Abstract

Optimal distinctiveness within a single policy has been rarely examined in both the market and non-market strategy literature. Both agency theory and Upper Echelons theory suggest that CEOs play a significant role in shaping firms’ strategic behavior. Given the growing importance of managerial talent in today’s complex, dynamic business environment, as well as an increasing focus on firms’ CSR policies, this study investigates the relationship among managerial ability, CEO tenure, and firms’ optimal distinctiveness in CSR practices. We specifically examine the effect of managerial ability (talent) on CSR emphasis differentiation and scope conformity. Using a sample of 28,593 firm-year observations from 1992-2013, we find that managerial ability is negatively related to CSR scope conformity and positively related to CSR emphasis differentiation. We also find that CEO tenure moderates the relationship between managerial ability and CSR conformity, such that as CEO tenure increases, the negative relationship between managerial ability and CSR conformity decreases. Our results contribute to the growing literature on the role of upper echelon characteristics in shaping firms’ strategic behavior and how more able CEOs deal with pressure for legitimacy and competitive advantage in their CSR practices. We provide implications for scholars and practitioners seeking to understand how managerial ability and CEO tenure impact firms’ CSR strategies.

Keywords

Introduction

The competition for talented CEOs has increased over the years (Acharya et al., 2016). Companies are in pursuit of CEOs who are talented and who can improve the overall competitiveness of firms. More able CEOs have become a central topic of interest to business scholars due to the huge impact the CEO plays in today’s business environment (Chatjuthamard et al., 2021; Hesarzadeh & Bazrafshan, 2019; Lin et al., 2021). The literature suggests that the effect of the CEO on the firm’s key decisions and outcomes has significantly increased over the past few decades (Hambrick, 2007; Quigley & Hambrick, 2015). The Upper Echelons theory contends that top executives are the most influential decision makers in almost all organizations and that part of the outsized focus on the CEO by external stakeholders is attributed to the power the CEO holds at the top of the organization (Gupta et al., 2017; Quigley & Hambrick, 2015). Such importance and power are justifiable given the increasing complexity and dynamism of today’s business environment and the role that the CEO plays in making the most important strategic decisions of the firm.

One of the key roles a CEO plays in any firm is determining how the firm responds to various pressures from different stakeholder groups: pressure for compliance (scope conformity) and pressure for competitive advantage (emphasis differentiation) (Barlow et al., 2019; Taeuscher & Rothe, 2021; Zhang et al., 2020). Organizational researchers have long been concerned with the question of how firms can strategically manage different pressures to reach an optimal level of response where it addresses the institutional pressures for conformity to achieve legitimacy but also design and implement competitive actions in response to competitive pressures to achieve a competitive advantage (Pan et al., 2020; Zhang et al., 2020). Balancing those twin pressures is not abstract. Well-known “conformists” such as Nestlé and ExxonMobil hew closely to industry CSR templates, whereas “differentiators” such as Unilever and Patagonia pursue visible, tightly focused initiatives that depart from sectoral norms. These contrasts foreground the central polarity our study investigates, CSR scope conformity versus emphasis differentiation, and preview how CEO ability may steer firms toward one path or the other.

Balancing legitimacy-seeking conformity with competitively oriented differentiation is a classic CSR tension. We argue that managerial ability, conceptualized as the skill to deploy firm resources both effectively (doing the right things) and efficiently (doing things right) (Demerjian et al., 2012), acts as the decision heuristic that resolves this tension. Able CEOs evaluate every CSR option through an impact-per-dollar calculus: which initiative satisfies salient stakeholder claims with the smallest expenditure of slack? Targeted, high-visibility projects typically dominate broad, imitative portfolios on that metric, because they signal responsibility while preserving resources for market-facing investments. Consequently, higher managerial ability nudges firms toward emphasis differentiation, a focused set of CSR domains aligned with firm capabilities, rather than scope conformity, which spreads resources thinly across all domains merely to mimic peers. In short, resource-allocation acumen drives able CEOs to craft CSR strategies that are simultaneously legitimate and competitively distinctive (McWilliams & Siegel, 2000).

Upper echelon theory (UET) has been an important framework for understanding the relationship between top management team (TMT) characteristics and organizational outcomes. Whereas prior UET studies have mostly treated managerial ability as a direct predictor, we argue that CEO tenure is an internal contingency: it augments structural power and deepens firm-specific knowledge, thereby intensifying or constraining the behavioral expression of ability in CSR decisions (Finkelstein, 1992). Our study therefore theorizes and tests an ability × tenure interaction: does resource-allocation acumen steer firms toward broader scope conformity or sharper emphasis differentiation, and how does accumulated tenure intensify or mute this effect? By answering these questions, we refine UET’s explanation of non-market strategy without invoking external industry forces. Specifically, we argue that our study sheds light on the potential limits of UET in explaining how internal power contingencies condition executive imprinting. Our study makes three distinct contributions to theory and practice. First, we extend Upper Echelons Theory by demonstrating that managerial ability not only affects performance outcomes but systematically shapes strategic choices between CSR conformity and differentiation, a mechanism previously unexplored in the literature. Second, we identify CEO tenure as a critical internal contingency that attenuates the ability’s effect on CSR strategy, revealing when and why high-ability CEOs may converge toward industry norms despite their superior resource-allocation skills. Third, for practitioners, our findings suggest that boards seeking CSR differentiation should not only recruit high-ability CEOs but also consider optimal tenure horizons, as extended tenure may diminish the strategic distinctiveness that able CEOs initially bring to CSR initiatives.

The recent literature emphasizes how CSR is implemented and how the firm’s CSR policy properties may influence external audience perceptions (Al-Shammari et al., 2022). Attention-based evidence similarly shows that who gets noticed shapes nonmarket evaluations and outcomes (Born et al., 2024). Moreover, since CSR is a resource-consuming policy that requires time, efforts, attention and organizational resources, it becomes more important to examine how more able CEOs conduct CSR and design its policies. Thus, we examine the relationship between CEO ability and the firm’s optimal distinctiveness within the CSR policy of the firm. Additionally, we examine whether CEO tenure moderates this relationship. CEO tenure is regarded as an indicator of CEO power, CEO experience and knowledge about the firm, and CEO cognitive ability. Thus, we examine whether more able CEOs with more years of service at the firm will differ in their optimal distinctiveness pursuit. We contribute to the growing literature on optimal distinctiveness within a single policy by shedding light on a key predictor of how firms respond to varying sources of pressures within a single policy, namely the CSR behavior of the firm. We also add to the existing literature on the role of CEO tenure in shaping the firm’s behavior within non-market strategy.

Literature Review

Theoretical Background: Upper-Echelons and Optimal Distinctiveness

Consistent with Hambrick and Mason’s (1984) Upper Echelons Theory (UET), we explain CSR scope choices through the cognitive bases and values of CEOs. Institutional theory appears only as a boundary condition in that it supplies the conformity pressure our focal executives confront, while agency logic is referenced narrowly, CEO tenure proxies internal power and discretion (Darouichi et al., 2021). This hierarchy keeps the explanatory core squarely within UET. Upper Echelons Theory (UET) proposes that top executives, particularly CEOs, significantly influence organizational strategy and outcomes through their cognitive frames, values, and experiences. We organize the paper around Upper-Echelons Theory as our one home literature, and we utilize two enriching lenses, institutional conformity pressure and agency-based power, that bound CEOs’ discretion. Research on optimal distinctiveness offers insights into how CEOs construct and define their identities, specifically in relation to the self and the collective (Brewer, 1991; Oyserman et al., 2002; Turner & Oakes, 1994). According to Quigley and Hambrick (2015), the “CEO effect” on firm performance has increased, with more able CEOs being associated with higher levels of firm performance. However, Pan et al. (2020) found that firms labeled as high or low rank by analysts tend to have higher institutional immunity, leading to higher levels of nonconformity in regard to corporate social responsibility (CSR), while firms labeled as middle rank have lower immunity and tend to conform to CSR practices similar to their industry peers.

Subsequent research indicates that CEO characteristics, such as age, gender, and managerial ability, impact a firm’s CSR practices (Zhang et al., 2020). Zhang et al. found that CEO managerial ability has a negative effect on conformity and a positive effect on differentiation in CSR practices, while CEO tenure moderates these relationships. Female CEOs were found to have a negative effect on differentiation in CSR practices. In addition, firm-level factors such as firm age, size, and slack resources were significantly related to both conformity and differentiation in CSR practices (Zhang et al., 2020). Environmental factors may also moderate the relationship between conformity and differentiation in CSR practices (Pan et al., 2020).

CEOs’ ability to efficiently and effectively utilize a firm’s resources and capabilities is important in CSR practices (Acharya et al., 2016; Custódio & Metzger, 2013; Lin et al., 2021). The debate on the efficacy of CSR investments and how firms should conduct their CSR continues, with no consensus on a universal framework that applies to all companies due to fundamental differences between firms (Al-Shammari et al., 2022; Zhang et al., 2020). Optimal distinctiveness within the firm’s CSR policy has gained momentum and become more important in recent years (Pan et al., 2020; Schormair & Gilbert, 2021; She & Michelon, 2019; Zhang et al., 2020).

The UET suggests that CEOs with greater ability have a greater influence on strategic decisions, which can manifest as a greater emphasis on differentiation (Barney, 1986). Such CEOs may identify and capitalize on unique opportunities to gain a competitive advantage. Effective utilization of a firm’s resources and capabilities is key to achieving competitive advantage (Barney, 1991). A CEO’s ability can influence the identification and effective utilization of resources and capabilities and ultimately influence the firm’s strategic decisions.

The UET framework highlights the impact of top executives’ characteristics and experiences on firm practices. Research has shown that CEO ability, such as managerial ability, can have a significant effect on CSR practices. Understanding how CEO ability interacts with other firm-level factors in shaping CSR practices can provide valuable insights into how firms can best utilize their resources to achieve differentiation while also meeting the expectations of stakeholders. Therefore, in the following section, we review the literature on the impact of managerial ability on CSR practices and explore its potential implications for firm outcomes.

Managerial Ability

Managerial ability is the CEO’s cognitive capacity to convert resources into results (Demerjian et al., 2012); unlike CEO human capital (career experiences) or social capital (network ties), it is captured here with Data-Envelopment Analysis (DEA), which directly benchmarks input-output efficiency. Upper Echelons Theory suggests that the characteristics, experiences, and personalities of top executives, including the CEO, significantly influence their interpretations of situations and subsequently affect their decisions (Hambrick & Mason, 1984). This theory has been refined and expanded upon in subsequent research (Hambrick, 2007).

In a study, Pan et al. (2020) examined the impact of CEO ability on corporate social responsibility (CSR) conformity and differentiation. They found that more able CEOs were associated with lower levels of conformity and higher levels of differentiation in CSR practices. This suggests that more able CEOs may be more likely to deviate from industry norms and create unique CSR strategies for their firms. Quigley and Hambrick (2015) found that the “CEO effect” on firm performance has increased in recent decades, indicating the growing importance of CEO ability in determining firm outcomes.

Nevertheless, the relationship between managerial ability and firm outcomes might not be straightforward. Overall, the literature suggests that managerial ability is an important predictor of firm outcomes, but the relationship may be moderated by other factors such as CEO tenure. Future research could further explore the complex relationship between managerial ability and firm performance, as well as the potential moderating effects of other variables.

The CEO’s ability, which is a function of their knowledge, skills, and experience, is one key resource that can contribute to differentiation (Zhang & Rajagopalan, 2010). CEOs with greater ability are more likely to have a more efficient and effective approach in resource allocation, which allows them to identify unique opportunities and leverage the firm’s resources and capabilities to achieve differentiation. A CEO with a background in product design, for example, may be better equipped to develop innovative products that distinguish the company from competitors (Barney, 1991). The ability of a CEO can influence the creation and maintenance of a strong organizational culture that promotes differentiation. A CEO with strong leadership skills, for example, may be able to foster an innovative culture that encourages employees to generate and implement new ideas.

CEOs with higher ability may be less likely to conform to industry norms and instead take a more proactive approach to social responsibility in terms of CSR scope conformity (Jain & Jamali, 2016). A CEO’s ability to identify opportunities to create social value beyond industry norms and tailor CSR activities to the firm’s unique resources and capabilities can help them stand out. As a result, the firm’s CSR activities may not align with the expectations of the broader industry, resulting in a lower emphasis on CSR scope conformity. A CEO with a background in sustainability, for example, may prioritize environmental initiatives that are not widely used in the industry.

CEO Tenure

Related research also highlights that external evaluations shape CSR conformity. For example, Pan et al. (2020) show that analyst rankings create heterogeneous institutional immunity, influencing whether firms conform or differentiate in CSR. We suggest that CEO tenure may condition how executives navigate such external categorization pressures: long-tenured CEOs may be more accustomed to conformity when facing analyst scrutiny, while newer CEOs may use differentiation to challenge such labels. Other research has focused on the moderating role of CEO tenure on the relationship between managerial ability and organizational outcomes. A study by Zhang et al. (2020) found that CEO tenure moderates the relationship between managerial ability and conformity and differentiation in corporate social responsibility (CSR) practices. They discovered that as CEO tenure increased, the negative relationship between conformity and managerial ability diminished, as did the positive relationship between differentiation and managerial ability.

Overall, the literature suggests that CEO tenure is an important factor in organizational performance and can moderate the relationship between managerial ability and various outcomes. Further research is needed to fully understand the mechanisms through which CEO tenure influences these relationships.

