Abstract

Third-party distribution channels or intermediaries have become ubiquitous across a wide range of industries, offering firms access to new prospects and an opportunity to expand their customer base. Although prior work has investigated the short-term aggregate demand implications of intermediaries, the long-term customer relationship perspective has remained unexplored. Using customer-level data from a large U.S. hotel brand, we show that customers acquired via travel intermediaries (such as online travel agents or OTAs) have persistently different behaviors on several dimensions that matter for long-term value. Compared to customers acquired through brand-owned (direct) channels, intermediary-acquired customers spend 4.1% less per stay and purchase 3.8% less frequently. Intermediary-acquired customers, while displaying stronger channel inertia and lower multichannel engagement, purchase across a wider variety of brands (multibrand behavior). When we combine these behavioral estimates into a customer lifetime value (CLV) computation, we find that while intermediary-acquired customers have positive CLV, their CLV is 19.94% lower than customers acquired through brand-owned channels, revealing, for the first time, the long-term implications of such customer acquisition strategies. Through an optimal allocation model we show that, although the CLVs are lower for intermediaries, a firm maximizing customer value typically invests in both channels: the optimal share allocated to intermediaries rising proportionally with the intermediary’s acquisition efficiency and accessible prospect pool, and falling when the hotel is operating at capacity. In sum, our results show that although using intermediaries may be a viable strategy for customer acquisition, the purchase behaviors of these customers are significantly and meaningfully different from customers acquired via brand-owned channels, thus urging managers to adopt a more nuanced ‘frenemies’ approach to building a channel portfolio.

Keywords

“We actually embrace the OTAs and leverage their marketing and utilize them as a customer acquisition tool.” —Greg Mount (former) CEO Red Lions Hotel Group “We’ve had direct booking for an awfully long time. The hotel industry has always had intermediaries. There’s nothing new about it. We want relationships with our customers.” —Richard Solomon, (former) CEO of InterContinental Hotels Group “You guys all criticize me for how much I charge you for guests to come to your hotel. I think you’re looking at it wrong. Look at us as the cheapest source of referrals that you could imagine. If they come through me, you pay me once, and if they come back to me again and again, shame on you. You should make them a loyal customer.” —Dara Khosrowshahi, (former) CEO of Expedia

Introduction

With the rise of digital platforms and aggregators, intermediaries 1 have become ubiquitous across many industries. In the travel and hospitality industry, a hotel brand’s reservation systems seamlessly integrate with online travel agents (OTAs, e.g., Expedia or Booking). During low-demand periods, they can make room-nights available automatically and in real-time, 2 reducing the quantity of unsold rooms, avoiding lost revenues and improving operational efficiency (Avery et al., 2015). Similar examples exist in other industries. For instance, meal delivery services (such as DoorDash or UberEats) for the restaurant industry, or news aggregators (e.g., Flipboard, Metacritic) for the news industry. As such, most service providers work with intermediaries along with the brand-owned (direct) channels when optimizing their distribution channel portfolio. Therefore, intermediaries have become a critical component of revenue management systems and have received significant attention in the operations management literature (Anderson and Xie, 2012; Granados et al., 2018; Ye et al., 2018).

Increasingly, brands use intermediaries not only for the distribution of goods and services but also for customer acquisition. Against this backdrop, using the intermediary has long-term implications as firms build relationships with customers they acquire via those channels. From an operational perspective, the near-term decisions aimed at improving operational efficiency and boosting sales volume (such as slack management, revenue management, etc.) can have long-term consequences for the value of the customer base. Tensions that arise are illustrated in the opening quotes from Greg Mount, Richard Solomon, and Dara Khosrowshahi, all former executives in the hospitality and travel industries. On the one hand, firms recognize the benefits of intermediaries as a source of customer acquisition. On the other hand, service providers are skeptical about the value of customers acquired via intermediaries. Therefore, at the heart of this dilemma lies the difference in the overall long-term value of customers acquired via these channels.

This dilemma remains an especially urgent problem for firms in service industries (not just hotels but also restaurants, food delivery, and airlines, among others). For example, some firms (for example, Southwest Airlines) have chosen to completely bypass intermediaries and rely strictly on their own channels but have had mixed success (Akca and Rao, 2020). In the hospitality industry, hotel brands collaborate with OTAs but also invest millions of dollars into ‘book direct’ marketing campaigns (KalibriLabs, 2016). While prior research has documented advantages and disadvantages of using intermediaries by service providers (for a review, see Section 1.4 below), the challenges that arise for building relationships with intermediary-acquired customers remain mostly unanswered, both from an academic and practitioner standpoint.

What We Do

Our study aims to shed light on this dilemma by offering a ‘customer relationship’ based perspective on intermediaries and their role in customer acquisitions. Table 1 positions our study within existing literature that examines the role of intermediaries for customer acquisition. Our objectives are three-fold:

Study positioning: Customer acquisition via intermediaries.

Study positioning: Customer acquisition via intermediaries.

First, we investigate a variety of customer dimensions that are elicited post-acquisition. Much of the prior literature on this topic has focused on an aggregate view of intermediaries such as aggregate demand effects, search, new sales volume, etc. (see Table 1). To the best of our knowledge, this is the first investigation into the customer relationship impact of intermediaries. In other words, instead of only asking “how many?,” we ask “what kind?” of customers are acquired via intermediaries. We characterize the “kind” of customers in terms of customer relationship dimensions, specifically transaction, channel, and brand behaviors, in post-acquisition periods. We argue that firms using intermediaries for customer acquisition should consider their implications for customer behavior and customer lifetime value (CLV), as they have critical long-term financial impact (Kumar, 2008). This facilitates a more comprehensive relationship-based view of the impact of intermediaries.

Second, by focusing on repeat customers and looking beyond the first transaction, our study offers an approach to evaluating intermediaries in terms of their long-term customer value (CLV) implications. This is a clear departure from prior work that has largely focused on short-term and immediate effects (Table 1), such as their role in search and booking behavior (Ghose et al., 2014; Ursu, 2018), stimulating demand in brand-owned channels via the ‘Billboard’ effect (Anderson, 2009; Anderson and Han, 2017), or the bilateral market power dynamics (Akca and Rao, 2020; Hunold et al., 2020). Furthermore, to our knowledge, this is the first paper that assesses, in financial terms, the magnitude of the CLV lost to intermediary channels in the long-term.

Third, building on the preceding CLV analysis, we conduct simulations to illustrate how managers can design the channel portfolio that maximizes long-term customer equity (CE) by optimally allocating acquisition budgets between brand-owned and intermediary channels. We analytically derive the optimal budget allocations that maximize customer equity, considering the trade-offs between the customer's CLV, the channel’s (own and intermediary) effectiveness in acquiring new customers, and the size prospect pool. Finally, we compare the CE-maximizing strategy to rule-of-thumb decision heuristics that a manager might use. Across all comparisons, the CLV-based strategy outperforms heuristics. In additional simulations, we also extend the discussion to conditions where the service provider may face capacity constraints and/or unfilled rooms. These simulations serve as decision support tool for managers to engage with the empirical findings of our study.

We use a unique dataset of customers’ brand-owned and intermediary transactions from a large hotel brand based in the United States, operating multiple individual brands, to compare the behaviors and CLV of customers acquired through intermediaries to those acquired through brand-owned channels. Our results reveal that intermediaries have a significant impact on the quality of customer relationships through persistent differences in post-acquisition behaviors.

1. Persistent and significant differences in post-acquisition customer behavior

At the transactional level, we find that customers acquired through the intermediary spend significantly less (by 4.1%) and have significantly longer interpurchase times (3.8%) (i.e., purchase less frequently) compared to those acquired through brand-owned channels. We also find that customers acquired through intermediaries are less likely to choose a brand-owned channel for future purchases, thus reducing the firm’s chances of inducing customers to switch to more profitable brand-owned channels. In terms of multichannel and multibrand usage, we find that customers acquired through intermediaries use fewer channels but engage with the firm across more brands within the same price tier. These analyses reveal a persistent impact of intermediaries on customers’ post-acquisition behavior that is generally unfavorable to the firm. Notably, this is a new result since none of the prior literature (and practice) have investigated the customer relationship impacts of intermediary acquisitions, as highlighted in Table 1.

2. Intermediary impacts CLV… and subsequently customer equity

The customer behavioral differences observed are further exacerbated in terms of long-term customer value. Specifically, we find that although customers acquired through intermediaries have a positive lifetime value, but they are 19.94% less valuable than their directly acquired counterparts—largely owed to the differences in their post-acquisition behaviors described above. Notably, the CLV is still positive, meaning that while brands can still derive value from these customers, they need to be aware of the potential trade-offs involved in using intermediaries for customer acquisition.

3. However, the optimal customer acquisition strategy must include the intermediary

The optimal acquisition budget allocation simulations reveal interesting patterns that add nuance to the empirical findings. Given that the CLV of an intermediary-acquired customer is lower than the brand-owned channel, the firm may be tempted to allocate all of its budget toward own-channels. We show this to be true only when the firm is operating at full capacity and does not have slack capacity to accommodate the growth of the customer base. We find that when firm has slack capacity, the optimal decision is to allocate the acquisition budget proportionally across the brand-owned and the intermediary channels. The proportion depends on the relative acquisition efficiencies of the respective channels and the prospect pools available to the firm. We also demonstrate that, under certain conditions, the firm may be better off allocating the acquisition budget to the intermediary even though the CLVs may not be as high as the brand channel. Therefore, a customer equity maximizing budget allocation generally involves a proportional investment in both channels, unless the intermediary prospect pool is too small, the intermediary acquisition is too expensive, or a brand has limited capacity to accommodate additional customers.

