Abstract

Platform firms are increasingly investing in value-added services (VAS), believing these investments in VAS universally contribute to their success. Although many studies have examined platform firms’ core services (e.g., intermediation), systematic analyses of VAS provision strategies remain limited. In this article, we develop a game-theoretic model to analyze (1) the conditions under which platform firms benefit from providing VAS and (2) to which side(s) platform firms should provide VAS. We offer several insights. First, variable service costs are a critical yet previously neglected factor in governing platform firms’ VAS provision. Second, a comparison of equilibrium outcomes across three VAS provision strategies—one-sided unidirectional, two separate unidirectional, and bidirectional—reveals that the optimal strategy is jointly determined by variable service costs, cross-network externalities, and the asymmetry in the benefits of bidirectional VAS to the two platform sides. Specifically, when asymmetry is low, bidirectional VAS is optimal. When asymmetry is high, platform firms should provide unidirectional VAS to one side, considering the second side only when variable service costs are low or cross-network externalities are significant. Third, we explore the implications of VAS provision strategies for platform firms’ investment and pricing decisions. For example, when platform firms provide two separate unidirectional VAS, these investments are complementary. VAS could incentivize platform firms to offer price subsidies to one side of the platform. Finally, optimal VAS provision strategies do not always increase consumer surplus.

Introduction

In modern economies, platform firms play a pivotal role in providing core platform services 1 to connect two distinct groups of market participants (the “two sides” of the platform). 2 Prominent examples include credit card providers (e.g., Mastercard for consumers and merchants), video game consoles (e.g., Sony PlayStation for consumers and developers), operating systems (e.g., iOS for consumers and developers), and e-commerce markets (e.g., Alibaba for consumers and merchants). The intermediary nature of these core services has spurred extensive research examining how network externalities shape interactions between the two sides of the platform (Parker and Van Alstyne, 2005), the platform’s pricing strategies for core services (Rysman, 2009), and the design and implementation of governance strategies (Rietveld and Schilling, 2021) among others.

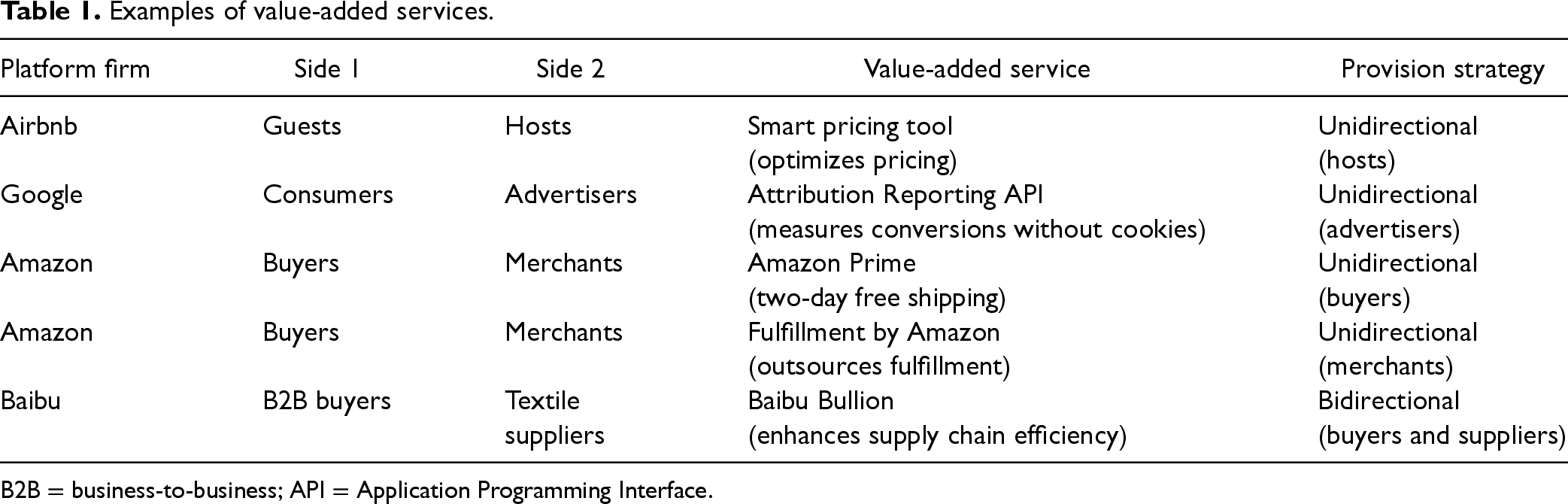

Driven by the growing need for differentiation and monetization, platform firms increasingly provide value-added services (VAS), that is, premium additions to core services that increase the utility of at least one side of the platform. As summarized in Table 1, platform firms adopt different VAS provision strategies for one or both sides of the platform. For example, Airbnb’s core service connects guests seeking accommodations with hosts offering properties, but its smart pricing tools enable hosts to optimize nightly rates based on demand fluctuations. Similarly, Google provides an Attribution Reporting Application Programming Interface (API) to help advertisers measure conversions without relying on third-party cookies. In e-commerce, Amazon delivers distinct VAS tailored to each side of its platform. For buyers, the Amazon Prime subscription offers benefits such as free two-day shipping. For merchants, the fulfillment by Amazon service allows them to outsource key order fulfillment tasks, including inventory management, storage, packing, shipping, and return handling. Baibu, a business-to-business (B2B) platform connecting textile suppliers with buyers such as wholesalers and clothing manufacturers, provides bidirectional VAS through its Baibu Bullion service. This VAS integrates transaction data from both sides of the platform with credit and loan application records, enhancing supply chain efficiency through faster approvals and real-time payments.

Examples of value-added services.

Examples of value-added services.

B2B = business-to-business; API = Application Programming Interface.

Despite the ubiquity of VAS, platform firms face significant challenges in strategizing their VAS provision. First, neither researchers nor practitioners provide systematic guidance on the conditions under which platform firms should provide VAS. Existing studies often assume that VAS are universally beneficial (Dou et al., 2016; Zhang et al., 2021). However, in practice, not all platform firms provide VAS, highlighting the need to identify the factors governing VAS provision decisions. A critical yet underexplored factor is the cost structure of VAS, which varies significantly across platform firms. For example, similar to Baibu, Smart Fabric connects upstream textile suppliers with downstream buyers through its core service. Smart Fabric introduced the “Internet of Things” (IoT), a VAS offering suppliers real-time demand information (e.g., order quantities and sizes) and buyers real-time supply insights (e.g., machine usage and delivery schedules). However, this VAS provision strategy entails both fixed investment costs (e.g., infrastructure for data exchange) and variable service costs (e.g., IoT sensors installed on suppliers’ machines for data collection).

Second, it is nontrivial to determine to which side(s) the platform firms should provide VAS. One option is to provide a single unidirectional VAS benefiting only one side of the platform. For example, Airbnb’s smart pricing tools directly benefit hosts by optimizing nightly rates, whereas guests derive no direct benefit. The second option involves providing two distinct unidirectional VAS, each tailored to one side of the platform. Amazon exemplifies this approach by offering Prime subscription services to buyers, providing benefits like free two-day shipping, and Fulfillment by Amazon to merchants, streamlining order fulfillment processes. The third option is to introduce a bidirectional VAS designed to benefit both sides of the platform simultaneously. For example, Baibu’s Bullion service enhances supply chain efficiency by simultaneously integrating transaction data from both sides of the platform. However, the equilibrium outcomes associated with each of these three VAS provision strategies remain unclear.

Third, determining the optimal level of VAS investment is complicated by (a) the number of sides served by VAS, (b) the size of cross-network externalities (CNEs), and (c) the platform’s pricing decisions. For example, it remains unclear whether two separate investments in unidirectional VAS for each side act as complements or substitutes. Furthermore, the role of CNEs in incentivizing or discouraging VAS investment is ambiguous because these externalities can lead to value transfer between sides. In addition, investments in one-sided unidirectional VAS may enhance platform valuations for both buyers and sellers—directly through improved service and indirectly via CNEs. Consequently, VAS provide platforms with an improved versatility of its pricing strategy.

Against this background, we develop a theoretical framework to address two key questions: (1) under what conditions should platform firms provide VAS, and (2) if VAS is provided, how should firms optimally strategize its provision with respect to which side(s)? In our framework, the platform firm operates as a profit-maximizing intermediary, connecting buyers and sellers who act as rational economic actors. The full game-theoretic model is structured into three stages. In the first stage, the platform firm determines whether to offer VAS and, if so, to which side(s) of the platform. In the second stage, given the chosen VAS provision strategy, the platform decides the optimal level of investment and sets participation prices for buyers and sellers. In the final stage, buyers and sellers make participation decisions based on the value they derive from the platform and their expectations about the participation of the other side.

