown that a country’s economic (e.g., Bushman, Piotroski, and Smith 2004) and cultural (e.g., Griffin et al. 2017) differences can contribute to different levels of corporate transparency. We thus argue that an important reason for inconclusive results is that the proposed moderators of CSR effectiveness are actually antecedents to a country’s environment for transparency. In general, previous studies have discussed only one of these antecedents while ignoring the other, thus leading to opaque results when one antecedent is not in line with the other (e.g., cultural values suggest an environment of low transparency, but development suggests one of high transparency). By focusing on corporate transparency instead of its individual antecedents, we enrich the literature on why CSR effectiveness differs between countries.

The following sections introduce signaling theory as a guiding framework for our study. We then review the relevant literature on CSR and corporate transparency. Next, we present four studies that investigate (1) how corporate transparency moderates the effect of CSR on the consumer–brand relationship (i.e., brand attachment and consumer behavior), (2) how CSR effectiveness depends on a country’s environment for transparency, (3) how consumer skepticism mediates the basic moderated relationship, and (4) how different types of corporate transparency (i.e., transparency about positive, negative, and mixed information) influence CSR effectiveness.

Literature Review

Signaling Theory

Signaling theory is built on the foundation that a signal receiver relies on observable information from a signal sender to reduce uncertainty about unobservable attributes (Spence 1973). The receiver interprets a signal and, depending on the perceived honesty of the signal, uses it as a proxy for the unobservable information (Connelly et al. 2011). Importantly, formal and informal institutions of the signaling environment influence the entire signaling process, including the signaler, the signal itself, and the receiver’s interpretation of the signal (Connelly et al. 2011). In addition, the effectiveness of signals varies depending on multiple conditions. For example, a firm may send several signals simultaneously, which may interact with one another (Steigenberger and Wilhelm 2018). In the case of two incoherent signals, the receiver may be confused about or doubt the signal’s genuineness, resulting in less effective transmission of the signal (Connelly et al. 2011). Moreover, the receiver tends to cognitively focus more on the negative signal, thus further distorting the original intent of signalers and weakening the signal’s effectiveness (Miyazaki, Grewal, and Goodstein 2005).

CSR as a Signal

Corporate social responsibility reflects the activities of an organization with respect to its perceived societal obligations, including environmental stewardship, commitment to diversity in hiring and promotion, community involvement, cultural activity sponsorship, and corporate philanthropy (Brown and Dacin 1997; Sen and Bhattacharya 2001). A company’s CSR efforts do not necessarily reflect an excellent product offering (Brown and Dacin 1997); however, CSR creates a context for customer evaluation (Sen and Bhattacharya 2001), which in turn may influence how customers think about a company, positively influence consumer–brand relationships, and motivate them to reward socially responsible companies (Brown and Dacin 1997; Sen and Bhattacharya 2001). In line with the signaling theory perspective, CSR can be interpreted as a signal to consumers and other stakeholders because it not only reveals information about a particular CSR project of the firm but also alleviates consumer uncertainty in a more general sense (Chernev and Blair 2015). Due to information asymmetry, consumers are unable to judge the moral character of a firm. Consumers may interpret CSR as a signal for an organization’s benevolence and good intentions due to the costs and effort of engaging in CSR activities (Su et al. 2016). In turn, such an interpretation can improve consumer–brand relationships (Eisingerich et al. 2011; Luo and Bhattacharya 2006; Moon, Lee, and Oh 2015) and strengthen a consumer’s brand attachment (Kull and Heath 2016).

In addition, signaling theory provides several explanations for low CSR effectiveness, such as low observability of a signal if consumers are not aware of a firm’s CSR activities (Connelly et al. 2011), a low fit between the signal and the object (Torelli, Monga, and Kaikati 2012), or distortions in the signaling environment (e.g., by competitors). In our case, we add two specific reasons: receivers’ interpretation of a signal and coherence between CSR and other firm signals. Subsequently, we briefly introduce receiver interpretation and revert to signal coherence when developing the proposed interaction between CSR and corporate transparency in the “Hypothesis Development” section. According to signaling theory, signal receivers’ interpretation can distort or enhance a signal’s effectiveness (Connelly et al. 2011). For example, CSR may be interpreted as originating from moral motives, or instrumental and suspicious ulterior motives (Ellen, Webb, and Mohr 2006; Yoon, Gürhan-Canli, and Schwarz 2006). In the case of such an interpretation, consumer skepticism about CSR increases, which diminishes the return on CSR for the firm (e.g., Skarmeas and Leonidou 2013). In signaling terms, consumers question the honesty of the signal when they doubt the sincerity of a CSR effort. In such a case, their relationship to the firm would suffer, and brand attachment may decrease.

Transparency as a Signal

Corporate transparency

In the context of consumer–brand relationships, this study focuses more on the recent view of information flows from companies to external stakeholders. We consider corporate transparency a firm trait or value that determines whether information is objective and accessible to its stakeholders (Liu et al. 2015). Specifically, companies should share information that is clear and easily understood and should facilitate access to third-party information. Companies should disseminate relevant and valid information that embodies truth, honesty, frankness, and candor and is without guile or concealment (Bell, Auh, and Eisingerich 2017; Bennis, Goleman, and Biederman 2008; O’Toole and Bennis 2009). As such, CSR and corporate transparency share a common root as a corporate signal. Consumers may reduce information asymmetry regarding the moral character or benevolence of the firm by relying on corporate transparency efforts as a cue. If a company is less open about a certain aspect, it may have a serious reason to conceal this information, which leads to doubts about the company’s moral character on a more general level. Conversely, high corporate transparency enables consumers to obtain clear and valuable information, which may reduce their perceived uncertainty in an exchange and increase their general trust (Lin 2007). The quality of the consumer–brand relationship is therefore enhanced.

Country environment for transparency

Importantly, according to signaling theory, formal and informal institutions of the signaling environment influence the signaler, the signal itself, and the receiver’s interpretation of the signal (Connelly et al. 2011). In our context, it means that country-level factors, such as economic development or culture, shape how firms employ transparency as a signal of benevolence and morality. Such country-level factors shape differences in a country’s environment for transparency. The environment may then constitute a frame that bounds firms from a specific country to a certain extent (Graafland and Noorderhaven 2020). There may be different effects of the country environment for transparency onto a firm’s corporate transparency. Governments could influence the transparency of firms directly through laws and regulations, or indirectly by shaping local stakeholders’ behavior. Even in a globalized world, domestic employees, customers, or investors often constitute the backbone of a company, and they are thus important intermediates that transfer the influence of the country environment for transparency into corporate transparency (Noorderhaven and Harzing 2003). Finally, the local civil society and media may function as transmitters between the country environment and corporate transparency. However, there is still considerable variance of transparency of firms within a country, as the corporate transparency signal is employed differently by firms in their fight for market share (Griffin et al. 2017). This variance is key so that corporate transparency can serve as a useful signal both for senders and recipients.