Study Contributions

This study contributes to the distribution channels literature by introducing a long-term, customer-centric perspective that has been largely overlooked. Prior research on intermediaries has traditionally focused on short-term, aggregate outcomes like in revenue management effects (e.g., Ye et al., 2018), opaque pricing channel effects (e.g., Granados et al., 2018; Mao et al., 2021; Ye et al., 2018), or search and billboard effects (e.g., Anderson, 2009; Ghose et al., 2014; Ursu, 2018). For instance, prior work has found a positive aggregate and immediate impact of intermediaries on booking behavior despite some cannibalization of the own channel (Granados et al., 2018), explainable through the ‘billboard’ effect (Anderson, 2009; Anderson and Han, 2017). Our study adds nuance to prior findings by showing that, if we take a long-term customer-centric perspective, the impact of intermediaries is more complex. Although the pros of acquiring new prospects and gaining short-term revenue are possible through intermediaries, the value of the ensuing customer relationships is questionable. Our study is the first to empirically document the lasting impact of the acquisition channel on future customer behaviors and, critically, on CLV—thus shifting the traditional short-term (transactional) view of intermediaries to a long-term customer-centric (relationship) one (Kumar, 2018).

Further, this paper contributes to the literature on the critical importance of the acquisition ‘moment’ from a customer equity standpoint (Chan et al., 2011; Datta et al., 2015; Peters et al., 2015). While extant work has found mixed effects of acquisition modes like referral marketing or search advertising, it has largely focused on acquisition modes that are either firm controlled (Datta et al., 2015; Maier and Wieringa, 2021; Verhoef and Donkers, 2005) or used only for communication (Chan et al., 2011). Our work investigates intermediaries that function as both communication and purchase channels, explicitly competing with the firm’s own offerings. This is a crucial distinction because, unlike communication-only platforms where the final purchase is on brand-owned channels, these intermediaries are competing sales platforms where customers can make repeat purchases, complicating the customer relationship (Susskind et al., 2016).

The study’s findings are new to the literature on customer relationship management (CRM) and the interplay of channels. Most of the CRM literature has focused on the impact of multichannel/omnichannel behaviors on the customer relationships and journeys (Kumar, 2018, 2024; Verhoef et al., 2010). We complement this stream of work by showing that the mode of acquisition can influence the future channel behavior of a customer. We document evidence of channel inertia, where customers acquired through intermediaries are less likely to switch to brand channels in the future (Henderson et al., 2021; Langer et al., 2012; Valentini et al., 2011), leading to further reduction in multichannel behaviors and eventually, lower CLV. 3

What is Known

The literature on intermediaries and distribution decisions, largely based on analytical modeling, has focused on pricing strategies (such as opaque pricing and selling) (Anderson and Xie, 2012; Chen et al., 2014; Mao et al., 2021; Shapiro and Shi, 2008), strategic contracts between service providers and intermediaries (Hunold et al., 2020; Toh et al., 2011), and revenue management (Ye et al., 2018). Using intermediaries as distribution channels can have many benefits for service providers. First, they can (partially) outsource services that a specialized third-party can deliver better and/or cheaper, such as restaurant reservation platforms (e.g., OpenTable and Resy). Second, they offer a unique growth opportunity by facilitating customer acquisition, especially when the customer base is inaccessible to the firm. For example, restaurant owners benefit from meal delivery services such as Door Dash as the platform opens up new markets. In the hotel industry (our empirical context), hotel brands embraced OTAs to dynamically manage slack inventory across multiple properties (Avery et al., 2015; Ye et al., 2018), to leverage the ‘billboard’ effect where listing on an OTA site may lead to increased non-OTA transactions overall (Anderson, 2009; Anderson and Han, 2017), and to expand their customer prospect pool through exposure during consumer search (Ghose et al., 2014; Ursu, 2018). Furthermore, with OTAs firms can better adjust to demand fluctuations through pricing strategies (Anderson and Xie, 2012; Chen et al., 2014; Mao et al., 2021).

However, the use of intermediaries can also have its downsides. First, intermediaries may charge significant commission rates, which affect the margins that a firm may earn from a transaction. In the hotel industry, for example, OTAs may charge anywhere between 10% to 25% of the booking price (Avery et al., 2015). Second, using intermediaries can lead to sales cannibalization in a firm’s more profitable brand channel (Abhishek et al., 2016; Granados et al., 2018; Wang et al., 2009). Third, intermediaries may also enter into restrictive contracts with service providers that allow them to exert influence on the provider’s pricing structure (Hunold et al., 2020; Toh et al., 2011). Finally, from a customer management perspective, firms cede some control of the customer’s experience by using intermediaries (Lemon and Verhoef, 2016). Prior research has shown that using intermediary touchpoints can weaken the evaluation of a firm because these touchpoints are more attributed to the intermediary and less associated with the firm (Kranzbühler et al., 2019).

It is worth noting that much of what is known in the literature is restricted to short-term aggregate revenue management. The literature is surprisingly silent on how intermediaries may shape the customer behaviors and the long-term customer relationships that service providers hope to nurture (see Table 1 for literature overview). Service providers (hotels) view intermediaries as a means by which they can access new prospect pools—customers who will later switch to more profitable brand-owned channels. As such, intermediaries continue to comprise a very large source of customers for firms (for example, nearly 40% of all hotel bookings come through intermediaries). In fact, a recent industry report from Expedia (one of the largest OTAs in the industry) touts the ‘customer value’ of Expedia customers (Expedia, 2024). Our research aims to provide (unbiased) clarity on how managers can assess intermediaries from a CLV perspective, a topic that has not been explored in literature.

Empirical Context

The institutional setting that we focus on is the hospitality sector, specifically the hotel industry. Attracting customers to a specific hotel—referred to as customer acquisition—is one of the key steps in the hotel marketing process. This is a complicated matter for hotels for at least two reasons. First, unlike a local retail business—where customers come from a geographical area proximate to the business, hotel customers are usually not local. As such, hotels have to reach out regionally, nationally, and sometimes globally to get the customers they need to fill rooms and reach desired occupancy levels. Second, hotels, in addition to their own efforts, need to rely on intermediaries for assistance in securing customers. However, carefully targeting this demand by carefully balancing the channel portfolio between brand and intermediary channels is a key challenge. These contextual realities make the hotel industry a particularly interesting context to study our research questions, largely due to the ripe competition between the hotel’s own channels and intermediaries or OTAs to acquire customers (Dev, 2012).

Data Overview

Our data comes from an anonymous hotel brand (a parent brand) headquartered in the United States, that operates multiple individual brands in its portfolio. The company has more than 5,000 hotels in its system all over the United States and the world, in three price levels or ‘tiers’: economy, mid-scale and premium. Our sample consists of customers who enrolled in the brand’s loyalty program between January 2014 and December 2017. The data-providing brand’s investor filings, disclosed in 2018/2019, stated that loyalty program members accounted for approximately one-third of occupancy. Reports from the American Hotel and Lodging Association (AHLA) and the Hospitality Sales & Marketing Association International (HSMAI), the hotel industry’s principal trade groups, revealed that loyalty program members accounted for about 25% of all economy tier rooms, 55% of all midscale rooms, and 56% of all upscale rooms. 4 The data provider has mostly economy and midscale hotels and their loyalty penetration approximates that of the overall industry. Throughout the observation window, the parent brand made their rooms available for booking via OTA websites in addition to their own channels, with a ‘price parity’ clause prohibiting the OTA from pricing below the brand-owned channel. We focus on customers who made bookings at any of the brand’s hotels in the US because an overwhelming majority of the sample of customers was based in the US and made bookings only at locations within the United States (see E-Companion A for geographic distribution of transactions).

In total, we observe 165,739 customers transacting across multiple brands affiliated with the parent brand. The data includes the specific hotel property at which the booking was made, the number of nights that were booked, room revenue (average daily rate or ADR multiplied by the number of nights stayed), folio revenue (the total bill, room revenue plus all other charges), and arrival and departure dates. Most critically, we observe the booking channel a customer used. More specifically, in this case, the OTA is the intermediary in question, and there are several brand-owned channels (website, phone, on-property reservations, global distribution system, among others). 5

The average room revenue per customer per stay is $128.97, and the average length of stay is 1.69 nights per stay across multiple tiers (69.64% of all stays at economy tiers, 14.94% of stays at mid-scale tiers and 15.43% of stays at premium tiers). The average interpurchase time (between stays) is 105 days, approximately 68% of the stays are booked through a brand-owned channel, and 32% of customers in the dataset make their first purchase through an intermediary. Detailed descriptive statistics split by tier are reported in E-Companion A. 6

Model-Free Evidence

Before specifying a statistical model to estimate the impact of intermediary acquisitions on customer behavior and CLV, we first examine the data through a series of model-free analyses.