Optimal Distinctiveness within the Firm’s CSR Policy

The optimal distinctiveness theory posits that firms face external pressures from different stakeholder groups to achieve certain expectations, including demands for conformity and differentiation within their CSR policies (Barlow et al., 2019; Zhang et al., 2020; Zhao et al., 2017). Scholars have examined how companies balance these pressures by adapting to external pressures from various stakeholders while also maintaining their competitive position through differentiation.

The role of the CEO is essential in shaping a firm’s strategic approach to CSR conformity and differentiation, influenced by the CEO’s values, personality traits, and social and professional experiences (Cao et al., 2015; Chatterjee & Hambrick, 2011; Gupta et al., 2017; Hawn & Ioannou, 2016; Lee et al., 2020; Palmer et al., 2020). Studies have explored the relationship between CSR conformity and differentiation and their effects on financial performance, analyst coverage, and market value. For example, Pan et al. (2020) found that firms labeled as high or low rank by analysts have higher institutional immunity, while middle-ranked firms tend to conform to CSR practices like their industry peers. Quigley & Hambrick (2015) found that the proportion of variance in performance explained by individual CEOs, or “the CEO effect,” has significantly increased over time.

Studies also stress the need for firms to design and implement their CSR actions intentionally so that they can be a source of differentiation (Barin Cruz et al., 2015; Graafland & Smid, 2019; Sauerwald & Su, 2019; Susanne Johansen & Ellerup Nielsen, 2012; Wang & Choi, 2013). For instance, Hawn and Ioannou (2016) argued that firms should focus on their internal CSR first and gradually engage in external CSR actions when the firm has developed enough tangible and intangible resources to engage in such externally oriented actions. Hawn and Ioannou (2016) also found that when firms continue to have a gap between their external and internal CSR over time, the financial effects of such actions will diminish.

Zhang et al. (2020) investigated the effects of conformity versus differentiation in CSR practices on evaluations by security analysts and responses of the financial market. The study found that while conformity in CSR scope enhances analyst coverage, differentiation in CSR emphasis leads to more favorable analyst recommendations and higher market value. Overall, these studies provide empirical evidence to support the argument that firms can achieve a balanced strategic approach to CSR conformity and differentiation that improves their competitive position while maintaining a sufficient level of legitimacy (Deephouse, 1999; Desai, 2018; Rhee et al., 2018).

Theory and Hypotheses

A key research question in this study examines the influence of more able (talented) CEOs on a firm’s optimal distinctiveness in CSR policy. It is reasonable to assume that managerial ability is negatively related to CSR conformity. Upper echelons Theory suggests that the characteristics, experiences, and values of top executives greatly influence their interpretation of situations and ultimately affect their decision-making (Hambrick & Mason, 1984). This suggests that more able CEOs, who may have a more diverse range of experiences and a stronger ability to interpret situations, may be less likely to conform to established industry practices and more likely to deviate from the norm. For example, a CEO with a strong track record of innovation may be less likely to conform to traditional CSR practices and instead seek out new and creative ways to address social and environmental issues. On the other hand, a CEO with less managerial ability may be more inclined to conform to established industry practices in order to minimize risk and ensure the organization is perceived as legitimate.

According to Upper Echelons Theory, CEOs with greater ability, potentially derived from a diverse range of experiences and a heightened capacity for situational interpretation, might be less inclined to conform to established industry norms and more likely to pursue innovative CSR practices. To illustrate this, consider the example of Patagonia, a company that has gained widespread recognition for its commitment to sustainable manufacturing practices. Rather than simply adhering to industry standards for environmental compliance, Patagonia has taken an innovative approach to reducing its environmental impact, investing in renewable energy, and promoting responsible manufacturing practices (Patagonia, n.d.). Similarly, Starbucks has implemented a range of CSR initiatives designed to improve the lives of coffee farmers and promote sustainable sourcing practices. Through its ethical sourcing program, Starbucks has made significant investments in farmer support centers, farmer loans, and farmer training programs, with the aim of improving the livelihoods of coffee farmers and promoting long-term sustainability in the coffee industry (Starbucks Coffee Company, 2023). These examples suggest that more able CEOs may be more inclined to engage in nonconformist CSR practices that go beyond traditional compliance measures, leveraging their diverse experiences and problem-solving skills to develop novel solutions to social and environmental challenges. Drawing on the cognitive-capability dimension of Upper Echelons Theory, we posit that high-ability CEOs’ superior information-processing capacity enables them to parse heterogeneous stakeholder claims and translate each salient claim into a precisely targeted CSR domain, thereby channeling resources toward differentiated emphases that achieve both legitimacy and competitive advantage (Nadkarni & Herrmann, 2010).

Furthermore, previous research has found that firms with high levels of institutional immunity, or those that are able to deviate from established industry practices without negative consequences, are more likely to be nonconformist in their CSR practices (Pan et al., 2020). This suggests that more able CEOs, who may have greater institutional immunity due to their reputation or resources, may be more likely to engage in nonconformist CSR practices.

In summary, the hypothesis that managerial ability is negatively related to CSR conformity is supported by both theoretical and empirical evidence. More able CEOs may be less likely to conform to traditional CSR practices and instead seek out new and innovative ways to address social and environmental issues, due to their diverse range of experiences, strong ability to interpret situations, and potentially higher levels of institutional immunity. More able CEOs are likely to choose a CSR path focusing on efficiency and effectiveness. Conforming to CSR scope involves dedicating substantial firm resources, time, and attention. Whereas emphasis differentiation is likely to be chosen by more able CEOs due to the focus rather than a wide spectrum of activities. Emphasis differentiation entails selecting perhaps the most relevant domains in which a company can focus its CSR efforts and differentiate itself from others. Therefore,

Managerial Ability is negatively related to CSR Conformity The literature suggests that the CEO plays a significant role in shaping the firm’s responses to various pressures and in making strategic decisions (Hambrick, 2007; Quigley & Hambrick, 2015). Given today’s increasingly complex and dynamic business environment, coupled with the pivotal role that CEOs play in decision-making, it becomes crucial to investigate how CEO characteristics influence a firm’s responses to external pressures like those associated with corporate social responsibility (CSR). There are several reasons to expect a positive relationship between managerial ability and CSR differentiation. First, more able CEOs may be more likely to have the cognitive and strategic skills necessary to design and implement CSR policies that are both effective at addressing external pressures for conformity and competitive in terms of creating a competitive advantage (Brown et al., 2020). For example, a more able CEO may be more likely to identify unique opportunities for the firm to differentiate itself through its CSR activities, such as by focusing on specific social or environmental issues that align with the firm’s core competencies or values. Second, more able CEOs may be more proactive in seeking out and responding to external pressures and opportunities related to CSR. For example, a more able CEO may be more likely to anticipate changes in consumer preferences or regulatory requirements and design CSR policies that anticipate and address such changes. This proactive approach may allow the firm to differentiate itself from competitors by being an early adopter of new CSR practices or by positioning itself as a leader in a particular area of CSR. Finally, more able CEOs are likely to be more effective in communicating the firm’s differentiated CSR activities to external stakeholders like consumers, investors, and regulators. For example, a more able CEO may be more adept at framing the firm’s CSR activities in a way that resonates with key stakeholders and differentiates the firm from competitors. Overall, we expect that more able CEOs will be better equipped to design and implement CSR policies that are both compliant with external pressures for conformity and differentiated in terms of their competitive impact. As such, we expect a positive relationship between managerial ability and CSR differentiation.

Managerial Ability is positively related to CSR Differentiation Agency theory suggests that as CEO tenure increases, the CEO may have more incentives to align their actions with the interests of all stakeholders and become more interested in building a socially acceptable profile (Chen et al., 2022; Darouichi et al., 2021). As a result, the CEO may be more likely to implement CSR practices that align with the general expectations of all stakeholders in the scope of the firm’s domains, leading to a decrease in the negative relationship between managerial ability and CSR conformity. This is supported by the study of Chen et al. (2019) which found that CEOs with more tenure may be more likely to align their actions with the interests of shareholders. With increasing CEO tenure, there may be better alignment with external norms and expectations due to greater experience in managing external relationships. This could result in a diminishing negative relationship between managerial ability and CSR conformity. This is consistent with the study of Koh and Reeb (2015), which found that firms with more tenured CEOs may be more experienced in managing external relationships and may be better able to align with external norms and expectations. Several examples from industry suggest that CEO tenure may be an important factor in shaping a firm’s CSR practices. For example, Unilever’s former CEO, Paul Polman, implemented the Sustainable Living Plan during his ten-year tenure, which aimed to double the company’s size while reducing its environmental footprint and increasing its social impact. Polman’s extended tenure allowed him to embed the plan into the company’s culture and operations, leading to increased CSR scope conformity (Polman, 2021). Similarly, PepsiCo’s former CEO, Indra Nooyi, implemented the Performance with Purpose initiative, which focused on sustainability, nutrition, and water stewardship, during her 12-year tenure. Nooyi’s extended tenure allowed her to oversee the implementation of the initiative and establish it as a core part of the company’s strategy. These examples suggest that CEO tenure may be an important factor in the development and implementation of a firm’s CSR practices. Upper Echelons Theory suggests that top executives play a significant role in shaping a firm’s strategic behavior. As CEO tenure increases, the CEO may have more influence within the organization and may be better able to shape the firm’s CSR strategy in a way that aligns with their personal beliefs and abilities, leading to a decrease in the negative relationship between managerial ability and CSR conformity. This is supported by the study of Gupta et al. (2017) which found that top executives with more tenure have more influence within the organization and may be better able to shape the firm’s strategy. As CEO tenure increases, the CEO may have more experience and knowledge about the company’s operations and may be better equipped to make strategic decisions that align with CSR norms and expectations. This could lead to an increase in CSR conformity and a decrease in the negative relationship between managerial ability and CSR conformity. A CEO with longer tenure may have built stronger relationships with key stakeholders, such as customers, employees, and regulators, which could lead to increased pressure to conform to CSR norms and expectations. This could lead to an increase in CSR conformity and a decrease in the negative relationship between managerial ability and CSR conformity. Theoretical arguments from agency theory and Upper Echelons Theory all suggest that as CEO tenure increases, the CEO may be more likely to align their actions with the interests of shareholders, better able to align with external norms and expectations, and have more influence within the organization to shape the firm’s CSR strategy (Chen et al., 2019; Gupta et al., 2017). In addition, as CEO tenure increases, the CEO may have more experience, knowledge, stronger relationships with key stakeholders, and a greater commitment to the long-term success of the firm, all of which may lead to increased CSR conformity and a decrease in the negative relationship between managerial ability and CSR conformity. In light of these arguments, we put forward the following formal hypothesis:

The negative relationship between managerial ability and CSR Conformity is moderated by CEO tenure in that as CEO tenure increases, the negative relationship between managerial ability and CSR conformity decreases. Research suggests that as CEOs gain more experience and tenure with a firm, they may become more risk-averse and less willing to deviate from established industry norms (Hambrick & Mason, 1984; Hambrick, 2007). This could involve implementing innovative CSR practices or strategies that differentiate the firm from its competitors. More able CEOs, on the other hand, may be more willing to take on such risks and pursue more differentiated CSR strategies in order to create a competitive advantage for their firm. In addition, research suggests that as CEOs gain more power and influence within a firm, they may be more able to shape the firm’s CSR strategy to align with their own values and preferences (Hambrick, 2007). For example, a CEO who is highly concerned with environmental issues may be more likely to push for the implementation of more environmentally friendly CSR practices, even if they differ from industry norms. However, as CEO tenure increases, the CEO may become more entrenched in their views and less open to alternative perspectives, leading to a decrease in the positive relationship between managerial ability and CSR differentiation. Real-world examples can help illustrate this relationship. For example, consider a CEO who has recently been hired to lead a firm in the consumer goods industry. This CEO may be more willing to pursue differentiated CSR strategies, such as implementing sustainable packaging or supporting fair trade practices, in order to differentiate the firm from its competitors and appeal to socially conscious consumers. However, as this CEO gains more tenure with the firm and becomes more established in their role, they may be less likely to take on such risks and may instead focus on maintaining industry norms in order to maintain the firm’s legitimacy. On the other hand, a CEO with high managerial ability and a strong commitment to sustainability may continue to pursue more differentiated CSR strategies throughout their tenure, even as they gain more power and influence within the firm.

The positive relationship between managerial ability and CSR differentiation is moderated by CEO tenure in that as CEO tenure increases, the positive relationship between managerial ability and CSR differentiation decreases.

Methods

Sample and Data

Our final sample is a combination of standard databases used in strategic management research. The choice of sample period is strictly determined by data availability to us. We begin with a combination of Standard & Poor’s Compustat North America and Execucomp. The former and latter databases are the sources of corporate financial characteristics and CEO features, respectively. We exclude observations belonging to highly regulated industries such as electric, gas, and sanitary services industry (SIC codes 4900-4999); finance, insurance, and real estate industry (SIC codes 6000-6999); and public administration industry (SIC codes 9000+) because in these industries very little, if at all, CSR related activities are left to managerial discretion (Petrenko et al., 2016; Peters & Taylor, 2017). After the elimination of missing values on independent and control variables, the process yields an unbalanced panel of 28,593 firm-year observations with 2,626 firms over the 1992-2013 period. KLD, the source of CSR data, covers 1991-2013 period. Industry averages are used to measure our dependent variables. Hence, we include industry-year with five or more observations only to avoid any possible biases from averaging (Chen, 2008). Ultimately, the usable unbalanced panel consists of 8,742 observations belonging to 1,427 individual companies between 1993 and 2013. In the endogeneity test section, we have found that although selection bias exists, the conclusions of this paper remain unchanged even after accounting for the bias.

