Abstract

Prior research on women in executive positions (WiE) has focused exclusively on the consequences of WiE by addressing how women executives influence firm strategy and performance, whereas little is known about the antecedents of WiE. However, to gain a comprehensive understanding of the overall impact of women executives on the firm, it is worthwhile to identify the triggers that prompt firms to appoint women executives for the first time. In this study, we have attempted to identify the antecedents of first appointments of women to executive teams (FAWE). On the basis of a theoretical frame incorporating the think crisis–think female perspective into the punctuated equilibrium model, we consider FAWE as the process of the transformational reform of an organization and examine the roles of three factors—firm performance (i.e., ROA and aspirational performance), environmental changes (i.e., industry dynamism, industry munificence, and industry complexity), and new CEO appointments—as antecedents of FAWE. We conducted a panel logistic regression analysis using 20 years of panel data (2000–2019) for Japanese listed firms. Our findings demonstrate that (1) poor firm performance (ROA and aspirational performance) was significantly related to the likelihood of FAWE in the subsequent year, and (2) a new CEO appointment was significantly related to the likelihood of FAWE in the subsequent year, whereas (3) hypotheses regarding environmental changes (industry dynamism, industry munificence, and industry complexity) were not confirmed. Implications for researchers and practitioners are discussed, along with the study’s limitations and suggestions for future research.

Keywords

Introduction

The percentage of women in executive positions (WiE) has grown significantly in recent years since the 2013 OECD Gender Recommendations, with the average percentage of WiE in listed firms in OECD member countries reported at 28.0% (OECD, 2023). However, a further analysis of a sample of listed firms in 50 countries/regions using OECD data reported that women still represent only a quarter (25.1%) of executive teams and that the percentage of WiE of listed firms in 20 of the 50 countries/regions is less than 20% (Denis, 2022). Among them, the percentage of WiE of listed firms in Japan is only 12.6% (OECD, 2023), and furthermore, one-third of listed firms have no women executives (Gender Equality Bureau Cabinet Office, Government of Japan, 2021). Thus, the percentage of WiE of listed firms is still low, and further theoretical and practical studies are needed to improve gender diversity in corporate leadership.

Existing studies on WiE can be divided into two broad categories: (1) the effectiveness of WiE and (2) the emergence of WiE. First, with respect to the effectiveness of WiE, previous studies have reported that WiE has a positive effect on organizational-level outcomes, such as financial performance (e.g., Hoobler et al., 2018; Jeong & Harrison, 2017), the launch of new products or services (Lyngsie & Foss, 2017), management innovations (Heyden et al., 2018), and risk taking (Faccio et al., 2016). Second, regarding the emergence of WiE, there are fewer studies compared to the effectiveness of WiE, and furthermore, the reported results are inconsistent. For example, based on the so-called bottom-up effect, some studies have found that the presence of more women in lower-level positions is positively correlated with the hiring and promotion of WiE (Cohen et al., 1998; Gould et al., 2018). Other studies have examined whether poor firm performance leads to WiE based on the assumption of the glass cliff, but these studies have produced inconsistent findings. Specifically, Ryan and Haslam (2005) reported that stock market declines were positively correlated with WiE, while Adams et al. (2009) found no significant relationship between deteriorating firm performance and WiE.

As discussed above, many previous WiE studies have shown that WiE is effective for firm performance. Both researchers and practitioners may therefore be interested in obtaining more definitive answers on how to increase the number of women executives for higher firm performance, i.e., on the antecedents of WiE. As mentioned above, while some studies have gradually clarified the antecedents of WiE, these studies assume that there is at least one woman on the board of directors. However, with some listed firms still without a single woman on their boards (especially in Japan, where one-third of listed firms have no women board members), clarifying the triggers for firms to appoint women executives for the first time would be a more urgent issue in the quest to examine the antecedents of WiE.

Identifying the antecedents driving firms to appoint women to executive positions for the first time is important because it allows us to extend the discussion of women’s leadership in firms, which has remained confined to the glass ceiling (or glass cliff) and firm strategy perspectives. Specifically, the existing literature on the appointment of directors and new CEOs and the composition of top management teams (TMTs) has been discussed from the perspective of firm strategy (e.g., Baysinger & Hoskisson, 1990; Westphal & Fredrickson, 2001). On the other hand, the appointment of female directors and female CEOs has as yet been discussed mainly from a glass ceiling or glass cliff perspective (e.g., Cook & Glass, 2014; Ryan et al., 2016). However, when a firm appoints a woman director for the first time, the perspective of firm strategy is necessary. In other words, the discussion of women’s leadership in firms needs to be considered from the perspective of firm strategy and firm transformation, not just from the glass ceiling or glass cliff perspective. In what follows, we address the importance of identifying the antecedents leading to firms’ first appointment of a woman to an executive team 1 (FAWE).

First, the nomination of a female executive is expected to elicit more rigorous discussion by shareholders and existing executive members than that of a male executive (Terjesen et al., 2009). Executive teams, such as TMTs and boards of directors, require the approval of shareholders and existing executive members for the addition of new members to executive positions (Withers et al., 2012). Although existing studies have focused only on the characteristics of the women candidates being nominated (Glass & Cook, 2016), it is also necessary to consider the executive team that nominates the candidate and the circumstances of the firm involved in order to better understand the nomination of women to executive positions.

Second, a firm’s decision to appoint a woman executive for the first time may be driven by forces different from those driving decisions to increase the number of women executives when at least one woman already serves on the firm’s executive team. Given the similarity-attraction theory (Byrne, 1971), which posits that people tend to like and be most attracted to others who are similar to themselves, executive teams that are made up solely of men are likely to show a strong inertia in favor of preserving team homogenization (Boone et al., 2004). In that light, when a firm appoints a woman for the first time, there will obviously be significant resistance, and winning approval for the appointment will be more difficult than it is in firms with at least one woman already on the executive team. Studies report that when women are on the board of directors, other women are more likely to be appointed (Cook & Glass, 2015). Therefore, it will be valuable to examine the potential factors (e.g., the firm’s performance, the industry fluctuations, the firm’s CEO turnover, etc.) that might lead to the decision to appoint a woman executive for the first time, despite strong resistance from members of the executive team (that is, to explore the antecedents of FAWE).

Third, a firm’s first appointment of a woman executive can be considered to be part of a radical organizational change in the firm, from the following two perspectives: (1) it targets gender, which has historically been discussed in terms of inequality and disparity (Mun & Jung, 2018), and (2) it causes a significant change in the perception of the firm’s strategic decision-making body, the executive team (Hambrick & Mason, 1984). However, existing studies have ignored the perspective that a firm’s first appointment of a woman executive is one of the most critical examples there is of “organizational change.”

Therefore, drawing on a theoretical frame incorporating the think crisis–think female (TCTF) perspective into the punctuated equilibrium model (PEM), in this study, we attempt to clarify the factors behind firms’ first appointments of women to their executive teams. Firstly, the PEM assumes that firms move into a transformation period when the executive teams decide that a deep structural change is necessary due to various factors that make it impossible to maintain a state of equilibrium (Gersick, 1991; Tushman & Romanelli, 1985). Particularly, PEM scholars have argued that three factors lead to radical change: (1) firm performance, (2) environmental change, and (3) the appointment of a new CEO (Romanelli & Tushman, 1994; Tushman & Romanelli, 1985). Secondly, the TCTF argument posits that “in times of crisis people may think female” (Ryan et al., 2011, p. 470), implying that FAWE would be part of a transformational period. Specifically, it is expected that the likelihood of FAWE increases when firms move into a period of deep structural change (i.e., radical change) due to poor firm performance or the appointment of a new CEO. Therefore, combining the two theories above, we assume that FAWE is more likely to occur in three situations: declining firm performance, environmental fluctuations, and the appointment of a new CEO (i.e., when a firm is in need of radical change).

We analyze our hypotheses regarding the above three antecedents— firm performance (i.e., return on assets [ROA] and aspirational performance), environmental changes (i.e., industry dynamism, industry munificence, and industry complexity), and appointment of a new CEO—using 20 years of panel data from publicly traded Japanese firms. Compared with other OECD countries, Japan has an overwhelmingly low rate of women as executives, and, in most Japanese firms, men still dominate the executive teams (OECD, 2017, 2023). Therefore, FAWE in Japan is relatively easily recognized as a radical change, making Japan the optimal context for examining the model in this study.