Aggregate Descriptives

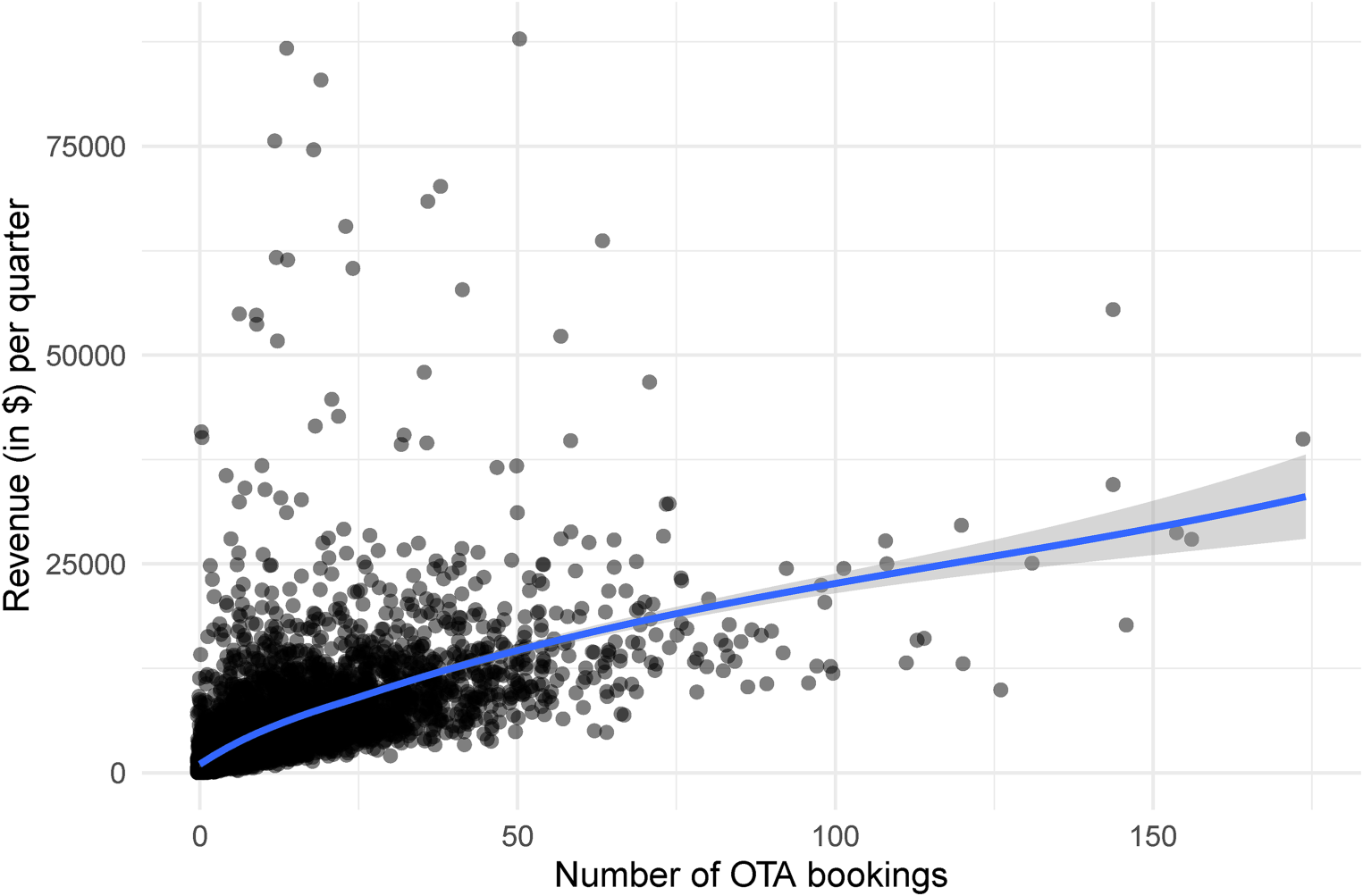

Figure 1 plots the site-level revenue against their share of third-party bookings from sites that report at least one transaction. We see from this figure that the share of intermediary bookings appears to be positively related to the revenue earned at each hotel location, in agreement with prior literature which has also focused on aggregate behaviors (Granados et al., 2018). Looking at this initial evidence, a manager might conclude that these acquisitions are beneficial and increase their investment in intermediaries. While this may be true in aggregate, it doesn’t consider the underlying customer behavior that may be important to consider. Our next set of model-free analyses provides additional insights into customer behaviors across acquisition channels.

Model-free evidence: Share of OTA bookings vs. revenue.

Disaggregate analyses

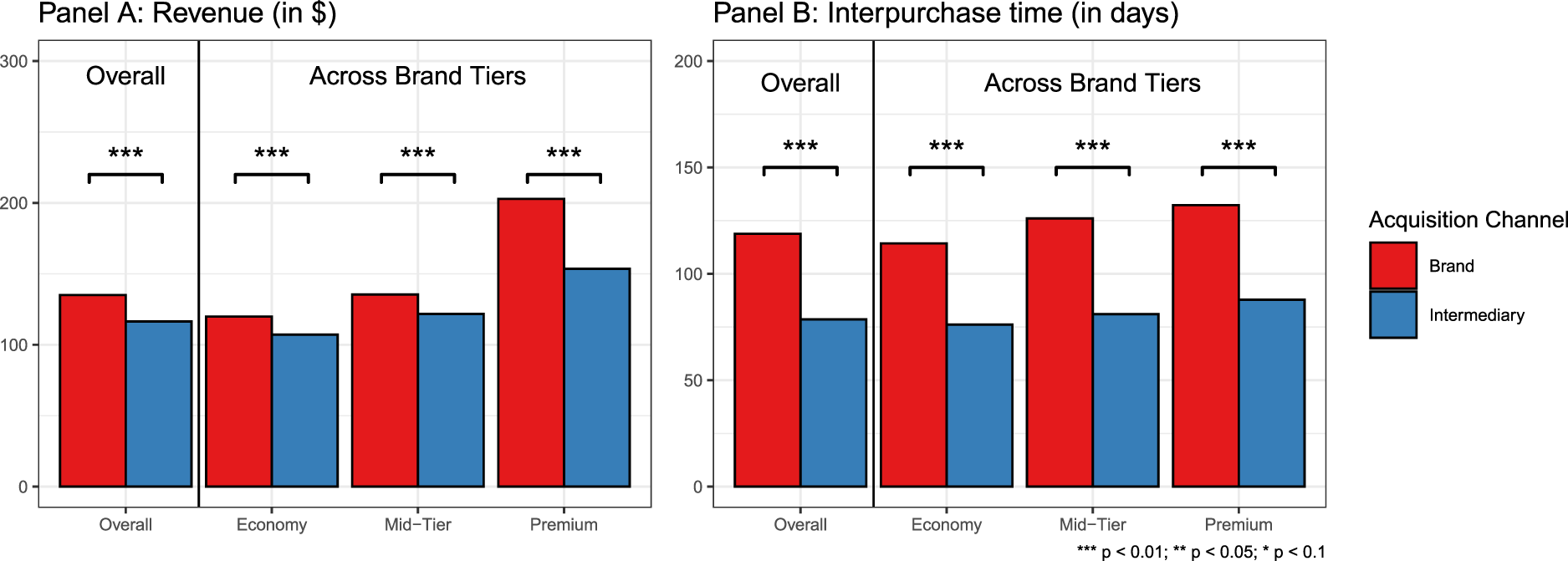

Given the large share of hotel bookings originating from intermediaries, it is important to understand whether customers acquired through different channels differ and whether such differences persist over time. We classify customers based on their first transaction as either intermediary-acquired or brand-acquired and plot the differences in behaviors in Figure 2. Intermediary-acquired customers generate significantly lower revenue per stay than brand-acquired customers, a pattern that holds across tiers (Figure 1: Panel A), providing initial evidence of a negative revenue impact of intermediary acquisition. Note that the only difference between the two groups (intermediary and brand-acquired customers) in the above analysis is the channel the customer used on the first transaction. In contrast, intermediary-acquired customers purchase more frequently, as measured by shorter interpurchase times, a result that is also consistent across tiers (Figure 2: Panel B).

Model-free evidence: Intermediaries vs. firm channels.

Taken together, Figures 1 and 2 offer conflicting evidence about the value of third-party acquired customers. On the one hand, third-party acquired customers spend less (in terms of revenue) across tiers. On the other hand, the initial evidence suggests that intermediary-acquired customers have a higher purchase frequency than brand-acquired customers. The model-free analyses, though revealing, may suffer from several confounds arising from observable and unobservable factors.

We then compared the frequency of channel switching against transaction frequency for all 61,274 repeat buyers in Table 2. The columns in Table 2 denote the frequency of channel switching. A customer is coded as having switched from one channel to another if they booked with an intermediary at the current occasion and used the brand-owned channel on the following purchase occasion (or vice versa). The rows in Table 2 denote the transaction frequency or number of transactions. Each cell contains the number of customers within each combination. The diagonal elements represent customers who switched channels on every occasion. We see initial evidence of high channel inertia where most customers continue to book through their first channel of purchase, while a smaller number of customers exhibit switching behavior. For example, 5,799 (73.21% of repeat buyers) never switched channels and 2,121 (26.79%) switched once. Going down the rows, we see that customers with a higher transaction frequency also tend to “stick” with the initial channel. In comparison, the diagonal elements are substantially smaller, suggesting that customers with high switching frequency are quite uncommon.