Hypothesis Development

Brand Attachment

The marketing literature has suggested that different variables can be used to capture consumer–brand relationships, such as attitude strength and attachment. Among them, brand attachment is often viewed as the ultimate indicator of the consumer–brand relationship, rather than attitude strength or purchase intention (e.g., Park, Eisingerich, and Park 2013; Thomson 2006). Consumers have been shown to become attached to different brands, including product brands, digital service brands, and country brands (Fritze et al. 2020; Liu et al. 2020). Brand attachment can be defined as the strength of the bond connecting the brand with consumers’ self (Park et al. 2010). This brand–self linkage can involve myriad emotional feelings such as happiness and pride from brand–self display (Park et al. 2013), which fits with the idea that consumers examine signals of benevolence and morality about a firm’s character. It has also been suggested as an important driver of consumers’ brand loyalty (Khamitov, Wang, and Thomson 2019), brand equity (Heinberg et al. 2020), advocacy, purchase intention, and actual purchase behavior (Park et al. 2013). Other variables, such as attitude strength, are a less important predictor of key behavioral outcome variables (Park et al. 2010). In addition, attitude strength does not correspond as well as brand attachment to the proposed signaling argument because it mainly focuses on consumers’ cognitive judgment of a brand and the confidence with which it is held (Petty, Brinol, and DeMaree 2007).

Moderation of Corporate Transparency

In line with signaling theory, the effectiveness of a corporate signal depends on the coherence of different signals from the same firm (Connelly et al. 2011; Miyazaki, Grewal, and Goodstein 2005). In our case, we propose that the link between CSR and brand attachment may be altered depending on different levels of corporate transparency.

The literature has already identified a relatively obvious link between transparency and CSR. It is important to design a CSR policy in a transparent way (Dubbink, Graafland, and Van Liedekerke 2008) and CSR reporting also needs to be conducted transparently to reach important stakeholders (Fernandez-Feijoo, Romero, and Ruiz 2014). We argue that transparency, even if it is not related to CSR information (e.g., transparency about a firm’s products, reputation, or financial stability), helps consumers gain valuable information to reduce perceived risk and simplify their decision-making process (Lin 2007). In this case, corporate transparency facilitates the perception of honesty, openness, and a commitment to truth that is also implicit in CSR-focused thinking. Like CSR, corporate transparency also communicates the company’s self-transcendent value of caring for others and confidence in its own products. It stands to reason that a company with something to hide has less motivation to be transparent (Doorey 2011). Consumers value the extra effort made by a firm to share critical information openly insofar as it supports their decision-making process (Bell, Auh, and Eisingerich 2017; Pechmann 1992; Trifts and Häubl 2003). Thus, high transparency encourages consumers to trust the firm, enhances the positive effect of CSR, and, in turn, contributes to the consumer–brand relationship. Formally, we hypothesize the following:

Moderation of Country Environment for Transparency

The literature has identified a range of country-level factors that shape corporate transparency. A country’s political economy and institutional setting affect corporate transparency (Bushman, Piotroski, and Smith 2004). The institutional context in a country, for example, contributes to how much information firms disclose and whether media and society demand transparency from firms (Heinberg, Ozkaya, and Taube 2018; Millar et al. 2005). In addition, a country’s national culture can influence the level of firm transparency (Davis and Ruhe 2003). Evidently, the country context only constitutes a framework for firms, and there is still considerable variance of corporate transparency within a country (Griffin et al. 2017), which makes transparency a reliable signal for consumers.

To specifically test whether transparency differences in the country environment are responsible for differences in the degree of CSR effectiveness, we consider three countries (i.e., China, Japan, and the United States) that differ in terms of country-level antecedents of transparency and, consequently, their level of transparency. According to World Bank estimates, China has a weaker rule of law and regulatory quality than either Japan or the United States (World Bank 2018). Thus, judicial and governmental forces that demand transparency from firms are expected to be weaker. Similarly, societal forces that could urge companies into a higher level of transparency (e.g., society, the media) are weaker in China, stronger in Japan, and strongest in the United States (Reporters Without Borders 2019).

Several data sources that attempt to measure the level of corporate transparency confirm our initial logic. According to our definition, corporate transparency can be directed at different stakeholders (e.g., governments, investors, suppliers, customers), but because transparency is a trait reflective of a firm’s values, the transparency level toward certain stakeholders mirrors the transparency level toward other stakeholders (Bushman, Piotroski, and Smith 2004). As such, available country indices provide a good indication of how much firms from a particular country value transparency. For example, the corruption watchdog Transparency International has found that only 20% of Chinese firms have reported on anticorruption programs. This figure is higher for firms from Japan (40%) and even higher for firms in the United States (74%) (Transparency International 2014). In addition to reporting on corruption, companies’ transparency is also apparent in their corporate governance. Standard & Poor’s has assessed publicly listed firms in numerous countries on dimensions such as corporate ownership structure, investor rights, financial transparency, and information disclosure, as well as board and management structures and processes (Patel and Dallas 2002). Again, Chinese firms score low (45), Japanese firms score medium-high (61), and U.S. firms score the highest (70) (Cosset, Somé, and Valéry 2016; Patel, Balic, and Bwakira 2002; Patel and Dallas 2002). PricewaterhouseCoopers has created an “opacity index.” Opacity can be understood as the opposite of corporate transparency and has been defined as “the lack of clear, accurate, formal, easily discernible, and widely accepted practices in the broad arena where business, finance, and government meet” (Barth et al. 2001). On this metric, China scores the highest (87), Japan scores in the middle (60), and the U.S. has the lowest score (36). The ranking has been updated numerous times, and while opacity scores fluctuate, the ranking among the three countries has remained consistent (Kurtzman and Yago 2009). Thus, we hypothesize the following:

Moderated Mediation of Consumer Skepticism

To summarize our previous discussion on signaling theory, both corporate transparency and CSR activities can signal sincerity or goodwill and help achieve the desired benefit for a company. In addition, the signal receiver “uses seemingly unrelated competitive market signals of the signal sender to cross-validate meanings inferred from signals that are of direct concern” (Heil and Robertson 1991, p. 410).

When a signal is ambiguous, stakeholders start an “attribution process aimed at uncovering the underlying motive” (Ogunfowora, Stackhouse, and Oh 2018, p. 528). Drawing on this key idea, we argue that signal incoherence between CSR and corporate transparency stirs up feelings of ambiguity, thus triggering consumer skepticism regarding the motive of the signal, which in turn decreases CSR effectiveness.

According to CSR research, CSR is effective if consumers perceive a moral (i.e., value-driven) motive for CSR and ineffective if consumers perceive an instrumental (i.e., ego-driven) motive (Ellen, Webb, and Mohr 2006; Wagner, Lutz, and Weitz 2009). In addition, a perceived moral motivation can increase CSR effectiveness by decreasing consumer skepticism (Skarmeas and Leonidou 2013). In signaling theory terms, only CSR driven by moral motives will indicate an honorable character of the firm to the consumer, while instrumental CSR activities will lead consumers to question if the organizational character of the firm is indeed caring and benevolent—in other words, if the CSR signal is honest (Su et al. 2016; Vlachos, Panagopoulos, and Rapp 2013). According to psychological research, when an actor displays positive behavior but there appear to be ulterior motives, the behavior is unlikely to be attributed to the actor’s positive disposition (Yoon, Gürhan-Canli, and Schwarz 2006). In line with this view, when a company engages in positive behavior (e.g., CSR activities) in the hope of building a strong consumer–brand relationship, consumers’ skepticism regarding the signaler’s genuine intention may be aroused if other contextual information raises suspicion (e.g., the company does not seem to display sufficient corporate transparency). Under such conditions, CSR activities may be ineffective.