We expect our study to make several contributions. First, one of the most important contributions of this study is the use of a combined theoretical model of PEM and TCTF to clarify the mechanisms of FAWE. The existing theories applied to the composition of the executive team have been useful in explaining the complexity of the executive team. For example, the law of requisite variety (Conant & Ashby, 1970) and resource dependency theory (Pfeffer & Salancik, 1978) have been used to explain the diversification of executive teams (Boone et al., 2004; Hillman et al., 2007). However, given that FAWE (1) is not a proxy of complexity in the composition of the executive team, and (2) is implemented in a way that breaks through strong homogenizing pressures (Boone et al., 2004), an adaptation of existing theories would be inappropriate. Based on the inadequacy of the theory used in the existing literature, in this study we attempt to elucidate the mechanism of FAWE using combined theoretical model of PEM (Tushman & Romanelli, 1985) and TCTF (Ryan & Haslam, 2007). Therefore, this research can make a contribution to the literature on the development of the new phenomenon of FAWE and the adaptation of PEM and TCTF knowledge to FAWE.

Second, unlike existing WiE studies that merely focus on the antecedents and outcomes of WiE (Gould et al., 2018; Post et al., 2022), we seek to uncover the mechanisms by which firms decide to hire women executives for the first time. By exploring an emerging phenomenon in the discussion of gender on executive teams, this study promises to provide the first and most important story that previous WiE studies have overlooked. At the same time, unlike studies that examined the antecedents of WiE assuming that women executives were already on the executive team, this study is expected to provide practical implications for firms that have not yet appointed women executives.

Third, this study has important managerial implications for firms and executive team members who are seeking to make their FAWE. Until now, career studies about women have provided practical implications only for women who wish to break through the glass ceiling (Glass & Cook, 2016) and have failed to provide sufficient practical implications for firms and their executive teams regarding actual appointments of women to executive positions. Firms that plan to conduct a FAWE may benefit from knowledge about the conditions that increase the likelihood of such an appointment. This study clarifies the circumstances under which the likelihood of FAWE increases, and thus provides firms with useful suggestions regarding specific actions to take if they are planning to appoint their first woman executive.

Theory and Hypotheses

Prior studies have widely tackled issues concerning teams with women executives and their influences, such as the effects that having women in executive positions exert on firms’ internal structures, strategies, and performance. For example, studies have reported a trickle-down effect in which the presence of WiE increases the proportion of women in lower positions (Ali et al., 2021; Gould et al., 2018). Also, many empirical studies have tested the effects of WiE on firm performance (e.g., Jeong & Harrison, 2017; Post & Byron, 2015). One of the most recent studies demonstrated that when a firm has women executives, that fact leads to changes in the firm’s strategies, because having women in their executive teams causes firms’ strategic decision-making to become change-oriented and reduces their risk-seeking (Post et al., 2022).

As already noted, most previous studies addressed just the effects of WiE, and only a few have attempted to identify its antecedents. The good news, however, is that although there has been little research, meaningful implications have been provided. For example, one study compared the human capital profiles of men and women newly appointed to boards and found that women were more internationally diverse than men and held MBA degrees (Singh et al., 2008). Another study examines the factors influencing women’s representation on boards of directors based on resource dependency theory (Hillman et al., 2007). The results confirmed that firm size, industry nature (i.e., industries with greater women employment bases), and firm network (i.e., number of links to other firms with women on their boards of directors) are positively related to the representation of women on boards of directors. In addition, a study has found that an increased presence of women on nomination committees is positively related to the level of gender diversity on the board (Kaczmarek et al., 2012).

Although previous studies have offered a few clues about WiE nominations, no research has clarified yet why and when firms implement their FAWE. As OECD statistics show, even among countries with advanced levels of WiE nominations, nowhere do women comprise the majority of executives (OECD, 2023). In other words, there are still many firms in which men dominate the executive teams, and in that light, FAWE remains an important issue for a multitude of firms. It is also possible to offer a new viewpoint on the existing academic discourses that tend to explain the phenomenon of women being promoted to executive team positions for the first time in terms of the glass ceiling or glass cliff (Cook & Glass, 2014; Ryan et al., 2016), by viewing it as a part of the strategic actions taken by firms. Therefore, by identifying specific predictors of firms’ first appointments of women executives, this study attempts to clarify when and why firms do so.

To do that, we needed a new theoretical explanation that was different from the theories applied in prior studies on WiE and TMT/board diversity (Boone et al., 2004; Hillman et al., 2007). Existing theories such as the resource dependency approach (Pfeffer & Salancik, 1978) and law of requisite variety (Conant & Ashby, 1970) were effective means to explain the complexity of composition in executive teams (i.e., TMT and board gender diversity). However, it is difficult to apply them to FAWE by firms. This is because FAWE is not a phenomenon relating to the complexity of executive teams, and because FAWE is implemented in a way that breaks through the strong inertia imposed by the desire for homogenization (Boone et al., 2004). Based on the above, as we will explain in the next section, we needed a new theoretical approach because the background logic of firms’ FAWE differs from general situations of WiE and TMT/board diversity.

FAWE as a Part of the Transformational Period

Drawing on a combined theoretical model of PEM and TCTF, we consider a firm’s first appointment of a woman to an executive position as part of its transformational period (Ryan et al., 2011; Ryan & Haslam, 2007), and we examined the impacts on FAWE of three factors that have been identified as leading to a transformational period—firm performance, environmental changes, and executive leadership (Romanelli & Tushman, 1994; Tushman & Romanelli, 1985).

In the PEM literature, organizational change is referred to as a “difference in form, quality, or state over time in an organizational entity” (Van De Ven & Poole, 1995, p. 512). The literature on PEM attempts to explain organizational change in terms of three components (Gersick, 1991; Tushman & Romanelli, 1985). The first is deep structure (described as strategic orientations by Tushman & Romanelli [1985]). This deep structure is the core of an organization, and “it can be described by the set of organization activities: (1) core beliefs and values regarding the organization, its employees and its environment; (2) products, markets, technology and competitive timing; (3) the distribution of power; (4) the organization’s structure; and (5) the nature, type and pervasiveness of control systems” (Tushman & Romanelli, 1985, p. 176). PEM scholars assume that in order for an organization to achieve high effectiveness and high performance, it is important to ensure alignment within and among the components of each deep structure (Siggelkow, 2002; Tushman & Romanelli, 1985).

The second important component of PEM, the equilibrium period, is a period in which the effectiveness and efficiency of the organization are improved by developing the alignment of this deep structure (Tushman & Romanelli, 1985). Therefore, the organization is expected to move strongly in the direction of convergence, and since the purpose of this convergence is to improve the alignment of the existing deep structure, the changes that occur are neither radical nor discontinuous; they are so-called incremental changes (Silva & Hirschheim, 2007; Tushman & Romanelli, 1985). However, an organization’s effectiveness (or performance) is reduced if it cannot ensure sufficient alignment within its deep structure or cannot respond to changing requirements based on external environmental changes (Tushman & Romanelli, 1985). In such a case, there will be two conflicting forces in the organization: inertia tending to strengthen the alignment of the deep structure and a desire for high performance by destroying the existing deep structure and establishing a new deep structure (Tushman & Romanelli, 1985).

When the decision is made by the executive leadership to establish a new deep structure, the organization moves from an equilibrium period to a transformation period (Silva & Hirschheim, 2007; Tushman & Romanelli, 1985). The purpose of this period of change is to destroy the existing deep structure and build a new one (Tushman & Romanelli, 1985). In other words, the organization attempts to adapt to the environment in a new way through a radical reform of its deep structure, or so-called radical change (Tushman & Romanelli, 1985).

TCTF is an argument developed mainly in the literature on glass cliffs (Ryan et al., 2011; Ryan & Haslam, 2005). Studies dealing with women’s careers point to a strong association between stereotypes of managers and men (i.e., “think manager – think male”; Schein, 1973). It has been pointed out that the “think manager - think male” phenomenon puts women at a disadvantage, making it difficult for them to grasp career opportunities. However, Ryan and her colleagues noted that when firms are in crisis, this strong tie weakens and the unfairly unfavorable evaluation of female candidates changes (Ryan et al., 2011; Ryan & Haslam, 2005). Specifically, the key characteristics of effective crisis-responsive leadership include “the ability of the leader to work towards agreement, underscore the need to get efforts and contributions from others, create commitment, provide help, motive followers, [and] promote cooperation” (Gartzia et al., 2012, p. 606), which have been shown to be consistent with stereotypes of women (i.e., TCTF). Indeed, supporting the assumption of TCTF, prior studies have reported that during crises such as poor firm performance, feminine traits are preferred and women are selected as leaders (Bruckmüller & Branscombe, 2010; Ryan et al., 2011).