The model-free evidence presented above presents initial but compelling evidence of the difference between intermediary and brand-owned acquisition channels on subsequent customer behavior. However, the above analyses only highlight patterns in the data that are correlational in nature and do not account for possibly confounding effects. In the next section, we delve deeper into this phenomenon through econometric models to estimate the difference between intermediary and brand-owned acquisitions on customer behavior after controlling for various confounding issues.

In this section, we first introduce a general modeling framework and empirical strategy to identify the impact of the first customer acquisition channel on future behavior. Following this, we define the primary outcome variables of interest and describe the functional form used to model the customers’ behavior.

Channel switching.

Channel switching.

We begin with a general regression specification that describes the impact of a customer’s first transaction channel (through intermediary vs. brand-owned channel) on subsequently observed behavior. Suppose there are

In the absence of an experimental design, a critical concern related to identification of the acquisition channel effect stems from endogeneity (Mithas et al., 2022). Endogeneity in the acquisition channel variable (

Simultaneity

A customer’s purchase behavior may be co-determined with their choice of purchase channel. For instance, customers may transact through the intermediary to obtain a lower price or to have more choice. In our case, simultaneity is concerning at the acquisition moment, given that our main variable of interest (

Self-Selection

Endogeneity may also be caused by self-selection, meaning that the acquisition of customers through intermediaries might be non-random. Individual factors (such as price sensitivity, need for variety, convenience, etc.) as well as market-level factors (such as room supply, destination popularity in case of the hospitality industry, etc.) may play a role in driving a prospective customer toward intermediaries. To mitigate the effect of self-selection in the acquisition stage (customer’s first transaction), we adopt an exact matching approach (see E-Companion B for details). Briefly, for every intermediary-acquired customer, we match a brand-acquired customer who made a transaction for the same week, the same tier, in the same state, and paid the same price per night. As a result, for every intermediary-acquired customer there is at least one brand-acquired customer who is comparable in terms of location, brand category, price paid, time, and purchase channel (online). This new subsample of matched customers (intermediary and brand-acquired) allows us to control for destination-level and time-specific unobserved factors that may create selection bias at the time of acquisition.

We also include a rich set of observable controls (

A customer’s probability of being acquired by an intermediary (vs. brand) channel may be related to time-invariant unobservable factors such as price sensitivity, search costs, etc. While we note that customers are matched on price paid on the acquisition channel, price sensitivity might exist in subsequent transactions. In traditional panel data settings, one would use individual fixed effects to account for these time invariant customer-level unobservables. In our setting, however, we cannot use customer fixed effects because our main variable of interest (acquisition channel) is time-invariant. Therefore, in all our specifications, we use random effects specifications. Specifically, we include customer-level random effects (

Omitted Variables

Even after controlling for simultaneity, selection issues, and for site-specific and customer-specific time invariant factors as well as quarterly fixed effects, there may still be some unobserved factors within

We use Gaussian copulas to account for the correlation between the acquisition channel and the error term on the subsequent observations. Specifically, we consider the copula method for a discrete endogenous variable and insert an additional term in the regression (the control function), which allows us to consistently estimate the model. This copula term is defined as

Final Model Specification

The final model, shown in equation (2) includes our main effect, controls for observed and unobserved heterogeneity, as well as the endogeneity correction. The unobserved factors (

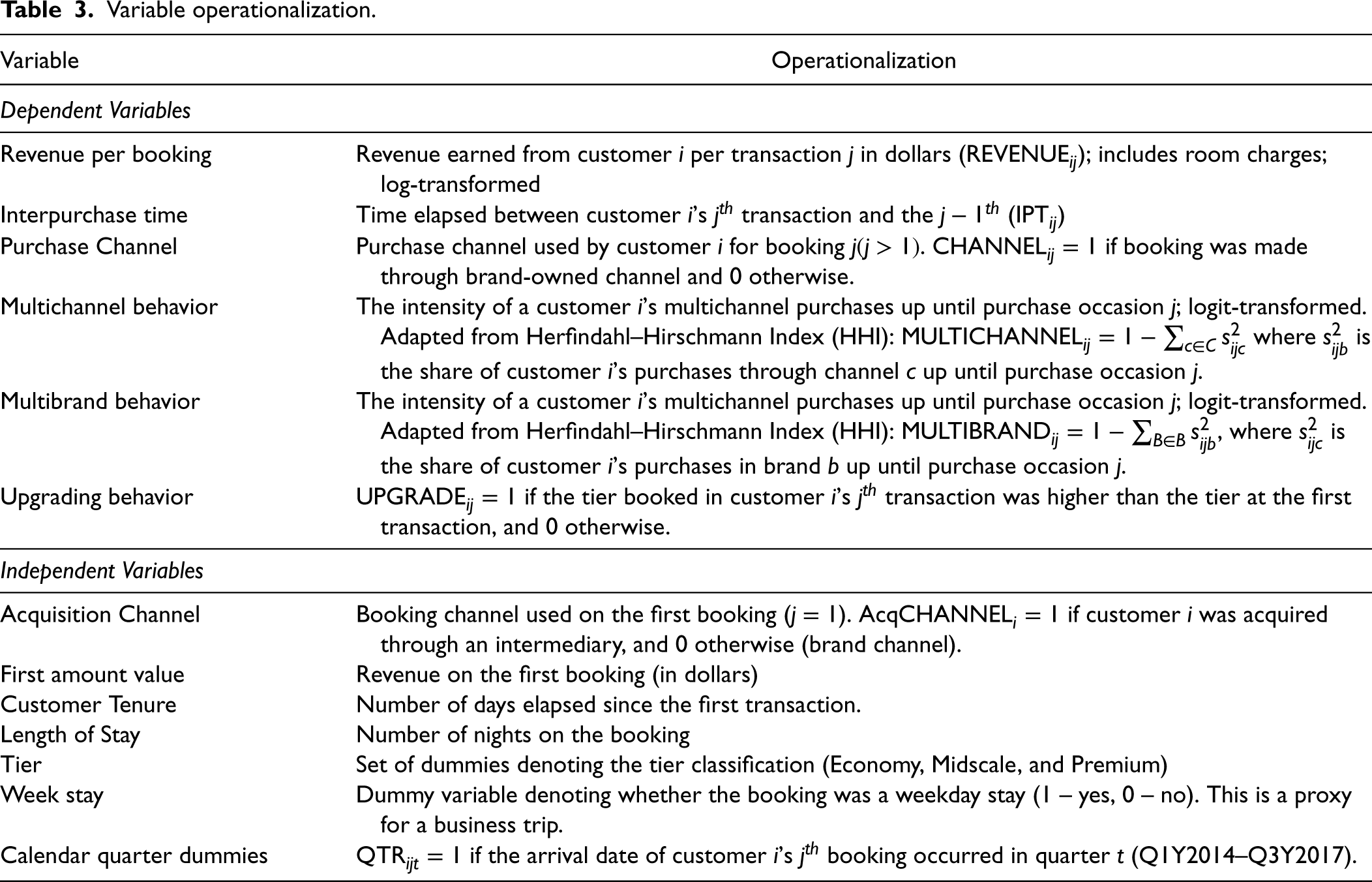

The dependent variables of interest in this research fall into three broad categories representing different aspects of customer behavior: purchase behavior, (multi)channel behavior, and (multi) brand behavior, all helping us calculate lifetime value. Table 3 provides details on operationalization of all variables. We report the full descriptive statistics and correlation matrix in E-Companion A due to space constraints.

Variable operationalization.

Variable operationalization.

Purchase Behavior

The purchase behavior variables include revenue per stay (in dollars) and interpurchase time of a customer’s transactions. We model folio revenue per stay (

Channel Behavior

Channel behavior refers to how customers use transaction channels after acquisition. We examine (a) whether the initial acquisition channel (

Brand Behavior

Brand behavior captures whether customers engage with multiple brands or upgrade to higher tiers. We assess (a) if intermediary-acquired customers shop across more brands, and (b) if they are more likely to upgrade (e.g., from economy to mid-scale). Multibrand behavior is measured as

Independent Variables

In terms of the independent variables, our primary focus is to estimate the impact of the acquisition channel on a customer’s subsequent transactions with the service provider. The main covariate of interest