Moderation of Types of Transparent Information

It is important to acknowledge the complex nature of transparency. Transparency pertains to not only how much information is revealed but also what type. Companies can be transparent about positive, negative, or mixed (both positive and negative) information. Research on signaling theory often takes the view that firms would only deliberately communicate positive information and thus “insiders generally do not send…negative signals” (Connelly et al. 2011, p. 45). Thus, there is not much research on how disclosing mixed and negative information could influence the effect of transparency. Some early evidence suggests that the type of information firms disclose influences the effect of transparency (e.g., Fabrizio and Kim 2019), but it is still unclear how the type of disclosed information influences transparency’s role as a signal.

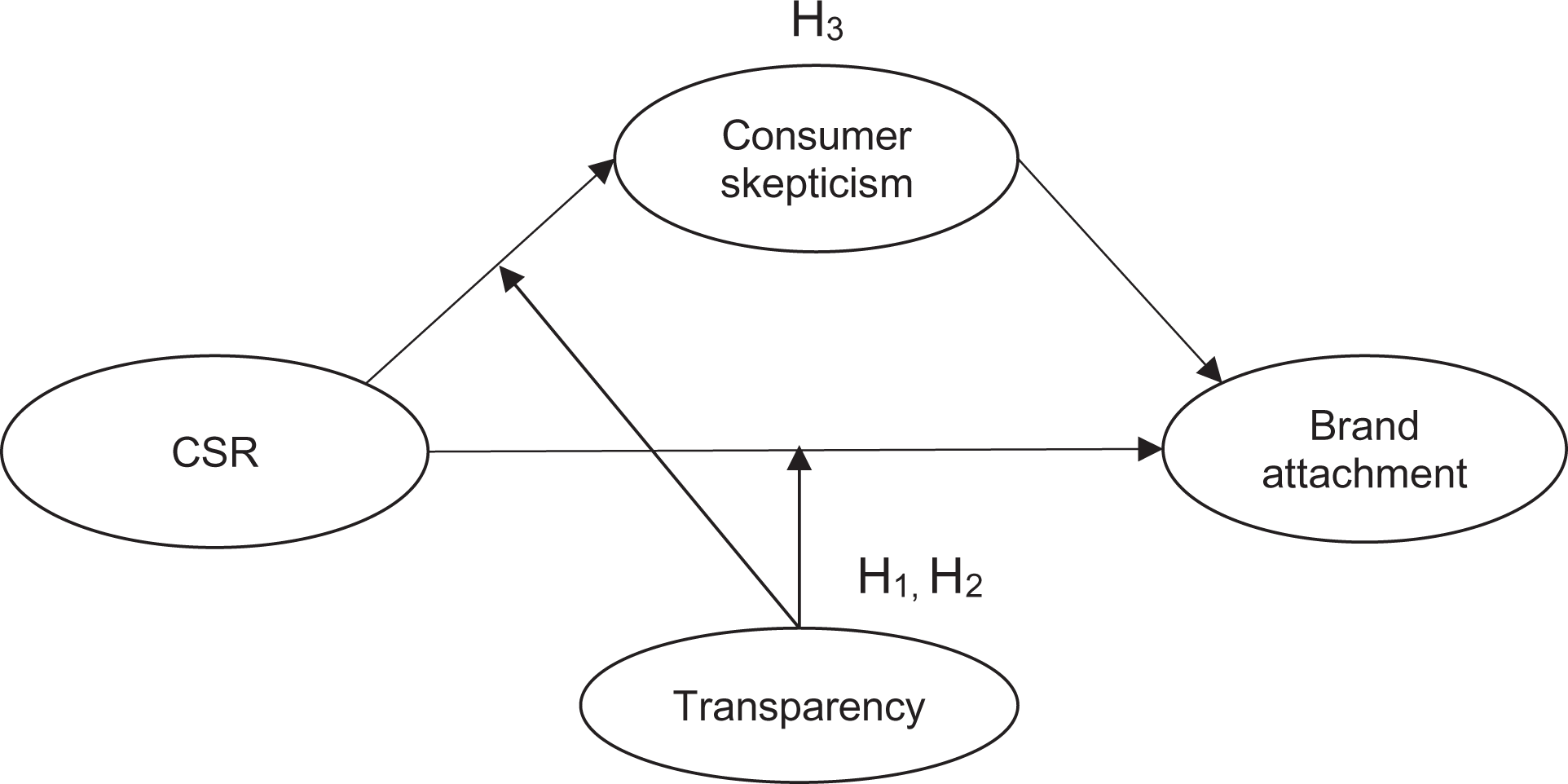

One would hope that firms would be very transparent and reveal essentially everything, but it is reasonable to think that firms will be more transparent about some aspects (e.g., positive information) of their business and less transparent about others (e.g., negative information). So, it is important to take the valence of information into consideration when examining transparency. According to signaling theory, disclosing mixed or even negative information may enhance the credibility of the transparency signal. However, although transparency in such adverse circumstances may signal honesty and openness, it may also harm the consistency or clarity of the signal (Erdem and Swait 1998). Thus, the effects of credibility and consistency of the transparency signal may vary depending on the type of information conveyed. To better understand the circumstances when transparency is advisable, we also examine different types of corporate transparency (i.e., transparency about positive, negative, and mixed information). Figure 1 summarizes our proposed research model.

Conceptual model.

Empirical Analysis

To test our hypotheses, we rely on four studies (Table 1). Study 1 tests the moderation of the CSR–brand attachment relationship by corporate transparency in an experiment. Study 2 then employs survey data and hierarchical modeling to determine whether Study 1 findings can be expanded to country differences in terms of corporate transparency. Study 3 aims to explore the logic of why corporate transparency moderates the CSR–brand attachment link by examining the mediating role of consumer skepticism in an experiment. Finally, Study 4 tests the notion of whether corporate transparency is always an important moderator, or whether its effect depends on the type of information a firm shares. To substantiate our results, we have relied on a behavioral dependent variable in this final experiment.

Overview of Studies and Levels of Analysis.

Study 1

Participants and procedure

Study 1 tests the moderating effect of corporate transparency on the relationship between CSR associations and brand attachment in an online experiment. Our sample comprised 352 participants from China recruited from the Sojump platform in exchange for monetary compensation (male = 48%, female = 52%). We selected China because its country environment is generally associated with low corporate transparency (Patel and Dallas 2002). Thus, a better understanding of the effects of corporate transparency will be particularly valuable for Chinese firms. In addition, findings from such a context could provide strong support for the notion that even in an adverse setting, individual corporate efforts of transparency are possible. We selected Chinese Merchants Bank as the focal brand, which is a familiar banking brand in China (Mbrand familiarity = 5.26, SD = .98; 1 = “not at all familiar,” and 7 = “very familiar”). We adopted a 2 (CSR: high vs. control) × 2 (transparency: high vs. control) between-subjects design. Participants were randomly allocated to one of the conditions. We controlled for participants’ existing satisfaction and familiarity with the brand and their involvement with banking, as we are using a real brand (e.g., Herz and Diamantopoulos 2017). We primed CSR associations and corporate transparency with reading tasks (see Web Appendix 3). The transparency reading stimuli were developed from the definition of transparency and adapted from Liu et al (2015). The CSR reading stimuli were adapted from the companies’ CSR report. Both tasks were pretested with experts in transparency and CSR and revised accordingly. We measured brand attachment as the dependent variable using a four-item scale (for all measurement items, see Web Appendix 4) (α = .86; 1 = “strongly disagree,” and 7 = “strongly agree”).