Measures

Dependent Variables

We operationalize two continuous variables, conformity and differentiation, following Zhang et al. (2020). An industry sets CSR-related norms gradually. Conformity measures the extent to which a firm meets industry expectations. Thus, the conformity score for a firm goes up if a firm aligns its CSR portfolio with the established industry practice. The conformity score is calculated focusing on six CSR fields – environmental, community, employee, diversity, product, and governance. To compute the relative importance of these CSR fields, we employ the concept network method and generate a weight per CSR spectrum. Initially, we construct a two-mode network with firms in the rows and six CSR fields in the columns, segmented by year. Each number in this matrix signifies the corporate net score in a particular CSR aspect. Second, a transformation converts the matrix into a one-mode network with CSR fields only. Numbers in this second matrix show the relative importance of each CSR field to a firm and the strength of association among the CSR types. A strong connection reflects a higher importance of those CSR fields for that industry-year combination. These numbers are the sources of Eigenvector centrality values, signifying the status of a particular CSR field is in the network. Further, for each CSR dimension, we generate a binary dummy variable. Net benefits to society from CSR activities matter ultimately because ‘net’ takes into account CSR related costs as well. So, any CSR aspect helps society ultimately if the net score is positive for the field. Therefore, dummy is 1 if the net CSR score is greater than 0 and 0 otherwise (Li, Li, & Minor, 2016). Finally, we multiply the dummy of each CSR field by the respective eigenvector value from the previous year and sum the products belonging to six unique CSR dimensions to generate the corporate conformity score (Zhang et al., 2020). More specifically,

Contrastingly, CSR differentiation represents how different, both magnitude and direction wise, a firm is compared to its counterparts in the same industry with respect to CSR behavior. The measure uses a firm’s net CSR scores, continuous variables, unlike

Independent Variable

The managerial ability measure is operationalized following Demerjian et al. (2012). It estimates efficiency in managing corporate resources. The first step of this multistep process is the generation of industry (as defined by two-digit Fama-French SIC) wise corporate efficiency using data envelopment analysis (DEA) that requires inputs and an output. In such a model net sales or revenue is the output and the input group consists of costs of goods sold; selling, general, and administrative expenses; net property, plant, and equipment; net operating leases; net R&D; purchased goodwill; and other intangible assets. In essence, the following optimization problem requires a solution-

However, both firm features and CEO characteristics contribute to the DEA-generated efficiency estimates. One of the ways to separate managerial influence from corporate impacts is to subtract corporate contributions from

According to Demerjian et al. (2012), these controls are highly capable of helping or hurting managerial efforts. Therefore, the residual or the unexplained part of

Control Variables

We include a number of control variables following the existing literature. Included CEO characteristics are tenure, natural logarithm of number of years at a firm as CEO (Walls & Berrone, 2017; Kang et al., 2021; Petrenko et al., 2016); CEO age, natural logarithm of number of age in years (Walls & Berrone, 2017; Kang et al., 2021; Petrenko et al., 2016); and gender, dummy variable equals to 1 if woman CEO and 0 otherwise (Kang et al., 2021). Additionally, we incorporate a binary variable set to 1 if a firm undergoes a CEO change in a given year, and 0 otherwise (Borgholthaus et al., 2021). Firm features control for firm age, natural logarithm of number of number of years since a firm appeared in Compustat for the first time (Kang et al., 2021); size, natural logarithm of net sales (Kang et al., 2021); ROA, Earnings before interest, taxes, depreciation, and amortization scaled by total assets (Chatjuthamard et al., 2016); adjusted ROA, firm ROA relative to industry median ROA (Campbell, 1996); leverage, debt-to-equity ratio (Walls & Berrone, 2017); slack, cash and short-term investments scaled by total assets (Chatjuthamard et al., 2016); R&D intensity, research and development expenditures scaled by net sales (Walls & Berrone, 2017; Kang et al., 2021); and advertisement intensity, advertisement expenditures scaled by net sales (Walls & Berrone, 2017; Kang et al., 2021). We replace missing research and development expenditures and advertisement expenditures by 0 and include two dummy variables equaling 1 (0) if either of the expenditures is non-missing (missing) (Koh & Reeb, 2015). Additionally, year dummies control for time trend (Walls & Berrone, 2017; Demerjian et al., 2012).

Model Estimation

We estimate the following equation using fixed-effects (FE) regression technique with robust standard errors clustered at firm level to test the hypotheses –

The FE model is recommended because it is free from any biases caused by time-invariant and firm-specific unobservable factors (Wooldridge, 2010). Indeed, both Hausman test statistics are statistically significant at 1% level for both conformity (275.30***) and differentiation (242.60***). Rejection of Hausman test nulls implies that firm-specific unobserved characteristics are related to the observed regressors. This, in turn, makes regressors and the error terms correlated i.e., firm-specific heterogeneity exists and matters. In fact, the correlation between panel-specific error term and regressors is quite high for both conformity (−0.60) and differentiation (−0.71). Consequently, FE and random effects (RE) should yield quite different outcomes. Additionally, cross sectional dimension is greater than time series in the final sample of analysis. Being robust to serial correlation and heteroskedasticity, FE is preferred over RE for this sample because RE assumes absence of such correlations.

Although FE is reliable in mitigating spurious correlations and endogeneity issues at least partially by canceling firm-specific, time-invariant, and unobservable features due to its focus on within firm variations only, interactions may reduce such reliability by making FE depend on between firm variations too (Shaver, 2019). As a further warranted check, in the robustness check section we include results from correlated random effects models that strengthen our initial FE findings.

Analysis and Results

Summary Statistics

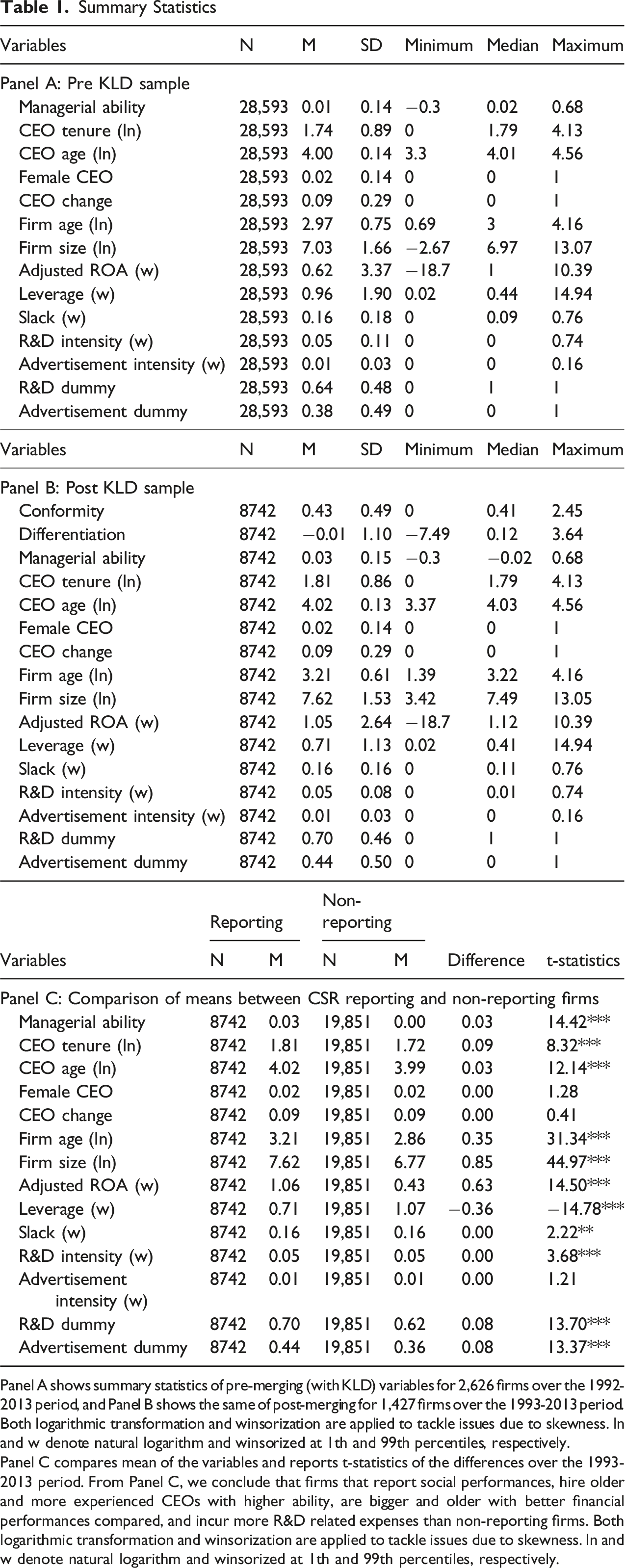

Panel A shows summary statistics of pre-merging (with KLD) variables for 2,626 firms over the 1992-2013 period, and Panel B shows the same of post-merging for 1,427 firms over the 1993-2013 period. Both logarithmic transformation and winsorization are applied to tackle issues due to skewness. ln and w denote natural logarithm and winsorized at 1th and 99th percentiles, respectively.

Panel C compares mean of the variables and reports t-statistics of the differences over the 1993-2013 period. From Panel C, we conclude that firms that report social performances, hire older and more experienced CEOs with higher ability, are bigger and older with better financial performances compared, and incur more R&D related expenses than non-reporting firms. Both logarithmic transformation and winsorization are applied to tackle issues due to skewness. ln and w denote natural logarithm and winsorized at 1th and 99th percentiles, respectively.

Pairwise Correlation Coefficients

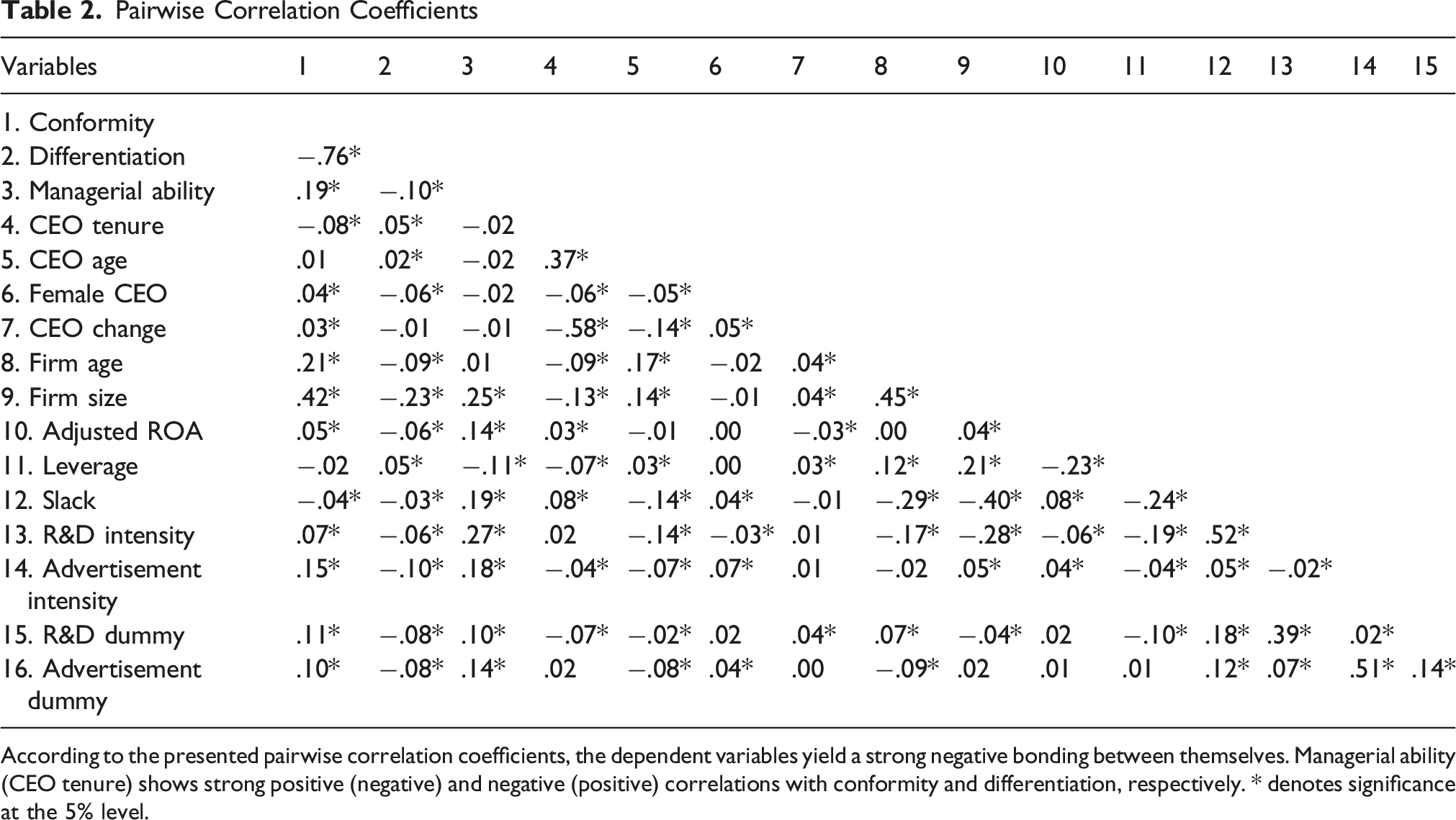

According to the presented pairwise correlation coefficients, the dependent variables yield a strong negative bonding between themselves. Managerial ability (CEO tenure) shows strong positive (negative) and negative (positive) correlations with conformity and differentiation, respectively. * denotes significance at the 5% level.