Our analytical model incorporates several notable elements. First, it captures all feasible VAS provision strategies: core service only, a one-sided unidirectional VAS, two separate unidirectional VAS, and a bidirectional VAS. This comprehensive framework provides insights into platform firms’ optimal VAS provision strategies as well as their corresponding investment and pricing decisions across various scenarios. Second, the model accounts for the heterogeneity in buyers’ and sellers’ valuations of the core service as well as the CNEs inherent in two-sided platforms. By doing so, it reflects the nuanced interplay between these factors. Third, the model explicitly incorporates variable service costs. For many non-digital and some digital services, providing VAS entails significant costs related to installation, software customization, and technical integration among others. By incorporating variable service costs, our model extends the discussion of VAS strategies into a dimension that has been largely overlooked in the literature.

This article makes several contributions to theory and practice. First, we extend the literature on strategies for two-sided markets by identifying variable service costs as a critical factor in VAS provision. A key practical implication is that platforms should introduce VAS when variable service costs are sufficiently low. Second, our theoretical framework provides a comprehensive comparison of multiple strategies, decomposing the relative impacts of (a) variable service costs, (b) CNEs, and (c) asymmetry in the benefits of bidirectional VAS for the two platform sides. When asymmetry is low, platform firms are incentivized to offer bidirectional VAS. Conversely, when asymmetry is high, platform firms should provide unidirectional VAS and make it accessible to both sides only when variable service costs are low or CNEs are significant. Third, our analyses shed light on investment and pricing decisions under VAS provision. Specifically, we show that two separate investments in unidirectional VAS, one for each side, are complementary. Furthermore, in some cases, the platform firm may subsidize one side of the platform, depending on CNEs, variable service costs, and investment efficiency, to encourage market participation. Last, our findings reveal that a platform’s optimal VAS provision strategy does not always increase consumer surplus. Notably, the main findings remain qualitatively unchanged when accounting for the heterogeneity in investment efficiencies between the two sides of the platform.

The remainder of this article is structured as follows. In Section 2, we provide an overview of the related literature and outline our contributions. In Section 3, we characterize VAS user participation and develop a decision-making model for platform firms offering only the core service in a baseline scenario. Section 4 extends our model to incorporate VAS provision strategies that platform firms may adopt in addition to the core service. Sections 5 and 6 compare all feasible VAS provision strategies, examining their investment decisions, price subsidies, social welfare, and investment efficiencies. Finally, Section 7 presents our conclusions and a discussion of the implications. All proofs are provided in the Section EC.2 of the E-Companion.

Our study is related to three strands of literature: service innovation by digital platforms, platform openness strategies, and platform pricing strategies.

The pioneering work in platform service innovation and product development, including Bhargava and Choudhary (2004) and Parker and Van Alstyne (2005), addresses product design issues of monopolistic infomediaries and other services, including information-goods versioning and social welfare improvement. Zhu and Iansiti (2012) theoretically and empirically investigated a video game market incumbent and entrant competing on quality and installed base, with the platforms’ quality and price being exogenous. González-Maestre and Martínez-Sánchez (2015) and Roger (2017) studied the endogenous quality choices of two competing media platforms and reveal different duopoly equilibria given CNEs for a two-sided market and firms’ quadratic product or service-development cost functions. Anderson et al. (2014) build a strategic model to investigate the trade-off between investing in platform performance and holding back investment to facilitate video game development, assuming asymmetric impact on the market’s two sides. Specifically, investment in platform performance benefits buyers (video game players) but hurts sellers (game developers).

Most platform firms offer information-based goods (Broekhuizen et al., 2021; Parker and Van Alstyne, 2005). However, studies on information goods’ development costs primarily consider traditional markets (Banker and Kemerer, 1989; Jones and Mendelson, 2011; Lehmann-Grube, 1997; Wei and Nault, 2008). In a two-sided market, innovation costs typically follow a convex functional form. For example, Hagiu and Spulber (2013) explored how the scale parameter of a platform’s quadratic investment cost function affects its pricing and first-party content investment strategies.

Recent literature has examined platform firms’ VAS innovations. Dou et al. (2016) investigated one-sided VAS investment and pricing strategies for two-sided platforms. In a follow-up study, Dou et al. (2018) find that the optimal level of VAS investment decreases in the presence of negative intragroup network externalities. Sui et al. (2023) studied the impact of competition on platforms’ VAS investments by including two competing platforms using a Hotelling model and incorporating multi-homing of platform users. Similarly, Tan et al. (2020) explored the key trade-offs behind integration tool investment and its interaction with pricing decisions in a two-sided market.

Existing literature examines how VAS adds a new dimension to a platform’s offerings but lacks a comprehensive understanding of VAS provision strategies. Most studies (Dou et al., 2016, 2018; Tan et al., 2020) focus on platforms’ investment and pricing decisions on VAS. Additionally, prior studies (Dou et al., 2016, 2018; Sui et al., 2023) discuss only a single VAS type without directly comparing feasible VAS provision strategies. As a result, the literature has not established optimal market scenarios for VAS provision or the best VAS strategy. Moreover, current discussions neglects variable service costs, inaccurately projecting that VAS are always beneficial (Zhang et al., 2021).

Our study is also related to openness issues in the platform literature (Broekhuizen et al., 2021). The literature strand has extensively documented the phenomenon of two-sided (Anderson et al., 2022; Cohen and Zhang, 2022) and multiple-sided platforms (Evans, 2003; Staykova and Damsgaard, 2015). Studies have investigated when it is optimal for firms to transform to digital platforms (Hagiu, 2007), when they should provide service to each side of the market (Hagiu and Wright, 2019), and whether a platform should open to competitors (Cohen and Zhang, 2022). Nevertheless, existing studies provide little guidance on how many market sides a platform firm should offer VAS.

The seminal papers on two-sided markets focus extensively on platform pricing issues (Armstrong, 2006; Caillaud and Jullien, 2003; Hagiu, 2004, 2006; Parker and Van Alstyne, 2000; Rochet and Tirole, 2006). Parker and Van Alstyne (2000) explored a monopoly platform’s pricing structure and show that deciding which side of a two-sided market to subsidize depends on relative cross-side network externalities. Caillaud and Jullien (2003) developed an imperfect price competition model between two platforms using two-part tariffs. Rochet and Tirole (2006) build a two-sided pricing model for competing platforms and show the determinants of price allocation and end-user surplus under profit and nonprofit governance structures. Hagiu (2004) studies platform pricing and social efficiency under both structures, showing that either can be socially efficient. Armstrong (2006) develops two-sided pricing models for profit- and social welfare-maximizing platforms, finding that the equilibrium depends on cross-group externalities, fee structure, and whether users are single- or multi-homing. Hagiu (2006) explores two-sided markets where sellers arrive before buyers, focusing on pricing and platform commitment.

In some two-sided markets, researchers have identified significant intragroup network externalities (e.g., Bardey et al., 2014; Belleflamme and Toulemonde, 2009; Li et al., 2011; Yoo et al., 2002) and introduced them, along with intergroup externalities, to address the monopolistic or competitive pricing question. Lin et al. (2011) examined the two-sided pricing strategy of a profit-maximizing platform monopolist while considering seller-side innovation decisions and price competition, where sellers engage in both finite- and infinite-horizon innovation races; Reisinger (2014) incorporates heterogeneous trading behaviors into a two-part tariff competition between two-sided platforms. Wang et al. (2019) proposed a price competition model for duopoly platforms and analyze the effects of government regulation on equilibrium profit and social welfare. In practice, the two-sided pricing theory has been applied to various platforms, including credit cards (Rochet and Wright, 2010; Wright, 2003), media (Ferrando et al., 2008; Reisinger, 2012), computer or smartphone operating systems (Boudreau, 2010), ride-hailing (Cachon et al., 2017; Wang et al., 2016), and grocery delivery (Kung and Zhong, 2017).

Studies have also examined the interplay between pricing strategy and VAS investment. Dou et al. (2016) showed that users with VAS are always priced higher than those with only core services, while opposite user sides given no VAS investment may either receive an increased or decreased price, depending on the relative magnitude of mutual CNEs. Tan et al. (2020) suggested that considering integration investment can create market regimes where standard pricing results shown in the platform literature do not hold. Reducing prices on one side of a market in response to increasing the network’s benefit to the other may be suboptimal in the presence of integration investment. Prior work by Dou et al. (2016, 2018) assumes users are homogeneous in their VAS valuation, which may not accurately reflect their decisions. Moreover, without a comprehensive comparison among feasible VAS provision strategies, pricing strategy variations under different investment scenarios remain underexplored.