Results

Manipulation check results show that our manipulation of CSR association (MCSR = 5.35, Mcontrol = 5.03; t(350) = 4.471, p < .001) and transparency (Mtransparency = 5.36, Mcontrol = 5.08; t(350) = 4.15, p < .001) using priming was successful. There is no difference in age (F(1, 352) = .580, p > .05) or gender (F(1, 352) = 3.293, p > .05) among the manipulation conditions. In addition, we control regional differences at the operational level. An analysis of variance result shows no significant difference on the variable of interest, brand attachment, among the different Chinese provinces (F (26,325) = .850, p = .680 > .05).

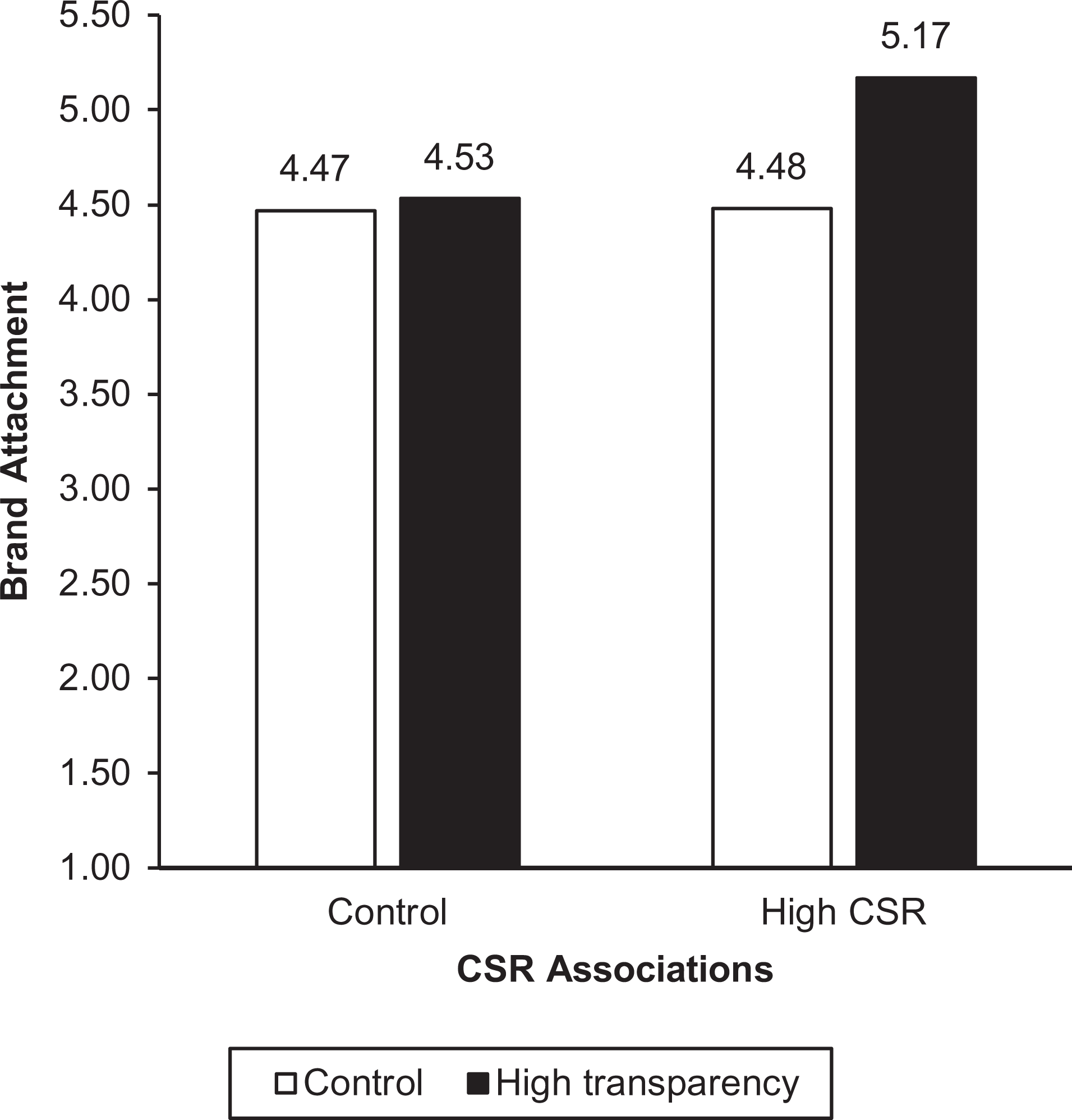

Results from an analysis of variance reveal that the main effects of CSR (MCSR = 4.82 vs. Mcontrol = 4.50; F(1, 348) = 9.83, p < .01) and corporate transparency (Mtransparency = 4.85 vs. Mcontrol = 4.48; F(1, 348) = 13.01, p < .001). Moreover, the CSR × transparency two-way interaction is significant (F(1, 348) = 9.47, p < .01) such that perceptions of high corporate transparency increase the difference in brand attachment between high-CSR condition and controls. Specifically, while brand attachment was significantly higher in the high-CSR condition than in the control condition under high transparency (MCSR = 5.17 vs. Mcontrol = 4.53; t(175) = 4.41, p < .001), the difference between the high-CSR condition and the control condition was not significant when transparency was at the control level (MCSR = 4.48 vs. Mcontrol = 4.47; t(173) = .04, p = .967) (see Figure 2). These results establish that perceived corporate transparency is a boundary condition for the effect of CSR associations on brand attachment, in support of H1.

Study 1: Effect of CSR and corporate transparency on brand attachment.

Study 2

Sampling

As discussed, we selected China, Japan, and the United States to represent countries with distinct environments that trigger low, medium, and high levels of corporate transparency, respectively. The three countries represent the largest economies in the world according to gross domestic product and, as we have indicated, differ remarkably in terms of transparency in their corporate environments.