Effect of Managerial Ability on Conformity and Differentiation

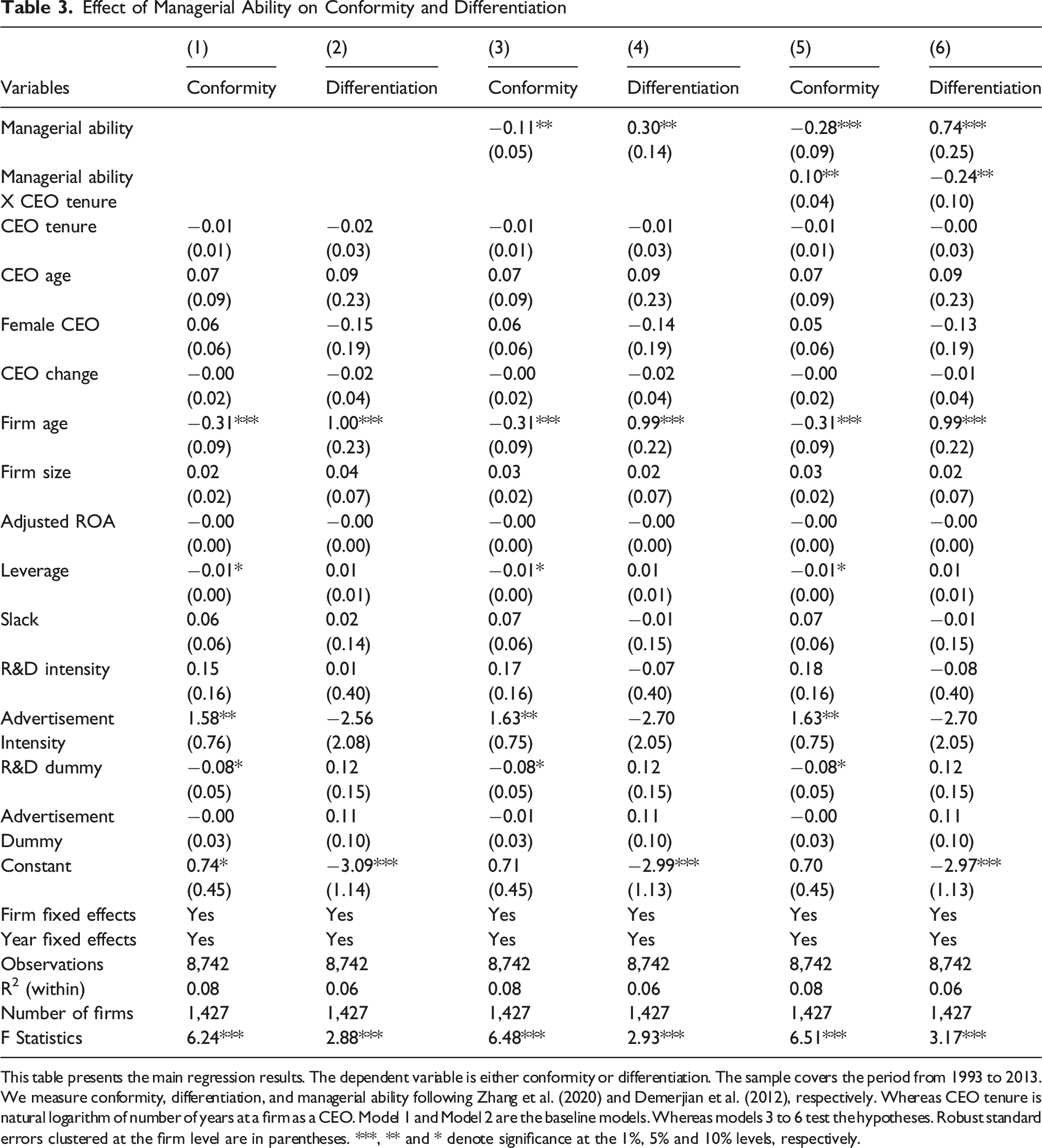

This table presents the main regression results. The dependent variable is either conformity or differentiation. The sample covers the period from 1993 to 2013. We measure conformity, differentiation, and managerial ability following Zhang et al. (2020) and Demerjian et al. (2012), respectively. Whereas CEO tenure is natural logarithm of number of years at a firm as a CEO. Model 1 and Model 2 are the baseline models. Whereas models 3 to 6 test the hypotheses. Robust standard errors clustered at the firm level are in parentheses. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

It is also worth examining the effects of some control variables. Specifically, we find that a mature firm appears to discourage conformity and encourage differentiation. We also show that leverage dampens conformity efforts, while advertisement intensity favors conformity.

Next, we interact the managerial ability and CEO tenure in Model 5 and Model 6 to test hypotheses 2a and 2b, respectively. A positive coefficient on Managerial ability X CEO tenure in Model 5 informs that CEO tenure makes the negative relationship between conformity and managerial ability less negative. In other words, the adverse effect of managerial ability on conformity falls with rising CEO tenure. Similarly, the negative coefficient on the interaction term in Model 6 makes the positive differentiation-managerial ability association less positive, providing support to hypothesis 2b.

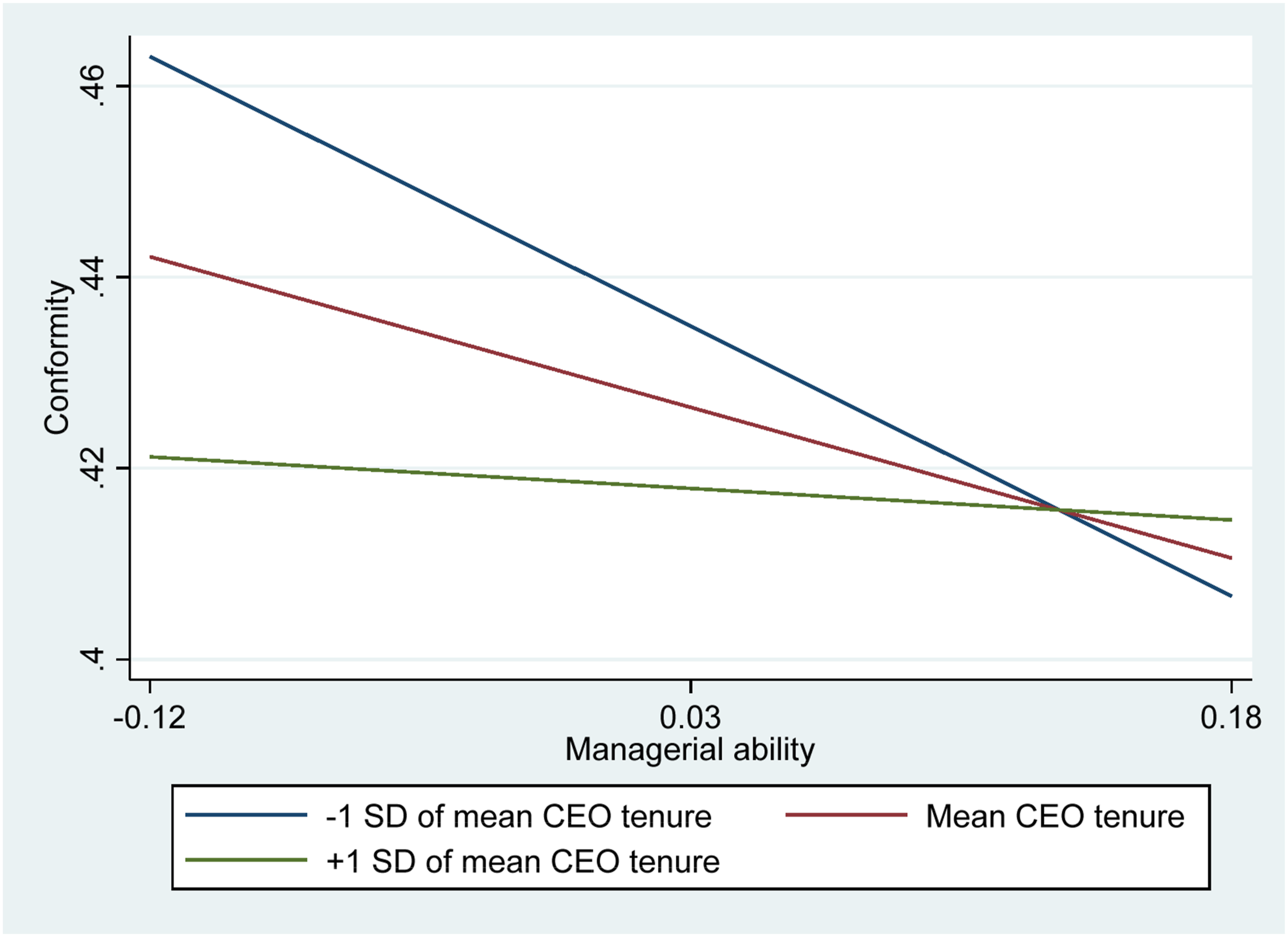

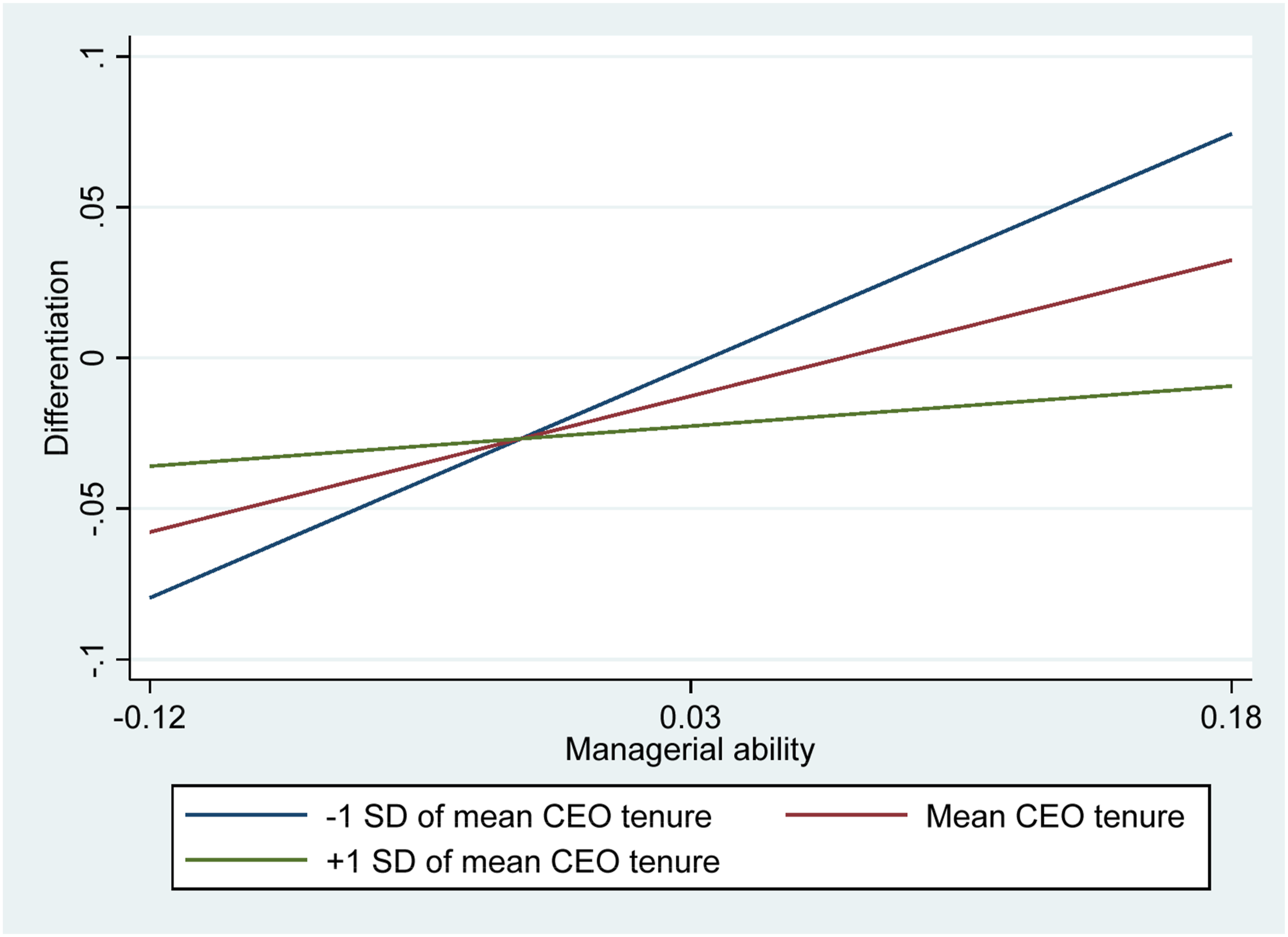

For visualization purposes, we plot these interactions in Figures 1 and 2, corresponding to Models 5 and 6, respectively. Non-parallel lines in both figures signify that the effects of managerial ability vary by CEO tenure. All downward and upward sloping lines in Figures 1 and 2 signify negative and positive conformity-managerial ability and differentiation-managerial ability relationships, respectively. For example, the adverse marginal impact of managerial ability falls from −0.29 to −0.26 as CEO tenure rises from 1 SD below mean to 1 SD above mean CEO tenure. Similarly, the positive marginal effect on differentiation of managerial ability falls from 0.77 to 0.70 with an increase in CEO tenure from −1 SD of mean CEO tenure to +1 SD of mean CEO tenure. CEO Tenure’s Moderating Role in Conformity-Managerial Ability. Figure 1 Displays the Positive Moderating Role of CEO Tenure in the Negative Conformity and Managerial Ability Association. The Negative Association is Exemplified by the Downward Sloping Lines. The Highest and Least Absolute Slopes Correspond to the Lowest and Highest CEO Tenure, Respectively CEO Tenure’s Moderating Role in Differentiation-Managerial Ability. Figure 2 Displays the Negative Moderating Role of CEO Tenure in the Positive Differentiation and Managerial Ability Association. The Positive Association is Exemplified by the Upward Sloping Lines. The Highest and Least Slopes Correspond to the Lowest and Highest CEO Tenure, Respectively