This research builds on the digital platform VAS literature and aims to fill multiple research gaps. First, we develop a theoretical model incorporating buyer and seller heterogeneity, CNEs, endogenous platform pricing and investment decisions, and asymmetry in bidirectional VAS benefits. Second, our study extends VAS provision and investment discussions about variable service costs when introducing the services, an area the literature has neglected. Our complete cost structure exploration generates meaningful discussions on how variable service costs influence a platform’s VAS provision decisions and investment and pricing strategies. Our comprehensive theoretical framework addresses all feasible VAS strategies a two-sided platform could pursue. Instead of an individual VAS application scenario, our analyses provide an in-depth examination of platforms’ VAS provision decisions across multiple market settings. Finally, by incorporating CNEs, two-sided service valuation heterogeneity, and variable VAS costs, the study extends our understanding of platform firms’ VAS investment and pricing strategies, as well as their underlying mechanisms, in realistic market settings.

Model Setup

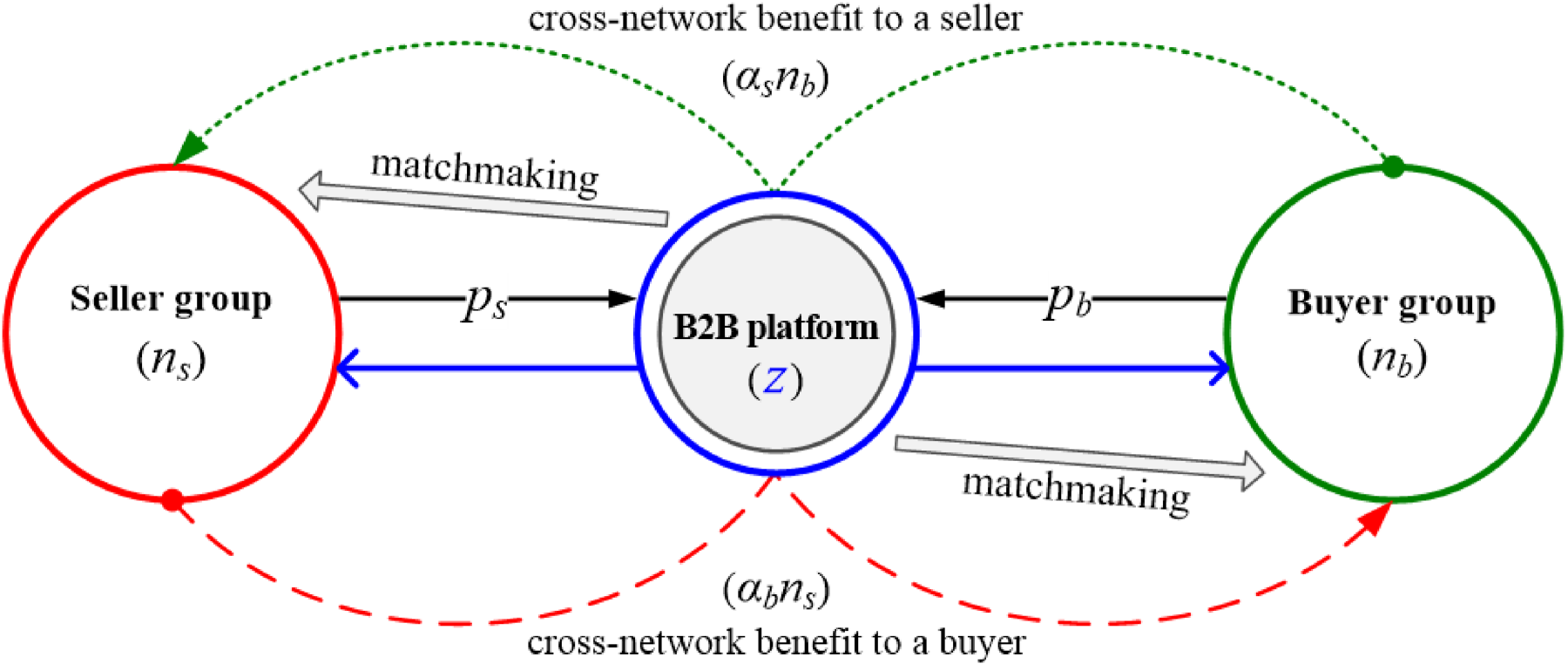

We use a B2B e-commerce platform as the practical scenario for our model. Our analysis focuses on a platform firm (e.g., Smart Fabric) and its interactions with buyers (e.g., wholesalers and clothing manufacturers) and sellers (e.g., textile suppliers). The basic framework is illustrated in Figure 1. The platform provides a core service (e.g., intermediation) to two sides (buyers and sellers), who are required to pay participation fees to access the service. In addition, buyer (seller) participation generates cross-network benefits for the other side of the platform, enhancing the value provided by the platform.

Basic framework of a platform firm in business-to-business (B2B).

The value that a buyer or seller derives from participating in the platform consists of three additive components: (i) the value of the core service, (ii) cross-network externalities (hereafter, CNEs), and (iii) added benefits from VAS. This specification aligns with prior studies (Anderson et al., 2014; Bhargava and Choudhary, 2004; Kauffman et al., 2000; Parker and Van Alstyne, 2005; Saloner et al., 1995). The value of the core service depends on the platform’s service nature. We use

We denote

In addition to its core service, the platform may provide VAS to one or both sides of the platform (recall Table 1). Following the literature (e.g., Hagiu and Spulber, 2013), VAS is assumed to generate additional value, denoted as

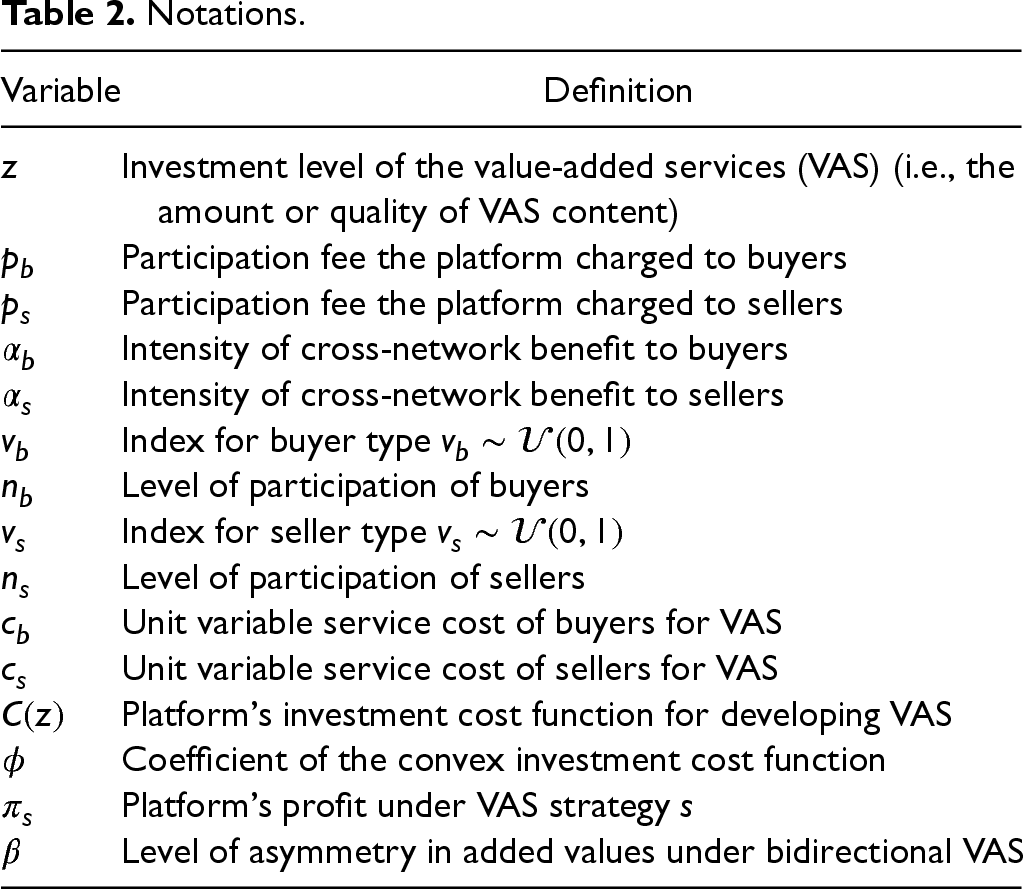

Notations.