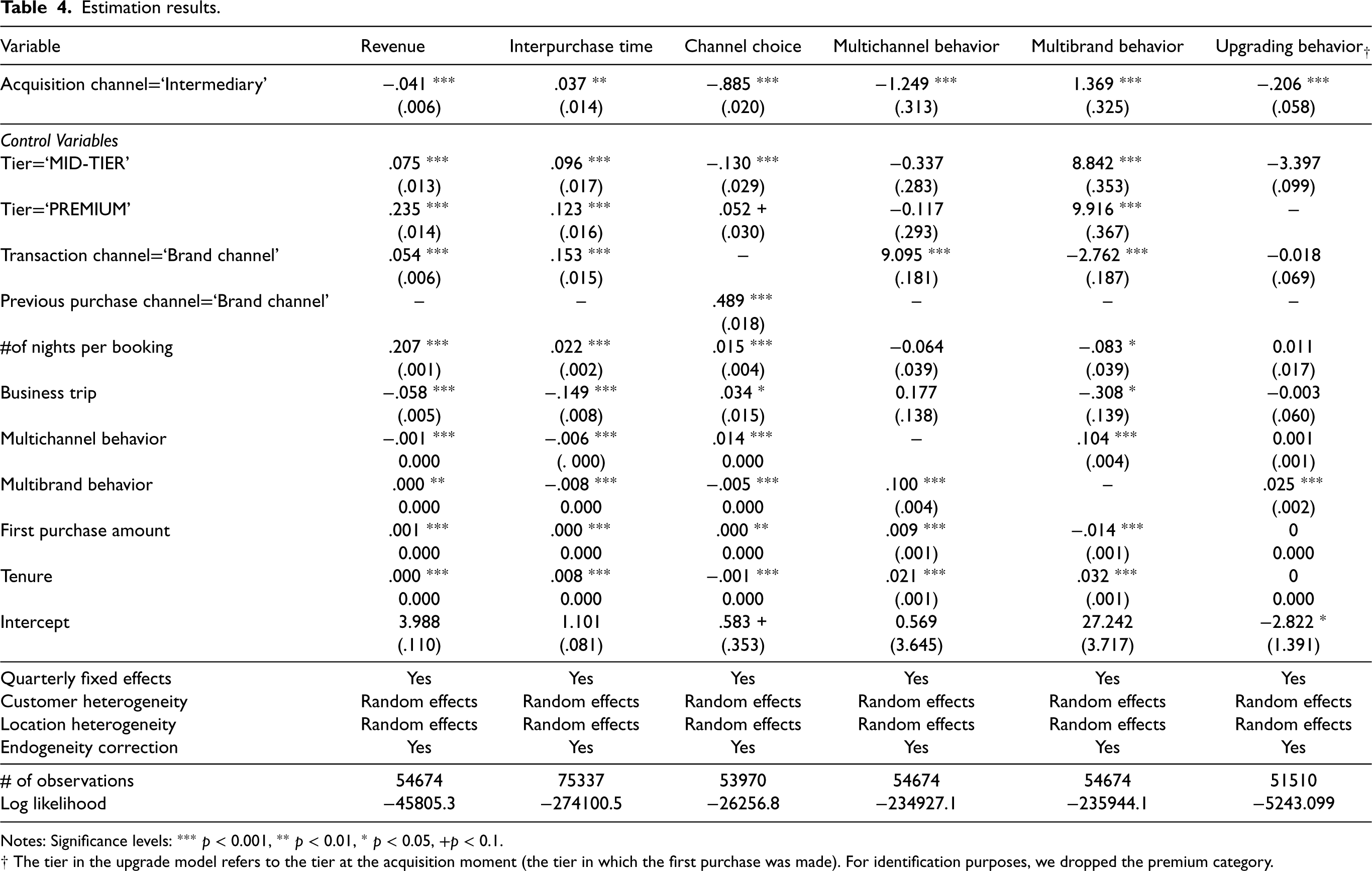

We estimated the model for each dependent variable (according to equation (2)) including observed and unobserved heterogeneity as well as the Gaussian copula endogeneity correction term. Table 4 presents the estimation results describing the effect of intermediary acquisitions for each of the dependent variables. We organize the discussion of the results in the following manner. We first describe the effect of intermediary acquisitions on purchase behavior: the revenue, and the interpurchase time. Next, we discuss the estimates capturing the effect of intermediary acquisitions on customer purchase channel behavior: modeling the probability of transacting via the brand channel and the intensity of multichannel behavior. Finally, we look at the impact of intermediary acquisitions on customer’s intensity of transacting with multiple brands.

Estimation results.

Estimation results.

Notes: Significance levels:

Purchase Behavior

The first column of Table 4 reports the revenue model estimates. We find a significant negative effect of intermediary acquisitions on revenue per stay: customers acquired via intermediaries spend 4.10% less per stay than brand-acquired customers. Interpreted in a log-linear framework, this percentage loss compounds across transactions. For context, a 200-room hotel with 50% occupancy and average room revenue of $130 would earn about $195,000 less per year if all customers came through intermediary channels. The effect is especially concerning given that hotel profit margins average only 10%.

9

Turning to tier-level analyses, revenue is highest for premium tiers (

The second column of Table 4 reports interpurchase time estimates from a Weibull AFT model with gamma frailty for unobserved customer heterogeneity. Intermediary acquisition lengthens interpurchase time by 3.8% (

Taken together, the interpurchase time and revenue model results reveal noticeable patterns in customer purchase behavior. The two types of customers, intermediary acquired and brand-acquired, are quite different in terms of their spending and frequency of purchases, and the acquisition channel is an important indicator of the differences (even after controlling for various confounds). Customers acquired through intermediaries spend less (revenue) and transact less frequently (repeat purchase behavior) than brand-acquired customers.

Multichannel Behavior

We capture a customer’s channel behavior in two ways—(a) the choice of transaction channel and (b) the intensity of channel use. First, to understand the lasting impact of the acquisition channel on future channel choice behavior, we estimate a binary Probit using standard maximum likelihood approaches and report the results in column 3 of Table 4. We see from the table that customers acquired through intermediaries are significantly less likely to choose a brand-owned channel for their future purchases (

The second model captures the intensity of multichannel behavior and provides additional insights about the persistent differences between intermediary and brand-acquired customers. Recall that the dependent variable here captures the usage of different purchase channels: the intermediary, and a number of different brand-owned channels. The low values indicate that the customer tends to use the same channel. Specifically,

Taken together, the two models of channel behavior point to strong inertia in channel use. First, the purchase channel that a customer uses on the first purchase is a strong signal for future channel behavior, in the sense that intermediary-acquired customers are less likely to switch to brand-owned channels and tend to purchase through fewer channels altogether. Furthermore, as customers continue transacting, the channel behavior is reinforced. The higher the channel inertia, the harder it is for firms to induce customers (e.g., through hotels’ “book direct” campaigns) to switch to more profitable brand channels. Thus, although intermediary acquisitions may increase the volume of transactions and number of customers overall, managers should not expect that these customers would easily switch to brand channels.

Multibrand Behavior

Given that the focal parent brand operates multiple individual brands using the same loyalty program, it becomes relevant for the company to know whether newly acquired customers engage across the brands in the portfolio and whether such customers upgrade to purchase from higher tiers. In other words, do intermediary acquired customers use multiple brands within the parent brand’s portfolio? To answer this, we adopt a two-pronged measure of multibrand behavior. Our first dependent variable measures the intensity with which a customer engages across the brand universe (

Robustness Checks and Additional Analyses

Alternative methods to handle endogeneity

As an alternative to a Gaussian copula method, we consider instrumental variable approach to alleviate concerns regarding endogeneity due to supply side issues, that is, common firm-level shocks that might influence customers to flock towards intermediary or brand-owned channels. Because it doesn’t not rely on strong ignorability assumptions, an IV-based method would help alleviate some self-selection issues such as price sensitivity driving the results (Mithas et al., 2022). Our instrument variable is constructed using Google search interest data, which approximate the demand trends for OTAs. A similar identification strategy was employed in Maier and Wieringa (2021). We use Google trends for the names of the popular OTAs, and also for generic search terms to capture OTA popularity at time

Data Considerations and Subsample Analyses

Next, to check whether the effects are an artifact of pooling the data across tiers, we conducted subsample analyses for each tier. The results (reported in E-Companion C.2 due to space constraints) continue to be robust. Across tiers, the acquisition effect of intermediaries on revenue continues to be negative and significant, except for the premium brand where the effect is not significant. We also separately estimated the model for leisure and business travel segments, since it is possible that the purchase behavior of a customer varies significantly depending on the purpose of the visit. We identify business trips by arrival date falling on a weekday. The results continue to remain robust (E-Companion C.2).

Furthermore, we investigate the channel-switching behavior of intermediary-acquired customers. To this end, we re-estimated the channel choice model on the subsample of intermediary acquired and brand-acquired customers (see E-Companion D). While brand-acquired customers exhibit channel inertia, we observe the opposite for intermediary-acquired customers. As such, intermediary-acquired customers are less likely to return to a brand-owned channel even if they used it in the previous transaction. Additionally, we focused on intermediary-acquired customers and studied early (first-transaction) predictors of switching to a brand-owned channel (see E-Companion D). For example, the probability of switching to a brand-owned channel increases when the first purchase amount is higher, indicating that the first purchase continues to play a persistent role in channel switching as well. We also find that the time between the first and second purchase is another important factor that is correlated with channel switching. The longer the time between the first and second purchases, the lower the probability of switching to a brand-owned channel. However, we note that these effects are correlational and not strictly causal.

Joint Estimation

We also estimated our target models jointly to account for customer-specific correlation of observed behaviors. Specifically, we focused on estimating the revenue, channel choice, multichannel behavior and multibrand behavior jointly.

10

We specified that four equations are correlated via the individual-specific random effects that follow a multivariate normal distribution

Dynamic Models

Finally, we re-estimated our revenue and interpurchase time models including lagged dependent variables, a price-per-night control variable, and an autoregressive error structure (Becker et al., 2019). Including lagged dependent variables would help alleviate endogeneity concerns, where the unobserved confounders are time invariant or slow moving. The results (reported in E-Companion C.4) remain robust.