Endogeneity Tests

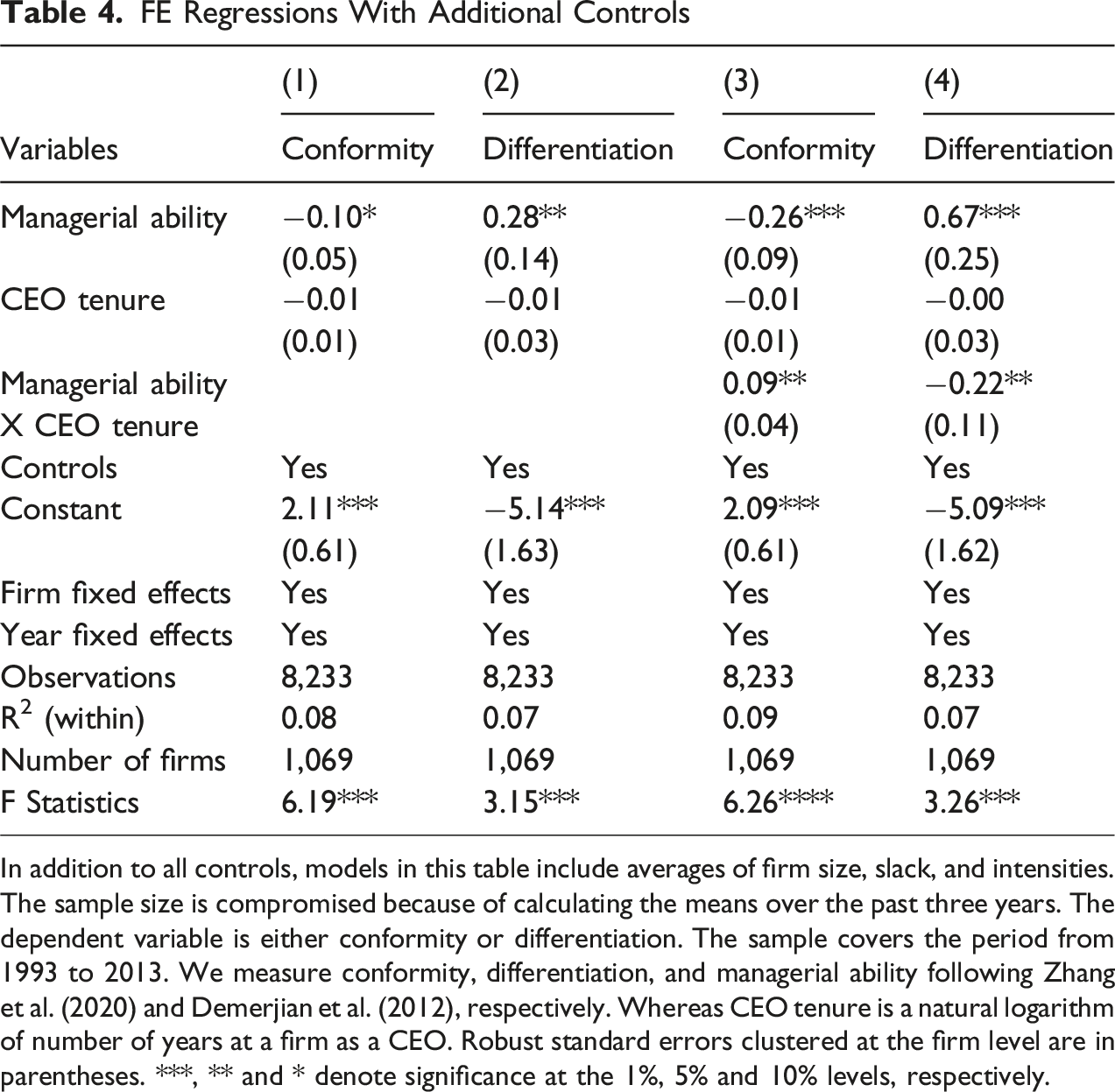

FE Regressions With Additional Controls

In addition to all controls, models in this table include averages of firm size, slack, and intensities. The sample size is compromised because of calculating the means over the past three years. The dependent variable is either conformity or differentiation. The sample covers the period from 1993 to 2013. We measure conformity, differentiation, and managerial ability following Zhang et al. (2020) and Demerjian et al. (2012), respectively. Whereas CEO tenure is a natural logarithm of number of years at a firm as a CEO. Robust standard errors clustered at the firm level are in parentheses. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

Managerial ability not only influences conformity and differentiation, but it is also likely that firms hire CEOs with specific ability scores to meet certain levels of CSR performance. This makes managerial ability depend on conformity and differentiation. We adhere to the instrumental variable approach to tackle this reverse causality issue. Existing literature documents industry average of a potential endogenous independent variable as a valid and strong instrument to it (Chen et al., 2019). Hence, company managerial ability is instrumented by annual industry average managerial ability (of other firms), which should statistically explain the ability, rather than any of the dependent variables. The effective F statistics of Montiel-Pflueger robust weak-instrument test is 114.13 that is greater than 37.42, the critical value at 5% confidence level. This proves validity, relevance, and strength of the instrumental variable (Abdurakhmonov et al., 2022). Also, statistically insignificant endogeneity test statistics in case of both conformity (0.12, p = .73) and differentiation (0.18, p = .67) reflect absence of concerning level of endogeneity in the relationships tested. Further, Davidson-MacKinnon test of exogeneity yields statistics of 0.03 (p = .87) and 1.18 (p = .28) in case of conformity and differentiations as the explained, respectively. Non-rejection of the null implies that any potential endogeneity is not biasing our results (Abdurakhmonov et al., 2022). As an additional endogeneity check we resort to IV-probit model. We created two binary variables – one for conformity and another for differentiation. Both binary measures take the value 1 if the corresponding dependent variable is positive and 0 otherwise. In both cases, the models fail to reject the null of the Wald test (χ2 = 1.57; p = .21 for conformity and χ2 = 0.29; p = .59 for differentiation), implying unlikeliness of concerning level of endogeneity in the sample.

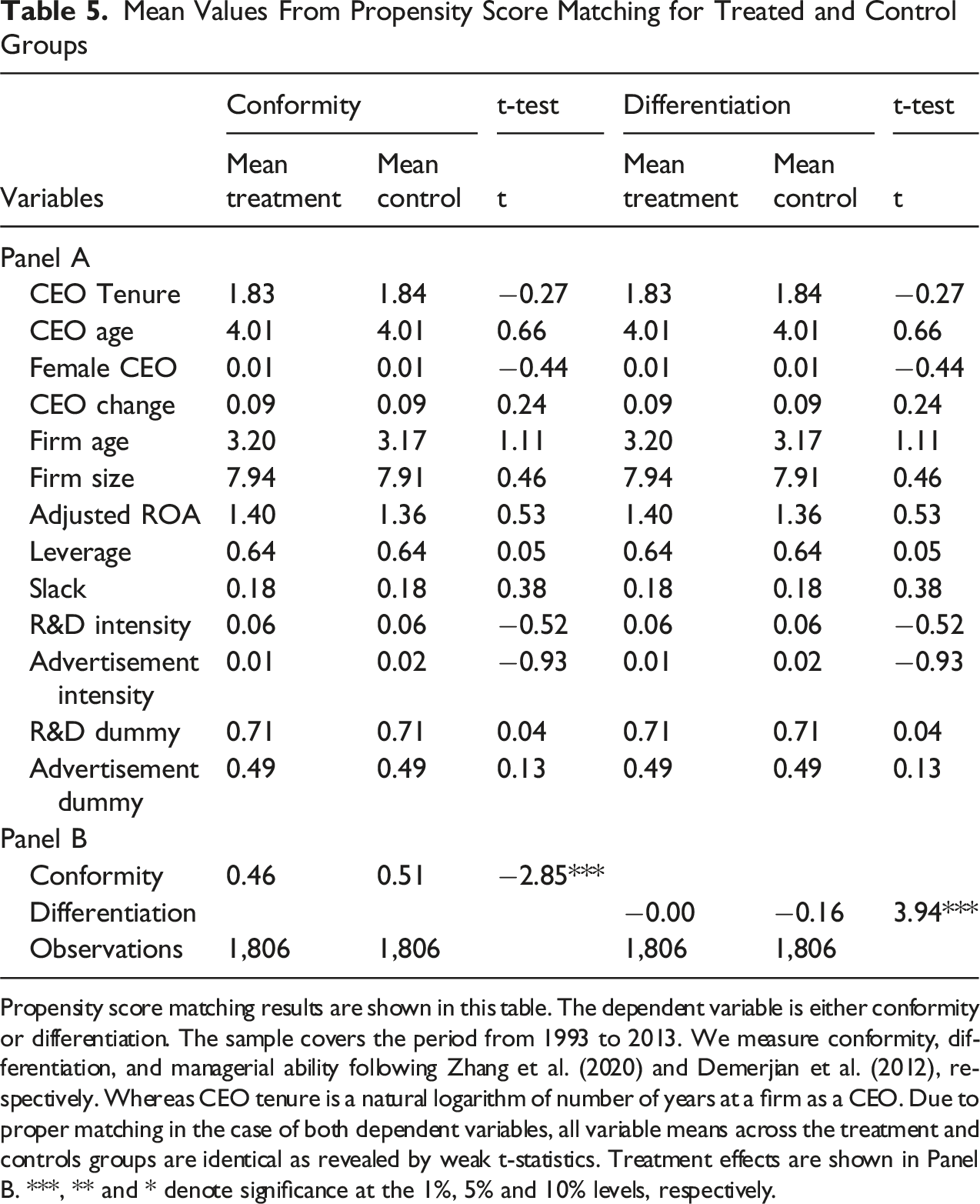

Mean Values From Propensity Score Matching for Treated and Control Groups

Propensity score matching results are shown in this table. The dependent variable is either conformity or differentiation. The sample covers the period from 1993 to 2013. We measure conformity, differentiation, and managerial ability following Zhang et al. (2020) and Demerjian et al. (2012), respectively. Whereas CEO tenure is a natural logarithm of number of years at a firm as a CEO. Due to proper matching in the case of both dependent variables, all variable means across the treatment and controls groups are identical as revealed by weak t-statistics. Treatment effects are shown in Panel B. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

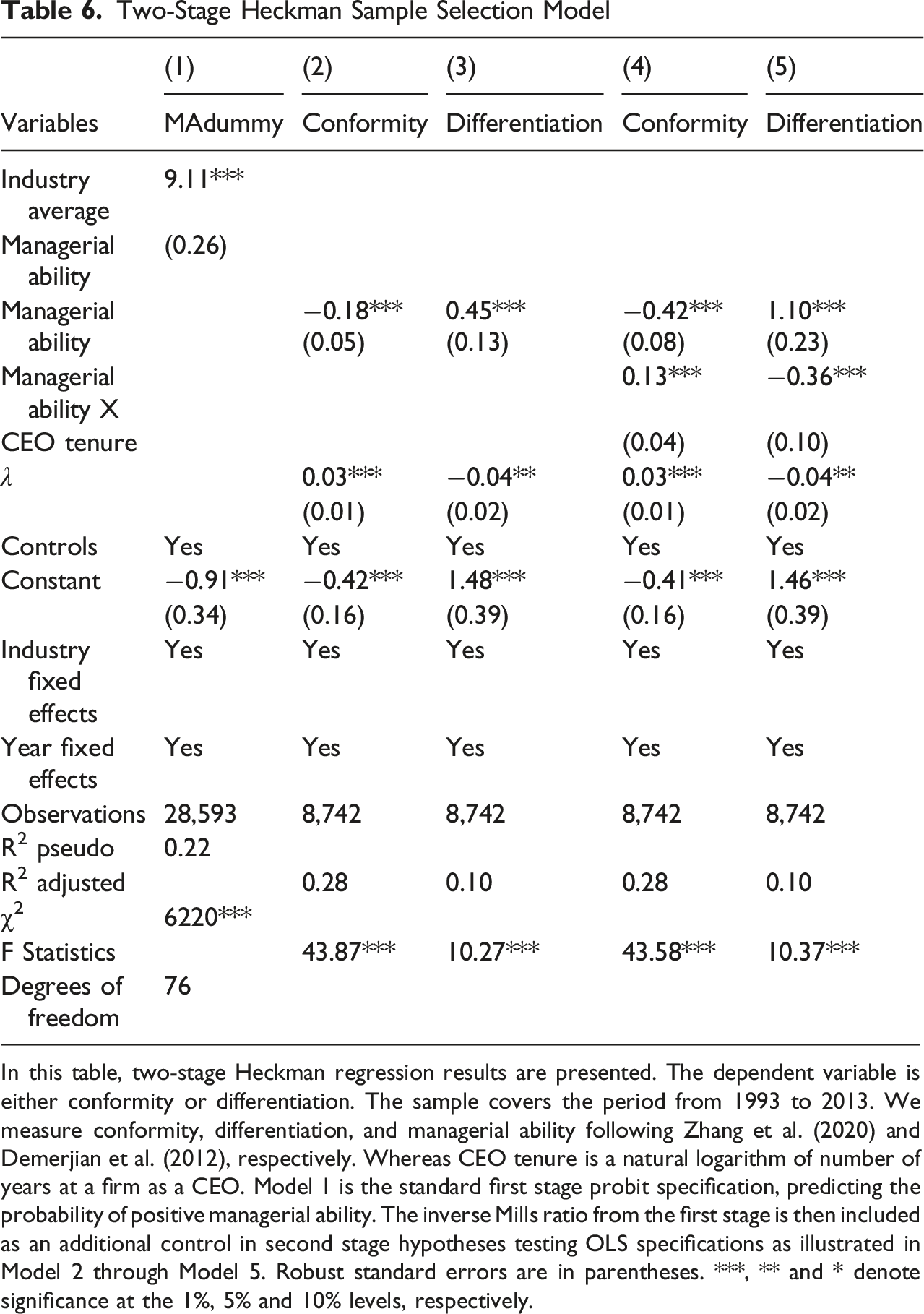

Two-Stage Heckman Sample Selection Model

In this table, two-stage Heckman regression results are presented. The dependent variable is either conformity or differentiation. The sample covers the period from 1993 to 2013. We measure conformity, differentiation, and managerial ability following Zhang et al. (2020) and Demerjian et al. (2012), respectively. Whereas CEO tenure is a natural logarithm of number of years at a firm as a CEO. Model 1 is the standard first stage probit specification, predicting the probability of positive managerial ability. The inverse Mills ratio from the first stage is then included as an additional control in second stage hypotheses testing OLS specifications as illustrated in Model 2 through Model 5. Robust standard errors are in parentheses. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