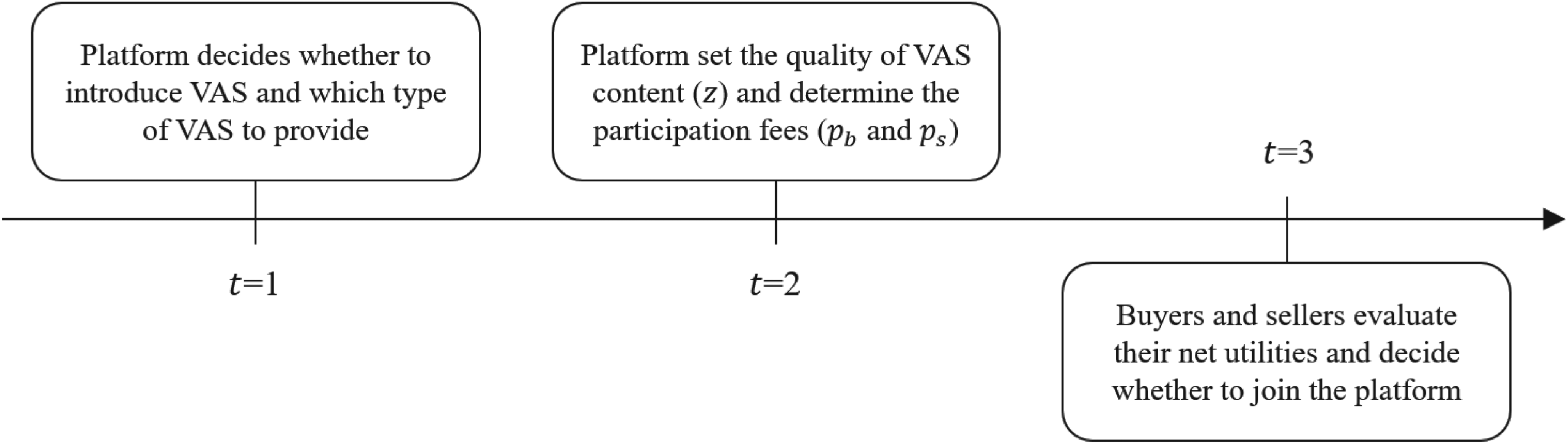

In this article, the full game involves three parties: buyers, sellers, and the platform firm. The sequence of the game is depicted in Figure 2. First, the platform firm determines whether to provide VAS, the number of sides to which the platform firm provides VAS, and the VAS provision strategy. Second, under the adopted VAS provision strategy, the platform decides the investment level in VAS and sets participation fees

Timeline of the game.

Based on our model setup, the utilities that a buyer and seller enjoy by participating on the platform with only its core service provided can be represented as follows:

Let

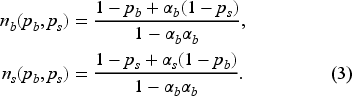

For any given participation fees (i.e.,

The feasibility of this equilibrium is conditional. In particular, if the size of CNE is too large, that is,

The modeled platform firm’s revenue mainly stems from buyer and seller participation fees. In the baseline model (Case I: no-VAS), only the core service is provided to both sides of the platform. Following prior research on information goods and services (Bhargava and Choudhary, 2004; Hagiu and Spulber, 2013; Jones and Mendelson, 2011; Roger, 2017), we assume that the platform incurs negligible (zero) marginal costs of reproduction and distribution for the core service provided. Thus, the platform’s profit can be specified as

Based on the platform’s profit function, we first establish the market equilibrium under the baseline case when the platform provides its core service only. The participation fees, market participation proportions, and platform profits are summarized in the following Lemma 1.

When the platform serves both sides of the market with core service only, the participation fees charged to the two sides are

In this baseline case, pricing is the most important strategy for the platform because both buyer and seller groups must pay the participation fee to access the core service on the platform. As we assume CNEs are in reasonable ranges (i.e.,

In the baseline case where the platform provides only its core service,

the participation fee increases with the focal side’s CNEs (i.e., the side with higher CNEs pays a relatively higher participation fee.

This corollary suggests that either buyers or sellers can benefit indirectly through CNE. Consider buyers as the focal side, when the size of CNE for buyers increases, the total perceived value of buyers increases, allowing the platform to charge increased participation fees to buyers. However, a greater size of CNE of the other side (sellers) motivates the platform to encourage more participation from the focal side (buyers) through price reductions.

Following the baseline scenario with only a core service provided by the platform, we examine four VAS provision strategies. VAS can be provided in various forms, each focusing on different side(s) of the platform. Specifically, in addition to its core service (Case I: no-VAS), the platform may provide a unidirectional VAS to one side of the platform (Case II: uni-VAS), two separate unidirectional VAS to each side of the platform (Case III: 2uni-VAS), or a bidirectional VAS that benefits both sides of the platform simultaneously (Case IV: bi-VAS).

Although the literature has studied VAS provision strategies (Dou et al., 2016; Tan et al., 2020; Zhang et al., 2021), it lacks a comprehensive examination and comparison across these strategies. More importantly, two fundamental questions—when should a platform consider providing VAS and to which side(s) the platform should provide VAS—remain underexplored. Some studies concentrate on VAS investment and pricing strategies but overlook the optimal market conditions for providing VAS (e.g., Dou et al., 2016). Other related studies incorrectly project that VAS are always beneficial for platforms (e.g., Zhang et al., 2021). To bridge this gap in the literature, we examine the market equilibria and investigate pricing and investment strategies under various VAS provision scenarios. For clarity of analytical exposition but without loss of generality, instead of using buyer and seller, we use subscripts

One-Sided Unidirectional VAS

When a platform firm provides a one-sided unidirectional VAS, the service directly benefits only one side of the platform. For instance, the smart pricing tools provided by Airbnb directly assist hosts in optimizing pricing based on demand, but buyers neither use the service nor directly benefit from them. Between the two sides of the platform

In practice, it is rare that the either side of a market can be fully served by a platform. To exclude extreme cases where one or both sides of the market is fully served, we assume investment efficiency is not extremely high (i.e., the investment cost parameter

Beyond the fixed investment cost, VAS provision incurs variable service costs. Significant efforts are required to make the service accessible. For instance, to monitor upstream manufacturing and improve resource planning, Smart Fabric required sellers to install IoT sensors in their facilities for data collection. Thus, each participating individual from side

Investment in VAS allows the platform to reconsider its pricing strategy. Lemma 2 examines the influences on the platform’s decisions on participation fees when the firm decides to introduce unidirectional VAS to side

When the platform provides unidirectional VAS to only one side (e.g., side Side The impact of investment in side

The additional utility generated by increasing VAS investment enhances side

Based on the pricing strategy discussed above and following backward induction, we derive optimal VAS investment and the related market equilibrium in Lemma 3.

When the platform provides unidirectional VAS to only one side (e.g., side

A one-sided unidirectional VAS can directly benefit only one side of a platform. To enhance their competitive advantage, platforms sometimes consider introducing two separate VAS (one to each side). For instance, to enhance the online shopping experience, Amazon.com has introduced the Prime membership program offering subscribers free and premium delivery services. Meanwhile, to improve the efficiency of logistics and operations, the platform provides Fulfillment by Amazon to sellers. The service innovations benefit the two sides directly and separately. Providing two separate unidirectional VAS enhances the value for both sides and influences their utilities as follows:

Because the platform must develop VAS tailored to the needs of each side of the market separately, the two unidirectional VAS incur separate development costs. In addition, because VAS is introduced to both sides, both their participation leads to variable service costs for the platform. Thus, the platform’s profit function should include both fixed VAS development costs, that is,

Under two separate unidirectional VAS, the investment in one side’s unidirectional VAS allows the platform to increase participation fees for participants on that side (i.e.,

When the platform provides two separate unidirectional VAS to each side, it may reconsider its pricing strategy by adjusting each side’s participation fees accordingly. As summarized in Lemma 4, because two separate unidirectional VAS provide both direct and indirect benefits, both sides (buyers and sellers) are expected to be more willing to participate. Thus, the platform can charge higher participation fees. For the side with greater (smaller) CNE, their participation fees increase (decrease) with the investment in unidirectional VAS to the other side. The result is mainly driven by the CNE because the side with greater CNE (e.g.,

On a two-sided platform, investment in one side’s VAS directly increases the focal side’s utility while also indirectly benefiting the other side through CNE. One might expect two separate investments in unidirectional VAS to be substitutes, but Proposition 1 finds that the two investments are complementary. When the platform increases its investment in side

When the platform provides two separate unidirectional VAS, VAS investment in one side’s VAS complements investment in the other side (i.e.,

Proposition 1 reveals that although participation prices increase after the platform introduces two unidirectional VAS, the increased utility sufficiently compensates for the increased price. Driven by CNE, investing in one side’s VAS increases the marginal benefit of investing in VAS on the other side, creating a complementary effect between the investments on the two sides. Such a complementarity motivates an increase in the cross-side investment, which creates greater CNE for the focal side of the platform. Therefore, both sides are more willing to participate when the platform increases investments in either side of the market under two separate unidirectional VAS.