We found this PEM and TCTF argument useful in explaining FAWE. An executive team dominated by men can be interpreted as representing part of the deep structure (e.g., the distribution of power; Tushman & Romanelli, 1985). The continued nomination of male candidates to the executive team in order to maintain homogeneity can also be understood as convergence that takes place during the equilibrium period. However, as the PEM literature points out, if the organization’s effectiveness is reduced due to a lack of alignment of the deep structure or changes in the environment (Tushman & Romanelli, 1985), the executive team may make the decision to move from an equilibrium period to a transformation period. PEM scholars consider radical change in a transformation period to be change that destroys the existing deep structure. Therefore, the executive team, which has been monopolized by men, is also subject to reform. According to the TCTF literature, when firms are attempting to make executive team changes in a crisis, evaluations of female candidates change and are more favorable toward female candidates than under usual situations. Therefore, female candidates are expected to be more likely to be nominated for executive positions during a crisis than during usual situations. Thus, the combination of the PEM and the TCTF perspective can explain FAWE when a firm is in crisis.

Hypotheses Development

On the basis of the punctuated equilibrium literature (Romanelli & Tushman, 1994; Tushman & Romanelli, 1985), we posit that three factors, (1) firm performance, (2) environmental change, and (3) executive leadership, will lead to FAWE, which is a radical change for an organization.

Firm Performance

Firm performance is one of the most popular measurements of business activity success (e.g., Schimmer & Brauer, 2012). In the PEM literature, firm performance is a direct indicator of a firm’s political and economic success (Tushman & Romanelli, 1985). In the case of high performance, the organization’s deep structure can be assumed to be functioning. However, in the case of low performance, the organization’s deep structure is deemed to be dysfunctional and more likely to move from an equilibrium period to a transformation period (Gersick, 1991; Tushman & Romanelli, 1985). Therefore, it is valid to assume that firm performance is an important factor indicating a sense of urgency that an organization needs to implement radical change, and that firms with sustained poor performance are more likely to implement radical change (Romanelli & Tushman, 1994). According to the PEM literature, when radical change is required, firms often begin by restructuring their executive teams, such as appointing new boards from outside the firm, before implementing new strategies or making new investments (Gersick, 1991; Tushman et al., 1986). This is because a new executive team with different skills and fresh perspectives is “a powerful tool in managing frame-breaking change” (Tushman et al., 1986, p. 42).

We assume that firms, especially those with male-dominated executive teams, may restructure their executive teams by appointing (for the first time) women executives (Ryan et al., 2011; Ryan & Haslam, 2007). Based on the above TCTF argument, when a firm faces a crisis situation, the evaluation of female candidates, who under usual circumstances are disadvantaged by strong stereotypical ties between men and managers, changes, and women are more likely to be evaluated favorably in opportunities for promotion to executive team positions. Thus, in such a crisis situation, it is expected that the appointment of women to management positions will increase, especially in firms with executive teams dominated by men; this could be an opportunity to appoint women to executive positions for the first time.

To summarize the above discussion, we assume firms under pressure to make radical change due to sustained declining firm performance to have an increased likelihood of implementing FAWE, which represents a difference from firms’ traditional customs for nominating executives. On this basis, we propose the following:

Objective firm performance is negatively related to the likelihood of a firm’s first appointment of a woman executive.

Firm performance can be captured not only by objective indicators, but also by subjective indicators (Singh et al., 2016). In particular, since the PEM literature emphasizes the perceptions of senior management in the transition from an equilibrium period to a transformation period (Tushman & Romanelli, 1985), it is important to understand how the executive team evaluates firm performance.

According to performance feedback theory (Greve, 2003b), when evaluating their performance, executive teams have an aspiration level that serves as a reference point for evaluating whether their performance is a success or failure (Xu et al., 2019). Generally, when firm performance is above the aspiration level, the executive team evaluates the firm’s performance as a success and conducts a slack search, which is action to maintain competitive advantage over the medium to long term (Xu et al., 2019). On the other hand, when firm performance is below the aspiration level, the executive team evaluates firm performance as a failure and conducts a problemistic search to improve performance (Greve, 2003a). When setting aspiration level, executive teams primarily refer to their own past performance (historical aspiration) and the performance of their peers (social aspiration) (Shinkle, 2012).

When firm performance is above the aspiration level, firms are expected to maintain the status quo. Therefore, it is expected that the transition from equilibrium periods to transformational periods in the PEM literature will not take place and that male-only executive teams will continue to nominate men for executive positions by existing executive management nomination practices. On the other hand, when firm performance falls below the aspiration level, the executive team evaluates past activities as a failure and initiates a problemistic search to overcome the crisis. This can be interpreted as a transition from equilibrium periods to transformational periods in the PEM literature. During a transformation period, the executive team attempts to break with existing practices by appointing new executives (Gersick, 1991; Tushman et al., 1986). In that case, based on the TCTF above, the evaluation of women candidates will change and it will be more likely that women candidates will be nominated for new executive team positions. Based on the above discussion, we expect that firms whose firm performance falls below their aspiration level will be more likely to implement FAWE the following year than firms whose performance is above their aspiration level. Therefore, we set up the following hypothesis:

Subjective firm performance is negatively related to the likelihood of a firm’s first appointment of a woman executive.

Environmental Changes

External environmental factors should also be considered as drivers for radical change in a firm. This is because even if the alignment of the firm’s internal deep structure is established, if the firm is unable to respond appropriately to new environmental demands arising from environmental change, its effectiveness will decrease (Tushman & Romanelli, 1985). Pearson and Mitroff (1993) also point out that firms face crises not only due to firm performance but also due to changes in the external environment. Specifically, changes in the external environment, such as technological, legal, and institutional, have been discussed as potentially having a significant impact on organizational change (Greenwood & Hinings, 1996; Park, 2007).

Empirical studies that consider the external environment often use the three dimensions of the task environment presented by Dess and Beard (1984): dynamism, munificence, and complexity. Industry dynamism, which is defined as “the extent to which a firm faces an environment that is predictable and stable or changing and uncertain” (Datta et al., 2005, p. 138), has typically been used to express the magnitude of turbulence within an industry (Dess & Beard, 1984). These uncertainties suggest to the organization that its deep structure may not be compatible with its environment in the near future, forcing the organization to deal with uncertainty (Tushman & Romanelli, 1985). The uncertainty and turbulence represented by industrial dynamism is one of the main components of the perception of crisis (Ghobadian et al., 2022; Herrnann, 1963). Thus, when industry dynamism is high, firms are more likely to perceive a crisis. Firms faced with a crisis make radical changes that involve deep structural changes. As discussed above, according to existing PEM studies, radical change in a firm begins with a reorganization of the executive team (Gersick, 1991; Tushman et al., 1986). At that time, based on the TCTF argument, it is assumed that women candidates are more likely to be appointed as executive members in crisis situations. In particular, it would increase the likelihood that firms with previously men-dominated executive teams would appoint women executives for the first time (Ryan & Haslam, 2005). Therefore, we expect the following:

Industry dynamism is positively related to the likelihood of first appointments of women executives.

We also consider industry munificence to be related to the likelihood of FAWE. Industry munificence refers to “the extent to which the environment can support sustained growth” (Nielsen & Nielsen, 2013, p. 376). Generally, it represents an abundance of resources and opportunities in an industry (Chen et al., 2017; Luciano et al., 2020) and implies lower taxes, governmental incentives, fast growth markets, and so on (DeCarolis & Deeds, 1999; Rueda-Manzanares et al., 2008). When the level of industry munificence is high, firms may benefit without adopting unconventional strategies. In this case, the firm will not radically transform its deep structure. However, in industries with a low degree of industry munificence, resources and opportunities are scarce, and competition for firms to gain profits will be intense (Andrevski et al., 2014). In this case, firms are placed in a crisis where conventional strategies do not work, and firms are more likely to implement radical transformations to adapt to the environment. A typical response of firms during this crisis is to change top managers (Gersick, 1991; Tushman et al., 1986). Based on the TCTF argument above, it is assumed that the evaluation of female candidates will be more positive than in normal situations, increasing the likelihood of FAWE. Therefore, we predict that the likelihood of FAWE increases when the degree of industry munificence is low.

Industry munificence is negatively related to the likelihood of firms’ first appointments of women executives.

The final industry characteristic under consideration is the complexity of the industry. Industry complexity is characterized by “the diversity and breadth of an organization’s activities” (Child, 1972, p. 3), which reflects the intensity of the competitive environment (Luciano et al., 2020). A highly complex industry features many firms competing with no dominant companies maintaining strong leadership positions. Consequently, industries with higher levels of complexity are typically more competitive, with firms adopting short-term orientations and being more susceptible to crises compared to those in less complex industries (Chen et al., 2017). In such complex industries, firms and their decision-makers are compelled to innovate in order to secure their position within the environment (Luciano et al., 2020). Drawing on the above discussion, it is posited that firms in more complex environments are more inclined to undertake radical changes in response to crises. Thus, according to the TCTF rationale, it is expected that women will be more frequently appointed to executive positions for the first time in more complex environments compared to those in less complex environments. Therefore, we put forward Hypothesis 2c.

Industry complexity is positively related to the likelihood of firms’ first appointments of women executive.