Potential Explanation for the Main Effects

Although we focus more on an “empirics-first” approach (Golder et al., 2023; Spearman and Hopp, 2021) toward describing the phenomenon using real-world data, we offer plausible theoretical explanations for our findings. We view the findings through the lens of customer journeys (specifically concepts of “branded outsourcing” (Kranzbühler et al., 2019)), which are critical in a multichannel environment. From a consumer journey lens, the intermediary is essentially a partner-owned touchpoint (Hamilton and Price, 2019; Lemon and Verhoef, 2016). As such, the customer’s first experience with the focal service provider is shaped by the intermediary’s platform which competes with the firms’s own channels. This initial interaction is critical, as consumers form rapid and lasting judgments from brief experiences (Ambady et al., 2006; Peracchio and Luna, 2006). Indeed, customers acquired through intermediaries are exposed to intermediary marketing and may have a limited experience of the focal firm’s marketing. Therefore, a OTA-acquired customer is less likely to build associations with the service provider. In other words, they are more likely to attribute this touchpoint in the customer journey to the intermediary and not to the focal firm. As a consequence, the customer will have stronger associations and attributions of the purchase channel with the intermediary, compared to the brand-acquired customer (Kranzbühler et al., 2019). If customers perceive the intermediary touchpoints as positive, then using a intermediary channel for acquisitions can weaken brand associations and evaluations of the focal firm (Weiner, 2000). For customers acquired through brand-owned channels, on the other hand, the firm is able to curate the customer experience and journey through its branding (Hamilton and Price, 2019). As such, the brand associations are more likely to be positive (compared to OTA-acquired customers). As such, we expect that the behaviors of OTA-acquired customers would be markedly worse than their brand-acquired counterparts. This mechanism is particularly germane to our focal empirical context, where the service provider operates multiple brands (across price tiers) and numerous franchises through the same loyalty program (similar to Marriott, Hilton, Hyatt hotels etc.).

Consumers generally exhibit inertia when it comes to switching channels because of various factors including value alignment, channel loyalty, and convenience (Ansari et al., 2008; Cazaubiel et al., 2020; Konus et al., 2008; Melis et al., 2015). This is especially true for intermediaries, where the customer is often encouraged to continue booking through the OTA channel. Switching to a new channel (and staying with it) requires time and effort to learn a new design, user interface, etc. Our findings, especially in the channel choice model, empirically concur. OTA acquired customers are very unlikely to switch to a brand-owned channel, and the firm’s efforts (e.g., book direct campaigns) in switching customers to own channels are often moot.

A CLV-Driven Acquisition Channel Strategy

Historically, distribution channel management has been an operations management decision primarily focused on maximizing efficiency and revenue, such as managing slack (Ye et al., 2018). We offer a different perspective that managers may consider. We advocate an acquisition channel strategy with customer value at the center. Up until now, we have evaluated the effect of intermediary acquisitions on customer behavior. In this section, we build on this idea by first evaluating the long-term customer value implications of using intermediaries. We then design a service provider’s optimal acquisition channel strategy—one where a manager allocates their acquisition budget across brand channels and intermediaries to maximize the value of all customers acquired via the two channels (to maximize customer equity).

Customer Lifetime Value

To understand the long-term financial implications of intermediaries, we can compare the lifetime value of a customer acquired via the brand-owned channel to a customer acquired by the intermediary channel. Specifically, in the following analysis, we combine the model-based predictions from the revenue, channel choice, and interpurchase time models to calculate CLV from two distinct customers: a firm and an intermediary-acquired customer. This exercise allows us to offer insights into the long-term influence of acquisition channels. Because our setting is non-contractual, we express a customer’s CLV as the discounted value of future cash flows as follows,

11

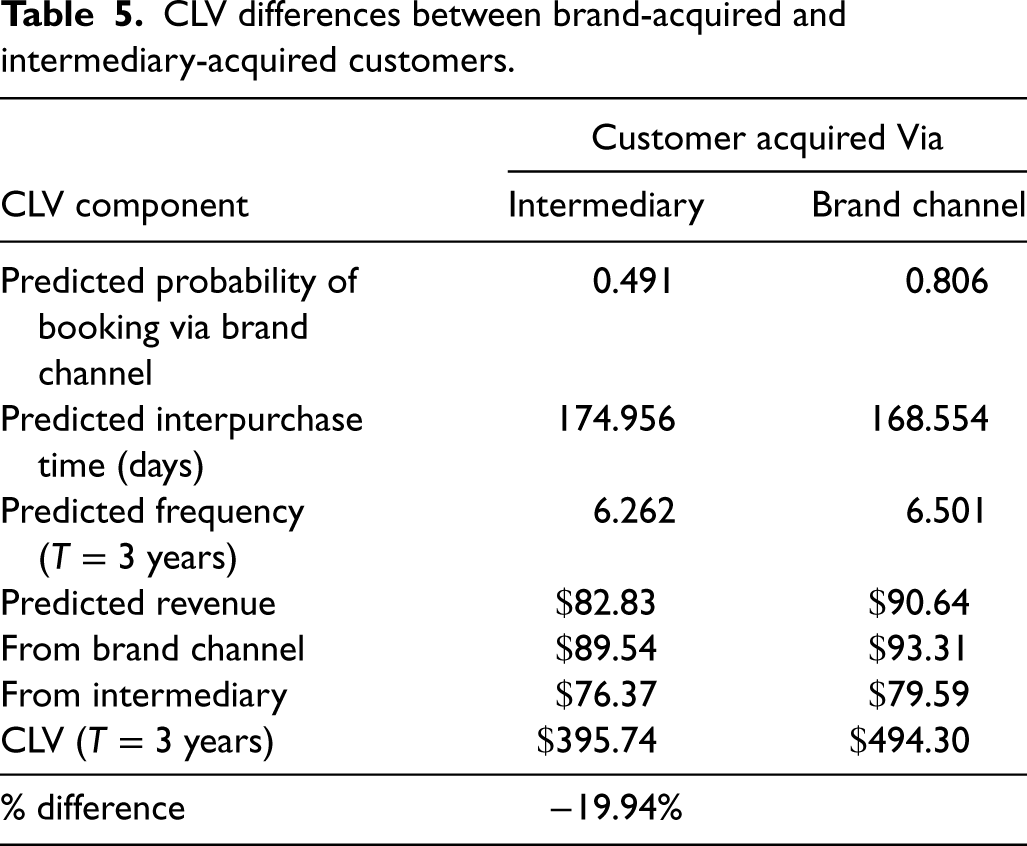

We compare the CLV for an average customer acquired through the intermediary to their counterpart acquired through a brand-owned channel in Table 5 13 . Intermediary-acquired customers are, in the long run, 19.94% less valuable in lifetime value than brand-acquired customers. This gap is driven by their lower purchase frequency, lower transaction revenue, and greater use of lower-margin intermediary channels. Even with a conservative 10% commission rate, the revenue impact of intermediary acquisitions is substantial and consistently below that of brand-acquired customers. Notably, intermediary-acquired customers who subsequently book directly generate more revenue than brand-acquired customers who book via the intermediary, highlighting the potential value of encouraging direct bookings. However, channel switching is rare (see Table 2 and E-Companion D). In summary, these results underscore that intermediary acquisition channels can have a significant and lasting impact on CLV.

CLV differences between brand-acquired and intermediary-acquired customers.

So far, our focus has been on capturing the behavior of brand-acquired and intermediary-acquired customers after the acquisition moment. In this section, we illustrate how managers can use the calculated CLV to design long-term value-maximizing channel management strategies before acquiring customers. We begin by specifying a service provider’s problem. The service provider aims to maximize customer equity from customers acquired via two channels.

We assume that the

Since

In this section, we considered a general problem, where the firm can freely move resources between two channels and has slack capacity to accommodate all newly acquired customers. In the E-Companion F, we provide the derivation of the analytical solution, together with a discussion of a constrained problem, where a firm is facing a capacity constraint and an opportunity cost on unsold rooms.