Following the game sequence, we derive the equilibrium for the two separate unidirectional VAS in Lemma 5.

When the platform provides two separate unidirectional VAS to each side of the market, the optimal investments made in the two separate services should be set as follows:

The optimal fees charged for participation are as follows:

The total profit for the platform is as follows:

In addition to CNE, variable service costs and investment efficiency play important roles in shaping the platform’s pricing and VAS investment decisions.

With two separate unidirectional VAS, the platform invests more in the side with lower variable service costs. The resulting VAS investment gap enlarges when investment efficiency improves (as

As Corollary 2 shows, high variable service costs discourage the platform from additional VAS investment, and the side with lower variable costs receives increased investment. When investment becomes increasingly efficient, the platform becomes increasingly aggressive in VAS investment. Hence, the side with lower variable costs receives greater investments, leading to an enlarged service quality gap between the two sides of the market.

Some VAS are bidirectional in nature. For example, the Baibu Bullion service enables data exchanges from two sides of the market simultaneously and leads to direct benefits for both buyers and sellers. Providing bidirectional VAS to both sides entails variable service costs (e.g., installation and customization) to integrate both buyers and sellers on the platform. Unlike the case of two separate unidirectional VAS, bidirectional VAS are cost-efficient because the same amount of investment benefits both sides of the market. However, because bidirectional VAS are “one fits both” services, it usually does not generate the same amount of value to each side. Therefore, when investigating the platform’s decision on bidirectional VAS, we introduce parameter

Similar to the other VAS strategies, bidirectional VAS may incur variable service costs to make the service accessible, which can be captured by the

As the two user groups benefit differently from the bidirectional VAS, the platform can adjust its pricing strategy to incorporate the asymmetry in benefits of VAS, as summarized in Proposition 2.

When the platform increases investment in bidirectional VAS:

Side Side Both sides are more willing to participate with increased investment in bi-VAS, although side

As revealed in Proposition 2, both sides of the platform have to pay increased participation fees when the platform increases its investment in the bidirectional VAS. For side

Proposition 2 confirms that bidirectional VAS always drive participation from both sides of the market. However, due to the asymmetric direct benefits of the services, as long as side

The equilibrium under bidirectional VAS is summarized in Lemma 6.

When the platform provides bidirectional VAS to both sides of the market, the optimal quality level should be set as

The platform firm has several prospective VAS provision strategies: (I) no VAS, (II-s) one unidirectional VAS for sellers, (II-b) one unidirectional VAS for buyers, (III) two separate unidirectional VAS, (IV-s) a seller-focused bidirectional VAS, and (IV-b) a buyer-focused bidirectional VAS. This section examines the feasible conditions for VAS provision and compares across all feasible strategies for a platform firm.

Feasibility of VAS Provision Strategies

Compared to core service, VAS increase sellers’ or buyers’ perceived value of participating on a platform directly or indirectly through CNE. Intuitively, with investment in VAS, platforms can attract more participation from both sides of the market and could gain additional profits. Nevertheless, VAS provision also induces cost. On the one hand, providing VAS requires significant efforts in research and development, which leads to additional investment costs for the platform. On the other hand, making VAS accessible to users incurs additional variable service costs. For instance, to enable data exchange with sellers, Smart Fabric installed IoT devices and customized its software interface for individual users, which incurred significant variable service costs.

Prior studies have explored the feasibility of the one-sided or two separate VAS strategies. Nevertheless, neglecting variable service costs can lead to an inaccurate projection that introducing VAS is always an optimal decision for platforms. Our work contributes to the VAS literature by providing comprehensive analysis and accounting for the non-negligible variable service costs in a platform’s VAS provision strategy.