Executive Leadership

While the above two factors (i.e., firm performance and environmental changes) increase the likelihood that a firm will move from an equilibrium period to a transformation period, they do not automatically cause this (Tushman & Romanelli, 1985). In the PEM literature, executive leadership is a crucial factor.

The perception of the executive team, especially the CEO, plays an important role in determining whether to keep the firm in an equilibrium period or transition to a transformation period (Tushman & Romanelli, 1985). This is because if the executive team does not make the decision to change, the organization will remain in an equilibrium period (Tushman & Romanelli, 1985). However, the literature shows that an incumbent CEO tends to be committed to the existing strategy because he or she shaped the firm’s previous decisions (Karaevli & Zajac, 2013; Tushman & Romanelli, 1985). In such a case, it would be difficult to move from an equilibrium period to a transformation period. On the other hand, if the CEO is newly appointed, he or she will be less committed to the existing strategy (Miller, 1993), and less hesitant to transform the deep structure. CEO succession literature points out that CEOs are likely to change during a crisis (Castrogiovanni et al., 1992). Therefore, new CEOs often replace other executive teams (Georgakakis & Buyl, 2020; Ma & Seidl, 2018). In such cases, following the logic of TCTF, women are more likely to be appointed to executive teams. Therefore, it is assumed that a new CEO who decides to change the deep structure will be more likely to implement FAWE in order to change the other components of the deep structure, as described above.

The appointment of a new CEO is positively related to the likelihood of the firm’s first appointment of a woman executive.

Methods

Sample

To examine what drives firms to enact their first appointment of a woman executive, we used cases of FAWE in Japanese listed firms (in a nonfinancial industry) as our sample. In Japanese firms, the management level, including that of executive teams, is dominated by men. The prominent gender role gap in managerial positions in Japan stems from the characteristics of patriarchal Japanese society, as well as from the work-related values and legal systems established by that patriarchy (Kato & Kodama, 2018). An example of this is the clear distinction between gender roles in Japan, which is strongly reflected in the characteristics of Japan’s human resources management systems. Gender-based role distinctions (marriage, childbirth, etc.) make it difficult for women to carry on working at the firm and continue their careers (Mun & Jung, 2018). The ratio of women in management positions thus remains low in Japan and the ratio of WiE, in particular, is extremely low. In fact, according to OECD statistics (OECD, 2023), the ratio of women on boards of directors in Japan (12.6% in 2021) is less than half the OECD average (28.0% in 2021).

The ratio of women in executive positions in firms in Japan has been improving in recent years, and the government is focusing on policies to support this growth of WiE (Gender Equality Bureau Cabinet Office, 2020). Nevertheless, it is indisputable that executive teams in Japan remain dominated by men, and in comparison with other countries, the implementation of FAWE in an extremely homogeneous society such as Japan’s is more likely to be recognized as a discontinuous change for firms. Therefore, Japan provides an ideal context for examining FAWE from the PEM perspective.

Western firms tend to make a clear distinction between TMTs, who make strategic decisions, and the board of directors, who monitor the firm (Denis & McConnell, 2003). In Japan, however, few firms have a clearly independent TMT and board of directors, and in many, TMT members also serve as directors (Yoshikawa et al., 2007, 2020). Considering the uniqueness of corporate governance in Japan, in this study we focus on executive teams whose members serve as both TMTs and board members. This executive team also differs from the supra-TMT (Finkelstein & Hambrick, 1996) because it serves both the TMT role and the board role. Typical positions are syacho (president), fuku syacho (vice president), sennmu (senior managing director), jyomu (managing director), and torishimariyaku (board director). We used data on executive teams from Yakuin Shikiho, 2 a database provided by Toyo Keizai Inc., which collects information on executive teams, primarily those of publicly traded Japanese firms, and is frequently utilized in research on executive teams in Japan (e.g., Mun & Jung, 2018; Tanikawa & Jung, 2016, 2019). For data on firms, we took data recorded by Nikkei NEEDS, a database that is also widely used in empirical research on Japanese firms (e.g., Nakauchi & Wiersema, 2015; Xu & Zeng, 2021). Using these databases, we constructed panel data for the 20-year period from 2000 to 2019.

Variables

Dependent Variable: Firms’ First Appointment of a Woman to an Executive Position

Referring to the Yakuin Shikiho data, FAWE, our outcome variable, was operationalized as a dummy variable. Specifically, given a base year t, we assigned a value of 1 to cases in which the executive team had been composed entirely of men 1 year earlier (t – 1) but included women in the base year t, and we assigned 0 to all other cases. Additionally, we used the value of FAWE 1 year after the base year (t + 1) as the dependent variable because of the effect of reverse causality between the independent variables and FAWE and because the PEM assumes that radical transformation occurs in a relatively short period of time (Romanelli & Tushman, 1994).

Independent Variables

Following existing research (Romanelli & Tushman, 1994; Tushman & Romanelli, 1985) that adopted the PEM, we adopted three factors that prompt firms to make radical changes—firm performance, environmental changes, and newly appointed CEOs—as independent variables.

First, we used ROA as our measure for objective firm performance. Return on assets is the variable most frequently used to indicate firm performance (Singh et al., 2018). The ROA data we used were collected using Nikkei NEEDS, their value obtained by dividing a firm’s profit by its total capital in the base year t. Because ROA is more easily affected by annual outliers than the other variables used in this study, in accordance with existing studies (Cannella et al., 2008), we used the average ROA for the base year t and the previous 2 years (i.e., we averaged the ROAs for t, t – 1, and t – 2).

In this study, we employed aspirational performance as subjective firm performance, which is often used in previous studies as a perception of executive team performance (Greve, 1998). Several ways have been used in the literature to measure aspirational performance (Bromiley & Harris, 2014; Xu et al., 2019). In this study we adopted measures by Xu et al. (2019). Following previous studies based on behavioral theory of the firm (Greve, 1998; 2003b), Xu et al. (2019) identify aspirational performance as historical aspirational performance and social aspirational performance. Historical performance is based on comparisons with the firm’s own past performance, and social performance is based on comparisons with firms in the same industry (Xu et al., 2019). Following Xu et al. (2019), we used ROA and a spline function to distinguish between performance below and above aspirations. Regarding historical aspirational performance, when a firm’s ROA in base year t is lower than that of the previous year (i.e., t – 1), it was recorded as indicating below historical aspiration. When this was the case, we used the value of the ROA of the previous year (t –1) minus that of base year t, and assigned a value of 0 to all other firms. In addition, when a firm’s ROA in base year t exceeded that of the previous year (t – 1), it was recorded as indicating above historical aspiration. In this case, we used the value of the ROA of base year t minus that of the previous year (t – 1), and assigned 0 to all other firms. From the above operationalization, if below historical aspiration has a positive relationship with FAWE in the following year, it means that historical aspiration and FAWE are negatively related. For social aspirational performance, when a firm’s ROA was below the industry average, it was recorded as indicating below social aspiration, and we used the value of industry average ROA minus the firm’s ROA. We assigned 0 for firms whose ROA exceeded the industry average. Conversely, firms whose ROA exceeded the industry average we recorded as being above social aspiration, and used the value of the ROA of the firm minus the industry average ROA and assigned 0 otherwise. Similar to historical aspiration, above, if below social aspiration has a positive relationship with FAWE in the following year, it means that social aspiration and FAWE have a negative relationship.

We manipulated industry dynamism and munificence using sales over the previous 5 years, including the base year t (t – 4 to t) (Dess & Beard, 1984; Nielsen & Nielsen, 2013). Specifically, in accordance with Nielsen and Nielsen (2013), we operationalized industry dynamism, measured by dividing the standard error of the slope coefficient by the mean value of sales for each industry. In addition, industry munificence was calculated as the rate of growth (the regression coefficient of year on annual average sales for each industry) divided by the mean value of sales for the previous 5 years (Nielsen & Nielsen, 2013). In operationalizing industry complexity, we employed the four-firm concentration ratio (CR4) as a measure of industry concentration, which serves as a proxy for industry complexity (Chen et al., 2017). To this end, we first identified the leading four firms based on sales in each industry for the base year t. Subsequently, we calculated the CR4 as the ratio of the combined sales of these top four firms to the total sales of the industry. It is important to note that, within this framework, a lower CR4 value signifies greater industry complexity.

We manipulated having a newly appointed CEO as a dummy variable using data from Yakuin Shikiho. Specifically, in base year t, if the CEO had changed from the previous year (t −1), this value was set to 1; if not, it was set to 0.

Controls

We adopted as control variables several variables that could affect FAWE, starting with the firm-related variables of firm size and firm age. In general, firm size is closely related to a firm’s internal complexity and bureaucracy; thus, we expected that the appointment of executives would be constrained by past decisions (Chen & Hambrick, 1995). Similarly, firm age has a significant impact on a firm’s internal culture and customs (Li et al., 2020). In particular, newer firms are expected to have different internal cultures and customs from older firms, making firm age an important control variable. We used the logarithmic value of the number of employees in the base year t for firm size. For firm age, we used the number of years from the year of the firm’s founding to base year t.