We use a multilevel structural equation modeling approach to test H2 (Hox 2010). This technique enables us to include a large number of real brands, thus improving the external validity of our study. In addition, by accounting for a nested data structure, we avoid the underestimation of standard errors and thus decrease the probability of Type 1 errors. We selected fast-moving consumer goods (FMCGs) as an appropriate category for Study 2 to achieve the generalizability of our findings beyond services. Consumers tend to be generally familiar with FMCGs, and many FMCGs are household names (Heinberg, Ozkaya, and Taube 2016). We excluded brands from categories specific to particular consumer segments (e.g., infant products, pets, alcohol). We selected brands using a two-step process. First, we relied on desk and field research to compile a list of suitable domestic firms in each market (i.e., those firms with local headquarters). According to our argument, transparency in each firm depends on the country context. The country effect would be strongest for local firms, as neither their transparency nor CSR policy is influenced by foreign headquarters. Next, we conducted a pilot study (n = 100 in each country) to ensure consumer familiarity with FMCG brands associated with each firm and then selected 22 firms (with a total of 28 associated brands) in the United States, 22 firms (with a total of 25 associated brands) in China, and 27 firms (with a total of 33 associated brands) in Japan. We used quota sampling based on age, gender, and brand in an online panel from a reputable market research agency for the main study. We confined our sample to age groups between 18 and 55 years to assure general internet literacy and to circumvent possible stronger intergenerational differences in China. Older consumers in China have enjoyed fewer benefits from economic reforms and often display distinctive shopping behaviors relative to younger generations (Heinberg, Ozkaya, and Taube 2016). Overall, we collected 800 valid responses in the United States, 628 in China, and 839 in Japan (approximately 28 per brand), and our samples represent the countries’ overall populations in terms of gender and age groups. We surveyed each respondent employing an online questionnaire only about one brand, which was assigned using a random process. Respondents first answered questions about the brand (dependent/control variable) and then about the CSR of the firm associated with the brand (independent variable).

Measurement

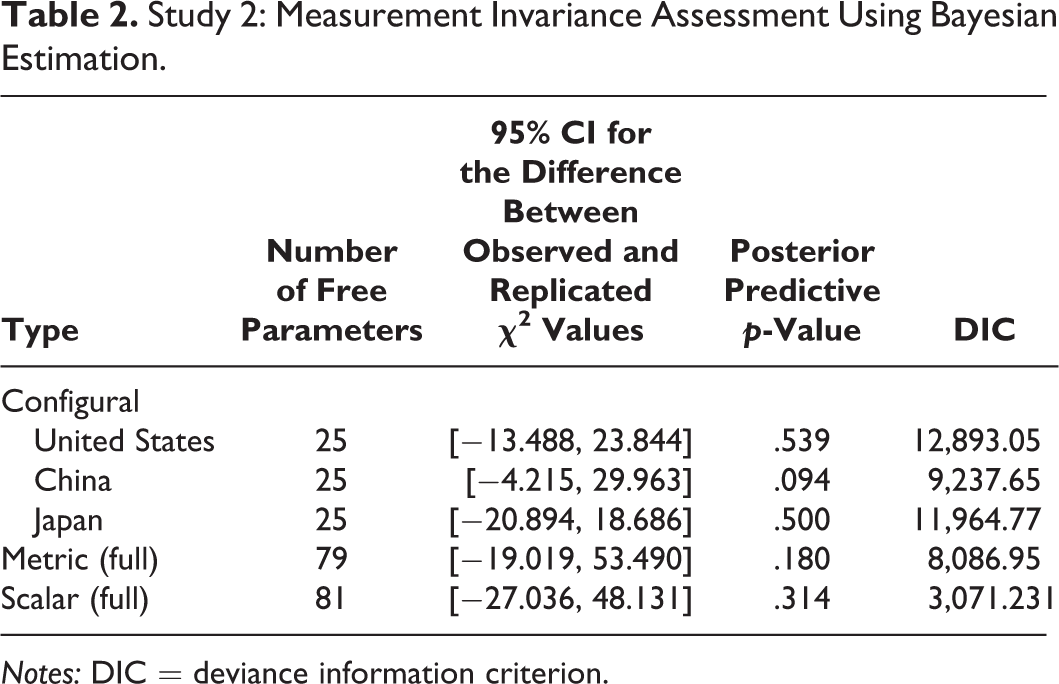

Measurement of the variables at the individual level builds on established research. We measured brand attachment using three items adapted from Batra et al. (2012) and Park et al. (2010) (“I feel emotionally connected to [brand],” “I feel a bond to [brand],” and “[Brand] feels like a good friend”), and our CSR construct is based on the work of Walsh, Beatty, and Shiu (2009) (“[Firm] seems environmentally responsible,” “[Firm] would reduce its profit to ensure a clean environment,” and “[Firm] seems to make an effort to create jobs”) (see Web Appendix 4). We tested whether brand attachment is significantly correlated to potential demographic (age, gender, education), or regional variation related confounds but only identify a slight positive correlation of education and our dependent variable. Therefore, we include education as a control variable in our further data analysis. We employed the translation/back-translation method using bilingual marketing researchers to establish the idiomatic equivalence of our scales (Hult et al. 2008). Subsequently, we assessed measurement invariance using a Bayesian estimator to match the estimation of our structural model, which also relied on a Bayesian approach. For Bayesian models, there is satisfactory model fit if (1) the posterior predictive p-value is above the significance threshold (i.e., >.05) and (2) the 95% confidence interval (CI) of the replicated chi-square includes zero (Van den Schoot et al. 2013). Using this approach, we establish configural measurement invariance, full metric invariance, and full scalar invariance (Table 2).

Study 2: Measurement Invariance Assessment Using Bayesian Estimation.

Notes: DIC = deviance information criterion.

We relied on seven-point Likert scales to assess our items and tested our scales rigorously for validity and reliability. All constructs exceeded the average variance extracted threshold of .5, and Cronbach’s alpha coefficients for the measures ranged from .792 to .950 (Bagozzi and Yi 1988) (see Table 3). In addition, we established discriminant validity using Fornell and Larcker’s (1981) stringent procedure.

Study 2: Correlation Matrix and Summary Statistics.

*p < .05.

Notes: Average variances extracted are on the boldfaced diagonal; squared correlations are above the diagonal; correlations are below the diagonal.

Common method testing is not a major concern in our case. First, we tested the relationships at the individual level in two experiments, in which we manipulated the independent variable (Studies 1 and 3). Second, our country-level moderators are formed by assigning the firm’s origin to each of the countries, which does not cause common method issues. Finally, our individual-level variables are directed at different entities (i.e., brands for our dependent and control variables and firms for our independent variable), which should decrease potential bias caused by the common method. However, because these measures are still examined using the same survey instrument, we assessed common method bias of our level-one variables by including a marker variable (Podsakoff et al. 2003). This variable (i.e., the item “Brown is my favorite color”) has no theoretical relationship with any variable, and we set the relationship between the marker variable and our remaining level-one variables to equal strength. The effect size of the loading is small (.042), and including this factor has only a negligible effect on our results; most importantly, it does not change our hypothesized relationships. Therefore, we conclude that common method testing of our individual-level variables is not a serious concern in our case. In addition, we examined the variance inflation factor to test for multicollinearity and find a value of 1.051, well below the generally accepted cutoff of 10 (Hair et al. 2010).

Results

We use a Bayesian multilevel structural equation modeling approach to explore the effect of corporate differences rooted in firm origins on the CSR–brand attachment relationship (Rabe-Hesketh, Skrondal, and Pickles 2004). We assessed relationships using 95% credibility intervals and the default diffuse priors in Mplus (i.e., normal for β and inverse gamma for σ2; Muthén and Muthén 2017). Research has shown that these priors are accurate and superior to the maximum likelihood–based method, especially for complex models such as multilevel structural equation models (Rupp, Dey, and Zumbo 2004). Following Heinberg, Ozkaya, and Taube (2016), we apply a stepwise procedure (see Table 4). First, we examine firm-level variance in relation to individual-level variance (null model) and obtain a coefficient of .199, which is generally regarded as medium-sized (Hox 2010). Next, we add our individual-level variables (fixed effects individual level). The random-effects models then add a random intercept and finally the random slope. All models reveal an increase in model fit and a steady decline of residual variance (Table 4), which provides support for the proposed model (Heinberg, Ozkaya, and Taube 2016).