Robustness Tests

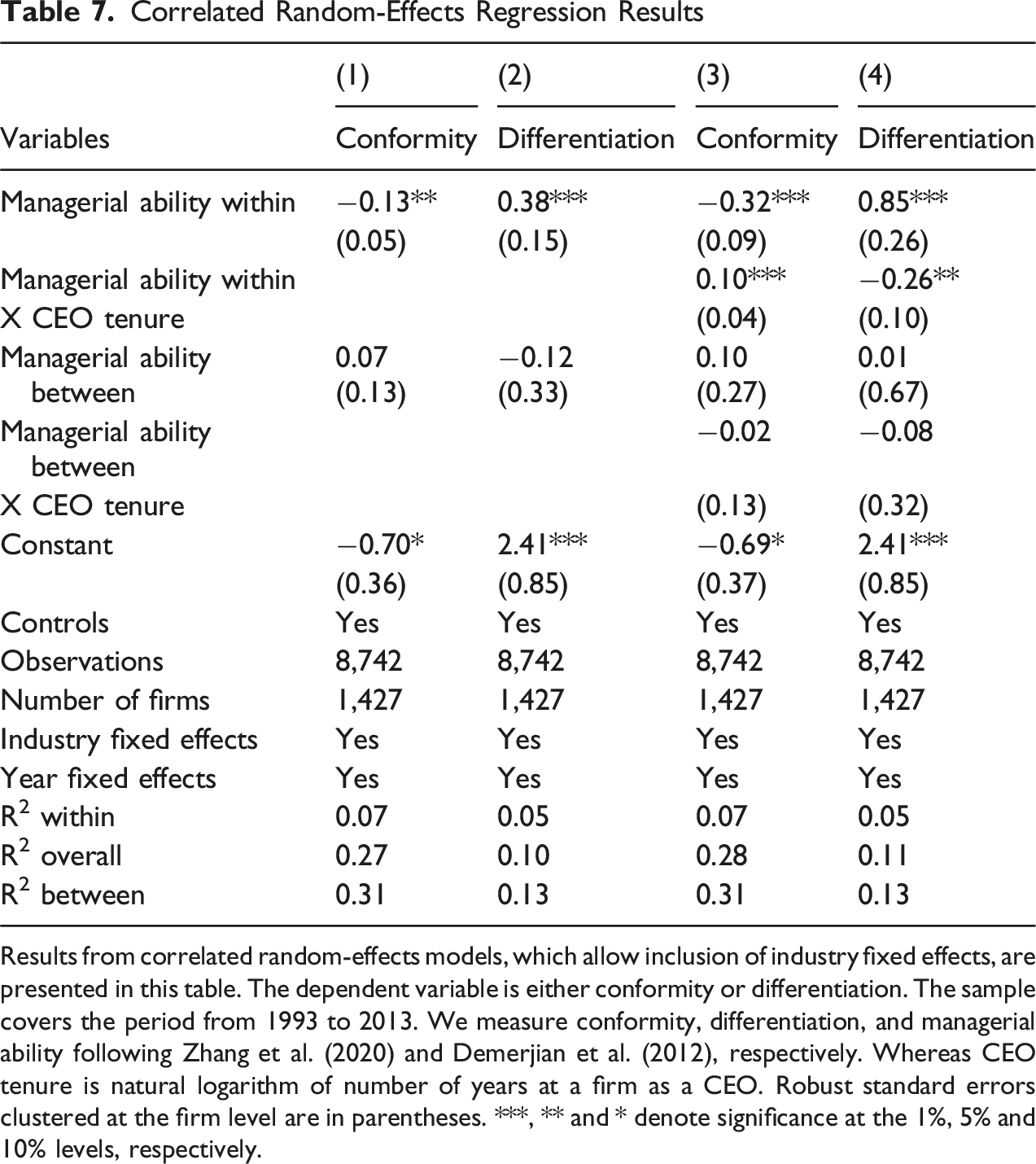

Correlated Random-Effects Regression Results

Results from correlated random-effects models, which allow inclusion of industry fixed effects, are presented in this table. The dependent variable is either conformity or differentiation. The sample covers the period from 1993 to 2013. We measure conformity, differentiation, and managerial ability following Zhang et al. (2020) and Demerjian et al. (2012), respectively. Whereas CEO tenure is natural logarithm of number of years at a firm as a CEO. Robust standard errors clustered at the firm level are in parentheses. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

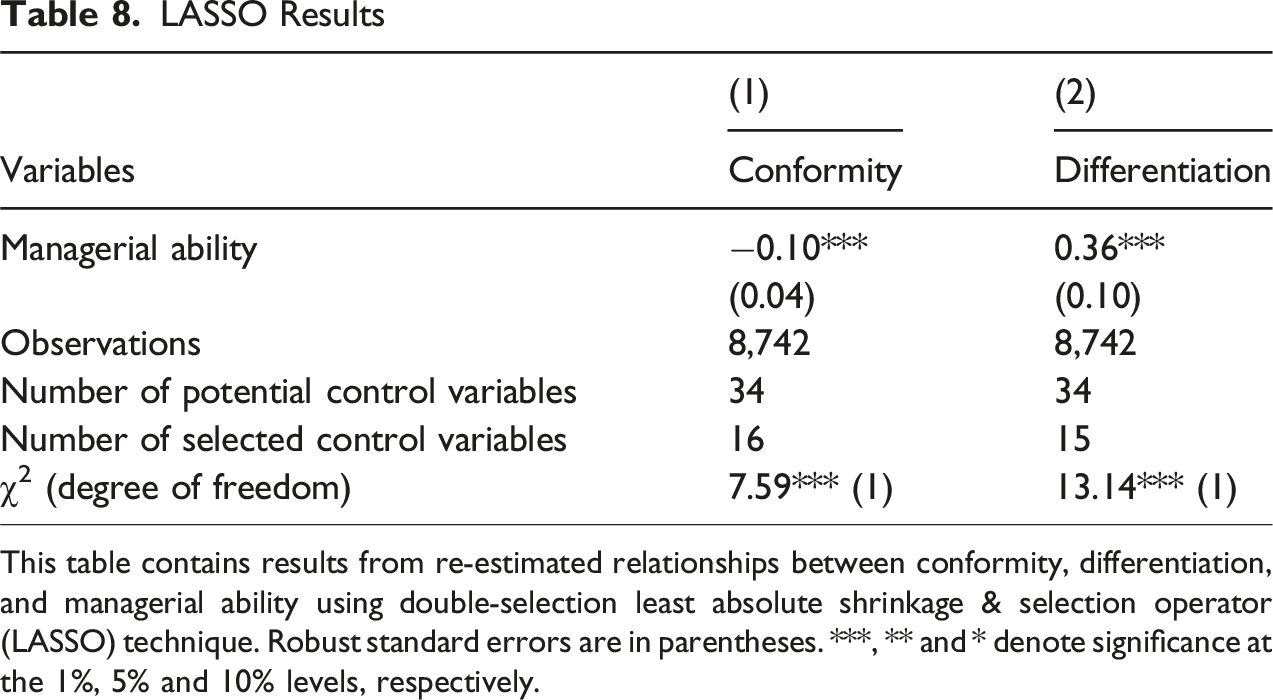

LASSO Results

This table contains results from re-estimated relationships between conformity, differentiation, and managerial ability using double-selection least absolute shrinkage & selection operator (LASSO) technique. Robust standard errors are in parentheses. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

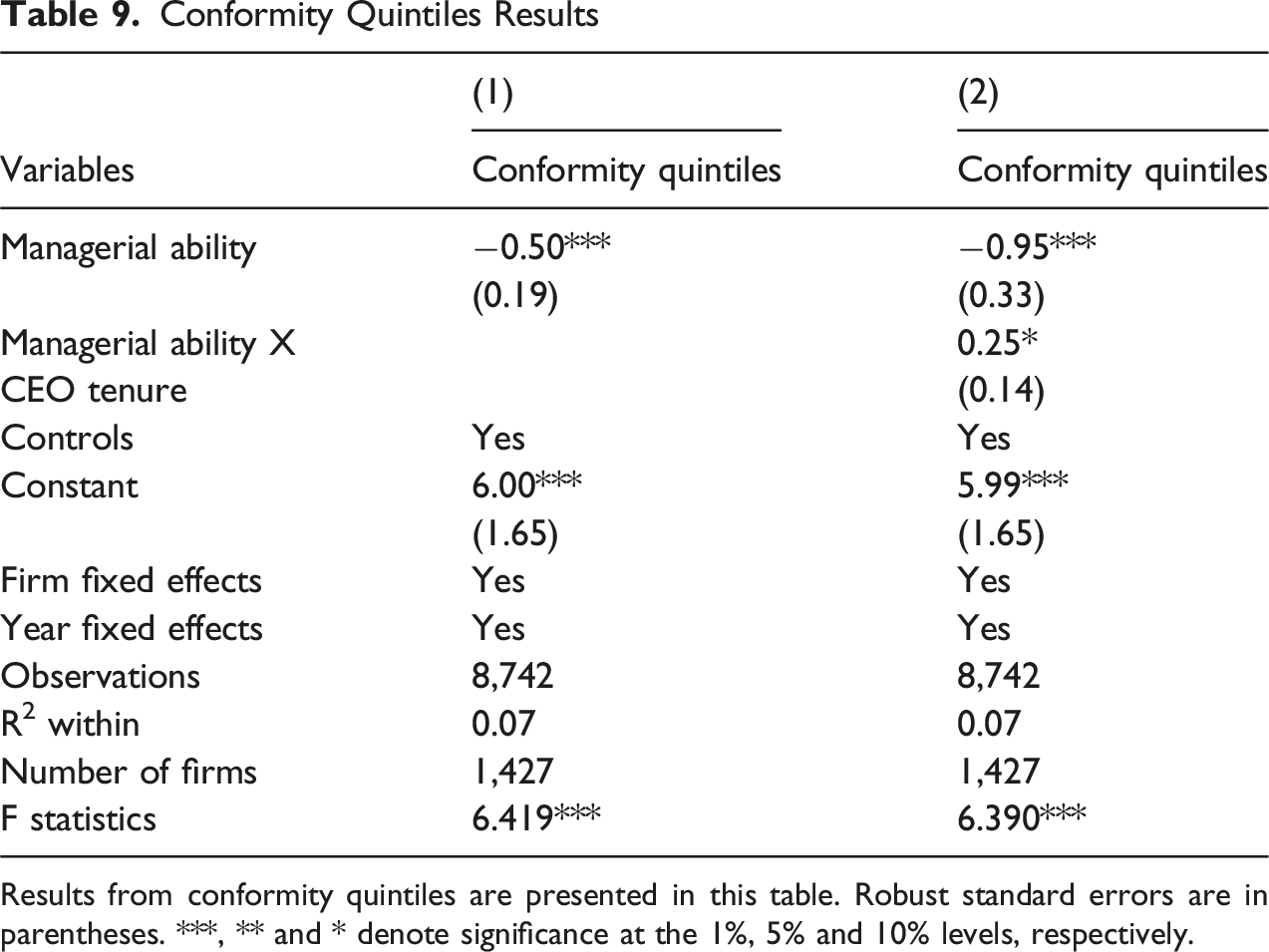

Conformity Quintiles Results

Results from conformity quintiles are presented in this table. Robust standard errors are in parentheses. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