In addition to the CEO, executive team members are also involved in the nomination of new executive team members (Withers et al., 2012), so the characteristics of existing executive team members are also important control variables. For instance, executive team size is an important control variable, because large executive teams can take time to reach consensus and can hinder decisions that do not align with existing practices (e.g., FAWE; Goodstein et al., 1994). We measured executive team size by the number of executive team members in base year t.

Executive team average age and executive team average tenure are also important factors. The average age of the executive team represents its average generational values; generally, executive teams with a high average age are considered to have more conservative values (Muth & Donaldson, 1998). Therefore, we expected that relatively young executive team members would be more likely than older ones to make decisions that differed from previous nomination patterns. Additionally, existing studies have noted that young-tenured executive teams are more likely to make strategic changes than more senior-tenured executive teams (Richard et al., 2019; Wiersema & Bantel, 1992). Therefore, we believed it likely that young-tenured executive teams would be more likely to perform radical changes such as FAWE than their older counterparts. In this study, we calculated the average age and the average tenure of executive teams in base year t and included them in the model. For the average tenure of the executive team, logarithmic values were used. In addition, the turnover of executive team members is another important control variable. This is because new executive team members are often appointed to fill vacancies (Hermalin & Weisbach, 1988; Withers et al., 2012). Therefore, when the number of executive team departures is high, the likelihood of FAWE in the following year is expected to increase. We operationalize executive team turnover as the number of executive departures in the base year t.

Not only is a firm’s first appointment of a woman to an executive position greatly influenced by the characteristics of the existing executive team and the firm, it is also influenced by factors outside the firm. For example, the industry to which a firm belongs is an important control variable. In our case, we anticipated that customs regarding the nomination of women to executive teams, and also the number of women who were candidates for such a nomination, would differ between industries employing high numbers of women, including in nonmanagerial positions (e.g., the service industry), and industries in which fewer women are employed (e.g., the construction industry). Therefore, we included an industry dummy in our analytical model, with each dummy variable being included in the analysis model with reference to the Nikkei NEEDS industry classifications, which we used to collect the firm-related data.

Moreover, although the number of women in executive positions has been extremely limited in Japan to date (OECD, 2023), it has been increasing at a more rapid pace in recent years. Therefore, to examine the precise effects of the independent variables in this study, it was necessary to eliminate the year effects. Accordingly, we created dummy variables for each year used in the analysis and included them in the analytical model.

Analytical Methods

The samples used in the analysis of this study were panel data with a 20-year span (2000–2019). An ordinary least squares (OLS) regression analysis was therefore not suitable, because previous studies have indicated that OLS “does not account for dependence among multiple observations from the same firm and thus may not provide consistent coefficient estimates” (Mun & Jung, 2018, p. 424). Additionally, we manipulated FAWE as a dummy variable, so with the distribution of the outcome variable in mind, it was not desirable to use the usual OLS regression analysis.

Consequently, we tested the hypotheses using a panel logistic regression analysis. Specifically, we used a Stata (version 18.0) xtlogit command. Analysis was performed using all of the control variables in this study (Model 1 of Table 2). Next, we included all of the variables (Model 2 of Table 2).

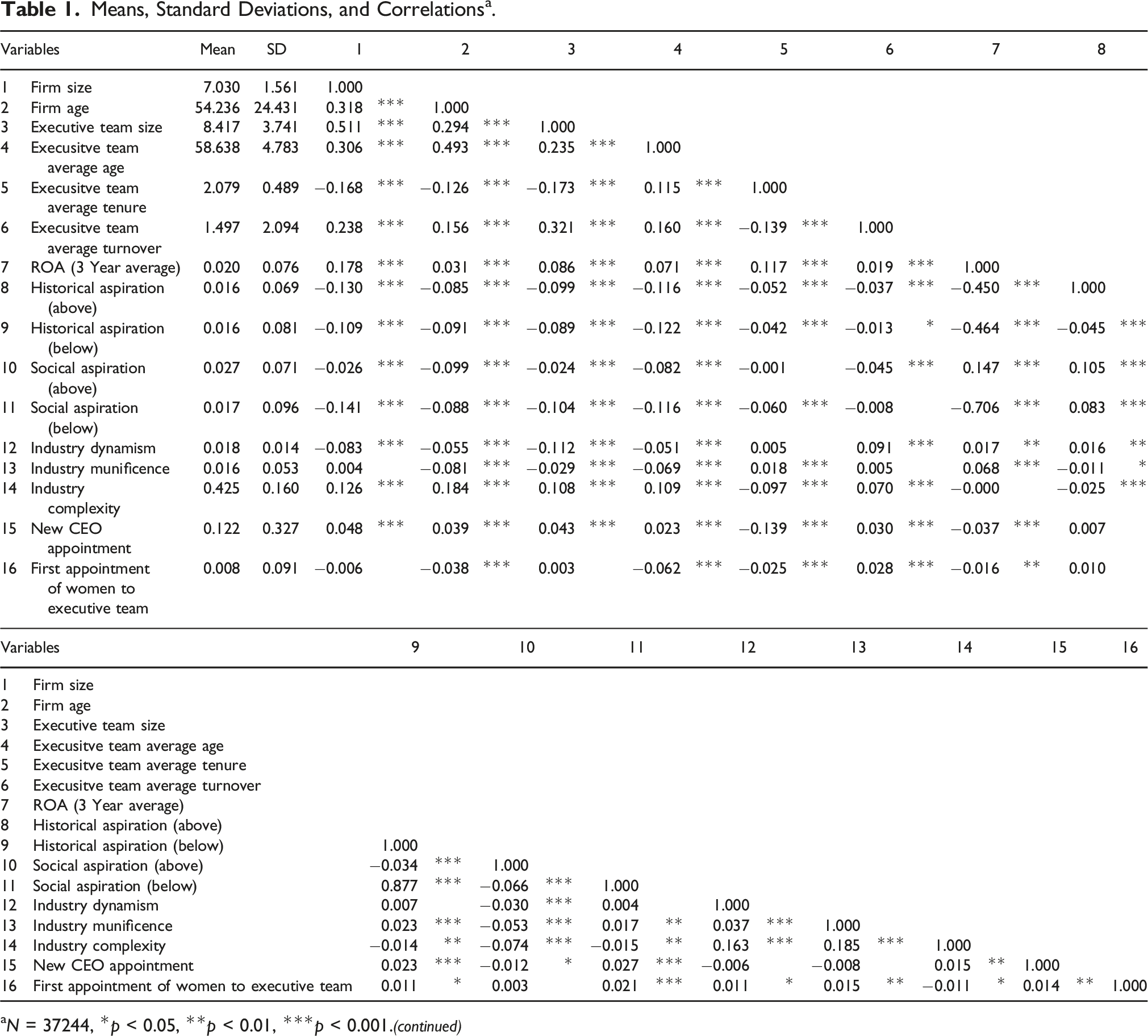

Means, Standard Deviations, and Correlations a .

aN = 37244, *p < 0.05, **p < 0.01, ***p < 0.001.

Results

Table 1 shows the means, standard deviations, and correlation coefficients of all the variables used in this study.