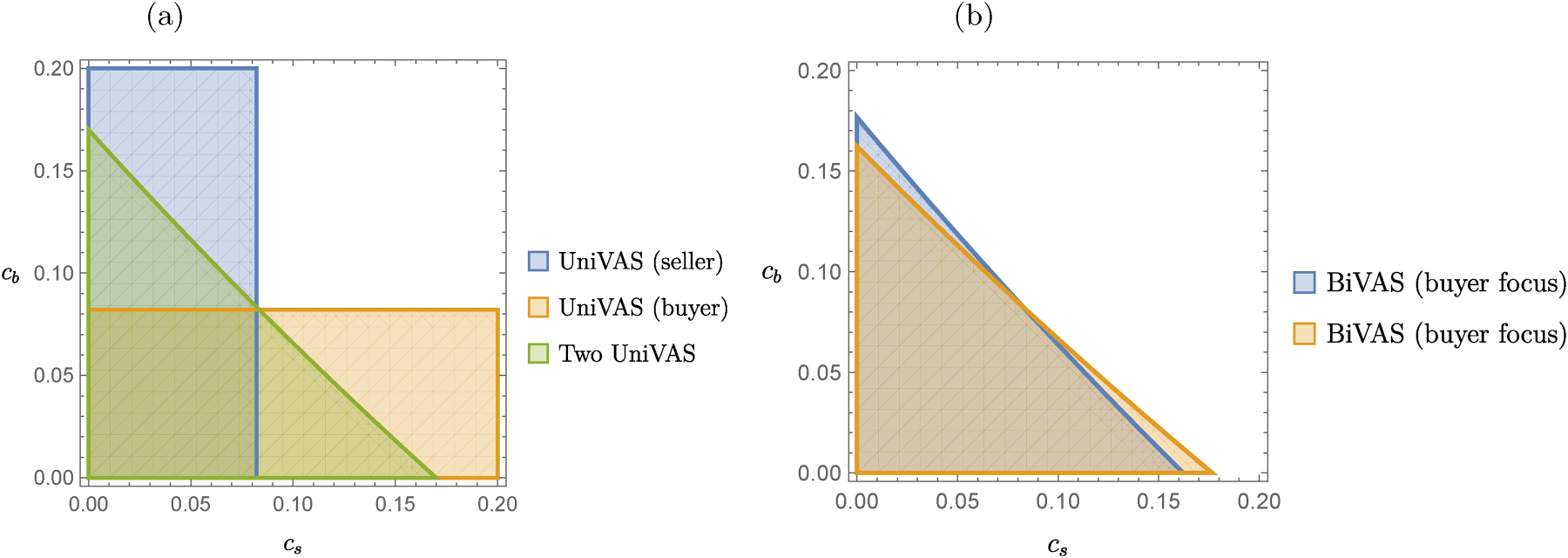

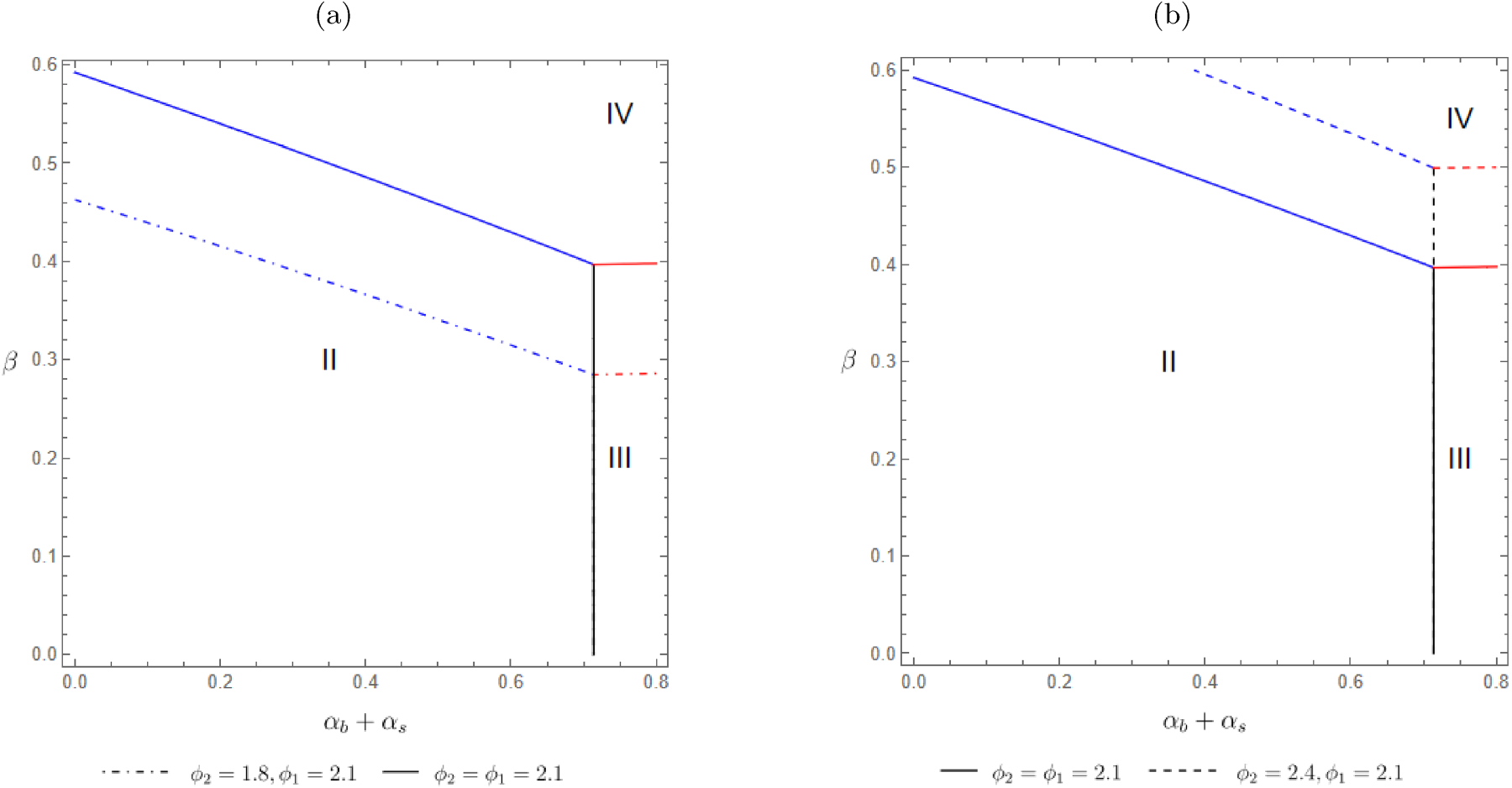

As summarized in Proposition 3, when variable service costs are non-negligible, introducing VAS is not always the optimal solution. Figure 3 depicts the market conditions under which the platform should consider introducing VAS rather than providing its core service only. It compares all VAS provision strategies to the baseline case (I: no-VAS) separately and illustrates that the platform should consider providing VAS only when the variable service costs are low.

Conditions under which platform should consider introducing value-added services (VAS): (a) unidirectional VAS provision and (b) bidirectional VAS provision. Notes:

The platform should introduce VAS only when variable service costs are sufficiently low (

Figure 3 shows that bidirectional VAS with a focus on side

When the platform considers only one unidirectional VAS, it must decide whether to make it accessible to sellers or buyers. Similarly, when the platform introduces a bidirectional VAS, it needs to decide whether to focus the service on buyers or sellers, with the opposite side receiving discounted utility

The platform should provide unidirectional VAS to (or focus bidirectional VAS on) the side with a lower service cost when it introduces a unidirectional (or bidirectional) VAS.

Lemma 7 demonstrates that the variable service costs are an important factor that determines the preferred side of the market for the platform to offer unidirectional VAS or concentrate its bidirectional VAS. Specifically, when deciding which way to direct unidirectional VAS, the side with the lower service cost will be able to access the service, while with bidirectional VAS, the same side will benefit from the full added value.

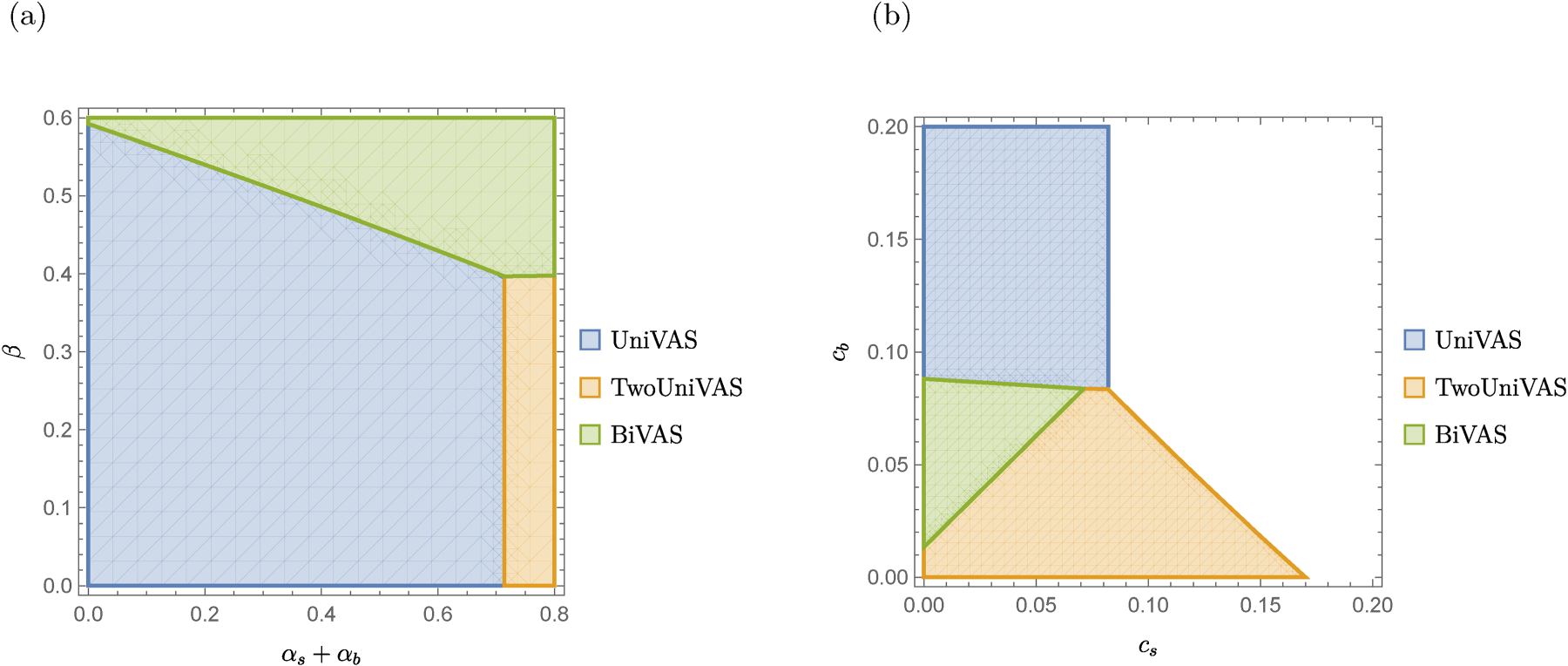

When a platform designs its VAS provision strategy, it should first evaluate whether introducing VAS is beneficial. According to Proposition 3, when the variable service costs of introducing VAS are sufficiently low (i.e.,

The platform’s ideal choice of VAS depends on the asymmetry level of added value and variable service cost:

When the asymmetry of added value in bidirectional VAS is minimal (or Otherwise, the platform should choose unidirectional VAS, prioritizing the side with a lower service cost (i.e., side

Compared to unidirectional VAS, bidirectional VAS have the advantage of cost efficiency as the investment can benefit two sides of the market at the same time. However, the added service quality through bidirectional VAS may not be symmetric to buyers and sellers. When

When the asymmetry level of added value in bidirectional VAS is low (

Optimal VAS provision strategy: (a) optimal VAS strategy (by CNE and asymmetry) (

Figure 4(b) illustrates the impact of unit variable service costs on the platform’s optimal VAS strategy. Generally, the platform should provide unidirectional VAS to one side of the market (e.g., sellers) only when the other side’s (e.g., buyers) variable service costs are large. Otherwise, the platform should consider offering VAS to both sides of the market. Given the asymmetry of added value in bidirectional VAS, it should be preferred by the platform when side

This section further investigates investment decisions, potential price subsidies, and social welfare implications. We also examine an extended scenario in which investment inefficiency is different for unidirectional versus bidirectional VAS provision. Without loss of generality, we assume the sellers’ (side

VAS Investments

VAS investments can be influenced by factors such as CNE, variable service costs, and investment cost inefficiency. More importantly, VAS investment level directly impacts the utility of one side of the market and indirectly increases the utility of the other side through CNE. As one of the key factors influencing service quality on a platform, it is important to understand optimal investment levels for different VAS strategies.

As revealed in Proposition 1, investments in separate VAS for each side have a complementary effect. Consequently, investment levels under two separate unidirectional VAS are expected to be higher than those under a one-sided VAS. Therefore, this subsection focuses on the comparison between VAS investments when both sides receive direct service quality improvements through VAS (i.e., two separate unidirectional VAS and bidirectional VAS).