In Scenario A, we assume that the total acquisition budget is

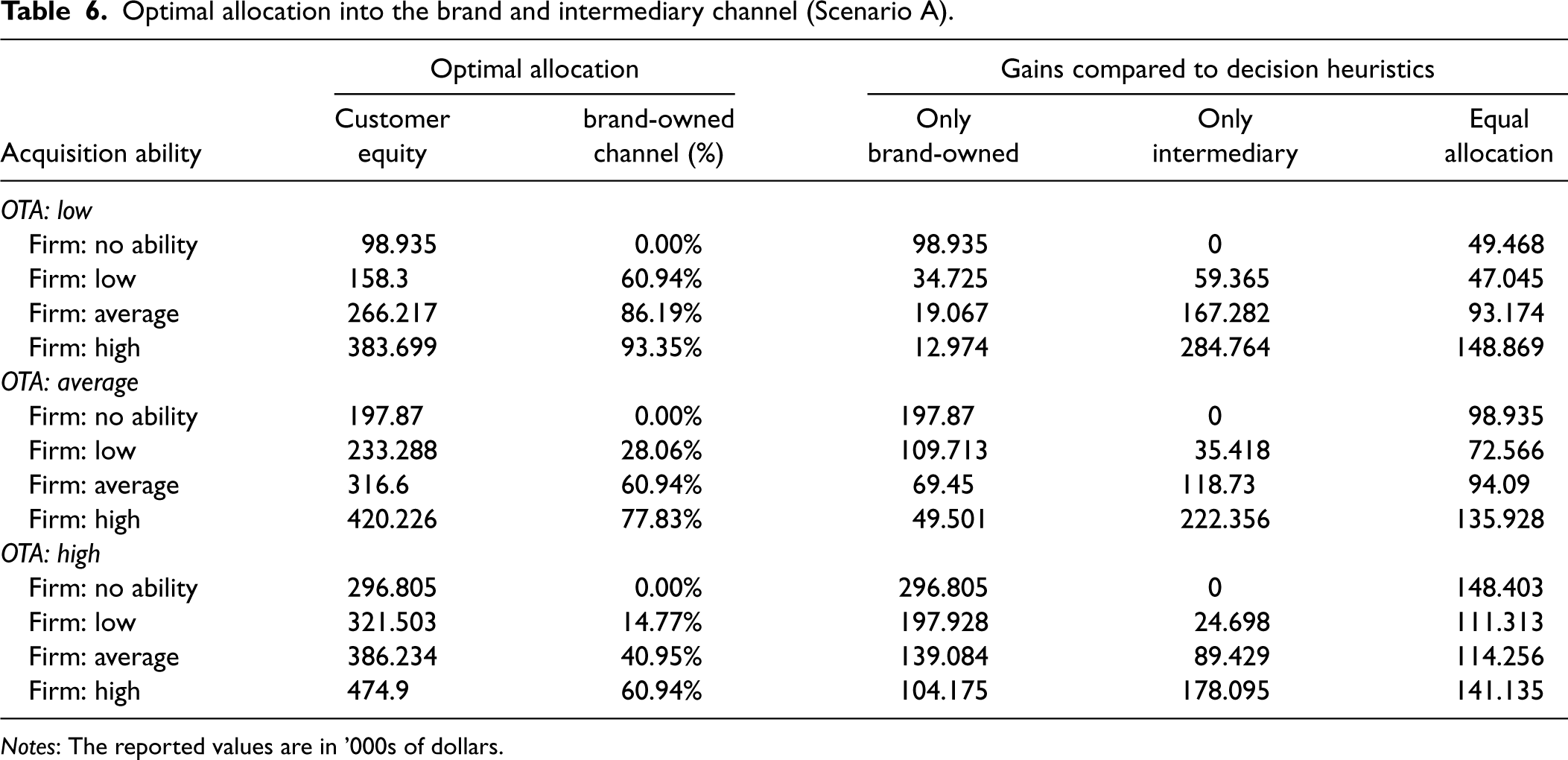

The optimal resource allocation for this scenario, obtained according to equation (6) is presented in Table 6. Specifically, for different combinations of firm’s and intermediary’s acquisition ability, we report the maximum customer equity (

Optimal allocation into the brand and intermediary channel (Scenario A).

Optimal allocation into the brand and intermediary channel (Scenario A).

Notes: The reported values are in ’000s of dollars.

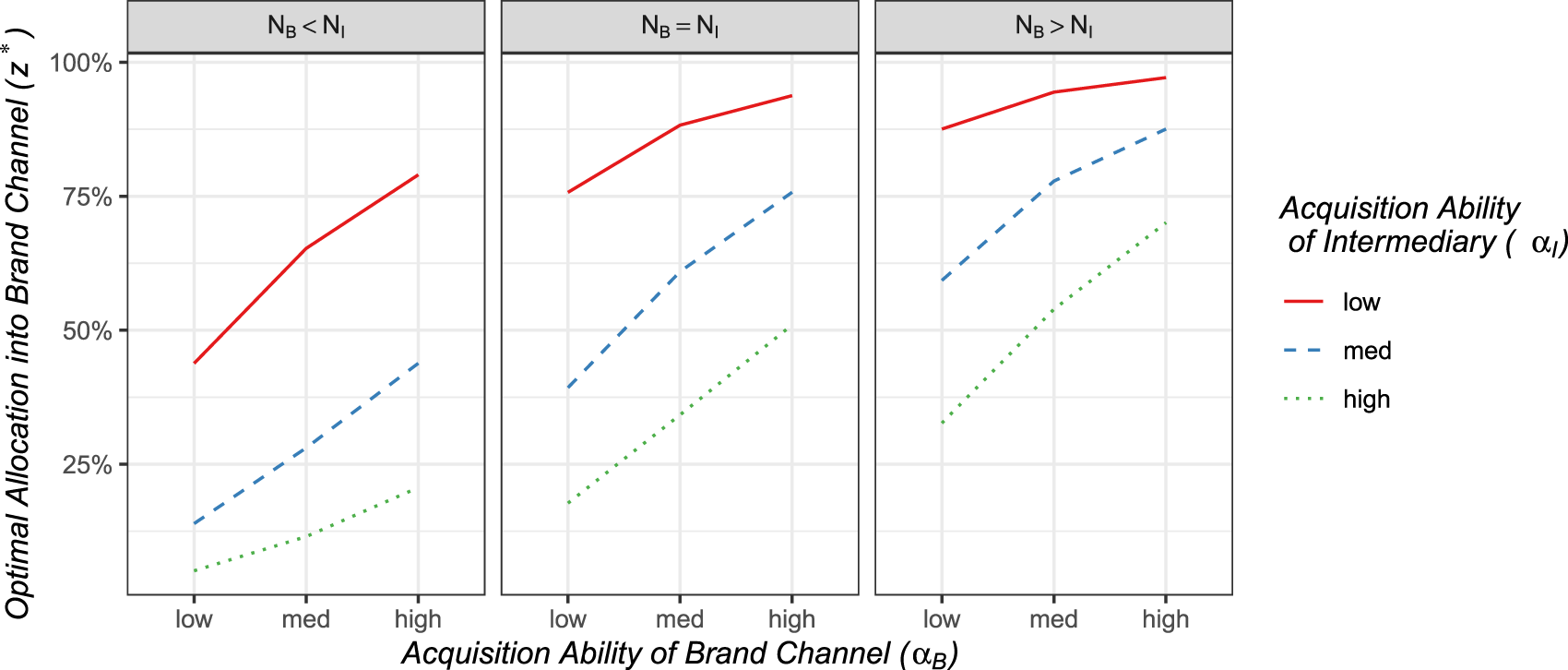

For examples presented in Table 6, the firm’s optimal allocation always involves using an intermediary, generally leading to gains over all three rule-of-thumb decision heuristics. For example, if the intermediary has a low acquisition efficiency, the firm with a low acquisition efficiency should invest 39.06% of the budget into the intermediary. In extreme cases, when the firm cannot acquire customers via its own channels, it should spend all its resources on customer acquisition via an intermediary channel. Even if the OTA channel has low acquisition ability, this strategy will yield an additional $47.045 over investing into two channels proportionally. In Scenario B, we consider varying sizes of the prospect pool for intermediary and brand-owned channel. Figure 3 illustrates this visually. At the extreme, when the intermediary has a low acquisition efficiency (

Optimal Allocation of Acquisition Budgets for varying market sizes (Scenario B). Notes: This figure describes the optimal allocation of acquisition budgets into the brand channel for various market conditions. The y-axis is the optimal allocation (

In summary, the results from the optimization presented here and also in E-Companion F show that, there is nuance in allocating resources to brand versus intermediary channels. In light of the empirical findings—that the CLV from an intermediary acquired customer is significantly lower than a brand channel, hotel managers may be inclined to invest all the acquisition budget in brand channels. As we show in E-Companion F, this holds true if the firm is operating at full capacity and has limited resources (capacity) to meet the potential demand. However, when a firm has a slack capacity to make available in the brand-owned and intermediary channels, the optimal decision is to allocate the budget proportionally across two channels, and this proportion depends on relative acquisition efficiencies and market sizes in respective channels. Generally, the intermediary can offset a lower CLV, by giving access to a larger prospect pool or having a higher acquisition efficiency (relative to that of the firm). Furthermore, under certain market conditions, an optimal decision would be to allocate the majority of the acquisition budget to the intermediary, for example, when

Through a series of empirical analyses of data from a hotel company with thousands of hotels under multiple brands, we analyze the difference between the lifetime value of customers acquired via intermediaries compared to the lifetime value of customers acquired via brand-owned channels across several relevant dimensions. On the one hand, intermediary-acquired customers spend 4.1% less per stay and transact 3.8% less often compared to brand-acquired customers. They also engage with fewer channels (lower multichannel behavior) and are more likely to be loyal to the intermediary. On the other hand, intermediary-acquired customers tend to shop across a wider range of brands within a firm’s portfolio. Additional analyses reveal that, while intermediary-acquired customers generally have a positive lifetime value (CLV) in the long-term, their CLV is 19.94% less than brand-acquired customers.

To explore this further, we solved an optimal resource allocation problem where we derived a closed form solution for a service provider trying to allocate acquisition budgets across two distribution channels, its own brand channel and intermediary. We show that, while the CLV differences are quite significant, other market forces, such as the firm’s own capacity, acquisition efficiency and market size, play an important role in the allocation of resources. Below, we discuss the contributions of this study both to academic literature and managerial practice.