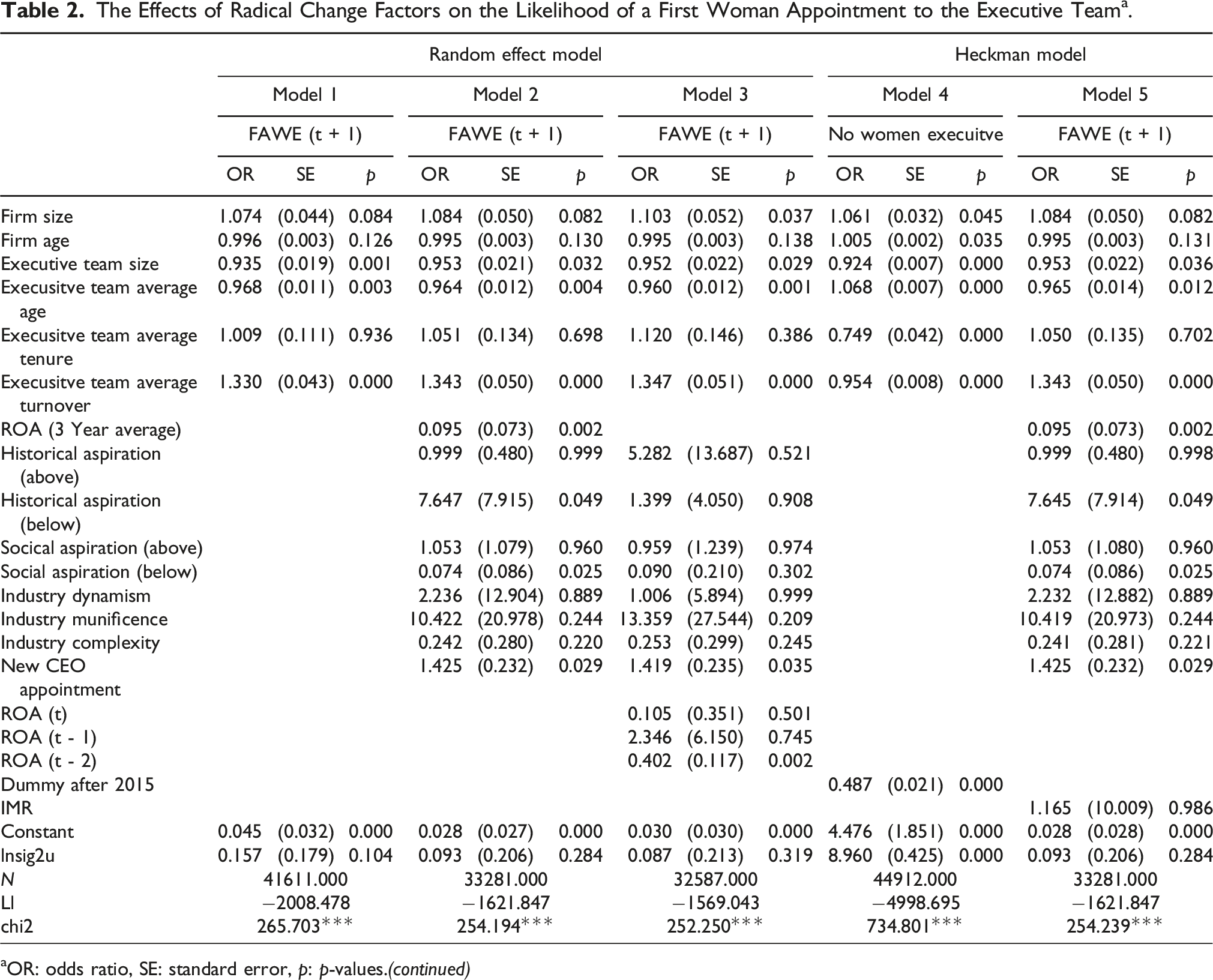

The Effects of Radical Change Factors on the Likelihood of a First Woman Appointment to the Executive Team a .

aOR: odds ratio, SE: standard error, p: p-values.

Hypothesis 1 examined the impact of firm performance on the likelihood of a firm making its first appointment of a woman executive. Specifically, Hypothesis 1a predicted that ROA would be negatively related to FAWE in the subsequent year and the expectation of Hypothesis 1b was that below aspirational performance would be positively related to FAWE in the subsequent year. The results of Model 2 in Table 2 confirm a significant relationship between ROA and the likelihood of FAWE in the following year (OR = 0.095, p = .002). This result means that Hypothesis 1a was supported. Regarding the impact of aspirational performance on FAWE, we found that below historical aspirational performance increases the likelihood of FAWE in the following year (OR = 7.647, p = .049). Regarding the relationship between social aspirational performance and FAWE, we confirmed a significant negative relationship between below social aspirational performance and FAWE (OR = 0.074, p = .025). These results mean that only Hypothesis 1b is partially supported.

Hypothesis 2 explored the impact of environmental changes on the likelihood of firms appointing women executives for the first time (FAWE), with specific predictions regarding industry dynamism (2a), industry munificence (2b), and industry complexity (2c). Hypothesis 2a anticipated a positive relationship with industry dynamism, 2b a negative relationship with industry munificence, and 2c a positive relationship with industry complexity regarding the likelihood of FAWE. However, the analysis of Model 2 revealed no significant relationship between industry dynamism (OR = 2.236, n.s.), industry munificence (OR = 10.422, n.s.), or industry complexity (OR = 0.242, n.s.) and the likelihood of FAWE, leading to the conclusion that Hypotheses 2a, 2b, and 2c were not supported.

Hypothesis 3 examined the relationship between a newly appointed CEO and firms’ likelihood of appointing their first woman to an executive position. Specifically, we predicted that new CEO appointments would have a positive impact on the likelihood of firms’ FAWE in the subsequent year. Looking at the data for Model 2, listed in Table 2, we found that a new CEO appointment significantly increased the likelihood of FAWE during the subsequent year (OR = 1.425, p = .029). Thus, when all independent variables are included in the analytical model, Hypothesis 3 was supported.

Additional Analyses

To confirm the robustness of the results of our study, we conducted additional analyses. These analyses include a panel logistic regression analysis using single-year ROA as an independent variable, addressing sample selection with a Heckman regression and handling omitted variable bias and endogeneity with instrumental variables estimation.

Based on the theoretical foundation of PEM, which assumes that sustained performance decline leads to radical organizational change (Romanelli & Tushman, 1994), in this study we operationalized ROA as a 3-year average. However, some existing studies include values for each year directly in the model when using multi-year organizational performance (e.g., Duru et al., 2016; Rayton, 2003). Therefore, we conducted an additional analysis, testing our hypotheses by including ROA for each of the 3 years (i.e., t, t − 1, and t − 2) independently.

As shown in Model 3 of Table 2, we found similarities with the results of the main analysis, above. First, concerning the relationship between ROA and FAWE, we could not confirm a significant relationship with FAWE for ROA at t (OR = 0.105, n.s.) and t − 1 (OR = 2.346, n.s.). For ROA at t − 2, on the other hand, we found a negative relationship with FAWE, as hypothesized in this study (OR = 0.402, p = .002).

Regarding other independent variables, for aspirational performance, both below historical aspiration (OR = 1.399, n.s.) and below social aspiration (OR = 0.090, n.s.) failed to confirm a significant relationship with FAWE. Similarly, we could not confirm a significant relationship between industrial dynamism (OR = 1.006, n.s.), industrial munificence (OR = 13.359, n.s.), and industrial complexity (OR = 0.253, n.s.). Conversely, we were able to confirm a significant positive relationship between new CEO appointment and FAWE, similar to the main analysis, above (OR = 1.419, p = .035). The finding that ROA in t−2 has a significant negative relationship with FAWE may be interpreted in terms of the objective performance characteristic of ROA and the research context of this study—the Japanese corporate governance system. ROA is an objective performance measure and it is difficult to determine whether the ROA for the year in question is a success or failure when compared to aspirational performance, which is a subjective measure. The stagnation of ROA is not a direct indication of a change in the power structure within the executive team, such as a change in CEO. Therefore, it may take more time for a weak ROA to be perceived as a crisis compared to other antecedent factors. Even if the ROA for the year in question is identified as a crisis, it may take some time before it manifests in the form of FAWE due to the nature of the executive team. In Japan in particular, the proportion of female executives during the sample period was extremely small. Therefore, the pool of candidates for female executives was insufficient, and it is expected to have taken time to select suitable candidates. It is also noted that Japanese firms, including their executive teams are relatively slow in term of decision-making (Jung et al., 2023; Ward et al., 1995; Yates & de Oliveira, 2016). This contextual situation can also be interpreted as the cause of the significant impact of only ROA in t−2.

Second, we addressed potential sample selection bias using the Heckman regression estimation, which is pivotal in adjusting for biases arising from our dependent variable, FAWE. Given that FAWE only occurs in firms lacking female executives in the prior year, firms with existing female executives were necessarily excluded from our sample. This condition could introduce sample selection bias, which we have now corrected for using the two-stage Heckman model.

In the first step of our Heckman estimation, we created a dummy variable for firms without female executives (i.e., firms without female executives = 1, other firms = 0) and used this as our dependent variable. This model also included a control variable pertinent to this study, impacting the selection mechanism. Notably, we omitted year dummies from our selection model but included a specific dummy for the post-2015 period. This inclusion is justified by significant regulatory and cultural shifts in Japan after 2015—notably, the enactment of the Act on the Promotion of Women’s Active Engagement in Professional Life and the adoption of the Corporate Governance Code by the Financial Services Agency and Tokyo Stock Exchange, both mandating diversity in executive roles (Japanese Law Translation, 2015; The Council of Experts Concerning the Corporate Governance Code, 2015).

These legislative and regulatory changes serve as a unique instrument in our selection model, influencing the likelihood of female executive appointments. Our findings, as presented in Table 2 (Models 4 and 5), indicate that the variables introduced since 2015 have had a significant and negative impact on the dummy variable for firms without female executives in our sample (OR = 0.487, p. < .000). In the second step, we incorporated the inverse Mills ratio (IMR) calculated from the first step, which further validated our results by adjusting for any residual selection bias. The value of the IMR was not significantly related to FAWE, indicating that sample selection did not have a significant impact on the results of this study (OR = 1.165, p = n.s.). However, even when including the IMR, there was no substantial change in the verification of our hypothesis.