When the platform provides VAS to the two sides separately, it can determine the optimal investment level for each side (i.e.,

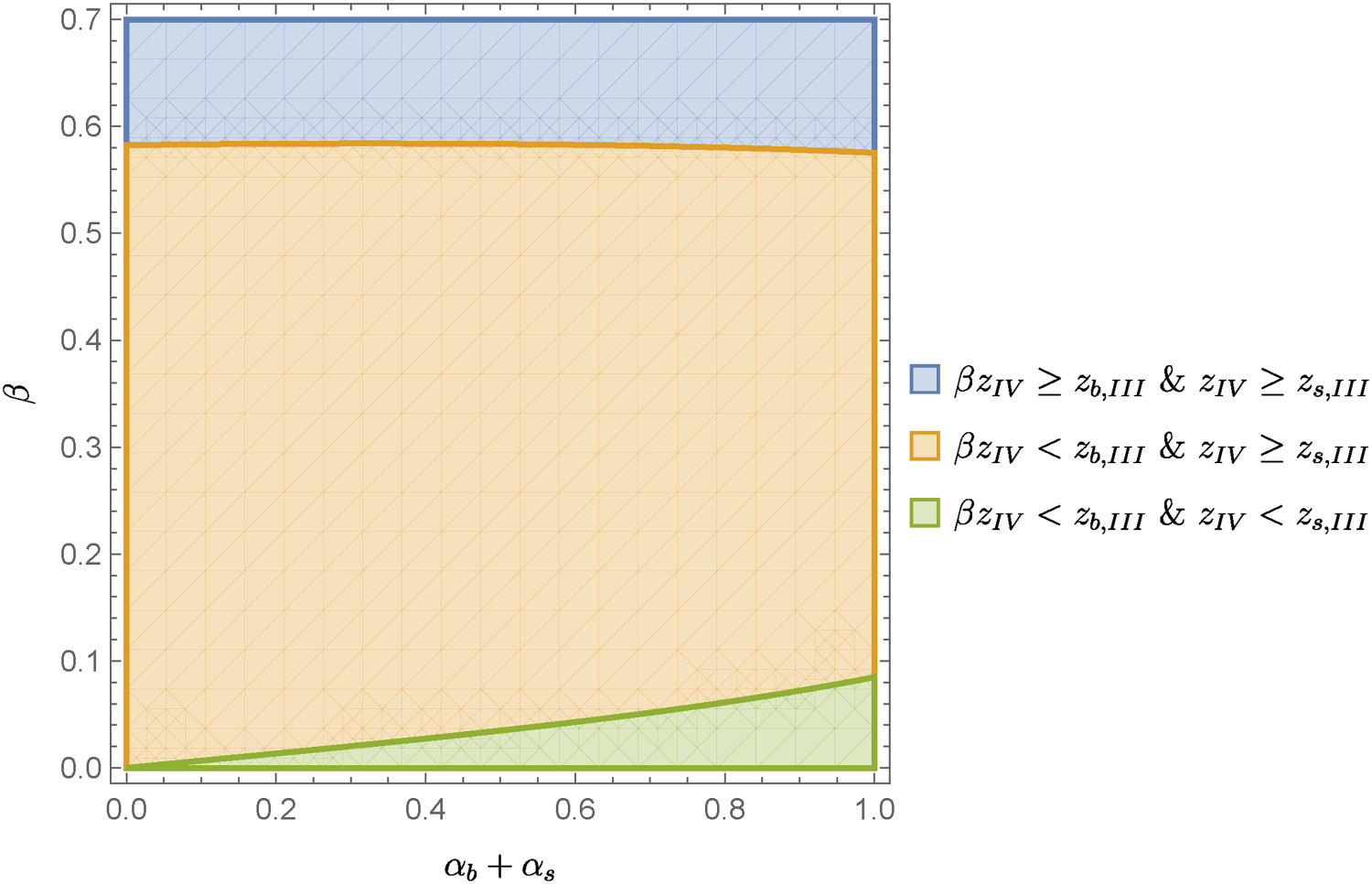

While both bidirectional and two separate unidirectional VAS enhance the service quality for both market sides, the two sides’ preferences may vary depending on the asymmetry in the added value of bidirectional VAS ( For low asymmetry (i.e., For moderate asymmetry (i.e., For high asymmetry (i.e.,

Figure 5 illustrates the investment level comparison between the two VAS strategies. The asymmetry in added values (

Investments under two UniVAS (III) and BiVAS (IV). Notes:

However, when the asymmetry (

Last, when asymmetry is high (or

In a two-sided platform, pricing is an important strategy for platforms to maintain their competitive advantage and achieve further growth. It has been shown that price subsidies can be an effective strategy for platforms to grow during the early stage (Lian and Van Ryzin, 2021). With VAS provision, platforms reinforce the value provided to buyers and sellers. Due to the asymmetric nature of the two-sided marketplace (e.g., asymmetric CNE, different unit variable service costs), platforms may consider price subsidies to enhance both sides’ incentives to participate under VAS.

To understand the feasibility of price subsidies, we first consider the platform firm’s pricing decision when it provides only its core service. Then, we compare the participation fees under different VAS strategies to the baseline case. The market conditions for feasible price subsidies are summarized in Proposition 6.

Compared with the scenario when the platform provides only its core service:

Under one unidirectional VAS to side With two unidirectional VAS, the side with lower CNE may receive subsidies if its variable service cost is sufficiently small and the other side’s cost is high enough; In bidirectional VAS, the side with discounted added values could receive price subsidies if the asymmetry in added value is sufficiently large or its variable service cost is sufficiently small.

Price (or participation fee), as a crucial lever for the platform, influences the incentives of both sides to participate in the platform marketplace. Due to network effects, this influence is further amplified by CNEs. Under the one-sided unidirectional VAS, as users in group

When the platform chooses to provide two separate unidirectional VAS, side

If the platform provides bidirectional VAS to both sides of the market, the platform should subsidize the side that receives discounted added values when the asymmetry level is large (or

Based on the discussions regarding the participation of the two sides on the platform, this subsection examines the implications on social welfare based on VAS strategies implemented by the platform. The overall social welfare consists of the profit of the platform and the surplus from both buyers and sellers in the market, which can be derived based on the equilibrium under each VAS strategy. However, the comparison is analytically intractable. Therefore, we mainly discuss the overall social welfare based on the numerical observations.

The VAS provision strategy chosen by the platform may not always maximize social welfare. Therefore, policymakers might consider further incentivizing the platform to make VAS more accessible to both sides of the market, thus enhancing social welfare.