Study 2: Results of Multilevel Structural Equation Modelling.

*p < .05.

Notes: DIC = deviance information criterion.

To examine H2, we first assess the effect between CSR and brand attachment, which is significant (B = .523; 95% Bayesian credibility interval = [.491, .555]). Our hypothesis predicts the strongest relationship between CSR and brand attachment for U.S. firms, a weaker relationship for Japanese firms, and the weakest relationship for Chinese firms. We used dummy coding to test the difference between the United States and Japan and between China and Japan. In support of H2, the relationship between CSR and brand attachment is significantly stronger for the first dummy variable (United States vs. Japan: B = .878; 95% Bayesian credibility interval = [.580, .999]) and significantly weaker for the second dummy variable (China vs. Japan: B = –.480; 95% Bayesian credibility interval = [–.727, –.222]).

Additional analyses

To gain additional support for our logic that the country differences in the CSR–brand attachment relationship are indeed rooted in differences of corporate transparency, we have identified a proxy measure for corporate transparency (see Web Appendix 5). Results confirm a weaker level of corporate transparency in China, a medium one in Japan, and a higher one in the United States. In addition, we find that corporate transparency moderates the effect of CSR on brand attachment.

To further consider the implications of our results for international marketing, we have carried out two additional explorations. First, as explained previously, we have included only domestic firms in our sample to achieve a clear country environment effect and avoid bias of a potential foreign influence on a firm’s CSR or transparency policy. In our data collection, we have also included a limited number of foreign firms, which enabled us to further test our hypotheses. As developed in Web Appendix 6, we receive support for our hypotheses, even when our sample is not limited to domestic firms. Second, such foreign influence may also be at play if a domestic firm is active in foreign markets. We have controlled for such an effect in our data analysis and receive additional confidence in our hypothesis (see Web Appendix 7).

Study 3

Participants and procedure

Study 3 includes 140 participants from China, recruited using the Sojump platform for monetary compensation. We removed 15 invalid responses (e.g., failure to pass the attention check), leaving a total of 125 valid responses (male = 47, female = 78). We selected the same focal brand as in Study 1. We employed a single-factor (CSR: high vs. control) between-subjects design. We manipulated consumers’ CSR associations as in Study 1. We measured transparency as a continuous variable in Study 3 to reveal a better perspective on the boundary of the moderating effect. After priming, participants reported their evaluation of corporate transparency associations and assessed their skepticism and brand attachment. We measured corporate transparency with a four-item scale developed by Liu et al. (2015) (α = .78; 1 = “strongly disagree,” and 7 = “strongly agree”; for a complete list of measurement items, see Web Appendix 4). We measured skepticism by asking participants to indicate their inferences about the sincerity of the company’s motive for pursuing the CSR activity. Specifically, we asked respondents to assess the following statement: “[Chinese Merchants Bank] does not sincerely care about consumers’ poverty reduction or environmental protection issues” (adapted from Yoon, Gürhan-Canli, and Schwarz [2006]).

Results

A t-test shows that our manipulation of CSR association using priming was successful (MCSR = 5.68, Mcontrol = 5.31; t(120) = 2.38, p < .05). In addition, we did not identify any significant differences between the CSR group and the control group for the control variables: familiarity (MCSR = 5.56, Mcontrol = 5.55; t(123) = .04, n.s.), attitude (MCSR = 5.77, Mcontrol = 5.78; t(123) = −.09, n.s.), and satisfaction (MCSR = 5.80, Mcontrol = 5.65; t(123) = 1.04, n.s.).

We hypothesized that skepticism mediates the effect of CSR on brand attachment and that transparency moderates the path between CSR and skepticism. We tested this moderated mediation model using Hayes’s (2013) PROCESS macro for Model 7 with 5,000 bootstrapped samples (see Table 5). In support of H3, PROCESS results show evidence of a significant moderating effect of transparency on the relationships between CSR and skepticism (B = −.45, SE = .19; t = −2.41, p < .05). In addition, controlling for CSR, we find that skepticism had a significant effect on brand attachment (B = −.49, SE = .07; t = −7.48, p < .001), while the direct effect of CSR on brand attachment is reduced to nonsignificance (B = −.13, SE = .13; t = .98, p = .33) after including skepticism.

Study 3: Regression Result of the Mediation Effect of Consumer Skepticism.

*p < .05.

**p < .01.

***p < .001.

Notes: DV = dependent variable.

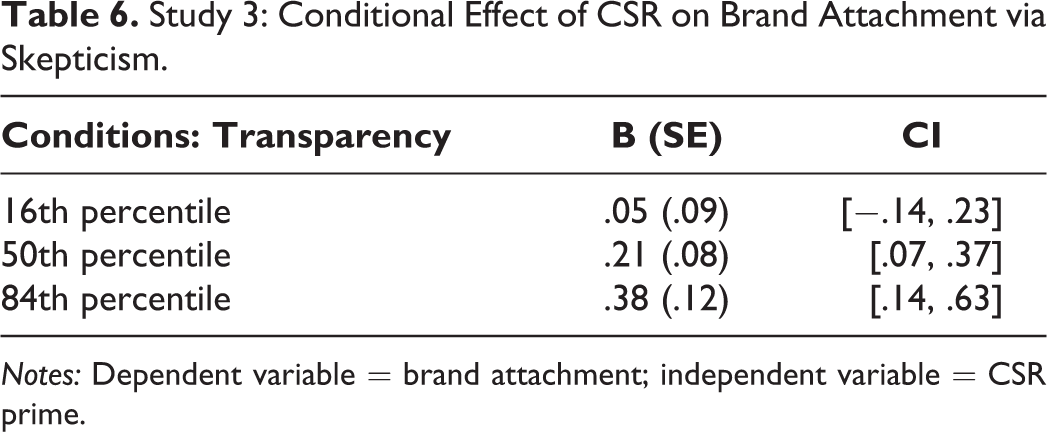

PROCESS also allowed for a deeper probing of the moderating effect of transparency on the CSR–skepticism relationship (Table 6). Specifically, it allowed for inferential tests of the effect at the quantiles. We find evidence for a significant indirect effect of CSR on brand attachment at the higher levels of transparency (50th percentile of transparency: 95% CI = [.07, .37]; 84th percentile of transparency: 95% CI = [.14,.63]). We did not obtain a significant effect for the lower level of transparency (16th percentile of transparency: 95% CI = [−.14, .23]) (see details in Figure 3). The results indicate that when transparency is high, CSR positively influences brand attachment via reduced skepticism; however, when transparency is low, CSR does not positively influence brand attachment.

Study 3: Conditional Effect of CSR on Brand Attachment via Skepticism.

Notes: Dependent variable = brand attachment; independent variable = CSR prime.

Study 3: Effect of CSR on skepticism at different levels of corporate transparency.