First, regarding the relationship between firm performance and FAWE, a significant negative relationship was observed with past ROA (OR = 0.095, p = .002), below historical aspirational performance (OR = 7.645, p = .049), as well as a positive relationship with below social aspirational performance (OR = 0.074, p = .025). Additionally, a positive relationship between the appointment of a new CEO and FAWE was confirmed (OR = 1.425, p = .029). Finally, no significant relationships were observed for industry-related variables (industry dynamism: OR = 2.232, p = n.s., industry munificence: OR = 10.419, p = n.s., industry complexity: OR = 0.241, p = n.s.). These results replicate the findings of the main analysis, confirming the robustness of our study’s outcomes.

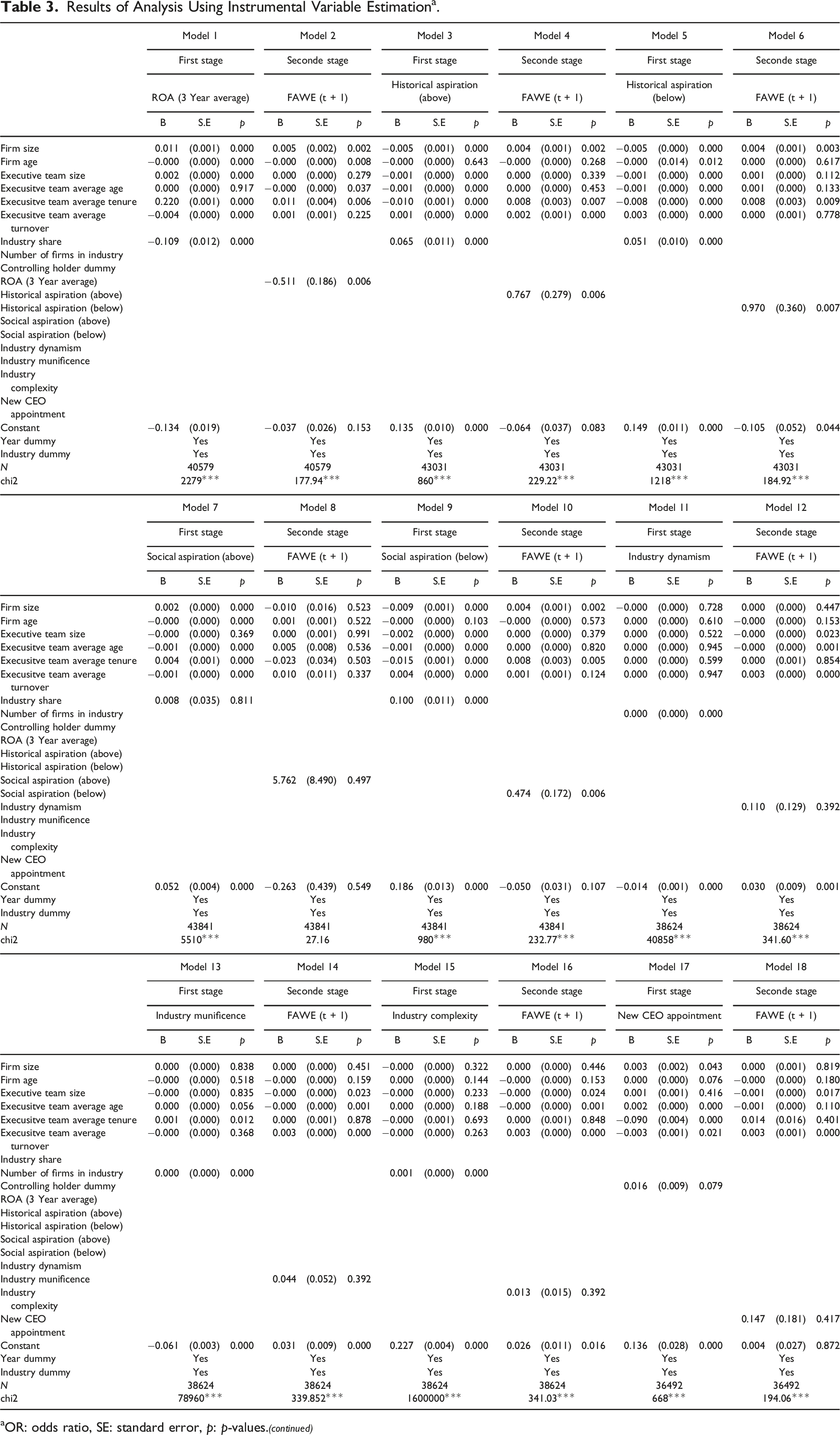

Second, we tested the hypotheses of this study using instrumental variables estimation. Our analytical model includes a total of eight independent variables (e.g., ROA, aspirational performance, environmental changes, and new CEO appointment). For instrumental variables, it is necessary to include original instrumental variables that are more than the number of potential endogenous variables (i.e., independent variables) not included in the regression model (Murray, 2006). Therefore, it is neither theoretically nor practically feasible to identify more than eight original instrumental variables. Hence, each independent variable was examined individually in this study.

We used three instrumental variables separately. First, for independent variables related to performance (i.e., ROA, historical aspirational performance, social aspirational performance), we used industry share (sales ratio within the same industry) as the instrumental variable. Industry share represents the power, favorable signals, and economic health of a company within an industry (Bhattacharya et al., 2022; Weiss, 1968). Research on industry share or market share suggests that a company’s share within an industry is positively related to profitability (Bhattacharya et al., 2022; Szymanski et al., 1993). Based on these points, it is reasonable to use industry share as an instrumental variable for our performance-related variables.

Industry share is a variable related to individual companies and is unlikely to directly affect industry-related variables. Therefore, for industry-related variables, we used the number of firms constituting the industry. The annual value of the number of firms in the industry was used. The number of firms constituting an industry significantly impacts the industry’s characteristics. For example, industries with few firms, such as infrastructure-related industries (e.g., gas and oil), are relatively stable due to consistent demand and significant government regulation. On the other hand, industries with many companies, such as the service industry, are unstable, with frequent changes in major leading companies. Thus, the number of firms in the industry can reasonably be used as a variable that directly influences the industry-based environmental characteristics (i.e., industry dynamism, industry munificence, and industry complexity).

Finally, for the appointment of a new CEO, we used variables related to corporate governance. Specifically, the existence of a controlling shareholder was used. According to Tokyo Stock Exchange (Tokyo Stock Exchange, 2020), the controlling shareholder is defined as the shareholder who owns more than 50% of the company’s shares. The CEO’s replacement is often determined by the parent company’s convenience, rather than the firm’s performance, with former executives from the parent company frequently being appointed as CEOs of related subsidiaries, especially in Japan (Wiersema et al., 2018). Therefore, the existence of a controlling shareholder is expected to significantly influence the appointment of a new CEO.

Moreover, these three variables are assumed not to be directly related to FAWE—the dependent variable of this study. For instance, industry share represents a company’s relative power within the industry, which is unlikely to directly influence the appointment of the first female executive. Similarly, the number of firms constituting the industry is reasonably assumed to influence FAWE through its impact on industry characteristics rather than directly affecting FAWE. Finally, the presence of a controlling shareholder is expected to influence FAWE through internal firm processes, such as CEO appointments, rather than directly impacting FAWE.

Results of Analysis Using Instrumental Variable Estimation a .

aOR: odds ratio, SE: standard error, p: p-values.

These results indicate that not all outcomes of our main analysis were replicated when using the Heckman regression model and instrumental variables estimation. However, many of our hypotheses were supported by the findings. Therefore, we conclude that the results of this study exhibit a certain level of robustness, even when using our additional analyses.

Discussion and Conclusions

The purpose of this study is to clarify the drivers for implementing a firm’s FAWE. Specifically, drawing on a theoretical frame incorporating the TCTF perspective (Ryan & Haslam, 2005) into the PEM (Tushman & Romanelli, 1985), we proposed and tested whether firm performance (as measured by ROA and aspirational performance), environmental changes (in the form of industry dynamism, industry munificence, and industry complexity), and the appointment of a new CEO would significantly predict a firm’s FAWE. Using panel data of publicly traded Japanese firms over the past 20 years, we clarified that, as predicted, ROA, aspirational performance, and having a newly appointed CEO were significantly related to firms’ FAWE in the subsequent year. However, we could not confirm a significant relationship between environmental changes and the likelihood of FAWE in the subsequent year.

This study theoretically extends the WiE literature from an exclusive focus on the glass ceiling or glass cliff perspective to the firm strategy perspective, and empirically provides a comprehensive understanding of WiE-related phenomena that begin before and continue after women join executive teams, and include their impact on firm performance.