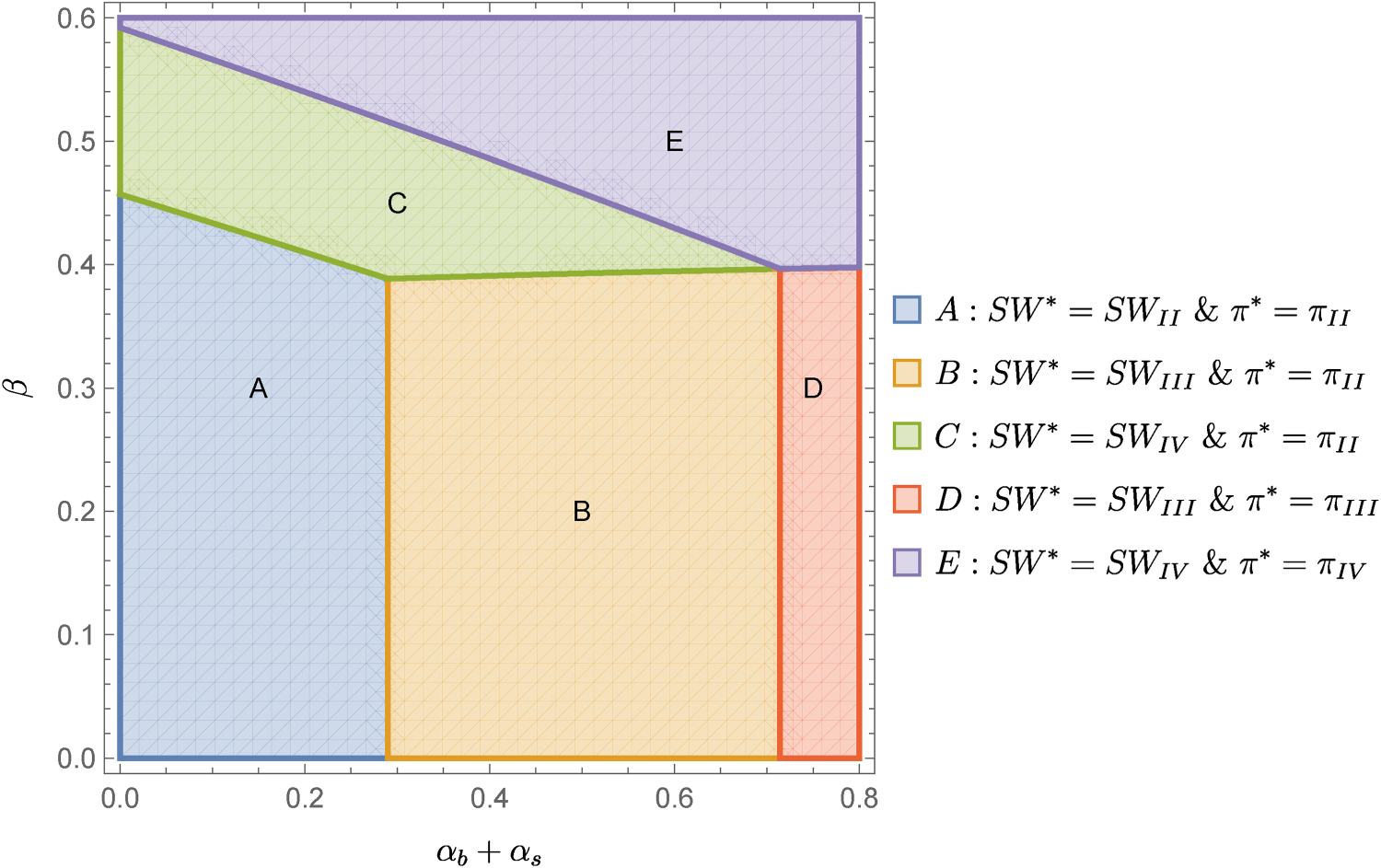

The optimal VAS strategies for platform profit or social welfare have been highlighted in Figure 6. Comparing with Figure 4(a), the optimal VAS strategy for platform also generates the highest social welfare in Regions A, D, and E, where the recommended VAS strategy is one unidirectional VAS to the side with lower service cost, two separate unidirectional VAS, and a bidirectional VAS, respectively. In contrast, in Regions B and C, where the platform chooses to provide unidirectional VAS to only one side of the market (i.e., the side with a lower service cost), the overall social welfare can be further improved when the platform also offers VAS to the other side (either through two separate unidirectional VAS or one bidirectional VAS). This can be caused by the substantial service costs and the investment costs of providing VAS, which reduce the platform’s incentives to add VAS to the side with higher service costs when the overall cross-network externally (

Social welfare implications of value-added services (VAS) provision strategies. Notes:

VAS provision enhances user satisfaction on both sides of a two-sided platform, expands market coverage, and generates profits for a platform. However, platforms incur a cost when developing and implementing VAS. In our main analysis, we assume a uniform investment inefficiency parameter

In this extension, we consider a generalized scenario where the investment inefficiency parameter is different for unidirectional versus bidirectional VAS development. Specifically, we assume an investment inefficiency parameter

Figure 7 shows how the relative difference in investment inefficiency impacts the platform’s optimal VAS strategy. The solid lines denote the boundary conditions for the platform’s optimal strategy when the investment inefficiencies for unidirectional VAS and bidirectional VAS are identical. Figure 7(a) depicts the scenario where it is more efficient to develop the bidirectional VAS (where bidirectional VAS has a relatively low investment inefficiency parameter

Differentiated investment inefficiency. Notes:

The comparison in Figure 7 demonstrates that the platform’s optimal choices among the three VAS provision strategies remain qualitatively robust as investment inefficiency changes, although the difference leads to shifts in the boundaries. In general, the platform should still prefer to introduce one unidirectional VAS to one side of the market when aggregated CNE is small and asymmetry under bidirectional VAS is large. Providing two separate unidirectional VAS is optimal only when aggregated CNE is sufficiently large. Providing bidirectional VAS can be more profitable than two unidirectional VAS when aggregated CNE is large and asymmetry under bidirectional VAS is small. As the service innovation under the bidirectional VAS becomes more efficient (or investment inefficiency parameter

Despite the prevalent adoption of VAS by platform firms, the literature lacks a systematic analysis of optimal VAS provision strategies. To address this gap, we develop a theoretical framework to investigate (i) the key drivers of VAS provision decisions, (ii) the trade-offs in different VAS provision strategies, and (iii) VAS investment and pricing decisions. We explicitly model the long-overlooked variable service costs of providing VAS and the asymmetry in the benefits of bidirectional VAS across the two sides. In addition, building on the literature, our comprehensive theoretical model incorporates buyer and seller heterogeneity, endogenous investment and pricing decisions for both sides of the platform, and CNEs to analyze the factors driving VAS decisions. Notably, the main findings remain qualitatively unchanged when accounting for the heterogeneity in investment efficiencies between the two sides of the platform.

Managerial Takeaways

Our research offers a practical framework for platform firms to evaluate VAS initiatives and design optimal strategies. Below, we offer several key managerial takeaways.

Evaluating the cost structure of VAS provision is a top priority. Despite conventional wisdom suggesting that VAS provision encourages participation and benefits platforms, we show that platforms must carefully evaluate whether a VAS-driven surplus can surpass any non-negligible variable service costs incurred. Such costs influence a platform’s decision on VAS provision. That is, the platform should introduce VAS only when variable service costs are sufficiently low. Determining the optimal VAS strategy is nontrivial. In scenarios where VAS provision is profitable, the provision of bidirectional VAS depends on the degree of asymmetry in added value. When asymmetry is low—meaning the VAS provides relatively equal added value to both sides of the platform—the platform firm should consider providing bidirectional VAS that benefit both sides simultaneously. In contrast, when asymmetry is high, platforms should consider implementing unidirectional VAS by prioritizing the side with lower service costs while considering the second side only when variable service costs are also low or its CNEs are strong. Investing in the synergy. We find that investments in both sides of the platform are complementary. Driven by CNEs, investing in VAS on one side increases the marginal benefit of investing in VAS on the other side. As a result, increased investments in two separate unidirectional VAS always attract more market participation from both sides, suggesting that platform firms need to invest in the synergy between the two sides to maximize marginal return on investment. Leveraging price subsidies. Providing price subsidies may be an effective lever for platforms that provide VAS. When platforms implement one-sided unidirectional VAS, they may provide price subsidies to the side without VAS if its CNEs are relatively weak. When platforms provide two separate unidirectional VAS or a bidirectional VAS, they may consider subsidizing one side of their market when the incurred variable service costs and CNEs are both at low levels. Social welfare may (not) be a bonus. We find that the platform’s optimal VAS strategies may not always benefit consumer surplus. Due to the unavoidable costs of VAS investments and additional variable service costs, the platform may hesitate to offer VAS to both sides of the market. Overall social welfare could be further improved if VAS could be provided to both sides through bidirectional or separate unidirectional VAS when the platform finds it profitable to introduce unidirectional VAS to only one side. This offers valuable insights for policymakers, who might consider additional measures such as subsidizing platform firms to further incentivize them to provide VAS to both platform sides.

Future Directions

There are several limitations that offer potential directions for future research. First, our model does not consider potential market competition among sellers. VAS may reduce the perceived difference among products or services offered by sellers and impact their incentives for differentiation. Future work could examine the impact of VAS on competition among sellers. Other future work could incorporate competition among platforms to provide further insight into VAS strategies under different market competition levels. In addition, our model assumes that all variable VAS costs are taken on by platforms. Future studies may explore contract alternatives between platforms and participants. For instance, platform firms may find it profitable to charge participation fees on one side of a market and offer its services to the other side at no charge. Finally, future research could investigate the impact of more integrated service portfolios (e.g., the combination of a bidirectional VAS with a unidirectional VAS to only one platform side).

Supplemental Material

sj-pdf-1-pao-10.1177_10591478251332713 - Supplemental material for Strategizing Value-Added Services for Platform Firms

Supplemental material, sj-pdf-1-pao-10.1177_10591478251332713 for Strategizing Value-Added Services for Platform Firms by Liwen Hou, Xinxue (Shawn) Qu, Yixing Chen and Ling Xue in Production and Operations Management

Footnotes

Acknowledgments

The authors are grateful for the valuable suggestions from Yun (Alicia) Wang and Xiaoyan Xu.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The first author appreciates the support by the National Science Foundation of China [Grant 72171146].

Notes

How to cite this article

Hou L, Qu X(S), Chen Y and Xue L (2025) Strategizing Value-Added Services for Platform Firms. Production and Operations Management 34(10): 3289–3308.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.