Academic Contributions

This research makes several important contributions to academic literature. First, we extend the literature on distribution channels by moving beyond the traditional focus on short-term, aggregate outcomes. While prior work has extensively studied operational aspects like revenue management and the immediate impact of billboard effects, our study introduces a long-term, customer-centric lens. We are the first to empirically document the lasting consequences of the acquisition channel on a wide array of future customer behaviors and, most critically, on CLV. This shifts the evaluation of intermediaries from a purely operational or transactional assessment to a strategic, relationship-focused one.

Second, our work adds a crucial dimension to the literature on the customer acquisition moment. Extant research has primarily examined acquisition modes that are either controlled by the firm (like referral programs) or serve a purely communicative function. We investigate intermediaries that act as competing sales platforms, functioning as both communication and purchase channels. This distinction is vital, as these intermediaries are not merely touchpoints in a firm-controlled journey but are active competitors for the customer’s loyalty and repeat business, thereby adding a new layer of complexity to the understanding of customer equity in this context.

Finally, we bridge the literature on customer relationship management (CRM) and multichannel behavior. While prior work has explored the impact of customers’ multichannel usage on their relationships with firms, we demonstrate that the initial mode of acquisition is a powerful predictor of future channel behavior. By showing that intermediary-acquired customers exhibit strong channel inertia and are less likely to switch to brand channels, we link the acquisition event directly to subsequent multichannel dynamics and, ultimately, to the overall value of the customer relationship.

Managerial Implications

OTAs account for anywhere between 30% and 40% of all hotel bookings worldwide, and there is a constant tussle between brand-owned channels and OTAs about who owns the customer. Hotel brands are increasingly trying to push customers to book directly (KalibriLabs, 2016), while hoping to induce channel switching among customers acquired through intermediaries. We find that this line of thinking is overly optimistic. Below, we discuss the risks and potential benefits of acquiring customers through intermediaries, basing our recommendations on the findings of this study.

Over Reliance on OTAs for Customer Acquisition is Risky

Transactions, Bookings, and Long-Term Value: We find that the acquisition moment is an important signal to firms about the future customer behavior. Specifically, we find that customers acquired via intermediaries tend to have lower transaction revenues, book less frequently and through fewer channels than those acquired through brand channels. The estimated 4.1% revenue drop per transaction roughly translates to a difference of $195,000 yearly for an average-sized hotel, which is quite significant. This has profound implications for long-term customer value as well. We find that the CLV of an OTA-acquired customer is 19.4% lower than brand-acquired customers. As such, hotel managers should be cautious about over-relying on OTAs for customer acquisition, as this could lead to a relatively less profitable customer base in the long run. Channel Switching: Our findings of channel inertia suggests that customers acquired through intermediaries are less likely to switch to brand channels, a stated objective of many hotel brands. This result is in line with prior findings in other contexts that suggests that much of the inertia effects may be attributable to channel loyalty (Chen and Hitt, 2002; Langer et al., 2012). As such, managers need to rethink the effectiveness of OTA partnerships, particularly in terms of getting these customers to book directly in the future. While we do not empirically offer strategies to induce channel switching, we note that the motivations for customers to switch channels may include better pricing, loyalty rewards, or personalized offers that are more compelling than those provided by the intermediaries (Ansari et al., 2008; Cazaubiel et al., 2020; Konus et al., 2008; Melis et al., 2015).

The Silver Lining to OTA-Acquisitions

Although the above findings paint a somewhat bleak picture for OTA-acquired customers, there are some silver linings to consider. OTA-acquired customers’ CLV is still positive: Although the CLV of an OTA-acquired customer is significantly lower than that of a brand-acquired customer, it remains positive—indicating that these customers are still a net profitable opportunity for the firm. This suggests that investing in intermediaries can be worthwhile when (a) they provide access to new prospect pools that are otherwise inaccessible through brand channels, or (b) the goal is to manage unfilled rooms (slack) rather than to drive primary customer acquisition. Multibrand behavior: The study finds that OTA-acquired customers are more likely to shop across a hotel brand’s multiple offerings, hinting toward variety-seeking behavior. As such, the customer is more likely to stay within the brand portfolio in case the brand they desire is ‘sold out’ on a particular purchase occasion, opening cross-selling opportunities for the firm. However, we also find that the OTA-acquired customers are less likely to upgrade to higher tier brands. Thus, it would be difficult for service providers to upgrade such customers and reap the benefits. The ‘optimal’ channel strategy still involves using intermediaries: Our analytical findings suggest that despite relatively lower CLVs, intermediaries should still play a role in the optimal acquisition budget allocations. We show that under specific conditions (the channels acquisition effectiveness and the size of the prospect pool), the firm should proportionally allocate resources toward OTA channels. Managers can directly use our findings in conjunction with the analytical results to design optimal acquisition budgets to maximize customer equity depending on market conditions and management heuristics (acquisition efficiency, market size, own capacity, etc.).

In summary, if intermediary channels can provide “incremental” business to the focal firm that does not cannibalize the firm’s owned channels, then it is a friend. If it only dilutes the firm’s efforts by replacing higher margin “direct” business with higher cost/lower margin “indirect” business, then it is an enemy. Given our findings, firms are well-advised to treat intermediary acquisition channels as “frenemies” by befriending them during “need periods” to help clear excess capacity and keep them at arm’s length when the firm can acquire its own customers.

Limitations and Avenues for Future Research

Although the models and data utilized are rich and robust in many ways, our research has its limitations. We discuss these below and outline potential avenues for future research.

First, from a research design and conceptualization standpoint, we make substantive and practical contributions in estimating the CLV of the intermediary acquired customers empirically. Furthermore, although we conceptualize the theoretical mechanisms underlying our findings to be based on concepts of outsourcing of customer experience (Kranzbühler et al., 2019), we do not have the data to formally test the mechanisms. We leave such an investigation to future work.

Second, our analysis only includes acquired customers who made a purchase and provided an email address or signed-up for the company’s loyalty program, which is how we were able to track transaction data over time. While we acknowledge this limitation, it does not in principle adversely affect the conclusions of this study. There might be customers who (1) do not make repeated transactions, or (2) repeat transactions without subscribing to the loyalty program. Managing relationships and building loyalty with such customers are likely to be even more challenging than those discussed in the paper.

Third, from an econometric standpoint, we have taken several steps to ensure that our findings are robust to alternative explanations that may be driven by endogeneity concerns. However, as with all observational analyses, we cannot definitively rule out all potential sources of bias. Given that OTA channels may also be correlated with unobserved customer characteristics (e.g., price sensitivity), future research could explore experimental designs to further validate our findings.

Fourth, although we note that the channel inertia effect is consistent across brand and OTA channels, it may be driven by differences in loyalty program incentives from the OTA. While the biggest OTAs were running their loyalty programs during the entire observation window, our data don’t allow us to formally test whether this is the explanation for the channel inertia effect. More generally, we do not have information on the relationship of a customer with the intermediary prior to acquisition. However, this research is not alone in this challenge and is shared by almost all loyalty program data. Typical CRM data only includes information for customers who are enrolled in the loyalty program, after the time when they first sign up. This data limitation does open interesting new avenues for academic-practitioner partnerships that may explore these customer dynamics further. For instance, future research combining (potentially multiple) OTA and firm loyalty program data would be able to study the interplay (and switching) between these channels and whether channel loyalty exists more broadly.

Fifth, while we present CLV-based budget allocation as a starting point for aligning channel decisions with long-term customer outcomes, it also opens several promising avenues for future research. For example, dynamic optimal control methods (Bruce et al., 2012; Rubel and Naik, 2017) could be used to study allocation strategies that account for both short- and long-run effects of intermediary channels. Although our focus is on the initial acquisition channel, examining post-acquisition cross-channel spillovers and dynamics would be a valuable extension. This would allow researchers to explicitly incorporate the billboard effect (Anderson, 2009) into direct-channel acquisition costs and, in turn, CLV estimates. However, prior evidence suggests that these cost savings are likely modest relative to the CLV differences we document, especially given OTA commissions (Anderson, 2009; Anderson and Han, 2017). Nonetheless, future work could examine how optimal resource allocation changes under symmetric or asymmetric spillovers and interdependent customer behaviors, potentially using a vector autoregressive (VAR) framework.

Supplemental Material

sj-pdf-1-pao-10.1177_10591478261437885 - Supplemental material for Customer Acquisition Through Intermediaries (vs. Brand) Shapes Lifetime Value: Evidence From the Hotel Industry

Supplemental material, sj-pdf-1-pao-10.1177_10591478261437885 for Customer Acquisition Through Intermediaries (vs. Brand) Shapes Lifetime Value: Evidence From the Hotel Industry by Agata Leszkiewicz, Sarang Sunder, V Kumar and Chekitan S Dev in Production and Operations Management

Footnotes

Acknowledgments

The authors are grateful to the multibrand global hotel company for the data which enabled this investigation, and to the many executives who championed our project and provided useful insights, all of whom wish to remain anonymous, and participants at the 2017 Cornell Center for Hospitality Research Annual Conference who provided useful feedback on the initial idea. The authors thank Renu for copyediting the manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

How to cite this article

Leszkiewicz A, Sunder S, Kumar V, and Dev CS (2026) Customer Acquisition Through Intermediaries (vs. Brand) Shapes Lifetime Value: Evidence From the Hotel Industry. Production and Operations Management XX(XX) 1–22.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.