Theoretical Implications

The findings of this study make three theoretical contributions. The first is the application of the punctuated equilibrium perspective to explain firms’ motivation to appoint women executives for the first time. Prior research has accounted for WiE nominations by using various theories, such as the law of requisite variety (Conant & Ashby, 1970) and resource dependency theory (Pfeffer & Salancik, 1978). Despite this abundance of theories, however, none could directly explain under which conditions a firm is more likely to implement their FAWE. To address that research question, we applied the PEM. Specifically, considering firms’ FAWE as part of a process of radical change, we proposed and examined whether firm performance, environmental changes, and new CEO appointments—the three factors that promote radical organizational change—were significantly related to the likelihood that a firm would make its first appointment of a woman to an executive position. The results suggest that explanations based on the PEM are effective in the case of firms’ appointments of women in executive positions, especially when they are the first such appointments. Therefore, this study has expanded the theoretical foundations provided in existing WiE research by offering a new and effective theoretical option (i.e., the PEM).

Second, by integrating PEM and TCTF, we have extended the discourse of existing research. In the first place, based on the theoretical model of PEM, it allowed us to theoretically postulate and empirically examine three causes of radical organizational change, namely, low firm performance, industry fluctuations, and the appointment of a new CEO. By doing so, we were able to extend existing TCTF studies that have focused solely on poor firm performance as a cause for the appointment of women executives (e.g., Cook & Glass, 2014; Ryan et al., 2011). Next, adding the TCTF perspective to PEM allowed for a more specific examination of radical organizational change. Specifically, although PEM research suggests that radical organizational change begins with executive team restructuring (Gersick, 1991; Tushman et al., 1986), it remains unclear as to how to restructure the executive team. From the perspective of the TCTF, this study empirically examined the theoretical assumption that when a firm is facing a crisis and radical change is required, the executive team restructuring involves the appointment of women as executives (especially the appointment of women executives for the first time). Therefore, by incorporating the TCTF perspective into the PEM, this study could provide suggestions on how executive team reorganization is specifically carried out.

Third, our findings suggest that firms’ internal and external factors can influence FAWE differently. Specifically, we found that firms’ internal factors, including firm performance and the appointment of a new CEO, were significantly related to the likelihood of firms making their first appointment of a woman to an executive position, whereas hypotheses on firms’ external factors (industry dynamism, industry munificence, and industry complexity) were not significantly related to the likelihood of FAWE. Tushman and Romanelli (1985) pointed out that environmental changes may be ignored until recognition is forced through performance declines that are caused by the lack of a deep structure-environment fit. Our findings support this theoretical assumption.

Practical Implications

This study also provides practical implications. Our results suggest specific actions for firms that want to hire their first woman executive. By using the PEM, we found that firms implement their FAWE under conditions in which radical change is encouraged. In particular, our results show that poor firm performance and having a newly appointed CEO increased the likelihood of firms deciding to nominate their first woman executive. As existing studies have already indicated, the appointment of a new CEO is an important event that influences firm strategy and internal structure (Schepker et al., 2017). Adding to those previous studies, the results of this study reveal that the appointment of a new CEO also had a significant impact on whether the firm hired a woman executive for the first time. Therefore, a new CEO and the members of the executive team who support the new CEO should understand that the best time for hiring a first woman executive is immediately after a new CEO takes office.

The findings of this study suggest that firms seeking to hire their first woman executive may consider poor performance as an opportunity to do so. The decision to appoint a woman executive member, however, would require a rationale-based explanation that would be acceptable to all relevant decision makers. Since the main purpose of this study is to identify antecedents of FAWE, we did not focus on its outcomes. Meanwhile, recent studies have indicated that it is precisely in times of poor performance that a recovery can be expected through the appointment of women executives, providing a rationale to convince those involved in hiring decisions. For example, Jeong and Harrison (2017) found in a meta-analysis that the appointment of women to upper management is positively correlated with long-term financial performance. Yanadori et al. (2021) provide more practical implications by revealing that narrowing the gender wage gap within the TMT may improve firm performance through the active promotion of women members to the TMT.

As revealed in this study, the executive team may need to collaborate with HR managers, in case FAWE becomes necessary due to a decline in firm performance or is made possible by the appointment of a new CEO. Specifically, in the case of a first attempt to appoint a woman to the board, given the gender balance gap in management positions, it is more advantageous to have a pool of women candidates in the internal labor market than to appoint from among women candidates in the external labor market (Ali et al., 2021; Bilimoria et al., 2008). Thus, the role of the HR department will be important in the process of attracting and recommending sufficient numbers of women candidates from within the firm. To achieve FAWE efficiently and effectively, it would be important for the executive team to constantly share with HR managers the qualification requirements that upper management envisions for women executives. For example, a frequent interface between management and HR managers and continuous monitoring of HR programs would be effective (Srimannarayana, 2010).

Limitations and Future Research

As with most research, this study has limitations. First, our results were dependent on the context in which the study was conducted. To examine the antecedent factors for firms’ FAWE, we used publicly traded Japanese firms, whose executive teams were, and remain for the most part, dominated by men (OECD, 2023). Thus, we confirmed more cases of FAWE by the firms in our study than would be the case among firms in countries in which women have already been appointed to executive teams in large numbers. Those countries would provide the optimal context for performing a quantitative examination, which by definition requires a large number of observations. However, because this is an empirical study targeting only one country, we could not eliminate the possibility that the results were influenced by contexts peculiar to Japan. In particular, FAWE was recognized as a radical change, with discussions conducted from the perspective of the PEM. However, in Japan, which has an enormous gender gap, many people may perceive FAWE as an especially radical change. Therefore, to examine the generalizability of the results of our study, we need to determine whether FAWE can be explained by factors that promote radical change in the context of other countries as well. In that light, future research that examines the models used in this study in countries with different degrees of gender role gaps, and that conducts comparative studies with Japan, may prove critical.

Relatedly, the sample collection period for this study was long (i.e., 20 years). Therefore, the sample of this study included firms that conducted the FAWE for the outcome variable more than once. We tested our hypotheses by including firms with multiple FAWEs based on the theoretical assumption that radical change can occur multiple times over 20 years. However, our hypotheses were not supported when we excluded firms that had performed FAWE multiple times. The result implies that firms that frequently implement FAWE do not implement FAWE as an organizational change. Therefore, it would be desirable that our hypotheses be tested in future to examine the generalizability of our findings, considering different countries, sample collection periods, number of FAWEs, etc.

The study’s second limitation is that we failed to identify significant effects of environmental changes (e.g., industry dynamism, industry munificence, and industry complexity) on FAWE. On the other hand, however, the non-significant relationship between environmental change and FAWE can also be interpreted as being due to the study’s research design. The likelihood of FAWE, a very rare phenomenon, was used as the outcome variable for this study. Therefore, to ensure a sufficient number of observations, we used a sample period of 20 years and multiple industries. For this reason, we used industry dynamism, industry munificence and industry complexity, which are proxies of general environmental change. In the PEM literature, however, environmental change is viewed as radical change in technology, institutions, and other aspects of the environment that disrupt the internal alignment of existing deep structures (Tushman & Romanelli, 1985). Therefore, if the impact of environmental change on FAWE is to be examined in strict accordance with the PEM literature, it is necessary that the impact on FAWE of legal or institutional change events in specific industries be examined. In fact, the results of our analysis did not allow us to test our hypotheses on environmental change due to the excessive variation in the coefficients of the independent variables for industry (i.e., industry dynamism, industry munificence and industry complexity). Therefore, we hope that future work will examine the impact on FAWE of radical environmental change events in specific industries.

Furthermore, the effects of other environmental factors could also be examined using different theoretical frameworks. For example, previous studies on institutional theory, and particularly institutional isomorphism, have noted that coercive, mimetic, and normative pressures affect various elements and activities of an organization (DiMaggio & Powell, 1983). Indeed, several studies addressing executive team composition have found impacts from factors outside the organization (Grosvold & Brammer, 2011; Upadhyay & Triana, 2021). Therefore, we encourage future researchers to include and examine other potential environmental factors.

Finally, limitations also exist regarding the estimation method of our model in this study. In this study, we operationalized FAWE as a dummy variable and estimated our model with a panel logistic regression analysis. However, there are concerns about using logistic regression analysis to estimate very rare events such as the one in this study (King & Zeng, 2001; Noguera et al., 2013). In this study, we used a Heckman regression and instrumental variables estimation to confirm the robustness of our main analytical results, ensuring the consistency of the findings. However, in order to make the findings more robust, it is desirable that in future, the hypotheses of this study be tested in a more multifaceted way by employing different estimation methods, research designs, and methodologies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by JSPS KAKENHI Grant Numbers 17H02564, 22KK0222, 23K20163, 23K20629.