Study 4

Study 4 extends our findings in two ways. First, it examines an actual behavioral response, as this is logically connected to brand attachment (Park et al. 2013) and key to marketers’ interests. Second, the study examines different types of corporate transparency (i.e., transparency about positive, negative, and mixed (i.e., both positive and negative) information) to better understand the circumstances when transparency is advisable.

Participants and procedure

One hundred ninety-five students participated in the study as part of a regular course at a university. They were incentivized with a draw for twenty Amazon vouchers at a total value of US$100. Fifteen participants were removed (nine failed the attention check, four guessed the study purpose, and two indicated that they had done a similar study before), leaving a final sample size of 180 (88 male, 66 female, 19 other, 7 prefer not to say).

We employed a single-factor (transparency types: high transparency about positive information, high transparency about negative information, high transparency about mixed information, low transparency, and control) between-subjects design. We selected McDonald’s as the focal brand due to its general familiarity. We measured participants’ CSR associations with McDonald’s at the beginning of the study with a scale adapted from Stanaland, Lwin, and Murphy (2011). Then, we provided readings to participants about how product recalls could have different implications for a company (positive vs. negative vs. mixed) to prime participants’ perception of product recall information for the three high-transparency conditions (transparency about positive information vs. negative information vs. mixed information). Then, they all read an excerpt about how McDonald’s had experienced a major product recall and been transparent. For the low-transparency conditions, participants directly read an excerpt about how McDonald’s had experienced a major product recall and not been transparent about it. In addition, we included a control group, who did not read anything. By doing so, we manipulated different types of transparency with the same product recall scenarios to avoid potential confounding (see Web Appendix 8).

Participants then saw an option of checking the box to sign up for newsletters about updates from McDonald’s. They could decide to sign up or not. We also examined the success of the perceived McDonald’s transparency manipulation employing an adapted scale from Liu et al. (2015). Next, we checked the manipulation of information positivity by asking them what they thought would be the long-term implications of product recalls for a company (from “bad/negative/unfavorable” to “good/positive/favorable”). Finally, we also measured some control variables, including participants’ familiarity with and attitude toward McDonald’s, and believability of the excerpts about McDonald’s they just read.

Results

Manipulation check results show a significant difference in transparency among different conditions (F(3, 140) = 7.48, p < .001; Mhigh trans pos = 4.28, Mhigh trans neg = 4.12, Mhigh trans mix = 3.96, Mlow trans = 2.75) and a significant difference in perceived positivity of the information (F(3, 140) = 13.98, p < .001; M high trans pos = 4.92, Mhigh trans neg = 2.46, Mhigh trans mix = 3.65, Mlow trans = 3.76), confirming that our manipulation is successful.

We ran a logistic regression using PROCESS Model 1, with newsletter sign-up behavior as the dependent variable, CSR as the independent variable, and transparency type as moderator. We included brand familiarity, attitude, and excerpts’ believability as control variables. As Table 7 shows, the logistic regression is significant (χ2 = 57.53, d.f. = 12, p < .001; Cox and Snell R2 = .27, Nagelkerke R2 = .42). In addition, the interaction between CSR and transparency types is significant (χ2 = 16.93, d.f. = 3, p < .01). Table 8 and Figure 4 provide detailed results on the effect of CSR across different types of transparency.

Study 4: Logistic Regression of Newsletter Sign-Up on CSR and Transparency.

Notes: IV = independent variable. Dependent variable = probability of signing up for the newsletter. Coding for the categorical transparency type variable for analysis: high transparency positive: W1 = 0, W2 = 0, W3 = 0, W4 = 0; high transparency negative: W1 = 1, W2 = 0, W3 = 0, W4 = 0; high transparency mixed: W1 = 0, W2 = 1, W3 = 0, W4 = 0; low transparency: W1 = 0, W2 = 0, W3 = 1, W4 = 0; control: W1 = 0, W2 = 0, W3 = 0, W4 = 1.

Study 4: Effect of CSR on Newsletter Signing Up Across Transparency Types.

Notes: Dependent variable = probability of signing up newsletter; independent variable = CSR.

Study 4: Effect of CSR on newsletter sign-up behavior across transparency types.

The results show that sign-up for newsletters is higher for higher CSR associations, only when the company is being transparent about either positive (B = 1.01, Z = 2.17, p < .05) or mixed (both positive and negative; B = .78, Z = 2.37, p < .05) information. When there is no transparency information (control, p = .27) or when the company is being transparent about negative information (p = .35), CSR associations do not necessarily generate newsletter sign-up. More importantly, when the company is low in transparency, CSR associations show a marginally significant negative effect on newsletter sign-up (B = −1.26, SE = .68, Z = −1.84, p = .07). The results indicate that only when a company is transparent about positive or mixed information is a CSR initiative effective; when the transparency is about negative information, it at least does not hurt the company’s CSR efforts. However, when the company is nontransparent, CSR efforts could potentially backfire.

A potential explanation for our results can be found in signaling theory. According to our argument, corporate transparency can facilitate CSR effectiveness because it reduces information asymmetry with regard to the moral character or benevolence of the firm. We explained this effect with the rationale that transparency suppresses skepticism about the signal sender’s intention. While transparency about mixed or even negative information may seem like a sign of honesty and openness, the information itself may also raise suspicion among the signal’s recipients, potentially rendering the transparency signal ineffective. In terms of signaling theory, the consistency of the signal may be harmed (Connelly et al. 2011). Research has shown that the degree to which each component reflects the intended whole is an important factor that influences the clarity of a signal (Erdem and Swait 1998). In a nutshell, transparency about mixed or negative information may convey inconsistency and ambiguity and thus attenuate the intended signal about benevolence and morality.

Discussion and Implications

Theoretical Contributions

This study makes several theoretical contributions. First, it contributes to recent research on corporate transparency. Given today’s proliferation of information technology and social media, consumers demand greater transparency from companies (Liu et al. 2015). We show that transparency not only is important for its direct benefit but also signals consumers about the sincerity of a firm’s social responsibility practices. Corporate transparency is thus a boundary condition for the effect of CSR activities, such that CSR activities that are not aligned with transparency practices yield limited benefit to firms. We link the two signals of corporate transparency and CSR to enrich the understanding of when CSR benefits a company. While prior research has identified transparency as a prerequisite in CSR reporting (Dubbink, Graafland, and Van Liedekerke 2008; Fernandez-Feijoo, Romero, and Ruiz 2014), the boundary condition of corporate transparency for CSR effectiveness has not been discussed. Our findings also enrich the understanding of the role of different types of corporate transparency in relation to positive, negative, and mixed information. We find that transparency is only beneficial for a firm in terms of raising CSR effectiveness in the case of positive and mixed information. While low transparency lowers the effects of a firm’s CSR efforts, transparency in the case of negative information does not interact with CSR and thus does not appear to harm a firm’s CSR efforts.