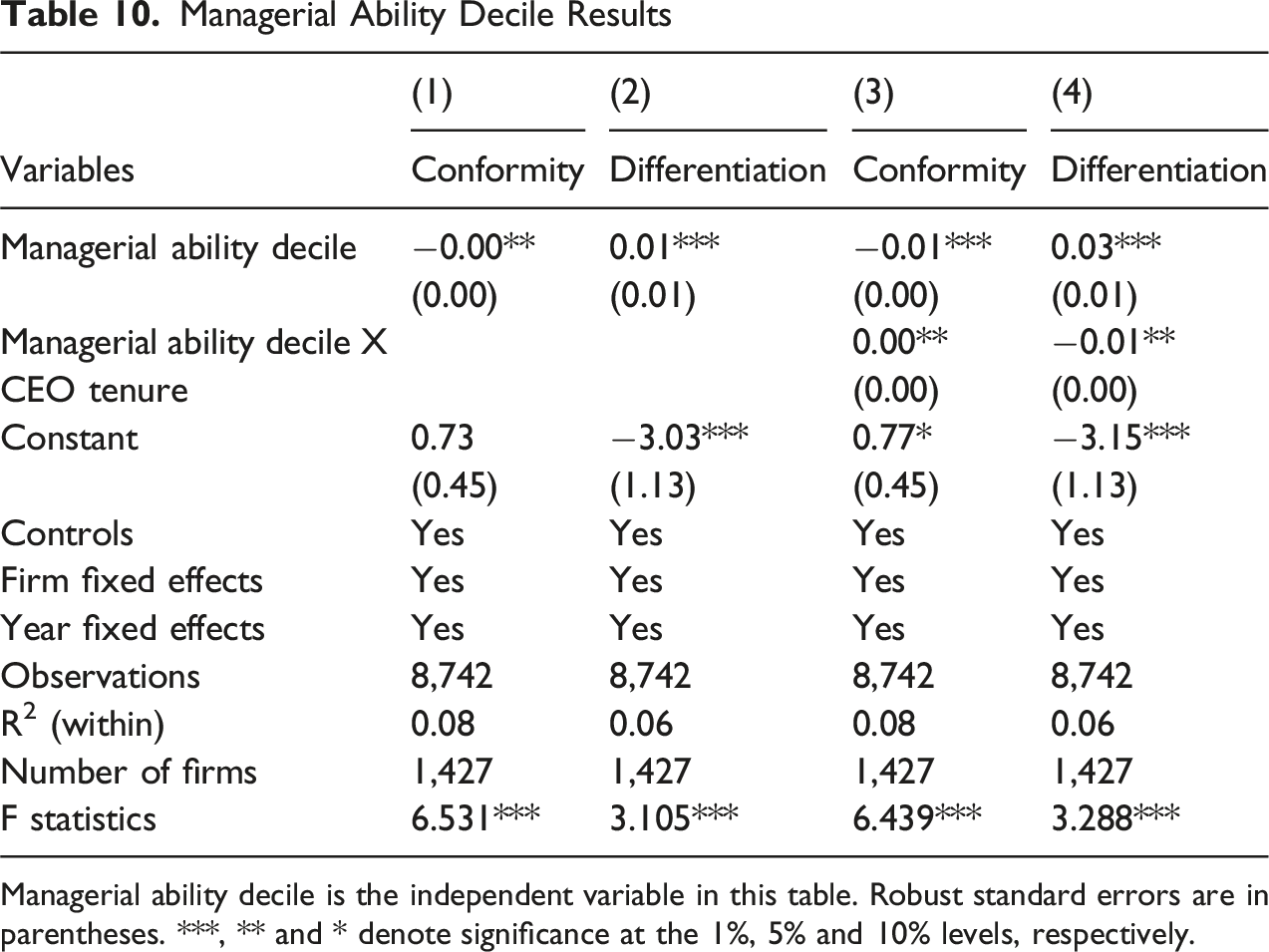

Managerial Ability Decile Results

Managerial ability decile is the independent variable in this table. Robust standard errors are in parentheses. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

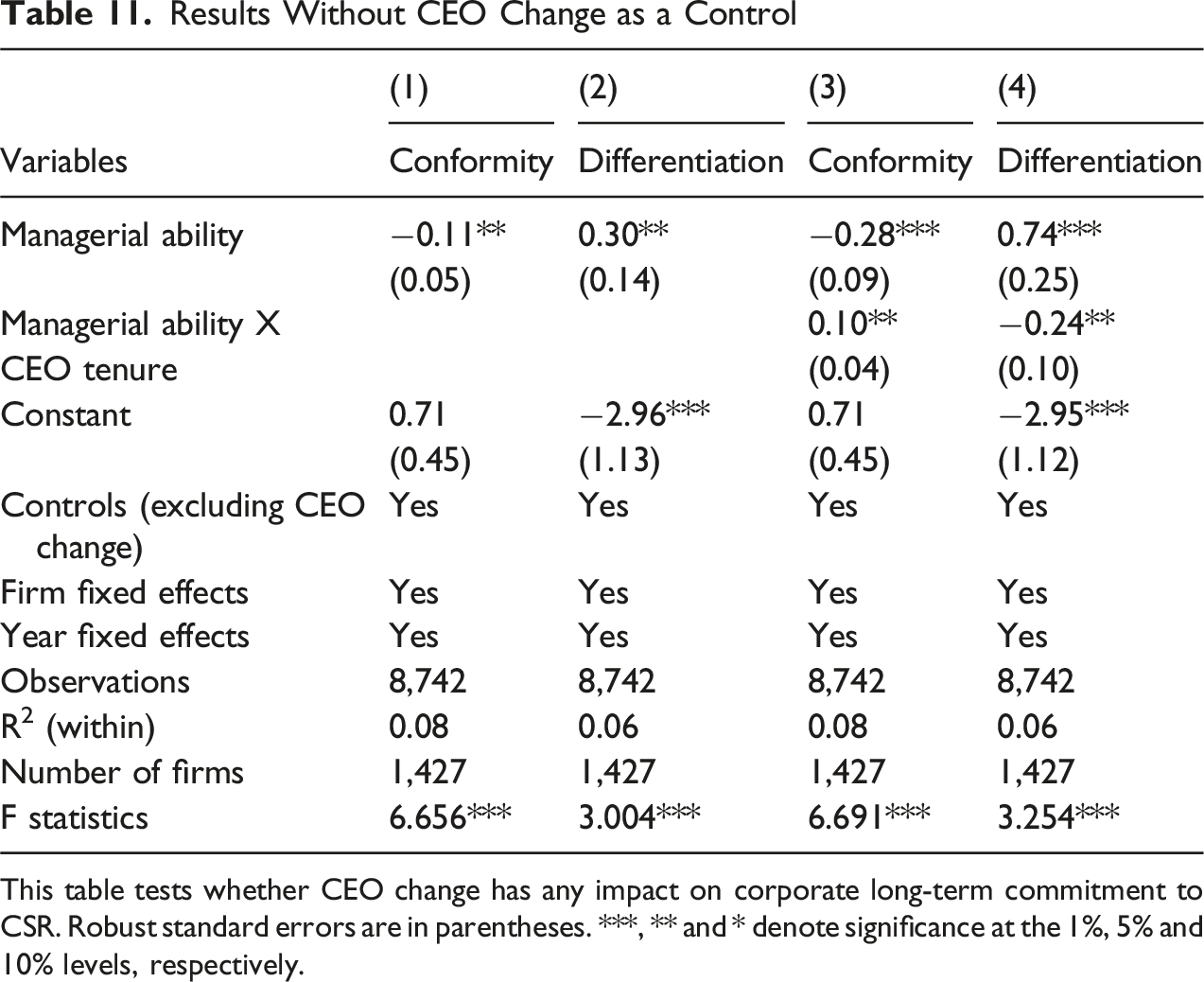

Results Without CEO Change as a Control

This table tests whether CEO change has any impact on corporate long-term commitment to CSR. Robust standard errors are in parentheses. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

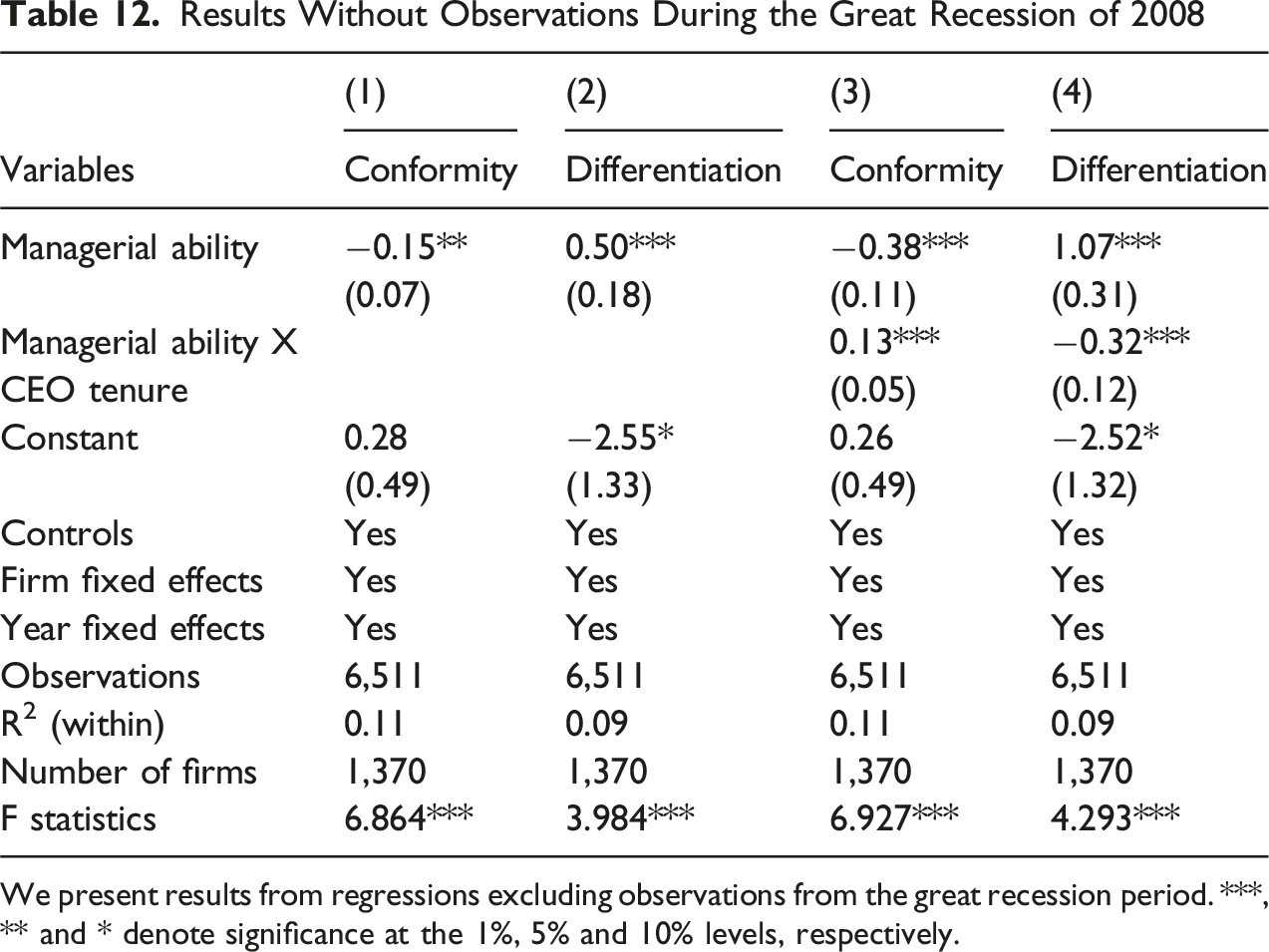

Results Without Observations During the Great Recession of 2008

We present results from regressions excluding observations from the great recession period. ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

Again, we rerun our models using alternative measures of firm size (natural logarithm of total assets or number of employees), industry adjusted ROA (income before extraordinary items or operating income before depreciation or earnings before interest, taxes, depreciation, and amortization), other industry adjusted financial performance (ROE, net income scaled by value of common equity or ROI, net income scaled by total invested capital or ROS, net income scaled by net sales), leverage (total liabilities or total long-term debt or total long-term debt plus current debts scaled by total assets), and slack (current or quick ratio). The outcomes are similar to the main results.

Discussion

The main objective of this study was to examine the relationship between CEO managerial ability and corporate social responsibility (CSR) conformity and differentiation, and the moderating role of CEO tenure in this relationship. In line with prior research, we found that managerial ability is positively related to CSR differentiation, but the relationship between managerial ability and CSR conformity is negative. We also found that CEO tenure moderates the relationship between managerial ability and both CSR conformity and differentiation. Specifically, as CEO tenure increases, the negative relationship between managerial ability and CSR conformity becomes less negative, while the positive relationship between managerial ability and CSR differentiation becomes less positive.

The findings of this study contribute to the existing literature on CEO characteristics and organizational outcomes in several ways. First, our study adds to the growing body of research on the role of CEO characteristics in shaping organizational behavior. Prior research has identified a number of factors that can influence CEO behavior and decision-making, including age, experience, gender, and tenure (Hambrick & Mason, 1984; Hambrick & Cannella, 2007; Zhang et al., 2020). Our study contributes to this literature by demonstrating that managerial ability is an important predictor of CSR outcomes and non-market strategies (Al-Shammari et al., 2025), and that the relationship between managerial ability and CSR conformity and differentiation is moderated by CEO tenure.

Second, our study contributes to the literature on CSR conformity and differentiation. While prior research has examined the antecedents and consequences of these two constructs (Pan et al., 2020; Quigley & Hambrick, 2015), little is known about the role of CEO characteristics in shaping firms’ CSR strategies. Our study fills this gap by showing that managerial ability is related to both conformity and differentiation, and that the relationship between managerial ability and these outcomes is moderated by CEO tenure.