Second, we examine the boundary condition of CSR effectiveness from the perspective of information processing at an individual level. Today’s state of information inundation has made a deluge of information available to consumers. As such, consumers have a higher standard for information, both in terms of what information is provided and the manner in which the company provides it. Thus, when making decisions, consumers rely on specific company signals, such as corporate transparency and CSR. In the case of conflicting signals, consumers try to uncover the underlying motives of signaling. This process can be particularly harmful to CSR-related signals, as skepticism with regard to the motive of doing good is a key reason for poor CSR effectiveness (Skarmeas and Leonidou 2013). We argue that consumers tend to question the honesty of a signal when it is not cohesive with other signals from the same sender, and we demonstrate that consumer skepticism regarding the genuineness of the signal increases when corporate transparency is not in line with CSR. Our research thus echoes prior studies directed at disentangling the importance of moral motives for CSR (Ellen, Webb, and Mohr 2006; Wagner, Lutz, and Weitz 2009). We extend extant knowledge by identifying corporate transparency as a key mechanism to help firms manage consumer suspicions with regard to CSR motives. We demonstrate that if a company performs well in both CSR and corporate transparency domains, consumer skepticism will be suppressed, thus enhancing the link between CSR and brand attachment.

Finally, this study contributes to the international marketing literature by proposing a new country-level moderator that addresses why CSR is more effective in certain countries than others. Specifically, we demonstrate that CSR is most effective for creating brand attachment in countries with high corporate transparency (e.g., the United States) and least effective in countries with low corporate transparency (e.g., China). Although corporate transparency has been named as one of the key trends in international branding (Steenkamp 2020), previous studies have generally investigated only one of the potential country factors that may contribute to the country environment for transparency (e.g., economic or institutional development, culture) but ignored the role of the environment itself. Understandably, a country might perform differently in terms of these antecedents, which would help explain conflicting findings in the literature (Auger et al. 2010; Eisingerich and Rubera 2010; Jean et al. 2016; Kim and Choi 2013).

Managerial Implications

This study highlights important points for company managers to achieve their desired outcomes from CSR activities. We establish that corporate transparency is a necessary condition for CSR effectiveness. Organizations should be careful when initiating CSR activities without coherent transparency practices, as expensive CSR activities may have no benefit. The findings suggest that businesses struggling to benefit from their CSR investments and activities should examine their transparency-relevant activities. In this sense, we suggest that transparency functions as a precondition for CSR so that consumers will respond positively to an organization’s CSR efforts only if they can “see through” the company and quickly identify and process valuable information. Importantly, consumers’ demand for transparency not only is related to CSR information but also includes all related fields of business activity. For example, there may be touchpoints related to transparency with regard to a firm’s own product portfolio, third-party product reviews, a firm’s balance sheet, and a firm’s lawful behavior.

In addition, our findings demonstrate that consumers appreciate signal coherence, which helps decrease their skepticism with regard to the honesty of a signal. Organizations should thus investigate different marketing activities jointly to maintain coherent signals and trace reasons for consumer skepticism. For example, CSR initiatives should be examined in conjunction with other communication activities. Otherwise, ambiguity among signals may lead consumers to doubt an organization’s goodwill and discourage them from building a strong relationship with its brand.

Moreover, previous studies also indicate corporate transparency as an outcome of national difference. Following this logic, this study further examines the interacting effects of national transparency and CSR in China, Japan, and the United States. As such, corporate transparency is an important issue for both policy makers and managers. Policy makers can help shape a more transparent environment, for example, by enabling media and society to effectively monitor a firm’s behavior or by encouraging standards for corporate governance. Managers need to recognize that corporate transparency is a valuable asset even under adverse circumstances such as reporting mixed (i.e., both positive and negative) information or in an environment that might be lacking in transparency (as exemplified in two experimental studies taking China as a case). By doing so, they can increase consumer attachment directly and improve the effectiveness of other corporate signals such as CSR.

Limitations and Further Research

There are some limitations to this study, which highlight promising avenues for future research. First, our country sample is too small to examine which antecedents of the country environment for transparency (i.e., economic/institutional development and culture) are meaningful and how they interact. While initial research has addressed questions related to individual antecedents of corporate transparency (e.g., Bushman, Piotroski, and Smith 2004; Griffin et al. 2017), a country-level study that considers the interplay of antecedents of corporate transparency in relation to the effectiveness of CSR could provide useful insights. In addition, a larger sample size at the country level would also enable insights into more detailed factors of corporate transparency like the legal environment, media, consumer activism, and economic imbalances. Furthermore, it would be interesting to investigate cases of firms that strongly deviate from the transparency frame set by their country environment and if there is less variance of corporate transparency in more transparent environments.

Second, we were only able to touch on the effect of a firm’s international activity to its corporate transparency, and many important research questions remain. Our preliminary insight that domestic firms that also sell products beyond their own borders profit from a stronger CSR–brand attachment effect (Web Appendix 7) would need to be confirmed by additional research. Such logic would be similar to findings for CSR, in which it has been demonstrated that firms tend to upgrade their CSR when acting in a foreign environment with more advanced CSR practices (e.g., Kang 2013). Because CSR and corporate transparency are interacting according to our findings, it would also be worthwhile to investigate cases in which the international target market has a lower CSR standard to examine the potential moderator of a level of CSR standard in a foreign country. Moreover, as indicated in our additional analyses section, when examining a sample of foreign brands separately, we did not find significant differences between countries. Future research is needed to investigate if this effect is due to different consumer expectations toward the transparency of foreign brands, or the wider variance of corporate transparency of firms originating from diverse countries. In addition, investigating the role of foreign brands in elevating corporate transparency of domestic competitors would be a worthwhile avenue of research.

Third, future research is needed to provide a more granular picture of the overall results we presented. For example, we tested the country moderation separately from the moderated mediation analysis via consumer skepticism. Future research is necessary to confirm these findings in a combined study and add robustness to our study, which employed a one-item measurement of consumer skepticism. In addition, building on the logic that corporate transparency and CSR are separate signals, we examined corporate transparency as a moderator. However, potential additional relationships between these variables (e.g., as a mediator) or in terms of the fit between both variables deserve attention. Furthermore, we identified culture as an antecedent of corporate transparency. While we found support for differences between countries, our preliminary tests of regional variation did not indicate significant effects. Future research would need to confirm these results and investigate potential reasons. Are cross-cultural differences simply larger than subcultural differences, or is corporate transparency determined by a country’s culture because a firm’s business activity is often not limited to one region in a country? Another area that deserves additional research is generational differences. Our results suggest no significant differences between generations for the CSR–brand attachment relationship. However, we find some evidence that there may be a three-way interaction between the country, consumer age, and the CSR effect. This could indicate stronger intergenerational differences in emerging markets compared with developed markets and thus demands future research. Finally, our finding that the type of information a firm is transparent about (good/mixed/bad) moderates CSR effectiveness would need to be extended to an international context. In such a study, types of transparency should also be manipulated with a different scenario to add robustness to our findings.

Supplemental Material

Supplemental Material, sj-pdf-1-jig-10.1177_1069031X20981870 - A Bad Job of Doing Good: Does Corporate Transparency on a Country and Company Level Moderate Corporate Social Responsibility Effectiveness?

Supplemental Material, sj-pdf-1-jig-10.1177_1069031X20981870 for A Bad Job of Doing Good: Does Corporate Transparency on a Country and Company Level Moderate Corporate Social Responsibility Effectiveness? by Martin Heinberg, Yeyi Liu, Xuan Huang and Andreas B. Eisingerich in Journal of International Marketing

Footnotes

Associate Editor

Amir Grinstein

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.