Ultimately, our study holds implications for both practitioners and policymakers. Our findings suggest that CEO managerial ability is an important factor to consider when designing and implementing CSR strategies. In particular, firms with more able CEOs may be more likely to pursue differentiated CSR strategies, while those with less able CEOs may be more likely to conform to industry norms. This suggests that organizations should prioritize the hiring of more able CEOs, as they may be more likely to implement CSR practices that create a competitive advantage.

Furthermore, our study underscores the moderating role of CEO tenure in the relationship between managerial ability and CSR outcomes. As CEO tenure increases, the positive relationship between managerial ability and CSR differentiation becomes weaker. This suggests that organizations should consider rotating CEOs or implementing other measures to prevent CEOs from becoming too entrenched in their views and less open to alternative perspectives.

Our study’s findings corroborate the argument that managerial ability has a positive relationship with CSR differentiation and a negative one with CSR conformity. This highlights the importance of considering how managerial ability can shape a firm’s approach to CSR. Our results suggest that more able CEOs may prefer a differentiation strategy, which is more efficient, less costly, and more relevant to stakeholders, compared to a conformity strategy. Additionally, our results show that the relationship between managerial ability and CSR conformity is moderated by CEO tenure, with the negative relationship decreasing as CEO tenure increases. These findings have implications for both researchers and practitioners as they highlight the importance of considering the role of managerial ability in shaping a firm’s approach to CSR and the potential for changes in this relationship over time.

Theoretical Implications

Our findings generate four precise theoretical advances. First, we extend Upper Echelons Theory by identifying a specific cognitive mechanism, resource-allocation efficiency, through which CEO characteristics translate into strategic choices. While prior UET research documents that CEO ability affects firm performance, we demonstrate HOW ability operates: high-ability CEOs’ superior information-processing capacity (Nadkarni & Herrmann, 2010) enables them to map stakeholder claims onto targeted CSR domains, manifesting as emphasis differentiation rather than broad conformity. This reveals the ability as a filtering mechanism that shapes how CEOs interpret and respond to institutional pressures.

Second, we refine rather than integrate institutional theory by showing that conformity pressure operates as a boundary condition for UET predictions. Specifically, high-ability CEOs do not ignore legitimacy demands, but rather satisfy them more efficiently through focused, high-impact CSR initiatives. This selective response to institutional pressure, achieving legitimacy through differentiation rather than wholesale conformity, suggests that managerial discretion and institutional constraints are not opposing forces but can be strategically reconciled through resource-allocation expertise.

Third, we advance CEO tenure literature by documenting a specific behavioral mechanism underlying the tenure-performance relationship. Our interaction findings reveal that tenure accumulation shifts high-ability CEOs from differentiation toward conformity, suggesting that power consolidation paradoxically reduces strategic distinctiveness. This ‘convergence effect’ reconciles conflicting findings in tenure research: early-tenure CEOs leverage ability for differentiation (consistent with fresh perspective arguments), while late-tenure CEOs converge toward industry norms despite retained ability (consistent with entrenchment arguments). The key insight is that tenure moderates not ability itself but its strategic expression.

Finally, firm size may represent an important and relevant factor in the relationship between CEO ability and firm’s CSR policies (De Meulenaere et al., 2021; Yuan et al., 2019), but not in the simplistic way often discussed. Larger companies are bound by an increased public scrutiny and their actions and policies draw more attention from major stakeholders and activists such as the media and analysts (Al-Shammari et al., 2022; Aouadi & Marsat, 2018; Harrison et al., 2018; Zhang et al., 2020), which can intensify legitimacy pressures and limit the extent to which highly capable CEOs can pursue CSR initiatives that distinguish them from competitors. On the other hand, smaller businesses may have greater margin of freedom due to the lower profile they have and less attention they receive from the media and other major stakeholder groups (Chiu & Sharfman, 2011; Udayasankar, 2008), allowing their CEOs to implement CSR in innovative and impactful ways that would enhance their unique identity and visibility. This perspective builds on the literature that ties firm’s size to the visibility profile and thus the overall pressure the firm faces. It contends that firm size is not just a variable to control for but a critical factor that indirectly influences how managerial talent translates into unique CSR practices through visibility/public pressure. Future investigations could thus explore whether the legitimacy/visibility pressures that larger companies face will promote conformity, while smaller enterprises facilitate more radical differentiation, thereby addressing a significant gap in understanding how organizational scale interacts with executive talent in shaping CSR strategies.

Limitations

Several limitations in our study warrant consideration when interpreting the results. First, our sample consists of publicly listed firms, which may not be representative of all firms, especially privately owned firms. Additionally, our sample is limited to firms with available data in the KLD database, which may introduce bias. Moreover, because the sample is restricted to U.S. listed firms, the findings may not travel to institutional contexts with different legitimacy logics; cross-national tests would bolster external validity.

Second, our measures of managerial ability, CEO tenure, and the control variables may be subject to measurement error. In particular, our measure of managerial ability is based on analysts’ perceptions, which may not fully capture a CEO’s actual ability. Additionally, our measure of CEO tenure may not accurately capture the length of time a CEO has been with the firm, as it is based on calendar years rather than actual days worked.

Despite these limitations, our study offers significant insights into how CEO managerial ability relates to CSR conformity and differentiation. Future research could extend our study by using a larger, more diverse sample and including measures of CSR performance or impact. Additionally, longitudinal studies that track changes in CSR practices over time could help to further understand the mechanisms driving the relationships we have identified.

Future Research

Building directly on our theoretical implications, we identify two theory-driven avenues of future research. First, scholars should examine “differentiation windows,” which are time-bounded periods triggered by exogenous shifts (e.g., rating-methodology revisions, regulatory guidance, or salient stakeholder events) during which the legitimacy penalty for selective nonconformity temporarily falls. Under Upper Echelons Theory (UET), higher managerial ability should increase the precision with which CEOs detect and exploit such windows, reallocating resources toward distinctive CSR actions when the risk–return frontier improves. Second, researchers should analyze board expertise composition (e.g., domain expertise, CSR/governance, regulatory experience) as a moderator that channels or constrains the conversion of managerial ability into CSR differentiation through both advice (cognitive resources) and monitoring (risk calibration) mechanisms. Together, these directions move beyond generic moderators and specify when and how ability translates into optimal distinctiveness.

Future research could also explore more nuanced boundary conditions that shape the ability-CSR relationship. While we examined CEO tenure as an internal contingency, the ability-differentiation relationship may exhibit important nonlinearities based on firm life cycle stage. Specifically, high-ability CEOs in mature firms facing legitimacy threats may need to balance differentiation with selective conformity, while those in growth-stage firms may have greater latitude for CSR innovation. This suggests examining how organizational age interacts with competitive dynamics to create ‘differentiation windows’, periods when deviation from CSR norms yields maximum returns. Additionally, future work could investigate how board expertise composition moderates the ability-CSR relationship. Boards with deep sustainability expertise may amplify able CEOs’ differentiation strategies by providing specialized knowledge resources, while boards dominated by financial experts may constrain CSR innovation regardless of CEO ability. Such research would address the understudied question of how governance structures either unleash or constrain managerial ability in non-market domains.

Finally, future research could extend our study by exploring the consequences of CSR differentiation for firms. For example, research could examine whether firms with more differentiated CSR strategies experience superior financial performance, stakeholder relations, or reputation. Such research would provide valuable insights for firms considering the trade-offs between conformity and differentiation in their CSR strategies.

Conclusion

In conclusion, our study illuminates the relationship between CEO managerial ability and Corporate Social Responsibility (CSR) in terms of both conformity and differentiation. Our results suggest that CEO managerial ability is positively related to CSR differentiation, but this relationship is moderated by CEO tenure. Specifically, as CEO tenure increases, the positive relationship between managerial ability and CSR differentiation decreases. These findings provide important insights for researchers and practitioners on the role of CEO characteristics in shaping firm-level CSR practices. Future research could explore other CEO characteristics, such as values and personality, and their impact on CSR strategy. Additionally, examining the mediating mechanisms through which CEO managerial ability affects CSR differentiation could provide further insight into this relationship.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated and/or analyzed during the current study are from Wharton Research Data Services, which is accessible only through subscriptions. Therefore, the databases used in the current study are publicly unavailable.

Author Biographies

Appendix

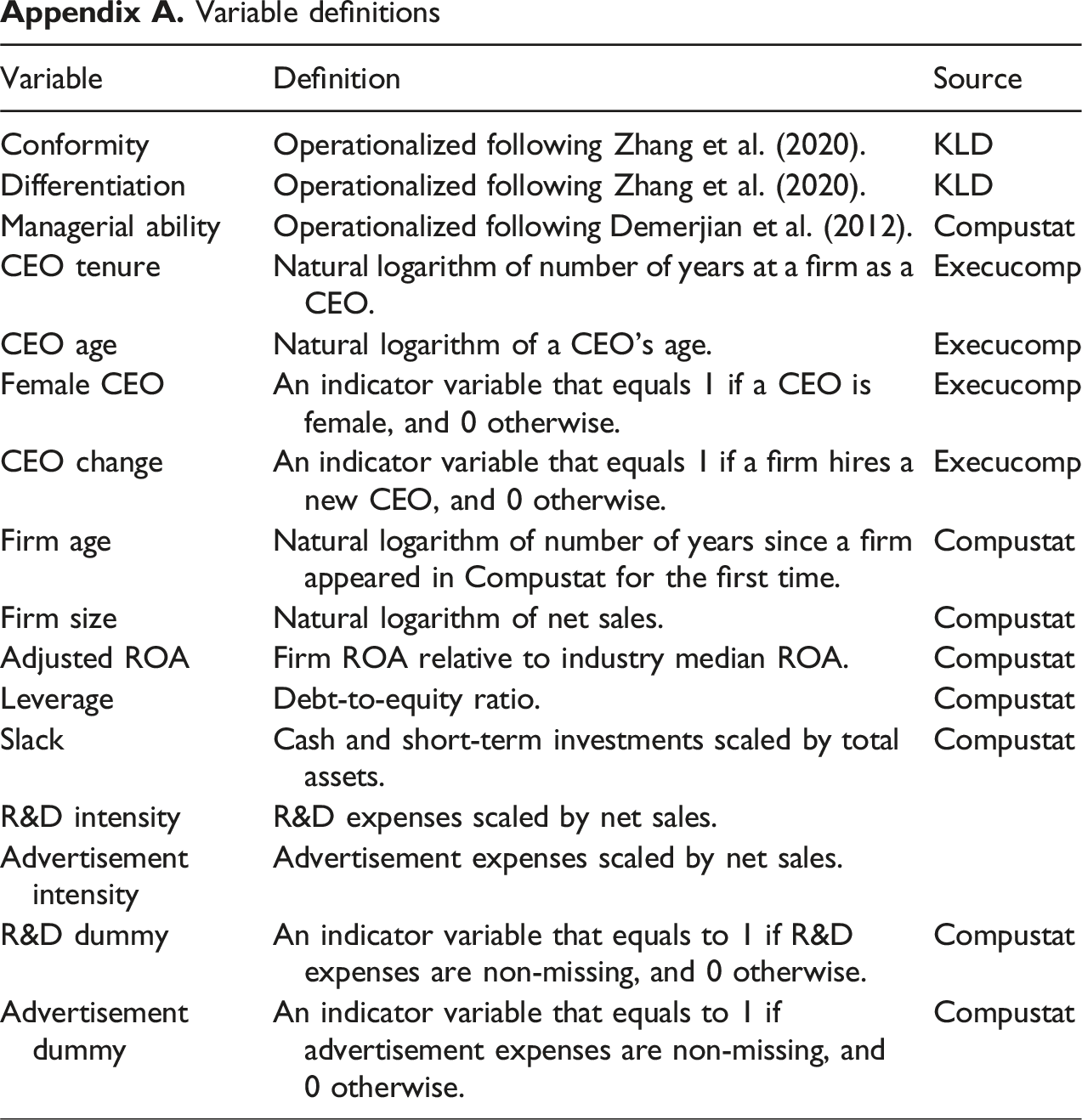

Variable definitions

Variable

Definition

Source

Conformity

Operationalized following Zhang et al. (2020).

KLD

Differentiation

Operationalized following Zhang et al. (2020).

KLD

Managerial ability

Operationalized following Demerjian et al. (2012).

Compustat

CEO tenure

Natural logarithm of number of years at a firm as a CEO.

Execucomp

CEO age

Natural logarithm of a CEO’s age.

Execucomp

Female CEO

An indicator variable that equals 1 if a CEO is female, and 0 otherwise.

Execucomp

CEO change

An indicator variable that equals 1 if a firm hires a new CEO, and 0 otherwise.

Execucomp

Firm age

Natural logarithm of number of years since a firm appeared in Compustat for the first time.

Compustat

Firm size

Natural logarithm of net sales.

Compustat

Adjusted ROA

Firm ROA relative to industry median ROA.

Compustat

Leverage

Debt-to-equity ratio.

Compustat

Slack

Cash and short-term investments scaled by total assets.

Compustat

R&D intensity

R&D expenses scaled by net sales.

Advertisement intensity

Advertisement expenses scaled by net sales.

R&D dummy

An indicator variable that equals to 1 if R&D expenses are non-missing, and 0 otherwise.

Compustat

Advertisement dummy

An indicator variable that equals to 1 if advertisement expenses are non-missing, and 0 otherwise.

Compustat